As filed with the Securities and Exchange Commission on October 14, 2011

Registration No. 333-____

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

|

Pre-Effective Amendment No. __

|

[ ]

|

|

|

Post-Effective Amendment No. __

|

[ ]

|

|

|

(Check appropriate box or boxes)

|

PROFESSIONALLY MANAGED PORTFOLIOS

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street

Milwaukee, Wisconsin 53202

(Address of Principal Executive Offices)

Registrant’s Telephone Number, including Area Code: (626) 914-7363

Elaine E. Richards, Esq.

U.S. Bancorp Fund Services, LLC

2020 E. Financial Way, Suite 100

Glendora, CA 91741

(Name and Address of Agent for Service)

Copies to:

Domenick Pugliese, Esq.

Paul Hastings LLP

Park Avenue Tower

75 East 55th Street

New York, NY 10022

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended.

It is proposed that this filing will become effective on November 14, 2011 pursuant to Rule 488 under the Securities Act of 1933, as amended.

No filing fee is required because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

|

Title of Securities Being Registered:

|

Shares of common stock, no par value per share, of the

Brown Advisory Small-Cap Fundamental Value Fund

|

Brown Advisory Funds

Brown Advisory Small Companies Fund

(formerly known as the Brown Cardinal Small Companies Fund)

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

(800) 540-6807

November [●], 2011

Dear Shareholder,

We are sending this information to you because you are a shareholder of the Brown Advisory Small Companies Fund, formerly known as the Brown Cardinal Small Companies Fund (the “Small Companies Fund”), a series of Professionally Managed Portfolios (the “Trust”). After careful consideration, Brown Investment Advisory Incorporated (“Brown Advisory”), the Small Companies Fund’s investment adviser, recommended and the Trust Board approved the reorganization of the Small Companies Fund into the Brown Advisory Small Cap Fundamental Value Fund (the “Fundamental Value Fund”), an existing series of the Trust (the “Reorganization”). Brown Advisory also serves as the investment adviser to the Fundamental Value Fund.

As further explained in the enclosed information statement/prospectus, upon satisfaction of the conditions set forth in the Agreement and Plan of Reorganization, your current shares in the Small Companies Fund will be exchanged for shares of the Fundamental Value Fund at the closing of the Reorganization. This exchange is expected to be a tax free exchange for shareholders. You may, however, purchase and redeem shares of the Small Companies Fund in the ordinary course until the last business day before the closing. Purchase and redemption requests received after that time will be treated as purchase and redemption requests for shares of the Fundamental Value Fund received in connection with the Reorganization.

More information on the Fundamental Value Fund, reasons for the proposed Reorganization and benefits to Small Companies Fund shareholders is contained in the enclosed information statement/prospectus. You should review the information statement/prospectus carefully and retain it for future reference. Shareholder approval is not required to effect the Reorganization which is expected to close on or about December 16, 2011.

Sincerely,

________________________

[Name/Title]

Brown Investment Advisory Incorporated

INFORMATION STATEMENT/PROSPECTUS

November [●], 2011

REORGANIZATION OF

BROWN ADVISORY SMALL COMPANIES FUND

(formerly known as the Brown Cardinal Small Companies Fund)

A series of Professionally Managed Portfolios

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

(800) 540-6807

IN EXCHANGE FOR SHARES OF

BROWN ADVISORY SMALL CAP FUNDAMENTAL VALUE FUND

A series of Professionally Managed Portfolios

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

(800) 540-6807

WE ARE NOT ASKING YOU FOR A PROXY AND

YOU ARE REQUESTED NOT TO SEND US A PROXY

This information statement/prospectus is being furnished to shareholders of the Brown Advisory Small Companies Fund (the “Small Companies Fund”), a series of Professionally Managed Portfolios (“PMP”), in connection with an Agreement and Plan of Reorganization (the “Reorganization Agreement”) by and between Professionally Managed Portfolios (“PMP”), on behalf of the Brown Advisory Small Cap Fundamental Value Fund (the “Fundamental Value Fund”), a series of PMP, and PMP, on behalf of the Small Companies Fund. The Reorganization Agreement provides for the reorganization of the Small Companies Fund into the Fundamental Value Fund (the “Reorganization”). PMP is an open-end investment management companies organized as a Massachusetts business trust. Brown Investment Advisory Incorporated (“Brown Advisory”) is the investment adviser to both the Small Companies Fund and the Fundamental Value Fund. Brown Advisory will continue to be responsible for providing investment advisory or portfolio management services to the Fundamental Value Fund following the Reorganization.

If you need additional copies of this information statement/prospectus, please contact the Small Companies Fund at 1-800-540-6807 or in writing at Brown Advisory Small Companies Fund, c/o U.S. Bancorp Fund Services, LLC, P.O. Box 701, Milwaukee, Wisconsin 53201-0701. Additional copies of this information statement/prospectus will be delivered to you promptly upon request. For a free copy of the Small Companies Fund’s annual report for the fiscal year ended June 30, 2011 or its most recent semi-annual report, please contact the Small Companies Fund at 1-800-540-6807 or in writing at Brown Advisory Small Companies Fund, c/o U.S. Bancorp Fund Services, LLC, P.O. Box 701, Milwaukee, Wisconsin 53201-0701.

How the Reorganization Will Work

|

·

|

The Small Companies Fund will transfer all of its assets and liabilities to the Fundamental Value Fund.

|

|

·

|

The Fundamental Value Fund will issue that number of shares of its common stock to the Small Companies Fund in an amount that will equal, in aggregate net asset value, the aggregate net asset value of the shares of the Small Companies Fund on the last business day preceding the closing of the Reorganization.

|

|

·

|

The Fundamental Value Fund will open accounts for the Small Companies Fund shareholders, crediting the shareholders, in exchange for their shares of the Small Companies Fund, with that number of full and fractional shares of the Fundamental Value Fund that are equivalent in aggregate net asset value to the aggregate net asset value of the shareholders’ shares in the Small Companies Fund at the time of the Reorganization.

|

|

·

|

PMP will then dissolve the Small Companies Fund.

|

Brown Advisory and the PMP Board (the “Board”) carefully considered the proposed Reorganization, as well as potential alternatives for the Small Companies Fund, including the liquidation of the Small Companies Fund and the continued viability of the Small Companies Fund as a stand alone entity. After careful consideration, the Board approved the Reorganization. A copy of the form of the Reorganization Agreement is attached to this information statement/prospectus as Appendix A. The Reorganization Agreement is not required to be approved by the shareholders of the Small Companies Fund. Accordingly, shareholders of the Small Companies Fund are not being asked to vote on or approve the Reorganization Agreement.

This information statement/prospectus sets forth the basic information regarding the Reorganization. You should read it and keep it for future reference.

For simplicity, actions are described in this information statement/prospectus as being taken by either the Small Companies Fund or the Fundamental Value Fund (which are collectively referred to as the “Funds” and are each referred to as a “Fund”), although all actions are actually taken by PMP on behalf of the Funds.

The following documents have been filed with the U.S. Securities and Exchange Commission (the “SEC”) and are incorporated by reference in this information statement/prospectus:

|

·

|

The Prospectus and Statement of Additional Information for both the Small Companies Fund and the Fundamental Value Fund, dated October 31, 2011, are incorporated by reference to Post-Effective Amendment No. [●] to PMP’s Registration Statement on Form N-1A (File No. 811-05037), filed with the SEC on October [●], 2011.

|

|

·

|

The audited financial statements of the Small Companies Fund and the Fundamental Value Fund dated June 30, 2011 are incorporated by reference to the Annual Report of the Funds for the fiscal year ended June 30, 2011, filed on Form N-CSR (File No. 811-05037) with the SEC on September 8, 2011.

|

|

·

|

The Statement of Additional Information relating to this information statement/prospectus dated November [●], 2011.

|

This information statement/prospectus will be mailed on or about November [●], 2011 to shareholders of record of the Small Companies Fund as of October 31, 2011 (the “Record Date”). .

Copies of these materials and other information about PMP, the Small Companies Fund and the Fundamental Value Fund are available upon request and without charge by writing to the addresses below or by calling the telephone numbers listed as follows:

Brown Advisory Funds

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

(800) 540-6807 (toll free)

www.brownadvisoryfunds.com

Shareholder approval is not required to effect the Reorganization. No action on your part is required to effect the Reorganization.

ii

The SEC has not approved or disapproved the Fundamental Value Fund shares to be issued in the Reorganization nor has it passed on the accuracy or adequacy of this information statement/prospectus. Any representation to the contrary is a criminal offense.

No person has been authorized to give any information or to make any representations other than those contained in this information statement/prospectus and in the materials expressly incorporated herein by reference and, if given or made, such other information or representations must not be relied upon as having been authorized by the Funds.

_____________________________________

iii

Table of Contents

|

Table of Contents

|

|

|

Page

|

|

|

SUMMARY

|

1

|

|

INFORMATION ABOUT THE REORGANIZATION

|

11

|

|

ADDITIONAL INFORMATION ABOUT THE FUNDS

|

15

|

|

AVAILABLE INFORMATION

|

19

|

|

LEGAL MATTERS

|

20

|

|

EXPERTS

|

20

|

|

OTHER MATTERS

|

20

|

|

Appendix A – Form of Agreement and Plan of Reorganization

|

Appendix A-1

|

|

Appendix B – Investment Policies and Restrictions

|

Appendix B-1

|

|

Appendix C – Shareholder Information for the Fundamental Value Fund

|

Appendix C-1

|

|

Appendix D – Financial Highlights

|

Appendix D-1

|

iv

SUMMARY

The following is a summary of more complete information appearing later in this information statement/prospectus or incorporated herein. You should read carefully the entire information statement/prospectus, including the Reorganization Agreement, the form of which is attached as Appendix A, because it contains details that are not in the summary.

As used herein,, the term “Reorganization” refers collectively to: (1) the transfer of all of the assets and liabilities of the Small Companies Fund to the Fundamental Value Fund; (2) the issuance of shares of common stock by the Fundamental Value Fund to the Small Companies Fund in an amount that will equal, in aggregate net asset value, the aggregate net asset value of the shares of the Small Companies Fund on the last business day preceding the closing of the Reorganization; (3) the opening of accounts by the Fundamental Value Fund for the Small Companies Fund shareholders, the crediting of Small Companies Fund shareholders, in exchange for their shares of the Small Companies Fund, with that number of full and fractional shares of the Fundamental Value Fund that are equivalent in aggregate net asset value to the aggregate net asset value of the shareholders’ shares in the Small Companies Fund at the time of the Reorganization; and (4) the ultimate redemption by PMP of the shares of the Small Companies Fund prior to its dissolution.

The Reorganization is expected to be a tax-free reorganization for federal income tax purposes under Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). For information on the tax consequences of the Reorganization, see the sections entitled “Summary – Federal Income Tax Consequences of the Reorganization” and “Information About the Reorganization – Federal Income Tax Consequences” in this information statement/prospectus.

Comparison of the Small Companies Fund to the Fundamental Value Fund

|

Small Companies Fund

|

Fundamental Value Fund

|

|||

|

Form of Organization

|

A diversified series of PMP, an open-end investment management company organized as a Massachusetts business trust.

|

Same.

|

||

|

Net Assets as of

October 31, 2011

|

$[●]

|

$[●]

|

||

|

Investment Adviser and

Portfolio Manager

|

Investment Adviser:

Brown Advisory

Portfolio Manager:

Mr. J. David Schuster is responsible for day-to-day management of the Fund’s portfolio.

|

Same.

|

||

|

Annual Operating

Expenses as a Percentage

of Average Net Assets for

the Fiscal Year

|

The Fund’s Institutional Shares have an expense cap of 1.40%; however the total operating expense ratio for the fiscal year ended June 30, 2011 was 1.23%.

The Fund’s Advisor Shares have an expense cap of 1.60%; however the total operating expense ratio for the fiscal year ended June 30, 2011 was 1.74%.

|

The Fund’s Institutional Shares have an expense cap of 1.40%; however the total operating expense ratio for the fiscal year ended June 30, 2011 was 1.24%.

The Fund’s Advisor Shares, which have not yet commence operations, have an expense cap of 1.60%; however the estimated total operating expense ratio for the Fund’s Advisor Shares is 1.68%.

|

||

|

Investment Objective

|

The Fund seeks to achieve long-term capital appreciation. The investment objective is not designated as a “fundamental policy” within the meaning of the Investment Company Act of 1940, as amended (the “1940 Act”), and may be changed by the Fund’s Board of Trustees (the “PMP Board”) without shareholder approval.

|

Same.

|

1

|

Small Companies Fund

|

Fundamental Value Fund

|

|

Primary Investments

|

Under normal circumstances, the Fund invests at least 80% of the value of its net assets (plus borrowings for investment purposes) in equity securities of small companies (“80% Policy”). Small companies, according to the Advisor, are companies whose market capitalizations are generally less than $4 billion at the time of purchase. The Fund must provide shareholders with 60 days’ prior written notice if it changes its 80% Policy.

The Fund invests primarily in equity securities of companies that trade in the U.S. securities markets and that the Advisor believes are undervalued based on the companies’ ability to generate cash flow beyond that required for normal operations and reinvestment in the business. Excess cash flow, among other things, are used to pay dividends, make acquisitions, pay down debt and/or buy back stock.

|

Under normal circumstances, the Fund invests at least 80% of the value of its net assets (plus borrowings for investment purposes) in equity securities of small capitalization companies (“80% Policy”). Small companies, according to the Advisor, are companies whose market capitalizations are generally less than $4 billion at the time of purchase. The Fund must provide shareholders with 60 days’ prior written notice if it changes its 80% policy.

The Advisor may invest up to 15% of its assets in foreign equity securities, including in emerging markets. With respect to 20% of its assets, the Fund may also invest in foreign or domestic debt securities, including distressed debt securities (limited to 5% or less of its assets). Debt securities in which the Fund may invest may be rated by a Nationally Recognized Statistical Rating Agency or may be unrated and judged by the Advisor to be of comparable quality. The Fund may engage in options, futures contracts and options on futures to seek to achieve the Fund’s investment objective, manage the portfolio, mitigate risks, hedge risks, equitize cash or to enhance total return.

|

||

|

Investment Strategies

and Process

|

The Advisor’s Process — Purchasing Portfolio Securities. The Advisor seeks companies that are believed to have stable and predictable businesses that generate cash flow in excess of what is needed to pay all expenses and reinvest in the business, and have competent and motivated management teams. The Advisor also seeks companies whose securities are undervalued because of temporary issues that are likely to be resolved in the near future.

The Advisor focuses on gathering information on companies that are not well known to most institutional investors, by developing opinions on companies or businesses that are contrary to prevailing thinking, or by investigating corporate events (such as substantial share repurchases or insider buying) that may signal a company’s undervaluation. Once investment opportunities are identified, the Advisor researches prospective companies by analyzing regulatory financial disclosures, and by speaking with industry experts and company management. The purpose of this research is to get a clear understanding of the company’s business model, competitive advantages and capital allocation discipline.

The Advisor anticipates that the Fund’s portfolio will consist of 45 to 60 positions, broadly diversified across industries and market sectors. Position sizes will generally range from 1% to 4% of net assets measured at cost at the time of investment. The Advisor considers several factors in determining position size including:

|

The Advisor’s Process. The Advisor seeks investment opportunities in companies with valuations whose market prices are selling at a discount to their estimated intrinsic business values. The Advisor’s valuation discipline attempts to estimate the range of a company’s business value by considering past, current or future earnings, cash flows, book value, sales or growth rates relative to the company’s history, industry, or the broader market. The Advisor seeks to find companies that are:

· Out-of-favor;

· Over-looked;

· Under-followed in the market; and

· Often trade at price levels which do not reflect

the Advisor’s assessment of their fundamental

economic value.

If a valuation analysis indicates that a company is priced at an appropriate discount to its long-term earnings potential, the Fund may also invest in cyclical companies or companies that experienced a temporary setback.

The Fund may also invest in securities whose prices are low relative to their asset valuation or private market valuation. These may include companies that the Advisor believes are:

· Extremely oversold or neglected due to adverse

events or complex capital structures;

|

2

|

Small Companies Fund

|

Fundamental Value Fund

|

|

· The predictability of the business;

· The level of the stock price relative to the targeted

purchase price; and

· Trading liquidity and catalysts that should result in

stock price appreciation. Such catalysts may

include the redeployment of excess cash to benefit

shareholders, a turnaround in operations, the sale

or liquidation of unprofitable operations, an accretive

acquisition or merger, a change in management, an

improvement in industry prospects or the cessation

of circumstances which have depressed operating

results.

The Advisor’s Process — Selling Portfolio Securities. The Advisor regularly monitors the companies in the Fund’s portfolio to determine if there have been any fundamental changes in the companies. The Advisor may sell a security or reduce its position if:

· The security’s expected return falls below 20% either

due to price appreciation or adverse changes in the

company’s fundamentals;

· The market capitalization of the company reaches $5

billion; or

· There are better relative values elsewhere or if funds

are needed for other purposes.

|

· Mired in company-specific or industry-related

turnarounds;

· Undergoing financial or operational restructuring,

including spin-offs, reorganizations, liquidations,

mergers and acquisitions;

· In possession of hidden value in the form of assets

on their balance sheets that are underappreciated by

the market.

The Advisor seeks catalysts or inflection points that may unlock shareholder value by narrowing the gap between current market price and underlying business value. Examples of catalysts or inflection points include:

· Changes in regulation, management, or business mix;

· Industry consolidation;

· Cost reduction initiatives;

· Acquisition or merger activity;

· New products or investments;

· Share repurchases;

· Asset sales; or

· Cyclical recoveries.

The Advisor seeks a measure of downside protection for the Fund by purchasing investments for the Fund’s portfolio whose risk-reward relationship meets certain criteria established by the Advisor. More specifically, the Advisor estimates a reasonable worst case low price for each security and rejects those that have unacceptable spreads between that price and the company’s current stock price.

The Advisor’s Process — Purchasing Portfolio Securities. The Advisor performs an in-depth qualitative and quantitative analysis to distinguish companies that the Advisor believes may exhibit some of the following characteristics:

· Free cash flow providing flexibility for growth and/or return of shareholder value;

· High and/or increasing returns on capital;

· Hidden asset value or operations unrecognized by the market;

· Sustainable and/or expanding profitability;

· Market leadership and/or market share growth potential;

· Financial stability, including strong balance sheet and modest use of debt;

· Effective management team sensitive to shareholder interests;

· Sound business strategy and competitive advantages;

· Franchise value defensible by proprietary products, differentiated services or systems, customer captivity, lowest-cost production, or identifiable brands;

|

3

|

Small Companies Fund

|

Fundamental Value Fund

|

|

· Product cycles, pricing flexibility, rational investment or new product development, and segment or geographic mix that supports stability and growth; or

· Attractive valuation.

Advisor’s Process — Selling Portfolio Securities. The Advisor regularly monitors the companies in the Fund’s portfolio to determine if there have been any material changes in the companies. The Advisor may sell a security or reduce its position if:

· The security has reached its target price level and reward to risk ratio is unattractive;

· The security is no longer valued at a discount to its intrinsic economic value, or is overvalued relative to market expectations;

· The company’s fundamentals change in a material, long-term manner, fail to meet investment criteria, or are no longer reliable in estimating the underlying business value;

· Unrealized catalysts or management inability to enhance shareholder value result in “value trap;”

· A more attractively valued alternative, either existing holding or new investment, offers greater reward to risk potential or if funds are needed for other purposes;

· The security becomes too large of a position size; or

· Any other factors may contribute to under-performance.

|

||||

|

Temporary Strategies

|

Temporary Defensive Position. In order to respond to adverse market, economic, political or other conditions, the Fund may assume a temporary defensive position that is inconsistent with its principal investment strategies and invest, without limitation, in cash or prime quality cash equivalents (including commercial paper, certificates of deposit, banker’s acceptances and time deposits). A defensive position, taken at the wrong time, may have an adverse impact on the Fund’s performance. The Fund may be unable to achieve its investment objective during the employment of a temporary defensive measure.

|

Same.

|

4

|

Small Companies Fund

|

Fundamental Value Fund

|

|

Fundamental and Non-

Fundamental Investment

Policies and Restrictions

|

For a more complete description of the Fund’s fundamental and non-fundamental investment policies and restrictions, see Appendix B.

In general, the Fund has adopted fundamental policies that, subject to certain exceptions, limit or restrict the Fund with respect to the following activities: (1) borrowing money, (2) concentrating its investments in any particular industry or group of industries, (3) with respect to 75% of its assets, purchasing more than a certain amount in any one issuer, (4) acting as an underwriter of securities issued by others, (5) investing directly in real estate or interests in real estate, (6) lending any security or making any other loan, (7) purchasing or selling physical commodities, and (8) issuing senior securities.

The Fund has adopted non-fundamental policies that, subject to certain exceptions, limit or restrict the Fund with respect to the following activities: (1) investing in other investment companies, except as permitted under the 1940 Act, (2) short selling, unless it is done “against the box”, (3) purchasing securities on margin, (4) investing in options except for hedging purposes, (5) investing in companies for the purpose of exercising control of management, (6) purchasing a security if the total of borrowings would exceed 5% of the value of its total assets, and (7) investing more than 15% of its net assets in illiquid securities.

The Fund is a diversified series of PMP.

|

Same.

|

||

|

Management and Other

Fees

|

Management Fee. The Fund pays a management fee to Brown Advisory at an annual rate of 1.00% of the Fund’s average daily net assets.

Administration Fees. The Fund pays a separate fee for administration, fund accounting and transfer agency services to U.S. Bancorp Fund Services, LLC (“USBFS”). Additionally, the Fund pays separate fees for custodial services to U.S. Bank, National Association (“US Bank”).

|

Same.

|

||

|

Distribution

|

Quasar Distributors, LLC provides distribution services to the Fund. The Fund, on behalf of its Advisor Shares, has adopted a distribution plan pursuant to Rule 12b-1 under the 1940 Act.

|

Same.

|

||

|

Expense Limitations and

Overall Expenses

|

Brown Advisory has contractually agreed to reduce all or a portion of its advisory fee and/or reimburse Fund expenses to ensure that the Fund’s total annual fund operating expenses (exclusive of interest, taxes, transaction costs including brokerage commissions and dividend and interest expense on securities sold short, and extraordinary expenses) do not exceed 1.40% for the Institutional Shares and 1.60% for the Advisor shares, as a percentage of the Fund’s average net assets, indefinitely, but at least through October 31, 2012. The contractual waivers and expense reimbursements may be changed or eliminated at any time after October 31, 2012 by the Board of Trustees upon 60 days notice to Brown Advisory, or by Brown Advisory with the consent of the Board of Trustees.

|

Same.

|

5

|

Small Companies Fund

|

Fundamental Value Fund

|

|

Buying Shares

|

You may buy shares directly from the Fund through its transfer agent or through third-party financial intermediaries.

|

Same.

|

||

|

Exchange Privilege

|

You may exchange your Fund shares of the same class for shares of certain other Brown Advisory Funds.

|

Same.

|

||

|

Selling Shares

|

Shares of the Fund will be sold at the net asset value per share calculated after the Fund receives your request in good order.

If the account is registered in your name, you may sell your shares by contacting the Fund by mail or telephone as described in detail in the Fund’s Prospectus. Redemptions may also be made through third-party financial intermediaries, such as fund supermarkets or broker-dealers, who may charge a commission or other transaction fee.

A redemption fee of 1.00% is imposed on shares redeemed within 14 days of purchase.

|

Same.

|

Comparison of Principal Risks of Investing in the Funds

A discussion regarding certain principal risks of investing in the Funds is set forth below. Where applicable, differences between the Fundamental Value Fund and the Small Companies Fund have been highlighted. This discussion is qualified in its entirety by the more extensive discussion of risk factors set forth in the Funds’ Prospectuses and the Statements of Additional Information. As with all mutual funds, there is the risk that you could lose all or a portion of your investment in the Fund. An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The following are the principal risks that could affect the value of your investment:

Equity and General Market Risk (Both Funds). Common stocks are susceptible to general stock market fluctuations and to volatile increases and decreases in value. The stock market may experience declines or stocks in the Fund’s portfolio may not increase their earnings at the rate anticipated. The Fund’s NAV and investment return will fluctuate based upon changes in the value of its portfolio securities.

Value Company Risk (Both Funds). The stock of value companies can continue to be undervalued for long periods of time and not realize its expected value. The value of the Fund may decrease in response to the activities and financial prospects of an individual company.

Smaller Company Risk (Both Funds). Securities of companies smaller than larger companies may be more volatile and as a result, the price of smaller companies may decline more in response to selling pressure.

6

Management Risk (Both Funds). The Fund may not meet its investment objective based on the Advisor’s success or failure to implement investment strategies for the Fund.

REIT and Real Estate Risk (Both Funds). The value of the Fund’s investments in REITs may change in response to changes in the real estate market such as declines in the value of real estate, lack of available capital or financing opportunities, and increases in property taxes or operating costs.

Convertible Securities Risk (Both Funds). The value of convertible securities tends to decline as interest rates rise and, because of the conversion feature, tends to vary with fluctuations in the market value of the underlying securities.

Foreign Securities/Emerging Markets Risk (Fundamental Value Fund only). Foreign securities (including ADRs), including those issued in emerging markets are subject to additional risks including international trade, currency, political, regulatory and diplomatic risks. Securities issued in emerging markets have more risk than securities issued in more developed foreign markets.

ADR Risk (Small Companies Fund only). ADRs may be subject to some of the same risks as direct investment in foreign companies, which includes international trade, currency, political, regulatory and diplomatic risks.

Derivatives Risk (Fundamental Value Fund only). The risks of investments in options, futures contracts and options on futures contracts include imperfect correlation between the value of these instruments and the underlying assets; risks of default by the other party to the derivative transactions; risks that the transactions may result in losses that partially or completely offset gains in portfolio positions; and risks that the derivative transactions may not be liquid.

ETF Risk (Both Funds). ETFs may trade at a discount to the aggregate value of the underlying securities and although expense ratios for ETFs are generally low, frequent trading of ETFs by the Fund can generate brokerage expenses. Shareholders of the Fund will indirectly be subject to the fees and expenses of the individual ETFs in which the Fund invests.

Private Placement Risk (Both Funds). The Fund may invest in privately issued securities of domestic common and preferred stock, convertible debt securities, ADRs, REITs and ETFs, including those which may be resold only in accordance with Rule 144A under the Securities Act of 1933, as amended (“1933 Act”). Privately issued securities are restricted securities that are not publicly traded. Delay or difficulty in selling such securities may result in a loss to the Fund.

Other Consequences of the Reorganization

Management Fee and Structure. Brown Advisory serves as the investment adviser to both the Small Companies Fund and the Fundamental Value Fund. After the Reorganization, Brown Advisory will continue to serve as the investment adviser to the Fundamental Value Fund. The Small Companies Fund and the Fundamental Value Fund each pay a management fee equal to the following annual percentage of average daily net assets:

|

Small Companies Fund

Management Fee – Paid to Brown Advisory

|

Fundamental Value Fund

Management Fee – Paid to Brown Advisory

|

|

1.00%

|

1.00%

|

Under the investment advisory agreement between Brown Advisory and PMP, on behalf of the Fundamental Value Fund, the annual management fee rate payable by the Fundamental Value Fund is the same as the rate currently payable to Brown Advisory by the Small Companies Fund. The investment advisory agreements are further described under “Additional Information About the Funds – Investment Advisory Agreement,” below.

Expense Limitation. Brown Advisory and PMP have entered into an operating expense limitation agreement under which Brown Advisory has agreed to waive its management fees and/or reimburse expenses of the Fundamental Value Fund to ensure that the Fundamental Value Fund’s total annual operating expenses of the Fundamental Value Fund’s shares (exclusive of interest on tax expenses, brokerage commissions, extraordinary and non-recurring expenses, AFFE and dividends and interest on short portions) 1.40% for the Institutional Shares and 1.60% for the Advisor shares, as a percentage of the Fund’s average net assets, but at least through October 31, 2012, which is the same expense limitations for the Small Companies Fund. The agreement remains in effect indefinitely, and at a minimum through October 31, 2012, and may be terminated by the PMP Board.

7

Past Performance

Set forth below is performance information that provides some indication of the risks of investing in the Small Companies Fund and the Fundamental Value Fund. The charts show changes in each Fund’s performance of Institutional Shares from year-to-year. The tables show how the average annual returns of each class of shares for the periods shown compare to a broad-based market index.

Effective April 12, 2010, the Brown Advisory Small Companies Fund (formerly, the Brown Cardinal Small Companies Fund), a series of Forum Funds (the “Predecessor Small Companies Fund”) reorganized into the Small Companies Fund, which is a series of PMP. Similarly, effective April 12, 2010, the Brown Advisory Small-Cap Fundamental Value Fund, a series of Forum Funds (the “Predecessor Fundamental Value Fund”) reorganized into the Fundamental Value Fund, which is a series of PMP. Performance shown prior to April 12, 2010 is that of each of the Predecessor Funds.

Performance information represents only past performance, before and after taxes, and does not necessarily indicate future results. Updated performance information is available online at www.brownadvisoryfunds.com or by calling 800-540-6807 (toll free).

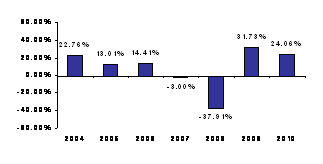

| Brown Advisory Small Companies Fund

– Institutional Shares

Calendar Year Total Returns

|

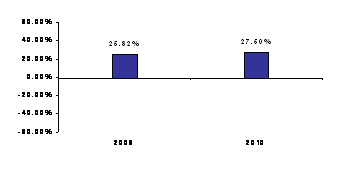

Brown Advisory Small-Cap Fundamental Value Fund

– Institutional Shares

Calendar Year Total Returns

|

|

|

|

|

| The Small Companies Fund’s calendar year-to-date total return as of September 30, 2011 was -10.52%. During the periods shown in the chart, the highest quarterly return was 22.39% (for the quarter ended June 30, 2009) and the lowest quarterly return was -25.09% (for the quarter ended September 30, 2008). |

The Fundamental Value Fund’s calendar year-to-date total return as of September 30, 2011 was -9.22%. During the periods shown in the chart, the highest quarterly return was 17.41% (for the quarter ended December 31, 2010) and the lowest quarterly return was -10.11% (for the quarter ended June 30, 2010).

|

8

Average Annual Total Returns

The after-tax returns shown in the following table are intended to show the impact of assumed federal income taxes on an investment in the Small Companies Fund. The “Return After Taxes on Distributions” shows the effect of taxable distributions (investment company taxable income and capital gains distributions), but assumes that you still hold Fund shares at the end of the period. The “Return After Taxes on Distributions and Sale of Fund Shares” shows the effect of both taxable distributions and any taxable gain or loss that would be realized if Fund shares were sold at the end of the specified period. The after tax returns are calculated using the highest individual federal marginal income tax rates in effect and do not reflect the impact of state and local taxes. our actual after-tax returns depend on your tax situation and may differ from those shown. The after-tax returns are not relevant if you hold your Fund shares through a tax-deferred account, such as a 401(k) plan or an individual retirement account.

|

For the period ended December 31, 2010

|

1 Year

|

5 Years

|

Since Inception

|

|

Small Companies Fund(1)

|

|||

|

Institutional Shares

|

|||

|

– Return Before Taxes

|

24.06%

|

2.40%

|

7.38%

|

|

– Return After Taxes on Distributions

|

23.98%

|

1.72%

|

6.51%

|

|

– Return After Taxes on Distributions and Sale of Fund Shares

|

15.73%

|

1.93%

|

6.17%

|

|

Advisor Shares

|

|||

|

– Return Before Taxes

|

23.51%

|

1.89%

|

6.86%

|

|

Russell 2000® Index(2)

|

26.85%

|

4.47%

|

7.02%

|

|

For the period ended December 31, 2010

|

1 Year

|

5 Years

|

Since Inception

|

|

Fundamental Value Fund(3)

|

|||

|

Institutional Shares

|

|||

|

– Return Before Taxes

|

27.50%

|

N/A

|

26.66%

|

|

– Return After Taxes on Distributions

|

26.13%

|

N/A

|

25.63%

|

|

– Return After Taxes on Distributions and Sale of Fund Shares

|

18.30%

|

N/A

|

22.50%

|

|

Advisor Shares

|

|||

|

– Return Before Taxes

|

26.93%

|

N/A

|

26.09%

|

|

Russell 2000® Value Index(4)

|

24.50%

|

N/A

|

22.52%

|

|

(1)

|

Institutional Shares of the Small Companies Fund commenced operations on October 31, 2003 as part of the Predecessor Small Companies Fund. (Prior to April 25, 2006, the Institutional Shares was an unnamed class of shares.) Advisor Shares commenced operations on May 1, 2006 as part of the Predecessor Small Companies Fund. Performance shown prior to inception of the Advisor Shares is based on the performance of Institutional Shares, adjusted for the higher expenses applicable to Advisor Shares.

|

|

(2)

|

The Russell 2000® Index measures the performance of the smallest 2,000 companies in the Russell 3000® Index and represents approximately 8% of the total market capitalization of the Russell 3000® Index. The Index reflects no deduction for fees, expenses or taxes. The “Since Inception” return shown for the Index is as of October 31, 2003, correlating to the “Since Inception” date of the Small Companies Fund. You may not invest directly in an Index.

|

|

(3)

|

Institutional Shares of the Fundamental Value Fund commenced operations on December 31, 2008 as part of the Predecessor Fundamental Value Fund. Advisor Shares of the Fundamental Value Fund commenced operations July 28, 2011. Performance shown prior to inception of the Advisor Shares is based on the performance of Institutional Shares, adjusted for the higher expenses applicable to Advisor Shares.

|

|

(4)

|

The Russell 2000® Value Index measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Index reflects no deduction for fees, expenses or taxes. The “Since Inception” return shown for the Index is as of December 31, 2008, correlating to the “Since Inception” date of the Fundamental Value Fund. You may not invest directly in an Index.

|

The Funds’ Fees and Expenses

The following Summary of Fund Expenses shows the current fees and expenses for the Small Companies Fund compared to the Fundamental Value Fund (based on the fiscal year ended June 30, 2011) and the pro forma fees and expenses of the Fundamental Value Fund for the same period assuming the Reorganization had occurred on July 1, 2011.

9

Summary of Fund Fees and Expenses

|

Shareholder Fees

(fees paid directly from your investment)

|

Small Companies Fund

|

Fundamental Value Fund

|

Fundamental Value Fund

(Pro Forma)

|

|||

|

Institutional Shares

|

Advisor Shares

|

Institutional Shares

|

Advisor Shares

|

Institutional Shares

|

Advisor Shares

|

|

|

Maximum Sales Charge (Load) imposed on Purchases

(as a % of the offering price)

|

None

|

None

|

None

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load) imposed on Redemptions (as a % of the sale price)

|

None

|

None

|

None

|

None

|

None

|

None

|

|

Redemption Fee (as a % of amount redeemed within 14

days of purchase)

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

|

Exchange Fee(as a % of amount exchanged within 14

days of purchase)

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

|

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of

the value of your investment)

|

Small Companies Fund

|

Fundamental Value Fund

|

Fundamental Value Fund

(Pro Forma)

|

|||

|

Institutional Shares

|

Advisor Shares

|

Institutional Shares

|

Advisor Shares

|

Institutional Shares

|

Advisor Shares

|

|

|

Management Fees

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

1.00%

|

|

Distribution and/or Service (12b-1) Fees(1)

|

0.00%

|

0.25%

|

0.00%

|

0.25%

|

0.00%

|

0.25%

|

|

Other Expenses

|

0.23%

|

0.24%

|

0.24%

|

0.19%(2)

|

0.18%

|

0.13%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.00%

|

0.26%

|

0.26%

|

0.26%

|

0.26%

|

|

Total Annual Fund Operating Expenses(3)

|

1.23%

|

1.49%

|

1.50%

|

1.70%

|

1.44%

|

1.64%

|

|

|

Effective July 1, 2011, the Rule 12b-1 fees for the Advisor Shares were lowered from 0.50% to 0.25%. For that reason, the Total Annual Fund Operating Expenses have been restated to reflect the reduction of the Distribution and/or Service (12b-1) Fees. Accordingly, the figure does not correlate to the Ratio of Operating Expenses to Average Net Assets Before Expense Reimbursement provided in the Financial Highlights located in Appendix D of this information statement/prospectus.

|

|

|

Other Expenses for the Advisor Shares of the Fundamental Value Fund are based on estimated customary Fund expenses for the current fiscal year because that class has recently commenced operations.

|

|

|

The Total Annual Fund Operating Expenses do not correlate to the Ratios to Average Net Assets – Gross Expenses provided in the Financial Highlights Section Financial Highlights located in Appendix D of this information statement/prospectus, which reflects the operating expenses of the Fund and does not include Acquired Fund Fees and Expenses.

|

Example of Effect on Fund Expenses

The Example is intended to help you compare the costs of investing in the Small Companies Fund with the cost of investing in the Fundamental Value Fund, assuming the Reorganization has been completed. The Example assumes that you invest $10,000 in the specified Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, and that each Fund’s total operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

|

One Year

|

Three Years

|

Five Years

|

Ten Years

|

|

|

Small Companies Fund

|

||||

|

Institutional Shares

|

$125

|

$390

|

$676

|

$1,489

|

|

Advisor Shares

|

$152

|

$471

|

$813

|

$1,779

|

|

Fundamental Value Fund

|

||||

|

Institutional Shares

|

$153

|

$474

|

$818

|

$1,791

|

|

Advisor Shares

|

$173

|

$536

|

$923

|

$2,009

|

|

Fundamental Value Fund (Pro Forma)

|

||||

|

Institutional Shares

|

$147

|

$456

|

$787

|

$1,724

|

|

Advisor Shares

|

$167

|

$517

|

$892

|

$1,944

|

Portfolio Turnover

The Small Companies Fund and the Fundamental Value Fund each pay transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year ended June 30, 2011, the portfolio turnover rate for the Small Companies Fund was 32% and the portfolio turnover rate for the Fundamental Value Fund was 67%.

10

Federal Income Tax Consequences of the Reorganization

As a condition to the Reorganization, each Fund will have received an opinion of counsel to the effect that the Reorganization should qualify as a tax-free reorganization for federal income tax purposes within the meaning of Section 368(a) of the Code. Accordingly, neither the Funds nor their shareholders should recognize any gain or loss for federal income tax purposes as a result of the Reorganization. In addition, the tax basis and the holding period of the Fundamental Value Fund shares received by each shareholder of the Small Companies Fund in the Reorganization should be the same as the tax basis and holding period of the Small Companies Fund shares given up by such shareholder in the Reorganization; provided that, with respect to the holding period for the Fundamental Value Fund shares received, the Small Companies Fund’s shares given up must have been held as capital assets by the shareholder. See “Information About the Reorganization – Federal Income Tax Consequences,” below.

* * * * * * * * * * * * *

The preceding is only a summary of certain information contained in this information statement/prospectus relating to the Reorganization. This summary is qualified by reference to the more complete information contained elsewhere in this information statement/prospectus, the Prospectuses and Statements of Additional Information of the Small Companies Fund and the Fundamental Value Fund, and the Reorganization Agreement. Shareholders should read this entire information statement/prospectus carefully.

INFORMATION ABOUT THE REORGANIZATION

Reasons for the Reorganization. The Reorganization is part of a continuing effort by Brown Advisory to streamline and rationalize its mutual fund product offerings. After careful consideration, Brown Advisory has determined that, there were no meaningful distinctions between the investment strategies, risks and portfolios of the Small Companies Fund and the Fundamental Value Fund. In addition, as the Small Companies Fund no longer engaged Cardinal Capital Management L.L.C. as sub-advisor, this resulted in a duplication of portfolio management effort, as the same investment management team at Brown Advisory was responsible for managing two very similar funds. As a result, Brown Advisory recommended, and the Board approved, the Reorganization of the smaller Small Companies Fund into the larger Fundamental Value Fund. In considering Brown Advisory’s recommendation, the Board considered a number of factors which are discussed in more detail below, including potential alternatives to the Reorganization. Pursuant to the Agreement and Plan of Reorganization, Brown Advisory has agreed to bear all expenses incurred in connection with the Reorganization.

Following the Reorganization, the investment advisory fee paid by the Fundamental Value Fund (1.00% of the Fund’s average daily net assets) will be the same as the investment advisory fee paid by the Small Companies Fund (1.00% of the Fund’s average daily net assets). Brown Advisory has agreed to retain an expense cap for the Fundamental Value Fund following the Reorganization, which is indefinite, but at a minimum through October 31, 2012, which is the same as the expense cap in effect for the Small Companies Fund.

Reorganization Agreement. The Reorganization Agreement sets forth the terms by which the Small Companies Fund will be reorganized into the Fundamental Value Fund. The form of the Reorganization Agreement is attached as Appendix A and the description of the Reorganization Agreement contained herein is qualified in its entirety by the attached Reorganization Agreement. The following sections summarize the material terms of the Reorganization Agreement and the federal income tax treatment of the reorganization.

The Reorganization. The Reorganization Agreement provides that upon the transfer of all of the assets and liabilities of the Small Companies Fund to the Fundamental Value Fund, the Fundamental Value Fund will issue to the Small Companies Fund that number of full and fractional Fundamental Value Fund shares having an aggregate net asset value equal in value to the aggregate net asset value of the Small Companies Fund, calculated as of the closing date of the Reorganization (the “Closing Date”). The Small Companies Fund will redeem its shares in exchange for the Fundamental Value Fund shares received by it and will distribute such shares to the shareholders of the Small Companies Fund in complete liquidation of the Small Companies Fund. Small Companies Fund shareholders will receive Fundamental Value Fund shares based on their respective holdings in the Small Companies Fund as of the last business day preceding the Closing Date (the “Valuation Time”).

11

Upon completion of the Reorganization, each shareholder of the Small Companies Fund will own that number of full and fractional shares of the Fundamental Value Fund having an aggregate net asset value equal to the aggregate net asset value of such shareholder’s shares held in the Small Companies Fund as of the Valuation Time. Such shares will be held in an account with the Fundamental Value Fund identical in all material respects to the account currently maintained by the Small Companies Fund for such shareholder.

Until the Valuation Time, shareholders of the Small Companies Fund will continue to be able to redeem their shares at the net asset value next determined after receipt by the Small Companies Fund’s transfer agent of a redemption request in proper form. Redemption and purchase requests received by the transfer agent after the Valuation Time will be treated as requests received for the redemption or purchase of shares of the Fundamental Value Fund received by the shareholder in connection with the Reorganization. After the Reorganization, all of the issued and outstanding shares of the Small Companies Fund will be canceled on the books of the Small Companies Fund and the transfer agent’s books of the Small Companies Fund will be permanently closed.

The Reorganization is subject to a number of conditions, including, without limitation, the receipt of a legal opinion from counsel addressed to the Small Companies Fund and the Fundamental Value Fund with respect to certain tax issues, as more fully described in “Federal Income Tax Consequences” below, and the parties’ performance in all material respects of their respective agreements and undertakings in the Reorganization Agreement. Assuming satisfaction of the conditions in the Reorganization Agreement, the Closing Date of the Reorganization will be at the close of business on December 16, 2011, or such other date as is agreed to by the parties.

The Reorganization Agreement may not be changed except by an agreement signed by each party to the Agreement.

Federal Income Tax Consequences. Subject to the assumptions and limitations discussed below, the following discussion describes the material U.S. federal income tax consequences of the Reorganization to shareholders of the Small Companies Fund. This discussion is based on the Code, applicable Treasury regulations, and federal administrative interpretations and court decisions in effect as of the date of this information statement/prospectus, all of which may change, possibly with retroactive effect. Any such changes could alter the tax consequences described in this summary.

This discussion of material U.S. federal income tax consequences of the Reorganization does not address all aspects of U.S. federal income taxation that may be important to a holder of Small Companies Fund shares in light of that shareholder’s particular circumstances or to a shareholder subject to special rules.

In addition, this discussion does not address any other state, local or foreign income tax or non-income tax consequences of the Reorganization or of any transactions other than the Reorganization.

Note: Small Companies Fund shareholders are urged to consult their own tax advisers to determine the particular U.S. federal income tax or other tax consequences to them of the Reorganization and the other transactions contemplated herein.

The Small Companies Fund and the Fundamental Value Fund will each receive an opinion from the law firm of Paul Hastings LLP substantially to the effect that, based on certain facts, assumptions and representations made by the Small Companies Fund and the Fundamental Value Fund, on the basis of existing provisions of the Code, current administrative rules and court decisions, for federal income tax purposes:

(a) The Reorganization will constitute a tax-free reorganization within the meaning of Section 368(a) of the Code, and the Acquired Fund and the Acquiring Fund will each be a party to a reorganization within the meaning of Section 368(b) of the Code.

(b) No gain or loss will be recognized by the Acquired Fund upon the transfer of all of its assets to the Acquiring Fund in exchange solely for the Acquiring Fund Shares and the assumption by the Acquiring Fund of the Acquired Fund’s liabilities or upon the distribution of the Acquiring Fund Shares to the Acquired Fund’s shareholders in exchange for their shares of the Acquired Fund.

(c) No gain or loss will be recognized by the Acquiring Fund upon the receipt by it of all of the assets of the Acquired Fund in exchange solely for Acquiring Fund Shares and the assumption by the Acquiring Fund of the liabilities of the Acquired Fund.

12

(d) The adjusted tax basis of the assets of the Acquired Fund received by the Acquiring Fund will be the same as the adjusted tax basis of such assets to the Acquired Fund immediately prior to the Reorganization.

(e) The holding period of the assets of the Acquired Fund received by the Acquiring Fund will include the holding period of those assets in the hands of the Acquired Fund immediately prior to the Reorganization.

(f) No gain or loss will be recognized by the shareholders of the Acquired Fund upon the exchange of their Acquired Fund Shares for the Acquiring Fund Shares (including fractional shares to which they may be entitled) and the assumption by the Acquiring Fund of the liabilities of the Acquired Fund.

(g) The aggregate adjusted tax basis of the Acquiring Fund Shares received by the shareholders of the Acquired Fund (including fractional shares to which they may be entitled) pursuant to the Reorganization will be the same as the aggregate adjusted tax basis of the Acquired Fund Shares held by the Acquired Fund’s shareholders immediately prior to the Reorganization.

(h) The holding period of the Acquiring Fund Shares received by the shareholders of the Acquired Fund (including fractional shares to which they may be entitled) will include the holding period of the Acquired Fund Shares surrendered in exchange therefore, provided that the Acquired Fund Shares were held as a capital asset on the Closing Date.

Capital losses incurred in tax years beginning prior to December 23, 2010 can generally be carried forward to each of the eight years succeeding the loss year to offset future capital gains. Capital losses incurred in tax years beginning on or after December 23, 2010 can generally be carried forward indefinitely to offset future capital gains. The Fundamental Value Fund will inherit the tax attributes of the Small Companies Fund, including any available capital loss carryforwards, as of the Closing Date. In general, it is not expected that any such capital loss carryforwards will be subject to an annual limitation for federal income tax purposes in connection with the Reorganization because the Reorganization should either: (1) qualify as a type “F” tax-free reorganization under the Code, including a mere change in identity, form or place of reorganization of one corporation, however effected; or (2) not involve more than a 50% change of ownership. For federal income tax purposes, the Small Companies Fund had capital loss carryforwards at June 30, 2011 as follows:

|

Date of Expiration

|

Amount

|

|

|

June 30, 2017

|

$29,086,676

|

A successful challenge to the tax-free status of the Reorganization by the Internal Revenue Service (the “IRS”) would result in a Small Companies Fund shareholder recognizing gain or loss with respect to each Small Companies Fund share equal to the difference between that shareholder’s basis in the share and the fair market value, as of the time of the Reorganization, of the Fundamental Value Fund shares received in exchange therefor. In such event, a shareholder’s aggregate basis in the shares of the Fundamental Value Fund received in the exchange would equal such fair market value, and the shareholder’s holding period for the shares would not include the period during which such shareholder held Small Companies Fund shares.

If any of the representations or covenants of the parties as described herein is inaccurate, the tax consequences of the transaction could differ materially from those summarized above. Furthermore, the description of the tax consequences set forth herein will neither bind the IRS, nor preclude the IRS or the courts from adopting a contrary position. No assurance can be given that contrary positions will not successfully be asserted by the IRS or adopted by a court if the issues are litigated. No ruling has been or will be requested from the IRS in connection with this transaction. No assurance can be given that future legislative, judicial or administrative changes, on either a prospective or retroactive basis, or future factual developments, would not adversely affect the accuracy of the conclusions stated herein. Therefore, shareholders may find it advisable to consult their own tax adviser as to the specific tax consequences to them under the federal income tax laws, as well as any consequences under other applicable state or local or foreign tax laws given each shareholder’s own particular tax circumstances.

Board Considerations

In considering and approving the Reorganization at two meetings held on August 8 and 9, 2011 and September 30, 2011, the PMP Board discussed the future of the Small Companies Fund and the advantages of reorganizing the Small Companies Fund into the Fundamental Value Fund. Among other things, the PMP Board also reviewed, with the assistance of outside legal counsel, the overall proposal for the Reorganization, the principal terms and conditions of the Reorganization Agreement, including that the Reorganization be consummated on a tax-free basis, and certain other materials provided prior to and during the meeting and at other meetings throughout the past year.

13

In considering the Reorganization, the PMP Board took into account a number of additional factors. Some of the more prominent considerations are discussed further below. The PMP Board considered the following matters, among others and in no order of priority:

|

·

|

Both the Small Companies Fund and the Fundamental Value Fund have an investment objective of achieving long-term capital appreciation and have similar principal investment strategies;

|

|

·

|

The fundamental investment restrictions are identical between the two Funds;

|

|

·

|

The Brown Advisory personnel that manage the Small Companies Fund also manage the Fundamental Value Fund;

|

|

·

|

The PMP Board will continue to oversee the Fundamental Value Fund;

|

|

·

|

The management fee for each of the Funds are identical;

|

|

·

|

The contractual expense limitations that Brown Advisory has agreed to maintain for the Small Companies Fund is identical to the contractual expense limitations of the Fundamental Value Fund;

|

|

·

|

Following the Reorganization, the total operating expense ratio for the Fundamental Value Fund is expected to be less than the Small Companies Fund (not including acquired fund fees and expenses);

|

|

·

|

The Rule 12b-1 fees for each Funds’ Advisor Shares are identical;

|

|

·

|

The Reorganization, as contemplated by the Reorganization Agreement, will be a tax free reorganization;

|

|

·

|

The costs of the Reorganization, as contemplated by the Reorganization Agreement, will be borne by Brown Advisory; and

|

|

·

|

The interests of the current shareholders of the Small Companies Fund and the Fundamental Value Fund will not be diluted as a result of the Reorganization.

|

The Board also considered alternatives to the Reorganization, such as the liquidation of the Small Companies Fund. In considering the alternative of liquidation, the Board noted that (1) shareholders not wishing to become part of the Fundamental Value Fund could redeem their shares of the Small Companies Fund at any time prior to closing without penalty and (2) that the Reorganization would allow shareholders of the Small Companies Fund who wished to retain their investment after the Reorganization to do so in a registered mutual fund with a similar investment strategy managed by the very same investment adviser and portfolio team in a substantially similar manner while, at the same time, retaining the benefit of the use of the Small Companies Fund’s capital loss carryforward amounts. The PMP Board also discussed the alternative of maintaining the Small Companies Fund as a stand alone entity. In this regard the Board considered that Brown Advisory was no longer inclined to maintain the management of the Small Companies Fund as a separate entity, since it was so similar to the Fundamental Value Fund.

Furthermore, the Board considered that Rule 17a-8(a)(3) permits a merger of affiliated companies without obtaining shareholder approval if certain conditions are met as noted below:

|

·

|

No fundamental policy of the merging company is materially different from the fundamental policy of the surviving company;

|

|

·

|

No advisory contract between the merging company is materially different from an advisory contract of the surviving company;

|

|

·

|

Trustees of the merging company who are not interested persons of the merging company and who were elected by its shareholders, will comprise a majority of the trustees of the surviving company who are not interested persons of the surviving company; and

|

14

|

·

|

Any distribution fees authorized to be paid by the surviving company pursuant to Rule 12b-1 are no greater than the distribution fees of the merging company.

|

The Board noted that all these conditions had been met. After consideration of the factors noted above, together with other factors and information considered to be relevant, the PMP Board determined that the Reorganization is in the best interests of the Small Companies Fund and Fundamental Values Fund shareholders, and accordingly, unanimously approved the Reorganization with the Fundamental Value Fund and the Reorganization Agreement.

Costs and Expenses of the Reorganization. The Reorganization Agreement provides that all expenses of the Reorganization will be borne by Brown Advisory. Such expenses include, without limitation: (a) expenses associated with the preparation and filing of this information statement/prospectus; (b) postage; (c) printing; (d) accounting fees; and (e) legal fees incurred by PMP.

Capitalization. The following table sets forth the capitalization of the Small Companies Fund and the Fundamental Value Fund, and on a pro forma basis the successor Fundamental Value Fund, as of October 31, 2011 after giving effect to the Reorganization.

|

Fund Capitalization as of October 31, 2011

|

Net Assets

|

Shares Outstanding

|

Net Asset Value

Per Share

|

|

Small Companies Fund

|

$[●]

|

[●]

|

$[●]

|

|

Fundamental Value Fund

|

$[●]

|

[●]

|

$[●]

|

|

Fundamental Value Fund (Pro Forma)

|

$[●]

|

[●]

|

$[●]

|

ADDITIONAL INFORMATION ABOUT THE FUNDS

Investment Adviser. Each Fund’s investment adviser is Brown Advisory, 901 S. Bond Street, Suite 400, Baltimore, Maryland 21231. Brown Advisory is a wholly-owned subsidiary of Brown Investment Advisory & Trust Company, a trust company operating under the laws of Maryland. Brown Investment Advisory & Trust Company is a wholly-owned subsidiary of Brown Advisory Holdings Incorporated, a holdings company incorporated under the laws of Maryland in 1998. Prior to 1998, Brown Investment Advisory & Trust Company operated as a subsidiary of Bankers Trust under the name of Alex. Brown Capital Advisory & Trust Company. Brown Advisory and its affiliates have provided investment advisory and management services to clients for over 10 years. As of October 31, 2011, Brown (excluding an affiliated broker-dealer) had approximately $[●] of assets under management.

Purchase, Redemption and Exchange Policies. The purchase, redemption and exchange policies for the Funds are identical and are highlighted below. For a more complete discussion of the Funds’ purchase, redemption and exchange policies, please see Appendix C.

|

Type of Account

|

Minimum

Initial

Investment

|

Minimum Additional Investment

|

|

Institutional Shares

|

||

|

– Standard Accounts

|

$250,000

|

$100

|

|

– Traditional and Roth IRA Accounts

|

$1,000

|

$0

|

|

– Accounts with Systematic Investment Plans

|

$250

|

$100

|

|

Advisor Shares

|

||

|

– Standard Accounts

|

$2,000

|

$100

|

|

– Traditional and Roth IRA Accounts

|

$1,000

|

N/A

|

|

– Accounts with Systematic Investment Plans

|

$250

|

$100

|

|

– Qualified Retirement Plans

|

N/A

|

N/A

|

15

|

Purchase, Redemption

and Exchange Policies

|

Small Companies Fund

|

Fundamental Value Fund

|

||

|

Purchases

|

By check, wire, telephone, automatic investment plan, through a broker-dealer or other third-party financial intermediary.

|

Same.

|

||

|

Redemptions

|

By check, wire, telephone, systematic withdrawal plan, or electronic funds transfer.

|

Same.

|

||

|

Exchange Privileges

|

Permitted between the same share classes within the Brown Advisory fund family.

|

Same.

|

||

|

Redemption/Exchange Fees

|

1.00% on shares redeemed within 14 days of purchase.

|

Same.

|

||

|

Market Timing Policies

|

The Fund discourages excessive, short-term trading and other abusive trading practices and the Fund may use a variety of techniques to monitor trading activity and detect abusive trading practices. These steps may include, among other things, the imposition of redemption fees, if necessary, monitoring trading activity, or using fair value pricing when appropriate, under procedures as adopted by the PMP Board when Brown Advisory determines current market prices are not readily available. As approved by the Board, these techniques may change from time to time as determined by the Fund in its sole discretion.

|

Same.

|

Distributions. The Small Companies Fund and Fundamental Value Fund generally distribute substantially all of their investment company taxable income and net capital gain, if any, at least annually.

Tax Information. Both Funds’ distributions are taxable, and are taxed as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account.

Payments to Broker-Dealers and Other Financial Intermediaries. If you purchase the Small Companies Fund or the Fundamental Value Fund through a broker-dealer or other financial intermediary (such as a bank), the Funds and/or their related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Small Companies Fund and/or the Fundamental Value Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Investment Advisory Agreement. Under the advisory agreement with PMP, on behalf of both the Small Companies Fund and the Fundamental Value Fund, Brown Advisory supervises the management of the Funds’ investments and business affairs. At its expense, Brown Advisory provides office space and all necessary office facilities, equipment and personnel for servicing the investments of the Fund. As compensation for its services, the Funds each pay to Brown Advisory a monthly advisory fee at the annual rate of 1.00% of the average daily net asset value of the Fund. In addition to the advisory fees, each Fund incurs other expenses such as custodian, transfer agency, interest, Acquired Fund Fees and Expenses and other customary Fund expenses. (Acquired Fund Fees and Expenses are indirect fees that the Fund incurs from investing in the shares of other investment companies.) Brown Advisory has contractually agreed to reduce its fees and/or pay Fund expenses (excluding Acquired Fund Fees and Expenses, interest, taxes and extraordinary expenses) to limit Total Annual Fund Operating Expenses to the amounts shown below of each Class’s average net assets.

16

|

Expense Caps

|

Institutional Shares

|

Advisor Shares

|

|

Brown Advisory Small-Cap Fundamental Value Fund

|

1.40%

|

1.60%

|

|

Brown Advisory Small Companies Fund

|

1.40%

|

1.60%

|

Any reduction in advisory fees or payment of expenses made by Brown Advisory is subject to reimbursement by the Fund if requested by Brown Advisory, and the Board approves such reimbursement in subsequent fiscal years. This reimbursement may be requested by Brown Advisory if the aggregate amount actually paid by a Fund toward operating expenses for such fiscal year (taking into account any reimbursements) does not exceed the Expense Cap. Brown Advisory is permitted to be reimbursed for fee reductions and/or expense payments it made in the prior three fiscal years. The Fund must pay its current ordinary operating expenses before Brown Advisory is entitled to any reimbursement of fees and/or expenses. The current Expense Cap is in place indefinitely, but at a minimum through October 31, 2012. The Expense Cap may be terminated at any time by the Board of Trustees upon 60 days notice to the Advisor, or by the Advisor with the consent of the Board.

Please refer to “Summary – Summary of Fund Expenses” which illustrates the pro forma operating expenses for the Fundamental Value Fund after giving effect to the Reorganization. A discussion regarding the PMP Board’s basis for approving the investment advisory agreement will be included in the Fundamental Value Fund’s next semi-annual report to shareholders for the fiscal period ending December 31, 2011.

Description of the Securities to be Issued; Rights of Shareholders. Set forth below is a description of the Fundamental Value Fund shares to be issued to the shareholders of the Small Companies Fund in the Reorganization. Also set forth below is a discussion of the rights of shareholders of each Fund. Because both Funds are series of PMP, the Funds’ shares have identical characteristics.