UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER

REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-04973 | |

| Exact name of registrant as specified in charter: | Voyageur Insured Funds | |

| Address of principal executive offices: | 2005 Market Street | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | David F. Connor, Esq. | |

| 2005 Market Street | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | (800) 523-1918 | |

| Date of fiscal year end: | August 31 | |

| Date of reporting period: | August 31, 2013 |

Item 1. Reports to Stockholders

|

Annual report

Delaware

Tax-Free Arizona Fund

Delaware Tax-Free California Fund Delaware Tax-Free Colorado Fund Delaware Tax-Free Idaho Fund Delaware Tax-Free New York Fund August

31, 2013

Fixed income mutual funds |

|

Carefully consider the Funds’

investment objectives, risk factors, charges, and expenses before

investing. This and other information can be found in the Funds’

prospectuses and, if available, their summary prospectuses, which may be

obtained by visiting delawareinvestments.com or calling 800 523-1918.

Investors should read the prospectus and, if available, the summary

prospectus carefully before investing. |

|

You can obtain shareholder

reports and prospectuses online instead of in the mail. Visit delawareinvestments.com/edelivery. |

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Tax-Free Arizona Fund, Delaware Tax-Free California Fund, Delaware Tax-Free Colorado Fund, Delaware Tax-Free Idaho Fund, and Delaware Tax-Free New York Fund at delawareinvestments.com.

- 24-hour access to your account information

- Obtain share prices

- Check your account balance and recent transactions

- Request statements or literature

- Make purchases and redemptions

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services.

Investments in Delaware Tax-Free Arizona Fund, Delaware Tax-Free California Fund, Delaware Tax-Free Colorado Fund, Delaware Tax-Free Idaho Fund, and Delaware Tax-Free New York Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

| Table of contents | ||

| Portfolio management review | 1 | |

| Performance summaries | 7 | |

| Disclosure of Fund expenses | 22 | |

| Security type/sector allocations | 25 | |

| Schedules of investments | 30 | |

| Statements of assets and liabilities | 68 | |

| Statements of operations | 72 | |

| Statements of changes in net assets | 74 | |

| Financial highlights | 84 | |

| Notes to financial statements | 114 | |

| Report of independent registered | ||

| public accounting firm | 128 | |

| Other Fund information | 129 | |

| Board of trustees/directors and | ||

| officers addendum | 136 | |

| About the organization | 144 |

Unless otherwise noted, views expressed herein are current as of Aug. 31, 2013, and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Funds’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2013 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

| Portfolio management review | |

| Delaware Investments® state tax-free funds | September 10, 2013 |

| Performance preview (for the year ended August 31, 2013) | |||||

| Delaware Tax-Free Arizona Fund (Class A shares) | 1-year return | -6.62 | % | ||

| Barclays Municipal Bond Index (benchmark) | 1-year return | -3.70 | % | ||

| Lipper Arizona Municipal Debt Funds Average | 1-year return | -5.84 | % | ||

For complete, annualized performance for Delaware Tax-Free Arizona Fund, please see the table on page 7.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

The Lipper Arizona Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Arizona (double tax-exempt) or a city in Arizona (triple tax-exempt).

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

| Delaware Tax-Free California Fund (Class A shares) | 1-year return | -5.63 | % | ||

| Barclays Municipal Bond Index (benchmark) | 1-year return | -3.70 | % | ||

| Lipper California Municipal Debt Funds Average | 1-year return | -4.68 | % |

For complete, annualized performance for Delaware Tax-Free California Fund, please see the table on page 10.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

The Lipper California Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in California (double tax-exempt) or a city in California (triple tax-exempt).

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

| Delaware Tax-Free Colorado Fund (Class A shares) | 1-year return | -6.56 | % | ||

| Barclays Municipal Bond Index (benchmark) | 1-year return | -3.70 | % | ||

| Lipper Colorado Municipal Debt Funds Average | 1-year return | -4.78 | % |

For complete, annualized performance for Delaware Tax-Free Colorado Fund, please see the table on page 13.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

The Lipper Colorado Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Colorado (double tax-exempt) or a city in Colorado (triple tax-exempt).

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

1

Portfolio management

review

Delaware

Investments® state tax-free funds

| Delaware Tax-Free Idaho Fund (Class A shares) | 1-year return | -6.99 | % | ||

| Barclays Municipal Bond Index (benchmark) | 1-year return | -3.70 | % | ||

| Lipper Other States Municipal Debt Funds Average | 1-year return | -6.01 | % |

For complete, annualized performance for Delaware Tax-Free Idaho Fund, please see the table on page 16.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

The Lipper Other States Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation on a specified city or state basis.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

| Delaware Tax-Free New York Fund (Class A shares) | 1-year return | -6.27 | % | ||

| Barclays Municipal Bond Index (benchmark) | 1-year return | -3.70 | % | ||

| Lipper New York Municipal Debt Funds Average | 1-year return | -6.11 | % |

For complete, annualized performance for Delaware Tax-Free New York Fund, please see the table on page 19.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

The Lipper New York Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in New York (double tax-exempt) or a city in New York (triple tax-exempt).

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Economic backdrop

U.S. economic growth continued its uneven, but slow upward trend throughout the Funds’ fiscal year ended Aug. 31, 2013.

It was a similar story with the employment picture, as the jobless rate continued to tick downward, yet remained high at 7.3% in August 2013. Weaker-than-desired jobs data and a benign inflation outlook led to the U.S. Federal Reserve keeping its target short-term interest rate close to zero, where it has been hovering for close to five years.

The Fed also continued to buy $85 billion worth of bonds a month, with the aim of lowering long-term interest rates and stimulating the economy.

Despite discussion among Fed officials about “tapering” the bond purchases this year, this program remained in place throughout the fiscal period.

Municipal bond market conditions

The municipal bond market posted reasonably even performance for the majority of the Funds’ fiscal year. However, bond prices began to decline between June and August, in conjunction with investors’ concerns as interest rates rose over the summer. Despite its earlier gains, the municipal bond market (as measured by the Barclays Municipal Bond Index) lost approximately 3.7% for the Funds’ full fiscal year.

The rise in interest rates was one of two main factors affecting the performance of the municipal bond market during the Funds’ fiscal year. The second involved two well-publicized credit events. In July, the city of Detroit filed for Chapter 9 bankruptcy protection, while in December 2012, credit rating agency Moody’s Investors Service (Moody’s) downgraded the

2

general obligation bonds of Puerto Rico from Baa1 to Baa3, the lowest tier of the investment grade bond universe.

The impact of this latter event on the municipal bond market was especially significant, as Puerto Rico securities are widely held by U.S. municipal bond portfolio managers (Puerto Rico bonds, like those of all U.S. territories, are generally exempt from income taxes in all 50 states). Investors feared an additional downgrade would precipitate substantial selling on the part of the many fund managers who face limitations on the amount of noninvestment grade debt that can be held in their portfolios. Consequently, Puerto Rico securities underperformed dramatically.

For the full fiscal year, securities with longer maturities and lower credit ratings significantly lagged their shorter-dated, higher-rated counterparts — the reverse of conditions seen in recent years — as investors proved less willing to take on either credit risk or interest rate risk.

In our view, the fundamental backdrop for municipal securities remained positive during the year, despite the overall price declines of the asset class. Although declining demand for municipal securities put downward pressure on prices, weaker-than-anticipated supply of new municipal debt counterbalanced these challenging performance factors.

Economic backdrop in the states

Economic characteristics across each state, briefly noted:

Arizona’s diverse economy is still slowly recovering from the global financial crisis. In July 2013, nonfarm employment was up 3% from a year earlier. While there has been some improvement in the economy, the unemployment rate remained elevated at 8% as of July 2013, well above the national rate. Arizona’s personal income per capita is below the national level.

The governor signed the 2014 $8.8 billion General Fund budget into law on June 17, 2013. This represents a 3.4% increase from fiscal 2013. Base revenues are projected to increase by 4.9%. However, one-time factors, including the expiration of the temporary $0.01 sales tax, would reduce 2014 collections by $253 million compared to fiscal 2013. This would result in an ending balance of $298 million and a Budget Stabilization Fund of $450 million. (Data: bls.gov; Moody’s; Arizona Joint Legislative Budget Committee.)

California enjoys a large, diverse, and wealthy economy that mirrors that of the nation. The gross state product is $1.8 trillion, which amounts to 13% of U.S. gross domestic product. In July 2013, nonfarm employment was up 1.6% from a year earlier, and the state’s unemployment rate improved to 8.7% from 10.7% a year earlier. Per-capita economic measures remain strong, with gross state product and personal income at 112% and 107% of the nation, respectively.

State revenues for fiscal 2013 came in 2% above budget and 19.9% above the prior year (in part due to temporary tax increases). Through the first two months of fiscal 2014, General Fund revenues were 2.7% below estimates but 7.4% above the prior year. The governor signed a $96.3 billion 2014 General Fund budget that provided for a $1.1 billion reserve. The budget found room for additional spending on education, social services, and healthcare. The budget overhauls the state’s K–12 system by

3

Portfolio management

review

Delaware

Investments® state tax-free funds

committing new funding to low-income districts and districts that primarily serve English-language learners. It also expands Medicaid to 1.4 million low-income residents.

Estimates suggest that the state’s wall of debt may be reduced to less than $27 billion at the end of fiscal 2013 and to less than $5 billion by the end of fiscal 2017. (Data: bls.gov; California State Controller’s Office; Moody’s.)

Colorado’s economy is diverse, with below-average employment concentration in manufacturing and a variety of service-sector strengths. In July 2013, nonfarm employment was up 2.7% from a year earlier, and Colorado’s unemployment rate was at 7.1%, slightly lower than the national rate of 7.4%.

Colorado is a wealthy state, with per-capita income equal to 110% of the U.S. average. Preliminary revenues for fiscal 2013 show 10.9% growth over fiscal 2012 and 5.8% growth over the March forecast. These revenues will permit the funding of a 5% statutory reserve and the funding of a $1.1 billion transfer to the State Education Fund.

The governor signed an $8 billion 2014 General Fund budget into law in April 2013. This represents a 6.8% increase over fiscal 2013. The budget projects that General Fund revenue will be $181.4 million greater than the required reserve at the end of fiscal 2014. (Data: bls.gov; Colorado Office of State Planning and Budgeting; Moody’s.)

Idaho’s economy has expanded and diversified in recent years, benefiting from population growth. However, an above-average dependence on the natural resource sector remains. In July 2013, nonfarm employment was up 2.7% from a year earlier, and the unemployment rate was low at 6.6%, down from 7.5% in July 2012. Idaho’s fiscal 2013 revenues came in 3.5% above budget and 6.3% above the prior year.

The state passed its $2.8 billion 2014 General Fund budget, a 2.9% increase over fiscal 2013’s budget. It included a 2% increase in education spending and a personal property tax relief package exempting the first $100,000 valuation of personal property taxes. (Data: bls.gov; Idaho Division of Management; State Controller’s website. Note that budget figures do not include expansion of Medicaid eligibility.)

New York has a mature, broad-based, wealthy economy that attracts a highly educated and global workforce. In July 2013, nonfarm employment was up 0.9% from a year earlier, and the unemployment rate was at 7.5%, slightly above the national rate.

State tax collections totaled $66.3 billion in fiscal 2013, 3.1% higher than fiscal 2012. This was just above February estimates but still below initial estimates due to unexpected costs from Hurricane Sandy. The state ended fiscal 2013 with a General Fund balance of $1.61 billion, 9.9% less than the prior year but still 9.2% more than the last financial projection. This includes a $1.4 billion combined balance in the Tax Stabilization Reserve Fund and Rainy Day Fund.

Lawmakers signed off on a $135.1 billion All Funds Fiscal 2014 budget that closed a $1.3 billion gap with no new taxes or fees and actually cut taxes for businesses. Through the first four months of fiscal 2014, state tax collections were 13.3% higher than fiscal 2013 due to stronger personal income tax collections in April. (Data: bls.gov; New York Division of Budget; Moody’s; Office of the New York State Comptroller.)

4

Sticking to our strategy

Amid volatile market conditions, we kept our management strategy consistent. Our approach is known as a “bottom-up” way of investing, which means we consider securities one at a time, each on its individual merits. We conduct exhaustive research and choose the combination of bonds we believe offer a favorable risk-reward trade-off for the Funds’ shareholders.

Based on our confidence in our credit research, we maintained an emphasis on bonds with credit ratings of A and BBB, representing the mid-to-lower tier of the investment grade bond universe. We believe this segment of the marketplace may potentially provide better long-term value for diligent investors who are able to conduct the necessary research.

We also paid close attention to shifts in the market landscape, making subtle adjustments to the composition of the Funds’ portfolios that resulted in a somewhat more conservative position over time.

For example, roughly midway through the Funds’ fiscal year we believed it was prudent to protect the portfolios from a potential rise in long-term interest rates. This entailed modestly reducing the Funds’ exposure to longer-maturity securities. These shifts represented only subtle changes to the Funds’ portfolios.

Within the Funds

Some of the most notable detractors from the Funds’ performance were issued by Puerto Rico. Because Puerto Rico bonds generally provide investors with the same income-tax benefits as in-state municipal debt, these securities are often employed by state-specific portfolio managers to add diversification or to keep a fund 100% invested.

Delaware Tax-Free Arizona Fund, Delaware Tax-Free California Fund, Delaware Tax-Free Colorado Fund, and Delaware Tax-Free Idaho Fund each saw disappointing performance from their holdings in various Puerto Rico bonds, whose returns ranged from approximately -19% to -39% during the Funds’ fiscal year. Other Puerto Rico positions greatly hampered results as well. In Delaware Tax-Free Colorado Fund, Delaware Tax-Free Idaho Fund, and Delaware Tax-Free New York Fund, holdings in Puerto Rico Electric Power Authority (PREPA) bonds were significant underperformers, whose returns ranged from -24% to -38%. PREPA securities had lower-investment-grade credit ratings and suffered from investors’ worries concerning Puerto Rico.

Within Delaware Tax-Free Arizona Fund and Delaware Tax-Free California Fund, the laggard Puerto Rico bonds were issued by Puerto Rico Sales Tax Financing Corporation.

On the positive side of the ledger, all of the Funds’ top-performing bonds were issued within their respective states:

- Within Delaware Tax-Free Arizona Fund,

the strongest-performing securities were Maricopa County industrial development bonds issued to raise funds for the Phoenix West Prison; these bonds advanced by 5% during the fiscal year. Similarly, bonds for Aspen Place at the

Sawmill Improvement District in Flagstaff also

delivered a total return of approximately

5%.

5

Portfolio management

review

Delaware

Investments® state tax-free funds

- Within Delaware Tax-Free California Fund, San Diego Redevelopment Agency bonds for the Centre City Redevelopment Project, rated BBB by Standard & Poor’s (S&P), returned approximately 6% for the period. Multifamily housing bonds issued by the Santa Clara Housing Authority for the RiverTown Apartments project, rated A3 by Moody’s, posted a total return of approximately 5.5%.

- Within Delaware Tax-Free Colorado Fund, stronger performers included bonds issued by the Baptist Road Rural

Transportation Authority to fund road

improvements. These nonrated bonds, with a 2026

maturity date, rose approximately 13% during

the fiscal period. To a lesser extent, the Fund

also benefited from AAA/Aaa-rated

Colorado Housing and Finance Authority

bonds, reflecting the favorable market

backdrop for higher-rated

issues.

- Within Delaware Tax-Free Idaho Fund, strong performers included bonds issued by the Industrial Development Corporation of Power County. These BBB+/Baa1-rated issues, which were issued with a coupon of 6.45% and will

mature in 2032, gained 6% during the Fund’s

fiscal year, a rate of return that was matched

by the Fund’s next-strongest performer, a

local improvement bond issued by the city of

Coeur d’Alene.

- Within Delaware Tax-Free New York Fund, nonrated New York City corporate-backed bonds issued for American Airlines returned approximately 14% during the Fund’s fiscal year. Another notable performer was a Nassau County tobacco settlement bond, whose revenue stream is secured by a settlement agreement between the tobacco industry and multiple states. This security, rated B- by S&P and due to mature in 2046, returned 13% during the fiscal year.

6

| Performance summaries | |

| Delaware Tax-Free Arizona Fund | August 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

|

Fund and benchmark performance1,2 |

Average annual total returns through August 31, 2013 |

||||||||||

| 1 year | 5 years | 10 years | |||||||||

| Class A (Est. April 1, 1991) | |||||||||||

| Excluding sales charge | -6.62 | % | +3.80 | % | +3.84 | % | |||||

| Including sales charge | -10.85 | % | +2.84 | % | +3.36 | % | |||||

| Class B (Est. March 10, 1995) | |||||||||||

| Excluding sales charge | -6.99 | % | +3.10 | % | +3.22 | % | |||||

| Including sales charge | -10.55 | % | +2.84 | % | +3.22 | % | |||||

| Class C (Est. May 26, 1994) | |||||||||||

| Excluding sales charge | -7.30 | % | +3.02 | % | +3.07 | % | |||||

| Including sales charge | -8.19 | % | +3.02 | % | +3.07 | % | |||||

| Barclays Municipal Bond Index | -3.70 | % | +4.52 | % | +4.48 | % | |||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 8. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus.

Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from March 1, 2013, through Feb. 28, 2014. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

7

Performance

summaries

Delaware Tax-Free Arizona

Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Bond ratings are determined by a nationally recognized statistical rating organization.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees (excluding certain fees and expenses) in order to prevent total annual fund operating expenses from exceeding 0.59% of the Fund’s average daily net assets from Dec. 28, 2012, through Dec. 27, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 0.90% | 1.65% | 1.65% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.84% | 1.59% | 1.59% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

8

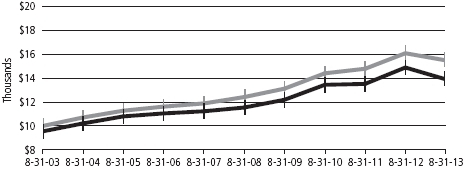

Performance of a $10,000

investment1

Average annual

total returns from Aug. 31, 2003, through Aug. 31, 2013

| For period beginning Aug. 31, 2003, through Aug. 31, 2013 | Starting value | Ending value | ||

|

|

Barclays Municipal Bond Index | $10,000 | $15,496 | |

|

|

Delaware Tax-Free Arizona Fund — Class A shares | $9,550 | $13,910 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 8. Please note additional details on pages 7 through 9.

The chart also assumes $10,000 invested in the Barclays Municipal Bond Index as of Aug. 31, 2003. The Barclays Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||

| Class A | VAZIX | 928916204 | |||

| Class B | DVABX | 928928639 | |||

| Class C | DVACX | 928916501 |

9

| Performance summaries | |

| Delaware Tax-Free California Fund | August 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through August 31, 2013 | ||||||

| 1 year | 5 years | 10 years | |||||

| Class A (Est. March 2, 1995) | |||||||

| Excluding sales charge | -5.63% | +4.87% | +4.61% | ||||

| Including sales charge | -9.92% | +3.90% | +4.13% | ||||

| Class B (Est. Aug. 23, 1995) | |||||||

| Excluding sales charge | -6.07% | +4.15% | +3.98% | ||||

| Including sales charge | -9.71% | +3.90% | +3.98% | ||||

| Class C (Est. April 9, 1996) | |||||||

| Excluding sales charge | -6.41% | +4.08% | +3.83% | ||||

| Including sales charge | -7.32% | +4.08% | +3.83% | ||||

| Barclays Municipal Bond Index | -3.70% | +4.52% | +4.48% | ||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 11. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from March 1, 2013, through Feb. 28, 2014. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

10

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Bond ratings are determined by a nationally recognized statistical rating organization.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees (excluding certain fees and expenses) in order to prevent total annual fund operating expenses from exceeding 0.57% of the Fund’s average daily net assets from Dec. 28, 2012, through Dec. 27, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 0.97% | 1.72% | 1.72% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.82% | 1.57% | 1.57% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

11

Performance

summaries

Delaware

Tax-Free California Fund

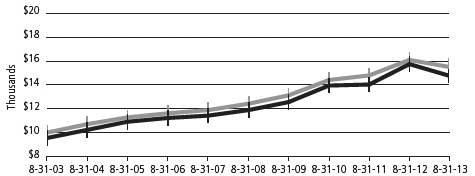

Performance of a $10,000

investment1

Average annual

total returns from Aug. 31, 2003, through Aug. 31, 2013

| For period beginning Aug. 31, 2003, through Aug. 31, 2013 | Starting value | Ending value | ||

|

|

Barclays Municipal Bond Index | $10,000 | $15,496 | |

|

|

Delaware Tax-Free California Fund — Class A shares | $9,550 | $14,976 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 11. Please note additional details on pages 10 through 12.

The chart also assumes $10,000 invested in the Barclays Municipal Bond Index as of Aug. 31, 2003. The Barclays Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||

| Class A | DVTAX | 928928829 | |||

| Class B | DVTFX | 928928811 | |||

| Class C | DVFTX | 928928795 |

12

| Delaware Tax-Free Colorado Fund | August 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through August 31, 2013 | ||||||

| 1 year | 5 years | 10 years | |||||

| Class A (Est. April 23, 1987) | |||||||

| Excluding sales charge | -6.56% | +3.83% | +3.97% | ||||

| Including sales charge | -10.77% | +2.88% | +3.49% | ||||

| Class B (Est. March 22, 1995) | |||||||

| Excluding sales charge | -6.93% | +3.15% | +3.35% | ||||

| Including sales charge | -10.54% | +2.89% | +3.35% | ||||

| Class C (Est. May 6, 1994) | |||||||

| Excluding sales charge | -7.23% | +3.07% | +3.20% | ||||

| Including sales charge | -8.14% | +3.07% | +3.20% | ||||

| Barclays Municipal Bond Index | -3.70% | +4.52% | +4.48% | ||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 14. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus.

Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from March 1, 2013, through Feb. 28, 2014. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

13

Performance

summaries

Delaware

Tax-Free Colorado Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Bond ratings are determined by a nationally recognized statistical rating organization.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees (excluding certain fees and expenses) in order to prevent total annual fund operating expenses from exceeding 0.59% of the Fund’s average daily net assets from Dec. 28, 2012, through Dec. 27, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 0.93% | 1.68% | 1.68% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.84% | 1.59% | 1.59% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

14

Performance of a $10,000

investment1

Average annual

total returns from Aug. 31, 2003, through Aug. 31, 2013

| For period beginning Aug. 31, 2003, through Aug. 31, 2013 | Starting value | Ending value | ||

|

|

Barclays Municipal Bond Index | $10,000 | $15,496 | |

|

|

Delaware Tax-Free Colorado Fund — Class A shares | $9,550 | $14,076 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 14. Please note additional details on pages 13 through 15.

The chart also assumes $10,000 invested in the Barclays Municipal Bond Index as of Aug. 31, 2003. The Barclays Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||

| Class A | VCTFX | 928920107 | |||

| Class B | DVBTX | 928928787 | |||

| Class C | DVCTX | 92907R101 |

15

| Performance summaries | |

| Delaware Tax-Free Idaho Fund | August 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through August 31, 2013 | ||||||

| 1 year | 5 years | 10 years | |||||

| Class A (Est. Jan. 4, 1995) | |||||||

| Excluding sales charge | -6.99% | +3.28% | +3.77% | ||||

| Including sales charge | -11.20% | +2.34% | +3.30% | ||||

| Class B (Est. March 16, 1995) | |||||||

| Excluding sales charge | -7.71% | +2.52% | +3.15% | ||||

| Including sales charge | -11.30% | +2.25% | +3.15% | ||||

| Class C (Est. Jan. 11, 1995) | |||||||

| Excluding sales charge | -7.70% | +2.51% | +3.00% | ||||

| Including sales charge | -8.60% | +2.51% | +3.00% | ||||

| Barclays Municipal Bond Index | -3.70% | +4.52% | +4.48% | ||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 17. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

16

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Bond ratings are determined by a nationally recognized statistical rating organization.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees (excluding certain fees and expenses) in order to prevent total annual fund operating expenses from exceeding 0.63% of the Fund’s average daily net assets from Dec. 28, 2012, through Dec. 27, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 0.94% | 1.69% | 1.69% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.88% | 1.63% | 1.63% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

17

Performance

summaries

Delaware Tax-Free

Idaho Fund

Performance of a $10,000

investment1

Average annual

total returns from Aug. 31, 2003, through Aug. 31, 2013

| For period beginning Aug. 31, 2003, through Aug. 31, 2013 | Starting value | Ending value | ||||

|

|

Barclays Municipal Bond Index | $10,000 | $15,496 | |||

|

|

Delaware Tax-Free Idaho Fund — Class A shares | $9,550 | $13,821 | |||

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 17. Please note additional details on pages 16 through 18.

The chart also assumes $10,000 invested in the Barclays Municipal Bond Index as of Aug. 31, 2003. The Barclays Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||

| Class A | VIDAX | 928928704 | |||

| Class B | DVTIX | 928928746 | |||

| Class C | DVICX | 928928803 |

18

|

Delaware Tax-Free New York Fund |

August 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through August 31, 2013 | |||||||

| 1 year | 5 years | 10 years | ||||||

| Class A (Est. Nov. 6, 1987) | ||||||||

| Excluding sales charge | -6.27% | +4.41% | +4.45% | |||||

| Including sales charge | -10.49% | +3.45% | +3.98% | |||||

| Class B (Est. Nov. 14, 1994) | ||||||||

| Excluding sales charge | -6.67% | +3.73% | +3.82% | |||||

| Including sales charge | -10.29% | +3.47% | +3.82% | |||||

| Class C (Est. April 26, 1995) | ||||||||

| Excluding sales charge | -7.00% | +3.63% | +3.67% | |||||

| Including sales charge | -7.91% | +3.63% | +3.67% | |||||

| Barclays Municipal Bond Index | -3.70% | +4.52% | +4.48% | |||||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 20. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus.

Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from March 1, 2013, through Feb. 28, 2014. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

19

Performance

summaries

Delaware Tax-Free New

York Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

Bond ratings are determined by a nationally recognized statistical rating organization.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees (excluding certain fees and expenses) in order to prevent total annual fund operating expenses from exceeding 0.55% of the Fund’s average daily net assets from Dec. 28, 2012, through Dec. 27, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 1.01% | 1.76% | 1.76% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.80% | 1.55% | 1.55% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

20

Performance of a $10,000

investment1

Average annual

total returns from Aug. 31, 2003, through Aug. 31, 2013

| For period beginning Aug. 31, 2003, through Aug. 31, 2013 | Starting value | Ending value | ||||

|

|

Barclays Municipal Bond Index | $10,000 | $15,496 | |||

|

|

Delaware Tax-Free New York Fund — Class A shares | $9,550 | $14,754 | |||

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 20. Please note additional details on pages 19 through 21.

The chart also assumes $10,000 invested in the Barclays Municipal Bond Index as of Aug. 31, 2003. The Barclays Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||

| Class A | FTNYX | 928928274 | |||

| Class B | DVTNX | 928928266 | |||

| Class C | DVFNX | 928928258 |

21

Disclosure of Fund

expenses

For the six-month period from March

1, 2013 to August 31, 2013 (Unaudited)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. These following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from March 1, 2013 to Aug. 31, 2013.

Actual expenses

The first section of the tables shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the tables shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Funds’ expenses shown in the tables reflect fee waivers in effect. The expenses shown in each table assume reinvestment of all dividends and distributions.

22

| Delaware Tax-Free Arizona Fund | |||||||||||||||||

| Expense analysis of an investment of $1,000 | |||||||||||||||||

| Beginning | Ending | Expenses | |||||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||||

| 3/1/13 | 8/31/13 | Expense Ratio | 3/1/13 to 8/31/13* | ||||||||||||||

| Actual Fund return† | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 914.60 | 0.84% | $ | 4.05 | ||||||||||

| Class B | 1,000.00 | 914.30 | 0.84% | 4.05 | |||||||||||||

| Class C | 1,000.00 | 911.30 | 1.59% | 7.66 | |||||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.97 | 0.84% | $ | 4.28 | ||||||||||

| Class B | 1,000.00 | 1,020.97 | 0.84% | 4.28 | |||||||||||||

| Class C | 1,000.00 | 1,017.19 | 1.59% | 8.08 | |||||||||||||

| Delaware Tax-Free California Fund | |||||||||||||||||

| Expense analysis of an investment of $1,000 | |||||||||||||||||

| Beginning | Ending | Expenses | |||||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||||

| 3/1/13 | 8/31/13 | Expense Ratio | 3/1/13 to 8/31/13* | ||||||||||||||

| Actual Fund return† | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 912.70 | 0.82% | $ | 3.95 | ||||||||||

| Class B | 1,000.00 | 912.00 | 0.82% | 3.95 | |||||||||||||

| Class C | 1,000.00 | 908.60 | 1.57% | 7.55 | |||||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,021.07 | 0.82% | $ | 4.18 | ||||||||||

| Class B | 1,000.00 | 1,021.07 | 0.82% | 4.18 | |||||||||||||

| Class C | 1,000.00 | 1,017.29 | 1.57% | 7.98 | |||||||||||||

| Delaware Tax-Free Colorado Fund | |||||||||||||||||

| Expense analysis of an investment of $1,000 | |||||||||||||||||

| Beginning | Ending | Expenses | |||||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||||

| 3/1/13 | 8/31/13 | Expense Ratio | 3/1/13 to 8/31/13* | ||||||||||||||

| Actual Fund return† | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 914.80 | 0.84% | $ | 4.05 | ||||||||||

| Class B | 1,000.00 | 914.50 | 0.84% | 4.05 | |||||||||||||

| Class C | 1,000.00 | 911.50 | 1.59% | 7.66 | |||||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.97 | 0.84% | $ | 4.28 | ||||||||||

| Class B | 1,000.00 | 1,020.97 | 0.84% | 4.28 | |||||||||||||

| Class C | 1,000.00 | 1,017.19 | 1.59% | 8.08 | |||||||||||||

23

Disclosure of Fund expenses

| Delaware Tax-Free Idaho Fund | |||||||||||||||||

| Expense analysis of an investment of $1,000 | |||||||||||||||||

| Beginning | Ending | Expenses | |||||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||||

| 3/1/13 | 8/31/13 | Expense Ratio | 3/1/13 to 8/31/13* | ||||||||||||||

| Actual Fund return† | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 920.60 | 0.88% | $ | 4.26 | ||||||||||

| Class B | 1,000.00 | 916.90 | 1.63% | 7.88 | |||||||||||||

| Class C | 1,000.00 | 917.00 | 1.63% | 7.88 | |||||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.77 | 0.88% | $ | 4.48 | ||||||||||

| Class B | 1,000.00 | 1,016.99 | 1.63% | 8.29 | |||||||||||||

| Class C | 1,000.00 | 1,016.99 | 1.63% | 8.29 | |||||||||||||

| Delaware Tax-Free New York Fund | |||||||||||||||||

| Expense analysis of an investment of $1,000 | |||||||||||||||||

| Beginning | Ending | Expenses | |||||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||||

| 3/1/13 | 8/31/13 | Expense Ratio | 3/1/13 to 8/31/13* | ||||||||||||||

| Actual Fund return† | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 913.60 | 0.80% | $ | 3.86 | ||||||||||

| Class B | 1,000.00 | 913.90 | 0.80% | 3.86 | |||||||||||||

| Class C | 1,000.00 | 909.80 | 1.55% | 7.46 | |||||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,021.17 | 0.80% | $ | 4.08 | ||||||||||

| Class B | 1,000.00 | 1,021.17 | 0.80% | 4.08 | |||||||||||||

| Class C | 1,000.00 | 1,017.39 | 1.55% | 7.88 | |||||||||||||

*“Expenses Paid During Period” are equal to the relevant Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

†Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns.

24

| Security type/sector allocations | |

| Delaware Tax-Free Arizona Fund | As of August 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | ||||

| Municipal Bonds* | 97.83 | % | |||

| Corporate Revenue Bonds | 9.04 | % | |||

| Education Revenue Bonds | 18.85 | % | |||

| Electric Revenue Bonds | 7.23 | % | |||

| Healthcare Revenue Bonds | 22.02 | % | |||

| Lease Revenue Bonds | 11.01 | % | |||

| Local General Obligation Bonds | 2.74 | % | |||

| Pre-Refunded Bonds | 3.66 | % | |||

| Resource Recovery Revenue Bond | 1.93 | % | |||

| Special Tax Revenue Bonds | 16.78 | % | |||

| Transportation Revenue Bonds | 3.32 | % | |||

| Water & Sewer Revenue Bond | 1.25 | % | |||

| Short-Term Investment | 0.26 | % | |||

| Total Value of Securities | 98.09 | % | |||

| Receivables and Other Assets Net of Liabilities | 1.91 | % | |||

| Total Net Assets | 100.00 | % | |||

* As of the date of this report, Delaware Tax-Free Arizona Fund held bonds issued by or on behalf of territories of the United States as follows:

| Territory | (as a % of fixed income investments) | |||

| Guam | 1.38 | % | ||

| Puerto Rico | 6.57 | % | ||

25

| Security type/sector allocations | |

| Delaware Tax-Free California Fund | As of August 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds* | 97.73 | % |

| Corporate Revenue Bonds | 5.50 | % |

| Education Revenue Bonds | 10.91 | % |

| Electric Revenue Bonds | 6.45 | % |

| Healthcare Revenue Bonds | 15.68 | % |

| Housing Revenue Bonds | 3.74 | % |

| Lease Revenue Bonds | 9.14 | % |

| Local General Obligation Bonds | 8.25 | % |

| Pre-Refunded Bonds | 2.05 | % |

| Resource Recovery Revenue Bond | 0.99 | % |

| Special Tax Revenue Bonds | 14.78 | % |

| State General Obligation Bonds | 7.83 | % |

| Transportation Revenue Bonds | 7.72 | % |

| Water & Sewer Revenue Bonds | 4.69 | % |

| Short-Term Investment | 0.48 | % |

| Total Value of Securities | 98.21 | % |

| Receivables and Other Assets Net of Liabilities | 1.79 | % |

| Total Net Assets | 100.00 | % |

* As of the date of this report, Delaware Tax-Free California Fund held bonds issued by or on behalf of territories of the United States as follows:

| Territory | (as a % of fixed income investments) | |

| Puerto Rico | 2.87 | % |

| U.S. Virgin Islands | 0.31 | % |

26

| Delaware Tax-Free Colorado Fund | As of August 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds* | 97.60 | % |

| Corporate Revenue Bonds | 1.32 | % |

| Education Revenue Bonds | 7.60 | % |

| Electric Revenue Bonds | 5.75 | % |

| Healthcare Revenue Bonds | 29.65 | % |

| Housing Revenue Bonds | 1.22 | % |

| Lease Revenue Bonds | 4.17 | % |

| Local General Obligation Bonds | 12.03 | % |

| Pre-Refunded Bonds | 13.81 | % |

| Special Tax Revenue Bonds | 14.43 | % |

| Transportation Revenue Bonds | 6.05 | % |

| Water & Sewer Revenue Bonds | 1.57 | % |

| Short-Term Investments | 0.69 | % |

| Total Value of Securities | 98.29 | % |

| Receivables and Other Assets Net of Liabilities | 1.71 | % |

| Total Net Assets | 100.00 | % |

* As of the date of this report, Delaware Tax-Free Colorado Fund held bonds issued by or on behalf of territories of the United States as follows:

| Territory | (as a % of fixed income investments) | |

| Guam | 1.44 | % |

| Puerto Rico | 6.69 | % |

27

| Security type/sector allocations | |

| Delaware Tax-Free Idaho Fund | As of August 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds* | 95.67 | % |

| Corporate Revenue Bonds | 7.83 | % |

| Education Revenue Bonds | 9.97 | % |

| Electric Revenue Bonds | 3.10 | % |

| Healthcare Revenue Bonds | 9.48 | % |

| Housing Revenue Bonds | 2.45 | % |

| Lease Revenue Bonds | 6.36 | % |

| Local General Obligation Bonds | 24.40 | % |

| Pre-Refunded Bonds | 4.03 | % |

| Special Tax Revenue Bonds | 17.98 | % |

| Transportation Revenue Bonds | 9.20 | % |

| Water & Sewer Revenue Bond | 0.87 | % |

| Short-Term Investments | 1.28 | % |

| Total Value of Securities | 96.95 | % |

| Receivables and Other Assets Net of Liabilities | 3.05 | % |

| Total Net Assets | 100.00 | % |

* As of the date of this report, Delaware Tax-Free Idaho Fund held bonds issued by or on behalf of territories of the United States as follows:

| Territory | (as a % of fixed income investments) | |

| Guam | 1.05 | % |

| Puerto Rico | 10.27 | % |

| U.S. Virgin Islands | 1.41 | % |

28

| Delaware Tax-Free New York Fund | As of August 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds* | 95.91 | % |

| Corporate Revenue Bonds | 8.12 | % |

| Education Revenue Bonds | 22.06 | % |

| Electric Revenue Bonds | 2.50 | % |

| Healthcare Revenue Bonds | 16.50 | % |

| Housing Revenue Bonds | 0.81 | % |

| Lease Revenue Bonds | 9.64 | % |

| Local General Obligation Bonds | 6.67 | % |

| Pre-Refunded Bonds | 1.17 | % |

| Special Tax Revenue Bonds | 16.45 | % |

| State General Obligation Bonds | 0.81 | % |

| Transportation Revenue Bonds | 6.98 | % |

| Water & Sewer Revenue Bonds | 4.20 | % |

| Total Value of Securities | 95.91 | % |

| Receivables and Other Assets Net of Liabilities | 4.09 | % |

| Total Net Assets | 100.00 | % |

* As of the date of this report, Delaware Tax-Free New York Fund held bonds issued by or on behalf of territories of the United States as follows:

| Territory | (as a % of fixed income investments) | |

| Guam | 0.32 | % |

| Puerto Rico | 3.16 | % |

| Virgin Islands | 0.13 | % |

29

| Schedules of investments | |

| Delaware Tax-Free Arizona Fund | August 31, 2013 |

| Principal amount | Value | ||||||

| Municipal Bonds – 97.83% | |||||||

| Corporate Revenue Bonds – 9.04% | |||||||

| • | Maricopa County Pollution Control | ||||||

| (Public Services-Palo Verde Project) | |||||||

| Series B 5.20% 6/1/43 | $ | 1,500,000 | $ | 1,636,470 | |||

| • | Navajo County Pollution Control Revenue | ||||||

| (Arizona Public Services-Cholla) | |||||||

| Series D 5.75% 6/1/34 | 1,500,000 | 1,663,050 | |||||

| Pima County Industrial Development Authority Pollution | |||||||

| Control Revenue (Tucson Electric Power) | |||||||

| 5.75% 9/1/29 | 750,000 | 763,845 | |||||

| Series A 5.25% 10/1/40 | 3,400,000 | 3,203,378 | |||||

| Salt Verde Financial Senior Gas Revenue | |||||||

| 5.00% 12/1/37 | 1,000,000 | 915,660 | |||||

| 8,182,403 | |||||||

| Education Revenue Bonds – 18.85% | |||||||

| Arizona Health Facilities Authority | |||||||

| Healthcare Education Revenue (Kirksville College) | |||||||

| 5.125% 1/1/30 | 1,500,000 | 1,505,925 | |||||

| Arizona State University Certificates of Participation | |||||||

| (Research Infrastructure Project) | |||||||

| 5.00% 9/1/30 (AMBAC) | 1,395,000 | 1,422,635 | |||||

| Arizona State University Energy Management Revenue | |||||||

| (Arizona State University Tempe Campus II Project) | |||||||

| 4.50% 7/1/24 | 1,000,000 | 1,031,540 | |||||

| Arizona State University Series C 5.50% 7/1/25 | 330,000 | 365,577 | |||||

| Glendale Industrial Development Authority Revenue | |||||||

| (Midwestern University) | |||||||

| 5.00% 5/15/31 | 645,000 | 633,061 | |||||

| 5.125% 5/15/40 | 1,305,000 | 1,235,052 | |||||

| Northern Arizona University | |||||||

| 5.00% 6/1/36 | 475,000 | 471,770 | |||||

| 5.00% 6/1/41 | 1,240,000 | 1,221,598 | |||||

| Phoenix Industrial Development Authority | |||||||

| (Choice Academies Project) 5.625% 9/1/42 | 1,250,000 | 1,065,063 | |||||

| (Eagle College Preparatory Project) | |||||||

| Series A 5.00% 7/1/43 | 1,500,000 | 1,247,700 | |||||

| (Great Hearts Academic Project) | |||||||

| 6.30% 7/1/42 | 500,000 | 471,885 | |||||

| 6.40% 7/1/47 | 500,000 | 471,580 | |||||

| (Rowan University Project) 5.00% 6/1/42 | 2,000,000 | 1,850,800 | |||||

30

| Principal amount | Value | ||||||

| Municipal Bonds (continued) | |||||||

| Education Revenue Bonds (continued) | |||||||

| Pima County Industrial Development Authority | |||||||

| Educational Revenue | |||||||

| (Edkey Charter School Project) 6.00% 7/1/48 | $ | 1,000,000 | $ | 845,900 | |||

| (Tucson Country Day School Project) 5.00% 6/1/37 | 1,500,000 | 1,220,130 | |||||

| Tucson Industrial Development Authority Lease Revenue | |||||||

| (University of Arizona-Marshall Foundation) | |||||||

| Series A 5.00% 7/15/27 (AMBAC) | 1,000,000 | 983,180 | |||||

| University of Arizona Board of Rights | |||||||

| Series A 5.00% 6/1/38 | 1,000,000 | 1,013,020 | |||||

| 17,056,416 | |||||||

| Electric Revenue Bonds – 7.23% | |||||||

| Maricopa County Pollution Control | |||||||

| (El Paso Electric Palo Verde Project) | |||||||

| Series A 4.50% 8/1/42 | 2,165,000 | 1,752,936 | |||||

| Mesa Utilities System Revenue 5.00% 7/1/18 (NATL-RE) | 1,500,000 | 1,720,635 | |||||

| Pinal County Electric District #3 5.25% 7/1/41 | 2,000,000 | 2,018,400 | |||||

| Salt River Project Agricultural Improvement & Power | |||||||

| District Electric System Revenue | |||||||

| Series A 5.00% 12/1/30 | 1,000,000 | 1,051,680 | |||||

| 6,543,651 | |||||||

| Healthcare Revenue Bonds – 22.02% | |||||||

| Arizona Health Facilities Authority Revenue | |||||||

| (Banner Health) Series A 5.00% 1/1/43 | 1,000,000 | 955,530 | |||||

| (Phoenix Children’s Hospital) Series A 5.00% 2/1/42 | 2,600,000 | 2,310,230 | |||||

| Glendale Industrial Development Authority Hospital | |||||||

| Revenue (John C. Lincoln Health) 5.00% 12/1/42 | 2,205,000 | 2,031,841 | |||||

| Maricopa County Industrial Development | |||||||

| Authority Health Facilities Revenue | |||||||

| (Catholic Healthcare West) Series A | |||||||

| 5.25% 7/1/32 | 970,000 | 991,369 | |||||

| 5.50% 7/1/26 | 1,000,000 | 1,034,500 | |||||

| 6.00% 7/1/39 | 2,500,000 | 2,608,950 | |||||

| Puerto Rico Industrial Tourist Educational Medical & | |||||||

| Environmental Control Facilities | |||||||

| Financing Authority (Auxilio Mutuo) Series A 6.00% 7/1/33 | 1,615,000 | 1,491,743 | |||||

| Scottsdale Industrial Development Authority | |||||||

| Hospital Revenue (Scottsdale Healthcare) | |||||||

| Series A 5.25% 9/1/30 | 1,250,000 | 1,249,888 | |||||

31

Schedules of

investments

Delaware Tax-Free

Arizona Fund

| Principal amount | Value | ||||||

| Municipal Bonds (continued) | |||||||

| Healthcare Revenue Bonds (continued) | |||||||

| Tempe Industrial Development Authority Revenue | |||||||

| (Friendship Village) Series A 6.25% 12/1/42 | $ | 1,200,000 | $ | 1,169,220 | |||

| University of Arizona Medical Center Hospital Revenue | |||||||

| 6.00% 7/1/39 | 1,500,000 | 1,525,620 | |||||

| 6.50% 7/1/39 | 2,500,000 | 2,651,899 | |||||