UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05009

COLORADO BONDSHARES —

A TAX-EXEMPT FUND

(Exact name of registrant as specified in its charter)

1200 17TH STREET, SUITE 850

DENVER, COLORADO 80202-5808

(Address of principal executive offices) (Zip code)

FRED R. KELLY, JR.

1200 17TH STREET, SUITE 850

DENVER, COLORADO 80202-5808

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-572-6990

Date of fiscal year end: 09/30

Date of reporting period: 09/30/2023

| ITEM 1. | REPORTS TO STOCKHOLDERS | |

| ITEM 2. | CODE OF ETHICS | |

| ITEM 3. | AUDIT COMMITTEE FINANCIAL EXPERT | |

| ITEM 4. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | |

| ITEM 5. | AUDIT COMMITTEE OF LISTED REGISTRANTS | |

| ITEM 6. | INVESTMENTS | |

| ITEM 7. | DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES | |

| ITEM 8. | PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES | |

| ITEM 9. | PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS | |

| ITEM 10. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | |

| ITEM 11. | CONTROLS AND PROCEDURES | |

| ITEM 12. | DISCLOSURE OF SECURITIES LENDING ACTIVITIES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES | |

| ITEM 13. | EXHIBITS | |

| (a)(2)(i) | ||

| (99.302) Interim President’s (Principal Executive Officer) Section 302 Certification | ||

| (a)(2)(ii) | ||

| (99.302) Interim Treasurer’s (Principal Financial Officer) Section 302 Certification | ||

| (b) | ||

ITEM 1. REPORT S TO STOCKHOLDERS.

November 22, 2023

Dear Shareholders:

Almost every penny I have ever made in investing resulted from taking the opposing view. Common wisdom though changing right now says bonds are bad. Turn the clock back as little as just 2 years and you will remember that the most distasteful thing was to leave your money in cash yielding nothing. With the benefit of hindsight, we now know that though it was punitive at the time, cash was precisely the wisest thing to do. It’s easy to see it now, not so easy then. Most felt the need to make their money work a little harder.

Today, we have the mirror image. The safe, reassuring thing to do is to invest short, protect principal and temporarily lock in returns that we have not seen for years. It’s the easy choice which makes me think it’s not the lucrative thing to do. What will the world look like just a couple of years down the road? My view is that it’s better to now take the longer view and lock in to an already established income stream which will endure beyond next week, next month, next year. I might be just a little biased but the best one I know of is Colorado BondShares.

At this stage, we are already in the longest, deepest downturn in the bond market history. Never before have we seen three bad years in a row. Weigh the odds — do you think that such an anomaly already “long in the tooth” continues forever or do you think that at some point it returns to a more normal configuration? No one knows the exact timing of the change but every day that passes, gets us closer to paydirt with potential gains. While you are waiting, you get a dividend approximating 5% (mostly tax exempt) meaning you get to keep most of what you earn and don’t have to share it with anybody. Those of you who are reinvesting your dividends are benefitting from buying more shares at a cheaper cost thereby averaging down and building equity for the future. BondShares was never intended as a get rich quick investment. Instead, it is a time honored, patient method of investing based on potentially generating good income and participating in some healthy gains and the miracle of compounding. It is not well suited for short term analysis and needs time to work best.

Think about the standard thirty-year mortgage on your house. You borrow the purchase price and if you don’t pay it off early you end up paying three times the original amount with two thirds going to interest. Wouldn’t it be nice to be on the other side of that transaction where you more or less put up a

third and prospectively get two times your investment in interest earnings over the years? Looking at it this way, the price paid initially becomes less significant over time because it is the smallest piece of the overall results. Plus, you will get your principal back upon the maturity of the bonds even if there are times when the current market price is listed at less than par. In short, that’s what BondShares offers. The fund has seen some spectacular snap backs in price in the past not that history always repeats or adequately predicts.

Now, please review at your leisure the details of our operations for the fiscal year ended September 30th. I wish they were better with regard to the price but they were positive in most other respects and managed to rank us as #1 in our peer group according to Lipper.

Thank you for hanging in there with us. We value you more than you will ever know.

Sincerely,

Fred R. Kelly, Jr.

Portfolio Manager

Officers and Trustees

George N. Donnelly, Chairman of the Board of Trustees, Interim President, Secretary, Treasurer and Trustee

Bruce G. Ely, Trustee

James R. Madden, Trustee

Fred R. Kelly, Jr., Portfolio Manager

Investment Adviser

Freedom Funds Management Company

Transfer, Shareholder Servicing, and Dividend Disbursing Agent

Freedom Funds Management Company

Distributor

Colorado Financial Service Corporation

Custodian of Portfolio Securities

UMB Bank, N.A.

Independent Registered Public Accounting Firm

Plante & Moran, PLLC

Special Legal Counsel

Kutak Rock LLP

This report is submitted for the general information of the shareholders of Colorado BondShares — A Tax-Exempt Fund. This report must be preceded or accompanied by a Prospectus of the Fund. The prospectus contains information concerning the investment policies and expenses of the portfolio in addition to other pertinent information. Shares of Colorado BondShares — A Tax-Exempt Fund are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including possible loss of the principal amount invested.

FEDERAL INCOME TAX INFORMATION

(unaudited)

The Fund hereby designates the following amount for the Fund’s fiscal year ended September 30, 2023:

Exempt interest dividends: 94.10%

In early 2024, shareholders will receive information regarding all dividends and distributions paid to them by the Fund during calendar year 2023. Regulations of the U.S. Treasury Department require the Fund to report this information to the Internal Revenue Service.

Individual shareholders should refer to their Form 1099s or other tax information to determine the calendar year amounts to be included on their 2023 tax returns. Shareholders should consult their tax advisers.

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

The fiscal year ended September 30, 2023 marked the second year of the Federal Reserve’s campaign to slow inflation by increasing interest rates. Although the outcomes of higher rates did not materialize immediately, many parts of economy and financial markets are now feeling their effects. Economic activity is slowing in the US and the valuations of many financial assets have declined. Fortunately, inflation has decreased off its highs too. Colorado BondShares — A Tax Exempt Fund (“Fund”) has not been immune to these policies, as reflected by the price of the Fund, which is hovering around an all-time low. Even though the interest rate hikes have pushed down the Fund’s price from its high, the fundamentals of the Fund’s underlying investments are still robust, highlighting the merits of the Fund’s strategy to focus on conservatively positioned investments.

As of September 2023, inflation in the US had declined notably from its peak. However, it is still too high from the perspective of the policymakers, motivating them to continue to keep rates at an elevated level. Additionally, the strength of the US labor market is supporting their position that the economy can handle high rates for the time being. Since there is a lag in the transmission of interest rate changes, the trick will be properly timing when to adjust the policy. High rates have already had a notable effect on banks, one of the economy’s most important asset classes. Rising interest rates have adversely impacted the value of their long-term holdings, causing some to collapse (Silicon Valley Bank), others to be forced into a fire-sale (First Republic Bank), and the remaining ones to tighten their lending standards. The repercussions of these events are reducing the availability of credit, a pivotal ingredient of economic growth. Engineering a soft landing is a difficult task, especially when the economies of China and Europe are slowing as well, and one should not be surprised if the Federal Reserve overshoots on the downside. The possibility of this scenario is accounted for in the Fund’s current positioning, and the Fund will look to capitalize on this situation, if it arises, by buying attractively priced bonds.

Like the US economy, Colorado’s economy continues to expand but at a slower pace. Although the state was not the recipient of as many corporate relocations this year as in years past, it was successful in one very important one. At the end of July, the federal government announced that the headquarters of Space Command will remain in Colorado Springs instead of moving to Huntsville, Alabama. Not only does Space Command currently employ a large number of individuals, but it also has the potential to grow markedly in the future. Furthermore, the growth of Space Command should benefit the private industries that serve it, particularly aerospace companies. Since Colorado has the second largest aerospace economy in the US, this decision will further strengthen this cluster, which is one of the state’s economic pillars along with technology, energy, and finance. Colorado should benefit tremendously from this.

A large portion of the Fund’s investments are secured by property taxes connected to residential real estate. As mortgage rates have increased to levels not seen in over 20 years, home sales have declined significantly. However, existing home sales have fallen by much more than new homes sales, and it is important to highlight why. First, most of the largest homebuilders operating in Colorado are publicly traded companies that use low amounts of debt. Additionally, their business models are based on turnover rather than margin, which motivates them to discount the selling price of new homes to drive/maintain the pace of sales. Recently, this discount has been expressed through interest rate buy-downs, which has lowered the overall price of a new home, thereby driving demand. Second, most existing homeowners have already locked in a low mortgage rate. Consequently, if they moved laterally, their monthly mortgage payment would increase notably as a result of the new rate. This is motivating people to remain in their existing homes, which is putting downward pressure on the existing inventory of homes and pushing homebuyers to the new

1

home sales market. This has positive ramifications for many of the bonds owned by the Fund. The proceeds of these bonds are usually used to finance the infrastructure of large residential developments — roads, water, and utilities — and they are repaid with a portion of the property taxes on the homes that are eventually built within that development. Therefore, their financial health is more closely tied to the new home sales market than the existing home sales market, which is larger and often drives many of the statistics cited across the media. The resilience of the new home sales market is supporting the fundamentals of these investments.

Some of the Fund’s investments are secured by property taxes connected to commercial real estate. The interest rate increases have affected the valuation of these asset classes as well but not uniformly across all sectors. Office valuations have been the most adversely impacted of all the commercial real estate sectors, stemming from high vacancy rates and limited financing options. These trends have been especially pronounced in class B buildings. Fortunately, the Fund has very limited exposure to the office market, allowing it to avoid the fallout that is occurring. The fundamentals of the industrial market have slowed from their frenzied high but are still strong, driven by the change in the retail distribution channel from in person at stores to online through warehouses. As a result of the strong industrial fundamentals over the past few years, a record-breaking amount of supply was completed or started construction, increasing the risk of investing in the sector. To mitigate risk, the Fund only invested in a handful of deals backed by industrial buildings that were conservatively structured and that had sizable pre-leasing already in place. Apartment rents surged after COVID lockdowns were lifted, motivating developers to start numerous projects. Denver’s development pipeline is currently greater than 30,000 units. Although this level of supply is very high from a historical perspective, it will most likely only cause indigestion. Most of the US, including Denver, is dealing with a housing shortage, and this added supply should be absorbed as a result of that situation, even if in a choppy manner. Finally, even though the COVID lockdowns created a very difficult environment for retail real estate, the sector’s fundamentals have been improving of late, supported by a dearth of new supply. Most of the Fund’s exposure to retail real estate is focused on convenience retail situated near large residential housing developments, which is benefiting from the current environment.

The Fund also has a notable allocation to bonds secured by charter schools. This sector has many favorable characteristics. Charter schools receive funding on a per pupil basis. In order to boost/maintain funding, the school’s administrators need to increase/sustain enrollment, which is often correlated to their students achieving high test scores. This creates accountability with the teachers and school administrators, which drives them to excel at teaching while being mindful of costs. Additionally, these bonds are typically collateralized by real estate, providing another layer of downside protection. The administrators of the charter schools backing the Fund’s investments showed their talents over recent years as they were able to maintain enrollment levels despite the turbulent environment, thereby supporting the credit of the underlying bonds.

For most of the year, yields in the municipal bond market were range-bound, resulting in the majority of the return of these bonds being driven by their coupon rather than fluctuations in the value of their principal. A similar situation unfolded within many other parts of the bond market, such as investment grade and high yield bonds. However, towards the end of the fiscal year, the yields of long-dated Treasuries began to rise. These increases adversely affected the value of the municipal and overall bond markets. If the yields in the Treasury market continue to rise, they could have a negative impact on the prices in the municipal bond market. However, the Fund capitalized on the recent rate increases by purchasing new bonds at discounted prices, which then increased the Fund’s dividend. The Fund will likely execute similar strategy if rates continue rising in the future.

2

For the year ending September 30, 2023, the Fund produced a total return of 4.21%, when excluding its sales charge. Although the Fund produced a positive total return for the year, its price still remains at a subdued level versus where it has traded historically. This has been driven by the elevated yields in the Treasury market, which have been influenced by the interest rate increases implemented by the Federal Reserve. The credit profiles of the Fund’s underlying investments remain strong, and these investments continue to produce a stable stream of cash flows, which have been used to support the Fund’s dividend. During the year, the Fund distributed $0.45 versus $0.38 last year, an increase of 18%. The rise of the dividend was driven by using the Fund’s large cash balance to opportunistically buy attractively priced bonds over the last two years. Finally, the Fund continues to perform well versus its competitors. According to Lipper Inc., the Fund was ranked as the number one performing municipal bond fund in its class. This outperformance was driven by a handful of factors, such as creating a diversified portfolio with a sizeable allocation to variable rate securities and cash, not using leverage to augment returns, and diligently underwriting and monitoring all investments to ensure that the Fund only acquires and owns bonds with robust credit profiles.

3

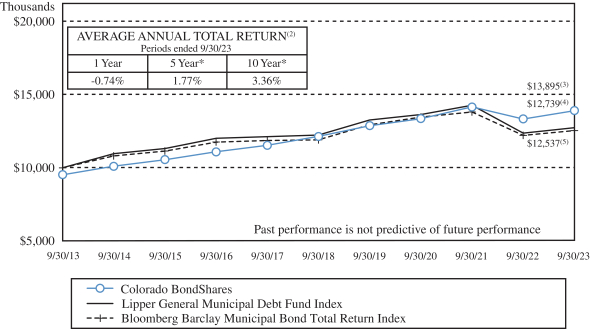

PERFORMANCE SUMMARY (Unaudited)

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN

COLORADO BONDSHARES(1)

THE LIPPER GENERAL MUNICIPAL DEBT FUND INDEX(4)

AND THE BLOOMBERG BARCLAY MUNICIPAL BOND TOTAL RETURN INDEX(5)

| (1) | Total return is the percentage change in the value of a hypothetical investment that has occurred in the indicated period of time, taking into account the imposition of the sales charge and other fees and assuming the reinvestment of all dividends and distributions. Past performance is not indicative of future performance. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares of the Fund. |

| * | Fiscal year ended September 30, 2016 includes a principal write down of approximately $14.5 million due to an adverse decision by the Colorado State Court of Appeal on the Marin Metropolitan District bonds that is a non-recurring event outside of the control of the Fund. |

| (2) | Average annual total return reflects the hypothetical annually compounded return that would have produced the same cumulative total return if the Fund’s performance had been constant over the entire period. Average annual total returns for the one-year, five-year and ten-year periods ended September 30, 2023 are -0.74%, 1.77%, and 3.36%, respectively. Average annual total includes the imposition of the sales charge and assumes the reinvestment of all dividends and distributions. Past |

4

| performance is not indicative of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares of the Fund. |

| (3) | Includes reinvestment of dividends and adjustment for the maximum sales charge of 4.75%. |

| (4) | The Lipper General Municipal Debt Fund Index is a non-weighted index of the 30 largest funds that invest at least 65% of assets in municipal debt issues in the top four credit ratings. The Lipper General Municipal Debt Fund Index reflects no deductions for fees, expenses or taxes, includes reinvestment of dividends but does not reflect any adjustment for sales charge. |

| (5) | The Bloomberg Barclay Municipal Bond Total Return Index which replaced the Barclays Capital Municipal Bond Total Return Index (the “Barclay Index”) is considered representative of the broad market for investment grade, tax-exempt and fixed-rate bonds with long-term maturities (greater than two years) selected from issues larger than $50 million. You cannot invest directly in this index. This index is not professionally managed and does not pay any commissions, expenses or taxes. If this index did pay commissions, expenses or taxes, its returns would be lower. The Fund selected the Bloomberg Barclay Index to compare the returns of the Fund to an appropriate broad-based securities market index. You should note, however, that there are some fundamental differences between the portfolio of securities invested in by the Fund and the securities represented by the Bloomberg Barclay Index. Unlike the Fund which invests primarily in not rated securities on issues of any size, the Bloomberg Barclay Index only includes securities with a rating of at least “Baa” by Moody’s Investor Services, Inc. from an issue size of no less than $50 million. Some of these differences between the portfolio of the Fund and the securities represented by the Bloomberg Barclay Index may cause the performance of the Fund to differ from the performance of the Bloomberg Barclay Index. |

5

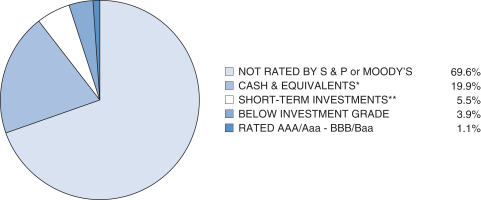

CREDIT QUALITY (unaudited)

Colorado BondShares — A Tax-Exempt Fund

Based on a Percentage of Total Net Assets as of September 30, 2023

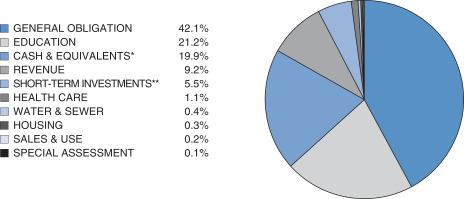

SECTOR BREAKDOWN (unaudited)

Colorado BondShares — A Tax-Exempt Fund

Based on a Percentage of Total Net Assets as of September 30, 2023

* Cash & equivalents include cash and receivables less liabilities.

** Short-term investments include securities with a maturity date or redemption feature of one year or less, as identified in the Schedule of Investments.

6

Officers and Trustees of the Fund

The following tables list the trustees and officers of the Fund, together with their address, age, positions held with the Fund, the term of each office held and the length of time served in each office, principal business occupations during the past five years and other directorships, if any, held by each trustee and officer. Each trustee and officer has served in that capacity for the Fund continuously since originally elected or appointed. The Board of Trustees supervises the business activities of the Fund. Each trustee serves as a trustee until termination of the Fund unless the trustee dies, resigns, retires, or is removed. The Statement of Additional Information of the Fund includes additional information about Fund trustees and is available, without charge, upon request. Shareholders may call (800) 572-0069 to request the Statement of Additional Information.

| Name, Address and Age |

Position held with the Fund and Length of Time Served |

Principal Occupation During the Past Five Years: |

Other Directorships Held By Director | |||

| Non-Interested Trustees | ||||||

| Bruce G. Ely 1200 17th Street, Suite 850 Denver CO 80202 Age: 72 |

Trustee since July 2002 | Mr. Ely was a Regional Director for Cutwater Asset Management, a wholly owned subsidiary of MBIA, Inc., until his retirement in September 2013. | None | |||

| James R. Madden 1200 17th Street, Suite 850 Denver CO 80202 Age: 79 |

Trustee since September 2004 | Mr. Madden has owned Madden Enterprises, a real estate company that owns and leases commercial buildings and real estate, for the past thirty years. He is also a stockholder and director of The Community Bank in western Kansas. He has been a bank director for 25 years. | None | |||

| Interested Trustees* | ||||||

| George N. Donnelly 1200 17th Street, Suite 850 Denver CO 80202 Age: 76 |

Chairman of the Board of Trustees, Trustee since inception of the Fund in 1987 and Interim President, Secretary and Treasurer of the Fund since September 26, 2008 | Mr. Donnelly was a Senior Regional Vice President for Phoenix Life Insurance Company until his retirement in January 2010. | None | |||

*George N. Donnelly is an “interested person” of the Fund as defined in the Investment Company Act of 1940 (the “1940 Act”) by virtue of his position as both an officer and a trustee of the Fund as described in the table above. None of the trustees nor the officers of the Fund have any position with the Investment Adviser, the principal underwriter of the Fund, the distribution agent of the Fund, the service agent of the Fund or the custodian of the Fund, or any affiliates thereof. There is no family relationship between any officers and trustees of the Fund.

7

Compensation

The Board met two times during the fiscal year ended September 30, 2023. The following tables show the compensation paid by the Fund to each of the trustees during that year:

| Name of Person, Position(s) with the Fund |

Aggregate Compensation from Fund |

Pension or Retirement Benefits Accrued As Part of Fund Expenses |

Total Compensation from Fund Paid to Such Person |

|||||||||

| Non-Interested Trustees |

||||||||||||

| Bruce G. Ely, Trustee |

$ | 2,000 | N/A | $ | 2,000 | |||||||

| James R. Madden, Trustee |

2,000 | N/A | 2,000 | |||||||||

| Interested Trustees |

||||||||||||

| George N. Donnelly, Trustee, Interim President, Secretary and Treasurer |

1,000 | N/A | 1,000 | |||||||||

No officer or trustee of the Fund received remuneration from the Fund in excess of $60,000 for services to the Fund during the fiscal year ended September 30, 2023. The officers and trustees of the Fund, as a group, received $5,000 in compensation from the Fund for services to the Fund during the 2023 fiscal year.

Other Information

Proxy Voting Record

The Fund does not invest in equity securities. Accordingly, there were no matters relating to a portfolio security considered during the 12 months ended June 30, 2023 with respect to which the Fund was entitled to vote. Applicable regulations require us to inform you that the foregoing proxy voting information is available on the SEC website at http://www.sec.gov or you may call us at 1-800-572-0069.

Quarterly Statement of Investments

The Fund files a complete schedule of investments with the Securities and Exchange Commission for the first and third quarters of each fiscal year. For periods ending prior to March 31, 2019, this information was filed on Form N-Q. For periods ending on or after March 31, 2019, the Fund will file on Form N-PORT. Shareholders may view the filed Form N-Q and N-PORT by visiting the Commission’s website at http://www.sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling 1-800-732-0330 or you may call us at 1-800-572-0069.

8

Trustees Approve Advisory Agreement

The Board of Trustees (the “Trustees”) of Colorado BondShares — A Tax-Exempt Fund unanimously approved the continuance of the Fund’s Investment Advisory and Service Agreement with Freedom Funds Management Company (“Freedom Funds”) at a meeting held on October 5, 2023. In approving the Advisory Agreement, the Trustees, including the disinterested trustees, considered the reasonableness of the advisory fee in light of the extent and quality of the advisory services provided and any additional benefits received by Freedom Funds or its affiliates in connection with providing services to the Fund, compared the fees charged by Freedom Funds to those paid by similar funds, and analyzed the expenses incurred by Freedom Funds with respect to the Fund. The Trustees also considered the Fund’s performance relative to a selected peer group, the expense ratio of the Fund in comparison to other funds of comparable size, and other factors. The Trustees determined that the Fund’s advisory fee structure was fair and reasonable in relation to the services provided and that approving the agreement was in the best interests of the Fund and its shareholders. Matters considered by the Trustees in connection with its consideration of the Advisory Agreement included, among other things, the following:

1. Investment Adviser Services

Freedom Funds manages the assets of the Fund, including making purchases and sales of portfolio securities consistent with the Fund’s investment objectives and policies. In addition, Freedom Funds administers the Fund’s daily business affairs such as providing accurate accounting records, computing accrued income and expenses of the Fund, computing the daily net asset value of the Fund, assuring proper dividend disbursements, proper financial information to investors, and notices of all shareholders’ meetings, and providing sufficient office space, storage, telephone services, and personnel to accomplish these responsibilities. In considering the nature, extent and quality of the services provided by Freedom Funds, the Trustees believe that the services provided by Freedom Funds have provided the Fund with superior results. At the same time, Freedom Fund’s fee structure is equal to or lower than the comparable funds. The Trustees noted the Fund’s focus is inherently more labor intensive. Under the circumstances, the Trustees found the fee structure to be justified.

2. Investment Performance

The Trustees reviewed the performance of the Fund compared to other similar funds, and reported that the current (as of September 30, 2023) net asset value was $8.41 per share and the current distribution yield (based on net asset value) was 5.54% (also as of September 30, 2023). Since the overall structure of the portfolio was satisfactory and the performance of the Fund, measured in terms of distribution yield and total return, was comparable amongst its peer group, no changes to either the type of assets or manner of operations were recommended.

3. Expense Ratios

The Trustees reviewed the performance (measured by distribution yield), fees and expense ratios of all municipal bond funds in our peer group. The Trustees considered the fact that the Fund’s unique focus on non-rated bonds, while geared toward producing superior investment results, often required additional expenses. While expenses can vary with non-rated bonds (principally as a result of litigation with respect to defaulted issues and higher monitoring costs occasioned by less readily available information), the Trustees noted the Fund’s performance for the current year.

9

4. Management Fees and Expenses

The Trustees reviewed the investment advisory fee rates payable by the Fund to Freedom Funds. As part of its review, the Trustees considered the estimated advisory fees and the Fund’s estimated total expense ratio for the one-year period as of October 2023 as compared to other municipal bonds in its peer group identified by Freedom Funds. After reviewing the foregoing information, and in light of the nature, extent and quality of the services provided by Freedom Funds, the Trustees concluded that the advisory fees charged by Freedom Funds for the advisory and related services to the Fund and the Fund’s total expense ratio are reasonable. The management fee is one half of one percent of total net assets managed. Such fee is payable to Freedom Funds on a monthly basis. This fee is comparable to other municipal bond funds identified by Freedom Funds and is consistent with national funds many times the Fund’s size.

5. Profitability

The Trustees reviewed the level of profits realized by Freedom Funds and relevant affiliates thereof in providing investment and administrative services to the Fund. The Trustees considered the level of profits realized without regard to revenue sharing or other payments by Freedom Funds and its affiliates to third parties in respect to distribution of the Fund’s securities. The Trustees also considered other direct or indirect benefits received by Freedom Funds and its affiliates in connection with its relationship with the Fund and found that there were none. The Trustees concluded that, in light of the foregoing factors and the nature, extent and quality of the services provided by Freedom Funds, the profits realized by Freedom Funds are reasonable.

6. Economies of Scale

In reviewing advisory fees and profitability, the Trustees also considered the extent to which Freedom Funds and its affiliates, on the one hand, and the Fund, on the other hand, can expect to realize benefits from economies of scale as the assets of the Fund increase. The Trustees acknowledged the difficulty in accurately measuring the benefits resulting from the economies of scale with respect to the management of any specific fund or group of funds, particularly in an environment where costs are rising due to changing regulations. The Trustees reviewed data summarizing the increases and decreases in the assets of the Fund over various time periods, and evaluated the extent to which the total expense ratio of the Fund and Freedom Fund’s profitability may have been affected by such increases or decreases. Between October 2022 and September 30, 2023, total net assets of the Fund under management by Freedom Funds decreased from $1,675.7 billion to $1,646.1 billion. The number of shares of the Fund that have been redeemed has been less than the number of new shares issued by the Fund, and as a result the Fund continues to grow at what the Trustees determined was a healthy level.

Based upon the foregoing, the Trustees concluded that the benefits from the economies of scale are currently being shared equitably by Freedom Funds and the Fund. The Trustees also concluded that the structure of the advisory fee can be expected to cause Freedom Funds, its affiliates and the Fund to continue to share such benefits equitably and that breakpoints need not be instituted at this time.

After requesting and reviewing these and other factors that they deemed relevant, the Trustees concluded that the continuation of the Advisory Agreement was in the best interest of the Fund and its shareholders.

10

Freedom Funds also serves as the transfer agent, shareholder servicing agent and dividend disbursing agent for the Fund, pursuant to a Transfer Agency and Service Agreement (the “Service Agreement”).

Freedom Funds’ duties under the Service Agreement include processing purchase and redemption transactions, establishing and maintaining shareholder accounts and records, disbursing dividends declared by the Fund and all other customary services of a transfer agent, shareholder servicing agent and dividend disbursing agent. As compensation for these services, the Fund may pay Freedom Funds at a rate intended to represent Freedom Funds’ cost of providing such services. This fee would be in addition to the investment advisory fee payable to Freedom Funds under the Advisory Agreement.

11

FUND EXPENSES (unaudited)

The following examples are intended to help you understand the ongoing costs (in dollars) of investing in the Fund and compare these costs with those of other mutual funds. The examples (actual and hypothetical 5% return) are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

As a shareholder of Colorado BondShares — A Tax-Exempt Fund (the “Fund’) you can incur two types of costs:

| • | Sales charges (front loads) on fund purchases and |

| • | Ongoing fund costs, including management fees, administrative services, and other fund expenses. All mutual funds have operating expenses. Operating expenses, which are deducted from the Fund’s gross income, directly reduce the investment return of the Fund. |

Actual Fund Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in shareholder reports of other funds.

Six Months Ended September 30, 2023

| Colorado BondShares — A Tax- Exempt Fund |

Beginning Account Value 04/01/23 |

Ending Account Value 09/30/23 |

Expenses Paid During Period(1) | ||||||||||||

| Based on Actual Fund Return |

$ | 1,000.00 | $ | 995.21 | $ | 3.05 | |||||||||

| Based on Hypothetical 5% Annual Return Before Expenses |

$ | 1,000.00 | $ | 1,021.95 | $ | 3.09 | |||||||||

| (1) | The expenses shown in this table are equal to the Fund’s annualized expense ratio of 0.61% for fiscal year ended September 30, 2023, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. |

Please note that expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher. You can find more information about the Fund’s expenses in the Financial Statements section of this report. For additional information on operating costs please see the Fund’s prospectus.

12

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of

Colorado BondShares — A Tax-Exempt Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Colorado BondShares — A Tax-Exempt Fund (the “Fund”) as of September 30, 2023, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years ended September 30, 2023 and 2022, and the related notes (collectively referred to as the “financial statements”) and the financial highlights for each of the five years ended September 30, 2023. In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Colorado BondShares — A Tax-Exempt Fund as of September 30, 2023, the results of its operations for the year then ended, the changes in net assets for each of the two years ended September 30, 2023 and 2022, and the financial highlights for each of the five years ended September 30, 2023, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

The Fund’s management is responsible for these financial statements and financial highlights. Our responsibility is to express an opinion on the Fund’s financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audits also included evaluating the

13

accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of September 30, 2023 by correspondence with the custodian and the transfer agent. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2014.

Grand Rapids, Michigan

November 27, 2023

14

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments

September 30, 2023

| Colorado Municipal Bonds 67.3% | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado 100.0% | ||||||||||||||||||

| Aberdeen MD #1 – Series A – 2035 |

12/1/2035 | 7.50% | $ | 1,600,000 | $ | 476,000 | ||||||||||||

| Anthology West MD #4 – Series A – 2041(g) |

12/15/2041 | 6.25% | 1,100,000 | 977,273 | ||||||||||||||

| Anthology West MD #5 – Series A – 2049 |

12/1/2049 | 4.88% | 4,630,000 | 3,658,533 | ||||||||||||||

| Anthology West MD #5 – Series B – 2049(g) |

12/15/2049 | 7.63% | 698,000 | 607,658 | ||||||||||||||

| Aspen Street MD – Series A – 2050(g) |

12/1/2050 | 5.13% | 4,300,000 | 3,227,322 | ||||||||||||||

| Banning Lewis Ranch Regional MD – Series A – 2048 |

12/1/2048 | 5.38% | 2,500,000 | 2,255,925 | ||||||||||||||

| Banning Lewis Ranch Regional MD – Series B – 2041(g) |

12/15/2041 | 7.75% | 625,000 | 573,775 | ||||||||||||||

| Base Village MD #2 – Series B – 2048(g) |

12/15/2048 | 6.50% | 3,500,000 | 2,223,410 | ||||||||||||||

| Belford North MD – Series A – 2050 |

12/1/2050 | 5.50% | 4,000,000 | 3,352,560 | ||||||||||||||

| Belford North MD – Series B – 2050(g) |

12/15/2050 | 8.50% | 3,475,000 | 3,094,661 | ||||||||||||||

| Bennett Crossing MD #1 – Series A – 2049 |

12/1/2049 | 6.13% | 6,160,000 | 5,636,708 | ||||||||||||||

| Bennett Ranch MD #1 – Series A – 2051 |

12/1/2051 | 5.00% | 3,000,000 | 2,405,430 | ||||||||||||||

| Bennett Ranch MD #1 – Series B – 2051(g) |

12/15/2051 | 7.50% | 1,221,000 | 1,044,553 | ||||||||||||||

| Bent Grass MD – Series A – 2049 |

12/1/2049 | 5.25% | 1,690,000 | 1,473,494 | ||||||||||||||

| Bradburn MD #2 – Series C – 2051(g) |

12/15/2051 | 7.50% | 3,271,000 | 2,789,542 | ||||||||||||||

| Bramming Farm MD #1 – Series A – 2044 |

12/1/2044 | 6.00% | 1,910,000 | 1,731,740 | ||||||||||||||

| Brighton Crossing MD #4 – Series A – 2037 |

12/1/2037 | 5.00% | 1,050,000 | 981,866 | ||||||||||||||

| Brighton Crossing MD #4 – Series A – 2047 |

12/1/2047 | 5.00% | 4,685,000 | 4,103,498 | ||||||||||||||

| Brighton Crossing MD #4 – Series B – 2047(g) |

12/1/2047 | 7.00% | 670,000 | 586,840 | ||||||||||||||

| Brighton Crossing MD #6 – Series A – 2035 |

12/1/2035 | 5.00% | 525,000 | 477,136 | ||||||||||||||

| Brighton Crossing MD #6 – Series A – 2040 |

12/1/2040 | 5.00% | 1,545,000 | 1,321,547 | ||||||||||||||

| Brighton Crossing MD #6 – Series A – 2050 |

12/1/2050 | 5.00% | 9,020,000 | 7,255,417 | ||||||||||||||

| Broomfield Village MD #2 – Series A – 2049 |

12/1/2049 | 5.00% | 1,480,000 | 1,266,688 | ||||||||||||||

| Buckley Yard MD #2 – Series A – 2052 |

12/1/2052 | 6.25% | 6,800,000 | 6,199,900 | ||||||||||||||

| Buckley Yard MD #2 – Series B – 2052(g) |

12/15/2052 | 9.25% | 1,569,000 | 1,471,691 | ||||||||||||||

| Castleview MD #2 – Series A – 2050 |

12/1/2050 | 5.00% | 3,435,000 | 2,770,843 | ||||||||||||||

| Castleview MD #1 – Series A – 2050(g) |

12/1/2050 | 5.00% | 4,727,000 | 3,553,806 | ||||||||||||||

| Cherry Creek South MD #5 – Series A – 2051(g) |

12/1/2051 | 6.00% | 22,500,000 | 17,240,400 | ||||||||||||||

| Cherry Hills City MD – Series A – 2047(g) |

12/1/2047 | 5.00% | 1,380,000 | 1,134,760 | ||||||||||||||

| Cielo MD – Series A – 2050(g) |

12/1/2050 | 5.25% | 12,442,000 | 9,506,683 | ||||||||||||||

| City Center West Residential MD #2 – Series A – 2049 |

12/1/2049 | 5.00% | 2,080,000 | 1,749,155 | ||||||||||||||

| City Center West Residential MD #2 – Series B – |

12/15/2049 | 7.75% | 1,425,000 | 1,244,339 | ||||||||||||||

| Cityset MD #2 – Series A – 2030 |

12/1/2030 | 3.50% | 5,625,000 | 4,838,681 | ||||||||||||||

| Cityset MD #2 – Series A – 2040 |

12/1/2040 | 4.38% | 8,360,000 | 6,824,602 | ||||||||||||||

| Cityset MD #2 – Series A – 2045 |

12/1/2045 | 4.50% | 3,180,000 | 2,510,006 | ||||||||||||||

15

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| Clear Creek Transit MD #2 – Series A – 2050 |

12/1/2050 | 5.00% | $ | 2,000,000 | $ | 1,617,180 | ||||||||||||

| Cloverleaf MD – Series A – 2051 |

12/1/2051 | 6.00% | 2,330,000 | 2,166,853 | ||||||||||||||

| Cloverleaf MD – Series B – 2051(g) |

12/15/2051 | 9.25% | 1,034,000 | 999,402 | ||||||||||||||

| Colliers Hill MD #3 – Series A – 2040 |

12/1/2040 | 5.25% | 8,300,000 | 7,455,641 | ||||||||||||||

| Colliers Hill MD #3 – Series A – 2048 |

12/1/2048 | 5.50% | 18,250,000 | 16,060,183 | ||||||||||||||

| Colliers Hill MD #3 – Series B – 2043(g) |

12/15/2043 | 8.50% | 2,213,000 | 1,922,610 | ||||||||||||||

| Colorado Centre MD – Series B – 2032(g)(i) |

1/1/2032 | 0.00% | 6,592,306 | 3,427,999 | ||||||||||||||

| Colorado Centre MD – Series A – 2027(e)(i) |

1/1/2027 | 0.00% | 2,074,674 | 1,778,037 | ||||||||||||||

| Colorado Centre MD – Series A – 2027(f)(i) |

1/1/2027 | 9.00% | 2,131,449 | 1,428,071 | ||||||||||||||

| CECFA Swallow Academy – Series A – 2027(m) |

11/15/2027 | 5.35% | 3,245,000 | 3,053,870 | ||||||||||||||

| CECFA Addenbrooke Classical Academy – Series A – 2027(m) |

6/1/2027 | 4.50% | 24,385,000 | 23,561,031 | ||||||||||||||

| CECFA Imagine Charter School at Firestone – Series A – 2027(m) |

6/1/2027 | 4.50% | 17,380,000 | 16,792,730 | ||||||||||||||

| CECFA Monarch Montessori – Series A – 2025(m) |

5/15/2025 | 4.75% | 8,325,000 | 8,068,507 | ||||||||||||||

| CECFA Academy Of Advanced Learning – Series A – 2027(m) |

6/1/2027 | 4.38% | 8,420,000 | 7,809,718 | ||||||||||||||

| CECFA Chavez/Huerta Preparatory – Series A – |

7/1/2027 | 4.38% | 36,520,000 | 34,588,092 | ||||||||||||||

| CECFA Swallows Charter Academy – Series A – |

11/15/2027 | 4.38% | 6,560,000 | 5,953,856 | ||||||||||||||

| CECFA Vanguard Classical School – Series A – |

7/1/2027 | 4.38% | 24,045,000 | 21,998,530 | ||||||||||||||

| CECFA Third Future School – Series A – 2029(m) |

7/1/2029 | 4.25% | 5,645,000 | 4,867,401 | ||||||||||||||

| CECFA Grand Peak Academy – Series A – 2031(m) |

7/1/2031 | 4.00% | 2,150,000 | 1,782,823 | ||||||||||||||

| CECFA Grand Peak Academy – Series A – 2041(m) |

7/1/2041 | 4.25% | 5,040,000 | 3,579,005 | ||||||||||||||

| CECFA Grand Peak Academy – Series A – 2051(m) |

7/1/2051 | 4.50% | 13,070,000 | 8,639,924 | ||||||||||||||

| CECFA Doral Academy – Series A – 2028(m) |

7/15/2028 | 4.50% | 19,405,000 | 17,613,919 | ||||||||||||||

| CECFA Civica Career & Collegiate Academy – Series A – 2029(m) |

7/15/2029 | 4.75% | 7,790,000 | 7,088,121 | ||||||||||||||

| CECFA Chavez/Huerta Academy – Series A – 2027(m) |

7/1/2027 | 4.50% | 8,220,000 | 7,819,193 | ||||||||||||||

| CECFA Mountain Sage Community School – Series A – 2029(m) |

7/1/2029 | 4.75% | 8,760,000 | 8,266,286 | ||||||||||||||

| CECFA Mountain Song Community School – Series A – 2029(m) |

7/1/2029 | 4.75% | 5,810,000 | 5,487,952 | ||||||||||||||

| CECFA CEC / Aurora Charter School – Series A – |

7/1/2032 | 5.00% | 80,470,000 | 75,622,487 | ||||||||||||||

16

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| CECFA CEC / CSEC BC Project – Series A – 2032(m) |

1/1/2032 | 4.88% | $ | 4,060,000 | $ | 3,825,170 | ||||||||||||

| CECFA CEC / CSEC BC Project – Series A – 2037(m) |

1/1/2037 | 5.00% | 3,595,000 | 3,309,485 | ||||||||||||||

| CECFA CEC / CSEC BC Project – Series A – 2042(m) |

1/1/2042 | 5.13% | 40,335,000 | 36,511,645 | ||||||||||||||

| CECFA Global Village Academy – Senior Bonds – |

6/15/2029 | 5.85% | 11,630,000 | 11,457,643 | ||||||||||||||

| CECFA Fort Collins Montessori School – Series A – 2029(m) |

7/1/2029 | 6.13% | 17,790,000 | 17,728,447 | ||||||||||||||

| Colorado Crossing MD #2 – Series A – 2047 |

12/1/2047 | 5.00% | 4,000,000 | 2,860,080 | ||||||||||||||

| Colorado Crossing MD #2 – Series A – 2050 |

12/1/2050 | 5.00% | 4,000,000 | 2,815,000 | ||||||||||||||

| 700 Kalamath LLC – Series A – 2013(a)(j) |

12/1/2013 | 0.00% | 3,755,000 | 4,000,000 | ||||||||||||||

| CHFA / Casey’s Pond Living – Series A – 2032(l) |

6/1/2032 | 0.00% | 8,110,000 | 4,055,000 | ||||||||||||||

| CHFA / Casey’s Pond Living – Series A – 2042(l) |

6/1/2042 | 0.00% | 10,665,000 | 5,332,500 | ||||||||||||||

| CHFA / Casey’s Pond Living – Series A – 2047(l) |

6/1/2047 | 0.00% | 8,600,000 | 4,300,000 | ||||||||||||||

| Colorado International Center MD #3 – Series A – 2031 |

12/1/2031 | 4.63% | 586,000 | 537,005 | ||||||||||||||

| Conestoga MD #2 – Series A – 2051(g) |

12/1/2051 | 5.25% | 1,625,000 | 1,339,569 | ||||||||||||||

| Conifer MD – Series A – 2030(j) |

12/1/2030 | 0.00% | 10,000,000 | 4,163,366 | ||||||||||||||

| Conifer MD – Series A – 2032(j) |

12/1/2032 | 0.00% | 1,450,000 | 603,688 | ||||||||||||||

| Conifer MD – Series A – 2033(j) |

12/1/2033 | 0.00% | 1,550,000 | 645,322 | ||||||||||||||

| Constitution Heights MD – Series A – 2049 |

12/1/2049 | 5.00% | 1,765,000 | 1,508,581 | ||||||||||||||

| Copperleaf MD #9 – Series A – 2051(g) |

12/1/2051 | 4.88% | 8,175,000 | 5,998,897 | ||||||||||||||

| Country Club Highlands MD – Series A – 2037 |

12/1/2037 | 7.25% | 1,030,000 | 947,600 | ||||||||||||||

| Dacono Urban Renewal Authority – Series A – 2039(g) |

12/1/2039 | 6.25% | 2,969,000 | 2,680,384 | ||||||||||||||

| Dakota Ridge MD – Series A – 2052(g) |

12/1/2052 | 6.00% | 2,339,000 | 1,987,448 | ||||||||||||||

| Deer Creek Villas MD – Series A – 2055 |

12/1/2055 | 5.00% | 6,085,000 | 4,799,422 | ||||||||||||||

| Denver Intl Business Center MD #1 – Series B – 2048(g) |

12/1/2048 | 6.00% | 4,585,000 | 4,327,415 | ||||||||||||||

| Denver West Promenade MD – Series A – 2031 |

12/1/2031 | 5.13% | 500,000 | 482,985 | ||||||||||||||

| Denver West Promenade MD – Series B – 2046(g) |

12/15/2046 | 6.00% | 500,000 | 451,665 | ||||||||||||||

| E86 MD – Series A – 2051(g) |

12/1/2051 | 5.13% | 4,060,000 | 3,126,890 | ||||||||||||||

| Eagle Brook MD – Series A – 2051(g) |

12/1/2051 | 5.00% | 1,600,000 | 1,284,624 | ||||||||||||||

| Erie Highlands MD #2 – Series A – 2048 |

12/1/2048 | 5.25% | 6,000,000 | 5,250,360 | ||||||||||||||

| Erie Highlands MD #2 – Series B – 2048(g) |

12/15/2048 | 7.63% | 1,819,000 | 1,599,247 | ||||||||||||||

| Fitzsimons Village MD #1 – Series A – 2049 |

12/1/2049 | 5.00% | 1,042,000 | 854,325 | ||||||||||||||

| Fitzsimons Village MD #1 – Series B – 2049(g) |

12/15/2049 | 7.00% | 611,000 | 518,953 | ||||||||||||||

| Fitzsimons Village MD #3 – Series A – 2026 |

12/1/2026 | 4.00% | 1,640,000 | 1,530,546 | ||||||||||||||

| Fitzsimons Village MD #3 – Series A – 2031 |

12/1/2031 | 4.00% | 500,000 | 424,210 | ||||||||||||||

| Fitzsimons Village MD #3 – Series A – 2041 |

12/1/2041 | 4.00% | 4,445,000 | 3,144,615 | ||||||||||||||

| Fitzsimons Village MD #3 – Series A – 2055 |

12/1/2055 | 4.25% | 9,660,000 | 6,279,483 | ||||||||||||||

17

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| Flying Horse MD #2 – Series B – 2050(g)(m) |

12/15/2050 | 7.25% | $ | 15,405,000 | $ | 13,335,492 | ||||||||||||

| Flying Horse MD #3 – Series A – 2049(g) |

12/1/2049 | 6.00% | 2,965,000 | 2,648,842 | ||||||||||||||

| Golden Eagle Acres MD #2 – Series A – 2051(g) |

12/1/2051 | 4.50% | 3,325,000 | 2,341,332 | ||||||||||||||

| Green Gables MD #2 – Series B – 2048(g) |

12/15/2048 | 8.25% | 1,689,000 | 1,528,055 | ||||||||||||||

| Green Valley Ranch East MD #6 – Series A – 2050 |

12/1/2050 | 5.88% | 3,325,000 | 3,045,833 | ||||||||||||||

| Greenspire MD #1 – Series A – 2051 |

12/1/2051 | 5.13% | 1,925,000 | 1,590,185 | ||||||||||||||

| Greenways MD #1 – Series A – 2051(g) |

12/1/2051 | 4.63% | 6,845,000 | 4,532,280 | ||||||||||||||

| Hess Ranch MD #6 – Series A – 2049 |

12/1/2049 | 5.00% | 5,000,000 | 4,126,700 | ||||||||||||||

| Hidden Creek MD – Series A – 2045(g) |

12/1/2045 | 4.63% | 3,430,000 | 2,548,936 | ||||||||||||||

| Highlands Mead MD – Series A – 2050 |

12/1/2050 | 5.13% | 1,395,000 | 1,155,771 | ||||||||||||||

| Hogback MD – Series A – 2041 |

12/1/2041 | 5.00% | 725,000 | 626,531 | ||||||||||||||

| Hogback MD – Series A – 2051 |

12/1/2051 | 5.00% | 1,550,000 | 1,252,834 | ||||||||||||||

| Horizon MD #2 – Series A – 2051(g) |

12/1/2051 | 4.50% | 11,657,000 | 7,632,770 | ||||||||||||||

| Hunter’s Overlook MD #5 – Series B – 2049(g) |

12/15/2049 | 8.50% | 1,827,000 | 1,627,601 | ||||||||||||||

| Hunter’s Overlook MD #7 – Series A – 2051(g) |

12/1/2051 | 5.50% | 3,525,000 | 2,961,247 | ||||||||||||||

| Hyland Village MD – Series A – 2027 |

12/1/2027 | 10.00% | 4,770,000 | 2,623,500 | ||||||||||||||

| Indy Oak Tod MD – Series A – 2050 |

12/1/2050 | 5.50% | 1,075,000 | 1,093,920 | ||||||||||||||

| Indy Oak Tod MD – Series B – 2050(g) |

12/15/2050 | 8.00% | 736,000 | 791,428 | ||||||||||||||

| Inspiration MD – Series B – 2036(g) |

12/15/2036 | 5.00% | 788,000 | 670,359 | ||||||||||||||

| Iron Works Village MD – Series A – 2048 |

12/1/2048 | 5.88% | 1,500,000 | 1,548,780 | ||||||||||||||

| Jay Grove MD – Series A – 2051(g) |

12/1/2051 | 4.25% | 2,450,000 | 1,702,554 | ||||||||||||||

| Jefferson Center MD #1 – Series B – 2050(g) |

12/15/2050 | 5.75% | 14,414,000 | 13,039,769 | ||||||||||||||

| Karl’s Farm MD #2 – Series A – 2040 |

12/1/2040 | 5.38% | 1,155,000 | 1,031,889 | ||||||||||||||

| Karl’s Farm MD #2 – Series A – 2050 |

12/1/2050 | 5.63% | 3,030,000 | 2,627,798 | ||||||||||||||

| The Lakes MD #4 – Series A – 2061(g) |

12/1/2061 | 5.50% | 20,080,000 | 15,317,426 | ||||||||||||||

| Lanterns MD #2 – Series A – 2050(g) |

12/1/2050 | 4.50% | 12,492,000 | 8,490,563 | ||||||||||||||

| Legato Community Authority – Series A – 2036 |

12/1/2036 | 4.00% | 2,130,000 | 1,684,574 | ||||||||||||||

| Legato Community Authority – Series A – 2046 |

12/1/2046 | 5.00% | 1,000,000 | 805,220 | ||||||||||||||

| Legato Community Authority – Series A – 2051 |

12/1/2051 | 5.00% | 2,500,000 | 1,956,500 | ||||||||||||||

| Lincoln Meadows MD – Series A – 2031 |

12/1/2031 | 8.00% | 6,775,000 | 7,039,293 | ||||||||||||||

| Littleton Village MD #2 – Series A – 2045 |

12/1/2045 | 5.38% | 1,624,000 | 1,494,486 | ||||||||||||||

| Littleton Village MD #2 – Series B – 2028(g) |

12/15/2028 | 7.63% | 1,140,000 | 1,103,497 | ||||||||||||||

| Loretto Heights Community Authority – Series A – |

12/1/2051 | 4.88% | 12,750,000 | 9,270,398 | ||||||||||||||

| Marin MD – Series A – 2028(a)(j) |

12/1/2028 | 0.00% | 17,485,000 | 1,573,650 | ||||||||||||||

| Mayfield MD – Series A – 2050 |

12/1/2050 | 5.75% | 1,190,000 | 1,086,875 | ||||||||||||||

| Mayfield MD – Series B – 2050(g) |

12/15/2050 | 8.25% | 622,000 | 566,113 | ||||||||||||||

18

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| Mayfield MD – Series C – 2050 |

12/15/2050 | 3.00% | $ | 766,000 | $ | 268,667 | ||||||||||||

| Meadows MD #1 – Series A – 2029(k) |

6/1/2029 | 8.00% | 30,730,000 | 29,426,433 | ||||||||||||||

| Meadows MD #2 – Series A – 2029(k) |

6/1/2029 | 8.00% | 23,830,000 | 22,819,131 | ||||||||||||||

| Meadows MD #7 – Series A – 2029(k) |

6/1/2029 | 8.00% | 15,440,000 | 14,785,035 | ||||||||||||||

| Meadowlark MD – Series A – 2040 |

12/1/2040 | 4.88% | 1,045,000 | 868,176 | ||||||||||||||

| Meadowlark MD – Series A – 2050 |

12/1/2050 | 5.13% | 1,505,000 | 1,247,495 | ||||||||||||||

| Mirabelle MD #2 – Series A – 2049 |

12/1/2049 | 5.00% | 1,250,000 | 1,051,838 | ||||||||||||||

| Mirabelle MD #2 – Series B – 2049(g) |

12/15/2049 | 7.38% | 1,473,000 | 1,273,143 | ||||||||||||||

| Monument Junction MD #1 – Series A – 2051(g) |

12/1/2051 | 5.75% | 12,258,000 | 9,935,967 | ||||||||||||||

| Mount Carbon MD – Series C – 2043 |

6/1/2043 | 0.00% | 521,078 | 521,078 | ||||||||||||||

| Mountain Brook MD – Series A – 2051 |

12/1/2051 | 4.75% | 7,740,000 | 5,533,945 | ||||||||||||||

| Mountain Brook MD – Series A – 2041 |

12/1/2041 | 4.50% | 1,000,000 | 761,240 | ||||||||||||||

| Mountain Shadows MD – Series A – 2035 |

12/1/2035 | 5.00% | 500,000 | 467,050 | ||||||||||||||

| Mountain Shadows MD – Series B – 2046(g) |

12/15/2046 | 7.50% | 1,800,000 | 1,602,828 | ||||||||||||||

| Mountain Shadows MD – Series C – 2040(g) |

12/15/2040 | 10.00% | 1,994,000 | 1,835,577 | ||||||||||||||

| Muegge Farms MD #1 – Series A – 2051(g) |

12/1/2051 | 5.00% | 6,300,000 | 4,875,003 | ||||||||||||||

| Muegge Farms MD #3 – Series A – 2051(g) |

12/1/2051 | 5.50% | 10,431,000 | 8,375,884 | ||||||||||||||

| Murphy Creek MD #3 – Series A – 2026 |

12/1/2026 | 6.00% | 2,540,000 | 2,540,000 | ||||||||||||||

| Murphy Creek MD #3 – Series A – 2035 |

12/1/2035 | 6.13% | 1,880,000 | 1,880,000 | ||||||||||||||

| Murphy Creek MD #5 – Series A – 2052 |

12/1/2052 | 6.00% | 2,645,000 | 2,413,245 | ||||||||||||||

| Nine Mile MD – Series A – 2030 |

12/1/2030 | 4.63% | 1,125,000 | 1,036,553 | ||||||||||||||

| Nine Mile MD – Series A – 2040 |

12/1/2040 | 5.13% | 2,500,000 | 2,227,925 | ||||||||||||||

| North Range MD #3 – Series A – 2040 |

12/1/2040 | 5.00% | 2,000,000 | 1,750,400 | ||||||||||||||

| Painted Prairie Improvement Authority – Series A – 2029 |

12/1/2029 | 4.00% | 1,000,000 | 913,620 | ||||||||||||||

| Palisade Park North MD #2 – Series A – 2047 |

12/1/2047 | 5.63% | 1,740,000 | 1,602,610 | ||||||||||||||

| Parkdale Community Authority – Series A – 2040 |

12/1/2040 | 5.00% | 3,140,000 | 2,778,460 | ||||||||||||||

| Parkdale Community Authority – Series A – 2050 |

12/1/2050 | 5.25% | 5,620,000 | 4,710,178 | ||||||||||||||

| Parkdale Community Authority – Series B – |

12/15/2050 | 7.75% | 2,424,000 | 2,111,813 | ||||||||||||||

| Parker Automotive MD – Series A – 2045 |

12/1/2045 | 5.00% | 1,906,000 | 1,680,253 | ||||||||||||||

| Parker Automotive MD – Series B – 2032(g) |

12/15/2032 | 8.00% | 3,785,000 | 3,575,311 | ||||||||||||||

| Pioneer Community Authority – Series B – |

12/15/2050 | 6.75% | 24,592,000 | 21,188,959 | ||||||||||||||

| The Plaza MD #1 – Series A – 2040(m) |

12/1/2040 | 5.00% | 7,850,000 | 7,069,082 | ||||||||||||||

| Powhaton Community Authority – Series A – |

12/1/2051 | 5.00% | 7,450,000 | 5,871,345 | ||||||||||||||

19

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| Pronghorn Valley MD – Series A – 2041 |

12/1/2041 | 3.75% | $ | 515,000 | $ | 374,663 | ||||||||||||

| Pronghorn Valley MD – Series A – 2051 |

12/1/2051 | 4.00% | 4,400,000 | 3,055,756 | ||||||||||||||

| PFA / Colorado Skies Academy – Series A – |

7/1/2025 | 5.63% | 10,290,000 | 9,940,552 | ||||||||||||||

| PFA / Monument Academy – Series A – 2026(m) |

6/1/2026 | 5.00% | 28,570,000 | 27,535,480 | ||||||||||||||

| Ravenna MD – Series A – 2046 |

12/1/2046 | 5.00% | 33,685,000 | 28,857,940 | ||||||||||||||

| Ravenna MD – Series B – 2056(g) |

12/15/2056 | 7.50% | 8,000,000 | 6,931,200 | ||||||||||||||

| Reata Ridge Village MD #2 – Series A – 2049 |

12/1/2049 | 5.00% | 1,803,000 | 1,542,521 | ||||||||||||||

| Rendezvous MD #4 – Series B – 2048(g) |

10/15/2048 | 8.00% | 1,189,000 | 1,048,044 | ||||||||||||||

| Remuda Ridge MD – Series A – 2051(g) |

12/1/2051 | 5.63% | 5,520,000 | 4,475,892 | ||||||||||||||

| Reserve MD #2 – Series A – 2045 |

12/1/2045 | 5.00% | 500,000 | 433,055 | ||||||||||||||

| Rex Ranch MD – Series B – 2047(g) |

12/15/2047 | 7.88% | 445,000 | 461,349 | ||||||||||||||

| Ritoro MD – Series B – 2049(g) |

12/15/2049 | 8.50% | 2,190,000 | 2,210,805 | ||||||||||||||

| Riverdale Peaks II MD – Series A – 2025 |

12/1/2025 | 6.40% | 930,000 | 762,600 | ||||||||||||||

| Riverdale Peaks II MD – Series A – 2035 |

12/1/2035 | 6.50% | 1,135,000 | 930,700 | ||||||||||||||

| Riverview MD – Series A – 2041 |

12/1/2041 | 5.00% | 1,105,000 | 935,968 | ||||||||||||||

| Riverview MD – Series A – 2051 |

12/1/2051 | 5.00% | 2,075,000 | 1,659,938 | ||||||||||||||

| Rock Creek MD – Series A – 2041 |

12/1/2041 | 4.50% | 2,230,000 | 1,706,062 | ||||||||||||||

| Rock Creek MD – Series A – 2050 |

12/1/2050 | 4.75% | 3,880,000 | 2,788,478 | ||||||||||||||

| Rock Creek MD – Series A – 2031(g) |

12/1/2031 | 4.00% | 3,432,000 | 2,943,420 | ||||||||||||||

| Rose Hill Acres MD – Series A – 2050 |

12/1/2050 | 5.00% | 2,990,000 | 2,453,863 | ||||||||||||||

| Rose Hill Acres MD – Series B – 2050(g) |

12/15/2050 | 8.75% | 910,000 | 812,566 | ||||||||||||||

| Roxborough Village MD – Series A – 2042(f)(i) |

12/31/2042 | 0.00% | 242,645 | 26,691 | ||||||||||||||

| RRC MD #2 – Series A – 2051(g) |

12/1/2051 | 5.25% | 5,625,000 | 4,432,275 | ||||||||||||||

| Sabell MD – Series A – 2050(g) |

12/1/2050 | 5.00% | 1,055,000 | 868,107 | ||||||||||||||

| Sabell MD – Series B – 2050(g) |

12/15/2050 | 8.25% | 605,000 | 534,929 | ||||||||||||||

| Silver Peaks East MD – Series A – 2051(g) |

12/1/2051 | 5.00% | 5,410,000 | 4,190,261 | ||||||||||||||

| 64th Avenue ARI Authority – Series A – 2043(g) |

12/1/2043 | 6.50% | 5,000,000 | 4,537,850 | ||||||||||||||

| Solitude MD – Series A – 2026(j) |

12/1/2026 | 7.00% | 3,520,000 | 2,486,263 | ||||||||||||||

| Southglenn MD – Series A – 2030 |

12/1/2030 | 5.00% | 2,285,000 | 2,216,381 | ||||||||||||||

| Southglenn MD – Series A – 2046 |

12/1/2046 | 5.00% | 2,100,000 | 1,819,965 | ||||||||||||||

| Southlands MD #1 – Series A – 2037 |

12/1/2037 | 5.00% | 500,000 | 468,615 | ||||||||||||||

| Southlands MD #1 – Series A – 2047 |

12/1/2047 | 5.00% | 3,000,000 | 2,633,460 | ||||||||||||||

| Southshore MD #2 – Series B – 2041(g) |

12/15/2041 | 4.13% | 9,690,000 | 8,824,295 | ||||||||||||||

| Spring Hill MD #3 – Series A – 2052 |

12/1/2052 | 6.75% | 10,305,000 | 9,947,932 | ||||||||||||||

| Spring Valley MD #4 – Series A – 2040 |

12/1/2040 | 5.00% | 1,410,000 | 1,217,944 | ||||||||||||||

| Spring Valley MD #4 – Series A – 2050 |

12/1/2050 | 5.12% | 1,775,000 | 1,430,987 | ||||||||||||||

20

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Colorado Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado (Continued) | ||||||||||||||||||

| Spring Valley MD #4 – Series B – 2050(g) |

12/15/2050 | 7.63% | $ | 2,811,000 | $ | 2,408,437 | ||||||||||||

| St Vrain Lakes MD #2 – Series A – 2037 |

12/1/2037 | 5.00% | 4,000,000 | 3,726,320 | ||||||||||||||

| St Vrain Lakes MD #2 – Series A – 2047 |

12/1/2047 | 5.13% | 3,050,000 | 2,690,314 | ||||||||||||||

| St Vrain Lakes MD #2 – Series B – 2047(g) |

12/15/2047 | 7.63% | 1,083,000 | 1,017,164 | ||||||||||||||

| STC MD #2 – Series A – 2025 |

12/1/2025 | 3.00% | 555,000 | 525,602 | ||||||||||||||

| STC MD #2 – Series A – 2029 |

12/1/2029 | 4.00% | 1,615,000 | 1,466,759 | ||||||||||||||

| STC MD #2 – Series A – 2038 |

12/1/2038 | 5.00% | 15,160,000 | 13,425,241 | ||||||||||||||

| STC MD #2 – Series B – 2049(g) |

12/15/2049 | 8.00% | 3,954,000 | 3,490,908 | ||||||||||||||

| Sterling Ranch MD #2 – Series A – 2032 |

12/1/2032 | 5.25% | 1,340,000 | 1,275,332 | ||||||||||||||

| Sterling Ranch MD #2 – Series A – 2042 |

12/1/2042 | 5.50% | 5,645,000 | 5,146,490 | ||||||||||||||

| Sterling Ranch MD #2 – Series A – 2051 |

12/1/2051 | 5.75% | 11,750,000 | 10,616,478 | ||||||||||||||

| Stetson Ridge MD #3 – Series B – 2042(g)(m) |

12/15/2042 | 7.50% | 301,000 | 265,687 | ||||||||||||||

| Stone Ridge MD #2 – Series A – 2031 |

12/1/2031 | 0.00% | 11,896,000 | 1,903,360 | ||||||||||||||

| Tallyn’s Reach MD #3 – Series A – 2038 |

11/1/2038 | 5.13% | 2,070,000 | 2,072,650 | ||||||||||||||

| Third Creek MD #1 – Series A – 2037 |

12/1/2037 | 4.50% | 1,130,000 | 924,329 | ||||||||||||||

| Third Creek MD #1 – Series A – 2042 |

12/1/2042 | 4.50% | 3,140,000 | 2,376,635 | ||||||||||||||

| Third Creek MD #1 – Series A – 2051 |

12/1/2051 | 4.75% | 7,390,000 | 5,318,953 | ||||||||||||||

| Thompson Crossing MD #4 – Series A – 2039 |

12/1/2039 | 5.00% | 1,410,000 | 1,273,399 | ||||||||||||||

| Thompson Crossing MD #4 – Series A – 2049 |

12/1/2049 | 5.00% | 1,315,000 | 1,089,806 | ||||||||||||||

| Trails At Crowfoot MD #3 – Series B – 2049(g) |

12/15/2049 | 9.00% | 3,135,000 | 2,817,613 | ||||||||||||||

| Valagua MD – Series A – 2037 |

12/1/2037 | 0.00% | 11,500,000 | 2,300,000 | ||||||||||||||

| Villages At Murphy Creek MD #1 – Series A – 2051(g) |

12/1/2051 | 5.50% | 12,358,000 | 9,836,474 | ||||||||||||||

| Vincent Village MD – Series A – 2051 |

12/1/2051 | 5.00% | 1,970,000 | 1,552,242 | ||||||||||||||

| Waterfall MD #1 – Series A – 2052 |

12/1/2052 | 5.25% | 2,295,000 | 1,961,468 | ||||||||||||||

| Westcreek MD #2 – Series A – 2048 |

12/1/2048 | 5.38% | 1,300,000 | 1,152,866 | ||||||||||||||

| Westerly MD #4 – Series A – 2031 |

12/1/2031 | 4.13% | 600,000 | 519,414 | ||||||||||||||

| Westerly MD #4 – Series A – 2040 |

12/1/2040 | 5.00% | 2,255,000 | 1,958,513 | ||||||||||||||

| Westerly MD #4 – Series A – 2050 |

12/1/2050 | 5.00% | 5,250,000 | 4,222,943 | ||||||||||||||

| White Buffalo MD #3 – Series A – 2050 |

12/1/2050 | 5.50% | 4,780,000 | 4,145,885 | ||||||||||||||

| Wild Plum MD – Series A – 2049 |

12/1/2049 | 5.00% | 595,000 | 617,069 | ||||||||||||||

| Willow Springs MD – Series B – 2049(g) |

12/15/2049 | 7.75% | 650,000 | 564,779 | ||||||||||||||

| Woodmen Heights MD #2 – Series B – 2040(g) |

12/15/2040 | 7.50% | 3,358,000 | 2,963,166 | ||||||||||||||

| Wyndham Hill MD #2 – Series B – 2049(g) |

12/15/2049 | 7.63% | 9,600,000 | 8,476,992 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Colorado (amortized cost $1,254,667,894) |

1,330,071,152 | 1,107,768,764 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Colorado Municipal Bonds |

$ | 1,330,071,152 | $ | 1,107,768,764 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

21

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Short-Term Municipal Bonds 5.5% | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Colorado 73.9% | ||||||||||||||||||

| Boulder Housing Authority / Broadway East – Series A – 2037(LOC 1) |

9/1/2037 | 4.03% | $ | 1,440,000 | $ | 1,440,000 | ||||||||||||

| Boulder College of Massage – Series A – |

10/15/2031 | 0.00% | 4,315,000 | 2,337,500 | ||||||||||||||

| Broomfield URA / Event Center – Series A – 2030(LOC 2) |

12/1/2030 | 3.95% | 7,185,000 | 7,185,000 | ||||||||||||||

| CHFA / Ready Foods – Series A – 2032(LOC 1) |

1/1/2032 | 4.03% | 4,470,000 | 4,470,000 | ||||||||||||||

| Colorado Springs Utilities – Series A – |

11/1/2041 | 4.05% | 1,100,000 | 1,100,000 | ||||||||||||||

| ECCV Water & Sanitation District – Series A – 2023(c) |

11/15/2023 | 5.00% | 1,011,000 | 1,009,686 | ||||||||||||||

| Jeffco Business Center MD #1 – Series A – |

5/1/2024 | 8.00% | 1,006,000 | 1,013,564 | ||||||||||||||

| Ravenna MD – Series A CABs – 2023(d) |

12/1/2023 | 5.00% | 325,000 | 321,805 | ||||||||||||||

| Rockinghorse MD #2 – Series A CABs – 2024 |

1/1/2024 | 6.00% | 3,565,000 | 3,580,579 | ||||||||||||||

| Rockinghorse MD #2 – Series B – 2024 |

1/1/2024 | 6.50% | 3,885,000 | 3,906,134 | ||||||||||||||

| Inspiration MD – Series C CABs – 2024(b) |

6/1/2024 | 5.00% | 1,115,000 | 1,109,960 | ||||||||||||||

| Sheridan Redevelopment Agency / Santa Fe – |

12/1/2029 | 4.00% | 39,195,000 | 39,195,000 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Colorado (amortized cost $68,195,833) |

68,612,000 | 66,669,228 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Multi-State 18.0% | ||||||||||||||||||

| Freddie Mac VR – 2045(LOC 4) |

12/15/2045 | 4.01% | 16,280,000 | 16,280,000 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Multi-State (amortized cost $16,280,000) |

16,280,000 | 16,280,000 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Oregon 6.4% | ||||||||||||||||||

| Multnomah County Hospital – Series A – 2023(m) |

10/1/2024 | 5.45% | 5,815,000 | 5,815,000 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Oregon (amortized cost $5,815,000) |

5,815,000 | 5,815,000 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| South Dakota 1.0% | ||||||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2024(m) |

1/1/2024 | 8.28% | 950,000 | 940,918 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| South Dakota (amortized cost $950,000) |

950,000 | 940,918 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Oklahoma 0.5% | ||||||||||||||||||

| Haskell County Public Facilities – Series B – |

4/1/2024 | 5.25% | 450,000 | 447,282 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Oklahoma (amortized cost $450,000) |

450,000 | 447,282 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

22

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Short-Term Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| Puerto Rico 0.1% | ||||||||||||||||||

| Puerto Rico – Series A – 2024 |

7/1/2024 | 3.20% | $ | 15,095 | $ | 14,582 | ||||||||||||

| Puerto Rico / Sales Tax – Series A – 2024 |

7/1/2024 | 4.79% | 55,000 | 53,244 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Puerto Rico (amortized cost $66,645) |

70,095 | 67,826 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Short-Term Municipal Bonds |

$ | 92,177,095 | $ | 90,220,254 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Other Municipal Bonds 5.1% | ||||||||||||||||||

| South Dakota 86.9% | ||||||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare – Series A – 2036(m) |

1/1/2036 | 5.75% | $ | 6,055,000 | $ | 4,424,207 | ||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare – Series A – 2026(m) |

1/1/2026 | 5.00% | 1,740,000 | 1,620,010 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare – Series A – 2031(m) |

1/1/2031 | 5.50% | 3,565,000 | 2,886,188 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series B – 2038(g)(m) |

1/1/2038 | 6.00% | 6,120,000 | 5,000,040 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series C – 2038(m) |

1/1/2038 | 6.00% | 5,450,000 | 4,452,650 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2025(m) |

1/1/2025 | 8.28% | 1,030,000 | 989,027 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2026(m) |

1/1/2026 | 8.28% | 1,115,000 | 1,050,464 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2027(m) |

1/1/2027 | 8.28% | 1,205,000 | 1,121,771 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2028(m) |

1/1/2028 | 8.28% | 1,305,000 | 1,204,228 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Gaming – Series A – 2033(m) |

1/1/2033 | 8.28% | 8,670,000 | 7,774,649 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2025(m) |

7/1/2025 | 5.75% | 740,000 | 707,085 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2026(m) |

7/1/2026 | 5.75% | 785,000 | 735,930 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2027(m) |

7/1/2027 | 5.75% | 830,000 | 761,965 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2028(m) |

7/1/2028 | 5.75% | 875,000 | 789,163 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2029(m) |

7/1/2029 | 5.75% | 930,000 | 823,655 | ||||||||||||||

23

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Other Municipal Bonds (Continued) | Maturity |

Coupon |

Principal |

Value |

||||||||||||||

| South Dakota (Continued) | ||||||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2030(m) |

7/1/2030 | 5.75% | $ | 980,000 | $ | 853,247 | ||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2031(m) |

7/1/2031 | 5.75% | 1,040,000 | 891,124 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2032(m) |

7/1/2032 | 5.75% | 1,095,000 | 923,698 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2033(m) |

7/1/2033 | 5.75% | 1,160,000 | 964,865 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2034(m) |

7/1/2034 | 5.75% | 1,225,000 | 1,005,627 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2035(m) |

7/1/2035 | 5.75% | 1,300,000 | 1,054,170 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2040(m) |

7/1/2040 | 6.00% | 7,730,000 | 5,991,368 | ||||||||||||||

| Flandreau Santee Sioux Tribe / Healthcare NH – Series A – 2045(m) |

7/1/2045 | 6.25% | 10,395,000 | 7,844,899 | ||||||||||||||

| Lower Brule Sioux Tribe – Series A – 2025(m) |

3/1/2025 | 5.88% | 945,000 | 892,449 | ||||||||||||||

| Oglala Sioux Tribe / Healthcare – Series A – |

7/1/2028 | 5.50% | 2,200,000 | 1,995,004 | ||||||||||||||

| Oglala Sioux Tribe / Healthcare – Series A – |

7/1/2037 | 6.00% | 9,270,000 | 7,204,088 | ||||||||||||||

| Oglala Sioux Tribe / Healthcare – Series B – |

9/1/2041 | 6.50% | 5,880,000 | 4,592,633 | ||||||||||||||

| Oglala Sioux Tribe – Series A – 2024(m) |

10/1/2024 | 5.50% | 1,985,000 | 1,946,908 | ||||||||||||||

| Oglala Sioux Tribe – Series C – 2026(m) |

10/1/2026 | 8.00% | 800,000 | 770,280 | ||||||||||||||

| Oglala Sioux Tribe – Series A – 2027(m) |

10/1/2027 | 4.50% | 2,370,000 | 2,130,772 | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| South Dakota (amortized cost $88,786,301) |