|

o

|

Preliminary Proxy Statement

|

|

o

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

|

|

o

|

Definitive Proxy Statement

|

|

o

|

Definitive Additional Materials

|

|

x

|

Soliciting Material Pursuant to §240.14a-12

|

|

x

|

Fee not required.

|

|

o

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

|

|

(1)

|

Title of each class of securities to which transaction applies:

|

|

(2)

|

Aggregate number of securities to which transaction applies:

|

|

(3)

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

|

|

(4)

|

Proposed maximum aggregate value of transaction:

|

|

(5)

|

Total fee paid:

|

|

o

|

Fee paid previously with preliminary materials.

|

|

o

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

|

|

(1)

|

Amount Previously Paid:

|

|

(2)

|

Form, Schedule or Registration Statement No.:

|

|

(3)

|

Filing Party:

|

|

(4)

|

Date Filed:

|

Presentation to ISS Opposing the Proposed Dell Take-Private Transaction June 24, 2013 Southern Asset Management, Inc. Advisor to Longleaf Partners Funds

The Case for Protecting Stockholders o Evercore Partners, the advisor to the Board's Special Committee, has reported to the board of Dell that, based on projections by the Boston Consulting Group, the advisor to Dell, Silver Lake could realize an average annualized rate of return of up to 44.7% and Michael Dell could realize an average annualized rate of return of up to 50.1%(1) during the next 4 to 5 years on their investment in the Michael Dell/Silver Lake take-private transaction now presented for stockholder consideration and action at the special meeting of Dell stockholders on July 18. o In light of the Boston Consulting Group projections and Evercore estimates, Icahn and Southeastern believe the board of directors of Dell should have acted to secure those gains for stockholders. Instead, it agreed to a break-up fee of up to $450 million and a protective Merger Agreement for the Michael Dell/Silver Lake transaction, which have the effect of dampening third-party interest in Dell and which Icahn and Southeastern view as highly inappropriate under the circumstances. o Icahn and Southeastern believe that it would be a sad outcome for stockholders and would reflect poorly on all who are involved in this process if, after purchasing shares at what Icahn and Southeastern perceive to be a substantially undervalued price, Michael Dell and Silver Lake earned Evercore's estimated returns on their investment and that it would be even worse if Dell were sold (or broken up) by Michael Dell and Silver Lake in a transaction or transactions with one or more strategic acquirers in the near future and for a very large profit. o Icahn and Southeastern believe the board could have done more - much more - to afford stockholders an opportunity to achieve the very same gains now pursued by Michael Dell and Silver Lake. However, Dell instead appears to be engaging in a campaign to highlight Dell's bleak outlook in the PC market, obscuring the robust performance and future of the ~$13 billion in acquisitions Dell has made in recent years, which were paid for by Dell's current owners. Icahn and Southeastern believe that Dell is conducting this campaign to prompt stockholders into supporting what Icahn and Southeastern believe is a bad deal for stockholders and a very good deal for Michael Dell and Silver Lake. o It is interesting to note that, in the recent past, rather than emphasize the negatives of the PC business, Dell has highlighted the strengths of the Enterprise Solutions business - accelerated growth, strong margins, and recurring revenues. We look forward to the results of the discovery in the current stockholder action against Dell to better understand the financial outlook that Michael Dell/Silver Lake are sharing with lenders in comparison to the dire picture they are now painting for stockholders. o Icahn and Southeastern believe that Dell's owners deserve better and can achieve more by voting against the Michael Dell/Silver Lake transaction and by electing new directors who will act to secure for stockholders the very same gains that Michael Dell and Silver Lake hope to lock in for themselves. (1) Evercore Partners 2/4/13 presentation to the Board.

Overview We believe the take-private transaction substantially undervalues Dell while superior alternatives exist. o Michael Dell and Silver Lake would not pursue a take-private transaction unless they thought it was a good deal for them (3d right arrow) Silver Lake has delivered a gross IRR of 27% since inception(1) o Icahn and Southeastern believe that: 1. The take-private transaction substantially undervalues the Company 2. The Enterprise Solutions Group (ESG) and Dell Services businesses are the future of Dell 3. Stockholders have funded the Company's turnaround and should be given the opportunity to benefit from their investment o Icahn and Southeastern believe that the sale process could not maximize value: 1. A go-shop process seldom results in a superior proposal in management-led buyouts 2. The Merger Agreement's restrictive definition of a "superior proposal" would exclude most, if not all, leveraged recapitalization transactions, despite the fact that such transactions could be economically superior and would give stockholders the option of sharing in the Company's future (1) Reuters article 4/18/13, Silver Lake Raises $10.3 Billion Private Equity Fund.

Dell’s Strategic Rationale

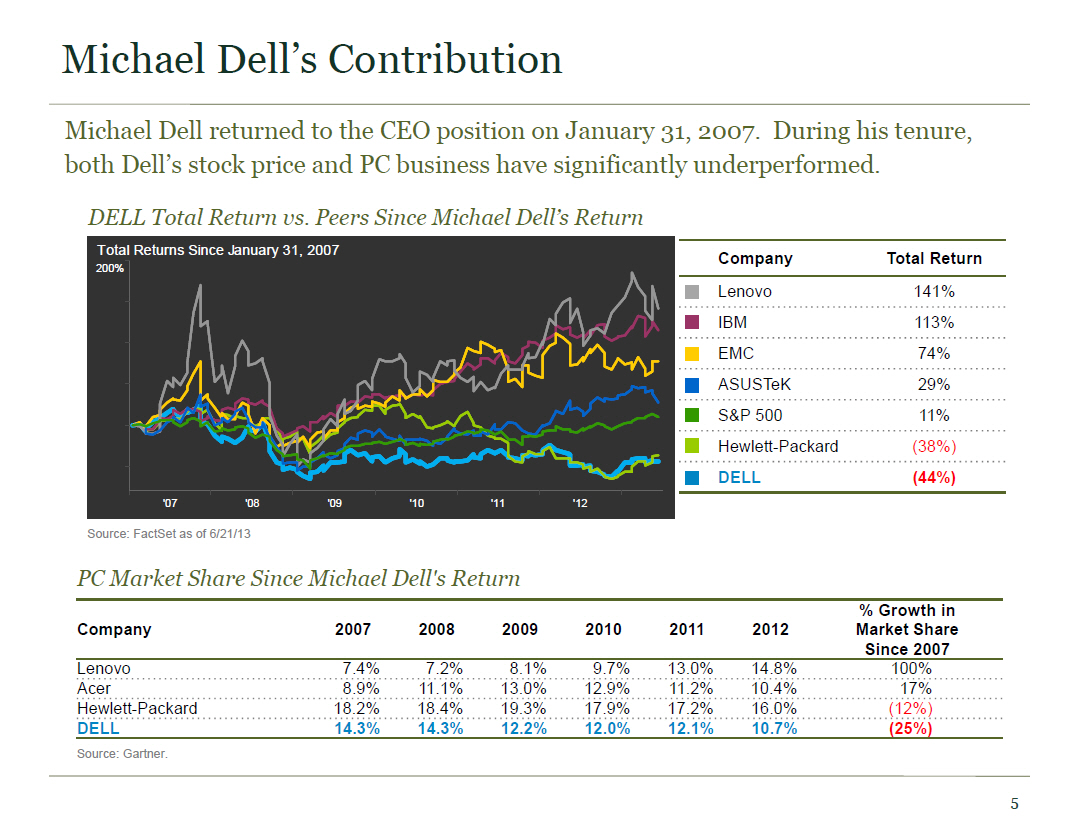

Michael Dell's Contribution Michael Dell returned to the CEO position on January 31, 2007. During his tenure, both Dell's stock price and PC business have significantly underperformed. DELL Total Return vs. Peers Since Michael Dell's Return Total Returns Since January 31, 2007 200% Company Total Return Lenovo 141% IBM 113% EMC 74% ASUSTeK 29% S&P 500 11% Hewlett-Packard (38%) DELL (44%) '07 '08 '09 '10 '11 '12 Source: FactSet as of 6/21/13 PC Market Share Since Michael Dell's Return % Growth in Company 2007 2008 2009 2010 2011 2012 Market Share Since 2007 Lenovo 7.4% 7.2% 8.1% 9.7% 13.0% 14.8% 100% Acer 8.9% 11.1% 13.0% 12.9% 11.2% 10.4% 17% Hewlett-Packard 18.2% 18.4% 19.3% 17.9% 17.2% 16.0% (12%) DELL 14.3% 14.3% 12.2% 12.0% 12.1% 10.7% (25%) Source: Gartner.

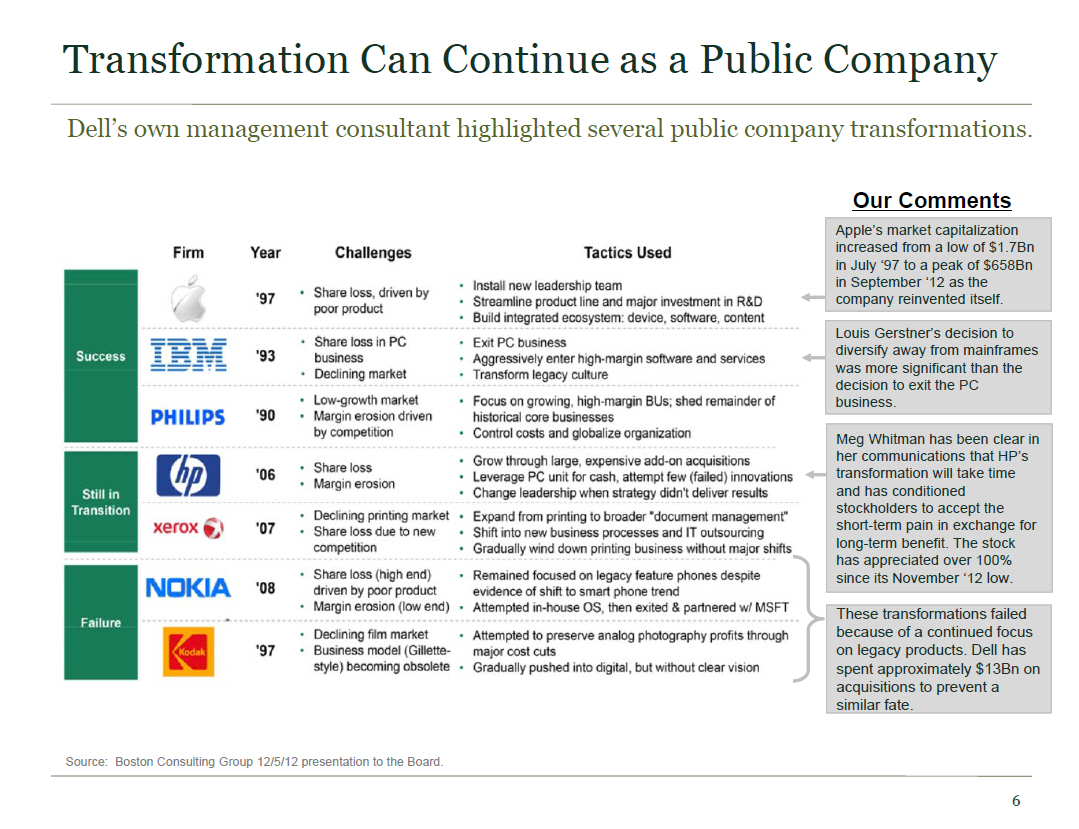

Dell's own management consultant highlighted several public company transformations. Our Comments Apple's market capitalization increased from a low of $1.7Bn in July '97 to a peak of $658Bn in September '12 as the company reinvented itself. Louis Gerstner's decision to diversify away from mainframes was more significant than the decision to exit the PC business. Meg Whitman has been clear in her communications that HP's transformation will take time and has conditioned stockholders to accept the short-term pain in exchange for long-term benefit. The stock has appreciated over 100% since its November '12 low. These transformations failed because of a continued focus on legacy products. Dell has spent approximately $13Bn on acquisitions to prevent a similar fate. Source: Boston Consulting Group 12/5/12 presentation to the Board. Transformation Can Continue as a Public Company Success Still in Transition Failure Firm Year Challenges Tactics Used '97 '93 '90 '06 '07 '08 '97 Share loss, driven by poor product Install new leadership team Streamline product line and major investment in R&D Build integrated ecosystem; device, software, content Share loss in PC business Declining market Exit PC business Aggressively enter high-margin software and services Transform legacy culture Low-growth market Margin erosion driven by competition Focus on growing, high-margin BUs; shed remainder of historical core businesses Control costs and globalize organization Share loss Margin erosion Grow through large, expensive add-on acquisitions Leverage PC unit for cash, attempt few (failed) innovations Change leadership when strategy didn't deliver results Declining printing market Share loss due to new competition Expand from printing to broader "document management" Shift into new business processes and IT outsourcing Gradually wind down printing business without major shifts Share loss (high end) driven by poor product Margin erosion (low end) Attempted in-house OS, then exited & partnered w/MSFT Declining film market Business model (Gillette-style) becoming obsolete Attempted to preserve analog photography profits through major cost cuts Gradually pushed into digital, but without clear vision

Dell's Strategic Rationale Dell's own management consultant found little strategic rationale to take Dell private. Believe many of the "take-private" value levers could (in principle) be applicable to Dellas public company Potential value levers Description Applicable to public? A "Commit to win" in Core Denali 8 Drive organic growth in New Denali o Maximize life cycle cash flow, not margin percent Drive share to preserve scale (e.g.$450 product, Tier 4-6 Ch1na,etc) Move decision making center of organization to Asia o Integrate products to create differentiated solution for clients o Increase focus on advantaged mid-market segment o Segment and upgrade selling organization, build solutions approach C Implement aggressive cost takeout Aggressivelyimplement simplification and cost take-out (NDBM) Program-manage large-scale cost reduction programs Delayer the organization D Align org and talent o Create COO,recruit I change senior talent to align with strategy o Align external reporting with internal roles, resourcing,and metrics o Drive strong execution discipline,with focus on the "6-8 key priorities" E Tightly align management incentives F Ensure discipline of capital allocation G Enhance capital strategy o Remove quarterly EPS constraint, drive towards 3-6 yr exit profile ? o Require mgt purchase of equity (money at risk,not options) ? o Revisit M&A activity - ensure clear investment thesis for acquisition o Drive Integration of existing acquisitions o Increase debt leverage to boost equity returns ? o Access OUS cash tax-efficiently o Arbitrage valuation multiple (buy low,sell h1gh) Source: Boston Consulting Group 12/5/12 presentation to the Board.

Questions to Dell's Stockholders o Do Dell's owners need the Board or Michael Dell to protect them from the risks of an alternative transaction as proposed by Icahn and Southeastern(1), or do Dell's owners need to protect themselves from an opportunistic purchase by Michael Dell and Silver Lake? o We find it difficult to believe that Dell's owners - including many of the world's leading institutional investors, hedge funds and other sophisticated investors - are incapable of absorbing the risks associated with a conservatively leveraged balance sheet, when Michael Dell and Silver Lake are eagerly seeking to do just that and much more. o Why is the Board pushing a deal that would force stockholders to sell their shares at what Icahn and Southeastern perceive to be a substantially undervalued price? Haven't Dell's owners earned the right to share in the substantial potential returns on investment estimated by Evercore for Michael Dell and Silver Lake? (1) Any alternative proposal by Icahn and Southeastern would be contingent upon the proposed take-private transaction being defeated, the election of a new Dell Board of Directors, and approval by that new Board.

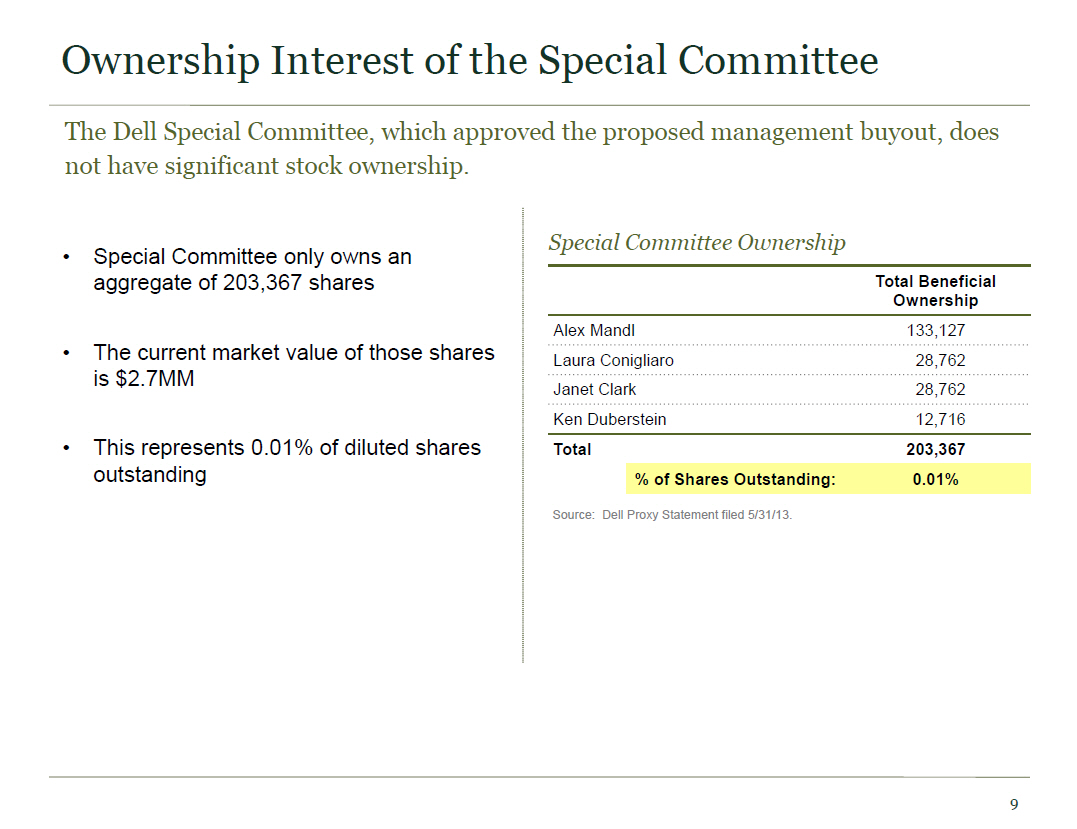

Ownership Interest of the Special Committee The Dell Special Committee, which approved the proposed management buyout, does not have significant stock ownership. o Special Committee only owns an aggregate of 203,367 shares Special Committee Ownership Total Beneficial Ownership o The current market value of those shares is $2.7MM o This represents 0.01% of diluted shares outstanding Alex Mandl 133,127 Laura Conigliaro 28,762 Janet Clark 28,762 Ken Duberstein 12,716 Total 203,367 % of Shares Outstanding: 0.01% Source: Dell Proxy Statement filed 5/31/13.

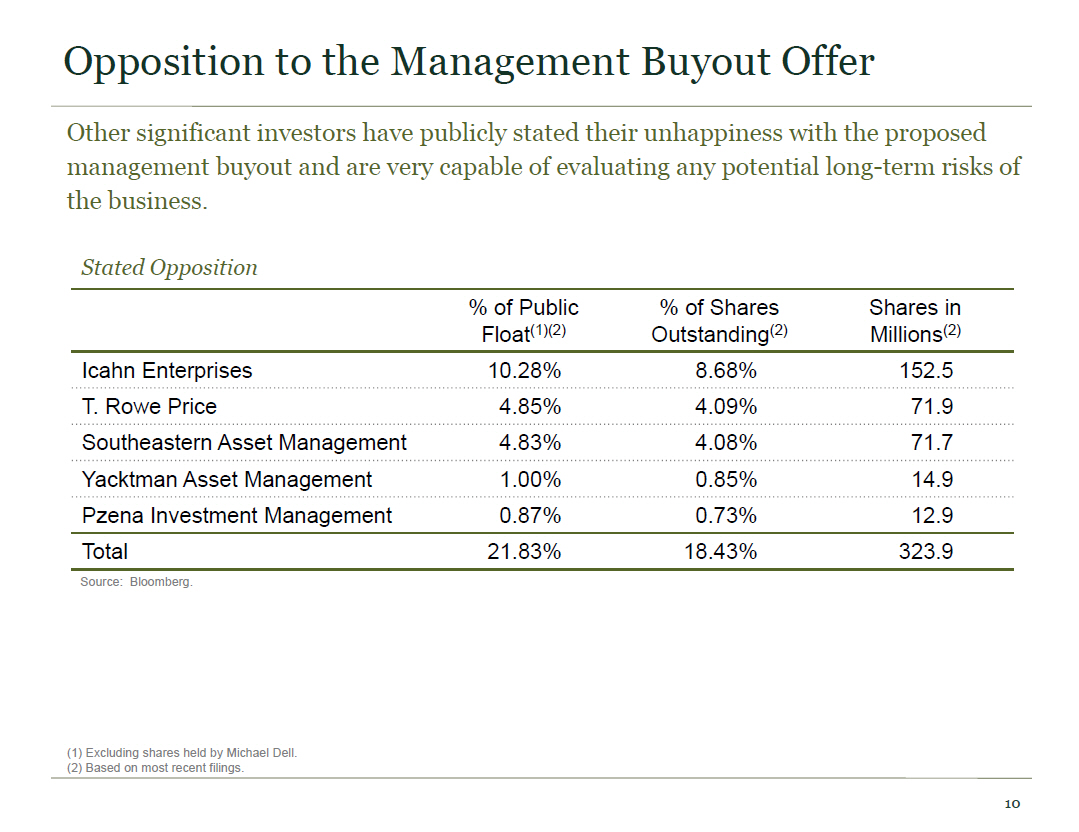

Opposition to the Management Buyout Offer Other significant investors have publicly stated their unhappiness with the proposed management buyout and are very capable of evaluating any potential long-term risks of the business. Icahn Enterprises 10.28% 8.68% 152.5 T. Rowe Price 4.85% 4.09% 71.9 Southeastern Asset Management 4.83% 4.08% 71.7 Yacktman Asset Management 1.00% 0.85% 14.9 Pzena Investment Management 0.87% 0.73% 12.9 Total 21.83% 18.43% 323.9 Source: Bloomberg. Stated Opposition (1) Excluding shares held by Michael Dell. (2) Based on most recent filings. % of Public Float(1)(2) % of Shares Outstanding(2) Shares in Millions(2)

The Case for Dell's Future 11

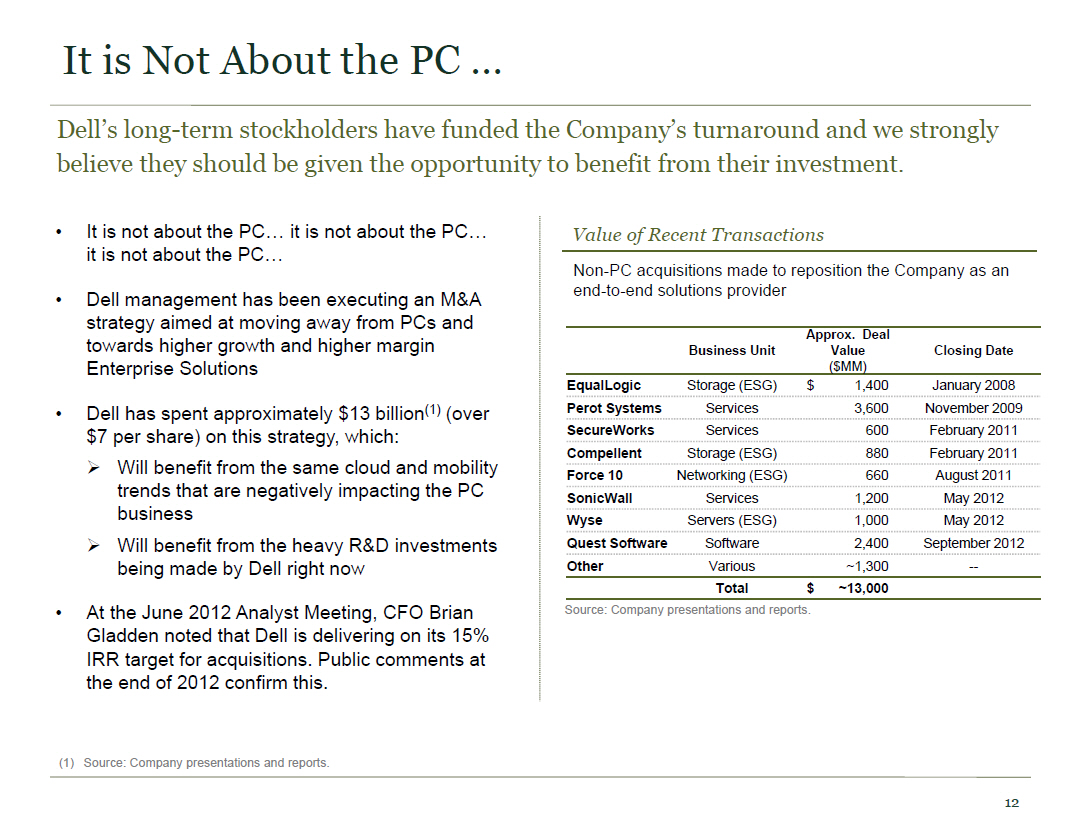

It is Not About the PC Dell's long-term stockholders have funded the Company's turnaround and we strongly believe they should be given the opportunity to benefit from their investment. o It is not about the PC... it is not about the PC... it is not about the PC... o Dell management has been executing an M&A strategy aimed at moving away from PCs and Value of Recent Transactions Non-PC acquisitions made to reposition the Company as an end-to-end solutions provider Approx. Deal towards higher growth and higher margin Business Unit Value Closing Date Enterprise Solutions o Dell has spent approximately $13 billion(1) (over $7 per share) on this strategy, which: (3d right arrow) Will benefit from the same cloud and mobility trends that are negatively impacting the PC business (3d right arrow) Will benefit from the heavy R&D investments being made by Dell right now o At the June 2012 Analyst Meeting, CFO Brian Gladden noted that Dell is delivering on its 15% IRR target for acquisitions. Public comments at the end of 2012 confirm this. ($MM) EqualLogic Storage (ESG) $ 1,400 January 2008 Perot Systems Services 3,600 November 2009 SecureWorks Services 600 February 2011 Compellent Storage (ESG) 880 February 2011 Force 10 Networking (ESG) 660 August 2011 SonicWall Services 1,200 May 2012 Wyse Servers (ESG) 1,000 May 2012 Quest Software Software 2,400 September 2012 Other Various ~1,300 -- Total $ ~13,000 Source: Company presentations and reports. (1) Source: Company presentations and reports.

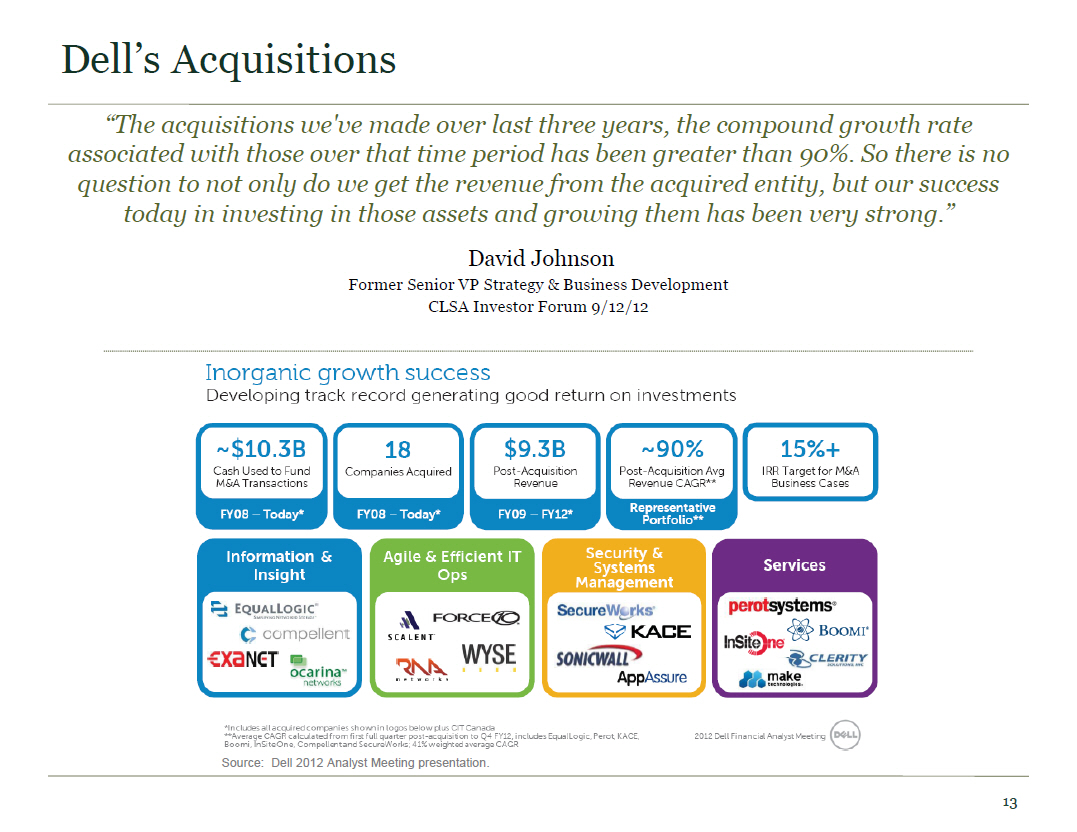

Dell's Acquisitions "The acquisitions we've made over last three years, the compound growth rate associated with those over that time period has been greater than 90%. So there is no question to not only do we get the revenue from the acquired entity, but our success today in investing in those assets and growing them has been very strong." David Johnson Former Senior VP Strategy & Business Development CLSA Investor Forum 9/12/12 Source: Dell 2012 Analyst Meeting presentation.

Enterprise Solutions(1) is the Future In our opinion, Michael Dell and his partners at Silver Lake want to capture the upside of the Company's recent strategic investments and growth initiatives in Enterprise Solutions. o In Q1, Enterprise Solutions accounted for 65% of segment operating income: (3d right arrow) Enterprise Solutions Group's operating income increased 71% (3d right arrow) Dell Services revenue grew 2% even as PC revenue declined 10% (3d right arrow) Enterprise Solutions accounted for 65% of operating income despite the fact that Dell Software reported a loss due to accounting associated with acquisitions: "In a public company the accounting rules associated with acquisitions are quite onerous. You have to take a lot of write-offs upfront, and basically take a haircut on the deferred income like maintenance revenue...That makes it very difficult for a software business acquisition to look profitable in the short term."(2) John Swainson, President Dell Software o We believe Enterprise Solutions will continue to contribute an outsized portion of Dell's operating income as compared to Enterprise Solutions' total revenue contribution o We believe that, at the completion of this transformation, Dell's future owners will realize valuation multiples significantly higher than those reflected in today's stock price due to the higher percentage of higher growth and higher margin non-PC earnings (1) Also known as NEW Dell. Includes the Enterprise Solutions Group, Dell Software, and Dell Services. (2) TechWeekEurope article 6/20/13, Software Will Make A Quarter of Dell's Profits - Swainson.

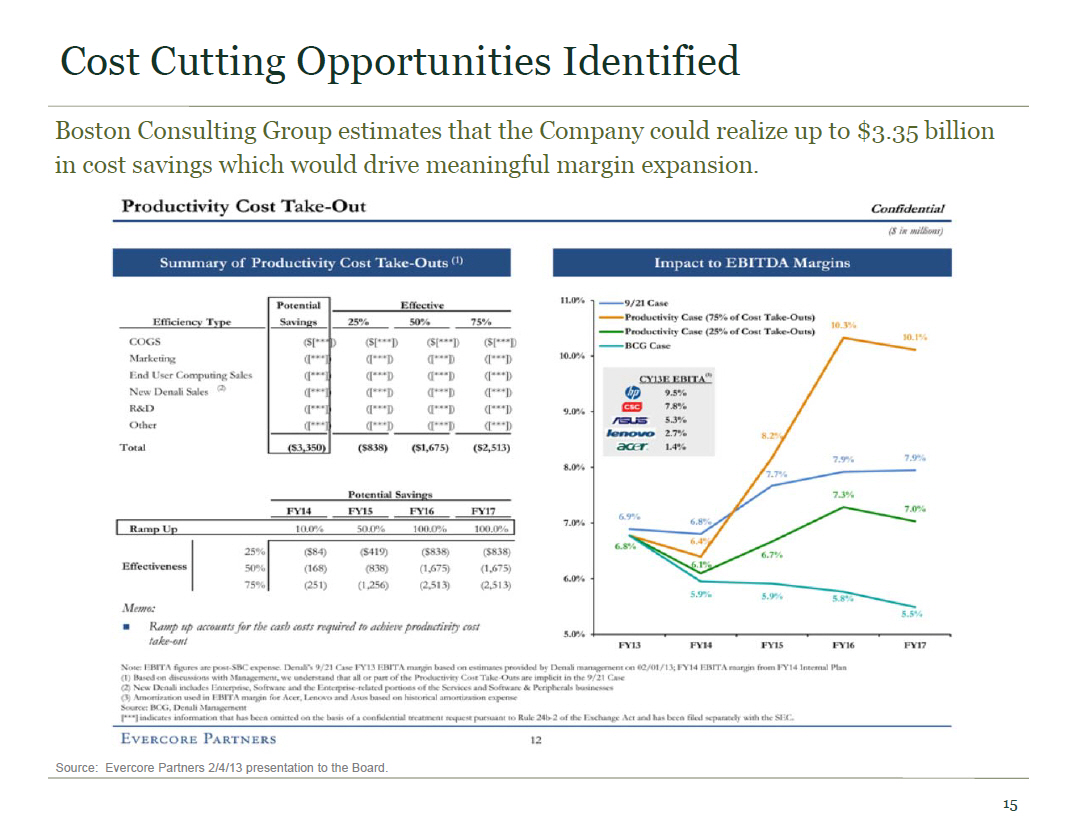

Productvity Cost Take-Out Confidential ($ in millions) Summary of Productivity Cost Take-Outs(1) Impact to EBITDA Margins Efficiency Type Potential Savings Effective 25% 50% 75% COGS Marketing End User Computing Sales New Denali Sales (2) Other Total ($3,350) ($838) ($1,675) ($2,513) Potential Savings FY14 FY15 FY16 FY 17 Ramp Up 10.0% 50.0% 100.0% 100.0% Effectiveness 25% ($84) ($419) ($838) ($838) 50% (168) (838) (1,675) (1,675) 75% (251) (1,256) (2,513) (2,513) Memo: Ramp up accounts for the cash costs requried to achieve productivity cost take-out Note: EBITA figures are post SBC expense. Denali managment on 02/01/13; FY14 EBITA margin from FY14 Internal Plan (1) Based on discussions with Managment, we understand that all or part of the Productivity Cost Take-Outs are implicit in the 9/21 Case (2) New Denali includes Enterprise, Sofeware and the Enterprise-related positions of the Servces and Sofeware & Peripherals businesses (3) Amorization used in EBITA margin for Acer, Lenovo and Asus based on historical amortization expense Source: BCG, Denali Managment [ ] indicates information that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Exchange Act and has been filed separtely with the SEC.

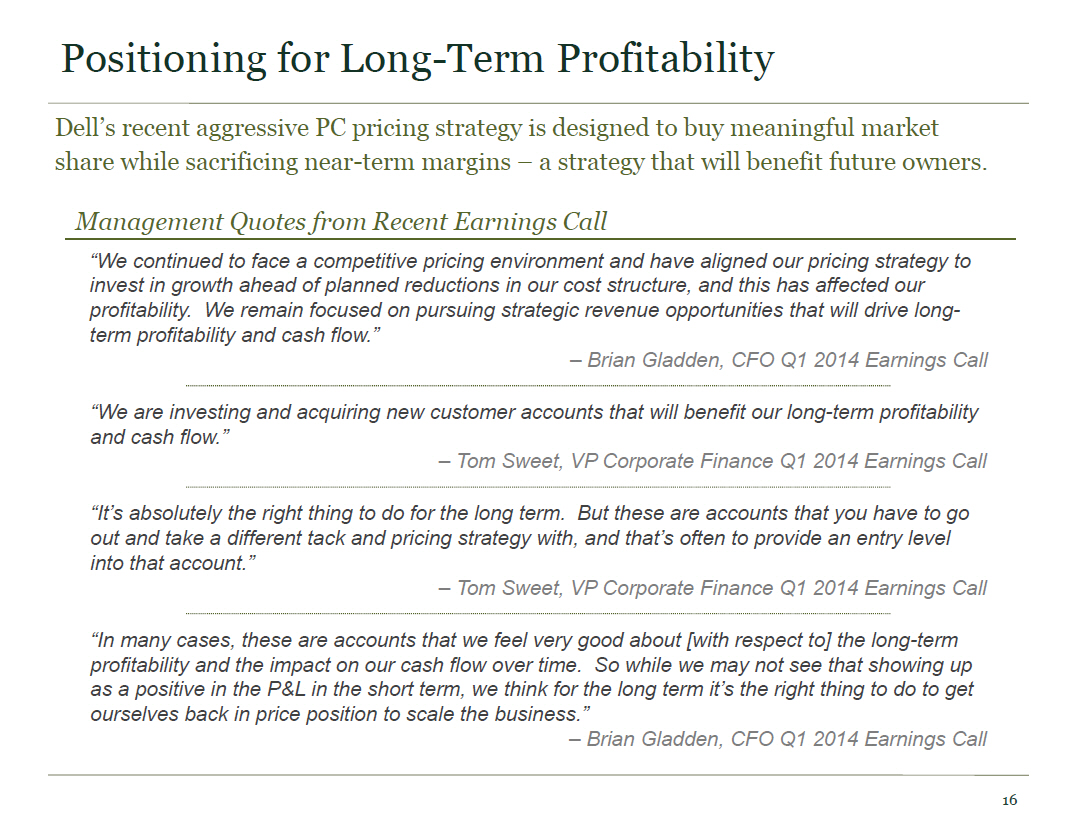

Positioning for Long-Term Profitability Dell's recent aggressive PC pricing strategy is designed to buy meaningful market share while sacrificing near-term margins - a strategy that will benefit future owners. Management Quotes from Recent Earnings Call "We continued to face a competitive pricing environment and have aligned our pricing strategy to invest in growth ahead of planned reductions in our cost structure, and this has affected our profitability. We remain focused on pursuing strategic revenue opportunities that will drive long- term profitability and cash flow." - Brian Gladden, CFO Q1 2014 Earnings Call "We are investing and acquiring new customer accounts that will benefit our long-term profitability and cash flow." - Tom Sweet, VP Corporate Finance Q1 2014 Earnings Call "It's absolutely the right thing to do for the long term. But these are accounts that you have to go out and take a different tack and pricing strategy with, and that's often to provide an entry level into that account." - Tom Sweet, VP Corporate Finance Q1 2014 Earnings Call "In many cases, these are accounts that we feel very good about [with respect to] the long-term profitability and the impact on our cash flow over time. So while we may not see that showing up as a positive in the P&L in the short term, we think for the long term it's the right thing to do to get ourselves back in price position to scale the business." - Brian Gladden, CFO Q1 2014 Earnings Call

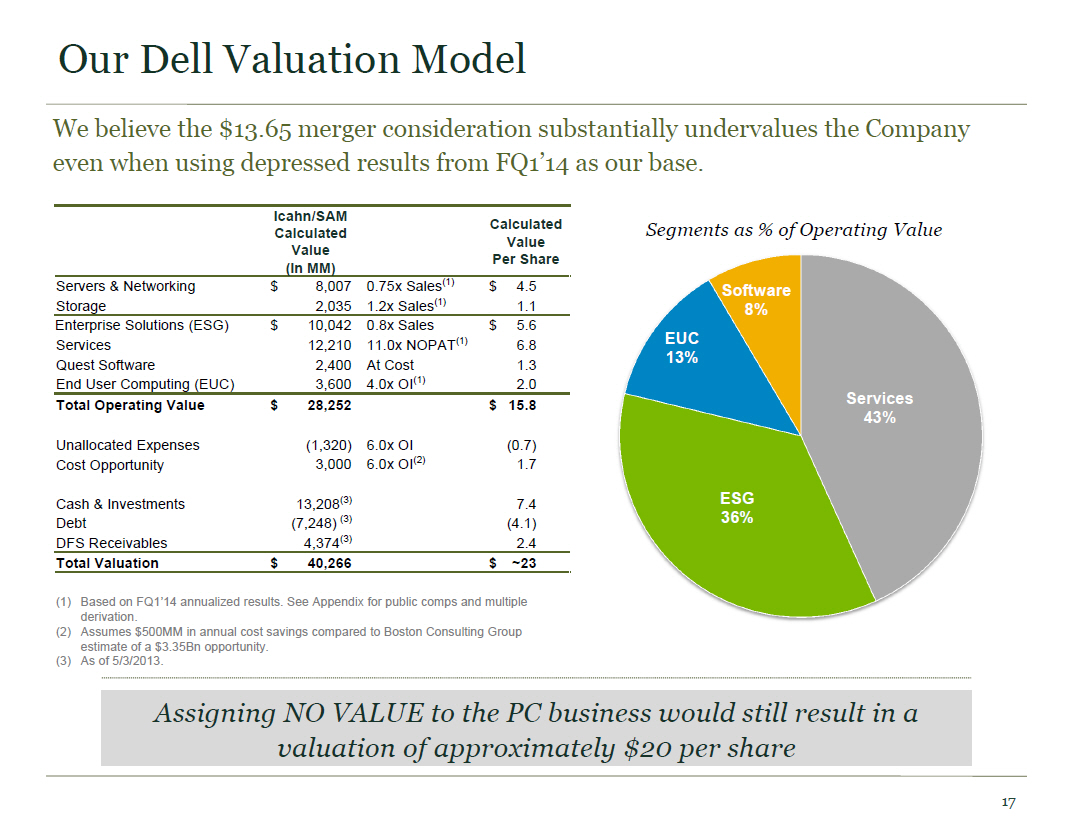

Our Dell Valuation Model We believe the $13.65 merger consideration substantially undervalues the Company even when using depressed results from FQ1'14 as our base. Icahn/SAM Calculated Calculated Value Value (In MM) Per Share Segments as % of Operating Value Servers & Networking $ 8,007 0.75x Sales(1) $ 4.5 Storage 2,035 1.2x Sales(1) 1.1 Enterprise Solutions (ESG) $ 10,042 0.8x Sales $ 5.6 Services 12,210 11.0x NOPAT(1) 6.8 Quest Software 2,400 At Cost 1.3 End User Computing (EUC) 3,600 4.0x OI(1) 2.0 Total Operating Value $ 28,252 $ 15.8 Unallocated Expenses (1,320) 6.0x OI (0.7) Cost Opportunity 3,000 6.0x OI(2) 1.7 Cash & Investments 13,208(3) 7.4 Debt (7,248) (3) (4.1) DFS Receivables 4,374(3) 2.4 Total Valuation $ 40,266 $ ~23 EUC 13% Software 8% ESG 36% Services (1) Based on FQ1'14 annualized results. See Appendix for public comps and multiple derivation. (2) Assumes $500MM in annual cost savings compared to Boston Consulting Group estimate of a $3.35Bn opportunity. (3) As of 5/3/2013. Assigning NO VALUE to the PC business would still result in a valuation of approximately $20 per share

Illustrative EPS of a Potential Dell Self Tender Alternative(1) Using Various Earnings Assumptions (1/2) A Dell self tender would be highly accretive and result in pro forma EPS significantly higher than current levels. Illustrative Example: 1,118MM Shares Tendered Earnings Case Assumed Adjusted Last Quarter BCG Base Case BCG 25% Case BCG 75% Case Annualized (FY'15) (FY'15) (FY'15) Non-GAAP Operating Income 2,800(2) 3,300(3) 3,700(3) 4,500(3) Less: Est. Foregone DFS Income (323) (250)(4) (250)(4) (250)(4) Less: Net Interest Expense(5) (556) (556) (556) (556) Pro Forma Pretax Income 1,921 2,494 2,894 3,694 Tender Offer $14 per share $14 per share $14 per share $14 per share Shares Tendered 1,118 1,118 1,118 1,118 Pro Forma Shares Outstanding 670 670 670 670 Pro Forma Pretax EPS $2.87 $3.72 $4.32 $5.51 (1) Any alternative proposal by Icahn and Southeastern would be contingent upon the proposed take-private transaction being defeated, the election of a new Dell Board of Directors, and approval by that new Board. (2) Assumes FQ'14 annualized non-GAAP operating income of $590MM adjusted for Dell Software's acquisition-accounting related loss. Assumes Dell Software operating income of $100MM, which is approximately equal to Quest Software's trailing twelve months operating income at the time of the acquisition. (3) Source: Dell Proxy Statement filed 5/31/13. (4) Assumes in FY'15 DES begins to rebuild receivables balance. (5) Assumes 5.5% cost of debt and 0.5% interest income.

Illustrative EPS of a Potential Dell Self Tender Alternative(1) Using Various Earnings Assumptions (2/2) Assuming only half of the $3,350MM cost opportunity identified by the Boston Consulting Group would further increase EPS. Illustrative Example: 1,118MM Shares Tendered Earnings Case Assumed Adjusted Last Quarter BCG Base Case Annualized (FY'15) Non-GAAP Operating Income 2,800(2) 3,300(3) Plus: Cost Savings(4) 1,675 1,675 Less: Est. Foregone DFS Income (323) (250)(5) Less: Net Interest Expense(6) (556) (556) Pro Forma Pretax Income 3,596 4,169 Tender Offer $14 per share $14 per share Shares Tendered 1,118 1,118 Pro Forma Shares Outstanding 670 670 Pro Forma Pretax EPS $5.37 $6.22 (1) Any alternative proposal by Icahn and Southeastern would be contingent upon the proposed take-private transaction being defeated, the election of a new Dell Board of Directors, and approval by that new Board. (2) Assumes FQ'14 annualized non-GAAP operating income of $590MM adjusted for Dell Software's acquisition-accounting related loss. Assumes Dell Software operating income of $100MM, which is approximately equal to Quest Software's trailing twelve months operating income at the time of the acquisition. (3) Source: Dell Proxy Statement filed 5/31/13. (4) Assumes half of the $3,350MM cost opportunity estimated by the Boston Consulting Group. (5) Assumes in FY'15 DES begins to rebuild receivables balance. (6) Assumes 5.5% cost of debt and 0.5% interest income.

Reasonable Utilization of the Balance Sheet Icahn and Southeastern's Dell self tender proposal(1) could comfortably be financed utilizing Dell's balance sheet. o Under the Michael Dell/Silver Lake Proposal, the Net Debt/EBITDA multiple is approximately 3.7x(2) o Under Icahn and Southeastern's Dell self tender proposal, the maximum pro forma Net Debt/EBITDA multiple is 1.7x o Michael Dell claims that our proposal for a Dell self tender would restrict the Company's financial flexibility and jeopardize customer perception and employee retention(3). However, a Dell self tender proposal would result in a maximum leverage multiple of 1.7x as opposed to the 3.7x leverage multiple under the proposed Michael Dell/Silver Lake take-private transaction Pro Forma Leverage # Of Shares Tendered (MM) Pro Forma Gross Debt ($MM) Pro Forma Cash ($MM) Pro Forma Net Debt ($MM) Pro Forma Net Debt/EBITDA(4) 875 7,025 4,900 2,125 0.7x 1,000 8,838 4,900 3,938 1.2x 1,118 10,547 4,900 5,647 1.7x (1) Any alternative proposal by Icahn and Southeastern would be contingent upon the proposed take-private transaction being defeated, the election of a new Dell Board of Directors, and approval by that new Board. (2) Assumes FY'14 Final Board Case EBITDA of $3.6Bn and pro forma net debt for the Michael Dell/Silver Lake transaction. (3) Dell materials filed 6/21/13. (4) Assumes Final FY'14 Board Case EBITDA of $3.3Bn, which is pro forma for loss of DFS income.

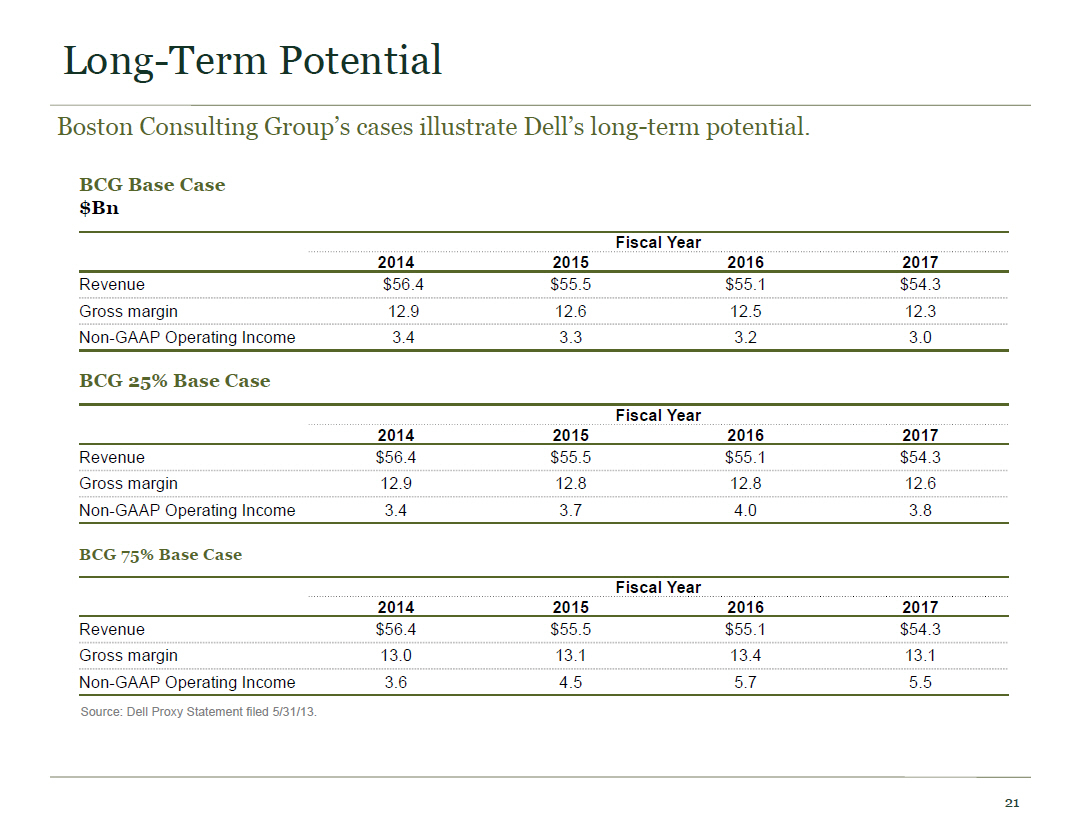

Long-Term Potential Boston Consulting Group's cases illustrate Dell's long-term potential. BCG Base Case $Bn Fiscal Year 2014 2015 2016 2017 Revenue $56.4 $55.5 $55.1 $54.3 Gross margin 12.9 12.6 12.5 12.3 Non-GAAP Operating Income 3.4 3.3 3.2 3.0 BCG 25% Base Case Fiscal Year 2014 2015 2016 2017 $56.4 $55.5 $55.1 $54.3 Revenue Gross margin 12.9 12.8 12.8 12.6 Non-GAAP Operating Income 3.4 3.7 4.0 3.8 BCG 75% Base Case Fiscal Year 2014 2015 2016 2017 Revenue $56.4 $55.5 $55.1 $54.3 Gross margin 13.0 13.1 13.4 13.1 Non-GAAP Operating Income 3.6 4.5 5.7 5.5 Source: Dell Proxy Statement filed 5/31/13.

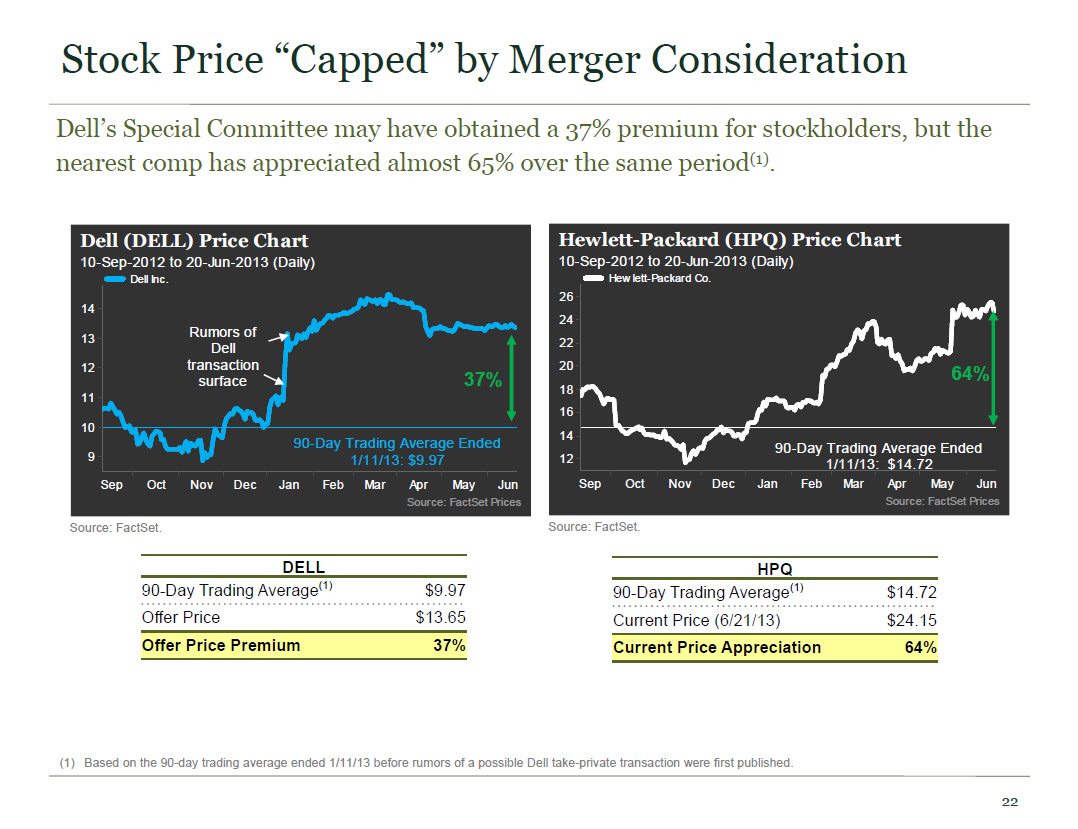

Stock Price "Capped" by Merger Consideration Dell's Special Committee may have obtained a 37% premium for stockholders, but the nearest comp has appreciated almost 65% over the same period(1). Dell (DELL) Price Chart 10-Sep-2012 to 20-Jun-2013 (Daily) Dell Inc. Hewlett-Packard (HPQ) Price Chart 10-Sep-2012 to 20-Jun-2013 (Daily) Hew lett-Packard Co. Rumors of transaction surface 90-Day Trading Average Ended 1/11/13: $9.97 90-Day Trading Average Ended 1/11/13: $14.72 Source: FactSet Prices Source: FactSet Prices Source: FactSet. Source: FactSet. DELL 90-Day Trading Average(1) $9.97 Offer Price $13.65 Offer Price Premium 37% HPQ 90-Day Trading Average(1) $14.72 Current Price (6/21/13) $24.15 Current Price Appreciation 64% (1) Based on the 90-day trading average ended 1/11/13 before rumors of a possible Dell take-private transaction were first published.

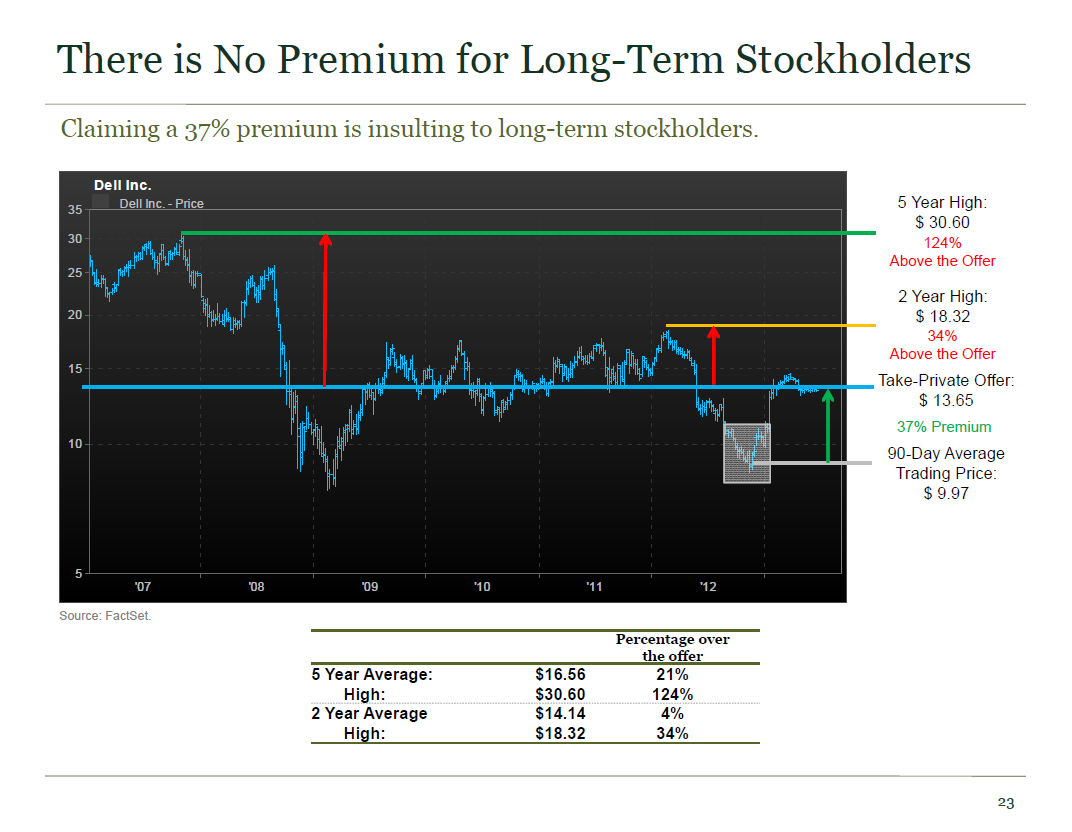

There is No Premium for Long-Term Stockholders Claiming a 37% premium is insulting to long-term stockholders. Dell Inc. - Price 5 Year High: $ 30.60 124% Above the Offer 2 Year High: $ 18.32 34% Above the Offer Take-Private Offer: $ 13.65 37% Premium 90-Day Average Trading Price: $ 9.97 Source: FactSet. Percentage over the offer 5 Year Average: $16.56 21% High: $30.60 124% 2 Year Average $14.14 4% High: $18.32 34%

Dell's Sale and Governance Process

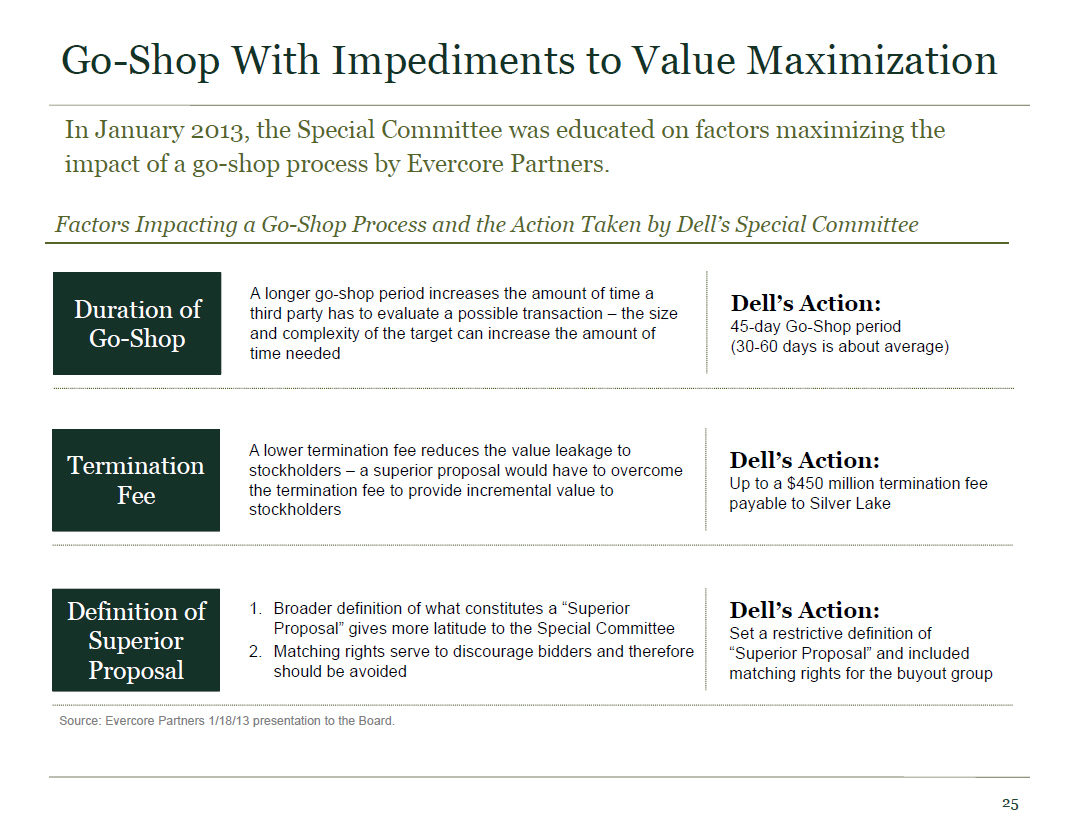

Go-Shop With Impediments to Value Maximization In January 2013, the Special Committee was educated on factors maximizing the impact of a go-shop process by Evercore Partners. Factors Impacting a Go-Shop Process and the Action Taken by Dell's Special Committee Duration of Go-Shop A longer go-shop period increases the amount of time a third party has to evaluate a possible transaction - the size and complexity of the target can increase the amount of time needed Dell's Action: 45-day Go-Shop period (30-60 days is about average) Termination Fee A lower termination fee reduces the value leakage to stockholders - a superior proposal would have to overcome the termination fee to provide incremental value to stockholders Dell's Action: Up to a $450 million termination fee payable to Silver Lake Definition of Superior Proposal 1. Broader definition of what constitutes a "Superior Proposal" gives more latitude to the Special Committee 2. Matching rights serve to discourage bidders and therefore should be avoided Dell's Action: Set a restrictive definition of "Superior Proposal" and included matching rights for the buyout group Source: Evercore Partners 1/18/13 presentation to the Board.

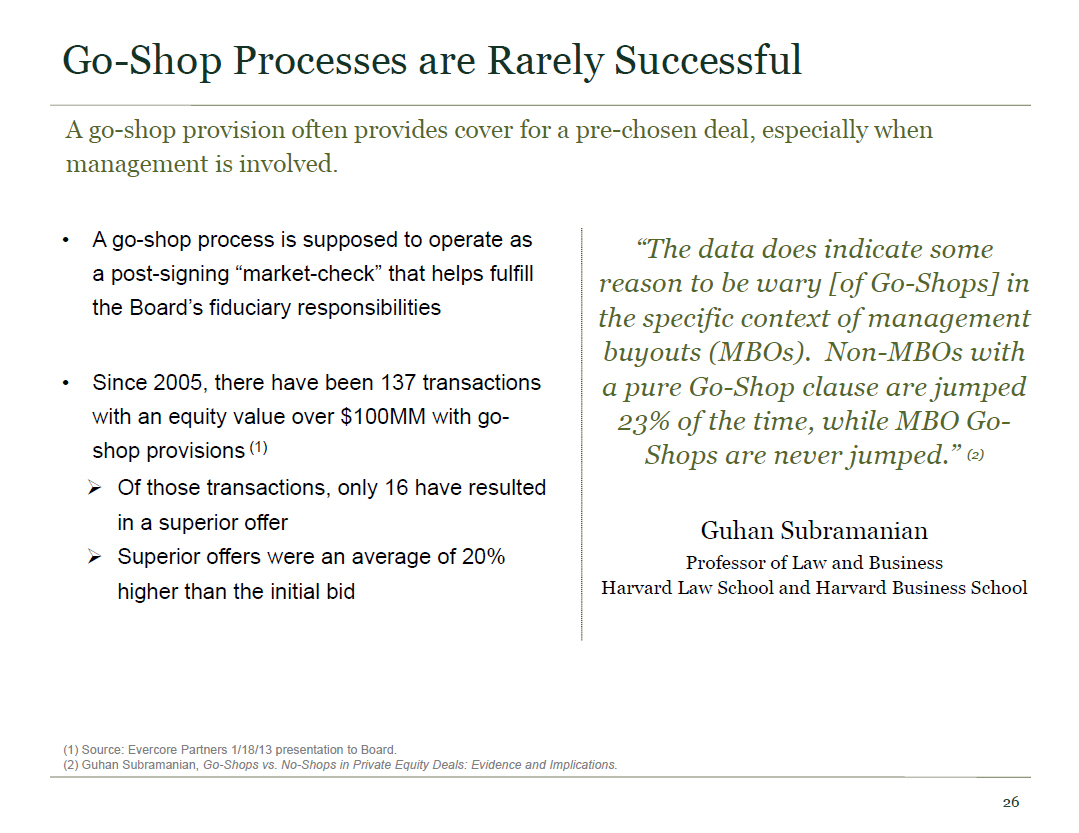

Go-Shop Processes are Rarely Successful A go-shop provision often provides cover for a pre-chosen deal, especially when management is involved. o A go-shop process is supposed to operate as a post-signing "market-check" that helps fulfill the Board's fiduciary responsibilities o Since 2005, there have been 137 transactions with an equity value over $100MM with go- shop provisions (1) (3d right arrow) Of those transactions, only 16 have resulted in a superior offer (3d right arrow) Superior offers were an average of 20% higher than the initial bid "The data does indicate some reason to be wary [of Go-Shops] in the specific context of management buyouts (MBOs). Non-MBOs with a pure Go-Shop clause are jumped 23% of the time, while MBO Go- Shops are never jumped." (2) Guhan Subramanian Professor of Law and Business Harvard Law School and Harvard Business School (1) Source: Evercore Partners 1/18/13 presentation to Board. (2) Guhan Subramanian, Go-Shops vs. No-Shops in Private Equity Deals: Evidence and Implications.

Efficacy of Go-Shop Provisions The Special Committee was made aware of the limited efficacy of Go-Shop Provisions. Efficacy of Go-Shop Provisions Confidential o Since 2005, there have been 137 transaction with equity values greater than $100million with go-shop provisions Of those transaction. only 16 or 12% resulted in aupcrior offer The superior offers on average were 20% grearer than the initial bid ($in millions) EVERCORE PARTNERS Source: Evercore Partners 1/18/13 presentation to Board. Announced Deals with "Go-Shop" & Topped Initial Date Target Initial Bidder Competing Bidder Equity Value TEV Go-Shop Period % Prem. on Initial Bid 3/09/12 Quest Software Insite Venture Ptrs Denali $2,148 $2,272 60 days 21.7% 10/01/10 Dynamex Greenbriar Equity Transforce 244 223 40 days 10.6% 08/13/10 Dynegy Blackstone Icahn Enterprises 542 4,760 40 days 10.0% 12/28/09 AMICAS Thomas Bravo Merge Healthcare 219 211 45 days 18.7% 11/13/09 Silicon Storage Technology Mgmt / Prophet Equity Microchip Technology 201 126.0 45 days 35.7% 11/02/09 Diedrich Coffee Peet's Coffee & Tea Green Mountain Coffee Roasters 200 201 21 days 34.6% 04/24/09 SumTotal System Accel-KKR Vista Equity Partners 152 117 31 days 27.6% 02/26/09 CKE Restaurants Thomas H. Lee Apollo Management 694 1,005 40 days 13.6% 02/05/09 Triad Hospitals Goldman Sachs / CCMP Community Health Systems 4,440 5,882 40 days 7.5% 06/16/08 Greenfield Online Quadrangle Group Microsoft / ZM Capital 408 376 50 days 12.9% 6/22/07 Barneys New York Istithmar World Capital / CVC Fast Retailing Co 942 942 30 days 14.2% 6/01/07 Everlast Worldwide Hidary Group Brands Holdings 133 163 30 days 24.5% 05/24/07 Eagle Global Logistics Jim Crane / Centerbridge / Woodbridge CEVA Logistics / Apollo Magmt 1,939 1,952 20 days 31.9% 03/08/07 Catalina Marketing Corp ValueAct Capital Hellman Friedman 1,511 1,591 45 days 1.2% 03/02/07 AeroFlex General Atlantic / Francisco Ptrs Veritas Captial 1,081 1,071 43 days 7.4% 05/19/05 Maytag Ripplewood / GS Capital Partners Whirlpool 1,677 2,585 30 days 50.0% Note: Updated as of Decemeber 31, 2012. Bold indicates ultimate purchasers Source: SDC, Merger Metrics

Impediments and Deal Protections The Special Committee agreed to a suite of deal protection measures that significantly handicap a third-party's ability to pursue an alternative transaction, especially one where existing stockholders have the choice to receive cash or participate in the Company's future. The restrictive definition of a Superior Proposal, together with other express terms of the Merger Agreement, act as almost impossible barriers for any potential bidder to be a superior proposal: (3d right arrow) As defined by the Merger Agreement, a Superior Proposal in the form of a dividend or share repurchase must result in a single person (not the Company) owning 50% or more of the outstanding shares (almost impossible) even if such a recapitalization would be an economically superior alternative to the Michael Dell/Silver Lake deal for ALL stockholders not named Michael Dell (3d right arrow) Before the Merger Agreement was finalized, Southeastern made it clear that it would view a recapitalization in which stockholders can participate as superior, but the Special Committee nonetheless approved terms that would make such a transaction virtually impossible to achieve (3d right arrow) Icahn and Southeastern believe that stockholders are capable of evaluating the risk of the business and do not need a Special Committee that owns practically no stock to choose to transfer those risks (and significant upside) to a very sophisticated buyout group The Special Committee has made securing financing for an alternative transaction a challenge: (3d right arrow) The Special Committee is unable to provide information or engage in discussions concerning any of our proposals unless such offer falls squarely within the definition of a "Superior Proposal" (3d right arrow) The significant termination fee (up to $450 million plus diligence fees) payable to Silver Lake (3d right arrow) Onerous matching rights for Michael Dell/Silver Lake Stockholders should be given an easier path to support an alternative transaction by voting for new directors: (3d right arrow) By holding a combined Annual Meeting and Special Meeting, stockholders would have had a real choice to reject theMichael Dell/Silver Lake deal and at the same time elect new directors on our proposed platform (3d right arrow) Unfortunately, the Board has chosen to hold a separate Special Meeting rather than hold both meetings concurrently Source: Dell Proxy Statement filed 3/29/13.

Dell's Stockholders Deserve Better Stockholders have the power to demand and receive more. o If the Michael Dell/Silver Lake transaction is rejected: 1) It can be amended 2) The Board can (and, in Icahn and Southeastern's opinion, probably would) explore the many alternatives to the Michael Dell/Silver Lake proposal, as proposed by Icahn and Southeastern, among others 3) Dell's owners can elect new directors in support of a platform to implement the proposed $14 per share Dell self tender. Icahn and Southeastern have given advanced notice of their intent to run a slate of directors at the 2013 Annual Meeting o Under these circumstances, Icahn and Southeastern believe that predictions about a precipitous decline in the market value of Dell stock if the Michael Dell/Silver Lake transaction is rejected by shareholders are exaggerated

Conclusion Dell's owners should reject the Michael Dell/Silver Lake transaction and force Board exploration and pursuit of an alternative transaction that would enable Dell's existing owners to reap the benefits of their multi-year investment in Dell's transformation - the value that Michael Dell and Silver Lake would keep for themselves.

Appendix

Public Comps Storage NTM Multiples Company EV/Sales EV/OCF EV/OI P/E EMC 2.4x 6.3x 6.9x 12.4x NetApp 1.3x 6.5x 9.6x 13.8x Average 1.9x 6.4x 8.3x 13.1x Services NTM Multiples Company EV/Sales EV/OCF EV/OI P/E Accenture 1.3x 9.7x 10.5x 17.3x Computer Sciences 0.6x 3.6x 6.6x 12.2x Wipro 2.6x 9.0x 9.8x 12.8x Cognizant 2.7x 8.6x 8.9x 14.5x Average 1.8x 7.7x 9.0x 14.2x End User Computing NTM Multiples Company EV EV/Sales EV/OCF EV/OI P/E Lenovo 6,403 0.2x 5.3x 6.2x 12.5x Acer 1,020 0.1x 5.8x 9.2x 25.7x Asustek 5,776 0.4x 6.4x 6.8x 9.6x Average 0.2x 5.9x 7.4x 15.9x Integrated Solutions NTM Multiples Company EV EV/Sales EV/OCF EV/OI P/E Hewlett-Packard 60,525 0.4x 4.3x 5.6x 6.7x Source: FactSet as of 6/21/13.

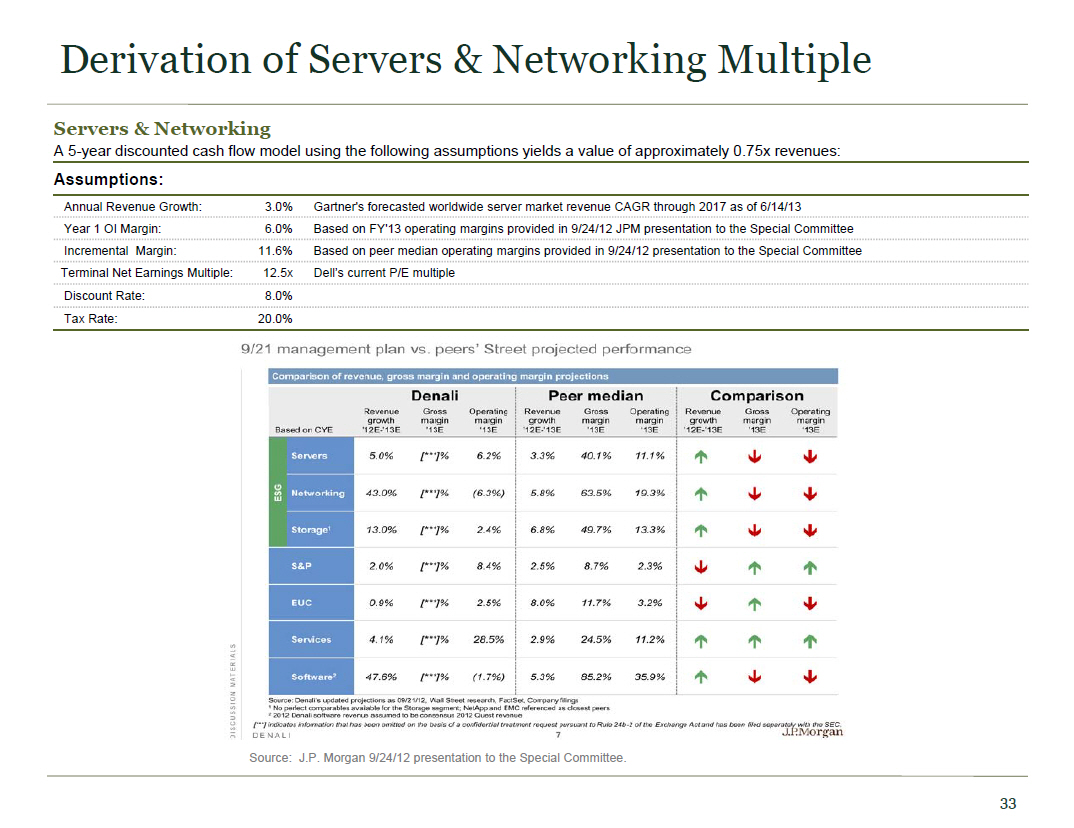

Derivation of Servers & Networking Multiple Servers & Networking A 5-year discounted cash flow model using the following assumptions yields a value of approximately 0.75x revenues: Assumptions: Annual Revenue Growth: 3.0% Gartner's forecasted worldwide server market revenue CAGR through 2017 as of 6/14/13 Year 1 OI Margin: 6.0% Based on FY'13 operating margins provided in 9/24/12 JPM presentation to the Special Committee Incremental Margin: 11.6% Based on peer median operating margins provided in 9/24/12 presentation to the Special Committee Terminal Net Earnings Multiple: 12.5x Dell's current P/E multiple Discount Rate: 8.0% Tax Rate: 20.0% 9/21 managment plan vs. peers' Street projected performance Comparision of revenue, gross margin and operating margin projections Denali Peer median Comparison Based on CYE Revenue growth '12E-13E Gross margin '13E Operating margin '13 E Revenue growth '12E-'13E Gross margin '13E Revenue growth '12E-'13E Gross margin '13E Operating margin '13E Servers 5.0% []% 6.2% 3.3% 40.1% 11.1% ESG Networking 43.0% []% (6.3%) 5.8% 63.5 19.3% Storage1 13.0% []% 2.4% 6.8% 49.7% 13.3% S&P 2.0% []% 8.4% 2.5% 8.7% 2.3% EUC 0.9% []% 2.5% 8.0% 11.7% 3.2% Services 4.1% []% 28.5% 2.9% 24.5% 11.2% Software2 47.6% []% (1.7%) 5.3% 85.2% 35.9% Source: Denali's updated projections as 09/21/12, Wall Street research, FactSet, Company filings 1 No perfect comparables available for the Storage segment; NetApp and EMC referenced as closest peers 2 2012 Denali software revenue assumed to be consensus 2012 Quest revenue [] indidicates infomration that has been omitted on the basis of a confidential treatment request pursuant to Rule 24b-2 of the Exchange Act and has been filed separately with the SEC. DENALI J.P.Morgan Source: J.P. Morgan 9/24/12 presentation to the Special Committee.

Important Disclosure Information SPECIAL NOTE REGARDING THIS PRESENTATION THIS PRESENTATION INCLUDES INFORMATION BASED ON DATA FOUND IN FILINGS WITH THE SECURITIES AND EXCHANGE COMMISSION, INDPENDENT INDUSTRY PUBLICATIONS AND OTHER SOURCES. ALTHOUGH WE BELIEVE THAT THE DATA IS RELIABLE, WE HAVE NOT SOUGHT, NOR HAVE WE RECEIVED, PERMISSION FROM ANY THIRD-PARTY TO INCLUDE THEIR INFORMATION IN THIS PRESENTATION. MANY OF THESTATEMENTS IN THIS PRESENTATION REFLECT OUR SUBJECTIVE BELIEF ICAHN ENTERPRISES L.P. ("ICAHN") AND SOUTHEASTERN ASSET MANAGEMENT, INC. ("SAM") HAVE FILED A PRELIMINARY PROXY STATEMENT WITH THE SEC REGARDING THE MANAGEMENT BUYOUT PROPOSAL OF DELL, AS CONTEMPLATED BY THE AGREEMENT AND PLAN OF MERGER, DATED AS OF FEBRUARY 5, 2013, BY AND AMONG DENALI HOLDING INC., DENALI INTERMEDIATE INC., DENALI ACQUIROR INC. AND DELL. BEFORE MAKING ANY VOTING DECISION, STOCKHOLDERS OF DELL ARE URGED TO READ ICAHN AND SAM'S DEFINITIVE PROXY STATEMENT, WHEN IT BECOMES AVAILABLE, CAREFULLY IN ITS ENTIRETY, BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION ABOUT THE MANAGEMENT BUYOUT PROPOSAL. STOCKHOLDERS OF DELL MAY OBTAIN FREE COPIES OF THE DEFINITIVE PROXY STATEMENT, WHEN IT BECOMES AVAILABLE, AND OTHER DOCUMENTS FILED WITH, OR FURNISHED TO, THE SEC BY SAM AND ICAHN AT THE SEC'S WEBSITE AT WWW.SEC.GOV OR BY CONTACTING D.F. KING & CO. TOLL-FREE AT 1-800-347-4750. INFORMATION RELATING TO THE PARTICIPANTS IN SUCH PROXY SOLICITATION IS CONTAINED IN THE SCHEDULE 13D FILED BY CARL C. ICAHN AND HIS AFFILIATES ON MAY 10, 2013, AS AMENDED THORUGH THE DATE HEREOF, AND THE SCHEDULE 13D FILED BY SOUTHEASTERN ASSET MANAGEMENT, INC. AND ITS AFFILIATES ON FEBRUARY 8, 2013, AS AMENDED THROUGH THE DATE HEREOF. FORWARD-LOOKING STATEMENTS Certain statements contained in this presentation are forward-looking statements including, but not limited to, statements that are predications of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Forward-looking statements are not guarantees of future performance or activities and are subject to many risks and uncertainties. Due to such risks and uncertainties, actual events or results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Forward-looking statements can be identified by the use of the future tense or other forward-looking words such as "believe," "expect," "anticipate," "intend," "plan," "estimate," "should," "may," "will," "objective," "projection," "forecast," "management believes," "continue," "strategy," "position" or the negative of those terms or other variations of them or by comparable terminology. Important factors that could cause actual results to differ materially from the expectations set forth in this press release include, among other things, the factors identified under the section entitled "Risk Factors" in Dell's Annual Report on Form 10-K for the year ended February 1, 2013 and under the section entitled "Cautionary Statement Concerning Forward-Looking Information" in Dell's Definitive Proxy Statement filed on May 31, 2013. Such forward-looking statements should therefore be construed in light of such factors, and SAM and Icahn are under no obligation, and expressly disclaim any intention or obligation, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.