Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 1, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-13687

CEC ENTERTAINMENT, INC.

(Exact name of registrant as specified in its charter)

| Kansas | 48-0905805 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 4441 West Airport Freeway Irving, Texas |

75062 | |

| (Address of principal executive offices) | (Zip Code) | |

(972) 258-8507

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $0.10 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of July 1, 2011, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the common stock beneficially held by non-affiliates of the registrant was $772,385,955. The aggregate market value was determined based on the closing price of the common stock on July 1, 2011.

As of February 13, 2012, an aggregate of 18,157,502 shares of the registrant’s common stock, par value $0.10 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement, to be filed pursuant to Section 14(a) of the Securities Exchange Act of 1934 in connection with the registrant’s 2012 annual meeting of stockholders, are incorporated by reference in Part III of this report.

Table of Contents

CEC ENTERTAINMENT, INC.

| Page | ||||||

| 3 | ||||||

| PART I | ||||||

| ITEM 1. |

4 | |||||

| ITEM 1A. |

8 | |||||

| ITEM 1B. |

12 | |||||

| ITEM 2. |

13 | |||||

| ITEM 3. |

14 | |||||

| ITEM 4. |

14 | |||||

| PART II | ||||||

| ITEM 5. |

15 | |||||

| ITEM 6. |

18 | |||||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

20 | ||||

| ITEM 7A. |

37 | |||||

| ITEM 8. |

37 | |||||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

62 | ||||

| ITEM 9A. |

62 | |||||

| ITEM 9B. |

62 | |||||

| PART III | ||||||

| ITEM 10. |

63 | |||||

| ITEM 11. |

63 | |||||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

63 | ||||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

63 | ||||

| ITEM 14. |

63 | |||||

| PART IV | ||||||

| ITEM 15. |

63 | |||||

| SIGNATURES | 64 | |||||

| EXHIBIT INDEX | ||||||

2

Table of Contents

Within this report, unless otherwise indicated, any use of the terms “CEC Entertainment,” the “Company,” “we,” “us,” and “our” refer to CEC Entertainment, Inc and its subsidiaries.

Cautionary Statement Regarding Forward-Looking Statements

Certain statements in this report, other than historical information, may be considered “forward-looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, and are subject to various risks, uncertainties and assumptions. Statements that are not historical in nature, and which may be identified by the use of words such as “may,” “should,” “could,” “believe,” “predict,” “potential,” “continue,” “plan,” “intend,” “expect,” “anticipate,” “future,” “project,” “estimate,” and similar expressions (or the negative of such expressions) are forward-looking statements. Forward-looking statements are made based on management’s current expectations and beliefs concerning future events and, therefore, involve a number of assumptions, risks and uncertainties, including the risk factors described in Item 1A “Risk Factors” of this Annual Report on Form 10-K. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may differ from those anticipated, estimated or expected. Factors that could cause actual results to differ materially from those contemplated by forward-looking statements include, but are not limited to:

| • | Our ability to successfully implement our business development strategies; |

| • | Unanticipated costs and delays in implementing our business development strategies; |

| • | Changes in consumer discretionary spending and general economic conditions; |

| • | Competition in both the restaurant and entertainment industries; |

| • | Increases in food, labor and other operating costs; |

| • | Changes in consumers’ health, nutrition and dietary preferences; |

| • | Negative publicity concerning food quality, health, safety and other issues; |

| • | Continued existence or occurrence of certain public health issues; |

| • | Loss of certain key personnel; |

| • | Disruptions in the financial markets affecting the availability and cost of credit and our ability to maintain adequate insurance coverage; |

| • | Disruption of our commodity distribution system; |

| • | Our dependence on a few global providers for the procurement of games and rides; |

| • | Government regulations, litigation, product liability claims and product recalls; |

| • | Adverse effects of local conditions, natural disasters and other events; |

| • | Fluctuations in our quarterly results of operations due to seasonality; |

| • | Disruptions of our information technology systems; |

| • | Risks in connection with owning and leasing real estate; |

| • | Our ability to adequately protect our trademarks or other proprietary rights; and |

| • | Conditions in foreign markets. |

The forward-looking statements made in this report relate only to events as of the date on which the statements were made. Except as may be required by law, we undertake no obligation to update our forward-looking statements to reflect events and circumstances after the date on which the statements were made or to reflect the occurrence of unanticipated events.

3

Table of Contents

General

Chuck E. Cheese’s® is a nationally recognized leader in family dining and entertainment. CEC Entertainment, Inc. was incorporated in the state of Kansas in 1980. We consider the family dining and entertainment center business to be our sole reportable operating segment.

Company Overview

We develop, operate and franchise family dining and entertainment centers (also referred to as “stores”) under the name “Chuck E. Cheese’s” in 48 states and seven foreign countries or territories. Chuck E. Cheese’s stores feature musical and comic entertainment by robotic and animated characters, arcade-style and skill-oriented games, video games, rides, and other activities intended to appeal to our primary customer base of families with children between two and 12 years of age. All of our stores offer dining selections consisting of a variety of beverages, pizzas, sandwiches, appetizers, a salad bar, and desserts.

We believe that the dining and entertainment components of our business are interdependent, and therefore we primarily manage and promote them as an integrated product. Our typical guest experience involves a combination of wholesome family dining and entertainment, comprised of token-operated games and rides, and attractions provided free-of-charge. This integrated product drives our business development strategies as we endeavor to drive guest traffic into our stores, benefiting both dining and entertainment revenue.

The first Chuck E. Cheese’s opened in 1977. As of January 1, 2012, we and our franchisees operate a total of 556 Chuck E. Cheese’s stores located in 48 states and seven foreign countries or territories. As of January 1, 2012, we operated 507 Company-owned Chuck E. Cheese’s stores located in 44 states and Canada and our franchisees operated a total of 49 stores located in 15 states, Puerto Rico, Guam, Guatemala, Chile, Saudi Arabia, and the United Arab Emirates. See Item 2. “Properties” for more information regarding the number and location of Chuck E. Cheese’s stores.

Business Development Strategy

Our business development strategy is focused on maintaining and evolving our existing stores, developing high sales volume Company-owned stores primarily in densely populated areas, and selling development rights to franchisees in domestic and international markets where we do not currently intend to open Company-owned stores.

Existing Stores. We believe that in order to maintain the appeal of and consumer demand for our concept, we must continually reinvest in our existing stores in situations where we believe it would enhance the experience of our customers and where we believe the return on investment warrants the capital expenditure. For our existing stores, we currently utilize the following capital initiatives: (a) game enhancements; (b) major remodels; and (c) store expansions. While initiatives such as expansions may capitalize on incremental revenue growth opportunities, we believe our capital initiatives involving major remodels and game enhancements serve more to preserve our existing sales base and cash flows over the long term.

Game enhancements include replacing a portion of the store’s games and rides with new and, to a lesser extent, refurbished equipment. We believe game enhancements are necessary to maintain the relevance and appeal of our games and rides. In addition, game enhancements enable us to introduce improvements in game and ride technology. We completed 137 game enhancements in 2011. We currently expect to enhance the games and rides at approximately 120 to 130 stores in fiscal 2012 at an average cost of approximately $0.1 million to $0.2 million per store.

We undertake periodic major remodels when there is a need to improve the overall appearance or layout of a store or when we introduce concept changes or enhancements to our stores. The major remodel initiative typically includes interior design modifications that allow us to more effectively utilize space allocated to the playroom area of the store, increasing the number of games and rides and developing a new interior identity. We completed 11 major remodel initiatives in 2011. We currently expect to complete approximately five to ten major remodels in fiscal 2012 at an average cost of approximately $0.7 million per store.

We believe store expansions improve the quality of the guests’ experience because the additional square footage allows us to increase the number and variety of games, rides, and other entertainment offerings in the expanded stores. In addition to expanding the square footage of a store, store expansions typically include all components of a major remodel and result in an increase in the store’s seat count. We completed 33 store expansions in 2011. We currently expect to complete approximately 23 to 27 store expansions in fiscal 2012 at an average cost of approximately $1.0 million per store.

4

Table of Contents

New Company Store Development. Our plan for the development of new Company-owned stores focuses on opening high sales volume stores primarily in densely populated areas. During 2011, we opened four new Company-owned stores, including two stores we relocated. The new stores we opened in 2009 and 2010, including franchisee stores we purchased, have an average square footage of approximately 14,000 to 15,000 square feet and generated average annual sales of approximately $2.0 million per store in 2011. Over the next four years we plan to accelerate our store growth plan and expect to open approximately 50 new stores, of which 12 to 15 are planned to open in 2012 at an average cost of approximately $2.6 million to $2.7 million per store. New store growth includes opening new stores and relocating existing stores and could include franchise stores we acquire.

We periodically reevaluate the site characteristics of our stores and will consider relocating a store if certain site characteristics considered essential for the success of a store deteriorate, more desirable property becomes available or we are unable to negotiate acceptable lease terms with the existing landlord.

See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information regarding our capital initiatives and related capital expenditures.

New Domestic Franchise Store Development. We added one new domestic franchise store in 2011, and we purchased one store from a franchisee in January 2012. Currently, our domestic franchisees have rights to develop an additional nine stores. We are currently offering franchise development rights in approximately 14 domestic markets.

International Growth. We maintain a formalized strategic plan for international growth as we believe that we have an opportunity to further expand the Chuck E. Cheese’s concept globally. In 2011, our international franchisees opened one new store located in Chile and one new store located in Saudi Arabia. In 2012, we plan on continuing to seek international franchise growth by actively seeking franchise partners in certain countries in Latin America, Asia, and the Middle East for franchising our concept internationally. In 2011, we signed four new franchise development agreements, which grant the right to develop a total of 22 franchise stores in Mexico, Panama, Costa Rica and Saudi Arabia. Under our international franchise agreements, we currently expect franchisees to open approximately four to six international franchise stores in fiscal 2012, three of which are currently under construction.

Store Design

Chuck E. Cheese’s are typically located in shopping centers or in free-standing buildings near shopping centers. Chuck E. Cheese’s stores are typically divided into three areas: (1) a kitchen and related areas (cashier and prize area, salad bar, manager’s office, technician’s office, restrooms, etc.), (2) a showroom area, and (3) a playroom area. The average size of our existing stores is approximately 12,000 square feet. Total table and chair seating in both the showroom and playroom areas generally average between 400 to 450 guests per store. The showroom area of each Chuck E. Cheese’s typically features a variety of comic and musical entertainment by life-sized animatronic characters, together with video monitors and animated props, arranged in various stage-type settings. The playroom area features a variety of arcade-style and skill-oriented games, video games, rides, and other forms of entertainment.

Food and Beverages

Each Chuck E. Cheese’s offers a variety of pizzas, sandwiches, appetizers, a salad bar, and desserts. Soft drinks, coffee, and tea are also served, along with beer and wine where permitted by local laws. We continuously focus on delivering a quality-driven product and believe the quality of our food compares favorably with that of our competitors. We believe the introduction of a new pizza in 2011 has provided a very consistent and improved product to our customer. The majority of the food, beverages, and other supplies used in Company-owned stores are currently distributed under a system-wide agreement with a major food distributor. We believe that this distribution system creates certain cost and operational efficiencies for us.

Approximately 47.7%, 49.0%, and 49.9% of our Company store sales were derived from food and beverage sales during fiscal years 2011, 2010, and 2009, respectively.

Entertainment and Merchandise

Each Chuck E. Cheese’s store includes a showroom area featuring musical entertainment presented by life-sized animatronic characters and playroom area offering arcade-style and skill-oriented games, video games, rides, and other forms of entertainment. Tokens are used to activate the games and rides in the playroom area. All of our games and rides are activated with one token. A number of skill-oriented games dispense tickets that can be redeemed by guests for prize merchandise such as toys and plush items. Our guests can also purchase this merchandise directly for cash. Also included in the playroom area of our stores are tubes and tunnels suspended from or reaching to the ceiling known as Sky Tubes® or other free attractions for young children. We place a limited amount of table and chair seating in the playroom areas of our Company-owned store so that parents can more closely observe and interact with their children as they play the games and ride the rides.

Approximately 52.3%, 51.0%, and 50.1% of our Company store sales were derived from entertainment and merchandise sales during fiscal years 2011, 2010, and 2009, respectively.

5

Table of Contents

Marketing

The primary customer base for our stores consists of families with children between two and 12 years of age. We conduct advertising campaigns focused on families with young children that feature the family entertainment experiences available at Chuck E. Cheese’s with the primary objective of increasing the frequency of customer visits. Our advertising campaign generally includes TV, radio, print, interactive and social media, in-store, and other promotional components. While the primary advertising medium we use continues to be television, due to its broad access to family audiences and our belief in its ability to effectively communicate the Chuck E. Cheese’s experience, we intend to increase our advertising online and on radio, as well as our overall advertising to parents. The television advertising campaigns are supplemented by promotional offers in newspapers, cross promotions with companies that target a similar customer base, our website, Internet advertising campaigns, and e-mail.

Franchising

As of January 1, 2012, a total of 49 Chuck E. Cheese’s stores were operated by our franchisees. Of these stores, 36 are located domestically in the United States and 13 are located internationally in Puerto Rico, Guam, Guatemala, Chile, Saudi Arabia, and the United Arab Emirates.

Our standard franchise agreement grants to the franchisee the right to construct and operate a store and use our associated trade names, trademarks, and service marks within the standards and guidelines established by us. Most of our existing franchise agreements have an initial term of 15 to 20 years and include a 10-year renewal option. The standard agreement provides us with a right of first refusal should a franchisee decide to sell a store. We may enter into area development agreements, which grant franchisees exclusive rights to open a specified number of stores in a designated geographic area within a specified period of time. In addition to an initial franchise fee, the franchisee is charged a continuing monthly royalty fee equal to a certain percentage of their gross monthly sales.

We and our franchisees created the International Association of CEC Entertainment, Inc. (the “Association”) to discuss and consider matters of common interest relating to the operation of Company-owned and franchised Chuck E. Cheese’s. Routine business matters of the Association are conducted by a board of directors of the Association, composed of five members appointed by us and five members elected by the franchisees. The Association serves as an advisory council, which among other responsibilities, oversees expenditures from the funds established and managed by the Association. These funds include (1) the Advertising Fund, a fund that pays the costs of development, purchasing and placement of advertising programs, including Internet website, (2) the Entertainment Fund, a fund established to develop and improve audio-visual and animated entertainment attractions, as well as the development and implementation of new entertainment concepts, and (3) the Media Fund, a fund primarily designated for the purchase of national network television advertising. The Association is included in our Consolidated Financial Statements as a variable interest entity in which we have a controlling interest.

The franchise agreements governing existing franchised Chuck E. Cheese’s in the United States currently require each franchisee to pay to the Association a monthly contribution equal to a certain percentage of their gross monthly sales. Additionally, under these franchise agreements, we are required, with respect to Company-owned stores, to spend for local advertising and to contribute to the Advertising Fund and the Entertainment Fund at the same rates as our franchisees. We and our franchisees could be required to make additional contributions to fund any deficits that may be incurred by the Association. The franchise agreements governing existing franchised Chuck E. Cheese’s outside of the United States currently require each franchisee to pay a certain percentage of their gross monthly sales to us to fund various advertising and media costs.

Approximately 0.6%, 0.5%, and 0.5% of our total revenues were derived from royalties, franchise and area development fees and other miscellaneous franchise income during fiscal years 2011, 2010, and 2009, respectively.

Foreign Operations

As of January 1, 2012, we operated a total of 14 Company-owned stores in Canada. During fiscal years 2011, 2010, and 2009, our Canada stores generated total revenues of approximately $22.2 million, $21.8 million, and $20.8 million, respectively, representing approximately 2.7%, 2.7%, and 2.5% of our total revenues in each respective fiscal year. As of January 1, 2012, approximately $18.4 million, or approximately 2.7%, of the total net book value of our long-lived assets were located in Canada.

Additionally, as of January 1, 2012, our international franchisees operated a total of 13 stores located in Puerto Rico, Guam, Guatemala, Chile, Saudi Arabia, and the United Arab Emirates. The total revenues derived from our international franchisees are not material in relation to our total revenues.

These foreign activities are subject to various risks of conducting business in a foreign country, including changes in foreign currency, laws and regulations and economic and political stability. See Item 1A. “Risk Factors” for more information regarding the risks associated with our operations located in foreign markets. As of January 1, 2012, we do not believe that we are materially dependent on these foreign operations.

Suppliers

We currently use a network of 20 distribution centers owned by a single distributor to distribute most of the products and supplies used in our stores. We have not entered into any hedging arrangements to reduce our exposure to commodity price volatility associated with commodity prices; however, we typically enter into short term purchasing arrangements, which may contain pricing designed to minimize the impact of commodity price fluctuations.

We procure games, rides, and other entertainment-related equipment from a limited number of suppliers. The number of suppliers from which we purchase games, rides, and other entertainment-related equipment has declined due to industry consolidation over the past several years coupled with a lower overall global demand.

6

Table of Contents

Competition

The family dining industry and the entertainment industry are highly competitive, with a number of major national and regional chains operating in each of these spaces. In this regard, we compete for customers on the basis of (1) our name recognition; (2) the price, quality, variety, and perceived value of our food and entertainment offerings; (3) the quality of our customer service, and (4) the convenience and attractiveness of our facilities. Although there are other concepts that presently utilize the combined family dining and entertainment format, these competitors primarily operate on a regional or market-by-market basis. To a lesser extent, we may also compete directly and/or indirectly with other dining and entertainment formats including, full-service and quick-service restaurants appealing to families with young children, the quick service pizza segment, movie theaters, and themed amusement attractions.

We believe that our principal competitive strengths consist of our established recognized brand, the quality of the food and service we provide our customer, the quality and variety of our entertainment offerings, and the location and attractiveness of our stores. We also believe that our competitive strengths include our tenured management team’s knowledge of the family dining and entertainment industries relative to our target market of families with young children.

Intellectual Property

We own various trademarks, including “Chuck E. Cheese’s” and the Chuck E. Cheese character image used in connection with our business, which have been registered with the appropriate patent and trademark offices. The duration of such trademarks is unlimited, subject to continued use and renewal. We believe that we hold the necessary rights for protection of the trademarks considered essential to conduct our business. We believe our trade name and our ownership of trademarks in the names and character likenesses featured in the operation of our stores provide us with an important competitive advantage and we actively seek to protect our interests in such property.

Seasonality

Our operating results fluctuate seasonally due to the timing of school vacations, holidays, and changing weather conditions. As a result, we typically generate higher sales volumes during the first and third quarters of each fiscal year. School operating schedules, holidays, and weather conditions may affect sales volumes in some operating regions differently than others. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved for the full fiscal year.

Government Regulation

We and our franchisees are subject to various federal, state and local laws and regulations affecting the development and operation of Chuck E. Cheese’s, including, but not limited to, those that impose restrictions, levy a fee or tax, or require a permit or license, or other regulatory approval, and those that relate to the operation of video and arcade games and rides, the preparation and sale of food and beverages, the sale and service of alcoholic beverages, and building and zoning requirements. We and our franchisees are also subject to laws governing relationships with employees, including minimum wage requirements, overtime, working and safety conditions, immigration status requirements, and child labor laws. A significant portion of our store personnel are paid at rates related to the minimum wage established by federal, state, and municipal law and, accordingly, increases in such minimum wage result in higher labor costs to us. We are also subject to the Fair Labor Standards Act, the Americans with Disabilities Act, and Family Medical Leave Act mandates. In addition, we are subject to regulation by the Federal Trade Commission, Federal Communications Commission, and must also comply with certain state laws, which govern the offer, sale, and termination of franchises and the refusal to renew franchises.

Working Capital Practices

Information about our working capital practices is contained under the caption “Overview of Liquidity” included in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

Employees

As of January 1, 2012, we employed approximately 17,300 employees, including approximately 16,900 in the operation of our Company-owned stores and approximately 400 employed in our corporate office. None of our employees are members of any union or collective bargaining group. We believe that our employee relations are satisfactory and we have not experienced any work stoppages at any of our stores.

Each Chuck E. Cheese’s store typically employs a general manager, one or two managers, an electronic specialist who is responsible for repair and maintenance of the animatronic characters, games and rides, and approximately 20 to 40 food preparation and service employees, many of whom work part-time. Our staffing requirements are seasonal and the number of people we employ at our stores will fluctuate throughout the year.

7

Table of Contents

Available Information

Our principal executive offices are located at 4441 W. Airport Freeway, Irving, Texas 75062, and our telephone number is (972) 258-8507. We maintain a website at www.chuckecheese.com.

We file annual, quarterly and current reports, proxy statements, and other information with the United States Securities and Exchange Commission (the “SEC”). You may read and copy any reports, statements and other information filed by us at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549-0102. Please call (800) SEC-0330 for further information on the Public Reference Room. The SEC also maintains an Internet website (www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers, including us, that we file electronically with the SEC.

We make available, free of charge, on or through the investor information section of our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, statements of changes in beneficial ownership of securities, and amendments to those reports and statements as soon as reasonably practicable after electronic filing or furnishing of such material with the SEC. The address for our website is www.chuckecheese.com.

Documents available on our website include, among others, our (a) Corporate Governance Guidelines, (b) Code of Business Conduct and Ethics, (c) Code of Ethics for the Chief Executive Officer, President and Senior Financial Officers (the “Code of Ethics”), (d) Complaint and Reporting Procedures for Accounting and Auditing Matters, and (e) Charters for the Audit, Compensation, and Nominating/Corporate Governance Committees of the Board of Directors. These documents are also available in print, free of charge, to any stockholder who requests a copy from the Secretary, Meredith W. Bjorck, at 4441 W. Airport Freeway, Irving, Texas 75062. We intend to disclose future amendments to, or waivers from, certain provisions of the Code of Ethics on our website.

Our business operations and the implementation of our business strategy are subject to significant risks inherent in our business, including, without limitation, the risks and uncertainties described below. The occurrence of any one or more of the risks or uncertainties described below and elsewhere in this Annual Report on Form 10-K could have a material effect on our financial condition, results of operations and cash flows. While we believe we have identified and discussed below the key risk factors that affect our business, there may be additional risks and uncertainties that are not presently known or that are not currently believed to be significant that may adversely affect our business, operations, industry, financial position and financial performance in the future. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond our control or are subject to change, actual results could be materially different.

We may not be successful in the implementation of our business development strategies, which could adversely affect our business and our consolidated results of operations.

Our continued growth depends, to a significant degree, on our ability to successfully implement our long-term growth strategies. As part of our long-term growth strategy, we plan to open additional new stores in selected markets, remodel and expand certain of our existing stores and upgrade the games, rides and entertainment at some of our existing stores. The opening and success of new Chuck E. Cheese’s stores is dependent on various factors, including but not limited to the availability of suitable sites, the negotiation of acceptable lease terms for such locations, our ability to meet construction schedules, our ability to manage such expansion and hire and train personnel to manage the new stores, the potential cannibalization of sales at our adjacent stores located in the market, as well as general economic and business conditions. Our ability to successfully open new stores or remodel, expand, or upgrade the entertainment at existing stores will also depend upon the availability of sufficient capital for such purposes, including operating cash flow, our existing credit facility, future debt financings, future equity offerings, or a combination thereof. There can also be no assurance that we will be successful in opening and operating the number of anticipated new stores on a timely or profitable basis. There can be no assurance that we can continue to successfully remodel or expand our existing facilities or upgrade the games and entertainment. Our growth is also dependent on our ability to continually evolve and update our business model to anticipate and respond to changing customer needs and competitive conditions. There can be no assurance that we will be able to successfully anticipate changes in competitive conditions or customer needs or that the market will accept our business model.

Part of our growth strategy depends on our ability to attract new international franchisees to recently opened markets and the ability of these franchisees to open and operate new stores on a profitable basis. As we do not have a history of significant international growth experience, there can be no assurance that we will be able to successfully execute this strategy in the future. Delays or failures in identifying desirable franchise partners and opening new franchised stores could adversely affect our planned growth. Our new franchisees depend on the availability of financing to construct and open new stores. If these franchisees experience difficulty in obtaining adequate financing for these purposes, our growth strategy and franchise revenues may be adversely affected.

8

Table of Contents

We may incur significant costs and experience significant delays in connection with our business development strategies, which could impair our ability to grow our business and could harm our consolidated results of operations.

Our long-term growth is dependent on the success of strategic initiatives to increase the number of our stores, enhance the facilities of existing stores and effectively advertise and market our concept to our target audience. We incur significant costs each time we open a new store and other expenses when we relocate or remodel existing stores. The expenses of opening, relocating or remodeling any of our stores may be higher than anticipated. If we are unable to open or are delayed in opening new or relocated stores, we may incur significant costs, which may adversely affect our consolidated financial results. If we are unable to remodel or are delayed in remodeling stores, we may incur significant costs, which may adversely affect our consolidated financial results. In addition, our inability to effectively implement our marketing and advertising strategies may adversely affect our consolidated financial results.

Changes in consumer discretionary spending and general economic conditions could reduce sales at our stores and have an adverse effect on our consolidated financial results.

Purchases at our stores are discretionary for consumers and, therefore, our results of operations are susceptible to economic slowdowns and recessions. We are dependent in particular upon discretionary spending by consumers living in the communities in which our stores are located. A significant portion of our stores are clustered in certain geographic areas. Currently, a total of 166 Chuck E. Cheese’s stores are located in California, Texas, and Florida (163 are Company-owned and 3 are franchised locations). A significant weakening in the local economies of these geographic areas, or any of the areas in which our stores are located, may cause consumers to curtail discretionary spending, which in turn could reduce our Company store sales and have an adverse effect on our consolidated financial results.

The future performance of the U.S. and global economies are uncertain and are directly affected by numerous national and global financial and other factors that are beyond our control. Increases in credit card, home mortgage and other borrowing costs and declines in housing values could weaken the U.S. economy leading to a decrease in consumer spending. It is difficult to predict the severity and the duration of such a decrease. We believe that consumers generally are more willing to make discretionary purchases, including at our stores, during periods in which favorable economic conditions prevail. Further, fluctuations in the retail price of gasoline and the potential for future increases in gasoline and other energy costs may affect consumers’ disposable incomes available for entertainment and dining. Changes in consumer spending habits as a result of a recession or a reduction in consumer confidence are likely to reduce our sales performance, which could have a material effect on our business, results of operations or financial condition. In addition, these economic factors may affect our level of spending on planned capital initiatives at our stores, and thereby impact our future sales.

The restaurant and entertainment industries are highly competitive and that competition could harm our consolidated operating results.

We believe that our combined restaurant and entertainment center concept puts us in a niche, which combines elements of both the restaurant and entertainment industries. As a result, to some degree, we compete with entities in both industries. The family dining industry and the entertainment industry are highly competitive, with a number of major national and regional chains operating in each of these spaces. Although other restaurant chains presently utilize the concept of combined family dining-entertainment operations, we believe these competitors operate primarily on a local, regional, or market-by-market basis. Within the traditional restaurant sector, we compete with other casual dining restaurants on a nationwide basis with respect to price, quality and speed of service, type and quality of food, personnel, the number and location of restaurants, attractiveness of facilities, effectiveness of advertising and marketing programs, and new product development. Such competitive market conditions, including the effectiveness of our advertising and promotion and the emergence of significant new competition, could adversely affect our consolidated financial results.

Increases in food, labor, and other operating costs could adversely affect our profitability.

The performance of our stores is affected by changes in the costs for food products we purchase, including cheese, dough, chicken, and beef. The commodity prices for these food products vary throughout the year and may be affected by changes in demand, supply, and other factors beyond our control. A material increase in our food costs could negatively affect our profit margins and adversely affect our consolidated financial results.

A significant number of our store-level employees are subject to various minimum wage requirements. Several states and cities in which we operate stores have established a minimum wage higher than the federally mandated minimum wage. There may be similar increases implemented in other jurisdictions in which we operate or seek to operate. Changes in the minimum wage could increase our labor costs and may have an adverse effect on our profit margins and our consolidated financial results.

The performance of our stores is also adversely affected by increases in the price of utilities on which the stores depend, such as natural gas, whether as a result of inflation, shortages, or interruptions in supply, or otherwise. Our business also incurs significant costs for and including among other things, insurance, marketing, taxes, real estate, borrowing, and litigation, all of which could increase due to inflation, rising interest rates, changes in laws, competition, or other events beyond our control.

Changes in consumers’ health, nutrition, and dietary preferences could adversely affect demand for our menu offerings and adversely affect our consolidated financial results.

Our industry is affected by consumer preferences and perceptions. Changes in prevailing health or dietary preferences and perceptions may cause consumers to avoid certain products we offer in favor of alternative or healthier foods. If consumer eating habits change significantly and we are unable to respond with appropriate menu offerings, it could adversely affect our consolidated financial results.

9

Table of Contents

Negative publicity concerning food quality, health, safety or other issues could negatively affect our brand image and adversely affect our consolidated financial results.

Food service businesses can be adversely affected by litigation and complaints from guests, consumer groups or government authorities resulting from food quality, illness, injury or other health concerns or operating issues stemming from one store or a limited number of stores. Publicity concerning food-borne illnesses, injuries caused by food tampering and safety issues may negatively affect our operations, reputation and brand. Such publicity may have a significant adverse impact on our consolidated financial results.

Our target market of children between the ages of two and 12 and families with young children may be highly sensitive to adverse publicity that may arise from an actual or perceived negative event within one or more of our stores. There can be no assurance that we will not experience negative publicity regarding one or more of our stores, and the existence of negative publicity could materially and adversely affect our brand image with our customers and our consolidated financial results.

Public health issues may adversely affect our consolidated financial results,

Our business may be impacted by certain public health issues including epidemics, pandemics and the rapid spread of certain illness and contagious diseases. To the extent that our guests feel uncomfortable visiting public locations, particularly locations with a large number of children, due to a perceived risk of exposure to a public health issue, we could experience a reduction in guest traffic, which could adversely affect our consolidated financial results.

We are dependent on the service of certain key personnel, and the loss of any of these personnel could harm our business.

The success of our business is highly dependent upon the continued employment of Richard M. Frank, our Executive Chairman, Michael H. Magusiak, our President and Chief Executive Officer, and other members of our senior management team. Although the Company has entered into employment agreements with each of Mr. Frank and Mr. Magusiak, they can voluntarily leave the Company at any time and the loss of the services of either of such individuals could have a material adverse effect upon our business and development. Our success will also depend upon our ability to retain and attract additional skilled management personnel to our senior management team and at our operational level. There can be no assurances that we will be able to retain the services of Messrs. Frank or Magusiak, senior members of our management team or the required operational support at the store level in the future.

Disruptions in the financial markets may adversely affect the availability and cost of credit and compromise our ability to maintain adequate insurance coverage.

Disruptions in the financial markets may adversely affect the availability of credit already arranged and the availability and cost of credit in the future. Failures of significant financial institutions could adversely affect our access to and reduce the alternative sources of liquidity needed to operate our business. Any disruption could require us to take measures to conserve cash until the markets stabilize or until alternative credit arrangements or other funding for our business needs can be arranged. Such measures could include deferring or curtailing our capital expenditures and other discretionary uses of cash.

We rely on insurance to mitigate our exposure to catastrophic losses we may sustain to our property, claims by our employees, customers, or other third parties. Although we believe we have historically obtained adequate levels of insurance coverage through well rated and capitalized firms, disruptions in the financial markets may affect our ability to obtain coverage under existing policies or purchase insurance under new policies at reasonable rates in the future. Additionally, we are potentially at risk if our insurance carriers become insolvent. As a result, we could potentially be exposed to financial losses, which could adversely affect our consolidated financial results.

Any disruption of our commodity distribution system, which currently utilizes a single distributor, could adversely affect our business and our consolidated financial results.

We use a single distributor to distribute most of the products and supplies used in our stores. Any failure by this distributor to adequately distribute products or supplies to our stores could increase our costs and have a material adverse effect on our consolidated financial results and our operations.

Our procurement of games and rides is dependent upon a few global providers, the loss of any of whom could adversely affect our business.

Our ability to continue to procure new games, rides, and other entertainment-related equipment is important to our business strategy. The number of suppliers from which we can purchase games, rides, and other entertainment-related equipment is limited due to industry consolidation over the past several years coupled with a lower overall global demand. To the extent that the number of suppliers continues to decline, we could be subject to the risk of distribution delays, pricing pressure, lack of innovation, and other associated risks.

10

Table of Contents

We are subject to various government regulations, which may adversely affect our operations and financial performance.

The development and operation of our stores are subject to various federal, state, and local laws and regulations in many areas of our business, including, but not limited to, those that impose restrictions, levy a fee or tax, or require a permit or license, or other regulatory approval, and those that relate to the operation of video and arcade games and rides, the preparation of food and beverages, the sale and service of alcoholic beverages, and building and zoning requirements. Difficulties or failure in obtaining required permits, licenses, or other regulatory approvals could delay or prevent the opening of a new store, and the suspension of, or inability to renew, a license or permit could interrupt operations at an existing store. We are also subject to laws governing our relationship with employees, including minimum wage requirements, overtime, health insurance mandates, working and safety conditions, immigration status requirements, and child labor laws. Additionally, potential changes in federal labor laws, including “card check” regulations, could result in portions of our workforce being subjected to greater organized labor influence. This could result in an increase to our labor costs. A significant portion of our store personnel are paid at rates related to the minimum wage established by federal, state and municipal law. Increases in such minimum wage result in higher labor costs, which may be partially offset by price increases and operational efficiencies. Additionally, we are subject to certain laws and regulations that govern our handling of customers’ personal information. A failure to protect the integrity and security of our customers’ personal information could expose us to litigation, as well as materially damage our reputation with our customers. While we endeavor to comply with all applicable laws and regulations, governmental and regulatory bodies may change such laws and regulations in the future, which may require us to incur substantial cost increases. If we fail to comply with applicable laws and regulations, we may be subject to various sanctions, and/or penalties and fines or may be required to cease operations until we achieve compliance, which could have a material adverse effect on our consolidated financial results and operations.

Our stores may be adversely affected by local conditions, natural disasters, and other events.

Certain regions in which our stores are located may be subject to adverse local conditions, natural disasters, and other events. If severe weather, such as heavy snowfall or extreme temperatures, discourages or restricts customers in a particular region from traveling to our stores, our sales could be adversely affected. If severe weather conditions occur during the first and third quarters of the year, the adverse impact to our sales and profitability could be even greater than at other times during the year because we generate a significant portion of our sales and profits during these periods. Natural disasters including tornadoes, hurricanes, floods, and earthquakes may damage our stores or other operations, which may adversely affect our consolidated financial results. Additionally, demographic shifts in the areas where our stores are located could adversely impact our consolidated financial results and operations.

Our business is highly seasonal and quarterly results may fluctuate significantly as a result of this seasonality.

We have experienced, and in the future could experience, quarterly variations in revenues and profitability as a result of a variety of factors, many of which are outside our control, including the timing of school vacations, holidays, and changing weather conditions. We typically generate higher sales volumes and profitability in the first and third quarters of each fiscal year compared to the second and fourth quarters. If there is a material decrease in the guest traffic in our stores during the first and third quarters of the year, our operating results will be adversely affected for that quarter and further, may have an adverse effect on our consolidated financial results for the fiscal year.

We face litigation risks from customers, employees, franchisees and other third parties in the ordinary course of business.

Our business is subject to the risk of litigation by customers, current and former employees, suppliers, stockholders, or others through private actions, class actions, administrative proceedings, regulatory actions, or other litigation. The outcome of litigation, particularly class action lawsuits and regulatory actions, is difficult to assess or quantify. Plaintiffs in these types of lawsuits may seek recovery of very large or indeterminate amounts, and the magnitude of the potential loss relating to such lawsuits may remain unknown for substantial periods of time. The cost to defend future litigation may be significant. There may also be adverse publicity associated with litigation that could decrease customer acceptance of our food or entertainment offerings, regardless of whether the allegations are valid or whether we are ultimately found liable.

We face risks with respect to product liability claims and product recalls, which could adversely affect our reputation, our business, and our consolidated results of operations.

We purchase merchandise from third-parties and offer this merchandise to customers in exchange for prize tickets or for sale. This merchandise could be subject to recalls and other actions by regulatory authorities. Changes in laws and regulations could also impact the type of merchandise we offer to our customers. We have experienced, and may in the future experience, issues that result in recalls of merchandise. In addition, individuals have asserted claims, and may in the future assert claims, that they have sustained injuries from third-party merchandise offered by us, and we may be subject to future lawsuits relating to these claims. There is a risk that these claims or liabilities may exceed, or fall outside of the scope of, our insurance coverage. Any of the issues mentioned above could result in damage to our reputation, diversion of development and management resources, or reduced sales and increased costs, any of which could harm our business.

If we are unable to maintain and protect our information technology systems and technologies, we could suffer disruptions in our business, damage our reputation with customers, and incur substantial costs.

The operation of our business is heavily dependent upon the implementation, integrity, security, and successful functioning of our computer networks and information systems, including the point-of-sales systems in our stores, data centers that process transactions, and various software applications used in our operations. In the ordinary course of our business, we also collect and store sensitive data, including intellectual property, our proprietary business information and that of our customers, suppliers and business partners, and personally identifiable information of our customers and employees, our computer networks and information systems. A failure of our systems to operate effectively as a result of a cyber attack, damage to, interruption, or failure of any of these systems could result in a failure to meet our reporting obligations, or result in material misstatements in our consolidated financial statements, or cause losses due to disruption of our business operations. These adverse situations could also lead to loss of sales or profits or cause us to incur additional development costs. In addition, despite our efforts to secure our computer networks and information systems, security could be compromised or confidential information could be misappropriated resulting in a loss of customers’ or employees’ personal information, negative publicity, harm to our business and reputation, or cause us to incur costs to reimburse third parties for damages.

11

Table of Contents

We are continuously subject to risks from litigation and regulatory action regarding advertising to our market of children between the ages of two and 12 years old. In addition, since certain of our stores serve alcoholic beverages, we are subject to “dram shop” statutes. These statutes generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. Although we believe we are adequately covered by insurance, a judgment against us under a “dram shop” statute in excess of the liability covered could have a material adverse effect on our business, consolidated results of operations, cash flows, and financial condition.

Under certain circumstances plaintiffs may file certain types of claims, which may not be covered by insurance. In some cases, plaintiffs may seek punitive damages, which may also not be covered by insurance. Any litigation we face could have a material adverse effect on our business, consolidated results of operations, cash flows, and financial condition.

We are subject to risks in connection with owning and leasing real estate, which could adversely affect our consolidated results of operations.

As an owner and lessee of the land and/or building for our Company-owned stores, we are subject to all of the risks generally associated with owning and leasing real estate, including changes in the supply and demand for real estate in general and the supply and demand for the use of the stores. Any obligation to continue making rental payments with respect to leases for closed stores could adversely affect our consolidated financial results.

We may not be able to adequately protect our trademarks or other proprietary rights, which could harm our business.

We own certain common law trademark rights and a number of federal and international trademark and service mark registrations and proprietary rights relating to our operations. We believe that our trademarks and other proprietary rights are important to our success and our competitive position. We, therefore, devote appropriate resources to the protection of our trademarks and proprietary rights. The protective actions that we take, however, may not be enough to prevent unauthorized usage or imitation by others, which could harm our image, brand, or competitive position and, if we commence litigation to enforce our rights, we may incur significant legal fees.

We cannot be assured that third parties will not claim that our trademarks or menu offerings infringe upon their proprietary rights. Any such claim, whether or not it has merit, may result in costly litigation, cause delays in introducing new menu items in the future, interfere with our international development agreements, or require us to enter into royalty or licensing agreements. As a result, any such claim could have a material adverse effect on our business, results of operations, cash flows, and financial condition.

Unanticipated conditions in foreign markets could adversely affect our ability to operate effectively in those markets.

In addition to our stores in the United States, we currently own stores in Canada. In addition, franchisees own stores domestically and in Puerto Rico, Guam, Guatemala, Chile, Saudi Arabia and the United Arab Emirates. We and our franchisees are subject to the regulatory and economic and political conditions of any foreign market in which we and our franchisees operate stores. Any change in the laws and regulations and economic and political stability of these foreign markets may adversely affect our consolidated financial results. Changes in foreign markets that may affect our consolidated financial results include, but are not limited to, taxation, inflation, currency fluctuations, political instability, economic instability, war, increased regulations and quotas, tariffs, and other protectionist measures. Additionally, our long-term growth strategy includes adding franchisees in additional foreign markets in the future. To the extent unfavorable conditions exist in the foreign markets we plan to expand into, we and our international franchise partners may not be successful in opening the number of anticipated new stores on a timely and profitable basis. Delays or failures in opening new foreign market store locations could adversely affect our planned growth.

ITEM 1B. Unresolved Staff Comments.

None.

12

Table of Contents

The following table summarizes information regarding the number and location of stores we and our franchisees operated as of January 1, 2012:

| Domestic |

Company- Owned Stores |

Franchised Stores |

Total | |||||||||

| Alabama |

6 | 1 | 7 | |||||||||

| Alaska |

1 | - | 1 | |||||||||

| Arizona |

2 | 7 | 9 | |||||||||

| Arkansas |

6 | - | 6 | |||||||||

| California |

77 | 3 | 80 | |||||||||

| Colorado |

10 | - | 10 | |||||||||

| Connecticut |

6 | 1 | 7 | |||||||||

| Delaware |

2 | - | 2 | |||||||||

| Florida |

26 | - | 26 | |||||||||

| Georgia |

16 | - | 16 | |||||||||

| Hawaii |

- | 2 | 2 | |||||||||

| Idaho |

1 | - | 1 | |||||||||

| Illinois |

22 | - | 22 | |||||||||

| Indiana |

13 | - | 13 | |||||||||

| Iowa |

5 | - | 5 | |||||||||

| Kansas |

4 | - | 4 | |||||||||

| Kentucky |

5 | - | 5 | |||||||||

| Louisiana |

9 | 2 | 11 | |||||||||

| Maine |

1 | - | 1 | |||||||||

| Maryland |

14 | - | 14 | |||||||||

| Massachusetts |

11 | - | 11 | |||||||||

| Michigan |

18 | - | 18 | |||||||||

| Minnesota |

6 | - | 6 | |||||||||

| Mississippi |

3 | 2 | 5 | |||||||||

| Missouri |

8 | - | 8 | |||||||||

| Montana |

- | 1 | 1 | |||||||||

| Nebraska |

2 | - | 2 | |||||||||

| Nevada |

6 | - | 6 | |||||||||

| New Hampshire |

2 | - | 2 | |||||||||

| New Jersey |

15 | - | 15 | |||||||||

| New Mexico |

3 | - | 3 | |||||||||

| New York |

22 | - | 22 | |||||||||

| North Carolina |

13 | 2 | 15 | |||||||||

| North Dakota |

- | 1 | 1 | |||||||||

| Ohio |

19 | 1 | 20 | |||||||||

| Oklahoma |

3 | - | 3 | |||||||||

| Oregon |

1 | 3 | 4 | |||||||||

| Pennsylvania |

23 | - | 23 | |||||||||

| Rhode Island |

1 | - | 1 | |||||||||

| South Carolina |

7 | - | 7 | |||||||||

| South Dakota |

2 | - | 2 | |||||||||

| Tennessee |

12 | - | 12 | |||||||||

| Texas |

60 | - | 60 | |||||||||

| Utah |

- | 3 | 3 | |||||||||

| Virginia |

11 | 4 | 15 | |||||||||

| Washington |

9 | 3 | 12 | |||||||||

| West Virginia |

1 | - | 1 | |||||||||

| Wisconsin |

9 | - | 9 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total domestic |

493 | 36 | 529 | |||||||||

|

|

|

|

|

|

|

|||||||

| International |

||||||||||||

| Canada |

14 | - | 14 | |||||||||

| Chile |

- | 3 | 3 | |||||||||

| Guam |

- | 1 | 1 | |||||||||

| Guatemala |

- | 2 | 2 | |||||||||

| Puerto Rico |

- | 3 | 3 | |||||||||

| Saudi Arabia |

- | 3 | 3 | |||||||||

| United Arab Emirates |

- | 1 | 1 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total international |

14 | 13 | 27 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total stores in operation |

507 | 49 | 556 | |||||||||

|

|

|

|

|

|

|

|||||||

13

Table of Contents

Company Store Leases

Of the 507 Company-owned Chuck E. Cheese’s stores as of January 1, 2012, 59 occupy owned premises and 448 are leased.

The terms of our store leases vary in length from lease to lease, although a typical lease provides for an initial primary term of 10 years, with two additional five-year options to renew. As of January 1, 2012, four of our leases were month-to-month and the current lease terms (i.e., before consideration of available renewal option periods) of our remaining 444 store leases will expire on various dates through 2028 and provide renewal options that expire at various dates through 2045, as described in the table below:

| Current Noncancelable Lease Term to Expire |

Number of Stores |

Available

Renewal Options Expiring Through |

||||||

| 2012 |

24 | 2017 - 2032 | ||||||

| 2013 |

44 | 2018 - 2033 | ||||||

| 2014 |

53 | 2019 - 2034 | ||||||

| 2015 |

64 | 2020 - 2035 | ||||||

| 2016 |

60 | 2021 - 2036 | ||||||

| 2017 through 2028 |

199 | 2022 - 2045 | ||||||

|

|

|

|||||||

| 444 | ||||||||

|

|

|

|||||||

These leases generally require us to pay the cost of repairs, other maintenance costs, insurance, and real estate taxes and, in some instances, may provide for additional rent equal to the amount by which a percentage of revenues exceed the minimum rent. It is common for us to take possession of leased premises prior to the commencement of rent payments for the purpose of constructing leasehold improvements.

Corporate Office and Warehouse Facilities

We lease a 76,556 square foot office building in Irving, Texas, which serves as our corporate office and support services center. This lease expires in May 2015, with options to renew through May 2025.

We also have separate leases for three warehouse buildings for a total of 169,030 square feet of warehouse space in Topeka, Kansas, which primarily serves as storage and refurbishing facilities for our store fixtures and game equipment. One lease is on a month-to-month basis and the other two leases will expire in August and September 2013, respectively.

From time to time, we are involved in various inquiries, investigations, claims, lawsuits, and other legal proceedings that are incidental to the conduct of our business. These matters typically involve claims from customers, employees or other third parties involved in operational issues common to the retail, restaurant and entertainment industries. Such matters typically represent actions with respect to contracts, intellectual property, taxation, employment, employee benefits, personal injuries and other matters. A number of such claims may exist at any given time and there are currently a number of claims and legal proceedings pending against us.

In the opinion of our management, after consultation with legal counsel, the amount of liability with respect to claims or proceedings currently pending against us is not expected to have a material effect on our consolidated financial condition, results of operations or cash flows.

ITEM 4. Mine Safety Disclosures.

None.

14

Table of Contents

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock is listed on the New York Stock Exchange under the symbol “CEC”. The following table sets forth the highest and lowest sale price for our common stock during each quarterly period within the two most recent fiscal years, as reported on the New York Stock Exchange:

| Fiscal 2011 | Fiscal 2010 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| 1st Quarter |

$ | 39.66 | $ | 35.42 | $ | 38.56 | $ | 31.93 | ||||||||

| 2nd Quarter |

$ | 42.71 | $ | 35.75 | $ | 41.79 | $ | 34.39 | ||||||||

| 3rd Quarter |

$ | 42.75 | $ | 25.83 | $ | 37.38 | $ | 30.44 | ||||||||

| 4th Quarter |

$ | 35.71 | $ | 26.63 | $ | 41.36 | $ | 32.51 | ||||||||

As of February 13, 2012, there were approximately 1,867 stockholders of record. The number of stockholders of record does not include a substantially greater number of beneficial holders of our common stock, whose shares are held in “street name” with brokers, banks, and other financial institutions.

Dividends and Issuer Purchases of Equity Securities

On February 22, 2011, our Board of Directors (“Board”) approved the initiation of a quarterly cash dividend of $0.20 per share and on November 1, 2011, increased the quarterly cash dividend by 10% to $0.22 per share. We expect to continue to pay quarterly dividends. However, there can be no assurance that future dividends will be declared or paid.

No dividends were declared during 2010. The table below presents dividends declared during 2011:

| Declaration Date |

Record Date | Dividend Payable Date |

Dividend Payable per Share |

Total Amount of Dividends Declared |

||||||||||||

| February 22, 2011 |

March 24, 2011 | April 21, 2011 | $ | 0.20 | $ | 4.0 million | ||||||||||

| May 3, 2011 |

June 2, 2011 | July 7, 2011 | 0.20 | 3.9 million | ||||||||||||

| August 2, 2011 |

September 8, 2011 | October 6, 2011 | 0.20 | 3.8 million | ||||||||||||

| November 1, 2011 |

December 1, 2011 | January 5, 2012 | 0.22 | 4.1 million | ||||||||||||

|

|

|

|

|

|||||||||||||

| $ | 0.82 | $ | 15.8 million | |||||||||||||

|

|

|

|

|

|||||||||||||

On February 21, 2012, our Board declared a cash dividend of $0.22 per share, which will be paid on April 19, 2012 to stockholders of record on March 22, 2012.

The actual declaration and payment of future dividends, the amount of any such dividends, and the establishment of record and payment dates, if any, is subject to final determination by the Board each quarter after its review of our then-current strategy, applicable debt covenants, and financial performance and position, among other things. See “Item 1A. Risk Factors” for a discussion of factors that might affect our financial performance and compliance with debt covenants, including covenants that affect our ability to pay dividends. Also, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Financial Condition, Liquidity and Capital Resources – Debt Financing” and Note 6 “Revolving Credit Facility” of our Consolidated Financial Statements under Item 8. “Financial Statements and Supplementary Data” for a description of restrictions on our ability to pay dividends under our revolving credit facility agreement.

15

Table of Contents

The following table presents information related to repurchases of our common stock during the fourth quarter of 2011 and the maximum dollar value of shares that may yet be purchased pursuant to our stock repurchase program:

| Issuer Purchases of Equity Securities |

||||||||||||||||

| Period |

Total Number of Shares Purchased(1) |

Average Price Paid Per Share(1) |

Total Number of Shares Purchased As Part of Publicly Announced Plans or Programs |

Maximum Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs(2) |

||||||||||||

| October 3 – October 30, 2011 |

168 | $ | 33.41 | — | $ | 85,681,464 | ||||||||||

| October 31 – November 27, 2011 |

198,200 | $ | 33.92 | 197,975 | $ | 78,965,399 | ||||||||||

| November 28, 2011 – January 1, 2012 |

520,121 | $ | 33.88 | 520,121 | $ | 61,345,586 | ||||||||||

|

|

|

|

|

|||||||||||||

| Total |

718,489 | $ | 33.87 | 718,096 | $ | 61,345,586 | ||||||||||

|

|

|

|

|

|||||||||||||

| (1) | For the periods ended October 30, 2011 and November 27, 2011, the total number of shares purchased included 168 shares and 225 shares, respectively, tendered by employees at an average price per share of $33.41 and $32.85, respectively, to satisfy tax withholding requirements on the vesting of restricted stock awards, which are not deducted from shares available to be purchased under our share repurchase program. Shares tendered by employees to satisfy tax withholding requirements were considered purchased at the closing price of our common stock on the date of vesting. |

| (2) | We may repurchase shares of our common stock under a plan authorized by our Board. On July 25, 2005, the Board approved a stock repurchase program, which authorized us to repurchase up to $400 million of our common stock and on October 22, 2007 and October 27, 2009 our Board authorized $200 million increases each. The stock repurchase program, which does not have a stated expiration date, authorizes us to make repurchases in the open market, through accelerated share repurchases or in privately negotiated transactions. |

Pursuant to our current revolving credit facility agreement, there are restrictions on the amount of our repurchases of our common stock and cash dividends that we may pay on our common stock. We currently plan to utilize our earnings to finance anticipated capital expenditures, reduce our outstanding debt, pay dividends, and potentially repurchase our common stock. See the discussion of our current revolving credit facility under Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition, Liquidity and Capital Resources—Debt Financing” and under Note 6 “Revolving Credit Facility” to our Consolidated Financial Statements under Item 8. “Financial Statements and Supplementary Data”.

16

Table of Contents

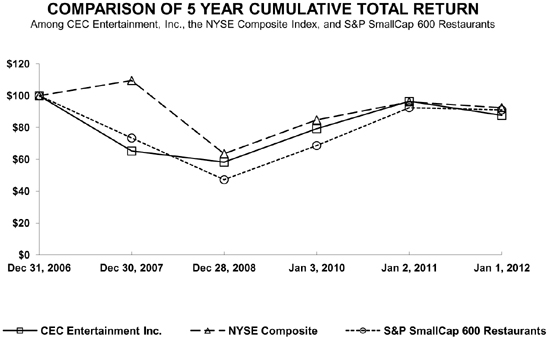

Stock Performance Graph

The graph below compares the annual change in the cumulative total stockholder return on our common stock over the last five fiscal years ended January 1, 2012, with the cumulative total return on the NYSE Composite Index and the S&P SmallCap 600 Restaurants Index. The comparison assumes an investment of $100 on December 31, 2006 in our common stock and in each of the foregoing indices and assumes the reinvestment of dividends. Our stock price performance shown in the graph below may not be indicative of future stock price performance.

| Dec. 31 2006 |

Dec. 30 2007 |

Dec. 28 2008 |

Jan. 3 2010 |

Jan. 2 2011 |

Jan. 1 2012 |

|||||||||||||||||||

| CEC Entertainment, Inc. |

$ | 100.00 | $ | 65.27 | $ | 58.26 | $ | 79.30 | $ | 96.47 | $ | 87.66 | ||||||||||||

| NYSE Composite |

$ | 100.00 | $ | 109.58 | $ | 63.58 | $ | 84.83 | $ | 96.18 | $ | 92.50 | ||||||||||||

| S&P SmallCap 600 Restaurants |

$ | 100.00 | $ | 73.42 | $ | 47.24 | $ | 68.69 | $ | 92.50 | $ | 91.14 | ||||||||||||

The performance graph and related text are being furnished to and not filed with the SEC, and will not be deemed to be “soliciting material” or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate such information by reference into such a filing.

17

Table of Contents

ITEM 6. Selected Financial Data.

The following selected financial data presented below should be read in conjunction with Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Consolidated Financial Statements under Item 8. “Financial Statements and Supplementary Data”.

| Fiscal Year(1) | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in thousands, except per share and store number amounts) | ||||||||||||||||||||

| Statement of Earnings Data: |

||||||||||||||||||||

| Company store sales |

$ | 815,894 | $ | 813,133 | $ | 814,563 | $ | 810,693 | $ | 781,665 | ||||||||||

| Franchise fees and royalties |

5,284 | 4,115 | 3,783 | 3,816 | 3,657 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenues |

821,178 | 817,248 | 818,346 | 814,509 | 785,322 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Company store operating costs: |

||||||||||||||||||||

| Cost of food, beverage, entertainment and merchandise (exclusive of items shown separately below) |

128,351 | 124,882 | 128,245 | 131,416 | 126,413 | |||||||||||||||

| Labor expenses |

222,596 | 222,337 | 223,084 | 223,331 | 214,147 | |||||||||||||||

| Depreciation and amortization |

80,826 | 79,716 | 77,101 | 74,805 | 70,701 | |||||||||||||||

| Rent expense |

74,992 | 70,425 | 67,695 | 65,959 | 63,734 | |||||||||||||||

| Other store operating expenses |

126,847 | 128,075 | 123,986 | 119,990 | 113,789 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Company store operating costs |

633,612 | 625,435 | 620,111 | 615,501 | 588,784 | |||||||||||||||

| Other costs and expenses: |

||||||||||||||||||||

| Advertising expense |

34,989 | 35,282 | 36,641 | 34,736 | 30,651 | |||||||||||||||

| General and administrative expenses |

51,859 | 50,693 | 50,629 | 55,970 | 51,705 | |||||||||||||||

| Asset impairments |

2,739 | 936 | — | 282 | 9,638 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||