UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One) | |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended | |

OR | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number

United States Lime & Minerals, Inc.

(Exact name of Registrant as specified in its charter)

|

|

|

|

Registrant’s telephone number, including area code: (

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | |||

Non-accelerated filer | ☐ | Smaller reporting company | ||

Emerging growth company | ||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of Common Stock held by non-affiliates computed as of the last business day of the Registrant’s quarter ended June 30, 2023: $

Number of shares of Common Stock outstanding as of February 27, 2024:

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference from the Registrant’s definitive Proxy Statement to be filed for its 2024 Annual Meeting of Shareholders. Part IV incorporates certain exhibits by reference from the Registrant’s previous filings.

TABLE OF CONTENTS

ii

PART I

ITEM 1. BUSINESS.

General.

United States Lime & Minerals, Inc. (the “Company,” the “Registrant,” “We” or “Our”), which was incorporated in 1950, conducts its business primarily through its Lime and Limestone Operations segment. The Company’s Other operations relate to its natural gas interests.

The Company’s principal corporate office is located at 5429 LBJ Freeway, Suite 230, Dallas, Texas 75240. The Company’s telephone number is (972) 991-8400 and its internet address is www.uslm.com. The Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as well as the Company’s definitive proxy statement filed pursuant to Section 14(a) of the Exchange Act, are available free of charge on the Company’s website as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities and Exchange Commission (the “SEC”).

Lime and Limestone Operations.

Business and Products. The Company, through its Lime and Limestone Operations, is a manufacturer of lime and limestone products, supplying primarily the construction (including highway, road, and building contractors), industrial (including paper and glass manufacturers), metals (including steel producers), environmental (including municipal sanitation and water treatment facilities and flue gas treatment processes), roof shingle manufacturers, oil and gas services, and agriculture (including poultry producers) industries. The Company is headquartered in Dallas, Texas and operates lime and limestone plants and distribution facilities in Arkansas, Colorado, Louisiana, Missouri, Oklahoma and Texas through its wholly owned subsidiaries, Arkansas Lime Company, ART Quarry TRS LLC (DBA Carthage Crushed Limestone), Colorado Lime Company, Mill Creek Dolomite, LLC, Texas Lime Company, U.S. Lime Company, U.S. Lime Company-Shreveport, U.S. Lime Company-St. Clair and U.S. Lime Company-Transportation.

The Company produces high-quality limestone from its open-pit quarries and underground mines that it sells as crushed limestone or processes further to produce several higher-value lime and limestone products, including pulverized limestone (“PLS”), quicklime, hydrated lime, and lime slurry. PLS (also referred to as ground calcium carbonate) is produced by applying heat to dry the limestone, which is then ground to granular and finer sizes. Quicklime (calcium oxide) is produced by heating limestone to very high temperatures in kilns in a process called calcination. Hydrated lime (calcium hydroxide) is produced by reacting quicklime with water in a controlled process. Lime slurry (milk of lime) is a suspended solution of calcium hydroxide produced by mixing quicklime with water in a lime slaker.

Crushed limestone is used primarily in construction aggregates. PLS is used in the production of construction materials, such as roof shingles and asphalt paving, as an additive to agriculture feeds, in the production of glass, as an agricultural soil enhancement, in flue gas treatment for utilities and other industries requiring scrubbing of emissions for environmental purposes and for mine safety dust in coal mining operations. Quicklime is used primarily in metal processing, in flue gas treatment, in soil stabilization for highway, road, and building construction, as well as for oilfield roads and drill sites, in the manufacturing of paper products, and in municipal sanitation and water treatment facilities. Hydrated lime is used primarily in municipal sanitation and water treatment facilities, in soil stabilization for highway, road, and building construction, in flue gas treatment, in asphalt as an anti-stripping agent, as a conditioning agent for oil and gas drilling mud, and in the production of chemicals. Lime slurry is used primarily in soil stabilization for highway, road and building construction.

Product Sales. In 2023, the Company sold almost all of its lime and limestone products in the states of Arkansas, Arizona, Colorado, Illinois, Iowa, Kansas, Louisiana, Mississippi, Missouri, Oklahoma, Tennessee, and Texas. Sales were made primarily by the Company’s ten sales employees who call on current and potential customers and solicit orders, which are generally made on a purchase-order basis. The Company also receives orders in response to bids that it prepares and submits to current and potential customers.

1

Principal customers for the Company’s lime and limestone products are construction customers (including highway, road, and building contractors), industrial customers (including paper manufacturers and glass manufacturers), metals producers (including steel producers), environmental customers (including municipal sanitation and water treatment facilities and flue gas treatment processes), roof shingle manufacturers, oil and gas services companies, and poultry producers.

Approximately 650 customers accounted for the Company’s sales of lime and limestone products during 2023. No single customer accounted for more than 10% of such sales. The Company is generally not subject to significant customer demand and credit risks as its customers are considerably diversified within its geographic region and by industry concentration. However, given the nature of the lime and limestone industry, the Company’s profits are very sensitive to changes in sales volumes, prices, and costs.

Lime and limestone products are transported by truck and rail to customers generally within a radius of 400 miles of each of the Company’s plants. All of the Company’s 2023 sales were made within the United States.

Seasonality. The Company’s sales have typically reflected seasonal trends, with the largest percentage of total annual shipments and revenues normally being realized in the second and third quarters. Lower seasonal demand normally results in reduced shipments and revenues in the first and fourth quarters. Inclement weather conditions generally have a negative impact on the demand for lime and limestone products supplied to construction-related customers, as well as on the Company’s open-pit quarrying operations.

Limestone Mineral Resources and Reserves. The Company’s limestone mineral resources and reserves contain at least 96% calcium carbonate (CaCO3). The Company has four subsidiaries that extract limestone from open-pit quarries: Texas Lime Company (“Texas Lime”), which operates the Texas Lime Quarry and is located near Cleburne, Texas; Arkansas Lime Company (“Arkansas Lime”), which operates the Batesville Quarry and is located near Batesville, Arkansas; ACT Holdings, Inc. (“ACT”), which owns the Love Hollow Quarry and is located near Cushman, Arkansas; and Mill Creek Dolomite, LLC (“Mill Creek”), acquired by the Company in February 2022, which operates the Mill Creek Quarry and is located near Mill Creek, Oklahoma. U.S. Lime Company-St. Clair (“St. Clair”) extracts limestone from the St. Clair Mine, an underground mine located near Marble City, Oklahoma. Carthage Crushed Limestone (“Carthage”) extracts limestone from the Carthage Mine, an underground mine located in Carthage, Missouri. Colorado Lime Company (“Colorado Lime”) owns property containing limestone deposits at Monarch Pass, Colorado. Existing crushed limestone stockpiles on the property are being used to provide feedstock to the Company’s plant in Delta, Colorado. Access to all properties is provided by paved roads and, in the case of Arkansas Lime, St. Clair, Carthage, and Mill Creek, also by rail.

The following table shows annual mined tons of limestone (in thousands) at the Company’s mining properties for the years ended December 31, 2023, 2022, and 2021:

Tons Mined | ||||

(in thousands of tons) | ||||

Mine/Location | 2023 | 2022 | 2021 | |

Texas Lime Quarry | 1,575 | 1,610 | 1,421 | |

Batesville Quarry | 785 | 1,017 | 898 | |

Love Hollow Quarry | 266 | 57 | - | |

St. Clair Mine | 477 | 533 | 414 | |

Carthage Mine | 625 | 645 | 687 | |

Mill Creek Quarry(1) | 169 | 162 | N/A | |

Total Production | 3,897 | 4,024 | 3,420 | |

(1) The Company acquired Mill Creek in February 2022. Tons mined only include production subsequent to the acquisition.

The Company engaged SYB Group, LLC (“SYB”) to serve as the Qualified Person (“QP”) to prepare estimates of the Company’s limestone mineral resources and reserves, as of December 31, 2021, at its quarries and mines at Texas Lime, Batesville, Love Hollow, and St. Clair (collectively, the “Material Properties”) and provide Technical Report

2

Summaries (“TRSs”) to file as Exhibits 96.1-96.4 to its Report on its Form 10-K for the year ended December 31, 2021. The QP was not retained to prepare estimates at Carthage, Mill Creek, or Colorado because the Company had not completed a drilling program sufficient to enable the QP to prepare estimates of the limestone mineral resources and reserves at those properties.

During 2023, the Company engaged SYB to update its TRSs for the Material Properties as of December 31, 2023, primarily to update economic assumptions, including costs and recovery rates, and extend the point of reference to include the respective crushing circuits at each site. The Company has not conducted a drilling program on any of the Material Properties subsequent to the effective date of the 2021 TRSs. Updated resources and reserves have been calculated using a $12.70 per ton price assumption for crushed limestone based on the U.S. Geological Survey Mineral Commodity Summaries 2023. Updates to the TRSs did not have a material effect on any of the Company’s mineral resources or reserves.

Summaries of the Company’s total limestone mineral resources and reserves for all Material Properties as of December 31, 2023 and 2022 are shown below. The terms Mineral Resource, Measured Resources, Indicated Resources, Mineral Reserves, Proven Reserves, and Probable Reserves are defined in accordance with SEC Regulation S-K subpart 229.1300 governing disclosures by registrants engaged in mining operations. Limestone mineral resources are presented exclusive of limestone mineral reserves. Limestone mineral resources as of December 31, 2022, have been recast from the prior year presentation to present as exclusive of limestone mineral reserves in order to conform to the current year presentation.

Summary of Total Limestone Mineral Resources - Exclusive of Mineral Reserves - as of December 31, 2023, Based on $12.70 per Ton | ||||||

| Cutoff Grade | Indicated | Cutoff Grade | Measured + Indicated | Cutoff Grade | |

18,193 | Above 96.0% (CaCO3) | 137,986 | Above 96.0% (CaCO3) | 156,179 | Above 96.0% (CaCO3) | |

Summary of Total Limestone Mineral Resources - Exclusive of Mineral Reserves - as of December 31, 2022, Based on $12.70 per Ton | ||||||

| Cutoff Grade | Indicated | Cutoff Grade | Measured + Indicated | Cutoff Grade | |

18,193 | Above 96.0% (CaCO3) | 137,986 | Above 96.0% (CaCO3) | 156,179 | Above 96.0% (CaCO3) | |

Summary of Total Limestone Mineral Reserves as of December 31, 2023, Based on $12.70 per Ton | ||||||

Proven Reserves | Cutoff Grade | Probable Reserves | Cutoff Grade | Total Mineral Reserves | Cutoff Grade | |

157,863 | Above 96.0% (CaCO3) | 72,037 | Above 96.0% (CaCO3) | 229,900 | Above 96.0% (CaCO3) | |

Summary of Total Limestone Mineral Reserves as of December 31, 2022, Based on $12.70 per Ton | ||||||

Proven Reserves | Cutoff Grade | Probable Reserves | Cutoff Grade | Total Mineral Reserves | Cutoff Grade | |

161,071 | Above 96.0% (CaCO3) | 72,037 | Above 96.0% (CaCO3) | 233,108 | Above 96.0% (CaCO3) | |

Set forth below is a description of each of the Company’s limestone mining properties. The Company considers the four mining properties associated with Texas Lime, Batesville, Love Hollow, and St. Clair to be material for purposes of application of SEC Regulation S-K subpart 229.1300. Included in the description of each of these four Material Properties are disclosures with respect to such property’s limestone mineral resources and reserves. For additional information with respect to the Material Properties, see the TRSs prepared by SYB, updated as of December 31, 2023, in Exhibits 96.1-96.4 to this Report on Form 10-K.

3

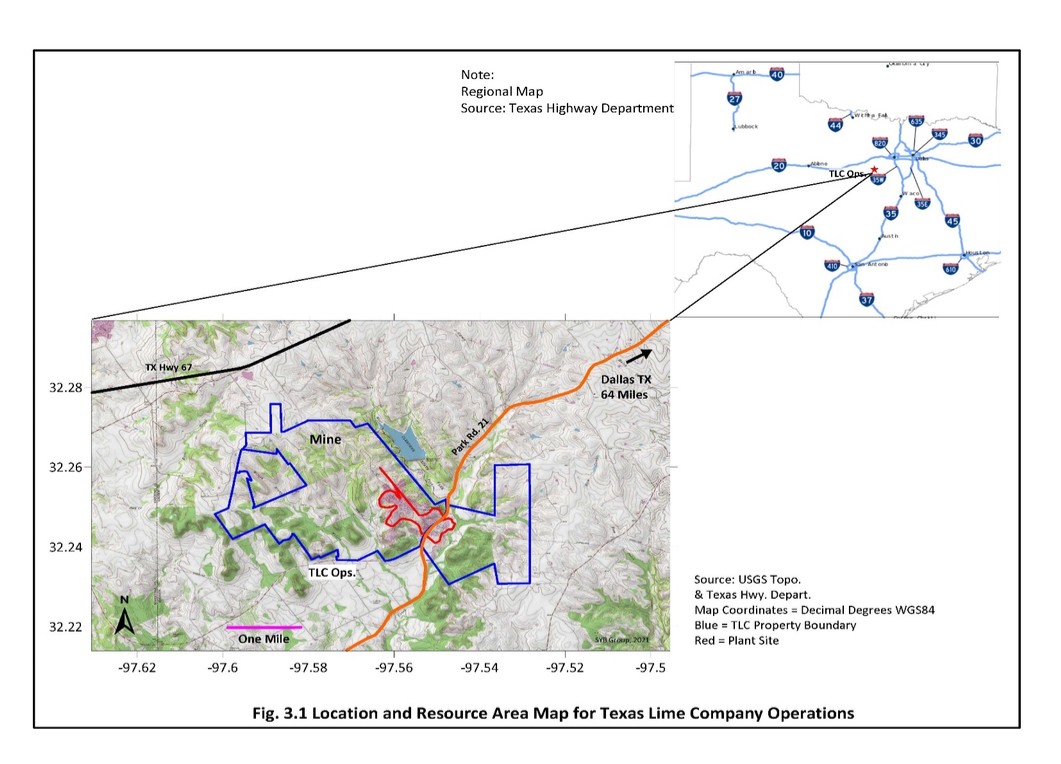

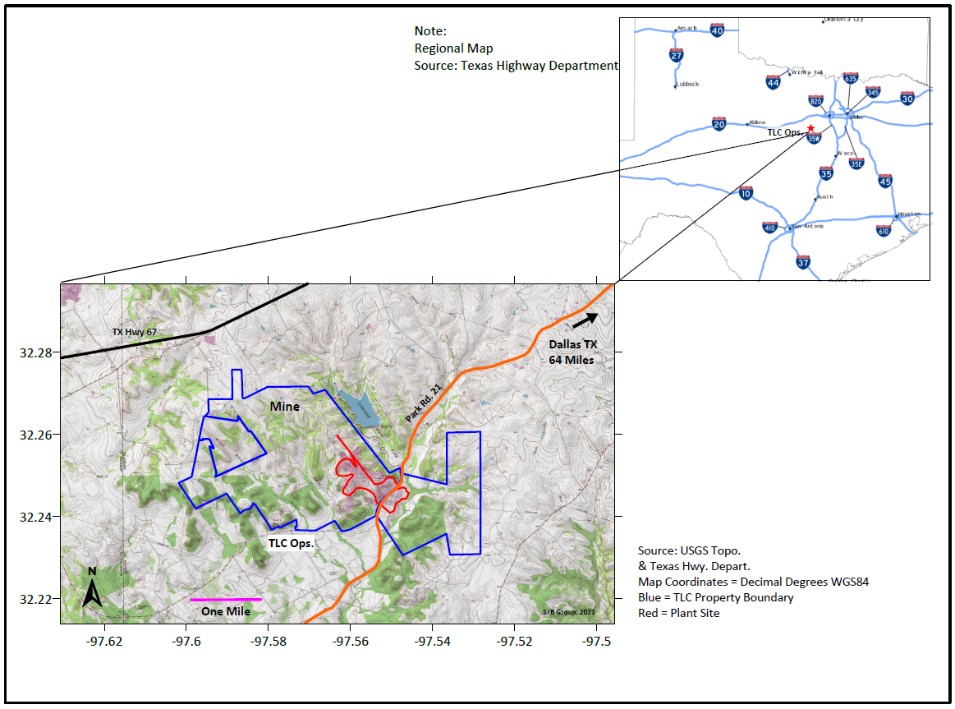

Texas Lime owns the Texas Lime Quarry and has crushed limestone, PLS, quicklime, and hydrated lime production facilities, located on approximately 5,200 acres of land in Johnson County, Texas that contains known high-quality limestone mineral resources in a bed averaging 25 to 35 feet in thickness. As of December 31, 2023, the total net book value of the Texas Lime Quarry was $13.8 million. As of December 31, 2023, the Texas Lime Quarry had 60.0 million tons of proven limestone mineral reserves and 47.5 million tons of probable limestone mineral reserves. Based on the current level of production and recovery rates, the Company estimates that these reserves are sufficient to sustain its limestone operations for approximately 65 years.

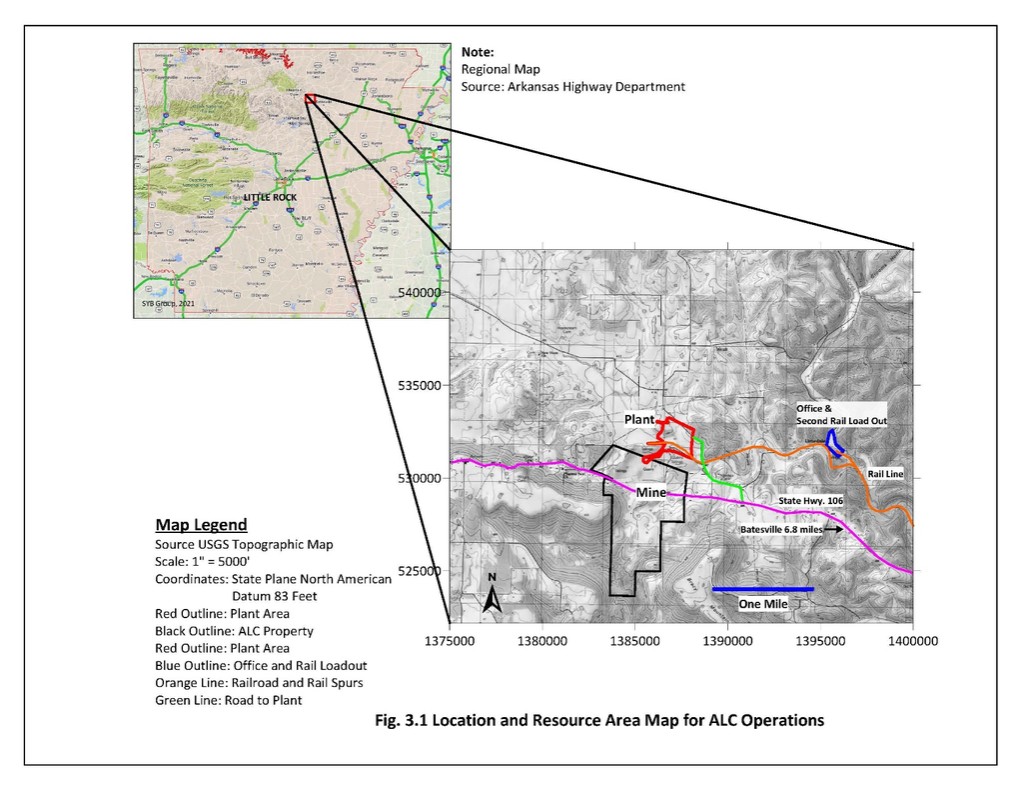

The following is a map of the Texas Lime Quarry location:

4

The tables below summarize the limestone mineral resources and reserves at the Texas Lime Quarry as of December 31, 2023 and 2022:

Texas Lime Quarry - Summary of Limestone Mineral Resources - Exclusive of Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Resources (tons) | Cutoff Grade | Processing Recovery | Resources (tons) | Cutoff Grade | Processing Recovery | |

Measured Mineral Resources | - | 96.0(CaCO3) | N/A | - | 96.0(CaCO3) | N/A | |

Indicated Mineral Resources | - | - | N/A | - | - | N/A | |

Total Measured + Indicated Resources | - | 96.0(CaCO3) | N/A | - | 96.0(CaCO3) | N/A | |

Texas Lime Quarry - Summary of Limestone Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Reserves (tons) | Cutoff Grade | Mining Recovery | Reserves (tons) | Cutoff Grade | Mining | |

Proven Reserves | 59,989 | 96.0(CaCO3) | 95% | 61,564 | 96.0(CaCO3) | 95% | |

Probable Reserves | 47,532 | 96.0(CaCO3) | 95% | 47,532 | 96.0(CaCO3) | 95% | |

Total Mineral Reserves | 107,521 | 96.0(CaCO3) | 95% | 109,096 | 96.0(CaCO3) | 95% | |

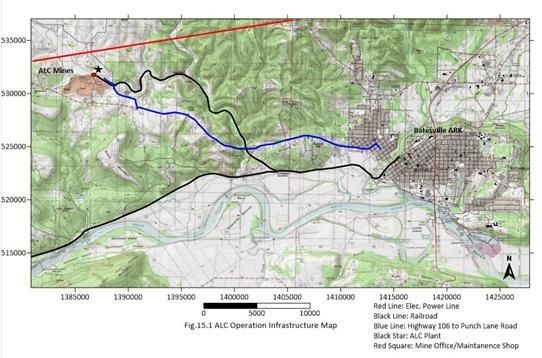

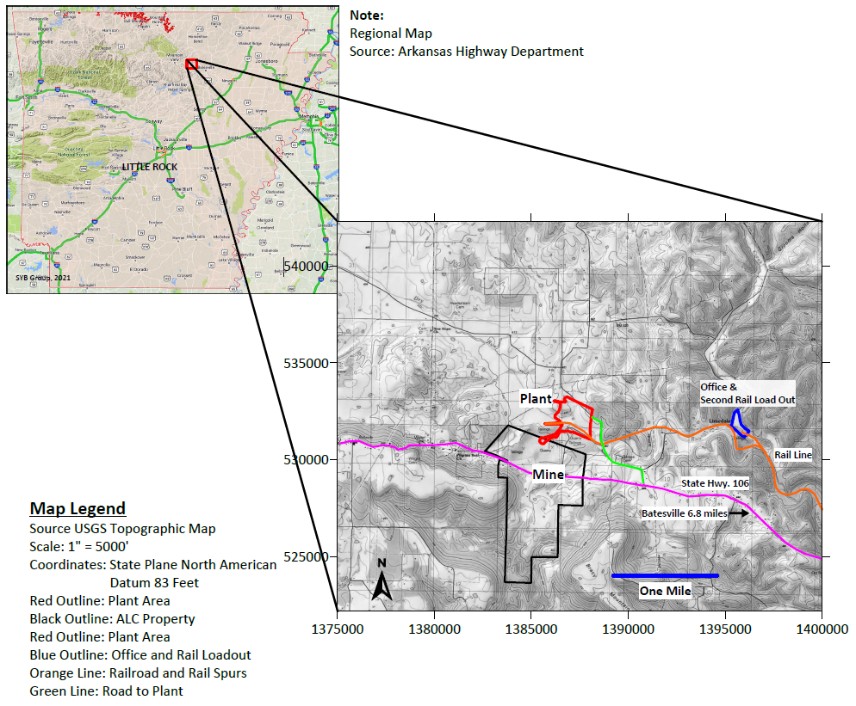

Arkansas Lime owns the Batesville Quarry and has crushed limestone, PLS, quicklime, and hydrated lime production facilities, located on approximately 1,260 acres of land located in Independence County, Arkansas that contains known high-quality limestone mineral resources in a bed averaging 60 feet in thickness. As of December 31, 2023, the Batesville Quarry had a net book value of $4.1 million. As of December 31, 2023, the Batesville Quarry had 8.2 million tons of indicated limestone mineral resources, 7.4 million tons of proven limestone mineral reserves, and 3.5 million tons of probable limestone mineral reserves. Based on forecasted production levels and recovery rates, the Company estimates that these reserves are sufficient to sustain its limestone operations for approximately 20 years.

5

The following is a map of the Batesville Quarry location:

The tables below summarize the limestone mineral resources and reserves at the Batesville Quarry as of December 31, 2023 and 2022:

Batesville Quarry - Summary of Limestone Mineral Resources - Exclusive of Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Resources (tons) | Cutoff Grade | Processing Recovery |

| Resources (tons) | Cutoff Grade | Processing Recovery |

Measured Mineral Resources | - | 96.0(CaCO3) | N/A | - | 96.0(CaCO3) | N/A | |

Indicated Mineral Resources | 8,239 | 96.0(CaCO3) | N/A | 8,239 | 96.0(CaCO3) | N/A | |

Total Measured + Indicated Resources | 8,239 | 96.0(CaCO3) | N/A | 8,239 | 96.0(CaCO3) | N/A | |

6

Batesville Quarry - Summary of Limestone Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Reserves (tons) | Cutoff Grade | Mining Recovery(1) | Reserves (tons) | Cutoff Grade | Mining Recovery(1) | |

Proven Reserves | 7,407 | 96.0(CaCO3) | 82%/75% | 8,192 | 96.0(CaCO3) | 82%/75% | |

Probable Reserves | 3,458 | 96.0(CaCO3) | 82%/75% | 3,458 | 96.0(CaCO3) | 82%/75% | |

Total Mineral Reserves | 10,865 | 96.0(CaCO3) | 82%/75% | 11,650 | 96.0(CaCO3) | 82%/75% | |

(1) Mining recovery is listed as open-pit/underground recovery.

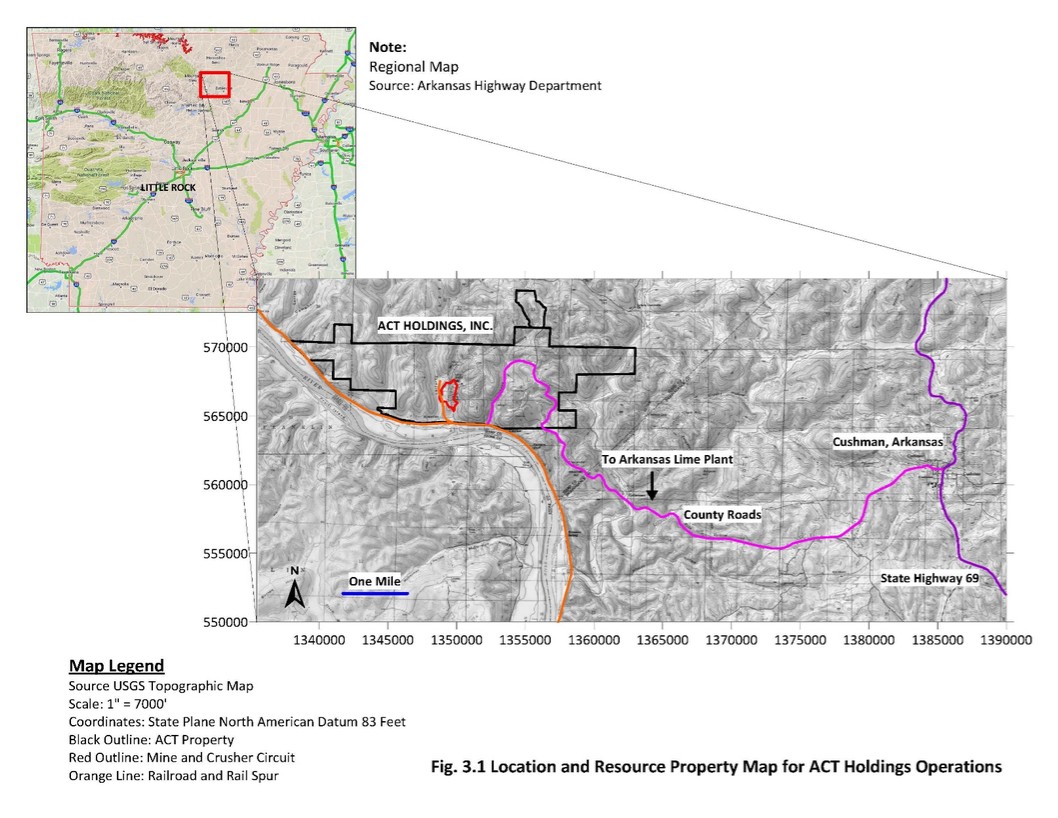

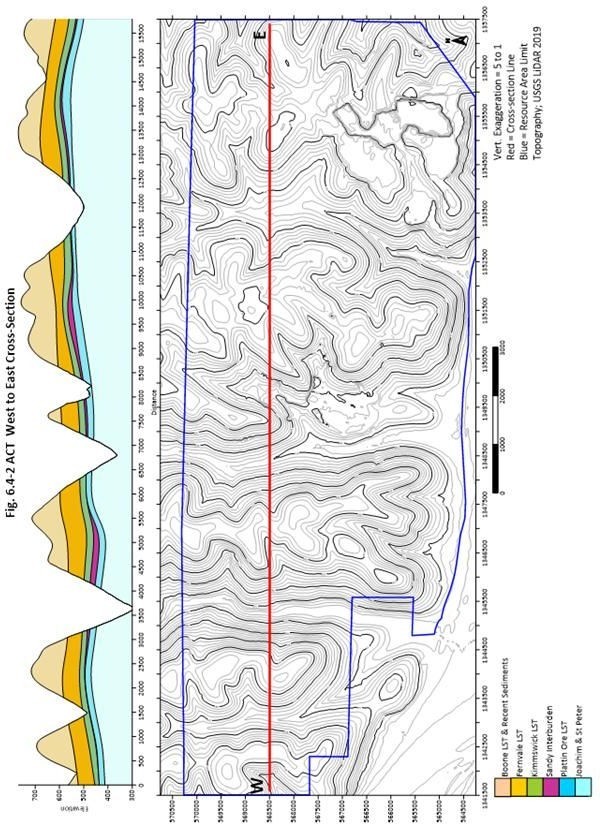

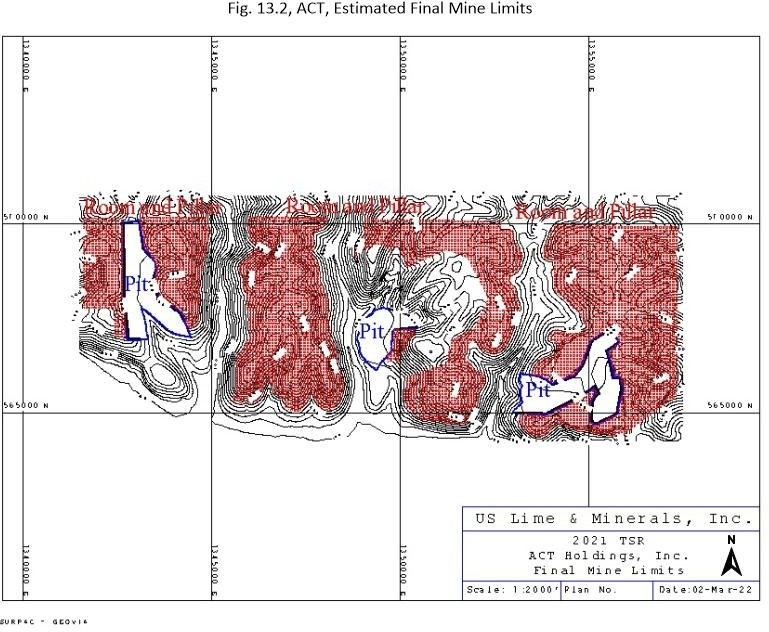

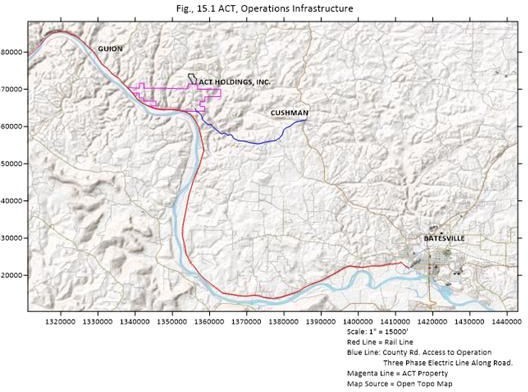

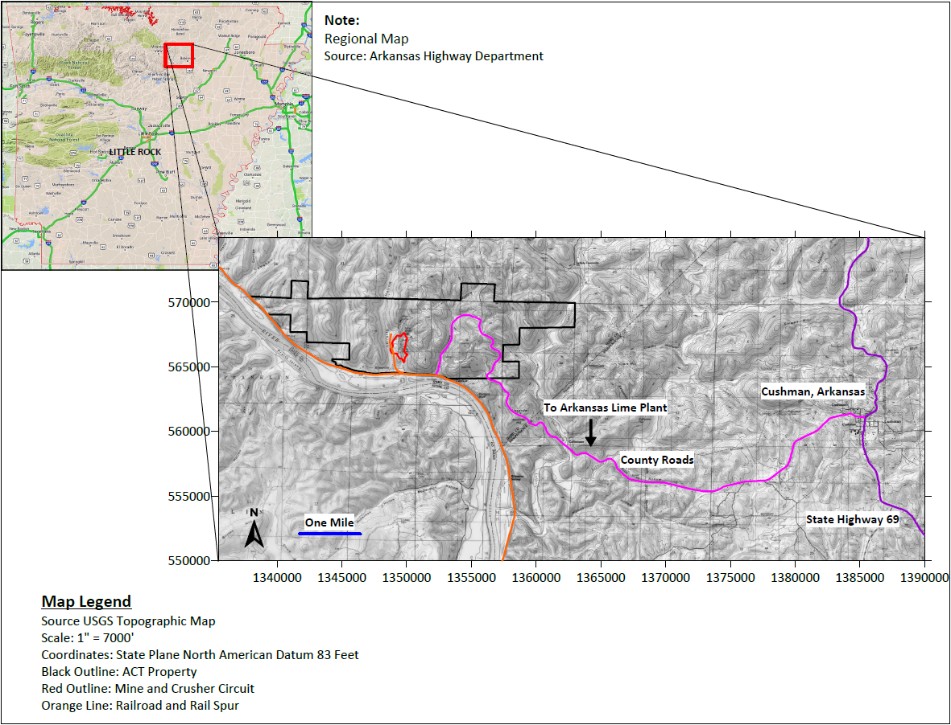

In 2005, the Company acquired the Love Hollow Quarry, which is owned by ACT and associated with Arkansas Lime, located on approximately 2,500 acres of land in Izard County, Arkansas. In 2022, the Company improved and developed the transportation infrastructure between the Love Hollow Quarry and Arkansas Lime’s production facilities, incurred other development costs to prepare the Love Hollow Quarry for mining, and began sourcing a portion of the Arkansas Lime plant’s limestone requirements from the Love Hollow Quarry. As of December 31, 2023, the Love Hollow Quarry had a net book value of $4.9 million. As of December 31, 2023, the Love Hollow Quarry had 10.4 million tons of measured limestone mineral resources, 68.2 million tons of proven limestone mineral reserves, and 21.0 million tons of probable limestone mineral reserves. Based on forecasted production levels and recovery rates, the Company estimates that these reserves are sufficient to sustain its limestone operations for approximately 80 years

The following is a map of the Love Hollow Quarry:

7

The tables below summarize the limestone mineral resources and reserves at the Love Hollow Quarry as of December 31, 2023 and 2022:

Love Hollow Quarry - Summary of Limestone Mineral Resources - Exclusive of Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Resources (tons) | Cutoff Grade | Processing Recovery | Resources (tons) | Cutoff Grade | Processing Recovery | |

Measured Mineral Resources | 10,392 | 96.0(CaCO3) | N/A | 10,392 | 96.0(CaCO3) | N/A | |

Indicated Mineral Resources | - | - | N/A | - | - | N/A | |

Total Measured + Indicated Resources | 10,392 | 96.0(CaCO3) | N/A | 10,392 | 96.0(CaCO3) | N/A | |

Love Hollow Quarry - Summary of Limestone Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Reserves (tons) | Cutoff Grade | Mining Recovery(1) | Reserves (tons) | Cutoff Grade | Mining Recovery(1) | |

Proven Reserves | 68,176 | 96.0(CaCO3) | 95%/75% | 68,442 | 96.0(CaCO3) | 95%/75% | |

Probable Reserves | 21,047 | 96.0(CaCO3) | 95%/75% | 21,047 | 96.0(CaCO3) | 95%/75% | |

Total Mineral Reserves | 89,223 | 96.0(CaCO3) | 95%/75% | 89,489 | 96.0(CaCO3) | 95%/75% | |

(1) Mining recovery is listed as open-pit/underground recovery

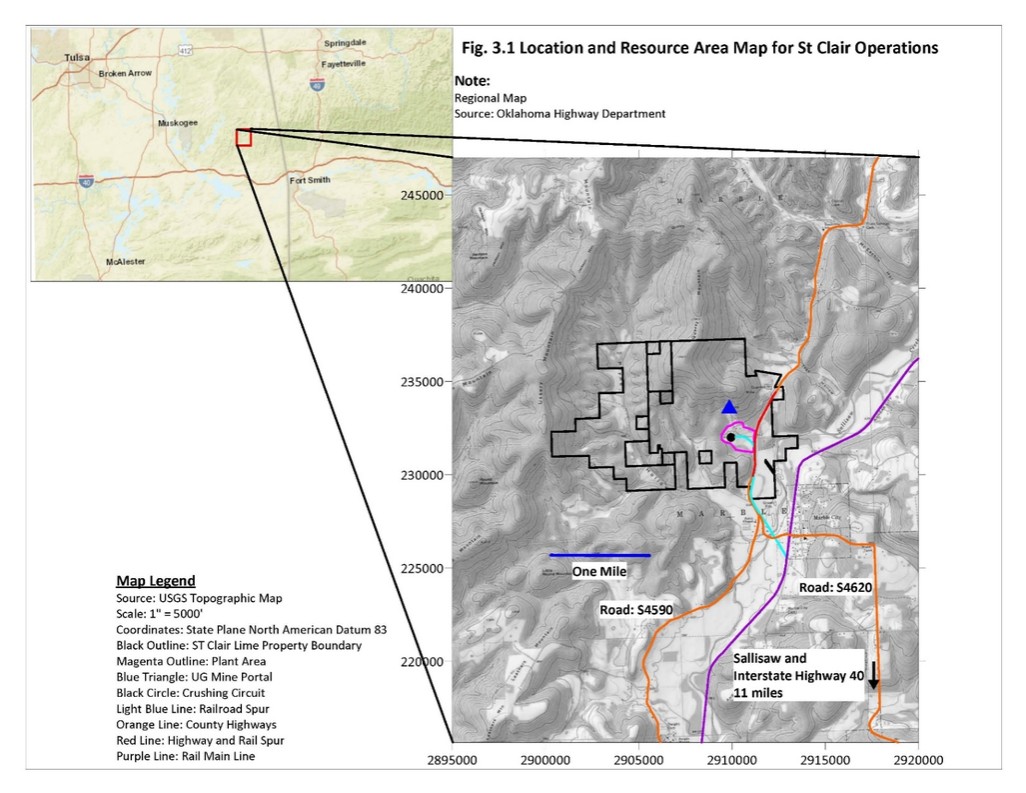

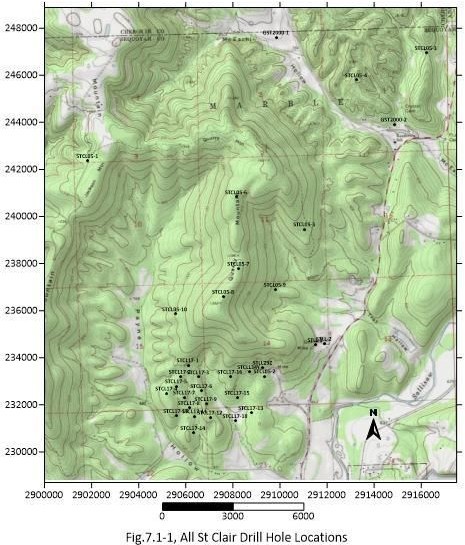

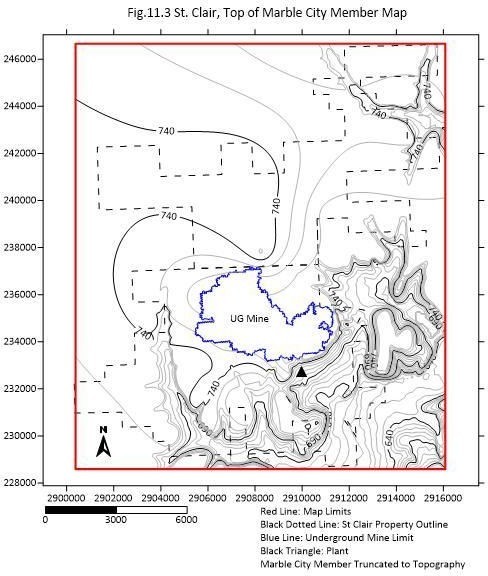

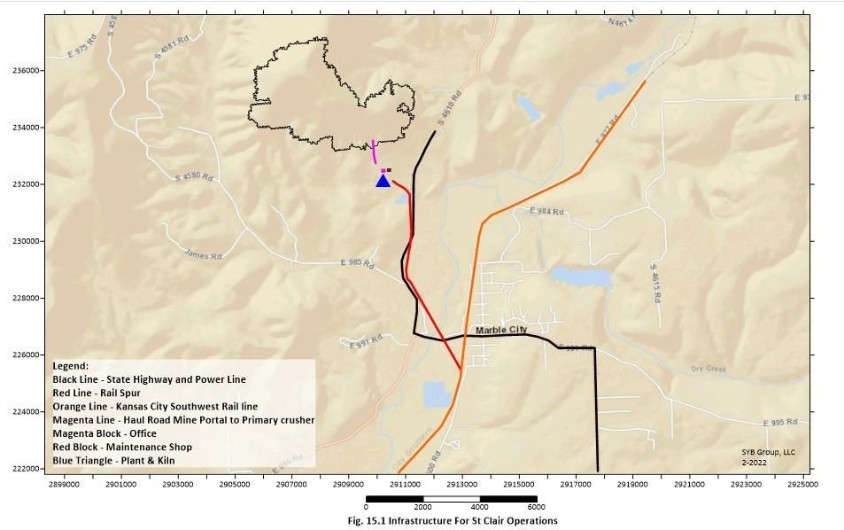

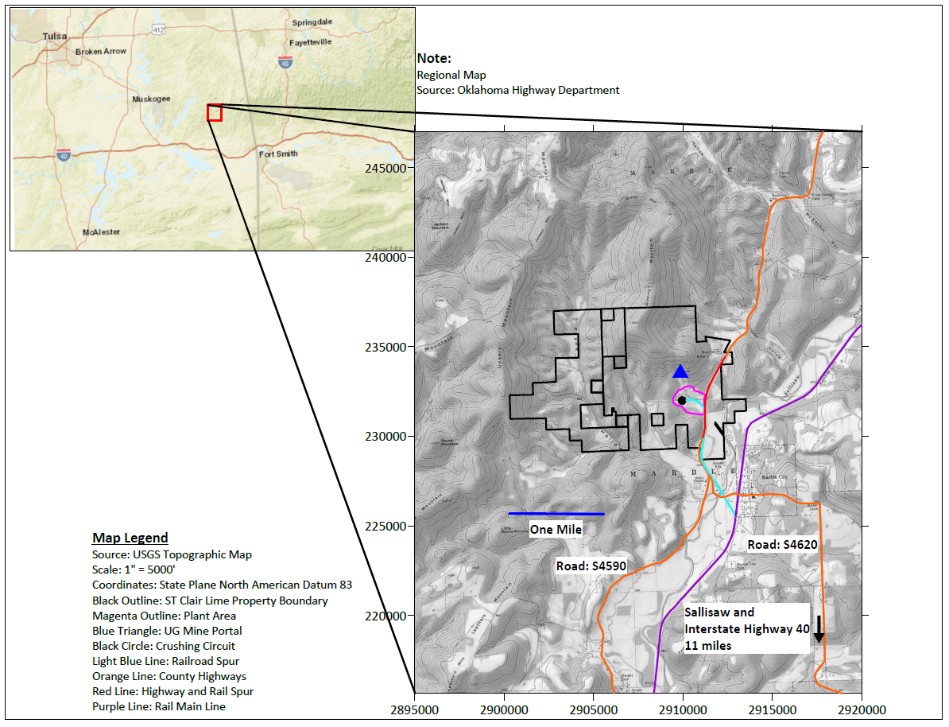

St. Clair operates the St. Clair Mine and has crushed limestone, PLS, quicklime, and hydrated lime production facilities located on approximately 1,400 acres that it owns in Sequoyah County, Oklahoma containing high-quality limestone resources and also has long-term mineral leases that provide the right to mine high-quality limestone resources contained in approximately 1,340 adjacent acres. As of December 31, 2023, the St. Clair Mine had a net book value of $7.6 million. As of December 31, 2023, the St. Clair Mine had 7.8 million tons of measured limestone mineral resources, 129.7 million tons of indicated limestone mineral resources, and 22.3 million tons of proven limestone mineral reserves. Based on the current levels of production and recovery rates, the Company estimates that these reserves are sufficient to sustain its limestone operations for approximately 50 years.

8

The following is a map of the St. Clair Mine:

The tables below summarize the limestone mineral resources and reserves at the St. Clair Mine as of December 31, 2023 and 2022:

St. Clair Mine - Summary of Limestone Mineral Resources - Exclusive of Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Resources (tons) | Cutoff Grade | Processing Recovery | Resources (tons) | Cutoff Grade | Processing Recovery | |

Measured Mineral Resources | 7,801 | 96.0(CaCO3) | N/A | 7,801 | 96.0(CaCO3) | N/A | |

Indicated Mineral Resources | 129,747 | 96.0(CaCO3) | N/A | 129,747 | 96.0(CaCO3) | N/A | |

Total Measured + Indicated Resources | 137,548 | 96.0(CaCO3) | N/A | 137,548 | 96.0(CaCO3) | N/A | |

9

St. Clair Mine - Summary of Limestone Mineral Reserves | |||||||

as of December 31, 2023 |

| as of December 31, 2022 | |||||

Resource Category | Reserves (tons) | Cutoff Grade | Mining Recovery | Reserves (tons) | Cutoff Grade | Mining Recovery | |

Proven Reserves | 22,291 | 96.0(CaCO3) | 81% | 22,873 | 96.0(CaCO3) | 81% | |

Probable Reserves | - | 96.0(CaCO3) | 81% | - | 96.0(CaCO3) | 81% | |

Total Mineral Reserves | 22,291 | 96.0(CaCO3) | 81% | 22,873 | 96.0(CaCO3) | 81% | |

Carthage operates the Carthage Mine and has crushed limestone production facilities located on approximately 800 acres that it owns containing high-quality limestone. In addition, Carthage has the right to mine the high-quality limestone contained in approximately 760 adjacent acres pursuant to long-term mineral leases.

Mill Creek operates the Mill Creek Quarry and production facilities located on approximately 570 acres that it owns where it mines and processes crushed dolomitic limestone.

Colorado Lime acquired the Monarch Pass Quarry in November 1995 and has not carried out any mining on the property. The Monarch Pass Quarry, which had been operated for many years until the early 1990s, contains a mixture of limestone types, including high-quality calcium limestone.

Internal Controls Over Limestone Mineral Resources and Reserves Estimates. Internal control procedures followed by the Company’s Quality Control/Quality Assurance Laboratories (“QC/QA Lab”) and its contract geologists when assessing properties for limestone mineral resources and reserves estimates are clearly defined. Core drilling is conducted under the direct supervision of the geologists, and all core data is logged using a standard protocol. The geologists are responsible for examining the core and compiling an interval list for X-Ray Florescence (“XRF”) analysis. Splits of cores are bagged and labeled with the depth interval to be analyzed, with the remaining split boxed and stored for reference. Bagged intervals are submitted to the Company’s certified QC/QA Lab for XRF analysis, with any samples not destroyed by the testing process retained at the Company’s core storage facility. On an ongoing basis, the QC/QA Lab analyzes production samples for cutoff grade consistency with expectations used in the estimates for limestone mineral resources and reserves.

When classifying limestone mineral resources and reserves, the Company’s contract geologists apply a fixed cutoff grade and set parameters of geologic confidence to classify the respective resources and reserves. Company management reviews the geologists’ assessments for reasonableness.

Quarrying and Mining. The Company extracts limestone by the open-pit method at its Texas, Batesville, Love Hollow, and Mill Creek Quarries. The Monarch Pass Quarry is also an open-pit quarry but is not being mined at this time. The open-pit method consists of removing any overburden comprising soil and other substances, including inferior limestone, and then extracting the exposed high-quality limestone. The Company removes such overburden by utilizing both its own employees and equipment and those of outside contractors. Open-pit mining is generally less expensive than underground mining. The principal disadvantage of the open-pit method is that operations are subject to inclement weather and overburden removal. The limestone is extracted by drilling and blasting, utilizing standard mining equipment. At the St. Clair and Carthage mines, the Company mines limestone underground using room and pillar mining. The Company has no knowledge of any recent changes in the physical quarrying or mining conditions on any of our properties that have materially affected quarrying or mining operations.

Plants and Facilities. After extraction, the limestone is further crushed and screened to produce crushed limestone, and, in the case of PLS, ground and dried, or, in the case of quicklime, processed in kilns. Quicklime may then be further processed in hydrators and slakers to produce hydrated lime and lime slurry. The Company produces and distributes crushed limestone, PLS, and quicklime products at five plants, six lime slurry facilities, and three terminal facilities. All of its plants and facilities are accessible by paved roads, and, in the case of the Arkansas Lime, St. Clair and Carthage plants, the Love Hollow Quarry, and the terminal facilities, also by rail.

10

In addition to the Company’s production of crushed limestone at each of its plants, the following Company plants produce additional lime and limestone products:

The Texas Lime plant has an annual capacity of approximately 470 thousand tons of quicklime from two preheater rotary kilns. The plant also has PLS equipment, which, depending on the product mix, has the capacity to produce approximately 800 thousand tons of PLS annually.

The Arkansas Lime plant is situated at the Batesville Quarry. Utilizing three preheater rotary kilns, this plant has an annual capacity of approximately 650 thousand tons of quicklime. The Arkansas Lime plant is approximately 21 miles from the Love Hollow Quarry, to which it is connected by railroad. Arkansas Lime’s PLS and hydrating facilities are situated on a tract of 290 acres located approximately two miles from the Batesville Quarry, to which it is connected by a Company-owned railroad. The PLS equipment, depending on the product mix, has the capacity to produce approximately 300 thousand tons of PLS annually.

The St. Clair plant has an annual capacity of approximately 250 thousand tons of quicklime from one vertical kiln and one preheater rotary kiln. The plant also has PLS equipment, which has the capacity to produce approximately 150 thousand tons of PLS annually.

The Carthage plant has facilities located next to the Carthage Mine that produce both crushed limestone and PLS. The equipment has the capacity to produce approximately 900 thousand tons annually.

The Mill Creek plant has facilities located next to the Mill Creek Quarry that produce dolomitic PLS products. The equipment has the capacity to produce approximately 300 thousand tons annually.

The Company also maintains lime hydrating and bagging equipment at the Texas, Arkansas, and St. Clair plants. Storage facilities for lime and limestone products at each plant consist primarily of cylindrical tanks, which are considered by the Company to be adequate to protect its lime and limestone products and to provide an available supply for customers’ needs at the expected volumes of shipments. Equipment is maintained at each plant to load trucks and, at the Arkansas Lime, St. Clair, and Mill Creek plants, to load railroad cars.

Colorado Lime operates a limestone grinding and bagging facility with an annual capacity of approximately 125 thousand tons, located on approximately three and one-half acres of land in Delta, Colorado.

During 2023, the Company’s utilization rate was approximately 66% of its total annual production capacity for the plants in its Lime and Limestone Operations.

U.S. Lime Company (“US Lime”) uses quicklime to produce lime slurry, and has four Houston area facilities, including two distribution terminals connected to railroads, to serve the Greater Houston area construction market and four facilities to serve the Dallas-Ft. Worth Metroplex. The Company established U.S. Lime Company-Transportation to deliver some of the Company’s products to its customers and facilities primarily in Texas.

U.S. Lime Company - Shreveport operates a distribution terminal in Shreveport, Louisiana, which is connected to a railroad, to provide lime storage, hydrating, slurrying, and distribution capacity to service markets in Louisiana and East Texas.

The Company believes that its plants and facilities are adequately maintained and insured.

Human Capital Resources. The Company is committed to attracting and retaining the best and brightest talent to meet the current and future needs of its business. Attracting, retaining, motivating, and investing in the development of human capital resources is a critical part of the Company’s commitment to environmental, social, and governance (“ESG”) and sustainability issues.

At December 31, 2023, the Company employed 333 persons, 111 of whom were represented by unions. The Company is a party to three collective bargaining agreements. The collective bargaining agreement for the Texas facilities expires in November 2026. The collective bargaining agreement for the Carthage facilities expires in May 2025. The Company successfully negotiated a new collective bargaining agreement for the Arkansas facilities in

11

February 2024, which has been ratified by the union. The agreement for the Arkansas facilities expires in January 2029. Overall, the Company believes that its employee relations are generally good.

Employee Retention and Incentivization. The Company has entered into an employment agreement with Timothy W. Byrne, its President and Chief Executive Officer. Mr. Byrne’s employment agreement became effective as of January 1, 2020 for a five-year term and will continue for successive one-year periods unless the Company or Mr. Byrne gives at least one-year’s prior written notice of intent not to renew. Under the employment agreement, in addition to the possibility of a discretionary cash bonus, Mr. Byrne is entitled each year to an EBITDA cash bonus opportunity under the United States Lime & Minerals, Inc. Amended and Restated 2001 Long-Term Incentive Plan (the “Plan”), and he is also entitled to grants of equity awards under the Plan.

Mr. Byrne’s employment agreement provides that Mr. Byrne is subject to certain forfeiture/clawback and share ownership provisions designed to align Mr. Byrne’s financial interests with those of the Company’s long-term shareholders, and to ensure that he is incentivized not to take actions that may benefit the Company and its shareholders in the short-term at the expense of long-term corporate value creation and sustainability. In particular, in entering into the employment agreement with Mr. Byrne, the Company’s Board of Directors and Compensation Committee were sensitive to how Mr. Byrne’s leadership and actions could further the Company’s various objectives, including human capital resources development and executive succession planning.

With respect to the Company’s broader employee base, certain employees are eligible to receive annual cash bonuses based on discretionary determinations. Except in the case of Mr. Byrne, the Company has not adopted a formal or informal annual bonus arrangement with pre-set performance goals. Rather, the determination to pay a cash bonus, if any, is made in December each year based on the past performance of the individual and the Company or on the attainment of non-quantified performance goals during the year. In either such case, the discretionary bonus may be based on the specific accomplishments of the individual and/or on the overall performance of the Company. The amounts of the discretionary bonuses for 2023 were based on each employee’s individual performance and accomplishments, as well as those of the Company, including productivity, sales, controlling costs, and contributions made to special projects.

In addition to cash bonuses, the Company makes equity awards to certain individuals under the Plan. The Company uses equity awards granted under the Plan as a means to attract, retain, and motivate the Company’s directors, officers, employees, and consultants. The Company views the use of equity awards under the Plan as an important means of aligning the interests of its employees with those of its shareholders.

Employee Health and Safety. The Company believes that it is responsible to its employees to provide a safe and healthy workplace environment. The Company seeks to accomplish this by: training employees in safe work practices; openly communicating with employees; following safety standards and establishing and improving safe work practices; involving employees in safety processes; and recording, reporting, and investigating accidents, incidents, and losses to avoid reoccurrence.

Employee Development and Training. The Company encourages and supports the growth and development of its employees. It advances continual learning and career development through ongoing performance and development conversations or evaluations with employees and internally and externally developed training programs. The Company also provides reimbursement for certain educational programs relating to the Company’s business.

Employee Diversity and Inclusion. The Company is committed to fostering a work environment that values and promotes diversity and inclusion. This commitment includes providing equal access to, and participation in, equal employment opportunities, programs, and services, without regard to a person’s gender, nationality, race, and ethnicity. The Company is focused on the development and fair treatment of its employees, including equal employment hiring practices and policies, anti-harassment, and anti-retaliation policies. The Company is continuing to invest in efforts to create a more diverse and inclusive workforce and workplace environment.

Competition. The lime industry is highly regionalized and competitive, with price, quality, ability to meet customer demands and specifications, proximity to customers, personal relationships, and timeliness of deliveries being the prime competitive factors. The Company’s competitors are predominantly private companies.

12

The lime industry is characterized by high barriers to entry, including: the scarcity of high-quality limestone deposits on which the required zoning and permitting for extraction can be obtained; the need for lime plants and facilities to be located close to markets, paved roads, and railroad networks to enable cost-effective production and distribution; clean air and anti-pollution regulations, including those related to greenhouse gas emissions, which make it more difficult to obtain permitting for new sources of emissions, such as lime kilns; and the high capital cost of the plants and facilities. These considerations reinforce the premium value of operations having permitted, long-term, high-quality limestone resources and good locations and transportation relative to markets.

Lime producers tend to be concentrated on known high-quality limestone formations where competition takes place principally on a regional basis. While the steel industry and environmental-related users are the largest market sectors, the lime industry also counts chemical users and other industrial users, including paper manufacturers, oil and gas services and highway, road and building contractors, among its major customers.

In recent years, the lime industry has experienced reduced demand from certain industries as they experience cyclical or secular downturns. For example, demand from the Company’s steel and oil and gas services customers tends to vary with the demand for their products and services, which has continued to be cyclical. In addition, utility plants are continuing to use more natural gas and renewable sources for power generation instead of coal, with the permitting of new coal-fired utility plants becoming extremely difficult, which reduces their demand for lime and limestone for flue gas treatment processes. These reductions in demand have resulted in increased competitive pressures, including pricing and competition for certain customer accounts, in the industry.

Consolidation in the lime industry has left the three largest companies accounting for more than two-thirds of North American production capacity. In addition to the consolidations, and often in conjunction with them, many lime producers have undergone modernization and expansion and development projects to upgrade their processing equipment in an effort to improve operating efficiency. The Company believes that its modernization and expansion projects in Texas, Arkansas, and Oklahoma and its recent acquisitions, along with its lime slurry operations in Texas, should allow it to continue to remain competitive, protect its markets and position itself for the future. In addition, the Company will continue to evaluate internal and external opportunities for expansion, growth and increased profitability, as conditions warrant, or opportunities arise. The Company may have to revise its strategy or otherwise consider ways to enhance the value of the Company, including by entering into strategic partnerships, mergers or other transactions.

Compliance with Government Regulations. The Company is subject to various federal, state, and local laws and regulations that may materially impact the Company’s financial condition, results of operations, cash flows and competitive position. These include laws and regulations relating to the environment, zoning and land use, mine permitting and operations, mine safety, and reclamation and remediation.

Environmental Laws. The Company owns or controls large areas of land on which it operates limestone quarries, two underground mines, lime plants, and other facilities with inherent environmental responsibilities, compliance costs, and liabilities. These include maintenance and operating costs for pollution control equipment, the cost of ongoing monitoring and reporting programs, the cost of reclamation efforts, and other similar environmental costs and liabilities.

The Company’s operations are subject to various federal, state, and local laws and regulations relating to the environment, health and safety, and other regulatory matters, including the Clean Air Act, the Clean Water Act, the Resource Conservation and Recovery Act, the Comprehensive Environmental Response, Compensation and Liability Act, and analogous state and local laws (“Environmental Laws”). These Environmental Laws grant the United States Environmental Protection Agency (the “EPA”) and state governmental agencies the authority to promulgate and enforce regulations that could result in substantial expenditures on pollution control, waste management, permitting compliance activities, and mining reclamation. Many Environmental Laws also authorize private citizens and interest groups to file lawsuits in court to enforce alleged violations. Changes in policy or political leadership may affect how Environmental Laws are interpreted or enforced by the EPA and state governmental agencies. The failure to comply with Environmental Laws may result in administrative and civil penalties, injunctive relief, and criminal prosecution. The Company has not been named as a potentially responsible party in any federal superfund cleanup site or state-led cleanup site.

13

The rate of change of Environmental Laws continues to be rapid, and compliance can require significant expenditures. Permits and other authorizations under Environmental Laws are required for the Company’s operations, and such permits are subject to modification during the permit renewal process and, in very rare instances, could be revoked.

The Clean Air Act and analogous state laws require the Company to obtain authorization to construct or modify existing facilities, and its lime plants are subject to operating permits that have significant ongoing compliance costs. Over time, the EPA has increased the stringency of the National Ambient Air Quality Standards (“NAAQS”), which are used to establish air emission permitting limits under the Clean Air Act. The EPA has lowered ozone standards and reclassified areas where State Implementation Plans (the “SIPs”) exist. In 2015, the EPA issued a rule establishing the ground-level ozone NAAQS at 70 parts per billion. The EPA has proposed redesignating the Dallas-Fort Worth nonattainment area, which includes the Texas Lime facility, as severe under the 2008 standard 8-hour ozone classifications. The EPA has also published a finding that Texas, among 11 other states, failed to submit required SIP revisions and has given Texas until May 2025 to submit a complete SIP. Texas is in the process of developing regulations in response to the redesignations to reduce emissions of nitrogen oxides and volatile organic compounds, which will likely involve more stringent permitting requirements for stationary sources.

In February 2024, the EPA issued a final rule reducing the NAAQS for fine particulate matter. This regulation will significantly increase nonattainment areas across the United States, potentially including areas where the Company operates. States with delegated permitting authority under the Clean Air Act will be required to revise their SIPs accordingly.

In January 2023, under Section 112 of the Clean Air Act, the EPA proposed amendments to the National Emission Standards for Hazardous Air Pollutants (“NESHAPs”) for lime plants, which would revise the standards required to meet the maximum achievable control technology (“MACT”) at major sources of hazardous air pollutants within the lime industry. The proposed MACT rule would establish stringent emission limitations for four hazardous air pollutants which will require additional pollution control equipment at lime kilns subject to the rule. While the proposed rule has not been finalized, it is uncertain what limits the EPA will ultimately impose on the lime industry and what emission controls may be required by the final MACT rule. It is likely, however, that the final rule will incorporate more stringent standards than existing standards, which could require additional expenditures for designing, constructing, operating, and maintaining pollution control equipment necessary for compliance.

EPA regulations require large emitters of greenhouse gases, including the Company’s plants, to collect and report greenhouse gas emissions data. The EPA has previously indicated that it will use the data collected through the greenhouse gas reporting rules to decide whether to promulgate future greenhouse gas emission limits. The EPA and delegated states also regulate greenhouse gas emissions under the New Source Review permitting and Federal Operating Permit programs for facilities that are otherwise subject to permitting based on their emissions of conventional, non-greenhouse gas pollutants. Thus, any new facilities or major modifications to existing facilities that exceed the federal New Source Review emission thresholds for conventional pollutants may be required to use “best available control technology” and energy efficiency measures to minimize greenhouse gas emissions.

Although the timing and impact of climate change legislation and of regulations limiting greenhouse gas emissions are uncertain, the consequences of such legislation and regulation are potentially significant for the Company because the production of CO2 is inherent in the manufacture of lime through the calcination of limestone and combustion of fossil fuels. In February 2021, the current Administration rejoined the Paris Agreement. The Agreement commits the United States to reduce greenhouse gas emissions by 26 to 28 percent below 2005 levels by 2025. Future regulation related to the Paris Agreement or other greenhouse gas rulemakings could affect New Source Review permitting or other permitting programs and, thereby, increase the time and costs of plant upgrades and expansions. The passage of climate change legislation, and other regulatory initiatives by the Congress, the states, or the EPA that restrict or tax emissions of greenhouse gases, could adversely affect the Company. There is no assurance that changes in the law or regulations will not be adopted, such as the imposition of greenhouse gas emission limits, a carbon tax, a cap-and-trade program requiring the Company to purchase carbon credits, or other measures that would require reductions in emissions or changes to raw materials, fuel use, or production rates. Such changes, if adopted, could have a material adverse effect on the Company’s financial condition, results of operations, cash flows, and competitive position.

14

These and similar rulemakings could increase the cost of future plant modifications or expansions, may make it difficult or impossible to obtain new authorizations and permits for new facilities, may require the Company to purchase emissions offsets as a condition of new authorizations and permits, and may increase compliance costs and have a material adverse effect on the Company’s financial condition, results of operations, cash flows, and competitive position.

In addition to regulation, several court cases have been filed and decisions issued that may increase the risk of claims being filed by third parties against companies for their greenhouse gas emissions. Such cases may seek to challenge air permits, to force reductions in greenhouse gas emissions, or to recover damages for alleged climate change impacts.

The Company also holds permits for process water and storm water discharges and must comply with the Clean Water Act and analogous state laws and regulations. Any failure to comply with these permits could result in fines or other penalties. Material changes to the terms of these permits or changes to regulations affecting water discharges in the future could also increase compliance costs.

The manufacturing of quicklime and hydrated lime requires significant volumes of water. The Company operates multiple groundwater wells to provide water to its plants. Groundwater pumping is subject to increased regulation, and in some areas the Company is required to obtain permits from groundwater conservation districts to pump groundwater. Any failure to comply with these permits could result in fines or other penalties, and future changes that restrict the quantities of groundwater that may be pumped may increase compliance costs.

The Company incurred capital expenditures related to environmental matters of $1.5 million, $0.8 million, and $0.5 million in 2023, 2022, and 2021, respectively. The Company’s recurring costs associated with managing environmental permitting and waste recycling and disposal (e.g., used oil and lubricants) and maintaining pollution control equipment amounted to $0.9 million, $0.4 million, and $0.7 million in 2023, 2022, and 2021, respectively.

Mine Safety. The Company’s mining operations are also subject to regulation under the Federal Mine Safety and Health Act of 1977 (the “Mine Act”). The Mine Act has been construed as authorizing the Mine Safety and Health Administration (“MSHA”) to issue citations and orders pursuant to the legal doctrine of strict liability, or liability without fault. If, in the opinion of an MSHA inspector, a condition that violates the Mine Act or regulations promulgated pursuant to it exists, then a citation or order will be issued regardless of whether the operator had any knowledge of, or fault in, the existence of that condition. Many of the Mine Act standards include one or more subjective elements, so that issuance of a citation or order often depends on the opinions or experience of the MSHA inspector involved and the frequency and severity of citations and orders will vary from inspector to inspector.

Whenever MSHA believes that a violation of the Mine Act, any health or safety standard, or any regulation has occurred, it may issue a citation or order which describes the violation and fixes a time within which the operator must abate the violation. In some situations, such as when MSHA believes that conditions pose a hazard to miners, MSHA may issue an order requiring cessation of operations, or removal of miners from the area of the mine, affected by the condition until the hazards are corrected. Whenever MSHA issues a citation or order, it has authority to propose a civil penalty or fine, as a result of the violation, that the operator is ordered to pay.

Citations and orders can be contested before the Federal Mine Safety and Health Review Commission (the “Commission”), and as part of that process, are often reduced in severity and amount, and are sometimes vacated. The Commission is an independent adjudicative agency that provides administrative trial and appellate review of legal disputes arising under the Mine Act. These cases may involve, among other questions, challenges by operators to citations, orders, and penalties that they have received from MSHA, or complaints of discrimination by miners under section 105 of the Mine Act.

For further information, see Exhibit 95.1 to this Report on Form 10-K.

Reclamation and Remediation. The Company recognizes legal reclamation and remediation obligations associated with the retirement of long-lived assets at their fair value at the time the obligations are incurred (“Asset Retirement Obligations” or “AROs”). Some of the states the Company operates in have reclamation regulations to properly reclaim surface mines. These regulations require permitting with the respective state to ensure reclamation

15

obligations are met. Over time, the liability for AROs is recorded at its present value each period through accretion expense, and the capitalized cost is amortized over the useful life of the related asset. Upon settlement of the liability, the Company either settles the ARO for its recorded amount or recognizes a gain or loss. AROs are estimated based on studies and the Company’s process knowledge and estimates and are discounted using an appropriate interest rate. The AROs are adjusted when further information warrants an adjustment. The Company believes its accrual of $1.5 million for AROs at December 31, 2023 is reasonable.

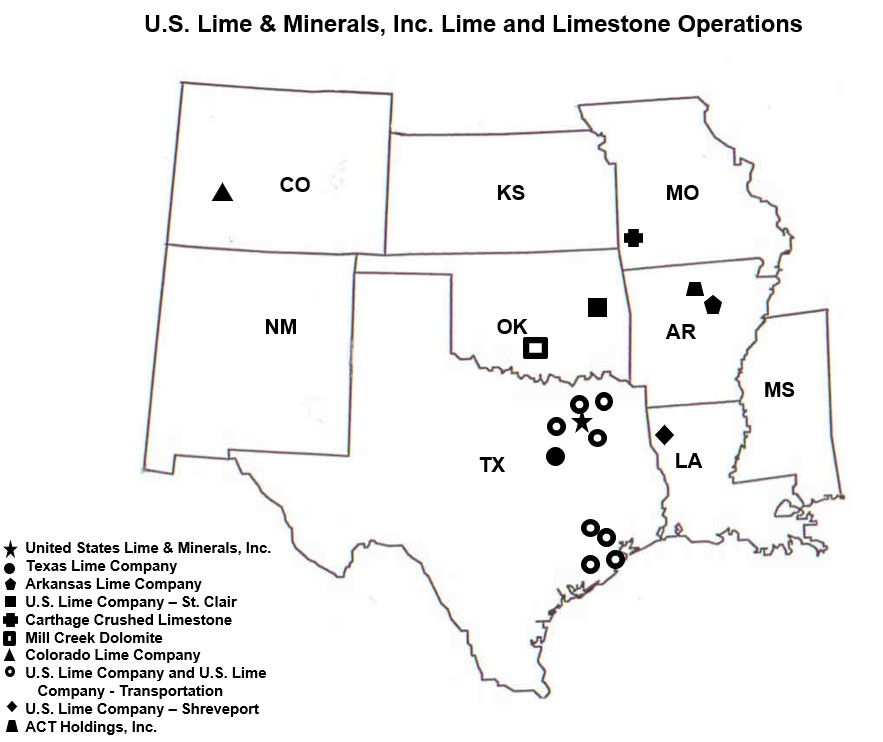

Map of United States Lime & Minerals, Inc. Lime and Limestone Operations.

Other.

The Company’s Other operations, consisting of its natural gas interests, are conducted through its wholly owned subsidiary, U.S. Lime Company – O&G, LLC (“U.S. Lime – O&G”) and consist principally of a lease with respect to oil and gas rights on the Johnson County, Texas property, located in the Barnett Shale Formation. Pursuant to the lease, U.S. Lime – O&G has royalty interests ranging from 15.4% to 20% in oil and gas produced from any successful wells drilled on the leased property and an option to participate in any well drilled on the leased property as a 20% non-operated working interest owner. At December 31, 2023, the overall average interest under the oil and gas rights lease was 34.7% on 33 producing wells.

16

U.S. Lime – O&G has also entered into a drillsite agreement with an operator that has an oil and gas lease covering approximately 538 acres of land contiguous to our Johnson County, Texas property. Pursuant to the drillsite agreement, U.S. Lime – O&G has a 3% royalty interest and a 12.5% non-operated working interest. At December 31, 2023, U.S. Lime – O&G had a combined 12.4% royalty and non-operated working interest on 6 active wells drilled on a padsite located on the Johnson County, Texas property.

No new wells have been completed since 2011, and there are no plans to drill additional wells under either the oil and gas lease or the drillsite agreement. The carrying values of the long-lived assets related to the Company’s natural gas interests were $0.4 million as of December 31, 2023.

ITEM 1A. RISK FACTORS.

Industry Risks

Our Lime and Limestone Operations are affected by general economic conditions in the United States and specific economic conditions in particular industries.

General and industry specific economic conditions in the United States could lead to reduced demand for our lime and limestone products. Specifically, demand from our utility customers has decreased due to the continuing trend in the United States to retire coal-fired utility plants. Our construction, steel, and oil and gas services customers reduce their purchase volumes, at times, due to cyclical economic conditions in their industries. Any overall reduction in demand for lime and limestone products could result in increased competitive pressures, including pricing pressure and competition for certain customer accounts, from other lime producers.

For us to maintain or increase our profitability, we must maintain or increase our revenues and improve cash flows, manage our capital expenditures, and control our operational and selling, general and administrative expenses. If we are unable to maintain our revenues and control our costs in these uncertain economic and regulatory times, our financial condition, results of operations, cash flows, and competitive position could be materially adversely affected.

Our mining and other operations are subject to operating risks that are beyond our control, which could result in materially increased operating expenses and decreased production and shipment levels that could materially adversely affect our Lime and Limestone Operations and their profitability.

We mine limestone in open-pit and underground mining operations and process and distribute that limestone through our plants and other facilities. Certain factors beyond our control could disrupt our operations, adversely affect production and shipments, and increase our operating costs, all of which could have a material adverse effect on our results of operations. These include geological formation problems that may cause poor mining conditions, variability of chemical or physical properties of our limestone, an accident or other major incident at a site that may cause all or part of our operations to cease for some period of time and increase our expenses, mining, processing, and plant equipment failures and unexpected maintenance problems that may cause disruptions and added expenses, strikes, job actions, or other work stoppages that may disrupt our operations or those of our suppliers, contractors, or customers and increase our expenses, and adverse weather conditions and natural disasters, such as hurricanes, tornadoes, excessive rains, flooding, ice storms, freezing weather, drought, and other natural events, that may affect operations, transportation, fuel supply, or customers.

If any of these conditions or events occurs, our operations may be disrupted, we could experience a delay or halt of production or shipments, our operating costs could increase significantly, and we could be exposed to fines, penalties, assessments, and other liabilities. If our insurance coverage is limited or excludes a given condition or event, we may not be able to recover in full the losses that we may incur as a result of such conditions or events, some of which may be substantial.

17

The lime and limestone industry is highly regionalized and competitive.

Our competitors are predominately large private companies. The primary competitive factors in the lime industry are price, quality, ability to meet customer demands and specifications, proximity to customers, personal relationships, and timeliness of deliveries, with varying emphasis on these factors depending upon the specific product application. To the extent that one or more of our competitors becomes more successful with respect to any key competitive factor, we may find it difficult to increase or maintain our prices or to retain certain customer accounts, and our financial condition, results of operations, cash flows, and competitive position could be materially adversely affected.

Business and Financial Risks

In the normal course of our Lime and Limestone Operations, we face various business and financial risks, including increased energy, labor, and parts and supplies costs, that could have a material adverse effect on our financial position, results of operations, cash flows, and competitive position. Not all risks are foreseeable or within our ability to control.

These risks arise from various factors, including, but not limited to, fluctuating demand and prices for our lime and limestone products, including as a result of downturns in the economy and in the construction, industrial, steel, and oil and gas services industries, and reduced demand from coal-fired utility plants, increased competitive pressures from other lime producers, changes in inflationary expectations, changes in legislation and regulations, including Environmental Laws, health and safety regulations, and requirements to renew or obtain operating permits, our ability to produce and store quantities of lime and limestone products sufficient in amount and quality to meet customer demands and specifications, the success of our modernization, expansion and development, and acquisition strategies, the uncertainty of our ability to sell our increased production capacity at acceptable prices, our ability to execute our strategies and complete projects on time and within budget, our ability to integrate, refurbish, and/or improve acquired facilities, our access to capital, volatile costs, especially energy costs, inclement weather and the effects of seasonal trends.

We receive most of our coal and petroleum coke by rail, so the availability of sufficient solid fuels to run our plants could be diminished significantly in the event of major rail disruptions. Domestic coal and petroleum coke may also be exported, which can increase competition and prices for the domestic supply. In addition, our freight costs to deliver our lime and limestone products are high relative to the value of our products, and they have generally increased in recent years. Our costs for delivery of solid fuels, as well as our products, also increase as demand for rail and trucking by other industries increases, and changes to Department of Transportation rules and regulations can reduce the availability of trucks, truck drivers, and rail cars to deliver solid fuels to our plants and deliver our products to our customers. Recent events, such as the ongoing conflicts in Ukraine, Israel, and the broader Middle East, and the sanctions and other actions resulting therefrom, could further increase our energy costs. If we are unable to continue to pass along our increasing energy, labor, and parts and supplies costs to customers through higher prices or surcharges, or unable to timely receive contracted supplies of solid fuel to run our plants, our financial condition, results of operations, cash flows, and competitive position could be materially adversely affected.

We quote our lime and limestone products on a delivered price basis to certain customers, which requires us to estimate future delivery costs. Our actual delivery costs may exceed these estimates, which would reduce our profitability.

Delivery costs are impacted by the price of diesel. When diesel prices increase, we incur additional fuel surcharges from freight companies that cannot be passed on to our customers that have been quoted a delivered price. Material increases in the price of diesel could have a material adverse effect on the Company’s profitability.

18

To maintain our competitive position in the lime and limestone industry, we may need to continue to increase the efficiency of our operations, expand production capacity, and sell any resulting increased production at acceptable prices.

We have in the past, and may in the future, undertake additional modernization and expansion and development projects and acquisitions. Given current and projected demand for lime and limestone products, we cannot guarantee that any such project or acquisition would be successful, that we would be able to sell any resulting increased production at acceptable prices, or that any such sales would be profitable. We are unable to predict future demand and prices, given the current economic and regulatory uncertainties in the United States economy as a whole and in particular industries, and cannot provide any assurance that current levels of demand and prices will continue or that any future increases in demand or prices can be maintained.

We may be limited in our ability to insure against certain risk of our operations.

Mining limestone and producing lime and limestone products involve risks which could result in damage to our facilities, personal injury, and environmental damage. Although we maintain insurance in an amount that we consider adequate, liabilities might exceed policy limits, in which event we could incur significant costs that could adversely affect our financial position, results of operations, cash flows, and competitive position. Additionally, the risks inherent in mining limestone and the production of lime and limestone products may significantly increase the cost of obtaining adequate insurance coverage, or make some coverage unavailable.

We may be adversely affected by any disruption in, or failure of, our information technology systems, including due to cybersecurity risks and incidents.

We rely upon the capacity, reliability, and security of our information technology (“IT”) systems for our mining, manufacturing, sales, financial, and administrative functions. We also face the challenge of supporting our IT systems and implementing upgrades when necessary, including the prompt detection and remediation of any cybersecurity risks or incidents.

Our cybersecurity processes are focused on the prevention, detection, mitigation, and remediation of damage from computer viruses, natural disasters, unauthorized access, cyber-attack, and other cybersecurity risks and threats. However, our cybersecurity processes may not be successful in preventing unauthorized access, intrusion, disclosure, and damage. Risks and threats to our systems can derive from human error, fraud, or malice on the part of employees or third parties, ransomware, or technological failure. Any failure, threat, or incident involving our IT systems could adversely impact our mining and manufacturing operations, sales or financial and administrative functions, or result in the compromise of personal or other confidential information of our employees, customers, or suppliers.

To the extent any such cybersecurity threat or incident results in disruption to our operations or sales or loss or disclosure of, or damage to, our data or confidential information, our costs could increase, and our reputation, business, results of operations, competitive position, and financial condition could be materially adversely affected. Additionally, should we experience a cybersecurity incident, we may incur substantial costs, including remediation costs, such as liability for stolen assets or information, repairs of system damage, legal expenses, and losses and costs associated with regulatory actions.

Our financial condition, results of operations, cash flows, and competitive position could be materially adversely impacted by pandemics, epidemics, or disease outbreaks, such as the COVID-19 pandemic.

Disruptions caused by pandemics, epidemics, or disease outbreaks, such as COVID-19, could materially adversely impact our financial condition, results of operations, cash flows, and competitive position. The COVID-19 pandemic had an impact on our business and operations, particularly as it related to rising costs and supply chain delays and disruptions.

New or future variants of the COVID-19 virus or other pandemics, epidemics, or disease outbreaks and governmental responses to such events could similarly disrupt our business and operations. A pandemic, epidemic, or disease outbreak may limit our ability to produce, sell, and deliver our lime and limestone products to our customers; cause key management and plant-level employees not to be available to us; result in mine and plant shutdowns due to

19

contagion, in which case we may not be able to shift production to our other mines and plants; cause delays and disruptions to our supply chain as it relates to our suppliers, as well as delay and disrupt the supply chains of our customers; impede our ability to maintain and repair our plants and equipment; negatively impact our modernization, expansion, and development plans; negatively impact our ability to integrate acquisitions; as well as adversely impact demand and prices for our lime and limestone products and increase our costs.

Governmental, Legal, and Regulatory Risks

Our Lime and Limestone Operations are subject to general and industry specific regulations. Changes to the regulatory environment could increase our cost of compliance and adversely impact our financial condition, results of operations, cash flows, and competitive position.

We are in a period of economic and regulatory uncertainty, which has been heightened by the current divides in the branches of the United States federal government and the upcoming federal elections. The Administration and Congress may initiate actions to increase regulation of certain industries, including the lime industry, and may take other steps to restrict oil and gas drilling, reduce the use of coal, or regulate domestic manufacturing. There can be no assurance that any of these actions, if adopted, will not increase costs for our customers or increase our cost of compliance with zoning and land use, mine permitting and operating, mine safety, reclamation and remediation, and environmental laws. In addition, a variety of factors, including uncertainty with respect to governmental fiscal and budgetary constraints, including the timing and amount of construction and infrastructure spending, changes to tax laws, legislative impasses, extended government shutdowns, fallout from downgrades and potential U.S. government defaults on its obligations, pandemics, trade wars, tariffs, social unrest, international incidents, and increased inflationary pressures and interest rates, could have a material adverse effect on our financial condition, results of operations, cash flows, and competitive position.

We incur environmental compliance costs and liabilities in our Lime and Limestone Operations, including capital, maintenance, and operating costs, with respect to pollution control equipment, the cost of ongoing monitoring programs, the cost of reclamation and remediation efforts, and other similar costs and liabilities relating to our compliance with Environmental Laws. We expect these costs and liabilities to continue or increase, such as possible new costs, taxes, and limitations on operations, including regulation of greenhouse gas emissions. Similar environmental costs and liabilities may also be faced by some of our customers.

The rate of change of Environmental Laws has been rapid over the last decade, and we may face possible new uncertainties, costs and liabilities, taxes, and limitations on operations, including those related to climate change initiatives. Changes in policy or political leadership may affect how Environmental Laws are interpreted or enforced by the EPA and state governmental agencies. The current Administration has signaled its intent to increase regulation under Environmental Laws and has issued multiple executive orders reversing prior deregulation. We expect our expenditure requirements for future environmental compliance, including complying with nitrogen dioxide, sulfur dioxide, ozone, and particulate matter emission under the NAAQS and regulation of greenhouse gas emissions, to continue or increase. Discovery of currently unknown conditions and unforeseen costs and liabilities could require additional expenditures.

The regulation of greenhouse gas emissions remains an issue for us and some of our customers. In February 2021, the current Administration rejoined the Paris Agreement, under which the United States committed to reduce greenhouse gas emissions. There is no assurance that changes in the law or regulations will not be adopted, such as the imposition of greenhouse gas emission limits, a carbon tax, a cap-and-trade program requiring companies to purchase carbon credits, or other measures that would require reductions in emissions or changes to raw materials, fuel use, or production rates. These changes, if adopted, could have a material adverse effect on our financial condition, results of operations, cash flows and competitive position.

More stringent regulation of greenhouse gas emissions could also adversely affect the competitiveness of some of our customers, including coal-fired power plants, and indirectly the demand for our lime and limestone products. For example, our utility customers are continuing to switch from coal to natural gas or renewable sources for power generation for environmental and regulatory as well as cost reasons, thus reducing demand for our lime and limestone products for flue gas treatment processes.

20

We intend to comply with all Environmental Laws and believe our accrual for environmental costs and liabilities at December 31, 2023 is reasonable. Because many of the requirements are subjective and therefore not quantifiable or presently determinable, or may be affected by additional legislation and rulemaking, including those related to climate change and greenhouse gas emissions, there is no assurance that we will be able to successfully secure new permits in connection with our future modernization and expansion and development projects, and it is not possible to accurately predict the aggregate future costs and liabilities relating to environmental compliance and their effect on our financial condition, results of operations, cash flows, and competitive position.

Our lime and limestone operations are subject to various mine safety and reclamation and remediation obligations.

Our mining operations are subject to mine safety regulation under the Mine Act. The Mine Act has been construed as authorizing MSHA to issue citations and orders pursuant to the legal doctrine of strict liability, or liability without fault. Citations and orders can be contested before the Commission, and as part of that process, are often reduced in severity and amount, and are sometimes vacated.

We also have legal reclamation and remediation obligations associated with the retirement of AROs. Over time, the liability for AROs is recorded at its present value each period through accretion expense, and the capitalized cost is amortized over the useful life of the related asset. Upon settlement of the liability, we either settle the ARO for its recorded amount or recognize a gain or loss. We believe our accrual for AROs is reasonable, but there can be no assurance that any amounts accrued will be sufficient to meet our reclamation and remediation obligations at any point in time.

We intend to comply with all mining regulations and all of our reclamation and remediation obligations. If we fail to comply with such regulations and obligations, such noncompliance may adversely impact our financial condition, results of operations, cash flows, and competitive position.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

ITEM 1C. CYBERSECURITY

Risk Management and Strategy. We have designed and implemented processes to assess, identify, manage, detect, and respond to material cybersecurity risks and threats to our IT systems, including the prevention, detection, mitigation, and remediation of cybersecurity incidents in order to protect the confidentiality, integrity, and availability of our IT systems and the information residing on those systems. These processes are part of our overall risk management process and are embedded in our operating policies, procedures, and controls.

To protect our IT systems and information from cybersecurity risks, we use various security tools that help prevent, identify, escalate, investigate, resolve, and recover from identified cybersecurity vulnerabilities and incidents in a timely manner. These include, but are not limited to, internal reporting, monitoring, and detection tools. We also utilize a third-party security operations center connected to a networks operation center to identify, investigate, and resolve any cybersecurity threats and incidents.

We regularly assess technological risks to our IT systems and information and monitor our IT systems for potential vulnerabilities and risks. We frequently conduct mandatory cybersecurity and IT systems awareness training for all employees with access to our systems. We also conduct regular reviews and tests of our IT cybersecurity processes, including reviews, assessments, and exercises.

We aim to incorporate responsible practices throughout our cybersecurity risk management processes. Our cybersecurity strategy focuses on implementing effective and efficient controls, technologies, and other processes to assess, identify, and manage material cybersecurity risks to our IT systems and information. As a part of this process, we engage independent third-party specialists to review our cybersecurity environment, including formal reviews and assessments, and we request specific, actionable recommendations for improvement.

21

While we have not, as of the date of this Report on Form 10-K, experienced a cybersecurity threat or incident that has materially impacted our business or operations, there can be no guarantee that we will not experience such a threat or incident in the future. A material cybersecurity threat or incident could adversely impact our mining and manufacturing operations, our sales or financial and administrative functions, or result in the compromise of personal or other confidential information of our employees, customers, or suppliers. For this reason, we maintain cybersecurity liability insurance to provide additional support, expertise, and resources to help ensure the integrity of our cybersecurity processes through regular reviews and assessments, to provide incident response assistance and expertise, and to provide a level of financial protection in the event of cybersecurity incident related costs and losses. See "Risk Factors - We may be adversely affected by any disruption in, or failure of, our information technology systems, including due to cybersecurity risks and incidents.”