|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES |

|||||||||||||||||

|

SECURITIES AND EXCHANGE COMMISSION |

|||||||||||||||||

|

Washington, D.C. 20549 |

|||||||||||||||||

|

FORM 10-Q |

|||||||||||||||||

|

(Mark One) |

|||||||||||||||||

|

[x] |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

||||||||||||||||

|

For the quarterly period ended September 30, 2016 |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

OR |

|

|

|

|

|

|

|

|

|

|

[ ] |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

||||||||||||||||

|

For the transition period from to |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commission file number 001-09712 |

|||||||||||||||||

|

|

|

(Exact name of Registrant as specified in its charter) |

|||||||||||||||||

|

Delaware |

|

|

62-1147325 |

||||||||||||||

|

(State or other jurisdiction of incorporation or organization) |

|

|

(IRS Employer Identification No.) |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8410 West Bryn Mawr, Chicago, Illinois 60631 |

|||||||||||||||||

|

(Address of principal executive offices) (Zip code) |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Registrant’s telephone number, including area code: (773) 399-8900 |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|||||||||||||||

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

[x] |

[ ] |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). |

[x] |

[ ] |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. |

|||||||||||||||||

|

Large accelerated filer |

[ ] |

Accelerated filer |

[x] |

Non-accelerated filer |

[ ] |

Smaller reporting company |

[ ] |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). |

[ ] |

[x] |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date. |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Class |

|

|

Outstanding at September 30, 2016 |

||||||||||||||

|

Common Shares, $1 par value |

|

|

51,812,225 Shares |

||||||||||||||

|

Series A Common Shares, $1 par value |

|

|

33,005,877 Shares |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

United States Cellular Corporation |

||

|

|

|

|

|

Quarterly Report on Form 10-Q |

||

|

For the Quarterly Period Ended September 30, 2016 |

||

|

|

|

|

|

Index |

Page No. |

|

|

|

|

|

|

|

Management Discussion and Analysis of Financial Condition and Results of Operations |

|

|

|

||

|

|

||

|

|

||

|

|

||

|

|

||

|

|

||

|

|

||

|

|

Supplemental Information Relating to Non-GAAP Financial Measures |

|

|

|

||

|

|

||

|

|

||

|

|

Private Securities Litigation Reform Act of 1995 Safe Harbor Cautionary Statement |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

||

|

|

||

|

|

||

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

United States Cellular Corporation Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

The following discussion and analysis should be read in conjunction with United States Cellular Corporation’s (“U.S. Cellular”) interim consolidated financial statements and notes included herein, and with the description of U.S. Cellular’s business, its audited consolidated financial statements and Management's Discussion and Analysis (“MD&A”) of Financial Condition and Results of Operations included in U.S. Cellular’s Annual Report on Form 10-K (“Form 10-K”) for the year ended December 31, 2015. Analysis of U.S. Cellular’s financial results compares the three and nine months ended September 30, 2016 to the three and nine months ended September 30, 2015. Calculated amounts and percentages are based on the underlying actual numbers rather than the numbers rounded to millions as presented.

This report contains statements that are not based on historical facts, including the words “believes,” “anticipates,” “intends,” “expects” and similar words. These statements constitute and represent “forward looking statements” as this term is defined in the Private Securities Litigation Reform Act of 1995. Such forward looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results, events or developments to be significantly different from any future results, events or developments expressed or implied by such forward looking statements. See Private Securities Litigation Reform Act of 1995 Safe Harbor Cautionary Statement for additional information.

U.S. Cellular uses certain “non-GAAP financial measures” throughout the MD&A. A discussion of the reason U.S. Cellular determines these metrics to be useful and a reconciliation of these measures to their most directly comparable measures determined in accordance with accounting principles generally accepted in the United States of America (“GAAP”) are included in the Supplemental Information Relating to Non-GAAP Financial Measures section within the MD&A of this Form 10-Q Report.

U.S. Cellular owns, operates, and invests in wireless markets throughout the United States. U.S. Cellular is an 83%-owned subsidiary of Telephone and Data Systems, Inc. (“TDS”). U.S. Cellular’s strategy is to attract and retain wireless customers through a value proposition comprised of a high-quality network, outstanding customer service, and competitive devices, plans, and pricing, all provided with a local focus.

|

OPERATIONS |

|

|

|

U.S. Cellular Mission and Strategy

U.S. Cellular’s mission is to provide exceptional wireless communication services which enhance consumers’ lives, increase the competitiveness of local businesses, and improve the efficiency of government operations in the mid-sized and rural markets served.

In 2016, U.S. Cellular will continue to execute on its strategies to grow revenues by increasing its customer base, driving smartphone adoption and ongoing data usage monetization. Strategic efforts include:

- U.S. Cellular deployed 4G LTE as a result of U.S. Cellular’s strategic initiative to enhance its network. 4G LTE reaches 99% of postpaid connections and 98% of cell sites. The adoption of data-centric smartphones and connected devices is driving significant growth in data traffic. At the end of the third quarter of 2016, 77% of postpaid connections had 4G capable devices, with the LTE network handling 90% of data traffic. U.S. Cellular continues to devote efforts to enhance its network capabilities with the deployment of VoLTE technology and plans a multi-year roll out beginning with one market in early 2017. VoLTE, when deployed commercially, will enable customers to utilize the LTE network for both voice and data services, and will enable enhanced services such as high definition voice, video calling and simultaneous voice and data sessions. The deployment of VoLTE also will expand U.S. Cellular’s ability to offer roaming services to additional carriers.

- U.S. Cellular continued to enhance its spectrum position and monetize non-strategic assets by entering into multiple agreements with third parties. Certain of these agreements involve the purchase of licenses for cash, while others involve the exchange of licenses in non-operating markets for other licenses in operating markets and cash. As a result of the closing of multiple exchange agreements in the nine months ended September 30, 2016, U.S. Cellular received $15 million of cash and recognized gains of $16 million. The remaining license purchase and exchange transactions are expected to close in the fourth quarter of 2016, at which point U.S. Cellular expects to recognize additional gains. See Note 5 — Acquisitions, Divestitures and Exchanges for additional information related to these transactions.

- U.S. Cellular is focused on expanding its solutions available to business and government customers, including a growing suite of machine-to-machine solutions across various categories. U.S. Cellular will continue to enhance its advanced wireless services and connected solutions for consumer, business and government customers.

- U.S. Cellular is committed to continuous innovation so as to provide customers in the markets it serves with the latest technology that can enhance their lives or businesses. During the third quarter of 2016, U.S. Cellular successfully tested 5G technology in both indoor and outdoor environments for the first time. The company plans additional tests geared towards understanding the propagation characteristics of the new technology and contributing to the development of 5G standards. When deployed commercially, 5G technology is expected to help address customers’ growing demand for data services as well as create opportunities for new services requiring high speed and low latency.

All defined terms in this MD&A are used as defined in the Notes to Consolidated Financial Statements, and additional terms are defined below:

- 4G LTE – fourth generation Long-Term Evolution which is a wireless broadband technology.

- 5G – fifth generation wireless broadband technology.

- Account – represents an individual or business financially responsible for one or multiple associated connections. An account may include a variety of types of connections such as handsets and connected devices.

- Auction 97 – An FCC auction of AWS-3 spectrum licenses that ended in January 2015.

- Auctions 1000, 1001, and 1002 – Auction 1000 is an FCC auction of 600 MHz spectrum licenses being held in 2016 involving: (1) a “reverse auction” in which broadcast television licensees submit bids to voluntarily relinquish spectrum usage rights in exchange for payments (referred to as Auction 1001); (2) a “repacking” of the broadcast television bands in order to free up certain broadcast spectrum for other uses; and (3) a “forward auction” of licenses for spectrum cleared through this process to be used for wireless communications (referred to as Auction 1002).

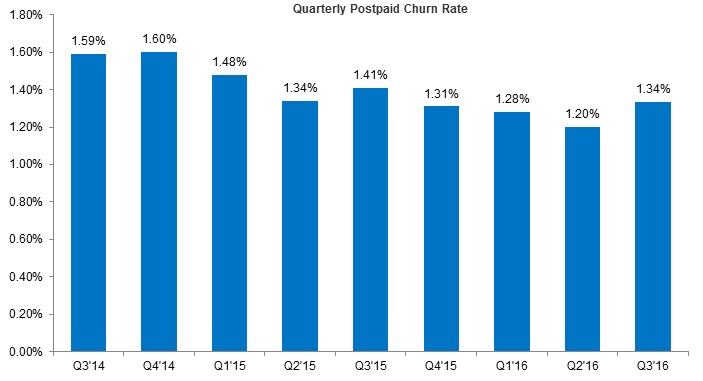

- Churn Rate – represents the percentage of the connections that disconnect service each month. These rates represent the average monthly churn rate for each respective period.

- Connections - individual lines of service associated with each device activated by a customer. This includes smartphones, feature phones, tablets, modems, and machine-to-machine devices.

- FCC – Federal Communications Commission.

- Gross Additions – represents the total number of new connections added during the period, without regard to connections that were terminated during that period.

- Machine-to-Machine or M2M – technology that involves the transmission of data between networked devices, as well as the performance of actions by devices without human intervention. U.S. Cellular sells and supports M2M solutions to customers, provides connectivity for M2M solutions via the U.S. Cellular network, and has partnerships with device manufacturers and software developers which offer M2M solutions.

- Net Additions – represents the total number of new connections added during the period, net of connections that were terminated during that period.

- Postpaid Average Billings per Account (“Postpaid ABPA”) – non-GAAP metric is calculated by dividing total postpaid service revenues plus equipment installment plan billings by the average number of postpaid accounts and by the number of months in the period.

- Postpaid Average Billings per User (“Postpaid ABPU”) – non-GAAP metric is calculated by dividing total postpaid service revenues plus equipment installment plan billings by the average number of postpaid connections and by the number of months in the period.

- Postpaid Average Revenue per Account (“Postpaid ARPA”) – metric is calculated by dividing total postpaid service revenues by the average number of postpaid accounts and by the number of months in the period.

- Postpaid Average Revenue per User (“Postpaid ARPU”) – metric is calculated by dividing total postpaid service revenues by the average number of postpaid connections and by the number of months in the period.

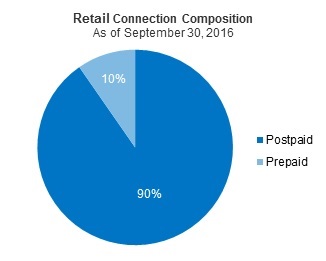

- Retail Connections – the sum of postpaid connections and prepaid connections.

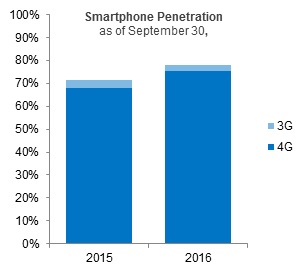

- Smartphone Penetration – is calculated by dividing postpaid smartphone connections by postpaid handset connections.

- Universal Service Fund (“USF”) – A system of telecommunications collected fees and support payments managed by the FCC intended to promote universal access to telecommunications services in the United States.

- VoLTE – Voice over Long-Term Evolution is a technology specification that defines the standards and procedures for delivering voice communications and related services over 4G LTE networks.

|

|

|

||||||

|

|

|

YTD 2015 |

YTD 2016 |

|

|||

|

|

Postpaid Connections |

|

|

|

|||

|

|

|

Gross Additions |

591,000 |

586,000 |

|

||

|

|

|

Net Additions |

43,000 |

75,000 |

|

||

|

|

|

Churn |

1.41% |

1.27% |

|

||

|

|

|

Handsets |

1.32% |

1.17% |

|

||

|

|

|

Connected Devices |

2.31% |

1.97% |

|

||

|

|

|

Connections – end of period |

4,341,000 |

4,484,000 |

|

||

|

|

Prepaid Net Additions |

32,000 |

93,000 |

|

|||

|

|

Retail Connections – end of period |

4,721,000 |

4,964,000 |

|

|||

|

The increase in postpaid net additions in 2016 is driven by improvement in postpaid churn. Postpaid churn declined over the past two years due to enhancements in the customer experience and improvement in the overall credit mix of gross additions. In addition, U.S. Cellular continues to see growth in postpaid net additions from connected devices. The increase in prepaid net additions was due primarily to successful promotional activity. |

|||||||

|

Smartphones represented 92% and 87% of total postpaid handset sales for the nine months ended September 30, 2016 and 2015, respectively. As a result, smartphone penetration increased to 78% of the postpaid handset base as of September 30, 2016, up from 72% a year ago. Smartphone customers generally use more data than feature phone customers, thereby driving growth in service revenues. Continued growth in customer usage related to data services and products may result in increased operating expenses and the need for additional investment in spectrum, network capacity and network enhancements. |

|

|

|

|

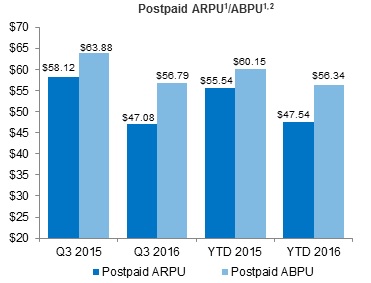

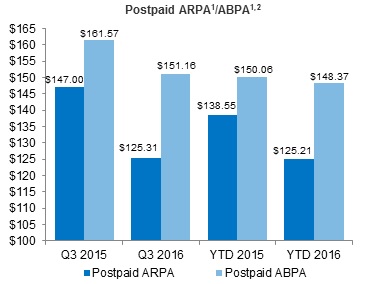

1 The discontinuation of the loyalty rewards points program had the effect of increasing Postpaid ARPU/ABPU and Postpaid ARPA/ABPA by $4.48 and $11.34 for the three months ended September 2015, respectively, and $1.50 and $3.74 for the nine months ended September 2015, respectively.

2 Postpaid ABPU and Postpaid ABPA are non-GAAP financial measures. Refer to Supplemental Information Relating to Non-GAAP Financial Measures within this MD&A for a reconciliation of this measure. |

|

Postpaid ARPU and Postpaid ARPA decreased for the three and nine months ended September 30, 2016 due primarily to the impact of the loyalty rewards points program that was discontinued in September 2015, industry-wide price competition, and discounts on shared data plans provided to customers on equipment installment plans and those providing their own device at the time of activation or renewal. Postpaid ARPU also decreased due to growth in the number of connected devices, which on a per unit basis contribute less revenue than handsets. These factors were partially offset by the impacts of continued adoption of smartphones and the related increase in service revenues from data usage.

Equipment installment plans increase equipment sales revenue as customers pay for their wireless devices in installments at a total device price that is generally higher than the device price offered to customers in conjunction with alternative plans that are subject to a service contract. Equipment installment plans also have the impact of reducing service revenues as many equipment installment plans provide for reduced monthly access charges. In order to show the trends in total service and equipment revenues received, U.S. Cellular has presented Postpaid ABPU and Postpaid ABPA, which are calculated as Postpaid ARPU and Postpaid ARPA plus average monthly equipment installment plan billings per connection and account, respectively.

Equipment installment plan billings increased for the three and nine months ended September 30, 2016 due to increased adoption of equipment installment plans by postpaid customers. Postpaid ABPU and ABPA decreased in 2016 as the increase in equipment installment plan billings was more than offset by the decline in Postpaid ARPU and ARPA discussed above. U.S. Cellular expects the adoption and penetration of equipment installment plans to continue to increase as plan offerings shift more toward equipment installment plans. Effective in September 2016, new postpaid handset sales to retail consumers are made under equipment installment plans; business and government customers may purchase equipment under either installment plans or alternative plans that are subject to a service contract.

|

|

|

|

|

Three Months Ended |

|

Nine Months Ended |

|||||||||||||

|

|

|

|

|

|

September 30, |

|

September 30, |

||||||||||||

|

|

|

|

|

|

|

|

|

|

2016 vs. |

|

|

|

|

2016 vs. |

|||||

|

|

|

|

|

|

2016 |

|

2015 |

|

2015 |

|

2016 |

|

2015 |

|

2015 |

||||

|

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Retail service |

|

$ |

|

$ |

|

(14)% |

|

$ |

|

$ |

|

(10)% |

|||||||

|

Inbound roaming |

|

|

|

|

|

(25)% |

|

|

|

|

|

(20)% |

|||||||

|

Other |

|

|

|

|

|

12% |

|

|

|

|

|

7% |

|||||||

|

|

Service revenues |

|

|

|

|

|

(14)% |

|

|

|

|

|

(10)% |

||||||

|

Equipment sales |

|

|

|

|

|

38% |

|

|

|

|

|

42% |

|||||||

|

|

Total operating revenues |

|

|

|

|

|

(6)% |

|

|

|

|

|

(2)% |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

System operations (excluding Depreciation, amortization and accretion reported below) |

|

|

|

|

|

(1)% |

|

|

|

|

|

(2)% |

|||||||

|

Cost of equipment sold |

|

|

|

|

|

(2)% |

|

|

|

|

|

2% |

|||||||

|

Selling, general and administrative |

|

|

|

|

|

(1)% |

|

|

|

|

|

(2)% |

|||||||

|

|

|

|

|

|

|

|

|

|

(2)% |

|

|

|

|

|

- |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Operating cash flow* |

|

|

|

|

|

(21)% |

|

|

|

|

|

(9)% |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Depreciation, amortization and accretion |

|

|

|

|

|

2% |

|

|

|

|

|

3% |

|||||||

|

(Gain) loss on asset disposals, net |

|

|

|

|

|

>100% |

|

|

|

|

|

33% |

|||||||

|

(Gain) loss on sale of business and other exit costs, net |

|

|

|

|

|

N/M |

|

|

|

|

|

100% |

|||||||

|

(Gain) loss on license sales and exchanges |

|

|

|

|

|

70% |

|

|

|

|

|

89% |

|||||||

|

|

Total operating expenses |

|

|

|

|

|

1% |

|

|

|

|

|

9% |

||||||

|

Operating income |

|

$ |

|

$ |

|

(88)% |

|

$ |

|

$ |

|

(92)% |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Net income |

|

$ |

|

$ |

|

(73)% |

|

$ |

|

$ |

|

(78)% |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Adjusted EBITDA* |

|

$ |

|

$ |

|

(16)% |

|

$ |

|

$ |

|

(5)% |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Capital expenditures |

|

$ |

|

$ |

|

(23)% |

|

$ |

|

$ |

|

(18)% |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* |

Represents a non-GAAP financial measure. Refer to Supplemental Information Relating to Non-GAAP Financial Measures within this MD&A for a reconciliation of this measure. |

||||||||||||||||||

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

N/M - Percentage change not meaningful |

|||||||||||||||||||

|

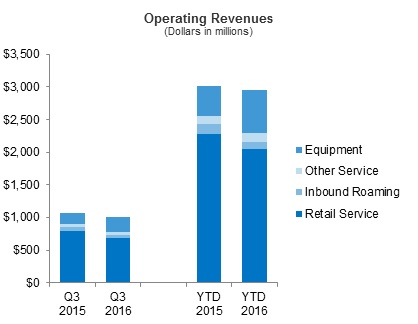

Service revenues consist of:

Equipment revenues consist of:

|

Key components of changes in the statement of operations line items were as follows:

Total operating revenues

Service revenues decreased for the three and nine months ended September 30, 2016 as a result of (i) a decrease in retail service revenues driven by the $58 million impact of the loyalty rewards program that ended in September 2015; (ii) industry-wide price competition, including discounts on shared data plans provided to customers on equipment installment plans and those providing their own device at the time of activation or renewal; and (iii) reductions in inbound roaming revenues driven by lower roaming rates. Such reductions were partially offset by an increase in the average connections base and continued adoption of smartphones and shared data plans.

Federal USF revenue was $23 million and $69 million for the three and nine months ended September 30, 2016, respectively, which remained flat when compared to the same periods last year. Pursuant to the FCC's Reform Order (“Reform Order”), U.S. Cellular’s Federal USF support was to be phased down at the rate of 20% per year beginning July 1, 2012. The Phase II Mobility Fund was not operational as of July 2014 and, therefore, as provided by the Reform Order, the phase down was suspended at 60% of the baseline amount. U.S. Cellular will continue to receive USF support at the 60% level until the FCC takes further action. At this time, U.S. Cellular cannot predict the changes that the FCC might make to the USF high cost support program and, accordingly, cannot predict whether such changes will have a material adverse effect on U.S. Cellular’s business, financial condition or results of operations.

Equipment sales revenues increased for the three months ended September 30, 2016 when compared to the three months ended September 30, 2015 due primarily to a shift in mix to sales under equipment installment plans together with an increase in average revenue per device sold under such plans. Equipment installment plan sales contributed $192 million and $89 million during the three months ended September 30, 2016 and 2015, respectively.

Equipment sales revenues increased for the nine months ended September 30, 2016 when compared to the nine months ended September 30, 2015 due to an overall increase in the number of devices sold, and a shift in mix to sales under equipment installment plans together with an increase in average revenue per device sold under such plans. Equipment installment plan sales contributed $501 million and $226 million during the nine months ended September 30, 2016 and 2015, respectively. Equipment installment plan connections represented 40% and 23% of total postpaid connections as of September 30, 2016 and 2015, respectively.

System operations expenses decreased by modest amounts for the three and nine months ended September 30, 2016 when compared to the same periods last year.

U.S. Cellular expects system operations expenses to increase in the future to support the continued growth in cell sites and other network facilities as it continues to add capacity, enhance quality and deploy new technologies as well as to support increases in total customer data usage. However, these increases are expected to be offset to some extent by cost savings generated by shifting data traffic to the 4G LTE network from the 3G network.

Cost of equipment sold

Cost of equipment sold decreased for the three months ended September 30, 2016 when compared to the three months ended September 30, 2015 as a result of a decrease in the average cost per device sold driven by the lower cost of smartphones and to a lesser extent the lower sales of accessories. Cost of equipment sold included $200 million and $113 million related to equipment installment plan sales for the three months ended September 30, 2016 and 2015, respectively. Loss on equipment, defined as Equipment sales revenues less Cost of equipment sold, was $41 million and $114 million for the three months ended September 30, 2016 and 2015.

Cost of equipment sold increased for the nine months ended September 30, 2016 when compared to the nine months ended September 30, 2015 primarily as the result of a 4% increase in devices sold, partially offset by a decrease in the average cost per device sold. Cost of equipment sold included $534 million and $305 million related to equipment installment plan sales for the nine months ended September 30, 2016 and 2015, respectively. Loss on equipment was $144 million and $318 million for the nine months ended September 30, 2016 and 2015, respectively.

Selling, general and administrative expenses

Selling, general and administrative expenses decreased by modest amounts for the three and nine months ended September 30, 2016 when compared to the same periods last year. This decrease was attributable to various expense reductions that were partially offset by a $13 million expense recognized in the three months ended September 30, 2016 as a result of the termination of a naming rights agreement.

Depreciation, amortization, and accretion expenses

The increases in Depreciation, amortization, and accretion expenses for the three and nine months ended September 30, 2016 were mainly driven by the increase in amortization expense related to billing system upgrades.

(Gain) loss on asset disposals, net

The increases in Loss on asset disposals were primarily driven by more disposals of certain network assets during the three and nine months ended September 30, 2016 when compared to the same periods last year.

(Gain) loss on sale of business and other exit costs, net

The net gain for the nine months ended September 30, 2015 was due primarily to a $108 million gain recognized on sale of towers and certain related contracts, assets and liabilities.

(Gain) loss on license sales and exchanges, net

The net gains in 2016 and 2015 were due to gains recognized on license exchange transactions with third parties. See Note 5 — Acquisitions, Divestitures and Exchanges in the Notes to Consolidated Financial Statements for additional information.

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

Three Months Ended |

Nine Months Ended |

|||||||||||||

|

|

|

|

|

|

September 30, |

|

September 30, |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

2016 vs. |

|

|

|

|

|

|

|

2016 vs. |

|

|

|

|

|

|

2016 |

|

2015 |

|

2015 |

|

2016 |

|

2015 |

|

2015 |

||||

|

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Operating income |

|

$ |

|

$ |

|

(88)% |

$ |

|

$ |

|

(92)% |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Equity in earnings of unconsolidated entities |

|

|

|

|

|

(5)% |

|

|

|

|

- |

||||||||

|

Interest and dividend income |

|

|

|

|

|

51% |

|

|

|

|

59% |

||||||||

|

Interest expense |

|

|

|

|

|

(32)% |

|

|

|

|

(37)% |

||||||||

|

Other, net |

|

|

|

|

|

20% |

|

|

|

|

26% |

||||||||

|

Total investment and other income |

|

|

|

|

|

(14)% |

|

|

|

|

(10)% |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Income before income taxes |

|

|

|

|

|

(69)% |

|

|

|

|

(77)% |

||||||||

|

Income tax expense |

|

|

|

|

|

(63)% |

|

|

|

|

(76)% |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Net income |

|

|

|

|

|

(73)% |

|

|

|

|

(78)% |

||||||||

|

Less: Net income attributable to noncontrolling interests, net of tax |

|

|

|

|

|

(53)% |

|

|

|

|

(84)% |

||||||||

|

Net income attributable to U.S. Cellular shareholders |

|

$ |

|

$ |

|

(73)% |

$ |

|

$ |

|

(78)% |

||||||||

Equity in earnings of unconsolidated entities

Equity in earnings of unconsolidated entities represents U.S. Cellular’s share of net income from entities in which it has a noncontrolling interest and that are accounted for by the equity method. U.S. Cellular’s investment in the Los Angeles SMSA Limited Partnership (“LA Partnership”) contributed $17 million and $19 million to Equity in earnings of unconsolidated entities for the three months ended September 30, 2016 and 2015, respectively, and $57 million and $58 million for the nine months ended September 30, 2016 and 2015, respectively.

See Note 7 — Investments in Unconsolidated Entities in the Notes to Consolidated Financial Statements for additional information.

Interest and dividend income

Interest and dividend income increased due to imputed interest income recognized on equipment installment plans of $13 million and $9 million during the three months ended September 30, 2016 and 2015, respectively, and $37 million and $24 million during the nine months ended September 30, 2016 and 2015, respectively.

See Note 3 — Equipment Installment Plans in the Notes to Consolidated Financial Statements for additional information.

Interest expense

The increase in Interest expense for the three and nine months ended September 30, 2016 is primarily driven by U.S. Cellular’s issuance of $300 million of 7.25% Senior Notes due 2064 in November 2015 and borrowing of $225 million on its senior term loan facility that was drawn in July 2015.

Income tax expense

U.S. Cellular’s effective tax rate on Income before income taxes for the three and nine months ended September 30, 2016 was 46.0% and 41.4%, respectively, and for the three and nine months ended September 30, 2015 was 38.5% and 39.2%, respectively. The effective tax rates for the three and nine month periods primarily reflect a normalized combined rate of federal and state taxes, but are also affected by certain discrete items in each period which increase or decrease the effective tax rate for each period. Because certain discrete items are not annualized, these rates may not be indicative of the annual rate for 2016.

Net income attributable to noncontrolling interests, net of tax

The decrease for the three and nine months ended September 30, 2016 is due primarily to lower income from certain partnerships in 2016.

Liquidity and Capital Resources

Sources of Liquidity

U.S. Cellular operates a capital-intensive business. Historically, U.S. Cellular has used internally-generated funds and also has obtained substantial funds from external sources for general corporate purposes. In the past, U.S. Cellular’s existing cash and investment balances, funds available under its revolving credit facility, funds from other financing sources, including a term loan and other long-term debt, and cash flows from operating, investing and financing activities, including sales of assets or businesses, provided sufficient liquidity and financial flexibility for U.S. Cellular to meet its normal day-to-day operating needs and debt service requirements, to finance the build-out and enhancement of markets and to fund acquisitions, primarily of spectrum licenses. There is no assurance that this will be the case in the future.

U.S. Cellular believes that existing cash and investment balances, funds available under its revolving credit facility, and expected cash flows from operating and investing activities provide liquidity for U.S. Cellular to meet its normal day-to-day operating needs and debt service requirements for the coming year. Although U.S. Cellular currently has a significant cash balance, in certain recent periods, U.S. Cellular has incurred negative free cash flow (defined as Cash flows from operating activities less Cash paid for additions to property, plant and equipment) and this will continue in the future if operating results do not improve or capital expenditures are not reduced. U.S. Cellular currently expects to have negative free cash flow in 2016 due to anticipated growth in equipment installment plan receivables combined with significant capital expenditures.

U.S. Cellular may require substantial additional capital for, among other uses, funding day-to-day operating needs, working capital, acquisitions of providers of wireless telecommunications services, spectrum license or system acquisitions, system development and network capacity expansion, debt service requirements, the repurchase of shares, the payment of dividends, or making additional investments. It may be necessary from time-to-time to increase the size of the existing revolving credit facility, to put in place a new credit facility, or to obtain other forms of financing in order to fund potential expenditures. U.S. Cellular’s liquidity would be adversely affected if, among other things, U.S. Cellular is unable to obtain short or long-term financing on acceptable terms, U.S. Cellular makes significant spectrum license purchases in FCC auctions or from other parties, the LA Partnership discontinues or reduces distributions compared to historical levels, or Federal USF and/or other regulatory support payments continue to decline. In addition, although sales of assets or businesses by U.S. Cellular have been an important source of liquidity in recent periods, U.S. Cellular does not expect a similar level of such sales in the future, which will reduce a source of liquidity. In recent years, U.S. Cellular’s credit rating has declined to sub-investment grade.

There can be no assurance that sufficient funds will continue to be available to U.S. Cellular or its subsidiaries on terms or at prices acceptable to U.S. Cellular. Insufficient cash flows from operating activities, further changes in its credit ratings, defaults of the terms of debt or credit agreements, uncertainty of access to capital, deterioration in the capital markets, reduced regulatory capital at banks which in turn limits their ability to borrow and lend, other changes in the performance of U.S. Cellular or in market conditions or other factors could limit or restrict the availability of financing on terms and prices acceptable to U.S. Cellular, which could require U.S. Cellular to reduce its acquisition, capital expenditure and business development programs, reduce the acquisition of spectrum licenses, and/or reduce or cease share repurchases and/or the payment of dividends. U.S. Cellular cannot provide assurance that circumstances that could have a material adverse effect on its liquidity or capital resources will not occur. Any of the foregoing would have an adverse impact on U.S. Cellular’s businesses, financial condition or results of operations.

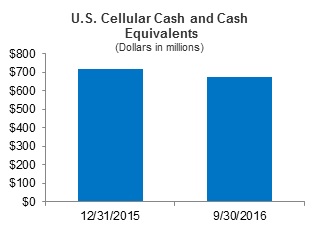

Cash and Cash Equivalents

Cash and cash equivalents include cash and money market investments. The primary objective of U.S. Cellular’s Cash and cash equivalents is for use in its operations and acquisition, capital expenditure and business development programs.

|

|

At September 30, 2016, U.S. Cellular’s cash and cash equivalents totaled $674 million compared to $715 million at December 31, 2015. The majority of U.S. Cellular’s Cash and cash equivalents was held in bank deposit accounts and in money market funds that invest exclusively in U.S. Treasury Notes or in repurchase agreements fully collateralized by such obligations. U.S. Cellular monitors the financial viability of the money market funds and direct investments in which it invests and believes that the credit risk associated with these investments is low. |

U.S. Cellular has a revolving credit facility available for general corporate purposes. In June 2016, U.S. Cellular entered into a new $300 million revolving credit agreement with certain lenders and other parties. As a result of the new agreement, U.S. Cellular’s revolving credit agreement due to expire in December 2017 was terminated. Amounts under the new revolving credit facility may be borrowed, repaid and reborrowed from time-to-time until maturity in June 2021. Certain U.S. Cellular wholly-owned subsidiaries have jointly and severally unconditionally guaranteed the payment and performance of the obligations of U.S. Cellular under the revolving credit agreement. As of September 30, 2016, there were no outstanding borrowings under the revolving credit facility, except for letters of credit, and U.S. Cellular’s unused capacity under its revolving credit facility was $284 million. The continued availability of the new revolving credit facility requires U.S. Cellular to comply with certain negative and affirmative covenants, maintain certain financial ratios and provide representations on certain matters at the time of each borrowing. See Note 8 — Debt in the Notes to Consolidated Financial Statements for additional information.

In June 2016, U.S. Cellular also amended and restated its senior term loan credit facility. Certain modifications were made to the financial covenants and subsidiary guarantees were added in order to align with the new revolving credit agreement. There were no significant changes to the maturity date or other key terms of the agreement.

U.S. Cellular believes it was in compliance with all of the financial covenants and requirements set forth in its revolving credit facility and the senior term loan credit facility as of September 30, 2016.

U.S. Cellular has in place an effective shelf registration statement on Form S-3 to issue senior or subordinated debt securities.

The proceeds from any of the aforementioned financing facilities are available for general corporate purposes, including spectrum purchases and capital expenditures.

The long-term debt payments due for the remainder of 2016 and the next four years represent less than 3% of U.S. Cellular’s total long-term debt obligation measured as of September 30, 2016.

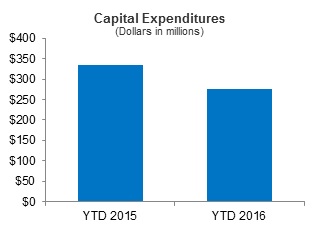

Capital Expenditures

Capital expenditures (i.e., additions to property, plant and equipment and system development expenditures), which include accruals and capitalized interest, in 2016 and 2015 were as follows:

|

|

U.S. Cellular’s capital expenditures for 2016 are expected to be approximately $500 million. These expenditures are expected to be for the following general purposes:

|

U.S. Cellular plans to finance its capital expenditures program for 2016 using primarily Cash flows from operating activities and, as necessary, existing cash balances and borrowings under its revolving credit agreement and/or other long-term debt.

Acquisitions, Divestitures and Exchanges

U.S. Cellular may be engaged from time-to-time in negotiations relating to the acquisition, divestiture or exchange of companies, properties or wireless spectrum. In general, U.S. Cellular may not disclose such transactions until there is a definitive agreement. U.S. Cellular assesses its existing wireless interests on an ongoing basis with a goal of improving the competitiveness of its operations and maximizing its long-term return on capital. As part of this strategy, U.S. Cellular reviews attractive opportunities to acquire additional wireless operating markets and wireless spectrum, including pursuant to FCC auctions. U.S. Cellular also may seek to divest outright or include in exchanges for other wireless interests those interests that are not strategic to its long-term success.

On July 15, 2016, the FCC announced U.S. Cellular as a qualified bidder in the FCC’s forward auction of 600 MHz spectrum licenses, referred to as Auction 1002, which then commenced on August 16, 2016. In recent FCC auctions, U.S. Cellular has not been a bidder, but has participated as a limited partner in “designated entities” that qualified for a 25% bidding credit on licenses won in the auction. U.S. Cellular will not participate through a designated entity in Auction 1002. See “Regulatory Matters — FCC Auction 1002.” Prior to becoming a qualified bidder, U.S. Cellular was required to make an upfront payment, the size of which established its initial bidding eligibility. Accordingly, in the second quarter of 2016, U.S. Cellular made an upfront payment to the FCC of $143 million. If U.S. Cellular becomes a winning bidder in the auction, it could be required to make additional payments to the FCC that could be substantial. In such event, U.S. Cellular could finance such payments from its existing cash balances, borrowings under its revolving credit agreement and/or additional long-term debt. Further, if U.S. Cellular is not the winning bidder for any licenses, or is the winning bidder for licenses with an aggregate bid price that is less than the upfront payment, all or a portion of the upfront payment will be refunded to U.S. Cellular.

In 2015 and 2016, U.S. Cellular entered into multiple spectrum license purchase agreements. The aggregate purchase price for these spectrum licenses is $56 million, of which $46 million closed in the nine months ended September 30, 2016. In 2016, U.S. Cellular also entered into multiple agreements with third parties to transfer FCC licenses in non-operating markets and receive FCC licenses in operating markets. The agreements provide for the transfer of certain AWS and PCS spectrum licenses and approximately $29 million, net, in cash to U.S. Cellular, in exchange for U.S. Cellular transferring certain AWS, PCS and 700 MHz spectrum licenses to the third parties. Through September 30, 2016, certain of the exchange transactions have closed and U.S. Cellular has received $15 million of cash in conjunction with such closed transactions. The remaining license purchase and exchange transactions are expected to close in the fourth quarter of 2016. See Note 5 — Acquisitions, Divestitures and Exchanges in the Notes to Consolidated Financial Statements for additional information related to these transactions.

Variable Interest Entities

U.S. Cellular consolidates certain entities as “variable interest entities” under GAAP. See Note 9 — Variable Interest Entities in the Notes to Consolidated Financial Statements for additional information related to these variable interest entities. U.S. Cellular may elect to make capital contributions and/or advances to variable interest entities in order to fund their operations.

Common Share Repurchase Program

U.S. Cellular has repurchased and expects to continue to repurchase its Common Shares, subject to its repurchase program. Share repurchases made under this program in 2016 and 2015 were as follows:

|

|

Nine Months Ended |

|||||

|

|

|

September 30, |

||||

|

|

|

2016 |

|

2015 |

||

|

Number of shares |

|

|

||||

|

Average cost per share |

$ |

|

$ |

|||

|

Dollar Amount (in millions) |

$ |

|

$ |

|||

For additional information related to the current repurchase authorization, see Unregistered Sales of Equity Securities and Use of Proceeds.

Contractual and Other Obligations

There were no material changes outside the ordinary course of business between December 31, 2015 and September 30, 2016 to the Contractual and Other Obligations disclosed in Management’s Discussion and Analysis of Financial Condition and Results of Operations included in U.S. Cellular’s Form 10-K for the year ended December 31, 2015.

Off-Balance Sheet Arrangements

U.S. Cellular had no transactions, agreements or other contractual arrangements with unconsolidated entities involving “off-balance sheet arrangements,” as defined by SEC rules, that had or are reasonably likely to have a material current or future effect on its financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

Consolidated Cash Flow Analysis

U.S. Cellular operates a capital- and marketing-intensive business. U.S. Cellular makes substantial investments to acquire wireless licenses and properties and to construct and upgrade wireless telecommunications networks and facilities as a basis for creating long-term value for shareholders. In recent years, rapid changes in technology and new opportunities have required substantial investments in potentially revenue‑enhancing and cost-reducing upgrades to U.S. Cellular’s networks. U.S. Cellular utilizes cash on hand, cash from operating activities, cash proceeds from divestitures and dispositions of investments, short-term credit facilities and long-term debt financing to fund its acquisitions (including licenses), construction costs, operating expenses and share repurchases. Cash flows may fluctuate from quarter-to-quarter and year-to-year due to seasonality, the timing of acquisitions and divestitures, capital expenditures and other factors. The following discussion summarizes U.S. Cellular's cash flow activities for the nine months ended September 30, 2016 and 2015.

2016 Commentary

U.S. Cellular’s Cash and cash equivalents decreased $41 million in 2016. Net cash provided by operating activities was $415 million in 2016 due primarily to net income of $54 million plus non-cash items of $450 million and distributions received from unconsolidated entities of $55 million, including a $10 million distribution from the LA Partnership. This was partially offset by changes in working capital items which decreased cash by $144 million. The decrease in working capital items was due primarily to a $160 million increase in equipment installment plan receivables, which are expected to continue to increase and further require the use of working capital in the near term. This was partially offset by a federal tax refund of $28 million related to an overpayment of the 2015 tax liability, which resulted from the enactment of federal bonus depreciation in December 2015.

The net cash provided by operating activities was offset by Cash flows used for investing activities of $449 million. Cash paid for additions to property, plant and equipment totaled $280 million. In June 2016, U.S. Cellular made a deposit of $143 million to the FCC for its participation in Auction 1002. Cash paid for acquisitions and licenses in 2016 was $46 million partially offset by Cash received from divestitures and exchanges of $20 million. See Note 5 — Acquisitions, Divestitures and Exchanges in the Notes to Consolidated Financial Statements for additional information related to these transactions.

Cash flows used for financing activities were $7 million, reflecting ordinary activity such as scheduled repayments of debt.

2015 Commentary

U.S. Cellular’s Cash and cash equivalents increased $385 million in 2015. Net cash provided by operating activities was $555 million in 2015 due to net income of $250 million plus non-cash items of $168 million, distributions received of $45 million and positive changes in working capital items of $92 million. The LA Partnership did not make a distribution in 2015.

Cash flows used for investing activities were $377 million in 2015. Cash paid for additions to property, plant and equipment totaled $407 million in 2015. During 2015, a $278 million payment was made by Advantage Spectrum L.P. (see Note 9 — Variable Interest Entities in the Notes to Consolidated Financial Statements) to the FCC for licenses for which it was the provisional winning bidder in Auction 97. Cash received from divestitures and exchanges in 2015 included $145 million related to licenses and $142 million related to the sale of 359 towers and certain related contracts, assets and liabilities.

Cash flows from financing activities were $207 million due primarily to U.S. Cellular borrowing $225 million on its senior term loan credit facility in July 2015.

Other Information

In October 2016, U.S. Cellular was informed by the general partner of the LA Partnership that U.S. Cellular will receive a distribution of $19 million in November 2016.

Consolidated Balance Sheet Analysis

The following discussion addresses certain captions in the consolidated balance sheet and changes therein. This discussion is intended to highlight the significant changes and is not intended to fully reconcile the changes. Changes in financial condition during 2016 are as follows:

Other current assets

Other current assets decreased $30 million due primarily to the receipt of a federal income tax refund of $28 million in March 2016.

Assets held for sale

Assets held for sale increased $16 million due to reclassification of Licenses to this account as a result of exchanges with third parties. The license exchange agreements are expected to close in the fourth quarter of 2016. See Note 5 — Acquisitions, Divestitures and Exchanges in the Notes to Consolidated Financial Statements for additional information.

Other assets and deferred charges

Other assets and deferred charges increased $195 million due primarily to an upfront payment of $143 million to the FCC to establish U.S. Cellular’s initial bidding eligibility for its participation in Auction 1002 and a $75 million increase in the long-term portion of unbilled equipment installment plan receivables, net, due to the offering of longer term equipment installment plan contracts and the increased adoption of such contracts. See Note 3 — Equipment Installment Plans and Note 5 — Acquisitions, Divestitures and Exchanges in the Notes to Consolidated Financial Statements for additional information related to these balances.

Other current liabilities

Other current liabilities decreased $27 million due primarily to a decline in the amounts due to agents driven by lower sales volume and mix shift to lower cost devices.

Supplemental Information Relating to Non-GAAP Financial Measures

U.S. Cellular sometimes uses information derived from consolidated financial information but not presented in its financial statements prepared in accordance with U.S. GAAP to evaluate the performance of its business. Certain of these measures are considered “non-GAAP financial measures” under U.S. Securities and Exchange Commission Rules. Specifically, U.S. Cellular has referred to the following measures in this Form 10-Q Report:

- EBITDA

- Adjusted EBITDA

- Operating cash flow

- Free cash flow

- Adjusted free cash flow

- Postpaid ABPU

- Postpaid ABPA

Following are explanations of each of these measures.

Adjusted EBITDA and Operating Cash Flow

Adjusted EBITDA (earnings before interest, taxes, depreciation, amortization and accretion) is defined as net income adjusted for the items set forth in the reconciliation below. Operating cash flow is defined as net income adjusted for the items set forth in the reconciliation below. Adjusted EBITDA and Operating cash flow are not measures of financial performance under GAAP and should not be considered as alternatives to Net income or Cash flows from operating activities, as indicators of cash flows or as measures of liquidity. U.S. Cellular does not intend to imply that any such items set forth in the reconciliation below are non-recurring, infrequent or unusual; such items may occur in the future.

Management uses Adjusted EBITDA and Operating cash flow as measurements of profitability, and therefore reconciliations to Net income are deemed appropriate. Management believes Adjusted EBITDA and Operating cash flow are useful measures of U.S. Cellular’s operating results before significant recurring non-cash charges, gains and losses, and other items as presented below as they provide additional relevant and useful information to investors and other users of U.S. Cellular’s financial data in evaluating the effectiveness of its operations and underlying business trends in a manner that is consistent with management’s evaluation of business performance. Adjusted EBITDA shows adjusted earnings before interest, taxes, depreciation, amortization and accretion, and gains and losses, while Operating cash flow reduces this measure further to exclude Equity in earnings of unconsolidated entities and Interest and dividend income in order to more effectively show the performance of operating activities excluding investment activities. The following table reconciles Adjusted EBITDA and Operating cash flow to the corresponding GAAP measure, Net income.

|

|

|

Three Months Ended |

|

Nine Months Ended |

|||||||||

|

|

|

|

September 30, |

|

September 30, |

||||||||

|

|

2016 |

|

2015 |

|

2016 |

|

2015 |

||||||

|

(Dollars in millions) |

|

|

|

|

|

|

|

|

|

|

|

||

|

Net income (GAAP) |

$ |

|

$ |

|

$ |

|

$ |

||||||

|

Add back: |

|

|

|

|

|

|

|

||||||

|

|

Income tax expense |

|

|

|

|

|

|

|

|||||

|

|

Interest expense |

|

|

|

|

|

|

|

|||||

|

|

Depreciation, amortization and accretion |

|

|

|

|

|

|

|

|||||

|

EBITDA (Non-GAAP) |

|

|

|

|

|

|

|

||||||

|

Add back or deduct: |

|

|

|

|

|

|

|

||||||

|

|

(Gain) loss on sale of business and other exit costs, net |

|

|

|

|

|

|

|

|||||

|

|

(Gain) loss on license sales and exchanges, net |

|

|

|

|

|

|

|

|||||

|

|

(Gain) loss on asset disposals, net |

|

|

|

|

|

|

|

|||||

|

Adjusted EBITDA (Non-GAAP) |

|

|

|

|

|

|

|

||||||

|

Deduct: |

|

|

|

|

|

|

|

||||||

|

|

Equity in earnings of unconsolidated entities |

|

|

|

|

|

|

|

|||||

|

|

Interest and dividend income |

|

|

|

|

|

|

|

|||||

|

|

Other, net |

|

|

|

|

|

|

|

|||||

|

Operating cash flow (Non-GAAP) |

|

|

|

|

|

|

|

||||||

|

Deduct: |

|

|

|

|

|

|

|

||||||

|

|

Depreciation, amortization and accretion |

|

|

|

|

|

|

|

|||||

|

|

(Gain) loss on sale of business and other exit costs, net |

|

|

|

|

|

|

|

|||||

|

|

(Gain) loss on license sales and exchanges, net |

|

|

|

|

|

|

|

|||||

|

|

(Gain) loss on asset disposals, net |

|

|

|

|

|

|

|

|||||

|

Operating income (GAAP) |

$ |

|

$ |

|

$ |

|

$ |

||||||

Free Cash Flow and Adjusted Free Cash Flow

The following table presents Free cash flow and Adjusted free cash flow. Management uses Free cash flow as a liquidity measure and it is defined as Cash flows from operating activities less Cash paid for additions to property, plant and equipment. Adjusted free cash flow is defined as Cash flows from operating activities (which includes cash outflows related to the Sprint decommissioning), as adjusted for cash proceeds from the Sprint Cost Reimbursement (which are included in Cash flows from investing activities in the Consolidated Statement of Cash Flows), less Cash paid for additions to property, plant and equipment. Free cash flow and Adjusted free cash flow are non-GAAP financial measures which U.S. Cellular believes may be useful to investors and other users of its financial information in evaluating liquidity, specifically, the amount of cash generated by business operations (including cash proceeds from the Sprint Cost Reimbursement), after Cash paid for additions to property, plant and equipment.

|

|

Nine Months Ended September 30, |

|||||

|

|

|

2016 |

|

2015 |

||

|

(Dollars in millions) |

|

|

|

|

|

|

|

Cash flows from operating activities (GAAP) |

$ |

|

$ |

|||

|

Less: Cash paid for additions to property, plant and equipment |

|

|

|

|||

|

|

Free cash flow (Non-GAAP) |

$ |

|

$ |

||

|

Add: Sprint Cost Reimbursement1 |

|

|

|

|||

|

|

Adjusted free cash flow (Non-GAAP) |

$ |

|

$ |

||

|

|

|

|

|

|

|

|

|

1 |

On May 16, 2013, pursuant to a Purchase and Sale Agreement, U.S. Cellular sold customers and certain PCS spectrum licenses to subsidiaries of Sprint Corp. fka Sprint Nextel Corporation (“Sprint”) in U.S. Cellular’s Chicago, central Illinois, St. Louis and certain Indiana/Michigan/Ohio markets in consideration for $480 million in cash. The Purchase and Sale Agreement also contemplated certain other agreements. These agreements require Sprint to reimburse U.S. Cellular up to $200 million (the “Sprint Cost Reimbursement”) for certain network decommissioning costs, network site lease rent and termination costs, network access termination costs, and employee termination benefits for specified engineering employees. |

|||||

Postpaid ABPU and Postpaid ABPA

U.S. Cellular presents Postpaid ABPU and Postpaid ABPA to reflect the revenue shift from Service revenues to Equipment sales resulting from the increased adoption of equipment installment plans. Postpaid ABPU and Postpaid ABPA, as previously defined, are non-GAAP financial measures which U.S. Cellular believes are useful to investors and other users of its financial information in showing trends in both service and equipment sales revenues received from customers.

|

|

|

Three Months Ended September 30, |

|

Nine Months Ended September 30, |

|||||||||

|

|

2016 |

|

2015 |

|

2016 |

|

2015 |

||||||

|

(Dollars and connection counts in millions) |

|

|

|

|

|

|

|

|

|

|

|

||

|

Calculation of Postpaid ARPU |

|

|

|

|

|

|

|

||||||

|

Postpaid service revenues |

$ |

|

$ |

|

$ |

|

$ |

||||||

|

Average number of postpaid connections |

|

|

|

|

|

|

|

||||||

|

Number of months in period |

|

|

|

|

|

|

|

||||||

|

|

Postpaid ARPU (GAAP metric) |

$ |

|

$ |

|

$ |

|

$ |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calculation of Postpaid ABPU |

|

|

|

|

|

|

|

||||||

|

Postpaid service revenues |

$ |

|

$ |

|

$ |

|

$ |

||||||

|

Equipment installment plan billings |

|

|

|

|

|

|

|

||||||

|

|

Total billings to postpaid connections |

$ |

|

$ |

|

$ |

|

$ |

|||||

|

Average number of postpaid connections |

|

|

|

|

|

|

|

||||||

|

Number of months in period |

|

|

|

|

|

|

|

||||||

|

|

Postpaid ABPU (Non-GAAP metric) |

$ |

|

$ |

|

$ |

|

$ |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calculation of Postpaid ARPA |

|

|

|

|

|

|

|

||||||

|

Postpaid service revenues |

$ |

|

$ |

|

$ |

|

$ |

||||||

|

Average number of postpaid accounts |

|

|

|

|

|

|

|

||||||

|

Number of months in period |

|

|

|

|

|

|

|

||||||

|

|

Postpaid ARPA (GAAP metric) |

$ |

|

$ |

|

$ |

|

$ |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calculation of Postpaid ABPA |

|

|

|

|

|

|

|

||||||

|

Postpaid service revenues |

$ |

|

$ |

|

$ |

|

$ |

||||||

|

Equipment installment plan billings |

|

|

|

|

|

|

|

||||||

|

|

Total billings to postpaid accounts |

$ |

|

$ |

|

$ |

|

$ |

|||||

|

Average number of postpaid accounts |

|

|

|

|

|

|

|

||||||

|

Number of months in period |

|

|

|

|

|

|

|

||||||

|

|

Postpaid ABPA (Non-GAAP metric) |

$ |

|

$ |

|

$ |

|

$ |

|||||

Application of Critical Accounting Policies and Estimates

U.S. Cellular prepares its consolidated financial statements in accordance with GAAP. U.S. Cellular’s significant accounting policies are discussed in detail in Note 1 — Summary of Significant Accounting Policies and Recent Accounting Pronouncements in the Notes to Consolidated Financial Statements and U.S. Cellular’s Application of Critical Accounting Policies and Estimates is discussed in detail in Management’s Discussion and Analysis of Financial Condition and Results of Operations, both of which are included in U.S. Cellular’s Form 10-K for the year ended December 31, 2015. There were no material changes to U.S. Cellular’s application of critical accounting policies and estimates during the nine months ended September 30, 2016.

Recent Accounting Pronouncements

See Note 1 — Basis of Presentation in the Notes to Consolidated Financial Statements for information on recent accounting pronouncements.

The discussion below includes updates related to recent regulatory developments. These updates should be read in conjunction with the disclosures previously provided under “Regulatory Matters” in U.S. Cellular’s Form 10-K for the year ended December 31, 2015.

FCC Auction 1002

On July 15, 2016, the FCC announced U.S. Cellular as a qualified bidder in the FCC’s forward auction of 600 MHz spectrum licenses, referred to as Auction 1002. The first stage of forward auction bidding began on August 16, 2016 and ended on August 30, 2016 when the forward auction failed to reach the reserve price established by the FCC based on the first stage reverse auction. The second stage of the reverse auction began on September 13, 2016 and was followed by a second stage forward auction which began and ended on October 19, 2016. As necessary, the FCC will run additional reverse and forward auctions that will result in progressively lower prices in each reverse auction and less available spectrum for wireless carriers in each forward auction, until the prices in the reverse and forward auctions clear. Following a final and successful stage of the forward auction, the FCC will conduct an Assignment Phase Auction to assign specific frequencies to winners of licenses. It is expected that this process will continue into 2017. As a result of its application to participate in Auction 1002, since February 10, 2016, U.S. Cellular has been subject to FCC anti-collusion rules that place certain restrictions on public disclosures and business communications with other companies relating to U.S. Cellular’s participation. These restrictions will continue until the down payment deadline for Auction 1002, which will be ten business days after release of the FCC’s Channel Reassignment Public Notice, following the end of the auction. These anti-collusion rules, which could last a year or more from February 10, 2016, may restrict the conduct of certain U.S. Cellular activities with other auction applicants as well as with nationwide providers of wireless services which are not applicants. The restrictions could have an adverse effect on U.S. Cellular’s business, financial condition or results of operations.

FCC Net Neutrality Order

U.S. Cellular previously disclosed that the FCC adopted rules relating to net neutrality which reclassified broadband internet access service under Title II, and that lawsuits had been filed challenging such rules and reclassification. In June 2016, the U.S. Court of Appeals for the District of Columbia Circuit upheld the FCC’s rules and reclassification. A request for a rehearing of this decision was filed in July 2016, and it is expected that this court decision also will be appealed and subject to further proceedings. U.S. Cellular cannot predict the outcome of any further proceedings or the impact on its business.

Private Securities Litigation Reform Act of 1995

Safe Harbor Cautionary Statement

This Form 10-Q, including exhibits, contains statements that are not based on historical facts and represent forward-looking statements, as this term is defined in the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical facts, that address activities, events or developments that U.S. Cellular intends, expects, projects, believes, estimates, plans or anticipates will or may occur in the future are forward-looking statements. The words “believes,” “anticipates,” “estimates,” “expects,” “plans,” “intends,” “projects” and similar expressions are intended to identify these forward-looking statements, but are not the exclusive means of identifying them. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results, events or developments to be significantly different from any future results, events or developments expressed or implied by such forward-looking statements. Such risks, uncertainties and other factors include those set forth below, as more fully described under “Risk Factors” in U.S. Cellular’s Form 10-K for the year ended December 31, 2015. However, such factors are not necessarily all of the important factors that could cause actual results, performance or achievements to differ materially from those expressed in, or implied by, the forward-looking statements contained in this document. Other unknown or unpredictable factors also could have material adverse effects on future results, performance or achievements. U.S. Cellular undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise. You should carefully consider the Risk Factors in U.S. Cellular’s Form 10-K for the year ended December 31, 2015, the following factors and other information contained in, or incorporated by reference into, this Form 10-Q to understand the material risks relating to U.S. Cellular’s business.

- Intense competition in the markets in which U.S. Cellular operates could adversely affect U.S. Cellular’s revenues or increase its costs to compete.

- A failure by U.S. Cellular to successfully execute its business strategy (including planned acquisitions, spectrum acquisitions, divestitures and exchanges) or allocate resources or capital could have an adverse effect on U.S. Cellular’s business, financial condition or results of operations.