UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the fiscal year ended December 31, 2021

or

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

Commission File Number: 001-09819

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

| (Registrant’s telephone number, including area code) | ||||||||||||||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of June 30, 2021, the aggregate market value of the common stock held by non-affiliates of the registrant was approximately $626,912,407 based on the closing sales price on the New York Stock Exchange of $18.66.

On February 25, 2022, the registrant had 36,665,805 shares outstanding of common stock, $0.01 par value, which is the registrant’s only class of common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement for the registrant’s 2022 Annual Meeting of Shareholders, expected to be filed pursuant to Regulation 14A within 120 days from December 31, 2021, are incorporated by reference into Part III of this Annual report on Form 10-K to the extent stated herein.

DYNEX CAPITAL, INC.

FORM 10-K

TABLE OF CONTENTS

| Page | |||||||||||

PART I. | |||||||||||

| Item 1. | Business | ||||||||||

| Item 1A. | Risk Factors | ||||||||||

| Item 1B. | Unresolved Staff Comments | ||||||||||

| Item 2. | Properties | ||||||||||

| Item 3. | Legal Proceedings | ||||||||||

| Item 4. | Mine Safety Disclosures | ||||||||||

| PART II. | |||||||||||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities | ||||||||||

| Item 6. | [Reserved] | ||||||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||

| Item 8. | Financial Statements and Supplementary Data | ||||||||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||||||||||

| Item 9A. | Controls and Procedures | ||||||||||

| Item 9B. | Other Information | ||||||||||

| Item 9C. | Disclosure Regarding Foreign Jurisdictions That Prevent Inspections | ||||||||||

| PART III. | |||||||||||

| Item 10. | Directors, Executive Officers and Corporate Governance | ||||||||||

| Item 11. | Executive Compensation | ||||||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | ||||||||||

| Item 14. | Principal Accountant Fees and Services | ||||||||||

| PART IV. | |||||||||||

| Item 15. | Exhibits and Financial Statement Schedules | ||||||||||

| Item 16. | Form 10-K Summary | ||||||||||

| SIGNATURES | |||||||||||

i

CAUTIONARY STATEMENT – This Annual Report on Form 10-K contains “forward-looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended (or “1933 Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (or “Exchange Act”). We caution that any such forward-looking statements made by us are not guarantees of future performance, and actual results may differ materially from those expressed or implied in such forward-looking statements. Some of the factors that could cause actual results to differ materially from estimates expressed or implied in our forward-looking statements are set forth in this Annual Report on Form 10-K for the year ended December 31, 2021. See Item 1A. “Risk Factors” as well as “Forward-Looking Statements” set forth in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report on Form 10-K.

In this Annual Report on Form 10-K, we refer to Dynex Capital, Inc. and its subsidiaries as the "Company,” “we,” “us,” or “our,” unless we specifically state otherwise or the context indicates otherwise.

PART I.

ITEM 1. BUSINESS

COMPANY OVERVIEW

Dynex Capital, Inc. commenced operations in 1988 and is an internally managed mortgage real estate investment trust (“REIT”), which primarily invests in residential and commercial mortgage-backed securities (“MBS”). We finance our investments principally with borrowings under repurchase agreements. Our objective is to provide attractive risk-adjusted returns to our shareholders over the long term that are reflective of a leveraged, high quality fixed income portfolio with a focus on capital preservation. We seek to provide returns to our shareholders primarily through the payment of regular dividends and through capital appreciation of our investments.

We are primarily invested in Agency MBS including residential MBS (“RMBS”), commercial MBS (“CMBS”) and CMBS interest-only (“IO”) securities. Agency MBS have an implicit guaranty of principal payment by an agency of the U.S. government or a U.S. government-sponsored entity (“GSE”) such as Fannie Mae and Freddie Mac. We also have investments in non-Agency MBS, which consist mainly of CMBS IO. Non-Agency MBS are issued by non-governmental enterprises and do not have a guaranty of principal payment.

INVESTMENT STRATEGY

Our investment strategy and the allocation of our capital to a particular sector or investment is driven by a “top-down” framework that focuses on the risk management, scenario analysis, and expected risk-adjusted returns of any investment. Key points of this framework include the following:

•understanding macroeconomic factors, including monetary and fiscal policies, and possible evolving outcomes, including but not limited to, the current state of the U.S. and global economies;

•understanding the regulatory environment, competition for assets, and the terms and availability of financing;

•sector analysis including understanding absolute returns, relative and risk-adjusted returns, and supply/demand metrics within each sector;

•security and financing analysis including sensitivity analysis on credit, interest rate volatility, liquidity, and market value risk; and

•managing performance and inherent portfolio risks, including but not limited to interest rate, credit, prepayment, and liquidity risks.

In allocating our capital and executing our strategy, we seek to balance the risks of owning specific types of investments with the earnings opportunity on the investment. At various times during the last decade, we have allocated capital to a variety of investments including adjustable-rate and fixed-rate Agency RMBS, Agency CMBS, investment grade and unrated non-Agency RMBS and CMBS, Agency and non-Agency CMBS IO, and residual interests in securitized mortgage loans. Our investments in non-Agency MBS are generally higher quality senior or mezzanine classes (typically rated 'A' or better by one or more of the nationally recognized statistical rating organizations) because they are typically more liquid (i.e., they are more easily converted into cash either through sales

1

or pledges as collateral for repurchase agreement borrowings) and have less exposure to credit losses than lower-rated non-Agency MBS. We regularly review our existing operations to determine whether our investment strategy or business model should change, including through capital reallocation, changing our targeted investments as well as hedging instruments, and shifting our risk position.

From time to time, we will analyze and evaluate potential business opportunities that we identify or are presented to us, including possible partnerships, mergers, acquisitions, or divestiture transactions that might be a strategic fit for our investment strategy or asset allocation or otherwise maximize value for our shareholders. Pursuing such an opportunity or transaction could require us to issue additional equity or debt securities.

The performance of our investment portfolio will depend on many factors including but not limited to interest rates, trends of interest rates, the steepness of interest rate curves, prepayment rates on our investments, demand for our investments, general market liquidity, economic and global political conditions, and the credit performance of our investments. In addition, our business model may be impacted by other factors such as the condition of the overall credit markets, which could impact the availability and costs of financing. See “Factors that Affect Our Results of Operations and Financial Condition” below, Item 1A of Part I, “Risk Factors”, and Item 7A of Part II, “Quantitative and Qualitative Disclosures About Market Risk” of this Annual Report on Form 10-K for further discussion.

RMBS. As of December 31, 2021, the majority of our investments in RMBS were Agency-issued pass-through securities collateralized primarily by pools of fixed-rate single-family mortgage loans. Monthly payments of principal and interest made by the individual borrowers on the mortgage loans underlying the pools are "passed through" to the security holders, after deducting GSE or U.S. Government agency guarantee and servicer fees. Mortgage pass-through certificates generally distribute cash flows from the underlying collateral on a pro-rata basis among the security holders. Security holders also receive guarantor advances of principal and interest for delinquent loans in the mortgage pools.

We also purchase to-be-announced securities (“TBAs” or “TBA securities”) as a means of investing in non-specified fixed-rate Agency RMBS, and from time to time, we may also sell TBA securities as a means of economically hedging our book value exposure to Agency RMBS. A TBA security is a forward contract (“TBA contract”) for the purchase (“long position”) or sale (“short position”) of a fixed-rate Agency MBS at a predetermined price with certain principal and interest terms and certain types of collateral. The actual Agency securities to be delivered are not identified until approximately 2 days before the settlement date. We hold long and short positions in TBA securities by executing a series of transactions, commonly referred to as “dollar roll” transactions, which effectively delay the settlement of a forward purchase (or sale) of a non-specified Agency RMBS by entering into an offsetting TBA position, net settling the paired-off positions in cash, and simultaneously entering into an identical TBA long (or short) position with a later settlement date. TBAs purchased or sold for a forward settlement date are generally priced at a discount relative to TBAs settling in the current month. This price difference, often referred to as “drop income”, represents the economic equivalent of net interest income (interest income less implied financing cost) on the underlying Agency security from trade date to settlement date. We account for all TBAs (whether net long or net short positions, or collectively “TBA dollar roll positions”) as derivative instruments because we cannot assert that it is probable at inception and throughout the term of an individual TBA transaction that its settlement will result in physical delivery of the underlying Agency RMBS, or that the individual TBA transaction will not settle in the shortest period possible.

CMBS. Substantially all of our CMBS investments as of December 31, 2021 were fixed-rate Agency-issued securities backed by multifamily housing loans. The loans underlying CMBS are generally fixed-rate with scheduled principal payments generally assuming a 30-year amortization period, but typically requiring balloon payments on average approximately 10 years from origination. These loans typically have some form of prepayment protection provisions (such as prepayment lock-out) or prepayment compensation provisions (such as yield maintenance or prepayment penalty), which provide us compensation if underlying loans prepay prior to us earning our expected return on our investment. Yield maintenance and prepayment penalty requirements are intended to create an economic disincentive for the loans to prepay, which we believe makes CMBS less costly to hedge relative to RMBS.

2

CMBS IO. CMBS IO are interest-only securities issued as part of a CMBS securitization and represent the right to receive a portion of the monthly interest payments (but not principal cash flows) on the unpaid principal balance of the underlying pool of commercial mortgage loans. We invest in both Agency-issued and non-Agency issued CMBS IO. The loans collateralizing Agency-issued CMBS IO pools are similar in composition to the pools of loans that collateralize CMBS as discussed above. Non-Agency issued CMBS IO are backed by loans secured by a number of different property types including office buildings, hospitality, and retail, among others. Since CMBS IO securities have no principal associated with them, the interest payments received are based on the unpaid principal balance of the underlying pool of mortgage loans, which is often referred to as the notional amount. Yields on CMBS IO securities are dependent upon the performance of the underlying loans. Similar to CMBS described above, the Company receives prepayment compensation as most loans in these securities have some form of prepayment protection from early repayment; however, there are no prepayment protections if the loan defaults and is partially or wholly repaid earlier because of loss mitigation actions taken by the underlying loan servicer. Because Agency CMBS IO generally contain higher credit quality loans, they have a lower risk of default than non-Agency CMBS IO. The majority of our CMBS IO investments are investment grade-rated with the majority rated ‘AAA’ by at least one of the nationally recognized statistical rating organizations.

FINANCING STRATEGY

We use leverage to enhance the returns on our invested capital by pledging our investments as collateral for borrowings primarily through the use of repurchase agreements. The amount of leverage we utilize depends upon a variety of factors, including but not limited to general economic, political and financial market conditions; the actual and anticipated liquidity and price volatility of our assets; the gap between the duration of assets and liabilities, including hedges; the availability and cost of financing the assets; our opinion of the credit worthiness of financing counterparties; the health of the U.S. residential mortgage and housing markets; our outlook for the level, slope and volatility of interest rates; the credit quality of the loans underlying our investments; the rating assigned to securities; and our outlook for asset spreads. Repurchase agreements generally have original terms to maturity of overnight to six months, though in some instances we may enter into longer-dated maturities depending on market conditions. We pay interest on our repurchase agreement borrowings at a rate usually based on a spread to certain short-term interest rates and fixed for the term of the borrowing. Borrowings under uncommitted repurchase agreements are renewable at the discretion of our lenders and do not contain guaranteed roll-over terms.

Repurchase agreement financing is provided principally by major financial institutions and broker-dealers acting as financial intermediaries for short-term cash investors including money market funds and securities lenders. Repurchase agreement financing exposes us to counterparty risk to such financial intermediaries, principally related to the excess of our collateral pledged over the amount borrowed. We seek to mitigate this risk by spreading our borrowings across a diverse set of repurchase agreement lenders. As of December 31, 2021, we did not have more than 5% of equity at risk with any of our repurchase agreement counterparties. In limited instances, a money market fund or securities lender has directly provided funds to us without the involvement of a financial intermediary typically at a lower cost than we would incur borrowing from the financial intermediary. Borrowing directly from these sources also reduces our risk to the financial intermediaries. Please refer to "Risk Factors-Risks Related to Our Financing and Hedging Activities" in Item 1A of Part I of this Annual Report on Form 10-K for additional information regarding significant risks related to repurchase agreement financing.

HEDGING STRATEGY

We use derivative instruments to economically hedge our exposure to adverse changes in interest rates resulting from our ownership of primarily fixed-rate investments financed with short-term repurchase agreements. Changes in interest rates can impact net interest income, the market value of our investments, and therefore, our book value per common share. In a period of rising interest rates, our earnings and cash flow may be negatively impacted by borrowing costs increasing faster than interest income from our assets, and our book value may decline as a result of declining market values of our MBS.

Our hedging strategy is dynamic and is based on our assessment of U.S. and global economic conditions and monetary policies. We frequently adjust our hedging portfolio based on our expectation of future interest rates,

3

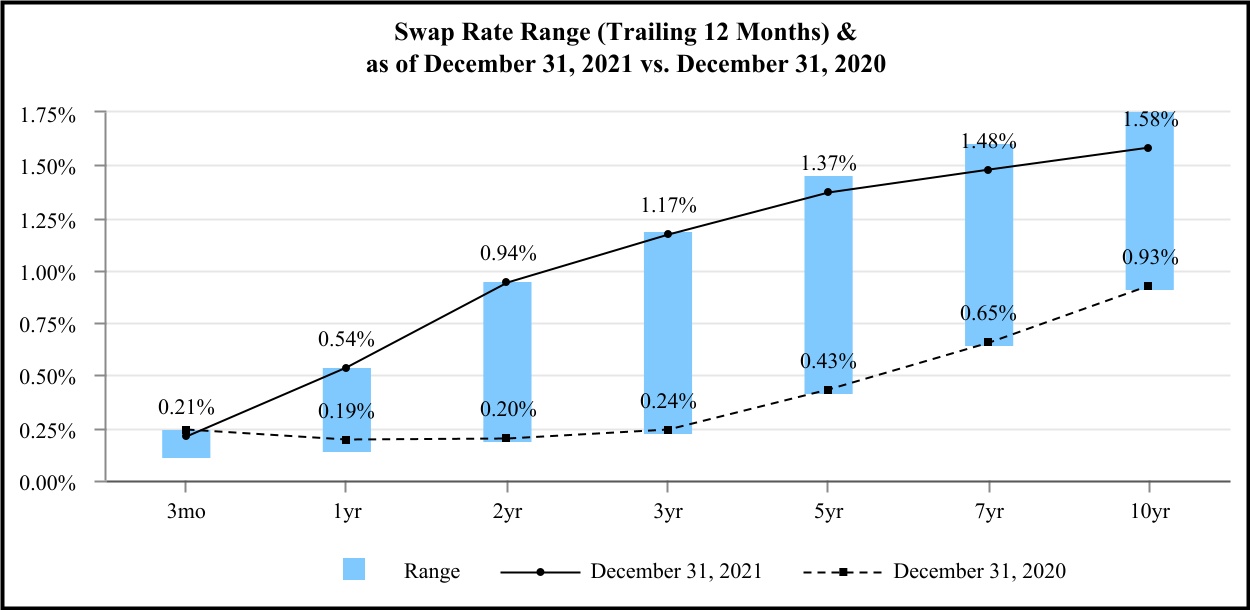

including the absolute level of rates and the slope of the yield curve versus market expectations. During 2021, we primarily used U.S. Treasury futures, options on U.S. Treasury futures, and options on interest rate swaps (“interest rate swaptions”) to mitigate adverse impacts of interest rate changes on our total economic return.

In conducting our hedging activities, we intend to comply with REIT and tax limitations on our hedging instruments which could limit our activities and the instruments that we may use. We also intend to enter into derivative contracts only with the counterparties that we believe have a strong credit rating to mitigate the risk of counterparty default or insolvency.

OPERATING POLICIES AND RISK MANAGEMENT

We invest our capital and manage our risk according to our “Investment Policy” and “Investment Risk Policy”, which are approved by our Board of Directors. These policies set forth investment and risk limitations as they relate to the Company's investment activities and set parameters for the Company's investment and capital allocation decisions. These policies also place limits on certain risks to which we are exposed, such as interest rate risk, prepayment risk, earnings at risk, liquidity risk, and shareholders’ equity at risk from changes in fair value of our investment securities, and also set forth limits for the Company’s overall leverage.

Our Investment Policy currently limits our investment in non-Agency MBS that are rated BBB+ or lower at the time of purchase by any of the nationally recognized statistical ratings organizations to $250 million in market value and limits our shareholders’ equity at risk with respect to such investments to a maximum of $50 million. We also conduct our own independent evaluation of the credit risk on any non-Agency MBS, such that we do not rely solely on the security’s credit rating. Our Investment Risk Policy requires us to perform a variety of stress tests to model the effect of adverse market conditions on our investment portfolio value and our liquidity.

Within the overall limits established by these policies, our investment and capital allocation decisions depend on prevailing market conditions and other factors and may change over time in response to opportunities available in different economic and capital market environments. Our Board of Directors may also adjust Investment and Investment Risk Policies of the Company from time to time based on macroeconomic expectations, market conditions, and risk tolerances among other factors.

In 2021, we entered into a services agreement with a third-party asset manager to license its proprietary trading, portfolio management, and risk reporting system and to provide the Company additional services including trade settlement and investment accounting services. We previously subscribed to this third-party’s risk reporting system, and in 2021, we implemented their trading and portfolio management systems and the trade settlement services. We expect to implement the investment accounting services in 2022. We believe this services agreement is an important step in furthering the foundation for a flexible, scalable, well-controlled and automated operating platform that supports our diversified investment, funding, and hedging strategies. Once this system is fully integrated and implemented into our day-to-day operations, we expect to realize operating efficiencies that should enhance our capability to more effectively manage increases in our capital base and assets under management. Furthermore, this system and relationship should allow us to expand our target asset classes with minimal additional costs.

In addition to the policies described above, we manage our operations and investments to comply with various REIT limitations (as discussed further below in “Operating and Regulatory Structure”) and to avoid qualifying as an investment company as such term is defined in the Investment Company Act of 1940, as amended, (the "1940 Act") or as a commodity pool operator under the Commodity Exchange Act.

Factors that Affect Our Results of Operations and Financial Condition

Our financial performance is largely driven by the performance of our investment portfolio and related financing and hedging activity and may be impacted by a number of factors including, but not limited to, the absolute level of interest rates, the relative slope of interest rate curves, changes in interest rates and market expectations of future interest rates, actual and estimated future prepayment rates on our investments, supply of and competition for investments, the influence of economic conditions on the credit performance of our investments, and market required

4

yields as reflected by market spreads. All of the above factors are influenced by market forces beyond our control such as macroeconomic and geopolitical conditions, market volatility, Federal Reserve policy, U.S. fiscal and regulatory policy, and foreign central bank and government policy. In addition, our business may be impacted by changes in regulatory requirements, including requirements to avoid qualifying as an investment company pursuant to the 1940 Act, and REIT requirements.

Our business model is also impacted by the availability and cost of financing and the state of the overall credit markets. Reductions or limitations in the availability of financing for our investments could significantly impact our business or force us to sell assets, potentially at losses. Disruptions in the repurchase agreement market outside of our control may also directly impact our availability and cost of financing. Repurchase agreement lending by larger U.S. domiciled banks has declined in recent years due to increased regulation and changes to regulatory capital requirements. Their repurchase market participation has been replaced by smaller independent broker dealers that are generally less regulated and by U.S. domiciled broker dealer subsidiaries of foreign financial institutions.

Please refer to Part I, Item 1A, "Risk Factors" as well as Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and Item 7A, "Quantitative and Qualitative Disclosures about Market Risk" of this Annual Report on Form 10-K for additional discussions of factors that have the potential to impact our results of operations and financial condition, including current events such as recent shifts in the Federal Reserve’s monetary policy and market trends.

ENVIRONMENTAL, SOCIAL, AND CORPORATE GOVERNANCE INITIATIVES

We believe that environmental, social, and corporate governance ("ESG") practices and initiatives are important in sustaining and growing the Company. Our ESG practices seek to create value by improving the environment and lives of our employees, investors, business partners, and the community. We assess our practices with a goal of meeting or exceeding industry and peer standards. We continually search for opportunities in pursuit of the long-term success of our business and to enhance the communities where we operate through corporate giving, employee volunteering, human capital development, and environmental sustainability programs.

Our Board of Directors has formal oversight of our ESG strategies, policies, activities, and communications, including for purposes of risk management. We have adopted the Sustainability Accounting Standards Board (“SASB”) Conceptual Framework, and we have made available on our website disclosures in accordance with the Financials Sector standards of the SASB. Additional details regarding our ESG practices and initiatives will also be available in our 2022 proxy statement.

Human Capital Strategy

The Company views its employees as its most important asset and as the key to managing a successful business for the benefit of all of our stakeholders. Our human capital strategy is designed to create an environment where our employees can grow professionally and contribute to the success of the Company. We believe a supportive, collaborative, engaging and equitable culture is key to attracting and retaining skilled, experienced and talented employees as well as fostering the development of the Company’s next generation of leaders.

As of December 31, 2021, we had 19 full and part-time employees. Our voluntary turnover rate was 0% for the three years ended December 31, 2021 and the average tenure of our employees is 14.5 years as of December 31, 2021. None of our employees are covered by any collective bargaining agreements, and we are not aware of any union organizing activity relating to our employees.

Diversity and Inclusion

We promote diversity within our workforce and believe diversity extends beyond gender, race, ethnicity, age and sexual orientation to include different perspectives, skills, and experiences and socioeconomic backgrounds. We hire based on qualifications and evaluate, recognize, reward and promote employees based on performance without regard to race, religion, color, national origin, disability, gender, gender identity, sexual orientation, stereotypes or

5

assumptions based thereon. In addition, equity is fundamental to our philosophy of fair and equitable treatment. We regularly review and analyze our compensation practices and engage in ongoing efforts to ensure pay equity within all levels of employment. We strive to maintain a corporate culture that is welcoming, inclusive, and respectful to all.

As of December 31, 2021, 53% of our employees were women or self-identified minorities.

Health, Safety, and Wellness

The Company strives to offer its employees a healthy work-life balance and an open environment in which they are encouraged to offer thoughts and opinions. Employees have a wide selection of resources available to help protect their health, well-being, and financial security, including an on-site gym (with limited access as necessary as a precaution during the COVID-19 pandemic), coverage of a substantial portion of their health insurance, and a competitive 401(k) company match. We provide our employees with access to flexible, comprehensive and convenient medical coverage intended to meet their needs and the needs of their families. In addition to standard medical coverage, we offer employees dental and vision coverage, health savings and flexible spending accounts, paid time off, employee assistance programs, voluntary short-term and long-term disability insurance, term life insurance, and other benefits. In addition, we have historically offered flexible working arrangements to accommodate the individual needs of our employees.

Since the beginning of the COVID-19 pandemic, we have taken precautionary measures and implemented procedures aligned with the Centers for Disease Control and Prevention to protect, manage, and communicate with our workforce to contain the impacts of the virus. Due to the COVID-19 pandemic, all employees are currently encouraged to work from home, and substantially all do, at least on a part-time basis. Like many companies, COVID-19 has increased our focus on health and safety efforts to protect our employees and their families from potential virus exposure, while ensuring that our critical operations remain fully supported.

Employee Development

Recognizing the vital role that human capital management serves in the long-term success of the Company, we have initiated a Human Capital Strategy Planning process, which is overseen by our Board of Directors, to formalize the process for management and development of employees. In addition to talent management and development initiatives, the Human Capital Strategy Planning process has included the following:

•development of organizational core values and a plan to integrate these values into a variety of human

capital processes and practices;

•offering of a personal development program for all employees;

•formalized process for determining current and future human capital requirements;

•implementation of improved performance measures designed to better determine individual and team developmental needs.

COMPETITION

The business models of mortgage REITs range from investing only in Agency MBS to investing substantially in non-investment grade MBS and originating and securitizing mortgage loans and investing in mortgage servicing rights. Some mortgage REITs will invest in RMBS and related investments only, some in CMBS and related investments only, and some in a mix. Each mortgage REIT will assume various types and degrees of risk in its investment strategy. In purchasing investments and obtaining financing, we compete with other mortgage REITs, broker-dealers and investment banking firms, GSEs, mutual funds, banks, hedge funds, mortgage bankers, insurance companies, governmental bodies, including the Federal Reserve, and other entities, many of which have greater financial resources and a lower cost of capital. Increased competition in the market may reduce the available supply of investments and may drive prices of investments to levels which would negatively impact our ability to earn an acceptable amount of income from these investments. Competition can also reduce the availability of borrowing capacity at our repurchase agreement counterparties as such capacity is not unlimited, and many of our repurchase agreement counterparties limit the amount of financing they offer to the mortgage REIT industry.

6

OPERATING AND REGULATORY STRUCTURE

Real Estate Investment Trust Requirements

As a REIT, we are required to abide by certain requirements for qualification as a REIT under the Internal Revenue Code of 1986, as amended (the “Tax Code”). To retain our REIT status, the REIT rules generally require that we invest primarily in real estate-related assets, that our activities be passive rather than active, and that we distribute annually to our shareholders amounts equal to at least 90% of our REIT taxable income, after certain deductions. Dividend distributions to our shareholders in excess of REIT taxable income are considered to be a return of capital to the shareholder.

We use the calendar year for financial reporting in accordance with GAAP as well as for tax purposes. Income determined under GAAP differs from income determined under U.S. federal income tax rules primarily because of temporary differences in income and expense recognition. The primary differences between our GAAP net income and our taxable income are (i) unrealized gains and losses on derivative instruments, which are recognized in net income for GAAP purposes but are excluded from taxable income until realized; and (ii) realized gains and losses on derivatives that are designated as tax hedges which are recognized in net income for GAAP purposes but are deferred and amortized for tax purposes over the original periods hedged by those derivatives (e.g., ten-years for a short position on a ten-year U.S. Treasury futures position). Recognition of deferred tax hedge gains and losses may be accelerated if the underlying instrument originally hedged is terminated or paid off. The following table provides the net deferred tax hedge gains as of December 31, 2021 that have already been recognized in our GAAP earnings but which will be recognized as taxable income (or reduce taxable income) over the periods indicated:

| Tax Year of Recognition for Remaining Hedge Gains (Losses), Net | December 31, 2021 | |||||||

| ($ in thousands) | ||||||||

| 2022 | $ | (1,982) | ||||||

| 2023 - 2025 | 7,281 | |||||||

| 2026 and thereafter | 21,685 | |||||||

| $ | 26,984 | |||||||

We also have tax net operating loss (“NOL”) carryforwards which were all generated prior to January 1, 2018. We have $17.4 million of NOL carryforward remaining as of December 31, 2021, of which $8.1 million will expire in 1 year and the remainder over the following 3 years if not used.

The following table summarizes our dividends declared per share and their related tax characterization for the periods indicated:

7

| Tax Characterization | Total Dividends Declared Per Share | ||||||||||||||||||||||

| Ordinary | Capital Gain | Return of Capital | |||||||||||||||||||||

| Common dividends declared: | |||||||||||||||||||||||

| Year ended December 31, 2021 | $ | 0.07506 | $ | — | $ | 1.48494 | $ | 1.56000 | |||||||||||||||

| Year ended December 31, 2020 | $ | — | $ | 1.66000 | $ | — | $ | 1.66000 | |||||||||||||||

| Preferred Series A dividends declared: | |||||||||||||||||||||||

| Year ended December 31, 2021 | $ | — | $ | — | $ | — | $ | — | |||||||||||||||

| Year ended December 31, 2020 | $ | — | $ | 0.87951 | $ | — | $ | 0.87951 | |||||||||||||||

| Preferred Series B dividends declared: | |||||||||||||||||||||||

| Year ended December 31, 2021 | $ | 0.63012 | $ | — | $ | — | $ | 0.63012 | |||||||||||||||

| Year ended December 31, 2020 | $ | — | $ | 1.90625 | $ | — | $ | 1.90625 | |||||||||||||||

| Preferred Series C dividends declared: | |||||||||||||||||||||||

| Year ended December 31, 2021 | $ | 1.72500 | $ | — | $ | — | $ | 1.72500 | |||||||||||||||

| Year ended December 31, 2020 | $ | — | $ | 1.12150 | $ | — | $ | 1.12150 | |||||||||||||||

Qualification as a REIT

Qualification as a REIT requires that we satisfy a variety of tests relating to our income, assets, distributions and ownership. The significant tests are summarized below.

Sources of Income. To continue qualifying as a REIT, we must satisfy two distinct tests with respect to the sources of our income: the “75% income test” and the “95% income test.” The 75% income test requires that we derive at least 75% of our gross income (excluding gross income from prohibited transactions) from certain real estate-related sources. In order to satisfy the 95% income test, 95% of our gross income for the taxable year must consist of either income that qualifies under the 75% income test or certain other types of passive income.

If we fail to meet either the 75% income test or the 95% income test, or both, in a taxable year, we might nonetheless continue to qualify as a REIT, if our failure was due to reasonable cause and not willful neglect and the nature and amounts of our items of gross income were properly disclosed to the Internal Revenue Service (the “IRS”). However, in such a case we would be required to pay a tax equal to 100% of any excess non-qualifying income.

Nature and Diversification of Assets. At the end of each calendar quarter, we must meet multiple asset tests. Under the “75% asset test,” at least 75% of the value of our total assets must represent cash or cash items (including receivables), government securities or real estate assets. Under the “10% asset test,” we may not own more than 10% of the outstanding voting power or value of securities of any single non-governmental issuer, provided such securities do not qualify under the 75% asset test or relate to taxable REIT subsidiaries. Under the “5% asset test,” ownership of any stocks or securities that do not qualify under the 75% asset test must be limited, in respect of any single non-governmental issuer, to an amount not greater than 5% of the value of our total assets (excluding ownership of any taxable REIT subsidiaries).

If we inadvertently fail to satisfy one or more of the asset tests at the end of a calendar quarter, such failure would not cause us to lose our REIT status, provided that (i) we satisfied all of the asset tests at the close of the preceding calendar quarter and (ii) the discrepancy between the values of our assets and the standards imposed by the asset tests either did not exist immediately after the acquisition of any particular asset or was not wholly or partially caused by such an acquisition. If the condition described in clause (ii) of the preceding sentence was not satisfied, we

8

still could avoid disqualification by eliminating any discrepancy within 30 days after the close of the calendar quarter in which it arose.

Ownership. In order to maintain our REIT status, we must not be deemed to be closely held and must have more than 100 shareholders. The closely held prohibition requires that not more than 50% of the value of our outstanding shares be owned by five or fewer persons at any time during the last half of our taxable year. The "more than 100 shareholders" rule requires that we have at least 100 shareholders for 335 days of a twelve-month taxable year. If we failed to satisfy the ownership requirements, we would be subject to fines and be required to take curative action to meet the ownership requirements in order to maintain our REIT status.

Exemption from Regulation under the Investment Company Act of 1940

We conduct our operations under the exemption provided under Section 3(c)(5)(C) of the 1940 Act, a provision available to companies primarily engaged in the business of purchasing and otherwise acquiring mortgages and other liens on and interests in real estate. According to the U.S. Securities and Exchange Commission (“SEC”) staff no-action letters, companies relying on this exemption must ensure that at least 55% of their assets are mortgage loans and other qualifying assets, and at least 80% of their assets are real estate-related. The 1940 Act requires that we and each of our subsidiaries evaluate our qualification for exemption under the 1940 Act. Our subsidiaries rely either on Section 3(c)(5)(C) of the 1940 Act or other sections that provide exemptions from registering under the 1940 Act, including Sections 3(a)(1)(C) and 3(c)(7). Under the 1940 Act, an investment company is required to register with the SEC and is subject to extensive restrictive and potentially adverse regulations relating to, among other things, operating methods, management, capital structure, leverage, dividends, and transactions with affiliates. We believe that we are operating our business in accordance with the exemption requirements of Section 3(c)(5)(C) of the 1940 Act. Please refer to Item 1A, "Risk Factors" of this Annual Report on Form 10-K for further discussion.

AVAILABLE INFORMATION

We are subject to the reporting requirements of the Exchange Act and its rules and regulations. The Exchange Act requires us to file reports, proxy statements, and other information with the SEC. These materials may be obtained electronically by accessing the SEC’s home page at www.sec.gov.

Our website can be found at www.dynexcapital.com. Our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, are made available free of charge through our website as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC.

Our Code of Conduct is available on our website, along with our Audit Committee Charter, our Whistleblower Policy, our Nominating and Corporate Governance Committee Charter, our Compensation Committee Charter, and our latest ESG disclosures under the SASB framework. We will post on our website amendments to the Code of Conduct or waivers from its provisions, if any, which are applicable to any of our directors or executive officers in accordance with the requirements of the SEC or the NYSE.

The information on our website is not a part of, nor is it incorporated by reference, into this report. Further, our references to the URLs for these websites are intended to be inactive textual references only.

9

ITEM 1A. RISK FACTORS

The following is a discussion of the risk factors that we believe are material to our business. These are factors which, individually or in the aggregate, we think could cause our actual results to differ significantly from anticipated or historical results. In addition to understanding the key risks described below, investors should understand that it is not possible to predict or identify all risk factors, and consequently, the following is not a complete discussion of all potential risks or uncertainties. Additionally, investors should not interpret the disclosure of a risk to imply that the risk has not already materialized.

RISKS RELATED TO OUR INVESTMENT ACTIVITIES

Declines in the market value of our investments could negatively impact our comprehensive income, shareholders’ equity, book value per common share, dividends, and liquidity.

Our investments fluctuate in value due to a number of factors including, among others, market volatility (including, for example, market volatility in the first half of 2020 due to the COVID-19 outbreak), geopolitical events (including, for example, war or other military conflicts, such as the military conflict between Russia and Ukraine) and changes in credit spreads, spot and forward interest rates, and actual and anticipated prepayments. Our investments may also fluctuate in value due to increased or reduced demand for the types of investments we own. The level of demand may be impacted by, among other things, interest rates, capital flows, economic conditions, and government policies and actions, such as purchases and sales by the Federal Reserve.

Changes in credit spreads represent the market’s valuation of the perceived riskiness of assets relative to risk-free rates. Credit spreads change based on a number of factors, including, but not limited to, macroeconomic or systemic factors specific to a particular security such as prepayment performance or credit performance, technical issues such as supply and demand for a particular type of security, market psychology, and Federal Reserve monetary policies. When credit spreads widen, the market value of our investments will decline because market participants typically require additional yield to hold riskier assets.

In addition, the market value of most of our investments will typically decrease as interest rates rise. If market values decrease significantly, we may experience a material reduction in our liquidity if we are forced to sell assets at losses in order to meet margin calls from our lenders to repay or renew repurchase agreements at maturity, or otherwise to maintain our liquidity. A material reduction in our liquidity could lead to a reduction of the dividend or potentially the payment of the dividend in Company stock subject to the Tax Code.

Interest rate fluctuations could negatively impact our net interest income, comprehensive income, book value per common share, dividends, and liquidity.

Interest rate fluctuations impact us in multiple ways. For example, in a period of rising rates, particularly increases in the targeted U.S. Federal Funds Rate (“Federal Funds Rate”), we may experience a decline in our profitability because our borrowing rates may increase faster than the interest coupons on our investments reset or our investments mature. Once the Federal Reserve announces a higher targeted range or if markets anticipate that the Federal Reserve is likely to announce a higher targeted range for the Federal Funds Rate, our borrowing costs are likely to immediately increase, negatively impacting our net interest income, dividend, and book value per common share.

Interest rate fluctuations may also negatively affect the market value of our securities, resulting in declines in comprehensive income, book value per common share, and liquidity. Since our investment portfolio consists substantially of fixed rate instruments, rising interest rates will reduce the market value of our MBS as a result of higher yield requirements by the market for these types of securities. Reductions in the market value of our MBS typically result in margin calls from our lenders, which impacts our liquidity. Declining interest rates may cause prepayments to increase, which would increase amortization expense of any premiums we pay to acquire our investments and thereby result in a decline in net interest income. In addition, declining interest rates may also result in declining market value on RMBS as market participants factor in potentially faster prepayment rates in the future.

It can be difficult to predict the impact on interest rates of unexpected and uncertain global political and economic events, such as the outbreak of the COVID-19 pandemic, epidemic disease, warfare (including the recent outbreak of hostilities between Russia and Ukraine), economic and international trade conflicts or sanctions, the

10

change in the U.S. presidential administration and political makeup of the Congress, or changes in the credit rating of the U.S. government, the United Kingdom, or one or more Eurozone nations; however, increased uncertainty or changes in the economic outlook for, or rating of, the creditworthiness of the U.S. government, the United Kingdom, or Eurozone nations may have adverse impacts on, among other things, the U.S. economy, financial markets, the cost of borrowing, the financial strength of counterparties we transact business with, and the value of assets we hold. Any such adverse impacts could negatively impact the availability to us of short-term debt financing, our cost of short-term debt financing, our business, and our financial results.

We invest in to-be-announced, or TBA, securities and execute TBA dollar roll transactions. It could be uneconomical to roll our TBA contracts or we may be unable to meet margin calls on our TBA contracts, which could negatively affect our financial condition and results of operations.

We execute TBA dollar roll transactions which effectively delay the settlement of a forward purchase (or sale) of a TBA by entering into an offsetting TBA position, net settling the paired-off positions in cash, and simultaneously entering an identical TBA long (or short) position with a later settlement date. Under certain market conditions, TBA dollar roll transactions may result in negative net interest income whereby the Agency RMBS purchased (or sold) for forward settlement under a TBA contract are priced at a premium to Agency RMBS for settlement in the current month. Market conditions could also adversely impact the TBA dollar roll market and, in particular, shifts in prepay expectations on Agency RMBS or changes in the reinvestment policy on Agency RMBS by the Federal Reserve. Under such conditions, it may be uneconomical to roll our TBA positions prior to the settlement date, and we could have to take physical delivery of the underlying securities and settle our obligations for cash, or in the case of a short position, we could be forced to deliver one of our Agency RMBS, which would mean using cash to pay off any repurchase agreement amounts collateralized by that security. We may not have sufficient funds or alternative financing sources available to settle such obligations. In addition, pursuant to the margin provisions established by the Mortgage-Backed Securities Division (“MBSD”) of the Fixed Income Clearing Corporation, we are subject to margin calls on our TBA contracts and our trading counterparties may require us to post additional margin above the levels established by the MBSD. Negative income on TBA dollar roll transactions or failure to procure adequate financing to settle our obligations or meet margin calls under our TBA contracts could result in defaults or force us to sell assets under adverse market conditions or through foreclosure and adversely affect our financial condition and results of operations.

Changes in monetary policy, either implied or implemented by the Federal Reserve, including its intention to increase the targeted Federal Funds Rate or alter the trajectory of its purchases of longer-term Treasury securities and fixed-rate Agency MBS could cause interest rates to rise and/or the yield curve to flatten which could negatively impact the market value of our investments and/or increase our borrowing costs.

In response to the COVID-19 pandemic, and in order to mitigate its implications for the U.S. economy and financial system, the Federal Reserve aggressively eased monetary policy in 2020 by reducing the Federal Funds Rate to a range of between 0% and 0.25%. The Federal Reserve has also been providing monetary policy stimulus by expanding the holdings of longer-term securities in its portfolio, including large-scale purchases of Treasury securities and fixed-rate Agency RMBS. Citing substantial progress toward the achievement of its goals of maximum employment and price stability, the Federal Reserve began tapering its net asset purchases in December 2021 and has subsequently continued increasing its pace of tapering. In addition, by keeping the Federal Funds Rate at the range of between 0% and 0.25%, the Federal Reserve has kept short-term interest rates low which has benefited our borrowing costs. Citing a strong labor market and an inflation level above 2% as evidence, the Federal Reserve announced in February 2022 that they expect it will soon be appropriate to raise the target range for the Federal Funds Rate. The combination of these actions have resulted in an increase in long-term interest rates and flattening of the yield curve, negatively impacting the market value of our investments during the fourth quarter of 2021 and so far into 2022. In addition, the markets have begun pricing in four to five rate hikes, and as such, our borrowing costs are likely to increase in 2022.

We invest in assets that are traded in over-the-counter (“OTC”) markets which are less liquid and have less price transparency than securities exchanges. Owning securities that are traded in OTC markets may increase our liquidity risk, particularly in a volatile market environment, because our assets may be more difficult to borrow

11

against or sell in a prompt manner and on terms acceptable to us, and we may not realize the full value at which we previously recorded the investments and/or may incur losses upon sale of these assets.

Though Agency MBS are generally deemed to be very liquid securities, turbulent market conditions, such as market conditions following the COVID-19 outbreak, may significantly and negatively impact the liquidity and market value of these assets. Non-Agency MBS are typically more difficult to value, less liquid, and experience greater price volatility than Agency MBS. In addition, market values for non-Agency MBS are typically more subjective than Agency MBS. In times of severe market stress, a market may not exist for certain of our assets at any price. If the MBS market were to experience a severe or extended period of illiquidity, lenders may refuse to accept our assets as collateral for repurchase agreement financing, which could have a material adverse effect on our results of operations, financial condition and business. A sudden reduction in the liquidity of our investments could limit our ability to finance or could make it difficult to sell investments if the need arises. If we are required to liquidate all or a portion of our portfolio quickly, we may realize significantly less than the fair value at which we have previously recorded our investments which would result in lower than anticipated gains or higher losses.

Prepayment rates on the mortgage loans underlying our investments may adversely affect our profitability, the market value of our investments, and our liquidity. Changes in prepayment rates may also subject us to reinvestment risk.

We are subject to prepayment risk to the extent that we own investments at premiums to their par value or at yields at a premium to current market yields. We amortize the premiums we pay on a security using the effective yield method, which is impacted by borrower prepayments of principal on the loans. Prepayments can occur both on a voluntary basis (i.e., the borrower elects to prepay the loan along with related prepayment fees, if applicable) and involuntary basis (i.e., a loan default and subsequent foreclosure and liquidation). RMBS have no prepayment protection while CMBS and CMBS IO have voluntary prepayment protection in the form of a prepayment lock-out on the loan for an initial period, or by yield maintenance or prepayment penalty provisions which serve as full or partial compensation for future lost interest income on the loan. In certain circumstances, compensation for voluntary prepayment on CMBS IO securities may not be sufficient to compensate us for the loss of future excess interest as a result of the prepayment. Prepayments on our investments are impacted by economic and market conditions, the level of interest rates, the general availability of mortgage credit, and other factors.

We have no protection from involuntary prepayments. The impact of involuntary prepayments on high premium investments including CMBS IO and higher coupon Agency CMBS is particularly acute since the investment consists entirely of premium. An increase in involuntary prepayments will result in the loss of investment premiums at an accelerated rate which could materially reduce our profitability and dividend. Involuntary prepayments typically increase in periods of economic slowdown or stress, such as the slowdown in economic activity experienced as a result of COVID-19, and actions taken as a result by the GSEs and federal, state and local governments. Defaults in loans underlying our CMBS IO, particularly loans in non-Agency CMBS IO securities collateralized by income producing properties such as retail shopping centers, office buildings, multifamily apartments and hotels, may increase as a result of economic weakness, such as that brought on by the COVID-19 pandemic.

Prepayments on Agency CMBS, which are often collateralized by a single loan, could result in margin calls by lenders in excess of our available liquidity, particularly for larger balance investments. Typically, there is a 20-day delay between the announcement of prepayments and the receipt of the cash from the prepayment; however, the repurchase agreement lender may initiate a margin call when the prepayment is announced. If we do not have liquidity available to cover the margin call at that time, we may be in default under the repurchase agreement until we receive the cash from the prepayment. Alternatively, we could be forced to sell assets quickly and on terms unfavorable to us to meet the margin call.

Increases in actual prepayment rates or market expectations of prepayment rates (voluntary or involuntary) could negatively impact our profitability and the market value of our investments, negatively impacting our book value. We are also more likely to experience margin calls from our lenders as a result of the decline in value of our securities, which would negatively impact our liquidity. Typically, prepayments will increase when interest rates are declining which can lead to reinvestment in lower yielding investments leading to lower net interest income and reduced profitability.

12

We may be subject to risks associated with inadequate or untimely services from third-party service providers, which may negatively impact our results of operations. We also rely on corporate trustees to act on behalf of us and other holders of securities in enforcing our rights.

Loans underlying non-Agency MBS we own are serviced by third-party service providers. These servicers provide for the primary and special servicing of these securities. In that capacity these service providers control all aspects of loan collection, loss mitigation, default management and ultimate resolution of a defaulted loan including as applicable the foreclosure and sale of the real estate owned. The servicer has a fiduciary obligation to act in the best interest of the securitization trust, but significant latitude exists with respect to certain of its servicing activities. We have no contractual rights with respect to these servicers. If a third-party servicer fails to perform its duties under the securitization documents, this may result in a material increase in delinquencies or losses to the securities. As a result, the value of the securities may be impacted, and we may incur losses on our investment.

In addition, should a servicer experience financial difficulties, it may not be able to perform its obligations. Due to application of provisions of bankruptcy law, servicers who have sought bankruptcy protection may not be required to make advance payments required under the terms of the agreements governing the securities of amounts due from loan borrowers. Even if a servicer were able to advance amounts in respect of delinquent loans, its obligation to make the advances may be limited to the extent that is does not expect to recover the advances due to the deteriorating credit of the delinquent loans. For Agency MBS, we expect that the GSEs will transfer the servicing or otherwise make the investors in Agency MBS whole. For non-Agency MBS, financial difficulties with the servicer could lead to a material increase in delinquencies or losses to the securities. As a result, the value of the securities may be impacted, and we may incur losses on our investment.

We also rely on corporate trustees to act on behalf of us and other holders of securities in enforcing our rights. Under the terms of most securities we hold we do not have the right to directly enforce remedies against the issuer of the security, but instead must rely on a trustee to act on behalf of us and other security holders. Should a trustee not be required to take action under the terms of the securities, or fail to take action, we could experience losses.

Provisions requiring yield maintenance charges, prepayment penalties, defeasance, or lock-outs in CMBS IO securities may not be enforceable.

Provisions in loan documents for mortgages in CMBS IO securities in which we invest requiring yield maintenance charges, prepayment penalties, defeasance, or lock-out periods may not be enforceable in some states and under federal bankruptcy law. Provisions in the loan documents requiring yield maintenance charges and prepayment penalties may also be interpreted as constituting the collection of interest for usury purposes. Accordingly, we cannot be assured that the obligation of a borrower to pay any yield maintenance charge or prepayment penalty under a loan document in a CMBS IO security will be enforceable. Also, we cannot be assured that foreclosure proceeds under a loan document in a CMBS IO security will be sufficient to pay an enforceable yield maintenance charge. If yield maintenance charges and prepayment penalties are not collected, or if a lock-out period is not enforced, we may incur losses to write-down the value of the CMBS IO security for the present value of the amounts not collected, and we will experience lower yields and lower interest income. This would also likely cause margin calls from any lender on the CMBS IO impacted which could have a material adverse effect on our liquidity.

We invest in securities guaranteed by Fannie Mae and Freddie Mac which are currently under conservatorship by the Federal Housing Finance Authority (“FHFA”). The ultimate impact on the operations of Fannie Mae and Freddie Mac from the conservatorships and the support they receive from the U.S. government is not determinable and could affect Fannie Mae and Freddie Mac in such a way that our business, operations and financial condition may be adversely affected.

As conservator, the FHFA has assumed all the powers of the shareholders, directors and officers of the GSEs with the goal of preserving and conserving their assets. At various times since implementation of the conservatorship, Congress has considered structural changes to the GSEs. The U.S. Treasury published the Treasury Housing Reform Plan in 2019 outlining proposed changes to the U.S. housing finance system, which could lead to the release of the GSEs from conservatorship. Furthermore, the FHFA released its Strategic Plan in October 2019, which included in part an outline for the GSEs exiting conservatorship. Recent events related to the COVID-19 outbreak and the associated economic slowdown have raised concerns at the FHFA that the GSEs may need additional capital in order to meet their obligations as guarantors on trillions of dollars of MBS. The market value of Agency MBS today is

13

highly dependent on the continued support of the GSEs by the U.S. government. If such support is modified or withdrawn, if the U.S. Treasury fails to inject new capital as needed, or if the GSEs are released from conservatorship, the market value of Agency MBS could significantly decline, making it difficult for us to obtain repurchase agreement financing and could force us to sell assets at substantial losses. Furthermore, any policy changes to the relationship between the GSEs and the U.S. government may create market uncertainty and have the effect of reducing the actual or perceived credit quality of securities issued by the GSEs. It may also interrupt the cash flow received by investors on the underlying MBS. Finally, reforms to GSEs could also negatively impact our ability to comply with the provisions of the 1940 Act (see further discussion below regarding the 1940 Act).

All of the foregoing could materially adversely affect the availability, pricing, liquidity, market value and financing of our assets and materially adversely affect our business, operations, financial condition and book value per common share.

Credit ratings assigned to debt securities by the credit rating agencies may not accurately reflect the risks associated with those securities. Changes in credit ratings for securities we own or for similar securities might negatively impact the market value of these securities.

Rating agencies rate securities based upon their assessment of the safety of the receipt of principal and interest payments on the securities. Rating agencies do not consider the risks of fluctuations in fair value or other factors that may influence the value of securities and, therefore, the assigned credit rating may not fully reflect the true risks of an investment in securities. Also, rating agencies may fail to make timely adjustments to credit ratings based on available data or changes in economic outlook or may otherwise fail to make changes in credit ratings in response to subsequent events, so the credit quality of our investments may be better or worse than the ratings indicate. We attempt to reduce the impact of the risk that a credit rating may not accurately reflect the risks associated with a particular debt security by not relying solely on credit ratings as the indicator of the quality of an investment. We make our acquisition decisions after factoring in other information that we have obtained about the loans underlying the security and the credit subordination structure of the security. Despite these efforts, our assessment of the quality of an investment may also prove to be inaccurate and we may incur credit losses in excess of our initial expectations.

Credit rating agencies may change their methods of evaluating credit risk and determining ratings on securities backed by real estate loans and securities. These changes may occur quickly and often. The market’s ability to understand and absorb these changes, and the impact to the securitization market in general, are difficult to predict. Such changes may have a negative impact on the value of securities that we own.

RISKS RELATED TO OUR FINANCING AND HEDGING ACTIVITIES

Our use of leverage, including repurchase agreements, to enhance returns to shareholders increases the risk of volatility in our results and could lead to material decreases in comprehensive income, shareholders’ equity, book value per common share, dividends, and liquidity.

Leverage increases returns on our invested capital if we can earn a greater return on investments than our cost of borrowing but can decrease returns if borrowing costs increase and we have not adequately hedged against such an increase. Further, using leverage magnifies the potential losses to shareholders’ equity and book value per common share if our investments’ fair market value declines, net of associated hedges.

Repurchase agreements are typically short-term financings with no guaranty of renewal at maturity and changes to terms of such financing may adversely affect our profitability and our liquidity. Our ability to fund our operations, meet financial obligations, and finance targeted asset acquisitions may be impacted by an inability to secure and maintain our financing through repurchase agreements or other borrowings with our counterparties. Because repurchase agreements are short-term commitments of capital, lenders may respond to adverse market conditions in a manner that makes it more difficult for us to renew or replace on a continuous basis our maturing short-term borrowings. Furthermore, in times of adverse market conditions, we may have to dispose of assets at significantly depressed prices and at inopportune times, which could result in significant losses, or we may be forced to curtail our asset acquisition activities if certain events occur including, for example, if we:

•are unable to renew our existing or are otherwise unable to access new funds under our financing arrangements;

•are unable to arrange for new financing on acceptable terms;

14

•default on our financial covenants contained in our financing arrangements; or

•become subject to larger haircuts under our financing arrangements requiring us to post additional collateral.

In addition, if the regulatory capital requirements imposed on certain of our lenders change, those lenders may be required to significantly increase the cost of the financing that they provide to us, or to increase the amounts of collateral they require as a condition to providing us with financing. At various times, our lenders have revised, and may continue to revise, their eligibility requirements for the types of assets that they are willing to finance or the terms of such financing arrangements, including increased haircuts and requiring additional cash collateral, based on, among other factors, the regulatory environment and a particular lender’s management of actual and perceived risk. Moreover, the amount of financing that we receive under our financing agreements will be directly related to our lenders’ valuation of the assets subject to such agreements. Typically, the master repurchase agreements that govern our borrowings grant the lender the absolute right to reevaluate the fair market value of the assets subject to such repurchase agreements at any time. These valuations may be different than the values that we ascribe to these assets and may be influenced by recent asset sales at distressed levels by forced sellers. If a lender determines in its sole discretion that the value of the assets has decreased, it has the right to initiate a margin call, which would require us to transfer additional assets to the lender without any advance of funds from the lender for such transfer or to repay a portion of the outstanding borrowings. We would also be required to post additional collateral if haircuts increase under a repurchase agreement. Furthermore, if we move financing from one repurchase agreement counterparty to another with larger haircut requirements, we would have to repay more cash to the original counterparty than we would be able to borrow from the new counterparty. In these situations, we could be forced to sell assets at significantly depressed prices to meet such margin calls and to maintain adequate liquidity, which could cause significant losses. Significant margin calls could have a material adverse effect on our results of operations, financial condition, business, liquidity, and ability to make distributions to our shareholders, and could cause the value of our capital stock to decline.

Our ability to access leverage in the conduct of our operations is impacted by the following:

•market conditions and overall market volatility and liquidity;

•regulation of our lenders and other regulatory factors;

•disruptions in the repurchase agreement market generally, or the infrastructure that supports it;

•the liquidity of our investments;

•the market value of our investments;

•maintaining our REIT status;

•the advance rates by our lenders on investment collateral pledged;

•the available liquidity and capital of our lenders, and;

•the willingness of our lenders to finance the types of investments we choose.

Many of these factors are beyond our control and are difficult to predict, which could lead to sudden and material adverse effects on our results of operations, financial condition, business, liquidity, and ability to make distributions to shareholders, and could force us to sell assets at significantly depressed prices to maintain adequate liquidity. Market dislocations, including those resulting from the COVID-19 outbreak or as a result of other future outbreaks involving other highly infectious or contagious diseases, could limit our ability to access funding or access funding on terms that we believe are attractive, which could have a material adverse effect on our financial condition.

For more information about our operating policies regarding our use of leverage, please see “Liquidity and Capital Resources” within Part II, Item 7 of our Annual Report on Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Our repurchase agreements and agreements governing certain derivative instruments may contain financial and nonfinancial covenants. Our inability to meet these covenants could adversely affect our financial condition, results of operations, and cash flows.

In connection with certain of our repurchase agreements and interest rate swap agreements, we are required to maintain certain financial and non-financial covenants. As of December 31, 2021, the most restrictive financial covenants require that we have a minimum of $30 million of liquidity and declines in shareholders’ equity no greater than 25% in any quarter and 35% in any year. In addition, virtually all of our repurchase agreements and interest rate swap agreements require us to maintain our status as a REIT and to be exempted from the provisions of the 1940 Act. Compliance with these covenants depends on market factors and the strength of our business and operating results.

15

Various risks, uncertainties and events beyond our control, including significant fluctuations in interest rates, market volatility and changes in market conditions, could affect our ability to comply with these covenants. Failure to comply with these covenants could result in an event of default, termination of an agreement, acceleration of all amounts owed under an agreement, and generally would give the counterparty the right to exercise certain other remedies under the repurchase agreement, including the sale of the asset subject to repurchase at the time of default, unless we were able to negotiate a waiver in connection with any such default related to failure to comply with a covenant. Any such waiver could be conditioned on an amendment to the underlying agreement and any related guaranty agreement on terms that may be unfavorable to us. If we are unable to negotiate a covenant waiver or replace or refinance our assets under a new repurchase facility on favorable terms or at all, our financial condition, results of operations and cash flows could be adversely affected. Further, certain of our repurchase agreements and interest rate swap agreements have cross-default, cross-acceleration or similar provisions, such that if we were to violate a covenant under one agreement, that violation could lead to defaults, accelerations, or other adverse events under other agreements, as well.

Our use of hedging strategies to mitigate our interest rate risk may not be effective and may adversely affect our net income, comprehensive income, liquidity, shareholders’ equity and book value per common share.

We may use a variety of derivative instruments to help mitigate increased financing costs and volatility in the market value of our investments from adverse changes in interest rates. Our hedging activity will vary in scope based on, among other things, our forecast of future interest rates, our investment portfolio construction and objectives, the actual and implied level and volatility of interest rates, and sources and terms of financing used. No hedging strategy can completely insulate us from the interest rate risks to which we are exposed. Interest rate hedging may fail to protect or could adversely affect our results of operations, book value and liquidity because, among other things:

•the performance of instruments used to hedge may not completely correlate with the performance of the assets or liabilities being hedged;

•available hedging instruments may not correspond directly with the interest rate risk from which we seek protection;

•the duration of the hedge may not match the duration of the related asset or liability given management’s expectation of future changes in interest rates or a result of the inaccuracies of models in forecasting cash flows on the asset being hedged;

•the value of derivatives used for hedging will be adjusted from time to time in accordance with GAAP to reflect changes in fair value and downward adjustments, or “mark-to-market losses,” will reduce our earnings, shareholders’ equity, and book value;

•the amount of income that a REIT may earn from hedging transactions (other than through taxable REIT subsidiaries) to offset interest rate losses may be limited by U.S. federal income tax provisions governing REITs;

•interest rate hedging can be relatively expensive, particularly during periods of volatile interest rates;

•the credit quality of the party owing money on the hedge may be downgraded to such an extent that it impairs our ability to sell or assign our side of the hedging transaction; and

•the party owing money in the hedging transaction may default on its obligation to pay.

Our hedging instruments can be traded on an exchange or administered through a clearing house or under bilateral agreements between us and a counterparty. Bilateral agreements expose us to increased counterparty risk, and we may be at risk of loss of any collateral held by a hedging counterparty if the counterparty becomes insolvent or files for bankruptcy. Moreover, the expected transition from LIBOR to alternative reference rates adds additional complications to our hedging strategies. For example, we may enter into Secured Overnight Financing Rate (“SOFR”) based swaps to hedge rising borrowing costs, which may not fully offset such rising costs as well as LIBOR-based swaps may have in the past.