As filed with the Securities and Exchange Commission on January 27, 2023

Securities Act Registration No. 033‑10451

Investment Company Act Registration No. 811‑04920

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 X

Post-Effective Amendment No. 123 X

and/or

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 X

Amendment No. 125 X

(Check appropriate box or boxes)

(Exact Name of Registrant as Specified in Charter)

505 Wakara Way, 3rd Floor

Salt Lake City, UT 84108

(Address of Principal Executive Offices)

Registrant’s Telephone Number, including Area Code: (801) 533‑0777

| (Name and Address of Agent for Service) | Copy to: | |

| Eric S. Bergeson Wasatch Advisors LP 505 Wakara Way, 3rd Floor Salt Lake City, UT 84108 |

Eric F. Fess Chapman and Cutler LLP 320 S. Canal Street Chicago, IL 60606 | |

Approximate Date of Proposed Public Offering: As soon as practicable following effectiveness.

It is proposed that this filing will become effective:

| ( ) | immediately upon filing pursuant to paragraph (b) |

| (X) | on |

| ( ) | 60 days after filing pursuant to paragraph (a)(1) |

| ( ) | on pursuant to paragraph (a)(1) |

| ( ) | 75 days after filing pursuant to paragraph (a)(2) |

| ( ) | on pursuant to paragraph (a)(2) of Rule 485. |

If appropriate, check the following box:

( ) this Post-Effective Amendment designates a new effective date for a previously filed Post-Effective Amendment.

WASATCHGLOBAL.COM JANUARY 31, 2023 2023 Prospectus Fund Investor Institutional. Fund Investor Institutional. Name Class Class Name Class Class Wasatch Core Growth Fund WGROX WIGRX Wasatch International Opportunities Fund WAIOX WIIOX Wasatch Emerging India Fund WAINX WIINX Wasatch International Select Fund WAISX WGISX Wasatch Emerging Markets Select Fund WAESX WIESX Wasatch Long/Short Alpha Fund WALSX WGLSX Wasatch Emerging Markets Small Cap Fund WAEMX WIEMX Wasatch Micro Cap Fund WMICX WGICX Wasatch Frontier Emerging Small Wasatch Micro Cap Value Fund WAMVX WGMVX Countries Fund WAFMX WIFMX Wasatch Small Cap Growth Fund WAAEX WIAEX Wasatch Global Opportunities Fund WAGOX WIGOX Wasatch Small Cap Value Fund WMCVX WICVX Wasatch Global Select Fund WAGSX WGGSX Wasatch Ultra Growth Fund WAMCX WGMCX Wasatch Global Value Fund FMIEX WILCX Wasatch U.S. Select Fund WAUSX WGUSX Wasatch Greater China Fund WAGCX WGGCX Wasatch-Hoisington U.S. Treasury Fund WHOSX _______˼ Wasatch International Growth Fund WAIGX WIIGX

Table of Contents

1

Wasatch Core Growth Fund® — Summary

Investment Objectives

Fees and Expenses of the Fund

The tables below describe the fees and expenses that you may pay if you buy, hold and sell shares of the Fund.

You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Investor Class Shares |

Institutional Class Shares | |

| Maximum Sales Charge (Load) Imposed on Purchases (as a % of offering price) | ||

| Redemption Fee (as a % of amount redeemed on shares held 60 days or less) | ||

| Exchange Fee |

| Investor Class Shares |

Institutional Class Shares | ||

| Management Fee | |||

| Other Expenses | |||

| Total Annual Fund Operating Expenses | |||

| Expense Reimbursement | ( | ||

| Total Annual Fund Operating Expenses After Expense Reimbursement1 |

| 1 | |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invested $10,000 in the applicable class of the Fund for the time periods indicated and then redeemed all of your shares at the end of those periods. The example also assumes that your investment had a 5% return each year and that operating expenses (as a percentage of net assets) of the Fund remained the same. This example reflects contractual fee waivers and reimbursements through January 31, 2024. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Core Growth Fund — Investor Class | $ |

$ |

$ |

$ |

| Core Growth Fund — Institutional Class | $ |

$ |

$ |

$ |

2

January 31, 2023

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). Higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 29 % of the average value of its portfolio.

3

Wasatch Core Growth Fund® — Summary

Principal Strategies

The Fund invests primarily in smaller growing companies at reasonable prices.

Under normal market conditions, we will invest the Fund’s net assets primarily in the equity securities, typically common stock, of smaller growing companies. We consider these companies to be companies we believe have typically exhibited consistent growth in earnings per share and that are relatively small, with minimum market capitalizations of $100 million and up to a maximum market capitalization at the time of purchase of $5 billion or the market capitalization of the largest company in the Russell 2000® Index as of its most recent reconstitution date, whichever is greater. The Russell 2000 Index reconstitution date is typically each year on or around July 1. As of the 2022 reconstitution date, the market capitalization of companies included in the Russell 2000 Index ranged from $27.8 million to $10.2 billion. The market capitalizations for the range of companies in the Russell 2000 Index are subject to change at its next reconstitution date.

The Fund may invest up to 20% of the Fund’s total assets in the equity securities (typically common stock) of foreign companies (companies that are incorporated in any country outside the United States and whose securities principally trade outside the United States). Securities issued by companies incorporated outside the United States whose securities are principally traded in the United States are not defined as foreign companies and are not subject to this limitation.

We focus on companies that we consider to be high quality. We use a process of “bottom-up” fundamental analysis to look for individual companies that we believe are stable and have the potential to grow steadily for long periods of time. Our analysis may include studying a company’s financial statements, building proprietary financial models, visiting company facilities, and meeting with executive management, suppliers and customers.

The Fund seeks to purchase stocks at prices we believe are reasonable relative to our projection of a company’s long-term earnings growth rate. The Fund’s secondary objective of income is achieved when fast growing portfolio companies pay dividends, generated by cash flow, typically after achieving growth targets.

The Fund may invest a large percentage of its assets (greater than 5%) in a particular region or market.

The Fund may invest a large percentage of its assets (greater than 5%) in a few sectors. As of the date of this Prospectus, these sectors were materials, heath care, consumer discretionary, industrials, financials, and information technology.

Principal Risks

The Fund is subject to the following principal investment risks:

Market Risk. Market risk is the risk that a particular security, or shares of the Fund in general, may fall in value. Securities are subject to market fluctuations caused by such factors as economic, political, regulatory or market developments, changes in interest rates and perceived trends in securities prices. Shares of the Fund could decline in value or underperform other investments due to, among other things, market movements over the short-term or over longer periods during more prolonged market downturns. In addition, local, regional or global events such as war, acts of terrorism, spread of infectious diseases or other public health issues, recessions, or other events could have a significant negative impact on the Fund and its investments. Such events may affect certain geographic regions, countries, sectors and industries more significantly than others. Such events could adversely affect the prices and liquidity of the Fund’s portfolio securities or other instruments and could result in disruptions in the trading markets. Any of such circumstances could have a materially negative impact on the value of the Fund’s shares and result in increased market volatility.

Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates rise or economic conditions deteriorate.

Additional Market Disruption Risk. In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Although the hostilities between the two countries may escalate and any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the

4

January 31, 2023

ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly.

Global Pandemic Risk. The value of the Fund’s investments may be impacted by global health crises or other events. For example, an outbreak of the respiratory disease designated as Covid-19 was first detected in China in December 2019 and subsequently spread internationally. The transmission of Covid-19 and efforts to contain its spread have resulted in international, national and local border closings and other significant travel restrictions and disruptions; significant disruptions to business operations across many industries, to supply chains and to customer activity; and have resulted in event cancellations and restrictions; service cancellations, reductions and other changes; significant challenges in health care service preparation and delivery; and quarantines, as well as general concern and uncertainty that has negatively affected the economic environment. These impacts also have caused significant market volatility and disruption which may continue over extended periods. The ultimate impact of Covid-19 or other health emergencies on the domestic and global economies is impossible to predict accurately. Less developed countries and their health systems may be more vulnerable to these impacts. The impact of this Covid-19 pandemic may be short term or may last for an extended period of time, and in either case could result in a substantial economic downturn or recession and may adversely impact the value of an investment in the Fund.

Stock Market Risk. The Fund’s investments may decline in value due to movements in the overall stock market.

Stock Selection Risk. The Fund is actively managed, and its performance therefore will reflect, in part, the ability of the portfolio manager(s) to select investments and to make investment decisions that are suited to achieving the Fund’s investment objective. The Advisor does not actively track the composition or weightings of market indexes (including the Fund’s benchmark index) or of the broader markets generally. As a result, the Fund could underperform its benchmark index and/or other funds with a similar investment objective and/or strategy or it may lose value even when the overall stock market is not in general decline.

Equity Securities Risk. Equity securities represent ownership in a company. They may be traded (bought or sold) on a securities exchange or stock market. Stock markets are volatile. The price of equity securities will fluctuate and can decline and reduce the value of a portfolio invested in equity securities. The value of equity securities purchased by the Fund could decline if the financial condition of the companies in which the Fund invests declines or if overall market and economic conditions deteriorate. The value of equity securities may also decline due to factors that affect a particular industry or industries such as labor shortages, an increase in production costs and changes in competitive conditions within an industry. In addition, the value of equity securities may decline due to, among other things, general market conditions not specifically related to a company or industry such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, changes in government regulations, the political situation, or generally adverse investor sentiment. Certain equity securities may be less liquid, meaning that they may be difficult to sell at a time or price that is desirable, than other types of securities, or they may be illiquid. Some securities exchanges or stock markets may also be less liquid or illiquid due to low trading volume. In addition, equity securities include common stock. Common stock holds the lowest priority in the capital structure of a company and therefore takes the largest share of the company’s risk and its accompanying volatility. The rights of common stockholders generally are subordinate to all other claims on a company’s assets, including preferred stockholders and debt holders with respect to the payment of dividends and upon the liquidation or bankruptcy of the issuing company. The common stock of a company that experiences financial distress may lose significant value or become worthless, and therefore the Fund could lose money if a company in which it invests becomes financially distressed.

Liquidity Risk. In addition, the trading market for a particular security or type of security in which the Fund invests may be significantly less liquid than developed or even emerging markets, and there may be little or no trading volume for a period of time for a particular security. Reduced liquidity will have an adverse impact on the Fund’s ability to sell such securities quickly at a desired price when necessary to meet the Fund’s liquidity needs or in response to a specific economic event. It may be difficult at times to sell such securities at any price, which could impact not only the daily net asset value (NAV) of the Fund, but also the composition of the portfolio if other securities must be sold to meet the Fund’s liquidity needs. Additionally, market quotations for such securities may be volatile and thus affect the daily NAV of the Fund.

5

Wasatch Core Growth Fund® — Summary

Smaller Company Stock Risk. Small- and mid-cap stocks may be very sensitive to changing economic conditions and market downturns. In particular, the issuers of small company stocks have more narrow markets for their products and services, fewer product lines, and more limited managerial and financial resources than larger issuers. The stocks of small companies may therefore be more volatile and the ability to sell these stocks at a desirable time or price may be more limited.

Growth Stock Risk. Growth stock prices may be more sensitive to changes in companies’ current or expected earnings than the prices of other stocks, and growth stock prices may fall or may not appreciate in step with the broader securities markets. Growth companies may be newer or smaller companies and may retain a large part of their earnings for research, development or investments in capital assets.

Sector and Industry Weightings Risk. To the extent the Fund emphasizes, from time to time, investments in a particular sector, the Fund will be subject to a greater degree to the risks particular to that sector, including the sectors described below. Market conditions, interest rates, and economic, political, regulatory, or financial developments could significantly affect all the securities in a single sector. If the Fund invests in a few sectors, it may have increased exposure to the price movements of securities in those sectors. The Fund may also from time to time make significant investments in an industry or industries within a particular sector. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. Adverse conditions in such industry or industries could have a correspondingly adverse effect on the financial condition of issuers. These conditions may cause the value of the Fund’s shares to fluctuate more than the values of shares of funds that invest in a greater variety of investments.

Materials Sector Risk. The materials sector includes companies in the chemicals, construction materials, containers and packaging, metals and mining, and paper and forest products industries. Changes in world events, political, environmental and economic conditions, energy conservation, environmental policies, commodity price volatility, changes in currency exchange rates, imposition of import and export controls, increased competition, and labor relations may adversely affect companies engaged in the production and distribution of materials. Other risks may include liabilities for environmental damage, depletion of resources, and mandated expenditures for safety and pollution control. Companies in the chemicals industry may be subject to risks associated with the production, handling and disposal of hazardous components. Metals and mining companies could be affected by supply and demand, operational costs, and liabilities for environmental damage.

Health Care Sector Risk. The health care sector includes companies in the health care equipment and services, and pharmaceuticals, biotechnology and life sciences industry groups. Health care companies are strongly affected by worldwide scientific or technological developments. Their products may rapidly become obsolete. Many health care companies are also subject to significant government regulation and may be affected by changes in government policies. Companies in the pharmaceuticals, biotechnology and life sciences industry group in particular are heavily dependent on patent protection, and the expiration of patents may adversely affect the profitability of such companies. These companies are also subject to extensive litigation based on product liability and other similar claims. Many new products are subject to government approval and the process of obtaining government approval can be long and costly, and even approved products are susceptible to obsolescence. These companies are also subject to competitive forces that may make it difficult to increase prices, or that may lead to price reductions.

Consumer Discretionary Sector Risk. The consumer discretionary sector includes companies in industries such as consumer services, household durables, leisure products, textiles, apparel and luxury goods, hotels, restaurants, retailing, e-commerce, and automobiles. Companies in the consumer discretionary sector may be significantly impacted by the performance of the overall domestic and global economy and by interest rates. The consumer discretionary sector relies heavily on disposable household income and spending. Companies in this sector may be subject to severe competition, which may have an adverse impact on their respective profitability. The retail industry can be significantly affected by changes in demographics, and consumer tastes and shopping habits, which can also affect the demand for, and success of, consumer products and services in the marketplace. The automotive industry is highly cyclical and can be significantly affected by labor relations and fluctuating component prices.

Industrials Sector Risk. The industrials sector includes companies in the capital goods, commercial and professional services and transportation industry groups, including companies engaged in the business of human capital management, business research and consulting, air freight and logistics, airlines, maritime shipping and transportation, railroads and trucking, transportation infrastructure, and aerospace and defense. Companies in the industrials sector can be significantly affected by general economic trends, including such factors as employment and economic growth, interest rate changes, changes in consumer spending, legislative and government regulation and spending, import controls, commodity prices, and worldwide competition. Changes in the economy, fuel prices, labor agreements, and insurance costs may result in occasional sharp price movements in transportation securities. Aerospace and defense companies rely, to a significant extent, on government demand for their products and services. The financial condition of, and investor interest in, aerospace and defense companies are heavily influenced by government defense spending policies.

6

January 31, 2023

Financials Sector Risk. The financials sector includes companies in the banks, diversified financials, and insurance industry groups. Companies in the financials sector are subject to extensive government regulation, can be subject to relatively rapid change due to increasingly blurred distinctions between service segments, and can be significantly affected by the availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition. Banking companies, including thrifts and mortgage finance and consumer finance companies, may be affected by extensive government regulation, which may limit both the amounts and types of loans and other financial commitments they can make, the interest rates and fees they can charge, and the amount of capital they must maintain. Profitability is largely dependent on the availability and cost of capital funds, and can fluctuate significantly when interest rates change. Credit losses resulting from financial difficulties of borrowers can negatively affect banking companies. Banking companies may also be subject to severe price competition. Competition is high among banking companies and failure to maintain or increase market share may result in lost market value. Capital markets, a sub-industry of diversified financials, may be affected by extensive government regulation as well as economic and other financial events that could cause fluctuations in the stock market, impacting the overall value of investments. The insurance industry may be affected by extensive government regulation and can be significantly affected by interest rates, general economic conditions, and price and marketing competition. Different segments of the insurance industry can be significantly affected by natural disasters, mortality and morbidity rates, and environmental clean-up.

Information Technology Sector Risk. The information technology sector includes companies in the software and services, technology hardware and equipment, and semiconductors and semiconductor equipment industry groups. Companies in the information technology sector are subject to rapid obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. Stocks of companies in the information technology sector, especially those of smaller, less-seasoned companies, tend to be more volatile than the overall market. Technological developments, fixed rate pricing, and the ability to retain skilled employees can significantly affect the industries in the information technology sector. Additionally, success in the internet services and infrastructure industry is subject to continued demand for internet services.

Foreign Securities Risk. Foreign securities are generally more volatile and less liquid than U.S. securities. Further, foreign securities may be subject to additional risks not associated with investments in U.S. securities. Differences in the economic and political environment, the amount of available public information, the amount of taxation, limitations on the use or transfer of Fund assets, the degree of market regulation, settlement practices, the potential for permanent or temporary termination of trading, and financial reporting, accounting and auditing standards, and, in the case of foreign currency-denominated securities, fluctuations in currency exchange rates, can have a significant effect on the value of a foreign security. More specifically, changes in currency exchange rates will affect the value of non-U.S. securities, the value of dividends and interest earned from such securities and gains and losses realized on the sale of such securities. The value of an investment denominated in a foreign currency will decline in U.S. dollar terms if that currency weakens against the U.S. dollar. The Fund may be invested in the local currency of a foreign country in connection with executing foreign securities transactions. When the Fund executes the securities transactions, there is the risk of the value of the foreign currency increasing or decreasing against the value of the U.S. dollar. While the Fund is permitted to hedge currency risks, the Advisor does not anticipate doing so at this time. Additionally, certain countries may restrict foreign investment in their securities and may utilize formal or informal currency-exchange controls or “capital controls.” Capital controls may impose restrictions on the Fund’s ability to repatriate investments or income. Such capital controls can also have a significant effect on the value of the Fund’s holdings.

Operational and Cybersecurity Risk. Cybersecurity breaches may allow an unauthorized party to gain access to Fund assets, customer data, or proprietary information, or cause the Fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affecting issuers of the Fund’s securities may negatively impact performance. Operational risk may arise from human error, errors by third parties, communication errors, or technology failures, among other causes. The Fund also relies on a range of services from third-parties, including custody. Any delay or failure in the services provided to the Fund may negatively affect the Fund and its ability to meet its investment objective. Although the Fund and the Fund’s investment adviser seek to reduce operational risks through controls and/or procedures, it is not possible to identify and address all such risks and there is no way to completely protect against or mitigate such risks.

Government and Regulatory Risk. The risk that governments or regulatory authorities may take actions that could adversely affect markets in which the Fund invests and in the economy, more generally. Government and regulatory authorities may also act to increase the scope or burden of regulations applicable to the Fund and to the companies in which the Fund invests. Such legislation or regulation could restrict the ability of the Fund to fully implement its investment strategies, either generally or with respect to certain securities, industries or countries and could limit or preclude the Fund’s ability to achieve its investment objective.

7

Wasatch Core Growth Fund® — Summary

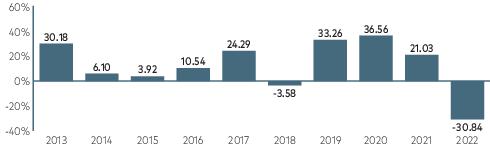

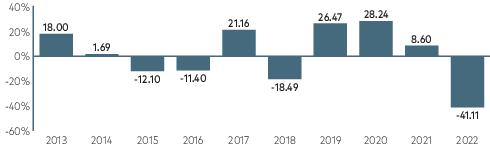

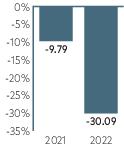

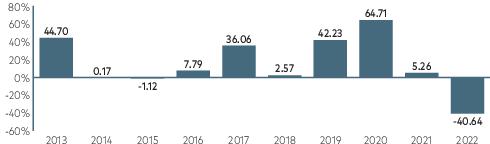

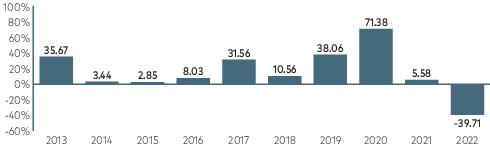

Historical Performance

The following tables provide information on how the Fund has performed over time. Performance in this section represents past performance (before and after taxes) which is not necessarily indicative of how the Fund will perform in the future. Performance for the Fund’s Investor Class shares would be substantially similar to that for Institutional Class shares because the shares are invested in the same portfolio of securities and would differ only to the extent that Institutional Class shares have different expenses. The bar chart below is intended to provide you with an indication of the risks of investing in the Fund by showing the Fund’s performance from year to year, as represented by the Investor Class of the Fund. The table below is designed to help you evaluate your risk tolerance by showing the best and worst quarterly performance of the Fund’s Investor Class for the calendar years shown in the bar chart. The average annual total returns table below allows you to compare the performance of the Fund’s Investor Class and Institutional Class shares over the time periods indicated to that of a broad-based market index and an additional index composed of securities similar to those held by the Fund. After-tax returns are shown for the Investor Class only. After-tax returns for the Institutional Class will vary. Performance information is updated regularly and is available on the Fund’s website wasatchglobal.com .

Wasatch Core Growth Fund — Investor Class

Year by Year Total Returns

Best and Worst Quarterly Returns

| - |

| 1 Year | 5 Years | 10 Years | |

| Investor Class (Inception Date |

|||

| Return Before Taxes | - |

||

| Return After Taxes on Distributions | - |

||

| Return After Taxes on Distributions and Sale of Fund Shares | - |

||

| Institutional Class (Inception Date |

|||

| Return Before Taxes | - |

||

| Russell 2000® Growth Index* (reflects no deductions for fees, expenses or taxes) | - |

||

| Russell 2000® Index* (reflects no deductions for fees, expenses or taxes) | - |

The Fund’s Investor Class returns after taxes on distributions and sale of Fund shares may be higher than the returns before taxes and after taxes on distributions because they include the effect of a tax benefit an investor may receive from capital losses that would have been incurred.

*All rights in the Russell 2000 and Russell 2000 Growth indexes vest in the relevant LSE Group company, which owns these indexes. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license. These indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in these indexes or (b)

8

January 31, 2023

investment in or operation of the Fund or the suitability of these indexes for the purpose they are being used herein.

The Russell 2000® Growth Index is an unmanaged total return index that measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 2000 Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. The Russell 2000 Index is an unmanaged total return index that measures the performance of the small-cap segment of the U.S. equities universe. The Russell 2000 Index is a subset of the Russell 3000 Index, representing approximately 7% of the total market capitalization of that index as of the most recent reconstitution. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. Effective January 31, 2023, the Fund changed its primary benchmark index from the Russell 2000 Index to the Russell 2000 Growth Index. The primary benchmark index better represents the securities held by the Fund. I/B/E/S (Institutional Brokers' Estimate System) gathers and compiles the different estimates made by stock analysts on the future earnings for publicly traded companies.

Portfolio Management

Investment Advisor

Wasatch Advisors LP d/b/a Wasatch Global Investors

Portfolio Managers

| JB Taylor Lead Portfolio Manager Since 2000 |

Paul Lambert Portfolio Manager Since 2005 |

Mike Valentine Portfolio Manager Since 2017 |

Purchase and Sale of Fund Shares

| Investment Minimums | Investor Class | Institutional Class |

| New Accounts | $2,000 | $100,000 |

| New Accounts with an Automatic Investment Plan | $1,000 | — |

| Individual Retirement Accounts (IRAs) | $2,000 | — |

| Coverdell Education Savings Accounts | $1,000 | — |

| Subsequent Purchases | Investor Class | Institutional Class |

| Regular Accounts and IRAs | $100 | $5,000 |

| Automatic Investment Plan | $50 per month and/or $100 per quarter |

— |

| • | Institutional Class shares are offered to all types of investors, provided that the investor meets the minimum investment threshold for Institutional Class shares. |

| • | Account minimums are waived for accounts held in qualified retirement or profit sharing plans opened through a third party service provider or record keeper, and may be waived for omnibus accounts established by financial intermediaries where the investment in the Fund is expected to meet the minimum investment amount within a reasonable time period as determined by the Advisor. Investors and/or registered investment advisors (RIAs) and broker-dealers may generally meet the minimum investment amount by aggregating multiple accounts with common ownership or discretionary control within the Fund. |

| • | You may purchase, sell (redeem) or exchange Fund shares on any day the New York Stock Exchange is open for business. |

| • | To open a new account directly with Wasatch Funds or to purchase shares for an existing account, go online at wasatchglobal.com. For a new account, complete and electronically submit the online application. Accounts for third parties, trusts, corporations, partnerships and other entities may not be opened online and are not eligible for online transactions. By telephone, complete the appropriate application and call a shareholder services representative at 800.551.1700 for instructions on how to open or add to an account via wire. To open a new account by mail, complete and mail the application and any other materials (such as a corporate resolution for corporate accounts) and a check. To add to an existing account, complete the additional investment form from your statement or write a note that includes the Fund name and Class of shares (i.e., Investor Class or Institutional Class), name(s) of investor(s) on the account and the account number. Send materials to: Wasatch Funds, P.O. Box 2172, Milwaukee, WI 53201-2172 or via overnight delivery to: Wasatch Funds, 235 W. Galena St., Milwaukee, WI 53212. |

| • | To sell shares purchased directly from Wasatch Funds, go online at wasatchglobal.com, or call a shareholder services representative at 800.551.1700 if you did not decline the telephone redemption privilege when establishing your account. |

9

Wasatch Core Growth Fund® — Summary

January 31, 2023

| Redemption requests may be sent by mail or overnight delivery to the appropriate address shown above. Include your name, Fund name, Class of shares (i.e., Investor Class or Institutional Class), account number, dollar amount of shares to be sold, your daytime telephone number, signature(s) of account owners (sign exactly as the account is registered) and Medallion signature guarantee (if required). For IRA accounts, please obtain an IRA Distribution Form online from wasatchglobal.com or by calling a shareholder services representative. | |

| • | Fund shares may be bought or sold through banks or investment professionals, including brokers that may have agreements with the Fund’s Distributor to offer shares when acting as an agent for the investor. An investor transacting in the Fund’s shares in these programs may be required to pay a commission and/or other forms of compensation to the bank, investment professional or broker. |

Tax Information

The Fund intends to make distributions. You will generally have to pay federal income taxes, and any applicable state or local taxes, on the distributions you receive from the Fund as ordinary income or capital gains unless you are investing through a tax exempt account such as a qualified retirement plan. Distributions on investments made through tax-deferred vehicles, such as 401(k) plans or IRAs, may be taxed later upon withdrawal of assets from those plans or accounts.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Advisor or its affiliates may pay the intermediary for the sale of shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary or your individual financial advisor to recommend the Fund over another investment. Ask your individual financial advisor or visit your financial intermediary’s website for more information.

10

Wasatch Emerging India Fund® — Summary

January 31, 2023

Investment Objective

The Fund’s investment objective is long-term growth of capital.

Fees and Expenses of the Fund

The tables below describe the fees and expenses that you may pay if you buy, hold and sell shares of the Fund.

You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Investor Class Shares |

Institutional Class Shares | |

| Maximum Sales Charge (Load) Imposed on Purchases (as a % of offering price) | ||

| Redemption Fee (as a % of amount redeemed on shares held 60 days or less) | ||

| Exchange Fee |

| Investor Class Shares |

Institutional Class Shares | ||

| Management Fee | |||

| Other Expenses | |||

| Total Annual Fund Operating Expenses |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invested $10,000 in the applicable class of the Fund for the time periods indicated and then redeemed all of your shares at the end of those periods. The example also assumes that your investment had a 5% return each year and that operating expenses (as a percentage of net assets) of the Fund remained the same. This example reflects contractual fee waivers and reimbursements through January 31, 2024. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Emerging India Fund — Investor Class | $ |

$ |

$ |

$ |

| Emerging India Fund — Institutional Class | $ |

$ |

$ |

$ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). Higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 25 % of the average value of its portfolio.

Principal Strategies

The Fund invests primarily in companies tied economically to India.

Under normal market conditions, we will invest at least 80% of the Fund’s net assets (plus borrowings for investment purposes) in the equity securities, typically common stock, of companies of all market capitalizations tied economically to India.

We will consider qualifying investments to be in companies that are listed on an Indian exchange, that have at least 50% of their assets in India, or that derive at least 50% of their revenues or profits from goods produced or sold, investments made, or services performed in India.

India is considered an emerging market. Companies in the India region with economic ties to India may be located in India, Bangladesh, Pakistan and Sri Lanka.

We use a process of quantitative screening followed by “bottom up” fundamental analysis to identify individual companies that we believe have above average revenue and earnings growth potential.

11

Wasatch Emerging India Fund® — Summary

The Fund is classified as a non-diversified mutual fund, which means that the Fund may invest a larger percentage of its assets in the securities of a small number of issuers than a diversified fund.

We may also invest in initial public offerings (IPOs).

Principal Risks

The Fund is subject to the following principal investment risks:

Market Risk. Market risk is the risk that a particular security, or shares of the Fund in general, may fall in value. Securities are subject to market fluctuations caused by such factors as economic, political, regulatory or market developments, changes in interest rates and perceived trends in securities prices. Shares of the Fund could decline in value or underperform other investments due to, among other things, market movements over the short-term or over longer periods during more prolonged market downturns. In addition, local, regional or global events such as war, acts of terrorism, spread of infectious diseases or other public health issues, recessions, or other events could have a significant negative impact on the Fund and its investments. Such events may affect certain geographic regions, countries, sectors and industries more significantly than others. Such events could adversely affect the prices and liquidity of the Fund’s portfolio securities or other instruments and could result in disruptions in the trading markets. Any of such circumstances could have a materially negative impact on the value of the Fund’s shares and result in increased market volatility.

Economic and Market Events Risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact the Fund’s performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Companies, including banks and financial services companies, could suffer losses if interest rates rise or economic conditions deteriorate.

Additional Market Disruption Risk. In February 2022, Russia commenced a military attack on Ukraine. In response, various countries, including the U.S., issued broad-ranging sanctions on Russia and certain Russian companies and individuals. Although the hostilities between the two countries may escalate and any existing or future sanctions could have a severe adverse effect on Russia’s economy, currency, companies and region, these events may negatively impact other regional and global economic markets of the World (including Europe and the United States), companies in such countries and various sectors, industries and markets for securities and commodities globally, such as oil and natural gas. Accordingly, the hostilities and sanctions may have a negative effect on the Fund’s investments and performance beyond any direct or indirect exposure the Fund may have to Russian issuers or those of adjoining geographic regions. The sanctions and compliance with these sanctions may impair the ability of the Fund to buy, sell, hold or deliver Russian securities and/or other assets, including those listed on U.S. or other exchanges. Russia may also take retaliatory actions or countermeasures, such as cyberattacks and espionage, which may negatively impact the countries and companies in which the Fund may invest. Accordingly, there may be a heightened risk of cyberattacks by Russia in response to the sanctions. The extent and duration of the military action or future escalation of such hostilities; the extent and impact of existing and any future sanctions, market disruptions and volatility; and the result of any diplomatic negotiations cannot be predicted. These and any related events could have a significant negative impact on the Fund’s investments as well as the Fund’s performance, and the value or liquidity of certain securities held by the Fund may decline significantly.

Global Pandemic Risk. The value of the Fund’s investments may be impacted by global health crises or other events. For example, an outbreak of the respiratory disease designated as Covid-19 was first detected in China in December 2019 and subsequently spread internationally. The transmission of Covid-19 and efforts to contain its spread have resulted in international, national and local border closings and other significant travel restrictions and disruptions; significant disruptions to business operations across many industries, to supply chains and to customer activity; and have resulted in event cancellations and restrictions; service cancellations, reductions and other changes; significant challenges in health care service preparation and delivery; and quarantines, as well as general concern and uncertainty that has negatively affected the economic environment. These impacts also have caused significant market volatility and disruption which may continue over extended periods. The ultimate impact of Covid-19 or other health emergencies on the domestic and global economies is

12

January 31, 2023

impossible to predict accurately. Less developed countries and their health systems may be more vulnerable to these impacts. The impact of this Covid-19 pandemic may be short term or may last for an extended period of time, and in either case could result in a substantial economic downturn or recession and may adversely impact the value of an investment in the Fund.

Stock Market Risk. The Fund’s investments may decline in value due to movements in the overall stock market.

Stock Selection Risk. The Fund is actively managed, and its performance therefore will reflect, in part, the ability of the portfolio manager(s) to select investments and to make investment decisions that are suited to achieving the Fund’s investment objective. The Advisor does not actively track the composition or weightings of market indexes (including the Fund’s benchmark index) or of the broader markets generally. As a result, the Fund could underperform its benchmark index and/or other funds with a similar investment objective and/or strategy or it may lose value even when the overall stock market is not in general decline.

Equity Securities Risk. Equity securities represent ownership in a company. They may be traded (bought or sold) on a securities exchange or stock market. Stock markets are volatile. The price of equity securities will fluctuate and can decline and reduce the value of a portfolio invested in equity securities. The value of equity securities purchased by the Fund could decline if the financial condition of the companies in which the Fund invests declines or if overall market and economic conditions deteriorate. The value of equity securities may also decline due to factors that affect a particular industry or industries such as labor shortages, an increase in production costs and changes in competitive conditions within an industry. In addition, the value of equity securities may decline due to, among other things, general market conditions not specifically related to a company or industry such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, changes in government regulations, the political situation, or generally adverse investor sentiment. Certain equity securities may be less liquid, meaning that they may be difficult to sell at a time or price that is desirable, than other types of securities, or they may be illiquid. Some securities exchanges or stock markets may also be less liquid or illiquid due to low trading volume. In addition, equity securities include common stock. Common stock holds the lowest priority in the capital structure of a company and therefore takes the largest share of the company’s risk and its accompanying volatility. The rights of common stockholders generally are subordinate to all other claims on a company’s assets, including preferred stockholders and debt holders with respect to the payment of dividends and upon the liquidation or bankruptcy of the issuing company. The common stock of a company that experiences financial distress may lose significant value or become worthless, and therefore the Fund could lose money if a company in which it invests becomes financially distressed.

Liquidity Risk. In addition, the trading market for a particular security or type of security in which the Fund invests may be significantly less liquid than developed or even emerging markets, and there may be little or no trading volume for a period of time for a particular security. Reduced liquidity will have an adverse impact on the Fund’s ability to sell such securities quickly at a desired price when necessary to meet the Fund’s liquidity needs or in response to a specific economic event. It may be difficult at times to sell such securities at any price, which could impact not only the daily net asset value (NAV) of the Fund, but also the composition of the portfolio if other securities must be sold to meet the Fund’s liquidity needs. Additionally, market quotations for such securities may be volatile and thus affect the daily NAV of the Fund.

Foreign Securities Risk. Foreign securities are generally more volatile and less liquid than U.S. securities. Further, foreign securities may be subject to additional risks not associated with investments in U.S. securities. Differences in the economic and political environment, the amount of available public information, the amount of taxation, limitations on the use or transfer of Fund assets, the degree of market regulation, settlement practices, the potential for permanent or temporary termination of trading, and financial reporting, accounting and auditing standards, and, in the case of foreign currency-denominated securities, fluctuations in currency exchange rates, can have a significant effect on the value of a foreign security. More specifically, changes in currency exchange rates will affect the value of non-U.S. securities, the value of dividends and interest earned from such securities and gains and losses realized on the sale of such securities. The value of an investment denominated in a foreign currency will decline in U.S. dollar terms if that currency weakens against the U.S. dollar. The Fund may be invested in the local currency of a foreign country in connection with executing foreign securities transactions. When the Fund executes the securities transactions, there is the risk of the value of the foreign currency increasing or decreasing against the value of the U.S. dollar. While the Fund is permitted to hedge currency risks, the Advisor does not anticipate doing so at this time. Additionally, certain countries may restrict foreign investment in their securities and may utilize formal or informal currency-exchange controls or “capital controls.” Capital controls may impose restrictions on the Fund’s ability to repatriate investments or income. Such capital controls can also have a significant effect on the value of the Fund’s holdings.

Emerging Markets Risk. In addition to the risks of investing in foreign securities in general, the risks of investing in the securities of companies domiciled in emerging market countries include increased political or social instability, economies based on only a few industries, unstable currencies, runaway inflation, as well as highly volatile, substantially smaller and less liquid securities markets, unpredictable shifts in policies relating to foreign investments, lack of protection for investors against

13

Wasatch Emerging India Fund® — Summary

parties that fail to complete transactions, lack of or limited government oversight over securities exchanges and brokers, and the potential for government seizure of assets or nationalization of companies or other government interference in which case the Fund could lose all or a significant portion of its investment in a country.

Indian Market and India Region Risk. Government actions, bureaucratic obstacles and inconsistent economic and tax reform policies within the Indian government have had a significant effect on the economy and could adversely affect market conditions, deter economic growth and reduce the profitability of private enterprises. Global factors and foreign actions may inhibit the flow of foreign capital on which India is dependent to sustain its growth. Large portions of many Indian companies remain in the hands of their founders (including members of their families). Family-controlled companies may have weaker and less transparent corporate governance, which increases the potential for loss and unequal treatment of investors. India experiences many of the market risks associated with developing economies, including relatively low levels of liquidity, which may result in extreme volatility in the prices of Indian securities. Religious, cultural and military disputes persist in India, and between India and Pakistan (as well as sectarian groups within each country). The threat of aggression in the region could hinder development of the Indian economy, and escalating tensions could impact the broader region, including China.

Because the Fund may invest a large percentage of its assets in India, the value of the Fund’s shares may be affected by events that adversely affect India and may fluctuate more than the value of a less concentrated fund’s shares.

Smaller Company Stock Risk. Small- and mid-cap stocks may be very sensitive to changing economic conditions and market downturns. In particular, the issuers of small company stocks have more narrow markets for their products and services, fewer product lines, and more limited managerial and financial resources than larger issuers. The stocks of small companies may therefore be more volatile and the ability to sell these stocks at a desirable time or price may be more limited.

Growth Stock Risk. Growth stock prices may be more sensitive to changes in companies’ current or expected earnings than the prices of other stocks, and growth stock prices may fall or may not appreciate in step with the broader securities markets. Growth companies may be newer or smaller companies and may retain a large part of their earnings for research, development or investments in capital assets.

Sector and Industry Weightings Risk. To the extent the Fund emphasizes, from time to time, investments in a particular sector, the Fund will be subject to a greater degree to the risks particular to that sector, including the sectors described below. Market conditions, interest rates, and economic, political, regulatory, or financial developments could significantly affect all the securities in a single sector. If the Fund invests in a few sectors, it may have increased exposure to the price movements of securities in those sectors. The Fund may also from time to time make significant investments in an industry or industries within a particular sector. The industries that constitute a sector may all react in the same way to economic, political or regulatory events. Adverse conditions in such industry or industries could have a correspondingly adverse effect on the financial condition of issuers. These conditions may cause the value of the Fund’s shares to fluctuate more than the values of shares of funds that invest in a greater variety of investments.

Consumer Staples Sector Risk. The consumer staples sector includes companies in the food and staples retailing, food, beverage and tobacco, and household and personal products industry groups. Companies in the consumer staples sector may be affected by demographics and product trends, competitive pricing, food fads, marketing campaigns, environmental factors, changes in consumer demands, the performance of the overall domestic and global economy, interest rates, consumer confidence and spending, and changes in commodity prices. Consumer staples companies may be subject to government regulations that may affect the permissibility of using various food additives and production methods. Tobacco companies may be adversely affected by regulation, legislation and/or litigation.

Materials Sector Risk. The materials sector includes companies in the chemicals, construction materials, containers and packaging, metals and mining, and paper and forest products industries. Changes in world events, political, environmental and economic conditions, energy conservation, environmental policies, commodity price volatility, changes in currency exchange rates, imposition of import and export controls, increased competition, and labor relations may adversely affect companies engaged in the production and distribution of materials. Other risks may include liabilities for environmental damage, depletion of resources, and mandated expenditures for safety and pollution control. Companies in the chemicals industry may be subject to risks associated with the production, handling and disposal of hazardous components. Metals and mining companies could be affected by supply and demand, operational costs, and liabilities for environmental damage.

Consumer Discretionary Sector Risk. The consumer discretionary sector includes companies in industries such as consumer services, household durables, leisure products, textiles, apparel and luxury goods, hotels, restaurants, retailing, e-commerce, and automobiles. Companies in the consumer discretionary sector may be significantly impacted by the performance of the overall domestic and global economy and by interest rates. The consumer discretionary sector relies heavily on disposable household income and spending. Companies in this sector may be subject to severe competition, which may have an adverse impact on

14

January 31, 2023

their respective profitability. The retail industry can be significantly affected by changes in demographics, and consumer tastes and shopping habits, which can also affect the demand for, and success of, consumer products and services in the marketplace. The automotive industry is highly cyclical and can be significantly affected by labor relations and fluctuating component prices.

Health Care Sector Risk. The health care sector includes companies in the health care equipment and services, and pharmaceuticals, biotechnology and life sciences industry groups. Health care companies are strongly affected by worldwide scientific or technological developments. Their products may rapidly become obsolete. Many health care companies are also subject to significant government regulation and may be affected by changes in government policies. Companies in the pharmaceuticals, biotechnology and life sciences industry group in particular are heavily dependent on patent protection, and the expiration of patents may adversely affect the profitability of such companies. These companies are also subject to extensive litigation based on product liability and other similar claims. Many new products are subject to government approval and the process of obtaining government approval can be long and costly, and even approved products are susceptible to obsolescence. These companies are also subject to competitive forces that may make it difficult to increase prices, or that may lead to price reductions.

Industrials Sector Risk. The industrials sector includes companies in the capital goods, commercial and professional services and transportation industry groups, including companies engaged in the business of human capital management, business research and consulting, air freight and logistics, airlines, maritime shipping and transportation, railroads and trucking, transportation infrastructure, and aerospace and defense. Companies in the industrials sector can be significantly affected by general economic trends, including such factors as employment and economic growth, interest rate changes, changes in consumer spending, legislative and government regulation and spending, import controls, commodity prices, and worldwide competition. Changes in the economy, fuel prices, labor agreements, and insurance costs may result in occasional sharp price movements in transportation securities. Aerospace and defense companies rely, to a significant extent, on government demand for their products and services. The financial condition of, and investor interest in, aerospace and defense companies are heavily influenced by government defense spending policies.

Information Technology Sector Risk. The information technology sector includes companies in the software and services, technology hardware and equipment, and semiconductors and semiconductor equipment industry groups. Companies in the information technology sector are subject to rapid obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. Stocks of companies in the information technology sector, especially those of smaller, less-seasoned companies, tend to be more volatile than the overall market. Technological developments, fixed rate pricing, and the ability to retain skilled employees can significantly affect the industries in the information technology sector. Additionally, success in the internet services and infrastructure industry is subject to continued demand for internet services.

Financials Sector Risk. The financials sector includes companies in the banks, diversified financials, and insurance industry groups. Companies in the financials sector are subject to extensive government regulation, can be subject to relatively rapid change due to increasingly blurred distinctions between service segments, and can be significantly affected by the availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition. Banking companies, including thrifts and mortgage finance and consumer finance companies, may be affected by extensive government regulation, which may limit both the amounts and types of loans and other financial commitments they can make, the interest rates and fees they can charge, and the amount of capital they must maintain. Profitability is largely dependent on the availability and cost of capital funds, and can fluctuate significantly when interest rates change. Credit losses resulting from financial difficulties of borrowers can negatively affect banking companies. Banking companies may also be subject to severe price competition. Competition is high among banking companies and failure to maintain or increase market share may result in lost market value. Capital markets, a sub-industry of diversified financials, may be affected by extensive government regulation as well as economic and other financial events that could cause fluctuations in the stock market, impacting the overall value of investments. The insurance industry may be affected by extensive government regulation and can be significantly affected by interest rates, general economic conditions, and price and marketing competition. Different segments of the insurance industry can be significantly affected by natural disasters, mortality and morbidity rates, and environmental clean-up.

Initial Public Offerings (IPOs) Risk. IPOs involve a higher degree of risk because companies involved in IPOs generally have limited operating histories and their prospects for future profitability are uncertain. Prices of IPOs may also be unstable due to the absence of a prior public market, the small number of shares available for trading and limited investor information.

Non-Diversification Risk. The Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund, which means it may have more exposure to the price movements of a single security or small group of securities than funds that diversify their investments among many companies.

15

Wasatch Emerging India Fund® — Summary

Operational and Cybersecurity Risk. Cybersecurity breaches may allow an unauthorized party to gain access to Fund assets, customer data, or proprietary information, or cause the Fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affecting issuers of the Fund’s securities may negatively impact performance. Operational risk may arise from human error, errors by third parties, communication errors, or technology failures, among other causes. The Fund also relies on a range of services from third-parties, including custody. Any delay or failure in the services provided to the Fund may negatively affect the Fund and its ability to meet its investment objective. Although the Fund and the Fund’s investment adviser seek to reduce operational risks through controls and/or procedures, it is not possible to identify and address all such risks and there is no way to completely protect against or mitigate such risks.

Government and Regulatory Risk. The risk that governments or regulatory authorities may take actions that could adversely affect markets in which the Fund invests and in the economy, more generally. Government and regulatory authorities may also act to increase the scope or burden of regulations applicable to the Fund and to the companies in which the Fund invests. Such legislation or regulation could restrict the ability of the Fund to fully implement its investment strategies, either generally or with respect to certain securities, industries or countries and could limit or preclude the Fund’s ability to achieve its investment objective.

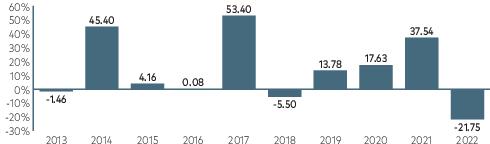

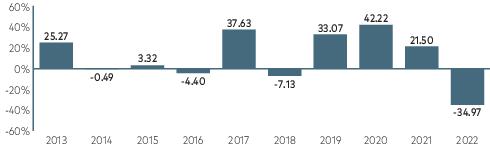

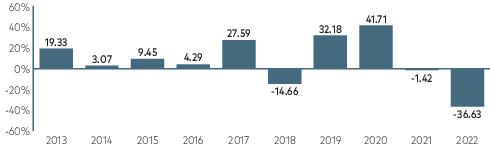

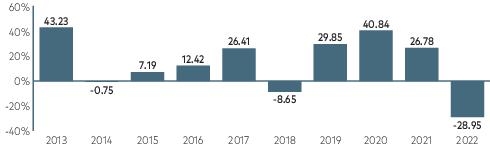

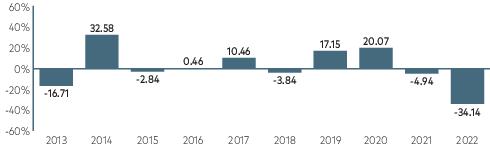

Historical Performance

The following tables provide information on how the Fund has performed over time. Performance in this section represents past performance (before and after taxes) which is not necessarily indicative of how the Fund will perform in the future. Performance for the Fund’s Investor Class shares would be substantially similar to that for Institutional Class shares because the shares are invested in the same portfolio of securities and would differ only to the extent that Institutional Class shares have different expenses. The bar chart below is intended to provide you with an indication of the risks of investing in the Fund by showing the Fund’s performance from year to year, as represented by the Investor Class of the Fund. The table below is designed to help you evaluate your risk tolerance by showing the best and worst quarterly performance of the Fund’s Investor Class for the calendar years shown in the bar chart. The average annual total returns table below allows you to compare the performance of the Fund’s Investor Class and Institutional Class shares over the time periods indicated to that of a broad-based market index. After-tax returns are shown for the Investor Class only. After-tax returns for the Institutional Class will vary. Performance information is updated regularly and is available on the Fund’s website wasatchglobal.com .

Wasatch Emerging India Fund — Investor Class

Year by Year Total Returns

Best and Worst Quarterly Returns

| - |

16

January 31, 2023

| 1 Year | 5 Years | 10 Years (Investor Class) |

Since Inception (Institutional Class) | |

| Investor Class (Inception Date |

||||

| Return Before Taxes | - |

N/A | ||

| Return After Taxes on Distributions | - |

N/A | ||

| Return After Taxes on Distributions and Sale of Fund Shares | - |

N/A | ||

| Institutional Class (Inception Date |

||||

| Return Before Taxes | - |

N/A | ||

| MSCI India IMI (Investable Market Index)* (reflects no deductions for fees, expenses or taxes) | - |

*Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indexes or financial products. This report is not approved or produced by MSCI.

Portfolio Management

Investment Advisor

Wasatch Advisors LP d/b/a Wasatch Global Investors

Portfolio Managers

| Ajay Krishnan, CFA Lead Portfolio Manager Since Inception |

Matthew Dreith, CFA Portfolio Manager Since 2016 |

Purchase and Sale of Fund Shares

| Investment Minimums | Investor Class | Institutional Class |

| New Accounts | $2,000 | $100,000 |

| New Accounts with an Automatic Investment Plan | $1,000 | — |

| Individual Retirement Accounts (IRAs) | $2,000 | — |

| Coverdell Education Savings Accounts | $1,000 | — |

| Subsequent Purchases | Investor Class | Institutional Class |

| Regular Accounts and IRAs | $100 | $5,000 |

| Automatic Investment Plan | $50 per month and/or $100 per quarter |

— |

| • | Institutional Class shares are offered to all types of investors, provided that the investor meets the minimum investment threshold for Institutional Class shares. |

| • | Account minimums are waived for accounts held in qualified retirement or profit sharing plans opened through a third party service provider or record keeper, and may be waived for omnibus accounts established by financial intermediaries where the investment in the Fund is expected to meet the minimum investment amount within a reasonable time period as determined by the Advisor. Investors and/or registered investment advisors (RIAs) and broker-dealers may generally meet the minimum investment amount by aggregating multiple accounts with common ownership or discretionary control within the Fund. |

| • | You may purchase, sell (redeem) or exchange Fund shares on any day the New York Stock Exchange is open for business. |

17

Wasatch Emerging India Fund® — Summary

January 31, 2023

| • | To open a new account directly with Wasatch Funds or to purchase shares for an existing account, go online at wasatchglobal.com. For a new account, complete and electronically submit the online application. Accounts for third parties, trusts, corporations, partnerships and other entities may not be opened online and are not eligible for online transactions. By telephone, complete the appropriate application and call a shareholder services representative at 800.551.1700 for instructions on how to open or add to an account via wire. To open a new account by mail, complete and mail the application and any other materials (such as a corporate resolution for corporate accounts) and a check. To add to an existing account, complete the additional investment form from your statement or write a note that includes the Fund name and Class of shares (i.e., Investor Class or Institutional Class), name(s) of investor(s) on the account and the account number. Send materials to: Wasatch Funds, P.O. Box 2172, Milwaukee, WI 53201-2172 or via overnight delivery to: Wasatch Funds, 235 W. Galena St., Milwaukee, WI 53212. |

| • | To sell shares purchased directly from Wasatch Funds, go online at wasatchglobal.com, or call a shareholder services representative at 800.551.1700 if you did not decline the telephone redemption privilege when establishing your account. Redemption requests may be sent by mail or overnight delivery to the appropriate address shown above. Include your name, Fund name, Class of shares (i.e., Investor Class or Institutional Class), account number, dollar amount of shares to be sold, your daytime telephone number, signature(s) of account owners (sign exactly as the account is registered) and Medallion signature guarantee (if required). For IRA accounts, please obtain an IRA Distribution Form online from wasatchglobal.com or by calling a shareholder services representative. |

| • | Fund shares may be bought or sold through banks or investment professionals, including brokers that may have agreements with the Fund’s Distributor to offer shares when acting as an agent for the investor. An investor transacting in the Fund’s shares in these programs may be required to pay a commission and/or other forms of compensation to the bank, investment professional or broker. |

Tax Information

The Fund intends to make distributions. You will generally have to pay federal income taxes, and any applicable state or local taxes, on the distributions you receive from the Fund as ordinary income or capital gains unless you are investing through a tax exempt account such as a qualified retirement plan. Distributions on investments made through tax-deferred vehicles, such as 401(k) plans or IRAs, may be taxed later upon withdrawal of assets from those plans or accounts.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Advisor or its affiliates may pay the intermediary for the sale of shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary or your individual financial advisor to recommend the Fund over another investment. Ask your individual financial advisor or visit your financial intermediary’s website for more information.

18

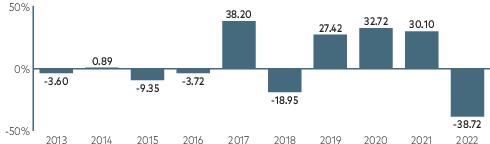

Wasatch Emerging Markets Select Fund® — Summary

January 31, 2023

Investment Objective

The Fund’s investment objective is long-term growth of capital.

Fees and Expenses of the Fund

The tables below describe the fees and expenses that you may pay if you buy, hold and sell shares of the Fund.

You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Investor Class Shares |

Institutional Class Shares | |

| Maximum Sales Charge (Load) Imposed on Purchases (as a % of offering price) | ||

| Redemption Fee (as a % of amount redeemed on shares held 60 days or less) | ||

| Exchange Fee |

| Investor Class Shares |

Institutional Class Shares | ||

| Management Fee | |||

| Other Expenses | |||

| Total Annual Fund Operating Expenses |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invested $10,000 in the applicable class of the Fund for the time periods indicated and then redeemed all of your shares at the end of those periods. The example also assumes that your investment had a 5% return each year and that operating expenses (as a percentage of net assets) of the Fund remained the same. This example reflects contractual fee waivers and reimbursements through January 31, 2024. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Emerging Markets Select Fund — Investor Class | $ |

$ |

$ |

$ |

| Emerging Markets Select Fund — Institutional Class | $ |

$ |

$ |

$ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). Higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 31 % of the average value of its portfolio.

Principal Strategies

The Fund invests primarily in companies of all market capitalizations that are tied economically to emerging market countries.

Under normal market conditions, we will invest at least 80% of the Fund’s net assets (plus borrowings for investment purposes) in the equity securities, typically common stock, of companies that are tied economically to emerging market countries.

Emerging market countries are those currently included in the Morgan Stanley Capital International (MSCI) Emerging Markets Index. We will consider qualifying investments to be in companies that are listed on an exchange in an emerging market country, that have at least 50% of their assets in an emerging market country, or that derive at least 50% of their revenues or profits from goods produced or sold, investments made, or services performed in an emerging market country.

19

Wasatch Emerging Markets Select Fund® — Summary

Under normal market conditions, the Fund will generally invest in 30 to 50 companies. However, we may invest in fewer or more companies when we believe that doing so will help our efforts to achieve the Fund’s investment objective.