Table of Contents

WASATCH FUNDS TRUST

Important Information for Shareholders of Wasatch Long/Short Fund

At a special meeting of shareholders of Wasatch Long/Short Fund (the “Target Fund”), a series of Wasatch Funds Trust (the “Trust”), you will be asked to vote on the reorganization of your fund into Wasatch Global Value Fund (formerly, Wasatch Large Cap Value Fund) (the “Acquiring Fund”), also a series of the Trust (the “Reorganization”). The Target Fund and the Acquiring Fund are collectively referred to herein as the “Funds” and individually as a “Fund.”

The Board of Trustees of the Trust, including the Independent Trustees, unanimously recommends that you vote FOR the proposal.

Although we recommend that you read the complete Proxy Statement/ Prospectus, for your convenience we have provided the following brief overview of the matter to be voted on.

Q. Why is the Reorganization being proposed?

A. Wasatch Advisors, Inc. (the “Advisor”), the investment adviser to the Target Fund and the Acquiring Fund, has proposed the Reorganization given the limited future growth prospects of the Target Fund, its relative poor performance and the economic infeasibility of the Target Fund over the long term in light of the costs associated with the continued operation of the Target Fund and its likely inability to attract assets in the foreseeable future. In evaluating the Target Fund and the Acquiring Fund, the Advisor recognized the material differences between the investment objectives and principal investment strategies of the Funds. In particular, the Target Fund is a long/short fund investing primarily in the equity securities of domestic companies by maintaining long and short equity positions, whereas the Acquiring Fund is a global value fund that invests primarily in the equity securities of foreign and domestic companies and does not employ a short sale strategy.

Although the investment objectives and strategies are materially different between the Target Fund and the Acquiring Fund, the Advisor has proposed the Reorganization with the Acquiring Fund due, in part, to the similar valuation process used by the Advisor to evaluate potential investments for the Funds despite the differing investment strategies; the overlap of portfolio holdings between the Funds; the relative performance of the Acquiring Fund compared to the Target Fund; the lower contractual management fee and estimated lower gross and net expense ratio (before and after fee waivers) of the combined fund for both share classes; the lower contractual expense cap of the Acquiring Fund, which would be in effect through January 31, 2020; and the anticipated federal income tax-free nature of the Reorganization compared to a taxable event for shareholders if the Target Fund was liquidated. For additional information, see “Approval of the Proposed Reorganization by the Board of Trustees” at page 47.

Table of Contents

Q. How will the Reorganization affect my shares?

A. Upon the closing of the Reorganization, each Target Fund shareholder will receive shares of the Acquiring Fund in an amount equal in total value to the total value of the Target Fund shares surrendered by such shareholder. Shareholders of Investor Class shares and Institutional Class shares of the Target Fund will receive the same class of shares of the Acquiring Fund.

Q. Will Target Fund shareholders incur sales loads or contingent deferred sales charges on Acquiring Fund shares received in the Reorganization?

A. No. Neither Fund charges a front-end sales load or a contingent deferred sales charge.

Q. Are the Funds managed by the same Advisor?

A. Both Funds are advised by Wasatch Advisors, Inc. Beginning October 2017, both Funds are managed by David Powers.

Q. How do the Funds’ investment objectives and principal investment strategies compare?

A. You should note that the Funds’ investment objectives and principal investment strategies are materially different. The Target Fund’s investment objective is capital appreciation, and the Acquiring Fund’s investment objective is capital appreciation and income. While the investment objectives of both Funds share a capital appreciation component, the Target Fund’s objective also includes income.

In addition, while both Funds invest primarily in equity securities, generally common stock, the Funds follow materially different investment strategies. The Target Fund is a long/short fund and pursues its investment objective by maintaining long equity positions and short equity positions. When the Target Fund takes a long position, it purchases the security outright. When the Fund takes a short position, it sells a security that it does not own in hope of repurchasing such security at a lower price. The use of both long and short positions allows the Advisor to invest based on both its positive and negative views on individual stocks. Unlike the Target Fund, the Acquiring Fund does not engage in short sales as a principal investment strategy but rather invests primarily in equity securities of domestic and foreign securities through a long only portfolio. The Target Fund further seeks to achieve higher risk-adjusted returns with lower volatility compared to the equity markets (as represented by the S&P 500), whereas the Acquiring Fund does not have a similar mandate.

The Target Fund also invests primarily in the equity securities of domestic companies and has limited exposure to foreign securities. The Acquiring Fund, however, is a global value fund that invests its net assets primarily in the equity securities of foreign and domestic companies of all market capitalizations. The Acquiring Fund will typically invest in securities issued by companies domiciled in at least three countries, including the United States. The Acquiring Fund will invest a significant portion of its total assets in securities of companies domiciled in foreign countries (under normal market conditions,

2

Table of Contents

at least 40% will be invested outside the United States, or if conditions are not favorable, 30% of its assets will be invested outside the United States). The Acquiring Fund is also permitted to invest a significant amount of its total assets at the time of purchase in securities issued by companies domiciled in emerging and frontier markets, which are those countries currently included in the Morgan Stanley Capital International (MSCI) EFM (Emerging + Frontier Markets) Index, including the Asia-Pacific region, Eastern Europe, the Middle East, Central and South America and Africa (under normal market conditions we expect to invest between 5% to 50% in securities domiciled in emerging and frontier markets). Securities issued by foreign companies incorporated outside the United States whose securities are principally traded in the United States are not defined as “foreign companies” and are not subject to this limitation. Accordingly, to qualify as a foreign company under the above limitations, the company must be incorporated outside the United States and its securities principally traded in a foreign jurisdiction.

As a principal investment strategy, the Target Fund is permitted to invest in early stage companies, initial public offerings, and fixed income securities of any maturity, including those that are less than investment grade known as “junk bonds.” The Acquiring Fund, however, is permitted to invest in investment grade fixed-income securities, early stage companies and IPOs but not as a principal investment strategy. The Acquiring Fund is not permitted to invest in “junk bonds.”

Beginning October 2017, the Funds share the same portfolio manager. Although the Funds have material differences in their investment strategies, the portfolio manager of the Funds employs a similar valuation analysis to evaluate potential investment opportunities for the Funds which emphasizes company fundamentals (such as, price-to-sales, price-to-book, price-to-earnings, price/earnings-to-growth ratios and discounted cash flow models) as well as considers other economic and market factors. Further, both Funds have generally acquired larger capitalization companies. In this regard, the Acquiring Fund is permitted to invest in companies of any size but is expected to invest a significant portion of the Fund’s assets in U.S. and foreign companies with a market capitalization of over US $5 billion at the time of purchase. The Target Fund also is permitted to invest in the equity securities of U.S. companies with a market capitalization of at least $100 million at the time of purchase, and the Target Fund has historically been invested in securities of over US $5 billion, similar to the Acquiring Fund. For comparison, as of June 30, 2018 the Target Fund invested 88% of its assets in securities of U.S. companies with a market capitalization of over US $5 billion and the Acquiring Fund invested 85% of its assets in securities of U.S. and foreign companies with a market capitalization of over US $5 billion. As of June 30, 2018, eighteen of the twenty larger cap U.S. companies held by the Target Fund (approximately 70% of the Target Fund’s portfolio) were also held by the Acquiring Fund.

A more detailed comparison of the principal investment strategies of the Funds is contained in the Proxy Statement/Prospectus. Please see the section entitled “Comparison of the Funds – Investment Objectives” and “Comparison of Funds – Principal Investment Strategies” for additional information.

3

Table of Contents

Q. Will the portfolio of the Target Fund be repositioned as a result of the Reorganization?

A. Yes. The Target Fund’s portfolio will be repositioned in connection with the Reorganization. The companies currently held in the Target Fund that are not also held in the Acquiring Fund (approximately 6% of the value of the Target Fund) will be sold prior to the Reorganization. In addition, the short positions in the Target Fund will be closed (approximately 22% of the value of the Target Fund) prior to the Reorganization. The total estimated expenses of the Reorganization of the Target Fund are $394,000 which includes, among other things, the legal, audit and proxy solicitation fees of approximately $338,000, and brokerage costs. Brokerage costs are the only transaction cost associated with the repositioning of the Target Fund, which are estimated at approximately $56,000 (0.09% of the Target Fund’s net assets) assuming it had occurred as of March 31, 2018. The Advisor and the Target Fund have agreed to split evenly the costs of the Reorganization, subject to contractual expense caps. Accordingly, based on these estimates, approximately $197,000 of these costs are expected to be paid by the Target Fund and approximately $197,000 will be paid by the Advisor. These are estimates and actual amounts may vary. There are some foreign securities that cannot be purchased until the Reorganization is complete. The Acquiring Fund and indirectly its shareholders (including former shareholders of the Target Fund who hold shares in the Acquiring Fund) are estimated to incur approximately $20,000 in brokerage commissions related to the acquisition of portfolio securities from cash received in the Reorganization. To the extent that the Target Fund’s expenses, including Reorganization expenses, exceed the Fund’s current expense cap, the Advisor will pay more of the Reorganization expenses as necessary to keep each Fund’s share classes operating within their respective expense cap.

Q. How do the principal risks of the Target Fund and the Acquiring Fund compare?

A. As both Funds invest in equity securities through long positions, both Funds are subject to market risk that the price of securities will decline. As a result of the differences in the principal investment strategies of the Funds, however, certain principal risks of the Funds are also materially different. As noted, the Target Fund as a long/short fund engages in short sales as a principal investment strategy and therefore is subject to risks associated with short sales, including experiencing losses if the market price of the security increases, reducing the returns of the Target Fund compared to if the Fund held only long positions, increasing the Target Fund’s liquidity risk and exposing the Target Fund to the risk that the third party will not honor its contract terms. Unlike the Target Fund, the Acquiring Fund does not employ a short sale strategy as a principal investment strategy and therefore does not have the related principal risk.

Unlike the Target Fund which invests primarily in the equity securities of domestic companies, the Acquiring Fund may invest a significant portion of its total assets in foreign securities, including in equity securities of companies domiciled in emerging and frontier markets. The Acquiring Fund is therefore exposed to risks associated with investing in foreign securities, including, among other things, more volatility; less

4

Table of Contents

liquidity; different regulatory, accounting and auditing standards; less publicly available information; fluctuations in currency exchange rates; and restrictions on repatriating investments or income and such risks can be further increased for emerging and frontier markets.

The Target Fund is also subject to certain additional principal risks related to investment strategies that are its principal investment strategies but are not principal investment strategies of the Acquiring Fund (including investments in initial public offerings, fixed-income securities including those that are less than investment grade, and early stage companies). A more detailed comparison of the principal risks of the Funds is contained in Proxy Statement/Prospectus. Please see the section entitled “ Risk Factors” for additional information.

Q. Do the Target Fund and the Acquiring Fund have different fundamental and non-fundamental investment restrictions?

A. The Target Fund and the Acquired Fund are both part of the Wasatch Funds Trust, and the Trust has adopted the same stated fundamental and non-fundamental investment restrictions for both Funds, subject to certain exceptions. In particular, the Acquiring Fund has a fundamental investment restriction, in general terms, prohibiting it from investing more that 5% of its total assets in any one issuer or holding more than 10% of the outstanding voting securities of such issuer except that up to 25% of the Acquiring Fund’s total assets may be invested without regard to such limitations, and various U.S. government, agency and instrumentality obligations or repurchase agreements secured by such obligations are also excluded from such limitations. The Target Fund does not have such a fundamental restriction. In addition, the Acquiring Fund has adopted the following two non-fundamental investment restrictions that the Acquiring Fund will not (a) make investments for the purpose of exercising control or management and (b) invest more than 10% of its total assets (taken at market value at the time of each investment) in Special Situations (i.e., companies in the process of reorganization or buy-out). The Target Fund has not adopted such non-fundamental investment restrictions. Further, the non-fundamental investment policies of the Funds may be changed upon Board approval without shareholder approval. See the section of the Proxy/Statement Prospectus entitled “Comparison of the Funds” for additional information regarding the Funds’ fundamental and non-fundamental investment restrictions.

Q. How do the investment performance of the Acquiring Fund and the Target Fund compare?

A. The Acquiring Fund formerly had been a large cap value fund investing primarily in the equity securities of domestic companies with a market capitalization of $5 billion at time of purchase and as of February 2017, the Acquiring Fund increased its ability to invest up to 20% of its total assets in the securities issued by foreign companies in developed or emerging markets. The Fund sought to further expand its foreign investment exposure becoming a global value fund as of October 31, 2017. Accordingly, the performance information prior to such date would be for the prior investment strategy and would not reflect the current investment strategy. In comparing

5

Table of Contents

past performance, the Investor Class shares of the Acquiring Fund outperformed the Investor Class shares of the Target Fund for the one-, three-, five- and ten-year periods ended December 31, 2017. Furthermore, based on the Investor Class shares for the calendar years from 2008 through 2017, the Acquiring Fund outperformed the Target Fund in six of those ten calendar years. Although the inception dates of the Institutional Class shares of the Global Value Fund and Long/Short Fund was January 31, 2012 and December 13, 2012, respectively, the performance of the Institutional Class of a Fund was similar to that of its Investor Class as the classes are invested in the same portfolio of securities and differences in performance between the classes would be principally attributed to differences in expenses. However, you should be aware that the usefulness of the comparisons of the performance may be limited given that the performance history of the Acquiring Fund does not reflect the recent changes to its principal investment strategies.

Q. How will the Reorganization impact fees and expenses?

A. Based on the unaudited annualized expenses as of March 31, 2018, the total gross and net annual operating expenses are expected to decrease for the shareholders of both classes of the Target Fund following the Reorganization. In this regard, the management fee will be reduced from 1.10% for the Target Fund to 0.90% for the combined Acquiring Fund for both classes. The total gross annual fund operating expenses of the Investor Class and Institutional Class shares of the Target Fund of 1.91% and 1.77%, respectively, are estimated to be reduced to 1.20% and 1.13%, respectively, based on the pro forma gross expenses of the combined fund as a result of the proposed Reorganization. The net annual fund operating expenses of the Investor Class and Institutional Class shares of the Target Fund of 1.86% and 1.36%, respectively, are estimated to be reduced to 1.10% and 0.95%, respectively, based on the pro forma net expenses of the combined fund as a result of the proposed Reorganization. Pro forma amounts are estimated and actual operating expenses may vary.

In addition, the total annual fund operating expenses after waivers is based on a contractual expense limitation agreement pursuant to which the Advisor has contractually agreed to waive fees and/or reimburse expenses of the Target Fund and the Acquiring Fund so that total annual operating expenses of each class of the respective Fund do not exceed certain levels (excluding interest, dividend expense on short sales/interest expense, taxes, brokerage commissions, other investment-related costs, acquired fund fees and expenses, and extraordinary expenses such as litigation and other expenses not incurred in the ordinary course of business). The expense limitation on both classes of the Acquiring Fund is lower than the expense limitation on the corresponding class of the Target Fund, and the contractual expense agreement of the Acquiring Fund will remain in effect through January 31, 2020 compared to January 31, 2019 for the Target Fund. If the expense cap of the Acquiring Fund is not renewed after January 31, 2020, the total annual fund operating expenses after waivers of the Acquiring Fund could increase depending upon, among other things, the size of the Acquiring Fund at that time.

6

Table of Contents

Under the expense limitation agreement of both Funds, the Advisor may recoup certain amounts previously paid. In this regard, to calculate the required waiver or reimbursement, the Advisor will waive or reimburse expenses each day that the amount of the annualized operating expenses of a class exceeds its expense limit; however, the Advisor may be reimbursed such amounts on any day during the fiscal year the annualized expenses of a class are below its expense limit to the extent the reimbursement does not cause the class’s expenses to exceed the expense cap. The Fund may only make repayments to the Advisor if such repayment does not cause the Fund’s expense ratio after the repayment is taken into account to exceed both (i) the expense cap in place at the time such amounts were waived; and (ii) the Fund’s current expense cap. Regardless of the ability to recoup expenses under the terms of the current expense limitation agreement, the Advisor has agreed that it will not attempt to recoup any Reorganization expenses from the Target Fund.

See the section entitled “Comparison of the Funds – Fees and Expenses” in the Proxy Statement/Prospectus for additional information.

Q. Why does the Board recommend the Reorganization?

A. The Board of Trustees, including the Independent Trustees, approved the Reorganization. The Board concluded that the Reorganization was in the best interests of the Target Fund and the Acquiring Fund and their respective shareholders, and further that the interests of existing shareholders of each Fund would not be diluted as a result of the Reorganization. The Board considered various factors in evaluating the Reorganization and reaching its conclusion, with no single factor identified as all-important or controlling, including, among other things:

| • | the compatibility of the Funds’ investment objectives, principal investments strategies and related risks; |

| • | the consistency of portfolio management; |

| • | the Funds’ relative sizes; |

| • | the relative fees and expense ratios of the Funds, including the contractual expense caps on the combined fund’s expenses for both share classes; |

| • | the anticipated federal income tax-free nature of the Reorganization; |

| • | the expected costs of the Reorganization and the extent to which the Funds would bear any such costs; |

| • | the terms of the Reorganization and whether the Reorganization would dilute the interests of the shareholders; |

| • | the effect of the Reorganization on shareholder rights; |

| • | alternatives to the Reorganization, and |

| • | any potential benefits of the Reorganization to the Advisor and its affiliates as a result of the Reorganization. |

7

Table of Contents

For a more complete discussion of the Board’s considerations, please see the section entitled “Approval of the Proposed Reorganization by the Board of Trustees” in the Proxy Statement/Prospectus.

Q. Will the Reorganization create a taxable event for me?

A. No. The Reorganization is intended to qualify as a tax-free reorganization for federal income tax purposes. It is expected that you will recognize no gain or loss for federal income tax purposes as a direct result of the Reorganization. Prior to the closing of the Reorganization, the Target Fund expects to distribute all of its net investment income and net capital gains, if any. The Target Fund is not expected to have any capital gain distributions as a direct result of the Reorganization. All or a portion of such a distribution may be taxable to Target Fund shareholders and will generally be taxed as ordinary income or capital gains for federal income tax purposes, unless you are investing through a tax-advantaged account such as an IRA or 401(k) plan (in which case you may be taxed upon withdrawal of your investment from such account). The tax character of such distributions will be the same regardless of whether they are paid in cash or reinvested in additional shares. In addition, the Target Fund may recognize gains or losses as a result of portfolio sales and closing of short positions effected prior to the Reorganization, including sales anticipated in connection with the repositioning described above. Such gains or losses may increase or decrease the net capital gains or net investment income to be distributed by the Target Fund to its shareholders, and may increase or decrease the Target Fund’s capital loss carryforwards. The Target Fund is expected to have significant short-term and long-term losses to be carried forward, subject to IRS limitations and expiration (“loss carryforwards”).

Q. Who will bear the costs of the Reorganization?

A. The costs of the Reorganization incurred by the Target Fund will be split equally between the Advisor and Target Fund, subject to the contractual expense cap limitations. The total estimated expenses of the Reorganization of the Target Fund are $394,000 which includes, among other things, the legal, audit and proxy solicitation fees of approximately $338,000, and brokerage costs. Brokerage costs are the only transaction cost associated with the repositioning of the Target Fund, which are estimated at approximately $56,000 (0.09% of the Target Fund’s net assets) assuming it had occurred as of March 31, 2018. These are estimates and actual amounts may vary. Amounts charged to the Target Fund will generally be allocated between its share classes based on the relative net assets of the share classes, except that each class separately bears expenses related specifically to that class. To the extent that the Target Fund’s expenses, (including any Reorganization expenses for which the Target Fund is responsible), exceed the Fund’s current contractual expense cap on the respective share class, the Advisor also will waive and/or reimburse the Target Fund’s expenses (including the portion of the Reorganization expenses allocated to the Target Fund) to the extent necessary for the Fund’s share classes to operate within their respective cap. Regardless of the ability to recoup expenses under the terms of the current expense limitation agreement, the Advisor has agreed that it will not seek to recoup any Reorganization expenses.

8

Table of Contents

In addition, the Acquiring Fund and indirectly its shareholders (including former shareholders of the Target Fund who hold shares in the Acquiring Fund ) also are estimated to incur approximately $20,000 in brokerage commission related to the acquisition of portfolio securities from cash received in the Reorganization.

If the Reorganization is not approved or completed, the Advisor will pay all expenses associated with the Reorganization. See the section entitled “The Proposed Reorganization—Reorganization Expenses” in the Proxy Statement/Prospectus for additional information.

Q. What is the timetable for the Reorganization?

A. If approved by the Target Fund’s shareholders at the special meeting of shareholders on August 30, 2018, the Reorganization of the Target Fund is expected to occur at the close of business on September 7, 2018 or as soon as practicable thereafter.

Q. What happens if shareholders do not approve the Reorganization?

A. If the Reorganization is not approved, the Board of Trustees will take such action as it deems to be in the best interests of the Target Fund, including continuing to operate the Target Fund as a stand-alone Fund, liquidating the Target Fund, or other options the Board of Trustees may consider.

General

Q. Whom do I call if I have questions?

A. If you need any assistance, or have any questions regarding the proposals or how to vote your shares, please call AST Fund Solutions, the proxy solicitor hired by the Target Fund, at (800) 628-8532 weekdays during its business hours of 9:00 a.m. to 10:00 p.m. Eastern time. Please have your proxy materials available when you call.

Q. How do I vote my shares?

A. You may vote in person, by mail, by telephone or over the Internet:

| • | To vote in person, please attend the special meeting of shareholders and bring your photographic identification. If you hold your Target Fund shares through a bank, broker or other nominee, you must also bring satisfactory proof of ownership of those shares and a “legal proxy” from the nominee. |

| • | To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. |

| • | To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. |

| • | To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide. |

9

Table of Contents

Q. Will anyone contact me?

A. You may receive a call from AST Fund Solutions, the proxy solicitor hired by the Target Fund, to verify that you received your proxy materials, to answer any questions you may have about the proposals and to encourage you to vote your proxy.

We recognize the inconvenience of the proxy solicitation process and would not impose on you if we did not believe that the matters being proposed were important. Once your vote has been registered with the proxy solicitor, your name will be removed from the solicitor’s follow-up contact list.

Q. How does the Board of Trustees suggest that I vote?

A. After careful consideration, the Board has agreed unanimously that the proposed Reorganization is in the best interests of the Target Fund and recommends that you vote “FOR” the proposal. If shareholders do not approve the Reorganization, the Board of Trustees will take such action as it deems to be in the best interests of the Target Fund, including continuing to operate the Fund as a stand-alone fund, liquidating the Fund, or such other options the Board of Trustees may consider.

Your vote is very important. We encourage you as a shareholder to participate in your Fund’s governance by returning your vote as soon as possible. If enough shareholders fail to cast their votes, your Fund may not be able to hold its shareholder meeting or the vote on the issue, and your Fund will be required to incur additional solicitation costs in order to obtain sufficient shareholder participation.

10

Table of Contents

WASATCH FUNDS TRUST

July 27, 2018

Dear Shareholders:

We are pleased to invite you to the special meeting of shareholders of Wasatch Long/Short Fund (the “Target Fund”) (the “Special Meeting”). The Special Meeting is scheduled for August 30, 2018, at 10:00 a.m. Mountain time, at the offices of Wasatch Advisors, Inc. at 505 Wakara Way, 3rd Floor, Salt Lake City, Utah 84018. At the Special Meeting, you will be asked to consider the reorganization of your fund into Wasatch Global Value Fund (formerly Wasatch Large Cap Value Fund) (the “Acquiring Fund” and together with the Target Fund, the “Funds” and each a “Fund”) (the “Reorganization”). It is important for you to recognize that the Acquiring Fund and the Target Fund have materially different investment strategies.

The Target Fund’s investment objective is capital appreciation, whereas the Acquiring Fund’s investment objective is capital appreciation and income. The Target Fund is a long/short fund that pursues its investment objective by primarily investing in equity securities of domestic companies through long and short positions, which means that when the Target Fund takes a long position, it purchases the security outright in hope that the price will rise, and when it takes a short position, it sells a security that it does not own in hope that the price will fall and the Fund can repurchase such security at a lower price. The use of both long and short positions allows the investment advisor to invest based on both its positive and negative views of individual stocks. Unlike the Target Fund, the Acquiring Fund does not engage in short sales as a principal investment strategy. While both Funds invest primarily in equity securities, the Acquiring Fund is a global value fund that invests primarily in equity securities of domestic and foreign securities (including companies domiciled in emerging and frontier markets) through a long only portfolio. As the Target Fund invests primarily in the equity securities of domestic companies, the Target Fund has limited exposure to foreign securities.

While there are differences in the investment objectives and strategies of the Funds, Wasatch Advisors, Inc. (the “Advisor”), each Fund’s investment adviser, has proposed the Reorganization due to, among other things, the limited growth prospects and economic infeasibility of the Target Fund over the long term, the similar analysis used by the portfolio manager to evaluate potential investments for both Funds despite the differing investment strategies, the overlap of portfolio holdings, the lower contractual management fee and estimated lower gross and net expense ratios (before and after fee waivers) of the combined fund for both share classes following the Reorganization, the lower contractual expense cap of the combined fund for both classes, and the tax consequences to shareholders if the Target Fund was liquidated compared to the anticipated tax-free nature of the Reorganization. Given the foregoing, the Advisor and Board of Trustees believe that it would be in the best interests of the Target Fund shareholders to reorganize the Target Fund into the Acquiring Fund and recommend that you vote “FOR” the Reorganization.

Table of Contents

Please review the attached Proxy Statement/Prospectus which provides more information about the proposal.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense and to assure that your shares are represented, please vote as promptly as possible, regardless of whether or not you plan to attend the Special Meeting. You may vote by mail, by telephone or over the Internet. To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide.

If you intend to attend the Special Meeting in person and you are a record holder of the Target Fund’s shares, in order to gain admission, you must show photographic identification, such as your driver’s license. If you intend to attend the Special Meeting in person and you hold your shares through a bank, broker or other nominee, in order to gain admission, you must show photographic identification, such as your driver’s license, and satisfactory proof of ownership of shares of the Target Fund, such as your voting instruction form (or a copy thereof) or broker’s statement indicating ownership as of a recent date. If you hold your shares in a brokerage account or through a bank or other nominee, you will not be able to vote in person at the Special Meeting unless you have previously requested and obtained a “legal proxy” from your broker, bank or other nominee and present it at the Special Meeting.

We appreciate your continued support and confidence in Wasatch and our family of funds.

Very truly yours,

Eric S. Bergeson

President

Table of Contents

JULY 27, 2018

WASATCH LONG/SHORT FUND

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON AUGUST 30, 2018

To the Shareholders:

Notice is hereby given that a special meeting of shareholders of Wasatch Long/Short Fund (the “Target Fund”), a series of Wasatch Funds Trust (the “Trust”), a Massachusetts business trust, will be held at the offices of Wasatch Advisors, Inc. at 505 Wakara Way, 3rd Floor, Salt Lake City, Utah 84018, on August 30, 2018 at 10:00 a.m., Mountain time (the “Special Meeting”), for the purposes described below.

| 1. | To approve an Agreement and Plan of Reorganization (and the related transactions) which provides for (i) the transfer of all the assets of the Target Fund to Wasatch Global Value Fund (formerly Wasatch Large Cap Value Fund) (the “Acquiring Fund”) in exchange solely for Investor Class and Institutional Class shares of beneficial interest of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Target Fund; and (ii) the pro rata distribution of Investor Class and Institutional Class shares of the Acquiring Fund to the shareholders of Investor Class and Institutional Class shares of the Target Fund, respectively, in complete liquidation and termination of the Target Fund (the “Reorganization”). |

| 2. | To transact such other business as may properly come before the Special Meeting. |

Only shareholders of record as of the close of business on June 30, 2018 are entitled to vote at the Special Meeting or any adjournments or postponements thereof.

All shareholders are cordially invited to attend the Special Meeting. In order to avoid delay and additional expense and to assure that your shares are represented, please vote as promptly as possible, regardless of whether or not you plan to attend the Special Meeting. You may vote by mail, by telephone or over the Internet. To vote by mail, please mark, sign, date and mail the enclosed proxy card. No postage is required if mailed in the United States. To vote by telephone, please call the toll-free number located on your proxy card and follow the recorded instructions, using your proxy card as a guide. To vote over the Internet, go to the Internet address provided on your proxy card and follow the instructions, using your proxy card as a guide.

If you intend to attend the Special Meeting in person and you are a record holder of the Target Fund’s shares, in order to gain admission, you must show photographic identification, such as your driver’s license. If you intend to attend the Special Meeting in person and you hold your shares through a bank, broker or other nominee, in order to gain admission, you must show photographic identification, such as your driver’s license, and satisfactory proof of ownership of shares of the Target Fund, such as your

Table of Contents

voting instruction form (or a copy thereof) or broker’s statement indicating ownership as of a recent date. If you hold your shares in a brokerage account or through a bank or other nominee, you will not be able to vote in person at the Special Meeting unless you have previously requested and obtained a “legal proxy” from your broker, bank or other nominee and present it at the Special Meeting.

| Eric S. Bergeson President |

Table of Contents

PROXY STATEMENT/PROSPECTUS

DATED JULY 30, 2018

Relating to the Acquisition of the Assets and Liabilities of

WASATCH LONG/SHORT FUND

By

WASATCH GLOBAL VALUE FUND

This Proxy Statement/Prospectus is being furnished to shareholders of Wasatch Long/Short Fund (the “Target Fund”), a series of Wasatch Funds Trust, a Massachusetts business trust (the “Trust”), and an open-end investment company registered under the Investment Company Act of 1940 Act, as amended (the “1940 Act”), and relates to the special meeting of shareholders of the Target Fund to be held at the offices of Wasatch Advisors, Inc. at 505 Wakara Way, 3rd Floor, Salt Lake City, Utah 84018, on August 30, 2018 at 10:00 a.m., Mountain time and at any and all adjournments and postponements thereof (the “Special Meeting”). This Proxy Statement/Prospectus is provided in connection with the solicitation by the Board of Trustees of the Trust (the “Board of Trustees” or the “Trustees”) of proxies to be voted at the Special Meeting. The purpose of the Special Meeting is to allow the shareholders of the Target Fund to consider and vote on the proposed reorganization (the “Reorganization”) of the Target Fund into Wasatch Global Value Fund (formerly Wasatch Large Cap Value Fund) (the “Acquiring Fund”), also a series of the Trust. The Target Fund and the Acquiring Fund are collectively referred to herein as the “Funds” and individually as a “Fund.”

If shareholders approve the Reorganization of the Target Fund and the Reorganization is completed, each Target Fund shareholder will receive shares of the Acquiring Fund in an amount equal in total value to the total value of the Target Fund shares surrendered by such shareholder. Shareholders of Investor Class shares of the Target Fund will receive Investor Class shares of the Acquiring Fund. Shareholders of Institutional Class shares of the Target Fund will receive Institutional Class shares of the Acquiring Fund. The Board of Trustees has determined that the Reorganization of the Target Fund is in the best interests of the Target Fund. The address, principal executive office and telephone number of the Funds and the Trust is 505 Wakara Way, 3rd Floor, Salt Lake City, Utah 84108, (800) 551-1700.

The enclosed proxy and this Proxy Statement/Prospectus are first being sent to shareholders of the Target Fund on or about July 30, 2018. Shareholders of record as of the close of business on June 30, 2018 are entitled to vote at the Special Meeting.

The Securities and Exchange Commission has not approved or disapproved these securities or determined whether the information in this Proxy Statement/ Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Table of Contents

This Proxy Statement/Prospectus concisely sets forth the information shareholders of the Target Fund should know before voting on the Reorganization (in effect, investing in Investor Class and Institutional Class shares of the Acquiring Fund, as applicable) and constitutes an offering of Investor Class and Institutional Class shares of beneficial interest of the Acquiring Fund. Please read it carefully and retain it for future reference.

The following documents have been filed with the Securities and Exchange Commission (“SEC”) and are incorporated into this Proxy Statement/Prospectus by reference:

| (i) | the Acquiring Fund’s Prospectus for Investor Class shares dated January 31, 2018, only insofar as it relates to the Acquiring Fund (File Nos. 033- 10451 and 811-04920); and |

| (ii) | the Acquiring Fund’s Prospectus for Institutional Class shares dated January 31, 2018, only insofar as it relates to the Acquiring Fund (File Nos. 033- 10451 and 811-04920); and |

| (iii) | the audited financial statements contained in the Acquiring Fund’s Annual Report, only insofar as they relate to the Acquiring Fund, for the fiscal year ended September 30, 2017 (File No. 811-04920); and |

| (iv) | the financial statements contained in the Acquiring Fund’s Semi-Annual Report, only insofar as they relate to the Acquiring Fund, for the six months ended March 31, 2018 (File No. 811-04920). |

The following documents contain additional information about the Funds and have been filed with the SEC and are incorporated into this Proxy Statement/Prospectus by reference:

| (i) | the Statement of Additional Information relating to the Reorganization, dated July 27, 2018 (the “Proxy Statement/Prospectus SAI”); and |

| (ii) | the Target Fund’s Prospectus for Investor Class shares dated January 31, 2018, only insofar as it relates to the Target Fund (File Nos. 33- 10451 and 811-04920); and |

| (iii) | the Target Fund’s Prospectus for Institutional Class shares dated January 31, 2018, only insofar as it relates to the Target Fund (File Nos. 33-10451 and 811-04920); and |

| (iv) | the audited financial statements contained in the Funds’ Annual Report, only insofar as they relate to the Funds, for the fiscal year ended September 30, 2017 (File No. 811-04920); and |

| (v) | the financial statements contained in the Funds’ Semi-Annual Report, only insofar as they relate to the Funds, for the six months ended March 31, 2018 (File No. 811-04920); and |

Table of Contents

| (vi) | the Target Fund’s Statement of Additional Information for Investor Class shares dated January 31, 2018, only insofar as it relates to the Target Fund (File Nos. 033- 10451 and 811-04920); and |

| (vii) | the Acquiring Fund’s Statement of Additional Information for Investor Class shares dated January 31, 2018, only insofar as it relates to the Acquiring Fund (File Nos. 033- 10451 and 811-04920); and |

| (viii) | the Target Fund’s Statement of Additional Information for Institutional Class shares dated January 31, 2018, only insofar as it relates to the Target Fund (File Nos. 033- 10451 and 811-04920); and |

| (ix) | the Acquiring Fund’s Statement of Additional Information for Institutional Class shares dated January 31, 2018, only insofar as it relates to the Acquiring Fund (File Nos. 033- 10451 and 811-04920). |

No other parts of the Funds’ Annual Report or Semi-Annual Report are incorporated by reference herein.

Copies of the foregoing may be obtained without charge by calling or writing the Funds at (800) 551-1700 or by writing to Wasatch Funds, P.O. Box 2172, Milwaukee WI 53201. If you wish to request the Proxy Statement/Prospectus SAI, please ask for the “Proxy Statement/Prospectus SAI.” In addition, the Acquiring Fund will furnish, without charge, a copy of its most recent annual report to a shareholder upon request. Any such request should be directed to the Acquiring Fund at the telephone number or address shown above.

The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the 1940 Act, and in accordance therewith files reports and other information with the SEC. Reports, proxy statements, registration statements and other information filed by the Trust (including the Registration Statement relating to the Acquiring Fund on Form N-14 of which this Proxy Statement/ Prospectus is a part) may be inspected without charge and copied (for a duplication fee at prescribed rates) at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549 or at the SEC’s Northeast Regional Office (3 World Financial Center, New York, New York 10281) or Midwest Regional Office (175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604). You may call the SEC at (202) 551-8090 for information about the operation of the Public Reference Room. You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

Table of Contents

TABLE OF CONTENTS

Table of Contents

| Compatibility of Investment Objectives, Principal Investment Strategies and Related Risks |

48 | |||

| 50 | ||||

| 50 | ||||

| 50 | ||||

| 51 | ||||

| 51 | ||||

| 52 | ||||

| 52 | ||||

| 53 | ||||

| 53 | ||||

| 53 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| Continuation of Shareholder Accounts, Plans and Privileges; Share Certificates |

56 | |||

| 56 | ||||

| 57 | ||||

| 60 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 65 | ||||

| 66 | ||||

| Information Filed with the Securities and Exchange Commission |

67 | |||

2

Table of Contents

| 67 | ||||

| 67 | ||||

| 69 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 70 | ||||

| 70 | ||||

| 70 | ||||

| 71 | ||||

| A-1 | ||||

| B-1 | ||||

3

Table of Contents

REORGANIZATION OF THE TARGET FUND INTO THE ACQUIRING FUND

The following is a summary of, and should be read in conjunction with, the more complete information contained in this Proxy Statement/Prospectus and the information attached hereto or incorporated herein by reference, including the form of Agreement and Plan of Reorganization.

As discussed more fully below and elsewhere in this Proxy Statement/Prospectus, the Board of Trustees is recommending that shareholders approve the Reorganization of the Wasatch Long/Short Fund (the Target Fund) into the Wasatch Global Value Fund (the Acquiring Fund). The Board of Trustees believes the proposed Reorganization is in the best interests of the Target Fund and that the interests of the Target Fund’s existing shareholders would not be diluted as a result of the Reorganization. The Reorganization is intended to qualify as a tax-free reorganization under Section 368(a) of the Internal Revenue Code of 1986. If shareholders of the Target Fund approve the Reorganization and it is completed, the Target Fund shareholders will become shareholders of the Acquiring Fund and will cease to be shareholders of the Target Fund.

Shareholders should read the entire Proxy Statement/Prospectus carefully together with the Acquiring Fund’s Prospectus that accompanies this Proxy Statement/Prospectus, which is incorporated herein by reference. Shareholders should read carefully and understand that the Target Fund and the Acquiring Fund have materially different investment strategies and objectives. See the section entitled “Comparison of the Funds” below for a comparison of investment policies, fees and expenses, and other matters. This Proxy Statement/Prospectus constitutes an offering of Investor Class and Institutional Class shares of the Acquiring Fund.

Wasatch Advisors, Inc. (“Wasatch” or the “Advisor”) serves as the investment adviser to each of the Funds. After considering the costs associated with the continued operation of the Target Fund, its relative poor performance and its limited future growth prospects and economic infeasibility over the long term given the costs of continued operation and its likely inability to attract assets in the foreseeable future, the Advisor has proposed the Reorganization of the Target Fund into the Acquiring Fund. Although the investment objectives and strategies are materially different between the Target Fund and the Acquiring Fund, the Advisor has proposed the Reorganization with the Acquiring Fund due, in part, to the similar valuation process used by the Advisor to evaluate potential investments for the Funds despite the differing investment strategies; the overlap of portfolio holdings between the Funds; the relative performance of the Acquiring Fund compared to the Target Fund; the lower contractual management fee and estimated lower gross and net expense ratio (before and after fee waivers) of the combined fund for both share classes, the lower contractual expense cap of the Acquiring Fund which would be in effect through January 31, 2020 and the anticipated federal income tax-free nature of the Reorganization compared to a taxable event for shareholders if the Target Fund was liquidated.

Table of Contents

This Proxy Statement/Prospectus is being furnished to shareholders of the Target Fund in connection with the proposed combination of the Target Fund into the Acquiring Fund pursuant to the terms and conditions of the Agreement and Plan of Reorganization entered into by (i) Wasatch Funds Trust (the “Trust”), on behalf of each Fund, and (ii) the Advisor (the “Agreement”).

The Agreement provides for (i) the transfer of all the assets of the Target Fund to the Acquiring Fund in exchange solely for Investor Class and Institutional Class shares of beneficial interest of the Acquiring Fund (“Acquiring Fund Shares”) and the assumption by the Acquiring Fund of all the liabilities of the Target Fund; and (ii) the pro rata distribution of Investor Class and Institutional Class shares of the Acquiring Fund to the shareholders of Investor Class and Institutional Class shares of the Target Fund, respectively, in complete liquidation and termination of the Target Fund.

If shareholders of the Target Fund approve the Reorganization and it is completed, Target Fund shareholders will become shareholders of the Acquiring Fund. The Board of Trustees has determined that the Reorganization is in the best interests of the Target Fund and that the interests of existing Target Fund shareholders would not be diluted as a result of the Reorganization. The Board of Trustees unanimously approved the Reorganization and the Agreement at a meeting held on November 7-8, 2017 (the “November Meeting”). The Board of Trustees recommends a vote “FOR” the Reorganization.

The costs of the Reorganization of the Target Fund will be split equally between the Advisor and Target Fund, subject to the contractual expense cap limitations. The total estimated expenses of the Reorganization are $394,000 which includes, among other things, the legal, audit and proxy solicitation fees of approximately $338,000, and brokerage costs. Brokerage costs are the only transaction cost associated with the repositioning of the Target Fund, which are estimated at approximately $56,000 (0.09% of the Target Fund’s net assets) assuming it had occurred as of March 31, 2018. These amounts are estimated and actual amounts may vary. Amounts charged to the Target Fund generally will be allocated between its share classes based on the relative net assets of the share classes, except that each class separately bears expenses related specifically to the class. To the extent that the Target Fund’s expenses (including any Reorganization expenses for which the Target Fund is responsible), exceed the Fund’s current contractual expense cap on the respective share class, the Advisor will waive and/or reimburse the Target Fund’s expenses (including the portion of the Reorganization expenses allocated to the Target Fund) to the extent necessary for the Fund’s share classes to operate within their contractual expense cap. Regardless of the ability to recoup expenses under the terms of the current expense limitation agreement, the Advisor has agreed that it will not seek to recoup any Reorganization expenses. Based on current expense levels, it is anticipated that the Advisor will absorb a significant portion of the Reorganization expenses charged to the Target Fund. In addition, the Acquiring Fund and indirectly its shareholders (including former shareholders of the Target Fund who hold shares in the Acquiring Fund) are estimated to incur approximately $20,000 in brokerage commission

2

Table of Contents

related to the acquisition of portfolio securities from cash received in the Reorganization. If the Reorganization is not approved or not completed, the Advisor will pay all expenses associated with the Reorganization.

The Board of Trustees is asking shareholders of the Target Fund to approve the Reorganization at the Special Meeting to be held on August 30, 2018. Approval of the Reorganization requires the affirmative vote of the holders of a majority of the total number of the Target Fund’s shares outstanding and entitled to vote. This means the vote of (1) 67% or more of the voting securities present at a meeting, if the holders of more than 50% of the outstanding voting securities are present or represented by proxy or (2) more than 50% of the outstanding voting securities, whichever is less. See “Voting Information and Requirements” below.

If shareholders of the Target Fund approve the Reorganization, it is expected that the Reorganization will occur at the close of business on September 7, 2018 or such other date as agreed to by the parties (the “Closing Date”). If the Reorganization is not approved, the Board of Trustees will take such action as it deems to be in the best interests of the Target Fund, including continuing to operate the Target Fund as a stand-alone Fund, liquidating the Target Fund, or other options the Board of Trustees may consider. The Closing Date may be delayed and the Reorganization may be abandoned at any time by the mutual agreement of the parties. In addition, either Fund may at its option terminate the Agreement at or before the closing due to (i) a breach by any other party of any representation, warranty or agreement contained in the Agreement to be performed at or before the closing, if not cured within 30 days of notification to the breaching party and prior to the closing, (ii) a condition precedent to the obligations of the terminating party that has not been met or waived and it reasonably appears that it will not or cannot be met or (iii) a determination by the Board of Trustees that the consummation of the transactions contemplated by the Agreement is not in the best interests of such Fund.

Comparison of Investment Objectives and Investment Policies

The Target Fund’s investment objective is capital appreciation. The Acquiring Fund’s investment objectives are to seek capital appreciation and income. The investment objective of each Fund may be changed without shareholder approval upon at least 60 days advance notice to shareholders of the applicable Fund.

Although both Funds invest primarily in equity securities, there are certain material differences in their investment strategies. The Target Fund pursues its investment objective by primarily investing in equity securities of domestic companies, maintaining long equity and short equity positions, whereas the Acquiring Fund pursues its investment objectives by primarily investing in equity securities of foreign and domestic companies through a long only portfolio. When evaluating a potential long or short investment for the Target Fund or a potential investment for the Acquiring Fund, the portfolio manager uses a comprehensive valuation analysis with particular emphasis on company fundamentals (such as, price-to-sales, price-to-book, price-to-earnings and price/earnings-to-growth ratios and discounted cash flow models) as well as considers other economic and market factors which is intended to establish a range for fair valuation or intrinsic company value

3

Table of Contents

for the potential investment. The portfolio manager of the Target Fund and the Acquiring Fund, however, may consider additional factors in determining an investment’s valuation as described in further detail in the section entitled “Comparison of the Funds –Principal Investment Strategies” of the Proxy Statement/Prospectus.

In pursuit of its investment objectives, under normal conditions, the Acquiring Fund will invest its net assets primarily in the equity securities of foreign and domestic companies of all market capitalizations. The Acquiring Fund will typically invest in securities issued by companies domiciled in at least three countries, including the United States. The Acquiring Fund will invest a significant portion of its total assets in securities of companies domiciled in foreign countries (under normal market conditions, at least 40% of its assets will be invested outside the United States, or if conditions are not favorable, 30% of its will be invested outside the United States). The Acquiring Fund is also permitted to invest a significant amount of its total assets at the time of purchase in securities issued by companies domiciled in emerging and frontier markets, which are those countries currently included in the Morgan Stanley Capital International (MSCI) EFM (Emerging + Frontier Markets) Index, including the Asia-Pacific region, Eastern Europe, the Middle East, Central and South America and Africa (under normal market conditions we expect to invest between 5% to 50% in securities domiciled in emerging and frontier markets). Securities issued by foreign companies incorporated outside the U.S. whose securities are principally traded in the United States are not defined as “foreign companies” and therefore are not subject to this limitation. Accordingly, to qualify as a foreign company under the above limitations, the company must be incorporated outside of the United States and its securities principally traded in a foreign jurisdiction. Although the Target Fund is permitted to invest in foreign securities, it is not a principal investment strategy of the Fund and therefore the Acquiring Fund has additional risks associated with its investments in foreign securities, including emerging and frontier markets.

With respect to the Target Fund, the Target Fund invests primarily in equity securities by maintaining long equity and short equity positions. Under normal market conditions, the Target Fund invests its assets in the equity securities of companies with market capitalizations of at least $100 million at the time of purchase that the Advisor has identified as being undervalued (long equity positions) and sell those securities (short equity positions) that the Advisor has identified as being overvalued. The Fund is permitted at any time have either a net long exposure or a net short exposure to the equity markets. The Target Fund is not managed to maintain either net long or net short market exposures. Although the Acquiring Fund may make short sales of securities, it is not a principal investment strategy of the Fund. Accordingly, the Target Fund will be subject to certain additional risks associated with its use of short sales. In addition, the Target Fund seeks to achieve a higher risk-adjusted return with lower volatility compared to equity markets in general (as represented by the S&P 500 Index). The Acquiring Fund does not have a similar mandate.

4

Table of Contents

While the Target Fund and the Acquiring Fund have materially different investment strategies, they have both been invested in securities of relatively large capitalization companies. The Target Fund also is permitted to invest in the equity securities of U.S. companies with a market capitalization of at least $100 million at the time of purchase, and the Target Fund has historically been invested in securities of over US $5 billion, similar to the Acquiring Fund. For comparison, as of June 30, 2018 the Target Fund invested 88% of its assets in securities of U.S. companies with a market capitalization of over US $5 billion and the Acquiring Fund invested 85% of its assets in securities of U.S. and foreign companies with a market capitalization of over US $5 billion. As of June 30, 2018, eighteen of the twenty larger cap U.S. companies held by the Target Fund (approximately 70% of the Target Fund’s portfolio) were also held by the Acquiring Fund.

As a principal investment strategy, the Target Fund also is permitted to invest in early stage companies, initial public offerings (“IPOs”), and fixed income securities of any maturity, including those that are less than investment grade. The Acquiring Fund, however, may invest in investment grade fixed-income securities, early stage companies and IPOs but not as a principal investment strategy. Both Funds are also permitted to invest a large percentage of their assets in a few sectors.

Although the Funds have some similar principal risks as a result of their exposure to equity securities, the principal risks of investing in each of the Funds have some significant differences due to the differences in principal strategies. In particular, the Target Fund is subject to short sales and market direction risks associated with its short sale strategy; interest rate risk, credit risk and non-investment grade risk associated with its ability to invest in fixed-income securities as a principal investment strategy; as well as smaller company stock risk, early stage company risk and initial public offering risk all of which are not principal risks of the Acquiring Fund. Similarly, the Acquiring Fund is subject to the principal risks associated with investing in foreign securities, including emerging market and frontier market risks, but these are not principal risks of the Target Fund. See the section of the Proxy Statement/Prospectus entitled “Risk Factors” for a comparison of and additional information regarding each Fund’s principal investment risks and “Comparison of the Funds” for additional information regarding the Funds’ investment strategies.

Relative Investment Performance

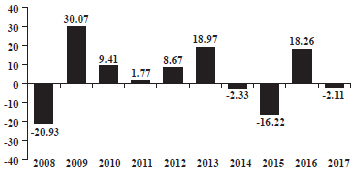

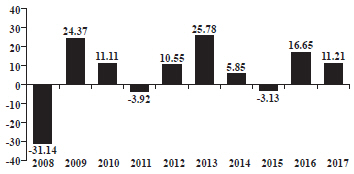

The Acquiring Fund formerly had been a large cap value fund investing primarily in the equity securities of domestic companies with a market capitalization of $5 billion at time of purchase and as of February 2017, the Acquiring Fund increased its ability to invest up to 20% of its total assets in the securities issued by foreign companies in developed or emerging markets. The Fund sought to further expand its foreign investment exposure becoming a global value fund as of October 31, 2017. Accordingly, the performance information prior to such date would be for the prior investment strategy and would not reflect the current investment strategy. In reviewing performance, the Investor Class shares of the Acquiring Fund outperformed the Investor Class shares of the Target Fund for the one-, three-, five- and ten-year periods ended December 31,

5

Table of Contents

2017. Furthermore, based on the Investor Class shares for the calendar years from 2008 through 2017, the Acquiring Fund outperformed the Target Fund in six of those ten calendar years. Although the inception dates of the Institutional Class shares of the Global Value Fund and Long/Short Fund was January 31, 2012 and December 13, 2012, respectively, the performance of the Institutional Class was similar to that of the Investor Class as the classes are invested in the same portfolio of securities and differences in performance between the classes would be principally attributed to differences in expenses. However, the usefulness of the comparisons of the performance may be limited given the performance history of the Acquiring Fund does not reflect the recent changes to its principal investment strategies.

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Funds have identical procedures for purchasing, exchanging and redeeming shares for each corresponding share class. The Target Fund and the Acquiring Fund each offer two classes of shares: Investor Class and Institutional Class shares. The corresponding classes of each Fund have the same investment eligibility criteria. The Target Fund normally declares and pays dividends from net investment income, if any, annually. The Acquiring Fund normally declares and pays dividends from net investment income, if any, quarterly. For each Fund, any net capital gains are normally distributed at least once a year. See “Comparison of the Funds—Distribution, Purchase, Redemption, Exchange of Shares and Dividends” below for a more detailed discussion.

Material Federal Income Tax Consequences of the Reorganization

As a condition to closing the Reorganization, the Target Fund and the Acquiring Fund will receive an opinion from Chapman & Cutler LLP., subject to certain representations, assumptions and conditions, substantially to the effect that the Reorganization will qualify as a tax-free reorganization under Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, it is expected that neither Fund will recognize any gain or loss for federal income tax purposes as a direct result of the Reorganization. Prior to the Closing Date, the Target Fund will declare a distribution of all of its net investment income and net capital gains, if any. All or a portion of such a distribution may be taxable to the Target Fund’s shareholders for federal income tax purposes.

Prior to the closing of the reorganization, the Target Fund will reposition its portfolio. For comparison, as of June 30, 2018 the Target Fund invested 88% of its assets in securities of U.S. companies with a market capitalization of over US $5 billion and the Acquiring Fund invested 85% of its assets in securities of U.S. and foreign companies with a market capitalization of over US $5 billion. As of June 30, 2018, eighteen of the twenty larger cap U.S. companies held by the Target Fund (approximately 70% of the Target Fund’s portfolio) were also held by the Acquiring Fund. The Target Fund’s portfolio will be repositioned in connection with the Reorganization. The companies currently held in the Target Fund that are not also held in the Acquiring Fund (approximately 6% of the value of the Target Fund) will be sold prior to the Reorganization. In addition, the short positions in the Target Fund will be closed (approximately 22% of the value of the Target Fund) prior to the Reorganization. If such purchases and sales had occurred

6

Table of Contents

as of March 31, 2018, it is estimated that such portfolio repositioning of the Target Fund would have resulted in total brokerage commissions or other transaction costs of approximately $56,000. Approximately $28,000 of these costs are expected to be paid by for the Target Fund and approximately $28,000 by the Advisor. These are estimates and actual amounts may vary. These transaction costs represent expenses of the Target Fund that will not be subject to the Target Fund’s expense cap and will be borne by the Target Fund and indirectly borne by the Target Fund’s shareholders. As of September 30, 2017, the Target Fund had unused short-term capital loss carryforwards of $26.2 million and long-term capital loss carryforwards of $127.7 million that will be used to offset any gains recognized by the Fund prior to the Reorganization. In the unlikely event that gains exceed the loss carryforwards, capital gains from such portfolio sales may result in increased distributions of net capital gain and net investment income. If such sales occurred as of March 31, 2018, the sales would not have resulted in increased distributions of net capital gain and net investment income to shareholders.

Taking into account the repositioning of the Target Fund, the Acquiring Fund is not expected to sell a material portion of the Target Fund’s assets received in the Reorganization in order to meet its investment policies and restrictions. An estimated $20,000 in brokerage commissions related to the acquisition of portfolio securities by the Acquiring Fund from cash received in the Reorganization is borne by the Acquiring Fund and indirectly by its shareholders (including former shareholders of the Target Fund who hold shares of the Acquiring Fund following the Reorganization).

For a more detailed discussion of the federal income tax consequences of the Reorganization, please see “The Proposed Reorganization—Material Federal Income Tax Consequences” below.

In evaluating the Reorganization, you should consider carefully the risks of the Acquiring Fund to which you will be subject if the Reorganization is approved and completed. Investing in a mutual fund involves risk, including the risk that you may receive little or no return on your investment or even that you may lose part or all of your investment. Because of these and other risks, you should consider an investment in the Acquiring Fund to be a long-term investment. An investment in the Acquiring Fund may not be appropriate for all shareholders. An investment in either Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. For a complete description of the risks of an investment in the Acquiring Fund, see the sections in the Acquiring Fund’s Prospectus for your share class entitled “Principal Risks” and “Wasatch Funds-Additional Information about the Funds.”

7

Table of Contents

Both Funds share many of the same principal risks associated with their investments in equity securities. Additionally, each Fund has principal risks unique to its principal investment strategies. The following table provides a comparison of the principal risks associated with an investment in each Fund. A description of each principal risk is also provided below.

| Principal Risks

|

Target Fund

|

Acquiring Fund

| ||

|

Stock Market Risk |

X |

X | ||

| Market Direction Risk |

X | |||

| Stock Selection Risk |

X | X | ||

| Short Sales Risk |

X | |||

| Smaller Company Stock Risk |

X | |||

| Early Stage Companies Risk |

X | |||

| Initial Public Offerings Risk |

X | |||

| Early Stage Companies Risk |

X | |||

| Value Investing Risk |

X | X | ||

| Interest Rate Risk & Effective Duration |

X | |||

| Credit Risk |

X | |||

| Non-Investment Grade Securities Risk |

X | |||

| Equity Securities Risk |

X | X | ||

| Foreign Securities Risk |

X | |||

| Emerging Markets Risk |

X | |||

| Frontier Markets Risk |

X | |||

| Portfolio Turnover Rate |

X | |||

| Sector and Industry Weightings Risk |

X | X | ||

| Consumer Discretionary Sector Risk |

X | X | ||

| Consumer Staples Sector Risk |

X | X | ||

| Energy Sector Risk |

X | X | ||

| Financials Sector Risk |

X | X | ||

| Health Care Sector Risk |

X | X | ||

| Industrials Sector Risk |

X | X | ||

| Information Technology Sector Risk |

X | X | ||

| Materials Sector Risk |

X | X | ||

| Real Estate Sector Risk |

X | X | ||

| Telecommunications Sector Risk |

X | X | ||

| Utilities Sector Risk |

X | X |

|

Principal Risk

|

Target Fund

|

Acquiring Fund

|

How They

| |||

|

Stock Market Risk

|

The Fund’s investments may decline in value due to movements in the overall stock market.

|

The Fund’s investments may decline in value due to movements in the overall stock market.

|

Same |

8

Table of Contents

| Principal Risk

|

Target Fund

|

Acquiring Fund

|

How

They

| |||

| Market Direction Risk | Since the Fund has both a “long” and a “short” portfolio, an investment in the Fund will involve market risks associated with different investment decisions than those made for a typical “long only” stock fund. The Fund’s results will suffer both when there is a general stock market advance and the Fund holds significant “short” equity positions, or when there is a general stock market decline and the Fund holds significant “long” equity positions.

|

Not a principal risk of the Acquiring Fund. | A principal risk of the Target Fund. Not a principal risk of the Acquiring Fund. | |||

| Stock Selection Risk | The Fund’s investment may decline in value even when the overall stock market is not in general decline. | The Fund’s investment may decline in value even when the overall stock market is not in general decline. | Same | |||

| Short Sales Risk | The Fund can make short sales of securities, which means it may experience a loss if the market price of the security increases between the date of the short sale and the date the security is replaced. Short sales may reduce a fund’s returns or increase volatility. In addition, a lender may request, or market conditions may dictate, that securities sold short be returned to the lender on short notice, which may result in the Fund having to buy the securities sold short at an unfavorable price to close out a short position. If this occurs, any anticipated gain to the Fund may be reduced or eliminated or the short sale may result in a loss.

In a rising stock market, the Fund’s short positions may significantly impact the Fund’s overall performance and cause the Fund to underperform traditional long-only equity funds or to sustain losses, particularly in a sharply rising market. The use of short sales may also cause the Fund to have higher expenses than other funds. |

Not a principal risk of the Acquiring Fund. | A principal risk of the Target Fund. Not a principal risk of the Acquiring Fund. | |||

9

Table of Contents

| Principal Risk

|

Target Fund

|

Acquiring Fund

|

How

They

| |||

| Because losses on short sales arise from increases in the value of the security sold short, such losses are theoretically unlimited. By contrast, a loss on a long position arises from decreases in the value of the security and is limited by the fact that a security’s value cannot go below zero. The use of short sales in combination with long positions in seeking to improve Fund performance or reduce overall portfolio risk may not be successful and may result in greater losses or lower positive returns than if the Fund held only long positions. In addition, the Fund’s short selling strategies may limit its ability to fully benefit from increases in the equity markets. Short positions also typically involve increased liquidity risk and the risk that the third party to the short sale may fail to honor its contract terms.

Furthermore, regulatory authorities in various countries, including the United States, have enacted temporary rules prohibiting the short-selling of certain stocks in response to market events. If regulatory authorities were to reinstitute such rules or otherwise restrict short selling, the Fund might not be able to fully implement its short-selling strategy.

The Fund will comply with guidelines established by the Securities and Exchange Commission and its prime broker with respect to coverage of short positions, and, if the guidelines so require, will set aside appropriate liquid assets in a segregated custodial account in the amount prescribed. As a result, there is the possibility that segregation of a large percentage of the Fund’s assets could impede portfolio management or the Fund’s ability to meet redemption requests or other current obligations.

|

||||||

10

Table of Contents

| Principal Risk

|

Target Fund

|

Acquiring Fund

|

How

They

| |||

| Smaller Company Stock Risk | Small- and mid-cap stocks may be very sensitive to changing economic conditions and market downturns. In particular, the issuers of small company stocks have more narrow markets for their products and services, fewer product lines, and more limited managerial and financial resources than larger issuers. The stocks of small companies may therefore be more volatile and the ability to sell these stocks at a desirable time or price may be more limited.

|

Not a principal risk of the Acquiring Fund. | A principal risk of the Target Fund. Not a principal risk of the Acquiring Fund. | |||

| Early Stage Companies Risk | Early stage companies may never obtain necessary financing, may rely on untested business plans, may not be successful in developing markets for their products or services, and may remain an insignificant part of their industry, and as such may never be profitable. Stocks of early stage companies may be illiquid, privately traded, and more volatile and speculative than the securities of larger companies.

|