Filed by Woodside Petroleum Ltd.

Pursuant to Rule 425 of the Securities Act of 1933

Subject Company: BHP Group Ltd (Commission File No.: 001-09526)

| ||||

|

ASX Announcement

Friday, 8 April 2022

ASX: WPL OTC: WOPEY |

Woodside Petroleum Ltd.

ACN 004 898 962

Mia Yellagonga 11 Mount Street Perth WA 6000 Australia

T +61 8 9348 4000 www.woodside.com.au | |||

INDEPENDENT EXPERT REPORT

Attached is the Independent Expert Report for the proposed merger between Woodside and BHP’s petroleum business.

The report should be read in conjunction with the Explanatory Memorandum released to the ASX today.

Contacts:

| INVESTORS

Damien Gare W: +61 8 9348 4421 M: +61 417 111 697 E: investor@woodside.com.au |

MEDIA

Christine Forster M: +61 484 112 469 E: christine.forster@woodside.com.au |

This ASX announcement was approved and authorised for release by Woodside’s Disclosure Committee.

| KPMG Corporate Finance | ABN: 43 007 363 215 | |||

|

A division of KPMG Financial Advisory Services (Australia) Pty Ltd Australian Financial Services Licence No. 246901 |

Telephone: +61 8 9263 7171 Facsimile: +61 8 9263 7129 www.kpmg.com.au | ||

| Level 8 235 St Georges Terrace |

||||

| Perth WA 6000 | ||||

| GPO Box A29 | ||||

| Perth WA 6837 | ||||

| Australia | ||||

The Directors

Woodside Petroleum Ltd

Mia Yellagonga

11 Mount Street

Perth WA 6000

8 April 2022

Dear Directors

Independent Expert Report and Financial Services Guide

Part One – Independent Expert Report

| 1 | Introduction |

On 16 August 2021, Woodside Petroleum Ltd (Woodside) announced that it was engaged in discussions with BHP Group Limited (BHP) regarding a potential merger involving BHP’s petroleum business (the Initial Announcement).

On 17 August 2021, Woodside and BHP jointly announced that they had entered into a merger commitment deed whereby, subject to confirmatory due diligence and the negotiation and execution of full form transaction documents, they would combine their respective oil and gas portfolios by way of an all-stock merger (the Proposed Transaction).

On 22 November 2021, Woodside announced that it had entered into a binding share sale agreement (SSA) with BHP in relation to the Proposed Transaction.

Under the Proposed Transaction, Woodside will acquire 100% of the issued share capital of BHP Petroleum International Pty Ltd (BHP Petroleum)1 with an effective date of 1 July 2021 (Effective Date), in exchange for the issue of 914,768,948 new ordinary shares in Woodside, which will be distributed in-specie as a dividend on a prorated basis to BHP shareholders (the Merger Consideration).

Prior to completion, Woodside and BHP Petroleum will carry on their respective businesses in the normal course.

1 References to BHP Petroleum include relevant BHP Petroleum controlled entities

| © 2022 KPMG an Australian partnership and a member firm of the KPMG global organisation of independent member firms affiliated

with KPMG International Limited, a private English company limited by guarantee. All rights reserved. |

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

On completion:

| ● | BHP will transfer to Woodside 100% of the issued capital of BHP Petroleum on a cash and debt-free basis, based on the balance sheet at the Effective Date, subject to various exclusions including certain legacy assets and liabilities that will remain with BHP |

| ● | BHP shareholders will hold approximately 48% of the issued capital in the post-merger Woodside2 (the Merged Group)3, which will remain listed on the Official List of ASX Limited (ASX) and will seek secondary listings on the New York Stock Exchange (NYSE) and the London Stock Exchange (LSE) |

| ● | BHP will make a cash payment to Woodside for the net cash flow generated by BHP Petroleum between the Effective Date and completion4 |

| ● | Woodside will make a cash payment to BHP in relation to cash dividends paid by Woodside between the Effective Date and completion that would have been received by BHP had the Merger Consideration been paid on the Effective Date. |

BHP has agreed to certain exclusivity arrangements with Woodside. These arrangements do not restrict BHP from considering superior proposals for BHP Petroleum in prescribed circumstances. Woodside has agreed to similar exclusivity arrangements in connection with any competing proposal for Woodside.

Completion of the Proposed Transaction requires the satisfaction of various conditions precedent and the approval of Woodside shareholders (Woodside Shareholders)5 under ASX Listing Rule 7.1.

The directors of Woodside (Directors) have, subject to the satisfaction of various conditions precedent, including an independent expert concluding, and continuing to conclude, that the Proposed Transaction is in the best interests of Woodside Shareholders, unanimously recommended Woodside Shareholders vote in favour of the Proposed Transaction and as at the date of this report have not withdrawn that support.

The Proposed Transaction is described more fully in section 5 of this report and in sections 3 and 10 of Woodside’s Merger Explanatory Memorandum (Explanatory Memorandum) to which this report is attached.

2 Woodside shares that would otherwise have been issued to “Ineligible Foreign Shareholders”, being a BHP shareholder whose address shown in the register of members of BHP is in a jurisdiction where BHP determines (acting reasonably and following consultation with Woodside) that it would be unlawful, unduly impracticable (in each case in respect of either BHP or Woodside) to distribute the new Woodside shares, will be sold by a nominated sales agent and the net proceeds after costs remitted to the relevant BHP shareholder and potentially “Selling Shareholders” where BHP may, at its discretion, offer Selling Shareholders a voluntary sale facility, whereby BHP Shareholders with less than a certain number of BHP Shares may elect for Woodside shares that would otherwise be issued to them to be sold and the sale proceeds remitted to that Selling Shareholder

3 which will comprise the combined oil, natural gas and natural gas liquids asset portfolios of Woodside and BHP Petroleum

4 or, if that amount is negative, Woodside will make a cash payment to BHP

5 Woodside has obtained relief from the Australian Securities and Investments Commission (ASIC) in relation to the operation of section 606 of the Corporations Act (the Act) with the result that shareholder approval is not being sought for the purpose of item 7 of s611 of the Act.

2

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Woodside is an Australian integrated supplier of energy, holding a portfolio of operated and non-operated production, development and exploration oil, gas and liquefied natural gas (LNG) upstream/midstream projects. Woodside’s principal petroleum assets include:

| ● | its 16.67% operating interest in the North West Shelf Project, Western Australia (NWS Project), producing LNG, pipeline natural gas, condensate and liquefied petroleum gas (LPG) |

| ● | its 90% operating interest in the Pluto LNG Project, Western Australia (Pluto LNG), producing LNG, pipeline natural gas and condensate |

| ● | its 60% and 33.33% respective operating interests in two floating production, storage and offloading (FPSO) vessels operating offshore Western Australia (Australia Oil), producing oil and gas |

| ● | its 13% non-operating interest in the Wheatstone LNG project, Western Australia (Wheatstone LNG), producing LNG, pipeline natural gas and condensate, including from the Julimar-Brunello Project in which Woodside holds a 65% interest. |

Woodside also has a number of advanced development projects in progress, including amongst others, the separate developments of the Scarborough gas resources located offshore Western Australia, the onshore Pluto Train 2 LNG processing facility and the Sangomar oil and gas field located offshore Senegal. In addition, Woodside holds an interest in a number of other Australian and international longer-term development/exploration assets.

Woodside also carries on marketing, trading and shipping activities and is developing a new energy business which is focused on maturing a portfolio of hydrogen and ammonia opportunities in Australia and internationally.

As at 24 March 2022, Woodside had a market capitalisation of A$32,668 million6.

BHP is the world’s largest diversified natural resources company by market capitalisation with over 80,000 employees and contractors, operating in over 90 locations around the world.

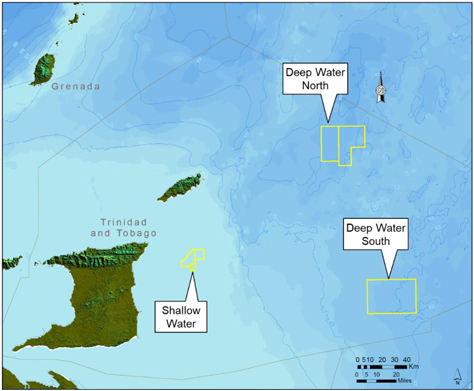

BHP Petroleum holds conventional oil and gas assets in the US Gulf of Mexico (GOM), Australia, Trinidad and Tobago, Algeria7 and Mexico, as well as appraisal and exploration options in Egypt, Trinidad and Tobago, central and western GOM, Eastern Canada and Barbados.

The Directors have requested KPMG Financial Advisory Services (Australia) Pty Ltd (of which KPMG Corporate Finance is a division) (KPMG Corporate Finance) prepare an Independent Expert Report (IER) to Woodside Shareholders in relation to the Proposed Transaction. The purpose of the IER is to set out whether, in our opinion, the Proposed Transaction is in the best interests of Woodside Shareholders as a whole.

6 All amounts are stated in Australian dollars (A$ or AUD) unless specifically noted otherwise

7 BHP Petroleum is currently in the process of divesting its Algerian assets. The treatment of the Algerian assets is discussed in more detail in Section 9.2.8 below.

3

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

The specific terms of the resolutions to be approved by Woodside Shareholders in relation to the Proposed Transaction are set out in the Notice of Annual General Meeting and Explanatory Memorandum to which this report is attached (together the Meeting Documents).

The sole purpose of this report is an expression of the opinion of KPMG Corporate Finance as to whether the Proposed Transaction is in the best interests of Woodside Shareholders. This report should not be used for any other purposes or by any other party. Our opinion should not be interpreted as representing a recommendation to Woodside Shareholders to either vote for or against the Proposed Transaction, which remains a matter solely for individual Woodside Shareholders to determine.

This report should be considered in conjunction with and not independently of the information set out in the Meeting Documents in their entirety.

KPMG Corporate Finance’s Financial Services Guide is contained in Part Two of this report.

| 2 | Technical Requirements |

There is no statutory requirement for Woodside to commission an IER in the present circumstances. However, it is a condition precedent to the Proposed Transaction that an IER is obtained, and the Directors recommendation of the Proposed Transaction is subject to, amongst other things, an independent expert concluding, and continuing to conclude, that the Proposed Transaction is in the best interests of Woodside Shareholders.

Accordingly, the Directors have engaged KPMG Corporate Finance to prepare an IER setting out whether, in our opinion, the Proposed Transaction is “in the best interests” of Woodside Shareholders taken as a whole.

| 2.1 | Basis of assessment |

In undertaking our work, we have referred to guidance provided by ASIC in its Regulatory Guides, in particular Regulatory Guide 111 ‘Content of expert reports’ (RG 111) which outlines the principles and matters which it expects a person preparing an IER to consider.

Whilst RG 111 focuses principally on reports prepared for change of control transactions, it notes that the principles set out in the guide may be relevant to independent expert reports commissioned for other purposes. It also provides that in deciding on the appropriate form of analysis for a report, an expert should bear in mind that the main purpose of the report is to adequately deal with the concerns that could reasonably be anticipated of those persons affected by the proposed transaction.

Having regard to the purpose of our report, we consider that the principal matter required to be considered by us in assessing whether the Proposed Transaction is “in the best interests” of Woodside Shareholders, is whether the proposed transaction is “fair and reasonable” to Woodside Shareholders. RG111.18 notes in the context of a change of control transaction that:

| ● | ‘fair and reasonable’ is not regarded as a compound phrase |

| ● | an offer is ‘fair’ if the value of the consideration is equal to or greater than the value of the shares subject to the offer |

| ● | an offer is ‘reasonable’ if it is ‘fair’ |

4

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | an offer might also be ‘reasonable’ if, despite being ‘not fair’, the expert believes that there are sufficient reasons for shareholders to accept the offer in the absence of any higher bid before the close of the offer. |

In a change of control transaction, the independent expert report is prepared for the benefit of target company shareholders and the comparison of value is made assuming 100% ownership of the ‘target’ company. In the current circumstances:

| ● | Woodside is the acquiring company and BHP Petroleum is the target |

| ● | Woodside Shareholders will, as a block, hold 52% of the Merged Group, and current Woodside Directors are expected to hold the significant majority of Board positions following completion of the Proposed Transaction |

| ● | Woodside Shareholders will continue to hold the same number of shares in Woodside both prior to and following completion of the Proposed Transaction8 |

| ● | our report is being prepared for the benefit of Woodside Shareholders not BHP shareholders |

| ● | following completion, there will be no individual shareholder holding more than 7% in the Merged Group. |

Accordingly, we consider the appropriate test in assessing whether the Proposed Transaction is fair to Woodside Shareholders is whether the value of a share in the Merged Group is greater than or equal to the value of a Woodside share prior to the Proposed Transaction.

In assessing the value of a share in the Merged Group, we have considered those synergies and cost savings reasonably able to be achieved that are expected to be available to Woodside in combining its existing portfolio of oil and gas assets with those held by BHP Petroleum. In addition, in order to ensure a consistent approach in the assessment of value, our analysis of both Woodside and the Merged Group has been undertaken on a 100% basis.

Reasonableness involves an analysis of qualitative and other factors that shareholders might consider prior to accepting an offer, such as, but not limited to:

| ● | the rationale for the Proposed Transaction |

| ● | the relative contribution of each party to the Merged Group, including Reserves and Resources and near-term production levels |

| ● | the impact of the Proposed Transaction on Woodside’s gearing, near-term earnings per share (EPS), asset backing per share |

| ● | the impact on Woodside’s share register and the liquidity of the market in Woodside’s shares |

| ● | any conditions associated with the Proposed Transaction |

8 Excluding the impact of new Woodside shares that might be issued to existing Woodside shareholders who are also shareholders in BHP at the record date

5

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | the consequences of not approving the Proposed Transaction. |

| 3 | Opinion |

As the Proposed Transaction is not a “control transaction” as defined by ASIC Regulatory Guides, the appropriate test in assessing whether it is fair to Woodside Shareholders is whether the value of a share in the Merged Group is greater than or equal to the value of a Woodside share prior to the Proposed Transaction.

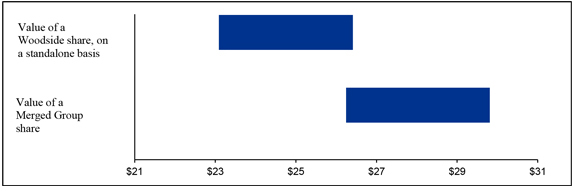

We have assessed the full underlying value of Woodside as a standalone entity to be in the range of US$16,978 million to US$19,424 million, which equates to an assessed value per Woodside share of between A$23.09 and A$26.429. This compares to our assessed full underlying value for the Merged Group in the range of US$37,242 million to US$42,302 million, which equates to an assessed value per Merged Group share of between A$26.25 and A$29.81.

We have also considered that based on our assessment of the full underlying value of Woodside and BHP Petroleum as standalone entities10, the aggregate 52% interest that Woodside Shareholders will hold in the Merged Group is broadly consistent with Woodside’s contribution to the Merged Group.

Based on these measures, the Proposed Transaction is, in our opinion, fair to Woodside Shareholders.

However, in considering this outcome we note that the Proposed Transaction is being undertaken:

| ● | at a time of significant geopolitical unrest. The recent invasion of Ukraine by Russia has resulted in a large number of Russia’s trading partners imposing targeted trade and financial system sanctions on Russia, significantly impeding Russia’s ability to undertake foreign trade, including in respect to oil and gas transactions. |

In addition, the United States (US), the United Kingdom (UK) and Australia have all announced bans on imports of Russian oil and gas and it is reported that the European Union (EU) is actively investigating ways in which it can reduce its reliance on Russian sourced oil and gas over the medium and long term.

This has led to significant global uncertainty in relation to both immediate supply shortfalls and longer-term continuity and security of supply chains, which in turn has resulted a sharp and rapid increase in benchmark oil prices

| ● | during a period of continuing uncertainty as to the rate of overall global and regional recovery from the impact of Covid-19 variants |

| ● | against a background of increasing focus by the global community on environmental, social and governance issues (ESG), including in relation to climate change and the contribution of fossil fuels to global warming and the transition to clean energy alternatives. |

9 Based on an AUD:USD exchange rate of approximately 0.747

10 Before the benefit of cost savings and other synergies expected to be realised as a result of the Proposed Transaction

6

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Whilst the impact of Covid-19 can be expected to be resolved over the short to medium term, the war in Ukraine and the transition to clean energy have a much greater potential to bring about significant long term structural change in global energy markets.

For instance, it is not inconceivable that the UK’s and EU’s efforts to reduce reliance on Russian sourced oil and gas could, over the longer term, result in a redirection of volumes by other market participants away from Woodside’s and BHP Petroleum’s principal markets, allowing the Merged Group to increase sales in these markets. In addition, Russia is a significant supplier of LNG into Asia, and any ongoing reluctance in this market to accept delivery from Russia would potentially add further demand for Australian supply.

In terms of the transition to clean energy, it is generally accepted that over the period to at least 2050, there is likely, based on current policy settings, to be a significant increase in the level of global consumption of energy; however market opinion in relation to the role oil and gas will play in meeting that demand is much more unsettled, with the final outcome expected to be heavily influenced by the speed, extent and success at which the global community transitions to clean energy alternatives, including hydrogen.

In addition, various regulatory and commercial market risks have been amplified in recent times for participants in the fossil fuel sector, including amongst other things, the possibility of executive and legislative change, in relation to tightening of restrictions on emissions, approach to carbon pricing, tax structures and requirements for regulatory approvals. Furthermore, there is evidence that ESG issues are impacting the flow of capital market and debt funding to oil and gas companies.

Each of these issues are evolving market dynamics, which clearly won’t be fully resolved in the short term, however, it is clear that oil and gas companies with strong cash flow generation supported by well-balanced asset portfolios and a robust financial position will be best placed to navigate the energy market transition. In our view, the Proposed Transaction strengthens Woodside’s position in each of these areas.

It is important that Woodside Shareholders recognise oil and gas asset values are inherently subjective. Whilst we consider the production and operational assumptions developed by us in conjunction with Gaffney, Cline & Associates Pty Ltd (GaffneyCline)11 in valuing the asset portfolios of Woodside and BHP Petroleum to be reasonable, and the macroeconomic assumptions adopted by us to reflect an appropriate mix of short-term factors and the potential for longer term structural change in the oil and gas industry, estimates of oil and gas asset values can change quickly and a range of credible operational and development scenarios could have been adopted, particularly in the current volatile environment, all of which could significantly impact value.

This being the case, whilst we have determined the Proposed Transaction to be fair and therefore, in accordance with RG111, the Proposed Transaction is also considered reasonable, we believe that proper evaluation of the Proposed Transaction requires Woodside Shareholders to consider both matters of value and also the broader commercial and qualitative aspects of the Proposed Transaction in deciding whether or not to vote for the Proposed Transaction, including:

11 the independent petroleum industry specialist engaged by Woodside, but with its scope of work set by us

7

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | the investment characteristics of holding a share in the Merged Group compared to continuing to hold a share in Woodside as a standalone entity |

| ● | the relative contribution by each entity to the Merged Group based on various metrics compared to the exchange ratio |

| ● | the implications for Woodside shareholders in the event the Proposed Transaction is not approved. |

Having considered the issue of fairness and each of the factors above, including the consequences of not approving the Proposed Transaction, we are of the opinion that, in the absence of a superior offer, the Proposed Transaction is in the best interests of Woodside Shareholders.

Further information in relation to each of the above and other matters we have considered in forming our opinion is set out below.

The decision whether or not to approve the Proposed Transaction is a matter for individual Woodside Shareholders based on their views as to value, expectations about future market conditions and their particular circumstances including investment strategy and portfolio structure, risk profile and tax position. Woodside Shareholders should consult their own professional advisor, if in doubt, regarding the action they should take in relation to the Proposed Transaction.

| 3.1 | Assessment of fairness |

We have assessed the underlying value of Woodside on a 100% basis prior to the Proposed Transaction to be in the range of US$16,978 million to US$19,424 million; which equates to an assessed value per Woodside share of between approximately A$23.09 to A$26.42 as summarised in the table below.

Table 1: Summary of Woodside standalone assessed market values

| Assessed Values | ||||||||||||

| All figures in US$ million (unless otherwise stated) | Reference | Low | High | |||||||||

| Market values of Woodside’s interests in petroleum assets | 11.3 | 23,180 | 25,615 | |||||||||

| Less: Net (debt) / cash |

11.3.12 | (3,101) | (3,101) | |||||||||

| Less: Net financial liabilities and other assets |

11.3.12 | (171) | (171) | |||||||||

| Less: Put option for Scarborough (payable to BHP) |

11.3.12 | (593) | (419) | |||||||||

| Less: Regret costs |

11.3.12 | (70) | (70) | |||||||||

| Less: NPV of NWC movements |

11.3.12 | (687) | (703) | |||||||||

| Less: NPV of future corporate overheads |

11.3.12 | (1,581) | (1,727) | |||||||||

| Total equity value | 16,978 | 19,424 | ||||||||||

| Number of ordinary shares (millions)2 | 11.3 | 984.0 | 984.0 | |||||||||

| Value per share - US$ | 17.25 | 19.74 | ||||||||||

| Value per share - A$3 | 23.09 | 26.42 | ||||||||||

Source: GaffneyCline’s Independent Technical Specialist Report (ITSR) and KPMG Corporate Finance analysis

Notes:

| 1. | May not add due to rounding |

| 2. | Current ordinary shares on issue include dividend reinvestment plan shares issued in March 2022 |

| 3. | Based on an exchange rate of approximately AUD:USD 0.747 |

8

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

In comparison, we have assessed the value of a share in the Merged Group on an equivalent basis to be in the range of US$37,242 million to US$42,302 million, which equates to an assessed value per Merged Group share of between approximately A$26.25 to A$29.81, as summarised below.

Table 2: Summary of Merged Group assessed market values

| Assessed Values | ||||||||||||

| All figures in US$ million (unless otherwise stated) | Reference | Low | High | |||||||||

| Woodside equity value | 11.3 | 16,978 | 19,424 | |||||||||

| BHP Petroleum equity value | 11.5 | 19,064 | 20,443 | |||||||||

| Add: Synergies expected to be achieved |

11.7 | 2,364 | 3,599 | |||||||||

| Add: Woodside regret costs |

11.7 | 70 | 70 | |||||||||

| Less: Transaction costs |

11.7 | (287) | (287) | |||||||||

| Less: Dividend payment |

11.7 | (830) | (830) | |||||||||

| Less: Locked box payment |

11.7 | (117) | (117) | |||||||||

| Merged Group equity value | 37,242 | 42,302 | ||||||||||

| Woodside ordinary shares | 984.0 | 984.0 | ||||||||||

| Add: New Woodside shares to be issued |

11.7 | 914.8 | 914.8 | |||||||||

| Merged Group shares (diluted) | 1,898.7 | 1,898.7 | ||||||||||

| Merged Group value per share (US$/share) | 19.61 | 22.28 | ||||||||||

| Merged Group value per share (A$/share)2 | 26.25 | 29.81 | ||||||||||

Source: GaffneyCline’s ITSR and KPMG Corporate Finance analysis

Notes:

| 1. | May not add due to rounding |

| 2. | Based on an exchange rate of approximately AUD:USD 0.747. |

As our range of assessed values for a Woodside share prior to the Proposed Transaction lies predominately below our range of assessed values for a share in the Merged Group on an equivalent basis, as shown in the chart below, the Proposed Transaction is fair to Woodside Shareholders.

Figure 1 - Comparison of assessed values

Source: KPMG Corporate Finance analysis

9

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

We have assessed the value of the equity in Woodside prior to the Proposed Transaction on a “sum-of-the-parts” basis by aggregating the estimated market values of its interest in each of its current and planned operations on a standalone basis, its other petroleum related assets and assets considered to be surplus to the petroleum assets and deducting net borrowings and non-trading liabilities.

Similarly, we have assessed the value of the equity of the Merged Group on a “sum-of-the-parts” basis by aggregating the estimated market values of Woodside and BHP Petroleum interests in each of their current and planned operations, their other petroleum related assets and assets considered to be surplus to the petroleum assets and deducting net borrowings and non-trading liabilities.

Our range of values for the Merged Group also includes the benefit of various costs savings and operational benefits expected to be realised by the Merged Group in bringing together the separate asset portfolios of Woodside and BHP Petroleum.

Woodside expects these benefits to total more than US$400 million per annum (pre-tax), of which in excess of US$250 million relates to operating and corporate cost savings, which are typically easier to identify and realise, with the remaining US$150 million relating to exploration expenditure. The benefit of these cost savings and synergies is expected to be realised progressively, with the full annual benefit achieved by 2024.

Woodside estimates that the implementation of the identified synergy opportunities would require one-off costs in the order of US$500 million to US$600 million to be incurred in the first two years following completion of the Proposed Transaction.

Whilst we consider there is a clear logic and basis for the level of synergies identified by Woodside, it is important to note that the realisation and final quantum of any benefit is not assured and will depend upon Woodside’s ability to successful integrate the two businesses. After assessing the risk that the cost savings and synergies may not emerge to the extent anticipated, the timing for realisation may take longer than planned and that additional unanticipated costs of realisation may emerge, we have adopted a range of US$2,364 million to US$3,599 million in relation to the post-tax net present value of annual cost savings and synergies for the purpose of our assessed values of the Merged Group rather than a single point estimate. This equates to a value per share in the Merged Group of approximately A$1.67 to A$2.54.

Whilst the abovementioned synergies and cost savings are expected to be realised as a result of combining the operations of Woodside and BHP Petroleum, having regard to the nature of these synergies and the likely profile of an alternative acquirer, we do not consider them to be unique to a business combination with BHP Petroleum only and would be available to a pool of purchasers.

In arriving at our range of values for Woodside and the Merged Group, we have placed reliance on the assumptions prepared by GaffneyCline in relation to reasonable production scenarios, including appropriate production inventories, operational expenditure (Opex), capital expenditure (Capex) and decommissioning and restoration (D&R) profiles for each of Woodside’s and BHP Petroleum’s near-term and planned production projects. In addition, GaffneyCline has assessed the value of other petroleum assets where discounted cash flow (DCF) was not considered an appropriate valuation methodology.

| 3.1.1 | Relative contributions – Full underlying value |

The table below summarises the values contributed by Woodside and BHP Petroleum based on our range of full underlying values for each of Woodside and BHP Petroleum as standalone entities.

10

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Table 3: Summary of Relative contributions – full underlying value

| US$m | Section ref |

Low | Relative contribution % |

High | Relative contribution % |

|||||||||||

| Full Underlying Value | ||||||||||||||||

| Woodside | 11.3 | 16,978 | 48 | 19,424 | 50 | |||||||||||

| BHP Petroleum1 | 11.5 | 18,234 | 52 | 19,613 | 50 | |||||||||||

Source: KPMG Corporate Finance analysis

Note 1: BHP Petroleum’s underlying values have been reduced to reflect the dividend payable to BHP of US$830 million in the event the Proposed Transaction is completed.

Woodside shareholders will collectively hold approximately 52% of the issued capital of the Merged Group, which exceeds Woodside’s relative contribution to the underlying value of the Merged Group. We note that the above assessed values represent the full underlying value of Woodside and BHP Petroleum as standalone entities but do not include the benefit of any cost savings and other synergies that may be realised. Woodside Shareholders will collectively participate to the extent of 52% in any additional benefits realised.

Our assessed values for a Merged Group share of between A$26.25 and A$29.81 lie below Woodside’s closing price of A$33.20 per share on 24 March 2022. This may reflect:

| ● | whilst our valuation of the Merged Group incorporates an uplift for the benefits of the Proposed Transaction, including for potential up to US$400 million in annual pre-tax synergies and other costs savings expected by Woodside to be realised progressively over the period to 2024, it does not include any uplift for Woodside’s expectation that the final quantum of costs savings and synergies could potentially exceed this amount |

| ● | the market is more bullish in relation to the value of the Merged Group’s asset portfolio, either in relation to the technical and operational assumptions estimated by GaffneyCline, including GaffneyCline’s assessment of the chance of development of various pre-production assets, or in relation to the macroeconomic assumptions adopted by us, including future commodity prices and discount rates. As noted, previously, given the current volatility in commodity markets, a range of macroeconomic assumptions could credibly be adopted, which has the potential to be accretive or dilutive to value. To assist readers in this regard we have included sensitivity analysis around key value drivers for each project in sections 11.3 and 11.5 of this report. |

Our valuations of each of Woodside and BHP Petroleum and their underlying asset portfolios are set out in greater detail in Sections 11.3 and 11.5 of this report and in GaffneyCline’s report is attached as Appendix 15.

We would normally also compare the share price implied by our standalone valuation of Woodside to Woodside’s share price immediately prior to the Initial Announcement. However given the significant movement in the key commodity prices since the Initial Announcement, which are reflected in our valuation but not the Initial Announcement share price, we do not consider such an analysis would be meaningful.

11

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| 3.2 | Assessment of reasonableness |

Whilst we have determined the Proposed Transaction to be fair based on our assessment of values and therefore, in accordance with RG 111, the Proposed Transaction is also considered reasonable, we have considered various matters that we believe Woodside Shareholders should also consider in deciding whether or not to vote for the Proposed Transaction. These include:

| ● | the change in the investment characteristics of holding a share in the Merged Group compared to Woodside as a standalone entity, including that Woodside Shareholders will benefit from a larger, more financially robust, geographically diverse business, with the potential for increased liquidity and investor interest |

| ● | the Proposed Transaction is expected to increase Woodside’s capacity to successfully navigate and take a leading position in relation to the transition to new energy |

| ● | the potential for Woodside Shareholders to participate in further operational and strategic synergies over and above those included by us in our assessed values for the Merged Group |

| ● | BHP Petroleum’s asset base provides Woodside with immediate access to significant development and growth opportunities, within a timeframe that is unlikely to otherwise have been available to Woodside as a standalone entity |

| ● | Woodside has indicated that it does not intend, at this time, to change its dividend policy |

| ● | the exchange ratio is broadly supported by various financial and other relative contribution measures |

| ● | it is arguable that, in theory, completion of the Proposed Transaction may reduce the prospect of Woodside Shareholders receiving an offer for their shares inclusive of a full premium for control |

| ● | the Directors of Woodside have advised the market that they intend to unanimously recommend Woodside Shareholders approve the Proposed Transaction12. |

Having considered each of these factors and the consequences of not accepting the Proposed Transaction, we are of the opinion that, whilst there are various factors that may not be attractive to Woodside Shareholders, the benefits of holding a share in the Merged Group are sufficient to conclude that Woodside Shareholders will, on balance, be better off by approving the Proposed Transaction.

Further information in relation to each of the above and other matters we have considered in forming our opinion is set out below.

12 Subject to no superior offer being received and the Independent Expert continuing to conclude that the Proposed Transaction is in the best interest of Woodside Shareholders

12

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| 3.2.1 | Investment characteristics of holding a share in the Merged Group |

In our view there are a number of investment benefits for Woodside Shareholders in holding an interest in the Merged Group compared to that of holding a share in Woodside as a standalone entity:

Stronger financial position

On completion of the Proposed Transaction, the Merged Group will hold, on a proforma 31 December 2021 basis, net tangible assets of approximately US$29,389 million, with a relatively modest gearing in the order of 8%13, which compares to a net tangible asset base for Woodside on a standalone basis in the order of US$14,229 million, with gearing of 22%. The fall in relative gearing levels reflects the benefit of BHP Petroleum’s net assets being acquired on a “cash-free, debt-free basis” and the acquisition being funded by the issue of new scrip rather than by cash.

This level of gearing compares to Woodside’s stated target gearing for the Merged Group in range of 15% - 35%, which is broadly consistent with the level of gearing currently employed by other large conventional oil and gas producers.

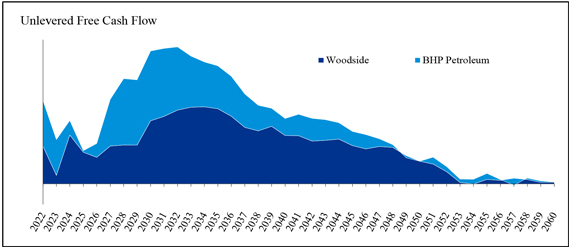

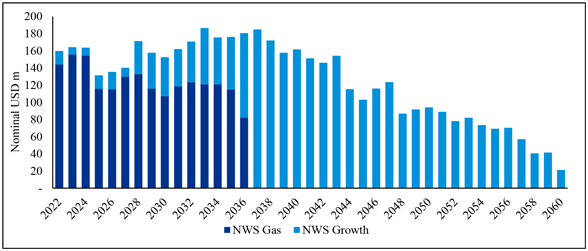

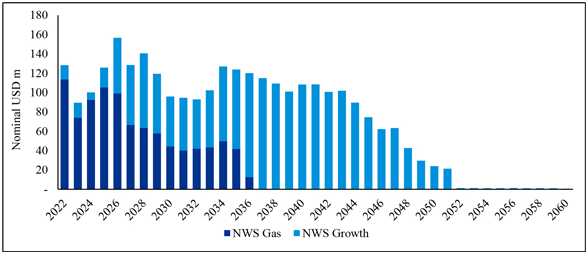

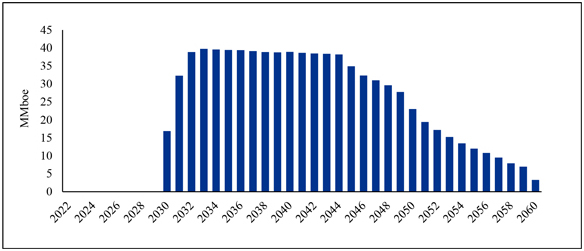

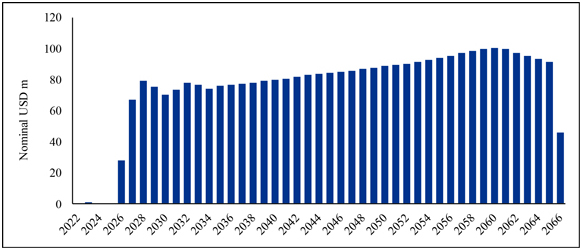

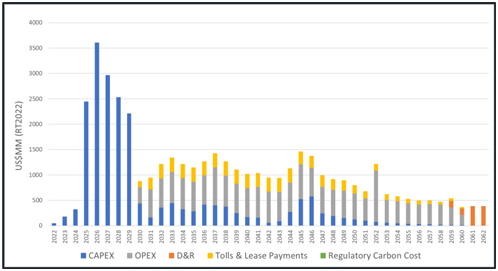

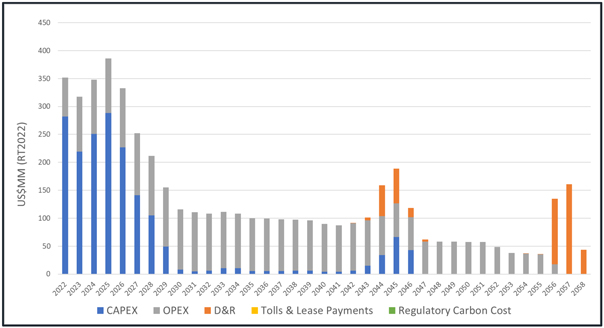

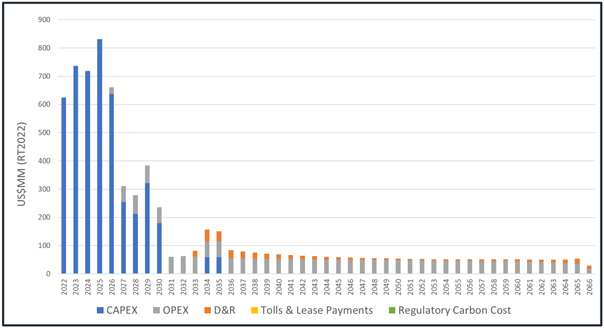

We also note that, as illustrated in figure 2 below, the combination of Woodside’s and BHP Petroleum’s assets is expected to significantly improve the level of net free cash flows available to the Merged Group, crucially, in the initial years when Woodside is looking to bring Scarborough/Pluto Train 2 and Sangomar into production, whilst also continuing to advance other growth opportunities, including its New Energy ambitions.

Figure 2 – Profile of net free cash flows over the period to 206014

Source: KPMG Corporate Finance analysis

13 which includes lease labilities and other financial liabilities. In the event these liability categories are excluded, the Merged Group’s proforma gearing falls to 4%, which compares to the gearing of Woodside’s as a standalone entity of 15% on the same basis.

14 Net free cash flows are based on the production; and operational, capital and D&R expenditure profiles assessed by GaffneyCline and the macroeconomic assumptions determined by KPMG Corporate Finance but are before exploration expenditure and the realisation of any operational and other cost savings and synergies.

13

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

On 16 December 2021, Moody’s re-affirmed Woodside’s Baa115 investment grade credit rating, with a negative outlook, noting that as a result of the significant spending and execution risks associated with the Scarborough/Pluto Train 2 project, it expected that, in the absence of the Proposed Transaction and/or further sell downs of project stakes, Woodside’s credit metrics “will be at weak levels for the rating, which could lead to a downgrade without other initiatives to improve its financial profile”.

Moody’s also observed that Woodside’s credit profile could weaken further in the absence of the Proposed Transaction, in part, reflecting BHP’s put option for the sale of its stake in the Scarborough project to Woodside, which if exercised, would require Woodside to fund in the order of an additional US$1,000 million without the cash flow that completion of the Proposed Transaction would provide.

Moody’s advised that its affirmation also considered the potential positive impacts of the Proposed Transaction, which “would significantly increase the scale of Woodside’s production and reserves, while materially improving diversity and providing substantial additional cash flow to fund growth” and that, completion of the Proposed Transaction would strengthen Woodside’s credit profile to more appropriate levels for its rating.

On 31 December 2021, S&P Global Ratings affirmed Woodside’s at BBB+16 investment grade credit rating, with a negative outlook.

Accordingly, in comparison to Woodside as a standalone entity, completion of the Proposed Transaction can be expected to provide greater scope for the Merged Group to source additional, and potentially cheaper, funding to progress its strategic initiatives.

Geographical, end-market and product mix diversification

At present, Woodside’s asset portfolio is principally focussed on LNG production and development projects, largely concentrated on the west coast of Australia, with its current LNG, LPG, condensate and oil production sold to customers primarily in Asia and its domestic gas (domgas) sold to customers in Western Australia. Whilst Woodside also holds interests in overseas oil and gas development projects, including in Senegal (Sangomar), Canada and Timor-Leste17, none of these are currently in production.

In contrast, the Merged Group will, in addition to the Woodside’s existing projects, also hold BHP Petroleum’s producing and development conventional oil and gas assets located in the GOM, Trinidad and Tobago and Mexico and on the east coast of Australia. In addition, BHP Petroleum also holds interests in the Woodside operated NWS Project and the Scarborough project, which will be consolidated by the Merged Group.

BHP Petroleum’s domgas production is largely sold on the east coast of Australia, whilst crude oil and gas is sold to customers in Japan, South Korea and China. Crude oil production from BHP Petroleum’s operations in the GOM is sold into global oil markets, with gas volumes sold into the US domestic gas market. Crude oil from BHP Petroleum’s Trinidad and Tobago operations is similarly sold into global oil markets, with gas volumes sold into the local gas market.

15 Obligations rated Baa are judged to be medium-grade and subject to moderate credit risk and as such may possess certain speculative characteristics. Moody’s appends numerical modifiers 1, 2, and 3 to each generic rating classification. The modifier 1 indicates that the obligation ranks in the higher end of its generic rating category

16 Obligations rated BBB are considered to have adequate capacity to meet financial commitments, but more subject to adverse economic conditions

17 Woodside has indicated it intends to exit its current projects in Myanmar

14

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

As a result of the combination of the oil and gas assets of Woodside and BHP Petroleum, the Merged Group will have a more balanced geographical, production and customer mix, which should translate to a reduced level of risk to overall portfolio values from any economic, regulatory or other shocks in any individual market.

Potential for increased liquidity in share trading and increased investor interest, but also for short term overhang

With a pro-forma market capitalisation following completion of the Proposed Transaction of A$63,038 million18, the Merged Group will be a top 10 company by market capitalisation19 on the ASX. This should result in a greater weighting being applied to its shares by fund and index managers in terms of investment allocations. Coupled with a much broader shareholder base and secondary listings on the NYSE and LSE, there is a reasonable basis to expect an increased level of trading in Woodside shares and a growing level of interest by international investors, which may translate into a positive re-rating of the Merged Group compared to Woodside as a standalone company (although it is arguable given the time that has elapsed since the Initial Announcement, an element of re-rating may already be reflected in Woodside’s current share price).

Potentially offsetting this benefit to some extent, at least in the short term, is the prospect for increased volatility in the Merged Group’s share price immediately following completion of the Proposed Transaction.

Woodside shares that would otherwise have been issued to “Ineligible Foreign Shareholders”20 and potentially “Selling Shareholders”21 for the purpose of the Proposed Transaction will be sold by a nominated sales agent and the net proceeds after costs remitted to the relevant BHP shareholder. Depending upon the volume of shares to be sold and the structure of the realisation program followed by the nominated sales agent, there is a potential for a temporary overhang in Woodside shares, adversely impacting trading prices, until cleared.

Furthermore, as noted previously in section 1 above, BHP is the world’s largest diversified natural resources company by market capitalisation. It is possible that certain current BHP shareholders may not wish to hold shares in a company with a principal focus and exposure to oil and gas assets and, as a result, may also seek to realise the Woodside shares issued to them in the period following completion of the Proposed Transaction.

18 Based on Woodside’s closing share price of A$33.20 on 24 March 2022 and 1,898.7 million shares on issue in the Merged Group

19 as at 24 March 2022

20 being a BHP shareholder, whose address shown in the register of members of BHP is in a jurisdiction where BHP determines (acting reasonably and following consultation with Woodside) that it would be unlawful, unduly impracticable (in each case in respect of either BHP or Woodside) to distribute the new Woodside shares

21 BHP may, at its discretion, offer Selling Shareholders a voluntary sale facility, whereby BHP Shareholders with less than a certain number of BHP Shares may elect for Woodside shares that would otherwise be issued to them to be sold and the sale proceeds remitted to that Selling Shareholder

15

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

As a result, existing Woodside Shareholders wishing to realise their existing Woodside shares in an orderly manner, may not be able to do so at an “undisturbed” price for an unknown period of time.

| 3.2.2 | The Proposed Transaction is expected to allow Woodside to take a leading position in relation to the transition to new energy |

Woodside has previously announced that it is targeting a 15% equity net emissions reduction by 2025, and a 30% equity net emissions reduction by 2030, with an aspiration to achieve net zero by 205022. Woodside expects these targets to be maintained for the Merged Group.

In addition, Woodside is pursuing opportunities to commercialise new energy products and lower-carbon services as part of its broader product mix. In December 2021, Woodside announced a new target to invest US$5,000 million in new energy products and lower-carbon services by 2030, assuming the Proposed Transaction is completed.

In addition to being more financially robust and better placed to pursue its new energy initiatives, the combination of the Woodside’s and BHP Petroleum’s skilled workforce can also be expected to deepen the Merged Group’s technical capabilities and its ability to manage the new energy transition issues facing the company.

| 3.2.3 | Potential to realise further synergies and cost savings over and above those included in our range of assessed values for the Merged Group |

Woodside’s evaluation of synergy opportunities yielded an initial target of over US$400 million in annual cost savings, which are expected to be realised progressively in the period after completion of the Proposed Transaction, with full implementation expected by early 2024. These costs savings and synergies have been reflected in our range of assessed values for the Merged Group.

As the integration process of Woodside and BHP Petroleum is undertaken, Woodside expects to identify further synergies and value creation opportunities in addition to the identified synergy opportunities above.

To the extent that further benefits are realised, Woodside Shareholders will, in aggregate, have a 52% interest in any upside realised.

| 3.2.4 | Completion of the Proposed Transaction provides immediate access to development and growth opportunities |

Woodside will, in addition to various production assets, gain immediate access to a suite of project development options through the acquisition of BHP Petroleum’s asset portfolio, including various sanctioned (being executed) and unsanctioned projects (unexecuted and awaiting FID) projects.

Immediate access to the operational cash flows provided by BHP Petroleum’s production assets and to a wider suite of development opportunities provides Woodside with increased optionality in terms of capital allocation and project sequencing with the view to maximising return on both Woodside’s existing development portfolio and those acquired with BHP Petroleum.

22 Target is for net equity Scope 1 and 2 greenhouse gas emissions, relative to a starting base of the gross annual average equity Scope 1 and 2 greenhouse gas emissions over 2016-2020 and may be adjusted (up or down) for potential equity changes in producing or sanctioned assets with a Final Investment Decision (FID) prior to 2021. Following completion of the Proposed Transaction, the starting base will be adjusted for the combined Woodside and BHP petroleum portfolio

16

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Woodside’s capital requirements in relation to the Scarborough/Pluto Train 2 and Sangomar projects over the near future, mean that it is unlikely that Woodside would, in the absence of the Proposed Transaction or a similar inorganic transaction, be able to replicate a similar project portfolio in the foreseeable future, nor would it be able to pursue its investment into new energy initiatives to the same extent.

| 3.2.5 | Woodside dividend policy is expected to remain unchanged |

Woodside has indicated that its current dividend policy is expected to be unchanged following completion of the Proposed Transaction.

The Woodside Board has the responsibility of approving dividends. The Woodside Board has determined there will be no change to Woodside’s dividend policy of a minimum of 50% of net profit after tax excluding non-recurring items in dividends. The Woodside Board’s dividend payout ratio target is between 50% to 80% of net profit after tax, excluding non-recurring items, subject to market conditions and investment requirements. Woodside will maintain the flexibility to consider opportunities to provide additional returns to shareholders through special dividends and share buy-backs in periods of excess cash generation.

| 3.2.6 | The relative contribution of each entity to the Merged Group is broadly consistent with the exchange ratio |

The table below shows the contribution of Proved and Probable (2P) Reserves23 and 2C Contingent Resources24, production and certain earnings measures that Woodside and BHP Petroleum will make to the Merged Group relative to the merger terms.

Table 4: Relative contributions to the Merged Group as at 31 December 2021

| Relative Contributions | Woodside | BHP Petroleum |

Contribution% | |||||||||||||||

| Woodside | BHP Petroleum |

|||||||||||||||||

| Reserves and Resources as at 31 December 20211, 2 | ||||||||||||||||||

| 2P (liquids3) million barrels (MMbbl) | 247.0 | 560.4 | 30.6% | 69.4% | ||||||||||||||

| 2P (gas) million barrels oil equivalent (MMboe)4 | 2,157.4 | 916.7 | 70.2% | 29.8% | ||||||||||||||

| Total 2P (MMboe) | 2,404.3 | 1,477.1 | 61.9% | 38.1% | ||||||||||||||

| 2C (liquids3) (MMbbl) | 590.0 | 558.8 | 51.4% | 48.6% | ||||||||||||||

| 2C (gas) (MMboe) | 3,961.0 | 823.8 | 82.8% | 17.2% | ||||||||||||||

| Total 2C (MMboe)5 | 4,551.0 | 1,382.6 | 76.7% | 23.3% | ||||||||||||||

| Production (MMboe) | ||||||||||||||||||

| CY21 (actual)6 | 91.1 | 102.3 | 47.1% | 52.9% | ||||||||||||||

| CY22 (projected)7 | 93.2 | 114.5 | 44.9% | 55.1% | ||||||||||||||

23 2P Reserves are proved reserves plus reserves that are deemed probable (at least 50 per cent likely) to be commercially recoverable

24 2C Contingent Resources is the best estimate of contingent resources. Contingent Resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations by application of development projects, but which are not currently considered to be commercially recoverable owing to one or more contingencies.

17

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| Relative Contributions | Woodside | BHP Petroleum |

Contribution% | |||||||||||||||||

| Woodside | BHP Petroleum |

|||||||||||||||||||

| Earnings ($ millions) | ||||||||||||||||||||

| CY21 Underlying EBITDA8,9 | 4,135 | 4,349 | 48.7% | 51.3% | ||||||||||||||||

| CY21 Underlying NPAT10,11 | 1,620 | 885 | 64.7% | 35.3% | ||||||||||||||||

Source: GaffneyCline’s ITSR, Woodside 2021 Annual Report, BHP Petroleum 2HY21, FY21 and 2HY20 financial reports and KPMG Corporate Finance analysis

Notes:

| 1. | Reserves and Resources included in the table above may differ from those reported by Woodside and BHP Petroleum (including those reported in Tables 7, 8, 9, 22 and 23 below) as the above figures reflect GaffneyCline’s assessment of Reserves and Resources as set out in the ITSR |

| 2. | Gas Reserves in the table above are inclusive of volumes consumed in operations (CIO or fuel) per GaffneyCline’s ITSR |

| 3. | Liquids reserves and resources includes oil, condensate, natural gas liquids and LPG |

| 4. | BHP Petroleum’s net gas Reserves and Resources have been converted from billion cubic feet (Bcf) to MMBoe by dividing by a conversion factor of 6.0 for all assets except the NWS Project, NWS Oil and Scarborough (including Thebe and Jupiter), where a conversion factor of 5.8 has been adopted (consistent with the factor adopted by KPMG Corporate Finance for the Woodside interest in those projects) |

| 5. | 2C Contingent Resources in this table are BHP Petroleum’s working interest fraction of the gross field resources |

| 6. | Production from Algeria and Neptune is excluded from BHP Petroleum production |

| 7. | Projected CY22 production has been based on the aggregate of the production profiles prepared by GaffneyCline for each of the individual assets |

| 8. | Underlying EBITDA for Woodside has been calculated as profit before tax add net finance costs, depreciation and amortisation and net impairment costs |

| 9. | Underlying EBITDA for BHP Petroleum has been calculated as profit before tax add net finance costs, depreciation and amortisation, net impairment costs, onerous lease costs, exploration leases and other one-off costs |

| 10. | Underlying NPAT for Woodside excludes amounts relating to cost write-offs, impairment losses, impairment reversals and prior period impacts |

| 11. | Underlying NPAT for BHP Petroleum has been calculated as profit before tax add net finance costs, net impairment costs, office onerous lease costs, exploration lease costs and other costs. |

This analysis indicates that:

| ● | whilst BHP Petroleum is contributing significantly less than the exchange ratio in relation to both aggregate 2P Reserves and 2C Contingent Resources on an MMboe basis, it is contributing approximately 69% of 2P liquids Reserves and 49% of 2C liquids Contingent Resources, which we consider to be one of the key drivers of the Proposed Transaction in terms of the Merged Group’s near term cash flows and earnings |

| ● | BHP Petroleum is contributing approximately 53% of actual CY21 MMboe production and a similar contribution to projected CY22 MMboe production |

| ● | BHP Petroleum is contributing approximately 51% of underlying CY21 EBITDA |

| ● | BHP Petroleum is contributing approximately 35% to the Merged Group’s CY21 underlying NPAT. This figure includes US$311 million in relation to BHP Petroleum pre-tax finance charges, which given the BHP Petroleum assets are being acquired on a cash-free, debt-free basis should be added-back. In addition, Woodside has identified that in order to achieve consistency with its accounting policies, a further net negative post tax adjustment of US$156 million is required. Adjusting for these would increase BHP Petroleum’s relative contribution to 39%. |

18

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Having regard to each of the above measures individually and in aggregate, we consider the relative contribution of BHP Petroleum to be broadly supportive of the exchange ratio.

| 3.2.7 | The potential for Woodside Shareholders to receive an offer for their shares inclusive of a full control premium may, in theory, be reduced |

Whilst following completion of the Proposed Transaction the Merged Group’s share register will be open, with no single shareholder holding over 7% of its share capital, Woodside will be of a size that:

| ● | there is no other logical domestic industry purchaser for the whole of Woodside |

| ● | the pool of potential international purchasers with the financial capacity to complete a takeover will be reduced and the likelihood of receiving approval for any acquisition under Australia’s Foreign Acquisition and Takeovers Act may be problematic. |

However, with a current market capitalisation of A$32,668 million, as at 24 March 2022, it is reasonably arguable that the pool of potential acquirers for Woodside as a standalone entity is already limited and would likely face the same regulatory hurdles.

Accordingly, whilst in theory completion of Proposed Transaction may reduce the prospects of Woodside Shareholders receiving an offer for their shares, this is unlikely to be a significant disadvantage.

| 3.3 | Consequences of not approving the Proposed Transaction |

In the event that the Proposed Transaction is not approved or any conditions precedent prevents the Proposed Transaction from being implemented, Woodside will continue to operate in its current form and remain listed on the ASX. As a consequence:

| ● | Woodside Shareholders will collectively continue to hold 100% of the issued capital of Woodside |

| ● | the implications of the Proposed Transaction, as summarised above, will not occur |

| ● | Woodside Shareholders will continue to be exposed to the benefits and risks associated with an investment in Woodside, which, over the medium to longer term, will, based on its current strategy, be closely aligned to the success or otherwise of the future development of the Scarborough/Pluto Train 2 and Sangomar projects as they move through their development and operational cycles |

| ● | BHP Petroleum will retain the right to exercise the put option for the sale of its interest in the Scarborough project, which, if exercised, will result in a significant leakage of funds from Woodside, along with, in the absence of a sell-down, an increased capital commitment during Scarborough’s construction phase, placing pressure on Woodside’s free cash flow position ahead of production, currently scheduled for 2026 |

| ● | there is the potential for Woodside’s credit rating to be downgraded, which, all other things equal, could lead to an increase in Woodside’s cost of funding |

| ● | the Woodside dividend payable to BHP in the event the Proposed Transaction is completed will not be paid. This payment, which totals approximately US$830 million is, in effect, the payment to BHP representing the cash dividend that would have been received by BHP shareholders had they had Woodside shareholders as at 1 July 2021 |

19

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | Woodside will not receive any “locked box payment” representing the net cash flow generated by BHP Petroleum over the period since 1 July 2021 to completion. Woodside has estimated this net cash inflow to be in the order US$900 million as at 31 December 2021 prior to accounting for any cash held in bank accounts beneficially controlled by BHP Petroleum |

| ● | A break fee may be payable depending upon the circumstances leading to the Proposed Transaction not proceeding |

| ● | Woodside will have incurred various costs related to the Proposed Transaction that will still be required to be paid. Woodside estimates that costs incurred will total in the order of US$100 million, pre-tax. |

Our opinion is based solely on information available as at the date of this report as set out in Appendix 2 of this report. We note that we have not undertaken to update our report for events or circumstances arising after the date of this report other than those of a material nature which would impact upon our opinion. We also refer readers to the limitations and reliance on information set out below in section 6 of our report.

| 4 | Other matters |

In forming our opinion, we have considered the interests of Woodside Shareholders as a whole. This advice therefore does not consider the financial situation, objectives or needs of individual Woodside shareholders. It is not practical or possible to assess the implications of the Proposed Transaction on individual Woodside shareholders as their financial circumstances are not known to us. The decision of Woodside shareholders as to whether to approve the Proposed Transaction is a matter for individuals based on, amongst other things, their risk profile, liquidity preference, investment strategy and tax position. Individual Woodside shareholders should therefore consider the appropriateness of our opinion to their specific circumstances before acting on it. As an individual’s decision to vote for or against the proposed resolutions may be influenced by his or her particular circumstances, we recommend that individual Woodside Shareholders, including residents of foreign jurisdictions, seek their own independent professional advice.

We understand that Woodside intends to seek a secondary listing of its shares on certain overseas stock exchanges and that this report may be required to be filed, purely for information purposes, with certain overseas regulatory authorities, along with other documentation, to facilitate these secondary listings. Readers of this report should note that our report has been prepared:

| ● | having principal regard to relevant provisions of Australian legislation and other applicable Australian regulatory requirements |

| ● | solely for the purpose of assisting Woodside Shareholders in considering the Proposed Transaction and for no other purpose. |

We do not assume any responsibility or liability to any other party as a result of reliance on or use of this report for any other purpose.

20

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

Neither the whole nor any part of this report or its attachments or any reference thereto may be included in or attached to any document, other than the Meeting Documents to be sent to Woodside Shareholders in relation to the Proposed Transaction, without the prior written consent of KPMG Corporate Finance as to the form and context in which it appears. KPMG Corporate Finance consents to the inclusion of this report in the form and context in which it appears in the Explanatory Memorandum.

All figures set out in this report are in nominal terms unless otherwise noted.

References to:

| ● | financial years have been abbreviated to FY |

| ● | calendar years have been abbreviated to CY (where different to the relevant entity’s FY) |

| ● | 6-month periods of a financial year have been abbreviated to HY. |

The above opinion should be considered in conjunction with and not independently of the information set out in the remainder of this report, including the appendices.

Yours faithfully

| Jason Hughes |

Bill Allen Authorised Representative |

Sean Collins Authorised Representative |

21

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| Contents |

||||||

| Part One – Independent Expert Report | 1 | |||||

| 1 | Introduction | 1 | ||||

| 2 | Technical Requirements | 4 | ||||

| 3 | Opinion | 6 | ||||

| 4 | Other matters | 20 | ||||

| 5 | Summary of the Proposed Transaction | 23 | ||||

| 6 | Scope of the report | 25 | ||||

| 7 | Industry overview | 28 | ||||

| 8 | Profile of Woodside | 29 | ||||

| 9 | Profile of BHP Petroleum | 65 | ||||

| 10 | Profile of the Merged Group | 88 | ||||

| 11 | Valuation Assessment | 101 | ||||

| Appendix 1 – KPMG Corporate Finance Disclosures | 166 | |||||

| Appendix 2 – Sources of information | 168 | |||||

| Appendix 3 – Overview of the oil and gas industry | 169 | |||||

| Appendix 4 – Production, operating and capital cost profiles | 206 | |||||

| Appendix 5 – Calculation of discount rates | 239 | |||||

| Appendix 6 – Listed companies – betas and gearing | 250 | |||||

| Appendix 7 – Selected upstream and midstream LNG production and processing comparable companies | 254 | |||||

| Appendix 8 – Upstream and midstream LNG production and processing comparable company multiples | 256 | |||||

| Appendix 9 – Selected conventional upstream hydrocarbon production comparable companies | 259 | |||||

| Appendix 10 – Conventional upstream hydrocarbon production comparable company multiples | 261 | |||||

| Appendix 11 – Selected upstream and midstream LNG production and processing comparable transactions | 264 | |||||

| Appendix 12 – Upstream and midstream LNG production and processing comparable transaction multiples | 265 | |||||

| Appendix 13 – Selected conventional upstream hydrocarbon production comparable transactions | 267 | |||||

| Appendix 14 – Conventional upstream hydrocarbon production comparable transaction multiples | 269 | |||||

| Appendix 15 – GaffneyCline report | 271 | |||||

| Part Two – KPMG FAS Corporate Finance Financial Services Guide | 272 | |||||

22

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| 5 | Summary of the Proposed Transaction |

| 5.1 | Consideration |

The principal terms of the Proposed Transaction as they affect Woodside Shareholders are, in broad terms, that in consideration for the acquisition of 100% of the issued capital of BHP Petroleum on a cash and debt free basis with an effective date of 1 July 2021, Woodside will:

| ● | issue new ordinary Woodside shares to BHP, equivalent to an approximate 48% shareholding in the Merged Group upon implementation. BHP will in turn immediately distribute these new Woodside shares to eligible BHP shareholders as a special dividend, which BHP intends to fully frank |

| ● | in the event that the net post-tax cashflows from the ordinary operations of BHP Petroleum (including any capital expenditure and/or receipts from the disposal of specified fixed assets) in the period between the Effective Date and completion of the Proposed Transaction are negative, re-imburse BHP the shortfall, or, in the event these net post-tax cash flows are positive, BHP will pay to Woodside this amount |

| ● | make a cash payment to BHP in relation to cash dividends paid by Woodside between the Effective Date and completion that would have been received by BHP had the Merger Consideration been paid on the Effective Date |

| ● | settle/receive the benefit of any other adjustments to the purchase consideration that may be required, either positive or negative, as a result of the operation of the SSA not captured in the abovementioned limbs. |

| 5.2 | Conditions precedent |

Completion of the Proposed Transaction is subject to the satisfaction25 of a number of conditions precedent as set out in the SSA, including, but not limited to:

| ● | all regulatory and other approvals, consents, clearances and permissions to give the Proposed Transaction effect having been obtained from all relevant bodies, including, amongst others, the Australian Competition and Consumer Commission (ACCC), the National Offshore Petroleum Titles Administrator, ASIC, ASX, the Committee on Foreign Investment in the US, and, if required, the Foreign Investment Review Board |

| ● | Woodside Shareholders approving the merger resolution |

| ● | the independent expert concluding that the Proposed Transaction is in the best interests of Woodside Shareholders and maintaining that opinion until Woodside Shareholders meet to vote on the Proposed Transaction |

| ● | each US Registration Statement has been declared effective by the US Securities and Exchange Commission (SEC) in accordance with the provisions of the US Securities Act and the US Exchange Act, as applicable |

25 Certain conditions precedent are able to be waived

23

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | approval by various foreign jurisdiction regulatory competition authorities including in Trinidad and Tobago, the People’s Republic of China, Japan, Mexico, Vietnam and Barbados. |

As at the date of this report, Woodside has confirmed that it is not aware of any reason to expect that the conditions precedent will not be satisfied or waived as required.

| 5.3 | London Stock Exchange and New York Stock Exchange listings |

Woodside must use its reasonable to endeavours to secure the approval of the regulatory authorities, the LSE and the NYSE that its shares, including the Woodside securities to be issued as consideration for the Proposed Transaction, will be listed on each bourse.

| 5.4 | Termination |

Both Woodside and BHP have the right to terminate the SSA in certain specified circumstances, including as a result of, inter alia:

| ● | the inability to satisfy a specified condition precedent by 30 June 202226 (the Cut-Off Date) |

| ● | a material breach by the other party of its obligations and/or the warranties given under the SSA, provided that in the case of a warranty breach, the loss can reasonably be expected to exceed US$500 million |

| ● | a half or more of the other party’s Board members or (only as expressly permitted under the SSA) a majority of the company’s own Board withdraw their support for the Proposed Transaction |

| ● | a material adverse event or change in condition or circumstances of the other party as defined in the SSA |

| ● | certain prescribed circumstances. |

| 5.5 | Reimbursement fee |

Woodside must pay to BHP and BHP must pay to Woodside a reimbursement fee of US$160 million in certain specified events and circumstances (Reimbursement Fee), including, inter alia, due to the termination of the SSA for a material breach of obligations or warranties which is unable to be remedied as required.

Further details in relation to the Proposed Transaction are set out in sections 3 and 10 of the Explanatory Memorandum to which this report is attached, and in Woodside’s and BHP’s announcements to the ASX on 17 August 2021 and 22 November 2021.

| 26 | which may be extended by agreement between the parties or in limited circumstances set out in the SSA |

24

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| 6 | Scope of the report |

| 6.1 | Purpose |

This report has been prepared by KPMG Corporate Finance for inclusion in the Explanatory Memorandum to accompany the Notice of Meeting convening a meeting of Woodside Shareholders on or around 19 May 2022. The purpose of the meeting will be to seek approval of the Proposed Transaction.

| 6.2 | Limitations and reliance on information |

In preparing this report and arriving at our opinion, we have considered the information detailed in Appendix 2 of this report. In forming our opinion, we have relied upon the truth, accuracy and completeness of any information provided or made available to us without independently verifying it. Nothing in this report should be taken to imply that KPMG Corporate Finance has in any way carried out an audit of the books of account or other records of either Woodside or BHP Petroleum for the purposes of this report.

Further, we note that an important part of the information base used in forming our opinion is comprised of the opinions and judgements of management. In addition, we have also had discussions with Woodside’s management and BHP Petroleum in relation to the nature of Woodside’s and BHP Petroleum’s business operations, its specific risks and opportunities, its historical results and its prospects for the foreseeable future. This type of information has been evaluated through analysis, enquiry and review to the extent practical. However, such information is often not capable of external verification or validation.

Woodside has been responsible for ensuring that information provided by it or its representatives is not false, misleading or incomplete. Complete information is deemed to be information which at the time of completing this report should have been made available to KPMG Corporate Finance and would have reasonably been expected to have been made available to KPMG Corporate Finance to enable us to form our opinion.

We have no reason to believe that any material facts have been withheld from us but do not warrant that our inquiries have revealed all of the matters which an audit or extensive examination might disclose. The statements and opinions included in this report are given in good faith, and in the belief that such statements and opinions are not false or misleading.

The information provided to KPMG Corporate Finance and GaffneyCline, the independent oil and gas technical specialist retained to assist us in the valuation of Woodside and BHP Petroleum, included forecasts/projections and other statements and assumptions about future matters (forward-looking financial information) prepared by the management of Woodside, including, but not limited, to cash flow forecasts for each of Woodside’s and BHP Petroleum’s production and development/growth assets.

Whilst KPMG Corporate Finance and GaffneyCline have relied upon this forward-looking financial information in preparing this report, Woodside remains responsible for all aspects of this forward-looking financial information. The forecasts and projections as supplied to us, including those provided by GaffneyCline, are based upon assumptions about events and circumstances which have not yet transpired. We have not tested individual assumptions or attempted to substantiate the veracity or integrity of such assumptions in relation to any forward-looking financial information, however we have made sufficient enquiries to satisfy ourselves that such information has been prepared on a reasonable basis. In making this assessment we have taken the following into account:

25

|

|

Woodside Petroleum Ltd Independent Expert Report and Financial Services Guide 8 April 2022 | |

| ● | Woodside has sophisticated management and reporting processes and is subject to the reporting requirements of a public company listed on the ASX and registered under the Act |

| ● | Woodside completed a significant level of due diligence enquiry in relation to the BHP Petroleum assets and the findings of these enquiries were reflected in Woodside’s forecast operational cash flows for BHP Petroleum |

| ● | KPMG Corporate Finance issued GaffneyCline, an independent and highly experienced petroleum industry technical specialist, with a scope of work to undertake various enquiries in relation to the forecast project information for Woodside and BHP Petroleum, including a review of technical and operational data and holding discussions with management in regard to the technical and operational assumptions underlying the forecast operations of both Woodside and BHP Petroleum. GaffneyCline has, where necessary, made adjustments to reflect its judgement and provided its preferred forecast production, operational and cost schedules to KPMG Corporate Finance |

| ● | the starting point for GaffneyCline’s work was operational plans provided by Woodside to GaffneyCline for each production/development asset. GaffneyCline also received information directly from BHP |

| ● | GaffneyCline has considered the requirements of the VALMIN Code in relation to appropriate valuation methodologies having had regard to the development status of each project |