Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05009

COLORADO BONDSHARES —

A TAX-EXEMPT FUND

(Exact name of registrant as specified in its charter)

1200 17TH STREET, SUITE 850

DENVER, COLORADO 80202-5808

(Address of principal executive offices) (Zip code)

FRED R. KELLY, JR.

1200 17TH STREET, SUITE 850

DENVER, COLORADO 80202-5808

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-572-6990

Date of fiscal year end: 09/30

Date of reporting period: 09/30/2017

Table of Contents

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

Table of Contents

November 17, 2017

Dear Shareholders:

We appear to be on the verge of experiencing tax reform for the first time in 30 years. When last completed in the Reagan Administration we were promised tax reduction and for many people the exact opposite occurred. While tax rates were indeed decreased, deductions were also severely curtailed resulting in higher effective rates. The tax burden was shifted from individuals to corporations. Offered in the spirit of fairness we ended up with the alternate minimum tax which subjected individuals to “tax creep” the likes of which had never been seen and was so onerous that an individual with too many children could suddenly be subject to additional tax. Heaven knows that those parents have already paid. Over the years, politicians have gradually put incentives back in the law such as the carried interest provision which should now be reversed, but probably will not be.

The direction this time is to reverse fields and shift the burden from corporations back to wealthy individuals. The premise is to make our corporations more competitive in the world market and allow them to do more hiring and more capital spending with a resultant positive effect on the economy. All of that sounds good but could either be inflationary or sow the seeds for the next recession. Government has a habit throughout history of stimulating at the wrong time. Don’t get me wrong, I am all in favor of Americans doing better and we all know that taxes are too high but there is not one iota of debt reduction anywhere in the proposed legislation. We are assured that this will be in the next phase but given the difficulty encountered with healthcare tax reform and the deep divisions in Congress it will be a miracle if we ever get around to that loathsome task of addressing entitlements. Some of the provisions like state and local tax deductions as well as home mortgage deductions are widely covered in the press. Other provisions are not and you may be hearing about those here first.

In the House version of the bill all private activity bonds issued after 12/31/2017 are no longer tax exempt. This potentially adversely affects low income housing, hospitals, airports, and charter schools which comprise 40% of the tax-exempt market. In my opinion, this is not adviseable from a public policy perspective and will likely cause a rush to market of all affected issuers causing a short-term glut and a long-term scarcity of tax-exempt bonds. The Senate version contains no such provision and in fact eliminates AMT treatment of bonds. The two diametrically opposed philosophies must be reconciled in the final version, which outcome cannot be predicted. However it ends up, Colorado BondShares will learn how to cope with the new rules as they become known. We are thankful that the proposals are not even more draconian than they are and they serve to make income from municipal bonds ever more attractive, which is good. Now you know the rest of the story. The changes, if adopted, are not expected to substantially change how the Fund does business.

For a detailed review of the Fund’s financial results please see the attached pages. According to Thomson Reuters we ended our year as the number one performing fund in our category. Don’t hold that against us; we will work harder and try to do better next year. Thanks to you the Fund reached new heights in terms of size and income distributed this year. We appreciate our shareholders very much and are honored to serve you.

Sincerely,

Fred R Kelly, Jr.

Portfolio Manager

Table of Contents

Table of Contents

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

When the Fund began in 1987, the goal was very simple and straightforward, “maximize income that is exempt from both Colorado and federal income taxes while simultaneously preserving capital.” Our specialty was honed in the Colorado non-rated municipal markets and refined over the last 30 years, while navigating inherent challenges that come along with this type of investment. Much of our success, since, has come from remaining true to the discipline of staying with what we do best in the market we know best. Because of this we have managed to weather the ups and downs of the economy, both locally and nationally, as well as interest rate volatility that often accompanies these changes.

This was especially true in 2017 fiscal year. The 4th quarter of 2016 was fraught with a number of interesting events beginning with the 2016 presidential election, punctuated with slight volatility in treasury yields and closing out the year as the Federal Reserve raised the target range for the federal funds from 0.5% to 0.75%. In 2017, the Federal Reserve, determined that the economy was continuing to strengthen and in a cautious move against inflation, raised the Fed rate causing the bond market to react with some modest downward pressure in prices. The current federal funds range is 1.00% to 1.25% with the expectation of another .25% in December of this year bringing it to 1.50%. It is expected that rates will go to 2% in 2018 and 3% in 2019. In addition, the Federal Reserve announced that it would begin reducing its balance sheet beginning with $10 billion in October 2017 and continuing every month until it reaches approximately $50 billion a month by October 2018.

Nationally, the U.S. economy continued its expansive growth through 2016 and into 2017 and expectations are for it to continue into 2018. International markets also experienced improved performance over earlier projections.

Locally, the Colorado economy continues to show positive markers for continued expansion, though at a slower pace than prior years. The March 17, 2017 publication of Focus Colorado: Economic and Revenue Forecast is quoted saying “The two-year downturn in the oil and gas industry appears to be at an end as rig counts have begun to increase in recent months.” The publication went on to say that both consumer spending and new job opportunities have contributed to a lower unemployment rate. Those predictions were tempered by factors such as full employment and an aging population of Baby Boomers, estimated to be over 50 million nationwide.

As detailed earlier, the municipal market struggled with price volatility through 4th quarter 2016 as well as 1st quarter 2017. During the 2nd and 3rd quarter 2017, prices gradually recovered. During that period, the Fund experienced net cash inflows that were driven by, among other things, yield-seeking investors. The incentive appears to be tax exempt income and relief from, potentially, new and higher taxes. Depending on their respective tax bracket, investors could garner substantial tax-equivalent yields, especially when compared to U.S. Treasuries or low yielding bank CDs. In calendar year 2017 (through October), the market posted over $363 billion in new municipal issuances, down about 10% year over year (MSRB/EMMA). However, municipal bond mutual funds reported an estimated $287 million net inflows just in the month of October (Investment Company Institute).

From 2011 through 2014, Colorado population expanded by 236,000 to 5.356 million. Experts have estimated that numbers will be close to 5.4 million for 2015 and 5.474 million for 2016. Current estimates for 2017 are projected to be in the vicinity of 5.632 million. Furthermore, it is expected that the population in the Denver Metro area will likely exceed 6 million by 2020 and possibly 7.8 million by 2040. Over eighty percent of Colorado’s population reside in the 12 counties that make up the Front Range. Given those statistics and

1

Table of Contents

the fact that the majority of our special district bonds are located within the Front Range, Management is confident that our investments in these districts will continue to prosper.

In spite of signs of slowing growth in the housing market in 2017, both multi-family and single-family homes remained a significant component of the Colorado municipal bond industry because of their dramatic effect on taxable land. The first quarter 2017 Metrostudy Executive Briefing (May 31, 2017) stated that new home starts in 1Q2017 were at the “highest quarterly levels since 3Q2007.” The report further stated that new housing starts were up 19% year over year, levels not seen since 1Q2007. Much of this is fueled by increased population in-migration (over 38,000, so far, in 2017) driving more job creation and wage and employment growth which, in turn, pushes the “demand needle” for more housing options. Review of third quarter 2017 data revealed existing home sales “remain high despite slowing in recent months.” The supply/demand ratio in the housing market has noticeably tightened and may be contributing to what some believe to be a “flattening” in housing demand. Home buyers appear to be responding negatively to escalating new home prices, making existing homes on the market appealing. In June of this year, there were 5,712 sales of existing homes, an increase of 1% year over year. Annual sales are up 6% at 57,477 (Metrostudy Executive Summary 2Q2017). Average days on the market are 23, the lowest in 15 years. The average price for existing detached homes was $498,762, highest on record. Average detached new home sales price is $534,870 (Metrostudy 2Q2017), up 4% for 12 months ending June. The report claims that “no time in Denver’s history has housing been as expensive as it is now with only 28% of new home starts priced below $400,000.” So, with higher home prices and potential interest rate hikes, new home buyers and existing home owners looking to “move up” are at the mercy of two factors: price and borrowing costs, both of which can put pressure on potential future sales. To date, the positive still appears to outweigh the negative. However, this slowing trend has prompted some to believe that these factors may be influencing household dynamics causing a change in family formation. Some would-be buyers are gravitating toward the townhome/duplex market while still others are remodeling their existing homes offering a more affordable option at improving their living situations. Townhome and Duplex starts are expected to reach all-time highs in 2018. The price trend in average rent is up 3.2%, over last year to $1,412. Going forward, we believe, rentals in the multi-family sector will continue to fill a need for those unable to qualify for lending guidelines. This year, “the attached product category comprises over 30% of all activity, the highest level since 2008” (Metrostudy Executive Summary, 2Q2017). Millennials may well provide the impetus for change in the housing market in future years, demanding smaller, more affordable homes with “smart technology”. Given that they now have overtaken the Baby Boomers and have become America’s largest generation, it is believed that their influence with builders may sufficiently sway them to re-focus on more affordable housing in the sub $400,000 market.

Charter schools continue to grow in number and have reached nearly 7,000 schools in the country, enrolling 3.1 million students with 1 million students on wait lists to get into charters. Charter schools exist in 43 states plus the District of Columbia. Colorado’s charter school law was passed in 1993. Schools opened quickly and by fall of 2016 there were 238 schools. Currently, charter schools constitute 27% of the bonds in the portfolio.

The combination of relatively low interest rates and tight underwriting spreads have put pressure on municipal bond funds to produce net positive returns for the year. Municipal bond mutual funds typically experience net cash inflows correlative with strong total return performance. This year’s performance proved to be a case in point. The Fund’s total return for fiscal year, ended 9/30/2017 was ranked #1 by Lipper when compared to peers in the “Other States Municipal Debt Fund” category. The results were highlighted by a number of positive events, one being the retirement of several bonds

2

Table of Contents

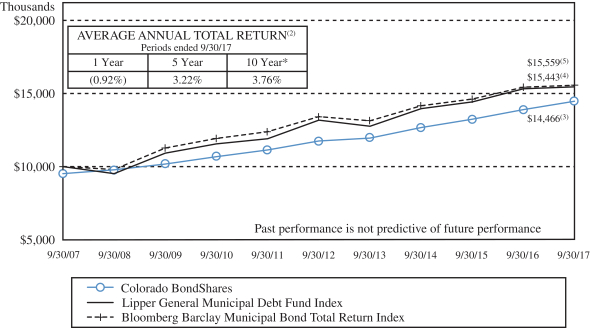

purchased in prior years at a deep discount with unpaid interest owed. The bonds were all paid off in full plus accrued interest. For the fiscal year ended September 30, 2017, the Fund recorded a total return of 4.03% at net asset value; the return was comprised of an investment income component of 4.54% and principal depreciation of -.51%. Some funds use leverage in an attempt to enhance their yields but the Fund did not. According to Thomson Reuters, the Fund ranked #1 in the 1-year, 3-year and 5-year category. The average annual total returns at the maximum offering price (including sales charges and reinvestment of all dividends and distributions) are -0.92%, 2.81%, 3.22%, 3.76% for the one, three, five and ten-year periods ended September 30, 2017, respectively.

A key factor which has contributed to the Fund’s stability in the past and continues going forward is management’s determination to maintain a shorter average duration (time period during which securities are likely to be held by the portfolio), which is among the lowest in our peer group. Through the majority of the year, the Fund carried a disproportionately high weighting of short-term bonds and cash in the portfolio, designed to lessen the exposure to market risk in a time when it appeared likely for interest rates to rise and spreads to widen. As low rates persisted, some Colorado issuers responded by refinancing their higher coupon debt for bonds with significantly lower rates. This effectively reduced their annual debt service payments and simultaneously improved the financial health of their districts. Additionally, some issuers, again taking advantage of the lower borrowing costs, made the decision to embark on new projects that had been delayed during the credit crisis years earlier. Both scenarios resulted in a plethora of new deals that came to our Colorado market in 2017. While the strategy of buying short maturities helped to protect principal, it did not maximize the current income stream. Distributions of $0.48/share in fiscal year 2017 compared slightly more favorable to $0.41/share in 2016 and $0.38/share in 2015. It is management’s philosophy that it is easier to recoup lost income than it is to recover principal losses. Until the risks posed by rising interest rates have abated, management will continue to exercise this methodology. Much of this year’s income may be attributed to longer term holdings being principally invested in not-rated tax-exempt bonds, with coupon rates that exceed average coupons currently available in the market. Not-rated securities are generally subject to greater credit risk than rated issues; but proper analysis by management may effectively mitigate these risks. It should be stated that past performance is not necessarily indicative of future performance, but it is one of many important factors to consider when evaluating a potential investment.

3

Table of Contents

PERFORMANCE SUMMARY (Unaudited)

COMPARISON OF CHANGE IN VALUE OF A $10,000 INVESTMENT IN

COLORADO BONDSHARES(1)

THE LIPPER GENERAL MUNICIPAL DEBT FUND INDEX(4)

AND THE BLOOMBERG BARCLAY MUNICIPAL BOND TOTAL RETURN INDEX(5)

| (1) | Total return is the percentage change in the value of a hypothetical investment that has occurred in the indicated period of time, taking into account the imposition of the sales charge and other fees and assuming the reinvestment of all dividends and distributions. Past performance is not indicative of future performance. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares of the Fund. |

| * | Fiscal year ended September 30, 2007 includes an interest payment of approximately $3.8 million representing four years of unpaid interest relating to the Fund’s holding of United Airlines/Denver International Airport bonds that is a non-recurring event outside of the control of the Fund. |

| * | Fiscal year ended September 30, 2016 includes a principal write down of approximately $14.5 million due to an adverse decision by the Colorado State Court of Appeal on the Marin Metropolitan District bonds that is a non-recurring event outside of the control of the Fund. |

| (2) | Average annual total return reflects the hypothetical annually compounded return that would have produced the same cumulative total return if the Fund’s performance had been constant over the |

4

Table of Contents

| entire period. Average annual total returns for the one-year, five-year and ten-year periods ended September 30, 2017 are (0.92%), 3.22%, and 3.76%, respectively. Average annual total includes the imposition of the sales charge and assumes the reinvestment of all dividends and distributions. Past performance is not indicative of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares of the Fund. |

| (3) | Includes reinvestment of dividends and adjustment for the maximum sales charge of 4.75%. |

| (4) | The Lipper General Municipal Debt Fund Index is a non-weighted index of the 30 largest funds that invest at least 65% of assets in municipal debt issues in the top four credit ratings. The Lipper General Municipal Debt Fund Index reflects no deductions for fees, expenses or taxes, includes reinvestment of dividends but does not reflect any adjustment for sales charge. |

| (5) | The Bloomberg Barclay Municipal Bond Total Return Index which replaced the Barclays Capital Municipal Bond Total Return Index (the “Barclay Index”) is considered representative of the broad market for investment grade, tax-exempt and fixed-rate bonds with long-term maturities (greater than two years) selected from issues larger than $50 million. You cannot invest directly in this index. This index is not professionally managed and does not pay any commissions, expenses or taxes. If this index did pay commissions, expenses or taxes, its returns would be lower. The Fund selected the Bloomberg Barclay Index to compare the returns of the Fund to an appropriate broad-based securities market index. You should note, however, that there are some fundamental differences between the portfolio of securities invested in by the Fund and the securities represented by the Bloomberg Barclay Index. Unlike the Fund which invests primarily in not rated securities on issues of any size, the Bloomberg Barclay Index only includes securities with a rating of at least “Baa” by Moody’s Investor Services, Inc. from an issue size of no less than $50 million. Some of these differences between the portfolio of the Fund and the securities represented by the Bloomberg Barclay Index may cause the performance of the Fund to differ from the performance of the Bloomberg Barclay Index. |

5

Table of Contents

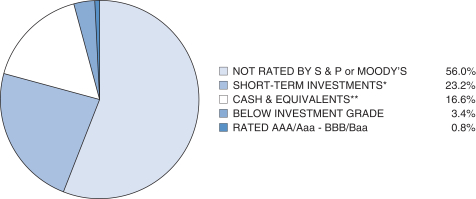

CREDIT QUALITY (unaudited)

Colorado BondShares — A Tax-Exempt Fund

Based on a Percentage of Total Net Assets as of September 30, 2017

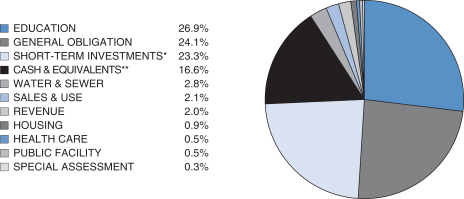

SECTOR BREAKDOWN (unaudited)

Colorado BondShares — A Tax-Exempt Fund

Based on a Percentage of Total Net Assets as of September 30, 2017

* Short-term investments include securities with a maturity date or redemption feature of one year or less, as identified in the Schedule of Investments.

** Cash & equivalents include cash and receivables less liabilities.

6

Table of Contents

Officers and Trustees of the Fund

The following tables list the trustees and officers of the Fund, together with their address, age, positions held with the Fund, the term of each office held and the length of time served in each office, principal business occupations during the past five years and other directorships, if any, held by each trustee and officer. Each trustee and officer has served in that capacity for the Fund continuously since originally elected or appointed. The Board of Trustees supervises the business activities of the Fund. Each trustee serves as a trustee until termination of the Fund unless the trustee dies, resigns, retires, or is removed. The Statement of Additional Information of the Fund includes additional information about Fund trustees and is available, without charge, upon request. Shareholders may call (800) 572-0069 to request the Statement of Additional Information.

| Name, Address and Age |

Position held with |

Principal Occupation |

Other Directorships | |||

| Non-Interested Trustees | ||||||

| Bruce G. Ely 1200 17th Street, Suite 850 Denver CO 80202 Age: 66 |

Trustee since July 2002 | Mr. Ely was a Regional Director for Cutwater Asset Management, a wholly owned subsidiary of MBIA, Inc., until his retirement in September 2013. | None | |||

| James R. Madden 1200 17th Street, Suite 850 Denver CO 80202 Age: 73 |

Trustee since September 2004 | Mr. Madden has owned Madden Enterprises, a real estate company that owns and leases commercial buildings and real estate, for the past thirty years. He is also a stockholder and director of The Community Bank in western Kansas. He has been a bank director for 25 years. | None | |||

| Interested Trustees* | ||||||

| George N. Donnelly 1200 17th Street, Suite 850 Denver CO 80202 Age: 70 |

Chairman of the Board of Trustees, Trustee since inception of the Fund in 1987 and Interim President, Secretary and Treasurer of the Fund since September 26, 2008 | Mr. Donnelly was a Senior Regional Vice President for Phoenix Life Insurance Company until his retirement in January 2010. | None | |||

*George N. Donnelly is an “interested person” of the Fund as defined in the Investment Company Act of 1940 (the “1940 Act”) by virtue of his position as both an officer and a trustee of the Fund as described in the table above. None of the trustees nor the officers of the Fund have any position with the Investment Adviser, the principal underwriter of the Fund, the distribution agent of the Fund, the service agent of the Fund or the custodian of the Fund, or any affiliates thereof. There is no family relationship between any officers and trustees of the Fund.

7

Table of Contents

Compensation

The Board of Trustees met four times during the fiscal year ended September 30, 2017. The following tables show the compensation paid by the Fund to each of the trustees during that year:

| Name of Person, Position(s) with the Fund |

Aggregate Compensation |

Pension or Retirement |

Total Compensation |

|||||||||

| Non-Interested Trustees |

||||||||||||

| Bruce G. Ely, Trustee |

$ | 2,400 | N/A | $ | 2,400 | |||||||

| James R. Madden, Trustee |

3,200 | N/A | 3,200 | |||||||||

| Interested Trustees |

||||||||||||

| George N. Donnelly, Trustee, Interim President, Secretary and Treasurer |

3,200 | N/A | 3,200 | |||||||||

No officer or trustee of the Fund received remuneration from the Fund in excess of $60,000 for services to the Fund during the fiscal year ended September 30, 2017. The officers and trustees of the Fund, as a group, received $8,800 in compensation from the Fund for services to the Fund during the 2017 fiscal year.

Other Information

Proxy Voting Record

The Fund does not invest in equity securities. Accordingly, there were no matters relating to a portfolio security considered during the 12 months ended June 30, 2017 with respect to which the Fund was entitled to vote. Applicable regulations require us to inform you that the foregoing proxy voting information is available on the SEC website at http://www.sec.gov or you may call us at 1-800-572-0069.

Quarterly Statement of Investments

The Fund files a complete statement of investments with the Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission’s website at http://www.sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling 1-800-732-0330 or you may call us at 1-800-572-0069.

8

Table of Contents

Trustees Approve Advisory Agreement

The Board of Trustees (the “Trustees”) of Colorado BondShares — A Tax-Exempt Fund approved the continuance of the Fund’s Investment Advisory and Service Agreement with Freedom Funds Management Company (“Freedom Funds”) at a meeting held on October 5, 2017. In approving the Advisory Agreement, the Trustees, including the disinterested trustees, considered the reasonableness of the advisory fee in light of the extent and quality of the advisory services provided and any additional benefits received by Freedom Funds or its affiliates in connection with providing services to the Fund, compared the fees charged by Freedom Funds to those paid by similar funds, and analyzed the expenses incurred by Freedom Funds with respect to the Fund. The Trustees also considered the Fund’s performance relative to a selected peer group, the expense ratio of the Fund in comparison to other funds of comparable size, and other factors. The Trustees determined that the Fund’s advisory fee structure was fair and reasonable in relation to the services provided and that approving the agreement was in the best interests of the Fund and its shareholders. Matters considered by the Trustees in connection with its consideration of the Advisory Agreement included, among other things, the following:

1. Investment Adviser Services

Freedom Funds manages the assets of the Fund, including making purchases and sales of portfolio securities consistent with the Fund’s investment objectives and policies. In addition, Freedom Funds administers the Fund’s daily business affairs such as providing accurate accounting records, computing accrued income and expenses of the Fund, computing the daily net asset value of the Fund, assuring proper dividend disbursements, proper financial information to investors, and notices of all shareholders’ meetings, and providing sufficient office space, storage, telephone services, and personnel to accomplish these responsibilities. In considering the nature, extent and quality of the services provided by Freedom Funds, the Trustees believe that the services provided by Freedom Funds have provided the Fund with superior results. At the same time, Freedom Fund’s fee structure is equal to or lower than the comparable funds. The Trustees noted the Fund’s focus is inherently more labor intensive. Under the circumstances, the Trustees found the fee structure to be justified.

2. Investment Performance

The Trustees reviewed the performance of the Fund compared to other similar funds, and reported that the current (as of September 30, 2017) net asset value was $9.05 per share and the current distribution yield (based on net asset value) was 4.18% (also as of September 30, 2017). Since the overall structure of the portfolio was satisfactory and the performance of the Fund, measured in terms of distribution yield and total return, was ahead of the other members of its peer group of Colorado funds (higher than the distribution yield of six comparable Colorado municipal bond funds), no changes to either the type of assets or manner of operations were recommended.

3. Expense Ratios

The Trustees reviewed the performance (measured by distribution yield), fees and expense ratios of six Colorado municipal bond funds (such six being the only such funds known to the Trustees at the time). The Fund was at the top of the list in terms of current yield and total performance; it had one of the lower expense ratios. The Trustees considered the fact that the Fund’s unique focus on not rated bonds, while

9

Table of Contents

geared toward producing superior investment results, often required additional expenses. While expenses can vary with not rated bonds (principally as a result of litigation with respect to defaulted issues and higher monitoring costs occasioned by less readily available information), the Trustees noted the Fund’s performance for the current year.

4. Management Fees and Expenses

The Trustees reviewed the investment advisory fee rates payable by the Fund to Freedom Funds. As part of its review, the Trustees considered the estimated advisory fees and the Fund’s estimated total expense ratio for the one-year period as of September 30, 2017 as compared to a group of six comparable Colorado municipal bond funds identified by Freedom Funds. After reviewing the foregoing information, and in light of the nature, extent and quality of the services provided by Freedom Funds, the Trustees concluded that the advisory fees charged by Freedom Funds for the advisory and related services to the Fund and the Fund’s total expense ratio are reasonable. The management fee is one half of one percent of total net assets managed. Such fee is payable to Freedom Funds on a monthly basis. This fee is comparable to the group of six competing Colorado municipal bond funds identified by Freedom Funds and is consistent with national funds many times the Fund’s size.

5. Profitability

The Trustees reviewed the level of profits realized by Freedom Funds and relevant affiliates thereof in providing investment and administrative services to the Fund. The Trustees considered the level of profits realized without regard to revenue sharing or other payments by Freedom Funds and its affiliates to third parties in respect to distribution of the Fund’s securities. The Trustees also considered other direct or indirect benefits received by Freedom Funds and its affiliates in connection with its relationship with the Fund and found that there were none. The Trustees concluded that, in light of the foregoing factors and the nature, extent and quality of the services provided by Freedom Funds, the profits realized by Freedom Funds are reasonable.

6. Economies of Scale

In reviewing advisory fees and profitability, the Trustees also considered the extent to which Freedom Funds and its affiliates, on the one hand, and the Fund, on the other hand, can expect to realize benefits from economies of scale as the assets of the Fund increase. The Trustees acknowledged the difficulty in accurately measuring the benefits resulting from the economies of scale with respect to the management of any specific fund or group of funds, particularly in an environment where costs are rising due to changing regulations. The Trustees reviewed data summarizing the increases and decreases in the assets of the Fund over various time periods, and evaluated the extent to which the total expense ratio of the Fund and Freedom Fund’s profitability may have been affected by such increases or decreases. Between October 2016 and September 30, 2017, total net assets of the Fund under management by Freedom Funds increased from $1,062.0 billion to $1,137.8 billion. The number of shares of the Fund that have been redeemed has been less than the number of new shares issued by the Fund, and as a result the Fund continues to grow at what the Trustees determined was a healthy level and the Fund is near its all-time high in terms of total assets.

Based upon the foregoing, the Trustees concluded that the benefits from the economies of scale are currently being shared equitably by Freedom Funds and the Fund. The Trustees also concluded that the

10

Table of Contents

structure of the advisory fee can be expected to cause Freedom Funds, its affiliates and the Fund to continue to share such benefits equitably and that breakpoints need not be instituted at this time.

After requesting and reviewing these and other factors that they deemed relevant, the Trustees concluded that the continuation of the Advisory Agreement was in the best interest of the Fund and its shareholders.

Freedom Funds also serves as the transfer agent, shareholder servicing agent and dividend disbursing agent for the Fund, pursuant to a Transfer Agency and Service Agreement (the “Service Agreement”).

Freedom Funds’ duties under the Service Agreement include processing purchase and redemption transactions, establishing and maintaining shareholder accounts and records, disbursing dividends declared by the Fund and all other customary services of a transfer agent, shareholder servicing agent and dividend disbursing agent. As compensation for these services, the Fund may pay Freedom Funds at a rate intended to represent Freedom Funds’ cost of providing such services. This fee would be in addition to the investment advisory fee payable to Freedom Funds under the Advisory Agreement.

11

Table of Contents

FUND EXPENSES (unaudited)

The following examples are intended to help you understand the ongoing costs (in dollars) of investing in the Fund and compare these costs with those of other mutual funds. The examples (actual and hypothetical 5% return) are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

As a shareholder of Colorado BondShares — A Tax-Exempt Fund (the “Fund’) you can incur two types of costs:

| • | Sales charges (front loads) on fund purchases and |

| • | Ongoing fund costs, including management fees, administrative services, and other fund expenses. All mutual funds have operating expenses. Operating expenses, which are deducted from the Fund’s gross income, directly reduce the investment return of the Fund. |

Actual Fund Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in shareholder reports of other funds.

Six Months Ended September 30, 2017

| Colorado BondShares — A Tax- Exempt Fund |

Beginning Account Value 04/01/17 |

Ending Account Value 09/30/17 |

Expenses

Paid During Period¹ | ||||||||||||

| Based on Actual Fund Return |

$ | 1,000.00 | $ | 1,037.58 | $ | 3.12 | |||||||||

| Based on Hypothetical 5% Annual Return Before Expenses |

$ | 1,000.00 | $ | 1,021.95 | $ | 3.09 | |||||||||

| (1) | The expenses shown in this table are equal to the Fund’s annualized expense ratio of 0.61% for fiscal year ended September 30, 2017, multiplied by the average account value over the period, multiplied by 183/365 to reflect the one-half year period. |

Please note that expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs would have been higher. You can find more information about the Fund’s expenses in the Financial Statements section of this report. For additional information on operating costs please see the Fund’s prospectus.

12

Table of Contents

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of

Colorado BondShares — A Tax-Exempt Fund

We have audited the accompanying statement of assets and liabilities of Colorado BondShares — A Tax-Exempt Fund (the “Fund”), including the schedule of investments, as of September 30, 2017, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years ended September 30, 2017 and 2016, and the financial highlights for each of the four years ended September 30, 2017, 2016, 2015, and 2014. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, audits of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of September 30, 2017, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Colorado BondShares — A Tax-Exempt Fund as of September 30, 2017, and the results of its operations for the year then ended, the changes in its net assets for each of the two years ended September 30, 2017 and 2016, and the financial highlights for each of the four years ended September 30, 2017, 2016, 2015, and 2014, in conformity with accounting principles generally accepted in the United States of America.

The financial statements of the Fund as of September 30, 2013, and for the year then ended, which included the financial highlights for the year ended September 30, 2013, were audited by other auditors, whose report dated November 27, 2013, expressed an unqualified opinion on those statements.

EKS&H LLLP

November 21, 2017

Denver, Colorado

13

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments

September 30, 2017

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — 53.3% | ||||||||||

| 1,600,000 | Aberdeen Metropolitan District No. 1 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2005, 7.50% to yield 8.00% due 12/1/2035 |

$ | 480,032 | |||||||

| 4,705,000 | Adonea Metropolitan District No. 2 LTD Tax (Convertible to Unlimited Tax) G.O. Series 2005A, 6.125% to yield 6.25% – 10.33% due 12/1/2025 |

3,573,683 | ||||||||

| 8,760,000 | Adonea Metropolitan District No. 2 LTD Tax (Convertible to Unlimited Tax) G.O. Series 2005A, 6.25% to yield 8.62% – 9.10% due 12/1/2035 |

6,653,658 | ||||||||

| 26,000,000 | Arista Metropolitan District Subordinate (Convertible to Parity) Special Revenue Series 2008, 9.25% to yield 8.125% – 16.442% due 12/1/2037 |

15,120,820 | ||||||||

| 1,775,000 | Banning Lewis Ranch Metropolitan District No. 3 G.O. LTD Tax Series 2015A, 6.125% to yield 6.25% due 12/1/2045 |

1,756,256 | ||||||||

| 4,315,000 | Boulder County Development Revenue (Boulder College of Massage Therapy Project) Series 2006A, 6.35% due 10/15/2031(a)(j) |

4,315,000 | ||||||||

| 2,162,000 | Bradburn Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2004, 8.00% due 12/15/2034 |

2,088,470 | ||||||||

| 1,185,000 | Brennan Metropolitan District G.O. LTD Tax Series 2016A, 5.25% due 12/1/2046 |

1,221,308 | ||||||||

| 516,000 | Brennan Metropolitan District Subordinate G.O. LTD Tax Series 2016B, 7.50% due 12/15/2046 |

494,034 | ||||||||

| 8,000,000 | Brighton Crossing Metropolitan District No. 4 G.O. (LTD Tax Convertible to Unlimited Tax) Refunding Series 2013, 7.00% 12/1/2023 |

8,029,600 | ||||||||

| 11,175,000 | Bromley Park Metropolitan District No. 2 G.O. LTD Tax Convertible Zero Coupon Series 2007B, 7.00% due 12/15/2037 |

10,760,631 | ||||||||

| 1,426,000 | Buffalo Run Mesa Metropolitan District LTD Tax G.O. Series 2004, 5.00% to yield 5.793% – 5.832% due 12/1/2034 |

1,300,426 | ||||||||

| 437,363 | Buffalo Run Mesa Metropolitan District LTD Tax G.O. Series 2006, 5.00% to yield 5.763% due 12/1/2037 |

396,233 | ||||||||

| 8,010,000 | Castle Oaks Metropolitan District G.O. LTD Tax Refunding and Improvement Series 2012, 5.50% due 12/1/2022(b) |

8,073,760 | ||||||||

| 2,860,000 | Castle Oaks Metropolitan District No. 3 G.O. LTD Tax Series 2015, 6.25% to yield 6.15% due 12/1/2044 |

3,042,010 | ||||||||

| 2,345,000 | Castle Oaks Metropolitan District No. 3 G.O. LTD Tax Completion Series 2016, 5.50% to yield 5.00% due 12/1/2045 |

2,410,191 | ||||||||

| 6,500,000 | Cimarron Metropolitan District LTD Tax (Convertible to Unlimited Tax) Revenue Series 2012, 6.00% due 12/1/2022 |

6,459,505 | ||||||||

| 3,501,000 | Colliers Hill Metropolitan District No. 2 Subordinate G.O. LTD Tax Series 2017B, 8.50% due 12/15/2047 |

3,348,601 | ||||||||

| 6,485,214 | Colorado Centre Metropolitan District LTD Tax and Special Revenue Series 1992B, 0.00% due 1/1/2032(g)(i)(j) |

3,404,738 | ||||||||

14

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 2,015,445 | Colorado Centre Metropolitan District LTD Tax and Special Revenue Series 1992A, principal only, due 1/1/2027(e)(i) |

$ | 1,604,173 | |||||||

| 2,014,408 | Colorado Centre Metropolitan District LTD Tax and Special Revenue Series 1992A, interest only, 9.00% due 1/1/2027(f)(i)(j) |

1,611,526 | ||||||||

| 3,467,434 | Colorado Educational and Cultural Facilities Authority Charter School Revenue (Carbon Valley Academy Project) A Charter School Created by St. Vrain Valley RE-1J Series 2006, 5.625% to yield 7.394% – 8.022% due 12/1/2036 |

2,881,992 | ||||||||

| 3,775,000 | Colorado Educational and Cultural Facilities Authority Charter School Revenue (Union Colony Charter School Project) A Charter School Created by Weld County School District No. 6 Series 2007, 5.75% to yield 3.737% due 12/1/2037 |

3,784,438 | ||||||||

| 7,391,000 | Colorado Crossing Metropolitan District No. 2 Limited Property Tax Supported Revenue Series 2017, 7.50% due 12/1/2047 |

7,414,429 | ||||||||

| 13,500,000 | Colorado Educational and Cultural Facilities Authority Charter School Revenue (Prospect Ridge Academy Project) A Charter School Authorized Through Adams 12 Five Star Schools Series 2017, 5.00% due 3/15/2023 |

13,554,405 | ||||||||

| 15,350,000 | Colorado Educational and Cultural Facilities Authority (Thomas MacLaren State Charter School Project) A Charter School Created by the State Charter School Institute Series 2017A, 5.00% due 6/1/2024 |

15,352,763 | ||||||||

| 11,635,000 | Colorado Educational and Cultural Facilities Authority (Apex Community School Project) A Charter School Created by the Douglas County School District Re. 1 Series 2017A, 5.25% due 7/1/2022 |

11,639,887 | ||||||||

| 500,000 | Colorado Educational and Cultural Facilities Authority Charter School Refunding and Improvement Revenue (University Lab School Project) Series 2015, A Charter School Chartered Through Weld County School District No. 6, 2.50% to yield 2.442% due 12/15/2019 |

501,600 | ||||||||

| 41,960,000 | Colorado Educational and Cultural Facilities Authority (Stargate Charter School Project) Charter School Improvement Revenue Series 2015A, A Charter School Chartered through Adams 12 Five Star Schools, 5.40% due 12/1/2020 |

41,835,798 | ||||||||

| 7,015,000 | Colorado Educational and Cultural Facilities Authority Charter School Refunding Revenue (Union Colony Elementary School Project) Series 2015, A Charter School Chartered through Weld County School District No. 6, 5.30% due 3/1/2020 |

7,014,579 | ||||||||

| 38,055,000 | Colorado Educational and Cultural Facilities Authority Charter School Refunding Revenue (American Academy Parker Facilities Project) A Charter School Created by Douglas County School District Re. 1 Series 2015, 4.20% due 12/1/2025 |

38,307,305 | ||||||||

| 8,620,000 | Colorado Educational and Cultural Facilities Authority Charter School Revenue Refunding and Improvement (Monarch Montessori of Denver Charter School Project) Series 2015A, 5.50% due 5/15/2020 |

8,608,966 | ||||||||

| 21,630,000 | Colorado Educational and Cultural Facilities Authority Charter School Refunding and Improvement Revenue Series 2016 (Prospect Ridge Academy Project) A Charter School Authorized Through Adams 12 Five Star Schools, 4.85% due 3/15/2023 |

21,609,019 | ||||||||

15

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 31,330,000 | Colorado Educational and Cultural Facilities Authority (Ability Connection Colorado Project) Refunding and Improvement Revenue Series 2014, 5.85% due 4/1/2019 |

$ | 31,566,542 | |||||||

| 3,570,000 | Colorado Educational and Cultural Facilities Authority (Swallow Charter Academy) Refunding and Improvement Revenue Series 2014, 5.70% due 11/15/2019 |

3,570,179 | ||||||||

| 27,570,000 | Colorado Educational and Cultural Facilities Authority Charter School Revenue, Series 2016, (American Academy Project) A Charter School Created by Douglas County School District Re. 1, 4.05% due 12/1/2026 |

26,993,511 | ||||||||

| 18,045,000 | Colorado Educational and Cultural Facilities Authority Charter School Revenue Series 2016 (Addenbrooke Classical Academy Project) A Charter School Created by Jefferson County School District No. 1, 4.50% due 6/1/2021 |

17,887,467 | ||||||||

| 3,755,000 | Colorado Housing and Finance Authority Economic Development Revenue (Micro Business Development Corporation Project) Series 2005, 6.75% due 12/1/2010(a)(j) |

3,755,000 | ||||||||

| 635,000 | Colorado International Center Metropolitan District No. 3 G.O. Refunding and Improvement (LTD Tax Convertible to Unlimited Tax) Series 2016, 4.625% due 12/1/2031 |

613,175 | ||||||||

| 2,940,000 | Colorado Springs Urban Renewal Authority Subordinate Tax Increment Revenue (University Village Project Refunding) Series 2016, 6.75% due 12/15/2030 |

2,787,443 | ||||||||

| 1,030,000 | Country Club Highlands Metropolitan District G.O. Limited Tax Series 2007, 7.25% due 12/1/2037 |

370,800 | ||||||||

| 2,100,000 | Cuchares Ranch Metropolitan District G.O. LTD Tax Refunding and Improvement Series 2016A, 5.00% due 12/1/2045 |

2,106,132 | ||||||||

| 500,000 | Denver West Promenade Metropolitan District Limited Tax (Convertible to Unlimited Tax) G.O. Series 2013, 5.125% due 12/01/2031 |

499,415 | ||||||||

| 500,000 | Denver West Promenade Metropolitan District Limited Tax (Convertible to Unlimited Tax) G.O. Series 2016, 6.00% due 12/15/2046 |

461,470 | ||||||||

| 5,508,000 | East Cherry Creek Valley Water and Sanitation District Water Activity Enterprise, Inc. Step Rate Water Revenue Series 2004, 6.00% due 11/15/2023(c) |

5,513,783 | ||||||||

| 4,500,000 | Elbert and Highway 86 Commercial Metropolitan District Public Improvement Fee Revenue Series 2008A, 7.50% due 12/1/2032 |

2,248,110 | ||||||||

| 2,000,000 | Erie Farm Metropolitan District G.O. LTD Tax Series 2016A, 5.50% due 12/1/2045 |

1,964,140 | ||||||||

| 2,620,000 | Erie Highlands Metropolitan District No. 1 G.O. LTD Tax Series 2015A, 5.75% due 12/1/2045 |

2,663,806 | ||||||||

| 708,000 | Erie Highlands Metropolitan District No. 1 Subordinate G.O. LTD Tax Series 2015B, 7.75% due 12/15/2045 |

706,216 | ||||||||

| 2,000,000 | Flatiron Meadows Metropolitan District G.O. LTD Tax Series 2016, 5.125% due 12/1/2046 |

1,992,340 | ||||||||

| 683,000 | Forest Trace Metropolitan District No. 3 Subordinate G.O. LTD Tax Series 2016B, 7.25% due 12/15/2046 |

642,191 | ||||||||

16

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 3,685,000 | Fronterra Village Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Refunding & Improvement Series 2007, 4.375% – 5.00% to yield 4.552% – 7.135% due 12/1/2017-2034 |

$ | 3,691,480 | |||||||

| 2,000,000 | Granby Ranch Metropolitan District LTD Tax G.O. Series 2006, 6.75% due 12/1/2036 |

2,000,360 | ||||||||

| 585,000 | Great Western Park Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2016A, 4.00% due 12/1/2026 |

572,651 | ||||||||

| 775,000 | Great Western Park Metropolitan District No. 2 Subordinate G.O. LTD Tax Series 2016B, 7.25% due 12/15/2046 |

723,416 | ||||||||

| 1,250,000 | Green Gables Metropolitan District No. 1 Series LTD Tax (Convertible to Unlimited Tax) G.O. Series 2016A, 5.30% due 12/1/2046 |

1,266,488 | ||||||||

| 740,000 | Green Gables Metropolitan District No. 1 Series LTD Tax G.O. Subordinate Series 2016B, 7.75% due 12/15/2046 |

715,484 | ||||||||

| 1,960,000 | Highlands Metropolitan District No. 2 LTD Tax (Convertible to Unlimited Tax) G.O. Series 2016A, 5.125% due 12/1/2046 |

1,863,196 | ||||||||

| 1,269,000 | Highlands Metropolitan District No. 2 Subordinate LTD Tax G.O. Series 2016B, 7.500% due 12/15/2046 |

1,219,560 | ||||||||

| 4,293,000 | Hyland Village Metropolitan District LTD Tax G.O. Variable Rate Bonds Series 2008, 6.50% to yield 21.595% due 12/1/2027 |

1,656,583 | ||||||||

| 1,006,000 | Jeffco Business Center Metropolitan District No. 1 LTD Tax G.O. Series 2000, 8.00% to yield 20.907% due 5/1/2020(j) |

905,400 | ||||||||

| 2,275,000 | Jefferson Center Metropolitan District No. 1 Refunding Revenue Series 2015, 4.75% due 12/1/2026 |

2,288,650 | ||||||||

| 150,000 | Lafayette City Center GID LTD Tax G.O. Series 1999, 5.75% to yield 7.60% due 12/1/2018 |

149,030 | ||||||||

| 2,590,000 | Lewis Pointe Metropolitan District LTD Tax (Convertible to Unlimited Tax) G.O. Series 2015A, 6.00% due 12/1/2044 |

2,596,993 | ||||||||

| 536,000 | Lewis Pointe Metropolitan District Junior Lien LTD Tax G.O. Series 2017C, 9.00% due 12/15/2047 |

334,394 | ||||||||

| 500,000 | Leyden Rock Metropolitan District No. 10 LTD Tax (Convertible to Unlimited Tax) G.O. Refunding and Improvement Series 2016A, 4.00% to yield 3.90% due 12/1/2025 |

500,595 | ||||||||

| 905,000 | Leyden Rock Metropolitan District No. 10 LTD Tax (Convertible to Unlimited Tax) G.O. Refunding and Improvement Series 2016A, 4.375% due 12/1/2033 |

897,389 | ||||||||

| 1,525,000 | Leyden Rock Metropolitan District No. 10 LTD Tax (Convertible to Unlimited Tax) G.O. Refunding and Improvement Series 2016A, 5.00% to yield 4.65% due 12/1/2045 |

1,549,705 | ||||||||

| 1,195,000 | Leyden Rock Metropolitan District No. 10 LTD Tax Subordinate G.O. Series 2016B, 7.25% due 12/15/2045 |

1,184,902 | ||||||||

| 1,700,000 | Littleton Village Metropolitan District No. 2 LTD Tax G.O. & Special Revenue Series 2015, 5.375% to yield 5.40% due 12/1/2045 |

1,710,948 | ||||||||

| 17,485,000 | Marin Metropolitan District LTD Tax G.O. Series 2008, 7.75% due 12/1/2028(a)(j) |

3,000,076 | ||||||||

17

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 1,405,000 | Marvella Metropolitan District G.O. LTD Tax Series 2016A, 5.125% due 12/1/2046 |

$ | 1,339,738 | |||||||

| 11,580,000 | Meadows Metropolitan District No. 1 G.O. LTD Tax Series 1989 A (reissued on 12/29/1993), 7.999% due 6/1/2029(k) |

12,140,819 | ||||||||

| 11,565,000 | Meadows Metropolitan District No. 2 G.O. LTD Tax Series 1989 B (reissued on 12/29/1993), 7.999% due 6/1/2029(k) |

12,125,093 | ||||||||

| 11,515,000 | Meadows Metropolitan District No. 7 G.O. LTD Tax Series 1989 C (reissued on 12/29/1993), 7.999% due 6/1/2029(k) |

12,072,671 | ||||||||

| 1,945,000 | MidCities Metropolitan District No. 2 Subordinate Special Revenue Refunding Series 2016B, 7.75% due 12/15/2046 |

1,834,505 | ||||||||

| 237,916 | Mount Carbon Metropolitan District LTD Tax and Revenue Refunding Series 2004A, 7.00% to yield 7.075% due 6/1/2043 |

141,256 | ||||||||

| 1,830,000 | Mount Carbon Metropolitan District LTD Tax and Revenue Refunding Series 2004B, 7.00% to yield 7.075% due 6/1/2043 |

1,086,508 | ||||||||

| 565,000 | Mount Carbon Metropolitan District LTD Tax and Revenue Refunding Series 2004C, due 6/1/2043(e) |

16,950 | ||||||||

| 1,800,000 | Mountain Shadows Metropolitan District LTD Tax Subordinate G.O. Series 2016B, 7.50% due 12/15/2046 |

1,757,358 | ||||||||

| 2,540,000 | Murphy Creek Metropolitan District No. 3 G.O. (LTD Tax Convertible to Unlimited Tax) Refunding and Improvement Series 2006, 6.00% to yield 7.90% due 12/1/2026 |

1,706,956 | ||||||||

| 1,880,000 | Murphy Creek Metropolitan District No. 3 G.O. (LTD Tax Convertible to Unlimited Tax) Refunding and Improvement Series 2006, 6.125% to yield 7.90% – 12.568% due 12/1/2035 |

1,263,416 | ||||||||

| 1,500,000 | Neu Towne Metropolitan District G.O. (LTD Tax Convertible to Unlimited Tax) Series 2004, 7.20% due 12/1/2023 |

398,010 | ||||||||

| 6,735,000 | North Pine Vistas Metropolitan District No. 2 LTD Tax G.O. Series 2016A, 6.75% due 12/1/2046 |

6,798,780 | ||||||||

| 1,810,000 | North Pine Vistas Metropolitan District No. 2 Subordinate LTD Tax G.O. Series 2016B, 8.50% due 12/15/2046 |

1,823,430 | ||||||||

| 4,345,000 | North Pine Vistas Metropolitan District No. 3 LTD Tax G.O. Series 2016A, 6.00% due 12/1/2036 |

4,387,364 | ||||||||

| 1,203,000 | North Pine Vistas Metropolitan District No. 3 Subordinate LTD Tax G.O. Series 2016B, 8.25% due 12/15/2046 |

1,213,213 | ||||||||

| 1,500,000 | Overlook Metropolitan District G.O. LTD Tax (Convertible to Unlimited Tax) Series 2016A, 5.50% due 12/1/2046 |

1,421,595 | ||||||||

| 2,650,000 | Palisade Metropolitan District No. 2 G.O. LTD Tax and Revenue Series 2016, 4.375% due 12/1/2031 |

2,665,264 | ||||||||

| 2,075,000 | Palisade Park North Metropolitan District No. 1 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2016A, 5.875% due 12/1/2046 |

1,985,692 | ||||||||

18

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 525,000 | Palisade Park North Metropolitan District No. 1 Subordinate G.O. LTD Tax Series 2016B, 8.00% due 12/15/2046 |

$ | 506,483 | |||||||

| 2,120,000 | Parker Automotive Metropolitan District G.O. Refunding Series 2016, 5.00% due 12/1/2045 |

2,016,035 | ||||||||

| 6,414,000 | Pioneer Metropolitan District No. 3 LTD Tax G.O. Refunding and Improvement Series 2016, 6.50% due 12/1/2046 |

6,009,854 | ||||||||

| 5,350,000 | The Plaza Metropolitan District No. 1 Revenue Refunding Series 2013, 5.00% to yield 4.892% due 12/1/2040 |

5,519,221 | ||||||||

| 2,340,000 | Potomac Farms Metropolitan District G.O. Refunding and Improvement (LTD Tax Convertible to Unlimited Tax) Series 2007A, 7.25% due 12/1/2037 |

1,505,533 | ||||||||

| 344,000 | Potomac Farms Metropolitan District G.O. Refunding and Improvement (LTD Tax Convertible to Unlimited Tax) Series 2007B, 7.625% due 12/1/2023 |

231,966 | ||||||||

| 1,040,000 | Promenade at Castle Rock Metropolitan District No. 1 LTD Tax G.O. Series 2015A, 5.125% due 12/1/2025 |

1,111,698 | ||||||||

| 34,320,000 | Public Finance Authority Charter School Refunding and Improvement Draw-Down Revenue (Colorado Early Colleges Project) Charter Schools Authorized Through the Colorado Charter School Institute Series 2016A, 4.25% due 7/1/2023 |

34,537,589 | ||||||||

| 9,345,000 | Public Finance Authority (West Ridge Academy Charter School Project) A Charter School Chartered through Weld County School District 6 Charter School Revenue Series 2017A, 5.50% due 12/1/2021 |

9,381,165 | ||||||||

| 3,500,000 | Reata North Metropolitan District LTD TAX G.O. Series 2007, 5.50% to yield 9.00% due 12/1/2032 |

2,555,210 | ||||||||

| 14,085,000 | Reata South Metropolitan District LTD TAX G.O. Series 2007A, 7.25% due 6/1/2037 |

13,398,075 | ||||||||

| 1,400,000 | Richards Farm Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2015A, 5.75% to yield 5.875% due 12/1/2045 |

1,363,880 | ||||||||

| 930,000 | Riverdale Peaks II Metropolitan District G.O. (LTD Tax Convertible to Unlimited Tax) Series 2005, 6.40% due 12/1/2025(l) |

381,337 | ||||||||

| 1,135,000 | Riverdale Peaks II Metropolitan District G.O. (LTD Tax Convertible to Unlimited Tax) Series 2005, 6.50% due 12/1/2035(l) |

431,345 | ||||||||

| 363,000 | Routt County LID No. 2002-1 Special Assessment Series 2004A, 6.50% to yield 6.59% due 8/1/2024 |

356,226 | ||||||||

| 211,640 | Roxborough Village Metropolitan District Series 1993B, principal only, 0.00% due 12/31/2021(e)(i)(j) |

121,799 | ||||||||

| 242,645 | Roxborough Village Metropolitan District Series 1993B, interest only, 10.41% due 12/31/2042(f)(i)(j) |

21,838 | ||||||||

| 1,000,000 | Sierra Ridge Metropolitan District No. 2 LTD Tax G.O. Series 2016A, 4.50% due 12/1/2031 |

988,590 | ||||||||

| 1,500,000 | Sierra Ridge Metropolitan District No. 2 Subordinate LTD Tax G.O. Series 2016B, 7.625% due 12/15/2046 |

1,437,990 | ||||||||

19

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 500,000 | Silver Peaks Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Series 2006, 5.75% due 12/1/2036 |

$ | 334,030 | |||||||

| 1,000,000 | Solaris Metropolitan District No. 3 (In the Town of Vail) Subordinate Limited Tax G.O. Refunding Series 2016B, 7% due 12/15/2046 |

949,860 | ||||||||

| 3,520,000 | Solitude Metropolitan District Senior G.O. LTD Tax Series 2006, 7.00% due 12/1/2026(j) |

2,745,600 | ||||||||

| 6,048,000 | Sorrel Ranch Metropolitan District G.O. (LTD Tax Convertible to Unlimited Tax) Series 2006, 5.75% to yield 7.585% due 12/1/2036 |

5,812,007 | ||||||||

| 1,960,000 | Southglenn Metropolitan District Special Revenue Refunding Series 2016, 3.00% to yield 3.07% due 12/1/2021 |

1,947,025 | ||||||||

| 5,202,000 | Southshore Metropolitan District No. 2 Subordinate LTD Tax G.O. Series 2017, 7.75% due 12/15/2042 |

5,182,440 | ||||||||

| 1,000,000 | STC Metropolitan District No. 2 LTD Tax G.O. Senior Series 2015A, 6.00% to yield 5.67% due 12/1/2038 |

1,000,690 | ||||||||

| 3,500,000 | STC Metropolitan District No. 2 LTD Tax G.O. Subordinate Series 2015B, 7.75% due 12/15/2038 |

3,504,585 | ||||||||

| 2,195,000 | Sterling Ranch Community Authority Board LTD Tax Supported Revenue Senior Series 2015A, 5.50% to yield 5.60% due 12/1/2035 |

2,203,934 | ||||||||

| 3,000,000 | Sterling Ranch Community Authority Board LTD Tax Supported Revenue Senior Series 2015A, 5.75% to yield 5.83% due 12/1/2045 |

3,020,610 | ||||||||

| 1,045,000 | Sterling Ranch Community Authority Board LTD Tax Supported Revenue Subordinate Series 2015B, 7.75% due 12/15/2045 |

1,032,868 | ||||||||

| 1,615,000 | Table Mountain Metropolitan District LTD Tax (Convertible to Unlimited Tax) G.O. Series 2016A, 5.25% due 12/1/2045 |

1,651,661 | ||||||||

| 570,000 | Table Mountain Metropolitan District Subordinate LTD Tax G.O. Series 2016B, 7.75% due 12/15/2045 |

569,783 | ||||||||

| 2,070,000 | Tallyn’s Reach Metropolitan District No. 3 LTD Tax (Convertible to Unlimited Tax) G.O. Refunding and Improvement Series 2013, 5.125% to yield 4.681% due 11/1/2038 |

2,158,286 | ||||||||

| 1,220,000 | Tallyn’s Reach Metropolitan District No. 3 Subordinate LTD Tax G.O. Series 2016A, 6.75% due 11/1/2038 |

1,219,890 | ||||||||

| 11,045,000 | United Water & Sanitation District (Lupton Lakes Water Storage Project and Water Activity Enterprise) Revenue Series 2006, 6.00% due 3/1/2021 |

11,075,374 | ||||||||

| 6,875,000 | United Water & Sanitation District Ravenna Project Water Activity Enterprise Convertible Capital Appreciation Series 2007, 6.125% due 12/1/2037 |

6,108,506 | ||||||||

| 6,637,000 | United Water & Sanitation District United Water Acquisition Project Water Activity Enterprise Revenue Refunding Series 2012, 6.00% due 12/1/2023 |

6,645,296 | ||||||||

| 1,934,000 | VDW Metropolitan District No. 2 Subordinate LTD Tax G.O. Series 2016B, 7.25% due 12/15/2045 |

1,889,847 | ||||||||

20

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Colorado Municipal Bonds — (Continued) | ||||||||||

| 11,500,000 | Valagua Metropolitan District G.O. LTD Tax Series 2008, 7.75% to yield 7.75% – 31.02% due 12/1/2037 |

$ | 2,639,940 | |||||||

| 355,000 | The Villas at Eastlake Reservoir Metropolitan District Subordinate G.O. LTD Tax Series 2016B, 8.00% due 12/15/2046 |

361,326 | ||||||||

| 2,250,000 | Waterfront Metropolitan District LTD Tax (Convertible to Unlimited Tax) G.O. Refunding & Improvement Series 2007, 4.25% to yield 7.794% due 12/1/2032 |

2,249,978 | ||||||||

|

|

|

|||||||||

| Total Colorado Municipal Bonds (amortized cost $630,274,635) |

$ | 606,176,844 | ||||||||

|

|

|

|||||||||

| Short-Term Municipal Bonds — 23.3% | ||||||||||

| 10,245,000 | Broomfield Urban Renewal Authority Tax Increment Revenue (Broomfield Event Center Project) Series 2005, 1.02%, due 12/1/2030 (LOC 1) |

$ | 10,245,000 | |||||||

| 3,435,000 | Colorado Housing and Finance Authority Multi-Family/Project Class I Adjustable Rate 2008 Series C-3, 0.95% due 10/1/2038 (LOC 2) |

3,435,000 | ||||||||

| 1,665,000 | Colorado Housing and Finance Authority Single Family Mortgage Class I Adjustable Rate 2006 Series A-2, 0.95% due 11/1/2034 (LOC 2) |

1,665,000 | ||||||||

| 12,555,000 | Colorado Housing and Finance Authority Single Family Mortgage Class II Adjustable Rate 2013 Series B, 0.96% due 11/1/2036 (LOC 4) |

12,555,000 | ||||||||

| 2,920,000 | Colorado Housing and Finance Authority Manufacturing Revenue (Ready Foods, Inc. Project) Series 2007A, 0.99% due 1/1/2032 (LOC 3) |

2,920,000 | ||||||||

| 7,730,000 | Colorado Springs (City of) Variable Rate Demand Utilities System Improvement Revenue Series 2010C, 0.95% due 11/1/2040 (LOC 5) |

7,730,000 | ||||||||

| 1,400,000 | Colorado Springs (City of) Variable Rate Demand Utilities System Improvement Revenue Series 2012A, 0.95% due 11/1/2041 (LOC 3) |

1,400,000 | ||||||||

| 19,800,000 | Colorado Springs Urban Renewal Authority Tax Increment Revenue (University Village Project) Series 2008A Senior, 7.00% to yield 7.00% – 9.00% due 12/1/2029(b) |

20,004,730 | ||||||||

| 6,400,000 | Colorado Springs Urban Renewal Authority Tax Increment Revenue (University Village Project) Series 2008B Subordinate (Convertible to Senior), 7.50% due 12/15/2029(b) |

6,599,040 | ||||||||

| 435,000 | Confluence Metropolitan District (in the town of Avon) Tax Supported Revenue Series 2007, 5.25% to yield 6.929% due 12/1/2017 |

434,622 | ||||||||

| 15,725,000 | Flying Horse Metropolitan District No. 2 Refunding and Improvement Subordinate LTD Tax G.O. Convertible Capital Appreciation Series 2013B, 8.00% due 12/15/2042(d) |

13,086,817 | ||||||||

| 39,200,000 | Freddie Mac Multifamily Variable Rate Certificates Class A Series M015, 1.00% due 5/15/2046 (LOC 6) |

39,200,000 | ||||||||

| 29,165,000 | Freddie Mac Multifamily Variable Rate Certificates Class A Series M021, 1.01% due 6/15/2036 (LOC 6) |

29,165,000 | ||||||||

| 10,590,000 | Freddie Mac Multifamily Variable Rate Certificates Class A Series M024, 1.00% due 7/15/2050 (LOC 6) |

10,590,000 | ||||||||

21

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Short-Term Municipal Bonds — (Continued) | ||||||||||

| 21,330,000 | Freddie Mac Multifamily Variable Rate Certificates Class A Series M-031, 0.98% due 12/15/2045 (LOC 6) |

$ | 21,330,000 | |||||||

| 36,560,000 | Freddie Mac Multifamily Variable Rate Certificates Class A Series M-033, 0.98% due 3/15/2049 |

36,560,000 | ||||||||

| 145,000 | Fronterra Village Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Refunding & Improvement Series 2007, 4.375% – 5.00% to yield 4.552% – 7.135% due 12/1/2017-2034 |

145,695 | ||||||||

| 620,000 | Fort Lupton Golf Course Revenue Anticipation Warrants Senior Series 1996A, 8.50% due 12/15/2015(a) |

6 | ||||||||

| 14,000,000 | PV Water and Sanitation Metropolitan District Capital Appreciation Revenue Series 2006, 6.00% due 12/15/2017(a)(d) |

3,325,000 | ||||||||

| 9,000,000 | Ravenna Metropolitan District G.O. LTD Tax Series 2007, 7.00% due 12/1/2037(j) |

9,000,000 | ||||||||

| 2,380,000 | Ravenna Metropolitan District Supplemental “B” Interest Registered Coupons, 8.25% due 12/1/2016(d)(j) |

2,380,000 | ||||||||

| 6,700,000 | Sheridan Redevelopment Agency Variable Rate Tax Increment Refunding Revenue (South Santa Fe Drive Corridor Redevelopment Project) Series 2011A-1, 1.00% due 12/1/2029 (LOC 5) |

6,700,000 | ||||||||

| 17,315,000 | SunAmerica Variable Rate Class A Series 2001-2, 1.00% due 7/1/2041 (LOC 6) |

17,315,000 | ||||||||

| 8,920,000 | United Water & Sanitation District Ravenna Project Water Activity Enterprise Capital Appreciation Revenue Refunding Series 2009, 6.50% due 12/15/2016(a)(d)(j) |

8,920,000 | ||||||||

|

|

|

|||||||||

| Total Short-Term Municipal Bonds (amortized cost $272,813,298) |

$ | 264,705,910 | ||||||||

|

|

|

|||||||||

| Other Municipal Bonds — 4.2% | ||||||||||

| 4,904,915 | Freddie Mac Multifamily Variable Rate Certificates Series M001 Class B, 7.80% due 4/1/2037(g)(j) |

$ | 4,904,915 | |||||||

| 6,055,000 | Flandreau Santee Sioux Tribe Tribal Health Care Revenue (Indian Health Service Joint Venture Construction Program Project) Series 2016, 5.75% due 1/1/2036 |

5,477,111 | ||||||||

| 4,125,000 | Flandreau Santee Sioux Tribe Tribal Health Care Revenue (Indian Health Service Joint Venture Construction Program Project) Series 2016, 5.00% due 1/1/2026 |

3,882,161 | ||||||||

| 3,565,000 | Flandreau Santee Sioux Tribe Tribal Health Care Revenue (Indian Health Service Joint Venture Construction Program Project) Series 2016, 5.50% due 1/1/2031 |

3,277,804 | ||||||||

| 450,000 | Haskell County, Oklahoma Public Facilities Authority Junior Lien Sales Tax Revenue Note Series 2015, 5.25% due 4/1/2024 |

445,559 | ||||||||

| 516,000 | The Industrial Development Authority of the City of Kansas City, Missouri Multi-family Housing Revenue (Alexandria Apartments) Series 2005A, 6.75% due 1/1/2028 |

518,100 | ||||||||

| 1,435,000 | Lower Brule Sioux Tribe (Lower Brule, South Dakota) Tribal Purpose Refunding Tax-Exempt Series 2014C, 5.875% due 3/01/2025 |

1,449,422 | ||||||||

22

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

Value |

|||||||||

| Other Municipal Bonds — (Continued) | ||||||||||

| 6,345,000 | The Hospital Facilities Authority of Multnomah County, Oregon Revenue Refunding (Odd Fellows Home-Friendship Health Center) Series 2013A, 5.45% due 9/15/2020 |

$ | 6,344,428 | |||||||

| 1,560,000 | Oglala Sioux Tribe (Pine Ridge, South Dakota) Essential Governmental Function Revenue and Refunding Series 2012, 5.00% due 10/1/2022 |

1,559,875 | ||||||||

| 1,985,000 | Oglala Sioux Tribe (Pine Ridge, South Dakota) Essential Governmental Function Revenue Tax-Exempt Series 2014B, 5.50% to yield 5.70% due 10/1/2024 |

2,000,622 | ||||||||

| 2,500,000 | Commonwealth of Puerto Rico G.O. 2014 Series A, 8.00% due 7/1/2035(a) |

1,212,500 | ||||||||

| 7,100,000 | Puerto Rico Sales Tax Financing Corporation Sales Tax Revenue Series 2007A Capital Appreciation 6.75% due 8/01/2045(d) |

1,485,462 | ||||||||

| 20,000,000 | Puerto Rico Sales Tax Financing Corporation Sales Tax Revenue Senior Series 2011C Capital Appreciation 8.00% due 8/01/2038(d) |

3,374,000 | ||||||||

| 10,000,000 | Puerto Rico Sales Tax Financing Corporation Sales Tax Revenue Senior Series 2011C Capital Appreciation 8.00% due 8/01/2039(d) |

1,579,800 | ||||||||

| 898,000 | The Industrial Development Authority of the City of St. Louis, Missouri Senior Housing Revenue (Grant School Apartments) Series 2005A, 6.75% due 5/1/2027 |

864,882 | ||||||||

| 5,655,000 | South Carolina Jobs-Economic Development Authority Economic Development Revenue (GREEN Midlands, LLC Project) Series 2016A, 5.25% due 12/1/2021 |

5,678,129 | ||||||||

| 3,495,000 | Tacoma, Washington (City of) Consolidated LID District No.65, 5.75% to yield 5.75% – 6.22% due 4/1/2043 |

3,496,468 | ||||||||

|

|

|

|||||||||

| Total Other Municipal Bonds (amortized cost $49,671,322) |

$ | 47,551,238 | ||||||||

|

|

|

|||||||||

| Colorado Capital Appreciation and Zero Coupon Bonds — 1.9% | ||||||||||

| 2,025,000 | Bramming Farm Metropolitan District No. 1 G.O. (LTD Tax Convertible to Unlimited Tax) Capital Appreciation Series 2015, 5.25% due 12/1/2044(d) |

$ | 1,998,918 | |||||||

| 520,000 | Colorado Health Facilities Authority Zero Coupon Retirement Housing Revenue (Liberty Heights Project) 1990 Subordinate Series B, 6.97% due 7/15/2020(b)(d) |

499,382 | ||||||||

| 7,470,000 | Conifer Metropolitan District Jefferson County Supplemental Interest Coupons Series 2006, 8.00% due 12/1/2010-12/1/2031(a)(d)(j) |

3,352,311 | ||||||||

| 7,205,000 | Southshore Metropolitan District No. 2 G.O. (LTD Tax Convertible to Unlimited Tax) Convertible Capital Appreciation Series 2015, 6.50% due 12/1/2042(d) |

7,208,819 | ||||||||

| 6,685,000 | Sterling Ranch Metropolitan District No. 2 G.O. LTD Tax Convertible Capital Appreciation Series 2015, 8.00% due 12/1/2045(d) |

5,121,245 | ||||||||

| 2,286,030 | United Water & Sanitation District Ravenna Project Water Activity Enterprise Capital Appreciation Subordinate Series 2006B, 7.00% due 12/15/2011(d)(j) |

2,171,729 | ||||||||

| 2,720,000 | Wildwing Metropolitan District No. 1 Capital Appreciation Revenue Series 2008, 7.50% due 12/1/2023(d) |

1,686,400 | ||||||||

|

|

|

|||||||||

| Total Colorado Capital Appreciation and Zero Coupon Bonds (amortized cost $22,645,952) |

$ | 22,038,804 | ||||||||

|

|

|

|||||||||

23

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| Face Amount |

|

Value |

||||||||||

| Colorado Taxable Bonds/Certificates/Notes — 0.8% | ||||||||||||

| 1,806,518 | 777 S High Street LLC, Tax Lien Receipt Certificates, 9.00% due 2/28/2019(j)(m) |

|

$ | 1,806,518 | ||||||||

| 7,105,000 | Public Finance Authority Charter School Refunding and Improvement Draw-Down Revenue (Colorado Early Colleges Project) Charter Schools Authorized Through the Colorado Charter School Institute Taxable Series 2016B, 5.75% due 7/1/2023 |

|

7,005,317 | |||||||||

| 227,347 | Note receivable from Tabernash Meadows, LLC, a Colorado limited liability company, 24.00% due 2/9/2002(a)(j) |

|

127,601 | |||||||||

|

|

|

|||||||||||

| Total Colorado Taxable Bonds/Certificates/Notes (amortized cost $9,138,865) |

|

$ | 8,939,436 | |||||||||

|

|

|

|||||||||||

| Total investments, at value (amortized cost $984,544,072) |

83.4% | $ | 949,412,232 | |||||||||

| Other assets net of liabilities |

16.6% | 188,404,978 | ||||||||||

|

|

|

|

|

|||||||||

| Net assets |

100.0% | $ | 1,137,817,210 | |||||||||

|

|

|

|

|

|||||||||

24

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| (a) | Defaulted or non-income producing based upon the financial condition of the issuer (see note 2 in notes to financial statements). |

| (b) | Originally issued as general obligation bonds but are now pre-refunded and are secured by an escrow fund consisting entirely of direct U.S. Government obligations. |

| (c) | Represents securities whose blended characteristics are reflective of a zero coupon bond and a step rate bond. Interest rate shown represents effective yield at acquisition. |

| (d) | Interest rate shown for capital appreciation and zero coupon bonds represents the effective yield at the date of acquisition. |

| (e) | Principal-only certificate represents the right to receive the principal payments on the underlying debt security upon maturity. The price of this security is typically more volatile than that of coupon-bearing bonds of the same maturity. |

| (f) | Interest-only certificate represents the right to receive semi-annual interest payments on the underlying debt security. The principal amount of the underlying security represents the notional amount on which current interest is calculated. The interest rate shown represents the effective yield at the date of acquisition. |

| (g) | Interest rate disclosed for cash flow bond represents the effective yield at September 30, 2017. Income on this security is derived from the cash flow of the issuer. |

| (h) | Represents current interest rate for a step rate bond. No step rate bonds were owned by the Fund at September 30, 2017. |

| (i) | Terms of security have been restructured since the original issuance. The total face amount of all such restructured securities approximates $10,969,352 and a value of $6,764,074 or less than 1.0% of net assets, as of September 30, 2017. |

| (j) | Securities valued at fair value (see note 2 in notes to financial statements). |

| (k) | See note 7 in notes to financial statements for further information on purchase accrued interest related to these bonds. |

| (l) | The Fund has entered into a forbearance agreement under which it agrees that the issuer may pay a reduced rate of interest in lieu of the contract rate for a period of time (see note 2 in notes to financial statements). |

| (m) | Tax lien receipt certificates. |

See accompanying notes to financial statements.

25

Table of Contents

Colorado BondShares

A Tax-Exempt Fund

Schedule of Investments — (Continued)

| (LOC) | These securities are Variable Rate Demand Obligations (“VRDO”) with scheduled principal and interest payments that have a guaranteed liquidity provider in the form of a letter of credit. These obligations bear interest at a rate that resets daily or weekly (see note 2 in notes to financial statements). The numbered list below corresponds to the liquidity provider associated with the respective LOC. |

1. BNP Paribas

2. FHLB Topeka

3. US Bank, N. A.

4. Royal Bank of Canada