UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|X| ANNUAL REPORT PURSUANT TO SECTION

13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2002

OR

|_|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

| Commission File Number |

Registrants, State

of Incorporation, Address, and Telephone Number |

I.R.S. Employer Identification No. |

||

| |

|

|

||

| 001-09120 | PUBLIC SERVICE

ENTERPRISE GROUP INCORPORATED (A New Jersey Corporation) 80 Park Plaza P.O. Box 1171 Newark, New Jersey 07101-1171 973 430-7000 http://www.pseg.com |

22-2625848 | ||

| 001-00973 | PUBLIC SERVICE

ELECTRIC AND GAS COMPANY (A New Jersey Corporation) 80 Park Plaza, P.O. Box 570 Newark, New Jersey 07101-0570 973 430-7000 http://www.pseg.com |

22-1212800 | ||

| 000-49614 | PSEG POWER LLC (A Delaware Limited Liability Company) 80 Park Plaza – T25 Newark, New Jersey 07102-4194 973 430-7000 http://www.pseg.com |

22-3663480 | ||

| 000-32503 | PSEG ENERGY HOLDINGS

LLC (A New Jersey Limited Liability Company) 80 Park Plaza –T22 Newark, New Jersey 07102-4194 973 456-3581 http://www.pseg.com |

22-2983750 |

Securities registered pursuant to Section 12 (b) of the Act:

| Registrant | Title of Each Class | Title of Each Class | Name of Each Exchange On Which Registered | |||||||

| |

||||||||||

| Public Service Enterprise | Common Stock without par value | New York Stock Exchange | ||||||||

| Group Incorporated | ||||||||||

| Public Service Electric and | Cumulative Preferred Stock | First and Refunding Mortgage Bonds: | ||||||||

| Gas Company | $100 par value Series: | Series | Due | |||||||

| 4.08% | 9 1/8% | BB | 2005 | |||||||

| 4.18% | 9 1/4% | CC | 2021 | |||||||

| 4.30% | 8 7/8% | DD | 2003 | New York Stock Exchange | ||||||

| 5.05% | 6 7/8% | MM | 2003 | |||||||

| 5.28% | 6 1/2% | PP | 2004 | |||||||

| 7% | SS | 2024 | ||||||||

| 7 3/8% | TT | 2014 | ||||||||

| 6 3/4% | UU | 2006 | ||||||||

| 6 3/4% | VV | 2016 | ||||||||

| 6 1/4% | WW | 2007 | ||||||||

| 6 3/8% | YY | 2023 | ||||||||

| 8% | 2037 | |||||||||

| 5% | 2037 | |||||||||

| PSEG Power LLC | NONE | NONE | NONE | |||||||

| PSEG Energy Holdings LLC | NONE | NONE | NONE | |||||||

Participating Equity Preference Securities (consisting of a Purchase Contract and a Preferred Trust Security of PSEG Funding Trust I (Registrant) and registered on the New York Stock Exhange.

Trust Originated Preferred Securities (Guaranteed Preferred Beneficial Interest in PSEG’s Debentures), $25 par value at 8.75%, issued by PSEG Funding Trust II (Registrant) and registered on the New York Stock Exchange.

Monthly Income Preferred Securities (Guaranteed Preferred Beneficial Interest in PSE&G’s Subordinated Debenture), $25 par value at 8.00%, issued by Public Service Electric and Gas Capital, L.P. (Registrant) and registered on the New York Stock Exchange.

Quarterly Income Preferred Securities (Guaranteed Preferred Beneficial Interest in PSE&G’s Subordinated Debentures), $25 par value at 8.125%, issued by PSE&G Capital Trust II (Registrant) and registered on the New York Stock Exchange.

Securities registered pursuant to Section 12 (g) of the Act:

| Registrant | Title of Class |

| Public Service Enterprise Group Incorporated | Floating Rate Capital Securities (Guaranteed Preferred Beneficial Interest in |

| PSEG’s Debentures), $1,000 par value issued by Enterprise Capital Trust II | |

| (Registrant), LIBOR plus 1.22%. | |

| Trust Originated Preferred Securities (Guaranteed Preferred Beneficial | |

| Interest in PSEG’s Debentures), $25 par value at 7.44%, issued by Enterprise | |

| Capital Trust I (Registrant). | |

| Trust Originated Preferred Securities (Guaranteed Preferred Beneficial | |

| Interest in PSEG’s Debentures), $25 par value at 7.25%, issued by Enterprise | |

| Capital Trust III (Registrant). | |

| Public Service Electric and Gas Company | 6.92% Cumulative Preferred Stock $100 par value |

| Medium-Term Notes, Series A | |

| PSEG Power LLC | Limited Liability Company Membership Interest |

| PSEG Energy Holdings LLC | Limited Liability Company Membership Interest |

The aggregate market value of the Common Stock of Public Service Enterprise Group Incorporated as of June 28, 2002 was $8,947,292,512 based upon the New York Stock Exchange Composite Transaction closing price. The aggregate market value of the Common Stock of Public Service Enterprise Group Incorporated held by non-affiliates as of January 31, 2003 was $7,949,509,112 based upon the New York Stock Exchange Composite Transaction closing price.

The number of shares outstanding of Public Service Enterprise Group Incorporated’s sole class of Common Stock, as of the latest practicable date, was as follows:

| Class | Outstanding at January 31, 2003 |

| |

|

| Common Stock, without par value | 225,326,222 |

PSEG Power LLC and PSEG Energy Holdings LLC are wholly-owned subsidiaries of Public Service Enterprise Group Incorporated and meet the conditions set forth in General Instruction I (1) (a) and (b) of Form 10-K and are filing their respective Annual Reports on Form 10-K with the reduced disclosure format authorized by General Instruction I.

As of January 31, 2003, Public Service Electric and Gas Company had issued and outstanding 132,450,344 shares of Common Stock, without nominal or par value, all of which were privately held, beneficially and of record by Public Service Enterprise Group Incorporated.

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports) and (2) have been subject to such filing requirements for the past 90 days. Yes |X| No |_|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. |X|

Indicate by check mark whether any registrant is an accelerated filer (as defined in Rule 12b-2 of the Act). Yes |X| No |_|

DOCUMENTS INCORPORATED BY REFERENCE

| Part of Form 10-K of Public Service Enterprise Group Incorporated | Documents Incorporated by Reference | |

| | ||

| III | Portions of the definitive Proxy Statement for the Annual Meeting of Stockholders of Public Service Enterprise Group | |

| Incorporated to be held April 15, 2003, which definitive Proxy Statement is expected to be filed with the Securities and | ||

| Exchange Commission on or about March 7, 2003, as specified herein. |

| TABLE OF CONTENTS | |||

| |

|||

| Page | |||

| PART I | |||

| Item 1. | Business | 1 | |

| General | 1 | ||

| Competitive Environment | 11 | ||

| Regulatory Issues | 12 | ||

| Customers | 18 | ||

| Employee Relations | 19 | ||

| Segment Information | 19 | ||

| Environmental Matters | 19 | ||

| Item 2. | Properties | 26 | |

| Item 3. | Legal Proceedings | 38 | |

| Item 4. | Submission of Matters to a Vote of Security Holders | 40 | |

| PART II | |||

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters | 41 | |

| Item 6. | Selected Financial Data | 42 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 44 | |

| Overview of 2002 and Future Outlook | 44 | ||

| Results of Operations | 51 | ||

| Liquidity and Capital Resources | 65 | ||

| Capital Requirements | 72 | ||

| Accounting Issues | 75 | ||

| Forward Looking Statements | 82 | ||

| Item 7A. | Qualitative and Quantitative Disclosures About Market Risk | 84 | |

| Item 8. | Financial Statements and Supplementary Data | 90 | |

| Financial Statement Responsibility | 91 | ||

| Independent Auditors’ Report | 95 | ||

| Consolidated Financial Statements | 99 | ||

| Notes to Consolidated Financial Statements | 118 | ||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 193 | |

| PART III | |||

| Item 10. | Directors and Executive Officers | 193 | |

| Item 11. | Executive Compensation | 197 | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management | 202 | |

| Item 13. | Certain Relationships and Related Transactions | 203 | |

| Item 14. | Disclosure Controls and Procedures | 204 | |

| PART IV | |||

| Item 15. | Exhibits, Financial Statement Schedules and Reports on Form 8-K | 213 | |

| Schedule II—Valuation and Qualifying Accounts | 215 | ||

| Signatures | 217 | ||

| Exhibit Index | 221 | ||

i

PART I

This combined Form 10-K is separately filed by Public Service Enterprise Group Incorporated (PSEG), Public Service Electric and Gas Company (PSE&G), PSEG Power LLC (Power) and PSEG Energy Holdings LLC (Energy Holdings). Information contained herein relating to any individual company is filed by such company on its own behalf. PSE&G, Power and Energy Holdings each make representations only as to itself and its subsidiaries and makes no other representations whatsoever as to any other company.

ITEM 1. BUSINESS

GENERAL

PSEG, PSE&G, Power and Energy Holdings

PSEG, incorporated under the laws of the State of New Jersey on July 25, 1985, with its principal executive offices located at 80 Park Plaza, Newark, New Jersey 07102, is an exempt public utility holding company under the Public Utility Holding Company Act of 1935 (PUHCA).

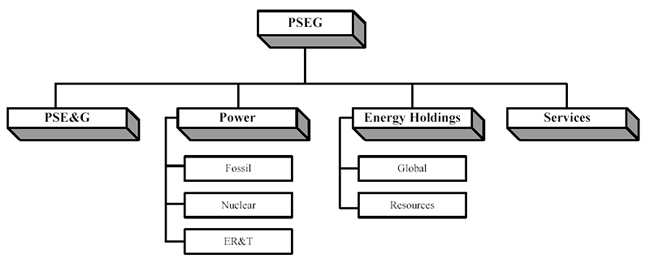

PSEG has four principal direct wholly-owned subsidiaries: PSE&G, Power, Energy Holdings and PSEG Services Corporation (Services). The following organization chart shows PSEG and its principal subsidiaries, as well as the principal operating subsidiaries of Power: PSEG Fossil LLC (Fossil), PSEG Nuclear LLC (Nuclear) and PSEG Energy Resources & Trade LLC (ER&T); and of Energy Holdings: PSEG Global Inc. (Global) and PSEG Resources LLC (Resources):

The regulatory structure which has historically governed the electric and gas utility industries in the United States has changed dramatically in recent years and continues to be in transition. Deregulation is essentially complete in New Jersey and is complete or underway in certain other states in the Northeast and across the United States (US). States have acted independently to deregulate the electric and gas utility industries. Experience in deregulating California, with energy shortages, high costs and financial difficulties of utilities and high profile bankruptcies have caused some states to re-evaluate and, in some cases, stop the move toward deregulation. The deregulation and restructuring of the nation’s energy markets, the unbundling of energy and related services, the diverse strategies within the industry related to holding, building, buying or selling generation capacity and the anticipated resulting industry consolidation have had, and are likely to continue to have, a profound effect on PSEG and its subsidiaries, providing it with new opportunities and exposing it to new risks. For further information, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation (MD&A) — Overview of 2002 and Future Outlook.

1

The National Energy Policy Act of 1992 (Energy Policy Act) laid the groundwork for competition in the wholesale electricity markets in the United States. This legislation expanded the Federal Energy Regulatory Commission’s (FERC) authority to order electric utilities to open their transmission systems to allow third-party suppliers to transmit, or “wheel,” electricity over their lines. In 1996, FERC initiated regulatory actions that resulted in expanded access to transmission lines, providing eligible third-party wholesale marketers clear transmission access. These actions have afforded power marketers, merchant generators, Exempt Wholesale Generators (EWGs) and utilities the opportunity to compete actively in wholesale energy markets, and afforded consumers the right to choose their energy suppliers.

Worldwide energy industry deregulation, restructuring, privatization and consolidation are creating opportunities and risks for PSEG, PSE&G, Power and Energy Holdings. Over recent years, PSEG has realigned its organizational structure to address the competitive environment brought about by the deregulation of the electric generation industry and has transitioned from primarily being a regulated New Jersey utility to operating as a competitive energy company with operations primarily in the Northeastern US and in other select domestic and international markets. As the unregulated portion of the business continues to grow, financial risks and rewards will be greater, financial requirements will change and the volatility of earnings and cash flows will increase. As of December 31, 2002, Power, PSE&G, and Energy Holdings comprised approximately 27%, 48% and 27% of PSEG’s consolidated assets and contributed approximately 60%, 26% and 18% of PSEG’s results, excluding certain charges. For additional information, see Item 7. MD&A — Overview of 2002 and Future Outlook.

PSE&G and Power

Following the enactment of the New Jersey Electric Discount and Energy Competition Act, as amended (Energy Competition Act), the New Jersey Board of Public Utilities (BPU) rendered its Final Decision and Order (Final Order) in 1999 relating to PSE&G’s rate unbundling, stranded costs and restructuring proceedings providing, among other things, for the transfer to an affiliate of all of PSE&G’s electric generation facilities, plant and equipment for $2.4 billion and all other related property, including materials, supplies and fuel at the net book value thereof, together with associated rights and liabilities. PSE&G, pursuant to the Final Order, transferred its electric generating facilities and wholesale power contracts to Power and its subsidiaries in August 2000 for $2.8 billion.

Subsequently, Power entered into a BPU approved fixed price requirements contract (Basic Generation Service (BGS) contract) to supply all of PSE&G’s load requirement for its electric customers not choosing an alternative supplier, which terminated on July 31, 2002, under which Power sold energy directly to PSE&G which in turn sold this energy to its customers. Subsequent to July 31, 2002, Power primarily sells its energy and capacity to third parties that supply New Jersey’s electric distribution companies (EDCs) participating in the BPU approved BGS auctions in New Jersey. PSE&G purchases the energy required to meet its customers’ needs from third party suppliers through such auction process.

BGS Supply

PSE&G is required to determine BGS suppliers by competitive bid in accordance with BPU requirements. In February 2002, an internet auction was held to determine who would supply BGS to PSE&G and the other three BPU regulated New Jersey electric utility companies for the period August 1, 2002 to July 31, 2003. As conditions of qualification to participate in this auction, energy suppliers agreed to execute the BGS Master Service Agreement and provide required security bonds within two days of BPU Certification of auction results, in addition to satisfying BPU credit worthiness requirements.

In February 2002 the BPU approved the BGS auction results and PSE&G secured contracts from a number of suppliers for its expected peak load of 9,600 MW through 96 notional tranches of 100 MW each. Under these contracts, the suppliers have the full load serving responsibility and bear the risks of volatility in energy prices due to various factors such as changes in weather, seasonality and transmission constraints. Subsequently, certain BGS suppliers experienced adverse credit issues and therefore, these suppliers assigned contracts to other parties. Under the BPU approved supply contracts, PSE&G is paying $.0511 per kWh to obtain electricity for BGS customers for the period from August 1, 2002 to July 31, 2003. Customers will continue to pay below-market regulated rates (BGS shopping credit) for this one-year period. Under PSE&G’s current rate structure, the difference is being

2

deferred and is expected to be recovered with interest through a future securitization. PSE&G estimates that the underrecovery relating to the BGS for the one-year period ending July 31, 2003 will amount to approximately $241 million.

As a result of the initial New Jersey BGS auction, Power contracted to provide energy to the direct suppliers of New Jersey electric utilities, including PSE&G, commencing August 1, 2002. Subsequently, a portion of the contracts with those bidders was reassigned to Power. Therefore, for a limited portion of the New Jersey retail load, Power will be a direct supplier to one utility, although this utility is not PSE&G.

New Jersey’s EDCs, including PSE&G, will provide two types of BGS service beginning in August 2003. The BPU authorized two concurrent auctions of New Jersey’s Basic Generation Service which were held in February 2003. The first was a general auction to procure approximately 15,500 MW of supply for ten-month and 34-month periods for smaller commercial and residential customers at seasonally-adjusted fixed prices. The other auction was held to procure approximately 2,600 MW of supply for larger customers for a 10-month period at hourly market prices. In total, the EDCs sought and obtained over 18,000 MW of combined full-requirements electric service. In February 2003, the BPU approved the auction results and PSE&G secured contracts from a number of suppliers to meet its requirements. Under the contracts, PSE&G is paying $.05386 and $.05560 per kWh for the ten-month tranche and 34-month tranche, respectively, to obtain electricity for customers for the periods beginning August 1, 2003.

Power was a participant in the BGS auction held in February 2003. Power entered into hourly energy price contracts to be a direct supplier of certain large customers for a ten-month period beginning August 1, 2003. Power also entered into contracts with third parties who are direct suppliers of New Jersey’s EDCs. Through these seasonally-adjusted fixed price contracts, Power will indirectly serve New Jersey’s smaller commercial and residential customers for ten-month and 34-month periods beginning August 1, 2003. Power believes that its obligations under these contracts are reasonably balanced by its available supply.

BGSS

On April 17, 2002, the BPU issued the Final Order approving the transfer of PSE&G’s gas supply business. Pursuant to such order, in May 2002, PSE&G transferred its gas supply contracts and gas inventory to Power for approximately $183 million and similarly, entered into a requirements contract with Power under which Power sells gas supply services directly to PSE&G needed to meet PSE&G’s Basic Gas Supply Service (BGSS) requirements. The contract term ends March 31, 2004, after which PSE&G has a three-year renewal option. As part of the agreement, PSE&G is providing Power the use of its peak shaving facilities at cost.

On May 1, 2002, the New Jersey Ratepayer Advocate filed a motion for the reconsideration of the BPU’s approval of the gas contract transfer. On October 31, 2002, the BPU issued an order denying the motion for reconsideration, except for the issue of valuation. The BPU retains the right to review the valuation of the contracts transferred if FERC modifies the capacity release rules prior to the contract expirations.

PSE&G

PSE&G is a New Jersey corporation, incorporated on July 25, 1924, with its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102. PSE&G is an operating public utility company engaged principally in the transmission and distribution of electric energy and gas service in New Jersey. PSE&G continues to own and operate its electric and gas transmission and distribution business. PSE&G Transition Funding LLC (Transition Funding), a bankruptcy remote subsidiary of PSE&G, was formed solely to issue $2.525 billion principal amount of transition bonds in connection with the securitization of $2.4 billion of PSE&G’s approved stranded costs approved for recovery by the BPU under the Energy Competition Act.

PSE&G supplies electric and gas service in areas of New Jersey in which approximately 5.5 million people, about 70% of the State’s population, reside. PSE&G’s electric and gas service area is a corridor of approximately 2,600 square miles running diagonally across New Jersey from Bergen County in the northeast to an area below the city of Camden in the southwest. The greater portion of this area is served with both electricity and gas, but some parts are served with electricity only and other parts with gas only. This heavily populated, commercialized and

3

industrialized territory encompasses most of New Jersey’s largest municipalities, including its six largest cities—Newark, Jersey City, Paterson, Elizabeth, Trenton and Camden—in addition to approximately 300 suburban and rural communities. This service territory contains a diversified mix of commerce and industry, including major facilities of many corporations of national prominence. PSE&G’s load requirements are almost evenly split among residential, commercial and industrial customers. PSE&G believes that it has all the franchises (including consents) necessary for its electric and gas distribution operations in the territory it serves. Such franchise rights are not exclusive.

PSE&G distributes electric energy and gas to end-use customers within its designated service territory. All electric and gas customers in New Jersey have the ability to choose an electric energy and/or gas supplier. Pursuant to BPU requirements, PSE&G serves as the supplier of last resort for electric and gas customers within its service territory who do not choose an alternate supplier. PSE&G earns no margin on the commodity portion of its electric and gas sales. PSE&G earns margins through the transmission and distribution of electricity and gas. PSE&G’s revenues are based upon tariffs approved by the BPU and the FERC for these services. The demand for electric energy and gas by PSE&G’s customers is affected by customer conservation, economic conditions, weather and other factors not within its control. Rates for gas sold in interstate commerce are not subject to cost of service ratemaking but are subject to competitive pricing. See Regulatory Issues and Item 7. MD&A, for a further discussion of these matters.

Power

Power is a Delaware limited liability company, formed on June 16, 1999, with its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102. Power is a multi-regional, independent wholesale energy supply company that integrates its generating asset operations with its wholesale energy, fuel supply, energy trading and marketing and risk management function with three principal direct wholly-owned subsidiaries: Nuclear, which owns and operates nuclear generating stations, Fossil, which develops, owns and operates domestic fossil generating stations and ER&T, which markets the capacity and production of Fossil’s and Nuclear’s stations and manages the commodity price risks or market risks related to generation. Power’s subsidiary, PSEG Power Capital Investment Company (Power Capital), provides certain financing for Power’s subsidiaries.

Power’s target market, which it refers to as the Super Region, extends from Maine to the Carolinas and from the Atlantic Coast to Indiana, encompassing 36% of the nation’s power consumption. Power is the single largest power supplier in its primary market, the PJM Interconnection area, one of the nation’s largest and most well developed energy markets.

Power’s generation portfolio consists of 13,055 MW of installed capacity which is diversified by fuel source and market segment. In addition, Power is currently constructing projects which are expected to increase capacity by over 2,900 MW through 2005, net of planned retirements. For additional information, see Item 2. Properties.

Power participates primarily in the PJM market, where the pricing of energy is based upon the locational marginal price (LMP) set through power providers’ bids. Because of transmission constraints, the LMP tends to be higher in congested areas reflecting the bid prices of the higher cost units that are dispatched to supply demand and alleviate transmission constraints when coordination is sufficient to satisfy demand within PJM. These bids are capped at $1,000 per megawatt-hour (MWh). In the event that available generation within PJM is insufficient to satisfy demand, PJM may institute emergency purchases from adjoining regions for which there is no price cap.

As Exempt Wholesale Generators (EWGs) under FERC, Power’s subsidiaries do not directly serve any retail customers. Power uses its generation facilities primarily for the production of electricity for sale at the wholesale level. For a discussion of BGS Supply in New Jersey, see PSE&G and Power above.

4

Electric Fuel Supply

The following table indicates MWh output of Power’s generating stations by source of energy in 2002 and the estimated MWh output by source for 2003:

| Actual | Estimated | ||||

| Source | 2002 | 2003 (A) | |||

| |

|||||

| Nuclear: | |||||

| New Jersey facilities | 41 | % | 38% | ||

| Pennsylvania facilities | 21 | % | 19% | ||

| Fossil: | |||||

| Coal: | |||||

| New Jersey facilities | 13 | % | 11% | ||

| Pennsylvania facilities | 13 | % | 12% | ||

| Connecticut facilities | — | 5% | |||

| Oil and Natural Gas: | |||||

| New Jersey facilities | 11 | % | 9% | ||

| New York facilities | — | — | |||

| Connecticut facilities | — | 3% | |||

| Mid-West facilities | — | 2% | |||

| Pumped Storage | 1 | % | 1% | ||

| |

|||||

| Total | 100 | % | 100% | ||

| (A) | No assurances can be

given that actual 2003 output by source will match estimates. | |

| Fossil

Fuel Supply | ||

| Fossil

has an ownership interest in twelve fossil generating stations in New Jersey,

one fossil generating station in New York, two fossil generating stations

in Connecticut and two fossil generating stations in Pennsylvania. Fossil

is also in the process of constructing a fossil generating station in Ohio

and another in Indiana. Fossil has an ownership interest in one hydroelectric

pumped storage facility in New Jersey. For additional information, see Item

2. Properties — Power — Electric Generation Properties. | ||

| Fossil

uses coal, natural gas and oil for electric generation. These fuels are

purchased through various contracts and in the spot market. The majority

of Power’s fossil generating stations obtain their fuel supply from

within the US. In order to minimize emissions levels, the Connecticut generating

facilities use a specific type of coal which is obtained from Indonesia.

Fossil does not anticipate any difficulties in obtaining adequate coal,

natural gas and oil supplies for these facilities over the next several

years, however, if the supply of coal from Indonesia or equivalent coal

from other sources was not available for the Connecticut facilities, additional

capital expenditures could be required to modify the existing plants. For

additional information, see Item 2. Properties — Power. | ||

| Nuclear

Fuel Supply | ||

| Nuclear

has an ownership interest in five nuclear generating units and operates

three of them; the Salem Nuclear Generating Station, Units 1 and 2 (Salem

1 and 2) each owned 57.41% by Nuclear and 42.59% by Exelon Generation LLC

(Exelon), and the Hope Creek Nuclear Generating Station (Hope Creek), 100%

owned by Nuclear. Exelon operates the Peach Bottom Atomic Power Station

Units 2 and 3 (Peach Bottom 2 and 3), each of which is 50% owned by Nuclear.

For additional information, see Item 2. Properties. | ||

| Power

has several long-term purchase contracts with uranium suppliers, converters,

enrichers and fabricators to meet the currently projected fuel requirements

for Salem and Hope Creek. On average, Power has various multi-year requirements-based

purchase commitments that total approximately $88 million per year to meet

Salem and Hope Creek fuel needs. Power has been advised by Exelon that it

has similar purchase contracts to satisfy the fuel requirements for Peach

Bottom. Nuclear does not anticipate any difficulties in obtaining adequate

fuel supplies for these facilities over the next several years. | ||

5 | ||

Gas Supply

As described above, Power sells gas to PSE&G. About 40% of the peak daily gas requirements are provided through firm transportation which is available every day of the year. The remainder comes from field storage, liquefied natural gas, seasonal purchases, contract peaking supply, propane and refinery/landfill gas. Following the gas contract transfer in May 2002, Power purchased gas for its gas operations directly from natural gas producers and marketers. These supplies were transported to New Jersey by four interstate pipeline suppliers.

Power has approximately 1.1 billion cubic feet per day of firm transportation capacity under contract to meet the primary needs of the gas consumers of PSE&G. In addition, Power supplements that supply with a total storage capacity of 81 billion cubic feet that provides .94 billion cubic feet per day of gas during the winter season.

Power expects to meet the energy-related demands of its firm customers during the 2002-2003 and 2003-2004 winter seasons. However, the sufficiency of supply could be affected by several factors not within Power’s control, including curtailments of natural gas by its suppliers, the severity of the winter weather and the availability of feedstocks for the production of supplements to its natural gas supply. The adequacy of supply of all types of gas is affected by the nationwide availability of all sources of fuel for energy production.

ER&T

ER&T purchases all of the capacity and energy produced by Fossil and Nuclear. In conjunction with these purchases, ER&T uses commodity and financial instruments designed to cover estimated commitments for BGS and other bilateral contract agreements. ER&T also markets electricity, capacity, ancillary services and natural gas products on a wholesale basis throughout the Super Region. ER&T is a fully integrated wholesale energy marketing and trading organization that is active in the long-term and spot wholesale energy markets.

ER&T’s principal objectives are to sell and deliver physical power from Power’s generating assets, reduce earnings volatility through hedging activities, manage gas supply and BGSS contracts, procure low cost fuel and natural gas supplies and produce net earnings from trading energy-related products around Power’s physical assets. ER&T does not engage in the practice of simultaneous trading for the purpose of increasing trading volume or revenue (also known as round trips). Consistent with its business objectives, ER&T measures performance based on net earnings and overall team performance, not on volume or gross revenues. These are also the metrics used to measure performance under its incentive compensation programs. For further information, see Note 12. Risk Management of the Notes to the Consolidated Financial Statements (Notes).

Energy Holdings

Energy Holdings is a New Jersey limited liability company formed on October 31, 2002, which merged wth PSEG Energy Holdings Inc., which was incorporated on June 20, 1989. Energy Holdings principal executive offices are located at 80 Park Plaza, Newark, New Jersey 07102. Energy Holdings has two principal direct wholly-owned subsidiaries; Global and Resources. During the second quarter of 2002, Energy Holdings announced its intention to sell the businesses of PSEG Energy Technologies Inc. (Energy Technologies). See Note 5. Discontinued Operations of the Notes.

Global and Resources have more than 100 financial and operating investments. Energy Holdings has pursued investment opportunities in the rapidly changing global energy markets, with Global focusing on the operating segments of the electric industries and Resources primarily making financial investments in these industries.

6

Energy Holdings’ portfolio is diversified by number, type and geographic location of investments. As of December 31, 2002, assets were comprised of the following types:

| December 31, 2002 | ||

| Leveraged Leases (A) | 42 | % |

| International Electric Facilities | 20 | % |

| International Generation Plants | 22 | % |

| Domestic Generation Plants | 10 | % |

| Energy Services | 3 | % |

| Other Passive Financial Investments | 2 | % |

| Other | 1 | % |

(A) Leveraged Leases are primarily in energy related facilities and are discussed further under Resources.

The characteristics of each of these investment types are described in more detail below.

Global

Global is an independent power producer and distributor which develops, acquires, owns and operates electric generation, transmission and distribution facilities and is engaged in power production and distribution, including wholesale and retail sales of electricity, in selected domestic and international markets.

Global realized substantial growth prior to 2002, but has been faced with significant challenges as the electricity privatization model has experienced stress. These challenges include the Argentine economic, political and social crisis, recent issues in India, financial and political pressures in Brazil and Venezuela and the soft power market in Texas. A worldwide recession and a series of disruptive events have slowed privitization in many countries. See Item 7. MD&A — Overview of 2002 and Future Outlook for further details.

Generally, Global has sought to minimize risk in the development and operation of its generation projects by selecting partners with complementary skills, structuring long-term power purchase contracts, arranging financing prior to the commencement of construction and contracting for adequate fuel supply. Historically, Global’s operating affiliates have entered into long-term power purchase contracts, thereby selling the electricity produced for the majority of the project life. However, two plants in Texas and two plants in China operate as merchant plants without long-term power purchase contracts and a plant in Poland will likely do so as well. For a further discussion of the oversupply of energy in the Texas power market, see Item 7. MD&A — Future Outlook.

Fuel supply arrangements are designed to balance long-term supply needs with price considerations. Global’s project affiliates generally utilize long-term contracts and spot market purchases. Energy Holdings believes that there are adequate fuel supplies for the anticipated needs of its generating projects. Energy Holdings also believes that transmission access and capacity are sufficient at this time for its generation projects.

Global, to the extent practical, attempts to limit its financial exposure associated with each project and to mitigate development risk, foreign currency exposure, interest rate risk and operating risk, including exposure to fuel costs, through contracts. For a further discussion of these risks, see Item 7A. Qualitative and Quantitative Disclosures About Market Risk. In addition, project loan agreements are generally structured on a non-recourse basis. Further, Global generally structures project financing so that a default under one project’s loan agreement will have no effect on the loan agreements of other projects or Energy Holdings’ debt.

Global has ownership interests in 34 operating generation projects (excluding those in Argentina which were fully impaired in 2002) totaling 5,384 MW (2,476 MW net) and eight projects totaling 2,329 MW (1,042 MW net) in construction. Of Global’s generation projects in operation or construction, 1,449 MW net or 41% are located in the United States. Global is actively involved, through its joint ventures, in managing the operations of 28 operating generation projects and will be actively involved in managing the operations of 6 projects in construction.

Global has invested in four distribution companies (excluding those in Argentina which were fully impaired in 2002) which serve approximately 2.9 million customers in Brazil, Chile and Peru. Global is actively involved in

7

managing the operations of these distribution companies in accordance with shareholder agreements and/or operating contracts. Rate-regulated distribution assets represented 37% of Global’s assets, or $1.4 billion, as of December 31, 2002.

As of December 31, 2002, Global’s assets, which include consolidated projects and those accounted for under the equity method, and share of project MW, by region are as follows:

| 2002 | MW | |||

| (Millions) | ||||

| Generation | ||||

| North America | $ | 647 | 1,449 | |

| Latin America (1) | 359 | 247 | ||

| Asia Pacific | 148 | 738 | ||

| Europe (2) | 772 | 856 | ||

| India (3) | 200 | 228 | ||

| Distribution | ||||

| Latin America (1) | 1,391 | N/A | ||

| Other | ||||

| Other (4) | 285 | N/A | ||

| | ||||

| Total Assets | $ | 3,802 | 3,518 | |

| | ||||

| (1) | Investments in Argentina were fully impaired in 2002. | |

| (2) | Europe and Africa. | |

| (3) | India and the Middle East. The Tanir Bavi Power Company Ltd. (Tanir Bavi) plant in India was sold in October 2002. | |

| (4) | Assets not allocated

to a specific project, including corporate receivables. | |

| For

additional information, see Item 7. MD&A — Future Outlook. | ||

| Global’s

strategic focus has shifted to one of improving profitability for currently

held investments, from one of significant growth. Near-term emphasis will

be placed on liquidity and completing current projects. Global has developed

or acquired interests in electric generation and/or distribution facilities

in the United States, Brazil, Chile, China, India, Italy, Peru, Poland,

Tunisia and Venezuela. In addition, projects are in construction in the

United States, China, Italy, Oman, Poland, South Korea and Taiwan. While

Energy Holdings still expects certain of its investments in Latin America

to contribute significantly to its earnings in the future, the political

and economic risks associated with this region could have a material adverse

impact on its remaining investments in the region. See Item 7. MD&A

— Future Outlook for additional information. | ||

| For

a discussion of the asset impairments due to the Argentine economic, political

and social crisis, see Note 13. Commitments and Contingent Liabilities and

Note 4. Asset Impairments of the Notes. Also see Note 4. Asset Impairments

and Note 5. Discontinued Operations of the Notes for a discussion of Global’s

sale of Tanir Bavi located in India. | ||

For additional information on Global’s investments in generation and distribution facilities, see Item 2. Properties. Resources Resources invests

in energy-related financial transactions and manages a diversified portfolio

of assets, including leveraged leases, operating leases, leveraged buyout

funds, limited partnerships and marketable securities. Also, the Demand

Side Management (DSM) business previously managed by Energy Technologies

was transferred | ||

8 | ||

to Resources as of December 31, 2002. Since it was established in 1985, Resources has grown its portfolio to include more than 60 separate investments. Resources expects to curtail its investment activity in the near-term.

DSM revenues are earned principally from monthly payments received from utilities, which represent shared electricity savings from the installation of the energy efficient equipment. For further discussion of the transfer of DSM to Resources, see Note 22. Related-Party Transactions of the Notes.

The major components of Resources’ investment portfolio as a percent of its total assets as of December 31, 2002 were:

| As of December 31, 2002 | |||||

| Amount | %

of Resources’ Total Assets |

||||

| (Millions) | |||||

| Leveraged Leases | |||||

| Energy-Related | |||||

| Foreign | $ | 1,181 | 38 | % | |

| Domestic | 1,272 | 41 | % | ||

| Real Estate – Domestic | 192 | 6 | % | ||

| Aircraft | |||||

| Foreign | 44 | 2 | % | ||

| Domestic | 61 | 2 | % | ||

| Commuter Railcars – Foreign | 86 | 3 | % | ||

| Industrial – Domestic | 8 | — | |||

| |

|

||||

| Total Leveraged Leases, net | 2,844 | 92 | % | ||

| |

|

||||

| Limited Partnerships | |||||

| Leveraged Buyout Funds | 93 | 3 | % | ||

| Other | 25 | 1 | % | ||

| |

|

||||

| Total Limited Partnerships | 118 | 4 | % | ||

| |

|

||||

| Marketable Securities | 5 | — | |||

| Other Investments | 33 | 1 | % | ||

| Owned Property | 59 | 2 | % | ||

| Current and Other Assets | 27 | 1 | % | ||

| |

|

||||

| Total Resources’ Assets | $ | 3,086 | 100 | % | |

| |

|

||||

As of December 31, 2002, no single investment represented more than 7.5% of Resources’ total assets.

Leveraged Lease Investments

Resources seeks a portfolio that provides a fixed rate of return, predictable income and cash flow and depreciation and amortization deductions for federal income tax purposes. Income on leveraged leases is recognized by a method which produces a constant rate of return on the outstanding net investment in the lease, net of the related deferred tax liability, in the years in which the net investment is positive. Any gains or losses incurred as a result of a lease termination are recorded as revenues as these events occur in the ordinary course of business of managing the investment portfolio.

In a leveraged lease, the lessor acquires an asset by investing equity representing approximately 15% to 20% of the cost and incurring non-recourse lease debt for the balance. The lessor acquires economic and tax ownership of the asset and then leases it to the lessee for a period of time no greater than 80% of its remaining useful life. As the owner, the lessor is entitled to depreciate the asset under applicable federal and state tax guidelines. In addition, the lessor receives income from lease payments made by the lessee during the term of the lease and from tax receipts associated with interest and depreciation deductions with respect to the leased property. Lease rental payments are unconditional obligations of the lessee and are set at levels at least sufficient to service the non-recourse lease debt. The lessor is also entitled to any residual value associated with the leased asset at the end of the

9

lease term. An evaluation of the after-tax cash flows to the lessor determines the return on the investment. Under generally accepted accounting principles, the lease investment is recorded on a net basis and income is recognized as a constant return on the net unrecovered investment.

Resources evaluates lease investment opportunities with respect to specific risk factors. Any future leveraged lease investments are expected to be made in energy-related assets. For further information relating to the curtailment of Energy Holdings’ investments in the near term, see Item 7. MD&A – Overview. The assumed residual value risk, if any, is analyzed and verified by third-parties at the time the investment is made. Credit risk is assessed and, if necessary, mitigated or eliminated through various structuring techniques, such as defeasance mechanisms and letters of credit. Resources does not take currency risk in its cross-border lease investments. Transactions are structured with rental payments denominated and payable in US Dollars. Resources, as a passive lessor or investor, does not take operating risk with respect to the assets it owns, so leases are structured with the lessee having an absolute obligation to make rental payments whether or not the assets operate. The assets subject to lease are an integral element in Resources’ overall security and collateral position. If such assets were to be impaired, the rate of return on a particular transaction could be affected. The operating characteristics and the business environment in which the assets operate are, therefore, important and must be understood and periodically evaluated. For this reason, Resources retains experts to conduct regular appraisals on the assets it owns and leases.

The ten largest lease investments for Resources as of December 31, 2002 were as follows:

| Investment | Description | Gross Investment Balances as of December 31, 2002 |

% of Resources’ Total Assets |

||||||||

|

|

|||||||||||

| (Millions) | |||||||||||

| Reliant | Three generating stations | $ | 221 | 7 | % | ||||||

| (Keystone, Conemaugh and | |||||||||||

| Shawville) | |||||||||||

| EME | Collins Electric Generation | 185 | 6 | % | |||||||

| Station | |||||||||||

| Seminole | Seminole Generation Station | 175 | 6 | % | |||||||

| Unit #2 | |||||||||||

| Dynegy | Two electric generating stations | 172 | 6 | % | |||||||

| EME | Two electric generating stations | 170 | 6 | % | |||||||

| (Powerton and Joliet) | |||||||||||

| ENECO | Gas distribution network | 141 | 5 | % | |||||||

| (Netherlands) | |||||||||||

| Grand Gulf | Nuclear generating station | 131 | 4 | % | |||||||

| Merrill Creek | Merrill Creek Reservoir Project | 129 | 4 | % | |||||||

| ESG | Electric distributing system | 108 | 3 | % | |||||||

| (Austria) | |||||||||||

| EZH | Electric generating station | 107 | 3 | % | |||||||

| (Netherlands) | |||||||||||

| $ | 1,539 | 50 | % | ||||||||

For further details on leases, see Item 7A. Qualitative and Quantitative Disclosures About Market Risk-Credit Risk-Energy Holdings.

Energy Technologies

Energy Technologies is an energy management company whose primary objective was to construct, operate and maintain heating, ventilating and air conditioning (HVAC) systems for and provide energy-related engineering, consulting and mechanical contracting services to industrial and commercial customers in the Northeastern and

10

Middle Atlantic United States. In June 2002, Energy Holdings adopted a plan to sell its interests in these HVAC/mechanical operating companies. The sale of these companies is expected to be completed by June 30, 2003. For more details, see Note 5. Discontinued Operations of the Notes and Item 7. MD&A — Results of Operations — Discontinued Operations — Energy Technologies.

Other Subsidiaries

Enterprise Group Development Corporation (EGDC), a commercial real estate property management business, has been conducting a controlled exit from the real estate business since 1993. EGDC’s strategy is to preserve the value of its assets to allow for the controlled disposition of its properties as favorable sales opportunities arise. EGDC directly owns a 100% interest in two parcels of land available for development located in New Jersey totaling $19 million. One of these parcels is classified as Assets Held for Sale. EGDC also owns an 80% general partnership interest in four partnerships which own and operate two buildings and land in New Jersey totaling $15 million. EGDC also owns a 100% interest in development land located in Maryland valued at $12 million. Together, the 100% wholly-owned land and the 80% general partnership interests represent 72% of the total assets of EGDC. Additionally, EGDC owns a 50% partnership interest in development land located in Virginia. Total assets of EGDC as of December 31, 2002 and 2001 were $63 million and $65 million, respectively.

PSEG Capital Corporation (PSEG Capital) has served as the financing vehicle, borrowing on the basis of a minimum net worth maintenance agreement with PSEG. As of December 31, 2002 PSEG Capital had debt outstanding of $252 million, which matures in May 2003, at which time the program will be terminated. For additional information including certain restrictions relating to the BPU Focused Audit, see Item 7. MD&A — Liquidity and Capital Resources.

Services

Services is a New Jersey Corporation with its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102. Services provides management and administrative services to PSEG and its subsidiaries. These include accounting, legal, communications, human resources, information technology, treasury and financial, investor relations, stockholder services, real estate, insurance, risk management, tax, library and information services, security, corporate secretarial and certain planning, budgeting and forecasting services. Services charges PSEG, PSE&G, Power and Energy Holdings a fair market rate for services provided.

COMPETITIVE ENVIRONMENT

PSE&G

As a regulated monopoly, PSE&G’s electric and gas transmission and distribution business has minimal risks from competition. Also, there has been minimal financial impact on PSE&G’s transmission and distribution business due to customers choosing alternate electric or gas suppliers.

Power

Power primarily contracts to provide energy to the direct suppliers of New Jersey electric utilities. In recent years Power has expanded into other areas of its target market, the Super Region, with acquisitions in New York and Connecticut and development in the Midwest. As markets continue to evolve, several types of competitors have or will emerge in Power’s target market. These competitors include merchant generators with or without trading capabilities, other utilities that have formed generation and/or trading affiliates, aggregators, wholesale power marketers or combinations thereof. These participants will compete with Power and one another buying and selling in wholesale power pools, entering into bilateral contracts and/or selling to aggregated retail customers. These participants can also be expected to adapt to changing market conditions, including developing new generating stations where a perceived capacity shortfall may exist. Power believes that its asset size and location, regional market knowledge and integrated functions will allow it to compete effectively in its selected markets. However, actions by developers, including Power, to build new generating stations has lead to an overbuild situation, causing energy and capacity prices to be depressed and possibly making some of its units uneconomical. The Midwest

11

market is expected to have excess capacity due to recent additions, which will negatively impact the expected returns of Power’s Lawrenceburg, Indiana and Waterford, Ohio facilities, presently under construction.

Additional legislation has been introduced within the last few years to further encourage competition at the retail level (often referred to as customer choice or retail access). No legislative proposal exists at the federal level. However, there is also a risk of re-regulation, if states decide to turn away from deregulation and allow regulated utilities to continue to own or reacquire and operate generating stations in a regulated and potentially uneconomical manner.

Power’s businesses are also under competitive pressure due to technological advances in the power industry and increased efficiency in certain energy markets. It is possible that advances in technology will reduce the cost of alternative methods of producing electricity to a level that is competitive with that of most central station electric production.

Energy Holdings

Energy Holdings and its subsidiaries are subject to substantial competition in the US as well as in the international markets from independent power producers, domestic and multi-national utility generators, fuel supply companies, energy marketers, engineering companies, equipment manufacturers, well capitalized investment and finance companies and affiliates of other industrial companies. Energy Holdings faces competition from companies of all sizes, having varying levels of experience, financial and human capital and differing strategies. Competition can be based on a number of factors, including price, reliability of service, the ability of Energy Holdings’ customers to utilize other sources of energy and credit quality of lease investments and partners.

Many states and countries are considering or implementing different types of regulatory and privatization initiatives that are aimed specifically at increasing competition in the power industry. The increased competition that has resulted from some of these initiatives, combined with certain overbuild situations, has contributed to a reduction in electricity prices in some markets, and puts pressure on Energy Holdings and other electric utilities to lower costs. Achieving and maintaining a lower cost of production will be increasingly important to compete effectively in the energy business. In the Texas market, excess capacity has led to uneconomical energy pricing, negatively effecting two generating stations in Texas. For additional information regarding the Texas power market, see Item 7. MD&A — Future Outlook.

Energy Holdings’ businesses are also under competitive pressure due to technological advances in the power industry and increased efficiency in certain energy markets. It is possible that advances in technology will reduce the cost of alternative methods of producing electricity to a level that is competitive with that of most central station electric production.

REGULATORY ISSUES

State Regulation

PSEG, PSE&G, Power and Energy Holdings

Focused Audit

In 1992, the BPU conducted a Focused Audit of the impact of PSEG’s non-utility businesses, owned by Energy Holdings, on PSE&G. Among other things, the BPU ordered that PSEG not permit Energy Holdings’ investments to exceed 20% of PSEG’s consolidated assets without prior notice to the BPU. In the Final Order issued in 1999, the BPU noted that, due to significant changes in the industry and, in particular PSEG’s corporate structure as a result of the Final Order, modifications to or relief from the BPU’s Focused Audit order might be warranted. PSE&G has notified the BPU that PSEG will eliminate PSEG Capital debt by the end of the second quarter of 2003 and that it believes that the Final Order otherwise supercedes the requirements of the Focused Audit. While, PSE&G and Energy Holdings believe that this issue will be satisfactorily resolved, no assurances can be given.

Affiliate Standards

In February 2000, the BPU approved affiliate standards and fair competition standards which apply to transactions between a public utility and those of its affiliates that provide competitive services to retail customers in New Jersey. In March 2000, the BPU issued a written order related to these matters. PSE&G filed a compliance plan in June 2000 to describe the internal policy and procedures necessary to ensure compliance with such Affiliate Standards. On February 8, 2002 and March 7, 2002, the BPU issued orders adopting the Competitive Service Audit reports on New Jersey’s electric and gas utilities. The audit report generally concluded that PSE&G was in compliance with the BPU’s affiliate standards. On July 1, 2002, PSE&G filed its Affiliate Standards compliance plan in accord with the BPU’s regulations. Also in July 2002, the BPU commenced its next regular audit of the state’s electric and gas utilities’ competitive activities. The objectives of these audits are to assure that neither the utilities nor their related competitive business segments enjoy an unfair competitive advantage over their competitors and to assure that there is no form of cross-subsidization of competitive services by utility operations or affiliates with which they are associated. The audits will be guided by the BPU’s Affiliate Standards requirements. A report is expected to be issued in the first quarter of 2003. The outcome cannot be determined at this time.

PSEG, Power and Energy Holdings

PSEG, Power and Energy Holdings’ affiliates are not subject to direct regulation by the BPU, except potentially with respect to certain asset sales, transfers of control, reporting requirements and affiliate standards.

PSE&G

As a New Jersey public utility, PSE&G is subject to comprehensive regulation by the BPU including, among other matters, regulation of intrastate rates and service and the issuance and sale of securities. As a participant in the ownership of certain transmission facilities in Pennsylvania, PSE&G is subject to regulation by the Pennsylvania Public Utility Commission (PPUC) in limited respects in regard to such facilities.

Electric Base Rate Case

On May 24, 2002, PSE&G filed an electric rate case with the BPU requesting an annual $250 million rate increase for its electric distribution business. The proposed rate increase includes $187 million of increased revenues relating to a $1.7 billion increase in PSE&G’s rate base, which is primarily due to the investment that PSE&G has made in its electric distribution facilities since its last rate case in 1992; $18 million in higher depreciation rates and $45 million to recover various other expenses, such as wages, fringe benefits and enhancements to security and reliability. The requested increase proposes a return on equity of 11.75% for PSE&G’s electric distribution business.

12

The proposed rate increase would significantly impact PSE&G’s earnings and operating cash flows. The non-depreciation portion of the noticed rate increase ($232 million) would have a positive effect on PSE&G’s earnings and operating cash flows. The depreciation portion of the rate increase ($18 million) would have no impact on PSE&G’s earnings, as the increased operating cash flows would be offset by higher depreciation charges.

In October 2002, the New Jersey Ratepayer Advocate and other parties filed testimony, with the Ratepayer Advocate recommending rate relief of approximately $87 million. Included in the Ratepayer Advocate’s position is a 9.50% return on equity compared to PSE&G’s requested 11.75% (approximately $45 million), a reduction in electric distribution depreciation expenses (approximately $100 million), and numerous other adjustments to PSE&G’s filing. The BPU has consolidated PSE&G’s service company filing relating to the transfer of certain assets from PSE&G to Services and its Street Lighting Tariff filing, which adjusts tariff levels for electricity for certain street lights, into the base rate proceeding for disposition.

In accordance with BPU’s Final Order implementing parts of the Energy Competition Act, PSE&G was required to provide temporary billing discounts in four steps totaling 13.9% during the four-year transition period ending July 31, 2003. The last step, a 4.9% decrease, took effect August 1, 2002. The combined effects of base rate relief, the BGS auction and amortization of various deferral balances, discussed below, is expected to yield rates comparable to those in effect at the beginning of the deregulation process. Neither PSEG nor PSE&G can predict the outcome of these rate proceedings at the current time. Discussions are continuing and hearings were held with an initial decision scheduled to be issued by May 1, 2003. The new rates are proposed to be effective August 1, 2003, consistent with the Final Order.

Non-Utility Generation (NUG) Contract Amendments

In June 2002, PSE&G announced that it had amended its NUG power purchase agreements with El Paso Corporation (El Paso) for its Camden, Bayonne and Eagle Point cogeneration facilities. El Paso paid PSE&G $167 million for the amendment and agreed to provide specified amounts of electric energy and capacity to PSE&G at a fixed price and obtain this energy and capacity either from existing plants or in the open market. The amended agreement has been approved by the BPU.

Deferral Proceeding

In August 2002, PSE&G filed a petition proposing changes to two components of its rates, the Societal Benefits Clause (SBC) and the Non-Utility Generation Transition Charge (NTC). The proposed result, if adopted, will result in an annual reduction of revenues of approximately $122 million or approximately a 3.4% reduction in amounts paid by customers effective on August 1, 2003. The case has been transferred to the Office of Administrative Law and a pre-hearing conference was held October 24, 2002. PSE&G cannot predict the outcome of this matter.

Deferral Audit

In September 2002, the BPU retained the services of two outside firms to conduct a review of New Jersey’s electric utilities’ deferred costs for compliance with BPU mandates. Audit work has been completed and a final draft report was filed with the BPU on December 16, 2002, with PSEG responding on December 30, 2002. Formal comments on the final report are to be incorporated in the Deferral Proceedings, discussed above.

PSE&G believes that the final report will support its current practices and not impact its financial position or results of operations.

13

Gas Base Rate Case and Commodity Charges

In January 2002, the BPU issued an order approving a settlement of PSE&G’s Gas Base Rate case under which PSE&G is receiving an additional $90 million of gas base rate revenues, approximately $8 million of which results from gas depreciation rate changes. This occurred simultaneously with PSE&G’s implementation of its previously approved Gas Cost Underrecovery Adjustment (GCUA) surcharge to recover the October 31, 2001 gas cost underrecovery balance of approximately $130 million over a three-year period with interest and with PSE&G’s reduction of its 2001-2003 Commodity Charges (formerly LGAC) by approximately $140 million. As a result of the settlement, PSE&G agreed not to request another gas base rate increase that would take effect prior to September 1, 2004.

The $130 million rate increase relating to the recovery of the GCUA over three years has no impact on earnings, however it will increase operating cash flows in a normal business environment. The reduction in PSE&G’s 2001–2003 commodity charges relates to its residential customers and will have no impact on earnings and will decrease operating cash flows assuming current cost levels and a normal business environment.

BGSS Filing

In September 2002, PSE&G filed to increase its Residential BGSS Commodity Charge on November 1, 2002 to recover approximately $89 million in additional revenues ($82 million of which is associated with an underrecovered balance) or a 7.4% rate increase for the typical residential gas heating customer. On January 8, 2003, the BPU approved the increase on a provisional basis, to be effective immediately and the case has been transferred to the Office of Administrative Law for hearings.

BGSS Design

On December 18, 2002, the BPU approved BGSS Commodity filing procedure changes based upon the form of generic settlement negotiated by the parties. An annual filing will be made each year by June 1 for rate relief expected by October 1. That rate relief may be supplemented by two potential self-implementing rate increases to the maximum of 5% of the residential customer’s bill on December 1st and February 1st. All increases will be reconciled in the annual filing. As a result of the delay in the implementation of the BGSS increase discussed above, PSE&G has filed for a 5% self-implementing rate increase to be effective on March 1, 2003 which would reduce the expected underrecovery from $61 million to $37 million. PSE&G cannot predict the outcome of this matter.

Federal Regulation

PSEG, PSE&G, Power and Energy Holdings

Public Utility Holding Company Act of 1935 (PUHCA)

PSEG has claimed an exemption from regulation by the Securities and Exchange Commission (SEC) as a registered holding company under the PUHCA, except for Section 9(a)(2), which relates to the acquisition of 5% or more of the voting securities of an electric or gas utility company. Fossil and Nuclear are (EWGs) and Global’s

14

investments include EWGs and foreign utility companies (FUCOs) under PUHCA. Failure to maintain status of these plants as EWGs or FUCOs could subject PSEG and its subsidiaries to regulation by the SEC under PUHCA.

If PSEG were no longer exempt under PUHCA, PSEG and its subsidiaries would be subject to additional regulation by the SEC with respect to their financing and investing activities, including the amount and type of non-utility investments. PSEG does not believe, however, that this would have a material adverse effect on it and its subsidiaries.

Other

PSE&G’s, Power’s and Energy Holdings’ domestic operations are subject to regulation by FERC with respect to certain matters, including interstate sales and exchanges of electric transmission, capacity and energy. PSE&G, Fossil, Nuclear and Global are also subject to the rules and regulations of the US Environmental Protection Agency (EPA), the US Department of Transportation (DOT) and the US Department of Energy (DOE). For information on environmental regulation, see Environmental Matters.

FERC

Regional Transmission Organization (RTO) Orders

In July 2002, the United States Court of Appeals, D.C. Circuit, issued an opinion in favor of PSE&G and certain other utility petitioners, reversing a previous order of the FERC relating to the restructuring of PJM into an Independent System Operator (ISO). The court ruled that FERC lacked authority to require the utility owners to give up certain statutory rights and should not have required a modification to the PJM ISO Agreement eliminating utility owners rights to file changes to rate design. The Court further noted that FERC lacked authority to require the utility owners to obtain approval of their withdrawal from the PJM ISO, finding that FERC had no jurisdiction to eliminate the withdrawal rights to which the utilities had agreed. Further, in ruling on a specific argument raised by PSE&G, the Court held that PSE&G did not have to modify a contract with Old Dominion Electric Cooperative to accommodate the PJM restructuring. See Note 13. Commitments and Contingent Liabilities of the Notes for additional information.

On remand, in December 2002, FERC refused to disclaim jurisdiction over a transmission owner’s withdrawal from an ISO. In January 2003, PSE&G together with several of the transmission owners filed for rehearing of the FERC decision. The potential outcome of this rehearing could have implications for FERC’s jurisdiction and authority to implement its standard market design, discussed below.

In January 2002, PJM and the Midwest ISO (MISO) announced that it had entered into negotiations to create a virtual uniform seamless market encompassing these two RTOs, shortly after the FERC granted RTO status to the MISO. PSE&G also is participating in a rate investigation by FERC into whether the “regional through-and-out rates” between MISO and PJM should be eliminated. The proceeding could result in lower rates paid by transmission customers. The impact of these developments on PSE&G, Power and Energy Holdings is uncertain because specific rules will not be known for some time and are subject to FERC approval, which cannot be assured.

In April 2002, PJM successfully implemented its “PJM West” expansion. Also, in December 2002, several major utilities in the Midwest and mid-atlantic area petitioned FERC to become transmission owners within PJM. Implementation of this filing would more than double the size of the current PJM region and would result in a market encompassing more than 153,000 MW of generation capacity and more than 128,000 MW of peak load. Portions of this expansion could become effective as early as Spring 2003 although a date for implementation cannot be determined with certainty even if the filing is accepted by FERC.

In December 2002, FERC granted full RTO status to PJM.

Standard Market Design

In July 2002, FERC issued a Notice of Proposed Rulemaking (NOPR) to create a Standard Market Design for the wholesale electricity markets in the United States. The NOPR seeks to improve the consistency of market rules

15

throughout the country, including issues related to reliability, market power concerns, transmission, pricing, congestion, governance and other issues. If adopted, standard market design could significantly affect transmission and generation operations in the various markets in which PSE&G, Power and Energy Holdings operate.

Other

FERC issued an advance NOPR seeking comments to help form the basis for a proposed rule to standardize power-plant interconnection requirements to ease market entry for new generation facilities. As part of the rulemaking, FERC also will reconsider its policy addressing how transmission owners treat the cost of system upgrades necessary to accommodate new generation, potentially resulting in a new methodology. The ultimate outcome of this rulemaking and its impact upon PSEG, PSE&G, Power and Energy Holdings cannot be predicted.

PJM also filed an alternative proposal to standardize its generator interconnection agreement and procedures within PJM. FERC accepted this proposal, which is currently in effect in PJM.

In January 2003, FERC also proposed a new transmission pricing policy that would give rate incentives to engage in certain transactions, including transfer of control of transmission facilities to a FERC-approved RTO; and joining an RTO but maintaining independence from market participants. FERC also proposed to award an incentive for new transmission facilities that are found appropriate pursuant to an RTO transmission planning process. The ultimate outcome of this proposal and its impact upon PSEG, PSE&G, Power and Energy Holdings cannot be predicted.

Power

Nuclear Regulatory Commission (NRC)

Operation of nuclear generating units involves continuous close regulation by the NRC. Such regulation involves testing, evaluation and modification of all aspects of plant operation in light of NRC safety and environmental requirements. Continuous demonstrations to the NRC that plant operations meet requirements are also necessary. The NRC has the ultimate authority to determine whether any nuclear generating unit may operate.

The NRC has issued orders to all nuclear power plants to implement compensatory security measures. Some of the requirements formalize a series of security measures that licensees had taken in response to advisories issued by the NRC in the aftermath of the September 11, 2001 terrorist attacks. Power has evaluated these orders for the Salem and Hope Creek facilities and does not expect the cost of implementation of the NRC measures to be material.

In accordance with NRC requirements, nuclear plants utilize various fire barrier systems to protect equipment necessary for the safe shutdown of the plant in the event of a fire. The NRC has identified certain issues at Salem and Power has made the majority of the necessary modifications to comply with these requirements, the cost of which was approximately $26 million for Power. Minor completion activities remain, the costs of which are not expected to be material.

Exelon has informed Power that, on July 3, 2001, an application was submitted to the NRC to renew the operating licenses for Peach Bottom 2 and 3. If approved, the current licenses would be extended by 20 years, to 2033 and 2034 for Peach Bottom 2 and 3, respectively. NRC review of the application is expected to take approximately two years.

In August 2002, the NRC issued a bulletin requiring that all operators of pressurized water reactor (PWR) nuclear unit submit certain information related to potential degradation of reactor vessel heads. In September 2002, Power provided the requested information for Salem. The response stated that a bare metal visual examination will be performed on the Salem reactor vessel heads during each unit’s next refueling outage, in compliance with the bulletin. If repairs are determined to be necessary, it is estimated that the repair would extend the outage by approximately four weeks. Bare metal visual inspections for Salem 1 and 2 were completed during 2002 and no degradation of the reactor heads was observed. On February 11, 2003 the NRC issued an order to all operators of PWR units concerning reactor vessel head inspections. The order confirms the previous bulletin’s

16

requirements of more intrusive and frequent future inspections, which apply to Salem 1 and 2. Power’s Hope Creek nuclear unit and the Peach Bottom 2 and 3 are unaffected as they are Boiling Water Reactor nuclear units. Power cannot predict what other actions the NRC may take on this issue.

Foreign Regulation

Energy Holdings

Global

Global’s electric distribution facilities in Latin America are rate-regulated enterprises. Rates charged to customers are established by governmental authorities and, excluding those rates at facilities in Argentina, which were fully impaired during 2002, are currently sufficient to cover all operating costs and provide a fair return in local currency terms. Global can give no assurances that future rates will be established at levels sufficient to cover such costs, provide a return on its investments or generate adequate cash flow to pay principal and interest on its debt or to enable it to comply with the terms of its debt agreements.

Brazil

Rio Grande Energia S.A. (RGE) is regulated by Agencia Nacional de Energia Eletrica (ANEEL), the national regulatory authority. ANEEL’s functions include granting and supervising electric utility concessions, approving electricity tariffs, issuing regulations and auditing distribution systems’ performance. The rate setting process for Brazilian distribution companies has two components, an annual adjustment which RGE applies for every April and which is embedded in the concession contract, and a rate revision which will be calculated for RGE in 2003 and every subsequent fifth year anniversary.

The current regulatory regime adjusts consumer electric tariffs based on a multiple-factor formula that includes recovery of wholesale inflation for previous periods, as well as an additional entitlement to pass through deferred US Dollar costs. This current regulatory structure would result in an increase of approximately 40% in the tariffs RGE would charge its customers starting in April 2003. ANEEL has issued a resolution indicating that new distribution tariffs will be calculated based on the replacement value of the electric utility companies’ assets, but has not yet determined the rate of return to be allowed on this asset base. In addition, current electric regulation also allows ANEEL to apply an additional upward or downward adjustment (known as the “X Factor”) to final tariff determinations in order to adjust expected financial returns on the replacement values of utility companies’ assets. The combination of these factors results in considerable uncertainty regarding future revenue and cash flow levels associated with Global’s investment in RGE. No assurances can be given that 2003 tariff increases will be approved on a timely basis or at a sufficient level to support planned levels of revenues and cash flows. For additional information, see Item 7. MD&A — Future Outlook.

ANEEL also monitors service quality by auditing the duration and frequency of outages, as well as several other performance measures. Global is implementing capital improvement budgets which attempt to meet the quality of service standards. Failure to meet required standards would result in penalties which, if assessed, would not be expected to have a material negative impact on RGE’s results of operations, although no assurances can be given.

RGE is currently engaged in a dispute with ANEEL which is seeking to mandate a reduction in RGE’s fixed asset base due to a pre-privatization review of Companhia Estadual de Energia’s (CEEE) asset base. This pre-privatization review was not brought to the attention of the bidders during the RGE privatization process. The result of such a decrease in RGE’s fixed asset base would be a likely reduction in RGE’s tariff of approximately $8 million during the next rate case as RGE’s return on fixed assets would be above the accepted level. RGE is currently contesting the matter.

17

Chile

Distribution companies in Chile, including Chilquinta Energia S.A. (Chilquinta) and Sociedad Austral de Electricidad S.A. (SAESA), are subject to rate regulation by the Comision Nacional de Energia (CNE), a national governmental regulatory authority. The Chilean regulatory framework has been in existence since 1982, with rates set every four years based on a model company. The tariff which distribution companies charge to regulated customers consists of two components: the actual cost of energy purchased plus an additional amount to compensate for the value added in distribution (DVA tariff). The DVA tariff considers allowed losses incurred in the distribution of electricity, administrative costs of providing service to customers, costs of maintaining and operating the distribution systems and an annual real return on investment of 6% to 14%, based on the replacement cost of distribution assets. Changes in electricity distribution companies’ cost of energy are passed through to customers, with no impact on the distributors’ margins (equal to the DVA tariff). Therefore, distributors, including SAESA and Chilquinta, are not affected by changes in the generation sector which affect prices.