Quartz Mountain Resources Ltd. - Exhibit 99.2 - Filed by newsfilecorp.com

|

| |

| |

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| |

| |

| MANAGEMENT'S DISCUSSION AND ANALYSIS |

| |

| |

| SIX MONTHS ENDED JANUARY 31, 2015

|

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

T A B L E O F C O N T E N T S

- 2 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

This Management's Discussion and Analysis ("MD&A") should

be read in conjunction with the unaudited condensed interim consolidated

financial statements of Quartz Mountain Resources Ltd. ("Quartz Mountain" or the

"Company") for the three and six months ended January 31, 2015 and audited

consolidated financial statements of Quartz Mountain Resources Ltd. and related

MD&A for the year ended July 31, 2014, as publicly filed on SEDAR at

www.sedar.com. All monetary amounts herein are expressed in Canadian dollars

unless otherwise stated.

The Company reports in accordance with International Financial

Reporting Standards ("IFRS") and the following disclosure, and associated

financial statements, are presented in accordance with IFRS.

For the purposes of the discussion below, date references refer

to calendar year and not the Company's fiscal reporting period.

This MD&A is prepared as of March 25, 2015.

Cautionary Note to Investors Concerning Forward-looking

Statements

This discussion includes certain statements that may be deemed

"forward-looking statements". All statements in this disclosure, other than

statements of historical facts, that address permitting, exploration drilling,

exploitation activities and events or developments that the Company expects are

forward-looking statements. Although the Company believes the expectations

expressed in such forward-looking statements are based on reasonable

assumptions, such statements are not guarantees of future performance and actual

results or developments may differ materially from those in the forward-looking

statements. Assumptions used by the Company to develop forward-looking

statements include the following: the Company’s projects will obtain all

required environmental and other permits and all land use and other licenses,

and no geological or technical problems will occur. Factors that could cause

actual results to differ materially from those in forward-looking statements

include market prices, exploration and exploitation successes, continuity of

mineralization, potential environmental issues and liabilities associated with

exploration, development and mining activities, uncertainties related to the

ability to obtain necessary permits, licenses and title and delays due to third

party opposition or litigation, exploration and development of properties

located within First Nations treaty and asserted territories may affect or be

perceived to affect treaty and asserted aboriginal rights and title, which may

cause permitting delays or opposition by First Nation communities, changes in

laws and government policies regarding mining and natural resource exploration

and exploitation, continued ability of the Company to raise necessary capital,

and general economic, market or business conditions. Investors are cautioned

that any such statements are not guarantees of future performance and actual

results or developments may differ materially from those projected in the

forward-looking statements. The Company reviews its forward looking statements

on an on-going basis and updates this information when circumstances require it.

- 3 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The information comprised in this MD&A relates to Quartz

Mountain Resources Ltd. and its subsidiary (together referred to as the

"Company"). Quartz Mountain Resources Ltd. is the ultimate parent entity of the

group.

Quartz Mountain is an exploration and development company

focused on acquiring and advancing promising mineral prospects in British

Columbia ("BC").

The Company holds a 100% interest in the Galaxie Project, which

is situated in the Stikine Terrane, a prospective region in northwestern BC that

hosts a number of important copper and gold deposits. There is potential for the

discovery of bulk tonnage copper-gold and/or molybdenum and vein-type precious

and base metal deposits in the project-area. Historical exploration identified

several copper occurrences, including the Gnat porphyry copper deposit.

In 2012, Quartz Mountain completed ground surveys in the

vicinity of the Gnat deposit and several other prospects across the property and

followed up with a two-hole drilling program at the Gnat deposit. Several new

targets were identified by the surveys. Drilling confirmed the presence of

porphyry mineralization at depth in the Gnat deposit. Intervals of 55.7 metres

grading 0.44% copper and 91.0 metres grading 0.37% copper were encountered in

the two holes drilled. Additional ground exploration was carried out in the

other target areas on the property in 2013. A series of alkali intrusions which

are known to be the principal hosts for porphyry copper-gold deposits elsewhere

in the Stikine-Iskut porphyry belt were observed in an area known as the Hu

target. The potential at Hu and at another target identified during the 2012

exploration program, called Dalvenie East warrants further exploration.

Market conditions, which have made financing for exploration

projects difficult over the past three years, prevail in 2015. The Company

continues to seek partners to joint venture or farm out Galaxie and its other

exploration project.

| 1.2.1 |

Agreements – Galaxie

Project |

Sale Agreement with Finsbury Exploration Ltd.

In August 2012, Quartz Mountain acquired a 100% interest in the

Galaxie Project from Finsbury Exploration Ltd. ("Finsbury") through a sale

agreement (the "Sale Agreement") dated July 27, 2012. The Galaxie Project

acquired from Finsbury included an area of 1,488 square kilometres, comprised of

three mineral claims totalling approximately 1,294 hectares (the "Gnat Pass

Property") and the surrounding mineral claims staked by Finsbury to that time.

Pursuant to the terms of the Sale Agreement, Quartz Mountain

issued 2,038,111 shares to Finsbury and also assumed the rights and obligations

of Finsbury under a mineral property purchase agreement (the "Bearclaw

Agreement") between Finsbury and Bearclaw Capital Corp. ("Bearclaw") relating to

the Gnat Pass Property. Quartz Mountain also assumed the rights and obligations

under a net smelter returns ("NSR") royalty agreement which requires the payment

to Bearclaw of a 1% NSR royalty on the Gnat Pass Property up to a maximum of

$7,500,000.

The remaining payment obligations to Bearclaw for the Gnat Pass

Property under the Bearclaw Agreement assumed by Quartz Mountain consisted

of:

| • |

a payment of $50,000 to Bearclaw (paid);

|

- 4 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| • |

the issuance of a convertible debenture (the “Debenture”)

to Bearclaw in the amount of $650,000, bearing an interest rate of 8% per

annum and with a maturity date of January 31, 2014 (issued; however, the

interest rate and maturity date were later amended – see below); and

|

| |

|

| • |

the issuance to Bearclaw of 1,000,000 shares in

the capital of Quartz Mountain (issued). |

July 2013 Amendment to the Debenture

In July 2013, Quartz Mountain and the holder of the Debenture

entered into an agreement to amend the Debenture, whereby the Galaxie Joint

Venture made a $50,000 principal payment toward the Debenture, reducing the

outstanding balance to $600,000. The interest rate was increased to 10% per

annum, and the maturity date was extended to October 31, 2014.

October 2014 Amendment to the Debenture

Effective October 1, 2014, Quartz Mountain and Bearclaw further

amended the terms of the Debenture (hereafter referred to as the “Amended

Debenture”), pursuant to which:

| • |

the Company made a principal payment of $50,000

to Bearclaw against the Debenture (completed October 8, 2014), |

| |

|

| • |

the remaining balance (the “Principal Sum”) of

$550,000 is repayable in equal annual installments of $50,000, commencing

on January 31, 2015; and |

| |

|

| • |

effective October 1, 2014, the principal amount

outstanding bears interest at 7.5% per annum, payable quarterly in

arrears. |

Upon a completion by the Company of an equity financing (the

“New Financing”) for a minimum amount of $1,000,000, at least 50% of any

outstanding balance of the then-outstanding Principal Sum along with any

interest accrued thereon will be automatically converted (the “Automatic

Conversion”) into the Company’s common shares. Bearclaw may elect to convert,

concurrent with the Automatic Conversion, any portion of the remaining 50% of

the then-outstanding Principal Sum and accrued interest thereon (the “Optional

Conversion”) into Quartz Mountain common shares. For the purposes of Automatic

Conversion and Optional Conversion, subject to the rules and policies of the TSX

Venture Exchange (“TSX-V”), the conversion price will be the greater of (i) the

volume-weighted average trading price of common shares of the Company on the

TSX-V for the 20 consecutive trading days ending on the fifth trading day

preceding the date of such conversion, and (ii) the price at which the Company

issues common shares pursuant to the New Financing. For the purposes of

Automatic Conversion and Optional Conversion of any accrued interest, the

conversion price will be the market price of the Company’s common shares on the

date of conversion. Except pursuant to these Automatic Conversion and Optional

Conversion provisions, Bearclaw does not have an option to convert the Amended

Debenture into the Company’s common shares.

| 1.2.2 |

Technical Programs – Galaxie

Project |

Exploration of the Galaxie Project was summarized in a

technical report (the “2013 technical report”) entitled “Technical Report on the

Galaxie Project, Liard Mining Division, British Columbia” effective date April 30, 2013 by B.K. (Barney) Bowen, PEng, and

updated with information on the 2013 program from Company files. No programs

have been carried out on the Galaxie Project in 2014 and none are planned for

2015.

- 5 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The Galaxie Project is located on Highway 37, approximately 24

kilometres south of Dease Lake, BC. The Project-area currently consists of 306

mineral claims covering an area of approximately 1,165 square kilometres.

Paved Highway 37 passes through the center of the Galaxie

Project and provides year-round direct access to the adjacent project-area,

including the Gnat Pass Property. Other parts of the Galaxie Project can be

accessed by helicopter.

The operating season for surface exploration is from early June

through to early October. Because of its close proximity to Highway 37, diamond

drilling activities at the Gnat deposit, which is within the Gnat Pass Property,

can be carried out throughout the year.

Dease Lake (population of about 600) offers an array of

services, including motel accommodations, food, fuel, a variety of small

equipment operators, post office, health clinic and government services. Mining

and exploration make up the most substantial industry. Regional Power manages

the off-grid Dease Lake Generating Station, located about 30 km west of Dease

Lake. The facility supplies the entire energy load for the community of Dease

Lake. Completion of a 287-kilovolt transmission line, extending 344 kilometres

from the existing Skeena substation south of Terrace to a new substation near

Bob Quinn Lake (located about 180 kilometres by road south of Dease Lake) was

recently announced by the BC government. It will supply the new mine development

under construction at Imperial Metals Corporation’s Red Chris Project by way of

a spur line from Bob Quinn Lake.

Geology and Mineralization

The Galaxie Project is underlain mainly by volcanic, intrusive

and lesser sedimentary rocks of the Middle Triassic to Lower Jurassic Stikine

Terrane which, elsewhere in northern British Columbia is known to host the large

Red Chris, Schaft Creek, Galore and KSM and Snowfield porphyry deposits. Upper

Triassic Stuhini Group volcanic rocks and a quartz feldspar porphyry dike

complex host the Gnat copper deposit. The Gnat deposit is located near the

northern contact of the Late Triassic to Middle Jurassic, multiphase Hotailuh

Batholith-Three Sisters Pluton intrusive complex, which occupies most of the

remainder of the Galaxie project-area and hosts a number of base and/or precious

metals prospects and showings.

History

The first record of exploration in the Gnat Pass Property area

was in 1960 when prospecting work by Cassiar Asbestos Corporation discovered

copper mineralization in the vicinity of Lower Gnat Lake. Since that time, at

least nine companies have explored the property completing geological mapping,

rock, soil and stream sediment geochemical sampling, magnetic and induced

polarization (“IP”) geophysical surveys and diamond drilling during the periods

of 1960-1971, 1990-1996 and in 2005. Most of the historical work focused on the

Gnat deposit, and occurrences in the vicinity.

During the period 1965-1969, previous operators completed

18,390 metres of diamond drilling in 110 holes in this area. Most of this

historical drilling was carried out in the Gnat deposit over an area measuring about 600 metres by 600 metres, down to a

maximum depth of about 300 metres below surface.

- 6 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

A historical estimate of "indicated reserves" of about 30

million tonnes grading 0.389% Cu for the Gnat Deposit was reported by Lytton

Minerals Ltd, in 1972. The estimate uses categories that are not recognized by

National Instrument 43-101 Standards of Disclosure for Mineral Projects. The

qualified person for the 2013 technical report has not done sufficient work to

classify the historical estimate as a current mineral resource or mineral

reserve. Quartz Mountain is not treating the historical estimate as current.

Past work on other mineral occurrences in the Galaxie Project

area includes:

| • |

At Hu, during the period 1969 to 2007, several mining

companies carried out: silt, soil and rock geochemical sampling;

geological mapping; Induced Polarization ("IP") and ground magnetic

surveys; and 22 bulldozer trenches. |

| |

|

| • |

At Disco, Stikine Moly and Stikine, during the period

1970-79, two companies carried out: silt, soil and rock geochemical

sampling; geological mapping; IP, ground magnetic and VLF surveys; and

limited hand trenching and test-pitting. |

| |

|

| • |

At Nup, during the period 1970 to 2008, six mining

companies and one individual carried out: silt, soil and rock geochemical

sampling; geological mapping; IP and ground magnetic surveys; and limited

hand trenching and test-pitting. Three diamond drilling programs (14

holes) tested porphyry molybdenum+/-copper showings and soil geochemical

anomalies. |

| |

|

| • |

At Pat, during the period 1971-76, two companies carried

out: grid soil surveys; IP and ground magnetic surveys; and a refraction

seismic survey. |

Prospecting and geochemical silt, soil and rock sampling

program carried out by a previous owner in 2011 identified a number of target

areas at Galaxie. Much of the work was outside of known areas of mineralization,

but some work did overlap with known mineral occurrences, including some of

those listed above.

Gnat Deposit

In 2012, Quartz Mountain relogged historical drill holes and

carried out geological mapping in the Gnat deposit-area. Two deep diamond drill

holes totaling 1,164 metres were also drilled to test for continuation of copper

mineralization beneath the historical reserve estimate. Hole GT12001 intersected

two intervals of significant copper mineralization, including 56 metres grading

0.44% Cu, well below the extent of the historical estimate, demonstrating that

porphyry-style copper mineralization in the Gnat deposit extends over a known

vertical range of about 500 metres. In their lower portions, both holes

encountered a major thrust fault which has structurally superimposed older

deposit host rocks over younger Hazelton Group sedimentary rocks.

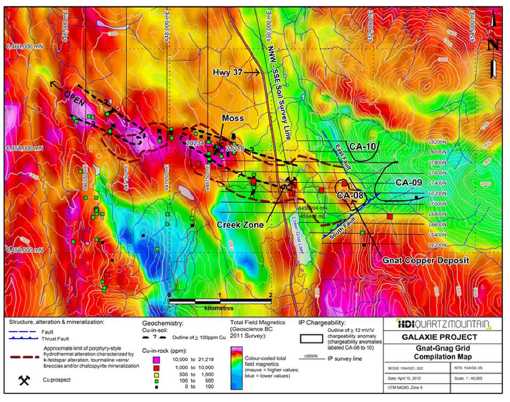

Geological mapping in the Gnat deposit area identified

porphyry-style hydrothermal alteration characterized by occurrences of

k-feldspar veining and flooding, tourmaline in veins or breccia bodies and

chalcopyrite mineralization over a west-northwest trending zone measuring about

3.5 kilometres long by 700 metres to 1,000 metres wide. Contained within this

large 'hydrothermal footprint' are the Creek Zone and Moss copper prospects, the

two main known mineralized zones outside of the Gnat deposit area (see figure

below).

- 7 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

There is considerable room to explore for new zones of copper

mineralization at moderate to greater depths in portions of the Gnat deposit, in

the Creek Zone and Moss prospect areas, and elsewhere along the 3.5

kilometre-long zone of porphyry-style hydrothermal alteration. Mineralization

may include porphyry-type deposits or more constrained, but possibly higher

grade, mineralized breccia bodies.

Other Targets

Preliminary prospecting of two gossans in the Dalvenie East

target-area in 2012 was successful in locating encouraging copper mineralization

in chalcopyrite +/- bornite veins up to 10 cm wide, hosted in chlorite-altered

diorite to monzodiorite wall rocks. Narrow k-feldspar alteration envelopes

surrounding the veins also contain chalcopyrite and bornite. Magnetic signatures

at Dalvenie East suggest that regional-scale faults, or subsidiary faults

related to them, could control vein-type or fault-controlled copper-gold

mineralization similar to that seen at the nearby Dalvenie prospect. This target

was not followed up in 2013.

In 2013, an associated company completed ground exploration

programs at some of the priority areas that Quartz Mountain had identified in

2012. At Hu, a series of alkali intrusions which are known to be the principal

hosts in the Stikine-Iskut porphyry belt for porphyry copper-gold deposits were

observed.

The potential of the intrusions at Hu and the Dalvenie East

target warrant further exploration.

- 8 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

ZNT Project

The Company holds a 100% interest in the ZNT property, which

consists of 21 claims covering an area of approximately 102 square kilometres

located in central British Columbia, some 15 kilometres southeast of the town of

Smithers, BC. The property was staked by Quartz Mountain in 2012. Target

definition was carried out in 2012 and 2013, and an initial drilling program was

done but no economic mineralization was encountered. No further work is

planned.

Angel's Camp Property

The Company retains a 1% net smelter return royalty payable to

the Company on any production from the Angel's Camp property located in Lake

County, Oregon. The Angel's Camp property is currently held by Alamos Gold

Inc.

The discussion in this section references calendar years and

dollar amounts are stated in United States dollars.

Copper prices increased from early 2009 until late 2011. From

that time, prices have been variable and weakened overall.

The average annual gold price steadily increased from 2008 to

2012. Gold prices trended lower in 2013, and have been variable but weakened

overall in 2014 and 2015.

An upward trend in silver prices began in 2010, and continued

to late September 2011; prices reached as high as $43/oz in 2011, resulting in

the highest average annual price since 2008. Prices ranged between $26/oz and

$35/oz between October 2011 and December 2012. Prices trended downward in 2013.

They have been variable in 2014 and 2015, with an overall decrease in the

average price.

Average annual prices for the past five years as well as the

average prices so far in 2015 for copper (Cu), gold (Au) and silver (Ag) are

shown in the table below:

| Calendar Year |

Metal Prices (US$) |

| Cu |

Au |

Ag |

| 2010 |

$ 3.42/lb |

$ 1,228/oz |

$ 20.24/oz |

| 2011 |

$ 4.00/lb |

$ 1,572/oz |

$ 35.25/oz |

| 2012 |

$ 3.61/lb |

$ 1,669/oz |

$ 31.16/oz |

| 2013 |

$ 3.32/lb |

$ 1,410/oz |

$ 23.80/oz |

| 2014 |

$ 3.11/lb |

$ 1,266/oz |

$ 19.08/oz |

| 2015 to the date of this MD&A |

$ 2.63/lb |

$ 1,220/oz |

$ 16.70/oz |

Source: www.metalprices.com

- 9 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| 1.3 |

SELECTED ANNUAL

INFORMATION |

Not required for interim MD&A.

| 1.4 |

SUMMARY OF QUARTERLY

RESULTS |

The amounts in the following table are expressed in thousands

of Canadian Dollars, except per share amounts and the weighted average number of

common shares outstanding. Minor differences are due to rounding.

| |

|

Jan-31 |

|

|

Oct-31 |

|

|

Jul-31 |

|

|

Apr-30 |

|

|

Jan-31 |

|

|

Oct-31 |

|

|

Jul-31 |

|

|

Apr-30 |

|

| |

|

2015 |

|

|

2014 |

|

|

2014 |

|

|

2014 |

|

|

2014 |

|

|

2013 |

|

|

2013 |

|

|

2013 |

|

| Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Exploration and evaluation |

$ |

1 |

|

$ |

5 |

|

$ |

(5 |

) |

$ |

6 |

|

$ |

25 |

|

$ |

236 |

|

$ |

(20 |

) |

$ |

160 |

|

| General and administration

|

|

103 |

|

|

176 |

|

|

112 |

|

|

139 |

|

|

187 |

|

|

165 |

|

|

242 |

|

|

326 |

|

| Share-based payments |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

23 |

|

|

28 |

|

| Loss from operations |

|

(104 |

) |

|

(181 |

) |

|

(107 |

) |

|

(145 |

) |

|

(212 |

) |

|

(401 |

) |

|

(245 |

) |

|

(514 |

) |

| Other items (ii) |

|

(7 |

) |

|

(10 |

) |

|

(10 |

) |

|

(9 |

) |

|

(8 |

) |

|

27 |

|

|

23 |

|

|

4 |

|

| Loss for the quarter |

$ |

(111 |

) |

$ |

(191 |

) |

$ |

(117 |

) |

$ |

(154 |

) |

$ |

(220 |

) |

$ |

(374 |

) |

$ |

(222 |

) |

$ |

(510 |

) |

| Loss per share |

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.01 |

|

$ |

0.02 |

|

| 1.5 |

RESULTS OF OPERATIONS AND FINANCIAL

CONDITION |

The following financial data has been prepared in accordance

with IFRS and is expressed in Canadian dollars unless otherwise stated.

| 1.5.1 |

Results of operations for the six months period ended

January 31, 2014 vs. 2013 |

The Company recorded a loss of $303,000 in the current six

months period compared to a loss of $594,000 in the comparative period of the

prior fiscal year, primarily due to a decrease in exploration and evaluation

(“E&E”) activities during the current period.

- 10 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

Total E&E costs during six months ended January 31, 2015

reduced to $6,000, compared to $261,000 in E&E costs during six months ended

January 31, 2014. The following tables provide a breakdown of exploration costs

incurred during the six month period ended January 31, 2015 and 2014:

| Six months ended

January 31, 2015 |

| E&E costs |

|

Galaxie |

|

|

Hotai |

|

|

ZNT |

|

|

Other |

|

|

Total |

|

| Assaying |

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

3,362 |

|

$ |

3,362 |

|

| Drilling |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Geological |

|

– |

|

|

– |

|

|

– |

|

|

1,675 |

|

|

1,675 |

|

| Graphics |

|

– |

|

|

– |

|

|

– |

|

|

85 |

|

|

85 |

|

| Property fees |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Site activities |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Sustainability |

|

– |

|

|

– |

|

|

– |

|

|

600 |

|

|

600 |

|

| Transportation |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Travel |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Total |

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

5,722 |

|

$ |

5,722 |

|

| Six months ended

January 31, 2015 |

| E&E costs |

|

Galaxie |

|

|

Hotai |

|

|

ZNT |

|

|

Other |

|

|

Total |

|

| Assaying |

$ |

7,274 |

|

$ |

1,053 |

|

$ |

12,104 |

|

$ |

– |

|

$ |

20,431 |

|

| Drilling |

|

– |

|

|

– |

|

|

90,773 |

|

|

– |

|

|

90,773 |

|

| Geological |

|

30,570 |

|

|

3,200 |

|

|

45,615 |

|

|

2,397 |

|

|

81,782 |

|

| Graphics |

|

204 |

|

|

– |

|

|

153 |

|

|

1,615 |

|

|

1,972 |

|

| Property fees |

|

208 |

|

|

– |

|

|

– |

|

|

– |

|

|

208 |

|

| Site activities |

|

8,530 |

|

|

676 |

|

|

19,136 |

|

|

– |

|

|

28,342 |

|

| Sustainability |

|

– |

|

|

34 |

|

|

17,148 |

|

|

– |

|

|

17,182 |

|

| Transportation |

|

4,770 |

|

|

– |

|

|

– |

|

|

– |

|

|

4,770 |

|

| Travel |

|

4,673 |

|

|

5,530 |

|

|

5,337 |

|

|

– |

|

|

15,540 |

|

| Total |

$ |

44,069 |

|

$ |

10,289 |

|

$ |

178,357 |

|

$ |

3,522 |

|

$ |

261,000 |

|

- 11 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The following table provides a breakdown of the administration

costs incurred:

| Administration costs |

|

Six months ended

|

|

|

Six months ended

|

|

| |

|

January 31, 2015 |

|

|

January 31, 2014 |

|

| Legal, accounting and audit

|

$ |

34,775 |

|

$ |

38,174 |

|

| Office and administration |

|

230,923 |

|

|

291,880 |

|

| Shareholder communication |

|

3,489 |

|

|

6,241 |

|

| Travel |

|

– |

|

|

6,853 |

|

| Trust and filing |

|

9,909 |

|

|

9,651 |

|

| Total |

$ |

279,096 |

|

$ |

352,799 |

|

| 1.5.2 |

Results of operations for the three months ended

January 31, 2014 vs. 2013 |

The Company recorded a loss of $111,000 in the current period

compared to a loss of $220,000 in the prior fiscal year, primarily due to a

decrease in E&E activities during the current period.

Total E&E costs during three months ended January 31, 2015

reduced to $1,000, compared to $25,000 in E&E costs during three months

ended January 31, 2014. The following tables provide a breakdown of exploration

costs incurred during the three month period ended January 31, 2015 and

2014:

|

Three months ended January 31, 2015 |

| E&E costs |

|

Galaxie |

|

|

Hotai |

|

|

ZNT |

|

|

Other |

|

|

Total |

|

| Assaying |

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

400 |

|

$ |

400 |

|

| Drilling |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Geological |

|

– |

|

|

– |

|

|

– |

|

|

800 |

|

|

800 |

|

| Graphics |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Property fees |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Site activities |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Sustainability |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Helicopter support |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Travel |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Total |

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

1,200 |

|

$ |

1,200 |

|

- 12 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| Three

months ended January 31, 2014 |

| E&E costs |

|

Galaxie |

|

|

Hotai |

|

|

ZNT |

|

|

Other |

|

|

Total |

|

| Assaying |

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

– |

|

$ |

– |

|

| Drilling |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Geological |

|

12,160 |

|

|

204 |

|

|

8,586 |

|

|

490 |

|

|

21,440 |

|

| Graphics |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Property fees |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Site activities |

|

– |

|

|

– |

|

|

3,323 |

|

|

– |

|

|

3,323 |

|

| Sustainability |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Helicopter support |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Travel |

|

– |

|

|

– |

|

|

– |

|

|

– |

|

|

– |

|

| Total |

$ |

12,160 |

|

$ |

204 |

|

$ |

11,909 |

|

$ |

490 |

|

$ |

24,763 |

|

The following table provides a breakdown of the administration

costs incurred:

| Administration costs |

|

Three months |

|

|

Three months |

|

| |

|

ended |

|

|

ended |

|

| |

|

January 31, 2015 |

|

|

January 31, 2014 |

|

| Legal, accounting and audit

|

$ |

4,484 |

|

$ |

36,898 |

|

| Office and administration |

|

93,652 |

|

|

141,568 |

|

| Shareholder communication |

|

1,911 |

|

|

3,420 |

|

| Travel |

|

– |

|

|

2,299 |

|

| Trust and filing |

|

2,395 |

|

|

2,885 |

|

| Total |

$ |

102,442 |

|

$ |

187,070 |

|

Historically, the Company's primary source of funding has been

the issuance of equity securities for cash through private placements to

sophisticated investors and institutions. The Company is in the process of

acquiring and exploring mineral property interests. The Company's continuing

operations are entirely dependent upon the ability of the Company to obtain the

necessary financing to complete the exploration and development of its projects,

the existence of economically recoverable mineral reserves at its projects, the

ability of the Company to obtain the necessary permits to mine, on future

profitable production of any mine and the proceeds from the disposition of its

mineral property interests.

At January 31, 2015, the Company had cash and cash equivalents

of $0.85 million and a working capital deficit of $2.3 million. Of the total

short-term liabilities of $3.2 million at January 31, 2015, $3.1 million was

payable to Hunter Dickinson Services Inc. ("HDSI"), a related party.

- 13 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

To address its working capital deficit at January 31, 2015, the

Company has taken the following mitigating measures:

| • |

the Company has entered into an agreement with

the holder of its convertible debenture to restructure the payment terms

of the debenture (see 1.2 Overview); and |

| |

|

| • |

the Company has obtained a confirmation from HDSI that

HDSI will continue to provide services to the Company and will not demand

repayment of amounts outstanding, prior to November 1, 2015.

|

Management believes that its liquid assets at January 31, 2015

are sufficient to meet its known obligations it expects to pay over the next 12

months and to maintain its mineral rights in good standing for this next 12

month period. The Company is actively managing its cash reserves, and curtailing

activities as necessary in order to ensure its ability to meet payments as they

come due.

Additional debt or equity financing, or joint ventures will be

required to fund additional exploration or development programs. The Company has

a reasonable expectation that additional funds will be available to meet ongoing

exploration and development costs. However, there can be no assurance that the

Company will continue to obtain additional financial resources or that it will

be able to achieve positive cash flows. If the Company is unable to obtain

adequate additional financing, the Company will be required to re-evaluate its

planned expenditures and will rely on short term borrowings to finance its

minimum expenditure requirement until additional funds can be raised through

financing activities.

General market conditions for junior exploration companies have

resulted in depressed equity prices, despite higher commodity prices. Although

the Company was able to successfully complete private placements in each of the

2012 and 2013 fiscal years, a further and continued deterioration in market

conditions will increase the cost of obtaining capital and limit the

availability of funds to the Company in the future. Accordingly, management is

actively monitoring the effects of the current economic and financing conditions

on our business and reviewing our discretionary spending, capital projects and

operating expenditures, and implementing appropriate cash and cash management

strategies.

The Company had no material commitments for capital

expenditures as at January 31, 2015. The Company has no lines of credit or other

sources of financing which have been arranged but are as of yet, unused.

At January 31, 2015, there were no externally imposed capital

requirements to which the Company is subject and with which the Company has not

complied.

As the Company continues to incur losses in support of the

advancement of exploration activities on its projects, shareholders’ equity is

in a deficit position.

| 1.8 |

OFF-BALANCE SHEET

ARRANGEMENTS |

None.

- 14 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| 1.9 |

TRANSACTIONS WITH RELATED

PARTIES |

Key management personnel

The required disclosure for the remuneration of the Company’s

key management personnel is provided in Note 8(a) of unaudited condensed interim

consolidated financial statements of the Company for the three and six months

ended January 31, 2015. These are also available at www.sedar.com.

Hunter Dickinson Inc.

Description of the relationship

Hunter Dickinson Inc. (“HDI”) and its wholly owned subsidiary

Hunter Dickinson Services Inc. ("HDSI") are private companies established by a

group of mining professionals engaged in advancing mineral properties for a

number of publicly-listed exploration companies, one of which is the

Company.

The following directors or officers of the Company also have a

role within HDSI.

| Individual |

Role within the Company |

Role within HDSI |

| Ronald Thiessen |

President, Chief Executive

Officer and Director |

Director |

| Lena Brommeland |

Executive Vice President . |

Employee |

| Robert Dickinson |

Director |

Director |

| Scott Cousens |

Director |

Director |

| Michael Lee |

Chief Financial Officer |

Employee |

| Trevor Thomas |

General Counsel and Corporate

Secretary |

Employee |

The business purpose of the related party transactions

HDSI provides technical, geological, corporate communications,

regulatory compliance, and administrative and management services to the

Company, on an as-needed and as-requested basis from the Company.

HDSI also incurs third party costs on behalf of the Company.

Such third party costs include, for example, directors and officers insurance,

travel, conferences, and technology services.

As a result of this relationship, the Company has ready access

to a range of diverse and specialized expertise on a regular basis, without

having to engage or hire full-time experts. The Company benefits from the

economies of scale created by HDSI which itself serves several clients. The Company is also able to eliminate many of its fixed costs,

including rent, technology, and other infrastructure which would otherwise be

incurred for maintaining its corporate offices.

- 15 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The measurement basis used

The Company procures services from HDSI pursuant to an

agreement dated July 2, 2010. Services from HDSI are provided on a non-exclusive

basis as required and as requested by the Company. The Company is not obligated

to acquire any minimum amount of services from HDSI. The fees for services from

HDSI are determined based on a charge-out rate for each employee performing the

service and for the time spent by the employee. Such charge-out rates are agreed

and set annually in advance.

Third party costs are billed at cost, without markup.

Ongoing contractual or other commitments resulting from the

related party relationship

There are no ongoing contractual or other commitments resulting

from the Company's transactions with HDSI, other than the payment for services

already rendered and billed. The agreement may be terminated upon 60 days'

notice by either of the Company or HDSI.

Transactions and balances

The required disclosure for the transactions and balances with

HDSI is provided in Note 8(b) of the accompanying unaudited condensed interim

consolidated financial statements of the Company for the three and six months

ended January 31, 2015. These are also available at www.sedar.com.

Not applicable.

| 1.11 |

PROPOSED TRANSACTIONS |

There are no proposed assets or business acquisitions or

dispositions, other than those in the ordinary course, before the board of

directors for consideration.

| 1.12 |

CRITICAL ACCOUNTING

ESTIMATES |

Not required. The Company is a Venture Issuer.

| 1.13 |

CHANGES IN ACCOUNTING POLICIES INCLUDING INITIAL

ADOPTION |

The required disclosure is provided in note 2 of the

accompanying financial statements.

- 16 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| 1.14 |

FINANCIAL INSTRUMENTS AND OTHER

INSTRUMENTS |

The carrying amounts of cash and cash equivalents, amounts

receivable, accounts payable and accrued liabilities, balances due to related

parties, and long term debt approximate their fair values.

| 1.15 |

OTHER MD&A

REQUIREMENTS |

| 1.15.1 |

Additional Disclosure for Venture Issuers Without

Significant Revenue |

| (a) |

exploration and evaluation assets

or expenditures |

The required disclosure is presented in the unaudited

condensed interim consolidated statements of comprehensive loss and

Section 1.5 of this MD&A. |

| |

|

|

| (b) |

expensed research and development

costs |

Not applicable |

| |

|

|

| (c) |

intangible assets arising from

development |

Not applicable |

| |

|

|

| (d) |

general and administration

expenses |

The required disclosure is presented in the unaudited

condensed interim consolidated statements of comprehensive loss and

Section 1.5 of this MD&A. |

| |

|

|

| (e) |

any material costs, whether expensed or recognized as

assets, not referred to in paragraphs (a) through (d) |

None |

| 1.15.2 |

Disclosure of Outstanding Share

Data |

The following details the share capital structure as at the

date of this MD&A:

| |

|

Number |

|

| Common shares |

|

27,299,513 |

|

| Share options |

|

828,000 |

|

The Debenture is subject to mandatory and optional conversion

provisions that trigger upon a completion by the Company of an equity financing

for a minimum amount of $1,000,000 (see Section 1.2 Overview).

| 1.15.3 |

Internal Controls over Financial Reporting

Procedures |

The Company's management, including the Chief Executive Officer

and the Chief Financial Officer, is responsible for establishing and maintaining

adequate internal control over financial reporting. Under the supervision of the

Chief Executive Officer and Chief Financial Officer, the Company's internal

control over financial reporting is a process designed to provide reasonable

assurance regarding the reliability of financial reporting and

the preparation of financial statements for external purposes in accordance with

IFRS. The Company's internal control over financial reporting includes those

policies and procedures that:

- 17 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

| • |

pertain to the maintenance of records that, in

reasonable detail, accurately and fairly reflect the transactions and

dispositions of the assets of the Company; |

| |

|

| • |

provide reasonable assurance that transactions are

recorded as necessary to permit preparation of financial statements in

accordance with IFRS, and that receipts and expenditures of the Company

are being made only in accordance with authorizations of management and

directors of the company; and |

| |

|

| • |

provide reasonable assurance regarding prevention or

timely detection of unauthorized acquisition, use or disposition of the

Company's assets that could have a material effect on the financial

statements. |

There has been no change in the design of the Company's

internal control over financial reporting that has materially affected, or is

reasonably likely to materially affect, the Company's internal control over

financial reporting during the period covered by this Management's Discussion

and Analysis.

| 1.15.4 |

Disclosure Controls and Procedures |

The Company has disclosure controls and procedures in place to

provide reasonable assurance that any information required to be disclosed by

the Company under securities legislation is recorded, processed, summarized and

reported within the appropriate time periods and that required information is

accumulated and communicated to the Company's management, including the Chief

Executive Officer and Chief Financial Officer, as appropriate, so that decisions

can be made about the timely disclosure of that information.

| 1.15.5 |

Limitations of Controls and Procedures |

The Company's management, including its Chief Executive Officer

and Chief Financial Officer, believe that any system of disclosure controls and

procedures or internal control over financial reporting, no matter how well

conceived and operated, can provide only reasonable, not absolute, assurance

that the objectives of the control system are met. Furthermore, the design of a

control system must reflect the fact that there are resource constraints and the

benefits of controls must be considered relative to their costs. Because of the

inherent limitations in all control systems, they cannot provide absolute

assurance that all control issues and instances of fraud, if any, within the

Company have been prevented or detected. These inherent limitations include the

realities that judgments in decision-making can be faulty and breakdowns can

occur because of simple error or mistake. Additionally, controls can be

circumvented by the individual acts of some persons, by collusion of two or more

people, or by unauthorized override of controls. The design of any system of

controls is also based in part upon certain assumptions about the likelihood of

future events, and there can be no assurance that any design will succeed in

achieving its stated goals under all potential future conditions. Accordingly,

because of the inherent limitations in a cost effective control system,

misstatements due to error or fraud may occur and not be detected.

- 18 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The risk factors associated with the principal business of the

Company are discussed below. Due to the nature of the Company's business and the

present stage of exploration and development of its projects in British

Columbia, an investment in the securities of Quartz Mountain is highly

speculative and subject to a number of risks. Briefly, these include the highly

speculative nature of the resources industry characterized by the requirement

for large capital investments from an early stage and a very small probability

of finding economic mineral deposits. In addition to the general risks of

mining, there are country-specific risks, including currency, political, social,

permitting and legal risk. An investor should carefully consider the risks

described below and the other information that Quartz Mountain furnishes to, or

files with, the Securities and Exchange Commission and with Canadian securities

regulators before investing in Quartz Mountain's common shares, and should not

consider an investment in Quartz Mountain unless the investor is capable of

sustaining an economic loss of the entire investment. The Company's actual

exploration and operating results may be very different from those expected as

at the date of this MD&A.

Going Concern Assumption

The Company's condensed interim consolidated financial

statements have been prepared assuming the Company will continue on a going

concern basis. However, unless additional funding is obtained, this assumption

will have to change. The Company has a negative working capital position, and

has incurred losses since inception. Failure to continue as a going concern

would require that Quartz Mountain's assets and liabilities be restated on a

liquidation basis, which could differ significantly from the going concern

basis.

Additional Funding Requirements

Further development of the Company's properties and continued

operations will require additional capital. The Company currently does not have

sufficient funds to fully develop the properties it holds. It is possible that

the financing required by the Company will not be available, or, if available,

will not be available on acceptable terms. If the Company issues treasury shares

to finance its operations or expansion plans, shareholders will suffer dilution

of their investment and control of the Company may change. If adequate funds are

not available, or are not available on acceptable terms, the Company will not be

able to take advantage of opportunities, or otherwise respond to competitive

pressures and remain in business. In addition, a positive production decision at

any of the Company's current projects or any other development projects acquired

in the future will require significant resources and funding for project

engineering and construction. Accordingly, the continuing development of the

Company's properties depends upon the Company's ability to obtain financing

through debt financing, equity financing, the joint venturing or disposition of

its current projects, or other means. There is no assurance that the Company

will be successful in obtaining the required financing for these or other

purposes, including for general working capital.

Future Profits/Losses and Production Revenues/Expenses

The Company has no history of operations or earnings, and

expects that its losses and negative cash flow will continue for the foreseeable

future. The Company currently has a limited number of mineral properties and

there can be no assurance that the Company will, if needed, be able to acquire

additional properties of sufficient technical merit to represent a compelling

investment opportunity. If the Company is unable to acquire additional

properties, its entire prospects will rest solely with its current projects and accordingly, the risk of

being unable to identify a mineral deposit will be higher than if the Company

had additional properties to explore. There can be no assurance that the Company

will ever be profitable in the future. The Company's operating expenses and

capital expenditures may increase in subsequent years as needed consultants,

personnel and equipment associated with advancing exploration, development and

commercial production of its current properties and any other properties that

the Company may acquire are added. The amounts and timing of expenditures will

depend on the progress of on-going exploration and development, the results of

consultants' analyses and recommendations, the rate at which operating losses

are incurred, the execution of any joint venture agreements with strategic

partners, and the Company's acquisition of additional properties and other

factors, many of which are beyond the Company's control. The Company does not

expect to receive revenues from operations in the foreseeable future, and

expects to incur losses unless and until such time as its current properties, or

any other properties the Company may acquire, commence commercial production and

generate sufficient revenues to fund its continuing operations. The development

of the Company's current properties and any other properties the Company may

acquire will require the commitment of substantial resources to conduct the

time-consuming exploration and development of properties. The Company

anticipates that it will retain any cash resources and potential future earnings

for the future operation and development of the Company's business. The Company

has not paid dividends since incorporation and the Company does not anticipate

paying dividends in the foreseeable future. There can be no assurance that the

Company will generate any revenues or achieve profitability. There can be no

assurance that the underlying assumed levels of expenses will prove to be

accurate. To the extent that such expenses do not result in the creation of

appropriate revenues, the Company's business may be materially adversely

affected. It is not possible to forecast how the business of the Company will

develop.

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

Exploration, Development and Mining Risks

Resource exploration, development, and operations are highly

speculative, characterized by a number of significant risks, which even a

combination of careful evaluation, experience and knowledge may not reduce,

including among other things, unsuccessful efforts resulting not only from the

failure to discover mineral deposits but from finding mineral deposits which,

though present, are insufficient in quantity and quality to return a profit from

production. Few properties that are explored are ultimately developed into

producing mines. Unusual or unexpected formations, formation pressures, fires,

power outages, labour disruptions, flooding, explosions, cave-ins, landslides

and the inability to obtain suitable or adequate machinery, equipment or labour

are other risks involved in the operation of mines and the conduct of

exploration programs. The Company will rely upon consultants and others for

exploration, development, construction and operating expertise. Substantial

expenditures are required to establish mineral resources and mineral reserves

through drilling, to develop metallurgical processes to extract the metal from

mineral resources, and in the case of new properties, to develop the mining and

processing facilities and infrastructure at any site chosen for mining.

No assurance can be given that minerals will be discovered in

sufficient quantities to justify commercial operations or that funds required

for development can be obtained on a timely basis. Whether a mineral deposit

will be commercially viable depends on a number of factors, some of which are:

the particular attributes of the deposit, such as size, grade and proximity to

infrastructure; metal prices, which are highly cyclical; and government

regulations, including regulations relating to prices, taxes, royalties, land tenure,

land use, importing and exporting of minerals, and environmental protection. The

exact effect of these factors cannot accurately be predicted, but the

combination of these factors may result in the Company not receiving an adequate

return on invested capital.

- 20 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The Company will carefully evaluate the political and economic

environment in considering any properties for acquisition.

Permits and Licenses

The operations of the Company will require licenses and permits

from various governmental authorities. There can be no assurance that the

Company will be able to obtain all necessary licenses and permits which may be

required to carry out exploration and development of the Galaxie Project.

Infrastructure Risk

The operations of the Company are carried out in geographical

areas which may lack adequate infrastructure and are subject to various other

risk factors. Mining, processing, development and exploration activities depend,

to one degree or another, on adequate infrastructure. Reliable roads, bridges,

power sources and water supply are important determinants which affect capital

and operating costs. Lack of such infrastructure or unusual or infrequent

weather phenomena, government or other interference in the maintenance or

provision of such infrastructure could adversely affect the Company's

operations, financial condition and results of operations.

Changes in Local Legislation or Regulation

The Company's mining and processing operations and exploration

activities are subject to extensive laws and regulations governing the

protection of the environment, exploration, development, production, exports,

taxes, labour standards, occupational health, waste disposal, toxic substances,

mine and worker safety, protection of endangered and other special status

species and other matters. The Company's ability to obtain permits and approvals

and to successfully operate in particular communities may be adversely impacted

by real or perceived detrimental events associated with the Company's activities

or those of other mining companies affecting the environment, human health and

safety of the surrounding communities. Delays in obtaining or failure to obtain

government permits and approvals may adversely affect the Company's operations,

including its ability to explore or develop properties, commence production or

continue operations. Failure to comply with applicable environmental and health

and safety laws and regulations may result in injunctions, fines, suspension or

revocation of permits and other penalties. The costs and delays associated with

compliance with these laws, regulations and permits could prevent the Company

from proceeding with the development of a project or the operation or further

development of a mine or increase the costs of development or production and may

materially adversely affect the Company's business, results of operations or

financial condition. The Company may also be held responsible for the costs of

addressing contamination at the site of current or former activities or at third

party sites. The Company could also be held liable for exposure to hazardous

substances.

- 21 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

Environmental Matters

All of the Company's operations are and will be subject to

environmental regulations, which can make operations expensive or prohibit them

altogether. The Company may be subject to potential risks and liabilities

associated with pollution of the environment and the disposal of waste products

that could occur as a result of its mineral exploration, development and

production. In addition, environmental hazards may exist on a property in which

the Company directly or indirectly holds an interest, which are unknown to the

Company at present and have been caused by previous or existing owners or

operators of the Company's projects. Environmental legislation provides for

restrictions and prohibitions on spills, releases or emissions of various

substances produced in association with certain mining industry operations which

would result in environmental pollution. A breach of such legislation may result

in the imposition of fines and penalties, or the requirement to remedy

environmental pollution, which would reduce funds otherwise available to the

Company and could have a material adverse effect on the Company. If the Company

is unable to fully remedy an environmental problem, it could be required to

suspend operations or undertake interim compliance measures pending completion

of the required remedy, which could have a material adverse effect on the

Company.

There is no assurance that future changes in environmental

regulation, if any, will not adversely affect the Company's operations. There is

also a risk that the environmental laws and regulations may become more onerous,

making the Company's operations more expensive. Many of the environmental laws

and regulations will require the Company to obtain permits for its activities.

The Company will be required to update and review its permits from time to time,

and may be subject to environmental impact analyses and public review processes

prior to approval of the additional activities. It is possible that future

changes in applicable laws, regulations and permits or changes in their

enforcement or regulatory interpretation could have a significant impact on some

portion of the Company's business, causing those activities to be economically

re-evaluated at that time.

Groups Opposed to Mining May Interfere with the Company's

Efforts to Explore and Develop its Properties

Organizations opposed to mining may be active in the regions in

which the Company conducts its exploration activities. Although the Company

intends to comply with all environmental laws and maintain good relations with

local communities, there is still the possibility that those opposed to mining

will attempt to interfere with the development of the Company's properties. Such

interference could have an impact on the Company's ability to explore and

develop its properties in a manner that is most efficient or appropriate, or at

all, and any such impact could have a material adverse effect on the Company's

financial condition and the results of its operations.

Market for Securities and Volatility of Share Price

There can be no assurance that active trading market in the

Company's securities will be established or sustained. The market price for the

Company's securities is subject to wide fluctuations. Factors such as

announcements of exploration results, as well as market conditions in the

industry or the economy as a whole, may have a significant adverse impact on the

market price of the securities of the Company.

- 22 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The stock market has from time to time experienced extreme

price and volume fluctuations that have often been unrelated to the operating

performance of particular companies.

Conflicts of Interest

The Company's directors and officers may serve as directors or

officers of other companies, joint venture partners, or companies providing

services to the Company or they may have significant shareholdings in other

companies. Situations may arise where the directors and/or officers of the

Company may be in competition with the Company. Any conflicts of interest will

be subject to and governed by the law applicable to directors' and officers'

conflicts of interest. In the event that such a conflict of interest arises at a

meeting of the Company's directors, a director who has such a conflict will

abstain from voting for or against the approval of such participation or such

terms. In accordance with applicable laws, the directors of the Company are

required to act honestly, in good faith and in the best interests of the

Company.

General Economic Conditions

Global financial markets have experienced a sharp increase in

volatility during the last few years. Market conditions and unexpected

volatility or illiquidity in financial markets may adversely affect the

prospects of the Company and the value of the Company's shares.

Reliance on Key Personnel

The Company is dependent on the continued services of its

senior management team, and its ability to retain other key personnel. The loss

of such key personnel could have a material adverse effect on the Company. There

can be no assurance that any of the Company's employees will remain with the

Company or that, in the future, the employees will not organize competitive

businesses or accept employment with companies competitive with the Company.

Furthermore, as part of the Company's growth strategy, it must

continue to hire highly qualified individuals. There can be no assurance that

the Company will be able to attract, train or retain qualified personnel in the

future, which would adversely affect its business.

Risks Related to Flow-Through Shares

Financing of the Company may involve the issuance of

flow-through common shares under the Income Tax Act (Canada). There is no

guarantee that there will not be any differences of opinion between the Canadian

federal and British Columbia provincial tax authorities with respect to the tax

treatment of flow-through common shares issued under a financing, if any, and

the activities contemplated by the Company's exploration and development

programs.

If the Company does not expend an amount equal to the gross

proceeds from the sale of flow-through common shares so as to incur sufficient

qualifying expenditures within the relevant timeframe, subscribers in the

flow-through financing may be reassessed. The Company shall be obligated to

indemnify any subscribers of flow-through common shares for tax payable pursuant

to any such reassessment pursuant to the terms and conditions set out in the

subscription agreements that the Company will enter into with each subscriber in a

flow-through financing. There can be no assurances that the Company will have

sufficient funds to satisfy such obligations.

- 23 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

Competition

The resources industry is highly competitive in all its phases,

and the Company will compete with other mining companies, many of which have

greater financial, technical and other resources. Competition in the mining

industry is primarily for: attractive mineral rich properties capable of being

developed and producing economically; the technical expertise to find, develop

and operate such properties; the labour to operate the properties; and the

capital for the purpose of funding such properties. Many competitors not only

explore for and mine certain minerals, but also conduct production and marketing

operations on a worldwide basis. Such competition may result in the Company

being unable to acquire desired properties, to recruit or retain qualified

employees or to acquire the capital necessary to fund its operations and develop

its properties. The Company's inability to compete with other mining companies

for these resources could have a materially adverse effect on the Company's

results of operation and its business.

Uninsurable Risks

In the course of exploration, development and production of

mineral properties, certain risks, and in particular, unexpected or unusual

geological operating conditions including rock bursts, cave ins, fires, flooding

and earthquakes may occur. It is not always possible to fully insure against

such risks and the Company may decide not to take out insurance against such

risks as a result of high premiums or other reasons.

Land Claims

In Canada, aboriginal interests, rights (including treaty

rights), claims and title may exist notwithstanding that they may be

unregistered or overlap with other tenures and interests granted to third

parties. Generally speaking, the scope and content of such rights are not well

defined and may be the subject of litigation or negotiation with the government.

The government has a legal obligation to consult First Nations on proposed

activities that may have an impact on asserted or proven aboriginal interests,

claims, rights or title. All of the mineral claims in the Company's projects are

identified by the Province of British Columbia as overlapping with areas in

which certain aboriginal groups have asserted aboriginal interests, rights,

claims or, title or undefined rights under historic treaties. Nevertheless,

potential overlaps between the Company's properties and existing or asserted

aboriginal interests, rights, claims or, title, or undefined rights under

historic treaties, may exist notwithstanding whether the Province of British

Columbia has identified such interests, rights, claims or, title, or undefined

rights under historic treaties.

Property Title

The acquisition of title to resource properties is a very

detailed and time consuming process. Title to, and the area of, resource claims

may be disputed. Although the Company believes it has taken reasonable measures

to ensure that title to the mineral claims comprising part of its projects are

held as described, there is no guarantee that title to any of

those claims will not be challenged or impaired. There may be valid challenges

to the title of any of the mineral claims comprising the Company's projects

that, if successful, could impair development or operations or both.

- 24 -

| QUARTZ MOUNTAIN RESOURCES LTD. |

| |

| FOR THE SIX MONTHS ENDED JANUARY 31, 2015 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

The Mineral Property Underlying the Company's Net Smelter

Return Royalty Interest Contains no Known Ore

The Company holds a 1% net smelter return ("NSR") royalty

interest on the Quartz Mountain Property (recently renamed "Angel's Camp"), an

exploration stage prospect in Oregon. The Company's interest in the property

will be limited to any future NSR that would be forthcoming only if or when any

mining commences on the property. There is currently no known body of ore on the

property. Extensive additional exploration work will be required to ascertain if

any mineralization may be economic.

- 25 -