UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-04973 | |

| Exact name of registrant as specified in charter: |

Voyageur Insured Funds

|

|

| Address of principal executive offices: | 2005 Market Street | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | David F. Connor, Esq. | |

| 2005 Market Street | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | (800) 523-1918 | |

| Date of fiscal year end: | August 31 | |

| Date of reporting period: | August 31, 2011 |

Item 1. Reports to Stockholders

|

Annual report

Delaware Tax-Free Arizona Fund

Delaware Tax-Free California Fund Delaware Tax-Free Colorado Fund Delaware Tax-Free Idaho Fund Delaware Tax-Free New York Fund August 31, 2011

Fixed income mutual funds

|

|

Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectus and, if available, their summary prospectuses, which may be obtained by visiting www.delawareinvestments.com or calling 800 523-1918. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

|

|

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit www.delawareinvestments.com/edelivery. |

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Tax-Free Arizona Fund, Delaware Tax-Free California Fund, Delaware Tax-Free Colorado Fund, Delaware Tax-Free Idaho Fund, and Delaware Tax-Free New York Fund at www.delawareinvestments.com.

Manage your investments online

- 24-hour access to your account information

- Obtain share prices

- Check your account balance and recent transactions

- Request statements or literature

- Make purchases and redemptions

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services.

Investments in Delaware Tax-Free Arizona Fund, Delaware Tax-Free California Fund, Delaware Tax-Free Colorado Fund, Delaware Tax-Free Idaho Fund, and Delaware Tax-Free New York Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

Table of contents

| Portfolio management review | 1 |

| Performance summaries | 9 |

| Disclosure of Fund expenses | 24 |

| Security type/sector allocations | 27 |

| Statements of net assets | 32 |

| Statements of operations | 72 |

| Statements of changes in net assets | 74 |

| Financial highlights | 84 |

| Notes to financial statements | 114 |

| Report of independent registered | |

| public accounting firm | 129 |

| Other Fund information | 130 |

| Board of trustees/directors and | |

| officers addendum | 136 |

| About the organization | 146 |

Unless otherwise noted, views expressed herein are current as of Aug. 31, 2011, and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Funds’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2011 Delaware Management Holdings, Inc.

All third-party trademarks cited are the property of their respective owners.

| Portfolio management review | ||

| Delaware Investments® state tax-free funds | September 6, 2011 | |

| Performance preview (for the year ended August 31, 2011) | ||||

| Delaware Tax-Free Arizona Fund (Class A shares) | 1-year return | +0.57% | ||

| Barclays Capital Municipal Bond Index (benchmark) | 1-year return | +2.66% | ||

| Lipper Arizona Municipal Debt Funds Average | 1-year return | +1.43% | ||

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Tax-Free Arizona Fund, please see the table on page 9.

For complete, annualized performance for Delaware Tax-Free Arizona Fund, please see the table on page 9.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The Lipper Arizona Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Arizona (double tax-exempt) or a city in Arizona (triple tax-exempt).

The Lipper Arizona Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Arizona (double tax-exempt) or a city in Arizona (triple tax-exempt).

| Delaware Tax-Free California Fund (Class A shares) | 1-year return | +0.83% | ||

| Barclays Capital Municipal Bond Index (benchmark) | 1-year return | +2.66% | ||

| Lipper California Municipal Debt Funds Average | 1-year return | +1.30% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Tax-Free California Fund, please see the table on page 12.

For complete, annualized performance for Delaware Tax-Free California Fund, please see the table on page 12.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The Lipper California Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in California (double tax-exempt) or a city in California (triple tax-exempt).

The Lipper California Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in California (double tax-exempt) or a city in California (triple tax-exempt).

| Delaware Tax-Free Colorado Fund (Class A shares) | 1-year return | +0.71% | ||

| Barclays Capital Municipal Bond Index (benchmark) | 1-year return | +2.66% | ||

| Lipper Colorado Municipal Debt Funds Average | 1-year return | +1.75% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Tax-Free Colorado Fund, please see the table on page 15.

For complete, annualized performance for Delaware Tax-Free Colorado Fund, please see the table on page 15.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The Lipper Colorado Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Colorado (double tax-exempt) or a city in Colorado (triple tax-exempt).

The Lipper Colorado Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in Colorado (double tax-exempt) or a city in Colorado (triple tax-exempt).

1

Portfolio management review

Delaware Investments® state tax-free funds

Delaware Investments® state tax-free funds

| Delaware Tax-Free Idaho Fund (Class A shares) | 1-year return | +0.56% | ||

| Barclays Capital Municipal Bond Index (benchmark) | 1-year return | +2.66% | ||

| Lipper Other States Municipal Debt Funds Average | 1-year return | +1.49% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Tax-Free Idaho Fund, please see the table on page 18.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

For complete, annualized performance for Delaware Tax-Free Idaho Fund, please see the table on page 18.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The Lipper Other States Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation on a specified city or state basis.

The Lipper Other States Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation on a specified city or state basis.

| Delaware Tax-Free New York Fund (Class A shares) | 1-year return | +0.63% | ||

| Barclays Capital Municipal Bond Index (benchmark) | 1-year return | +2.66% | ||

| Lipper New York Municipal Debt Funds Average | 1-year return | +1.03% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Tax-Free New York Fund, please see the table on page 21.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

For complete, annualized performance for Delaware Tax-Free New York Fund, please see the table on page 21.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

The Lipper New York Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in New York (double tax-exempt) or a city in New York (triple tax-exempt).

The Lipper New York Municipal Debt Funds Average compares funds that limit assets to those securities that are exempt from taxation in New York (double tax-exempt) or a city in New York (triple tax-exempt).

Economic backdrop

When the Funds’ fiscal year began in September 2010, many municipal bond investors appeared to be anticipating a moderately improving economy and, as a result, they were likely expecting interest rates to rise in 2011 (especially since rates had been trending at historically low levels). However, this optimism was soon muted as mounting data suggested a slowdown in U.S. economic growth and stimulated fears of a recession.

Ultimately, lackluster reports on gross domestic product (GDP), which measures the total dollar value of goods and services produced by the economy, confirmed the economy’s disappointing performance. The data reflected persistent weakness in economic output, including the following readings:

- In the third and fourth quarters of 2010, U.S. GDP expanded by annualized rates of 2.5% and 2.3%, respectively.

- During the first quarter of 2011, GDP grew at an annualized rate of just 0.4% — the weakest showing in seven quarters.

- Growth in the second quarter of 2011 came in only slightly better, at an estimated annualized rate of 1.0%.

(Data: U.S. Commerce Department)

Arguably, employment continued to be the Achilles’ heel of the economy. Even early in the fiscal year, amid decent economic growth, employment continued to struggle. At the start of the Funds’ fiscal year, unemployment was at a high rate of 9.6% and ticked further upward to 9.8% within several months. A period of optimism followed as the jobless

2

rate declined a full percentage point between November 2010 and March 2011. From there, however, the unemployment rate reversed course and rose to 9.0% in April, hovering close to that level for the remainder of the Funds’ fiscal year.

In the second half of the Funds’ fiscal year, the global economic picture worsened:

- In March 2011, the massive earthquake that struck Japan, followed by a devastating tsunami and nuclear crisis, hurt factory production and reduced worldwide economic output.

- The European debt crisis resurfaced and threatened to ensnare some of the continent’s larger economies, such as Italy and Spain.

- A political battle in Washington, D.C. over government spending and the lifting of the federal debt ceiling increased investor uncertainty and anxiety.

- Citing these severe political disagreements in the face of rising debt, credit-rating agency Standard & Poor’s (S&P) downgraded the long-term rating on U.S. sovereign debt. In what was the first such downgrade in history, the United States’ S&P rating went to AA+, one notch down from its former rating of AAA.

These mounting challenges and economic crosscurrents led to significant volatility in the financial markets. Despite the rating downgrade of U.S. bonds, many fixed income investors flocked to the perceived safety of U.S. Treasury debt, pushing interest rates even lower.

Economic conditions within each state, briefly noted

Arizona continued to be challenged by large budget shortfalls due to declines in sales tax revenues, much as it has in recent years. The effects of the housing downturn on the state’s economy have been significant, leading to a recovery period that we believe could exceed those of many other states.

Preliminary estimates for fiscal 2011 show the state’s general fund posting a base revenue growth of 11.6% (the first annual increase since 2007). This growth is aided by a temporary $0.01 sales tax increase as well as higher-than-expected individual income taxes.

(Data: U.S. Labor Department; Moody’s Investors Service.)

For its fiscal 2011, California’s general fund revenues were 7.7% higher than fiscal 2010. The state’s 2012 budget closed a $26.6 billion gap through actions that included spending cuts ($15.0 billion), revenue actions ($0.9 billion), and improved revenue collections ($8.3 billion), along with a range of other solutions ($2.9 billion). While the budget uses significantly fewer one-time solutions than those used in previous budgets, there are a number of measures that we believe may fail to materialize. These include $4 billion in additional revenue that has not been attributable to a particular revenue stream, and $2.4 billion in health and human services solutions that require federal consent. If the additional $4 billion in revenues does not materialize, up to $2.5 billion in automatic spending cuts will be triggered in January 2012.

(Source: U.S. Labor Department; California State Controller monthly reports; Moody’s Investors Service.)

3

Portfolio management review

Delaware Investments® state tax-free funds

Delaware Investments® state tax-free funds

Colorado’s economy is diverse, with a variety of service-sector strengths.

The state’s general fund revenues for fiscal 2011 increased 10.6% above fiscal 2010, due partly to growth in total wages, growth in consumer spending, growth in business outlays, and a surge in capital gains related to a rebound in the stock market. Colorado lawmakers passed a $7 billion general fund budget for fiscal 2012. The budget includes a $250 million cut to K–12 education, a general fund reserve of 4%, $100 million in the state education fund, and a transfer of $71 million in severance tax funds.

(Data: U.S. Labor Department; Colorado Office of State Planning and Budgeting; Moody’s Investors Service.)

In Idaho, the economy has expanded and diversified in recent years, benefiting from population growth. General fund receipts for fiscal 2011 were $2.44 billion, which was 3.6% above budget. Lawmakers closed a $92 million gap for the $2.5 billion fiscal 2012 budget, through measures that included cuts to education and Medicaid and a general 2.2% reduction across certain state agencies.

The budget represented a 3% increase over fiscal 2011 without relying on any tax increases.

(Data: U.S. Labor Department; Idaho Division of Financial Management; Idaho State Controller’s website.)

New York’s general fund receipts for fiscal 2011 totaled $54.4 billion and were 3.6% higher than fiscal 2010. For the first time since 2006, legislators adopted a budget before the April 1 deadline; they signed off on a $132.5 billion budget that includes steep spending cuts (especially to education and healthcare).

(Data: U.S. Labor Department; New York State Division of the Budget; Moody’s Investors Service; New York State Comptroller.)

Conditions within municipal bond markets

Municipal bonds benefited from a generally favorable market backdrop during the first two months of the Funds’ fiscal year. Inflation remained under control and interest rates trended downward, boosting the performance of fixed income securities. Two additional factors, more technical in nature, had a positive effect on municipal securities: supply of municipal bonds remained constrained, and demand remained healthy.

Beginning in November 2010, however, a number of factors combined to weigh on the municipal bond market:

- Many investors worried that renewed federal economic stimulus efforts would increase the risk of inflation.

- Expectations grew that Republican congressional election victories would mean the end of the federal Build America Bonds program and a potential increase in the supply of traditional tax-exempt debt.

4

- Worries mounted about the fiscal condition of many state and local governments and their ability to repay their debt. Investor anxiety about state finances was exacerbated by a heavy dose of negative headlines from various media outlets, including articles in The Wall Street Journal, The New York Times, and a particularly troubling segment that aired on the television program 60 Minutes in mid-December 2010.

Amid these conditions, the municipal bond market experienced two abrupt selloffs during the fourth quarter of 2010, setting in motion a wave of negative sentiment that spilled into early 2011. Within a very short time, municipal bond mutual funds went from an environment of strong inflows to one of strong outflows.

After January 2011, however, the situation stabilized, and trends turned favorable for tax-exempt bond investors. Rates on municipal securities generally decreased throughout the rest of the fiscal year, following Treasury bond yields downward (though not to the same degree).

Across the yield curve, municipal bonds saw their prices rise and their yields decline. Overall, the municipal yield curve steepened modestly during the Funds’ fiscal year, meaning that the difference between short- and long-term municipal bond yields increased.

The strongest-performing parts of the yield curve were the middle maturities — bonds with maturities ranging from six to eight years. Very short investments did not gain as much ground, nor did bonds on the longer end of the maturity range.

With regard to credit quality, medium-grade securities, or A-rated bonds, were the market’s best performers. Bonds with the highest level of credit quality, namely those with AAA or AA credit ratings, were the second-strongest performing segment, while bonds rated BBB, the lowest tier of the investment grade bond universe, trailed all other investment grade bonds. Overall, this breakdown in performance reflected investors’ preference for bonds with less credit risk during what was largely an uncertain market climate.

A temporarily defensive approach

Going into 2011, we believed a heightened level of risk pervaded the market, and we took temporary steps to attempt to position the Funds’ portfolios more defensively; this meant sacrificing some income-generation potential, but it ultimately translated to an increase in credit quality within each Fund.

Because we expected the supply of municipal bonds to build in the wake of the expiration of the Build America Bonds program — especially for bonds with longer maturities — we modestly reduced each Fund’s exposure to longer-dated bonds, while trimming each Fund’s position in lower-rated issues. In both cases, we did not believe these types of securities would perform well in an environment of increased bond supply. (We should stress that these changes took place at the margins of each Fund’s portfolio and reflected only minor adjustments.)

Initially, these adjustments did not work as well as we had hoped, given that mid-January was the high point for interest rates during the Funds’ fiscal year. At that time, investors’ credit fears generally

5

Portfolio management review

Delaware Investments® state tax-free funds

Delaware Investments® state tax-free funds

started to subside, and rates began to move downward. This trend worked against the higher-quality, shorter-duration positioning we had recently moved toward.

Thus, in mid-March we decided that our conservative approach was not serving the Funds’ shareholders as well as we had anticipated. When it became clear that the bond market was recovering, we took steps that included, among other actions, reducing each Fund’s allocation to cash. In redeploying that cash, we followed our traditional credit-selection process and focused on the types of bonds we more routinely invest in — bonds that we believe offer very good potential value relative to their inherent risk. As a result, we gradually moved each Fund’s portfolio to a less defensive posture.

Notable holdings within the Funds

With a few exceptions, the best-performing individual bonds across the five Funds shared a number of characteristics. In general, bonds with short- to medium-term maturities tended to enjoy better performance throughout the Funds’ fiscal year. Also, bonds with lower credit ratings typically underperformed their higher-rated counterparts, amid an environment in which many investors reduced their exposure to bond issuers with weaker credit quality.

Another important performance factor was the timing of bond purchases. As we discussed, the high point for interest rates was mid-January 2011, when bond prices were relatively low. The bonds that we introduced into the Funds during this general period provided good returns, given that their prices rebounded when market conditions subsequently improved.

For example, Delaware Tax-Free Arizona Fund benefited from its holdings in Phoenix Civic Improvement Corporation water bonds. With a 2023 maturity date, these bonds were within the solid-performing portion of the yield curve. They also held high credit ratings of Aa2 from Moody’s and AAA from S&P. In addition, they were added to the Fund’s portfolio in mid-February 2011 when bond prices were still low, so we were able to obtain what we thought was good value for these securities. They later performed very well in the market recovery and we subsequently sold the securities. A second water bond issue from the Arizona Water Infrastructure Finance Authority also contributed strong returns, due partly to the security’s top credit rating of Aaa/AAA and 2021 maturity date.

In contrast, several bonds issued by U.S. territories were the weakest individual performers for Delaware Tax-Free Arizona Fund. (Bonds issued by U.S. territories are generally tax-exempt for residents of all 50 states.) The worst-performing bonds in absolute terms were utility bonds issued by the Puerto Rico Electric Power Authority, which declined about 14% during the fiscal year. We sold these bonds in February 2011 at what we viewed as a fair price, but in retrospect the result of this transaction was disappointing, because we were unable to capture their subsequent price appreciation in the rising market during the rest of the Fund’s fiscal year. Another lackluster security in Delaware Tax-Free Arizona Fund was from the U.S. Virgin Islands Public Finance Authority. With lower-investment-grade credit ratings of Baa1/BBB+, the bond was vulnerable in an environment of investor risk aversion. We exited the

6

position during the Fund’s fiscal year as the bond became a less-than-ideal candidate for the portfolio.

The best-performing bonds in Delaware Tax-Free California Fund were issued by San Mateo Union High School District. These bonds were pre-refunded during the Fund’s fiscal year, immediately resulting in a significant price boost when they became backed by very high-quality, short-maturity debt. Other strong performers in the Fund’s portfolio included California Department of Water Resources bonds. These securities, with credit ratings of Aa3/AA- (by Moody’s and S&P, respectively) and a 2020 maturity date, were purchased in late December 2010 and later appreciated when investor sentiment rebounded. In contrast, several longer-dated California bond issues with 2036 maturity dates performed relatively poorly and shed about 6% of their value during the fiscal year. These disappointments included bonds issued by the California Educational Facilities Authority and California Municipal Finance Authority. We believe investor sentiment about the latter bonds was also hampered by their low-investment-grade credit rating.

The top-performing bonds in Delaware Tax-Free Colorado Fund were two education issues. The first came from the Douglas County School District, which gained close to 10% during the Fund’s fiscal year. These securities, which were rated Aa2 by Moody’s and nonrated by S&P, benefited from their 2022 maturity date, as they were positioned squarely in a favorably performing segment of the yield curve. The other significant education holding was issued by the Boulder, Larimer, and Weld Counties School District, which had a similar Aa2/nonrated credit profile by Moody’s and S&P, respectively, and a 2019 maturity date. Both factors contributed to the bonds’ 9% total return during the year. We sold the two aforementioned education issues during the course of the Fund’s fiscal year to make way for new opportunities in the Fund’s portfolio. Besides the negative impact of the ill-timed Puerto Rico bond sale mentioned earlier, the Fund was also hurt by the performance of University of Colorado Hospital Authority bonds. These securities were likewise sold at an inopportune moment in mid-February 2011 and thus were unable to share in the municipal bond market’s appreciation over the next half-year.

Within Delaware Tax-Free Idaho Fund, notable performers included a Boise City Airport revenue bond. This Aa3/nonrated (by Moody’s and S&P, respectively) bond carried a 2020 maturity date and was opportunistically purchased by the Fund in February 2011. It returned more than 10% during the Fund’s fiscal year. Another favorable performer was a University of Idaho revenue bond, which enjoyed solid credit quality and had an intermediate maturity. On the weaker side of the ledger, the Fund’s underperforming bonds included two Puerto Rico issues: public utility bonds issued by the Puerto Rico Electric Power Authority, and bonds backed by dedicated sales taxes.

Finally, strong performers within Delaware Tax-Free New York Fund included a bond issued by the New York State Dormitory Authority, which generated a 14% total return during the Fund’s fiscal year. With a 2021 maturity date, a solid credit rating of A (by Moody’s), and a well-timed introduction

7

Portfolio management review

Delaware Investments® state tax-free funds

Delaware Investments® state tax-free funds

to the Fund’s portfolio, all of these factors contributed to the bond’s solid performance. The story was similar for New York City Transitional Finance Authority bonds, whose Aa1/AAA credit rating (by Moody’s and S&P, respectively), 2025 maturity date, and mid-January 2011 acquisition all proved advantageous. On the negative side, Puerto Rico Electric Power Authority bonds were a disappointment. Other notable underperformers included New York City Industrial Development Agency bonds issued to help finance a new stadium for the New York Mets professional baseball franchise. These bonds, with maturities of 2046 and credit ratings of Baa1/BB+ (again by Moody’s and S&P, respectively), were, in our view, broadly undervalued by many investors during the Fund’s fiscal year. We sold the bonds as they became less-than-ideal candidates for the Fund’s positioning and overall composition.

8

| Performance summaries | |

| Delaware Tax-Free Arizona Fund | August 31, 2011 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | Average annual total returns through Aug. 31, 2011 | |||||

| 1 year | 5 years | 10 years | ||||

| Class A (Est. April 1, 1991) | ||||||

| Excluding sales charge | +0.57% | +4.12% | +4.33% | |||

| Including sales charge | -3.92% | +3.17% | +3.86% | |||

| Class B (Est. March 10, 1995) | ||||||

| Excluding sales charge | -0.18% | +3.32% | +3.71% | |||

| Including sales charge | -4.03% | +3.06% | +3.71% | |||

| Class C (Est. May 26, 1994) | ||||||

| Excluding sales charge | -0.17% | +3.34% | +3.56% | |||

| Including sales charge | -1.13% | +3.34% | +3.56% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 10. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

9

Performance summaries

Delaware Tax-Free Arizona Fund

Delaware Tax-Free Arizona Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding certain fees and expenses) from exceeding 0.59% of the Fund’s average daily net assets from Dec. 29, 2010, through Dec. 29, 2011. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||

| Total annual operating expenses | 0.92% | 1.67% | 1.67% | |||

| (without fee waivers) | ||||||

| Net expenses | 0.84% | 1.59% | 1.59% | |||

| (including fee waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

10

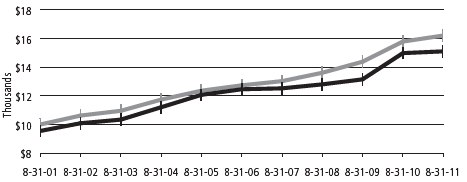

Performance of a $10,000 investment1

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

| For period beginning Aug. 31, 2001, through Aug. 31, 2011 | Starting value | Ending value | ||

|

|

Barclays Capital Municipal Bond Index | $10,000 | $16,208 | |

|

|

Delaware Tax-Free Arizona Fund — Class A Shares | $9,550 | $14,582 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2001, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 10. Please note additional details on pages 9 through 11.

The chart also assumes $10,000 invested in the Barclays Capital Municipal Bond Index as of Aug. 31, 2001. The Barclays Capital Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||||

| Class A | VAZIX | 928916204 | |||||

| Class B | DVABX | 928928639 | |||||

| Class C | DVACX | 928916501 | |||||

11

| Performance summaries | |

| Delaware Tax-Free California Fund | August 31, 2011 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | Average annual total returns through Aug. 31, 2011 | |||||

| 1 year | 5 years | 10 years | ||||

| Class A (Est. March 2, 1995) | ||||||

| Excluding sales charge | +0.83% | +3.93% | +4.70% | |||

| Including sales charge | -3.75% | +2.97% | +4.22% | |||

| Class B (Est. Aug. 23, 1995) | ||||||

| Excluding sales charge | +0.09% | +3.14% | +4.06% | |||

| Including sales charge | -3.77% | +2.88% | +4.06% | |||

| Class C (Est. April 9, 1996) | ||||||

| Excluding sales charge | -0.01% | +3.13% | +3.91% | |||

| Including sales charge | -0.97% | +3.13% | +3.91% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 13. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

12

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding certain fees and expenses) from exceeding 0.57% of the Fund’s average daily net assets from Dec. 29, 2010, through Dec. 29, 2011. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | ||||||

| Total annual operating expenses | 0.98 | % | 1.73 | % | 1.73 | % | |||

| (without fee waivers) | |||||||||

| Net expenses | 0.82 | % | 1.57 | % | 1.57 | % | |||

| (including fee waivers, if any) | |||||||||

| Type of waiver | Contractual | Contractual | Contractual | ||||||

13

Performance summaries

Delaware Tax-Free California Fund

Delaware Tax-Free California Fund

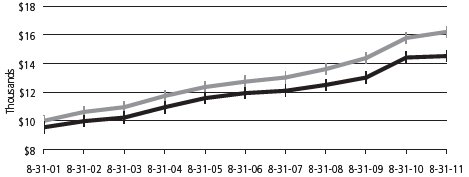

Performance of a $10,000 investment1

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

| For period beginning Aug. 31, 2001, through Aug. 31, 2011 | Starting value | Ending value | ||

|

|

Barclays Capital Municipal Bond Index | $10,000 | $16,208 | |

|

|

Delaware Tax-Free California Fund — Class A Shares | $9,550 | $15,105 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2001, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 13. Please note additional details on pages 12 through 14.

The chart also assumes $10,000 invested in the Barclays Capital Municipal Bond Index as of Aug. 31, 2001. The Barclays Capital Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||||

| Class A | DVTAX | 928928829 | |||||

| Class B | DVTFX | 928928811 | |||||

| Class C | DVFTX | 928928795 | |||||

14

| Delaware Tax-Free Colorado Fund | August 31, 2011 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | Average annual total returns through Aug. 31, 2011 | |||||

| 1 year | 5 years | 10 years | ||||

| Class A (Est. April 23, 1987) | ||||||

| Excluding sales charge | +0.71% | +4.00% | +4.29% | |||

| Including sales charge | -3.82% | +3.05% | +3.81% | |||

| Class B (Est. March 22, 1995) | ||||||

| Excluding sales charge | -0.04% | +3.23% | +3.67% | |||

| Including sales charge | -3.90% | +2.97% | +3.67% | |||

| Class C (Est. May 6, 1994) | ||||||

| Excluding sales charge | -0.03% | +3.22% | +3.53% | |||

| Including sales charge | -1.00% | +3.22% | +3.53% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 16. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

15

Performance summaries

Delaware Tax-Free Colorado Fund

Delaware Tax-Free Colorado Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding certain fees and expenses) from exceeding 0.59% of the Fund’s average daily net assets from Dec. 29, 2010, through Dec. 29, 2011. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||||

| Total annual operating expenses | 0.95 | % | 1.70 | % | 1.70 | % | ||

| (without fee waivers) | ||||||||

| Net expenses | 0.84 | % | 1.59 | % | 1.59 | % | ||

| (including fee waivers, if any) | ||||||||

| Type of waiver | Contractual | Contractual | Contractual | |||||

16

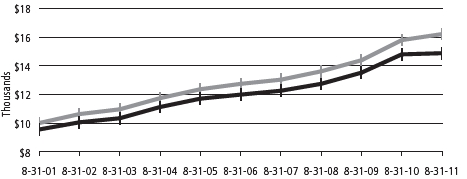

Performance of a $10,000 investment1

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

| For period beginning Aug. 31, 2001, through Aug. 31, 2011 | Starting value | Ending value | ||

|

|

Barclays Capital Municipal Bond Index | $10,000 | $16,208 | |

|

|

Delaware Tax-Free Colorado Fund — Class A Shares | $9,550 | $14,521 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2001, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 16. Please note additional details on pages 15 through 17.

The chart also assumes $10,000 invested in the Barclays Capital Municipal Bond Index as of Aug. 31, 2001. The Barclays Capital Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||||

| Class A | VCTFX | 928920107 | |||||

| Class B | DVBTX | 928928787 | |||||

| Class C | DVCTX | 92907R101 | |||||

17

| Performance summaries | |

| Delaware Tax-Free Idaho Fund | August 31, 2011 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | Average annual total returns through Aug. 31, 2011 | |||||

| 1 year | 5 years | 10 years | ||||

| Class A (Est. Jan. 4, 1995) | ||||||

| Excluding sales charge | +0.56% | +4.42% | +4.54% | |||

| Including sales charge | -3.96% | +3.46% | +4.06% | |||

| Class B (Est. March 16, 1995) | ||||||

| Excluding sales charge | -0.19% | +3.65% | +3.90% | |||

| Including sales charge | -4.07% | +3.39% | +3.90% | |||

| Class C (Est. Jan. 11, 1995) | ||||||

| Excluding sales charge | -0.20% | +3.64% | +3.76% | |||

| Including sales charge | -1.17% | +3.64% | +3.76% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 19. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

18

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding certain fees and expenses) from exceeding 0.63% of the Fund’s average daily net assets from Dec. 29, 2010, through Dec. 29, 2011. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||||

| Total annual operating expenses | 0.96 | % | 1.71 | % | 1.71 | % | ||

| (without fee waivers) | ||||||||

| Net expenses | 0.88 | % | 1.63 | % | 1.63 | % | ||

| (including fee waivers, if any) | ||||||||

| Type of waiver | Contractual | Contractual | Contractual | |||||

19

Performance summaries

Delaware Tax-Free Idaho Fund

Delaware Tax-Free Idaho Fund

Performance of a $10,000 investment1

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

| For period beginning Aug. 31, 2001, through Aug. 31, 2011 | Starting value | Ending value | ||

|

|

Barclays Capital Municipal Bond Index | $10,000 | $16,208 | |

|

|

Delaware Tax-Free Idaho Fund — Class A Shares | $9,550 | $14,874 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2001, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 19. Please note additional details on pages 18 through 20.

The chart also assumes $10,000 invested in the Barclays Capital Municipal Bond Index as of Aug. 31, 2001. The Barclays Capital Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||||

| Class A | VIDAX | 928928704 | |||||

| Class B | DVTIX | 928928746 | |||||

| Class C | DVICX | 928928803 | |||||

20

| Delaware Tax-Free New York Fund | August 31, 2011 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | Average annual total returns through Aug. 31, 2011 | |||||

| 1 year | 5 years | 10 years | ||||

| Class A (Est. Nov. 6, 1987) | ||||||

| Excluding sales charge | +0.63% | +4.56% | +4.80% | |||

| Including sales charge | -3.94% | +3.59% | +4.32% | |||

| Class B (Est. Nov. 14, 1994) | ||||||

| Excluding sales charge | -0.04% | +3.78% | +4.18% | |||

| Including sales charge | -3.92% | +3.52% | +4.18% | |||

| Class C (Est. April 26, 1995) | ||||||

| Excluding sales charge | -0.04% | +3.78% | +4.03% | |||

| Including sales charge | -1.01% | +3.78% | +4.03% | |||

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 22. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

21

Performance summaries

Delaware Tax-Free New York Fund

Delaware Tax-Free New York Fund

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

Funds that invest primarily in one state may be more susceptible to the economic, regulatory, and other factors of that state than funds that invest more broadly.

Substantially all dividend income derived from tax-free funds is exempt from federal income tax. Some income may be subject to the federal alternative minimum tax (AMT) that applies to certain investors. Capital gains, if any, are taxable.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Investments has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding certain fees and expenses) from exceeding 0.55% of the Fund’s average daily net assets from Dec. 29, 2010, through Dec. 29, 2011. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | |||||

| Total annual operating expenses | 1.07 | % | 1.82 | % | 1.82 | % | ||

| (without fee waivers) | ||||||||

| Net expenses | 0.80 | % | 1.55 | % | 1.55 | % | ||

| (including fee waivers, if any) | ||||||||

| Type of waiver | Contractual | Contractual | Contractual | |||||

22

Performance of a $10,000 investment1

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

Average annual total returns from Aug. 31, 2001, through Aug. 31, 2011

| For period beginning Aug. 31, 2001, through Aug. 31, 2011 | Starting value | Ending value | ||

|

|

Barclays Capital Municipal Bond Index | $10,000 | $16,208 | |

|

|

Delaware Tax-Free New York Fund — Class A Shares | $9,550 | $15,253 | |

1 The “Performance of $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on Aug. 31, 2001, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 22. Please note additional details on pages 21 through 23.

The chart also assumes $10,000 invested in the Barclays Capital Municipal Bond Index as of Aug. 31, 2001. The Barclays Capital Municipal Bond Index measures the total return performance of the long-term, investment grade tax-exempt bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Nasdaq symbols | CUSIPs | ||||||

| Class A | FTNYX | 928928274 | |||||

| Class B | DVTNX | 928928266 | |||||

| Class C | DVFNX | 928928258 | |||||

23

Disclosure of Fund expenses

For the six-month period from March 1, 2011 to August 31, 2011

For the six-month period from March 1, 2011 to August 31, 2011

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. These following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from March 1, 2011 to August 31, 2011.

Actual expenses

The first section of the tables shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the tables shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Funds’ expenses shown in the tables reflect fee waivers in effect. The expenses shown in each table assume reinvestment of all dividends and distributions.

24

Delaware Tax-Free Arizona Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | ||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | |||||||||||

| 3/1/11 | 8/31/11 | Expense Ratio | 3/1/11 to 8/31/11* | |||||||||||

| Actual Fund return | ||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,056.30 | 0.84% | $ | 4.35 | |||||||

| Class B | 1,000.00 | 1,051.40 | 1.59% | 8.22 | ||||||||||

| Class C | 1,000.00 | 1,052.20 | 1.59% | 8.22 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | ||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.97 | 0.84% | $ | 4.28 | |||||||

| Class B | 1,000.00 | 1,017.19 | 1.59% | 8.08 | ||||||||||

| Class C | 1,000.00 | 1,017.19 | 1.59% | 8.08 | ||||||||||

Delaware Tax-Free California Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | |||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||

| 3/1/11 | 8/31/11 | Expense Ratio | 3/1/11 to 8/31/11* | ||||||||||||

| Actual Fund return | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,074.50 | 0.82 | % | $ | 4.29 | |||||||

| Class B | 1,000.00 | 1,069.30 | 1.57 | % | 8.19 | ||||||||||

| Class C | 1,000.00 | 1,069.50 | 1.57 | % | 8.19 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,021.07 | 0.82 | % | $ | 4.18 | |||||||

| Class B | 1,000.00 | 1,017.29 | 1.57 | % | 7.98 | ||||||||||

| Class C | 1,000.00 | 1,017.29 | 1.57 | % | 7.98 | ||||||||||

Delaware Tax-Free Colorado Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | |||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||

| 3/1/11 | 8/31/11 | Expense Ratio | 3/1/11 to 8/31/11* | ||||||||||||

| Actual Fund return | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,059.80 | 0.84 | % | $ | 4.36 | |||||||

| Class B | 1,000.00 | 1,055.80 | 1.59 | % | 8.24 | ||||||||||

| Class C | 1,000.00 | 1,055.70 | 1.59 | % | 8.24 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.97 | 0.84 | % | $ | 4.28 | |||||||

| Class B | 1,000.00 | 1,017.19 | 1.59 | % | 8.08 | ||||||||||

| Class C | 1,000.00 | 1,017.19 | 1.59 | % | 8.08 | ||||||||||

25

Disclosure of Fund expenses

Delaware Tax-Free Idaho Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | |||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||

| 3/1/11 | 8/31/11 | Expense Ratio | 3/1/11 to 8/31/11* | ||||||||||||

| Actual Fund return | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,054.10 | 0.88 | % | $ | 4.56 | |||||||

| Class B | 1,000.00 | 1,050.20 | 1.63 | % | 8.42 | ||||||||||

| Class C | 1,000.00 | 1,050.20 | 1.63 | % | 8.42 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,020.77 | 0.88 | % | $ | 4.48 | |||||||

| Class B | 1,000.00 | 1,016.99 | 1.63 | % | 8.29 | ||||||||||

| Class C | 1,000.00 | 1,016.99 | 1.63 | % | 8.29 | ||||||||||

Delaware Tax-Free New York Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | |||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | ||||||||||||

| 3/1/11 | 8/31/11 | Expense Ratio | 3/1/11 to 8/31/11* | ||||||||||||

| Actual Fund return | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,059.40 | 0.80 | % | $ | 4.15 | |||||||

| Class B | 1,000.00 | 1,056.50 | 1.55 | % | 8.03 | ||||||||||

| Class C | 1,000.00 | 1,056.50 | 1.55 | % | 8.03 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | |||||||||||||||

| Class A | $ | 1,000.00 | $ | 1,021.17 | 0.80 | % | $ | 4.08 | |||||||

| Class B | 1,000.00 | 1,017.39 | 1.55 | % | 7.88 | ||||||||||

| Class C | 1,000.00 | 1,017.39 | 1.55 | % | 7.88 | ||||||||||

*“Expenses Paid During Period” are equal to the relevant Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

26

| Security type/sector allocations Delaware Tax-Free Arizona Fund |

As of August 31, 2011 |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds | 98.42 | % |

| Corporate Revenue Bonds | 8.50 | % |

| Education Revenue Bonds | 12.08 | % |

| Electric Revenue Bonds | 3.94 | % |

| Healthcare Revenue Bonds | 16.63 | % |

| Lease Revenue Bonds | 11.24 | % |

| Local General Obligation Bonds | 5.96 | % |

| Pre-Refunded Bonds | 3.16 | % |

| Special Tax Revenue Bonds | 14.14 | % |

| State & Territory General Obligation Bonds | 6.75 | % |

| Transportation Revenue Bonds | 6.22 | % |

| Water & Sewer Revenue Bonds | 9.80 | % |

| Total Value of Securities | 98.42 | % |

| Receivables and Other Assets Net of Liabilities | 1.58 | % |

| Total Net Assets | 100.00 | % |

27

| Security type/sector allocations Delaware Tax-Free California Fund |

As of August 31, 2011 |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds | 98.42 | % |

| Corporate Revenue Bonds | 7.75 | % |

| Education Revenue Bonds | 9.36 | % |

| Electric Revenue Bonds | 7.75 | % |

| Healthcare Revenue Bonds | 12.61 | % |

| Housing Revenue Bonds | 5.81 | % |

| Lease Revenue Bonds | 7.23 | % |

| Local General Obligation Bonds | 8.83 | % |

| Pre-Refunded Bonds | 3.90 | % |

| Resource Recovery Revenue Bond | 1.24 | % |

| Special Tax Revenue Bonds | 17.42 | % |

| State & Territory General Obligation Bonds | 9.07 | % |

| Transportation Revenue Bonds | 3.34 | % |

| Water & Sewer Revenue Bonds | 4.11 | % |

| Short-Term Investment | 0.71 | % |

| Total Value of Securities | 99.13 | % |

| Receivables and Other Assets Net of Liabilities | 0.87 | % |

| Total Net Assets | 100.00 | % |

28

| Delaware Tax-Free Colorado Fund | As of August 31, 2011 |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds | 99.09 | % |

| Corporate Revenue Bond | 1.16 | % |

| Education Revenue Bonds | 8.58 | % |

| Electric Revenue Bonds | 9.48 | % |

| Healthcare Revenue Bonds | 24.84 | % |

| Housing Revenue Bonds | 2.86 | % |

| Lease Revenue Bonds | 2.27 | % |

| Local General Obligation Bonds | 14.65 | % |

| Pre-Refunded Bonds | 10.91 | % |

| Special Tax Revenue Bonds | 10.76 | % |

| State & Territory General Obligation Bonds | 7.87 | % |

| Transportation Revenue Bonds | 5.11 | % |

| Water & Sewer Revenue Bonds | 0.60 | % |

| Short-Term Investment | 0.06 | % |

| Total Value of Securities | 99.15 | % |

| Receivables and Other Assets Net of Liabilities | 0.85 | % |

| Total Net Assets | 100.00 | % |

29

| Security type/sector allocations Delaware Tax-Free Idaho Fund |

As of August 31, 2011 |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds | 98.67 | % |

| Corporate Revenue Bonds | 5.99 | % |

| Education Revenue Bonds | 10.78 | % |

| Electric Revenue Bonds | 5.08 | % |

| Healthcare Revenue Bonds | 5.97 | % |

| Housing Revenue Bonds | 4.11 | % |

| Lease Revenue Bonds | 7.10 | % |

| Local General Obligation Bonds | 21.56 | % |

| Pre-Refunded Bonds | 5.05 | % |

| Special Tax Revenue Bonds | 14.97 | % |

| State General Obligation Bonds | 7.09 | % |

| Transportation Revenue Bonds | 8.51 | % |

| Water & Sewer Revenue Bonds | 2.46 | % |

| Short-Term Investments | 2.03 | % |

| Total Value of Securities | 100.70 | % |

| Liabilities Net of Receivables and Other Assets | (0.70 | %) |

| Total Net Assets | 100.00 | % |

30

| Delaware Tax-Free New York Fund | As of August 31, 2011 |

Sector designations may be different than the sector designations presented in other Fund materials.

| Security type/sector | Percentage of net assets | |

| Municipal Bonds | 98.08 | % |

| Corporate Revenue Bonds | 9.51 | % |

| Education Revenue Bonds | 26.53 | % |

| Electric Revenue Bonds | 3.69 | % |

| Healthcare Revenue Bonds | 11.70 | % |

| Housing Revenue Bonds | 1.42 | % |

| Lease Revenue Bonds | 6.73 | % |

| Local General Obligation Bonds | 5.71 | % |

| Pre-Refunded Bonds | 2.80 | % |

| Special Tax Revenue Bonds | 15.69 | % |

| State & Territory General Obligation Bonds | 5.55 | % |

| Transportation Revenue Bonds | 6.72 | % |

| Water & Sewer Revenue Bonds | 2.03 | % |

| Total Value of Securities | 98.08 | % |

| Receivables and Other Assets Net of Liabilities | 1.92 | % |

| Total Net Assets | 100.00 | % |

31

| Statements of net assets | |

| Delaware Tax-Free Arizona Fund | August 31, 2011 |

| Principal amount | Value | |||||

| Municipal Bonds – 98.42% | ||||||

| Corporate Revenue Bonds – 8.50% | ||||||

| Maricopa County Pollution Control (Palo Verde Project) | ||||||

| Series A 5.05% 5/1/29 (AMBAC) | $ | 2,000,000 | $ | 2,005,700 | ||

| •Series B 5.20% 6/1/43 | 1,500,000 | 1,551,015 | ||||

| • | Navajo County Pollution Control Revenue | |||||

| (Arizona Public Services-Cholla) | ||||||

| Series D 5.75% 6/1/34 | 1,500,000 | 1,713,600 | ||||

| Pima County Industrial Development Authority Pollution | ||||||

| Control Revenue (Tucson Electric Power San Juan) | ||||||

| 5.75% 9/1/29 | 750,000 | 759,990 | ||||