| 171 Collins Street Melbourne, Victoria 3000 Australia | ||||

| 6 April 2023

VIA EDGAR |

T +61 3 9606 3333 F +61 3 9609 3015 bhp.com | |||

United States Securities and Exchange Commission

Division of Corporate Finance

Office of Energy & Transportation

100 F Street, N.E.

Washington, D.C. 20549

United States of America

Attention: John Coleman and Craig Arakawa

| Re: | BHP Group Limited |

Form 20-F for the Fiscal Year Ended June 30, 2022

Filed September 6, 2022

File No. 001-09526

Dear Messrs. Coleman and Arakawa:

Thank you for your letter, dated March 10, 2023, setting out comments of the Staff of the Securities and Exchange Commission (the “Staff” and the “Commission”) relating to the Form 20-F for the year ended June 30, 2022 of BHP Group Limited (“BHP”, “we” or “our”).

BHP’s responses to the Staff’s comments are set out below. To assist in the Staff’s review, we have preceded our response with the text (in italics and bold type) of the comment as stated in your letter.

Form 20-F for the Fiscal Year Ended June 30, 2022

Exhibit 96, page 263

| 1. | Please revise your Western Australia Iron Ore Technical Report Summary to include the mine life for each mine area and provide a mine map of the final mine outline for each mining area as required by Item 601(b)(96)(iii)(B)(13) of Regulation S-K. |

BHP acknowledges the Staff’s comment. Beginning with its Annual Report on Form 20-F for the year ending June 30, 2023 (the “2023 Form 20-F”), BHP’s technical report summary (“TRS”) for Western Australia Iron Ore will include the mine life for each mine area and a mine map of the final mine outline for each mining area. Specifically, BHP intends to revise the corresponding disclosures in BHP’s TRS for Western Australia Iron Ore substantially as set out in the attached Appendix.

We note that Item 1302(b) of Regulation S-K requires filing a TRS only when disclosing for the first time mineral reserves or mineral resources or when there is a material change in the mineral reserves or mineral resources from the last TRS filed for the property. If BHP files an updated TRS for Western Australia Iron Ore as an exhibit to the 2023 Form 20-F, BHP undertakes to include the disclosures substantially as set out in the attached Appendix in that exhibit. If BHP does not file an updated TRS for Western Australia Iron Ore as an exhibit to the 2023 Form 20-F, BHP expects to update its previously-filed TRS by furnishing the information set out in the attached Appendix on a report on Form 6-K and incorporating that report by reference as an exhibit to the 2023 Form 20-F.

BHP Group Limited ABN 49 004 028 077 and its subsidiaries are members of the BHP Group. The BHP Group is headquartered in Melbourne, Australia.

Exhibit 96, page 263

| 2. | Please revise your technical reports to include annual cash flow forecasts based on an annual production schedule for the life of the project as required by Item 601(96)(iii)(B)(19)(ii) of Regulation S-K. This should include the entire discounted cash flow analysis. |

As discussed on the telephone call with the Staff on March 21, 2023, BHP believes it has disclosed the results of the economic analysis in accordance with Item 601(96)(iii)(B)(19)(ii) of Regulation S-K.

BHP’s disclosures in section 19 of each TRS are intended to confirm the economic viability of the reserves. Section 19.2 of each TRS sets out the results of the economic analysis based on:

| • | the annual production schedule of each asset, including the net present value and, where applicable, the internal rate of return and payback period of capital; and |

| • | annual cash flows, including sales revenue, operating and closure costs, capital expenditure, royalties, and taxes, as applicable, for the full mineral reserves production schedule. |

We respectfully submit that, consistent with the applicable requirements, the qualified persons have summarized the material information supporting the economic analysis that is presented. In particular, each TRS sets out the basis for the capital and operating costs, closure costs, royalties and taxes that are reflected in the annual cash flow analysis and, in relevant part, identifies the average unit cost and foreign exchange rate applied to such metrics throughout the annual cash flow. Section 19 of each TRS also includes the annual production schedule of the property, which is the most significant driver of the annual cash flow profiles. BHP believes that illustrating the annual cash flows and the annual production schedule, coupled with the description of the key assumptions, parameters and methods used to demonstrate economic viability, is an effective representation of the economic analysis.

Taking into account the Staff’s comment, and to further clarify where, in each TRS, BHP has presented additional detail concerning the capital and operating costs, closure costs, royalties and taxes reflected in the cash flows of each property, BHP will include statements similar to the following under the Cash Flow Summary table included in future filings of its Annual Report on Form 20-F, beginning with the 2023 Form 20-F (new language underlined and in bold noting that section references may be updated, as applicable):

The annual cash flows presented in Figure 19-2 reflect a number of inputs, including revenue, operating costs, capital expenditure, closure and rehabilitation costs and royalties and taxes. The annual cash flows, and those inputs, are summarized in the table above. Revenues represented in the annual cash flows reflect the production presented in the production schedule shown in Figure 19-1, and the application of the commodity prices described in section 19.1.2. For further detail on other contributing inputs, please refer to the description of operating costs and capital expenditures (sections 18.1 & 18.2), foreign exchange rates (section 19.1.3), closure and rehabilitation costs (section 17.5) and royalties and taxes (section 19.1.6).

Consistent with our response to comment one above, BHP undertakes to revise its disclosure as set out above in an updated TRS, to the extent applicable in the 2023 Form 20-F, or through furnishing the supplemental disclosure on a report on Form 6-K and incorporating that report by reference into the 2023 Form 20-F.

2

* * *

We are available to discuss any of the foregoing with you at your convenience. Please contact me if you wish to discuss the information provided in this response.

Very truly yours,

/s/ David Lamont

David Lamont

Chief Financial Officer

| cc: | Waldo D. Jones, Jr. (Sullivan & Cromwell) |

3

Appendix

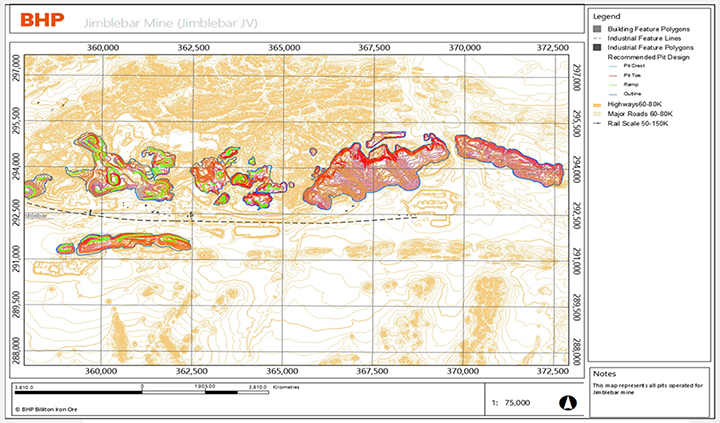

As discussed in BHP’s response to comment number one, it intends to make the following revisions to certain disclosures included in the technical report summary for Western Australia Iron Ore to include the mine life for each mine area and provide a mine map of the final mine outline for each mining area, beginning with its Annual Report on Form 20-F for the year ending June 30, 2023.

With respect to the mine life for each mine area, Table 13-9 at the beginning of section 13.3.1 Production rates and expected mine life of the WAIO technical report summary for the year ended June 30, 2022 will be amended and restated as shown below.

| Joint Venture |

Mining Area |

Production Life of Mining Area | ||

| Mt Goldsworthy JV |

Mining Area C | 22 Years (FY23 – FY44) | ||

| South Flank | 28 Years (FY23 – FY50) | |||

| Jimblebar JV |

Jimblebar | 30 Years (FY23 – FY52) | ||

| Newman Operations (Western Ridge) | 27 Years (FY25 – FY52) | |||

| Mt Newman JV |

Newman Operations | 30 Years (FY23 – FY52) | ||

With respect to the mine map of the final mine outline for each mining area, Figure 13-7 in section 13.2.9 Final Pit Maps of the WAIO technical report summary for the year ended June 30, 2022 will be amended and restated as shown below.

4

|

|

BHP Group Limited ABN 49 004 028 077 and its subsidiaries are members of the BHP Group. The BHP Group is headquartered in Melbourne, Australia.

5

|

|

6

|

|

7

|

|

8

|

|

9

|

|

10

|

|

11

|

|

12