Exhibit 1

| FOR IMMEDIATE RELEASE |

24 August 2016 |

|

|

| | 2016 Interim Results

|

| n | Reported billings up 9.3% at £25.319 billion, up 6.3% in constant currency |

| n | Reported revenue up 11.9% at £6.536 billion, up 5.2% at $9.367 billion, up 4.9% at €8.384 billion and down 2.7% at ¥1.042 trillion |

| n | Constant currency revenue up 8.9%, like-for-like revenue up 4.3% |

| n | Constant currency net sales up 8.1%, like-for-like net sales up 3.8% |

| n | Reported net sales margin of 13.7%, up 0.4 margin points versus last year, up 0.3 margin points in constant currency in line with the full year margin target and 0.3 margin points like-for-like |

| n | Headline reported profit before interest and tax £769 million up 14.9%, and up 10.3% in constant currency |

| n | Headline profit before tax £690 million up 15.8%, up 11.7% in constant currency |

| n | Profit before tax £425 million down 40.1%, down 45.5% in constant currency primarily reflecting net exceptional write-downs of £122 million, principally on the investment in comScore, in comparison to net exceptional gains of £203 million in the same period last year |

| n | Reported profit after tax £282 million down 53.1%, down 58.8% in constant currency |

| n | Headline diluted earnings per share 39.1p up 16.7%, up 11.5% in constant currency |

| n | Reported diluted earnings per share 18.9p down 56.0%, down 62.0% in constant currency |

| n | Dividends per share 19.55p up 22.9%, a pay-out ratio of 50%, in line with the revised target pay-out ratio of 50% |

| n | Share buy-backs of £197 million in the first half, down from £405 million last year, equivalent to 1.0% of the issued share capital against 2.0% last year |

| n | Return on equity slightly down at 15.5% for the 12 months to 30 June 2016 from 15.9% for the previous 12 month period, whilst weighted average cost of capital has fallen to 5.5% from 6.7% |

| n | Including associates and investments, revenue totals over $28 billion annually and people average over 200,000 |

2

Key figures

| £ million |

H1 2016 | D | reported | 1 | D | constant | 2 | H1 2015 | ||||||||||

| Billings |

25,319 | 9.3% | 6.3% | 23,156 | ||||||||||||||

| Revenue |

6,536 | 11.9% | 8.9% | 5,839 | ||||||||||||||

| Net sales |

5,594 | 11.0% | 8.1% | 5,041 | ||||||||||||||

| Headline EBITDA3 |

889 | 13.7% | 9.5% | 782 | ||||||||||||||

| Headline PBIT4 |

769 | 14.9% | 10.3% | 669 | ||||||||||||||

| Net sales margin5 |

13.7% | 0.4 | 6 | 0.3 | 6 | 13.3% | ||||||||||||

| Profit before tax |

425 | -40.1% | -45.5% | 710 | ||||||||||||||

| Profit after tax |

282 | -53.1% | -58.8% | 601 | ||||||||||||||

| Headline diluted EPS7 |

39.1p | 16.7% | 11.5% | 33.5p | ||||||||||||||

| Diluted EPS8 |

18.9p | -56.0% | -62.0% | 43.0p | ||||||||||||||

| Dividends per share |

19.55p | 22.9% | 22.9% | 15.91p |

First-half and Q2 highlights

| n | Reported billings increased by 9.3% to £25.319bn, up 6.3% in constant currency |

| n | Reported revenue growth of 11.9%, with like-for-like growth of 4.3%, 4.6% growth from acquisitions and 3.0% from currency, reflecting the weakness of sterling against the dollar and the euro |

| n | Reported net sales up 11.0% in sterling (up 4.3% in dollars, up 4.1% in euros but down 3.6% in yen), with like-for-like growth of 3.8%, 4.3% growth from acquisitions and 2.9% from currency |

| n | Constant currency revenue growth in all regions and business sectors, characterised by particularly strong growth geographically in Western Continental Europe and Asia Pacific, Latin America, Africa & the Middle East and Central & Eastern Europe, and functionally in advertising and media investment management and branding & identity, healthcare and specialist communications (including direct, digital and interactive) |

| n | Like-for-like net sales growth of 3.8%, a significant improvement over the first quarter growth rate of 3.2%, with the gap compared to revenue growth reversing in the second quarter, as the Group’s investment in technology enhanced the growth of advertising and media investment management net sales and as data investment management direct costs have been reduced |

| n | Reported headline EBITDA up 13.7%, with constant currency growth up 9.5%, reflecting both strong like-for-like net sales growth and margin improvement, with reported headline operating costs up 10.3%, rising less than revenue and net sales |

| n | Reported headline PBIT increased by 14.9%, up 10.3% in constant currency with the reported net sales margin, a more accurate competitive comparator, increasing by 0.4 margin points, and by 0.3 margin points on a constant currency basis, in line with the Group’s full year margin target |

| n | Reported headline diluted EPS 39.1p, up 16.7%, up 11.5% in constant currency. Dividends increased 22.9% to 19.55p, achieving a pay-out ratio of 50% in the first half, in line with the recently newly targeted pay-out ratio of 50% |

1 Percentage change in reported sterling

2 Percentage change at constant currency rates

3 Headline earnings before interest, tax, depreciation and amortisation

4 Headline profit before interest and tax

5 Headline profit before interest and tax, as a percentage of net sales

6 Margin points

7 Diluted earnings per share based on headline earnings

8 Diluted earnings per share based on reported earnings

3

| n | Average net debt increased by £612m (18%) to £3.986 billion compared to last year, at 2016 constant rates, continuing to reflect significant net acquisition spend and share repurchases of £831 million in the twelve months to 30 June 2016, more than offsetting the improvements in working capital in the same period |

| n | Return on equity for the 12 month period to 30 June 2016 slightly down to 15.5% from 15.9% for the previous 12 month period, reflecting the post-Brexit impact of a considerable weaker pound sterling on the Group’s net assets. This compares to a current weighted average after-tax cost of capital of 5.5% down from 6.7% |

| n | Creative and effectiveness domination recognised yet again in 2016 with the award of the Cannes Lion to WPP for most creative Holding Company for the sixth successive year since the award’s inception and another to Ogilvy & Mather Worldwide for the fifth consecutive year as the most creative agency network. Four WPP agency networks, Ogilvy & Mather Worldwide, Y&R, Grey and J. Walter Thompson Company finished in the top seven networks at Cannes in 2016, in positions one, three, six and seven respectively, an outstanding achievement. Grey New York and Ingo Stockholm were also voted the second and third most creative agencies in the world. For the fifth consecutive year, WPP was also awarded the EFFIE as the most effective Holding Company, with Ogilvy & Mather ranked the most effective agency |

| n | Continued strong performance in net new business despite recent hiccups |

| n | Particularly, following Brexit, accelerated implementation of growth strategy continues with revenue ratios for fast growth markets and new media raised from 35-40% to 40-45% over next four to five years. Quantitative revenue target of 50% already achieved |

Current trading and outlook

| n | July 2016 | July like-for-like revenue growth of 4.6% and net sales growth of 1.9% like-for-like, ahead of budget and the quarter 2 revised forecast. All regions and sectors (except data investment management) were positive, and showed a similar relative pattern to the first half, with advertising, media investment management, public relations and public affairs and specialist communications (including direct, digital and interactive) up strongly. Cumulative like-for-like revenue growth for the first seven months of 2016 is 4.3% and net sales growth 3.5%, ahead of target |

| n | FY 2016 quarter 2 revised forecast | Slight increase in like-for-like revenue growth from the quarter 1 revised forecast, as the scale of digital media purchases are forecast to increase, with revenue growth well over 3% and net sales growth over 3% and, following the strong first half, a slightly weaker second half, partly reflecting stronger comparatives in the second half of 2015. Headline net sales operating margin target improvement, as previously, of 0.3 margin points in constant currency |

| n | Dual Focus in 2016 | 1. Stronger than competitor revenue and net sales growth due to leading position in both faster growing geographic markets and digital, premier parent company creative position, new business, horizontality and strategically targeted acquisitions; 2. Continued emphasis on balancing revenue and net sales growth with headcount increases and improvement in staff costs to net sales ratio to enhance operating margins |

| n | Long-term targets | Above industry revenue and net sales growth due to geographically superior position in new markets and functional strength in new media, in data investment management, including data analytics and the application of new technology, creativity, effectiveness and horizontality; improvement in staff costs to net sales ratio of 0.2 or more depending on net sales growth; net sales operating margin expansion of 0.3 margin points or more on a constant currency basis, with an ultimate goal of almost 20%; and headline diluted EPS growth of 10% to 15% p.a. from revenue and net sales growth, margin expansion, strategically targeted small and medium-sized acquisitions and share buy-backs |

4

In this press release not all of the figures and ratios used are readily available from the unaudited interim results included in Appendix 1. Where required, details of how these have been arrived at are shown in the Appendices.

Review of Group results

Revenue

Revenue analysis

| £ million |

2016 | D | reported | D | constant9 | D | LFL10 | acquisitions | 2015 | |||||||||||||||

| First quarter |

3,076 | 10.5% | 9.0% | 5.1% | 3.9% | 2,783 | ||||||||||||||||||

| Second quarter |

3,460 | 13.2% | 8.8% | 3.5% | 5.3% | 3,056 | ||||||||||||||||||

| First half |

6,536 | 11.9% | 8.9% | 4.3% | 4.6% | 5,839 | ||||||||||||||||||

| Net sales analysis

|

||||||||||||||||||||||||

| £ million |

2016 | D | reported | D | constant | D | LFL | acquisitions | 2015 | |||||||||||||||

| First quarter |

2,616 | 8.1% | 6.7% | 3.2% | 3.5% | 2,419 | ||||||||||||||||||

| Second quarter |

2,978 | 13.6% | 9.4% | 4.3% | 5.1% | 2,622 | ||||||||||||||||||

| First half |

5,594 | 11.0% | 8.1% | 3.8% | 4.3% | 5,041 | ||||||||||||||||||

Reported billings were up 9.3% at £25.319 billion, and up 6.3% in constant currency. Estimated net new business billings of £1.930 billion ($2.992 billion) were won in the first half of the year, a good performance, once again, against £1.301 billion ($2.082 billion) in the same period last year. Generally, the Group continues to benefit from consolidation trends in the industry, winning assignments from existing and new clients, including several very large industry-leading advertising, media and digital assignments, the full benefit of which will be seen reflected in Group revenue later in 2016 and into 2017, although two recent losses have checked progress. Having said that, one of these losses, in particular, opens up a significant competitive restricted category for parts of our advertising and media investment management sector in the United States and Mexico.

Reportable revenue was up 11.9% at £6.536 billion. Revenue on a constant currency basis was up 8.9% compared with last year, the difference to the reportable number reflecting the continuing weakness of the pound sterling against the US dollar and the euro, particularly more recently, following the United Kingdom decision to exit the European Union. As a number of our current competitors report in US dollars, in euros and in yen, appendices 2, 3 and 4 show WPP’s interim results in reportable US dollars, euros and yen respectively. This shows that US dollar reportable revenue was up 5.2% to $9.367 billion, which compares with the $7.384 billion of our closest current US-based competitor, euro reportable revenue was up 4.9% to €8.384 billion, which compares with €4.753 billion of our nearest current European-based competitor and yen reportable revenue was down 2.7% to ¥1.042 trillion, which compares with ¥393 billion of our nearest current Japanese-based competitor.

As outlined in the First Quarter Trading Statement and previous Preliminary Announcements for the last few years, due to the increasing scale of digital media purchases within the Group’s media investment management businesses and of direct costs in data investment management, net sales is the more meaningful and accurate reflection of top line growth, although currently none of our competitors report net sales. The differences are shown below in a table that compares the Group’s like-for-like revenue and net sales against our direct competitors’ like-for-like revenue only performance over the last two years.

| 9 | Percentage change at constant currency exchange rates |

| 10 | Like-for-like growth at constant currency exchange rates and excluding the effects of acquisitions and disposals |

5

| First half | WPP Revenue |

WPP Net Sales |

OMC Revenue |

Pub Revenue |

IPG Revenue |

Havas Revenue |

||||||||||||||||||

| Revenue (local ‘m) |

£6,536 | £5,594 | $7,384 | €4,753 | $3,659 | €1,087 | ||||||||||||||||||

| Revenue ($‘m) |

$9,367 | $8,016 | $7,384 | $5,304 | $3,659 | $1,213 | ||||||||||||||||||

| Growth Rates (%)* |

4.3 | 3.8 | 3.6 | 2.8 | 5.1 | 3.0 | ||||||||||||||||||

| Quarterly like-for-like growth%* |

||||||||||||||||||||||||

| Q1/15 |

5.2 | 2.5 | 5.1 | 0.9 | 5.7 | 7.1 | ||||||||||||||||||

| Q2/15 |

4.5 | 2.1 | 5.3 | 1.4 | 6.7 | 5.5 | ||||||||||||||||||

| Q3/15 |

4.6 | 3.3 | 6.1 | 0.7 | 7.1 | 5.5 | ||||||||||||||||||

| Q4/15 |

6.7 | 4.9 | 4.8 | 2.8 | 5.2 | 3.1 | ||||||||||||||||||

| Q1/16 |

5.1 | 3.2 | 3.8 | 2.9 | 6.7 | 3.4 | ||||||||||||||||||

| Q2/16 |

3.5 | 4.3 | 3.4 | 2.7 | 3.7 | 2.7 | ||||||||||||||||||

| 2 Years cumulative like-for-like growth % |

|

|||||||||||||||||||||||

| Q1/15 |

12.2 | 6.3 | 9.4 | 4.2 | 12.3 | 10.1 | ||||||||||||||||||

| Q2/15 |

14.7 | 6.5 | 11.1 | 1.9 | 11.4 | 13.4 | ||||||||||||||||||

| Q3/15 |

12.2 | 6.3 | 12.6 | 1.7 | 13.4 | 11.5 | ||||||||||||||||||

| Q4/15 |

14.5 | 7.0 | 10.7 | 6.0 | 10.0 | 6.6 | ||||||||||||||||||

| Q1/16 |

10.3 | 5.7 | 8.9 | 3.8 | 12.4 | 10.5 | ||||||||||||||||||

| Q2/16 |

8.0 | 6.4 | 8.7 | 4.1 | 10.4 | 8.2 | ||||||||||||||||||

* The above like-for-like/organic revenue figures are extracted from the published quarterly trading statements issued by Omnicom Group (“OMC”), Publicis Groupe (“Pub”), Interpublic Group (“IPG”) and HAVAS (“Havas”)

On a like-for-like basis, which excludes the impact of acquisitions and currency, revenue was up 4.3% in the first half, with net sales up 3.8%, with the gap compared to revenue growth reversing in the second quarter, as the impact of the Group’s investment in technology had an increasingly positive impact on net sales and as data investment management direct costs reduced. In the second quarter, like-for-like revenue was up 3.5%, lower than the first quarter’s 5.1%, giving 4.3% for the first half, with net sales significantly stronger at 4.3%, following 3.2% in the first quarter, giving 3.8% for the first half, against comparatives of 4.9% and 2.3% for revenue and net sales respectively, in 2015.

Despite GDP growth in the 3.0-3.5% range with little inflation and consequent lack of pricing power, client data continues to reflect some increase in advertising and promotional spending – with the former tending to grow faster than the latter, which from our point of view is more positive – across most of the Group’s major geographic and functional sectors. Quarter two saw a continuation of the relative strength of advertising spending in fast moving consumer goods, especially. Nonetheless, clients understandably continue to demand increased effectiveness and efficiency, i.e. better value for money. Although corporate balance sheets are much stronger than pre-Lehman and confidence is higher as a result, the Brexit/Eurozone, Middle East, BRICs hard or soft landing (particularly now Brazil, Russia and China) and United States deficit uncertainties still demand caution. The over $7 trillion net cash lying virtually idle in those balance sheets, still seems destined to remain so, with companies, even after the recent upturn in merger activity, mostly unwilling to attempt excessive acquisition risk (except perhaps in our own industry) or expand capacity, particularly in mature markets, despite the Eurozone showing some signs of life.

Operating profitability

Reported headline EBITDA was up 13.7% to £889 million, up 9.5% in constant currency. Reported headline operating profit was up 14.9% to £769 million from £669 million, up 10.3% in constant currency. As has been noted before, our profitability tends to be more skewed to the second half of the year compared with some of our competitors.

6

Reported headline net sales operating margins were up 0.4 margin points at 13.7%, up 0.3 margin points in constant currency, in line with the Group’s full year margin target of a 0.3 margin points improvement, on a constant currency basis. On a like-for-like basis, operating margins were also up 0.3 margin points.

Given the significance of data investment management revenue to the Group, with none of our direct parent company competitors significantly present in that sector, net sales remain a much more meaningful measure of competitive comparative top line and margin performance. Net sales is a more appropriate measure because data investment management revenue includes pass-through costs, principally for data collection, on which no margin is charged and with the growth of the internet, the process of data collection becomes more efficient. In addition, the Group’s media investment management sub-sector is increasingly buying digital media as principal and as a result, the subsequent billings to clients have to be accounted for as revenue, as well as billings. We know competitors do have significantly increasing barter, telesales, food broking and field marketing operations, where the same issue arises and which remain opaque and undisclosed. As a result, reporting practices should be standardised, although there is limited recognition of this to date. Thus, revenue and revenue growth rates will tend to increase, although net sales and net sales growth will remain unaffected and the latter will present a clearer picture of underlying performance. Because of these two significant factors, the Group, whilst continuing to report revenue and revenue growth, focuses even more on net sales and the net sales operating margin.

On a reported basis, net sales operating margins, before all incentives11, were 15.9%, up 0.4 margin points, compared with 15.5% last year. The Group’s staff costs to net sales ratio, including incentives, fell by 0.1 margin points to 65.4% compared with 65.5% in the first half of 2015. This continues to reflect good staff costs to net sales ratio management, through better control of the growth of staff numbers and salary and related costs, as compared to net sales, than in the first half of 2015.

Operating costs

In the first half of 2016, headline operating costs12 increased by 10.3% and were up by 7.7% in constant currency, compared with reported net sales up 11.0% and constant currency net sales growth of 8.1%. Reported staff costs, excluding all incentives, were down 0.1 margin points at 63.2% of net sales and flat in constant currency. Incentive costs amounted to £121.6 million or 14.0% of headline operating profits before incentives and income from associates, compared to £111.6 million last year, or 14.8%, an increase of £10.0 million or 9.0%. Target incentive funding is set at 15% of operating profit before bonus and taxes, maximum at 20% and in some instances super-maximum at 25%. Reportable severance costs were £29.7 million versus £15.9 million for the same period last year. Variable staff costs were 6.2% of revenue and 7.2% of net sales, at the higher end of historical ranges and, again, reflecting good staff cost management and continued flexibility in the cost structure.

On a like-for-like basis, the average number of people in the Group, excluding associates, was 131,239 in the first half of the year, compared to 131,047 in the same period last year, a slight increase of 0.1%. On the same basis, the total number of people in the Group, excluding associates, at 30 June 2016 was 133,902, up 0.3% compared to 133,474 at 30 June 2015. This reflected, partly, the transfer of approximately 250 staff to IBM in the first half of 2016, the second phase of the strategic partnership agreement and IT transformation programme. Since 1 January 2016, on a like-for-like basis, the number of people in the Group has increased by 0.7% or over

| 11 | Short and long-term incentives and the cost of share-based incentives |

| 12 | Excludes direct costs, goodwill impairment, amortisation and impairment of acquired intangibles, investment gains and write-downs, gains on re-measurement of equity interests on acquisition of controlling interest and restructuring costs |

7

900 at 30 June 2016 (including the staff transferred to IBM), and also reflecting the continued caution by the Group’s operating companies in hiring and the usual seasonality of a relatively smaller absolute first half in comparison to the second half. On the same basis revenue increased 4.3%, with net sales up 3.8%.

Exceptional gains and investment write-downs

In the first half of 2016, the Group had net exceptional losses of £122 million, relating primarily to the write down of its investment in comScore, which has not released any financial statements in relation to its 2015 results, due to an internal investigation by their Audit Committee. Following the announcement of the internal investigation, the market value of comScore fell below the Group’s carrying value. The effect of the write down is to reverse the net gains recognised by the Group in 2014 and 2015 on the disposal of assets to comScore. The Group continues to monitor the position and welcomes the most recent management changes, although remains puzzled as to why the audit investigation has taken so long, remains unresolved and has proved so costly. It expects the situation to be resolved early on, in the second half of 2016, when comScore should announce the results of its investigation.

Interest and taxes

Net finance costs (excluding the revaluation of financial instruments) were £79.0 million compared to £73.4 million in the first half of 2015, an increase of £5.6 million, or 7.6%, reflecting higher levels of average net debt, partly offset by lower funding costs and more efficient management of cash pooling. The weighted average debt maturity is now 9 years, with a weighted average interest rate of 3.4% at 30 June 2016 versus 4.0% at 30 June 2015.

The headline tax rate rose by 1.0% to 21.0% (2015 20.0%), reflecting the levels and mix of profits in the countries in which the Group operates. The tax rate on the reported profit before tax was 33.7% (2015 15.3%), higher than the headline tax rate, largely because certain exceptional losses in the period were not tax deductible.

Earnings and dividend

Headline profit before tax was up 15.8% to £690 million from £596 million and up 11.7% in constant currency.

Reported profit before tax fell by 40.1% to £425 million from £710 million, or down 45.5% in constant currency. This reflected the significant difference between the net exceptional losses of £121.6 million, principally the comScore write-down, in the first half of 2016, compared with the net exceptional gains of £202.5 million in the first half of last year. Excluding these exceptional items, reported profit before tax would be up 7.8%. Reported profits attributable to share owners fell by 56.6% to £246 million from £566 million, again reflecting the impact of exceptional items. In constant currency, profits attributable to share owners fell by 62.5%.

Diluted headline earnings per share rose by 16.7% to 39.1p from 33.5p. In constant currency, diluted headline earnings per share rose by 11.5%. Diluted reported earnings per share fell by 56.0% to 18.9p from 43.0p and by 62.0% in constant currency, as a result of the net exceptional charges in the first half of 2016, compared with the net exceptional gains in the first half of last year.

As outlined in the June 2015 AGM statement, the achievement of the previous targeted pay-out ratio of 45% one year ahead of schedule, raised the question of whether the pay-out ratio target should be increased further. Following that review, your Board decided to up the dividend pay-out ratio to a target of 50%, to be achieved by 2017. Following your Company’s strong progress in 2015, the dividends were increased by 17% overall, with a balancing out of the interim and final

8

dividend payments, representing a pay-out ratio of 47.7%. As a result of continuing strong progress in the first half of 2016, your Board declares an interim dividend of 19.55p per share, an increase of 22.9% and a pay-out ratio of 50% for the first half, achieving the newly targeted pay-out ratio. The record date for the interim dividend is 7 October 2016, payable on 7 November 2016. Further details of WPP’s financial performance are provided in Appendices 1 to 4.

Regional review

The pattern of revenue and net sales growth differed regionally. The tables below give details of revenue and net sales, revenue and net sales growth by region for the second quarter and first half of 2016, as well as the proportion of Group revenue and net sales and operating profit and operating margin by region;

Revenue analysis

| £ million | Q2 2016 | D reported | D constant13 | D LFL14 | % group | Q2 2015 | % group | |||||||||||||||||||||

| N. America |

1,250 | 10.8% | 3.9% | 2.2% | 36.1% | 1,128 | 36.9% | |||||||||||||||||||||

| United Kingdom |

475 | 7.4% | 7.4% | 3.5% | 13.7% | 443 | 14.5% | |||||||||||||||||||||

| W. Cont. Europe |

726 | 21.6% | 12.3% | 6.2% | 21.0% | 596 | 19.5% | |||||||||||||||||||||

| AP, LA, AME, CEE15 |

1,009 | 13.6% | 13.9% | 3.4% | 29.2% | 889 | 29.1% | |||||||||||||||||||||

| Total Group |

3,460 | 13.2% | 8.8% | 3.5% | 100.0% | 3,056 | 100.0% | |||||||||||||||||||||

| £ million | H1 2016 | D reported | D constant | D LFL | % group | H1 2015 | % group | |||||||||||||||||||||

| N. America |

2,440 | 12.7% | 6.4% | 4.4% | 37.3% | 2,164 | 37.1% | |||||||||||||||||||||

| United Kingdom |

927 | 7.8% | 7.8% | 4.1% | 14.2% | 860 | 14.7% | |||||||||||||||||||||

| W. Cont. Europe |

1,342 | 17.4% | 10.8% | 5.4% | 20.5% | 1,143 | 19.6% | |||||||||||||||||||||

| AP, LA, AME, CEE |

1,827 | 9.3% | 11.6% | 3.4% | 28.0% | 1,672 | 28.6% | |||||||||||||||||||||

| Total Group |

6,536 | 11.9% | 8.9% | 4.3% | 100.0% | 5,839 | 100.0% | |||||||||||||||||||||

| Net sales analysis | ||||||||||||||||||||||||||||

|

£ million |

Q2 2016 | D reported | D constant | D LFL | % group | Q2 2015 | % group | |||||||||||||||||||||

| N. America |

1,084 | 12.7% | 5.7% | 4.0% | 36.4% | 962 | 36.7% | |||||||||||||||||||||

| United Kingdom |

400 | 7.3% | 7.3% | 3.4% | 13.4% | 373 | 14.2% | |||||||||||||||||||||

| W. Cont. Europe |

604 | 20.3% | 11.1% | 6.2% | 20.3% | 503 | 19.2% | |||||||||||||||||||||

| AP, LA, AME, CEE |

890 | 13.5% | 14.1% | 3.8% | 29.9% | 784 | 29.9% | |||||||||||||||||||||

| Total Group |

2,978 | 13.6% | 9.4% | 4.3% | 100.0% | 2,622 | 100.0% | |||||||||||||||||||||

|

£ million |

H1 2016 | D reported | D constant | D LFL | % group | H1 2015 | % group | |||||||||||||||||||||

| N. America |

2,103 | 12.0% | 5.8% | 4.0% | 37.6% | 1,877 | 37.2% | |||||||||||||||||||||

| United Kingdom |

775 | 7.2% | 7.2% | 3.3% | 13.8% | 723 | 14.3% | |||||||||||||||||||||

| W. Cont. Europe |

1,112 | 15.3% | 8.9% | 4.3% | 19.9% | 965 | 19.1% | |||||||||||||||||||||

| AP, LA, AME, CEE |

1,604 | 8.7% | 11.2% | 3.5% | 28.7% | 1,476 | 29.4% | |||||||||||||||||||||

| Total Group |

5,594 | 11.0% | 8.1% | 3.8% | 100.0% | 5,041 | 100.0% | |||||||||||||||||||||

Operating profit analysis (Headline PBIT)

| £ million | H1 2016 | % margin | H1 2015 | % margin | ||||||||||||

| N. America |

349 | 16.6% | 307 | 16.4% | ||||||||||||

| United Kingdom |

98 | 12.6% | 92 | 12.7% | ||||||||||||

| W. Cont. Europe |

138 | 12.4% | 103 | 10.7% | ||||||||||||

| AP, LA, AME, CEE |

184 | 11.5% | 167 | 11.3% | ||||||||||||

| Total Group |

769 | 13.7% | 669 | 13.3% | ||||||||||||

13 Percentage change at constant currency rates

14 Like-for-like growth at constant currency exchange rates and excluding the effects of acquisitions and disposals

15 Asia Pacific, Latin America, Africa & Middle East and Central & Eastern Europe

9

North America like-for-like revenue increased 2.2% in the second quarter, with like-for-like net sales growth stronger at 4.0%, slightly higher than the first quarter, as parts of the Group’s advertising and media investment management businesses investment in technology generated a higher growth rate in net sales compared to revenue, along with growth in data investment management. As a result, like-for-like revenue and net sales growth rates in the first half were similar at 4.4% and 4.0% respectively. Advertising and media investment management showed the strongest growth in the second quarter, with data investment management, public relations and public affairs and branding & identity all growing stronger in the second quarter, with parts of the Group’s healthcare businesses continuing to be more challenged.

United Kingdom like-for-like revenue, perhaps reflecting pre-Brexit vote uncertainties, was up 3.5%, slower than the first quarter growth of 4.7%, as the Group’s media investment management businesses grew less strongly, although still double digit, together with parts of the Group’s data investment management and public relations and public affairs businesses, which were also slower. Net sales overall showed a similar pattern to revenue, up slightly to 3.4% like-for-like in the second quarter, compared with 3.2% in the first quarter, with parts of the Group’s advertising, data investment management and healthcare businesses stronger than the first quarter.

Western Continental Europe, which remains patchy from a macro-economic point of view, showed considerable improvement in the second quarter, with like-for-like revenue growth up 6.2% in the second quarter, compared with 4.4% in the first quarter. Austria, Belgium, Denmark, Greece, Finland, Italy, the Netherlands, Norway and Sweden performed stronger than the first quarter, with France, Portugal and Spain more difficult. Net sales also improved over the first quarter, with like-for-like growth of 6.2%, compared with 2.3% in the first quarter, following a similar pattern to the growth in revenue.

In Asia Pacific, Latin America, Africa & the Middle East and Central & Eastern Europe, revenue growth was the same as the first quarter, at 3.4% like-for-like, but net sales improved markedly, up 3.8%, compared with 3.0% in the first quarter, on the same basis. Revenue growth in Latin America and Central & Eastern Europe showed an improving trend, with Asia Pacific, Africa and the Middle East slower. Net sales growth showed a similar trend to revenue, although Asia Pacific and the Middle East showed stronger comparative growth than revenue. In South East Asia, India, the Group’s second largest market in the region, remains a shining beacon, with like-for-like net sales growth over 17% in the second quarter. Indonesia, Japan, the Philippines, Singapore, Thailand and Vietnam all grew net sales well above the average, but Greater China remains sluggish. Net sales growth in the BRICs16 improved significantly in the second quarter, with all the major countries, except China, improving. The Next 1117 continued to grow more strongly, but slower than the first quarter.

In Central & Eastern Europe, like-for-like net sales grew strongly in the second quarter, up over 10%, with Croatia, Hungary, Poland, Romania, Russia and the Ukraine improving over the first quarter, and with the Czech Republic slightly slower. Sadly, the Group’s media measurement business in Russia was effectively expropriated by a recent Act passed by the Duma and control sold after the half-year end to a State controlled research institute.

| 16 | Brazil, Russia, India and China (accounting for over $1.2 billion revenue, including associates, in the first half) |

| 17 | Bangladesh, Egypt, Indonesia, South Korea, Mexico, Nigeria, Pakistan, Philippines, Vietnam and Turkey - the Group has no operations in Iran (accounting for over $500 million revenue, including associates, in the first half) |

10

Primarily reflecting the usually lower first-half seasonal pattern, the continued higher growth rates in the mature markets, and generally weaker foreign exchange rates in so called faster growth markets, only 28.7% of the Group’s net sales came from Asia Pacific, Latin America, Africa & the Middle East and Central & Eastern Europe, against the Group’s revised and strengthened strategic objective of 40-45% over the next four to five years. This was down on the same period last year, but up over one percentage point compared with the first quarter, reflecting in part the merger of most of the Group’s Australian and New Zealand assets with STW Communications Group Limited in Australia. The re-named WPP AUNZ became a listed subsidiary of the Group on 8 April 2016.

Business sector review

The pattern of revenue and net sales growth also varied by communications services sector and operating brand. The tables below give details of revenue and net sales, revenue and net sales growth by communications services sector, as well as the proportion of Group revenue and net sales for the second quarter and first half of 2016 and operating profit and operating margin by communications services sector;

Revenue analysis

| £ million |

Q2 2016 | D reported | D constant | D LFL | % group | Q2 2015 | % group | |||||||||||||||||||||

|

AMIM18 |

1,576 | 12.4% | 8.3% | 5.4% | 45.6% | 1,402 | 45.9% | |||||||||||||||||||||

| Data Inv. Mgt.19 |

652 | 5.8% | 2.0% | -0.4% | 18.8% | 616 | 20.1% | |||||||||||||||||||||

| PR & PA20 |

260 | 10.6% | 5.3% | 3.0% | 7.5% | 235 | 7.7% | |||||||||||||||||||||

| BI, HC & SC21 |

972 | 21.0% | 16.0% | 3.4% | 28.1% | 803 | 26.3% | |||||||||||||||||||||

| Total Group |

3,460 | 13.2% | 8.8% | 3.5% | 100.0% | 3,056 | 100.0% | |||||||||||||||||||||

| £ million |

H1 2016 | D reported | D constant | D LFL | % group | H1 2015 | % group | |||||||||||||||||||||

| AMIM |

2,963 | 12.3% | 9.6% | 6.6% | 45.4% | 2,638 | 45.2% | |||||||||||||||||||||

| Data Inv. Mgt. |

1,244 | 5.9% | 3.5% | 0.0% | 19.0% | 1,174 | 20.1% | |||||||||||||||||||||

| PR & PA |

499 | 8.8% | 4.7% | 2.7% | 7.6% | 459 | 7.9% | |||||||||||||||||||||

| BI, HC & SC |

1,830 | 16.7% | 13.1% | 4.0% | 28.0% | 1,568 | 26.8% | |||||||||||||||||||||

| Total Group |

6,536 | 11.9% | 8.9% | 4.3% | 100.0% | 5,839 | 100.0% | |||||||||||||||||||||

| Net sales analysis | ||||||||||||||||||||||||||||

| £ million |

Q2 2016 | D reported | D constant | D LFL | % group | Q2 2015 | % group | |||||||||||||||||||||

| AMIM |

1,301 | 12.2% | 8.3% | 5.8% | 43.7% | 1,160 | 44.3% | |||||||||||||||||||||

| Data Inv. Mgt. |

489 | 8.8% | 5.1% | 2.0% | 16.4% | 450 | 17.1% | |||||||||||||||||||||

| PR & PA |

256 | 10.8% | 5.5% | 3.2% | 8.6% | 231 | 8.8% | |||||||||||||||||||||

| BI, HC & SC |

932 | 19.4% | 14.5% | 3.7% | 31.3% | 781 | 29.8% | |||||||||||||||||||||

| Total Group |

2,978 | 13.6% | 9.4% | 4.3% | 100.0% | 2,622 | 100.0% | |||||||||||||||||||||

| £ million |

H1 2016 | D reported | D constant | D LFL | % group | H1 2015 | % group | |||||||||||||||||||||

| AMIM |

2,423 | 9.1% | 6.7% | 4.6% | 43.3% | 2,221 | 44.1% | |||||||||||||||||||||

| Data Inv. Mgt. |

922 | 7.6% | 5.1% | 1.0% | 16.5% | 857 | 17.0% | |||||||||||||||||||||

| PR & PA |

490 | 8.9% | 4.8% | 2.8% | 8.8% | 450 | 8.9% | |||||||||||||||||||||

| BI, HC & SC |

1,759 | 16.3% | 12.8% | 4.4% | 31.4% | 1,513 | 30.0% | |||||||||||||||||||||

| Total Group |

5,594 | 11.0% | 8.1% | 3.8% | 100.0% | 5,041 | 100.0% | |||||||||||||||||||||

| 18 | Advertising, Media Investment Management |

| 19 | Data Investment Management |

| 20 | Public Relations & Public Affairs |

| 21 | Branding & Identity, Healthcare and Specialist Communications |

11

Operating profit analysis (Headline PBIT)

| £ million | H1 2016 | % margin | H1 2015 | % margin | ||||||||||||

| AMIM |

369 | 15.2% | 330 | 14.9% | ||||||||||||

| Data Inv. Mgt. |

125 | 13.5% | 101 | 11.7% | ||||||||||||

| PR & PA |

71 | 14.4% | 66 | 14.7% | ||||||||||||

| BI, HC & SC |

204 | 11.6% | 172 | 11.4% | ||||||||||||

| Total Group |

769 | 13.7% | 669 | 13.3% | ||||||||||||

Advertising and Media Investment Management

As in the first quarter, advertising and media investment management remains the strongest performing sector. Like-for-like revenue grew by 5.4% in the second quarter, slower than the 7.9% seen in the first quarter, with a reduction in the growth rate in North America. However, like-for-like net sales growth was 5.8%, compared with 3.4% in the first quarter, as the Group’s investment in technology had an increasingly positive impact on net sales. The rate of growth in the Group’s advertising businesses improved in the second quarter, with North America, the United Kingdom, Western Continental Europe and the Middle East showing an improving trend, but overall remains challenging.

The Group gained a total of £1.930 billion ($2.992 billion) in net new business wins (including all losses and excluding retentions) in the first half, a significant increase compared to £1.301 billion ($2.082 billion) in the same period last year. Of this, J. Walter Thompson Company, Ogilvy & Mather Worldwide, Y&R and Grey generated net new business billings of £637 million ($987 million). Also, out of the Group total, GroupM, the Group’s media investment management company (which includes Mindshare, MEC, MediaCom, Maxus, GroupM Search, Xaxis and Essence), together with tenthavenue, generated net new business billings of £958 million ($1.485 billion).

On a reportable basis, net sales margins continued to improve, up 0.3 margin points to 15.2%.

Data Investment Management

On a like-for-like basis, data investment management revenue fell 0.4% in the second quarter, compared with growth of 0.5% in the first quarter, with all regions, except North America and Asia Pacific slower than the first quarter. However, like-for-like net sales grew 2.0%, compared with -0.1% in the first quarter, with all regions, except the United Kingdom, which was flat, showing net sales growth. Latin America grew over 5% with Asia Pacific up almost 4%. Reportable net sales margins improved strongly by 1.8 margin points, reflecting both good cost control and the benefit of the restructuring actions taken in 2014 and 2015.

Public Relations and Public Affairs

Public relations and public affairs like-for-like revenue increased 3.0% in the second quarter, compared with 2.3% in the first quarter. Like-for-like net sales showed a similar pattern, up 3.2% in the second quarter, compared with 2.3% in the first quarter, with all regions showing growth, particularly in Asia Pacific, Latin America and Africa. Cohn & Wolfe and parts of the specialist public relations and public affairs businesses in the United States and Germany performed particularly well. Reportable net sales margins fell slightly, down 0.3 margin points, although H+K Strategies, Ogilvy Public Relations, Cohn & Wolfe and the specialist public relations companies in this sector showed improved margins in the first half.

12

Branding and Identity, Healthcare and Specialist Communications

At the Group’s branding & identity, healthcare and specialist communications businesses (including direct, digital and interactive) like-for-like net sales grew 3.7% in the second quarter, compared with 5.2% in the first quarter. The Group’s branding & identity and direct, digital and interactive businesses grew strongly in the second quarter, with parts of the Group’s healthcare businesses in the United States and specialist communications businesses in Asia Pacific slower. Reportable net sales margins for this sector, as a whole, were up 0.2 margin points, with branding & identity and direct, digital and interactive margins up strongly, but with pressure in healthcare and specialist communications. Like-for-like, digital revenue now accounts for over 38% of Group revenue, up 1.0 percentage point from the previous year and grew by 7.2% in the first half with net sales up 7.1%.

Associates, Investments, People, Countries, Clients, Horizontality

Including 100% of associates and investments, the Group has annual revenue of over $28 billion and over 200,000 full-time people in over 3,000 offices in 113 countries, now including Cuba and Iran (through an affiliation agreement). The Group, therefore, has access to an unparalleled breadth and depth of marketing communications resources. It services 353 of the Fortune Global 500 companies, all 30 of the Dow Jones 30, 74 of the NASDAQ 100 and 781 national or multi-national clients in three or more disciplines. 494 clients are served in four disciplines and these clients account for almost 52% of Group revenue. This reflects the increasing opportunities for co-ordination between activities, both nationally and internationally. The Group also works with 400 clients in 6 or more countries. The Group estimates that well over a third of new assignments in the first half of the year were generated through the joint development of opportunities by two or more Group companies. Horizontality, or making sure our people in different disciplines work together for the benefit of clients, is clearly becoming an increasingly important part of client strategies, particularly as they continue to invest in brand in slower-growth markets and both capacity and brand in faster-growth markets.

Cash flow highlights

In the first half of 2016, operating profit was £554 million, non-cash exceptional losses £103 million, depreciation, amortisation and impairment £199 million, non-cash share-based incentive charges £52 million, net interest paid £81 million, tax paid £250 million, capital expenditure £143 million and other net cash inflows £25 million. Free cash flow available for working capital requirements, debt repayment, acquisitions, share re-purchases and dividends was, therefore, £459 million.

This free cash flow was absorbed by £226 million in net cash acquisition payments and investments (of which £21 million was for earnout payments with the balance of £205 million for investments and new acquisitions payments) and £197 million in share re-purchases, a total outflow of £423 million. This resulted in a net cash inflow of £36 million, before any changes in working capital and also reflects our strategic objectives of investing approximately £300-£400 million annually in acquisitions and investments and executing share buy-backs of 2-3% of the issued share capital.

A summary of the Group’s unaudited cash flow statement and notes as at 30 June 2016 is provided in Appendix 1.

13

Acquisitions

In line with the Group’s strategic focus on new markets, new media and data investment management, the Group completed 36 transactions in the first six months; 13 acquisitions and investments were in new markets and 23 in quantitative and digital. Of these, 9 were driven by individual client or agency needs and 9 were in both new markets and quantitative and digital.

Specifically, in the first six months of 2016, acquisitions and increased equity stakes have been completed in advertising and media investment management in the United Kingdom; in data investment management in the United States, Denmark, Greece, India and New Zealand; in public relations and public affairs in Canada, Switzerland, Turkey and Brazil; in branding & identity in the Netherlands; in direct, digital and interactive in the United States, the United Kingdom, Germany, China, Singapore, South Korea, Brazil, Colombia and Mexico; in healthcare in the United States; in sports marketing in the United States.

A further 6 acquisitions and investments were made in July and August, with two in advertising and media investment management in Turkey and Ecuador; and four in direct, digital and interactive in the United States, France, Turkey and China.

Balance sheet highlights

Average net debt in the first six months of 2016 was £3.986 billion, compared to £3.374 billion in 2015, at 2016 exchange rates. This represents an increase of £612 million. Net debt at 30 June 2016 was £4.249 billion, compared to £3.383 billion on 30 June 2015, an increase of £866 million. The increased average and period end net debt figures reflect significant net acquisition payments and share repurchases of £831 million, and a weakened pound sterling, offsetting a relative improvement in working capital.

Your Board continues to examine the allocation of its EBITDA of over £2.1 billion or over $2.7 billion, for the preceding twelve months and substantial free cash flow of over £1.2 billion, or over $1.6 billion per annum, also for the previous twelve months, to enhance share owner value. The Group’s current market capitalisation of £22.431 billion ($29.586 billion) implies an EBITDA multiple of 10.6 times, on the basis of the trailing 12 months EBITDA to 30 June 2016. Including net debt at 30 June of £4.249 billion, the Group’s enterprise value to EBITDA multiple is 12.6 times. The average net debt to EBITDA ratio is 1.89x, within the Group’s target range of 1.5-2.0x. Clearly, there may still be some scope for more leverage.

A summary of the Group’s unaudited balance sheet and notes as at 30 June 2016 is provided in Appendix 1.

Return of funds to share owners

As outlined in the June 2015 AGM statement, the achievement of the previously targeted pay-out ratio of 45% one year ahead of schedule, raised the question of whether the pay-out ratio target should be increased further. Following that review, your Board decided to up the dividend pay-out ratio to a target of 50%, to be achieved by 2017. Following your Company’s strong progress in 2015, the dividends were increased by 17% overall, with a balancing out of the interim and final dividend payments, representing a pay-out ratio of 47.7%. As a result of continuing strong progress in the first half of 2016, your Board declares an interim dividend of 19.55p per share, an increase of 22.9% and a pay-out ratio of 50% for the first half, achieving the newly targeted pay-out ratio.

During the first six months of 2016, 12.5 million shares, or 1.0% of the issued share capital, were purchased at a cost of £197 million and an average price of £15.70 per share.

14

Current trading

In July, like-for-like revenue and net sales were up 4.6% and 1.9% respectively. All regions and sectors (except data investment management) were positive, and showed a similar pattern to the first half, with advertising, media investment management, public relations and public affairs and specialist communications (including direct, digital and interactive) up strongly. The United Kingdom was stronger than the previous quarter, perhaps reflecting a post-Brexit vote recovery, driven by a weaker pound sterling. Cumulative like-for-like revenue and net sales growth for the first seven months of 2016 is now 4.3% and 3.5% respectively. The Group’s quarter 2 revised forecast, having been reviewed at the parent company level in the first half of August, indicates full year like-for-like revenue growth of well over 3% and net sales growth of over 3%, and a slightly weaker second half, partly reflecting more difficult comparatives in 2015 and the usual fourth quarter conservatism.

Outlook

Grinding it out

After another record year in 2015, the Group’s performance in the first seven months of the new financial year has been reasonably strong, as worldwide GDP growth, both nominal and real, seems to have slowed in the second half of last year and into the new year. Despite this, and pleasingly, bottom-line growth and operating margin improvement have been strong, above budget and last year and in line with target. Net sales growth in the second quarter was also better than the first quarter of 2015, with all geographies and sectors growing net sales on both a constant currency and like-for-like basis. Like-for-like revenue and net sales were up 4.3% and 3.8% respectively in the first six months, compared with 4.9% and 2.3% in the same period last year. Our operating companies are still hiring cautiously and responding to any geographic, functional and client changes in revenue – positive or negative. On a constant currency basis, operating profit is above budget and well ahead of last year and the increase in the net sales margin is in line with the Group’s full year target of a 0.3 margin points improvement, up 0.4 margin points on a reported basis and 0.3 margin points on a like-for-like basis.

Despite these encouraging results in the first half of 2016, good prospects for the rest of the year together with record results in 2015 in the Company’s thirtieth year, following sequential record results from 2011 onwards, clients generally remain cautious. Worldwide real and nominal GDP growth seem stuck in a range of 3.0-3.5%, with little inflation, consequently little or no pricing power for clients and a resultant focus on costs to achieve profit targets. Procurement and finance remain the dominant functions for understandable reasons, with marketing taking a back seat. Whilst there seems limited likelihood of a worldwide recession, that is two quarters of negative GDP growth globally, there have been and will be individual countries that go into recession, as Russia and Brazil already have and a post-Brexit United Kingdom might. This pressure on the top line growth rates has intensified, as the previously faster growth BRICs markets, with the exception of India, have lost their shine, even though the Western markets of the United States and United Kingdom and some Western Continental European markets, like Germany, Spain and Italy have perked up.

If you are running a legacy business, as many of our clients are, you face disrupters like Uber, Lyft and Airbnb at one end of the spectrum, zero-based cost budgeters like 3G and Coty at the other end, with seemingly short-term focused activist investors in the middle, like Nelson Peltz, Bill Ackman and Dan Loeb. There is, therefore, considerable pressure in the system. Moreover, the average managerial life expectancy of a United States CEO is currently 6-7 years, a CFO 5-6 years

15

and a CMO 2-3 years, although the latter has improved from 18 months recently! This cocktail of difficult trends result, logically, in a short-term focus, reinforced by the needs of quarterly reporting and similarly focused, short-term, institutional investor measurement and incentives.

Neither do the geo-political grey swans (known unknowns) help, let alone the possibility of black swans (unknown unknowns). In the immediate future, we face the implications of the June out Brexit vote in the United Kingdom, which may result, at least in the short-term or mid-term, in GDP weakness in the United Kingdom, the EU and possibly globally, let alone further political and economic uncertainty in the United Kingdom around Scottish Independence and further possible disintegration of the EU. Not forgetting the still unresolved question of Grexit, which has recently re-emerged or the upcoming elections in Europe. Political concerns also remain around the Ukraine, as well as the Middle East & Africa, including the migrant crisis and continued risk of terrorism. Add to this the potential impact of the rise of populism at both ends of the political spectrum in the United States Presidential election in November, although the risk of an unorthodox result seems to be diminishing. In the longer term, there are significant political and economic uncertainties surrounding three of the BRIC nations, Brazil, Russia and China, although we remain unabashed bulls on all three. However, all will take significant time to resolve, especially in the case of Russia. If all this was not enough, there are the continuing longer term fiscal deficit issues in the United States, the United Kingdom and the EU that have to be dealt with, along with the impact of the inevitable reversal of US, Japanese and EU quantitative easing and low interest policies at some point in time, although just as with global GDP growth, interest rates are likely to stay lower, longer than people anticipate.

Having said all this, there are positives. Countries and opportunities like Indonesia, the Philippines, Vietnam, Egypt, Nigeria, Mexico, Colombia and Peru and recently a post-Macri Argentina add to confidence. In addition maybe Cuba and even Iran (despite the continuing effective impact of sanctions, especially on US citizens) will also improve the sentiment along with a continuing mild recovery in Western Continental Europe.

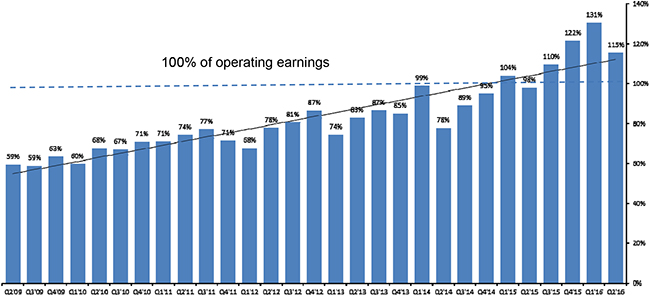

The impact of all this on corporates is clear. Multi-nationals are sitting on over $7 trillion of net cash and relatively unleveraged balance sheets. Caution, understandably, prevails and as a result, companies, in a sense, may be shrinking. Take for example the S&P 500. If you think of them as one company, share buy-backs and dividends are starting to exceed retained earnings and have done so in five out of the last six quarters.

S&P 500 Dividends & Buy-Backs as % of Operating Earnings

16

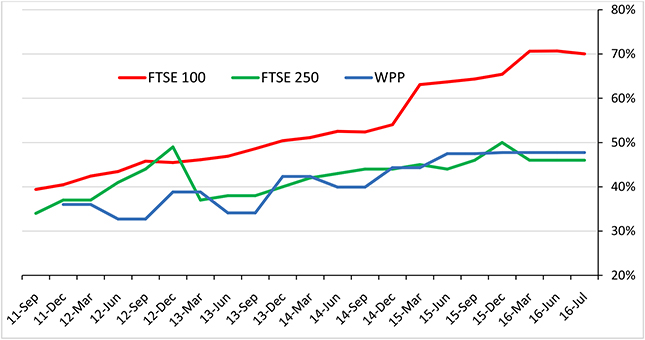

This chart clearly illustrates the conservatism that the current climate encourages, which has also had an impact on corporate investment as a proportion of GDP, which continues to decline, for example, in the United States. Corporate animal spirits are low. Interestingly, the companies that seem most expansive and willing to take risk are those that tend to offend good corporate governance, those that have controlled voting structures and consequently are prepared to take risks, without fear of failure and removal. And the habit is not confined to US listed companies. Take a look at the diminishing dividend cover of FTSE listed companies over recent years, which indicates increasing distribution of retained earnings.

Rising FTSE Dividend Pay-Out Ratios

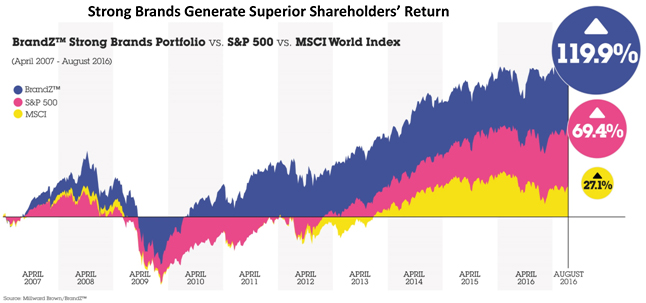

Needless to say, given what we do, we believe this approach to be a misguided one. There is a clear correlation between investment and innovation and long-term financial success. Take for example brand investment. If we and you had invested in the top ten brands in our annual BrandZ Top 100 Global Brands Financial Times survey over the last ten years, we would have outperformed the MSCI World Index by well over 400 per cent and the S&P 500 Index by almost 75%.

17

There is a clear correlation between investment in brands, top line like-for-like growth and total share owner return, through stock price appreciation. You cannot cost cut your way to long-term success. There is a finite limit to cutting costs, whilst there is no limit to top line growth, at least in theory, until you reach 100 per cent market share.

Despite this context, 2016’s first half top line growth has been above budget. Like-for-like revenue growth at 4.3%, was similar to the first half of 2015, with all geographies and sectors showing growth. Net sales growth, on the same basis, was up 3.8%, not as strong as the final quarter of 2015, but stronger than the full year growth of 3.3%. Our operating companies are still hiring cautiously and responding to any geographic, functional and client changes in revenue – positive or negative. On a constant currency basis, operating profit is well above budget and ahead of last year.

We see little reason, if any, for this pattern of behaviour to change in 2016, with continued caution being the watchword. There is certainly no evidence to suggest any such change in behaviour, although one or two institutional investors, including, most notably, Blackrock, Legal & General and the United Kingdom Government, are saying that they are tiring with some companies’ total focus on short-term cost cutting and would favour strategies based more on the long-term and top line growth and the end to quarterly reporting. Your Company, together with McKinsey & Co., Blackrock and Dow Chemical Co., amongst others, has joined an alliance to stimulate focus on long-term strategic thinking.

The pattern for 2016 looks very similar to 2015, but with the bonus of the maxi-quadrennial events of what has proven to be a visually-stunning Rio Olympics, a successful UEFA Euro Football Championships and, of course, the ratings-stimulating United States Presidential Election to boost marketing investments, as usual by up to 1% or so. Forecasts of worldwide real GDP growth for 2016 still hover around 3.0% to 3.5%, with recently reduced inflation estimates of 0.5% giving nominal GDP growth, in dollars (because of its strength), of even less than 3%. Advertising as a proportion of GDP should at least remain constant overall. Although it is still at relatively depressed historical levels, particularly in mature markets, post-Lehman, it should be buoyed by incremental branding investments in the under-branded faster growing markets.

18

Although consumers and corporates both seem to be increasingly cautious and risk averse, the latter should continue to purchase or invest in brands in both fast and slow growth markets to stimulate top line sales growth. Merger and acquisition activity may be regarded as an alternative way of doing this, particularly funded by cheap long-term debt, but we believe clients may regard this as a more risky way than investing in marketing and brand and hence growing market share, particularly as equity valuations continue to be strong. The recent, almost record spike in merger and acquisition activity, may be driven more by companies running out of cost-reduction opportunities in the existing businesses, rather than trying to find revenue growth opportunities or synergies. Although, in our own industry, the Bolloré Model, which unites ownership and control of telecommunications, media, content and agency services, is probably a unique approach, which challenges conventional wisdom.

Looking ahead to 2017, worldwide GDP forecasts by the so called experts indicate a slight strengthening, if anything, to 3.5-4.0%, real and nominal. If advertising as a percentage of GDP remains constant, which we believe it will, this should result in a similar growth rate for the industry. Although we are in the early stages of our rolling Three Year planning process and have not started the 2017 budgeting process, we see no reason why revenues and net sales cannot continue to grow at well over 3% and over 3% respectively in 2017, a very similar pattern to 2015 and 2016. Our new business record remains strong, despite recent bumps.

Financial guidance

For 2016, reflecting the first half net sales growth and quarter 2 revised forecast:

| n | Like-for-like revenue growth of well over 3% and net sales growth of over 3% |

| n | Target operating margin to net sales improvement of 0.3 margin points on a constant currency basis in line with full year margin target |

In 2016, our prime focus will remain on growing revenue and net sales faster than the industry average, driven by our leading position in the new markets, in new media, in data investment management, including data analytics and the application of technology, creativity, effectiveness and horizontality. At the same time, we will concentrate on meeting our operating margin objectives by managing absolute levels of costs and increasing our flexibility in order to adapt our cost structure to significant market changes and by ensuring that the benefits of the restructuring investments taken in 2014 and 2015 continue to be realised. The initiatives taken by the parent company in the areas of human resources, property, procurement, information technology and practice development continue to improve the flexibility of the Group’s cost base. Flexible staff costs (including incentives, freelance and consultants) remain close to historical highs of over 7% of net sales and continue to position the Group extremely well should current market conditions deteriorate.

The Group continues to improve co-operation and co-ordination among its operating companies in order to add value to our clients’ businesses and our people’s careers, an objective which has been specifically built into short-term incentive plans. We have, in addition, decided that an even more significant proportion, one-half, of operating company incentive pools are funded and allocated on the basis of Group-wide performance in 2016 and beyond. Horizontality has been accelerated through the appointment of 48 global client leaders for our major clients, accounting for approaching one third of total revenue of over $19 billion and 19 country and regional managers in a growing number of test markets and sub-regions, amounting to about half of the 113 countries in which we operate. Emphasis has been laid on knowledge-sharing in the areas of media investment management, healthcare, sustainability, government, new technologies, new markets, retailing, shopper marketing, internal communications, financial services and media, sport and entertainment. The Group continues to succeed, in co-ordinating investment geographically and functionally through parent company initiatives and winning Group pitches, despite one or two recent disappointments. For example, the Group has been very successful in

19

the recent wave of consolidation in the fast-moving consumer goods, travel, pharmaceutical and shopper marketing industries and the resulting “team” pitches. Whilst talent and creativity (in its broadest sense) remain the key potential differentiators between us and our competitors, increasingly differentiation can also be achieved in three additional ways – through application of technology, for example, Xaxis and AppNexus; through integration of data investment management, for example, Kantar and comScore; and lastly investment in content, for example, Imagina, Vice, Refinery 29, Truffle Pig, Media Rights Capital, Fullscreen, Indigenous Media, China Media Capital, Chime and Bruin.

Our business remains geographically and functionally well positioned to compete successfully and to deliver on our long-term targets:

| n | Revenue and net sales growth greater than the industry average |

| n | Improvement in net sales margin of 0.3 margin points or more, excluding the impact of currency, depending on net sales growth and staff cost to net sales ratio improvement of 0.2 margin points or more |

| n | Annual headline diluted EPS growth of 10% to 15% p.a. delivered through revenue growth, margin expansion, acquisitions and share buy-backs |

For further information:

| Sir Martin Sorrell |

} |

|||

| Paul Richardson |

} |

|||

| Lisa Hau |

} |

+44 20 7408 2204 | ||

| Feona McEwan |

} |

|||

| Chris Wade |

} |

|||

| Kevin McCormack |

} |

|||

| Fran Butera |

} |

+1 212 632 2235 | ||

| Juliana Yeh |

+852 2280 3790 | |||

www.wpp.com/investor

This announcement has been filed at the Company Announcements Office of the London Stock Exchange and is being distributed to all owners of Ordinary shares and American Depository Receipts. Copies are available to the public at the Company’s registered office.

The following cautionary statement is included for safe harbour purposes in connection with the Private Securities Litigation Reform Act of 1995 introduced in the United States of America. This announcement may contain forward-looking statements within the meaning of the US federal securities laws. These statements are subject to risks and uncertainties that could cause actual results to differ materially including adjustments arising from the annual audit by management and the Company’s independent auditors. For further information on factors which could impact the Company and the statements contained herein, please refer to public filings by the Company with the Securities and Exchange Commission. The statements in this announcement should be considered in light of these risks and uncertainties.

| Appendix 1: Interim results for the six months ended 30 June 2016 | 20 |

Unaudited condensed consolidated interim income statement for the six months ended 30 June 2016

| £ million |

|

Notes |

|

|

Six months ended 30 June |

|

|

Six months ended 30 June |

|

+/(-) | % |

|

Constant Currency1 +/(-) |

% |

|

Year ended 31 December 2015 |

| |||||||||

| Billings |

25,318.8 | 23,156.4 | 9.3 | 6.3 | 47,631.9 | |||||||||||||||||||||

| Revenue |

6 | 6,536.5 | 5,839.4 | 11.9 | 8.9 | 12,235.2 | ||||||||||||||||||||

| Direct costs |

(942.7 | ) | (798.7 | ) | (18.0 | ) | (14.0 | ) | (1,710.9 | ) | ||||||||||||||||

| Net sales |

6 | 5,593.8 | 5,040.7 | 11.0 | 8.1 | 10,524.3 | ||||||||||||||||||||

| Operating costs |

4 | (5,040.2 | ) | (4,251.8 | ) | (18.5 | ) | (16.2 | ) | (8,892.3 | ) | |||||||||||||||

| Operating profit |

553.6 | 788.9 | (29.8 | ) | (34.9 | ) | 1,632.0 | |||||||||||||||||||

| Share of results of associates |

4 | 15.9 | 16.0 | (0.6 | ) | (5.6 | ) | 47.0 | ||||||||||||||||||

| Profit before interest and taxation |

569.5 | 804.9 | (29.2 | ) | (34.4 | ) | 1,679.0 | |||||||||||||||||||

| Finance income |

5 | 43.1 | 38.1 | 13.1 | 15.2 | 72.4 | ||||||||||||||||||||

| Finance costs |

5 | (122.1 | ) | (111.5 | ) | (9.5 | ) | (4.7 | ) | (224.1 | ) | |||||||||||||||

| Revaluation of financial instruments |

5 | (65.4 | ) | (21.8 | ) | - | - | (34.7 | ) | |||||||||||||||||

| Profit before taxation |

425.1 | 709.7 | (40.1 | ) | (45.5 | ) | 1,492.6 | |||||||||||||||||||

| Taxation |

7 | (143.1 | ) | (108.6 | ) | (31.8 | ) | (30.5 | ) | (247.5 | ) | |||||||||||||||

| Profit for the period |

282.0 | 601.1 | (53.1 | ) | (58.8 | ) | 1,245.1 | |||||||||||||||||||

| Attributable to: |

||||||||||||||||||||||||||

| Equity holders of the parent |

245.8 | 566.2 | (56.6 | ) | (62.5 | ) | 1,160.2 | |||||||||||||||||||

| Non-controlling interests |

36.2 | 34.9 | (3.7 | ) | (4.1 | ) | 84.9 | |||||||||||||||||||

| 282.0 | 601.1 | (53.1 | ) | (58.8 | ) | 1,245.1 | ||||||||||||||||||||

| Headline PBIT |

6,19 | 768.7 | 669.1 | 14.9 | 10.3 | 1,774.0 | ||||||||||||||||||||

| Net sales margin |

6,19 | 13.7 | % | 13.3 | % | 0.4 | 2 | 0.3 | 2 | 16.9 | % | |||||||||||||||

| Headline PBT |

19 | 689.7 | 595.7 | 15.8 | 11.7 | 1,622.3 | ||||||||||||||||||||

| Earnings per share |

||||||||||||||||||||||||||

| Basic earnings per ordinary share |

9 | 19.1 | p | 43.7 | p | (56.3 | ) | (62.2 | ) | 90.0 | p | |||||||||||||||

| Diluted earnings per ordinary share |

9 | 18.9 | p | 43.0 | p | (56.0 | ) | (62.0 | ) | 88.4 | p | |||||||||||||||

1 The basis for calculating the constant currency percentage changes shown above and in the notes to this appendix are described in the glossary attached to this appendix.

2 Margin points.

21

Unaudited condensed consolidated interim statement of comprehensive income for the six months ended 30 June 2016

| £ million | Six months ended 30 June 2016 |

Six months ended 30 June 2015 |

Year ended 31 December |

|||||||||

| Profit for the period |

282.0 | 601.1 | 1,245.1 | |||||||||

| Items that may be reclassified subsequently to profit or loss: |

||||||||||||

| Exchange adjustments on foreign currency net investments |

990.9 | (316.0 | ) | (275.9 | ) | |||||||

| (Loss)/gain on revaluation of available for sale investments |

(1.4 | ) | (2.1 | ) | 206.0 | |||||||

| 989.5 | (318.1 | ) | (69.9 | ) | ||||||||

| Items that will not be reclassified subsequently to profit or loss: |

||||||||||||

| Actuarial gain on defined benefit pension plans | - | - | 33.5 | |||||||||

| Deferred tax on defined benefit pension plans | - | - | (5.2 | ) | ||||||||

| - | - | 28.3 | ||||||||||

| Other comprehensive income/(loss) relating to the period |

989.5 | (318.1 | ) | (41.6 | ) | |||||||

| Total comprehensive income relating to the period | 1,271.5 | 283.0 | 1,203.5 | |||||||||

| Attributable to: | ||||||||||||

| Equity holders of the parent | 1,199.7 | 257.0 | 1,121.6 | |||||||||

| Non-controlling interests | 71.8 | 26.0 | 81.9 | |||||||||

| 1,271.5 | 283.0 | 1,203.5 | ||||||||||

22

Unaudited condensed consolidated interim cash flow statement for the six months ended 30 June 2016

| £ million | Notes | Six months ended 30 June 2016 |

Six months 30 June 2015 |

Year ended 31 December |

||||||||||

| Net cash inflow/(outflow) from operating activities |

10 | 66.2 | (180.7 | ) | 1,359.9 | |||||||||

| Investing activities |

||||||||||||||

| Acquisitions and disposals |

10 | (182.8 | ) | (459.3 | ) | (669.5 | ) | |||||||

| Purchase of property, plant and equipment |

(126.7 | ) | (73.1 | ) | (210.3 | ) | ||||||||

| Purchase of other intangible assets (including capitalised computer software) |

(15.9 | ) | (17.0 | ) | (36.1 | ) | ||||||||

| Proceeds on disposal of property, plant and equipment |

9.7 | 11.2 | 13.4 | |||||||||||

| Net cash outflow from investing activities |

(315.7 | ) | (538.2 | ) | (902.5 | ) | ||||||||

| Financing activities |

||||||||||||||

| Share option proceeds |

5.3 | 5.4 | 27.6 | |||||||||||

| Cash consideration for non-controlling interests |

10 | (43.4 | ) | (7.9 | ) | (23.6 | ) | |||||||

| Share repurchases and buybacks |

10 | (196.8 | ) | (405.4 | ) | (587.6 | ) | |||||||

| Net (decrease)/increase in borrowings |

10 | (62.9 | ) | 141.1 | 492.0 | |||||||||

| Financing and share issue costs |

(0.5 | ) | (9.0 | ) | (11.4 | ) | ||||||||

| Equity dividends paid |

- | - | (545.8 | ) | ||||||||||

| Dividends paid to non-controlling interests in subsidiary undertakings |

(35.0 | ) | (25.7 | ) | (55.2 | ) | ||||||||

| Net cash outflow from financing activities |

(333.3 | ) | (301.5 | ) | (704.0 | ) | ||||||||

| Net decrease in cash and cash equivalents |

(582.8 | ) | (1,020.4 | ) | (246.6 | ) | ||||||||

| Translation differences |

237.3 | (39.9 | ) | (54.4 | ) | |||||||||

| Cash and cash equivalents at beginning of period |

1,946.6 | 2,247.6 | 2,247.6 | |||||||||||

| Cash and cash equivalents at end of period |

10 | 1,601.1 | 1,187.3 | 1,946.6 | ||||||||||

| Reconciliation of net cash flow to movement in net debt: |

||||||||||||||

| Net decrease in cash and cash equivalents |

(582.8 | ) | (1,020.4 | ) | (246.6 | ) | ||||||||

| Cash outflow/(inflow) from decrease/(increase) in debt financing |

63.4 | (132.1 | ) | (480.5 | ) | |||||||||

| Debt acquired |

(144.4 | ) | - | - | ||||||||||

| Other movements |

(46.4 | ) | (108.0 | ) | (124.0 | ) | ||||||||

| Translation differences |

(327.9 | ) | 153.2 | (84.3 | ) | |||||||||

| Movement of net debt in the period |

(1,038.1 | ) | (1,107.3 | ) | (935.4 | ) | ||||||||

| Net debt at beginning of period |

(3,210.8 | ) | (2,275.4 | ) | (2,275.4 | ) | ||||||||

| Net debt at end of period |

11 | (4,248.9 | ) | (3,382.7 | ) | (3,210.8 | ) | |||||||

23

Unaudited condensed consolidated interim balance sheet as at 30 June 2016

| £ million | Notes | 30 June 2016 |

30 June 2015 |

31 December 2015 |

||||||||||||

| Non-current assets |

||||||||||||||||

| Intangible assets: |

||||||||||||||||

| Goodwill |

12 | 12,293.5 | 10,057.3 | 10,670.6 | ||||||||||||

| Other |

13 | 2,036.7 | 1,714.2 | 1,715.4 | ||||||||||||

| Property, plant and equipment |

925.9 | 731.1 | 797.7 | |||||||||||||

| Interests in associates and joint ventures |

690.8 | 694.3 | 758.6 | |||||||||||||

| Other investments |

1,303.7 | 920.9 | 1,158.7 | |||||||||||||

| Deferred tax assets1 |

94.0 | 107.6 | 94.1 | |||||||||||||

| Trade and other receivables |

14 | 254.9 | 141.9 | 178.7 | ||||||||||||

| 17,599.5 | 14,367.3 | 15,373.8 | ||||||||||||||

| Current assets |

||||||||||||||||

| Inventory and work in progress |

408.8 | 321.7 | 329.0 | |||||||||||||

| Corporate income tax recoverable |

224.2 | 168.1 | 168.6 | |||||||||||||

| Trade and other receivables |

14 | 11,751.1 | 9,985.0 | 10,495.4 | ||||||||||||

| Cash and short-term deposits |

2,147.4 | 1,353.0 | 2,382.4 | |||||||||||||

| 14,531.5 | 11,827.8 | 13,375.4 | ||||||||||||||

| Current liabilities |

||||||||||||||||

| Trade and other payables |

15 | (13,868.2 | ) | (11,359.8 | ) | (12,685.0 | ) | |||||||||

| Corporate income tax payable2 |

(584.0 | ) | (571.9 | ) | (598.5 | ) | ||||||||||

| Bank overdrafts and loans |

(1,057.2 | ) | (518.7 | ) | (932.0 | ) | ||||||||||

| (15,509.4 | ) | (12,450.4 | ) | (14,215.5 | ) | |||||||||||

| Net current liabilities |

(977.9 | ) | (622.6 | ) | (840.1 | ) | ||||||||||

| Total assets less current liabilities |

16,621.6 | 13,744.7 | 14,533.7 | |||||||||||||

| Non-current liabilities |

||||||||||||||||

| Bonds and bank loans |

(5,339.1 | ) | (4,217.0 | ) | (4,661.2 | ) | ||||||||||

| Trade and other payables |

16 | (1,122.0 | ) | (707.5 | ) | (891.5 | ) | |||||||||

| Deferred tax liabilities1 |

(713.0 | ) | (556.1 | ) | (552.3 | ) | ||||||||||

| Provisions for post-employment benefits |

(260.4 | ) | (283.3 | ) | (229.3 | ) | ||||||||||

| Provisions for liabilities and charges |

(208.9 | ) | (173.2 | ) | (183.6 | ) | ||||||||||

| (7,643.4 | ) | (5,937.1 | ) | (6,517.9 | ) | |||||||||||

| Net assets |

8,978.2 | 7,807.6 | 8,015.8 | |||||||||||||

| Equity |

||||||||||||||||

| Called-up share capital |

17 | 133.0 | 132.7 | 132.9 | ||||||||||||

| Share premium account |

540.5 | 513.3 | 535.3 | |||||||||||||

| Shares to be issued |

- | 0.1 | - | |||||||||||||

| Other reserves |

824.4 | (226.0 | ) | (9.7 | ) | |||||||||||

| Own shares |

(760.7 | ) | (572.2 | ) | (719.6 | ) | ||||||||||

| Retained earnings |

7,782.5 | 7,619.6 | 7,698.5 | |||||||||||||

| Equity share owners’ funds |

8,519.7 | 7,467.5 | 7,637.4 | |||||||||||||

| Non-controlling interests |

458.5 | 340.1 | 378.4 | |||||||||||||

| Total equity |

8,978.2 | 7,807.6 | 8,015.8 | |||||||||||||

1 The Group has restated the balance sheet as at 30 June 2015 to reduce both the deferred tax assets and the deferred tax liabilities by £140.7 million. This is consistent with the current period presentation.

2 The Group has restated the balance sheet as at 30 June 2015 to reclassify £533.6 million of corporate income tax payable from non-current liabilities to current liabilities. This is consistent with the current period presentation.

24

Unaudited condensed consolidated interim statement of changes in equity for the six months ended 30 June 2016

| £ million | Called-up share capital |

Share premium account |

Other reserves |

Own shares |

Retained earnings |

Total equity share owners’ funds |

Non- controlling |

Total | ||||||||||||||||||||||||

| Balance at 1 January 2016 |

132.9 | 535.3 | (9.7 | ) | (719.6 | ) | 7,698.5 | 7,637.4 | 378.4 | 8,015.8 | ||||||||||||||||||||||

| Ordinary shares issued |

0.1 | 5.2 | - | - | - | 5.3 | - | 5.3 | ||||||||||||||||||||||||

| Treasury share additions |

- | - | - | (148.5 | ) | - | (148.5 | ) | - | (148.5 | ) | |||||||||||||||||||||

| Treasury share allocations |

- | - | - | 3.5 | (3.5 | ) | - | - | - | |||||||||||||||||||||||

| Net profit for the period |

- | - | - | - | 245.8 | 245.8 | 36.2 | 282.0 | ||||||||||||||||||||||||

| Exchange adjustments on foreign currency net investments | - | - | 955.3 | - | - | 955.3 | 35.6 | 990.9 | ||||||||||||||||||||||||

| Loss on revaluation of available for sale investments |

- | - | (1.4 | ) | - | - | (1.4 | ) | - | (1.4 | ) | |||||||||||||||||||||

| Comprehensive income |

- | - | 953.9 | - | 245.8 | 1,199.7 | 71.8 | 1,271.5 | ||||||||||||||||||||||||

| Dividends paid |

- | - | - | - | - | - | (35.0 | ) | (35.0 | ) | ||||||||||||||||||||||

| Non-cash share-based incentive plans (including share options) |

- | - | - | - | 52.0 | 52.0 | - | 52.0 | ||||||||||||||||||||||||

| Tax adjustments on share-based payments |