EXHIBIT 15.2

The Company’s responses to the requirements of Form 20-F (except for Item 16E “Purchases of Equity Securities by the Issuer and Affiliated Purchasers” and the US Audit Report of Independent Accountants, which is included under Item 18 “Financial Statements”) have been incorporated into this annual report by reference to the Company’s Report on Form 6-K dated March 22, 2006 which contains the Company’s Annual Report and Accounts 2005. Pursuant to Rule 12b-23(a) of the Securities Exchange Act of 1934, as amended, the information incorporated into this annual report by reference to such Form 6-K is attached as an exhibit hereto.

![]()

| Our 2005 highlights | ||||||

| Business Performance* | Total Results | |||||

| £ 5

664 m 2004 £4 063m |

Revenue

and other operating income |

£ 5

424 m 2004 £4 063m |

||||

| £ 2 138 m 2004 £1 320m |

Operating

profit before share of results from joint ventures and associates |

£ 2 344 m 2004 £1 407m |

||||

£ 2 380 m |

Total

operating profit including share of pre-tax operating results from joint ventures and associates |

£ 2 586 m 2004 £1 600m |

||||

| £ 1

357 m 2004 £829m |

Earnings | £ 1

528 m 2004 £886m |

||||

| 38.3 p 2004 23.5 p |

Earnings per share | 43.2 p 2004 25.1 p |

||||

| Dividend per share | 6.00 p 2004 3.81 p |

|||||

| * Business Performance excludes disposals and certain re-measurements and is presented as exclusion of these items provides readers with a clear and consistent presentation of the underlying operating performance of the Group’s ongoing business. Unless otherwise stated, financial operating information for the Group and its business segments presented in the statements of the Chairman and Chief Executive and in the Operating and financial review is based on BG Group’s Business Performance. See presentation of non-GAAP measures, page 152. See, also, Segmental analysis and results presentation, note 2, page 71, and Earnings per ordinary share, note 10, page 85, for a reconciliation of the differences between Business Performance and BG Group’s Total Results. | ||||||

| Contents | ||||||||

| 2 | [This section has intentionally been removed] | 51 | Remuneration report | |||||

| 4 | [This section has intentionally been removed] | 62 | [This section has intentionally been removed] | |||||

| 6 | Operating and financial review | 63 | Principal accounting policies | |||||

| 6 | BG Group’s global operations | 66 | Primary statements | |||||

| 8 | Strategy review | 71 | Notes to the accounts | |||||

| 12 | Future prospects | 128 | Supplementary information | From 1 January 2005, BG Group was required to prepare its consolidated financial statements in accordance with International Financial Reporting Standards (IFRS) endorsed by the European Union. The adoption of IFRS has resulted in the comparative information for 2003 and 2004 being restated. Further details on the restatement of the results previously reported under UK GAAP are given in Note 33, page 118. | ||||

| 13 | Operating review | 134 | Three year financial summary | |||||

| 21 | Financial review | 138 | Shareholder information | |||||

| 31 | Corporate Responsibility | 146 | Notice of Annual General Meeting | |||||

| 35 | Risk factors | 150 | Cross reference to Form 20-F | |||||

| 38 | Corporate governance | 151 | Index | |||||

| 38 | Governance framework | 152 | Presentation of non-GAAP measures | |||||

| 44 | Board of Directors | 153 | Definitions | |||||

| 46 | Executive Committee | |||||||

| 49 | Directors’ report | |||||||

|

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

1 |

Our vision

Natural gas is our business.

We are a rapidly growing company,

with expertise across the gas chain.

Our vision is to be the leading natural

gas company in the global energy

market

– operating responsibly

and delivering outstanding

value

to our shareholders.

Key events |

|

| • | Egyptian LNG Trains 1 and 2 and matching upstream supply onstream early |

| • | Record production of 183.8 mmboe, up 10% |

| • | Atlantic LNG Train 4 completed, further increasing Liquefied Natural Gas (LNG) supply |

| • | Awarded or acquired

new licences in Brazil, Canada, Egypt, India, Libya, Nigeria, Norway, the UK and the USA, increasing gross exploration acreage by over 45 000 km2 |

| • | Discoveries in Canada, Egypt, Mauritania, Trinidad and Tobago and the UK |

| • | Phase 1 expansion of Lake Charles LNG regasification facility completed |

| • | Sale of our interest in the North Caspian Sea PSA |

| • | Secured future additional LNG regasification capacity at Elba Island |

|

www.bg-group.com |

BG Group is a public limited company listed on the London and New York Stock Exchanges and registered in England & Wales. This is the report and accounts for the year ended 31 December 2005. It complies with UK regulations and incorporates the annual report on Form 20-F (except for the US Report of Independent Accountants, which is included in the Group’s Form 20-F filing with the US Securities and Exchange Commission) to meet US regulations.

| 6 | BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating

and financial review

BG Group’s global

operations(a)

|

For more information: www.bg-group.com | |

BG Group’s main activities

BG Group has skills across the gas chain, in the upstream, midstream and downstream.

| Exploration and Production (E&P) |  |

BG Group explores, develops, produces and markets gas and oil around the world. Around 73% of 2005 production was gas. The Group uses its technical, commercial and gas chain skills to deliver projects at low cost, whilst maximising the sales value of its hydrocarbons.

| Liquefied Natural Gas (LNG) |  |

BG Group’s LNG activities combine the development of LNG liquefaction and regasification facilities with the purchasing, shipping and sale of LNG. The Group uses its expertise in LNG to connect its own and other producers’ gas reserves to markets.

| BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

7 |

| Transmission and Distribution (T&D) |  |

BG Group’s T&D expertise and activities develop markets for natural gas and provide them with supply from its own and others’ reserves through transmission and distribution networks and complementary businesses.

| Power |  |

A large proportion of the worldwide demand for gas is attributable to power stations. BG Group develops, owns and operates gas-fired power generation plants.

| Other activities |  |

BG Group leverages its distribution customer base to develop complementary businesses that stimulate gas demand. These include compressed natural gas for vehicles and co-generation.

8 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial

review

Strategy review

| “We

are unique in our industry because we specialise in gas and have the skills to compete right across the gas chain.” |

||

| William Friedrich | Frank Chapman |

| Deputy Chief Executive | Chief Executive |

STRATEGY

BG Group

is an integrated gas company that aims to achieve strong growth and competitive

returns through a strategy focused on securing competitively priced gas and

bringing that

gas to high value markets.

BG Group’s competitive advantage stems from a deep understanding of gas markets combined with industry-leading skills in finding and commercialising gas. This capability allows BG Group to capture opportunities and develop projects that deliver value across the entire chain.

The strategy has remained fundamentally unchanged for some years because it continues to deliver value to shareholders and has proved robust in the face of developments in the business environment.

FUTURE

GROWTH

BG

Group’s

ability to achieve strong growth is underpinned by existing assets that have

a distinctive, low cost, long-life base with substantial growth potential.

In addition, other drivers of long-term growth are:

| • | incremental investments around existing assets; |

| • | the ability to connect assets to enhance value; and |

| • | new opportunities, building on core competencies. |

BG Group’s cost competitive, flexible LNG portfolio is of particular importance. Core US market access positions at Lake Charles and Elba Island anchor value from the upstream business – both from equity and contracted gas supplies. Over the next two years an important transition will occur as

Group-wide activities BG Group is a rapidly growing business with operations in over 20 countries and across five continents. BG Group is principally engaged in exploration and production and the development and supply of existing and emerging gas markets around the world. Gas discoveries often require complex chains of physical infrastructure and commercial agreements to deliver the gas to markets and BG Group has proven skills and experience in creating value from these chains. |

|||||

| BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

9 |

material long-term contracts come onstream to provide the major share of the LNG supply portfolio. It is anticipated that spot and short-term supply opportunities will continue to be available to the Group. BG Group expects to capture further value by taking arbitrage opportunities in response to short-term market conditions.

In addition to supplying high value markets in the USA and Europe, BG Group is also developing valuable positions in other markets including Brazil and India. These markets have material long-term growth potential driven by underlying economic growth. BG Group continues to grow its businesses along the gas chain and to play an active part in contributing to market development.

Exploration success will be an important determinant of long-term growth. At a time when accessing resources has become one of the central challenges for the industry, BG Group has substantially increased gross exploration acreage in the last year. This is expected to contribute to sustaining the Group’s growth in the next decade.

BUSINESS ENVIRONMENT

The advantages

of natural gas relative to other fossil fuels are well established. Natural gas

is relatively clean and can be supplied at a competitive cost from a geographically

diverse range of sources.

The energy industry continues to experience significant change. Oil and gas prices have risen over the year and continue to be at levels well above historical averages. The global gas business has seen an increase in inter-regional gas trade, driven by fundamental changes to supply and demand patterns. This is driving rapid growth in the LNG industry.

Competition and security of supply have become increasingly important factors. Sustained higher oil and gas prices and heightened geopolitical tensions have added to the concerns of major consumer countries, and raised doubts about the reliability of hydrocarbon imports.

In the context of the more demanding business environment, BG Group is highly competitive. This is primarily due to the following factors:

| • | BG Group has a distinctive, long-life, low cost asset base; |

| • | as LNG markets grow rapidly, BG Group has already established a cost competitive, flexible portfolio in theAtlantic Basin and is building on this position; |

| • | in the face of increasing competition, the Group continues to expand its portfolio of opportunities for continued growth; and |

| Positive outlook for gas | Energy

consumption (%) Compound annual growth rate 2000-2025 |

||||

|

Gas is predicted to grow faster than other competing fuels. Two key factors of gas demand driving energy policies across the world are security of supply and climate change. Gas is more abundant than oil and has the lowest carbon dioxide emissions of all hydrocarbon fuels. Many countries are converting to gas-fired power production to sustain growth and meet Kyoto targets. | ||||

| Natural gas | |||||

| Coal | |||||

| Renewables | |||||

| Oil | |||||

| Nuclear | |||||

| Source: EIA July 2005 | |||||

| • | BG Group continues to make good progress in broadening and deepening its exploration portfolio to underpin long-term growth. | ||||

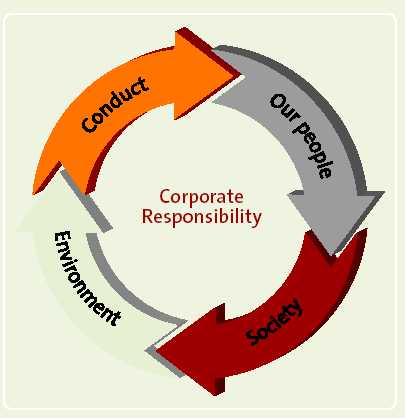

CORPORATE

RESPONSIBILITY BG Group believes that it is good business to operate responsibly and that successful relationships with host governments and neighbouring communities contribute to good and sustainable returns for shareholders. The BG Group Statement of Business Principles sets out beliefs and behaviours which guide the way the Group and its employees conduct business. The Business Principles apply to all Directors, officers and employees. The Corporate Responsibility section (page 31) summarises BG Group’s social and environmental performance. The 2005 Corporate Responsibility Report, a separate publication, contains more detail on this area. |

|||||

| 10 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating

and financial review

Strategy review continued

| Strategy in action |

BG Group’s strategy is to secure competitively priced resource (oil and gas) – both equity and contracted supply – and bring that resource to customers in high value markets.

Gas is often more difficult to commercialise than oil because, unlike oil, there is no globally traded market for gas. In addition, gas is more difficult to store and transport. As a result, specialist skills are required to put together gas chains that link resources to markets.

BG Group maintains a deep understanding of current gas demand and market trends and has been successful in creating markets for its gas.

Securing competitive supplies is an essential part of BG Group’s strategy, and cost leadership is a pre-requisite for long-term success. Although industry costs have been rising, BG Group is maintaining its competitive advantage in key performance metrics. The Group’s supplies remain cost competitive against peer companies.

| For more information: www.bg-group.com | ||

| Creating value across the gas chain |

BG Group’s understanding of market trends and industry-leading skills across the gas chain have allowed the Group to identify high quality opportunities.

| Exploration and Production | |

| CASE STUDY: UK | ||

| Securing competitively priced supply for the UK | ||

| In the UK, BG Group is working to maintain its supply position from a range of piped and LNG sources. The Group’s production hubs and infrastructure in the UK North Sea are adding value to new prospects and exploration acreage across the median line in Norway. The Group is importing gas from Europe via its share in the expanded Interconnector pipeline and is developing a LNG import terminal in Wales. | ||

|

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

11 |

| Liquefied

Natural Gas |

|

| Transmission | |

| CASE STUDY: USA | |

| LNG is key to accessing high value US market | |

| In the USA, the market access afforded by the Group’s regasification capacity at Lake Charles and Elba Island is adding value to the Group’s reserves in Trinidad and Tobago and Egypt and will underpin the Group’s continuing investment in Nigeria. It also allows the Group to purchase third-party LNG from sources such as Nigeria and Equatorial Guinea and to take advantage of LNG arbitrage opportunities. | |

| Power |

|

| Distribution | |

| CASE STUDY: EGYPT | |

| Building on success in Egypt | |

| Success in Egypt has been the result of first class project delivery combined with government alignment. The business started by supplying the domestic market but has rapidly developed into a LNG export scheme to target higher priced international markets. There is the potential for expansion at the liquefaction plant and through explorationof the Group’s new and existing acreage. | |

12 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating

and financial review

Future prospects

| Future prospects |

| Building on the Group’s distinctive |

| asset base, with new significant |

| projects and exploration acreage |

| driving the earnings trajectory out |

| to 2009 and beyond. |

| Key plans and opportunities | ||||||

| • | North Sea: Buzzard field and UK production hubs | • | Brazil: Comgas network growth and improved margins | |||

| • | Tunisia: Miskar and Hasdrubal fields | • | Kazakhstan: Karachaganak field de-bottlenecking, stabilisation and gas development | |||

| • | India: Panna/Mukta and Tapti fields plus new Krishna Godavari basin acreage | • | Nigeria: OKLNG and upstream position | |||

| • | Trinidad and Tobago: uncontracted reserves and additional liquefaction | • | USA: increases in LNG regasification capacity at Elba Island and Lake Charles | |||

| • | Egypt: Egyptian LNG Train 3 and new exploration plays | • | Further long-term LNG supply from Nigeria, Egypt and Trinidad and Tobago | |||

| Long-term growth – exploration and appraisal wells planned in 2006 | ||||||

GROWTH

FROM EXISTING ASSETS

BG

Group’s asset base is distinctive because of its low cost, long-life nature

and the potential it has for substantial embedded growth. Assets that were onstream

in 2003 are expected to produce almost as much in 2012, highlighting the strength

of the existing asset base. Examples of such assets include UK North Sea production

hubs, Tunisia, Karachaganak and Trinidad and Tobago.

In the LNG segment, BG Group has emerged as a leading LNG player in the Atlantic Basin. Embedded within the existing business, the Group has options to expand its regasification capacity to underpin new trains of liquefaction and new LNG purchase agreements.

MAJOR

NEW PROJECTS

BG

Group has a number of significant projects and further opportunities. These

include Buzzard, further development of Karachaganak, Hasdrubal, Comgas growth

and new LNG supplies from Nigeria, Trinidad and Tobago and Egypt.

As the majority of these opportunities are already within the Group’s portfolio, the risk to delivery is significantly lower than if the Group was to rely solely on accessing new exploration opportunities.

EXPLORATION

SUCCESS

BG

Group has also made progress in securing new gross exploration acreage, adding

over 45 000 km2

in

2005. This is expected to contribute towards sustaining the Group’s growth

well into the next decade from existing areas such as Brazil, Norway and Canada

and new areas including Alaska, Libya and Nigeria.

| 13 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating review

| Exploration and Production |

| BG Group’s high performing |

| E&P business had another |

| strong year in 2005. The 2006 |

| production target has been |

| increased to 600 000 boed. |

| Highlights | ||||||

| • | Total operating profit increased by 63% to £1 942 million | • | Acquired exploration acreage in Canada, India, Nigeria, Norway and the USA and successful in licensing rounds in Brazil, Egypt, Libya, Norway and the UK, increasing gross acreage by over 45 000 km2 | |||

| • | 29 exploration and appraisal wells drilled with 14 successful | |||||

| • | Successful exploration and appraisal wells in Canada (8), Egypt (1), Mauritania (2), Trinidad and Tobago (1) and the UK (2) | |||||

| • | Early start-up of Simian Sienna and Sapphire fields to supply Egyptian LNG Trains 1 and 2 | |||||

| †The countries are listed in order of production volume | ||||||

| (a), (b) and (c) See Definitions, page 153 for an explanation of how these figures are calculated. | ||||||

2005

PERFORMANCE†

Production

increased by 10% to 183.8 mmboe in 2005. The main contributors to this increase

were Kazakhstan (4.4 mmboe) and Egypt (21.1 mmboe). 2004 production volumes

rose by 7% (11 mmboe), due mainly to contributions from Kazakhstan and Egypt.

In 2005, proved reserves increased to 2 184 mmboe (2004 2 147 mmboe) after net additions and revisions to proved reserves of 219 mmboe. Full details can be found on page 128.

Of the 29 exploration and appraisal wells completed in 2005, 14 were successful. Successful wells were drilled in Canada (8), Egypt (1), Mauritania (2), Trinidad and Tobago (1) and the UK (2). At the beginning of 2006, there were two further discoveries in the UK and one in India.

UK

and Norway

The

UK accounted for around 30% of BG Group’s production in 2005. The principal

operating assets are the Armada and Seymour fields, the Blake Field, the Easington

Catchment Area (ECA fields), the Everest and Lomond fields, the J-Block (Joanne

and Judy) and Jade fields, and the Elgin/Franklin fields. BG Group also has

a 51.18% interest in the Central Area Transmission System (CATS).

The NW Seymour, Atlantic/Cromarty and Glenelg fields are due onstream in the first half 2006. Substantial progress was made on the Buzzard field, which is expected to begin production at the end of 2006.

BG Group announced discoveries in the Courageous, Jackdaw, Calloway and Banks fields at the turn of the year 2005-2006.

In the UK’s 23rd licensing round, held during 2005, BG Group was awarded four blocks and their operatorship, consolidating BG Group’s position in the Outer Moray Firth and central North Sea.

Since entry in early 2004, BG Group has secured 15 exploration licences offshore Norway, which include four licences awarded in the pre-defined licensing round in December 2005. Eight of these licences lie adjacent to the UK/Norway median line and close to the Group’s UK central North Sea core producing area and offshore infrastructure. Exploration drilling is expected to continue in 2006. In September 2005, BG Group farmed-in to production licence (PL) 251, taking a 20% interest. An exploration well discovered hydrocarbons but not in economic quantities. The Group also took an 80% interest in, and operatorship of, PL 274BS, which is adjacent to BG Group-operated PL 297 in the southern North Sea.

| 14 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Operating review continued

| Production (‘000 boed) | |||

| Production volumes have grown at a | |||

| compound average growth rate of 9% | |||

| between 2003 and 2005 | |||

| Actual gas | |||

| Actual oil and liquids | |||

| Target | |||

| Exploration and appraisal wells | |||

| BG Group’s success rate has averaged | |||

| 61% over the last three years | |||

| Total number of wells completed | |||

| Number of successful wells | |||

Egypt

BG Group

is operator

of two gas-producing areas offshore the Nile Delta – the Rosetta concession

and the West Delta Deep Marine (WDDM) concession (comprising the producing Scarab

Saffron, Simian Sienna and Sapphire fields and the Serpent, Saurus, Sequoia and

Solar discoveries). Total production from Egypt was 35 mmboe in 2005 (2004 14

mmboe).

2005 was a year of considerable progress for BG Group’s activities in Egypt. BG Group continues to be a key supplier to the domestic market through its Rosetta and Scarab Saffron fields and began supplying the Egyptian LNG export project in the second quarter 2005. Simian Sienna came onstream to supply Egyptian LNG Train 1 from April 2005, around the time that Rosetta Phase 2 began delivering to the domestic market. The Sapphire field came onstream in September 2005 to supply Train 2. Development of the Simian Sienna and Sapphire fields was accelerated in tandem with Egyptian LNG to come onstream three and nine months ahead of schedule, respectively.

In July 2005, the concession agreements for the El Manzala and El Burg offshore blocks were signed. Drilling on these new concessions is planned for 2007. In January 2006, BG Group also finalised terms for the North Sidi Kerir Deep concession, subject to ratification by the People’s Assembly.

The development of the Scarab Saffron fields provides an example of world class project delivery, producing first gas in March 2003, following discovery in May 1998. The Scarab Saffron development is one of the longest sub-sea tie backs in the world and the first deep water development in Egypt. Like Rosetta, Scarab Saffron has proved to be highly reliable and able to produce above its Daily Contracted Quantity (DCQ). The fields supply the domestic market (626 mmscfd rising to 726 mmscfd DCQ since October 2005). From the first quarter 2005, BG Group and partners began tolling 225 mmscfd of gas from Scarab Saffron through the SEGAS LNG plant located at Damietta. BG Group has agreed to purchase 0.7 mtpa of the related LNG output for markets in the Atlantic Basin (see LNG section page 16).

Kazakhstan

BG Group

is joint operator of the giant Karachaganak oil and gas condensate field (BG

Group 32.5%) in north-west Kazakhstan, one of the largest in the world. BG Group

produced around 35 mmboe net in Kazakhstan in 2005. Following the completion

of the Phase II

facilities in 2004, production in 2005 has increased, reaching a gross 2005 peak rate of over 402 000 boed. In 2005, in excess of 51 mmbbl (approximately 70%) of total field liquids were shipped through the Caspian Pipeline Consortium (CPC) pipeline (BG Group 2%) and sold at international prices. De-bottlenecking of the facility, which is expected to take western exports up to 7.7 mtpa, is expected to be onstream by the end of 2006. The remaining untreated production continues to be sold to Russian markets. In excess of 600 mmscfd of gas is re-injected into the reservoir during liquids production.

There was continued success with the Phase IIM drilling programme during 2005, which has seen individual well rates of up to 13 000 bopd, more than double the previous average.

BG Group plans to further increase production and export to western markets with a fourth stabilisation train in 2009, that will take western exports to over 10 mtpa, and Phase III expansion that is planned to further increase liquids and gas production in the next decade.

BG Group completed the disposal of its share in the North Caspian Sea PSA (BG Group 16.67%) in April 2005 for a pre-tax cash consideration of US$1.8 billion.

Trinidad and Tobago

BG Group

produced 18 mmboe of gas in Trinidad and Tobago during 2005. The BG Group-operated

Dolphin field in the East Coast Marine Area (ECMA) supplies gas into the domestic

market whilst the BG Group-operated North Coast Marine Area (NCMA) supplies gas

into Atlantic LNG Trains 2, 3 and 4 for export to North America. Sub-sea technology

was introduced to Trinidad and Tobago for the first time with the drilling of

two wells on

BG Group’s Dolphin Deep field, which are expected onstream in the first

half 2006 to supply Atlantic LNG Trains 3 and 4. BG Group also expects to supply

Atlantic LNG Train 4 from the Central Block field from mid-2006.

In February 2005, BG Group and partners announced a major gas discovery in the offshore Manatee 1 exploration well in Block 6d, ECMA.

Tunisia

BG Group

produced around 13 mmboe of gas and condensate in Tunisia during 2005. BG Tunisia

continues to supply approximately 50% of gas demand in the Tunisian market from

its Miskar

field (BG Group 100%). Miskar gas is processed at the Group’s onshore Hannibal

terminal and sold under long-term contract to the Tunisian state electricity

and gas company. Offshore compression was commissioned

| BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

15 |

in May 2005 to maintain the production plateau of the field. Infill drilling to extend Miskar is scheduled to commence in 2006.

Progress has been made on the development of the Hasdrubal field (BG Group 50%) and gross production of around 30 000 boed is expected onstream from 2009.

India

In 2005,

BG Group’s expanded Panna/Mukta and Tapti (PMT) fields produced over 9 mmboe

net. Currently, less than 9% of the power generated within India is fuelled by

natural gas, compared to an average of around 20% worldwide. BG Group believes

that this, together with potential for increasing gas penetration in the industrial,

commercial and residential market segments, offers growth opportunities.

Gas production at the PMT fields has increased by around 43% on a net basis since their acquisition in 2001. The Group is working with partners and the government to progress expansion projects that are planned to almost double PMT’s oil and gas production rate in the next four years. As part of this, BG Group and its partners are working towards bringing the mid Tapti field onstream in late 2007. Government approval for the US$492 million compression and processing platform was granted in 2005. The fourth wellhead platform on the south Tapti field is scheduled to come onstream in 2006 to help maintain a 250 mmscfd production rate.

In October 2004, the Government approved a US$200 million (gross) development plan for the Panna field and the EPC contract in respect of this development was awarded in 2004. The investment is expected to recover an additional 18 mmbbl of oil and 74 bcf of gas from the field. In addition, the Panna infill programme involves drilling 18 wells, expected to increase recovery by around 35 mmbbl and 130 bcf gas.

In December 2005, BG Group and ONGC agreed to jointly operate three offshore deep water exploration blocks in the Krishna Godavari Basin, on the east coast of India. Subject to agreeing farm-in arrangements and government approval, BG Group will hold a 50% interest in these blocks.

Thailand

BG Group

continues to invest in the Bongkot field, which accounts for over 20% of

Thailand’s domestic gas production. The successful commissioning of the

Sour Processing

Platform and further development phases are designed to

extend the life of the field into the next decade. In 2005, agreement was reached with gas buyer, the Petroleum Authority of Thailand, for the sale of additional gas averaging approximately 50 mmscfd over the next three years. This is over and above the DCQ (550 mmscfd). Record daily production levels for Bongkot were achieved during 2005.

Bolivia

BG Group

holds a number of E&P interests in Bolivia. Following the July 2004 referendum,

a new Hydrocarbons Law has been passed that marks a significant departure from

the principles that previously governed the hydrocarbon sector. A new administration

was elected in December 2005. BG Group continues to monitor the situation.

Gas continues to be delivered into the Bolivian and Brazilian markets from BG Group’s producing fields in Bolivia, including from the Margarita Early Production Facilities (BG Group 37.5%), which came onstream at the end of 2004.

Canada

In 2004,

BG Group acquired significant oil and gas acreage in Canada, of which a large

proportion was undeveloped, offering considerable exploration potential close

to existing

infrastructure.

The current producing assets are located in four core areas: Bubbles and Ojay (north-east part of British Columbia); Copton (western Alberta); and Waterton (south-western Alberta).

In May 2005, BG Group was awarded 110 196 net hectares in Blocks CMV 4 and CMV 7 (BG Group 70% and operator) in the North West Territories, extending BG Group’s activities into the Central Mackenzie Valley. A further 2 176 net hectares were acquired in Alberta and 6 150 net hectares in British Columbia, taking BG Group’s current total to around 346 000 hectares.

BG Group is continuing to explore the existing acreage and acquire additional land for its portfolio. Of 12 wells drilled in 2005, eight were successful.

Mauritania

BG Group

has a 13.084% interest in PSC A, and 11.630% in PSC B, other than the Chinguetti

field in which BG Group has 10.23% following the government exercising its back-in

right. Three other oil discoveries (Tiof, Tevet and Labeidna) have been made

in PSC B and a gas field (Banda) has been discovered in PSC A. The four-well

drilling campaign in 2005 resulted in one oil discovery (Labeidna) and also the

discovery of oil in Tevet Deep, although not in economic quantities. The Tiof

discovery is still under evaluation.

Associated gas has been found in all discoveries. Further exploration drilling is planned for 2006.

The Chinguetti field began production in February 2006 and is anticipated to have a peak production rate of 75 000 boed.

Brazil

In 2005,

drilling commenced on BM-S-10 block (BG Group 25%), BM-S-11 (BG Group 25%) and

on BG Group-operated BM-S-13 (BG Group 60%), all offshore São Paulo city.

In October 2005, BG Group was awarded ten blocks in the 7th licensing round, including six onshore blocks in the São Francisco Basin, two BG Group-operated blocks in shallow water and two deep water blocks in the Santos Basin, offshore São Paulo.

Libya

BG Group

was awarded three onshore exploration licences in the 2nd Libyan licensing round

in October 2005. Two licences are in the Sirte basin (BG Group 100% and operator)

and one

licence in the frontier Kufra basin (BG Group 50%).

Nigeria

BG Group

is developing an E&P and LNG position in Nigeria, one of the most prolific

hydrocarbon provinces in the Atlantic Basin. In January 2006, BG Group signed

a Production Sharing Contract (PSC) for Block 332 with the Nigerian National

Petroleum Corporation, which resulted in BG Group acquiring 45% and operatorship

in the deep water block, located in depths of 100 to 1 000 metres, around 100

km south-east of the commercial capital Lagos. The first phase of the two-part

work programme is expected to begin in 2006 with the acquisition of 3D seismic,

followed by the drilling

of an exploration well in 2007.

USA

In January

2006, BG Group signed a participation agreement for a 33.33% equity share in

2.1 million acres of land in the Foothills area of the Alaskan North Slope.

| 16 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Operating review continued

| Liquefied Natural Gas |

| During 2005, BG Group doubled |

| its number of operating |

| liquefaction trains from three |

| to six and doubled its capacity |

| at Lake Charles. |

| Highlights | ||||||

| • | Egyptian LNG Train 1 onstream three months early | • | Agreed to expand the storage and throughput capacity at Elba Island and option to participate in a new interstate pipeline | |||

| • | Egyptian LNG Train 2 onstream nine months early | • | PDA signed for OKLNG liquefaction plant | |||

| • | Atlantic LNG Train 4 onstream | • | MOU with Brass LNG for 2.0 mtpa for 20 years from 2010 | |||

| • | Supplied around 37% of US LNG imports | • | Letter of Agreement signed for sale and supply of LNG and construction of a LNG import terminal in Chile | |||

| • | Phase 1 expansion of Lake Charles regasification terminal onstream | |||||

2005 PERFORMANCE

Three

new trains of LNG came onstream – Trains 1 and 2 in Egypt and Train 4 in

Trinidad and Tobago. The first expansion phase of Lake Charles was completed

in the third quarter 2005, with the second phase on schedule for mid-2006. Construction

work commenced at the Brindisi and Milford Haven regasification projects. In

2005, 4.1 million tonnes of LNG was produced and the 2006 production target has

been increased by

3% to 7.1 mtpa.

LIQUEFACTION

Egypt

The first

cargo from Egyptian LNG Train 1 was despatched in May 2005, three months ahead

of schedule and in a record time of under six years from discovery of gas to

first cargo of LNG. Train 2 also came onstream in record time and despatched

its first cargo in September 2005.

Since the first quarter 2005, BG Group and partners have been tolling gas through SEGAS’ Damietta LNG plant under a five year contract. BG Gas Marketing Limited is also purchasing 0.7 mtpa of the related LNG for five years.

Trinidad and Tobago

The first

three trains of Atlantic LNG continued to perform well, and the fourth train,

one of the world’s largest operating trains of LNG (5.2 mtpa), came onstream

in December

2005.

Nigeria

BG Group

is jointly planning a liquefaction plant in Olokola (OKLNG) on the southwestern

coast of Nigeria. In February 2006, BG Group entered into a project development

agreement (PDA) with its partners, which provides the framework for the Front

End Engineering Design (FEED) phase. The project is planned to comprise four

trains of LNG of approximately 5.5 mtpa each. The LNG will be lifted by the project

sponsors.

REGASIFICATION

USA

Lake

Charles

During

2005, BG Group was responsible for meeting just over 1% of the US daily gas demand

and importing around 37% of LNG delivered into the USA.

The Phase 1 expansion of the Lake Charles plant by the operator Trunkline LNG came onstream in 2005. The increased capacity is contractually committed to BG Group, taking the Group’s total capacity rights from 0.63 bcfd up to 1.2 bcfd, with 1.5 bcfd peak send out.

Phase 2, which is expected to expand capacity further to 1.8 bcfd with 2.1 bcfd peaking capacity, is underway and is

|

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

17 |

scheduled for completion in mid-2006. Under the Phase 2 project, BG Group has further diversified its market destinations through firm capacity in the new 36" loop gas pipeline, completed in July 2005 by Trunkline Gas.

During the fourth quarter, Lake Charles received its first LNG cargoes from Egyptian LNG Train 2. From 2006, contracted supply will rise to 10 mtpa, with new long-term supply contracts from Trinidad and Tobago (Atlantic LNG Train 4) and Nigeria, and increase further from 2007 with supply from Equatorial Guinea. In addition, in February 2006, BG Group signed a Memorandum of Understanding (MOU) with Nigeria’s Brass LNG for the acquisition of 2.0 mtpa of LNG for 20 years, with initial deliveries expected to start during 2010. It is planned that cargoes will be delivered on an ex-ship basis to Lake Charles and Elba Island but BG Group will retain destination flexibility. During 2005, BG Group continued to source cargoes on the short-term market.

Gas Marketing

Since acquiring

capacity rights at Lake Charles in 2001 and Elba Island in 2004, BG Group has

put together an integrated gas marketing and distribution portfolio consisting

of access to over 15 intra-state pipelines, salt storage capacity and over 130

customers, providing BG Group with market and volume certainty. In a more competitive

market, BG Group secured 86 actual cargoes for delivery to the USA (36 cargoes

to Lake Charles and 50 cargoes to Elba Island) and remarketed a further 31 to

other higher value markets.

Elba Island

BG

Group and upstream partners’ LNG from Atlantic LNG Trains 2 and 3 is regasified

and marketed at Elba Island where the Group has had capacity and associated LNG

purchase and gas sales agreements since the end of 2003. In December 2005, BG

Group entered into agreements with El Paso Corporation to further expand the

storage and throughput capacity at the Elba Island terminal.

The expansion of Elba Island is planned to increase BG Group’s storage capacity at this terminal from 4 bcf to 8.2 bcf and increase vaporisation capacity from 675 mmscfd to 1.17 bcfd.

The expansion is expected to be completed by 2012. As part of the expansion project, BG Group also has rights to transportation capacity in the Elba Express Pipeline. This new 191 mile interstate pipeline is planned to deliver gas from Elba Island to additional markets in Georgia and, through interconnections

with other pipelines, to south-eastern and eastern USA. Both projects are expected to be filed for approval with the Federal Energy Regulatory Commission (FERC) in 2006.

Providence

Following

FERC’s rejection of their initial plans, BG LNG Services and KeySpan Corporation

continue to evaluate alternatives to address the issues raised by FERC regarding

the proposed upgrade to KeySpan’s LNG peak-shaving storage facility in Providence,

Rhode Island.

Italy

The

EPC contract for the 6.0 mtpa Brindisi regasification terminal was awarded at

the end of 2004. During 2005, BG Group acquired Enel’s share of equity rights

and capacity, taking its share to 4.8 mtpa priority capacity at the terminal.

The remaining 20% is set aside for third-party access, in compliance with Italian

regulatory requirements. In September 2005, in accordance with the provisions

of the second EU Gas Directive, agreement was reached between the Italian authorities

and the European Commission confirming these arrangements. Brindisi is now expected

to receive its first LNG deliveries during the fourth quarter 2009.

UK

Good

progress was made on the Dragon LNG regasification terminal at Milford Haven,

in Wales, during 2005. Completion is targeted for the fourth quarter 2007. During

2005, Ofgem and the European Commission granted the project exemption from the

regulated third-party access provisions imposed by the second EU Gas Directive.

Other areas

In February

2006, BG Group signed a Letter of Agreement with a group of Chilean gas buyers

for the supply of LNG and the development of a 2.5 mtpa LNG import terminal in

Quintero

Bay, Chile.

LNG SHIPPING

BG

Group’s shipping position remains a key enabler for the LNG business to

ensure delivery and flexibility under long-term contracts and to acquire short-term

cargoes and benefit from arbitrage opportunities.

BG Group expects to take delivery of three 145 000 cubic metre new-build ships in 2006 and four new-build ships in 2007, and has options for further ships beyond 2007.

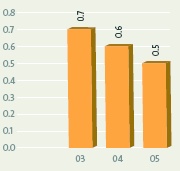

Production (mtpa)

LNG production has grown 21% per annum on a compound basis since 2003

| Actual | |

| Target | |

| LNG: Long-term firm supply | |||

| Firm supply | Commercial | ||

| (mtpa) | start-up | ||

| Atlantic LNG T2/3 | 2.1 | 2003 | |

| Nigeria LNG | 2.3 | Q1 2006 | |

| Egyptian LNG T2(a) | 3.5 | Q2 2006 | |

| Atlantic LNG T4(b) | 1.5 | Q3 2006 | |

| Equatorial Guinea | 3.3 | Q3 2007 | |

| Total Firm Supply(c) | 12.7 | Q3 2007 | |

| (a) | First cargo lifted in September 2005 |

| (b) | First cargo lifted in February 2006 |

| (c) | Excludes up to 1 mtpa of expected excess/de-bottlenecking volumes |

| 18 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Operating review continued

| Transmission and Distribution |

| The downstream business |

| continues to grow strongly, |

| with double-digit volume |

| growth from Comgas in 2005. |

Highlights

| • | Comgas continued to grow, with volumes up 14% |

| • | Strong volume growth at Mahanagar Gas |

| • | Additional compressed natural gas stations developed by Gujarat Gas |

| • | MetroGAS deconsolidated |

|

|

2005 PERFORMANCE

BG

Group’s transmission and distribution businesses had another strong year

during 2005, with increased customers and profitability.

Argentina

MetroGAS

(BG Group 26%) results were deconsolidated from the end of 2005 as a result of

financial restructuring. (See Financial review, page 23.)

Brazil

Comgas

(BG Group 60.1%) is Brazil’s largest gas distribution company. At the end

of 2005, it was serving around 485 000 customers in the São Paulo concession

area (2004

450 000; 2003 416 000).

Growth in the Brazilian economy coupled with higher demand from industrial, power and compressed natural gas (CNG) vehicle users resulted in an increase in Comgas sales volumes of 14% during 2005. Comgas operating profit increased by 53% to £147 million in 2005 (2004 £96 million), reflecting volume increases and margin improvements. The Comgas network was extended by 594 km during the year. This expansion is part of an ongoing five year expansion plan, which commenced in 2004. The expansion plan also involves the capture of higher margin residential customers, together with the simultaneous development of the industrial, natural gas vehicle (NGV) and co-generation markets.

India

Gujarat

Gas Company Limited (GGCL) (BG Group 65.1%) is India’s largest private gas

distribution company. In 2005, its sales volume increased by 17% to 811 mmcm

(2004 691 mmcm; 2003 771 mmcm). A better sales mix, including more industrial

customers, and cost savings improved margins to achieve a 42% increase in operating

profits in 2005 compared to 2004.

During 2005, GGCL signed over 500 mcmd of new gas supply contracts (2004 377 mcmd). Under its CNG for vehicles expansion programme, GGCL added five new stations in Surat, Gujarat, taking GGCL’s total number of stations to 12.

GGCL has completed its network expansion into the towns of Kim and Karanj, while expansion into the industrial area of Vapi is underway and is scheduled for completion in 2006. Ten new CNG stations are planned for Surat by mid-2006.

Mahanagar Gas Limited (MGL) (BG Group 49.75%), which owns a gas distribution business in Mumbai, saw its 2005 volumes rise 14% to 446 mmcm (2004 392 mmcm; 2003 297 mmcm).

|

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

19 |

Some of the increased volume at MGL in 2005 was stimulated by the growth of CNG through the installation of 21 new refuelling stations, taking the total number of stations to 117 at the end of 2005.

MGL has also expanded its network into the town of Thane and other areas in and around the city of Mumbai.

UK

The

Interconnector pipeline (BG Group 25%) has 20 bcma capacity to transport gas

from Bacton into the Continental European grid. The pipeline can also flow in

reverse. In December 2005, its reverse flow capacity was increased from 8.5 bcma

to 16.5 bcma. Reverse flow capacity is scheduled to be further expanded to 23.5

bcma by December 2006. With a growing UK requirement for imports and the UK becoming

a net gas importer in 2004, imports via the Interconnector continued to increase

in 2005.

In the first quarter 2005, BG Group and its partners completed the sale of Premier Transmission Limited (PTL) to Premier Transmission Financing Company.

| Throughput (bcma) |

|

| Volume throughput has increased by 3% per annum on a compound basis since 2003 |

|

| |

|

|

Actual |

| |

|

|

Target |

| |

|

| (a) | Reduction due to sale of PTL |

| (b) | Previous target of 14 bcma has been amended to allow for disposal of PTL and reduced holding in MetroGAS |

| Comgas (bcma) | |

| Comgas achieved double-digit volume growth year-on-year from 2003 to 2005 | |

|

|

| |

|

| Industrial | |

| |

|

|

Residential |

| |

|

| Commercial | |

| |

|

| NGV | |

| |

|

| Co-generation | |

| |

|

|

Power |

|

| |

|

| Source: Comgas | |

| 20 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Operating review continued

| Power & Other activities |

| BG Group has a profitable portfolio |

| of modern, fully contracted, |

| combined cycle gas power stations, |

| and leverages its distribution |

| customer base to develop |

| complementary businesses. |

| Highlights | ||||||

| • | Co-generation contracts entered commercial operation in India | • | Microgen signed a co-operation agreement with Gasunie to develop an appliance for the Dutch market | |||

| • | Opened more than 30 new Natural Gas Vehicle (NGV) stations in the states of São Paulo and Rio de Janeiro, taking the total to over 60 in Brazil | |||||

|

||||||

2005 PERFORMANCE

Performance

in the Power segment was largely unchanged from 2004. Other businesses were broadly

in line with last year.

Power

Premier

Power Limited (BG Group 100%) owns and operates the 1 316 MW Ballylumford

power station in Northern Ireland, which has supply agreements with Northern

Ireland Electricity. BG Group also has a 50% interest in the 1 130 MW Seabank

power station, near Bristol. In June 2005, the failure of a steam turbine

reduced availability at Seabank. Remedial works were completed during the

first quarter 2006.

In the Philippines, BG Group has a 40% stake in the Santa Rita (1 000 MW) and San Lorenzo (505 MW) power stations, which sell electricity under long-term agreements to Meralco, the Philippines’ largest power distribution company.

BG Group has a 20% interest in the Genting Sanyen 760 MW CCGT plant, located 70 km south of Kuala Lumpur, with long-term sales to Malaysia’s national power company.

In Italy, BG Group has a 33.68% share in Serene, which operates 400 MW of co-generation adjacent to Fiat Auto plants.

Other activities

In

Brazil, the Group, through its Iqara subsidiaries, operates co-generation and

related energy supply services and compressed natural gas stations supplying

natural gas vehicles in

São Paulo and Rio de Janeiro. BG Group disposed of its Brazil telecoms

businesses in December 2005.

In 2004, BG India Energy Services Pvt Ltd (BGIESPL) was established to deliver

co-generation to Indian customers, now at around 13 MW.

Microgen (BG Group 100%) is developing an innovative energy system for use in individual homes and small businesses. Generating electricity at the same time as water and space heating, it reduces consumption of externally generated power. The appliance is currently undergoing performance and reliability field trials.

In 2005, Microgen signed a co-operation agreement with Gasunie to develop an appliance for the Dutch market.

| 21 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Financial review

|

“Strong

growth in volumes and revenues was carried through to the bottom line resulting in a 64% increase in earnings.”* |

|||

| Ashley

Almanza Chief Financial Officer |

||||

| Financial results – Business Performance* | ||||||||||||||

| Revenue and other operating income | Total operating profit(a) | |||||||||||||

| 2005 | 2004 | 2003 | 2005 | 2004 | 2003 | |||||||||

| £m | £m | £m | £m | £m | £m | |||||||||

| Exploration and Production (b) | 3 074 | 2 148 | 1 787 | 1 942 | 1 189 | 954 | ||||||||

| Liquefied Natural Gas(b) | 1 631 | 1 098 | 945 | 172 | 92 | 77 | ||||||||

| Transmission and Distribution | 808 | 644 | 678 | 211 | 148 | 154 | ||||||||

| Power Generation | 227 | 187 | 168 | 113 | 116 | 124 | ||||||||

| Other activities | 15 | 8 | 3 | (58 | ) | (32 | ) | (30 | ) | |||||

| Less: intra-group sales | (91 | ) | (22 | ) | (17 | ) | ||||||||

| Total | 5 664 | 4 063 | 3 564 | 2 380 | 1 513 | 1 279 | ||||||||

| (a) | Total operating profit includes the Group’s share of pre-tax operating profits in joint ventures and associates. | ||

| (b) | Includes other operating income of £7 million (2004 £nil; 2003 £nil) in the E&P segment and £45 million (2004 £10 million; 2003 £6 million) in the LNG segment. | ||

The operations of BG Group comprise Exploration and Production (E&P), Liquefied Natural Gas (LNG), Transmission and Distribution (T&D), Power Generation (Power) and Other activities.

SUMMARY*

Strong growth in

volumes and revenues (see table above) was carried through to the bottom line,

resulting in a 64% increase in earnings. The successful completion and start-up

of a number of large integrated gas projects and the arrival of long-term LNG

supplies have enhanced the Group’s earnings and cash flow capacity and this

has been reflected in the proposed full year dividend of 6 pence per share, an

increase of 57%.

In November, the Group initiated a £1 billion share repurchase programme

following the receipt of exceptional pre-tax proceeds (US$1.8 billion) on

the sale of the Group’s interest in the North Caspian Sea PSA. The Group

also announced

an additional £900 million of investment in new projects. The Group remains

strongly financed, retaining the flexibility to execute its growth programme

and to pursue additional investment opportunities.

OPERATING RESULTS*

A strong

operating performance and favourable oil and gas prices resulted in a 57% increase

in total operating profit in 2005. Further detail of each segment’s operating

result (based on Business Performance) is given in the separate sections

below.

BG Group’s post-tax ROACE (see page 135) was 23.4% (2004 17.5%; 2003 16.8%) .

E&P

E&P’s

revenue and other operating income increased by 43% to £3 074 million from £2

148 million in 2004 and £1 787 million in 2003. The 2005 increase was primarily

driven by higher prices; higher production from West Delta Deep Marine in Egypt;

increased liquids exports from the Karachaganak field through the CPC pipeline;

and a full year’s contribution from assets acquired in 2004 in Canada, Trinidad

and Tobago and Egypt. Higher prices and US Dollar exchange rate movements contributed £674

million to the increase in revenue in 2005. The 2004 increase in revenue and

other operating income was driven principally by higher production volumes, whilst

higher realised prices,

| *Business Performance excludes disposals and certain re-measurements and is presented as exclusion of these items provides readers with a clear and consistent presentation of the underlying operating performance of the Group’s ongoing business. Unless otherwise stated, financial operating information for the Group and its business segments presented in the Operating and financial review is based on BG Group’s Business Performance. See presentation of non-GAAP measures, page 152. See, also, Segmental analysis and results presentation, note 2, page 71, and Earnings per ordinary share, note 10, page 85, for a reconciliation of the differences between Business Performance and BG Group’s Total Results. | ||

| Total operating profit* (£m) | ||

|

||

<

| 22 |

BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating and financial review

Financial review continued

| Exploration and Production | |||||||

| 2005 | 2004 | 2003 | |||||

| Production volumes (mmboe)(a) | |||||||

| – oil | 19.3 | 21.4 | 23.7 | ||||

| – liquids | 29.7 | 25.6 | 19.2 | ||||

| – gas | 134.8 | 119.8 | 113.1 | ||||

| 183.8 | 166.8 | 156.0 | |||||

| Average realised prices | |||||||

| – oil per barrel (UK£/US$) | 30.60/55.96 | 21.53/39.24 | 17.89/29.18 | ||||

| – liquids per barrel (UK£/US$) | 22.84/41.77 | 14.21/25.90 | 8.86/14.45 | ||||

| – UK gas per produced therm (pence) | 27.30 | 19.64 | 16.92 | ||||

| – international gas per produced therm (pence) | 17.27 | 13.95 | 13.67 | ||||

| – overall gas per produced therm (pence) | 20.15 | 16.18 | 15.16 | ||||

| Development expenditure (£m) | 683 | 620 | 486 | ||||

| Gross exploration expenditure (£m) | |||||||

| – capitalised exploration expenditure | 225 | 262 | 156 | ||||

| – other exploration expenditure | 111 | 74 | 36 | ||||

| 336 | 336 | 192 | |||||

| (a) | Production volumes exclude fuel gas. | ||

partially offset by adverse US Dollar exchange rate movements contributed a net £161 million to the 2004 increase in revenue.

Approximately 30% of the Group’s gas production in 2005 was in the UK, of which 70% was sold under various contracts. The remaining UK gas volumes are sold on a short-term basis. BG Group’s realised UK gas price per produced therm was 27.3 pence in 2005 compared to 19.6 pence in 2004 and 16.9 pence in 2003.

In 2005, the Group’s average realised international gas prices increased by 24% compared to the previous year. The increase in price reflects indexation to oil prices and is also a result of increased volumes from Canada, Tunisia, Egypt and India. In 2004, average realised international gas prices increased by 2% over the previous year.

Unit lifting costs were £1.19 per boe in 2005 compared with £1.03 per boe in 2004 and £0.91 per boe in 2003. Unit operating expenditure was £2.21 per boe in 2005 against £2.01 per boe in 2004 and £1.85 per boe in 2003. The increases in lifting and unit operating costs in 2005 were predominantly due to the impact of higher upstream prices on input costs, tariffs and royalties. The increase in costs in 2004 compared with 2003 was primarily due to the impact of higher oil prices on royalties and tariffs and start-up costs of the Karachaganak export facilities, all partially offset by the favourable effects of a weaker US Dollar.

Total E&P operating profit in 2005 increased by 63% to £1 942 million (2004 £1 189 million; 2003 £954 million). The increase reflected the 10% increase in

production volumes and higher prices, partially offset by a higher exploration charge. At constant UK£/US$ exchange rates and upstream prices, total operating profit for the segment in 2005 increased by 9%. The 25% increase in operating profit in 2004 reflected production growth from the Karachaganak field, new production from the Scarab Saffron and Canadian fields and higher prices, offset by the unfavourable effect of a weaker US Dollar exchange rate. At constant UK£/US$ exchange rates and upstream prices, total operating profit in 2004 increased by 5%.

Gross exploration expenditure in 2005 was £336 million (2004 £336 million; 2003 £192 million) including £225 million (2004 £262 million; 2003 £156 million) of expenditure that was capitalised. Well write-off costs were £70 million (2004 £52 million; 2003 £46 million).

LNG

Revenue

and other operating income increased to £1 631 million in 2005 (2004 £1

098 million; 2003 £945 million), reflecting BG Group’s increased activity

in the global LNG market. LNG shipping and marketing activity accounted for the

entire revenue and other operating income in all three years.

Total operating profit was £172 million in 2005 compared to £92 million in 2004 and £77 million in 2003. The increase in 2005 reflected higher profits from liquefaction (see below) and increased realisations achieved in the shipping and marketing business, including the benefit of re-directing 31 cargoes (2004 18 cargoes)

to higher value markets. Operating profit for the shipping and marketing business was £111 million in 2005 (2004 £51 million; 2003 £44 million).

Business development and other costs also increased in 2005 to £50 million (2004 £24 million; 2003 £23 million), reflecting higher levels of activity on new projects across the segment including the development of the OKLNG project in Nigeria. The increase in 2004 total operating profit reflected improved marketing margins and a strong performance at Atlantic LNG, partially offset by a weaker US Dollar. Contracts for the purchase of LNG and sale of natural gas via the Group’s shipping and marketing business are both linked primarily to the US Henry Hub reference price.

BG Group’s share of operating profits from its interests in liquefaction businesses in Trinidad and Tobago and Egypt was up £46 million to £111 million (2004 £65 million; 2003 £56 million). The increase in 2005 reflected the start-up of two liquefaction trains in Egypt and higher net-back margins to Atlantic LNG Train 1 in Trinidad and Tobago. The increase in 2004 compared to 2003 reflected the full year contribution from Atlantic LNG Train 3 together with higher prices at Atlantic LNG Train 1, partially offset by adverse exchange rate movements.

Atlantic LNG Train 4 commenced production in December 2005.

| BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

23 |

T&D

T&D’s

revenue in 2005 was £808 million (2004 £644 million; 2003 £678

million). Total operating profit in 2005, including the Group’s share

of operating profit in joint ventures and associates, was £211 million

(2004 £148 million; 2003 £154 million). The increase in revenue

in 2005 was principally due to higher volumes at Comgas and the strengthening

of the Brazilian Real and Argentine Peso exchange rates.

In 2005, Comgas’ revenue increased by 34% to £532 million, with a 14% increase in volumes and improved tariffs following the five year regulatory review. In 2004, there was a 2% increase in Comgas’ revenue to £397 million, with an 11% increase in volumes and higher prices being partially offset by a weaker Brazilian Real.

Comgas’ operating profit in 2005 rose 53% to £147 million (2004 £96 million; 2003 £95 million) due to volume growth, stronger exchange rates and lower gas costs. The operating profit in 2005 reflected a net benefit from lower gas costs of £13 million that will be passed back to customers through lower tariffs in the future. The increase in 2004 reflected an 11% increase in volumes and lower costs, largely offset by a weaker exchange rate.

MetroGAS’ revenue in 2005 was £164 million (2004 £150 million; 2003 £135 million). The £14 million increase in 2005 reflected higher prices and a stronger Argentine Peso. The £15 million increase in 2004 reflected 20% volume growth offset by a weaker Argentine Peso.

The £6 million increase in operating profit from MetroGAS in 2005 to £26 million (2004 £20 million; 2003 £18 million) reflected the price and volume growth referred to above.

In December 2005, BG Group announced that Gas Argentino S.A. (GASA), the parent company of MetroGAS, had reached agreement with its creditors for a comprehensive restructuring that converts financial indebtedness owed to those creditors into a 30% interest in GASA and a 19% interest in MetroGAS. The agreement, which is subject to regulatory approvals, reduces BG Group’s combined interest in MetroGAS to 26%. As a result, BG Group no longer controls GASA and MetroGAS and these companies have been deconsolidated from the date of the agreement. From the date of the agreement these companies are accounted for under the equity method and, as at 31 December 2005, are recognised at nil value in the Group’s Financial Statements.

BG Group’s share of operating profits in joint ventures and associates was

£42 million (2004 £40 million; 2003 £43 million). The 2005 result reflected increased volumes at Mahanagar Gas offset by the impact of the sale of Premier Transmission in March 2005.

Power

Power’s

revenue was £227 million in 2005 (2004 £187 million; 2003 £168

million). Revenue in all three years was attributable to Premier Power in

the UK and has risen in line with the terms of its power sales agreement with

Northern Ireland Electricity, which entitles changes in gas cost to form the

basis of the charge to be passed through to the customer.

Total operating profit of £113 million (2004 £116 million; 2003 £124 million) included the Group’s share of operating profits in joint ventures and associates of £89 million (2004 £88 million; 2003 £96 million) – attributable to the power plants at Seabank (UK), Santa Rita and San Lorenzo (the Philippines), Serene (Italy) and Genting Sanyen Power (Malaysia).

Total operating profit in 2005 included insurance income relating to operating income lost following the failure of one steam turbine at Seabank Power in June 2005. The 6% decrease in total operating profit in 2004 reflected weaker US Dollar exchange rates, which adversely affected the translation of results from the Philippine associate businesses.

Other

activities

Revenue

for Other activities in 2005 was £15 million (2004 £8 million; 2003

£3 million).

The total operating loss in 2005 was £58 million compared with £32 million in 2004 and £30 million in 2003. The loss in all three years related mainly to corporate costs and business development expense. The increase in operating loss in 2005 was primarily attributable to additional industry insurance premiums.

DISPOSALS

AND RE-MEASUREMENTS*

The following

items, described as ‘disposals and re-measurements’ are excluded

from Business Performance as exclusion of these items provides a clearer presentation

of the underlying performance of the Group. Disposals and re-measurements

amounted, in aggregate, to a profit of £206 million before tax and interest

(2004 £87 million; 2003 £116 million). For a full reconciliation

between BG Group’s Total Results and Business Performance, see note 2,

page 71. For further details of amounts comprising disposals and re-measurements,

see note 6, page 81.

Re-measurements included within other operating income amounted to a non-cash charge of £240 million, of which £239 million was recognised in the E&P

| E&P lifting costs | |

|

|

|

£ per boe |

|

$ per boe |

| E&P operating expenditure | |

|

|

|

£ per boe |

|

$ per boe |

| E&P

production volumes(a) (mmboe) Annual production has increased by 18% since 2003 |

|

|

|

| (a) | Production volumes exclude fuel gas |

* See presentation of non-GAAP measures, page 152.

| 24 | BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating

and financial review

Financial review

continued

Profit for the year

| Business | 2005 | Total | Business | 2004 | Total | Business | 2003 | Total | ||||||||||

| Disposals and | Disposals and | Disposals and | ||||||||||||||||

| Performance | remeasurements | Performance | remeasurements | Performance | remeasurements | |||||||||||||

| £m | £m | £m | £m | £m | £m | £m | £m | £m | ||||||||||

| Total operating profit(a) | 2 380 | 206 | 2 586 | 1 513 | 87 | 1 600 | 1 279 | 116 | 1 395 | |||||||||

| Net finance costs(b) | (51 | ) | 15 | (36 | ) | (67 | ) | – | (67 | ) | (71 | ) | – | (71 | ) | |||

| Tax(b) | (941 | ) | (41 | ) | (982 | ) | (589 | ) | (30 | ) | (619 | ) | (490 | ) | (32 | ) | (522 | ) |

| Profit for the year | 1 388 | 180 | 1 568 | 857 | 57 | 914 | 718 | 84 | 802 | |||||||||

| Minority interest | (31 | ) | (9 | ) | (40 | ) | (28 | ) | – | (28 | ) | (28 | ) | – | (28 | ) | ||

| Earnings | 1 357 | 171 | 1 528 | 829 | 57 | 886 | 690 | 84 | 774 | |||||||||

| Earnings per share (pence) | 38.3 | 4.9 | 43.2 | 23.5 | 1.6 | 25.1 | 19.6 | 2.3 | 21.9 | |||||||||

| (a) | Total operating profit includes the Group’s share of pre-tax operating profits in joint ventures and associates. |

| (b) | Includes the Group’s share in joint ventures and associates. |

segment and £1 million was recognised in the LNG segment. The charge primarily consisted of £224 million of mark-to-market movements on certain long-term UK gas contracts that fall within the scope of International Accounting Standard (IAS) 39, ‘Financial Instruments: Recognition and Measurement’. The charge in 2005 arises as a result of higher UK gas prices at the end of the year.

Re-measurements presented within finance costs include the gain on retranslation of MetroGAS’ US Dollar and Euro borrowings, which cannot be designated as hedges under IAS 39 (£14 million). In addition, there is a re-measurement charge of £13 million in respect of certain derivatives used to hedge foreign exchange and interest rate risk and foreign exchange gains on certain other borrowings in subsidiaries of £16 million that represent effective economic hedging activities but do not qualify for hedge accounting under IAS 39.

In 2005, the profit on disposal of non-current assets of £446 million (2004 £87 million profit; 2003 £116 million profit) included a pre-tax profit of £416 million on the disposal of BG Group’s 16.67% interest in the North Caspian Sea PSA (recognised in the E&P segment) and a pre- and post-tax profit on disposal of the Group’s 50% interest in Premier Transmission Limited of £13 million (recognised in the T&D segment).

During 2005, management committed to a plan to dispose of BG Group’s telecoms businesses in Brazil and India. The telecoms businesses in Brazil had been sold by 31 December 2005. The overall disposal programme resulted in a pre- and post-tax charge to the

* See presentation of non-GAAP measures, page 152.

2005 income statement of £32 million (recognised in the Other activities segment), comprising losses on disposals of £18 million and an impairment charge of £14 million.

GASA and its subsidiary MetroGAS have been deconsolidated (see note 6, page 81) resulting in a pre- and post-tax gain of £56 million. As the Group no longer controls MetroGAS, the value in use of Gasoducto Cruz del Sur has fallen below its carrying value, resulting in a pre-tax impairment charge of £8 million. Both amounts were recognised in the T&D segment.

In addition, £1 million of pre- and post-tax profit was recognised in the E&P segment following the disposal of the Group’s interest in a North Sea asset.

In 2004, the pre-tax profit on disposal of non-current assets included £66 million on the sale of BG Group’s interests in the Muturi Production Sharing Contract (Muturi PSC) and Tangguh LNG in Indonesia (£47 million recognised in the E&P segment and £19 million recognised in the LNG segment).

In 2003, profits on disposals included £76 million pre-tax and £44 million post-tax profits on the sale and swap of UK North Sea assets (recognised in the E&P segment); a £32 million pre- and post-tax profit on the sale of BG Group's interest in Phoenix Natural Gas Limited (recognised in the T&D segment); a £6 million pre- and post-tax profit on the partial sale of Brindisi LNG SpA (recognised in the LNG segment); and a £2 million pre- and post-tax profit on the release of costs relating to a prior year disposal (recognised in the Other activities segment).

FINANCE

COSTS*

In 2005,

BG Group’s net finance costs, including BG Group’s share of finance

costs for joint ventures and associates was £51 million (2004 £67 million; 2003 £71 million). The lower finance costs in 2005 reflected the reduction in net borrowings following the disposal of the Group’s interest in the North Caspian Sea PSA. Total net finance costs including re-measurements amounted to £36 million. There were no re-measurement finance items in 2004 and 2003.

TAXATION*

BG Group’s

tax charge in 2005 before disposals and re-measurements and including BG Group’s

share of taxation from joint ventures and associates was £941 million

(2004 £589 million; 2003 £490 million). Excluding disposals and

re-measurements, BG Group’s effective tax rate for 2005 was 40.4% (2004

40.7%; 2003 40.6%) .

Including disposals and re-measurements, and BG Group’s share of taxation from joint ventures and associates, the Group’s tax charge for 2005 was £982 million (2004 £619 million; 2003 £522 million), representing an effective tax rate of 38.5% (2004 40.4%; 2003 39.4%) . In 2005, the tax charge on disposals and remeasurements comprised a charge of £137 million that arose on the sale of BG Group’s interest in the North Caspian Sea PSA offset by a credit of £96 million that arose on the mark-to-market of certain commodity contracts.

In 2004, the tax charge on disposals and re-measurements of £30 million arose on the sale of BG Group’s interest in the Muturi PSC (£28 million) and shares in a listed company, GAIL (India) Limited (previously Gas Authority of India Limited) (£2 million).

The proposed increase in North Sea taxation to 50% is expected to add

| BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

25 |

Capital investment

| 2005 | 2004 | 2003 | ||||

| £m | £m | £m | ||||

| Intangible assets(a) | 235 | 294 | 201 | |||

| Property, plant and equipment | 1 160 | 1 061 | 607 | |||

| 1 395 | 1 355 | 808 | ||||

| Non-current asset investments and acquisitions | 121 | 539 | 246 | |||

| Total | 1 516 | 1 894 | 1 054 | |||

| (a) | Includes £60 million (2004 £150 million; 2003 £104 million) in respect of the Group’s interest in the North Caspian Sea PSA, which was classified as held for sale until its disposal in 2005. |

approximately 4% to the Group’s effective rate in 2006. The impact of the North Sea tax on the Group’s tax rate will vary according to the prices realised on North Sea production but is expected to diminish over time as more of the Group’s profits come from outside the UK. In addition there will be a one-off adjustment in 2006 to reflect the increased North Sea tax on opening deferred tax balances (not included in the 4% above), reflecting a credit of £61 million to restate the deferred tax asset associated with mark-to-market balances and a charge of £38 million for other deferred tax balances

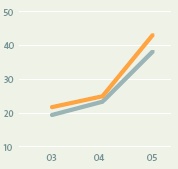

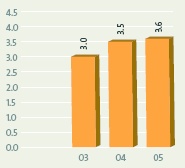

EARNINGS

AND EARNINGS PER SHARE*

Excluding

disposals and re-measurements, earnings (and earnings per share) were £1

357 million (38.3 pence) in 2005, £829 million (23.5 pence) in 2004 and

£690 million (19.6 pence) in 2003.

The growth in earnings and earnings per share is illustrated opposite.

Earnings (and earnings per share) including disposals and re-measurements were £1 528 million (43.2 pence) in 2005, £886 million (25.1 pence) in 2004 and £774 million (21.9 pence) in 2003.

A three year summary from 2003 to 2005 of the financial results of BG Group’s operations is set out on page 21.

CAPITAL

INVESTMENT

Capital

investment in 2005 was £1 516 million (2004 £1 894 million; 2003

£1 054 million) including £29 million for the acquisition of the

remaining 50% interest in Brindisi LNG SpA in Italy.

Capital investment in E&P (including capitalised exploration expenditure) was £935 million (2004 £1 380 million; 2003 £654 million). In 2005, this included expenditure in the UK, Egypt, Kazakhstan and Mauritania. E&P investment in 2004 included £355 million on the acquisition of subsidiary undertakings in Canada, Mauritania and Trinidad and Tobago and £120 million to acquire a further 40% interest in the Rosetta gas field in Egypt.

In 2003, capital investment included £104 million relating to the Group’s interest in the North Caspian Sea PSA.

Development expenditure (on proved properties) totalled £683 million compared with £620 million in 2004 and £486 million in 2003. Development expenditure in 2005 was primarily in respect of the West Delta Deep Marine field in Egypt, Buzzard and Atlantic/Cromarty fields in the UK, Panna/Mukta field in India and Chinguetti field in Mauritania. Development expenditure in 2004 was primarily in respect of the West Delta Deep Marine, Karachaganak, Buzzard, Atlantic/Cromarty and Miskar fields.

Capital investment in LNG in 2005 was £422 million compared with £417 million in 2004 and £301 million in 2003. Investment in 2005 included expenditure on LNG vessels under construction and due for delivery in 2006 and 2007 (financed through leases), £29 million on the acquisition of the remaining 50% of Brindisi LNG SpA and expenditure on the Atlantic LNG Train 4 liquefaction plant and the Dragon LNG terminal at Milford Haven. Investment in 2004 primarily related to the delivery of two LNG vessels and development of the Egyptian LNG Trains 1 and 2 and Atlantic LNG Train 4 liquefaction plants.

Capital investment in T&D in 2005 amounted to £136 million (2004 £66 million; 2003 £76 million). Expenditure in all three years was incurred mainly on the expansion of the Comgas network.

Capital investment in Power during 2005 was £3 million (2004 £3 million; 2003 £3 million).

CASH

FLOW

Cash flow

from operating activities in 2005 was £1 606 million – an increase

of £411 million compared with 2004 (2004 £1 195 million; 2003 £1

112 million), principally reflecting increased operating profit partially

offset by increased working capital associated with higher volumes and commodity

prices.

| Earnings per share (pence) | |

|

|

|

Including disposals and re-measurements |

|

Excluding disposals and re-measurements |

| • | earnings excluding disposals and re-measurements increased by 64% in 2005; |

| • | earnings per share excluding disposals and re-measurements increased by 63% in 2005; and |

| • | underlying earnings growth excluding the impact of upstream prices and US Dollar exchange movements increased by 17% in 2005. |

* See presentation of non-GAAP measures, page 152.

| 26 | BG GROUP ANNUAL REPORT AND ACCOUNTS 2005 |

Operating

and financial review

Financial review continued

| Cash flow before financing | ||||||

| 2005 | 2004 | 2003 | ||||

| £m | £m | £m | ||||

| Cash generated by operations | 2 489 | 1 582 | 1 444 | |||

| Income taxes paid | (883 | ) | (387 | ) | (332 | ) |

| Cash flows from investing activities | (62 | ) | (1 135 | ) | (811 | ) |

| Cash flow before financing | 1 544 | 60 | 301 | |||

| 2005 capital investment by geographical area (£m)(a) | ||||||

|

||||||

|

Europe | 447 | ||||

|

South America | 160 | ||||

|