UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-5047

Tax-Free Fund of Colorado

(Exact name of Registrant as specified in charter)

380 Madison Avenue

New York, New York 10017

(Address of principal executive offices) (Zip code)

Joseph P. DiMaggio

380 Madison Avenue

New York, New York 10017

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 697-6666

Date of fiscal year end: 12/31/11

Date of reporting period: 12/31/11

FORM N-CSR

ITEM 1. REPORTS TO STOCKHOLDERS.

|

|

|

Annual

Report

|

|

December 31, 2011

|

TAX-FREE FUND

OF

COLORADO

A tax-free income investment

|

|

Serving Colorado Investors For Close To 25 Years

Tax-Free Fund of Colorado

“Know Your Destination”

|

|

February, 2012

Dear Fellow Shareholder:

With all the turmoil going on in the financial markets lately, many people are asking themselves, “Just where should I put my money?”

While that would appear to be an important question to ask, we believe a more prudent question is, “What are you saving for?”

If it were possible to know in advance just when to buy or sell a security to maximize profit, constantly switching your investment vehicle, trying to capture the latest trend, could very well be uncomplicated. Unfortunately, “timing” the market with any degree of consistency is nearly impossible.

We have generally found that for the average investor switching continuously from one security to another in the management of his/her investment portfolio tends to be fruitless. Indeed, it may often prove to be an ill-advised exercise. With the degree of volatility inherent in the markets, missing an upturn or downturn could adversely affect your performance.

We believe the most practical way for you to invest is to focus on your goals, your time frame for achieving these goals, and your risk tolerance, instead of concentrating on what the market is or isn’t doing on a short-term basis.

As an investor in Tax-Free Fund of Colorado, we think it’s important for you to focus on your ultimate destination – capital preservation and tax-free income – the key objective of your Fund.

Since there may be many twists and turns on the road to financial health, what steps can you take to increase your odds of reaching your final destination safely?

|

|

·

|

Get assistance, if you need it – a financial professional can help answer your questions and get you going in the right direction.

|

|

|

·

|

Develop a map – where are you now? Where do you want to be? How long do you want to take to get there?

|

|

|

·

|

Make a plan and stick to it.

|

|

|

·

|

Periodically visit with your financial advisor to discuss your ongoing goals and circumstances.

|

NOT A PART OF THE ANNUAL REPORT

|

|

·

|

Develop an asset allocation model – in other words, diversify and don’t put all of your eggs in one basket.

|

|

|

·

|

Rebalance your portfolio periodically in line with your goals and timeline.

|

|

|

·

|

Stay focused on the long-term. You won’t stress about the little bumps along the way as long as you are sure you are on the right road.

|

But, there is more to investing in Tax-Free Fund of Colorado than just capital preservation. If keeping what you have were your only objective, your piggy bank could serve as just an appropriate depository.

Therefore, it should come as no surprise that another benefit that you gain from being an investor in Tax-Free Fund of Colorado is monthly double tax-free income.

To use an analogy, people who buy the Fund probably wouldn’t buy a cow hoping to sell it when its market price increases at some future date. They would buy the cow and keep it for its continuing stream of milk. In the case of Tax-Free Fund of Colorado, the continuing stream is in the form of tax-free dividends.

If capital preservation and tax-free income is your destination, your investment in Tax-Free Fund of Colorado puts you on a path with a fund that seeks this investment objective. As long as your financial plan is a sound one and is in line with your goals, it may be best not to get off the road looking for a short-cut. Chances are, you just may get lost.

Sincerely,

|

|

|

|

Lacy B. Herrmann

Founder and Chairman Emeritus |

Diana P. Herrmann

President |

Consideration should be given to the risks of investing, including: potential loss of value, market risk, interest rate risk, credit risk, and geographic concentration. Past performance does not guarantee future stability. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For certain investors, some dividends may be subject to Federal and state taxes.

NOT A PART OF THE ANNUAL REPORT

|

|

Serving Colorado Investors For Close To 25 Years

Tax-Free Fund of Colorado

ANNUAL REPORT

Management Discussion

|

|

2011 Review

The United States government came to within hours of defaulting, certain municipal governments now have a higher credit rating than the Federal government and the Federal Open Market Committee reintroduced monetary policy from the 1960’s named after a Chubby Checker song. While all of these items are ripe fodder for a media circus, the most exaggerated story of the past year has been from a banking analyst quoted as claiming “hundreds of billions” of municipal bonds may default this year. Just as the shelves of grocery stores were fearfully stripped due to media hysteria preceding Hurricane Irene, investors were unduly frightened by the unusual market volatility of a normally staid asset class.

And, much like the significance of Hurricane Irene was overstated by the media, the metaphorical storm of the municipal credit based defaults has proven significantly milder than initial headlines lead investors to believe. “Headline Risk” created by the financial media, however, has taken a toll on the municipal marketplace even despite the lesser level of defaults than predicted. Although distinct from credit risk, headline risk, has increased investor concerns regarding the municipal bond asset class. These concerns sent investors exiting the market at an inopportune time as bond prices decreased and yields rose. However, rising state revenues, meaningful expenditure reductions and attractive relative yields have overcome most fears as investors have returned to the municipal bond market.

Ironically, the impending default risk of the Federal government proved less troublesome to the municipal market than the aforementioned municipal bond headline risk. In May, the Treasury Department reported that the debt limit of $14.29 trillion had been reached, but it could keep the government functioning normally until August 2. With significant opposition, the House of Representatives approved an agreement on August 1, by a 269 to 161 vote. The Senate passed the measure the following day, hours before the deadline set by the Treasury and it was signed shortly thereafter by the President, which provided the ability to make the necessary appropriations by the narrowest of margins. While the last-minute deal may have avoided a default, the spectacle raised the eyebrows of citizens and investors questioning the ability of our Federal government to make decisions about national debt and budgeting issues. The resulting effect on the municipal bond market is difficult to quantify since the event was spread over a broad period of time and largely priced into the market by the time it ultimately unfolded. The resulting damage inflicted on the credit side was shouldered primarily by certain state and local governments dependent upon Federal appropriations.

1

MANAGEMENT DISCUSSION (continued)

On August 5, Standard & Poor’s downgraded the long-term sovereign credit rating of the United States of America for the first time ever. The rating of the nation was lowered one notch from AAA to AA+. The downgrade was largely credited to the instability of American policymaking, specifically the partisan fight over raising the nation’s debt ceiling. The market, in general, still views the nation in a triple-A light with Moody’s Investors Service affirming its Aaa U.S. rating and Fitch Ratings rating the sovereign debt of the Nation AAA. S&P analyzes state and local government credit quality independent of the Federal government placing certain state and local governments in higher ratings categories than the Nation, for the first time ever. S&P’s rating action and the negligible reaction of the municipal bond market to the downgrade demonstrate the resiliency of the municipal bond asset class. Furthermore, the effect on Colorado municipal bonds has been minor; the primary result being increased scrutiny of credits relying upon Federal appropriations. Nevertheless, the downgrade of the nation’s credit rating further reinforces the value of deep credit research and a disciplined approach to portfolio management.

The Federal Open Market Committee continues its efforts to reinvigorate the economy, this time with Operation Twist designed to lower yields on long-term bonds through the purchase of $400 billion of longer-term Treasuries, and sale of $400 billion of Treasuries that mature in three months to three years. The “twist” term refers to early 1960s-era operations wherein the central bank sold shorter-dated securities and bought longer-dated securities in an effort to drive down long-term rates and stimulate economic growth. The intention of the policy is to make home loans and business loans more attractive to consumers encouraging home purchases and business expansion. At the very least, the result of this policy will be to keep long-term rates on Treasuries low, which should have a corresponding effect on highly rated municipal bonds forcing investors seeking higher yields to either look further out on the yield curve or at lower rated or nonrated sectors. We intend to remain focused on maintaining high credit quality through our proprietary research and local expertise. Through our internal credit process we will seek to continue to review lower rated investment grade bonds to find credits with minimal risk that we believe will outperform the market.

Colorado’s economy continues to recover, albeit at a disconcertingly slow pace. The Colorado labor market improved slowly throughout the year producing a net gain of about 27,000 jobs during the year. While this is a positive sign, the 2011 job growth only represents approximately 20% of the jobs lost in the 2008 through 2010 period. Areas of strength included professional and business services, education and health services, and leisure and hospitality. Construction, information services, financial activities and the government sector all experienced declining employment during the year. The state unemployment rate ended the year at 7.9% versus 8.9% a year earlier.

The Colorado housing market continues to fare slightly better than the national market. Home prices declined approximately 2.7% in the state versus the national 4.7% decline. There was a wide variance in regional home price performance with Boulder and Fort Collins showing strength

2

MANAGEMENT DISCUSSION (continued)

while Pueblo, Grand Junction and Greeley remained near cyclical lows. The pace of residential foreclosures in the state has slowed to a 5 year low, but there is still an overhang of unsold, bank-owned homes or “shadow inventory” that inhibits a robust rebound in prices. The commercial real estate market has also remained lethargic with office vacancy rates in the Denver Metro area around 15% and industrial and retail vacancy rates of 6% and 7.8%, respectively. Tight credit conditions and low absorption rates will likely continue to plague this sector of the economy until there is greater job growth and increased demand for goods and services.

The Colorado municipal market experienced a significant contraction in new issues as state and local governments are generally not inclined to borrow for capital projects in the face of uncertain revenue streams and voter resistance to increased taxes for debt and operating mill levy increases. New issuance totaled approximately $3.8 billion for 2011 compared to $7-8 billion annually in the previous 5 years. Notable new issues during the year included $400 million Denver Public Schools, $416 million Colorado Health Facilities, and $203 million University of Colorado. We expect this low new issuance environment to remain as long as Colorado governments are required to make significant and difficult spending reductions to balance their budgets. It is important to note that the long history of Colorado governments’ ability and willingness to take the painful steps to protect principal and interest payments is a positive credit characteristic for bondholders.

The portfolio characteristics of Tax-Free Fund of Colorado were largely unchanged for the year. The weighted average maturity remained just above 11 years, credit quality was AA/A and the average interest rate on the bonds in the Fund was 5%. We seek to continue to emphasize the stability of the dividend by maintaining an average of over 6 years until the first call date for the securities in the Fund. As the municipal bond market recovered from depressed prices early in the year, shareholders in the Class Y shares experienced an 8.96% total return for the year. This return was comprised of two components: the percentage change in the share value, which was 4.92%, and the amount of income distributed, which was 4.04% for the year.

2012 Strategy

We have sought to maintain an investment strategy for Tax-Free Fund of Colorado that emphasizes intermediate maturities and investment grade credit quality securities for the past quarter century. Our goal has always been, and continues to be, providing an above average double tax-exempt dividend and a relatively stable share price. We will seek to accomplish this goal by limiting our interest rate sensitivity over the course of the year by reducing exposure to longer duration positions. Although it is difficult to see a meaningful increase in interest rates in the short run, we think now is a good time to prepare the portfolio for this eventuality. Bond prices have rebounded sharply from their lows earlier in 2011 and now offer, in our view, an opportunity to reduce the holdings that may be more volatile in a rising interest rate environment. Record low interest rates have generally tempted investors to add more risk to their portfolios by extending maturities to capture additional

3

MANAGEMENT DISCUSSION (continued)

yield. We believe that it is prudent to resist that temptation and seek to maintain a defensive position until more attractive yields are available.

Furthermore, we have sought to reduce or eliminated positions where our analysis uncovered deteriorating underlying credit quality or issuers that were not meeting their disclosure requirements. We intend to continue to add to sectors where our credit research provides a competitive advantage to purchase bonds benefitting from wide credit spreads. Areas we have been targeting are those on the periphery of the credit spreads still providing significant security such as unlimited tax backed general obligation bonds and revenue obligations with strong legal covenants. In addition, we have sought to continue to add to some of the high quality positions the Fund currently owns. We believe that our emphasis on research combined with a defensive interest rate posture should provide our shareholders with a stable share price and reliable double tax-exempt income stream.

Thank you for your investment in Tax-Free Fund of Colorado.

Performance data represents past performance, but does not guarantee future results. Investment return and principal value will fluctuate; shares, when redeemed, may be worth more or less than their original cost; current performance may be lower or higher than the data presented.

NOT FDIC INSURED – NO BANK GUARANTEE – MAY LOSE VALUE

4

PERFORMANCE REPORT

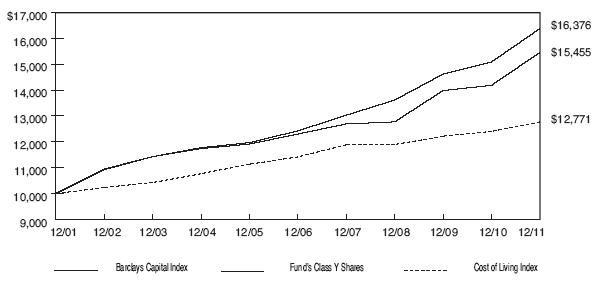

The following graph illustrates the value of $10,000 invested in the Class Y shares of Tax-Free Fund of Colorado for the 10-year period ended December 31, 2011 as compared with the Barclays Capital Quality Intermediate Municipal Bond Index (the “Barclays Capital Index”) and the Consumer Price Index (a cost of living index). The performance of each of the other classes is not shown in the graph but is included in the table below. It should be noted that the Barclays Capital Index does not include any operating expenses nor sales charges, and being nationally oriented, does not reflect state specific bond market performance.

| Average Annual Total Return | ||||||||||||||||

|

for periods ended December 31, 2011

|

||||||||||||||||

|

Since

|

||||||||||||||||

|

Class and Inception Date

|

1 Year

|

5 Years

|

10 Years

|

Inception

|

||||||||||||

|

Class A (commenced operations on 5/21/87)

|

||||||||||||||||

|

With Maximum Sales Charge

|

4.48 | % | 3.76 | % | 3.95 | % | 5.38 | % | ||||||||

|

Without Sales Charge

|

8.81 | 4.61 | 4.38 | 5.56 | ||||||||||||

|

Class C (commenced operations on 4/30/96)

|

||||||||||||||||

|

With CDSC

|

6.77 | 3.63 | 3.39 | 3.61 | ||||||||||||

|

Without CDSC

|

7.80 | 3.63 | 3.39 | 3.61 | ||||||||||||

|

Class Y (commenced operations on 4/30/96)

|

||||||||||||||||

|

No Sales Charge

|

8.96 | 4.67 | 4.45 | 4.78 | ||||||||||||

|

Barclays Capital Index

|

8.55 | 5.68 | 5.06 |

5.91

|

(Class A) | |||||||||||

|

5.26

|

(Class C & Y) | |||||||||||||||

Total return figures shown for the Fund reflect any change in price and assume all distributions within the period were invested in additional shares. Returns for Class A shares are calculated with and without the effect of the initial 4% maximum sales charge. Returns for Class C shares are calculated with and without the effect of the 1% contingent deferred sales charge (CDSC) imposed on redemptions made within the first 12 months after purchase. Class Y shares are sold without any sales charge. The rates of return will vary and the principal value of an investment will fluctuate with market conditions. Shares, if redeemed, may be worth more or less than their original cost. A portion of each class’s income may be subject to Federal and state income taxes. Past performance is not predictive of future investment results.

5

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees and Shareholders of

Tax-Free Fund of Colorado:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Tax-Free Fund of Colorado as of December 31, 2011 and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2011, by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Tax-Free Fund of Colorado as of December 31, 2011, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

February 28, 2012

6

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (21.4%)

|

(unaudited)

|

Value

|

||||||

|

Hospital (0.7%)

|

|||||||||

|

Rangely, Colorado Hospital District Refunding

|

|||||||||

| $ | 2,000,000 |

5.500%, 11/01/22

|

Baa1/NR/NR

|

$ | 2,145,740 | ||||

|

Metropolitan District (5.9%)

|

|||||||||

|

Arapahoe, Colorado Park & Recreation District

|

|||||||||

| 1,070,000 |

5.000%, 12/01/17 NPFG Insured Pre-Refunded

|

A1/NR/NR

|

1,115,443 | ||||||

|

Denver, Colorado International Business Center

|

|||||||||

|

Metropolitan District No.1, Refunding

|

|||||||||

| 2,090,000 |

5.125%, 12/01/25

|

NR/BBB/NR

|

2,115,979 | ||||||

|

Fraser Valley, Colorado Metropolitan Recreational

|

|||||||||

|

District

|

|||||||||

| 1,875,000 |

5.000%, 12/01/25

|

NR/A/NR

|

2,047,856 | ||||||

|

Hyland Hills Metro Park & Recreation District,

|

|||||||||

|

Colorado

|

|||||||||

| 875,000 |

4.375%, 12/15/26 ACA Insured

|

NR/NR/NR*

|

753,839 | ||||||

|

Lincoln Park, Colorado Metropolitan District,

|

|||||||||

|

Refunding & Improvement

|

|||||||||

| 1,535,000 |

5.625%, 12/01/20

|

NR/BBB-/NR

|

1,565,378 | ||||||

|

Meridian Metropolitan District, Colorado Refunding

|

|||||||||

| 1,645,000 |

4.500%, 12/01/23 Series A

|

NR/A-/A

|

1,760,315 | ||||||

|

North Metro Fire Rescue District, Colorado

|

|||||||||

| 1,200,000 |

4.625%, 12/01/20 AMBAC Insured

|

NR/AA/NR

|

1,339,332 | ||||||

|

Park Creek Metropolitan District, Colorado Revenue

|

|||||||||

|

Refunding & Improvement - Senior Property Tax

|

|||||||||

|

Support

|

|||||||||

| 2,000,000 |

5.500%, 12/01/21 AGMC Insured

|

NR/AA-/BBB+

|

2,337,260 | ||||||

|

Poudre Tech Metropolitan District, Colorado

|

|||||||||

|

Unlimited Property Tax Supported Revenue

|

|||||||||

|

Refunding & Improvement, Series B

|

|||||||||

| 1,990,000 |

5.000%, 12/01/28 AGMC Insured

|

NR/AA-/NR

|

2,252,421 | ||||||

|

Stonegate Village Metropolitan District, Colorado

|

|||||||||

|

Refunding & Improvement

|

|||||||||

| 500,000 |

5.000%, 12/01/23 NPFG Insured

|

Baa2/A-/NR

|

537,725 | ||||||

| 900,000 |

5.000%, 12/01/24 NPFG Insured

|

Baa2/A-/NR

|

9 67,059 | ||||||

|

Total Metropolitan District

|

16,792,607 | ||||||||

7

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School Districts (14.8%)

|

|||||||||

|

Adams & Arapahoe Counties, Colorado Joint School

|

|||||||||

|

District #28J

|

|||||||||

| $ | 2,500,000 |

5.500%, 12/01/23

|

Aa2/AA-/NR

|

$ | 2,972,900 | ||||

|

Adams & Weld Counties, Colorado School District

|

|||||||||

|

#27J

|

|||||||||

| 1,000,000 |

5.375%, 12/01/26 NPFG Insured

|

Aa2/AA-/NR

|

1,107,080 | ||||||

|

Arapahoe County, Colorado School District #001

|

|||||||||

|

Englewood

|

|||||||||

| 3,235,000 |

5.000%, 12/01/27

|

Aa2/NR/NR

|

3,761,690 | ||||||

|

Arapahoe County, Colorado School District #006

|

|||||||||

|

Littleton

|

|||||||||

| 1,000,000 |

5.250%, 12/01/21 NPFG Insured Pre-Refunded

|

Aa1/AA/NR

|

1,044,730 | ||||||

|

Boulder Larimer & Weld Counties, Colorado

|

|||||||||

| 1,260,000 |

5.000%, 12/15/26 AGMC Insured

|

Aa2/AA-/NR

|

1,400,679 | ||||||

| 1,500,000 |

5.000%, 12/15/28

|

Aa2/AA-/NR

|

1,698,840 | ||||||

|

Clear Creek, Colorado School District

|

|||||||||

| 1,000,000 |

5.000%, 12/01/16 AGMC Insured Pre-Refunded

|

Aa3/AA-/NR

|

1,042,470 | ||||||

|

Denver, Colorado City & County School District No. 1

|

|||||||||

| 3,000,000 |

5.250%, 12/01/27

|

Aa2/AA-/NR

|

3,471,060 | ||||||

|

Denver, Colorado City & County School District

|

|||||||||

|

No. 1 Series A

|

|||||||||

| 1,000,000 |

5.000%, 12/01/28

|

Aa2/AA-/NR

|

1,126,240 | ||||||

|

Denver, Colorado City & County School District

|

|||||||||

|

No. 1 Series C

|

|||||||||

| 1,900,000 |

3.000%, 12/01/23

|

Aa2/AA-/NR

|

1,997,280 | ||||||

|

El Paso County, Colorado School District #20

|

|||||||||

| 1,500,000 |

5.000%, 12/15/14 NPFG Insured Pre-Refunded

|

Aa2/NR/NR

|

1,566,435 | ||||||

| 1,085,000 |

5.500%, 12/15/23 NPFG Insured Pre-Refunded

|

Aa2/NR/NR

|

1,191,851 | ||||||

|

El Paso County, Colorado School District #20

|

|||||||||

| 1,500,000 |

4.500%, 12/15/25 AGMC Insured

|

Aa2/NR/NR

|

1,614,030 | ||||||

|

El Paso County, Colorado School District #20

|

|||||||||

|

Refunding

|

|||||||||

| 1,945,000 |

4.375%, 12/15/23

|

Aa2/NR/NR

|

2,251,337 | ||||||

|

Garfield County, Colorado School District

|

|||||||||

| 1,250,000 |

5.000%, 12/01/17 AGMC Insured Pre-Refunded

|

Aa2/NR/NR

|

1,303,087 | ||||||

8

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School Districts (continued)

|

|||||||||

|

Gunnison Watershed, Colorado School District

|

|||||||||

| $ | 1,025,000 |

5.250%, 12/01/26

|

Aa2/AA-/NR

|

$ | 1,174,732 | ||||

|

Jefferson County, Colorado School District #R-001

|

|||||||||

| 3,000,000 |

5.250%, 12/15/25 AGMC Insured

|

Aa2/AA-/NR

|

3,374,010 | ||||||

|

La Plata County, Colorado School District #9

|

|||||||||

| 1,500,000 |

5.000%, 11/01/18 NPFG Insured Pre-Refunded

|

NR/NR/NR*

|

1,558,095 | ||||||

|

La Plata County, Colorado School District #9-R

|

|||||||||

|

Durango Refunding

|

|||||||||

| 3,000,000 |

4.500%, 11/01/23

|

Aa2/NR/NR

|

3,477,090 | ||||||

|

Teller County, Colorado School District #2

|

|||||||||

|

Woodland Park

|

|||||||||

| 1,265,000 |

5.000%, 12/01/17 NPFG Insured Pre-Refunded

|

Aa2/AA-/NR

|

1,423,909 | ||||||

|

Weld County, Colorado School District #2

|

|||||||||

| 1,315,000 |

5.000%, 12/01/15 AGMC Insured

|

Aa2/AA-/NR

|

1,364,852 | ||||||

|

Weld County, Colorado School District #8

|

|||||||||

| 1,115,000 |

5.000%, 12/01/15 AGMC Insured Pre-Refunded

|

Aa2/AA-/NR

|

1,162,878 | ||||||

| 1,385,000 |

5.250%, 12/01/17 AGMC Insured Pre-Refunded

|

Aa2/AA-/NR

|

1,447,602 | ||||||

|

Total School Districts

|

42,532,877 | ||||||||

|

Total General Obligation Bonds

|

61,471,224 | ||||||||

|

Revenue Bonds (76.3%)

|

|||||||||

|

Airport (3.7%)

|

|||||||||

|

Denver, Colorado City & County Airport Revenue

|

|||||||||

|

System, Series A

|

|||||||||

| 1,210,000 |

5.250%, 11/15/28

|

A1/A+/A+

|

1,338,599 | ||||||

| 3,000,000 |

5.250%, 11/15/29

|

A1/A+/A+

|

3,297,360 | ||||||

|

Denver, Colorado City & County Airport Revenue

|

|||||||||

|

System, Series A Refunding

|

|||||||||

| 4,340,000 |

5.000%, 11/15/24

|

A1/A+/A+

|

4,870,782 | ||||||

|

Walker Field, Colorado Public Airport Authority

|

|||||||||

|

Airport Revenue

|

|||||||||

| 1,000,000 |

5.000%, 12/01/22

|

Baa2/NR/NR

|

1,016,820 | ||||||

|

Total Airport

|

10,523,561 | ||||||||

9

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Electric (3.1%)

|

|||||||||

|

Colorado Springs, Colorado Utilities Revenue

|

|||||||||

| $ | 1,660,000 |

5.000%, 11/15/17 Pre-Refunded

|

Aa2/AA/NR

|

$ | 1,728,077 | ||||

|

Colorado Springs, Colorado Utilities Revenue,

|

|||||||||

|

Refunding Series A

|

|||||||||

| 2,000,000 |

4.750%, 11/15/27

|

Aa2/AA/AA

|

2,202,200 | ||||||

|

Colorado Springs, Colorado Utilities Revenue,

|

|||||||||

|

Refunding Series A-1

|

|||||||||

| 1,000,000 |

4.000%, 11/15/26

|

Aa2/AA/AA

|

1,062,860 | ||||||

| 1,000,000 |

4.000%, 11/15/27

|

Aa2/AA/AA

|

1,051,010 | ||||||

|

Colorado Springs, Colorado Utilities Revenue

|

|||||||||

|

Refunding Series B

|

|||||||||

| 1,285,000 |

5.250%, 11/15/23

|

Aa2/AA/AA

|

1,506,495 | ||||||

|

Colorado Springs, Colorado Utilities Revenue

|

|||||||||

|

Subordinated Lien Improvement Series B

|

|||||||||

| 1,160,000 |

5.000%, 11/15/23

|

Aa2/AA/AA

|

1,242,882 | ||||||

|

Total Electric

|

8,793,524 | ||||||||

|

Higher Education (23.6%)

|

|||||||||

|

Adams State College, Colorado Auxiliary Facilities

|

|||||||||

|

Revenue Improvement Series A

|

|||||||||

| 1,000,000 |

5.200%, 05/15/27

|

Aa2/AA-/NR

|

1,110,120 | ||||||

|

Adams State College, Colorado Auxiliary Facilities

|

|||||||||

|

Revenue Refunding, Series B

|

|||||||||

| 3,000,000 |

4.500%, 05/15/29

|

Aa2/AA-/NR

|

3,159,240 | ||||||

|

Boulder, Colorado Development Revenue UCAR

|

|||||||||

| 1,880,000 |

5.000%, 09/01/27 NPFG Insured

|

A2/A+/NR

|

1,895,115 | ||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

Regis University Project

|

|||||||||

| 1,695,000 |

5.000%, 06/01/24 Radian Insured Pre-Refunded

|

NR/BBB/NR

|

1,872,416 | ||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

Student Housing - Campus Village Apartments

|

|||||||||

|

Refunding

|

|||||||||

| 2,935,000 |

5.375%, 06/01/28

|

NR/A/NR

|

3,052,517 | ||||||

10

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Higher Education (continued)

|

|||||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

University Corp. Atmosphere Project, Refunding

|

|||||||||

| $ | 1,700,000 |

5.000%, 09/01/22

|

A2/A+/NR

|

$ | 1,935,195 | ||||

| 1,635,000 |

5.000%, 09/01/28

|

A2/A+/NR

|

1,762,219 | ||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

University of Colorado Foundation Project

|

|||||||||

| 2,110,000 |

5.000%, 07/01/17 AMBAC Insured Pre-Refunded

|

NR/NR/NR*

|

2,157,032 | ||||||

| 1,865,000 |

5.375%, 07/01/18 AMBAC Insured Pre-Refunded

|

NR/NR/NR*

|

1,909,984 | ||||||

|

Colorado Educational & Cultural Facility Authority

|

|||||||||

|

Revenue Refunding, University of Denver Project

|

|||||||||

| 1,000,000 |

5.250%, 03/01/26 NPFG Insured

|

A1/A+/NR

|

1,171,970 | ||||||

|

Colorado Educational & Cultural Facility Authority

|

|||||||||

|

Revenue Refunding, University of Denver Project,

|

|||||||||

|

Series B

|

|||||||||

| 3,085,000 |

5.000%, 03/01/22 NPFG-FGIC Insured

|

A1/A+/NR

|

3,373,478 | ||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

University of Denver Project, Series B Refunding

|

|||||||||

| 3,620,000 |

5.250%, 03/01/23 NPFG Insured

|

A1/A+/AA

|

3,980,443 | ||||||

|

Colorado Mountain Jr. College District Student

|

|||||||||

|

Housing Facilities Enterprise

|

|||||||||

| 1,000,000 |

4.500%, 06/01/18 NPFG Insured

|

Baa2/BBB/NR

|

1,025,760 | ||||||

| 1,825,000 |

5.000%, 06/01/23 NPFG Insured

|

Baa2/BBB/NR

|

1,856,883 | ||||||

|

Colorado School of Mines Enterprise Refunding &

|

|||||||||

|

Improvement

|

|||||||||

| 1,455,000 |

5.000%, 12/01/24

|

Aa2/AA-/NR

|

1,621,801 | ||||||

|

Colorado State Board of Governors University

|

|||||||||

|

Enterprise System, Series A, Refunding and

|

|||||||||

|

Improvement

|

|||||||||

| 425,000 |

5.000%, 03/01/17 Pre-Refunded

|

Aa3/NR/NR

|

447,971 | ||||||

| 1,105,000 |

5.000%, 03/01/17 AMBAC Insured

|

Aa3/NR/NR

|

1,151,200 | ||||||

|

Colorado State Board of Governors University

|

|||||||||

|

Enterprise System, Series A

|

|||||||||

| 930,000 |

5.000%, 03/01/28 AGMC Insured

|

Aa3/AA-/NR

|

1,013,058 | ||||||

11

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Higher Education (continued)

|

|||||||||

|

Colorado State COP University of Colorado at

|

|||||||||

|

Denver Health Sciences Center Fitzsimons

|

|||||||||

|

Academic Projects Series B

|

|||||||||

| $ | 3,135,000 |

5.250%, 11/01/25 NPFG Pre-Refunded

|

Baa2/AA-/NR

|

$ | 3,651,366 | ||||

|

Mesa State College, Colorado Auxiliary Facilities

|

|||||||||

|

Enterprise

|

|||||||||

| 1,000,000 |

5.000%, 05/15/20 Syncora Guarantee, Inc. Insured

|

A2/NR/NR

|

1,056,890 | ||||||

|

Mesa State College, Colorado Auxiliary Facilities

|

|||||||||

|

Enterprise

|

|||||||||

| 2,000,000 |

5.700%, 05/15/26 Pre-Refunded

|

NR/AA-/NR

|

2,539,000 | ||||||

|

University of Colorado Enterprise System

|

|||||||||

| 2,325,000 |

5.000%, 06/01/15 AMBAC Insured Pre-Refunded

|

Aa2/AA-/NR

|

2,369,919 | ||||||

| 1,735,000 |

5.000%, 06/01/16 Pre-Refunded

|

Aa2/AA-/AAA

|

1,848,018 | ||||||

| 1,000,000 |

5.250%, 06/01/17 NPFG Insured Pre-Refunded

|

Aa2/AA-/NR

|

1,068,640 | ||||||

| 2,000,000 |

5.000%, 06/01/27

|

Aa2/AA-/AA+

|

2,280,900 | ||||||

| 2,000,000 |

4.750%, 06/01/27 Series A

|

Aa2/NR/AA+

|

2,236,220 | ||||||

|

University of Colorado Enterprise System, Refunding,

|

|||||||||

|

Series B

|

|||||||||

| 1,680,000 |

4.000%, 06/01/23

|

Aa2/AA-/AA+

|

1,849,865 | ||||||

|

University of Colorado Enterprise System, Refunding

|

|||||||||

|

& Improvement

|

|||||||||

| 3,905,000 |

5.000%, 06/01/24 NPFG Insured

|

Aa2/AA-/AA+

|

4,303,661 | ||||||

|

University of Northern Colorado Greeley Institutional

|

|||||||||

|

Enterprise Refunding, SHEIP, Series A

|

|||||||||

| 2,810,000 |

5.000%, 06/01/26

|

Aa2/AA-/NR

|

3,198,370 | ||||||

| 2,940,000 |

5.000%, 06/01/28

|

Aa2/AA-/NR

|

3,295,740 | ||||||

|

University of Northern Colorado Refunding

|

|||||||||

| 1,000,000 |

5.000%, 06/01/24 AGMC Insured

|

Aa3/AA-/NR

|

1,059,600 | ||||||

|

Western State College, Colorado Institutional

|

|||||||||

|

Enterprise, SHEIP, Series A

|

|||||||||

| 1,160,000 |

5.000%, 05/15/24 Insured

|

Aa2/AA-/NR

|

1,312,981 | ||||||

|

Western State College, Colorado, SHEIP

|

|||||||||

| 1,020,000 |

5.000%, 05/15/27

|

Aa2/AA-/NR

|

1,133,873 | ||||||

|

Total Higher Education

|

67,701,445 | ||||||||

12

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Hospital (10.7%)

|

|||||||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

Adventist Health/Sunbelt, Refunding

|

|||||||||

| $ | 2,500,000 |

5.125%, 11/15/29

|

Aa3/AA-/AA-

|

$ | 2,614,025 | ||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

Catholic Health

|

|||||||||

| 1,000,000 |

4.750%, 09/01/25 AGMC Insured

|

Aa2/AA/AA

|

1,054,620 | ||||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

Evangelical Lutheran Project Refunding

|

|||||||||

| 1,575,000 |

5.250%, 06/01/19

|

A3/A-/NR

|

1,689,896 | ||||||

| 1,000,000 |

5.250%, 06/01/21

|

A3/A-/NR

|

1,056,200 | ||||||

| 2,000,000 |

5.250%, 06/01/24

|

A3/A-/NR

|

2,076,240 | ||||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

NCMC, Inc., Project

|

|||||||||

| 2,000,000 |

5.250%, 05/15/26 Series A AGMC Insured

|

NR/AA-/A+

|

2,194,020 | ||||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

Poudre Valley Health Care Series F Refunding

|

|||||||||

| 4,760,000 |

5.000%, 03/01/25

|

A2/A/NR

|

4,848,631 | ||||||

|

Colorado Health Facility Authority Hospital Revenue

|

|||||||||

|

Refunding, Catholic Health, Series A

|

|||||||||

| 2,000,000 |

5.250%, 07/01/24

|

Aa2/AA/AA

|

2,235,800 | ||||||

|

Colorado Health Facility Authority Hospital Revenue,

|

|||||||||

|

Valley View Hospital Association, Refunding

|

|||||||||

| 1,500,000 |

5.500%, 05/15/28

|

NR/BBB+/NR

|

1,537,875 | ||||||

|

Colorado Health Facility Authority, Catholic Health

|

|||||||||

|

Initiatives, Series D

|

|||||||||

| 2,000,000 |

5.000%, 10/01/16

|

Aa2/AA/AA

|

2,295,300 | ||||||

| 1,000,000 |

6.000%, 10/01/23

|

Aa2/AA/AA

|

1,180,420 | ||||||

|

Colorado Health Facility Authority, Sisters

|

|||||||||

|

Leavenworth, Refunding

|

|||||||||

| 3,000,000 |

5.250%, 01/01/25

|

Aa3/AA/AA-

|

3,306,000 | ||||||

|

Denver, Colorado Health & Hospital Authority

|

|||||||||

|

Healthcare, Series A Refunding

|

|||||||||

| 2,000,000 |

5.000%, 12/01/18

|

NR/BBB/BBB+

|

2,115,600 | ||||||

| 1,500,000 |

5.000%, 12/01/19

|

NR/BBB/BBB+

|

1,562,760 | ||||||

13

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Hospital (continued)

|

|||||||||

|

Park Hospital District Larimer County, Colorado

|

|||||||||

|

Limited Tax Revenue

|

|||||||||

| $ | 1,010,000 |

4.500%, 01/01/21 AGMC Insured

|

Aa3/AA-/NR

|

$ | 1,057,642 | ||||

|

Total Hospital

|

30,825,029 | ||||||||

|

Housing (1.5%)

|

|||||||||

|

Colorado Housing & Finance Authority

|

|||||||||

| 130,000 |

6.050%, 10/01/16 Series 1999A3

|

Aa2/NR/NR

|

133,488 | ||||||

|

Colorado Housing & Finance Authority, Single

|

|||||||||

|

Family Program Refunding Series B

|

|||||||||

| 45,000 |

5.000%, 08/01/13 Series 2001

|

A1/A+/NR

|

44,971 | ||||||

|

Colorado Housing Finance Authority, Single Family

|

|||||||||

|

Mortgage

|

|||||||||

| 10,000 |

5.700%, 10/01/22 Series 2000C3

|

Aa2/AA/NR

|

10,170 | ||||||

|

Colorado Housing & Finance Authority, Single Family

|

|||||||||

|

Mortgage Class II

|

|||||||||

| 795,000 |

5.500%, 11/01/29

|

Aaa/AAA/NR

|

817,896 | ||||||

|

Colorado Housing Finance Authority, Single Family

|

|||||||||

|

Mortgage Class III Series A-5

|

|||||||||

| 2,495,000 |

5.000%, 11/01/34

|

A2/A+/NR

|

2,502,211 | ||||||

|

Colorado Housing Finance Authority, Single Family

|

|||||||||

|

Mortgage Subordinated

|

|||||||||

| 10,000 |

5.400%, 10/01/12 Series 2000D

|

A1/A+/NR

|

10,053 | ||||||

|

Colorado Housing and Finance Authority, Multi-

|

|||||||||

|

Family Project C1-II Series A-2

|

|||||||||

| 870,000 |

5.400%, 10/01/29

|

Aa2/AA/NR

|

9 11,830 | ||||||

|

Total Housing

|

4,430,619 | ||||||||

|

Lease (18.3%)

|

|||||||||

|

Adams 12 Five Star Schools, Colorado COP

|

|||||||||

| 1,770,000 |

4.625%, 12/01/24

|

Aa3/A+/NR

|

1,903,529 | ||||||

| 500,000 |

5.000%, 12/01/25

|

Aa3/A+/NR

|

544,040 | ||||||

|

Adams County, Colorado Corrections Facility COP,

|

|||||||||

|

Series B

|

|||||||||

| 1,600,000 |

5.000%, 12/01/26

|

Aa2/AA/NR

|

1,732,768 | ||||||

| 1,200,000 |

5.125%, 12/01/27

|

Aa2/AA/NR

|

1,301,040 | ||||||

14

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Lease (continued)

|

|||||||||

|

Aurora, Colorado COP, Refunding Series A

|

|||||||||

| $ | 1,500,000 |

5.000%, 12/01/26

|

Aa2/AA-/NR

|

$ | 1,667,295 | ||||

|

Brighton, Colorado COP Refunding Series A

|

|||||||||

| 1,865,000 |

5.000%, 12/01/24 AGMC Insured

|

Aa3/AA-/NR

|

2,080,426 | ||||||

|

Broomfield, Colorado COP

|

|||||||||

| 2,000,000 |

4.500%, 12/01/28

|

Aa3/NR/NR

|

2,128,200 | ||||||

|

Colorado Educational & Cultural Facilities Authority,

|

|||||||||

|

Aurora Academy Project

|

|||||||||

| 1,255,000 |

5.250%, 02/15/24 Syncora Guarantee, Inc. Insured

|

NR/A/NR

|

1,257,159 | ||||||

|

Colorado Educational & Cultural Facilities Authority,

|

|||||||||

|

Ave Maria School Project Refunding

|

|||||||||

| 1,000,000 |

4.850%, 12/01/25 Radian Insured

|

NR/NR/NR*

|

941,050 | ||||||

|

Colorado Educational & Cultural Facilities Authority,

|

|||||||||

|

Charter School - James, Refunding & Improvement

|

|||||||||

| 3,000,000 |

5.000%, 08/01/27 AGC Insured

|

NR/AA-/NR

|

3,031,830 | ||||||

|

Colorado Educational & Cultural Facilities Authority,

|

|||||||||

|

Peak to Peak Charter School, Refunding

|

|||||||||

| 1,500,000 |

5.250%, 08/15/24 Syncora Guarantee, Inc. Insured

|

NR/A/NR

|

1,514,100 | ||||||

|

Colorado State BEST COP Series G

|

|||||||||

| 3,000,000 |

4.250%, 03/15/23

|

Aa2/AA-/NR

|

3,324,690 | ||||||

|

Colorado State Higher Education Capital

|

|||||||||

|

Construction Lease

|

|||||||||

| 3,000,000 |

5.250%, 11/01/23

|

Aa2/AA-/NR

|

3,374,100 | ||||||

| 1,690,000 |

5.000%, 11/01/26

|

Aa2/AA-/NR

|

1,911,965 | ||||||

|

Denver, Colorado City and County COP (Botanical

|

|||||||||

|

Gardens)

|

|||||||||

| 2,015,000 |

5.250%, 12/01/22

|

Aa2/AA+/AA+

|

2,335,304 | ||||||

|

Douglas County, Colorado School District No. RE-1

|

|||||||||

|

Douglas & Elbert Counties COP

|

|||||||||

| 3,075,000 |

5.000%, 01/15/29

|

Aa2/NR/NR

|

3,316,418 | ||||||

|

El Paso County, Colorado COP (Judicial Complex

|

|||||||||

|

Project) Series A

|

|||||||||

| 1,820,000 |

4.500%, 12/01/26 AMBAC Insured

|

NR/AA-/NR

|

1,888,723 | ||||||

15

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Lease (continued)

|

|||||||||

|

El Paso County, Colorado COP (Pikes Peak Regional

|

|||||||||

|

Development Authority)

|

|||||||||

| $ | 1,925,000 |

5.000%, 12/01/18 AMBAC Insured

|

NR/AA-/NR

|

$ | 2,058,595 | ||||

|

Fort Collins, Colorado Lease COP Series A

|

|||||||||

| 3,020,000 |

4.750%, 06/01/18 AMBAC Insured

|

Aa1/NR/NR

|

3,273,438 | ||||||

|

Fremont County, Colorado COP Refunding &

|

|||||||||

|

Improvement Series A

|

|||||||||

| 2,075,000 |

5.000%, 12/15/18 NPFG Insured

|

Baa2/BBB/NR

|

2,153,975 | ||||||

|

Garfield County, Colorado COP Public Library

|

|||||||||

|

District

|

|||||||||

| 1,000,000 |

5.375%, 12/01/27

|

NR/A/NR

|

1,079,010 | ||||||

|

Gypsum, Colorado COP

|

|||||||||

| 1,050,000 |

5.000%, 12/01/28

|

NR/A+/NR

|

1,108,664 | ||||||

|

Northern Colorado Water Conservancy District COP

|

|||||||||

| 1,000,000 |

5.000%, 10/01/15 NPFG Insured

|

Baa2/AA-/NR

|

1,019,630 | ||||||

|

Pueblo, Colorado COP (Police Complex Project)

|

|||||||||

| 2,170,000 |

5.500%, 08/15/22 AGMC Insured

|

Aa3/AA-/NR

|

2,491,659 | ||||||

|

Rangeview Library District Project, Colorado COP

|

|||||||||

| 2,210,000 |

5.000%, 12/15/26 AGMC Insured

|

Aa3/AA-/NR

|

2,387,286 | ||||||

| 1,000,000 |

5.000%, 12/15/28 AGMC Insured

|

Aa3/AA-/NR

|

1,066,960 | ||||||

|

Westminster, Colorado COP

|

|||||||||

| 1,480,000 |

4.250%, 12/01/22 AGMC Insured

|

Aa3/AA-/NR

|

1,622,391 | ||||||

|

Total Lease

|

52,514,245 | ||||||||

|

Sales Tax (5.4%)

|

|||||||||

|

Boulder, Colorado Open Space Capital Improvement

|

|||||||||

| 1,630,000 |

5.000%, 07/15/17 NPFG Insured Pre-Refunded

|

Aa1/AA/NR

|

1,670,978 | ||||||

|

Boulder County, Colorado Open Space Capital

|

|||||||||

|

Improvement Series A

|

|||||||||

| 1,500,000 |

5.000%, 01/01/24 AGMC Insured Pre-Refunded

|

Aa3/AA/NR

|

1,693,305 | ||||||

|

Commerce City, Colorado Sales & Use Tax Revenue

|

|||||||||

| 1,000,000 |

5.000%, 08/01/21 AMBAC Insured

|

NR/A+/NR

|

1,090,190 | ||||||

|

Denver, Colorado City & County Excise Tax Revenue

|

|||||||||

|

Refunding Series A

|

|||||||||

| 4,000,000 |

5.250%, 09/01/19 AGMC Insured

|

Aa3/AA-/AA-

|

4,867,720 | ||||||

16

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Sales Tax (continued)

|

|||||||||

|

Gypsum County, Colorado Sales Tax & General Fund

|

|||||||||

|

Revenue

|

|||||||||

| $ | 1,690,000 |

5.250%, 06/01/30 AGMC Insured

|

NR/AA-/NR

|

$ | 1,769,177 | ||||

|

Park Meadows Business Implementation District,

|

|||||||||

|

Colorado Shared Sales Tax Revenue

|

|||||||||

| 1,500,000 |

5.300%, 12/01/27

|

NR/NR/NR*

|

1,401,990 | ||||||

|

Pueblo, Colorado Urban Renewal Authority,

|

|||||||||

|

Refunding & Improvement, Series B

|

|||||||||

| 1,250,000 |

5.250%, 12/01/28

|

A2/A/NR

|

1,378,863 | ||||||

|

Steamboat Springs, Colorado Redevelopment

|

|||||||||

|

Authority Tax Increment Refunding &

|

|||||||||

|

Improvement, Base Area Redevelopment Project

|

|||||||||

| 1,575,000 |

4.500%, 12/01/26

|

A1/NR/NR

|

1,703,347 | ||||||

|

Total Sales Tax

|

15,575,570 | ||||||||

|

Transportation (1.3%)

|

|||||||||

|

Regional Transportation District, Colorado COP,

|

|||||||||

|

Series A

|

|||||||||

| 3,500,000 |

5.000%, 06/01/25 AMBAC Insured

|

Aa3/A-/AA-

|

3,655,610 | ||||||

|

Water & Sewer (6.7%)

|

|||||||||

|

Aurora, Colorado Water Improvement Revenue First

|

|||||||||

|

Lien, Series A

|

|||||||||

| 1,250,000 |

5.000%, 08/01/25 AMBAC Insured

|

Aa2/NR/AA

|

1,387,537 | ||||||

|

Broomfield, Colorado Sewer and Waste Water

|

|||||||||

|

Revenue

|

|||||||||

| 1,985,000 |

5.000%, 12/01/15 AMBAC Insured

|

A1/NR/NR

|

2,010,229 | ||||||

|

Broomfield, Colorado Water Activity Enterprise

|

|||||||||

| 1,500,000 |

5.300%, 12/01/12 NPFG Insured

|

A1/NR/NR

|

1,512,780 | ||||||

| 1,730,000 |

5.250%, 12/01/13 NPFG Insured

|

A1/NR/NR

|

1,744,411 | ||||||

|

Colorado Water Resource & Power Development

|

|||||||||

|

Authority

|

|||||||||

| 2,675,000 |

5.000%, 09/01/16 NPFG Insured

|

Baa2/BBB/NR

|

2,856,365 | ||||||

| 1,855,000 |

5.000%, 09/01/17 NPFG Insured

|

Baa2/BBB/NR

|

1,971,902 | ||||||

17

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

|

Rating

|

|||||||||

|

Moody’s, S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Water & Sewer (continued)

|

|||||||||

|

Colorado Water Resource & Power Development

|

|||||||||

|

Authority Clean Water Revenue Series A

|

|||||||||

| $ | 260,000 |

5.000%, 09/01/12 Un-Refunded portion

|

Aaa/AAA/AAA | $ | 260,850 | ||||

|

Denver, Colorado City and County Wastewater

|

|||||||||

|

Revenue

|

|||||||||

| 1,560,000 |

5.000%, 11/01/15 NPFG Insured

|

Aa2/AAA/AAA

|

1,616,987 | ||||||

|

Erie, Colorado Water Enterprise Revenue, Series A

|

|||||||||

| 1,000,000 |

5.000%, 12/01/25 AGMC Insured

|

Aa3/NR/NR

|

1,102,920 | ||||||

|

Greeley, Colorado Water Revenue

|

|||||||||

| 1,920,000 |

4.200%, 08/01/24 NPFG Insured

|

Aa2/AA-/NR

|

2,014,368 | ||||||

|

Woodmoor, Colorado Water & Sanitation District #1

|

|||||||||

|

Enterprise

|

|||||||||

| 2,570,000 |

4.500%, 12/01/26

|

NR/AA-/NR

|

2,833,271 | ||||||

|

Total Water & Sewer

|

19,311,620 | ||||||||

|

Miscellaneous Revenue (2.0%)

|

|||||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

Independent School Revenue Refunding, Kent

|

|||||||||

|

Denver School Project

|

|||||||||

| 1,000,000 |

5.000%, 10/01/30

|

NR/A-/NR

|

1,054,360 | ||||||

|

Colorado Educational & Cultural Facility Authority,

|

|||||||||

|

Independent School Revenue Refunding, Vail

|

|||||||||

|

Mountain School Project

|

|||||||||

| 1,820,000 |

6.000%, 05/01/30

|

NR/BBB-/NR

|

1,856,819 | ||||||

|

Colorado Educational & Cultural Facility Authority

|

|||||||||

|

Revenue Charter School, Colorado Springs

|

|||||||||

|

Charter Academy

|

|||||||||

| 2,915,000 |

5.250%, 07/01/28

|

NR/A/NR

|

2,809,098 | ||||||

|

Total Miscellaneous Revenue

|

5,720,277 | ||||||||

|

Total Revenue Bonds

|

219,051,500 | ||||||||

|

Total Investments (cost $264,939,696 – note 4)

|

97.7%

|

280,522,724 | |||||||

|

Other assets less liabilities

|

2.3

|

6,489,794 | |||||||

|

Net Assets

|

100.0%

|

$ | 287,012,518 | ||||||

18

TAX-FREE FUND OF COLORADO

SCHEDULE OF INVESTMENTS (continued)

DECEMBER 31, 2011

| * |

Any security not rated (NR) by any of the Nationally Recognized Statistical Rating Organizations (“NRSRO” or credit rating agency) has been determined by the Investment Sub-Adviser to have sufficient quality to be ranked in the top four credit ratings if a credit rating were to be assigned by a NRSRO.

|

||||

|

|

|||||

|

Percent of

|

|||||

|

Portfolio Distribution By Quality Rating (unaudited)

|

Investments1

|

||||

|

Aaa of Moody’s or AAA of S&P or Fitch

|

1.0 | % | |||

|

Pre-Refunded Bonds2/Escrowed to Maturity Bonds

|

12.8 | ||||

|

Aa of Moody’s or AA of S&P or Fitch

|

55.4 | ||||

|

A of Moody’s or S&P or Fitch

|

21.2 | ||||

|

Baa of Moody’s or BBB of S&P or Fitch

|

8.5 | ||||

|

Not rated*

|

1.1 | ||||

| 100.0 | % | ||||

| 1 |

Where applicable, calculated using the highest rating of the three NRSROs.

|

||||

| 2 |

Pre-refunded bonds are bonds for which U.S. Govenment Obligations have been placed in escrow to retire the bonds at their earliest call date.

|

||||

|

PORTFOLIO ABBREVIATIONS:

|

|||||

|

ACA - American Capital Assurance Financial Guaranty Corp.

|

|||||

|

AGC - Assured Guaranty Corp.

|

|||||

|

AGMC - Assured Guaranty Municipal Corp.

|

|||||

|

AMBAC - American Municipal Bond Assurance Corp.

|

|||||

|

BEST - Building Excellent Schools Today

|

|||||

|

COP - Certificates of Participation

|

|||||

|

FGIC - Financial Guaranty Insurance Co.

|

|||||

|

NPFG - National Public Finance Guarantee

|

|||||

|

NR - Not Rated

|

|||||

|

SHEIP - State Higher Education Intercept Program

|

|||||

|

UCAR - University Corporation for Atmospheric Research

|

|||||

See accompanying notes to financial statements.

19

TAX-FREE FUND OF COLORADO

STATEMENT OF ASSETS AND LIABILITIES

DECEMBER 31, 2011

|

ASSETS

|

||||

|

Investments at value (cost $264,939,696)

|

$ | 280,522,724 | ||

|

Cash

|

4,338,767 | |||

|

Interest receivable

|

2,235,069 | |||

|

Receivable for Fund shares sold

|

564,016 | |||

|

Other assets

|

13,683 | |||

|

Total assets

|

287,674,259 | |||

|

LIABILITIES

|

||||

|

Dividends payable

|

337,032 | |||

|

Management fee payable

|

120,143 | |||

|

Payable for Fund shares redeemed

|

111,050 | |||

|

Distribution and service fees payable

|

3,310 | |||

|

Accrued expenses

|

90,206 | |||

|

Total liabilities

|

661,741 | |||

|

NET ASSETS

|

$ | 287,012,518 | ||

|

Net Assets consist of:

|

||||

|

Capital Stock - Authorized an unlimited number of shares, par value $0.01 per share.

|

$ | 269,951 | ||

|

Additional paid-in capital

|

271,941,338 | |||

|

Net unrealized appreciation on investments (note 4)

|

15,583,028 | |||

|

Accumulated net realized loss on investments

|

(831,704 | ) | ||

|

Undistributed net investment income

|

49,905 | |||

| $ | 287,012,518 | |||

|

CLASS A

|

||||

|

Net Assets

|

$ | 221,007,077 | ||

|

Capital shares outstanding

|

20,789,174 | |||

|

Net asset value and redemption price per share

|

$ | 10.63 | ||

|

Maximum offering price per share (100/96 of $10.63 adjusted to nearest cent)

|

$ | 11.07 | ||

|

CLASS C

|

||||

|

Net Assets

|

$ | 29,321,375 | ||

|

Capital shares outstanding

|

2,763,477 | |||

|

Net asset value and offering price per share

|

$ | 10.61 | ||

|

Redemption price per share (*a charge of 1% is imposed on the redemption

|

||||

|

proceeds of the shares, or on the original price, whichever is lower, if redeemed

|

||||

|

during the first 12 months after purchase)

|

$ | 10.61 | * | |

|

CLASS Y

|

||||

|

Net Assets

|

$ | 36,684,066 | ||

|

Capital shares outstanding

|

3,442,481 | |||

|

Net asset value, offering and redemption price per share

|

$ | 10.66 | ||

See accompanying notes to financial statements.

20

TAX-FREE FUND OF COLORADO

STATEMENT OF OPERATIONS

YEAR ENDED DECEMBER 31, 2011

|

Investment Income:

|

||||||||

|

Interest income

|

$ | 12,228,499 | ||||||

|

Expenses:

|

||||||||

|

Management fee (note 3)

|

$ | 1,359,990 | ||||||

|

Distribution and service fees (note 3)

|

365,023 | |||||||

|

Transfer and shareholder servicing agent fees

|

165,851 | |||||||

|

Trustees’ fees and expenses (note 8)

|

121,567 | |||||||

|

Legal fees (note 3)

|

89,490 | |||||||

|

Shareholders’ reports and proxy statements

|

51,538 | |||||||

|

Custodian fees (note 6)

|

24,576 | |||||||

|

Auditing and tax fees

|

21,850 | |||||||

|

Registration fees and dues

|

17,449 | |||||||

|

Insurance

|

13,260 | |||||||

|

Chief compliance officer services (note 3)

|

4,508 | |||||||

|

Miscellaneous

|

32,968 | |||||||

|

Total expenses

|

2,268,070 | |||||||

|

Expenses paid indirectly (note 6)

|

( 40 | ) | ||||||

|

Net expenses

|

2,268,030 | |||||||

|

Net investment income

|

9,960,469 | |||||||

|

Realized and Unrealized Gain (Loss) on Investments:

|

||||||||

|

Net realized gain (loss) from securities transactions

|

(776,492 | ) | ||||||

|

Change in unrealized appreciation on investments

|

13,671,367 | |||||||

|

Net realized and unrealized gain (loss) on investments

|

12,894,875 | |||||||

|

Net change in net assets resulting from operations

|

$ | 22,855,344 | ||||||

See accompanying notes to financial statements.

21

TAX-FREE FUND OF COLORADO

STATEMENTS OF CHANGES IN NET ASSETS

|

Year Ended

|

Year Ended

|

|||||||

|

December 31, 2011

|

December 31, 2010

|

|||||||

|

OPERATIONS:

|

||||||||

|

Net investment income

|

$ | 9,960,469 | $ | 10,512,273 | ||||

|

Net realized gain (loss) from securities transactions

|

(776,492 | ) | 346,685 | |||||

|

Change in unrealized appreciation (depreciation) on investments

|

13,671,367 | (7,701,088 | ) | |||||

|

Change in net assets from operations

|

22,855,344 | 3,157,870 | ||||||

|

DISTRIBUTIONS TO SHAREHOLDERS (note 10):

|

||||||||

|

Class A Shares:

|

||||||||

|

Net investment income

|

(7,925,888 | ) | (8,352,842 | ) | ||||

|

Class C Shares:

|

||||||||

|

Net investment income

|

(720,167 | ) | (655,304 | ) | ||||

|

Class Y Shares:

|

||||||||

|

Net investment income

|

(1,297,116 | ) | (1,512,329 | ) | ||||

|

Change in net assets from distributions

|

(9,943,171 | ) | (10,520,475 | ) | ||||

|

CAPITAL SHARE TRANSACTIONS (note 7):

|

||||||||

|

Proceeds from shares sold

|

47,054,769 | 79,757,891 | ||||||

|

Reinvested dividends and distributions

|

6,118,139 | 6,242,951 | ||||||

|

Cost of shares redeemed

|

(52,115,529 | ) | (56,440,080 | ) | ||||

|

Change in net assets from capital share transactions

|

1,057,379 | 29,560,762 | ||||||

|

Change in net assets

|

13,969,552 | 22,198,157 | ||||||

|

NET ASSETS:

|

||||||||

|

Beginning of period

|

273,042,966 | 250,844,809 | ||||||

|

End of period*

|

$ | 287,012,518 | $ | 273,042,966 | ||||

|

* Includes undistributed net investment income of:

|

$ | 49,905 | $ | 33,284 | ||||

See accompanying notes to financial statements.

22

TAX-FREE FUND OF COLORADO

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2011

1. Organization

Tax-Free Fund of Colorado (the “Fund”), a non-diversified, open-end investment company, was organized in February, 1987 as a Massachusetts business trust and commenced operations on May 21, 1987. The Fund is authorized to issue an unlimited number of shares and, since its inception to April 30, 1996, offered only one class of shares. On that date, the Fund began offering two additional classes of shares, Class C and Class Y Shares. All shares outstanding prior to that date were designated as Class A Shares and are sold at net asset value plus a sales charge of varying size (depending upon a variety of factors) paid at the time of purchase and bear a distribution fee. Class C Shares are sold at net asset value with no sales charge payable at the time of purchase but with a level charge for service and distribution fees for six years thereafter. Class C Shares automatically convert to Class A Shares after six years. Class Y Shares are sold only through institutions acting for investors in a fiduciary, advisory, agency, custodial or similar capacity, and are not offered directly to retail customers. Class Y Shares are sold at net asset value with no sales charge, no redemption fee, no contingent deferred sales charge (“CDSC”) and no distribution fee. On April 30, 1998, the Fund established Class I Shares which are offered and sold only through financial intermediaries and are not offered directly to retail customers. Class I Shares are sold at net asset value with no sales charge and no redemption fee or CDSC, although a financial intermediary may charge a fee for effecting a purchase or other transaction on behalf of its customers. Class I Shares may carry a distribution and a service fee. As of the report date, there were no Class I Shares outstanding. All classes of shares represent interests in the same portfolio of investments and are identical as to rights and privileges but differ with respect to the effect of sales charges, the distribution and/or service fees borne by each class, expenses specific to each class, voting rights on matters affecting a single class and the exchange privileges of each class.

2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America for investment companies.

|

a)

|

Portfolio valuation: Municipal securities which have remaining maturities of more than 60 days are valued each business day based upon information provided by a nationally prominent independent pricing service and periodically verified through other pricing services. In the case of securities for which market quotations are readily available, securities are valued by the pricing service at the mean of bid and asked quotations. If a market quotation or a valuation from the pricing service is not readily available, the security is valued at fair value determined in good faith under procedures established by and under the general supervision of the Board of Trustees. Securities which mature in 60 days or less are valued at amortized cost if their term to maturity at purchase is 60 days or less, or by amortizing their unrealized appreciation or depreciation on the 61st day prior to maturity, if their term to maturity at purchase exceeds 60 days.

|

|

b)

|

Fair Value Measurements: The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions

|

23

TAX-FREE FUND OF COLORADO

NOTES TO FINANCIAL STATEMENTS (continued)

DECEMBER 31, 2011

(unobservable inputs). These inputs are used in determining the value of the Fund’s investments and are summarized in the following fair value hierarchy:

Level 1 – Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, based on the best information available.

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the valuation inputs, representing 100% of the Fund’s investments, used to value the Fund’s net assets as of December 31, 2011:

|

Valuation Inputs

|

Investments in Securities

|

|||

|

Level 1 – Quoted Prices

|

$ | — | ||

|

Level 2 – Other Significant Observable Inputs —

|

||||

|

Municipal Bonds*

|

280,522,724 | |||

|

Level 3 – Significant Unobservable Inputs

|

— | |||

|

Total

|

$ | 280,522,724 | ||

* See schedule of investments for a detailed listing of securities.

|

c)

|