Item 1. |

Reports to Shareholders. |

|

Annual Report |

December 31, 2022 |

Beginning December 31, 2022, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of Sprott Focus Trust’s (“the Fund”) semi-annual and annual financial reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on www.sprottfocustrust.com and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor and your shares are held with our transfer agent, Computershare, you may log into your Investor Center account at www.computershare.com/investor and go to “Communication Preferences”. You may also call Computershare at 1.800.426.5523.

You may elect to receive all future reports in paper form at no cost to you. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports; if you invest directly with the Fund, you can call Computershare at 1.800.426.5523. Your election to receive reports in paper form will apply to all funds held in your account with your financial intermediary or, if you invest directly, to all

closed-end

funds you hold. Table of Contents

| 1 | ||||

| 2 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 21 | ||||

| 24 | ||||

| 25 | ||||

| 27 | ||||

Managed Distribution Policy

The Board of Directors of Sprott Focus Trust, Inc. (the “Fund”) has authorized a managed distribution policy (“MDP”). Under the MDP, the Fund pays quarterly distributions at an annual rate of 6% of the rolling average of the prior four quarter-end net asset values, with the fourth quarter distribution being the greater of this annualized rate or the distribution required by IRS regulations. With each distribution, the Fund will issue a notice to its stockholders and an accompanying press release that provides detailed information regarding the amount and composition of the distribution (including whether any portion of the distribution represents a return of capital) and other information required by the Fund’s MDP. You should not draw any conclusions about the Fund’s investment performance from the amount of distributions or from the terms of the Fund’s MDP. The Fund’s Board of Directors may amend or terminate the MDP at any time without prior notice to stockholders.

Performance

(Unaudited)

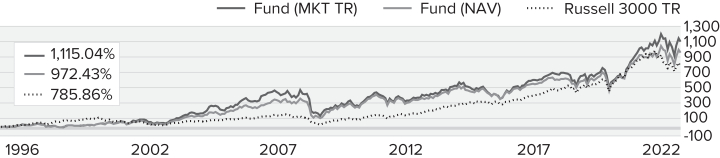

NAV Average Annual Total Returns

As of December 31, 2022 (%)

FUND |

1 YR |

3 YR |

5 YR |

10 YR |

15 YR |

20 YR |

SINCE INCEPTION |

INCEPTION DATE |

||||||||||||||||||||||||

| Sprott Focus Trust |

0.08 | 9.53 | 7.67 | 8.61 | 6.15 | 10.39 | 9.49 | 11/1/96 | 1 | |||||||||||||||||||||||

INDEX |

||||||||||||||||||||||||||||||||

| Russell 3000 TR Index 2 |

-19.21 | 7.07 | 8.79 | 12.13 | 8.66 | 9.88 | 8.69 | |||||||||||||||||||||||||

1 |

Royce & Associates, LLC served as investment adviser of the Fund from November 1, 1996 to March 6, 2015. After the close of business on March 6, 2015, Sprott Asset Management LP and Sprott Asset Management USA Inc. became the investment adviser and investment sub-adviser, respectively, of the Fund. |

2 |

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell ® is a trademark of Russell Investment Group. The Russell 3000 Total Return index measures the performance of the largest 3,000 U.S. companies. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. |

Important Performance and Risk Information

All performance information reflects past performance, is presented on a total return basis, net of the Fund’s investment advisory fee and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Current performance may be higher or lower than performance quoted. Returns as of the most recent month-end may be obtained at www.sprottfocustrust.com. The market price of the Fund’s shares will fluctuate, so shares may be worth more or less than their original cost when sold.

The Fund is a closed-end registered investment company whose shares of common stock may trade at a discount to their net asset value. Shares of the Fund’s common stock are also subject to the market risks of investing in the underlying portfolio securities held by the Fund.

The Fund’s shares of common stock trade on the Nasdaq Select Market. Closed-end funds, unlike open-end funds, are not continuously offered. After the initial public offering, shares of closed-end funds are sold on the open market through a stock exchange. For additional information, contact your financial advisor or call 203.656.2430. Investment policies, management fees and other matters of interest to prospective investors may be found in the closed-end fund prospectus used in its initial public offering, as revised by subsequent stockholder reports.

|

1 | MANAGER’S DISCUSSION (Unaudited) | ||

Sprott Focus Trust Sprott Focus Trust |

Whitney George

DEAR FELLOW SHAREHOLDERS,

We never thought we would be pleased to report that Sprott Focus Trust’s (FUND) performance was unchanged for the year, but here we are. Sprott Focus Trust was up 0.08% on a Net Asset Value (NAV) basis and down 0.91% in total market return in 2022 due to a very modest widening of the market price discount to NAV. We are proud of this performance, given that 2022 represented one of the worst years in four decades for traditionally balanced investors. Equity markets were broadly down, with the S&P 500 Index losing 18.11% and many popular asset sectors faring even worse. Fixed Income markets suffered their worst performance on record, with bonds declining 13.01% as measured by Bloomberg Barclays US Agg Total Return Value Unhedged USD Index.

FUND’s 0.08% NAV return for 2022 compares very favorably to the 19.21% decline in the Russell 3000 Total Return Index, FUND’s performance benchmark. Last year’s results for FUND also improved its longer-term relative performance. FUND’s

3-,

5-

and 10-year

NAV returns as of year end were 9.53%, 7.67% and 8.61%, respectively, compared to 7.07%, 8.79% and 12.13%, respectively, for the Russell 3000 TR Index. These results validate our long-term approach of investing in undervalued, high-quality companies while rewarding our patient shareholders. Last year we wrote, “Clearly, 2021 was a great year for most equity investors, and it set a high bar that is unlikely to be repeated in 2022. Yet, due to the many factors discussed in this letter, we remain optimistic about FUND’s prospects, especially on relative terms.” We got that right! Perhaps it would be wise for us to quit while we are ahead with predictions, but for 2023 we expect more of the same but anticipate less downside severity.

2022 was a roller coaster year for FUND’s performance. While the broad equity indices peaked on the first day, we had a very strong start to the year due to our overweighting in hard asset sectors, including energy, mining and steel. Like 2021, the big macroeconomic story in 2022 was the return of inflation. The unexpected and tragic Russian invasion of Ukraine accelerated what we believe to be long-term structural inflationary forces. Both deglobalization and decarbonization have been with us for several years but have many more years to play out. The Russia-Ukraine war brought those macro themes to the forefront for all to see and jump started the political war against inflation. As the Federal Reserve (“Fed”) began the most aggressive rate hiking cycle in decades, all markets beat a hasty retreat during 2022’s second quarter. We then enjoyed a nice recovery based on the disbelief that the Fed would or could increase interest rates at 75 basis points per meeting only to

slump again in late summer/early fall, as central bankers repeated their resolve to fight inflation at any cost.

Finally, we experienced some recovery in the year’s final months as market participants began to forecast a recession that would bring an end to high inflation and, therefore, further rate hikes. Around mid October, Secretary of the Treasury Janet Yellen expressed concerns about liquidity in the U.S. Treasury market. The U.S. dollar peaked and liquidity conditions improved. Quite a ride last year! We expect inflation to moderate in 2023 because the year-over-year comparisons are easy. But the longer-term forces at work will not likely permit developed economies to sustainably return to anything close to the targeted 2% rate for a very long time. In 2023, we expect inflation targets will become more realistic, calculations will be adjusted, or both.

Portfolio Activity

Patience is an important investor attribute, especially during bear markets. Warren Buffett characterized it appropriately when he remarked, “the stock market is a device for transferring money from the impatient to the patient”. Great long-term investment opportunities often arise during periods like this, but without patience and its close companion discipline, investment results can suffer. Portfolio turnover was just shy of 20% for 2022, in line with last year, and with both years being somewhat below our typical level of activity as we continue to exercise patience and discipline during highly volatile and illiquid markets.

Five portfolio positions were liquidated in 2022, with our rationale for selling both Aclara Resources and Franklin Resources discussed in the semi-annual letter. During the year’s second half, we also exited Hochschild Mining, Industrias Bachoco and Western Digital. Hochschild Mining is a London-listed primary silver miner with three operating assets in South America. The company has struggled recently as the triple challenges of generally lower silver prices and declining ore grades were met with higher operating costs, negatively impacting near-term financial results. Over the medium term, there is skepticism about Hochschild’s ability to replace reserves and expand production as one of its key assets, the Pallancata silver/gold mine, nears depletion. The company is focused on brownfield exploration potential at key producing mine assets Inmaculada and San Jose, while construction continues at the newly acquired Mara Rosa project in Brazil. Despite the promise these initiatives represent, we chose to further consolidate our precious metals exposure among existing names in FUND’s portfolio where we have greater confidence.

Industrias Bachoco is the largest poultry producer in Mexico. During the year, the controlling Robinson Bours family (with approximately 73% economic and voting interest) initiated a voluntary tender offer for up to all of the outstanding shares of Bachoco, which are not

2

|

2022 Annual Report to Stockholders | MANAGER’S DISCUSSION (Unaudited) |

owned by the family or its affiliates at a price which we believe significantly undervalued the company. Despite our efforts with a consortium of local and foreign

co-investors,

we were unsuccessful in encouraging a higher offer price. Having little legal recourse in accordance with local Mexican securities regulations and having learned of their directors’ malintent, we sold our position into the modest recovery of Bachoco’s share price. Our investment in Western Digital Corporation has been a disappointment, despite the company enjoying leading competitive positions in critical technology products and solutions relating to data storage. Hard disk drives (HDDs) have been the prevailing data storage technology for decades, and of which Western Digital remains a strong competitor today. As demand for personal computers (PCs) declined, NAND flash memory technology replaced HDDs in most modern applications. Previous management, partly to remain relevant, orchestrated a transformative deal to acquire leading NAND flash memory provider SanDisk in 2016. The promised synergies from combining the two have not materialized in the six years since, and the company is now considering a separation. The only transformation we have seen has been in Western Digital’s capital structure, with its

pre-acquisition

net cash balance sheet now severely indebted. With a strategic review underway and the two as separately reporting business units since 2020, reversing the 2016 transaction looks likely. Having lost confidence in Western Digital’s management and considering the elevated balance sheet risk we try to mitigate through careful stock selection, we decided to redeploy sale proceeds into more compelling portfolio positions. We established a new position in Steel Dynamics earlier in the year, as discussed in the semi-annual letter. We also mentioned at

mid-year

that we had nibbled on four names we know well and whose share prices were near our buy targets, hoping for market dislocation to provide an opportunity to build new positions fully. Only Cirrus Logic and Exxon Mobil offered sufficient discounts to fair value to add further during the second half of 2022, with more patience needed with Lam Research and Sims Limited. In investing, as in life, patience usually pays. Performance Contributors and Detractors

Top Contributions to Performance

Year-to-date

1

| Helmerich & Payne, Inc. |

3.73 | |||

| Cal-Maine Foods, Inc. |

2.02 | |||

| Pason Systems Inc. |

1.44 | |||

| Nucor Corporation |

1.35 | |||

| Reliance Steel & Aluminum Co. |

1.26 |

1 |

Includes dividends. |

Top Detractors from Performance

Year-to-date

1

| Western Digital Corporation |

-2.10 | |||

| Kennedy-Wilson Holdings, Inc. |

-1.57 | |||

| Schnitzer Steel Industries, Inc. Class A |

-1.52 | |||

| Artisan Partners Asset Management, Inc. Class A |

-1.51 | |||

| THOR Industries, Inc. |

-0.93 |

1 |

Net of dividends. |

Figure 1

Figure 1 shows which positions contributed and detracted the most from FUND’s aggregate performance during the year. Helmerich & Payne, the leading drilling solutions provider to North American oil and gas producers, tops the list of contributors as its shares more than doubled during 2022, contributing 3.73% to FUND’s performance. Demand for drill rigs and related drilling services has recovered strongly, driving economic returns to levels not experienced since 2014. During its recent

year-end

results call with analysts, the company cited “significant momentum heading into fiscal 2023.” Comparisons by management to 2014 imply continued undervaluation in Helmerich & Payne shares, despite the great performance in 2022. The favorable conditions driving

Cal-Maine’s

earnings and share price in the first half of 2022 continued during the remainder of the year. Cal-Maine

Foods was FUND’s second-best contributor, adding 2.02% to overall performance. High feed costs and avian influenza driven supply disruptions continued to drive fresh shell egg pricing. Lower shell egg inventories near year end, combined with increased seasonal demand from the holiday baking season, resulted in several weeks of record-high egg prices in December. Pason Systems is a drilling services technology company serving oil and gas producers. Industry conditions steadily improved, along with increased demand for the company’s products and technology. Pason shares continued to outperform in the second half of 2022, advancing well for the full year and contributing 1.44% to FUND’s overall performance. Rounding out the top five contributors, Nucor Corporation and Reliance Steel & Aluminum contributed positively (contributing 1.35% and 1.26%, respectively) despite lower demand and pricing in the second half of the year. Both companies reported declines in revenues and operating profit recently. Nucor’s flexible production profile and Reliance Steel’s (LIFO) liquidation policy enabled both companies to mitigate the extreme cyclicality that has historically burdened less nimble integrated steel producers at cyclical troughs. Pricing of certain finished steel products improved in the final quarter of the year, lending support for a strong finish to a volatile year.

last-in-first-out

Western Digital was FUND’s top performance detractor for the year. The company’s troubles have been amply covered already in this letter. Still, we are reminded to be skeptical when evaluating future “transformational deals” that may arise since they generally have a poor record of success. One of our largest contributors in 2021, Kennedy-Wilson Holdings detracted from portfolio performance in 2022. Real estate investments, which are highly sensitive to changes in the cost of financing transactions, were negatively impacted by the Fed’s most aggressive rate hike cycle since 1980. Schnitzer Steel negatively impacted performance last year despite recording its second-best fiscal year in the company’s history. Notably, Schnitzer

2022 Annual Report to Stockholders

|

3 | MANAGER’S DISCUSSION (Unaudited) |

was named the world’s most sustainable company by Corporate Knights, a Canadian media and research company focused on sustainability. Schnitzer’s significant scrap recycling business and its net carbon-free electricity use for the second year were key considerations. Quite an achievement for a company in such a industry as steel.

hard-to-abate

Artisan Partners hampered FUND’s performance during the year as its business is tied quite closely to the general performance of global equity markets. Simply put, it isn’t easy to insulate oneself in a down year. Artisan’s longstanding track record of outperformance over full market cycles gives us confidence in its future, despite the short-term negative impact of declining markets. Finally, THOR Industries underperformed as fears of recession exacerbated declining sales and order backlogs as the year progressed. THOR’s track record in previous economic downcycles also offers great optimism about its ability to weather this downturn.

Positioning

Top 10 Positions

(% of Net Assets)

| The Buckle, Inc. |

4.7 | |||

| Federated Hermes, Inc. Class B |

4.6 | |||

| Helmerich & Payne, Inc. |

4.6 | |||

| Reliance Steel & Aluminum Co. |

4.6 | |||

| Pason Systems Inc. |

4.5 | |||

| Steel Dynamics, Inc. |

4.4 | |||

| Nucor Corporation |

4.4 | |||

| Westlake Corporation |

4.2 | |||

| AerSale Corporation |

4.2 | |||

| Vishay Intertechnology, Inc. |

4.1 |

Portfolio Sector Breakdown

(% of Net Assets)

| Materials |

37.4 | |||

| Financials |

15.0 | |||

| Energy |

12.3 | |||

| Consumer Discretionary |

8.7 | |||

| Real Estate |

8.3 | |||

| Industrials |

5.7 | |||

| Technology |

5.5 | |||

| Consumer Staples |

4.0 | |||

| Cash & Cash Equivalents |

3.1 |

Figure 2

FUND had 34 equity investments at year end, down from 35 a year ago, and its 10 largest positions accounted for 44.40% of the portfolio. Over recent years, the portfolio’s increased concentration has been a

by-product

of elevated valuations and our absolute value approach to security selection. As markets rallied, the available pool of undervalued securities shrank. We look forward to an expanding universe of high-quality companies to invest in as markets hopefully continue to fall and offer disciplined investors great long-term opportunities. Cash and cash equivalents are also a

by-product

of the opportunities we perceive from the bottom up; at just 3.15%, we are relatively fully invested at year end and quite content with portfolio positioning. We were able to reduce our cash position by spending approximately $4.9 million to repurchase 563,212 shares of FUND during the calendar year 2022. Materials remain our largest sector exposure at 37.39%. While the precious metals basket remains an attractive and core strategic exposure, this year marks another increased allocation to the steel sector. Four steel producers, Nucor Corp, Reliance Steel, Schnitzer Steel and Steel Dynamics comprise more than 16% of the portfolio at year end, versus 11% a year ago.

Portfolio Diagnostics

| Fund Net Assets |

$254 million | |||

| Number of Holdings |

34 | |||

| 2022 Annual Turnover Rate |

19.65% | |||

| Net Asset Value |

$8.49 | |||

| Market Price |

$7.97 | |||

| Average Market Capitalization 1 |

$3,330 million | |||

| Weighted Average P/E Ratio 2,3 |

8.82x | |||

| Weighted Average P/B Ratio 2 |

1.69x | |||

| Weighted Average Yield |

2.67% | |||

| Weighted Average ROIC |

27.63% | |||

| Weighted Average Leverage Ratio |

1.90x | |||

| Holdings ≥ 75% of Total Investments |

19 | |||

| U.S. Investments (% of Net Assets) |

74.18% | |||

| Non-U.S. Investments (% of Net Assets) |

25.82% |

Figure 3

1 |

Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Sprott believes offers a more accurate measure of average market cap than a simple mean or median. |

2 |

Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

3 |

The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (6.91% of holdings as of 12/31/2022). |

Outlook

Not to date ourselves, but we have been investing for a long time, and 2022 represented the beginning of our sixth bear market. Bear markets come in a couple of forms and always surprise the majority of investors. Some are short in duration and over before there is much time to capitalize on new opportunities, like the 1987 and 2020 bear markets. These short bear markets are often caused by systemic shocks like portfolio insurance gone wrong in 1987 or the

COVID-19

pandemic lockdown in 2020. Others are more prolonged, lasting two years or more, while markets adjust to a new paradigm. The 1980 “war against inflation” and the 2000 dot.com bubble burst are 4

|

2022 Annual Report to Stockholders | MANAGER’S DISCUSSION (Unaudited) |

examples of longer duration bear markets. Fortunately, bear markets always end and often lead to fabulous returns for those who are proactive and patient.

To us, the current bear market feels most like the 2000-2002 experience. The combination of free money (0% interest rates) and innovations in software, services, investing and even money (cryptocurrencies) accelerated during the

COVID-19

lockdown of 2020-2021. We found new ways to communicate and shop remotely. We learned new ways to invest in disruptive technologies, meme stocks and SPACs (blank check companies). We even invented new currencies that were believed to be more efficient and safer than U.S. dollars or gold. For anyone with more than a couple of decades of investment experience, this looks remarkably like the late 1990s. Back then, we had Alan Greenspan as Chairman of the Federal Reserve. He was probably the modern architect of the “Fed Put”, the concept that our central bankers could quickly step in and provide liquidity via low interest rates and printed cash to avert any emerging global economic crisis. This was demonstrated in 1998 during the implosion of the hedge fund Long-Term Capital Management and the Asian Crisis. At the same time, we enjoyed a boom in electronic and medical innovation. The Internet brought new ways to communicate and transact, creating the dot.com bubble. For a brief period, IPO shares became the most favored currency. Then in March of 2000, after we had passed into a new century without incident, the free money went away. Initially, the most speculative investments were liquidated, but eventually, all equity markets were pressured, leading to a negative wealth effect and ultimately a recession. Then, like now, plenty of overlooked and undervalued businesses could be bought in more traditional industries like food, energy and materials. But it took more than two years after the dot.com bubble burst for markets to sort out the survivors and thrivers in the newer industries. We are now in a similar situation, and we suspect that this bear market is not likely to be short. Certainly, events move faster today than 20 years ago and 2022 was a painful year. Yet, there are still large systematic issues to be addressed and powerful inflationary forces in energy and trade that are likely to keep interest rates higher for longer. The free money rocket fuel for markets is gone. Even when the Fed ends its interest rate hiking and quantitative tightening program, we will likely be in recession with only its severity left to debate. In 2023, we believe the sorting will begin and we have early clues as to how that might look. Gold and silver did their job of preserving wealth last year and have started this year strongly as more investors take notice. As we mentioned, traditional energy did well as the Russia-Ukraine war woke the developed world up to the real costs of decarbonization. Energy transition policies are bound to uncover large supply deficits in the basic essential materials required to produce cleaner power. A massive infrastructure plan should begin in earnest this year. Combined with trade policies calling for more onshoring or nearshoring of our

manufacturing base, this will produce a relatively favorable backdrop for our heavily weighted investment in steel producers, irrespective of more difficult economic conditions.

We believe Sprott Focus Trust is well positioned to continue to weather the current bear market. Higher inflation and interest rates have already compressed equity valuations, but our portfolio entered last year with historically low metrics in terms of value, and flow. That is still true as of this writing. We expect the focus to shift to individual industry and company fundamentals in the coming year. With near record high returns of capital and dividend yields and an unlevered balance sheet, FUND’s portfolio holdings should survive a bad recession and thrive if conditions are more benign. We will always be on the lookout for the new opportunities that will inevitably present themselves.

price-to-book

price-to-earnings

price-to-cash

As always, we would like to thank our partners at FUND, Matt Haynes and Basia Dworak, who contribute to all aspects of managing FUND. The finance and operations teams at Sprott in Toronto make our jobs fun and easy. Finally, we would like to thank our shareholders, many of them very long term, for their patience and support. It was a long time coming, but both active and value investing seem to have returned and we are excited about our prospects. Please feel free to call or email us with any questions or to say hello.

Sincerely,

W. Whitney George

Senior Portfolio Manager

January 25, 2023