UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

August 19, 2014

| BHP BILLITON LIMITED (ABN 49 004 028 077) (Exact name of Registrant as specified in its charter)

VICTORIA, AUSTRALIA (Jurisdiction of incorporation or organisation)

171 COLLINS STREET, MELBOURNE, VICTORIA 3000 AUSTRALIA (Address of principal executive offices) |

BHP BILLITON PLC (REG. NO. 3196209) (Exact name of Registrant as specified in its charter)

ENGLAND AND WALES (Jurisdiction of incorporation or organisation)

NEATHOUSE PLACE, VICTORIA, LONDON, UNITED KINGDOM (Address of principal executive offices) |

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

x Form 20-F ¨ Form 40-F

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934: ¨ Yes x No

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): n/a

19 August 2014

For Announcement to the Market

Name of Companies: BHP Billiton Limited (ABN 49 004 028 077) and

BHP Billiton

Plc (Registration No. 3196209)

Report for the year ended 30 June 2014

This

statement includes the consolidated results of the BHP Billiton Group, comprising BHP Billiton Limited and BHP Billiton Plc, for the year ended 30 June 2014 compared with the year ended 30 June 2013.

This page and the following 51 pages comprise the year end information given to ASX under Listing Rule 4.3A and released to the market under UK Listing Rule 9.7A. The 2014 BHP

Billiton Group annual financial report will be released in September.

The results are prepared in accordance with IFRS and are presented in US dollars.

US$ Million

Revenue up 1.9% to 67,206

Profit attributable to the members of the BHP Billiton Group up 23.2% to 13,832

Net Tangible

Asset Backing:

Net tangible assets per fully paid share were US$14.95 as at 30 June 2014, compared with US$13.05 as at 30 June 2013.

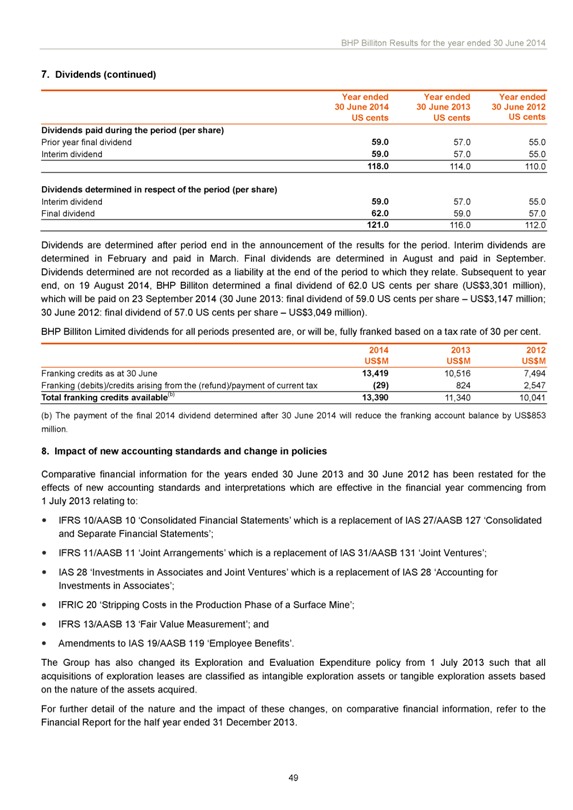

Dividends per share:

Final dividend for current period US 62 cents fully franked

(record date 5 September 2014; payment date 23 September 2014)

Final dividend for previous

corresponding period US 59 cents fully franked

This statement was approved by the Board of Directors.

Jane McAloon

Group Company Secretary

BHP Billiton Limited and BHP Billiton Plc

bhpbilliton

resourcing the future

NEWS RELEASE

Release Time IMMEDIATE

Date 19 August 2014

Number 15/14

BHP BILLITON RESULTS FOR THE YEAR ENDED 30 JUNE 2014

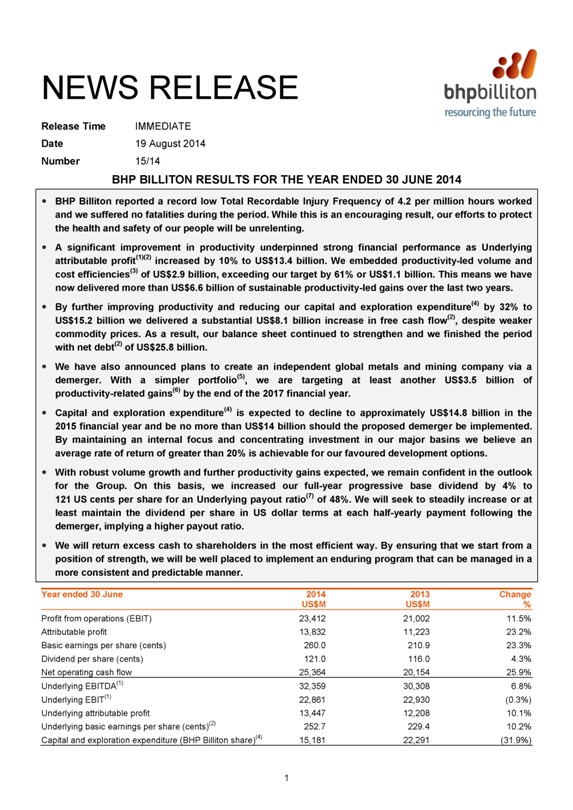

BHP Billiton reported a record low Total

Recordable Injury Frequency of 4.2 per million hours worked and we suffered no fatalities during the period. While this is an encouraging result, our efforts to protect the health and safety of our people will be unrelenting.

A significant improvement in productivity underpinned strong financial performance as Underlying attributable profit(1)(2) increased by 10% to US$13.4 billion. We embedded

productivity-led volume and cost efficiencies(3) of US$2.9 billion, exceeding our target by 61% or US$1.1 billion. This means we have now delivered more than US$6.6 billion of sustainable productivity-led gains over the last two years.

By further improving productivity and reducing our capital and exploration expenditure(4) by 32% to US$15.2 billion we delivered a substantial US$8.1 billion increase in free cash

flow(2), despite weaker commodity prices. As a result, our balance sheet continued to strengthen and we finished the period with net debt(2) of US$25.8 billion.

We

have also announced plans to create an independent global metals and mining company via a demerger. With a simpler portfolio(5), we are targeting at least another US$3.5 billion of productivity-related gains(6) by the end of the 2017 financial year.

Capital and exploration expenditure(4) is expected to decline to approximately US$14.8 billion in the 2015 financial year and be no more than US$14 billion should

the proposed demerger be implemented. By maintaining an internal focus and concentrating investment in our major basins we believe an average rate of return of greater than 20% is achievable for our favoured development options.

With robust volume growth and further productivity gains expected, we remain confident in the outlook for the Group. On this basis, we increased our full-year progressive base

dividend by 4% to 121 US cents per share for an Underlying payout ratio(7) of 48%. We will seek to steadily increase or at least maintain the dividend per share in US dollar terms at each half-yearly payment following the demerger, implying a higher

payout ratio.

We will return excess cash to shareholders in the most efficient way. By ensuring that we start from a position of strength, we will be well placed

to implement an enduring program that can be managed in a more consistent and predictable manner.

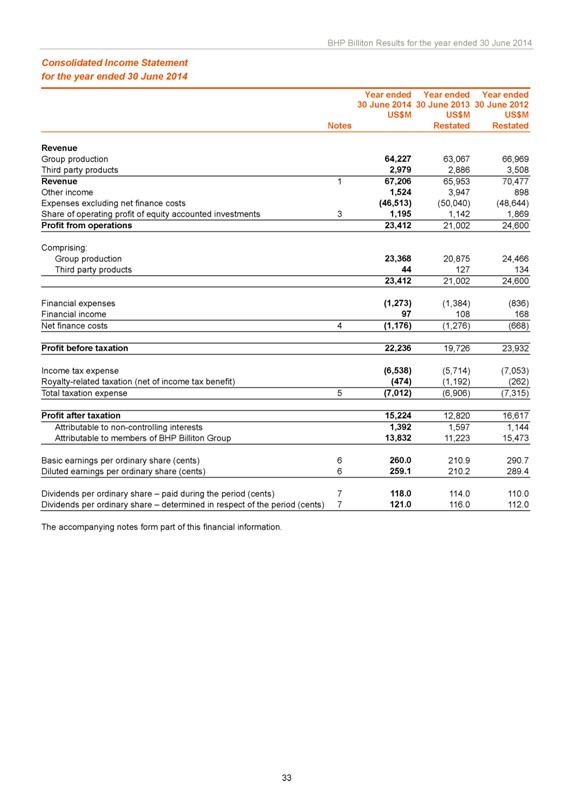

Year ended 30 June 2014 2013 Change

US$M US$M %

Profit from operations (EBIT) 23,412 21,002 11.5%

Attributable profit 13,832 11,223 23.2%

Basic earnings per share (cents) 260.0 210.9 23.3%

Dividend per share (cents) 121.0 116.0 4.3%

Net operating cash flow 25,364

20,154 25.9%

Underlying EBITDA(1) 32,359 30,308 6.8%

Underlying EBIT(1)

22,861 22,930 (0.3%)

Underlying attributable profit 13,447 12,208 10.1%

Underlying basic earnings per share (cents)(2) 252.7 229.4 10.2%

Capital and

exploration expenditure (BHP Billiton share)(4) 15,181 22,291 (31.9%)

| 1 |

News Release

Results for the 2014 financial year

BHP Billiton Chief Executive Officer, Andrew Mackenzie, said: “In the last 12 months we have delivered on our commitments. Our operational performance

continued to improve, enabling us to exceed production guidance for a number of our core commodities including iron ore, metallurgical coal and petroleum liquids. Productivity-led volume and cost efficiencies(3) of US$2.9 billion were US$1.1 billion

ahead of plan, meaning we have now embedded more than US$6.6 billion of sustainable, annualised productivity-led gains over the last two years.” He added: “BHP Billiton is becoming a simpler, more productive company and the demerger

proposal we have announced today is an important step forward. We plan to create an independent global metals and mining company based on a selection of high-quality aluminium, coal, manganese, nickel and silver assets. Separating these businesses

via a demerger has the potential to unlock shareholder value by allowing BHP Billiton to improve the productivity of its largest businesses more quickly and by creating a new company specifically designed to enhance the performance of its assets.

With a simpler portfolio(5), we are targeting at least another US$3.5 billion of productivity-related gains(6) by the end of the 2017 financial year.

“Our

Iron Ore business clearly illustrates this opportunity. At Western Australia Iron Ore, we now expect the debottlenecking of our mines and inner harbour infrastructure to increase our supply-chain capacity to 290 Mtpa (100 per cent basis). The

additional 65 Mtpa of capacity is likely to have a capital intensity below US$50 per annual tonne with the improvement in productivity and economies of scale also expected to significantly reduce unit costs. “With robust volume growth and

further productivity gains expected, we remain confident in the outlook for the Group. On this basis, we increased our full-year progressive base dividend by four per cent to 121 US cents per share for an Underlying payout ratio of 48 per cent. We

will seek to steadily increase or at least maintain the dividend per share in US dollar terms at each half-yearly payment following the demerger, implying a higher payout ratio.” He concluded by saying: “The pace at which our balance sheet

strengthens will also depend on external factors, such as commodity prices and foreign exchange rates. As in the past, we will return excess cash to shareholders in the most efficient way. By ensuring that we start from a position of strength, we

will be well placed to implement an enduring program that can be managed in a more consistent and predictable manner.”

2

BHP Billiton Results for the year ended 30 June 2014

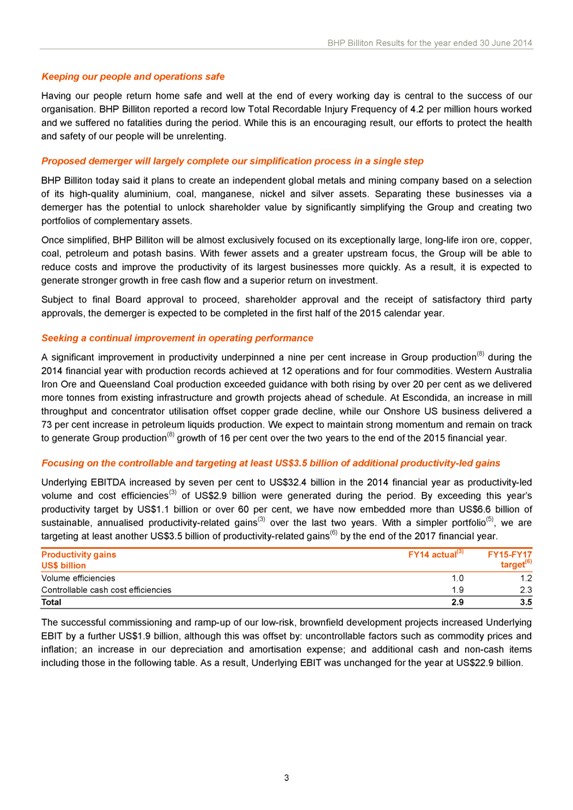

Keeping our people and operations safe

Having our people return home safe and

well at the end of every working day is central to the success of our organisation. BHP Billiton reported a record low Total Recordable Injury Frequency of 4.2 per million hours worked and we suffered no fatalities during the period. While this is

an encouraging result, our efforts to protect the health and safety of our people will be unrelenting.

Proposed demerger will largely complete our simplification

process in a single step

BHP Billiton today said it plans to create an independent global metals and mining company based on a selection of its high-quality

aluminium, coal, manganese, nickel and silver assets. Separating these businesses via a demerger has the potential to unlock shareholder value by significantly simplifying the Group and creating two portfolios of complementary assets.

Once simplified, BHP Billiton will be almost exclusively focused on its exceptionally large, long-life iron ore, copper, coal, petroleum and potash basins. With fewer assets and a

greater upstream focus, the Group will be able to reduce costs and improve the productivity of its largest businesses more quickly. As a result, it is expected to generate stronger growth in free cash flow and a superior return on investment.

Subject to final Board approval to proceed, shareholder approval and the receipt of satisfactory third party approvals, the demerger is expected to be completed in

the first half of the 2015 calendar year.

Seeking a continual improvement in operating performance

A significant improvement in productivity underpinned a nine per cent increase in Group production(8) during the 2014 financial year with production records achieved at 12

operations and for four commodities. Western Australia Iron Ore and Queensland Coal production exceeded guidance with both rising by over 20 per cent as we delivered more tonnes from existing infrastructure and growth projects ahead of schedule. At

Escondida, an increase in mill throughput and concentrator utilisation offset copper grade decline, while our Onshore US business delivered a 73 per cent increase in petroleum liquids production. We expect to maintain strong momentum and remain on

track to generate Group production(8) growth of 16 per cent over the two years to the end of the 2015 financial year.

Focusing on the controllable and targeting at

least US$3.5 billion of additional productivity-led gains

Underlying EBITDA increased by seven per cent to US$32.4 billion in the 2014 financial year as

productivity-led volume and cost efficiencies(3) of US$2.9 billion were generated during the period. By exceeding this year’s productivity target by US$1.1 billion or over 60 per cent, we have now embedded more than US$6.6 billion of

sustainable, annualised productivity-related gains(3) over the last two years. With a simpler portfolio(5), we are targeting at least another US$3.5 billion of productivity-related gains(6) by the end of the 2017 financial year.

Productivity gains FY14 actual(3) FY15-FY17

US$ billion target(6)

Volume efficiencies 1.0 1.2

Controllable cash cost efficiencies 1.9 2.3

Total 2.9 3.5

The successful commissioning and ramp-up of our low-risk, brownfield development

projects increased Underlying EBIT by a further US$1.9 billion, although this was offset by: uncontrollable factors such as commodity prices and inflation; an increase in our depreciation and amortisation expense; and additional cash and non-cash

items including those in the following table. As a result, Underlying EBIT was unchanged for the year at US$22.9 billion.

3

News Release

Additional items December 2013 half

year 2014 financial year

Underlying Underlying Underlying Underlying

US$

billion EBITDA EBIT EBITDA EBIT

Impairments(i) - (0.1) - (0.8)

Mine site

rehabilitation(ii) - - (0.3) (0.3)

Redundancies(iii) - - (0.1) (0.1)

Closure

costs(iv) - - (0.2) (0.2)

Other(v) (0.1) (0.1) (0.1) (0.1)

Total (0.1) (0.2)

(0.7) (1.5)

(i) Includes impairment charges at Energy Coal South Africa (US$292 million); charges for minor Gulf of Mexico assets (US$184 million); a charge in our

Potash business associated with the Port of Vancouver (US) (US$68 million) and other minor charges (US$253 million).

(ii) Represents a US$300 million charge

related to the revision of mine site rehabilitation provisions for the Group’s North American closed mines.

(iii) Includes redundancies from restructuring

programs in Iron Ore (US$63 million), Coal (US$40 million) and Aluminium, Manganese and Nickel (US$40 million).

(iv) Includes costs associated with the closure of

the Perseverance underground mine (US$21 million) and the cessation of smelting activities at Bayside (US$135 million).

(v) Includes UK pension plan charges

(US$112 million), the profit on sale of Liverpool Bay (US$120 million), the profit on sale of the Energy Coal South Africa Optimum Coal Purchase agreement (US$84 million) and an adjustment to the Browse divestment proceeds (US$143 million charge).

Underlying attributable profit increased by 10 per cent to US$13.4 billion in the 2014 financial year, benefitting from a reduction in the Group’s

adjusted effective tax rate(2) to 32.5 per cent. Attributable profit was US$13.8 billion and included exceptional items of US$385 million (after tax).

Strong

growth in free cash flow despite volatile commodity markets

By further improving productivity and reducing our rate of investment we delivered a substantial US$8.1

billion increase in free cash flow, despite weaker commodity prices. In this context, capital and exploration expenditure(4) declined by 32 per cent to US$15.2 billion in the period.

As a result, our balance sheet continued to strengthen and we finished the period with net debt of US$25.8 billion for a gearing ratio of 23 per cent. This includes US$757

million of finance leases that were brought to account in the June 2014 half year.

With robust volume growth and further productivity gains expected, we remain

confident in the outlook for the Group. On this basis, we have increased our full-year progressive base dividend by four per cent to 121 US cents per share (December 2013 half year: 59 US cents per share; June 2014 half year: 62 US cents per share).

This equates to an annual distribution of US$6.4 billion which is comfortably covered by free cash flow. In total, we have now returned US$64 billion in the form of dividends and buy-backs over the last 10 years, equivalent to an Underlying payout

ratio of approximately 50 per cent.

A strong balance sheet and selective investment will enable us to grow value and shareholder returns

Capital and exploration expenditure(4) is expected to decline to approximately US$14.8 billion in the 2015 financial year and be no more than US$14 billion should the proposed

demerger be implemented. Our investment plans will be optimised within this framework to deliver the best results in terms of net present value, internal rate of return, return on capital employed and operating margin.

At the end of the 2014 financial year, the group had eight major projects under development with a combined budget of US$14.1 billion. Beyond our current projects in execution, the

Group’s opportunity-rich portfolio remains a key point of differentiation and allows us to maintain an internal focus. As we concentrate investment in our major basins, fewer projects will pass through our tollgates and prospective investment

returns will rise. We believe that an average rate of return of greater than 20 per cent (ungeared, after tax, nominal dollars) is achievable for our favoured development options.

4

BHP Billiton Results for the year ended 30 June 2014

These growth options and our broader commitment to improve operating performance will underpin the longer-term growth of our progressive base dividend. In this context, we will

seek to steadily increase or at least maintain the dividend per share in US dollar terms at each half-yearly payment following the demerger, implying a higher payout ratio.

The pace at which our balance sheet strengthens will also depend on external factors, such as commodity prices and foreign exchange rates. As in the past, we will return excess

cash to shareholders in the most efficient way. By ensuring that we start from a position of strength, we will be well placed to implement an enduring program that can be managed in a more consistent and predictable manner.

Outlook

Economic outlook

The global economy grew at a moderate rate in the 2014 financial year. Momentum in the United States, Japan and the United Kingdom was underpinned by central bank monetary policy.

Europe’s economy improved marginally, although the recovery was constrained by high levels of unemployment. Emerging markets, including China, experienced a moderate slowdown.

In a relative sense, the Chinese economy continues to grow strongly with signs that it is rebalancing. Consumption continued to be supported by higher household incomes while fixed

asset investment softened, led by the property sector, as the central bank restricted access to credit. Rapid credit growth in the non-bank financial sector remained an important concern for policymakers.

We remain confident in the short to medium-term outlook for the Chinese economy. Measured stimulus recently introduced by the government demonstrates their commitment to maintain

economic growth above seven per cent. We believe consumption and services will continue to increase in importance, while the market’s role in allocating capital will be enhanced. Greater transparency within the fiscal system is also expected to

reshape the relationship between central and local government.

The underlying performance of the United States economy continued to improve despite the significant

disruption caused by severe weather in the March 2014 quarter. The curtailment of quantitative easing appears to have had a limited impact on sentiment as a solid increase in demand reflects a stronger labour market, rising disposable incomes, and

higher equities and housing prices. Business investment has been a weak link in the recovery so far as companies have responded slowly to better economic conditions, despite higher levels of profitability. An increase in capital spending will be

required to sustain the recovery in the medium term.

The Japanese economy has responded strongly to expansionary monetary and fiscal policy over the past year.

Investment spending and wages increased as corporate profits benefited from the depreciation of the yen, while an increase in the national sales tax in April had a limited impact on consumption. These factors have increased the potential for faster

growth in the short term, although a longer-term, sustainable recovery will be contingent on the scale and speed of structural reform.

With regard to the global

economy, stronger United States growth and an associated tightening of monetary policy could result in the rapid outflow of capital from emerging economies. However, developing nations with sound macroeconomic fundamentals would be less likely to

experience a severe impact from this transition.

Commodities

Commodity

markets were volatile in the second half of the 2014 financial year.

As anticipated, Chinese crude steel production growth decelerated in response to weakness in

the construction sector. On average, we expect the ratio of Chinese crude steel production growth to underlying GDP growth to remain below one, although seasonal factors and policy settings will continue to influence short-term output. Global steel

demand growth outside of China is likely to accelerate during the remainder of the 2014 calendar year.

5

News Release

The supply of steelmaking raw

materials has grown more quickly than demand. As predicted, lower-cost seaborne iron ore supply is increasingly displacing higher-cost Chinese domestic production. As this trend continues, the cost curve is likely to flatten as high-cost production

exits the market. In metallurgical coal, high-cost, uneconomic supply has remained resilient although we do expect to see an increasing number of production cuts, particularly in the United States. Given robust underlying demand growth for premium

hard coking coals, pricing for our products is likely to be well supported in the medium and longer term.

Indonesian and Australian exports continue to keep the

thermal coal market well supplied, prolonging the weaker pricing environment. While demand from key importing regions remains steady, prices are unlikely to respond unless uneconomic supply exits the market.

In copper, robust demand for refined metal, supply disruptions and a shortage of scrap has ensured that the market remains broadly balanced. We believe the longer-term fundamentals

for copper remain compelling as grade decline, rising costs and a scarcity of high-quality future development opportunities are likely to constrain supply. Demand growth, supply disruptions and geopolitical tension have continued to support crude

oil prices. We expect prices to remain supported by an increase in demand from non-OECD countries, which has recently outstripped demand from OECD countries.

United States natural gas prices benefited from a cold winter which reduced inventory levels significantly below the five-year average. In the longer term, demand

is expected to benefit from increasing industrial use, growth in gas fired power generation and the commencement of LNG exports. Conversely, high inventory levels at Asian utilities, mild summer temperatures and the commissioning of additional

supply have led to a decline in Asia-Pacific LNG prices from their February peak.

The nickel price rose sharply during the period as the Indonesian ore export ban

took effect in the March 2014 quarter. Demand growth remains robust given rising stainless steel production in China, Europe and the United States.

While aluminium

demand growth has been strong, new supply continues to offset the curtailment of high-cost capacity. However, we expect the premia currently being realised in certain regions to remain at elevated levels as warehouse bottlenecks are likely to take

some time to be resolved.

In summary, a balanced global economic outlook should provide support for our markets, albeit with more moderate rates of demand growth.

In the longer term, wealth creation and urbanisation will remain the primary drivers of commodities demand, although the transition to consumption-led growth in emerging economies should provide particular support for industrial metals, energy and

fertilisers.

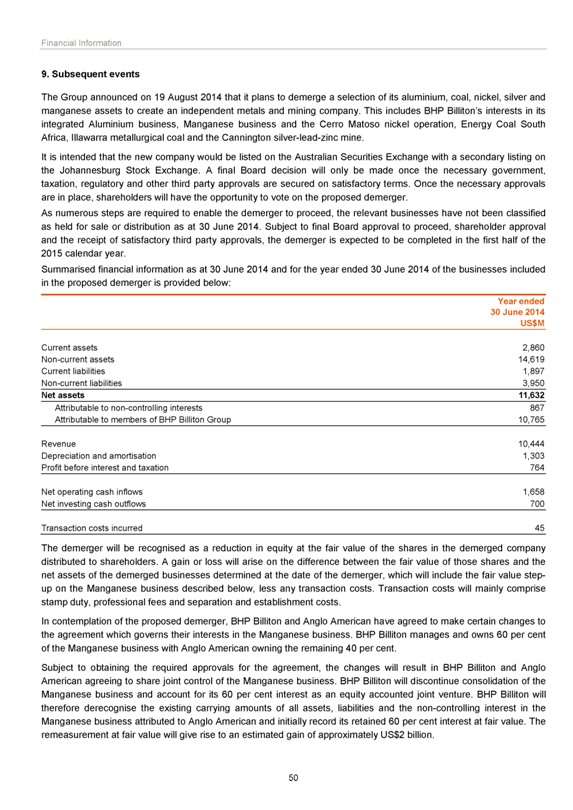

Projects

BHP Billiton’s development capability was

illustrated by the early completion of the WAIO Jimblebar Mine Expansion and Queensland Coal Caval Ridge projects in the 2014 financial year. A further four projects were successfully completed, namely: Macedon; North West Shelf North Rankin B Gas

Compression; Samarco Fourth Pellet Plant; and WAIO Port Blending and Rail Yard Facilities. The Newcastle Third Port Stage 3 project achieved mechanical completion while the Cerrejón P40 project delivered first coal. The port expansion

associated with the Cerrejón P40 project is currently being commissioned, although operational issues are expected to constrain capacity at approximately 35 Mtpa (100 per cent basis) in the medium term.

At the end of the 2014 financial year, BHP Billiton had eight major projects under development with a combined budget of US$14.1 billion. During the period the Group approved: an

investment of US$3.4 billion for the construction of a desalination facility designed to deliver sustainable water supply to Escondida over the long term; a US$2.6 billion investment to finish the excavation and lining of the Jansen Potash project

production and service shafts, and to continue the installation of essential surface infrastructure and utilities; and a US$212 million increase to the budget of the Escondida Oxide Leach Area project (OLAP) to US$933 million. While OLAP is now

scheduled for completion in the second half of the 2014 calendar year we expect no impact to production.

6

BHP Billiton Results for the year ended 30 June 2014

BHP Billiton’s share of capital and exploration expenditure(4) declined by 32 per cent during the 2014 financial year to US$15.2 billion. Our rate of investment is

expected to decline below our investment ceiling in the 2015 financial year with planned capital and exploration expenditure(4) of approximately US$14.8 billion.

Year ended Year ended

30 June 30 June

2014 2013

US$M US$M

Purchases of property, plant and equipment 15,993 22,243

Exploration expenditure 1,010 1,351

Capital and exploration expenditure (cash basis) 17,003 23,594

Add: equity

accounted investments 871 1,493

Less: capitalised deferred stripping(i) (1,421) (1,650)

Less: non-controlling interests (1,272) (1,146)

Capital and exploration expenditure (BHP

Billiton share)(ii) 15,181 22,291

(i) Includes US$243 million of capitalised deferred stripping attributable to non-controlling interests (June 2013 financial

year: US$292 million).

(ii) Represents the share of capital and exploration expenditure attributable to BHP Billiton shareholders on a cash basis. Includes BHP

Billiton proportionate share of equity accounted investments; excludes capitalised deferred stripping and non-controlling interests.

Projects completed or

delivered first production during the 2014 financial year

Business Project Capacity(i) Capital Date of initial

expenditure(i) production

US$M

Actual(ii) Budget Actual Target

Petroleum Macedon (Australia) 200 MMcf/d of gas. 1,200 1,050

Q3 CY13 CY13

71.43% (operator)

North West Shelf 2,500 MMcf/d of gas. 721 850

Q4 CY13 CY13

North Rankin B Gas

Compression

(Australia)

16.67% (non-operator)

Iron Ore Samarco Fourth Pellet Increases Samarco iron ore pellet 1,576 1,750 Q1 CY14 H1 CY14

Plant (Brazil) production capacity by 8.3 Mtpa to

50% 30.5 Mtpa.

WAIO Jimblebar Mine Increases mining and processing capacity 3,380 3,640(iii) Q3 CY13 Q4 CY13(iv)

Expansion (Australia) to 35 Mtpa with incremental (iv)

85% debottlenecking opportunities to 55

Mtpa.

WAIO Port Blending Optimises resource and enhances 916 1,000(iii) Q4 CY13 H2 CY14

and Rail Yard Facilities efficiency across the WAIO supply chain. (iv)

(Australia)

85%

Coal Caval Ridge Greenfield mine development to produce 1,706 1,870(iii) Q2 CY14 CY14

(Australia) an initial 5.5 Mtpa of export metallurgical

50% coal.

Newcastle Third Port Increases total coal terminal capacity from 367 367 Q3 CY13 CY14

Project

Stage 3 53 Mtpa to 66 Mtpa.

(Australia)

35.5%

Cerrejón P40 Project Increases saleable thermal coal production 437 437 Q4 CY13 CY13

(Colombia) by 8 Mtpa to approximately 40 Mtpa.

33.3%

10,303 10,964

7

News Release

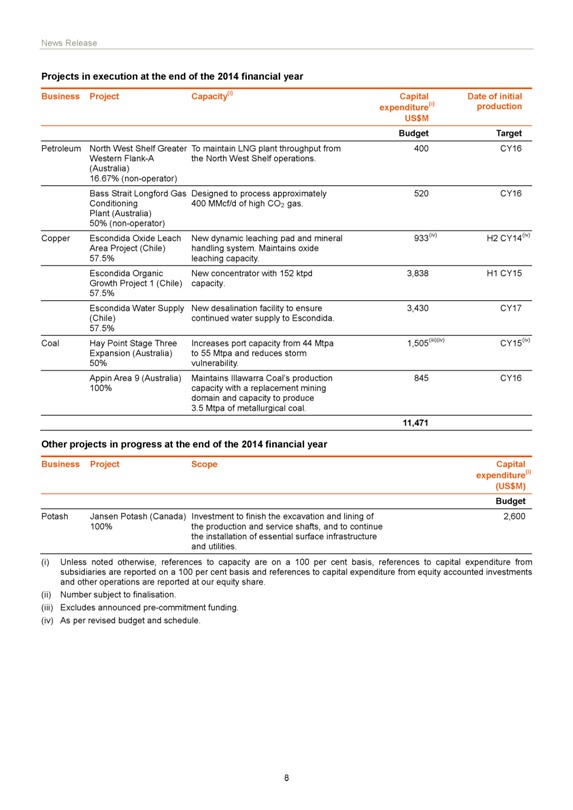

Projects in execution at the end of

the 2014 financial year

Business Project Capacity(i) Capital Date of initial

expenditure(i) production

US$M

Budget Target

Petroleum North West Shelf Greater To maintain LNG plant throughput from 400

CY16

Western Flank-A the North West Shelf operations.

(Australia)

16.67% (non-operator)

Bass Strait Longford Gas Designed to process approximately 520 CY16

Conditioning 400 MMcf/d of high CO2 gas.

Plant (Australia)

50% (non-operator)

Copper Escondida Oxide Leach New dynamic leaching pad and mineral 933(iv)

H2 CY14(iv)

Area Project (Chile) handling system. Maintains oxide

57.5%

leaching capacity.

Escondida Organic New concentrator with 152 ktpd 3,838 H1 CY15

Growth Project 1 (Chile) capacity.

57.5%

Escondida Water Supply New desalination facility to ensure 3,430 CY17

(Chile) continued water

supply to Escondida.

57.5%

Coal Hay Point Stage Three Increases port capacity

from 44 Mtpa 1,505(iii)(iv) CY15(iv)

Expansion (Australia) to 55 Mtpa and reduces storm

50% vulnerability.

Appin Area 9 (Australia) Maintains Illawarra Coal’s production 845

CY16

100% capacity with a replacement mining

domain and capacity to produce

3.5 Mtpa of metallurgical coal.

11,471

Other projects in progress at the end of the 2014 financial year

Business Project Scope

Capital

expenditure(i) (US$M)

Budget

Potash Jansen Potash (Canada) Investment to finish the excavation and lining of 2,600

100% the

production and service shafts, and to continue

the installation of essential surface infrastructure

and utilities.

(i) Unless noted otherwise, references to capacity are on a 100 per cent

basis, references to capital expenditure from subsidiaries are reported on a 100 per cent basis and references to capital expenditure from equity accounted investments and other operations are reported at our equity share.

(ii) Number subject to finalisation.

(iii) Excludes announced pre-commitment funding.

(iv) As per revised budget and schedule.

8

BHP Billiton Results for the year ended 30 June 2014

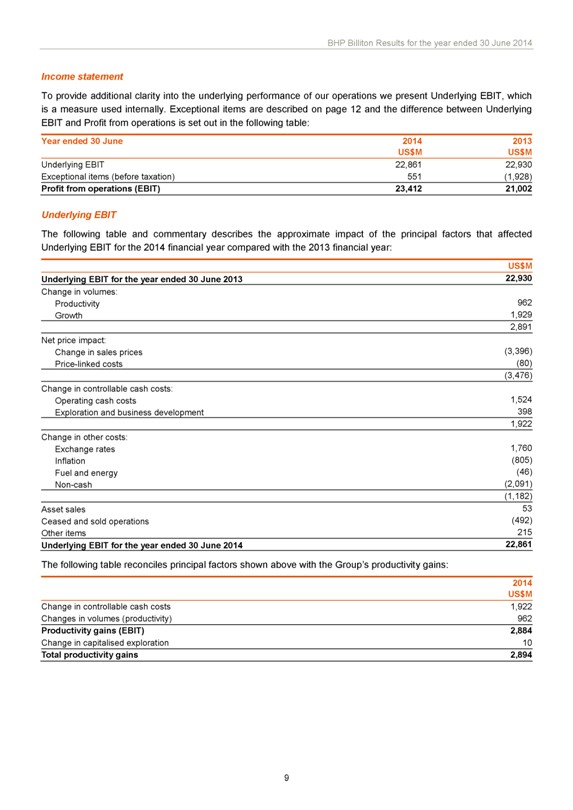

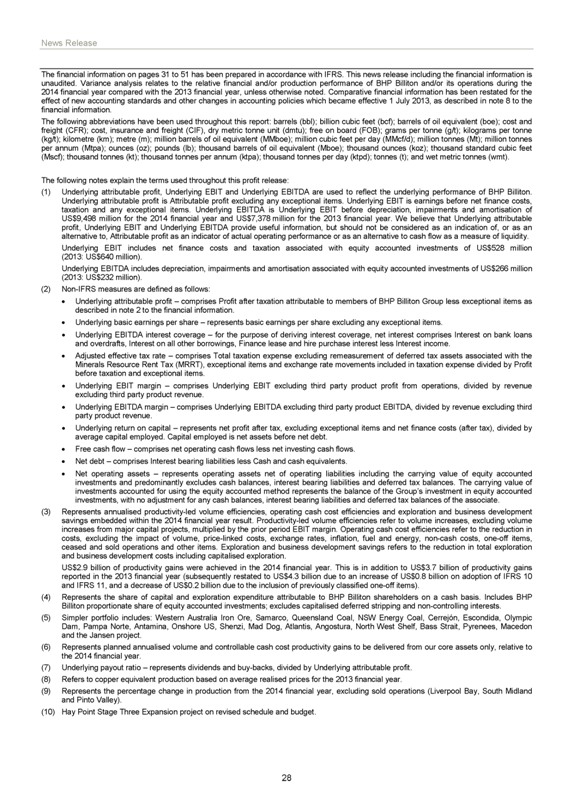

Income statement

To provide additional clarity into the underlying

performance of our operations we present Underlying EBIT, which is a measure used internally. Exceptional items are described on page 12 and the difference between Underlying EBIT and Profit from operations is set out in the following table:

Year ended 30 June 2014 US$M 2013 US$M

Underlying EBIT 22,861 22,930

Exceptional items (before taxation) 551 (1,928)

Profit from operations (EBIT)

23,412 21,002

Underlying EBIT

The following table and commentary describes

the approximate impact of the principal factors that affected Underlying EBIT for the 2014 financial year compared with the 2013 financial year:

Underlying EBIT

for the year ended 30 June 2013 US$M 22,930

Change in volumes:

Productivity

962

Growth 1,929

2,891

Net price impact:

Change in sales prices (3,396)

Price-linked costs (80)

(3,476)

Change in controllable cash costs:

Operating cash costs 1,524

Exploration and business development 398

1,922

Change in other costs:

Exchange rates 1,760

Inflation (805)

Fuel and energy (46)

Non-cash (2,091)

(1,182)

Asset sales 53

Ceased and sold operations (492)

Other items 215

Underlying EBIT for the year ended 30 June 2014 22,861

The following table reconciles principal factors shown above with the Group’s productivity gains:

2014 US$M

Change in controllable cash costs 1,922

Changes in volumes (productivity) 962

Productivity gains (EBIT) 2,884

Change in capitalised exploration 10

Total productivity gains 2,894

9

News Release

Volumes

Productivity-led volume efficiencies and the ramp-up of major projects underpinned a nine per cent increase in Group production(8) in the 2014 financial year and an additional

US$2.9 billion in Underlying EBIT. WAIO was the major contributor as the ramp-up of the Jimblebar mining hub and a series of productivity initiatives raised the capacity of our integrated supply chain and supported a US$1.8 billion increase in

Underlying EBIT. Despite the impact of natural field decline, stronger volumes in our Petroleum business generated an additional US$994 million of Underlying EBIT, reflecting 73 per cent growth in Onshore US liquids volumes and a near doubling of

production at Atlantis.

We expect to maintain strong momentum and remain on track to generate Group production(8) growth of 16 per cent over the two years to the

end of the 2015 financial year.

Prices

Lower average prices reduced

Underlying EBIT by US$3.4 billion in the 2014 financial year.

In metallurgical coal, an increase in seaborne supply and the resilience of higher cost, uneconomic

capacity led to a 20 per cent and 14 per cent decline in the average realised price of hard coking coal and weak coking coal, respectively. The average price received for thermal coal also declined by 14 per cent during the period. In total, lower

average realised prices in our Coal business reduced Underlying EBIT by US$1.5 billion.

A five per cent decline in the average realised price of copper reflected

the near-term rebalancing of the market while the acceleration of low-cost, seaborne iron ore supply growth, predominantly from Australia’s Pilbara region, weighed on prices in the June 2014 half year. In total, lower average realised prices

for copper and iron ore reduced Underlying EBIT by US$1.4 billion.

Nickel and aluminium prices rallied towards the end of the 2014 financial year but remained

lower on average for the period, reducing Underlying EBIT by a further US$258 million.

The value of diversification was again evident as higher average realised

prices for our petroleum products increased Underlying EBIT by US$219 million. In this context, the average price achieved for our natural gas sales book, covering domestic and international markets, increased by 16 per cent.

Price-linked costs decreased Underlying EBIT by US$80 million during the period, primarily reflecting higher royalty charges in our Petroleum and Iron Ore businesses.

Controllable cash costs

A broad-based improvement in productivity underpinned a significant

US$1.9 billion reduction in controllable cash costs(3) during the period.

Operating cash costs

The Group’s commitment to further improve the competitive position of its assets delivered tangible results in the 2014 financial year as operating cash costs declined by

US$1.5 billion. A general increase in labour and contractor productivity had the greatest impact, increasing Underlying EBIT by US$1.3 billion.

An improvement in

equipment productivity increased Underlying EBIT by a further US$268 million as contract stripping activities were further optimised at Queensland Coal. A reduction in consumable costs in our Aluminium, Manganese and Nickel business more than

accounted for a US$33 million decrease in Group supply costs.

Exploration and business development

The Group’s exploration expenditure declined by 25 per cent in the 2014 financial year to US$1.0 billion as we sharpened our focus on greenfield copper porphyry targets in

Chile and Peru, and high-impact liquids opportunities in the Gulf of Mexico, Western Australia and Trinidad and Tobago. The associated reduction in the Group’s exploration expense increased Underlying EBIT by US$331 million while a further

decline in business development expenditure increased Underlying EBIT by US$67 million.

10

BHP Billiton Results for the year ended 30 June 2014

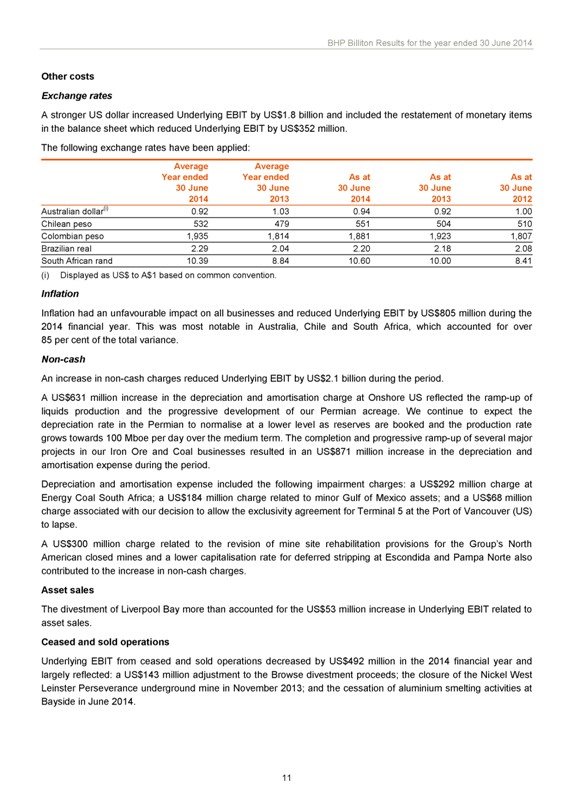

Other costs

Exchange rates

A stronger US dollar increased Underlying EBIT by US$1.8 billion and included the restatement of monetary items in the balance sheet which reduced Underlying EBIT by US$352

million.

The following exchange rates have been applied:

Average Year ended

30 June 2014

Average Year ended 30 June 2013

As at 30 June 2014

As at 30 June 2013

As at 30 June 2012

Australian dollar(i) 0.92 1.03 0.94 0.92 1.00

Chilean peso 532 479 551 504 510

Colombian peso 1,935 1,814 1,881 1,923 1,807

Brazilian real 2.29 2.04 2.20 2.18 2.08

South African rand 10.39 8.84 10.60 10.00 8.41

(i) Displayed as US$ to A$1

based on common convention.

Inflation

Inflation had an unfavourable impact on

all businesses and reduced Underlying EBIT by US$805 million during the 2014 financial year. This was most notable in Australia, Chile and South Africa, which accounted for over 85 per cent of the total variance.

Non-cash

An increase in non-cash charges reduced Underlying EBIT by US$2.1 billion during the

period.

A US$631 million increase in the depreciation and amortisation charge at Onshore US reflected the ramp-up of liquids production and the progressive

development of our Permian acreage. We continue to expect the depreciation rate in the Permian to normalise at a lower level as reserves are booked and the production rate grows towards 100 Mboe per day over the medium term. The completion and

progressive ramp-up of several major projects in our Iron Ore and Coal businesses resulted in an US$871 million increase in the depreciation and amortisation expense during the period.

Depreciation and amortisation expense included the following impairment charges: a US$292 million charge at Energy Coal South Africa; a US$184 million charge related to minor Gulf

of Mexico assets; and a US$68 million charge associated with our decision to allow the exclusivity agreement for Terminal 5 at the Port of Vancouver (US) to lapse.

A US$300 million charge related to the revision of mine site rehabilitation provisions for the Group’s North American closed mines and a lower capitalisation

rate for deferred stripping at Escondida and Pampa Norte also contributed to the increase in non-cash charges.

Asset sales

The divestment of Liverpool Bay more than accounted for the US$53 million increase in Underlying EBIT related to asset sales.

Ceased and sold operations

Underlying EBIT from ceased and sold operations decreased by US$492

million in the 2014 financial year and largely reflected: a US$143 million adjustment to the Browse divestment proceeds; the closure of the Nickel West Leinster Perseverance underground mine in November 2013; and the cessation of aluminium smelting

activities at Bayside in June 2014.

11

News Release

Other items

Other items increased Underlying EBIT by US$215 million and largely reflected an increase in margins at our equity accounted investments and an US$84 million profit related to the

sale of the Energy Coal South Africa Optimum Coal Purchase agreement. A US$112 million UK pension plan expense in our Petroleum business is also reported in this category.

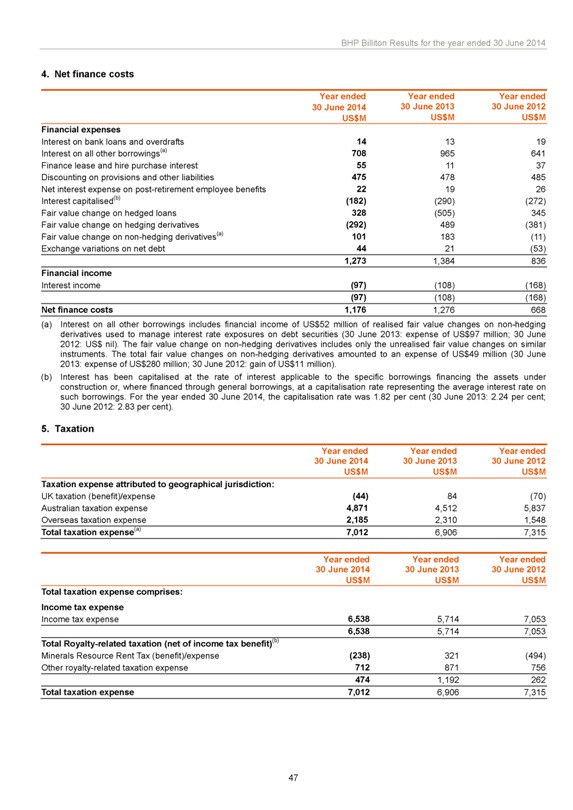

Net finance costs

Net finance costs of US$1.2 billion were largely unchanged from the prior

period.

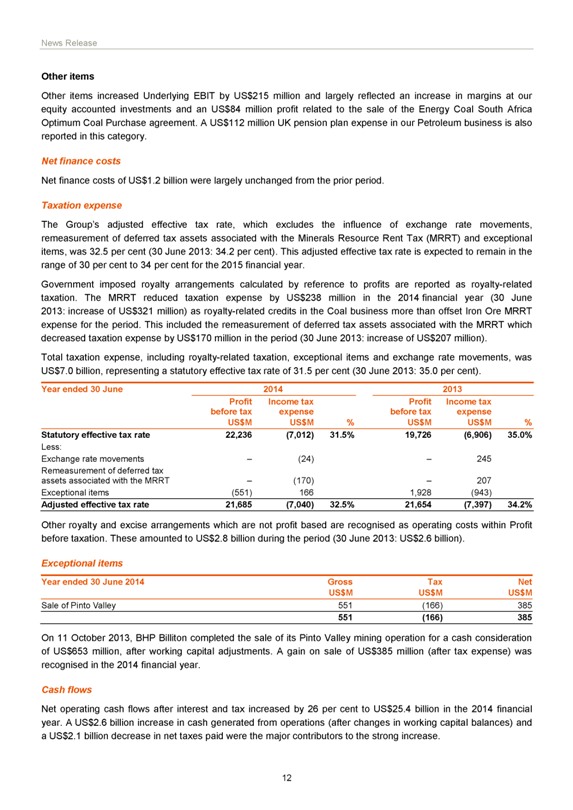

Taxation expense

The Group’s adjusted effective tax rate, which

excludes the influence of exchange rate movements, remeasurement of deferred tax assets associated with the Minerals Resource Rent Tax (MRRT) and exceptional items, was 32.5 per cent (30 June 2013: 34.2 per cent). This adjusted effective tax rate is

expected to remain in the range of 30 per cent to 34 per cent for the 2015 financial year.

Government imposed royalty arrangements calculated by reference to

profits are reported as royalty-related taxation. The MRRT reduced taxation expense by US$238 million in the 2014 financial year (30 June 2013: increase of US$321 million) as royalty-related credits in the Coal business more than offset Iron Ore

MRRT expense for the period. This included the remeasurement of deferred tax assets associated with the MRRT which decreased taxation expense by US$170 million in the period (30 June 2013: increase of US$207 million).

Total taxation expense, including royalty-related taxation, exceptional items and exchange rate movements, was US$7.0 billion, representing a statutory effective tax rate of 31.5

per cent (30 June 2013: 35.0 per cent).

Year ended 30 June

2014 2013

Profit before tax US$M

Income tax expense US$M

%

Profit before tax US$M

Income tax expense US$M

%

Statutory effective tax rate 22,236 (7,012) 31.5% 19,726 (6,906) 35.0%

Less:

Exchange rate movements - (24) - 245

Remeasurement of deferred tax assets associated with the

MRRT - (170) - 207

Exceptional items (551) 166 1,928 (943)

Adjusted effective

tax rate 21,685 (7,040) 32.5% 21,654 (7,397) 34.2%

Other royalty and excise arrangements which are not profit based are recognised as operating costs within Profit

before taxation. These amounted to US$2.8 billion during the period (30 June 2013: US$2.6 billion).

Exceptional items

Year ended 30 June 2014

Gross US$M

Tax US$M

Net US$M

Sale of Pinto Valley 551 (166) 385

551 (166) 385

On 11 October 2013, BHP Billiton completed the sale of its Pinto Valley mining operation for a cash consideration of US$653 million, after working capital adjustments. A gain on

sale of US$385 million (after tax expense) was recognised in the 2014 financial year.

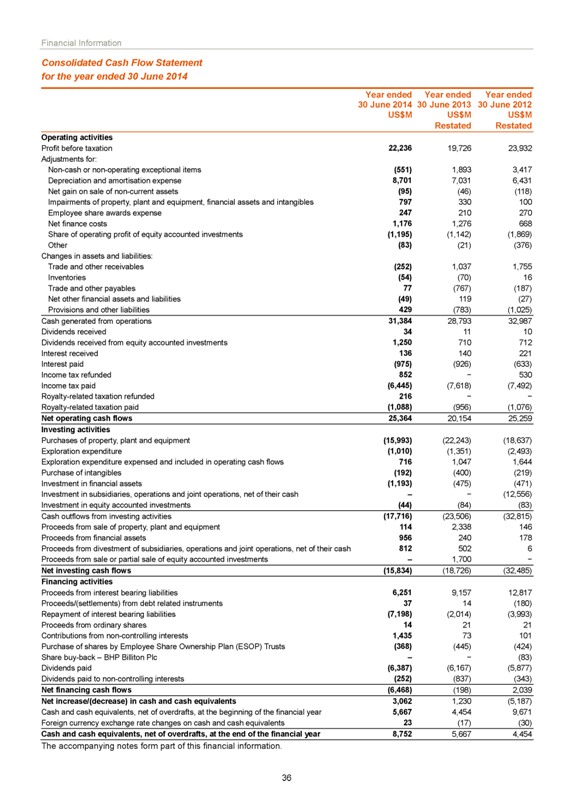

Cash flows

Net operating cash flows after interest and tax increased by 26 per cent to US$25.4 billion in the 2014 financial year. A US$2.6 billion increase in cash generated from operations

(after changes in working capital balances) and a US$2.1 billion decrease in net taxes paid were the major contributors to the strong increase.

12

BHP Billiton Results for the year ended 30 June 2014

Net investing cash outflows decreased by US$2.9 billion to US$15.8 billion during the period. This reflected a US$6.6 billion reduction in capital and exploration

expenditure partially offset by a decline in proceeds from asset sales of US$2.9 billion. Expenditure on major growth projects totalled US$13.1 billion, including US$5.6 billion on petroleum projects and US$7.5 billion on minerals projects.

Sustaining capital expenditure and other items totalled US$2.9 billion. Exploration expenditure was US$1.0 billion, including US$716 million classified within net operating cash flows.

Net financing cash flows included the proceeds from interest bearing liabilities of US$6.3 billion and contributions from non-controlling interests of US$1.4 billion. Proceeds from

interest bearing liabilities included the issuance of a four tranche Global Bond of US$5.0 billion. These inflows were more than offset by debt repayments of US$7.2 billion and dividend payments of US$6.4 billion.

Net debt finished the period at US$25.8 billion, a decrease of US$1.7 billion compared to the net debt position at 30 June 2013.

Dividend

BHP Billiton has a progressive dividend policy. The aim of this policy is to steadily

increase or at least maintain our base dividend in US dollars terms at each half-yearly payment. Our Board today determined to pay a final dividend of 62 US cents per share. As a result, our total dividend for the 2014 financial year increases by

four per cent to 121 US cents per share. We will seek to steadily increase or at least maintain the dividend per share in US dollar terms at each half-yearly payment following the demerger, implying a higher payout ratio.

The dividend to be paid by BHP Billiton Limited will be fully franked for Australian taxation purposes. Dividends for the BHP Billiton Group are determined in US dollars. However,

BHP Billiton Limited dividends are mainly paid in Australian dollars, and BHP Billiton Plc dividends are mainly paid in pounds sterling and South African rand to shareholders on the UK section and the South African section of the register,

respectively. Currency conversions will be based on the foreign currency exchange rates on the Record Date, except for the conversion into South African rand, which will take place on the last day to trade (cum dividend) on JSE Limited, being 29

August 2014. Please note that all currency conversion elections must be registered by the Record Date, being 5 September 2014. Any currency conversion elections made after this date will not apply to this dividend.

The timetable in respect of this dividend will be:

Last day to trade cum dividend on JSE

Limited (JSE) and currency conversion into rand 29 August 2014

Ex-dividend Date JSE 1 September 2014

Ex-dividend Date Australian Securities Exchange (ASX), London Stock Exchange (LSE) and New York Stock Exchange (NYSE) 3 September 2014

Record Date (including currency conversion and currency election dates, except for rand) 5 September 2014

Payment date 23 September 2014

American Depositary Shares (ADSs) each represent two fully paid

ordinary shares and receive dividends accordingly.

BHP Billiton Plc shareholders registered on the South African section of the register will not be able to

dematerialise or rematerialise their shareholdings between the dates of 1 September and 5 September 2014 (inclusive), nor will transfers between the UK register and the South African register be permitted between the dates of 29 August and 5

September 2014 (inclusive).

Details of the currency exchange rates applicable for the dividend will be announced to the relevant stock exchanges following

conversion and will appear on the Group’s website.

13

News Release

Debt management and liquidity

During the 2014 financial year, the Group issued a four tranche Global Bond comprising US$500 million Senior Floating Rate Notes due 2016 paying interest at 3

month US Dollar LIBOR plus 25 basis points, US$500 million 2.050 per cent Senior Notes due 2018, US$1.5 billion 3.850 per cent Senior Notes due 2023, and US$2.5 billion 5.000 per cent Senior Notes due 2043.

In February 2014, the Group redeemed all outstanding Petrohawk Energy Corporation 10.5 per cent Senior Notes due August 2014 and 7.875 per cent Senior Notes due June 2015 at the

applicable call prices. The aggregate principal value of the notes redeemed was approximately US$1.4 billion.

The Group has a US$6.0 billion commercial paper

program backed by a US$6.0 billion revolving credit facility. During the period, the Group’s revolving credit facilities, which consisted of US$1.0 billion expiring in December 2014 and US$5.0 billion expiring in December 2015, were replaced by

a US$6.0 billion revolving credit facility. The new facility has a five year maturity with two one-year extension options.

The Group’s balance sheet continued

to strengthen during the 2014 financial year, consistent with our commitment to maintain a solid A credit rating. At the end of the period, the Group’s cash and cash equivalents on hand were US$8.8 billion.

Subsequent to the period end, the Group redeemed all outstanding Petrohawk Energy Corporation 7.25 per cent Senior Notes due August 2018 and 6.25 per cent Senior Notes due June

2019 at the applicable call prices. The aggregate principal value of the notes redeemed was approximately US$1.8 billion.

Corporate governance

On 15 April 2014, we announced the appointment of Mr Malcolm Brinded as a Non-executive Director, and a member of the Sustainability Committee, effective from that date. During the

year, Carolyn Hewson was appointed to the Remuneration Committee and remains a member of the Risk and Audit Committee. The Remuneration Committee is comprised of Sir John Buchanan, Carlos Cordeiro, Pat Davies, Carolyn Hewson and John Schubert.

14

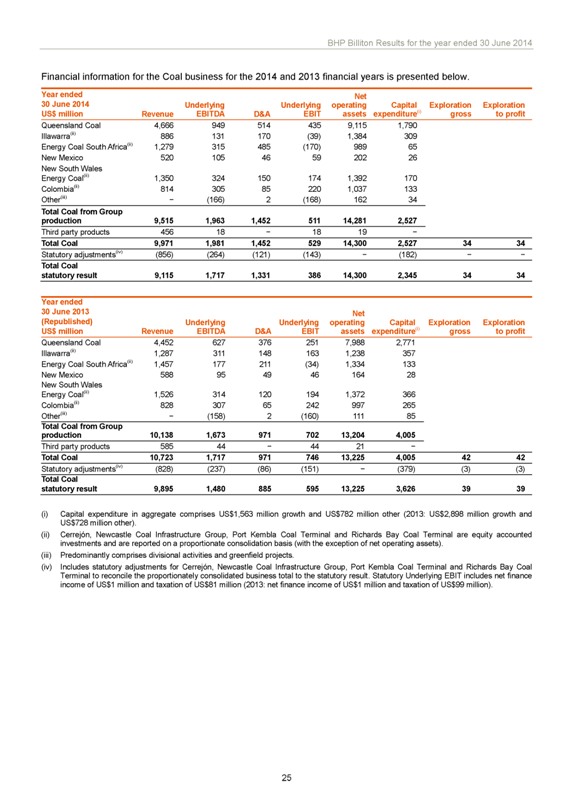

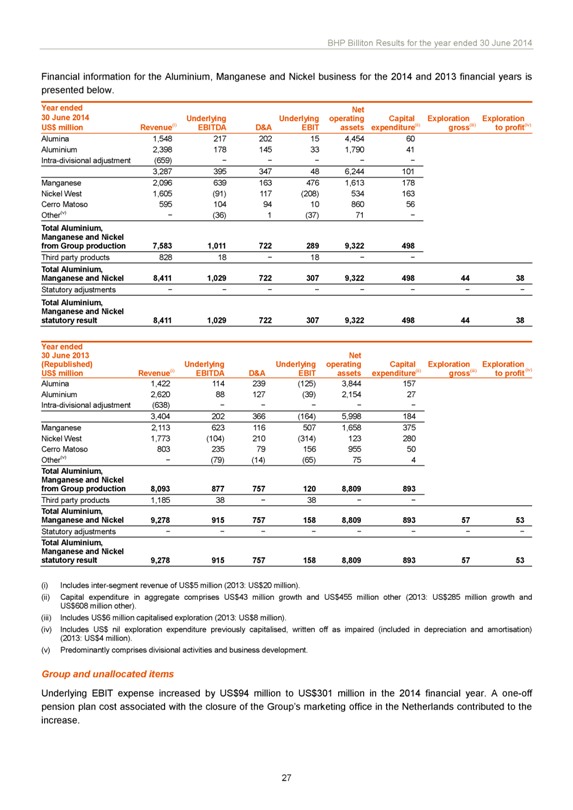

BHP Billiton Results for the year ended 30 June 2014

Business summary(i)

The following table provides a summary of the performance

of the Businesses for the 2014 financial year and the corresponding period.

Year ended 30 June 2014 US$ million Revenue(ii) Underlying EBIT(iii) Exceptional items

Profit from operations (EBIT) Net operating assets(iv) Capital expenditure(v) Exploration gross(vi) Exploration to profit(vii)

Petroleum and Potash 14,833 5,287 -

5,287 39,514 6,423 647 544

Copper 13,868 5,080 551 5,631 22,231 3,757 116 116

Iron Ore 21,356 12,102 - 12,102 23,390 2,949 169 56

Coal 9,115 386 - 386

14,300 2,345 34 34

Aluminium, Manganese and Nickel 8,411 307 - 307 9,322 498 44 38

Group and unallocated items(viii) 103 (301) - (301) 640 21 - -

Inter-segment adjustment (480)

- - - - - - -

BHP Billiton Group 67,206 22,861 551 23,412 109,397 15,993 1,010 788

Year ended 30 June 2013 (Republished) US$ million Revenue(ii) Underlying EBIT(iii) Exceptional items Profit from operations (EBIT) Net operating assets(iv) Capital expenditure(v)

Exploration gross(vi) Exploration to profit(vii)

Petroleum and Potash 13,224 5,636 1,273 6,909 37,525 7,675 764 709

Copper 14,537 5,639 355 5,994 20,074 3,930 274 274

Iron Ore 18,593 11,109 (827) 10,282 22,126

5,979 217 74

Coal 9,895 595 (79) 516 13,225 3,626 39 39

Aluminium, Manganese

and Nickel 9,278 158 (3,923) (3,765) 8,809 893 57 53

Group and unallocated items(viii) 501 (207) 1,273 1,066 328 140 - -

Inter-segment adjustment (75) - - - - - - -

BHP Billiton Group 65,953 22,930 (1,928) 21,002

102,087 22,243 1,351 1,149

(i) Group and business level information is reported on a statutory basis which, in relation to Underlying EBIT, includes net finance

costs and taxation associated with equity accounted investments.

(ii) Revenue is based on Group realised prices and includes third party products. Sale of third

party products by the Group contributed revenue of US$2,979 million and Underlying EBIT of US$44 million (2013: US$2,886 million and US$127 million).

(iii)

Underlying EBIT is defined as earnings before net finance costs, taxation and any exceptional items. Underlying EBIT is reported net of net finance costs of US$90 million and taxation of US$438 million associated with equity accounted investments

(2013: net finance costs of US$24 million and taxation of US$616 million). Underlying EBITDA, as reported within each business, is Underlying EBIT before depreciation, impairments and amortisation (D&A).

(iv) Net operating assets represents operating assets net of operating liabilities including the carrying value of equity accounted investments and predominantly excludes cash

balances, interest bearing liabilities and deferred tax balances. The carrying value of investments accounted for using the equity accounted method represents the balance of the Group’s investment in equity accounted investments, with no

adjustment for any cash balances, interest bearing liabilities and deferred tax balances of the associate.

(v) Capital expenditure is presented on a cash basis and

excludes capitalised interest and capitalised exploration. Capital expenditure in aggregate comprises US$13,130 million growth and US$2,863 million other (2013: US$18,678 million growth and US$3,565 million other). Comparative period capital

expenditure was previously reported on an accruals basis and has been restated on a cash basis.

(vi) Includes US$294 million capitalised exploration (2013: US$304

million).

(vii) Includes US$72 million exploration expenditure previously capitalised, written off as impaired (included in depreciation and amortisation) (2013:

US$102 million).

(viii) Includes the Group’s diamonds business (divested effective 10 April 2013), interest in titanium minerals (divested effective 3

September 2012), non-Potash corporate costs incurred by the former Diamonds and Specialty Products business, consolidation adjustments, unallocated items and external sales of freight and fuel via the Group’s transport and logistics operations.

15

News Release

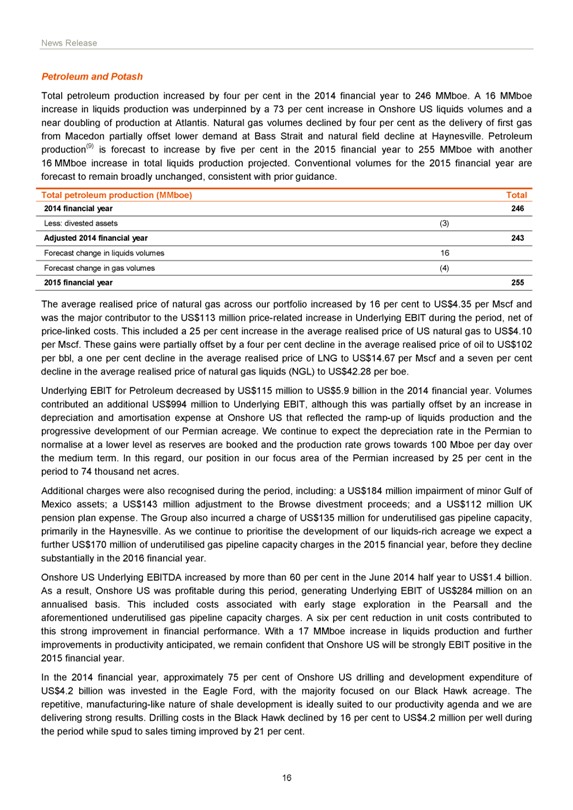

Petroleum and Potash

Total petroleum production increased by four per cent in the 2014 financial year to 246 MMboe. A 16 MMboe increase in liquids production was underpinned by a 73 per cent increase

in Onshore US liquids volumes and a near doubling of production at Atlantis. Natural gas volumes declined by four per cent as the delivery of first gas from Macedon partially offset lower demand at Bass Strait and natural field decline at

Haynesville. Petroleum production(9) is forecast to increase by five per cent in the 2015 financial year to 255 MMboe with another

16 MMboe increase in total

liquids production projected. Conventional volumes for the 2015 financial year are forecast to remain broadly unchanged, consistent with prior guidance.

Total

petroleum production (MMboe) Total

2014 financial year 246

Less: divested

assets (3)

Adjusted 2014 financial year 243

Forecast change in liquids

volumes 16

Forecast change in gas volumes (4)

2015 financial year 255

The average realised price of natural gas across our portfolio increased by 16 per cent to US$4.35 per Mscf and was the major contributor to the US$113 million

price-related increase in Underlying EBIT during the period, net of price-linked costs. This included a 25 per cent increase in the average realised price of US natural gas to US$4.10 per Mscf. These gains were partially offset by a four per cent

decline in the average realised price of oil to US$102 per bbl, a one per cent decline in the average realised price of LNG to US$14.67 per Mscf and a seven per cent decline in the average realised price of natural gas liquids (NGL) to US$42.28 per

boe.

Underlying EBIT for Petroleum decreased by US$115 million to US$5.9 billion in the 2014 financial year. Volumes contributed an additional US$994 million to

Underlying EBIT, although this was partially offset by an increase in depreciation and amortisation expense at Onshore US that reflected the ramp-up of liquids production and the progressive development of our Permian acreage. We continue to expect

the depreciation rate in the Permian to normalise at a lower level as reserves are booked and the production rate grows towards 100 Mboe per day over the medium term. In this regard, our position in our focus area of the Permian increased by 25 per

cent in the period to 74 thousand net acres.

Additional charges were also recognised during the period, including: a US$184 million impairment of minor Gulf of

Mexico assets; a US$143 million adjustment to the Browse divestment proceeds; and a US$112 million UK pension plan expense. The Group also incurred a charge of US$135 million for underutilised gas pipeline capacity, primarily in the Haynesville. As

we continue to prioritise the development of our liquids-rich acreage we expect a further US$170 million of underutilised gas pipeline capacity charges in the 2015 financial year, before they decline substantially in the 2016 financial year.

Onshore US Underlying EBITDA increased by more than 60 per cent in the June 2014 half year to US$1.4 billion. As a result, Onshore US was profitable during this

period, generating Underlying EBIT of US$284 million on an annualised basis. This included costs associated with early stage exploration in the Pearsall and the aforementioned underutilised gas pipeline capacity charges. A six per cent reduction in

unit costs contributed to this strong improvement in financial performance. With a 17 MMboe increase in liquids production and further improvements in productivity anticipated, we remain confident that Onshore US will be strongly EBIT positive in

the 2015 financial year.

In the 2014 financial year, approximately 75 per cent of Onshore US drilling and development expenditure of US$4.2 billion was invested in

the Eagle Ford, with the majority focused on our Black Hawk acreage. The repetitive, manufacturing-like nature of shale development is ideally suited to our productivity agenda and we are delivering strong results. Drilling costs in the Black Hawk

declined by 16 per cent to US$4.2 million per well during the period while spud to sales timing improved by 21 per cent.

16

BHP Billiton Results for the year ended 30 June 2014

Of the 24 operated drilling rigs in action at the end of the period (30 June 2013: 40), 17 were in the Eagle Ford (30 June 2013: 31), four were in the Permian (30

June 2013: four), three were in the Haynesville (30 June 2013: four), while no rigs were in the Fayetteville (30 June 2013: one).

A total of 138 net wells were put

online in our prolific Black Hawk acreage during the period (2013 financial year: 66 net wells) with an average 30-day initial production rate of 1,140 boe per day. An average one-year cumulative production rate per well of 208 Mboe for the wells

put online in the 2013 financial year reflected advances in completions optimisation and the benefit of restricting initial flow rates. At the end of the period we had 284 net producing wells in the Black Hawk with an average rate of 82.4 Mboe per

day achieved in the June 2014 quarter (43.0 Mboe per day in the June 2013 quarter).

Onshore US 2014 financial year (2013 financial year) Liquids focused areas

(Eagle Ford and Permian) Gas focused areas (Haynesville and Fayetteville) Total

Capital expenditure US$ billion 3.6 (3.8) 0.6 (0.9) 4.2 (4.7)

Production MMboe 51.9 (33.4) 56.2 (65.8) 108.1 (99.2)

Production mix Natural gas 36% (42%)

100% (100%) 69% (80%)

Natural gas liquids 22% (23%) - (-) 11% (8%)

Crude and

condensate 42% (35%) - (-) 20% (12%)

Petroleum capital expenditure of approximately US$5.6 billion is planned in the 2015 financial year. In our Onshore US

business we will continue to prioritise investment in the liquids-rich Eagle Ford and Permian with up to 120 net wells expected to be put online in the Black Hawk. In our Conventional business, we will remain focused on high-return infill drilling

opportunities in the Gulf of Mexico and life extension projects at Bass Strait and North West Shelf.

Petroleum exploration expenditure for 2014 financial year was

US$600 million, of which US$369 million was expensed. During the period, BHP Billiton signed a production sharing contract for Block 23b (60 per cent interest and operator) and farmed into Blocks 23a and 14 (70 per cent interest and operator) in

Trinidad and Tobago. A US$750 million exploration program, largely focused on the Gulf of Mexico, Western Australia and the collection of seismic data in Trinidad and Tobago is planned for the 2015 financial year.

During the period, BHP Billiton completed the divestment of its 46.1 per cent interest in Liverpool Bay and its South Midland acreage in the Permian basin, Onshore US. Combined

proceeds of US$182 million were realised (before customary adjustments) and a gain on sale of US$116 million was recognised in Underlying EBIT.

Potash recorded an

Underlying EBIT loss of US$583 million. This included: a US$68 million impairment associated with our decision to allow the exclusivity agreement for Terminal 5 at the Port of Vancouver (US) to lapse; and a US$300 million charge related to the

revision of mine site rehabilitation provisions for the Group’s North American closed mines, which are managed by our Potash business. These charges were partially offset by a US$42 million reduction in exploration expense.

On 20 August 2013, BHP Billiton announced an additional investment of US$2.6 billion to finish the excavation and lining of the Jansen Potash project production and service shafts,

and to continue the installation of essential surface infrastructure and utilities. The overall project was 30 per cent complete at the end of the period with significant progress made on surface infrastructure and shaft excavation continuing.

17

News Release

Financial information for the

Petroleum and Potash business for the 2014 and 2013 financial years is presented below.

Year ended 30 June 2014 US$ million (i) Revenue(ii) Underlying EBITDA

D&A Underlying EBIT Net operating assets Capital expenditure(iii) Exploration gross(iv) Exploration to profit(v)

Bass Strait 1,885 1,555 132 1,423 2,864 259

North West Shelf(vi) 2,432 1,599 175 1,424 1,691 193

Atlantis 1,535 1,407 335

1,072 2,272 409

Shenzi 1,430 1,281 243 1,038 1,598 306

Mad Dog 217 171 16 155

461 83

Onshore US 4,264 2,270 2,426 (156) 26,945 4,226

Algeria 465 396 30 366

104 19

UK(vii) 155 70 52 18 (38) 15

Exploration - (369) 113 (482) 464 -

Other(viii) (ix) 2,027 1,744 735 1,009 1,907 369

Total Petroleum 14,410

10,124 4,257 5,867 38,268 5,879 600 497

Potash - (211) 74 (285) 2,255 544 47 47

Other(x) - (298) - (298) (1,009) - - -

Total Petroleum and Potash from Group

production 14,410 9,615 4,331 5,284 39,514 6,423 647 544

Third party products 437 3 - 3 - -

Total Petroleum and Potash 14,847 9,618 4,331 5,287 39,514 6,423 647 544

Statutory

adjustments(xi) (14) (3) (3) - - - - -

Total Petroleum and Potash statutory result 14,833 9,615 4,328 5,287 39,514 6,423 647 544

Year ended 30 June 2013 (Republished) US$ million (i) Revenue(ii) Underlying EBITDA D&A Underlying EBIT Net operating assets Capital expenditure(iii) Exploration gross(iv)

Exploration to profit(v)

Bass Strait 1,921 1,564 119 1,445 2,834 526

North

West Shelf 2,578 1,913 234 1,679 1,880 221

Atlantis 853 710 147 563 2,166 419

Shenzi 1,614 1,519 283 1,236 1,524 289

Mad Dog 276 233 98 135 420 89

Onshore US 2,987 1,508 1,795 (287) 25,019 4,699

Algeria 533 460 18 442 90 22

UK 244 95 46 49 45 8

Exploration - (522) 230 (752) 529 -

Other(viii) (ix) 2,032 1,746 282 1,464 1,973 794

Total Petroleum 13,038 9,226 3,252 5,974

36,480 7,067 675 620

Potash - (309) 25 (334) 1,758 608 89 89

Other(x) 18 (15)

- (15) (713) - - -

Total Petroleum and Potash from Group production 13,056 8,902 3,277 5,625 37,525 7,675 764 709

Third party products 175 11 - 11 - -

Total Petroleum and Potash 13,231 8,913 3,277 5,636

37,525 7,675 764 709

Statutory adjustments(xi) (7) (3) (3) - - - - -

Total

Petroleum and Potash statutory result 13,224 8,910 3,274 5,636 37,525 7,675 764 709

(i) Petroleum revenue from Group production includes: crude oil US$8,645

million (2013: US$7,604 million), natural gas US$3,119 million (2013: US$2,842 million), LNG US$1,614 million (2013: US$1,686 million), NGL US$916 million (2013: US$823 million) and other US$102 million (2013: US$76 million).

(ii) Includes inter-segment revenue of US$262 million (2013: US$ nil).

(iii) Capital

expenditure in aggregate comprises Petroleum US$5,600 million growth and US$279 million other (2013: US$6,883 million growth and US$184 million other) and Potash US$533 million growth and US$11 million other (2013: US$597 million growth and US$11

million other).

(iv) Includes US$231 million of Petroleum capitalised exploration (2013: US$153 million).

(v) Includes US$128 million of Petroleum exploration expenditure previously capitalised, written off as impaired (included in depreciation and amortisation) (2013: US$98 million).

18

BHP Billiton Results for the year ended 30 June 2014

(vi) Includes an expense of US$143 million incurred in May 2014 related to the purchase price adjustment for the Browse asset sale completed in the 2013 financial

year.

(vii) Includes an expense of US$112 million incurred in November 2013 related to the closure of the UK pension plan. Also includes a gain of US$120 million

related to the sale of the Liverpool Bay asset in March 2014.

(viii) Includes Macedon, Pyrenees, Stybarrow, Neptune, Minerva, Angostura, Genesis, Pakistan,

divisional activities, business development and ceased and sold operations. Also includes the Caesar oil pipeline and the Cleopatra gas pipeline which are equity accounted investments and are reported on a proportionate consolidation basis (with the

exception of net operating assets).

(ix) Includes an unrealised gain of US$74 million related to Angostura embedded derivative (2013: US$84 million unrealised

loss).

(x) Includes closed mining and smelting operations in Canada and the United States.

(xi) Includes statutory adjustments for the Caesar oil pipeline and the Cleopatra gas pipeline to reconcile the proportionately consolidated business total to the statutory result.

19

News Release

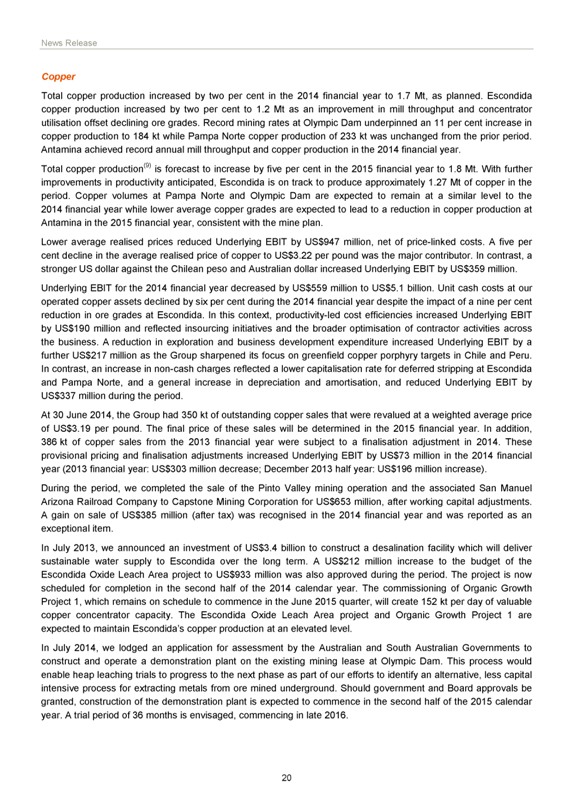

Copper

Total copper production increased by two per cent in the 2014 financial year to 1.7 Mt, as planned. Escondida copper production increased by two per cent to 1.2 Mt as an

improvement in mill throughput and concentrator utilisation offset declining ore grades. Record mining rates at Olympic Dam underpinned an 11 per cent increase in copper production to 184 kt while Pampa Norte copper production of 233 kt was

unchanged from the prior period. Antamina achieved record annual mill throughput and copper production in the 2014 financial year.

Total copper production(9) is

forecast to increase by five per cent in the 2015 financial year to 1.8 Mt. With further improvements in productivity anticipated, Escondida is on track to produce approximately 1.27 Mt of copper in the period. Copper volumes at Pampa Norte and

Olympic Dam are expected to remain at a similar level to the 2014 financial year while lower average copper grades are expected to lead to a reduction in copper production at Antamina in the 2015 financial year, consistent with the mine plan.

Lower average realised prices reduced Underlying EBIT by US$947 million, net of price-linked costs. A five per cent decline in the average realised price of copper

to US$3.22 per pound was the major contributor. In contrast, a stronger US dollar against the Chilean peso and Australian dollar increased Underlying EBIT by US$359 million. Underlying EBIT for the 2014 financial year decreased by US$559 million to

US$5.1 billion. Unit cash costs at our operated copper assets declined by six per cent during the 2014 financial year despite the impact of a nine per cent reduction in ore grades at Escondida. In this context, productivity-led cost efficiencies

increased Underlying EBIT by US$190 million and reflected insourcing initiatives and the broader optimisation of contractor activities across the business. A reduction in exploration and business development expenditure increased Underlying EBIT by

a further US$217 million as the Group sharpened its focus on greenfield copper porphyry targets in Chile and Peru. In contrast, an increase in non-cash charges reflected a lower capitalisation rate for deferred stripping at Escondida and Pampa

Norte, and a general increase in depreciation and amortisation, and reduced Underlying EBIT by US$337 million during the period.

At 30 June 2014, the Group had 350

kt of outstanding copper sales that were revalued at a weighted average price of US$3.19 per pound. The final price of these sales will be determined in the 2015 financial year. In addition, 386 kt of copper sales from the 2013 financial year were

subject to a finalisation adjustment in 2014. These provisional pricing and finalisation adjustments increased Underlying EBIT by US$73 million in the 2014 financial year (2013 financial year: US$303 million decrease; December 2013 half year: US$196

million increase).

During the period, we completed the sale of the Pinto Valley mining operation and the associated San Manuel Arizona Railroad Company to Capstone

Mining Corporation for US$653 million, after working capital adjustments. A gain on sale of US$385 million (after tax) was recognised in the 2014 financial year and was reported as an exceptional item.

In July 2013, we announced an investment of US$3.4 billion to construct a desalination facility which will deliver sustainable water supply to Escondida over the long term. A

US$212 million increase to the budget of the Escondida Oxide Leach Area project to US$933 million was also approved during the period. The project is now scheduled for completion in the second half of the 2014 calendar year. The commissioning of

Organic Growth Project 1, which remains on schedule to commence in the June 2015 quarter, will create 152 kt per day of valuable copper concentrator capacity. The Escondida Oxide Leach Area project and Organic Growth Project 1 are expected to

maintain Escondida’s copper production at an elevated level.

In July 2014, we lodged an application for assessment by the Australian and South Australian

Governments to construct and operate a demonstration plant on the existing mining lease at Olympic Dam. This process would enable heap leaching trials to progress to the next phase as part of our efforts to identify an alternative, less capital

intensive process for extracting metals from ore mined underground. Should government and Board approvals be granted, construction of the demonstration plant is expected to commence in the second half of the 2015 calendar year. A trial period of 36

months is envisaged, commencing in late 2016.

20

BHP Billiton Results for the year ended 30 June 2014

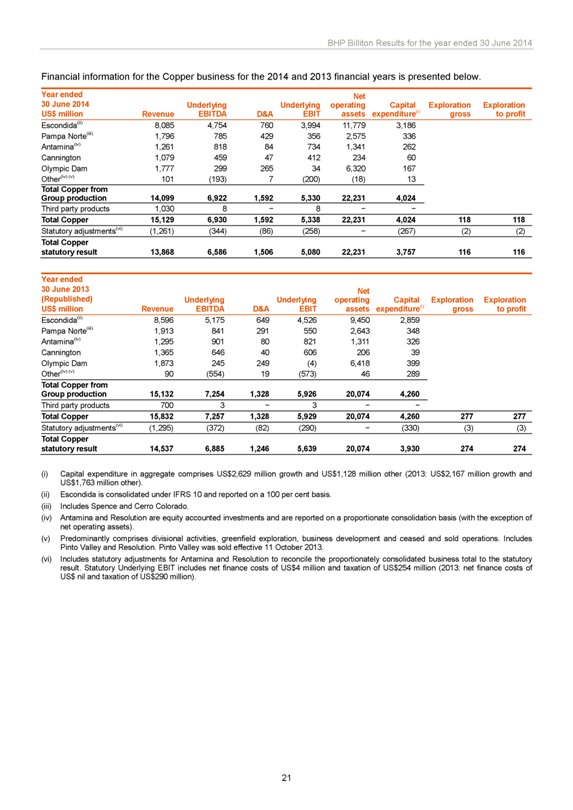

Financial information for the Copper business for the 2014 and 2013 financial years is presented below.

Year ended Net

30 June 2014 Underlying Underlying operating Capital Exploration Exploration

US$ million Revenue EBITDA D&A EBIT assets expenditure(i) gross to profit

Escondida(ii) 8,085 4,754 760 3,994 11,779 3,186

Pampa Norte(iii) 1,796 785

429 356 2,575 336

Antamina(iv) 1,261 818 84 734 1,341 262

Cannington 1,079

459 47 412 234 60

Olympic Dam 1,777 299 265 34 6,320 167

Other(iv) (v) 101

(193) 7 (200) (18) 13

Total Copper from

Group production 14,099 6,922 1,592

5,330 22,231 4,024

Third party products 1,030 8 - 8 - -

Total Copper 15,129

6,930 1,592 5,338 22,231 4,024 118 118

Statutory adjustments(vi) (1,261) (344) (86) (258) - (267) (2) (2)

Total Copper statutory result 13,868 6,586 1,506 5,080 22,231 3,757 116 116

Year ended

30 June 2013 Net

(Republished) Underlying Underlying operating Capital

Exploration Exploration

US$ million Revenue EBITDA D&A EBIT assets expenditure(i) gross to profit

Escondida(ii) 8,596 5,175 649 4,526 9,450 2,859

Pampa Norte(iii) 1,913 841 291 550 2,643 348

Antamina(iv) 1,295 901 80 821 1,311 326

Cannington 1,365 646 40 606 206 39

Olympic Dam 1,873 245 249 (4) 6,418 399

Other(iv) (v) 90 (554) 19 (573) 46

289

Total Copper from

Group production 15,132 7,254 1,328 5,926 20,074 4,260

Third party products 700 3 - 3 - -

Total Copper 15,832 7,257 1,328 5,929

20,074 4,260 277 277

Statutory adjustments(vi) (1,295) (372) (82) (290) - (330) (3) (3)

Total Copper statutory result 14,537 6,885 1,246 5,639 20,074 3,930 274 274

(i) Capital

expenditure in aggregate comprises US$2,629 million growth and US$1,128 million other (2013: US$2,167 million growth and US$1,763 million other).

(ii) Escondida is

consolidated under IFRS 10 and reported on a 100 per cent basis.

(iii) Includes Spence and Cerro Colorado.

(iv) Antamina and Resolution are equity accounted investments and are reported on a proportionate consolidation basis (with the exception of net operating assets).

(v) Predominantly comprises divisional activities, greenfield exploration, business development and ceased and sold operations. Includes Pinto Valley and Resolution. Pinto Valley

was sold effective 11 October 2013.

(v) Includes statutory adjustments for Antamina and Resolution to reconcile the proportionately consolidated business total to

the statutory result. Statutory Underlying EBIT includes net finance costs of US$4 million and taxation of US$254 million (2013: net finance costs of US$ nil and taxation of US$290 million).

21

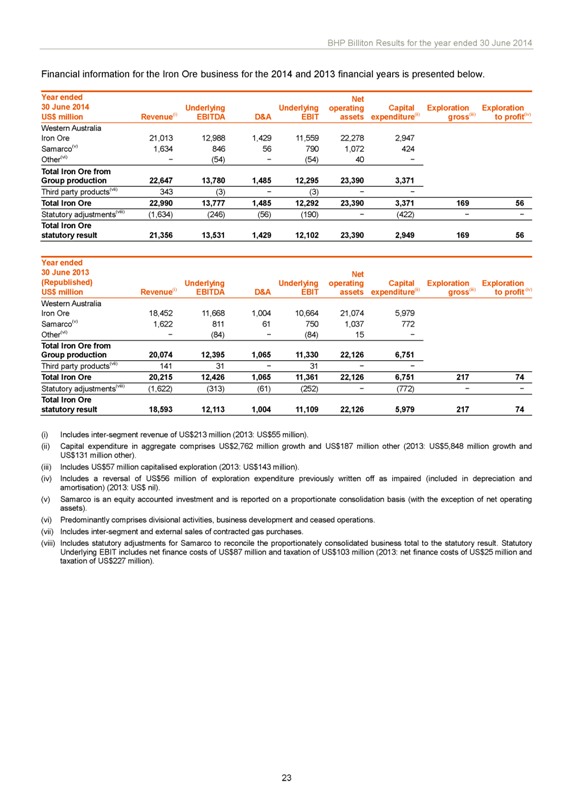

News Release

Iron Ore

Iron ore production increased by 20 per cent in the 2014 financial year to a record 204 Mt, exceeding initial full-year guidance by more than eight per cent. WAIO production

of 225 Mt (100 per cent basis) represents a fourteenth consecutive annual record and was underpinned by the early commissioning of Jimblebar and our productivity agenda, which raised the capacity of our integrated supply chain.

In the 2015 financial year WAIO production is expected to increase by a further 20 Mt to approximately 245 Mt (100 per cent basis). We expect additional productivity gains to

support another year of record performance despite the planned tie-in of shiploaders 1 and 2 during the December 2014 half year. Total iron ore production is forecast to increase by 11 per cent in the 2015 financial year to 225 Mt.

A low-cost option to expand Jimblebar to 55 Mtpa (100 per cent basis) and broader debottlenecking of our mines and inner harbour infrastructure are expected to underpin further

growth in WAIO supply-chain capacity to 290 Mtpa (100 per cent basis). The additional 65 Mtpa of capacity is likely to have a capital intensity below US$50 per annual tonne with the improvement in productivity and economies of scale also expected to

significantly reduce unit costs.

A six per cent fall in the average realised price of iron ore to US$103 per wet metric tonne (FOB) reduced Underlying EBIT by

US$864 million, net of price-linked costs, although this was partially offset by a weaker Australian dollar which increased Underlying EBIT by US$383 million. Iron ore sales, on average, were linked to the index price for the month of shipment, with

price differentials reflecting product quality.

Underlying EBIT for the 2014 financial year increased by US$993 million to US$12.1 billion. An 18 per cent increase

in WAIO sales volumes was the major contributor, adding US$1.8 billion to Underlying EBIT. Conversely, the progressive ramp-up of several major projects resulted in a US$425 million increase in depreciation and amortisation expense during the

period. Having redirected the WAIO supply-chain bottleneck away from the mines and back to the port, a 12 per cent reduction in unit costs to US$25.89 per tonne was achieved in the June 2014 half year.

WAIO unit costs (US$ million) FY13 FY14 H1 FY14 H2 FY14

Revenue 18,452 21,013 10,849 10,164

Underlying EBITDA 11,668 12,988 6,801 6,187

Cash costs (gross) 6,784 8,025

4,048 3,977

Less: freight 856 1,274 625 648

Less: royalties 1,192 1,497 744

753

Cash costs (net) 4,736 5,254 2,679 2,576

Sales (Mt, equity share) 160,955

190,843 91,327 99,516

Cash cost per tonne (US$) 29.42 27.53 29.33 25.89

A

number of major project milestones were achieved during the period, further underscoring Iron Ore’s track record in project delivery. For example, the Jimblebar Mine Expansion project delivered first production six months ahead of schedule and

the ramp-up to 35 Mtpa (100 per cent basis) is now expected before the end of the 2014 calendar year. The WAIO Port Blending and Rail Yard Facilities project and fourth pellet plant at Samarco were also completed during the period. The fourth pellet

plant is expected to ramp-up to 30.5 Mtpa (100 per cent basis) before the end of the 2015 financial year.

On 29 July 2014, BHP Billiton and ArcelorMittal signed an

agreement for the acquisition by ArcelorMittal of BHP Billiton’s 43.5 per cent stake in Euronimba Limited, which holds an effective 95 per cent interest in the Mount Nimba iron ore project in Guinea. Completion of the transaction is

subject to the receipt of regulatory approval and other customary closing conditions.

22

BHP Billiton Results for the year ended 30 June 2014

Financial information for the Iron Ore business for the 2014 and 2013 financial years is presented below.

Year ended Net

30 June 2014 Underlying Underlying operating Capital Exploration Exploration

US$ million Revenue(i) EBITDA D&A EBIT assets expenditure(ii) gross(iii) to profit(iv)

Western Australia

Iron Ore 21,013 12,988 1,429 11,559 22,278 2,947

Samarco(v) 1,634 846 56 790 1,072 424

Other(vi) - (54) - (54) 40 -

Total Iron Ore from

Group production 22,647 13,780 1,485 12,295 23,390 3,371

Third party products(vii) 343 (3) - (3) - -

Total Iron Ore 22,990 13,777 1,485 12,292 23,390

3,371 169 56

Statutory adjustments(viii) (1,634) (246) (56) (190) - (422) - -

Total Iron Ore statutory result 21,356 13,531 1,429 12,102 23,390 2,949 169 56

Year ended

30 June 2013 Net

(Republished) Underlying Underlying operating Capital Exploration Exploration

US$ million

Revenue(i) EBITDA D&A EBIT assets expenditure(ii) gross(iii) to profit (iv)

Western Australia

Iron Ore 18,452 11,668 1,004 10,664 21,074 5,979

Samarco(v) 1,622 811 61 750 1,037 772

Other(vi) - (84) - (84) 15 -

Total Iron Ore from

Group production 20,074 12,395 1,065 11,330 22,126 6,751

Third party products(vii) 141 31 - 31

- -

Total Iron Ore 20,215 12,426 1,065 11,361 22,126 6,751 217 74

Statutory