UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended April 1, 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number: 000-25121

_______________________________________________________________________

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

Registrant’s telephone number, including area code: (763 ) 551-7000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 1, 2023, 22,184,000 shares of the registrant’s Common Stock were outstanding.

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

INDEX

| Page | ||||||||

i | 2Q 2022 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

PART I: FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Condensed Consolidated Balance Sheets

(unaudited - in thousands, except per share amounts)

| April 1, 2023 | December 31, 2022 | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Accounts receivable, net of allowances of $ | |||||||||||

| Inventories | |||||||||||

| Prepaid expenses | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Non-current assets: | |||||||||||

| Property and equipment, net | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Goodwill and intangible assets, net | |||||||||||

| Deferred income taxes | |||||||||||

| Other non-current assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Shareholders’ Deficit | |||||||||||

| Current liabilities: | |||||||||||

| Borrowings under revolving credit facility | $ | $ | |||||||||

| Accounts payable | |||||||||||

| Customer prepayments | |||||||||||

| Accrued sales returns | |||||||||||

| Compensation and benefits | |||||||||||

| Taxes and withholding | |||||||||||

| Operating lease liabilities | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Non-current liabilities: | |||||||||||

| Operating lease liabilities | |||||||||||

| Other non-current liabilities | |||||||||||

| Total liabilities | |||||||||||

| Shareholders’ deficit: | |||||||||||

Undesignated preferred stock; | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total shareholders’ deficit | ( | ( | |||||||||

| Total liabilities and shareholders’ deficit | $ | $ | |||||||||

See accompanying notes to condensed consolidated financial statements.

1 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Condensed Consolidated Statements of Operations

(unaudited - in thousands, except per share amounts)

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Net sales | $ | $ | |||||||||

| Cost of sales | |||||||||||

| Gross profit | |||||||||||

| Operating expenses: | |||||||||||

| Sales and marketing | |||||||||||

| General and administrative | |||||||||||

| Research and development | |||||||||||

| Total operating expenses | |||||||||||

| Operating income | |||||||||||

| Interest expense, net | |||||||||||

| Income before income taxes | |||||||||||

| Income tax expense | |||||||||||

| Net income | $ | $ | |||||||||

| Basic net income per share: | |||||||||||

| Net income per share – basic | $ | $ | |||||||||

| Weighted-average shares – basic | |||||||||||

| Diluted net income per share: | |||||||||||

| Net income per share – diluted | $ | $ | |||||||||

| Weighted-average shares – diluted | |||||||||||

See accompanying notes to condensed consolidated financial statements.

2 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Condensed Consolidated Statements of Shareholders’ Deficit

(unaudited - in thousands)

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Total | ||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | $ | ( | |||||||||||||||||||||||

| Net income | — | — | — | ||||||||||||||||||||||||||

| Exercise of common stock options | — | — | |||||||||||||||||||||||||||

| Stock-based compensation | — | ||||||||||||||||||||||||||||

| Repurchases of common stock | ( | ( | ( | — | ( | ||||||||||||||||||||||||

| Balance at April 1, 2023 | $ | $ | $ | ( | $ | ( | |||||||||||||||||||||||

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Total | ||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | ( | $ | ( | |||||||||||||||||||||||

| Net income | — | — | — | ||||||||||||||||||||||||||

| Exercise of common stock options | — | — | |||||||||||||||||||||||||||

| Stock-based compensation | — | ||||||||||||||||||||||||||||

| Repurchases of common stock | ( | ( | ( | ( | ( | ||||||||||||||||||||||||

| Balance at April 2, 2022 | $ | $ | $ | ( | $ | ( | |||||||||||||||||||||||

See accompanying notes to condensed consolidated financial statements.

3 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows

(unaudited - in thousands)

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Stock-based compensation | |||||||||||

| Net loss on disposals and impairments of assets | |||||||||||

| Deferred income taxes | ( | ( | |||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | |||||||||||

| Inventories | ( | ||||||||||

| Income taxes | |||||||||||

| Prepaid expenses and other assets | ( | ||||||||||

| Accounts payable | ( | ||||||||||

| Customer prepayments | ( | ||||||||||

| Accrued compensation and benefits | ( | ( | |||||||||

| Other taxes and withholding | ( | ||||||||||

| Other accruals and liabilities | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Proceeds from sales of property and equipment | |||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Cash flows from financing activities: | |||||||||||

| Repurchases of common stock | ( | ( | |||||||||

| Net (decrease) increase in short-term borrowings | ( | ||||||||||

| Proceeds from issuance of common stock | |||||||||||

| Debt issuance costs | ( | ||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Net decrease in cash and cash equivalents | ( | ( | |||||||||

| Cash and cash equivalents, at beginning of period | |||||||||||

| Cash and cash equivalents, at end of period | $ | $ | |||||||||

See accompanying notes to condensed consolidated financial statements.

4 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

1. Business and Summary of Significant Accounting Policies

Business & Basis of Presentation

The Company prepared the condensed consolidated financial statements as of and for the three months ended April 1, 2023 of Sleep Number Corporation and its 100%-owned subsidiaries (Sleep Number or the Company), without audit, pursuant to the rules and regulations of the Securities and Exchange Commission (SEC) and they reflect, in the opinion of management, all normal recurring adjustments necessary to present fairly its financial position as of April 1, 2023 and December 31, 2022, and the consolidated results of operations and cash flows for the periods presented. The historical and quarterly consolidated results of operations may not be indicative of the results that may be achieved for the full year or any future period.

Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles (GAAP) have been condensed or omitted pursuant to such rules and regulations. These condensed consolidated financial statements should be read in conjunction with the most recent audited consolidated financial statements and related notes included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022 and other recent filings with the SEC.

2. Fair Value Measurements

5 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

3. Inventories

| April 1, 2023 | December 31, 2022 | ||||||||||

| Raw materials | $ | $ | |||||||||

| Work in progress | |||||||||||

| Finished goods | |||||||||||

| $ | $ | ||||||||||

4. Goodwill and Intangible Assets, Net

Goodwill and Indefinite-lived Intangible Assets

Goodwill was $64 1.4

Definite-lived Intangible Assets

| April 1, 2023 | December 31, 2022 | ||||||||||||||||||||||

| Gross Carrying Amount | Accumulated Amortization | Gross Carrying Amount | Accumulated Amortization | ||||||||||||||||||||

| Developed technologies | $ | $ | $ | $ | |||||||||||||||||||

| Patents | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

Developed technologies - amortization expense for the three months ended April 1, 2023 and April 2, 2022, was $0.4 million and $0.5 million, respectively.

Patents - amortization expense for both the three months ended April 1, 2023 and April 2, 2022, was $55

| 2023 (excluding the three months ended April 1, 2023) | $ | |||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| 2028 | ||||||||

| Thereafter | ||||||||

| Total future amortization for definite-lived intangible assets | $ | |||||||

5. Credit Agreement

6 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

security interest in substantially all of the Company’s assets and those of its subsidiaries and requires the Company to comply with, among other things, a maximum net leverage ratio (5.0 x) and a minimum interest coverage ratio (3.0 x).

The Company amended the Credit Agreement on October 26, 2022. The amendment, among other things, (a) provides relief from the requirement that the net leverage ratio not exceed 3.75 x for certain corporate actions including Permitted Capital Distributions for Performance or Taxes (as defined in the Credit Agreement) and certain acquisition activity; (b) increases the permissible net leverage ratio to 5.0 x for the three consecutive quarterly reporting periods ending July 1, 2023; (c) increases the commitment fee rate to 50 basis points and the margin applicable to interest rates for all borrowings by an additional 50 basis points, in each case if the net leverage ratio is greater than or equal to 4.5 x; and (d) replaces the option to borrow at an interest rate based on London Interbank Offered Rate (LIBOR) to one based on a Term SOFR Rate. The Term SOFR Rate equals the sum of (x) the Term SOFR Screen Rate (as defined in the Credit Agreement) for the applicable interest period (but in no event less than zero), plus (y) 0.10 %, plus (z) the margin based on Sleep Number’s net leverage ratio. For the quarterly reporting period ending September 30, 2023, and subsequent quarterly reporting periods, the maximum leverage ratio will be 4.5 x.

Under the terms of the Credit Agreement, the Company pays a variable rate of interest and a commitment fee based on its leverage ratio. The Credit Agreement matures in December 2026. The Company was in compliance with all financial covenants as of April 1, 2023.

| April 1, 2023 | December 31, 2022 | ||||||||||

| Outstanding borrowings | $ | $ | |||||||||

| Outstanding letters of credit | $ | $ | |||||||||

| Additional borrowing capacity | $ | $ | |||||||||

| Weighted-average interest rate | % | % | |||||||||

6. Leases

The Company leases its retail, office and manufacturing space under operating leases which, in addition to the minimum lease payments, may require payment of a proportionate share of the real estate taxes and certain building operating expenses. While the Company’s local market development approach generally results in long-term participation in given markets, the retail store leases generally provide for an initial lease term of to 10 years. The Company’s office and manufacturing leases provide for an initial lease term of up to 15 years. In addition, the Company’s mall-based retail store leases may require payment of variable rent based on net sales in excess of certain thresholds. Certain leases may contain options to extend the term of the original lease. The exercise of lease renewal options is at the Company’s sole discretion. Lease options are included in the lease term only if exercise is reasonably certain at lease commencement. The Company’s lease agreements do not contain any material residual value guarantees. The Company also leases vehicles and certain equipment under operating leases with an initial lease term of to six years .

The Company’s operating lease costs include facility, vehicle and equipment lease costs, but exclude variable lease costs. Operating lease costs are recognized on a straight-line basis over the lease term, after consideration of rent escalations and rent holidays. The lease term for purposes of the calculation begins on the earlier of the lease commencement date or the date the Company takes possession of the property. During lease renewal negotiations that extend beyond the original lease term, the Company estimates straight-line rent expense based on current market conditions. Variable lease costs are recorded when it is probable the cost has been incurred and the amount can be reasonably estimated.

At April 1, 2023, the Company’s finance right-of-use assets and lease liabilities were not significant.

7 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

Lease costs were as follows (in thousands):

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

Operating lease costs(1) | $ | $ | |||||||||

| Variable lease costs | $ | $ | |||||||||

___________________________

(1)Includes short-term lease costs which are not significant.

The maturities of operating lease liabilities as of April 1, 2023, were as follows(1) (in thousands):

| 2023 (excluding the three months ended April 1, 2023) | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| 2028 | |||||

| Thereafter | |||||

Total operating lease payments(2) | |||||

| Less: Interest | |||||

| Present value of operating lease liabilities | $ | ||||

___________________________

(1)Future payments for real estate taxes and certain building operating expenses for which the Company is obligated are not included in the operating lease liabilities. Total operating lease payments exclude $70 million of legally binding minimum lease payments for leases signed but not yet commenced.

(2)Includes the current portion of $81 million for operating lease liabilities.

Other information related to operating leases was as follows:

| April 1, 2023 | December 31, 2022 | |||||||||||||

| Weighted-average remaining lease term (in years) | ||||||||||||||

| Weighted-average discount rate | % | % | ||||||||||||

| Three Months Ended | ||||||||||||||

| (in thousands) | April 1, 2023 | April 2, 2022 | ||||||||||||

| Cash paid for amounts included in present value of operating lease liabilities | $ | $ | ||||||||||||

| Right-of-use assets obtained in exchange for operating lease liabilities | $ | $ | ||||||||||||

8 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

7. Repurchases of Common Stock

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Amount repurchased under Board-approved share repurchase program | $ | $ | |||||||||

| Amount repurchased in connection with the vesting of employee restricted stock grants | |||||||||||

| Total amount repurchased (based on trade dates) | $ | $ | |||||||||

As of April 1, 2023, the remaining authorization under the Board-approved $600 million share repurchase program was $348 million.

8. Revenue Recognition

Deferred contract assets and deferred contract liabilities are included in the condensed consolidated balance sheets as follows (in thousands):

| April 1, 2023 | December 31, 2022 | ||||||||||

| Deferred contract assets included in: | |||||||||||

| Other current assets | $ | $ | |||||||||

| Other non-current assets | |||||||||||

| $ | $ | ||||||||||

| April 1, 2023 | December 31, 2022 | ||||||||||

| Deferred contract liabilities included in: | |||||||||||

| Other current liabilities | $ | $ | |||||||||

| Other non-current liabilities | |||||||||||

| $ | $ | ||||||||||

Deferred revenue and costs related to SleepIQ® technology are currently recognized on a straight-line basis over the product's estimated life of 4.5 to 5.0 years because the Company’s inputs are generally expended evenly throughout the performance period. During the three months ended April 1, 2023 and April 2, 2022, the Company recognized revenue of $10 million and $9 million, respectively, that was included in the deferred contract liability balances at the beginning of the respective periods.

Revenue from goods and services transferred to customers at a point in time accounted for approximately 98

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Retail stores | $ | $ | |||||||||

| Online, phone, chat and other | |||||||||||

| Total Company | $ | $ | |||||||||

9 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

Obligation for Sales Returns

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Balance at beginning of year | $ | $ | |||||||||

| Additions that reduce net sales | |||||||||||

| Deductions from reserves | ( | ( | |||||||||

| Balance at end of period | $ | $ | |||||||||

9. Stock-based Compensation Expense

Total stock-based compensation expense (benefit) was as follows (in thousands):

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

Stock awards (1) | $ | $ | |||||||||

| Stock options | |||||||||||

Total stock-based compensation expense (1) | |||||||||||

| Income tax benefit | |||||||||||

| Total stock-based compensation expense, net of tax | $ | $ | |||||||||

___________________________

(1) Changes in stock-based compensation expense include the cumulative impact of the change in the expected achievements of certain performance targets.

10. Profit Sharing and 401(k) Plan

10 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

11. Net Income per Common Share

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Net income | $ | $ | |||||||||

| Reconciliation of weighted-average shares outstanding: | |||||||||||

| Basic weighted-average shares outstanding | |||||||||||

| Dilutive effect of stock-based awards | |||||||||||

| Diluted weighted-average shares outstanding | |||||||||||

| Net income per share – basic | $ | $ | |||||||||

| Net income per share – diluted | $ | $ | |||||||||

Additional potential dilutive stock-based awards totaling 1.1 million and 0.4 million for the three months ended April 1, 2023 and April 2, 2022, respectively, have been excluded from the diluted net income per share calculations because these stock-based awards were anti-dilutive.

12. Commitments and Contingencies

Warranty Liabilities

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Balance at beginning of year | $ | $ | |||||||||

| Additions charged to costs and expenses for current-year sales | |||||||||||

| Deductions from reserves | ( | ( | |||||||||

| Changes in liability for pre-existing warranties during the current year, including expirations | ( | ( | |||||||||

| Balance at end of period | $ | $ | |||||||||

Legal Proceedings

The Company is involved from time to time in various legal proceedings arising in the ordinary course of its business, including primarily commercial, product liability, employment and intellectual property claims. In accordance with U.S. generally accepted accounting principles, the Company records a liability in its consolidated financial statements with respect to any of these matters when it is both probable that a liability has been incurred and the amount of the liability can be reasonably estimated. If a material loss is reasonably possible but not known or probable, and may be reasonably estimated, the estimated loss or range of loss is disclosed. With respect to currently pending legal proceedings, the Company has not established an estimated range of reasonably possible material losses either because it believes that is has valid defenses to claims asserted against it, the proceeding has not advanced to a stage of discovery that would enable it to establish an estimate, or the potential loss is not material. The Company currently does not expect the outcome of pending legal proceedings to have a material effect on its consolidated results of operations, financial position or cash flows. Litigation, however, is inherently unpredictable, and it is possible that the ultimate outcome of one or more claims asserted against the Company could adversely impact its consolidated results of operations, financial position or cash flows. The Company expenses legal costs as incurred.

11 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SLEEP NUMBER CORPORATION

AND SUBSIDIARIES

Notes to Condensed Consolidated Financial Statements

(unaudited)

Shareholder Class Action Complaints

On December 14, 2021, purported Sleep Number shareholder, Steamfitters Local 449 Pension & Retirement Security Funds (Steamfitters), filed a putative class action complaint in the United States District Court for the District of Minnesota (the District of Minnesota) on behalf of all purchasers of Sleep Number common stock between February 18, 2021 and July 20, 2021, inclusive, against Sleep Number, Shelly Ibach and David Callen, the Company’s former Executive Vice President and Chief Financial Officer. Steamfitters alleges material misstatements and omissions in certain of Sleep Number’s public disclosures during the purported class period, in violation of Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, as amended (the Exchange Act). The complaint seeks, among other things, unspecified monetary damages, reasonable costs and expenses and equitable/injunctive or other relief as deemed appropriate by the District of Minnesota.

On February 14, 2022, a second purported Sleep Number shareholder, Ricardo Dario Schammas, moved for appointment as lead plaintiff in the action. On March 24, 2022, the District of Minnesota heard argument on Schammas’s motion, and subsequently appointed Steamfitters and Schammas as Co-Lead Plaintiffs (together, Co-Lead Plaintiffs). On July 19, 2022, Co-Lead Plaintiffs filed a consolidated amended complaint, which, like the predecessor complaint, asserts claims against Sleep Number, Shelly Ibach, and David Callen under Sections 10(b) and 20(a) of the Exchange Act. Co- Lead Plaintiffs purport to assert these claims on behalf of all purchasers of Sleep Number common stock between February 18, 2021 and July 20, 2021. Defendants moved to dismiss the consolidated complaint on September 19, 2022, which motion was heard by the Court on January 17, 2023, and remains pending.

Shareholder Derivative Complaint

On May 12, 2022, Gwendolyn Calla Moore, as the appointed representative of purported Sleep Number shareholder Matthew Gelb, filed a derivative action (the Derivative Action) in the District of Minnesota against Jean-Michel Valette, Shelly Ibach, Barbara Matas, Brenda Lauderback, Daniel Alegre, Deborah Kilpatrick, Julie Howard, Kathleen Nedorostek, Michael Harrison, Stephen Gulis, Jr., David Callen, and Kevin Brown. Moore purports to assert claims on behalf of Sleep Number for breaches of fiduciary duty, waste, and contribution under Sections 10(b) and 21(d) of the Exchange Act. Moore’s allegations generally mirror those asserted in the securities complaint described above. The Moore complaint seeks damages in an unspecified amount, disgorgement, interest, and costs and expenses, including attorneys’ and experts’ fees.

On September 13, 2022, the District of Minnesota entered a joint stipulation staying all proceedings in the Derivative Action pending the outcome of any motion to dismiss the Steamfitters consolidated amended complaint.

Stockholder Demand

On March 25, 2022, Sleep Number received a shareholder litigation demand (the “Demand”), requesting that the Board investigate the allegations in the securities class action complaint and pursue claims on Sleep Number’s behalf based on those allegations. On May 12, 2022, the Board established a special litigation committee to investigate the demand.

On October 5 and October 12, 2022, Sleep Number received two additional shareholder litigation demands, which adopted and incorporated the allegations and requests in the Demand. Both of these additional litigation demands were referred to the special litigation committee.

The special litigation committee has concluded that it would not be in the best interests of Sleep Number and its shareholders to take any of the actions requested in the demands at this time.

12 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) is intended to provide a reader of the Company’s condensed consolidated financial statements with a narrative from the perspective of management on its financial condition, results of operations, liquidity and certain other factors that may affect the Company’s future results. MD&A is presented in eight sections:

•Forward-Looking Statements and Risk Factors

•Business Overview

•Results of Operations

•Liquidity and Capital Resources

•Non-GAAP Data Reconciliations

•Off-Balance-Sheet Arrangements and Contractual Obligations

•Critical Accounting Policies

Forward-looking Statements and Risk Factors

The discussion in this Quarterly Report contains certain forward-looking statements that relate to future plans, events, financial results or performance. You can identify forward-looking statements by those that are not historical in nature, particularly those that use terminology such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “believe,” “estimate,” “plan,” “project,” “predict,” “intend,” “potential,” “continue” or the negative of these or similar terms. These statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and its present expectations or projections. These risks and uncertainties include, among others:

•Current and future economic conditions and consumer sentiment;

•Bank failures or other events affecting financial institutions;

•Increases in interest rates, which have increased the cost of servicing the Company’s indebtedness;

•Availability of attractive and cost-effective consumer credit options;

•Operating with minimal levels of inventory, which may leave the Company vulnerable to supply shortages;

•Sleep Number’s dependence on, and ability to maintain strong working relationships with, key suppliers and third parties;

•Rising commodity costs or third-party logistics costs and other inflationary pressures;

•Risks inherent in global-sourcing activities, including tariffs, geo-political turmoil, war, strikes, labor challenges, government-mandated work closures, outbreaks of pandemics or contagious diseases, and resulting supply shortages and production and delivery delays and disruptions;

•Risks of disruption due to health epidemics or pandemics, such as the COVID-19 pandemic;

•Regional risks related to having global operations and suppliers, including climate and other disasters;

•The effectiveness of the Company’s marketing strategy and promotional efforts;

•The execution of Sleep Number’s Total Retail distribution strategy;

•Ability to achieve and maintain high levels of product quality;

•Ability to improve and expand Sleep Number’s product line and execute successful new product introductions;

•Ability to prevent third parties from using the Company’s technology or trademarks, and the adequacy of its intellectual property rights to protect its products and brand;

•Ability to compete;

•Risks of disruption in the operation of any of the Company’s main manufacturing, distribution, logistics, home delivery, product development or customer service operations;

•The Company’s ability to comply with existing and changing government regulation;

•Pending or unforeseen litigation and the potential for associated adverse publicity;

•The adequacy of the Company’s and third-party information systems and costs and disruptions related to upgrading or maintaining these systems;

13 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

•The Company’s ability to withstand cyber threats that could compromise the security of its systems, result in a data breach or business disruption;

•Sleep Number’s ability, and the ability of its suppliers and vendors, to attract, retain and motivate qualified personnel;

•The volatility of Sleep Number stock;

•Environmental, social and governance (ESG) risks, including increasing regulation and stakeholder expectations; and

•The Company’s ability to adapt to climate change and readiness for legal or regulatory responses thereto.

Additional information concerning these, and other risks and uncertainties is contained under the caption “Risk Factors” in Part I, Item 1A. in the Company’s Annual Report on Form 10-K.

The Company has no obligation to publicly update or revise any of the forward-looking statements contained in this Quarterly Report on Form 10-Q.

Business Overview

Sleep Number is a wellness technology company. Over 14.5 million people have had their lives improved by the Company’s award-winning sleep innovations and are experiencing the physical, mental and emotional benefits of life-changing sleep performance. Sleep Number’s proprietary smart beds combine the physical and digital worlds, pairing exceptional sleep with a highly advanced digital technology platform. Only Sleep Number can provide a dynamic, adjustable and adaptive sleep experience that effortlessly responds to the needs of each sleeper helping them reach their full potential. More than two million Smart Sleepers benefit from the Company’s smart beds, which change with the sleeper over time and provide individualized sleep that is unique, like they are.

Sleep Number’s differentiated business model is guided by its purpose to improve the health and wellbeing of society through higher quality sleep. The Company partners with world-leading sleep and health institutions to bring the power of 19 billion hours of longitudinal sleep data to sleep science and research. The Company’s retail experience meets its consumers whenever and wherever they choose – through online and in-store touchpoints. And Sleep Number’s 5,000 mission-driven team members passionately deliver individualized sleep experiences for everyone.

Through investments in its consumer innovation strategy and vertically integrated business model, Sleep Number strengthens its competitive advantages and creates a digital flywheel for sustainable growth, driving consumer demand and performance. It generates revenue by marketing and selling its innovations directly to new and existing customers through exclusive, direct-to-consumer retail touch points including Stores, Online, Phone, and Chat (Total Retail). Sleep Number is committed to creating long-term superior value for all stakeholders as it focuses on the Company’s three performance drivers: (1) increasing consumer demand; (2) leveraging its vertically integrated business model; and (3) deploying capital efficiently.

Results of Operations

Quarterly and Year-to-Date Results

Quarterly and year-to-date operating results may fluctuate significantly as a result of a variety of factors, including increases or decreases in sales, timing, amount and effectiveness of advertising expenditures, changes in sales return rates or warranty experience, timing of investments in growth initiatives and infrastructure, timing of store openings/closings and related expenses, changes in net sales resulting from changes in the Company’s store base, timing of new product introductions and related expenses, timing of promotional offerings, competitive factors, changes in commodity costs, disruptions in global supplies or third-party service providers, seasonality of retail and bedding industry sales, consumer sentiment and general economic conditions. The extent to which these external factors will impact the Company’s business and its consolidated financial results will depend on future developments, which are highly uncertain and cannot be predicted. Therefore, the historical results of operations may not be indicative of the results that may be achieved for any future period.

14 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Highlights

Financial highlights for the three months ended April 1, 2023 were as follows:

•Net sales for the three months ended April 1, 2023 were consistent at $527 million with the prior-year period. Demand was impacted by historically low consumer sentiment.

•The net sales change consisted of a 2% comparable sales decrease in Total Retail offset by additional sales from 18 net new stores opened in the past 12 months that added 2 percentage points (ppt.) of growth. For additional details, see the components of total net sales change on page 16.

•Sales per store (sales for stores open at least one year, Total Retail, including online, phone and chat) on a trailing twelve-month basis for the period ended April 1, 2023 totaled $3.2 million, compared with $3.5 million for the same period last year.

•Operating income for the three months ended April 1, 2023 was $26 million, compared with $4 million in the prior-year period. The $22 million increase in operating income was driven by a 1.6 ppt. increase in the gross profit rate and a $14 million reduction in the operating expenses.

•The 1.6 ppt. gross profit rate increase was primarily due to pricing actions take over the past twelve months. See the Gross profit discussion on page 18 for additional details.

•The $14 million reduction in the Company’s operating expenses was mainly due to lower marketing expenses.

•Net income for the three months ended April 1, 2023 increased to $11 million, compared with $2 million for the same period one year ago. Net income per diluted share was $0.51, compared with $0.09 last year.

•The Company achieved an adjusted return on invested capital (Adjusted ROIC) of 20.4% on a trailing twelve-month basis for the period ended April 1, 2023, compared with 32.0% for the comparable period one year ago.

•The Company generated $19 million in cash from operating activities for the three months ended April 1, 2023, compared with $25 million for the same period one year ago.

•As of April 1, 2023, the Company had $471 million of borrowings under its revolving credit facility and available net liquidity of $347 million.

15 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

The following table sets forth the Company’s results of operations expressed as dollars and percentages of net sales. Figures are in millions, except percentages and per share amounts. Amounts may not add due to rounding differences.

| Three Months Ended | |||||||||||||||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||||||||||||||

| Net sales | $ | 526.5 | 100.0 | % | $ | 527.1 | 100.0 | % | |||||||||||||||

| Cost of sales | 216.3 | 41.1 | % | 224.8 | 42.7 | % | |||||||||||||||||

| Gross profit | 310.3 | 58.9 | % | 302.3 | 57.3 | % | |||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Sales and marketing | 230.5 | 43.8 | % | 240.3 | 45.6 | % | |||||||||||||||||

| General and administrative | 39.4 | 7.5 | % | 41.3 | 7.8 | % | |||||||||||||||||

| Research and development | 14.4 | 2.7 | % | 16.3 | 3.1 | % | |||||||||||||||||

| Total operating expenses | 284.3 | 54.0 | % | 297.9 | 56.5 | % | |||||||||||||||||

| Operating income | 25.9 | 4.9 | % | 4.4 | 0.8 | % | |||||||||||||||||

| Interest expense, net | 9.1 | 1.7 | % | 2.1 | 0.4 | % | |||||||||||||||||

| Income before income taxes | 16.8 | 3.2 | % | 2.3 | 0.4 | % | |||||||||||||||||

| Income tax expense | 5.4 | 1.0 | % | 0.2 | 0.0 | % | |||||||||||||||||

| Net income | $ | 11.5 | 2.2 | % | $ | 2.1 | 0.4 | % | |||||||||||||||

| Net income per share: | |||||||||||||||||||||||

| Basic | $ | 0.51 | $ | 0.09 | |||||||||||||||||||

| Diluted | $ | 0.51 | $ | 0.09 | |||||||||||||||||||

| Weighted-average number of common shares: | |||||||||||||||||||||||

| Basic | 22.3 | 22.8 | |||||||||||||||||||||

| Diluted | 22.6 | 23.6 | |||||||||||||||||||||

The percentage of total net sales, by dollar volume, was as follows:

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Retail stores | 87.1 | % | 84.3 | % | |||||||

| Online, phone, chat and other | 12.9 | % | 15.7 | % | |||||||

| Total Company | 100.0 | % | 100.0 | % | |||||||

The components of total net sales change, including comparable net sales changes, were as follows:

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Sales change rates: | |||||||||||

Retail comparable-store sales (1) | 1 | % | (14 | %) | |||||||

| Online, phone and chat | (18 | %) | 5 | % | |||||||

Total Retail comparable sales change (1) | (2 | %) | (11 | %) | |||||||

| Net opened/closed stores and other | 2 | % | 4 | % | |||||||

| Total Company | 0 | % | (7 | %) | |||||||

___________________________

(1)Stores are included in the comparable-store calculations in the 13th full month of operations. Stores that have been remodeled or repositioned within the same shopping center remain in the comparable-store base.

16 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Other sales metrics were as follows:

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

Average sales per store (1) (in thousands) | $ | 3,239 | $ | 3,487 | |||||||

Average sales per square foot (1) | $ | 1,060 | $ | 1,167 | |||||||

Stores > $2 million in net sales (2) | 75 | % | 82 | % | |||||||

Stores > $3 million in net sales (2) | 36 | % | 46 | % | |||||||

Average revenue per smart bed unit (3) | $ | 5,848 | $ | 4,905 | |||||||

___________________________

(1)Trailing-twelve months Total Retail comparable sales per store open at least one year.

(2)Trailing-twelve months for stores open at least one year (excludes online, phone and chat sales).

(3)Represents Total Retail net sales divided by Total Retail smart bed units.

The number of retail stores operating was as follows:

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Beginning of period | 670 | 648 | |||||||||

| Opened | 12 | 13 | |||||||||

| Closed | (11) | (8) | |||||||||

| End of period | 671 | 653 | |||||||||

17 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Comparison of Three Months Ended April 1, 2023 with Three Months Ended April 2, 2022

Net sales

Net sales for the three months ended April 1, 2023 of $527 million were consistent with the same period one year ago. Demand was impacted by historically low consumer sentiment.

The net sales change consisted primarily of a 2% comparable sales decrease in Total Retail offset by additional sales from 18 net new stores opened in the past 12 months that added 2 percentage points (ppt.) of growth.

The $0.6 million net sales decrease compared with the same period one year ago was comprised of the following: (i) a $10.6 million decrease in Total Retail comparable net sales; offset by (ii) a $10.0 million increase from net store openings. Total Retail smart bed unit sales decreased 16% compared with the prior year. Total Retail average revenue per smart bed unit increased by 19% to $5,848, compared with $4,905 in the prior-year period. Prior year average revenue per smart bed unit was impacted by a less favorable sales mix due to supply constraints impacting adjustable bases and smart bed deliveries at the higher end of the Company’s product line.

Gross profit

Gross profit of $310 million for the three months ended April 1, 2023 increased by $8 million, or 3%, compared with $302 million for the same period one year ago. The gross profit rate increased to 58.9% of net sales for the three months ended April 1, 2023, compared with 57.3% for the prior-year comparable period.

The current-year gross profit rate increase of 1.6 ppt. was mainly due to: (i) pricing actions taken over the past twelve months (1.8 ppt.); (ii) improvement in commodity prices and operating efficiencies (0.6 ppt.); and (iii) favorable product mix changes (0.6 ppt.); partially offset by (iv) incremental logistics and delivery costs including labor inflation and investments in our distribution network (0.5 ppt.); (v) 16% lower delivered smart bed volume (0.3 ppt.); and (vi) higher performance-based incentive compensation (0.2 ppt.). In addition, the gross profit rate will fluctuate from quarter to quarter due to a variety of other factors, including warranty expenses, and return and exchange costs.

Sales and marketing expenses

Sales and marketing expenses for the three months ended April 1, 2023 were $230 million, or 43.8% of net sales, compared with $240 million, or 45.6% of net sales, for the same period one year ago. The current-year sales and marketing expenses rate decrease of 1.8 ppt. was primarily due to lower media expense with a decrease in spend of 11% year-over-year.

General and administrative expenses

General and administrative (G&A) expenses totaled $39 million, or 7.5% of net sales, for the three months ended April 1, 2023, compared with $41 million, or 7.8% of net sales, in the prior-year period. The $1.9 million decrease in G&A expenses consisted mainly of: (i) $2.4 million reduction in employee compensation on lower headcount; (ii) a $0.8 million reduction in professional and consulting fees; (iii) a $0.5 million decrease in travel and training expenses; and (iv) a $1.9 million net decrease in other miscellaneous expenses; partially offset by (v) a $3.7 million increase in company-wide performance-based incentive compensation. The G&A expenses rate decreased by 0.3 ppt. in the current-year period, compared with the same period one year ago due to the items discussed above.

Research and development expenses

Research and development (R&D) expenses decreased to $14 million for the three months ended April 1, 2023, compared with $16 million with the same period last year on lower headcount. The Company continues to maintain a flexible mindset, to capitalize on profitable opportunities as the environment improves, and deliver tangible life-long health benefits for Smart Sleepers.

18 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Interest expense

Interest expense, net increased to $9 million for the three months ended April 1, 2023, compared with $2 million for the same period one year ago. The $7 million increase was mainly driven by a higher weighted-average interest rate compared with the same period one year ago.

Income tax expense

Income tax expense totaled $5 million for the three months ended April 1, 2023, compared with $0.2 million last year. The effective income tax rate for the three months ended April 1, 2023 was 31.9%, compared with 9.4% for the comparable period last year. Discrete tax expenses, primarily stock-based compensation excess tax expense, were $0.8 million for the three months ended April 1, 2023, compared with discrete tax benefits of $0.4 million in last year’s first quarter.

Liquidity and Capital Resources

Managing liquidity and capital resources is an important part of the Company’s commitment to deliver superior shareholder value over time. The Company’s primary sources of liquidity are cash flows provided by operating activities and cash available under its $825 million revolving credit facility. As of April 1, 2023, the Company does not have any off-balance sheet financing other than its $7 million in outstanding letters of credit. The cash generated from ongoing operations and cash available under the revolving credit facility are expected to be adequate to maintain operations, and fund anticipated expansion, strategic initiatives and contractual obligations such as lease payments and capital commitments for new retail stores for the foreseeable future.

Changes in cash and cash equivalents during the three months ended April 1, 2023 primarily consisted of $19 million of cash provided by operating activities offset by $16 million of cash used to purchase property and equipment, and $3 million of cash used to repurchase its common stock (based on settlement, in connection with the vesting of employee restricted stock grants).

The following table summarizes cash flows (in millions). Amounts may not add due to rounding differences:

| Three Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Total cash provided by (used in): | |||||||||||

| Operating activities | $ | 18.6 | $ | 24.6 | |||||||

| Investing activities | (15.6) | (19.6) | |||||||||

| Financing activities | (3.4) | (5.8) | |||||||||

| Net decrease in cash and cash equivalents | $ | (0.3) | $ | (0.8) | |||||||

Cash provided by operating activities for the three months ended April 1, 2023 was $19 million, compared with $25 million for the three months ended April 2, 2022. Significant components of the year-over-year change in cash provided by operating activities included: (i) a $9 million increase in net income for the three months ended April 1, 2023, compared with the same period one year ago; (ii) a $25 million fluctuation in accrued compensation and benefits primarily related to year-over-year changes in company-wide performance-based compensation that was earned in 2021 and paid in the first quarter of 2022, compared with no company-wide performance-based compensation earned in 2022 and paid in the first quarter of 2023; (iii) a $17 million fluctuation in customer prepayments due to timing of deliveries; and (iv) a $22 million fluctuation in prepaid expenses and other assets primarily due to the amount and timing of rebate payments.

Net cash used in investing activities to purchase property and equipment was $16 million for the three months ended April 1, 2023, compared with $20 million for the same period one year ago. The year-over-year decrease was primarily due to the timing of cash flows associated with investments in information technology.

Net cash used in financing activities was $3 million for the three months ended April 1, 2023, compared with $6 million for the same period last year. During the three months ended April 1, 2023, the Company repurchased $3 million of its stock (based on settlement dates, in connection with the vesting of employee restricted stock awards), compared with $51 million (based on settlement dates, $42 million under the Board-approved share repurchase program and $9 million

19 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

in connection with the vesting of employee restricted stock awards) during the same period one year ago. Short-term borrowings decreased by $0.4 million during the current-year period due to an $11.0 million increase in borrowings under the revolving credit facility to $471 million offset by an $11.4 million decrease in book overdrafts which are included in the net change in short-term borrowings. Short-term borrowings increased by $45 million during the prior-year period due to a $31 million increase in borrowings under the credit facility to $413 million and a $14 million increase in book overdrafts.

With the incremental macroeconomic pressures, in the second quarter of fiscal 2022, the Company suspended share repurchases under its Board-approved share repurchase program. At April 1, 2023, there was $348 million remaining authorization under the Board-approved $600 million share repurchase program. There is no expiration date governing the period over which the Company can repurchase shares.

The Company has a credit facility (Credit Agreement) which is for general corporate purposes, to meet its seasonal working capital requirements and to repurchase its stock. The Company amended the Credit Agreement on October 26, 2022. The amendment, among other things, (a) provides relief from the requirement that the net leverage ratio not exceed 3.75x for certain corporate actions including Permitted Capital Distributions for Performance or Taxes (as defined in the Credit Agreement) and certain acquisition activity; (b) increases the permissible net leverage ratio to 5.0x for the three consecutive quarterly reporting periods ending July 1, 2023; (c) increases the commitment fee rate to 50 basis points and the margin applicable to interest rates for all borrowings by an additional 50 basis points, in each case if the net leverage ratio is greater than or equal to 4.5x; and (d) replaces the option to borrow at an interest rate based on London Interbank Offered Rate (LIBOR) to one based on a Term SOFR Rate. The Term SOFR Rate equals the sum of (x) the Term SOFR Screen Rate (as defined in the Credit Agreement) for the applicable interest period (but in no event less than zero), plus (y) 0.10%, plus (z) the margin based on Sleep Number’s net leverage ratio. Under the terms of the Credit agreement, the Company pays a variable rate of interest and a commitment fee based on its leverage ratio.

At April 1, 2023, the Company had $471 million of borrowings under its revolving credit facility, $7 million in outstanding letters of credit and net liquidity available under the credit facility of $347 million. At April 1, 2023, the Company’s leverage ratio as defined in the credit agreement was 4.0x, the weighted-average interest rate on borrowings under the credit facility was 7.1% and the Company was in compliance with all financial covenants.

Sleep Number has an agreement with Synchrony Bank to offer qualified customers revolving credit arrangements to finance their purchases from the Company (Synchrony Agreement). The Synchrony Agreement contains financial covenants consistent with the credit facility, including a maximum net leverage ratio and a minimum interest coverage ratio. As of April 1, 2023, the Company was in compliance with all financial covenants.

20 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Non-GAAP Data Reconciliations

Earnings before Interest, Taxes, Depreciation and Amortization (Adjusted EBITDA)

The Company defines earnings before interest, taxes, depreciation and amortization (Adjusted EBITDA) as net income plus: income tax expense, interest expense, depreciation and amortization, stock-based compensation and asset impairments. Management believes Adjusted EBITDA is a useful indicator of its financial performance and its ability to generate cash from operating activities. The Company’s definition of Adjusted EBITDA may not be comparable to similarly titled definitions used by other companies. The table below reconciles Adjusted EBITDA, which is a non-GAAP financial measure, to the comparable GAAP financial measure.

Adjusted EBITDA calculations are as follows (in thousands):

| Three Months Ended | Trailing-Twelve Months Ended | ||||||||||||||||||||||

| April 1, 2023 | April 2, 2022 | April 1, 2023 | April 2, 2022 | ||||||||||||||||||||

| Net income | $ | 11,465 | $ | 2,074 | $ | 46,001 | $ | 89,186 | |||||||||||||||

| Income tax expense | 5,366 | 214 | 17,437 | 24,947 | |||||||||||||||||||

| Interest expense | 9,102 | 2,127 | 25,960 | 7,394 | |||||||||||||||||||

| Depreciation and amortization | 17,991 | 15,683 | 68,934 | 60,943 | |||||||||||||||||||

| Stock-based compensation | 4,639 | 4,133 | 13,729 | 20,930 | |||||||||||||||||||

| Asset impairments | 12 | 103 | 204 | 186 | |||||||||||||||||||

| Adjusted EBITDA | $ | 48,575 | $ | 24,334 | $ | 172,265 | $ | 203,586 | |||||||||||||||

Free Cash Flow

The Company’s “free cash flow” data is considered a non-GAAP financial measure and is not in accordance with, or preferable to, “net cash provided by operating activities,” or GAAP financial data. However, the Company is providing this information as it believes it facilitates analysis for investors and financial analysts.

The following table summarizes free cash flow calculations (in thousands):

| Three Months Ended | Trailing-Twelve Months Ended | ||||||||||||||||||||||

| April 1, 2023 | April 2, 2022 | April 1, 2023 | April 2, 2022 | ||||||||||||||||||||

| Net cash provided by operating activities | $ | 18,581 | $ | 24,558 | $ | 30,161 | $ | 212,970 | |||||||||||||||

| Subtract: Purchases of property and equipment | 15,556 | 19,604 | 65,406 | 74,958 | |||||||||||||||||||

| Free cash flow | $ | 3,025 | $ | 4,954 | $ | (35,245) | $ | 138,012 | |||||||||||||||

21 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Non-GAAP Data Reconciliations (continued)

Return on Invested Capital (Adjusted ROIC)

(dollars in thousands)

Adjusted ROIC is a financial measure the Company uses to determine how efficiently it deploys its capital. It quantifies the return the Company earns on its adjusted invested capital. Management believes Adjusted ROIC is also a useful metric for investors and financial analysts. The Company computes Adjusted ROIC as outlined below. Its definition and calculation of Adjusted ROIC may not be comparable to similarly titled definitions and calculations used by other companies.

The tables below reconcile adjusted net operating profit after taxes (Adjusted NOPAT) and total adjusted invested capital, which are non-GAAP financial measures, to the comparable GAAP financial measures (in thousands):

| Trailing-Twelve Months Ended | |||||||||||

| April 1, 2023 | April 2, 2022 | ||||||||||

| Adjusted net operating profit after taxes (Adjusted NOPAT) | |||||||||||

| Operating income | $ | 89,398 | $ | 121,527 | |||||||

Add: Operating lease expense (1) | 26,487 | 24,907 | |||||||||

Less: Income taxes (2) | (29,674) | (34,753) | |||||||||

| Adjusted NOPAT | $ | 86,211 | $ | 111,681 | |||||||

| Average adjusted invested capital | |||||||||||

| Total deficit | $ | (425,047) | $ | (469,213) | |||||||

Add: Long-term debt (3) | 470,991 | 413,709 | |||||||||

Add: Operating lease obligations (4) | 436,939 | 412,574 | |||||||||

| Total adjusted invested capital at end of period | $ | 482,883 | $ | 357,070 | |||||||

Average adjusted invested capital (5) | $ | 423,287 | $ | 348,804 | |||||||

Adjusted return on invested capital (Adjusted ROIC) (6) | 20.4 | % | 32.0 | % | |||||||

___________________________

(1) Represents the interest expense component of lease expense included in the Company’s financial statements under ASC 842, Leases.

(2) Reflects annual effective income tax rates, before discrete adjustments, of 25.6% and 23.7% for April 1, 2023 and April 2, 2022, respectively.

(3) Long-term debt includes existing finance lease liabilities.

(4) Reflects operating lease liabilities included in the Company’s financial statements under ASC 842.

(5) Average adjusted invested capital represents the average of the last five fiscal quarters’ ending adjusted invested capital balances.

(6) Adjusted ROIC equals Adjusted NOPAT divided by average adjusted invested capital.

Note - the Company’s ROIC calculation and data are considered non-GAAP financial measures and are not in accordance with, or preferable to, GAAP financial data. However, the Company is providing this information as it believe it facilitates analysis of the Company's financial performance by investors and financial analysts. The Company updated its Adjusted ROIC calculation effective beginning with the reporting period ended December 31, 2022, to reflect adjustments consistent with ASC 842. The prior period has been updated to reflect this calculation.

GAAP - generally accepted accounting principles in the U.S.

22 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

Off-Balance-Sheet Arrangements

As of April 1, 2023, the Company was not involved in any unconsolidated special purpose entity transactions. Other than it’s $7 million in outstanding letters of credit, the Company does not have any off-balance-sheet financing.

There have been no material changes in the Company’s contractual obligations since the end of fiscal 2022. See Note 5, Credit Agreement, of the Notes to the Condensed Consolidated Financial Statements for information regarding the Company’s credit agreement. See the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022 for additional information regarding its other contractual obligations.

Critical Accounting Policies

The Company discusses its critical accounting policies and estimates in Management’s Discussion and Analysis of Financial Condition and Results of Operations in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2022. There were no significant changes in the Company’s critical accounting policies since the end of fiscal 2022.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The Company is exposed to changes in market-based short-term interest rates that will impact net interest expense. If overall interest rates were one percentage point higher than current rates, annual net income would decrease by $3.4 million based on the $471 million of borrowings under the credit facility at April 1, 2023. The Company does not manage the interest-rate volatility risk of borrowings under the credit facility through the use of derivative instruments.

ITEM 4. CONTROLS AND PROCEDURES

Conclusions Regarding the Effectiveness of Disclosure Controls and Procedures

The Company maintains disclosure controls and procedures, as defined in Exchange Act Rule 13a-15(e), that are designed to ensure that information required to be disclosed by the Company in the reports that it files or submits under the Securities Exchange Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission’s rules and forms, and that such information is accumulated and communicated to the Company’s management, including its principal executive officer and principal financial officer, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure. The Company’s management, with the participation of its principal executive officer and principal financial officer, evaluated the effectiveness of the design and operation of the Company’s disclosure controls and procedures as of the end of the period covered by this quarterly report. Based on this evaluation, its principal executive officer and principal financial officer concluded that the Company’s disclosure controls and procedures were effective as of the end of the period covered by this quarterly report.

Changes in Internal Control

There were no changes in the Company’s internal control over financial reporting during the fiscal quarter ended April 1, 2023, that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

23 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

PART II: OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS

The Company’s legal proceedings are discussed in Note 12, Commitments and Contingencies, Legal Proceedings, in the Notes to Condensed Consolidated Financial Statements in this Quarterly Report on Form 10-Q.

ITEM 1A. RISK FACTORS

In addition to the risks discussed below and other information set forth in this Quarterly Report on Form 10-Q, the Company’s business, financial condition and operating results are subject to a number of risks and uncertainties, including both those that are specific to the Company’s business and others that affect all businesses operating in a global environment. Investors should carefully consider the information in this report under the heading, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and also the information under the heading, Risk Factors, in the Company’s most recent Annual Report on Form 10-K. The risk factors discussed in the Annual Report on Form 10-K and in this Quarterly Report on Form 10-Q do not identify all risks that the Company faces because its business operations could also be affected by additional risk factors that are not presently known to the Company or that it currently considers to be immaterial to its operations.

Bank failures or other events affecting financial institutions could adversely affect our liquidity and financial performance.

The recent and potential future disruptions in access to bank deposits or lending commitments due to bank failures and banking industry instability could materially and adversely affect the Company’s liquidity, access to cash and credit, and the Company’s business, financial condition and results of operations, as well those of the Company’s third-party suppliers or vendors. The recent closures of Silicon Valley Bank (SVB) and Signature Bank and their placement into receivership with the Federal Deposit Insurance Company (FDIC) along with the FDIC’s seizure and sale of First Republic Bank created market disruption and uncertainty with respect to the financial condition of a number of other banking institutions in the United States. While the Company does not have any direct exposure to SVB, Signature Bank, or First Republic Bank, the Company does maintain its cash at financial institutions, occasionally in balances that exceed the current FDIC insurance limits.

If other banks and financial institutions enter receivership or become insolvent in the future due to financial conditions affecting the banking system and financial markets, the Company’s ability to access its cash and cash equivalents, including transferring funds, making payments or receiving funds, and the Company’s access to credit, as well as those of its third-party suppliers or vendors, may be threatened and could have a material adverse effect on the Company’s business and financial condition.

24 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

(a) – (b) Not applicable.

(c) Issuer Purchases of Equity Securities

| Period | Total Number of Shares Purchased(1)(2) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs(1) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs(3) | ||||||||||||||||||||||

| January 1, 2023 through January 28, 2023 | 131 | $ | 34.13 | — | $ | 348,071,000 | ||||||||||||||||||||

| January 29, 2023 through February 25, 2023 | 445 | $ | 35.53 | — | $ | 348,071,000 | ||||||||||||||||||||

| February 26, 2023 through April 1, 2023 | 117,662 | $ | 28.42 | — | $ | 348,071,000 | ||||||||||||||||||||

| Total | 118,238 | $ | 28.45 | — | $ | 348,071,000 | ||||||||||||||||||||

___________________________

(1)The Company did not purchase any shares under its Board-approved $600 million share repurchase program (effective April 4, 2021), during the three months ended April 1, 2023.

(2)In connection with the vesting of employee restricted stock grants, the Company repurchased 118,238 shares of its common stock at a cost of $3.4 million during the three months ended April 1, 2023.

(3)There is no expiration date governing the period over which the Company can repurchase shares under it’s Board-approved share repurchase program. Any repurchased shares are constructively retired and returned to an unissued status.

ITEM 3. DEFAULTS UPON SENIOR SECURITIES

Not applicable.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

ITEM 5. OTHER INFORMATION

Not applicable.

25 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

ITEM 6. EXHIBITS

| Exhibit Number | Description | |||||||

10.1*† | ||||||||

10.2*† | ||||||||

| 10.3*† | ||||||||

| 10.4* | ||||||||

| 31.1* | ||||||||

| 31.2* | ||||||||

| 32.1* | ||||||||

| 32.2* | ||||||||

| 101.INS* | Inline XBRL Instance Document – the instance document does not appear in the Interactive Data File because its XBRL tags are embedded within the Inline XBRL document | |||||||

| 101.SCH* | Inline XBRL Taxonomy Extension Schema Document | |||||||

| 101.CAL* | Inline XBRL Taxonomy Extension Calculation Linkbase Document | |||||||

| 101.DEF* | Inline XBRL Taxonomy Extension Definition Linkbase Document | |||||||

| 101.LAB* | Inline XBRL Taxonomy Extension Label Linkbase Document | |||||||

| 101.PRE* | Inline XBRL Taxonomy Extension Presentation Linkbase Document | |||||||

| 104* | Cover Page Interactive Data File (formatted as inline XBRL and contained in Exhibit 101) | |||||||

* Filed Herein.

† Management contract or compensatory plan or arrangement.

(1) Portions of this exhibit have been redacted in compliance with Regulation S-K Item 601(b)(10).

26 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

SIGNATURES

Pursuant to the requirements of the Securities and Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| SLEEP NUMBER CORPORATION | |||||||||||

| (Registrant) | |||||||||||

| Dated: | May 9, 2023 | By: | /s/ Shelly R. Ibach | ||||||||

| Shelly R. Ibach | |||||||||||

| Chief Executive Officer | |||||||||||

| (principal executive officer) | |||||||||||

| By: | /s/ Joel J. Laing | ||||||||||

| Joel J. Laing | |||||||||||

| Chief Accounting Officer | |||||||||||

| (principal accounting officer) | |||||||||||

27 | 1Q 2023 FORM 10-Q | SLEEP NUMBER CORPORATION | |||||||

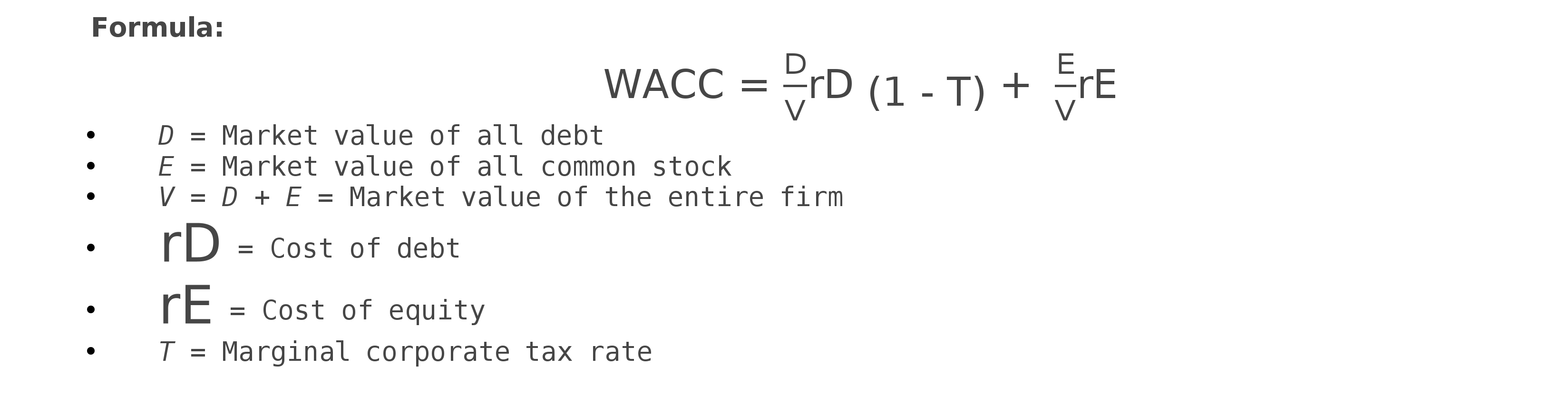

WACC is an approximation of the average rate of return a company expects to compensate all of its different investors. The WACC formula and key assumptions used in the Company’s WACC calculation are outlined below:

WACC is an approximation of the average rate of return a company expects to compensate all of its different investors. The WACC formula and key assumptions used in the Company’s WACC calculation are outlined below: