UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended September 30, 2016 or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from _____________ to _____________

Commission file number 0-21384

INTERNATIONAL PACKAGING AND LOGISTICS GROUP, INC.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 13-3367421 | |

| (State or Other Jurisdiction of | (I.R.S. Employer | |

| Incorporation or Organization) | Identification No.) |

17800 Castleton Street, Suite 386, City of Industry, California

(Address of Principal Executive Offices)

91748

(Zip Code)

(626)213-3945

(Registrant’s Telephone Number, Including Area Code)

7700 Irvine Center Drive, Suite 870, Irvine, California

___________________________________________

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] Yes [_]No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [_] | Accelerated filer [_] |

| Non-accelerated filer [_] | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2 of the Exchange Act).

[_] Yes [X] No

The number of shares outstanding of the Issuer’s common stock as of November 21, 2016 was 6,544,214.

International Packaging and Logistics Group, Inc.,

and Subsidiaries

FORM 10-Q for the Quarter Ended September 30, 2016

INDEX

| Page | ||||||

| PART I - FINANCIAL INFORMATION | ||||||

| Item 1. | Financial Statements | 3 | ||||

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 15 | ||||

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 19 | ||||

| Item 4. | Controls and Procedures | 19 | ||||

| PART II - OTHER INFORMATION | ||||||

| Item 1. | Legal Proceedings | 20 | ||||

| Item 1A. | Risk Factors | 20 | ||||

| Item 2. | Unregistered Sale of Equity Securities and Use of Proceeds | 35 | ||||

| Item 3. | Defaults Upon Senior Securities | 35 | ||||

| Item 4. | Mine Safety Disclosures | 35 | ||||

| Item 5. | Other Information | 35 | ||||

| Item 6. | Exhibits | 36 | ||||

| Signatures | 37 | |||||

| 2 |

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

International Packaging and Logistics Group, Inc., and Subsidiaries

Condensed Consolidated Balance Sheets

As of SEPTEMBER 30, 2016, and December 31, 2015

| September 30, | December 31, | |||||||

| 2016 | 2015 | |||||||

| (unaudited) | ||||||||

| Assets | ||||||||

| Current Assets | ||||||||

| Cash | $ | 6,256 | $ | 21,747 | ||||

| Accounts receivable, net | 56,948 | 3,521 | ||||||

| Other receivable | 81,369 | 90,841 | ||||||

| Prepaid expenses | 52,066 | 195,101 | ||||||

| Inventory, net | 276,493 | 118,900 | ||||||

| Total Current Assets | 473,132 | 430,110 | ||||||

| Property, plant and equipment, net | 2,662,255 | 2,404,650 | ||||||

| Intangible assets, net | 727,557 | 760,819 | ||||||

| Total Assets | $ | 3,862,944 | $ | 3,595,579 | ||||

| Liabilities and Stockholders' Equity | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued expenses | $ | 420,129 | $ | 23,444 | ||||

| Customer deposits | 21,557 | 62,368 | ||||||

| Taxes payable | 34,557 | 35,574 | ||||||

| Other payable | 132,823 | 92,661 | ||||||

| Advance from related parties | 2,697,060 | 1,353,321 | ||||||

| Short term loan | – | 1,080,614 | ||||||

| Total Current Liabilities | 3,306,126 | 2,647,982 | ||||||

| Total Liabilities | 3,306,126 | 2,647,982 | ||||||

| Stockholders' Equity | ||||||||

| Convertible preferred shares: $0.0001 par value, 50,000,000 shares authorized, 974,730 and zero Series A issued and outstanding as of September 30, 2016 and December 31, 2015, respectively | 98 | – | ||||||

| Common stock: $0.001 par value, 900,000,000 shares authorized, 6,544,214 and 2,040,000 issued and outstanding, as of September 30, 2016 and December 31, 2015, respectively | 6,544 | 2,040 | ||||||

| Additional paid-in capital | 851,079 | 815,681 | ||||||

| Stock subscription receivable | (41,289 | ) | – | |||||

| Accumulated other comprehensive loss | (41,977 | ) | (30,353 | ) | ||||

| Accumulated deficit | (532,393 | ) | (323,693 | ) | ||||

| Total Stockholders' equity-IPLO | 242,062 | 463,675 | ||||||

| Non-controlling interest subsidiaries | 314,756 | 483,922 | ||||||

| Total stockholders’ equity | 556,818 | 947,597 | ||||||

| Total Liabilities and Stockholders' Equity | $ | 3,862,944 | $ | 3,595,579 | ||||

See accompanying notes to these unaudited condensed consolidated financial statements

| 3 |

International Packaging and Logistics Group, Inc., and Subsidiaries

Condensed Consolidated Statements of Operations and Comprehensive Income

For the Three and Nine Months Ended September 30, 2016 and 2015

(Unaudited)

| Three Months Ended | Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Sales, net | $ | 149,021 | $ | 57,761 | $ | 455,017 | $ | 58,275 | ||||||||

| Cost of goods sold | 125,418 | 84,009 | 374,849 | 84,757 | ||||||||||||

| Gross Profit | 23,603 | (26,248 | ) | 80,168 | (26,482 | ) | ||||||||||

| Operating Expenses | ||||||||||||||||

| Selling expenses | 2,489 | 4,898 | 11,153 | 12,480 | ||||||||||||

| General and administrative | 141,414 | 14,841 | 400,551 | 170,896 | ||||||||||||

| Total Operating Expenses | 143,903 | 19,739 | 411,704 | 183,376 | ||||||||||||

| (Loss) from Operations | (120,300 | ) | (45,987 | ) | (331,536 | ) | (209,858 | ) | ||||||||

| Other income | ||||||||||||||||

| Other (expense) income | (392 | ) | (325 | ) | 14,752 | 13,111 | ||||||||||

| Interest expense, net | – | (46,909 | ) | (49,914 | ) | (107,895 | ) | |||||||||

| Total Other Income | (392 | ) | (47,234 | ) | (35,162 | ) | (94,784 | ) | ||||||||

| Net (Loss) Income from Continuing Operations before Income Taxes | |

|

(120,692 |

) |

|

|

(93,221 |

) |

|

|

(366,698 |

) |

|

|

(304,642 |

) |

| Income tax benefit (expense) | – | – | – | – | ||||||||||||

| Net (Loss) | (120,692 | ) | (93,221 | ) | (366,698 | ) | (304,642 | ) | ||||||||

| Less: net (loss) attributable to non-controlling interest | (59,139 | ) | (45,678 | ) | (179,682 | ) | (149,275 | ) | ||||||||

| Net (loss) attributable to the Company | (61,553 | ) | (47,543 | ) | (187,016 | ) | (155,367 | ) | ||||||||

| Earnings per weighted average share of common stock – basic and diluted | $ | (0.03 | ) | $ | (0.05 | ) | $ | (0.06 | ) | $ | (0.16 | ) | ||||

| Weighted average shares outstanding - basic and diluted | 6,544,214 | 2,040,000 | 6,544,214 | 2,040,000 | ||||||||||||

| Net (Loss) Income | (120,692 | ) | (93,221 | ) | (366,698 | ) | (304,642 | ) | ||||||||

| Other comprehensive (loss) | ||||||||||||||||

| Foreign currency translation (loss) | (69,153 | ) | (5,201 | ) | (22,792 | ) | (30,775 | ) | ||||||||

| Comprehensive (loss) | (189,845 | ) | (98,422 | ) | (389,490 | ) | (335,417 | ) | ||||||||

| Less: comprehensive (loss) attributable to non-controlling interest | (93,024 | ) | (48,226 | ) | (190,849 | ) | (164,354 | ) | ||||||||

| Comprehensive income (loss) attributable to the Company | $ | (96,821 | ) | $ | (50,194 | ) | $ | (198,641 | ) | $ | (171,063 | ) | ||||

See accompanying notes to these unaudited condensed consolidated financial statements

| 4 |

INTERNATIONAL PACKAGING AND LOGISTICS GROUP, INC., AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

FOR THE YEAR ENDED DECEMBER 31, 2015 AND NINE MONTHS ENDED SEPTEMBER 30, 2016

(UNAUDITED)

| Preferred Stock | Additional | Accumulated Other | Non | |||||||||||||||||||||||||||||||||||||

| Series A | Common Stock | Paid-In | Subscription | Comprehensive | Accumulated | Controlling | ||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Receivable | Income(Loss) | (Loss) | Interest | Total | |||||||||||||||||||||||||||||||

| December 31, 2014 | – | $ | – | 2,040,000 | $ | 2,040 | $ | 815,681 | – | $ | (6,855 | ) | $ | (147,439 | ) | $ | 675,841 | $ | 1,399,268 | |||||||||||||||||||||

| Net (Loss) | – | – | – | – | – | – | (23,498 | ) | (176,254 | ) | (191,919 | ) | (391,671 | ) | ||||||||||||||||||||||||||

| December 31, 2015 | – | $ | – | 2,040,000 | $ | 2,040 | $ | 815,681 | – | $ | (30,353 | ) | $ | (323,693 | ) | $ | 483,922 | $ | 947,597 | |||||||||||||||||||||

| Recapitalization | 947,730 | $ | 98 | 4,504,214 | (4,504 | ) | 35,398 | – | – | – | 40,000 | |||||||||||||||||||||||||||||

| Subscription Receivable | $ | (41,289 | ) | (41,289 | ) | |||||||||||||||||||||||||||||||||||

| Cumulative comprehensive (Loss) | – | – | – | – | – | – | (11,624 | ) | – | (11,168 | ) | (22,792 | ) | |||||||||||||||||||||||||||

| Net (Loss) | – | – | – | – | – | – | – | (208,700 | ) | (157,998 | ) | (366,698 | ) | |||||||||||||||||||||||||||

| September 30, 2016 (Unaudited) | 974,730 | $ | 98 | 6,544,214 | $ | 6,544 | $ | 851,079 | $ | (41,289 | ) | $ | (41,977 | ) | $ | (532,393 | ) | $ | 314,756 | $ | 556,818 | |||||||||||||||||||

See accompanying notes to these unaudited condensed consolidated financial statements

| 5 |

International Packaging and Logistics Group, Inc., and Subsidiaries

Condensed Consolidated Statements of Cash Flows

For the Nine Months Ended September 30, 2016 and 2015

(Unaudited)

| September 30 | September 30 | |||||||

| 2016 | 2015 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (366,698 | ) | $ | (304,642 | ) | ||

| Adjustments to reconcile net loss to net cash provided by operating activities: | ||||||||

| Depreciation expense | 148,167 | 77,223 | ||||||

| Amortization | 11,662 | 8,644 | ||||||

| Changes in operating assets and liabilities: (Increase) decrease in assets | ||||||||

| Accounts receivable | (54,259 | ) | – | |||||

| Other receivable | (13,431 | ) | (64,688 | ) | ||||

| Prepaid expenses | 139,336 | (1,798,501 | ) | |||||

| Inventory | (163,195 | ) | (98,017 | ) | ||||

| Increase (decrease) in liabilities | ||||||||

| Accounts payable and accrued expenses | 402,185 | 1,556,002 | ||||||

| Customer deposit | (39,562 | ) | 280,610 | |||||

| Tax payable | – | 10,622 | ||||||

| Other payable | 49,597 | 199,071 | ||||||

| Net cash provided by (used in) operating activities | 113,802 | (133,676 | ) | |||||

| Cash flows from investing activities: | ||||||||

| Purchase of property and equipment | (479,004 | ) | (444,651 | ) | ||||

| Purchase of land use rights | – | (329,664 | ) | |||||

| Net cash used in investing activities | (479,004 | ) | (774,315 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Advances from related parties | 1,414,203 | 773,556 | ||||||

| Repayment of loan | (1,064,073 | ) | – | |||||

| Net cash provided by (used in) financing activities | 350,130 | 773,556 | ||||||

| Effect of currency translation | (419 | ) | (1,052 | ) | ||||

| Net (decrease) in cash | (15,491 | ) | (135,487 | ) | ||||

| Cash at beginning of period | 21,747 | 140,317 | ||||||

| Cash at end of period | $ | 6,256 | $ | 4,830 | ||||

| Supplementary Disclosures of Cash Flow | ||||||||

| Cash paid during the period for: | ||||||||

| Interest | $ | 45,671 | $ | 107,696 | ||||

| Income taxes | $ | – | $ | – | ||||

See accompanying notes to these unaudited condensed consolidated financial statements

| 6 |

International Packaging and Logistics Group, Inc., and Subsidiaries

Notes to Unaudited Condensed Consolidated Financial Statements

September 30, 2016

NOTE 1 - ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization and Operations – International Packaging and Logistics Group, Inc., (The “Company” or “IPLO”), a Nevada corporation, was originally incorporated on June 2, 1986, in the state of Delaware. On April 17, 2008, the Company converted from a Delaware corporation to a Nevada Corporation.

On July 2, 2007, the Company through its wholly-owned subsidiary, YesRx.com (“YesRx”) acquired all the outstanding shares of H&H Glass, Inc. (“H&H Glass”), in exchange for 3,915,000 shares of its common stock in a reverse triangular merger.

On May 15, 2016, the Company, and Xiuhua Song (the “Purchaser”) entered into a Stock Purchase Agreement (the “Purchase Agreement”), pursuant to which IPLO (the “Seller”) would sell to the Purchaser, and the Purchaser will purchase from the Seller, an aggregate of 3,915,000 newly issued shares of IPLO Common Stock (the “Shares”), which Shares represent 87% of the issued and outstanding shares of Common Stock. On July 1, 2016, this transaction was completed.

On July 1, 2016, Standard Resources Ltd. (“Standard”) previously IPLO’s Majority Stockholder, and IPLO entered into a share purchase agreement (“H&H Vend Out”) whereby Standard would cancel 3,915,000 shares of IPLO common stock held by it in exchange for all of the outstanding shares of H&H Glass, Inc. (“H&H Glass”) The H&H Glass Vend Out was completed on August 31, 2016.

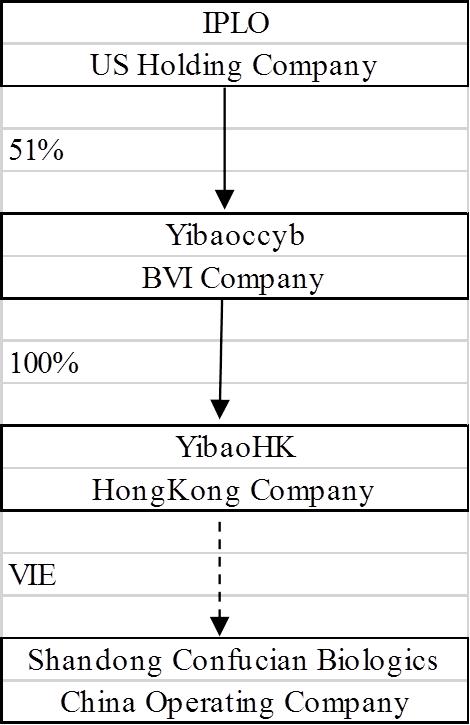

On July 1, 2016, the Company executed a Share Exchange Agreement (“Exchange Agreement”) by and among Yibaoccyb Limited, a British Virgin Islands limited liability company (“Yibaoccyb”), and the stockholders of 51% of Yibaoccyb’s common stock (the “Yibaoccyb Shareholders”), on the one hand, and the Company, on the other hand. Yibaoccyb owns 100% of YibaoConfucian Co., Ltd. (“YibaoHK”), a Hong Kong company. YibaoHK owns or will own 100% of Shenzhen Confucian Biologics Co. Ltd. (“Yibao WOFE”), which is a wholly foreign-owned enterprise (“WFOE”) under the laws of the Peoples’ Republic of China (“PRC” or “China”). On August 31, 2016, YibaoHK entered into a series of contractual arrangements with Shandong Confucian Biologics Co., Ltd. (“Shandong Confucian Biologics” or “Confucian”) which is a limited liability company headquartered in, and organized under the laws of, the PRC. The contractual arrangements are discussed below. Throughout this Form 10-Q, Yibaoccyb, Yibao WOFE and Shandong Confucian Biologics are sometimes collectively referred to as the “Yibao Group.”

The Exchange Agreement was completed on August 31, 2016 concurrent with the H&H Vend Out. The Company issued 2,040,000 shares of the Registrant’s common stock (the “IPLO Shares”) to the Yibaoccyb Shareholders in exchange for 51% of the common stock of Yibaoccyb (the “Exchange Agreement”).

Yibaoccyb Limited is a limited liability company incorporated under the laws of the British Virgin Islands on May 30, 2016. Other than all the issued and outstanding shares of Yibao Confucian Co. Ltd., Yibaoccyb has no other assets or operations.

YibaoHK is a limited liability company incorporated under the laws of the Hong Kong on June 15, 2016, which was formed by Yibaoccyb, a British Virgin Island. YibaoHK entered a series of contractual arrangements with the Shandong Confucian Biologics Co., Ltd.

Shandong Confucian Biologics was founded under the laws of the People's Republic of China on October 31, 2012. Confucian is in Food Industrial Park inside the economic development Zone of JinXiang County, Jining City in the province of Shan Dong in China. The Company is a limited liability company.

Confucian possesses manufacturing permits for food product, hygienic products, sanitary products, and health products. The Company's main business scope include technology study and transfer of Chondroitin and Garlic Oil; trading, cold storage, and pretreating of Garlic, fruit, and vegetables products; trading of Chemical products (excluding hazardous chemicals); Import and export of goods and technology (excluding those restricted by China government); the manufacturing and sale of health products including powder, granules, tablets, hard capsule, soft capsule products.

| 7 |

Details of the Company’s structure as of September 30, 2016 is as follow:

Reverse Merger Accounting – Since former Yibaoccyb security holders owned, after the Merger, approximately 87% of the Company’s shares of common stock, and because of certain other factors, including that the member of the Company's executive management is from Yibaoccyb, Yibaoccyb is deemed to be the acquiring company for accounting purposes and the Merger was accounted for as a reverse merger and a recapitalization in accordance with generally accepted accounting principles in the United States ("GAAP"). These unaudited condensed consolidated financial statements reflect the historical results of Confucian prior to the Merger and that of the combined Company following the Merger, and do not include the historical financial results prior to the completion of the Merger. Common stock and the corresponding capital amounts of the Company pre-Merger have been retroactively restated as capital stock shares reflecting the exchange ratio in the Merger.

Basis of Accounting and Presentation - The accompanying unaudited condensed financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America.

Principles of Consolidation - The accompanying unaudited condensed consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America. Confucian’s functional currency is Chinese Yuan (CNY), however, the accompanying consolidated condensed financial statements have been re-measured and presented in United States Dollars ($).

The consolidated financial statements include the accounts of IPL Group and its subsidiaries (collectively the “Company”). The Company’s subsidiaries include 51% of Yibaoccyb, YibaoHK and Confucian. 49% Yibaoccyb’s operating result was shown in minority interest on consolidated balance sheet.

Intercompany accounts and transactions have been eliminated upon consolidation.

Use of Estimates - The preparation of unaudited condensed financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimate and assumptions that affect certain reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

| 8 |

Cash and Cash Equivalents – For purpose of the statements of cash flows, the Company considers all highly liquid debt instruments purchased with a maturity of 90 days or less to be cash equivalents.

Accounts Receivable - The Company extends credit to its customers. Accounts receivable was recorded at the contract amount after deduction of trade discounts and, allowances, if any, and do not bear interest. The allowance for doubtful accounts, when necessary, is the Company’s best estimate of the amount of probable credit losses from accounts receivable. The Company determines the allowance based on historical write-off experience, customer specific facts and economic conditions.

As of September 30, 2016 and December 31, 2015, accounts receivable was $56,948 and $3,521, respectively. The Company believes that its accounts receivable are fully collectable and determined that an allowance for doubtful accounts was not necessary.

Account balances are charged off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. The Company does not have any off-balance-sheet credit exposure related to its customers.

Inventories - Inventory is valued at the lower of cost or market. Cost is determined using first-in, first-out method.

Inventory, comprised principally of finished goods, raw material and packaging material, are valued at the lower of cost or market.

| September 30, 2016 (Unaudited) | December 31, 2015 | |||||||

| Finished goods | $ | 199,304 | $ | 353 | ||||

| Raw materials | 55,741 | 79,282 | ||||||

| Packaging material | 21,420 | 33,859 | ||||||

| Supplies | 28 | 5,406 | ||||||

| Total | $ | 276,493 | $ | 118,900 | ||||

The Company periodically estimates an inventory allowance for estimated unmarketable inventories. Inventory amounts are reported net of such allowances, if any. There were no allowances for inventory as of September 30, 2016 and December 31, 2015.

Property, Plant and Equipment – Property, plant, and equipment are stated at cost less accumulated depreciation. The costs of a constructed asset are accumulated in the account Construction-in-Progress until the asset is placed into service. When the asset is completed and placed into service, the account Construction-in-Progress will be credited for the accumulated costs of the asset and will be debited to the appropriate Property, Plant and Equipment account. Depreciation begins after the asset has been placed into service.

Expenditures for maintenance and repairs are charged to operations; major expenditures for renewals and betterments are capitalized. Assets that are still kept in service after reaching the end of their estimated useful lives are depreciated over the estimated useful life of their residual value. Gain or loss on disposal of property, plant, and equipment is recognized as non-operating income or expenses.

Depreciation is computed by applying the following methods and estimated lives:

| Category | Estimated Life | Method | ||||

| Manufacturing equipment | 10 | Straight Line | ||||

| Office equipment | 5 | Straight Line | ||||

| Buildings | 20 | Straight Line | ||||

| 9 |

Intangible Assets - Land use rights represent the exclusive right to occupy and use a piece of land in the PRC during the contractual term of the land use right. Land use rights are carried at cost and charged to expense on a straight-line basis over the respective periods of the rights of 50 years or the remaining period of the rights upon acquisition.

Non-Controlling Interest – The Company accounted its non-controlling interest of 49% in Yibaoccyb. In consolidated financial statements classified as separate component of equity. In addition, net loss, and components of other comprehensive income are attributed to both the Company and non-controlling interest.

Revenue Recognition - The Company recognizes product revenue in accordance with ASC 605. ASC 605 requires that four basic criteria must be met before revenue can be recognized: (i) persuasive evidence of an arrangement exists, (ii) delivery has occurred, (iii) the price paid by the customer is fixed or determinable and (iv) collection of the resulting account receivable is reasonably assured. The Company recognizes revenue for product sales upon transfer of title to the customer. Customer purchase orders and/or contracts are generally used to determine the existence of an arrangement. Shipping documents and terms and the completion of any customer acceptance requirements, when applicable, are used to verify product delivery. The Company assesses whether a price is fixed or determinable based upon the payment terms associated with the transaction and whether the sales price is subject to refund or adjustment. The Company has no product returns or sales discounts and allowances because goods delivered and accepted by customers are normally not returnable.

Cost of goods sold- Cost of goods sold includes cost of inventory sold during the period, net of discounts and inventory allowances, freight and shipping costs, warranty and rework costs, and sales tax.

Impairment of Long-Live Assets – The Company applies FASB ASC 360, “Property, Plant and Equipment,” which addresses the financial accounting and reporting for the recognition and measurement of impairment losses for long-lived assets. In accordance with ASC 360, long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. The Company will recognize the impairment of long-lived assets in the event the net book value of such assets exceeds the future undiscounted cash flows attributable to those assets. There are no impairment of our long-lived assets for the nine months ended 2016 and 2015.

Income Taxes – The Company adopts FASB ASC Topic 740, "Income Taxes,” which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the consolidated financial statements or tax returns. Under this method, deferred income taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each period end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established, when necessary, to reduce deferred tax assets to the amount expected to be realized.

In accordance with ASC Topic 740-10, “Accounting for Uncertainty in Income Taxes — An Interpretation of FASB ASC Topic 740”, which requires income tax positions to meet a more-likely-than-not recognition threshold to be recognized in the financial statements. Tax positions that previously failed to meet the more-likely-than-not threshold should be recognized in the first subsequent financial reporting period in which that threshold is met. Previously recognized tax positions that no longer meet the more-likely-than-not threshold should be derecognized in the first subsequent financial reporting period in which that threshold is no longer met.

The application of tax laws and regulations is subject to legal and factual interpretation, judgment and uncertainty. Tax laws and regulations themselves are subject to change because of changes in fiscal policy, changes in legislation, the evolution of regulations and court rulings. Therefore, the actual liability may be materially different from our estimates, which could result in the need to record additional tax liabilities or potentially reverse previously recorded tax liabilities or deferred tax asset valuation allowance.

The Company has made a comprehensive review of its portfolio of tax positions in accordance with recognition standards established by ASC 740-10 and has not recognized any material uncertain tax positions.

In addition, companies in the PRC are required to pay an Enterprise Income Tax at 25%.

| 10 |

Foreign Currency Translation - The Company's functional currency is the Chinese Renminbi (RMB). The reporting currency is that of the US Dollar. Assets, liabilities and owners’ contribution are translated at the exchange rates as of the balance sheet date. Income and expenditures are translated at the average exchange rate of the year. The RMB is not freely convertible into foreign currency and all foreign currency exchange transactions must take place through authorized institutions. No representation is made that the RMB amounts could have been, or could be, converted into US dollar at the rates used in translation.

The exchange rates used to translate amounts in RMB into USD for the purposes of preparing the financial statements were as follows:

| September 30, 2016 | ||

| Balance sheet | RMB 6.67 to US $1.00 | |

| Statement of operation and other comprehensive income-nine-month period | RMB 6.58 to US $1.00 | |

| Statement of operation and other comprehensive income-three-month period | RMB 6.66 to US $1.00 | |

| December 31, 2015 | ||

| Balance sheet | RMB 6.36 to US $1.00 | |

| September 30, 2015 | ||

| Statement of operation and other comprehensive income-nine-month period | RMB 6.25 to US $1.00 | |

| Statement of operation and other comprehensive income-three-month period | RMB 6.30 to US $1.00 |

Fair Value of Financial Instruments – FASB ASC 820, “Fair Value Measurement” specifies a hierarchy of valuation techniques based upon whether the inputs to those valuation techniques reflect assumptions other market participants would use based upon market data obtained from independent sources (observable inputs). In accordance with ASC 820, the following summarizes the fair value hierarchy:

Level 1 Inputs— Unadjusted quoted market prices for identical assets and liabilities in an active market that the Company has the ability to access.

Level 2 Inputs— Inputs other than the quoted prices in active markets that are observable either directly or indirectly.

Level 3 Inputs— Inputs based on valuation techniques that are both unobservable and significant to the overall fair value measurements.

ASC 820 requires the use of observable market data, when available, in making fair value measurements. When inputs used to measure, fair value fall within different levels of the hierarchy, the level within which the fair value measurement is categorized is based on the lowest level input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs.

The Company did not identify any assets or liabilities that are required to be presented at fair value on a recurring basis. Carrying values of non-derivative financial instruments, including cash and cash equivalents, accounts receivable, inventories, prepaid expenses, advances from customers, accounts payable, taxes payable, accrued liabilities and other payables, and loan from bank, approximated their fair values due to the short maturity of these financial instruments. There were no changes in methods or assumptions during the periods presented.

Net Earnings (Loss) Per Share – Earnings/(loss) per common share is computed on the weighted average number of common shares outstanding during each year. Basic earnings per share is computed as net loss applicable to common stockholders divided by the weighted average number of common shares outstanding for the period. Diluted earnings per share reflects the potential dilution that could occur from common shares issuable through convertible preferred shares, stock options, warrants and other convertible securities when the effect would be dilutive. In this case, the Preferred Shares would not be dilutive since the conversion price is $3.00 and the quoted price is significantly lower than the conversion price. Therefore, there were no dilutive securities for the three and nine months ending September 30, 2016 and 2015, respectively.

| 11 |

NOte 2 - going concern

The Company sustained operating losses of $366,698 and $304,642 during the nine months ended September 30, 2016 and 2015, respectively. The Company has accumulated deficit of ($532,393) and ($323,693) as of September 30, 2016 and December 31, 2015, respectively. The Company’s continuation as a going concern is dependent on its ability to generate sufficient cash flows from operations to meet its obligations and/or obtain additional financing, as may be required.

The accompanying financial statements have been prepared assuming the Company will continue as a going concern; however, the above condition raises substantial doubt about the Company’s ability to do so. The financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result should the Company be unable to continue as a going concern.

NOte 3 - concentration of credit risk

We maintain our cash balance in several banks in China. These accounts are not insured and we believe are exposed to credit risk on cash. The cash balance in China as of September 30, 2016 and December 31, 2015 are $6,256 and $21,747 respectively.

NOTe 4 - other receivable

Total other receivable consists of balance of VAT receivable of $81,369 and $90,841 as of September 30, 2016 and December 31, 2015, respectively.

NOTe 5 - prepaid expenses

Prepaid expenses were comprised of the following:

| September 30, 2016 (Unaudited) | December 31, 2015 | |||||||

| Prepaid property and equipment | $ | 17,417 | $ | 183,018 | ||||

| Inventory | 9,387 | 1,275 | ||||||

| Utilities | 8,767 | 9,025 | ||||||

| Other | 16,495 | 1,783 | ||||||

| Total | $ | 52,066 | $ | 195,101 | ||||

Note 6- property, plant and equipment

Property, plant and equipment as of September 30, 2016 and December 31, 2015 are summarized as following:

| September 30, 2016 (Unaudited) | December 31, 2015 | |||||||

| Buildings | $ | 1,811,395 | $ | 1,864,722 | ||||

| Vehicles | 11,622 | 11,964 | ||||||

| Manufacturing equipment | 1,019,093 | 569,780 | ||||||

| Office equipment | 82,297 | 77,583 | ||||||

| Property, plant, and equipment - total | 2,924,407 | 2,524,049 | ||||||

| Less: accumulated depreciation | (262,152 | ) | (119,399 | ) | ||||

| Fixed assets, net | $ | 2,662,255 | $ | 2,404,650 | ||||

For the three-months ended September 30, 2016 and 2015, depreciation expense was $50,331 and $35,964, respectively. For the nine-months ended September 30, 2016 and 2015, depreciation expense was $148,167 and $77,223, respectively.

| 12 |

note 7- intangible assets - net

All land in the PRC is owned by the government and cannot be sold to any individual or entity. Instead, the government grants landholders a "land use right" after a purchase price for such "land use right" is paid to the government. The "land use right" allows the holder to use the land for 50 years and enjoys all the incidents of ownership of the land. As of September 30, 2016, and December 31, 2015, the land use rights net of amortization was $727,557 and $760,819, respectively. The use term was 50 years.

The summary of land use rights as of September 30, 2016 and December 31, 2015 are summarized as following:

| The land use right term | September 30, 2016 (Unaudited) | December 31, 2015 | ||||||

| May, 2013-April, 2063 | $ | 539,873 | $ | 555,766 | ||||

| Dec, 2015-Sep, 2065 | 202,444 | 208,404 | ||||||

| Dec, 2015-Sep, 2065 | 24,638 | 25,363 | ||||||

| Intangible assets- total | 766,955 | 789,534 | ||||||

| Less: accumulated amortization | (39,398 | ) | (28,715 | ) | ||||

| Intangible assets, net | $ | 727,557 | $ | 760,819 | ||||

For the three-months ended September 30, 2016 and 2015, amortization expense was $3,837 and $2,856, respectively. For the nine-months ended September 30, 2016 and 2015, amortization expense was $11,662 and $8,644, respectively.

note 8- short term loan

The Company entered a short-term loan agreement with rural credit cooperative of Shandong. The maximum loan amount is $1,543,734 and the balance was $0 and $1,080,614 as of September 30, 2016 and December 31, 2015, respectively. The term of the loan is from August 6, 2015 and expired at August 5, 2016. The Company paid off the loan using funds borrowed from related party-Shandong Yibao Biologics Co., Ltd. during the period ended September 30, 2016. The interest rate is fixed at 8.245%. Interest is calculated from the day the loan is used and due monthly. The loan was guaranteed by owner and collateralized with land use rights and 3 manufacturing buildings owned by the Company.

note 9- stockholderS’ equity

Common stock:

On July 1, 2016, Ms. Xiuhua Song paid USD $225,000 to purchase 3,915,000 shares from the Company.

On August 31, 2016, Standard cancelled 3,915,000 shares of the Company’s common stock in exchange from all of the outstanding shares of H&H Glass.

On August 31, 2016, the Company issued 2,040,000 shares to Yibaoccyb Shareholders in exchange for 51% of the common stock of Yibaoccyb.

Series A Preferred Shares:

The Series A Preferred shares are convertible into common shares on a 1:1 ratio at a fixed rate of $3 per share. Preferred shares have no voting rights, have no redemption rights and earn no dividends. Holders of Series A Convertible Preferred Stock are not permitted to convert their stock into common shares until the Company’s market capital reaches $15,000,000. Upon dissolution, liquidation or winding up of the Company, whether voluntary or involuntary, the holders of the then outstanding shares of Series A Convertible Preferred Stock shall be entitled to receive out of the assets of the Company the sum of $0.0001 per share (the “Liquidation Rate”) before any payment or distribution shall be made on any other class of capital stock of the Company ranking junior to the Series A Convertible Preferred Stock.

| 13 |

ASC Topic 480, “Distinguishing Liabilities from Equity,” establishes standards for how an issuer classifies and measures certain financial instruments with characteristics of both liabilities and equity.

A mandatorily redeemable financial instrument shall be classified as a liability unless the redemption is required to occur only upon the liquidation or termination of the reporting entity. A financial instrument issued in the form of shares is mandatorily redeemable if it embodies an unconditional obligation requiring the issuer to redeem the instrument by transferring its assets at a specified or determinable date (or dates) or upon an event certain to occur. A financial instrument that embodies a conditional obligation to redeem the instrument by transferring assets upon an event not certain to occur becomes mandatorily redeemable—and, therefore becomes a liability—if that event occurs, the condition is resolved, or the event becomes certain to occur.

The Company determined that the preferred shares are not mandatorily or conditionally redeemable and are properly classified as permanent equity in the accompanying unaudited condensed consolidated financial statements.

Subscription receivable

Subscription receivable includes unpaid stock issuance of 40,000 shares at $1 per share totaling $40,000 by issued Yibaoccyb and 10,000 shares at $0.13 per share total $1,289 issued by YibaoHK.

note 10- related party transactions

| Name of related party | Relationship | |

| Wenxiu Song | Owner of Shandong Confucian Biologics | |

| Hengchun Zhang | Owner of Shandong Confucian Biologics | |

| Qinbao Kong | Xiuhua Song's spouse | |

| Xiuhua Song | CEO and Director | |

| Shandong Yibao Biologics Co., Ltd. | Affiliated company with common shareholders |

The Company is still in start-up stage, to sustain the Company’s operating, construct manufacturing building and purchase equipment, current and previous owners along with its affiliated company needed to loan the Company money through their own account. In June 2016, Shandong Yibao Biologics Co., Ltd. advanced funds to the Company $1,064,073 to pay off the short-term loan. The Company has the following payables to related parties:

| September 30, 2016 (Unaudited) | December 31, 2015 | |||||||

| To Shandong Yibao Biologics Co., LTD | $ | 1,416,623 | $ | 218,672 | ||||

| To Xiuhua Song | 1,121,786 | 995,713 | ||||||

| To Wenxiu Song | – | 138,936 | ||||||

| To Hengchun Zhang | 152,536 | – | ||||||

| To Qingbao Kong | 6,115 | – | ||||||

| $ | 2,697,060 | $ | 1,353,321 | |||||

NOTE 11 - MAJOR SUPPLIERS AND CUSTOMERS

The Company purchases majority of its inventory and packaging supplies from four suppliers which accounted for 56.87% of the total purchases in nine-month period ended September 30, 2016.

The Company had two major customers for the nine-month period ended September 30, 2016: Ping Xiang Import and Export Company accounted for 65.29% of revenue and Jiangxi Financial Holding Group Co., Ltd accounted for 15.76% of revenue for the nine-month period ended September 30, 2016.

The Company purchases majority of its inventory and packaging supplies from four suppliers which accounted for 55.04% of the total purchases in nine-month period ended September 30, 2015.

The Company had one major customer for the nine-month period ended September 30, 2015: Ping Xiang Import and Export Company accounted for 100% of revenue for the nine-month period ended September 30, 2015.

| 14 |

ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

The information contained in this Form 10-Q is intended to update the information contained in our Annual Report on Form 10-K for the year ended December 31, 2015 and presumes that readers have access to, and will have read, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and other information contained in such Form 10-K. The following discussion and analysis also should be read together with our financial statements and the notes to the financial statements included elsewhere in this Form 10-Q.

The following discussion contains certain statements that may be deemed “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements appear in a number of places in this Report, including, without limitation, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements are not guarantees of future performance and involve risks, uncertainties and requirements that are difficult to predict or are beyond our control. Forward-looking statements speak only as of the date of this quarterly report. You should not put undue reliance on any forward-looking statements. We strongly encourage investors to carefully read the factors described in our Annual Report on Form 10-K for the year ended December 31, 2015 in the section entitled “Risk Factors” for a description of certain risks that could, among other things, cause actual results to differ from these forward-looking statements. We assume no responsibility to update the forward-looking statements contained in this quarterly report on Form 10-Q. The following should also be read in conjunction with the unaudited condensed Financial Statements and notes thereto that appear elsewhere in this report.

Overview

The Company is a manufacture and research based bio-science company. It has large capacity in manufacturing tablets, granule, oral liquid, powders, soft gels and capsules products. The Company distributes its products through its own network and white label products. It also has access to a member-based distribution system owned by its affiliated company.

The Company possesses manufacturing permits for food product, hygienic products, sanitary products, and health products. The Company's main business scope include technology study and transfer of Chondroitin and Garlic Oil; trading, cold storage, and pretreating of Garlic, fruit, and vegetables products; trading of Chemical products (excluding hazardous chemicals); Import and export of goods and technology (excluding those restricted by government); the manufacturing and sale of health products including powder, granules, tablets, hard capsule, soft capsule products.

Product Overview

The Company’s main products can be divided into two groups, one is health food products and the other is hygienic products.

Health Food Products

| · | Phytocholesterol tabletting candy, |

Phytosterol has strong anti-inflammatory effects to the human body, which can inhibit the absorption of cholesterol for human and biochemical synthesis of cholesterol. Promote the degradation and metabolism of cholesterol. Phytosterol can be used for prevention & therapy of coronary atherosclerosis heart disease. In treating ulcers, skin squamous carcinoma and cervical cancer has obvious curative effect. Can promote wound healing, make muscle proliferation, enhance capillary circulation; also can be used as blocking agent of formation of gallstones.

| · | Polydextrose tabletting candy, |

Regulating blood lipid, reduce fat accumulation preventing the fat.

| · | Dunaliella salina Haematococcus pluvialis tabletting candy, |

Replenishing the body's astaxanthin, Natural carotene and variety of minerals, have a great effect of antioxidant activity, protect skin, protect vision and improve immunity.

| 15 |

| · | Dunaliella salina Gum Base Candy, |

Dunaliella salina is rich in antioxidant needed by the human body health, resistance to radiation and enhance human immunity of natural carotenoids and 70 kinds of minerals and trace elements.

| · | Haematococcus pluvialis Gum Candy, |

The main components of Haematococcus Pluvialis is astaxanthin. It has six anti-aging effect: can be Anti-aging and protect the skin; Protect the eye health; helps to support the cardiovascular system, maintain a healthy joints and connective tissue; increases strength and endurance.

| · | Fish Oil Gum Candy, |

Adjusting blood liquid, prevent blood clots, cerebral thrombosis, cerebral hemorrhage and stroke; prevent arthritis and alzheimer's disease, improve the memory and vision, control presbyopia.

| · | Earthworm Protein tabletting Candy, |

Improve blood circulation, inhibiting platelet aggregation, reduce glucose concentrations, prevent blood clots, has the very good control efficiency for coronary heart disease, arteriosclerosis, and other hematologic disorders.

| · | Collagen Protein tabletting candy, |

It is rich in glycine, proline hydroxyproline and other amino acid needed for human body. Have a good health care effect for skin, hair, bones and muscles.

| · | Krill Oil Gum candy, |

It is rich in EPA and DHA. Enhancing health effects, including cardiovascular, nerve, bones, joints, vision, skin care, etc.

| · | Phosphatidylserine tabletting candy, |

Improve the function of brain; help to repair the injure of brain; promote the recovery of brainfag; protect central nervous system. Used for auxiliary treatment dementia and agedness memory loss.

| · | Milk Powder tabletting Candy. |

Milk tablet is kind of leisure food. Supplement of the nutrition of human needed in pecific environment.

Hygienic Products

The hygienic product line include the following products:

| · | Gel for women, |

Anti-bacteria product. Auxiliary treatment bacterial, mould sex vaginitis.

| · | Skin comfortable liquid |

Anti-bacteria product. Used for sterilization, antibacterial of skin. Inhibit the bromhidrosis and relief beriberi itch Shandong Confucian Biologics owns 100,000 stage purification workshops, advanced production lines and manufacturing equipment. The Company has a higher capacity for OEM processing of tablets, hard capsules, soft capsules, oral liquid, granules, and powders.

Plan of Operations

By following the Company motto of "being passionate for health industry, bringing together the world's resources, focusing on consumer demand, creating a “win-win situation", the Company is eager to develop businesses in the international health and pharmaceutical market.

The Company’s near term goal is to reach breakeven within a 6 month period time. In order to reach such goal, the Company is increasing its sales and production volume through arrangements and networking with its existing customers and its affiliated companies. Additionally, it plans to increase the size of its sales department to develop new customers.

The Company’s ultimate goal is to make the business profitable and competitive in the international health and pharmaceutical market. To achieve such goal, the Company needs to cooperate with other businesses having capital, market, technology, or products, recruit sufficient workforce and various talents to serve the company, and actively develop new technology and new product through research and development.

| 16 |

Results of Operations

Three and Nine Months Ending September 30, 2016 Compared to September 30, 2015

Revenue:

For the three months ending September 30, 2016 and 2015, revenues were $149,021 and $57,761 respectively, for an increase of $91,260 over the same period in 2015. For the nine months ending September 30, 2016 and 2015 revenues were $455,017 and $58,275 respectively, for an increase of $396,742 over the same period in 2015. The increase in revenue is a mainly due to the company was still in development stage and had not started material production.

Cost of Goods Sold:

Cost of goods sold for the three months ending September 30, 2016 and 2015 were $125,418 and $84,009 respectively, for an increase of $41,409 over the same period in 2015. Cost of goods sold for the nine months ending September 30, 2016 and 2015 were $374,849 and $84,757 respectively, for an increase of $290,092 over the same period in 2015. This increase is mainly due to the plant barely had started manufacture referenced above.

Gross Profit:

Gross profit was $23,603 and ($26,248) for the three months ending September 30, 2016 and 2015, an increase of $49,851 over the same period in 2015. The gross profit margin as a percent of sales for the three months ending September 30, 2016 and 2015 was 16% and (45%) respectively for an increase period to period. The reason for the change of negative margin to positive margin is that the Company was not start operation till December 2015, but the production line workers were trained months prior to December 2015, and salaries of the production line workers were included in the cost of goods sold.

Gross profit was $80,168 and ($26,482) for the nine months ending September 30, 2016 and 2015, an increase of $106,650 over the same period in 2015. The gross profit margin as a percent of sales for the nine months ending September 30, 2016 and 2015 was 18% and (45%) respectively for an increase period to period. The reason for the change of negative margin to positive margin is the same as explanations in preceding paragraph.

Operating Expenses:

Operating expenses for the three-month period ended September 30, 2016 and 2015 were $143,903 and $19,739 respectively for an increase of $124,164 (629%) from the same period prior year. The major expenses for the three-month period ended September 30, 2016 and 2015 consist of payroll, professional fees and depreciation. For three-month ended September, 30, 2016, payroll was $17,408, professional fee was $68,208 and depreciation was $50,331. For three-month ended September 30, 2015, the major expenses consist payroll of $7,753, and selling expenses of $4,898

Operating expenses for the nine-month period ended September 30, 2016 and 2015 were $411,704 and $183,376 respectively for an increase of $228,328 (125%) from the same period prior year. The major expenses for the nine-month period ended September 30, 2016 and 2015 consist payroll, professional fee and depreciation. Payroll was$43,265, professional fee was $174,184 and depreciation was $148,167 for nine-month ended September 30, 2016. For nine-month ended September 30, 2015, payroll was $28,153 and depreciation was $140,963.

Other Income (Expense):

Other income (expense) for the three months ended September 30, 2016 and 2015 was ($392) and ($47,234) respectively for a decrease of $46,842 over the same period in 2015. The main reason for the decrease is due to the Company paid off the short-term loan from bank on June 2016.

Other income (expense) for the nine months ended September 30, 2016 and 2015 was ($35,162) and ($94,784), respectively for a decrease of $59,623 over the same period in 2015.

| 17 |

Liquidity and Capital Resources

The Company suffered recurring losses from operations and has an accumulated deficit of $532,393 at September 30, 2016. The Company has a cash balance of $6,256 and negative working capital of $2,832,994as of September 30, 2016. The Company has incurred losses of $366,698 and $304,642 for the nine months ended September 30, 2016 and 2015, respectively. The Company has not continually generated significant revenues. Unless our operations continue to generate significant revenues and cash flows from operating activities, our continued operations will depend on whether we are able to raise additional funds through various sources, such as equity and debt financing, other collaborative agreements and strategic alliances. Our management is actively engaged in seeking additional capital to fund our operations in the short to medium term. Such additional funds may not become available on acceptable terms and there can be no assurance that any additional funding that we do obtain will be sufficient to meet our needs in the long term.

Net cash provided by operating activities for the nine months ended September 30, 2016 amounted to $113,802, which mainly consisted of the following: Net loss of $366,698 from operations plus the following; 1) an increase in accounts payable and accrued expenses of $402,185; 2) decrease in prepaid expense of $139,336; offset by 1) an increase in account receivable of $54,259; and 2) increase in another receivable of $13,431. Net cash used in operating activities for the nine months ended September 30, 2015 amounted to $(133,677), which mainly consisted of the following: Net loss of $304,642 from operations plus the following; 1) an increase in accounts payable and accrued expenses of $1,556,002; 2) an increase in other payable of 199,071; 3) an increase in customer deposit of $280,610; offset by 1) an increase in prepaid expense of $1,798,501; and 2) increase in inventory of $98,017.

Net cash used in investing activities for the nine months ended September 30, 2016 amounted to $479,004, which mainly consisted of the purchase of property and equipment. Net cash used in investing activities for the nine months ended September 30, 2015 amounted to $774,314, which mainly consisted of the purchase of property and equipment of $444,651 and the purchase of land use rights of $329,664.

Net cash provided by financing activities for the nine months ended September 30, 2016 amounted to $350,130, which mainly consisted of the increase of other payable-related party of $1,414,203; offset by repayment of loan of $1,064,073. Net cash provided by financing activities for the nine-month ended September 30, 2015 was $773,556 which was due to increased advance from related parties.

Capital Resources

Over the next twelve months, management believes there will not be sufficient working capital obtained from operations due to the Company in its early development stage.

Off-Balance Sheet Arrangements

As of September 30, 2016, we did not have any off-balance sheet arrangements as defined in Item 303(a)(4)(ii) of Regulation S-K.

| 18 |

ITEM 3. Quantitative and Qualitative Disclosures about Mark Risk

As a “smaller reporting company” as defined by Item 10 of Regulation S-K, the Company is not required to provide the information required by this Item.

ITEM 4. Controls and Procedures.

Evaluation of Disclosure Controls and Procedures:

As of September 30, 2016, we conducted an evaluation under the supervision and with the participation of the Company's Chief Executive Officer and the Chief Financial Officer, management has evaluated the effectiveness of the design and operation of the Company's disclosure controls and procedures. Based on that evaluation and because of the material weaknesses in our internal control over financial reporting described below, the Chief Executive Officer and the Chief Financial Officer have concluded that the Company's disclosure controls and procedures were not effective as of September 30, 2016.

Management identified the following control deficiencies that constitute material weaknesses that are not fully remediated as of the filing date of this report:

Our size has prevented us from being able to employ sufficient resources to enable us to have an adequate level of supervision and segregation of duties within our internal control system. There is mainly one person involved in processing of transactions. Therefore, it is difficult to effectively segregate accounting duties. We have hired an additional administrative person and retained an outside professional firm to assist in mitigating the separation of duties issues on an ongoing basis. The use of the outside firm has proven successful in assisting in the separation of duties. However, additional people are not needed to do the administrative work therefore segregation of duties will continue to be an ongoing weakness.

Similarly, the Shandong Confucian Biologic Co., Ltd. operation also has a material weakness due to lack of segregation of duties. Its size has prevented us from being able to employ sufficient resources to enable us to have an adequate level of supervision and segregation of duties within our internal control system. We have retained an outside professional firm to assist in the separation of duties on an ongoing basis. The use of the outside firm has proven successful in assisting in the separation of duties.

Limitations on the Effectiveness of Internal Controls

Disclosure controls and procedures, no matter how well designed and implemented, can provide only reasonable assurance of achieving an entity's disclosure objectives. The likelihood of achieving such objectives is affected by limitations inherent in disclosure controls and procedures. These include the fact that human judgment in decision-making can be faulty and that breakdowns in internal control can occur because of human failures such as simple errors or mistakes or intentional circumvention of the established process.

Changes in Internal Control over Financial Reporting

There were no changes in internal control over financial reporting that occurred during the current quarter covered by this report that have materially affected, or are reasonably likely to affect, the Company's internal control over financial reporting.

| 19 |

PART II. OTHER INFORMATION

ITEM 1. Legal Proceedings

None

ITEM 1A – RISK FACTORS

You should carefully consider the risks described below together with all of the other information included in this report before making an investment decision with regard to our securities. The statements contained in or incorporated into this offering that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Industry

Our businesses are subject to fluctuations in operating results due to general economic conditions, specific economic conditions in the industries in which it operates and other external forces.

Our businesses and operations could be affected by the following, among other factors:

| - | changes in general economic conditions and specific conditions in industries in which our businesses operate that can result in the deferral or reduction of purchases by end-use customers; |

| - | the effects of terrorist activity and international conflicts, which could lead to business interruptions; |

| - | the size, timing and cancellation of significant orders, which can be non-recurring; |

| - | market acceptance of new products and product enhancements; |

| - | announcements, introductions and transitions of new products by us or our competitors; |

| - | deferrals of customer orders in anticipation of new products or product enhancements introduced by us or our competitors; |

| - | changes in pricing in response to competitive pricing actions; |

| - | supply constraints; |

| - | the level of expenditures on research and development and sales and marketing programs; |

| - | our ability to achieve targeted cost reductions; |

| - | rising interest rates; and |

| - | excess facilities. |

| 20 |

The loss of Shandong Confucian Biologics as our operating business would have a material adverse effect on our business and the price of our common stock.

We have no equity ownership interest in Shandong Confucian Biologics. Our ability to control Shandong Confucian Biologics and consolidate its financial results is through a series of contractual agreements between it and YibaoHK. Management of Shandong Confucian Biologics is affiliates of us and the stockholders of Shandong Confucian Biologics are also our stockholders. Thus the VIE Agreements were not entered into as a result of arms’ length negotiations because the parties to the agreement are under common control. Ms. Song, our CEO and Chairman has control over of the shares of Shandong Confucian Biologics and of our common stock. The VIE Agreements may be terminated upon the termination of the business of Shandong Confucian Biologics. Any other termination would be a breach of the agreement. While the Company believes that the VIE Agreements are legal and enforceable under PRC law, these affiliates control the parties to the VIE Agreements and it could be possible for them to cause Shandong Confucian Biologics to breach the VIE Agreements and our unaffiliated investors would have little or no recourse because of the inherent difficulties in enforcing their rights since all our assets are located in the PRC. (See, PRC laws and regulations governing Shandong Confucian Biologics' current business are sometimes vague and uncertain.) In the event that management of Shandong Confucian Biologics decides to breach the VIE Agreements, the risk of loss of the affiliated shareholders of Shandong Confucian Biologics could be lower than unaffiliated investors and the interests of the management and shareholders of Shandong Confucian Biologics would be in conflict with the interest of our other stockholders.

Shandong Confucian Biologics’ failure to compete effectively may adversely affect our ability to generate revenue.

Shandong Confucian Biologics competes with other companies, many of whom are developing or can be expected to develop products similar to Shandong Confucian Biologics. Shandong Confucian Biologics’ market is a large market with many competitors. Many of its competitors are more established than Shandong Confucian Biologics is, and have significantly greater financial, technical, marketing and other resources than it presently possess. Some of Shandong Confucian Biologics’ competitors have greater name recognition and a larger customer base. These competitors may be able to respond more quickly to new or changing opportunities and customer requirements and may be able to undertake more extensive promotional activities, offer more attractive terms to customers, and adopt more aggressive pricing policies. We cannot assure you that Shandong Confucian Biologics will be able to compete effectively with current or future competitors or that the competitive pressures it faces will not harm it business.

We may not be able to effectively control and manage the growth of Shandong Confucian Biologics.

If Shandong Confucian Biologics’ business and markets grow and develop, it will be necessary for us to finance and manage expansion in an orderly fashion. An expansion would increase demands on its existing management, workforce and facilities. Failure to satisfy such increased demands could interrupt or adversely affect its operations and cause delay in production and delivery of its pharmaceutical prescription, over the counter and medical nutrient products as well as administrative inefficiencies.

We may require additional financing in the future and a failure to obtain such required financing will inhibit Shandong Confucian Biologics’ ability to grow.

The continued growth of Shandong Confucian Biologics’ business may require additional funding from time to time which we expect to raise in private placements of our equity or debt securities with accredited investors or by offering our securities for sale pursuant to an effective registration statement on a market where our common stock is traded. The proceeds of these funding will be forwarded to Shandong Confucian Biologics and accounted for as a loan to Shandong Confucian Biologics and eliminated during consolidation. The proceeds would be used for general corporate purposes of Shandong Confucian Biologics, which could include acquisitions, investments, repayment of debt and capital expenditures among other things. We may also use the proceeds to repurchase our capital stock or for our corporate overhead expenses. If we borrow funds we expect to be the primary obligor on any debt. Obtaining additional funding would be subject to a number of factors including market conditions, operating performance and investor sentiment, many of which are outside of our control. These factors could make the timing, amount, terms and conditions of additional funding unattractive or unavailable to us.

Our management believes that Shandong Confucian Biologics currently has sufficient funds from working capital to meet its current operating costs over the next 12 months.

| 21 |

The terms of any future financing may adversely affect your interest as stockholders.

If we require additional financing in the future, we may be required to incur indebtedness or issue equity securities, the terms of which may adversely affect your interests in us. For example, the issuance of additional indebtedness may be senior in right of payment to your shares upon our liquidation. In addition, indebtedness may be under terms that make the operation of Shandong Confucian Biologics' business more difficult because the lender's consent could be required before we take certain actions. Similarly the terms of any equity securities we issue may be senior in right of payment of dividends to your common stock and may contain superior rights and other rights as compared to your common stock. Further, any such issuance of equity securities may dilute your interest in us.

We may engage in future acquisitions that could dilute the ownership interests of our stockholders, cause us to incur debt and assume contingent liabilities.

We may review acquisition and strategic investment prospects that we believe would complement the current product offerings of Shandong Confucian Biologics, augment its market coverage or enhance its technical capabilities, or otherwise offer growth opportunities. From time to time we review investments in new businesses and expect to make investments in, and to acquire, businesses, products, or technologies in the future. We expect that when we raise funds from investors for any of these purposes we will be either the issuer or the primary obligor while the proceeds will be forwarded to Shandong Confucian Biologics and accounted for as a loan to Shandong Confucian Biologics and eliminated during consolidation. In the event of any future acquisitions, we could:

| · | issue equity securities which would dilute current stockholders’ percentage ownership; |

| · | incur substantial debt; |

| · | assume contingent liabilities; or |

| · | expend significant cash. |

These actions could have a material adverse effect on our operating results or the price of our common stock. Moreover, even if we do obtain benefits in the form of increased sales and earnings, there may be a lag between the time when the expenses associated with an acquisition are incurred and the time when we recognize such benefits. Acquisitions and investment activities also entail numerous risks, including:

| · | difficulties in the assimilation of acquired operations, technologies and/or products; |

| · | unanticipated costs associated with the acquisition or investment transaction; |

| · | the diversion of management’s attention from other business concerns; |

| · | adverse effects on existing business relationships with suppliers and customers; |

| · | risks associated with entering markets in which Shandong Confucian Biologics has no or limited prior experience; |

| · | the potential loss of key employees of acquired organizations; and |

| · | substantial charges for the amortization of certain purchased intangible assets, deferred stock compensation or similar items. |

We cannot ensure that we will be able to successfully integrate any businesses, products, technologies, or personnel that we might acquire in the future and our failure to do so could have a material adverse effect on our and/or Shandong Confucian Biologics' business, operating results and financial condition.

| 22 |

We are responsible for the indemnification of our officers and directors.

Our certificate of incorporation provides for the indemnification and/or exculpation of our directors, officers, employees, agents and other entities which deal with it to the maximum extent provided, and under the terms provided, by the laws and decisions of the courts of the state of Nevada. Since we do not hold any indemnification insurance, these indemnification provisions could result in substantial expenditures, which we may be unable to recoup, which could adversely affect our business and financial conditions. Xiuhua Song, our Chairman of Board, President, Chief Executive Officer, and Chief Financial Officer are key personnel with rights to indemnification under our certificate of incorporation.

We may not have adequate internal accounting controls. While we have certain internal procedures in our budgeting, forecasting and in the management and allocation of funds, our internal controls may not be adequate.

We are constantly striving to improve our internal accounting controls. We expect to continue to improve our internal accounting control for budgeting, forecasting, managing and allocating our funds and to better account for them as we grow. There is no guarantee that such improvements will be adequate or successful or that such improvements will be carried out on a timely basis. If we do not have adequate internal accounting controls, we may not be able to appropriately budget, forecast and manage our funds, we may also be unable to prepare accurate accounts on a timely basis to meet our continuing financial reporting obligations and we may not be able to satisfy our obligations under US securities laws.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and attestation of this assessment by our company's independent registered public accountants. The SEC extended the compliance dates for "non-accelerated filers," as defined by the SEC. Accordingly, we believe that the annual assessment of our internal controls requirement will first apply to our annual report for the 2007 fiscal year and the attestation requirement of management's assessment by our independent registered public accountants will first apply to our annual report for the 2009 fiscal year. The standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. We have not yet evaluated our internal controls over financial reporting in order to allow management to report on, and our independent auditors to attest to, our internal controls over financial reporting, as will be required by Section 404 of the Sarbanes-Oxley Act of 2002 and the rules and regulations of the SEC. We have never performed the system and process evaluation and testing required in an effort to comply with the management assessment and auditor certification requirements of Section 404, which will initially apply to us as of December 31, 2007 and December 31, 2009 respectively. Our lack of familiarity with Section 404 may unduly divert management's time and resources in executing the business plan. If, in the future, management identifies one or more material weaknesses, or our external auditors are unable to attest that our management's report is fairly stated or to express an opinion on the effectiveness of our internal controls, this could result in a loss of investor confidence in our financial reports, have an adverse effect on our stock price and/or subject us to sanctions or investigation by regulatory authorities. So far, our external auditors have not reported to our board of directors any significant weakness on our internal control and provided recommendations accordingly.

Shandong Confucian Biologics is Dependent On Certain Key Personnel And Loss Of These Key Personnel Could Have A Material Adverse Effect On Our and Shandong Confucian Biologics' Business, Financial Condition And Results Of Operations.

Our success is, to a certain extent, attributable to the management, sales and marketing, and manufacturing expertise of key personnel at Shandong Confucian Biologics. Xiuhua Song, our President, Chief Executive Officer and Chairman of the Board, performs key functions in the operation of our and Shandong Confucian Biologics' business. There can be no assurance that Shandong Confucian Biologics will be able to retain these officers after the term of their employment contracts expire. The loss of these officers could have a material adverse effect upon our business, financial condition, and results of operations. Shandong Confucian Biologics must attract, recruit and retain a sizeable workforce of technically competent employees. We do not carry key man life insurance for any of our key personnel or personnel at Shandong Confucian Biologics nor do we foresee purchasing such insurance to protect against a loss of key personnel and the key personnel of Shandong Confucian Biologics.

| 23 |

We and Shandong Confucian Biologics are dependent upon the services of Mrs. Song, for the continued growth and operation of our company because of his experience in the industry and his personal and business contacts in China. Neither we nor Shandong Confucian Biologics have an employment agreement with Mrs. Song and do not anticipate entering into an employment agreement in the foreseeable future. Although we have no reason to believe that Mrs. Song will discontinue her services with us or Shandong Confucian Biologics, the interruption or loss of his services would adversely affect our ability to effectively run Shandong Confucian Biologics' business and pursue its business strategy as well as our results of operations.

Shandong Confucian Biologics may not be able to hire and retain qualified personnel to support its growth and if it is unable to retain or hire these personnel in the future, its ability to improve its products and implement its business objectives could be adversely affected.

Competition for senior management and senior personnel in the PRC is intense, the pool of qualified candidates in the PRC is very limited, and Shandong Confucian Biologics may not be able to retain the services of its senior executives or senior personnel, or attract and retain high-quality senior executives or senior personnel in the future. This failure could materially and adversely affect our future growth and financial condition. Shandong Confucian Biologics expects to hire additional sales and plant personnel throughout fiscal year 2016 in order to accommodate its growth.

If Shandong Confucian Biologics fails to increase its brand recognition, it may face difficulty in obtaining new customers and business partners.

We believe that establishing, maintaining and enhancing Shandong Confucian Biologics’ brand in a cost-effective manner is critical to achieving widespread acceptance of Shandong Confucian Biologics’ current and future products and services and is an important element in Shandong Confucian Biologics' effort to increase its customer base and obtain new business partners. We believe that the importance of brand recognition will increase as competition in Shandong Confucian Biologics’ market develops. Some of Shandong Confucian Biologics’ potential competitors already have well-established brands in the pharmaceutical promotion and distribution industry. Successful promotion of Shandong Confucian Biologics’ brand will depend largely on its ability to maintain a sizeable and active customer base, its marketing efforts and its ability to provide reliable and useful products and services at competitive prices. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses Shandong Confucian Biologics incurs in building its brand. If Shandong Confucian Biologics fails to successfully promote and maintain its brand, or if Shandong Confucian Biologics incurs substantial expenses in an unsuccessful attempt to promote and maintain its brand, it may fail to attract enough new customers or retain its existing customers to the extent necessary to realize a sufficient return on its brand-building efforts, in which case Shandong Confucian Biologics' business, operating results and financial condition, further ours would be materially adversely affected.

Shandong Confucian Biologics' operating results may fluctuate as a result of factors beyond its control.