UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4861

Fidelity Garrison Street Trust

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Scott C. Goebel, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

|

Date of fiscal year end: |

July 31 |

|

|

|

|

Date of reporting period: |

July 31, 2011 |

Item 1. Reports to Stockholders

Fidelity® Commodity Strategy

Central Fund

Annual Report

July 31, 2011

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov. You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

CRC-ANN-0911 1.901057.101

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the fund's distributions from dividend income and capital gains (the profits earned upon the sale of securities that have grown in value, if any) and assuming a constant rate of performance each year. The $10,000 table and the fund's returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. During periods of reimbursement by Fidelity, a fund's total return will be greater than it would be had the reimbursement not occurred. How a fund did yesterday is no guarantee of how it will do tomorrow.

Average Annual Total Returns

|

Periods ended July 31, 2011 |

Past 1 |

Life of |

|

Fidelity® Commodity Strategy Central Fund |

21.28% |

14.59% |

A From October 7, 2009.

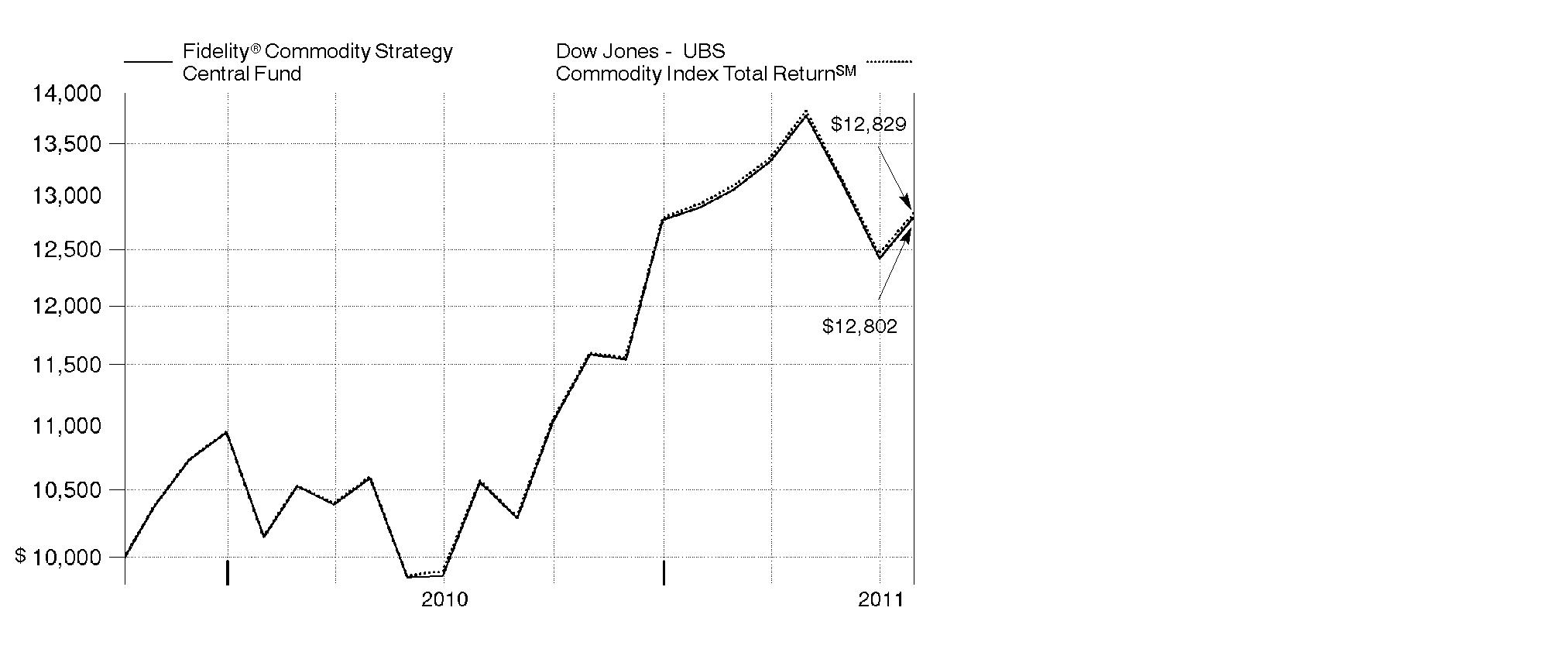

$10,000 Over Life of Fund

Let's say hypothetically that $10,000 was invested in Fidelity Commodity Strategy Central Fund on October 7, 2009, when the fund started. The chart shows how the value of your investment would have changed, and also shows how the Dow Jones - UBS Commodity Index Total ReturnSM performed over the same period.

Annual Report

Management's Discussion of Fund Performance

Market Recap: With few exceptions, commodities enjoyed very strong gains during the 12 months ending July 31, 2011, with precious metals being particularly good performers. Gold was up 37%, while silver rose 121%. Investors have traditionally flocked to precious metals in times of economic uncertainty as protection against the potential for higher inflation. Many agricultural commodities also performed very well, led by sugar, cotton and corn. All three rose sharply amid strong demand and fears of dwindling supply. The story was much different for wheat, however, as traders worried about the effects of political turmoil in North Africa and the Middle East on demand for the crop. The region accounts for approximately one-third of global wheat demand. Natural gas was the weakest-performing commodity, dropping 37% in response to projections for ample supply relative to demand. Against this backdrop, the Dow Jones - UBS Commodity Index Total ReturnSM rose 21.41%, compared with 19.65% for the broad U.S. stock market, as measured by the S&P 500® Index. Meanwhile, international equities, as tracked by the MSCI® EAFE® Index, gained 17.30%, while the Barclays Capital® U.S. Aggregate Bond Index - a proxy for the U.S. bond market - advanced 4.44%.

Comments from Bobe Simon, who oversees Fidelity® Commodity Strategy Central Fund as Portfolio Manager for Geode Capital Management, LLC: During the year, the Fund gained 21.28%, slightly trailing the Dow Jones - UBS index. The energy sector, comprising more than 30% of the index, stood out as a source of underperformance. Natural gas prices fell sharply, while crude oil gained just 6%, well below the benchmark return. The livestock sector, which makes up approximately 6% of the index and includes lean hogs and live cattle, also turned in a relatively weak result. However, the agriculture sector - representing the second-largest weighting in the index behind energy - enjoyed a good result, led by a roughly 3% stake in sugar, a 1% allocation to cotton and a 7% position in corn, the sector's three top-performing commodities. In contrast, wheat hampered performance, given that commodity's sharp decline. The industrial metals sector - consisting of aluminum, copper, zinc and nickel - outperformed the index, with the group gaining about 23%. Gold, and especially silver, did even better, leading the precious metals sector to a roughly 56% return, which nearly tripled the index's performance.

The views expressed above reflect those of the portfolio manager(s) only through the end of the period as stated on the cover of this report and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Annual Report

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (February 1, 2011 to July 31, 2011).

Actual Expenses

The first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

|

|

Annualized |

Beginning |

Ending |

Expenses Paid |

|

Actual |

.0451% |

$ 1,000.00 |

$ 993.70 |

$ .22 |

|

Hypothetical (5% return per year before expenses) |

|

$ 1,000.00 |

$ 1,024.57 |

$ .23 |

* Expenses are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Annual Report

Investment Changes (Unaudited)

The information in the following tables is based on the Fund's commodity-linked investments and excludes short-term investment-grade debt securities, cash and cash equivalents.

|

Commodity Instruments as of July 31, 2011* |

|||

|

|

% of fund's total |

% of fund's total |

|

|

Commodity Swaps |

84.3 |

97.6 |

|

Commodity Futures |

8.2 |

2.4 |

|

Commodity-Linked Notes |

7.5 |

0.0 |

|

Commodity Sector Diversification as of July 31, 2011 |

|||

|

|

% of fund's total |

% of fund's total |

|

|

Energy |

33.0 |

32.7 |

|

Grains |

21.1 |

22.8 |

|

Industrial Metals |

17.4 |

17.6 |

|

Precious Metals |

16.0 |

12.9 |

|

Softs |

6.8 |

8.3 |

|

Livestock |

5.7 |

5.7 |

* Investments in Commodity Swaps and Commodity-Linked Notes provide exposure to the commodities market via the Dow Jones-UBS Commodity Index Total Return, an unmanaged index composed of futures contracts on 19 physical commodities. The Fund does not invest directly in physical commodities.

Annual Report

Consolidated Investments July 31, 2011

Showing Percentage of Net Assets

|

Commodity-Linked Notes - 2.5% |

||||

|

|

Principal Amount |

Value |

||

|

Deutsche Bank AG: |

|

|

|

|

|

0.0253% 3/8/12 (b)(e)(f) |

|

$ 20,000,000 |

$ 20,130,349 |

|

|

0.0265% 3/15/12 (b)(e)(f) |

|

14,000,000 |

13,788,403 |

|

|

TOTAL COMMODITY-LINKED NOTES (Cost $34,000,000) |

33,918,752 |

|||

|

U.S. Treasury Obligations - 9.9% |

||||

|

|

||||

|

U.S. Treasury Bills, yield at date of purchase 0.05% to 0.12% 8/18/11 to

12/8/11 (c)(d) |

|

134,000,000 |

133,962,391 |

|

|

Money Market Funds - 87.6% |

|||

|

Shares |

|

||

|

Fidelity Cash Central Fund, 0.14% (a) |

1,184,933,895 |

1,184,933,895 |

|

|

TOTAL INVESTMENT PORTFOLIO - 100.0% (Cost $1,352,914,188) |

1,352,815,038 |

||

|

NET OTHER ASSETS (LIABILITIES) - 0.0% |

388,567 |

||

|

NET ASSETS - 100% |

$ 1,353,203,605 |

||

|

Futures Contracts |

|||||

|

|

Expiration Date |

Underlying Face Amount at Value |

Unrealized Appreciation/ |

||

|

Purchased |

|||||

|

Commodity Futures Contracts |

|||||

|

241 CBOT Corn Contracts |

Sept. 2011 |

$ 8,019,275 |

$ (539,866) |

||

|

119 CBOT Soybean Contracts |

Nov. 2011 |

8,075,638 |

(82,864) |

||

|

90 CBOT Soybean Oil Contracts |

Dec. 2011 |

3,047,220 |

(105,013) |

||

|

121 CBOT Wheat Contracts |

Sept. 2011 |

4,068,625 |

(446,927) |

||

|

65 CME Lean Hogs Contracts |

Oct. 2011 |

2,402,400 |

17,728 |

||

|

82 CME Live Cattle Contracts |

Oct. 2011 |

3,848,260 |

(76,480) |

||

|

74 COMEX Copper Contracts |

Sept. 2011 |

8,287,075 |

527,124 |

||

|

79 COMEX Gold Contracts |

Dec. 2011 |

12,886,480 |

509,040 |

||

|

23 COMEX Silver Contracts |

Sept. 2011 |

4,612,190 |

423,042 |

||

|

28 ICE Coffee Contracts |

Sept. 2011 |

2,515,275 |

(284,910) |

||

|

86 LME Aluminum Contracts |

Sept. 2011 |

5,621,713 |

128 |

||

|

16 LME Nickel Contracts |

Sept. 2011 |

2,398,368 |

178,054 |

||

|

48 LME Zinc Contracts |

Sept. 2011 |

2,979,600 |

224,542 |

||

|

30 NYBOT Cotton No. 2 Contracts |

Dec. 2011 |

1,526,550 |

(367,454) |

||

|

105 NYBOT Sugar Contracts |

Oct. 2011 |

3,505,656 |

489,464 |

||

|

36 NYMEX Heating Oil Contracts |

Sept. 2011 |

4,686,293 |

(40,550) |

||

|

263 NYMEX Natural Gas Contracts |

Sept. 2011 |

10,901,350 |

(1,284,688) |

||

|

36 NYMEX RBOB Gasoline Contracts |

Sept. 2011 |

4,623,545 |

103,038 |

||

|

174 NYMEX WTI Crude Contracts |

Sept. 2011 |

16,651,800 |

(654,580) |

||

|

TOTAL COMMODITY FUTURES CONTRACTS |

$ 110,657,313 |

$ (1,411,172) |

|||

|

|

|

The face value of futures purchased as a percentage of net assets is 8.2% |

|

Swap Agreements |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

Sept. 2011 |

$ 12,000,000 |

$ (53,247) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

Oct. 2011 |

17,200,000 |

591,311 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

August 2011 |

$ 3,000,000 |

$ 113,615 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

Oct. 2011 |

25,000,000 |

307,816 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

Nov. 2011 |

20,000,000 |

(215,726) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Barclays Bank PLC |

Oct. 2011 |

12,760,000 |

0 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

August 2011 |

41,500,000 |

451,515 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

August 2011 |

6,000,000 |

108,132 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

August 2011 |

5,700,000 |

75,406 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

Oct. 2011 |

41,700,000 |

698,124 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

Oct. 2011 |

$ 30,100,000 |

$ 1,068,313 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

Oct. 2011 |

38,000,000 |

974,227 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

Oct. 2011 |

6,400,000 |

67,716 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Credit Suisse First Boston |

Nov. 2011 |

15,800,000 |

(164,275) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Goldman Sachs |

August 2011 |

5,700,000 |

6,884 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Goldman Sachs |

Sept. 2011 |

15,200,000 |

(258,899) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Goldman Sachs |

Sept. 2011 |

19,500,000 |

326,055 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Goldman Sachs |

Oct. 2011 |

25,000,000 |

307,816 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Goldman Sachs |

Oct. 2011 |

$ 20,500,000 |

$ (153,847) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with JPMorgan Chase, Inc. |

Sept. 2011 |

24,100,000 |

(421,786) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with JPMorgan Chase, Inc. |

Sept. 2011 |

12,200,000 |

(177,503) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with JPMorgan Chase, Inc. |

August 2011 |

17,100,000 |

802,103 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with JPMorgan Chase, Inc. |

Oct. 2011 |

29,800,000 |

547,418 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with JPMorgan Chase, Inc. |

Oct. 2011 |

16,600,000 |

(246,956) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

August 2011 |

34,261,254 |

41,380 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

August 2011 |

34,261,581 |

41,380 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

August 2011 |

14,600,000 |

37,696 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

August 2011 |

$ 15,000,000 |

$ 118,905 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

August 2011 |

10,000,000 |

(43,670) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

Sept. 2011 |

15,800,000 |

(362,000) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Merrill Lynch, Inc. |

Sept. 2011 |

14,000,000 |

(203,692) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

August 2011 |

8,200,000 |

(449,021) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

August 2011 |

14,800,000 |

(94,040) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

August 2011 |

17,700,000 |

(77,296) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

August 2011 |

17,500,000 |

(156,830) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

Oct. 2011 |

20,000,000 |

246,253 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Morgan Stanley Capital Group, Inc. |

Sept. 2011 |

$ 31,900,000 |

$ (144,353) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

13,700,000 |

(8,947) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

9,800,000 |

116,879 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

15,000,000 |

198,160 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

26,000,000 |

206,572 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

20,000,000 |

(457,904) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

30,000,000 |

(268,482) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

August 2011 |

30,000,000 |

(268,482) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

Sept. 2011 |

10,000,000 |

167,312 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional Amount |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with Societe Generale |

Oct. 2011 |

$ 11,600,000 |

$ 297,322 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

August 2011 |

20,000,000 |

(1,240,126) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Sept. 2011 |

15,000,000 |

119,176 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Sept. 2011 |

46,200,000 |

(617,841) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Oct. 2011 |

12,700,000 |

(69,831) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Oct. 2011 |

33,200,000 |

684,789 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

August 2011 |

8,800,000 |

384,938 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Nov. 2011 |

10,000,000 |

210,802 |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Nov. 2011 |

30,800,000 |

160,431 |

||

|

Swap Agreements - continued |

|||||

|

|

Expiration Date |

Notional |

Value |

||

|

Total Return Swaps - continued |

|||||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Nov. 2011 |

$ 59,200,000 |

$ (442,596) |

||

|

Receive a return equal to Dow Jones-UBS Commodity Index Total Return and pay a floating rate based on 3-month US auction rate T-Bill plus a specified spread with UBS AG |

Nov. 2011 |

27,200,000 |

(293,296) |

||

|

|

$ 1,138,082,835 |

$ 2,587,800 |

|||

|

Legend |

|

(a) Affiliated fund that is available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC's website or upon request. |

|

(b) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $33,918,752 or 2.5% of net assets. |

|

(c) Security or a portion of the security was pledged to cover margin requirements for futures contracts. At the period end, the value of securities pledged amounted to $10,956,637. |

|

(d) Security or a portion of the security has been segregated as collateral for open swap agreements. At the period end, the value of securities pledged amounted to $85,172,351. |

|

(e) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end. |

|

(f) Security is indexed to the Dow Jones-UBS Commodity Index Total Return, multiplied by 3. Securities do not guarantee any return of principal at maturity but instead, will pay at maturity or upon exchange, an amount based on the closing value of the Dow Jones-UBS Commodity Index Total Return. Although these instruments are primarily debt obligations, they indirectly provide exposure to changes in the value of the underlying commodities. Holders of the security have the right to exchange these notes at any time. |

|

Affiliated Central Funds |

|

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows: |

|

Fund |

Income earned |

|

Fidelity Cash Central Fund |

$ 709,794 |

|

Consolidated Subsidiary |

|

|

Value, beginning of period |

Purchases |

Sales Proceeds |

Dividend |

Value, |

|

Fidelity Commodity Return Central Cayman Ltd. |

$ 33,682,432 |

$ 98,999,942 |

$ 25,000,053 |

$ - |

$ 140,659,146 |

|

Other Information |

|

The following is a summary of the inputs used, as of July 31, 2011, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in the accompanying Notes to Consolidated Financial Statements. |

|

Valuation Inputs at Reporting Date: |

||||

|

Description |

Total |

Level 1 |

Level 2 |

Level 3 |

|

Investments in Securities: |

||||

|

U.S. Government and Government Agency Obligations |

$ 133,962,391 |

$ - |

$ 133,962,391 |

$ - |

|

Commodity-Linked Notes |

33,918,752 |

- |

33,918,752 |

- |

|

Money Market Funds |

1,184,933,895 |

1,184,933,895 |

- |

- |

|

Total Investments in Securities: |

$ 1,352,815,038 |

$ 1,184,933,895 |

$ 167,881,143 |

$ - |

|

Derivative Instruments: |

||||

|

Assets |

||||

|

Futures Contracts |

$ 2,472,160 |

$ 2,472,160 |

$ - |

$ - |

|

Swap Agreements |

9,478,446 |

- |

9,478,446 |

- |

|

Total Assets |

$ 11,950,606 |

$ 2,472,160 |

$ 9,478,446 |

$ - |

|

Liabilities |

||||

|

Futures Contracts |

$ (3,883,332) |

$ (3,883,332) |

$ - |

$ - |

|

Swap Agreements |

(6,890,646) |

- |

(6,890,646) |

- |

|

Total Liabilities |

$ (10,773,978) |

$ (3,883,332) |

$ (6,890,646) |

$ - |

|

Total Derivative Instruments: |

$ 1,176,628 |

$ (1,411,172) |

$ 2,587,800 |

$ - |

|

Value of Derivative Instruments |

|

The following table is a summary of the Fund's value of derivative instruments by risk exposure as of July 31, 2011. For additional information on derivative instruments, please refer to the Derivative Instruments section in the accompanying Notes to Consolidated Financial Statements. |

|

Risk Exposure / |

Value |

|

|

|

Asset |

Liability |

|

Commodity Risk |

||

|

Futures Contracts (a) |

$ 2,472,160 |

$ (3,883,332) |

|

Swap Agreements (b) |

9,478,446 |

(6,890,646) |

|

Total Value of Derivatives |

$ 11,950,606 |

$ (10,773,978) |

|

(a) Reflects cumulative appreciation/(depreciation) on futures contracts as disclosed on the Consolidated Schedule of Investments. Only the period end variation margin is separately disclosed on the Consolidated Statement of Assets and Liabilities. |

|

(b) Value is disclosed on the Consolidated Statement of Assets and Liabilities in the Swap agreements, at value line-items. |

See accompanying notes which are an integral part of the consolidated financial statements.

Annual Report

Consolidated Financial Statements

Consolidated Statement of Assets and Liabilities

|

|

July 31, 2011 |

|

|

|

|

|

|

Assets |

|

|

|

Investment in securities, at value - See accompanying schedule: Unaffiliated issuers (cost $167,980,293) |

$ 167,881,143 |

|

|

Fidelity Central Funds (cost $1,184,933,895) |

1,184,933,895 |

|

|

Total Investments (cost $1,352,914,188) |

|

$ 1,352,815,038 |

|

Segregated cash with broker for futures contracts |

|

815,522 |

|

Receivable for fund shares sold |

|

10,090 |

|

Interest receivable |

|

512 |

|

Distributions receivable from Fidelity Central Funds |

|

100,553 |

|

Swap agreements, at value |

|

9,478,446 |

|

Prepaid expenses |

|

6,250 |

|

Total assets |

|

1,363,226,411 |

|

|

|

|

|

Liabilities |

|

|

|

Payable for investments purchased |

$ 2,065,740 |

|

|

Payable for fund shares redeemed |

188,735 |

|

|

Swap agreements, at value |

6,890,646 |

|

|

Accrued management fee |

35,439 |

|

|

Daily variation margin on futures contracts |

841,903 |

|

|

Other payables and accrued expenses |

343 |

|

|

Total liabilities |

|

10,022,806 |

|

|

|

|

|

Net Assets |

|

$ 1,353,203,605 |

|

Net Assets consist of: |

|

|

|

Paid in capital |

|

$ 1,310,197,706 |

|

Undistributed net investment income |

|

519,777 |

|

Accumulated undistributed net realized gain (loss) on investments |

|

41,408,644 |

|

Net unrealized appreciation (depreciation) on investments |

|

1,077,478 |

|

Net Assets, for 106,757,851 shares outstanding |

|

$ 1,353,203,605 |

|

Net Asset Value, offering price and redemption price per share ($1,353,203,605 ÷ 106,757,851 shares) |

|

$ 12.68 |

See accompanying notes which are an integral part of the consolidated financial statements.

Annual Report

Consolidated Financial Statements - continued

Consolidated Statement of Operations

|

|

Year ended July 31, 2011 |

|

|

|

|

|

|

Investment Income |

|

|

|

Interest |

|

$ 75,399 |

|

Income from Fidelity Central Funds |

|

709,794 |

|

Total income |

|

785,193 |

|

|

|

|

|

Expenses |

|

|

|

Management fee |

$ 244,349 |

|

|

Custodian fees and expenses |

6,252 |

|

|

Independent trustees' compensation |

1,596 |

|

|

Subsidiary directors' fees |

15,000 |

|

|

Total expenses before reductions |

267,197 |

|

|

Expense reductions |

(1,782) |

265,415 |

|

Net investment income (loss) |

|

519,778 |

|

Realized and Unrealized Gain (Loss) Net realized gain (loss) on: |

|

|

|

Investment securities: |

|

|

|

Unaffiliated issuers |

603,116 |

|

|

Futures contracts |

827,993 |

|

|

Swap agreements |

41,399,029 |

|

|

Total net realized gain (loss) |

|

42,830,138 |

|

Change in net unrealized appreciation (depreciation) on: Investment securities |

2,373 |

|

|

Futures contracts |

(1,743,067) |

|

|

Swap agreements |

(7,324,599) |

|

|

Total change in net unrealized appreciation (depreciation) |

|

(9,065,293) |

|

Net gain (loss) |

|

33,764,845 |

|

Net increase (decrease) in net assets resulting from operations |

|

$ 34,284,623 |

See accompanying notes which are an integral part of the consolidated financial statements.

Annual Report

Consolidated Statement of Changes in Net Assets

|

|

Year ended |

For the period |

|

Increase (Decrease) in Net Assets |

|

|

|

Operations |

|

|

|

Net investment income (loss) |

$ 519,778 |

$ 182,914 |

|

Net realized gain (loss) |

42,830,138 |

(9,008,035) |

|

Change in net unrealized appreciation (depreciation) |

(9,065,293) |

10,142,771 |

|

Net increase (decrease) in net assets resulting |

34,284,623 |

1,317,650 |

|

Distributions to shareholders from net investment income |

(108,747) |

(72,948) |

|

Distributions to shareholders from net realized gain |

(1,196,217) |

- |

|

Total distributions |

(1,304,964) |

(72,948) |

|

Share transactions |

1,350,824,480 |

196,300,785 |

|

Reinvestment of distributions |

1,304,964 |

72,948 |

|

Cost of shares redeemed |

(228,370,350) |

(1,153,583) |

|

Net increase (decrease) in net assets resulting from share transactions |

1,123,759,094 |

195,220,150 |

|

Total increase (decrease) in net assets |

1,156,738,753 |

196,464,852 |

|

|

|

|

|

Net Assets |

|

|

|

Beginning of period |

196,464,852 |

- |

|

End of period (including undistributed net investment income of $519,777 and undistributed net investment income of $109,966, respectively) |

$ 1,353,203,605 |

$ 196,464,852 |

|

Other Information Shares |

|

|

|

Sold |

107,230,264 |

18,731,082 |

|

Issued in reinvestment of distributions |

123,811 |

6,967 |

|

Redeemed |

(19,223,805) |

(110,468) |

|

Net increase (decrease) |

88,130,270 |

18,627,581 |

See accompanying notes which are an integral part of the consolidated financial statements.

Annual Report

Consolidated Financial Highlights

|

Years ended July 31, |

2011 |

2010 G |

|

Selected Per-Share Data |

|

|

|

Net asset value, beginning of period |

$ 10.55 |

$ 10.00 |

|

Income from Investment Operations |

|

|

|

Net investment income (loss) D |

.01 |

.01 |

|

Net realized and unrealized gain (loss) |

2.22 |

.55 |

|

Total from investment operations |

2.23 |

.56 |

|

Distributions from net investment income |

(.01) |

(.01) |

|

Distributions from net realized gain |

(.09) |

- |

|

Total distributions |

(.10) |

(.01) |

|

Net asset value, end of period |

$ 12.68 |

$ 10.55 |

|

Total Return B,C |

21.28% |

5.55% |

|

Ratios to Average Net Assets E,H |

|

|

|

Expenses before reductions |

.05% |

.06% A |

|

Expenses net of fee waivers, if any |

.05% |

.06% A |

|

Expenses net of all reductions |

.05% |

.06% A |

|

Net investment income (loss) |

.10% |

.13% A |

|

Supplemental Data |

|

|

|

Net assets, end of period (000 omitted) |

$ 1,353,204 |

$ 196,465 |

|

Portfolio turnover rate F |

33% |

109% A |

A Annualized

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Calculated based on average shares outstanding during the period.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

F Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

G For the period October 7, 2009 (commencement of operations) to July 31, 2010.

H Expense ratios reflect operating expenses of the Fund. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the Fund during periods when reimbursements or reductions occur. Expense ratios before reductions for start-up periods may not be representative of longer term operating periods. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the Fund.

See accompanying notes which are an integral part of the consolidated financial statements.

Annual Report

Notes to Consolidated Financial Statements

For the period ended July 31, 2011

1. Organization.

Fidelity Commodity Strategy Central Fund (the Fund) is a non-diversified fund of Fidelity Garrison Street Trust (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. Shares of the Fund are only offered to other investment companies and accounts managed by Fidelity Management & Research Company (FMR), or its affiliates (the Investing Funds).

2. Consolidated Subsidiary.

The Fund invests in certain commodity-linked derivative instruments through Fidelity Commodity Return Central Cayman Ltd., a wholly owned subsidiary (the "Subsidiary"). As of July 31, 2011, the Fund held $140,659,146 in the Subsidiary, representing 10.4% of the Fund's net assets.

The financial statements have been consolidated and include accounts of the Fund and the Subsidiary. Accordingly, all inter-company transactions and balances have been eliminated.

3. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies available only to other investment companies and accounts managed by FMR and its affiliates. The Fund's Consolidated Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of FMR.

A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) web site at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC web site or upon request.

4. Significant Accounting Policies.

The consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require

Annual Report

4. Significant Accounting Policies - continued

management to make certain estimates and assumptions at the date of the consolidated financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the consolidated financial statements were issued have been evaluated in the preparation of the consolidated financial statements. The following summarizes the significant accounting policies of the Fund:

Security Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Fund uses independent pricing services approved by the Board of Trustees to value its investments. When current market prices or quotations are not readily available or reliable, valuations may be determined in good faith in accordance with procedures adopted by the Board of Trustees. Factors used in determining value may include market or security specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The value used for net asset value (NAV) calculation under these procedures may differ from published prices for the same securities.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

Level 1 - quoted prices in active markets for identical investments

Level 2 - other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

Level 3 - unobservable inputs (including the Fund's own assumptions based on the best information available)

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The aggregate value of investments by input level, as of July 31, 2011 for the Fund's investments, is included at the end of the Fund's Consolidated Schedule of Investments. Valuation techniques used to value the Fund's investments by major category are as follows:

Debt securities, including restricted securities, are valued based on evaluated prices received from independent pricing services or from dealers who make markets in such securities. For U.S. government and government agency obligations, pricing services utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type as well as dealer supplied prices and are generally categorized as Level 2 in the hierarchy. For commodity-linked notes, pricing services generally consider the movement of an underlying commodity index as well as other terms of the contract including the leverage factor and any fee and/or interest components of the note and are categorized as Level 2 in the hierarchy. Swaps are marked-to-market daily

Annual Report

Notes to Consolidated Financial Statements - continued

4. Significant Accounting Policies - continued

Security Valuation - continued

based on valuations from independent pricing services or dealer-supplied valuations and changes in value are recorded as unrealized appreciation (depreciation). Pricing services utilize matrix pricing which considers comparisons to movements in the underlying index, interest rate curves, credit spread curves, default possibilities and recovery rates and, as a result, swaps are generally categorized as Level 2 in the hierarchy. When independent prices are unavailable or unreliable, debt securities and swaps may be valued utilizing pricing matrices which consider similar factors that would be used by independent pricing services. These are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

Futures contracts are valued at the settlement price or official closing price established each day by the board of trade or exchange on which they are traded and are categorized as Level 1 in the hierarchy. Investments in open-end mutual funds, including the Fidelity Central Funds, are valued at their closing net asset value each business day and are categorized as Level 1 in the hierarchy.

Investment Transactions and Income. For financial reporting purposes, the Fund's investment holdings and NAV include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day. Gains and losses on securities sold are determined on the basis of identified cost. Interest income and distributions from other Fidelity Central Funds are accrued as earned. Interest income includes coupon interest and amortization of premium and accretion of discount on debt securities. Investment income is recorded net of foreign taxes withheld where recovers of such taxes is uncertain.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company, including distributing substantially all of its taxable income and realized gains under Subchapter M of the Internal Revenue Code and filing its U.S. federal tax return. As a result, no provision for income taxes is required. As of July 31, 2011, the Fund did not have any unrecognized tax benefits in the consolidated financial statements. A fund's federal tax return is subject to examination by the Internal Revenue Service (IRS) for a period of three years.

Annual Report

4. Significant Accounting Policies - continued

Income Tax Information and Distributions to Shareholders - continued

The Subsidiary is classified as a controlled foreign corporation under Subchapter N of the Internal Revenue Code. Therefore, the Fund is required to increase its taxable income by its share of the Subsidiary's income. Net investment losses of the Subsidiary cannot be deducted by the Fund in the current period nor carried forward to offset taxable income in future periods.

Distributions are declared and recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the consolidated financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Temporary book-tax differences will reverse in a subsequent period.

Book-tax differences are primarily due to the controlled foreign corporation.

The federal tax cost of investment securities and unrealized appreciation (depreciation) as of period end on an unconsolidated basis were as follows:

|

Gross unrealized appreciation |

$ 130,349 |

|

Gross unrealized depreciation |

(6,020,427) |

|

Net unrealized appreciation (depreciation) on securities and other investments |

$ (5,890,078) |

|

|

|

|

Tax Cost |

$ 1,359,172,160 |

The tax-based components of distributable earnings as of period end were as follows:

|

Undistributed ordinary income |

$ 39,524,151 |

|

Undistributed long-term capital gain |

$ 590,288 |

|

Net unrealized appreciation (depreciation) |

$ (5,890,078) |

Under the recently enacted Regulated Investment Company Modernization Act of 2010 (the Act), the Fund will be permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to any losses incurred in pre-enactment taxable years, which generally expire after eight years from when they are incurred. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses rather than being considered all short-term as under previous law. The Fund's first fiscal year end subject to the Act will be July 31, 2012.

Annual Report

Notes to Consolidated Financial Statements - continued

4. Significant Accounting Policies - continued

Income Tax Information and Distributions to Shareholders - continued

The tax character of distributions paid was as follows:

|

|

July 31, 2011 |

July 31, 2010 |

|

Ordinary Income |

$ 1,304,964 |

$ 72,948 |

5. Operating Policies.

Indexed Securities. The Fund may invest in indexed securities whose values, interest rates and/or redemption prices are linked either directly or inversely to changes in foreign currencies, interest rates, commodities, indices, or other underlying instruments. These securities may be used to increase or decrease its exposure to different underlying instruments and to gain exposure to markets that might be difficult to invest in through conventional securities. Indexed securities may be leveraged, increasing their volatility relative to changes in their underlying instruments, but any loss is limited to the amount of the original investment. Gains (losses) realized upon the sale of indexed securities are included in realized gains (losses) on investment securities.

Restricted Securities. The Fund may invest in securities that are subject to legal or contractual restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are registered. Disposal of these securities may involve time-consuming negotiations and expense, and prompt sale at an acceptable price may be difficult. Information regarding restricted securities is included at the end of the Fund's Consolidated Schedule of Investments.

6. Derivative Instruments.

Risk Exposures and the Use of Derivative Instruments. The Fund primarily used derivative instruments (derivatives), including futures contracts and swap agreements, in order to meet its investment objectives. The strategy is to use derivatives to increase returns, to gain exposure to certain types of assets and to manage exposure to certain risks as defined below. The success of any strategy involving derivatives depends on analysis of numerous economic factors, and if the strategies for investment do not work as intended, the Fund may not achieve its objectives.

The Fund's use of derivatives increased or decreased its exposure to the following risk:

|

Commodity Risk |

Commodity risk is the risk that the value of a commodity will fluctuate as a result of changes in market prices. |

Annual Report

6. Derivative Instruments - continued

Risk Exposures and the Use of Derivative Instruments - continued

The Fund is also exposed to additional risks from investing in derivatives, such as liquidity risk and counterparty credit risk. Liquidity risk is the risk that the Fund will be unable to sell the derivative in the open market in a timely manner. Counterparty credit risk is the risk that the counterparty will not be able to fulfill its obligation to the Fund. Derivative counterparty credit risk is managed through formal evaluation of the creditworthiness of all potential counterparties. On certain over-the-counter derivatives, the Fund attempts to reduce its exposure to counterparty credit risk by entering into an International Swaps and Derivatives Association (ISDA) Master Agreement on a bilateral basis with each of its counterparties. The ISDA Master Agreement gives the Fund the right to terminate all transactions traded under such agreement if there is a certain deterioration in the credit quality of the counterparty. The ISDA Master Agreement gives each party the right, upon an event of default by the other party or a termination of the agreement, to close out all transactions traded under such agreement and to net amounts owed under each transaction to one net payable by one party to the other. Upon entering into a swap, the Fund is required to post an initial collateral amount (referred to as "Independent Amount"), as defined in the ISDA Master Agreement. The Fund is required to post additional collateral for the benefit of counterparties for unrealized losses on outstanding swap contracts. Collateral in the form of cash or securities, if required, is held in segregated accounts with the Fund's custodian bank in accordance with the collateral agreements entered into between the Fund, the swap counterparty and the Fund's custodian bank, and is identified in the Consolidated Schedule of Investments. The Fund could experience delays and costs in gaining access to the collateral even though it is held by the Fund's custodian bank. The Fund's maximum risk of loss from counterparty credit risk is generally the aggregate unrealized appreciation and unpaid counterparty payments in excess of any collateral pledged by the counterparty to the Fund. Counterparty risk related to exchange-traded futures contracts is minimal because of the protection provided by the exchange's clearinghouse. Derivatives involve, to varying degrees, risk of loss in excess of the amounts recognized in the Consolidated Statement of Assets and Liabilities.

Net Realized Gain (Loss) and Change in Net Unrealized Appreciation (Depreciation) on Derivatives. The table below, which reflects the impacts of derivatives on the financial performance of the Fund, summarizes the net realized gain (loss) and change in net unrealized appreciation (depreciation) for derivatives during the period.

Annual Report

Notes to Consolidated Financial Statements - continued

6. Derivative Instruments - continued

Net Realized Gain (Loss) and Change in Net Unrealized Appreciation (Depreciation) on Derivatives - continued

These amounts are included in the Consolidated Statement of Operations.

|

Risk Exposure / Derivative Type |

Net Realized |

Change in Net Unrealized Appreciation (Depreciation) |

|

Commodity Risk |

|

|

|

Futures Contracts |

$ 827,993 |

$ (1,743,067) |

|

Swap Agreements |

41,399,029 |

(7,324,599) |

|

Totals |

$ 42,227,022 |

$ (9,067,666) |

Futures Contracts. A futures contract is an agreement between two parties to buy or sell a specified underlying instrument for a fixed price at a specified future date. The Fund used futures contracts to manage its exposure to the commodities market.

Upon entering into a futures contract, a fund is required to deposit either cash or securities (initial margin) with a clearing broker in an amount equal to a certain percentage of the face value of the contract. Futures contracts are marked-to-market daily and subsequent payments (variation margin) are made or received by a fund depending on the daily fluctuations in the value of the futures contracts and are recorded as unrealized appreciation or (depreciation). This receivable and/or payable is included in daily variation margin on futures contracts in the Consolidated Statement of Assets and Liabilities. Realized gain or (loss) is recorded upon the expiration or closing of a futures contract. The net realized gain (loss) and change in net unrealized appreciation (depreciation) on futures contracts during the period is included in the Consolidated Statement of Operations.

The underlying face amount at value of open futures contracts at period end is shown in the Consolidated Schedule of Investments under the caption "Futures Contracts." This amount reflects each contract's exposure to the underlying instrument at period end. Securities deposited to meet initial margin requirements are identified in the Consolidated Schedule of Investments.

Certain risks arise upon entering into futures contracts, including the risk that an illiquid market limits the ability to close out a futures contract prior to settlement date.

Swap Agreements. A swap agreement (swap) is a contract between two parties to exchange future cash flows at periodic intervals based on a notional principal amount.

Details of swaps open at period end are included in the Consolidated Schedule of Investments under the caption "Swap Agreements." Swaps are marked-to-market daily and

Annual Report

6. Derivative Instruments - continued

Swap Agreements - continued

changes in value are recorded as unrealized appreciation or (depreciation) and reflected in the Consolidated Statement of Assets and Liabilities. Any upfront premiums paid or received upon entering a swap to compensate for differences between stated terms of the agreement and prevailing market conditions (e.g. credit spreads, interest rates or other factors) are recorded as realized gain or (loss) ratably over the term of the swap. Payments are exchanged at specified intervals, accrued daily commencing with the effective date of the contract and recorded as realized gain or (loss). Realized gain or (loss) is also recorded in the event of an early termination of a swap. The net realized gain (loss) and change in net unrealized appreciation (depreciation) on swaps during the period is included in the Consolidated Statement of Operations.

Risks of loss include commodity risk. In addition, there is the risk of failure by the counterparty to perform under the terms of the agreement and lack of liquidity in the market.

Total Return Swaps. Total return swaps are agreements between counterparties to exchange cash flows, one based on a market-linked return of an individual security or a basket of securities (i.e., an index), and the other on a fixed or floating rate. The Fund entered into total return swaps to manage its commodities market exposure.

7. Purchases and Sales of Investments.

Purchases and sales of securities, other than short-term securities, aggregated $34,306,911 and $5,908,734, respectively.

8. Fees and Other Transactions with Affiliates.

Management Fee and Expense Contract. FMR Co., Inc. (FMRC), an affiliate of FMR, provides the Fund with investment management services. The Fund does not pay any fees for these services. Pursuant to the Fund's management contract with FMRC, FMR pays FMRC a portion of the management fees it receives from the Investing Funds. In addition, under an expense contract, FMR also pays all other expenses of the Fund, excluding custody fees, the compensation of the independent Trustees, and certain exceptions such as interest expense.

FMR and its affiliates also provide investment management services to the Subsidiary. The Subsidiary pays FMR a monthly management fee at an annual rate of .30% of its net assets. The Subsidiary also pays certain other expenses including custody and directors fees.

Annual Report

Notes to Consolidated Financial Statements - continued

8. Fees and Other Transactions with Affiliates - continued

Sub-Adviser. Geode Capital Management, LLC (Geode), serves as sub-adviser for the Fund. Geode provides discretionary investment advisory services to the Fund and is paid by FMR for providing these services.

9. Expense Reductions.

FMR has voluntarily agreed to reimburse a portion of the Fund's operating expenses. For the period, the reimbursement reduced the expenses by $1,596.

In addition, through arrangements with the Fund's custodian, credits realized as a result of uninvested cash balances were used to reduce the Fund's expenses. During the period, these credits reduced the Fund's custody expenses by $186.

10. Other.

The Fund's organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

At the end of the period, mutual funds managed by FMR or an FMR affiliate were the owners of record of all of the outstanding shares of the Fund.

Annual Report

Report of Independent Registered Public Accounting Firm

To the Trustees of Fidelity Garrison Street Trust and the Shareholders of Fidelity Commodity Strategy Central Fund:

In our opinion, the accompanying consolidated statement of assets and liabilities, including the consolidated schedule of investments, and the related consolidated statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Fidelity Commodity Strategy Central Fund (a fund of Fidelity Garrison Street Trust) at July 31, 2011, the results of its operations, the changes in its net assets and the financial highlights for each of the periods indicated, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements") are the responsibility of the Fidelity Commodity Strategy Central Fund's management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at July 31, 2011 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

PricewaterhouseCoopers LLP

Boston, Massachusetts

September 20, 2011

Annual Report

Trustees and Officers

The Trustees and executive officers of the trust and fund, as applicable, are listed below. The Board of Trustees governs the fund and is responsible for protecting the interests of shareholders. The Trustees are experienced executives who meet periodically throughout the year to oversee the fund's activities, review contractual arrangements with companies that provide services to the fund, oversee management of the risks associated with such activities and contractual arrangements, and review the fund's performance. Except for James C. Curvey, each of the Trustees oversees 198 funds advised by FMR or an affiliate. Mr. Curvey oversees 419 funds advised by FMR or an affiliate.

The Trustees hold office without limit in time except that (a) any Trustee may resign; (b) any Trustee may be removed by written instrument, signed by at least two-thirds of the number of Trustees prior to such removal; (c) any Trustee who requests to be retired or who has become incapacitated by illness or injury may be retired by written instrument signed by a majority of the other Trustees; and (d) any Trustee may be removed at any special meeting of shareholders by a two-thirds vote of the outstanding voting securities of the trust. Each Trustee who is not an interested person (as defined in the 1940 Act) (Independent Trustee), shall retire not later than the last day of the calendar year in which his or her 75th birthday occurs. The Independent Trustees may waive this mandatory retirement age policy with respect to individual Trustees. The executive officers hold office without limit in time, except that any officer may resign or may be removed by a vote of a majority of the Trustees at any regular meeting or any special meeting of the Trustees. Except as indicated, each individual has held the office shown or other offices in the same company for the past five years.

Experience, Skills, Attributes, and Qualifications of the Fund's Trustees. The Governance and Nominating Committee has adopted a statement of policy that describes the experience, qualifications, attributes, and skills that are necessary and desirable for potential Independent Trustee candidates (Statement of Policy). The Board believes that each Trustee satisfied at the time he or she was initially elected or appointed a Trustee, and continues to satisfy, the standards contemplated by the Statement of Policy. The Governance and Nominating Committee also engages professional search firms to help identify potential Independent Trustee candidates who have the experience, qualifications, attributes, and skills consistent with the Statement of Policy. From time to time, additional criteria based on the composition and skills of the current Independent Trustees, as well as experience or skills that may be appropriate in light of future changes to board composition, business conditions, and regulatory or other developments, have also been considered by the professional search firms and the Governance and Nominating Committee. In addition, the Board takes into account the Trustees' commitment and participation in Board and committee meetings, as well as their leadership of standing and ad hoc committees throughout their tenure.

In determining that a particular Trustee was and continues to be qualified to serve as a Trustee, the Board has considered a variety of criteria, none of which, in isolation, was controlling. The Board believes that, collectively, the Trustees have balanced and diverse experience, qualifications, attributes, and skills, which allow the Board to operate effectively in governing the fund and protecting the interests of shareholders. Information about the specific experience, skills, attributes, and qualifications of each Trustee, which in each case led to the Board's conclusion that the Trustee should serve (or continue to serve) as a trustee of the fund, is provided below.

Annual Report

Board Structure and Oversight Function. Abigail P. Johnson is an interested person (as defined in the 1940 Act) and currently serves as Chairman. The Trustees have determined that an interested Chairman is appropriate and benefits shareholders because an interested Chairman has a personal and professional stake in the quality and continuity of services provided to the fund. Independent Trustees exercise their informed business judgment to appoint an individual of their choosing to serve as Chairman, regardless of whether the Trustee happens to be independent or a member of management. The Independent Trustees have determined that they can act independently and effectively without having an Independent Trustee serve as Chairman and that a key structural component for assuring that they are in a position to do so is for the Independent Trustees to constitute a substantial majority for the Board. The Independent Trustees also regularly meet in executive session. Kenneth L. Wolfe serves as Chairman of the Independent Trustees and as such (i) acts as a liaison between the Independent Trustees and management with respect to matters important to the Independent Trustees and (ii) with management prepares agendas for Board meetings.

Fidelity funds are overseen by different Boards of Trustees. The fund's Board oversees Fidelity's investment-grade bond, money market, and asset allocation funds and another Board oversees Fidelity's equity and high income funds. The asset allocation funds may invest in Fidelity funds that are overseen by such other Board. The use of separate Boards, each with its own committee structure, allows the Trustees of each group of Fidelity funds to focus on the unique issues of the funds they oversee, including common research, investment, and operational issues. On occasion, the separate Boards establish joint committees to address issues of overlapping consequences for the Fidelity funds overseen by each Board.

The Trustees operate using a system of committees to facilitate the timely and efficient consideration of all matters of importance to the Trustees, the fund, and fund shareholders and to facilitate compliance with legal and regulatory requirements and oversight of the fund's activities and associated risks. The Board, acting through its committees, has charged FMR and its affiliates with (i) identifying events or circumstances the occurrence of which could have demonstrably adverse effects on the fund's business and/or reputation; (ii) implementing processes and controls to lessen the possibility that such events or circumstances occur or to mitigate the effects of such events or circumstances if they do occur; and (iii) creating and maintaining a system designed to evaluate continuously business and market conditions in order to facilitate the identification and implementation processes described in (i) and (ii) above. Because the day-to-day operations and activities of the fund are carried out by or through FMR, its affiliates and other service providers, the fund's exposure to risks is mitigated but not eliminated by the processes overseen by the Trustees. While each of the Board's committees has responsibility for overseeing different aspects of the fund's activities, oversight is exercised primarily through the Operations and Audit Committees. Appropriate personnel, including but not limited to the fund's Chief Compliance Officer (CCO), FMR's internal auditor, the independent accountants, the fund's Treasurer and portfolio management personnel, make periodic reports to the Board's committees, as appropriate. The responsibilities of each committee, including their oversight responsibilities, are described further under "Standing Committees of the Fund's Trustees."