Exhibit 13

Annual Report to Stockholders

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

The following tables provide selected consolidated financial and operating data of Security Federal Corporation at and for the years indicated. In conjunction with the data provided in the following tables and in order to more fully understand our historical consolidated financial and operating data, you should also read our “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Consolidated Financial Statements and the accompanying notes included in this report.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | At and For the Year Ended December 31, |

| | 2022 | | 2021 | | 2020 | | 2019 | | 2018 |

| Balance Sheet Data at End of Period | (Dollars in Thousands, Except Per Share Data) |

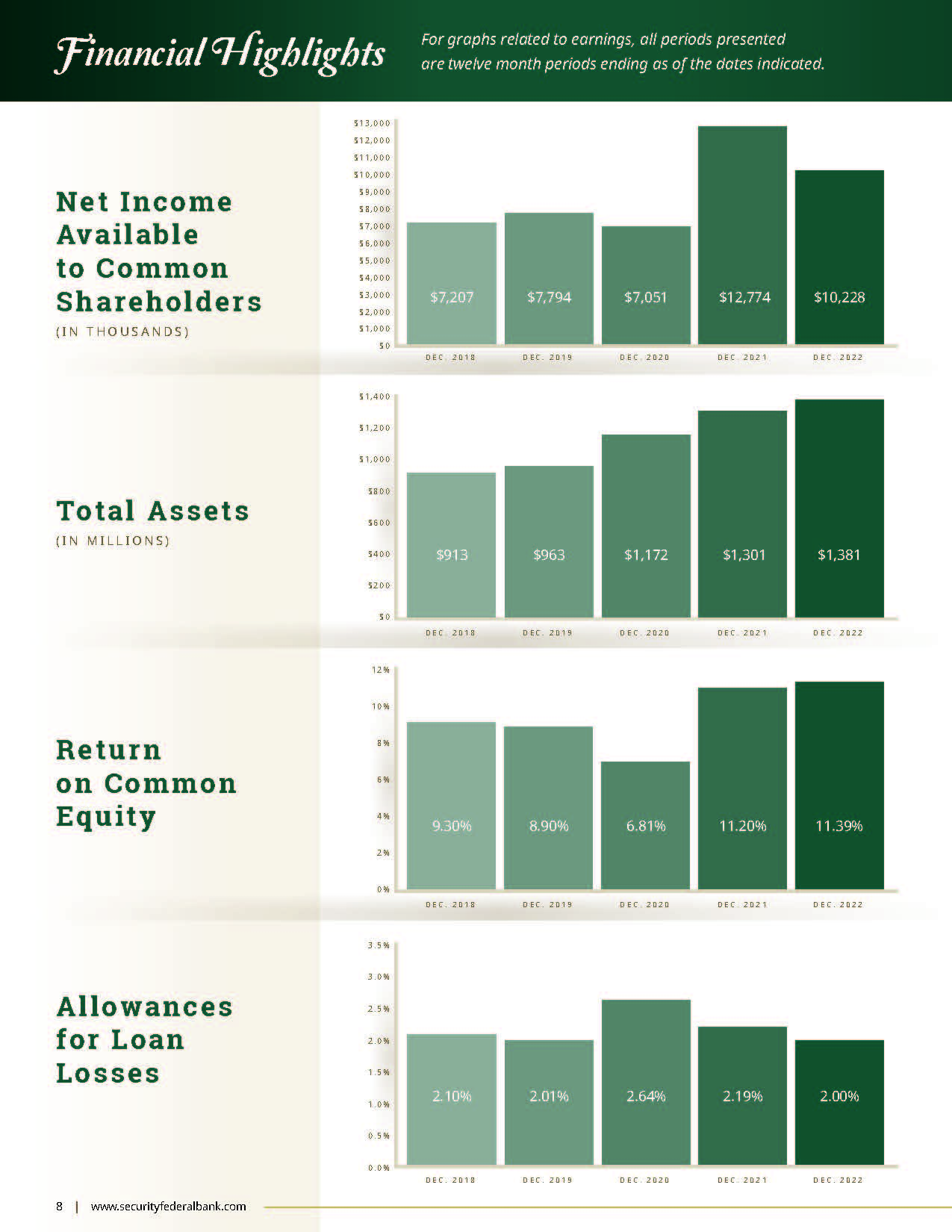

| Total Assets | $ | 1,381,366 | | $ | 1,301,214 | | $ | 1,171,710 | | $ | 963,228 | | $ | 912,614 |

| Cash and Cash Equivalents | 28,502 | | 27,623 | | 18,025 | | 12,536 | | 12,706 |

| Certificates of Deposit with Other Banks | 1,100 | | 1,100 | | 350 | | 950 | | 1,200 |

| Investment Securities | 717,586 | | 706,356 | | 607,579 | | 433,892 | | 409,894 |

Total Loans Receivable, Net (1) | 549,917 | | 499,497 | | 479,167 | | 452,859 | | 430,054 |

| Deposits | 1,110,085 | | 1,115,963 | | 918,096 | | 771,407 | | 767,497 |

| Advances From Federal Home Loan Bank ("FHLB") | — | | — | | 35,000 | | 38,138 | | 34,030 |

| Borrowings from Federal Reserve Bank ("FRB") | 44,080 | | — | | 48,700 | | — | | — |

| Total Shareholders' Equity | 160,233 | | 115,523 | | 111,906 | | 91,758 | | 80,518 |

| Common Shareholders' Equity | 77,284 | | 115,523 | | 111,906 | | 91,758 | | 80,518 |

| | | | | | | | | |

| Income Data | | | | | | | | | |

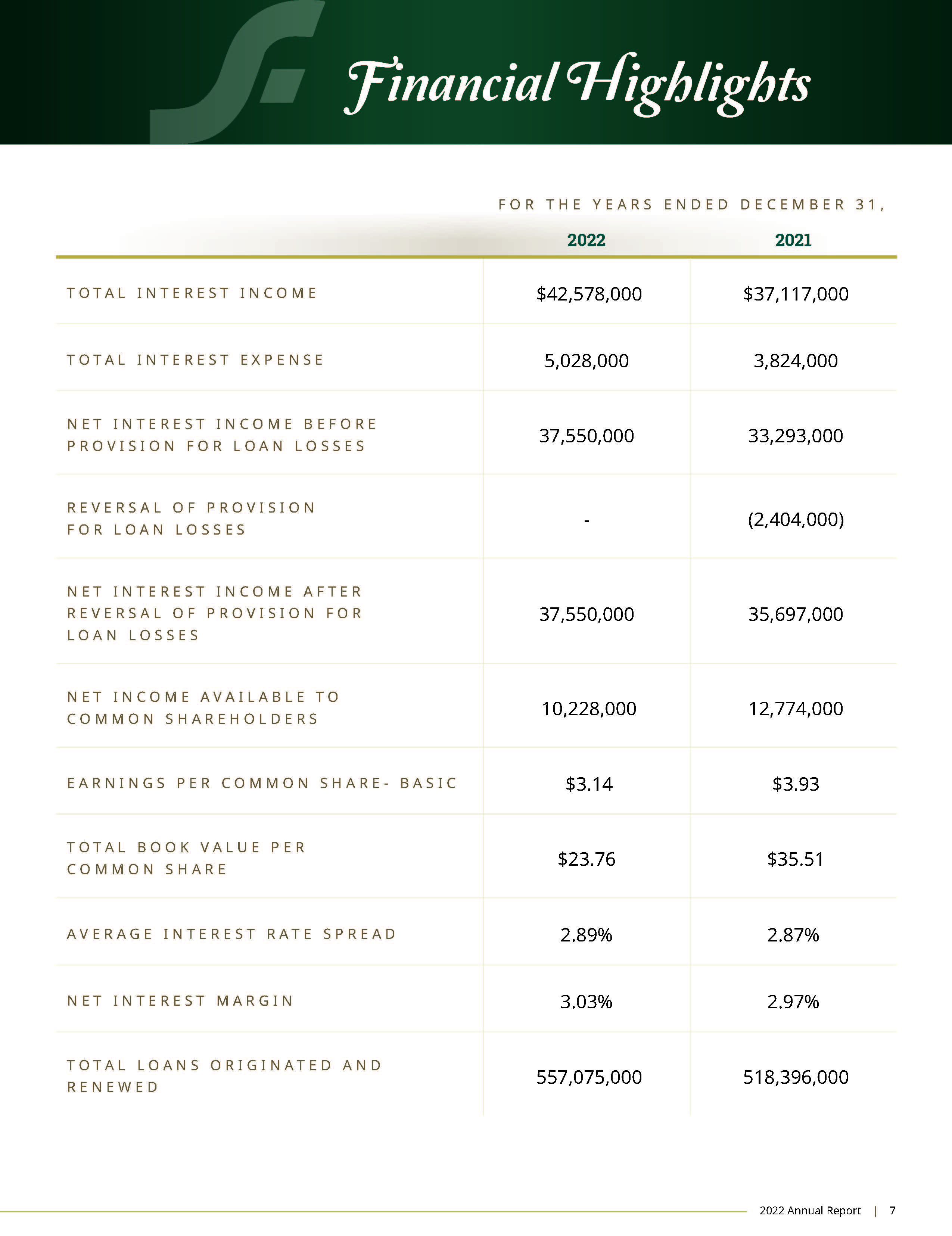

| Total Interest Income | $ | 42,578 | | $ | 37,117 | | $ | 37,096 | | $ | 36,934 | | $ | 33,072 |

| Total Interest Expense | 5,028 | | 3,824 | | 6,581 | | 8,311 | | 5,449 |

| Net Interest Income | 37,550 | | 33,293 | | 30,515 | | 28,623 | | 27,623 |

| (Reversal of) Provision for Loan Losses | — | | (2,404) | | 3,600 | | 375 | | 925 |

| Net Interest Income After (Reversal of) Provision for Loan Losses | 37,550 | | 35,697 | | 26,915 | | 28,248 | | 26,698 |

| Non-Interest Income | 9,612 | | 12,633 | | 11,421 | | 9,097 | | 7,669 |

| Non-Interest Expense | 34,225 | | 32,047 | | 29,708 | | 27,871 | | 25,590 |

| Income Taxes | 2,709 | | 3,509 | | 1,577 | | 1,680 | | 1,570 |

| Net Income | $ | 10,228 | | $ | 12,774 | | $ | 7,051 | | $ | 7,794 | | $ | 7,207 |

| | | | | | | | | |

| Per Common Share Data | | | | | | | | | |

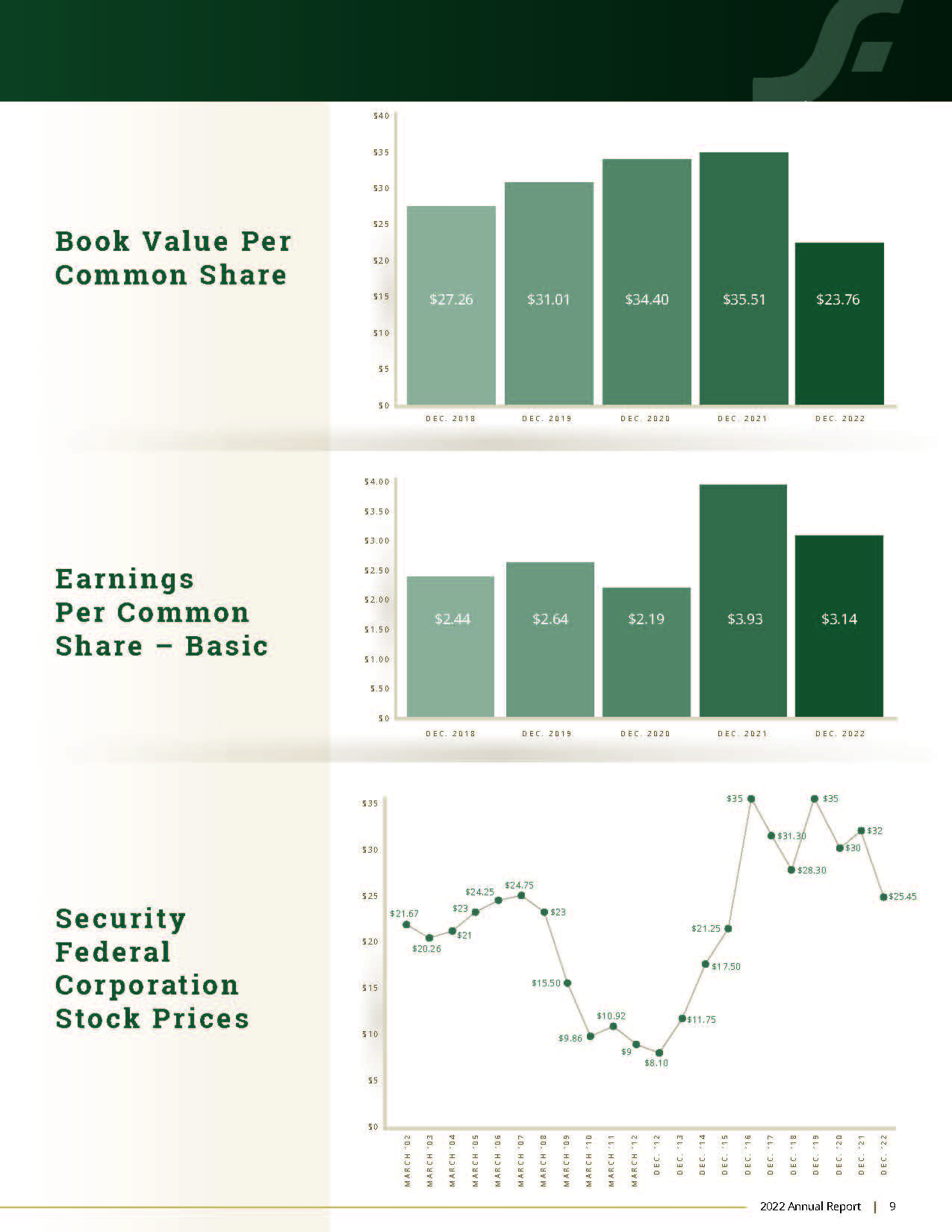

| Net Income Per Common Share (Basic) | $ | 3.14 | | $ | 3.93 | | $ | 2.19 | | $ | 2.64 | | $ | 2.44 |

| Cash Dividends Per Share | $ | 0.76 | | $ | 0.44 | | $ | 0.40 | | $ | 0.40 | | $ | 0.36 |

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Selected Consolidated Financial and Other Data

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2022 | | 2021 | | 2020 | | 2019 | | 2018 |

| Other Data | | | | | | | | | |

| | | | | | | | | |

| Average Interest Rate Spread | 2.89 | % | | 2.87 | % | | 2.91 | % | | 3.10 | % | | 3.27 | % |

| | | | | | | | | |

| Net Interest Margin (Net Interest Income / Average Earning Assets) | 3.03 | % | | 2.97 | % | | 3.04 | % | | 3.26 | % | | 3.38 | % |

| Average Interest-Earning Assets to Average Interest-Bearing Liabilities | 134.63 | % | | 128.62 | % | | 120.99 | % | | 116.83 | % | | 116.01 | % |

| Common Equity to Total Assets | 5.59 | % | | 8.88 | % | | 9.55 | % | | 9.53 | % | | 8.82 | % |

Non-Performing Assets to Total Assets (2) | 0.46 | % | | 0.22 | % | | 0.31 | % | | 0.43 | % | | 0.85 | % |

| Return on Assets | 0.75 | % | | 1.04 | % | | 0.63 | % | | 0.80 | % | | 0.81 | % |

| Return on Common Equity | 11.39 | % | | 11.20 | % | | 6.81 | % | | 8.90 | % | | 9.30 | % |

| Average Common Equity to Average Assets Ratio | 6.63 | % | | 9.27 | % | | 9.32 | % | | 9.05 | % | | 8.69 | % |

Dividend Payout Ratio on Common Shares(3) | 24.17 | % | | 11.20 | % | | 18.46 | % | | 14.41 | % | | 14.76 | % |

| Number of Full-Service Offices | 18 | | | 17 | | | 17 | | | 17 | | | 16 | |

(1) INCLUDES LOANS HELD FOR SALE

(2) NON-PERFORMING ASSETS CONSIST OF NON-ACCRUAL LOANS AND OTHER REAL ESTATE OWNED ("OREO")

(3) RATIO OF DIVIDENDS PAID ON COMMON SHARES TO NET INCOME AVAILABLE TO COMMON SHAREHOLDERS

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

General

The following discussion and analysis is presented to provide the reader with an understanding of the financial condition and the results of operations of Security Federal Corporation and its subsidiaries. The investment and other activities of the parent company, Security Federal Corporation (the “Company”), have had no significant impact on the results of operations for the periods presented in the Consolidated Financial Statements included herein. Because we conduct all of our material business operations through Security Federal Bank (the "Bank"), a wholly owned subsidiary of the Company, the following discussion of financial results are primarily indicative of the activities of the Bank. The Bank was founded in 1922 as a mutual building and loan association. In 1987, the Bank converted to a federally chartered stock savings bank. On December 28, 2011, the Bank completed a charter conversion from a federally chartered stock savings bank to a South Carolina chartered commercial bank. In connection with this transaction, the Company reorganized from a savings and loan holding company into a bank holding company.

The Bank has three wholly owned subsidiaries: Security Federal Investments, Inc. ("SFINV"), Security Federal Insurance, Inc. (“SFINS”) and Security Financial Services Corporation (“SFSC”). SFINV was formed to hold investment securities and allow for better management of the securities portfolio. SFINS is an insurance agency offering auto, business, and home insurance. Effective April 30, 2022, Collier Jennings Financial Corporation, a wholly owned subsidiary of SFINS, and its subsidiaries, Security Federal Auto Insurance, The Auto Insurance Store Inc., and Security Federal Premium Pay Plans Inc. ("SFPPP") and its wholly owned premium finance subsidiary were dissolved. SFPPP’s ownership interests in four other premium finance subsidiaries were disposed of at an immaterial gain. Additionally, effective April 30, 2022, previously inactive SFSC was dissolved.

In addition to the Bank, the Company has another wholly owned subsidiary, Security Federal Statutory Trust (the “Trust”), which issued and sold fixed and floating rate capital securities of the Trust. Under current accounting guidance, however, the Trust is not consolidated in the Company’s financial statements. Unless the context indicates otherwise, references to the "Company," "we," "us," and "our" shall include Security Federal Corporation, the Bank and the Bank's subsidiaries.

The principal business of the Bank is accepting deposits from the general public and originating consumer and commercial business loans as well as mortgage loans that enable borrowers to purchase or refinance one-to-four family residential real estate. The Bank also originates construction loans on single-family residences, multi-family dwellings, and commercial real estate, as well as loans for the acquisition, development and construction of residential subdivisions, and commercial projects. The Bank also provides trust services and it offers property and casualty insurance products through its subsidiary, SFINS.

The Bank's net income depends primarily on its interest rate spread which is the difference between the average yield earned on its loan and investment portfolios and the average rate paid on its deposits and borrowings. When the rate earned on interest-earning assets equals or exceeds the rate paid on interest-bearing liabilities, this positive interest rate spread will generate net interest income. The Bank’s interest spread is influenced by interest rates, deposit flows, and loan demands. Levels of non-interest income and operating expense are also significant factors in earnings.

Forward-Looking Statements

This document, including information incorporated by reference herein, may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements relate to our financial condition, results of operations, plans, objectives, future performance or business. Forward-looking statements are not statements of historical fact, are based on certain assumptions and are generally identified by use of the words "believes," "expects," "anticipates," "estimates," "forecasts," "intends," "plans," "targets," "potentially," "probably," "projects," "outlook" or similar expressions or future or conditional verbs such as "may," "will," "should," "would" and "could." Forward-looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, assumptions and statements about, among other things, expectations of the business environment in which we operate, projections of future performance or financial items, perceived opportunities in the market, potential future credit experience, and statements regarding our mission and vision. These forward-looking statements are based upon current management expectations and may, therefore, involve risk and uncertainties.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Our actual results, performance, or achievements may differ materially from those suggested, expressed, or implied by forward-looking statements as a result of a wide variety or range of factors, including, but not limited to:

•potential adverse impacts to economic conditions in our local market areas, other markets where the Company has lending relationships, or other aspects of the Company's business operations or financial markets, generally, resulting from the ongoing novel coronavirus of 2019 (“COVID-19”) and any governmental or societal responses thereto;

•the credit risks of lending activities, including changes in the level and trend of loan delinquencies and write-offs and changes in our allowance for loan losses and provision for loan losses that may be affected by deterioration in the housing and commercial real estate markets which may lead to increased losses and non-performing assets in our loan portfolio, and may result in our allowance for loan losses not being adequate to cover actual losses, and require us to materially increase our allowance for loan losses;

•changes in general economic conditions, either nationally or in our market areas;

•changes in the levels of general interest rates, and the relative differences between short and long term interest rates, deposit interest rates, our net interest margin and funding sources;

•the transition away from London Interbank Offered Rate ("LIBOR") toward new interest rate benchmarks;

•fluctuations in the demand for loans, the number of unsold homes, land and other properties and fluctuations in real estate values in our market areas;

•secondary market conditions for loans and our ability to originate and sell loans in the secondary market;

•results of examinations of the Company by the Board of Governors of the Federal Reserve System ("Federal Reserve") and the Bank by the Federal Deposit Insurance Corporation ("FDIC") and the South Carolina State Board of Financial Institutions, or other regulatory authorities, including the possibility that any such regulatory authority may, among other things, require us to increase our reserve for loan losses, write-down assets, change our regulatory capital position or affect our ability to borrow funds or maintain or increase deposits, or impose additional requirements or restrictions on us, any of which could adversely affect our liquidity and earnings;

•legislative or regulatory changes that adversely affect our business, including changes in banking, securities and tax law, and in regulatory policies and principles, or the interpretation of regulatory capital or other rules, and including changes as a result of COVID-19;

•our ability to attract and retain deposits;

•our ability to control operating costs and expenses;

•our ability to implement our business strategies;

•the use of estimates in determining the fair value of certain of our assets, which estimates may prove to be incorrect and result in significant declines in valuation;

•difficulties in reducing risks associated with the loans on our balance sheet;

•staffing fluctuations in response to product demand or the implementation of corporate strategies that affect our workforce and potential associated charges;

•disruptions, security breaches, or other adverse events, failures or interruptions in, or attacks on, our information technology systems or on the third-party vendors who perform several of our critical processing;

•our ability to retain key members of our senior management team;

•costs and effects of litigation, including settlements and judgments;

•our ability to manage loan delinquency rates;

•increased competitive pressures among financial services companies;

•changes in consumer spending, borrowing and savings habits;

•the availability of resources to address changes in laws, rules, or regulations or to respond to regulatory actions;

•our ability to pay dividends on our common stock;

•adverse changes in the securities markets;

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

•inability of key third-party providers to perform their obligations to us;

•changes in accounting policies and practices, as may be adopted by the financial institution regulatory agencies or the Financial Accounting Standards Board ("FASB"), including additional guidance and interpretation on accounting issues and details of the implementation of new accounting methods;

•other economic, competitive, governmental, regulatory, and technological factors affecting our operations, pricing, products and services; and

•the other risks described elsewhere in this annual report to shareholders and in the Company's other filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2022 ("2022 Form 10-K").

Some of these and other factors are discussed in the 2022 Form 10-K under Item 1A, “Risk Factors.” Such developments could have an adverse impact on our financial condition and results of operations.

Any of the forward-looking statements that we make may turn out to be inaccurate as a result of our beliefs and assumptions we make in connection with the factors set forth above or because of other unidentified and unpredictable factors. Because of these and other uncertainties, our actual future results may be materially different from the results indicated by these forward-looking statements and you should not rely on such statements. The Company undertakes no obligation to publish revised forward-looking statements to reflect the occurrence of unanticipated events or circumstances after the date hereof. These risks could cause our actual results for 2023 and beyond to differ materially from those expressed in any forward-looking statements by or on behalf of us, and could negatively affect the Company’s consolidated financial condition and consolidated results of operations, liquidity and stock price performance.

Critical Accounting Estimates

We prepare our consolidated financial statements in accordance with GAAP. In doing so, we have to make estimates and assumptions. Our critical accounting estimates are those estimates that involve a significant level of uncertainty at the time the estimate was made, and changes in the estimate that are reasonably likely to occur from period to period, or use of different estimates that we reasonably could have used in the current period, would have a material impact on our financial condition or results of operations. Accordingly, actual results could differ materially from our estimates. We base our estimates on past experience and other assumptions that we believe are reasonable under the circumstances, and we evaluate these estimates on an ongoing basis. We have reviewed our critical accounting estimates with the audit committee of our Board of Directors.

The significant accounting policies of the Company are described in Note 1 of the Notes to the Consolidated Financial Statements included herein.

The Company believes the allowance for loan losses is a critical accounting policy that requires the most significant judgments, estimates and assumptions used in preparation of the Consolidated Financial Statements. The impact of an unexpected large loss could deplete the allowance and potentially require increased provisions to replenish the allowance, which would negatively affect earnings. The Company provides for loan losses using the allowance method. Accordingly, all loan losses are charged to the related allowance and all recoveries are credited to the allowance for loan losses. Additions to the allowance for loan losses are provided by charges to operations based on various factors, which, in management’s judgment, deserve current recognition in estimating possible losses. Such factors considered by management include the fair value of the underlying collateral, stated guarantees by the borrower (if applicable), the borrower’s ability to repay from other economic resources, growth and composition of the loan portfolio, the relationship of the allowance for loan losses to the outstanding loans, loss experience, delinquency trends, and general economic conditions. Management evaluates the carrying value of the loan portfolio monthly and adjusts the allowance accordingly. While management uses the best information available to make evaluations, future adjustments may be necessary if economic conditions differ substantially from the assumptions used in making these evaluations. The allowance for loan losses is subject to periodic evaluations by bank regulatory agencies that may require adjustments to the allowance based upon the information that is available at the time of their examination. For a further discussion of the Company’s estimation process and methodology related to the allowance for loan losses, see the discussion under the section entitled “Financial Condition” and “Comparison of the Years Ended December 31, 2022 and 2021-Provision for Loan Losses” included herein.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

The Company values an impaired loan at the loan’s fair value if it is probable that the Company will be unable to collect all amounts due according to the contractual terms of the original loan agreement. Impaired loans are measured at the present value of expected cash flows, the market price of the loan, if available, or the value of the underlying collateral. Expected cash flows are required to be discounted at the loan’s effective interest rate. When the ultimate collectability of an impaired loan’s principal is in doubt, wholly or partially, all payments received are applied to principal. Once the recorded principal balance has been reduced to zero, any additional payments received are applied to interest income to the extent that any interest has been foregone. Any additional payments received are recorded as recoveries of any amounts previously charged off. When the repayment of the loan is not in doubt, payments are applied under the contractual terms of the loan agreement first to interest and then to principal.

The Company uses assumptions and estimates in determining income taxes payable or refundable for the current year, deferred income tax liabilities and assets for events recognized differently in its financial statements and income tax returns, and income tax expense. Determining these amounts requires analysis of certain transactions and interpretation of tax laws and regulations.

The Company exercises considerable judgment in evaluating the amount and timing of recognition of the resulting tax liabilities and assets. These judgments and estimates are reevaluated on a continual basis as regulatory and business factors change.

No assurance can be given that either the tax returns submitted by the Company or the income tax reported on the Consolidated Financial Statements will not be adjusted by either adverse rulings by the United States Tax Court, changes in the tax code, or assessments made by the Internal Revenue Service.

Asset and Liability Management

The objective of the Bank’s program of asset and liability management is to limit the Bank’s vulnerability to material and prolonged increases or decreases in interest rates, or "interest rate risk." As a financial institution, interest rate risk is the Bank's most significant market risk. The earnings and economic value of our shareholders’ equity varies in relation to changes in interest rates and the corresponding impact on the market values of our assets and liabilities. The Bank has an Asset Liability Management Committee (“ALCO”) who monitors the Bank’s asset liability strategy.

The asset/liability management process is designed to achieve relatively stable net interest margins and assure liquidity by coordinating the volumes, maturities or re-pricing opportunities of interest-earning assets, deposits and borrowed funds. It is the responsibility of the ALCO to determine and achieve the most appropriate volume and mix of interest-earning assets and interest-bearing liabilities, as well as ensure an adequate level of liquidity and capital, within the context of corporate performance goals. The ALCO meets regularly to review interest rate risk and liquidity in relation to present and potential market conditions and evaluate funding and balance sheet management strategies to ensure the level of risk is consistent with our asset/liability objectives.

Simulation is the principal tool used by the Bank in its ongoing effort to measure interest rate risk. Simulation involves the use of a financial modeling system that provides reports showing the current and future impact of changes in interest rates and our strategies and tactics. The Bank uses two dynamic methods: net interest income (“NII”) simulation and economic value of equity (“EVE”) analysis. The NII simulation models the impact that changes in interest rates will have on our earnings while EVE analysis models the impact those changes will have on the net present value of our asset and liability portfolios. These models take into account our contractual agreements with regard to investments, loans, deposits and borrowings, and also include assumptions surrounding market and customer behavior under different rate scenarios. The assumptions we use are based upon a combination of proprietary and market data that reflect historical results and current market conditions. These assumptions relate to interest rates, prepayments, deposit decay rates and the market value of certain assets and liabilities under the various interest rate scenarios. We use market data to determine prepayments and maturities of loans, investments and borrowings and use our own assumptions on deposit decay rates except for time deposits. Time deposits are modeled to reprice to market rates upon their stated maturities. We also assume that non-maturity deposits can be maintained with rate adjustments not directly proportionate to the change in market interest rates, based upon our historical deposit rates. We have demonstrated in the past that the tiering structure of our deposit accounts during changing rate environments results in relatively lower volatility and less than market rate changes in our interest expense for deposits. These assumptions are based upon our analysis of our customer base, competitive factors and historical experience.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

While these models are dependent on the accuracy of the assumptions that underlie the process, we believe that such modeling provides a better illustration of our sensitivity to interest rate risk than does a traditional static gap analysis. These tools provide our ALCO with the capability to estimate and manage the amount of earnings at risk in future periods and in selected interest rate risk environments.

NII Simulation- The Bank’s primary focus is on NII simulation. Using NII simulation, the Bank measures earnings exposure over both a 12 and 24 month period under multiple instantaneous rate shock scenarios. The Bank’s policy provides the maximum acceptable negative impact on net interest income and return on assets ("ROA") over each time horizon associated with each respective change in interest rates. Our ALCO monitors compliance with these policy limits and reports them to the Board of Directors quarterly.

The following table indicates the NII simulation scenarios modeled and the applicable policy parameters.

| | | | | | | | | | | | | | | | | | | | |

| Change in Market Rates | | Maximum Allowable Change in NII Over | | Maximum Allowable Change in ROA Over |

| (in Basis Points) | | 12 Months | 24 Months | | 12 Months | 24 Months |

| 400 | | (20)% | (20)% | | (40)% | (40)% |

| 300 | | (15)% | (15)% | | (30)% | (30)% |

| 200 | | (10)% | (10)% | | (20)% | (20)% |

| 100 | | (7.5)% | (7.5)% | | (10)% | (10)% |

| — | | —% | —% | | —% | —% |

| (100) | | (7.5)% | (7.5)% | | (10)% | (10)% |

| (200) | | (10)% | (10)% | | (20)% | (20)% |

| (300) | | (15)% | (15)% | | (30)% | (30)% |

| (400) | | (20)% | (20)% | | (40)% | (40)% |

The Bank performs a liquidity analysis, a component of managing liquidity risk and monitoring the Bank's asset liability strategy. This analysis compares outstanding sources of liquidity to applicable policy parameters. The Bank was in compliance with policy parameters as of December 31, 2022 and 2021. In addition, the Bank performs a Contingency Funding plan analysis which incorporates various simulations in order to evaluate Bank's funding resources under stressed conditions. Both the liquidity and Contingency Funding plan analysis are performed by the Bank's ALCO and presented to the Board of Directors quarterly.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

EVE simulation- The EVE analysis serves as an indicator of the extent to which the present value of our capital could change, given potential changes in interest rates. The difference represented by the present value of assets minus the present value of liabilities is defined as the economic value of equity. This measure assumes a static balance sheet and does not incorporate any growth assumptions, but does assume loan prepayments and certain other cash flows occur. It provides a measure of rate risk extending beyond the 12 or 24 month time horizon contained in the NII simulation analyses.

While an instantaneous and severe shift in interest rates is used in this analysis to provide an estimate of exposure under an extremely adverse scenario, a gradual shift in interest rates would have a much more modest impact. Since EVE measures the discounted present value of cash flows over the estimated lives of instruments, the change in EVE does not directly correlate to the degree that earnings would be impacted over a shorter time horizon, i.e., the next fiscal year. Further, EVE does not take into account factors such as future balance sheet growth, changes in product mix, change in yield curve relationships, and changing product spreads that could mitigate the adverse impact of changes in interest rates.

The following table indicates the EVE simulation scenarios modeled and the applicable policy parameters.

| | | | | | | | |

| Change in Market Rates (In Basis Points) | | Maximum Change in Economic Value of Equity |

| 400 | | (40)% |

| 300 | | (30)% |

| 200 | | (20)% |

| 100 | | (10)% |

| — | | —% |

| (100) | | (10)% |

| (200) | | (20)% |

| (300) | | (30)% |

| (400) | | (40)% |

In evaluating the Bank's exposure to interest rate risk, certain shortcomings inherent in the method of analysis described above are considered. No assurance can be given that changing economic conditions and other relevant factors impacting our net interest income will not cause actual occurrences to differ from underlying assumptions. For example, loan repayment rates and withdrawals of deposits will likely differ substantially from the assumptions used in the simulation models in the event of significant changes in interest rates due to the option of borrowers to prepay their loans and the ability of depositors to withdraw funds prior to maturity. In addition, this analysis does not consider any strategic changes to our balance sheet which management may consider as a result of changes in market conditions.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition - Assets

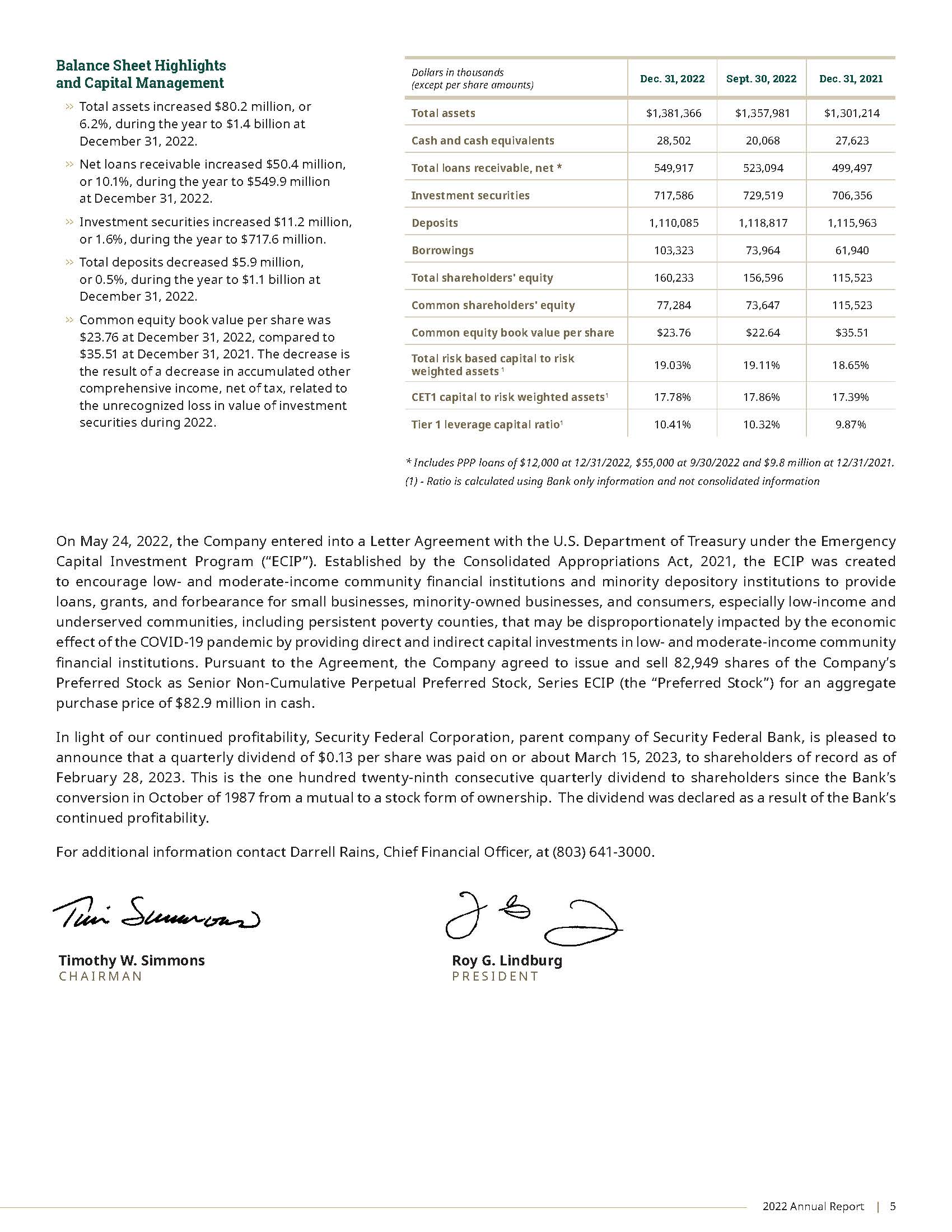

Total assets increased $80.2 million or 6.2% to $1.4 billion at December 31, 2022 from $1.3 billion at December 31, 2021. This increase was primarily due to increases in held to maturity ("HTM") investment securities, net loans receivable and, to a lesser extent other assets, partially offset by a decrease in available for sale ("AFS") investment securities.

Cash and cash equivalents increased $879,000 or 3.2% to $28.5 million at December 31, 2022 compared to $27.6 million at December 31, 2021. Total investment securities increased $11.2 million or 1.6% to $717.6 million at December 31, 2022 from $706.4 million at December 31, 2021 as purchases of investments exceeded maturities, sales and principal paydowns during the year. The Company purchased $210.3 million of investment securities during the year ended December 31, 2022 compared to $217.6 million during the prior year and sold $22.4 million of AFS investment securities during the year ended December 31, 2022 compared to no sales during 2021.

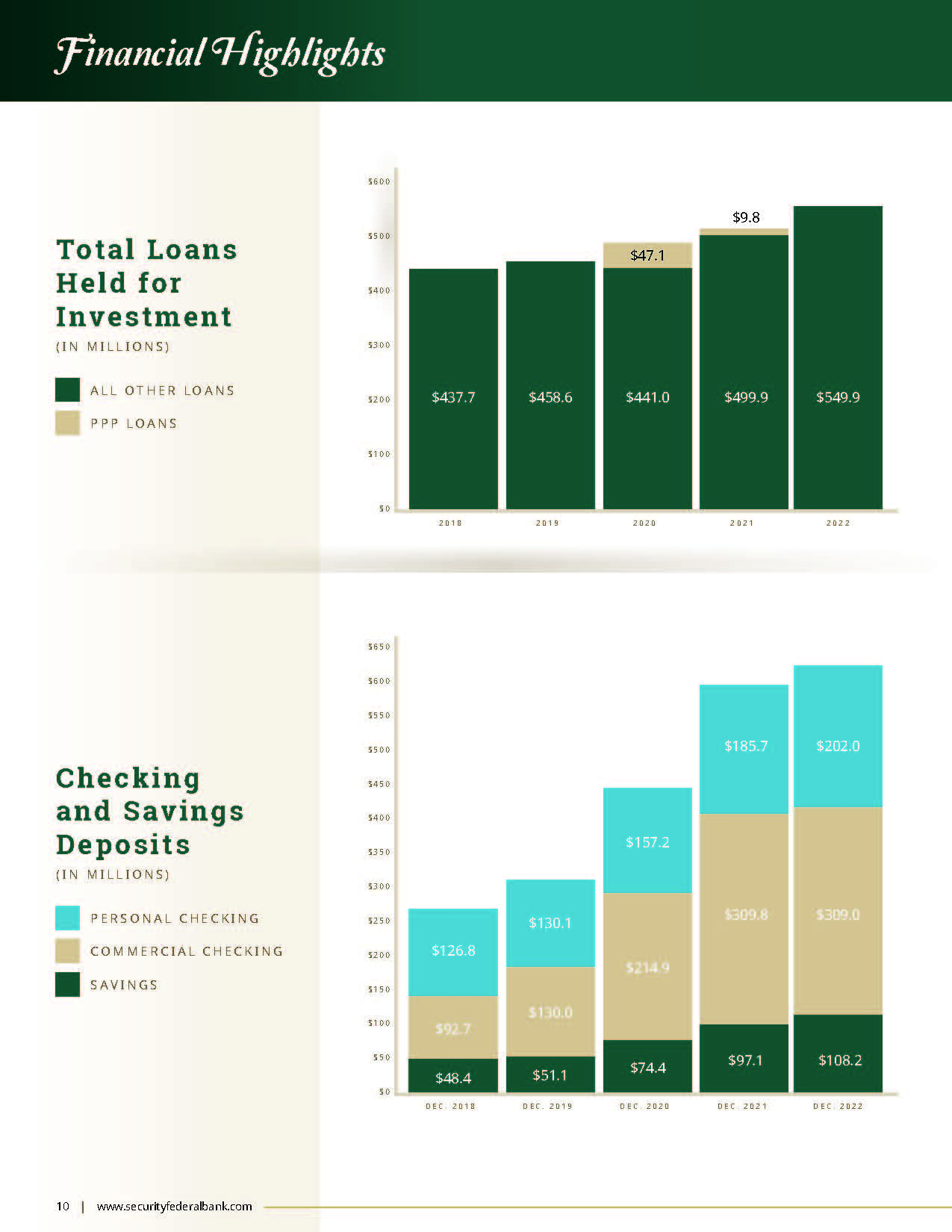

Loans receivable, net, including loans held for sale, increased $50.4 million or 10.1% to $549.9 million at December 31, 2022 from $499.5 million at December 31, 2021 primarily due to increases in construction, residential mortgage and commercial real estate loans. In addition, home equity lines of credit ("HELOCs") and other consumer loans also increased while commercial and agricultural loans decreased during 2022 compared to 2021.

Construction loans increased $12.6 million or 12.6% to $112.8 million at December 31, 2022 from $100.2 million at December 31, 2021. Residential mortgage loans held for investment increased $25.1 million or 29.5% to $110.1 million at December 31, 2022 from $85.0 million at December 31, 2021. Commercial real estate loans increased $24.4 million or 10.7% to $252.2 million at December 31, 2022 from $227.8 million at December 31, 2021.

Commercial and agricultural loans decreased $14.1 million or 31.4% to $30.6 million at December 31, 2022 from $44.7 million at December 31, 2021.

HELOCs increased $3.1 million or 10.9% to $31.7 million at December 31, 2022 from $28.6 million at December 31, 2021. Other consumer loans increased $2.2 million or 10.0% to $23.6 million at December 31, 2022 from $21.4 million at December 31, 2021.

Loans held for sale, comprised of fixed rate residential loans, decreased $3.1 million or 77.4% to $913,000 at December 31, 2022 from $4.0 million at December 31, 2021. Typically, long term, newly originated fixed rate residential real estate loans are not retained in the portfolio but are sold immediately in contrast to adjustable rate mortgage ("ARM") loans, which are generally retained in the portfolio. The Bank sells all its fixed rate residential loans on a service-released basis. Fixed rate residential loans sold to institutional investors, on a service-released basis totaled $48.5 million during the year ended December 31, 2022, $112.9 million during the year ended December 31, 2021 and $111.1 million during the year ended December 31, 2020.

Property and equipment, net increased $2.8 million or 10.8% to $28.0 million at December 31, 2022 from $25.2 million at December 31, 2021 due to capital costs related to branch improvements and construction of the Bank's newest branch.

Other assets increased $14.0 million or 267.2% to $19.2 million at December 31, 2022 from $5.2 million at December 31, 2021. The increase was primarily the result of a $14.6 million increase in net deferred taxes, which was related to increased unrealized losses in the AFS investment securities.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition - Non-Performing Assets

The Bank’s non-performing assets, which consist of non-accrual loans and OREO, increased $3.6 million or 127.3% to $6.4 million at December 31, 2022 from $2.8 million at December 31, 2021. Non-performing assets represented 0.5% and 0.2% of total assets at December 31, 2022 and 2021, respectively.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | At December 31, 2022 | | At December 31, 2021 | | $ | | % |

| (Dollars in thousands) | Amount | | Percent (1) | | Amount | | Percent (1) | | Change | | Change |

| Non-Performing Loans: | | | | | | | | | | | |

| Construction | $ | 115 | | 0.02 | % | | $ | 21 | | — | % | | $ | 94 | | | 447.6 | % |

| Residential Mortgage | 1,545 | | 0.28 | | | 1,389 | | 0.28 | | | 156 | | | 11.2 | |

| Commercial Real Estate | 4,282 | | 0.76 | | | 1,057 | | 0.21 | | | 3,225 | | | 305.1 | |

| Commercial and Agricultural | 113 | | 0.02 | | | 64 | | 0.01 | | | 49 | | | 76.6 | |

| HELOC | 189 | | 0.03 | | | 142 | | 0.03 | | | 47 | | | 33.1 | |

| Other Consumer | 29 | | 0.01 | | | 9 | | — | | | 20 | | | 222.2 | |

| Total Non-Performing Loans | 6,273 | | 1.12 | % | | 2,682 | | 0.53 | % | | 3,591 | | | 133.9 | % |

| | | | | | | | | | | |

| Other Non-Performing Assets: | | | | | | | | | | | |

| OREO | 120 | | 0.02 | % | | 130 | | 0.03 | % | | (10) | | | (7.7) | % |

| | | | | | | | | | | |

| Total Non-Performing Assets | $ | 6,393 | | 1.14 | % | | $ | 2,812 | | 0.56 | % | | $ | 3,581 | | | 127.3 | % |

| Total Non-Performing Assets as a Percentage of Total Assets | 0.46 | % | | | | 0.22 | % | | | | | | |

(1) PERCENT OF GROSS LOANS RECEIVABLE HELD FOR INVESTMENT, NET OF DEFERRED FEES AND LOANS IN PROCESS.

Non-performing loans increased in all loan categories during 2022 compared to 2021. The largest increase in non-performing loans was in the commercial real estate loan category, which increased $3.2 million or 305.1% to $4.3 million at December 31, 2022 from $1.1 million at December 31, 2021. The balance in non-performing commercial real estate loans consisted of three loans to three borrowers with an average loan balance of $1.1 million at December 31, 2022 compared to eight loans to six borrowers with an average loan balance of $151,000 at December 31, 2021.

Non-performing residential loans, which represented the second largest category of non-performing loans, increased $156,000 or 11.2% to $1.5 million at December 31, 2022 from $1.4 million at December 31, 2021. Non-performing residential mortgage loans at December 31, 2022 consisted of 16 loans to 16 borrowers with an average loan balance of $97,000, the largest of which was $250,000, compared to 12 loans to 12 borrowers with an average loan balance of $116,000, the largest of which was $274,000, at December 31, 2021.

Our strategy is to work with our borrowers to reach acceptable payment plans while protecting our interests in the underlying collateral. In the event an acceptable arrangement cannot be reached, we may have to acquire these properties through foreclosure or other means and subsequently sell, develop, or liquidate them.

The balance of loans classified as troubled debt restructurings ("TDRs") decreased $309,000 or 44.5% during the year ended December 31, 2022. The Bank had two TDRs totaling $385,000 at December 31, 2022 compared to three TDRs totaling $694,000 at December 31, 2021. At both December 31, 2022 and 2021, all TDRs were non-accruing. All TDRs are reviewed for impairment loss and included in impaired loans until paid off. TDR loans can be classified as either accrual or non-accrual. TDR loans are classified as non-accrual loans unless they have been performing in accordance with their modified terms for a period of at least six months in which case they are placed on accrual status. At December 31, 2022, the Bank had $5.6 million of impaired loans, including $385,000 in TDRs, compared to $2.3 million impaired loans, including $694,000 in TDRs, at December 31, 2021.

OREO decreased $10,000 or 7.7% to $120,000 at December 31, 2022 from $130,000 at December 31, 2021. At December 31, 2022, the balance of OREO consisted of five acres of commercial land in Aiken, South Carolina.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

The Bank reviews its loan portfolio and allowance for loan losses on a monthly basis. When determining the appropriate allowance for loan losses during the years ended December 31, 2022 and 2021, management took into consideration such factors as the national and state unemployment rates and related trends, national and state unemployment benefit claim levels and related trends, the amount of and timing of financial assistance provided by the government, inflation, consumer spending levels and trends, industries significantly impacted by the COVID-19 pandemic and a review of the Bank's largest commercial loan relationships.

Effective January 1, 2023, the Bank adopted Accounting Standards Update (“ASU”) No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, also known as CECL. CECL replaces the incurred loss impairment framework in current GAAP. Adoption of this guidance resulted in a $2.0 million increase in the allowance for credit losses, comprised of increases in the allowance for loan losses of $800,000 and the reserve for unfunded commitments of $1.2 million. The cumulative effect adjustment to retained earnings was $1.6 million, net of tax. For additional information, refer to “Recently Issued or Adopted Accounting Standards” in Note 1 of the Notes to Consolidated Financial Statements included herein.

Management will continue to closely monitor economic conditions and will work with borrowers as necessary to assist them through this challenging economic climate. Future additions to the Bank's allowance for loan losses are dependent on, among other things, the performance of the Bank's loan portfolio, the economy, changes in real estate values, and interest rates. There can be no assurance that additions to the allowance will not be required in future periods. The determination of the appropriate level of the allowance for loan losses inherently involves a high degree of subjectivity and requires us to make significant estimates of current credit risks and future trends, all of which may undergo material changes.

Deterioration in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside of our control, may require an increase in the allowance for loan losses. The ultimate impact will depend on future developments, which are highly uncertain and cannot be predicted. In addition, bank regulatory agencies periodically review our allowance for loan losses and may require an increase in the provision for possible loan losses or the recognition of further loan charge-offs, based on judgments different than those of management. If charge-offs in future periods exceed the allowance for loan losses, we will need additional provisions to increase the allowance for loan losses. Any increases in the allowance for loan losses will result in a decrease in net income and, possibly, capital, and may have a material adverse effect on our financial condition and results of operations. Management continually monitors its loan portfolio for the impact of local economic changes. The ratio of the allowance for loan losses to total loans was 2.09% and 2.19% at December 31, 2022 and 2021, respectively.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Financial Condition - Liabilities and Shareholders' Equity

Total deposits decreased $5.9 million or 0.5% to $1.11 billion at December 31, 2022 from $1.12 billion at December 31, 2021. The majority of the Bank’s deposits are originated within the Bank’s immediate market area. The Bank had brokered time deposits of $6.0 million and $10.0 million at December 31, 2022 and 2021, respectively. The Bank uses brokered time deposits to manage interest rate risk because they are accessible in bulk at rates typically only slightly higher than those in our market areas. A portion of these brokered time deposits give the Bank a call option that allows the Bank the choice to redeem them early should rates change. In addition, the Bank had $5.0 million in other brokered deposits at December 31, 2022. Total deposits at December 31, 2022, excluding brokered deposits, decreased $1.9 million or 0.2%. Brokered deposits were 1.0% and 1.3% of total deposits at December 31, 2022 and 2021, respectively.

Certificate of deposits that met or exceeded the FDIC insurance limit of $250,000 totaled $30.3 million and $39.4 million at December 31, 2022 and 2021, respectively. The following table summarizes the maturity schedule of certificates of deposit with a balance of $250,000 or more at December 31, 2022:

| | | | | |

| |

| | (In Thousands) |

| Within 3 Months | $ | 4,036 | |

| After 3 Months, Within 6 Months | 3,741 | |

| After 6 Months, Within 12 Months | 14,010 | |

| After 12 Months | 8,485 | |

| | $ | 30,272 | |

Total certificates of deposit scheduled to mature in one year or less totaled $96.2 million at December 31, 2022 compared to $118.1 million at December 31, 2021.

Management’s policy is to maintain deposit rates at levels that are competitive with other local financial institutions. Based on historical experience, we believe that a significant portion of maturing certificates of deposit will remain with the Bank.

The Bank had outstanding FHLB advances and borrowings from the "discount window" of the FRB of Atlanta totaling $0 and $44.1 million at December 31, 2022, respectively, compared to no such advances or borrowings at December 31, 2021. Depository institutions may borrow from the discount window for periods as long as 90 days, and borrowings are prepayable and renewable by the borrower on a daily basis.

Other borrowings increased $803,000 or 3.0% to $27.6 million at December 31, 2022 from $26.8 million at December 31, 2021. These borrowings consist of short-term repurchase agreements with certain commercial demand deposit customers for sweep accounts. The repurchase agreements typically mature within one to three days and the interest rate paid on these borrowings floats monthly with money market type rates. The interest rate paid on the repurchase agreements was 0.75% and 0.15% at December 31, 2022 and 2021, respectively. The Bank had pledged as collateral for these repurchase agreements AFS investment securities and HTM investment securities with amortized costs and fair values of $52.3 million and $49.8 million, at December 31, 2022, and $45.3 million and $45.2 million, at December 31, 2021, respectively.

At both December 31, 2022 and 2021, the Company had $5.2 million in junior subordinated debentures outstanding. In addition, the Company had $26.5 million and $30.0 million in subordinated debentures (“Notes”) outstanding at December 31, 2022 and 2021, respectively. During the year ended December 31, 2022, the Company repurchased $3.5 million in principal amount of the Notes. For additional information, refer to Note 12 and Note 14 of the Notes to Consolidated Financial Statements included herein.

Total shareholders' equity increased $44.7 million or 38.7% to $160.2 million at December 31, 2022 from $115.5 million at December 31, 2021. The increase was primarily attributable to an $82.9 million issuance of Senior Non-Cumulative Perpetual Preferred Stock, Series ECIP (the “Preferred Stock”) by the Company and net income of $10.2 million during 2022. These increases were partially offset by $2.5 million in dividends paid to common shareholders and a $46.0 million decrease in accumulated other comprehensive income, net of tax, related to the unrecognized loss in value of AFS investment securities during the year ended December 31, 2022. Book value per common share was $23.76 at December 31, 2022 compared to $35.51 at December 31, 2021.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Results of Operations

The following table presents the dollar amount of changes in interest income and interest expense for major components of interest-earning assets and interest-bearing liabilities. The table also distinguishes between the changes related to higher or lower outstanding balances and the changes related to the volatility of interest rates. For each category of interest-earning assets and interest-bearing liabilities, information is provided on changes attributable to: (1) changes in rate (multiplied by prior year volume); (2) changes in volume (multiplied by prior year rate); and (3) net change (the sum of the prior columns). For purposes of this table, changes attributable to both rate and volume, which cannot be segregated, have been allocated proportionately to the change attributable to volume and the change attributable to rate. Changes in income are calculated on a tax equivalent basis using the effective tax rate for the period.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Years Ended December 31, |

| | 2022 vs. 2021 | | 2021 vs. 2020 |

| (Decrease) Increase Due to

Change in | | (Decrease) Increase Due to

Change in |

| (Dollars in Thousands) | Volume | | Rate | | Net | | Volume | | Rate | | Net |

| Interest-Earning Assets: | | | | | | | | | | | |

Loans: (1) | $ | 591 | | | $ | (2,150) | | | $ | (1,559) | | | $ | (2) | | | $ | 924 | | | $ | 922 | |

| Taxable Investment Securities | 1,784 | | | 5,410 | | | 7,194 | | | 2,176 | | | (2,948) | | | (772) | |

Non-taxable Investment Securities (2) | 16 | | | (395) | | | (379) | | | 283 | | | (327) | | | (44) | |

| Deposits in Other Banks | 34 | | | 154 | | | 188 | | | (38) | | | (31) | | | (69) | |

| Total Interest-Earning Assets | $ | 2,425 | | | $ | 3,019 | | | $ | 5,444 | | | $ | 2,419 | | | $ | (2,382) | | | $ | 37 | |

| Interest-Bearing Liabilities: | | | | | | | | | | | |

| Deposits: | | | | | | | | | | | |

| Certificate Accounts | $ | (133) | | | $ | (139) | | | $ | (272) | | | $ | (474) | | | $ | (1,414) | | | $ | (1,888) | |

| Other Interest Bearing Deposits | 103 | | | 1,449 | | | 1,552 | | | 209 | | | (616) | | | (407) | |

| Total Deposits | (30) | | | 1,310 | | | 1,280 | | | (265) | | | (2,030) | | | (2,295) | |

| Borrowings | (252) | | | 176 | | | (76) | | | (125) | | | (337) | | | (462) | |

| Total Interest-Bearing Liabilities | (282) | | | 1,486 | | | 1,204 | | | (390) | | | (2,367) | | | (2,757) | |

Effect on Net Tax Equivalent Interest Income (2) | $ | 2,707 | | | $ | 1,533 | | | $ | 4,240 | | | $ | 2,809 | | | $ | (15) | | | $ | 2,794 | |

(1) INTEREST ON NON-ACCRUAL LOANS IS NOT INCLUDED IN INCOME, ALTHOUGH THEIR LOAN BALANCES ARE INCLUDED IN AVERAGE LOANS OUTSTANDING.

(2)THE TAX-EQUIVALENT INTEREST INCOME ADJUSTMENT RELATES TO THE TAX EXEMPT MUNICIPAL BONDS

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Average Balances, Interest Income and Expenses, and Average Yields and Rates

The following table compares detailed average balances, average yields on interest earning assets, and average costs of interest bearing liabilities at December 31, 2022 and 2021. The average balances were derived from the daily balances throughout the periods indicated. The average yields or costs were calculated by dividing the income or expense by the average balance of the corresponding assets or liabilities. Nonaccrual loans are included in earning assets in the following tables. Loan yields have been reduced to reflect the negative impact on our earnings of loans on nonaccrual status.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Year Ended December 31, |

| | | 2022 | | 2021 |

| (Dollars in thousands) | | Average Balance | | Interest | | Yield/Rate | | Average Balance | | Interest | | Yield/Rate |

| Interest-Earning Assets: | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Loans (1) | | $ | 525,396 | | | $ | 25,637 | | | 4.88 | % | | $ | 513,987 | | | $ | 27,196 | | | 5.29 | % |

Taxable Investment Securities | | 695,960 | | | 16,145 | | | 2.32 | % | | 591,387 | | | 8,952 | | | 1.51 | % |

Non-taxable Investments (2) | | 23,651 | | | 846 | | | 3.58 | % | | 23,351 | | | 1,225 | | | 5.25 | % |

| Deposits in Other Banks | | 3,649 | | | 203 | | | 5.56 | % | | 1,639 | | | 14 | | | 0.85 | % |

| Total Interest-Earning Assets | | $ | 1,248,656 | | | $ | 42,831 | | | 3.43 | % | | $ | 1,130,364 | | | $ | 37,387 | | | 3.31 | % |

| Interest-Bearing Liabilities: | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Checking, Savings and Money Market Accounts | | $ | 703,914 | | | $ | 2,304 | | | 0.33 | % | | $ | 616,098 | | | $ | 752 | | | 0.12 | % |

| Certificate Accounts | | 143,619 | | | 607 | | | 0.42 | % | | 172,995 | | | 879 | | | 0.51 | % |

| Total Interest-Bearing Deposits | | 847,533 | | | 2,911 | | | 0.34 | % | | 789,093 | | | 1,631 | | | 0.21 | % |

| | | | | | | | | | | | |

| Junior Subordinated Debt | | 5,155 | | | 180 | | | 3.49 | % | | 5,155 | | | 97 | | | 1.88 | % |

| Subordinated Debt | | 29,332 | | | 1,548 | | | 5.28 | % | | 30,000 | | | 1,575 | | | 5.25 | % |

FHLB Advances and Other Borrowings (3) | | 45,477 | | | 389 | | | 0.86 | % | | 54,593 | | | 521 | | | 0.95 | % |

| Total Interest-Bearing Liabilities | | $ | 927,497 | | | $ | 5,028 | | | 0.54 | % | | $ | 878,841 | | | $ | 3,824 | | | 0.44 | % |

| Net Interest Rate Spread | | | | | | 2.89 | % | | | | | | 2.87 | % |

Tax Equivalent Net Interest Income/Margin (2) | | | | $ | 37,803 | | | 3.03 | % | | | | $ | 33,563 | | | 2.97 | % |

Less: tax equivalent adjustment (2) | | | | 253 | | | | | | | 270 | | | |

| Net Interest Income | | | | $ | 37,550 | | | | | | | $ | 33,293 | | | |

(1) INTEREST INCOME FROM OTHER LOANS INCLUDED IN THE TABLES ABOVE AND BELOW INCLUDES DEFERRED PPP LOAN FEES OF $441,000 AND $4.7 MILLION RECOGNIZED DURING THE YEARS ENDED DECEMBER 31, 2022 AND 2021, RESPECTIVELY.

(2)TAX EQUIVALENT BASIS RECOGNIZES THE INCOME TAX SAVINGS WHEN COMPARING TAXABLE AND TAX-EXEMPT ASSETS AND WAS CALCULATED USING THE EFFECTIVE TAX RATE IN PLACE FOR THE YEARS ENDED DECEMBER 31, 2022 AND 2021. THE TAX-EQUIVALENT INTEREST INCOME ADJUSTMENT RELATES TO THE TAX EXEMPT MUNICIPAL BONDS INCLUDED IN OUR INVESTMENT PORTFOLIO DURING THE PERIODS INDICATED.

(3)INCLUDES FHLB ADVANCES, BORROWINGS FROM THE FRB AND REPURCHASE AGREEMENTS.

.

.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Comparison of the Years Ended December 31, 2022 and 2021

Net Income

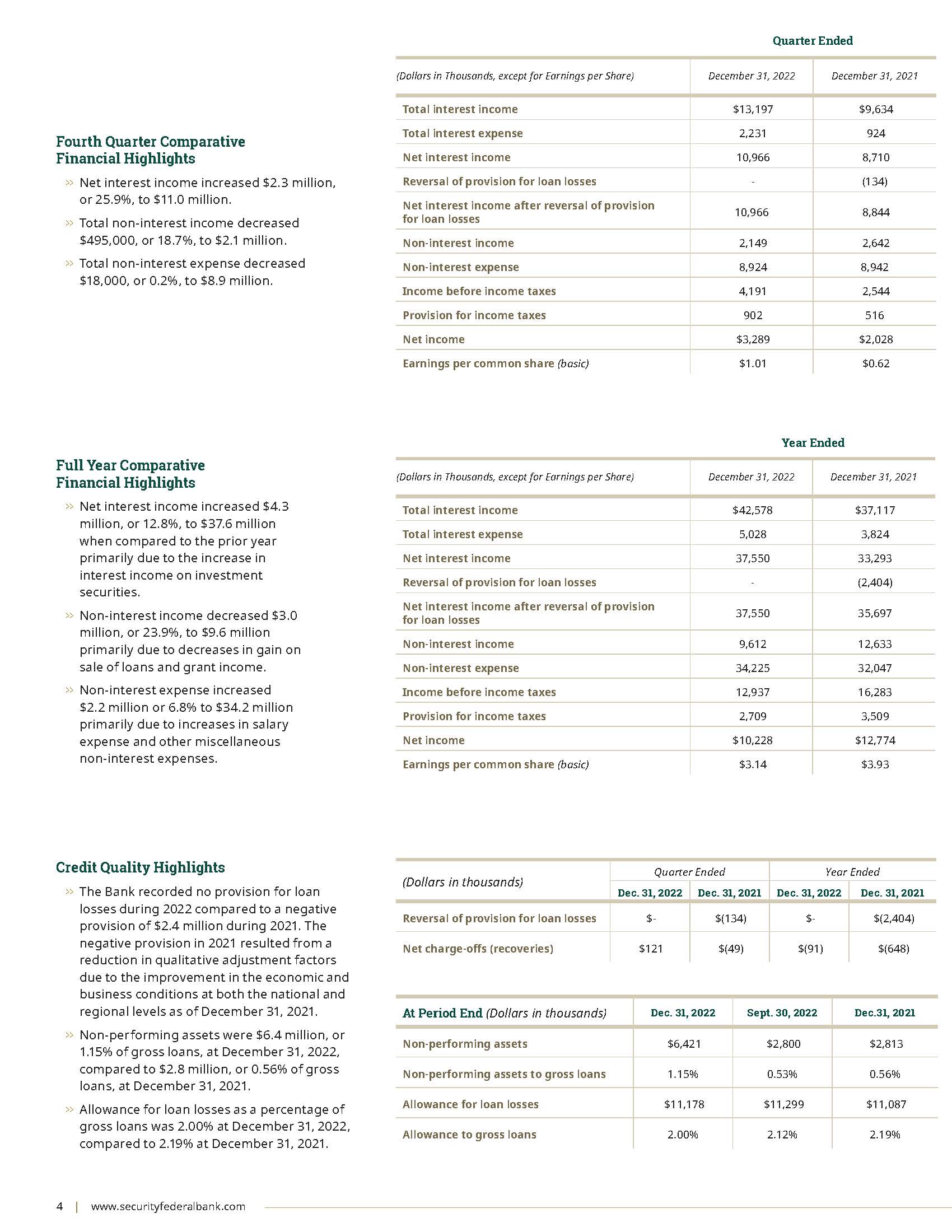

Net income decreased $2.6 million or 19.9% to $10.2 million or $3.14 per basic and diluted common share for the year ended December 31, 2022, compared to $12.8 million or $3.93 per basic and diluted common share for the year ended December 31, 2021. The decrease in net income during 2022 compared to the prior year was due to a decline in non-interest income and an increase in non-interest expense, partially offset by an increase in net interest income. Also contributing to the decrease in net income was a $2.4 million reversal of loan loss reserves during 2021 following significantly higher loan loss provisions recorded in 2020 in response to the potential and unknown economic impact of the ongoing COVID-19 pandemic compared to no provision for loan losses in 2022.

Net Interest Income

Net interest income increased $4.3 million or 12.8% to $37.6 million for the year ended December 31, 2022, compared to $33.3 million in 2021. The increase in net interest income was primarily due to higher interest income from investments, which was partially offset by an increase in interest expense. The net interest margin on a tax-equivalent basis increased six basis points to 3.03% for the year ended December 31, 2022 from 2.97% for the year ended December 31, 2021.

Total average interest-earning assets increased $118.3 million or 10.5% to $1.25 billion for the year ended December 31, 2022 from $1.13 billion for the year ended December 31, 2021 with a 12 basis point increase in the average yield earned on these assets. Average interest-bearing liabilities increased $48.7 million or 5.5% to $927.5 million for the year ended December 31, 2022 from $878.8 million for the year ended December 31, 2021 with an increase of 10 basis points in the average cost. The interest rate spread on a tax-equivalent basis increased two basis points to 2.89% for the year ended December 31, 2022 from 2.87% in 2021.

Total interest income increased $5.5 million or 14.7% to $42.6 million for the year ended December 31, 2022, compared to $37.1 million for the year ended December 31, 2021 as a result of increased interest income from taxable investments which was partially offset by lower interest income from loans and tax-exempt investments.

Total tax-equivalent interest income on investments increased $6.8 million, or 67.0%, due to a $104.9 million, or 17.1%, increase in the aggregate average balance of these interest-earning assets combined with an increase of 70 basis points in the average yield earned on these assets during 2022 when compared to 2021.

Interest income from loans decreased $1.6 million or 5.7% to $25.6 million for the year ended December 31, 2022 compared to $27.2 million for the year ended December 31, 2021. The decrease was primarily attributable to a decrease in deferred loan fees on PPP loans recognized in 2022. The Bank recognized $441,000 and $4.7 million in deferred loan fees on PPP loans during the years ended December 31, 2022 and 2021, respectively. There was no unamortized net deferred fees on PPP loans remaining at December 31, 2022. This decrease was partially offset by an increase of $11.4 million in the average balance of loans outstanding during the year ended December 31, 2022.

Total interest expense increased $1.2 million or 31.5% to $5.0 million for the year ended December 31, 2022, compared to $3.8 million for the year ended December 31, 2021 due to a 10 basis point increase in the average cost of interest-bearing liabilities combined with an increase of $48.7 million, or 5.5%, in the average balance of these liabilities.

The largest increase was in interest expense on deposits, which increased $1.3 million or 78.4% to $2.9 million in 2022 compared to $1.6 million in 2021. Average interest-bearing deposits increased $58.4 million or 7.4% to $847.5 million during the year ended December 31, 2022 compared to $789.1 million during 2021, while the average cost of those deposits increased 13 basis points to 0.34% during 2022 from 0.21% in 2021.

Interest expense on borrowings from the FRB and other borrowings decreased $132,000 or 25.3% to $389,000 during the year ended December 31, 2022 from $521,000 during the prior year. The decrease was attributable to a $9.1 million, or 16.7% decrease in the average balance of these liabilities combined with a decrease of nine basis points in the average cost to 0.86% in 2022 from 0.95% during 2021.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Provision for Loan Losses

The Company recorded no provision for loan losses for the year ended December 31, 2022 compared to a $2.4 million reversal of the provision for loan losses for the year ended December 31, 2021. The reversal of loan loss provision during 2021 was the result of a reduction in historical loss and qualitative adjustment factors related to improvement in the economic and business conditions at both the national and regional levels as of December 31, 2021. Non-performing assets increased $3.6 million, or 127.3%, to $6.4 million at December 31, 2022 from $2.8 million at December 31, 2021. Non-performing assets represented 0.46% and 0.22% of total assets at December 31, 2022 and 2021, respectively.

The amount of the provision is determined by management’s on-going monthly analysis of the loan portfolio and the adequacy of the allowance for loan losses. The Company has established policies and procedures for evaluating and monitoring the credit quality of the loan portfolio and for the timely identification of potential problem loans including internal and external loan reviews. The adequacy of the allowance for loan losses is reviewed monthly by the Asset Classification Committee and quarterly by the Board of Directors.

Management’s monthly review of the adequacy of the allowance includes three main components. The first component is an analysis of loss potential in various homogeneous segments of the portfolio based on historical trends and the risk inherent in each category. The historical loss periods used to calculate these ratios can range from one to ten years depending on which period is deemed a more relevant indicator of future losses. Currently, management applies a ten-year historical loss ratio to each loan category to estimate the inherent loss in these pooled loans.

The second component of management’s monthly analysis is the specific review and evaluation of significant problem credits identified through the Company’s internal monitoring system, including but not limited to classified loans, non-accrual loans and TDRs. These loans are evaluated for impairment and recorded in accordance with accounting guidance. All TDRs and substantially all non-accrual loans are individually evaluated for impairment. In accordance with our policy, non-accrual commercial loans with a balance less than $200,000 and non-accrual non-commercial (consumer, HELOC, residential mortgage) loans with a balance less than $100,000 are deemed immaterial and therefore excluded from the individual impairment review. For each loan deemed impaired, management calculates a specific reserve for the amount in which the recorded investment in the loan exceeds the fair value. This estimate is based on a thorough analysis of the most probable source of repayment, which is typically liquidation of the collateral.

The third component is an analysis of changes in qualitative factors that may affect the portfolio, including but not limited to: relevant economic trends that could impact borrowers’ ability to repay, industry trends, changes in the volume and composition of the portfolio, credit concentrations, or lending policies and the experience and ability of the staff and Board of Directors. Management also reviews and incorporates certain ratios such as percentage of classified loans, average historical loan losses by loan category, delinquency percentages, and the assignment of percentage targets of reserves in each loan category when evaluating the allowance. Once the analysis is completed, the three components are combined and compared to the allowance amount. Based on this, charges are made to the provision as needed.

Management believes the allowance for loan losses at December 31, 2022 is adequate based on its best estimates of the losses inherent in the loan portfolio, although there can be no guarantee as to these estimates. In addition, bank regulatory agencies may require additional provisions to the allowance for loan losses based on their judgments and estimates as part of their examination process. Because the allowance for loan losses is an estimate, there can be no guarantee that actual loan losses will not exceed the allowance for loan losses, or that additional increases in the allowance for loan losses will not be required in the future. A further decline in national and local economic conditions as a result of inflation, a recession, unemployment, money supply fluctuations or other factors could result in a material increase in the allowance for loan losses and may adversely affect the Company’s financial condition and results of operations.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

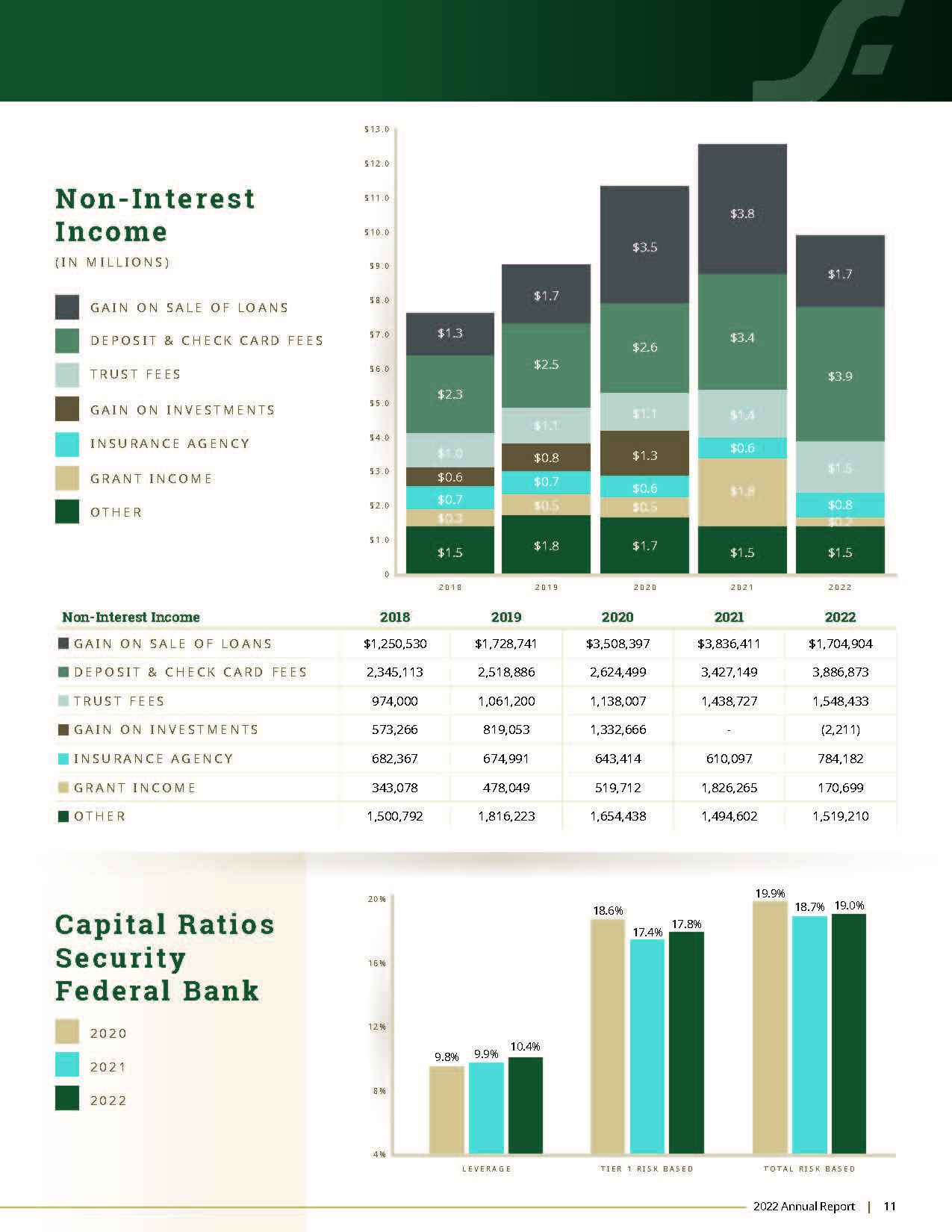

Non-Interest Income

Non-interest income decreased $3.0 million or 23.9% to $9.6 million for the year ended December 31, 2022 from $12.6 million for the year ended December 31, 2021. The decrease in non-interest income was primarily attributable to decreases in gain on sales of loans and grant income. These decreases in non-interest income were partially offset by increases in service fees on deposit accounts, insurance commissions, trust income, and ATM and check card fee income.

Gain on sales of loans decreased $2.1 million or 55.6% to $1.7 million for the year ended December 31, 2022 compared to $3.8 million in 2021 as the dollar volume of loans sold to investors decreased. The Bank sold $48.5 million of loans in 2022 compared to $112.9 million during 2021.

Insurance commissions increased $174,000 or 28.5% to $784,000 for the year ended December 31, 2022 compared to $610,000 in 2021 due to an increase in the number of insurance policies sold. Trust income increased $110,000 or 7.6% to $1.5 million during the year ended December 31, 2022 compared to $1.4 million in 2021 due to an increase in assets under management. ATM and check card fee income increased $346,000 or 14.0% to $2.8 million for the year ended December 31, 2022 compared to $2.5 million in 2021 reflecting higher transaction volume.

The Bank received $171,000 and $1.8 million in grant income during the years ended December 31, 2022 and 2021, respectively. During 2022, the Bank was awarded a $171,000 grant by the Community Development Financial Institutions ("CDFI") Fund Bank Enterprise Award ("BEA") program for the Bank's continued community development financing and service activities in the most economically distressed communities. During 2021, the Bank was awarded a $1.8 million grant by the CDFI Fund Rapid Response Program ("RRP") created to provide certified CDFIs with resources to help counter the economic impact of COVID-19 in distressed and underserved communities. The grant proceeds were used to fund qualified loans within the Bank’s target market areas, which satisfied the performance obligation of the grant.

Non-Interest Expense

Non-interest expense increased $2.2 million or 6.8% to $34.2 million during the year ended December 31, 2022 compared to $32.0 million during 2021. The increase in non-interest expense was primarily due to increases in compensation and employee benefits, a write-down of the value of land held for sale and other non-interest expenses, partially offset by a decrease in consulting expenses.

Compensation and employee benefits increased $890,000 or 4.6% to $20.1 million during the year ended December 31, 2022 from $19.2 million for the year ended December 31, 2021 primarily due to annual cost of living increases and an increase in the number of full time equivalent employees as a result of our newest branch added during the first quarter of 2022. Occupancy expense also increased by $190,000 primarily due to the addition of our newest branch located in Columbia, South Carolina.

A write-down of the fair value of land held for sale during the year ended December 31, 2022 based on an updated appraisal resulted in a $433,000 increase in non-interest expense.

Consulting expense decreased $497,000 or 41.4% to $705,000 for the year ended December 31, 2022 compared to $1.2 million during the prior year. The decrease was primarily due to a one-time expense of $605,000 for IT related consulting expenses incurred in 2021.

The Company incurred costs of $10,000 from the operation of OREO properties during the year ended December 31, 2022, compared to a net recovery of $116,000 during the prior year during which OREO sales exceeded write-downs and other costs. There were no sales of OREO properties during 2022 and therefore, no gain on OREO sales during 2022 compared to $105,000 in 2021.

Other non-interest expense increased $1.3 million or 35.8% to $4.7 million for the year ended December 31, 2022 compared to $3.4 million during 2021 due to increased operations and the addition of our newest branch added in 2022. As a result of the COVID-19 pandemic, some branch locations were not open during all twelve months of 2021. As of May 2021, all branches had reopened and resumed normal business hours.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Provision for Income Taxes

The provision for income taxes decreased $800,000 or 22.8% to $2.7 million during the year ended December 31, 2022 compared to $3.5 million for the year ended December 31, 2021 due to higher pre-tax income in 2021. The Company's combined federal and state effective tax rate was 20.9% for 2022 compared to 21.6% for 2021.

Comparison of the Years Ended December 31, 2021 and 2020

A comparison of our operating results for the 2021 and 2020 fiscal years may be found under the heading “Comparison of Operating Results for the Years Ended December 31, 2021 and 2020” in our Annual Report to Shareholders which was filed as Exhibit 13 to our Annual Report on Form 10-K for the year ended December 31, 2021.

Net cost of operation of OREO includes all expenses associated with OREO properties, including write-downs in value and

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Regulatory Capital

The following table reconciles the Bank's shareholders' equity to its various regulatory capital positions.

| | | | | | | | | | | |

| | December 31, |

| 2022 | | 2021 |

| | (In Thousands) |

Bank’s Shareholders’ Equity (1) | $ | 142,652 | | | $ | 124,983 | |

| Reduction for Goodwill | 1,200 | | | 1,200 | |

| Tangible Capital | 141,452 | | | 123,783 | |

| Core Capital | 141,452 | | | 123,783 | |

| Supplemental Capital | 9,956 | | | 8,923 | |

| Total Risk-Based Capital | $ | 151,408 | | | $ | 132,706 | |

(1)EXCLUDES UNREALIZED (LOSSES) GAINS ON INVESTMENT SECURITIES OF $(40.8) MILLION and $5.2 MILLION AT DECEMBER 31, 2022 AND 2021, RESPECTIVELY.

The Bank is subject to minimum capital requirements imposed by the FDIC. Based on capital levels at December 31, 2022, the Bank was considered to be well capitalized. At December 31, 2022, the Bank exceeded all regulatory capital requirements with Tier 1 leverage-based capital, Tier 1 risk-based capital, total risk-based capital, and common equity Tier 1 (CET1) capital ratios of 10.4%, 17.8%, 19.0%, and 17.8%, respectively.

CET1 consists of Tier 1 capital less all capital components that are not considered common equity. In addition to the FDIC’s minimum capital ratios, the Bank is required to maintain a capital conservation buffer consisting of additional CET1 capital greater than 2.5% of risk-weighted assets above the required minimum levels in order to avoid limitations on paying dividends, engaging in share repurchases, and paying discretionary bonuses. At December 31, 2022, the Bank’s capital conservation buffer was 11.0%.

For additional information regarding the Bank's and Company's regulatory capital compliance, see the discussion included in Note 16 of the Notes to Consolidated Financial Statements included herein.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Liquidity and Capital Resources

Liquidity refers to the ability to generate sufficient cash flows to fund current loan demand, repay maturing borrowings, fund maturing deposit withdrawals, and meet operating expenses. The Bank's primary sources of funds include deposits, scheduled loan and investment security repayments, including interest payments, maturities and sales of loans and investment securities, borrowings from the FRB, advances from the FHLB and cash flow generated from operations. The need for funds varies among periods depending on funding needs as well as the rate of amortization and prepayment on loans. The use of borrowings from the FRB, FHLB advances and other borrowings varies depending on loan demand, deposit inflows, and the use of investment leverage strategies that we might employee to increase net interest income.

The principal use of the Bank's funds is the origination of mortgages and other loans and the purchase of investment securities. Originations of new loans and renewals of previously funded loans on loans held for investment were $557.1 million during the year ended December 31, 2022 compared to $438.4 million during the year ended December 31, 2021. Purchases of investment securities totaled $210.3 million during 2022 compared to $217.6 million during 2021. Other uses of the Bank's funds during the year ended December 31, 2022 included repurchases of subordinated debentures and dividend payments to shareholders.

In the normal course of business, the Company makes off-balance sheet arrangements, including credit commitments to its customers to meet their financial needs. These arrangements involve, to varying degrees, elements of credit and interest rate risk not recognized in the consolidated statement of financial condition. The Bank makes personal, commercial, and real estate lines of credit available to customers and does issue standby letters of credit.

Commitments to extend credit to customers are subject to the Bank’s normal credit policies and are essentially the same as those involved in extending loans to customers. Unused lines of credit on HELOCs, credit cards, and commercial loans amounted to $173.3 million at December 31, 2022. HELOCs are made on a floating rate basis with final maturities of 15 to 20 years. The Bank issues fixed rate credit cards, currently at 9.99%, and variable rate rewards credit cards with a floating rate equal to prime plus 9.99%. Credit cards are renewed every three years. The Bank had undisbursed loans-in-process of $22.7 million at December 31, 2022, which will be disbursed over an average of 90 days, and are included in the total unused commitments above. These commitments to originate loans and future advances of lines of credit are expected to be funded from loan amortizations and prepayments, deposit inflows, maturing investments, and short-term borrowing capacity. See Note 19 of the Notes to the Consolidated Financial Statements included herein for additional information regarding our commitments and off-balance sheet arrangements.

We incur capital expenditures on an ongoing basis to expand and improve our product offerings, enhance and modernize our technology infrastructure, and to introduce new technology-based products to compete effectively in our markets. We evaluate capital expenditure projects based on a variety of factors, including expected strategic impacts (such as forecasted impact on revenue growth, productivity, expenses, service levels and customer retention) and our expected return on investment. The amount of capital investment is influenced by, among other things, current and projected demand for our services and products, cash flow generated by operating activities, cash required for other purposes and regulatory considerations. Based on current capital allocation objectives, there are no projects scheduled for capital investments in premises and equipment during 2023 that would materially impact liquidity. We also have purchase obligations, generally with remaining terms of less than three years and contracts with various vendors to provide services, including information processing, for periods generally ranging from one to five years, for which our financial obligations are dependent upon acceptable performance by the vendor. For the year ending December 31, 2023, we project that fixed commitments will include $518,000 of operating lease payments. See Note 5 of the Notes to the Consolidated Financial Statements included herein for additional information regarding our operating leases.

The Bank’s liquidity has been positively impacted by increases in deposit levels in recent years. During the year ended December 31, 2022, deposits decreased by $5.9 million after increasing by $197.9 million during the year ended December 31, 2021. Our liquid assets in the form of cash and cash equivalents, certificates of deposit at other banks and investments increased to $747.2 million at December 31, 2022 from $735.1 million at December 31, 2021. Total certificates of deposit scheduled to mature in one year or less totaled $96.2 million at December 31, 2022 compared to $118.1 million at December 31, 2021. Management’s policy is to maintain deposit rates at levels that are competitive with other local financial institutions. Based on historical experience, we believe that a significant portion of maturing certificates of deposit will remain with the Bank.

SECURITY FEDERAL CORPORATION AND SUBSIDIARIES

Management's Discussion and Analysis of Financial Condition and Results of Operations

Primary sources of short-term liquidity for the Bank include the Federal Reserve Bank discount window and a $50.0 million line of credit with the Pacific Coast Bankers Bank. In addition, at December 31, 2022, the Bank had $388.3 million in unused borrowing capacity at the FHLB. Management believes that future liquidity can be met through the Bank's deposit base, which had a balance of $1.11 billion at December 31, 2022, sales and maturities of investment securities, and loans sold to investors. During the years ended December 31, 2022 and 2021, the Bank sold $53.3 million and $118.4 million in loans, respectively.

Historically the Bank’s cash flow from operating activities has been relatively stable. The cash flows from investing activities vary with sales of investment securities and with the need to invest excess funds or utilize leverage strategies with the purchase of investment securities. The cash flows from financing activities vary depending on the need for borrowings from the FRB, FHLB advances and other borrowings. The Bank's management believes that the liquid assets combined with the available lines of credit provide adequate liquidity to meet current financial obligations for at least the next 12 months.

Security Federal Corporation is a separate legal entity from the Bank and must provide for its own liquidity and pay its own operating expenses. Sources of capital and liquidity for Security Federal Corporation include distributions from the Bank and the issuance of debt or equity securities, although there are regulatory restrictions on the ability of the Bank to pay dividends. At December 31, 2022, Security Federal Corporation (on an unconsolidated basis) had liquid assets of $28.8 million. The Company currently expects to continue the current practice of paying quarterly cash dividends on common stock subject to the Board of Directors' discretion to modify or terminate this practice at any time and for any reason without prior notice. Our current quarterly common stock dividend rate is $0.13 per share, as approved by our Board of Directors, which we believe is a dividend rate per share which enables us to balance our multiple objectives of managing and investing in the Bank, and returning a substantial portion of our cash to our shareholders. In addition to the quarterly dividends paid in 2022, the Company also paid a special cash dividend of $0.28 per share in 2022 to all shareholders of record as of March 31, 2022. Assuming continued payment during 2023 at this rate of $0.13 per share, our average total dividends paid each quarter would be approximately $422,875 based on the number of our current outstanding shares at December 31, 2022.

[Letterhead of Elliot Davis, LLP]

Report of Independent Registered Public Accounting Firm (PCAOB ID 149)

To the Shareholders and the Board of Directors of Security Federal Corporation:

Opinion on the Financial Statements