Registration No. 333-16881

File No. 811-04797

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [ ]

Post-Effective Amendment No.

24

[X]

and/or

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 [X]

Amendment No. 35

Oppenheimer EQUITY INCOME fund, INC.

(Exact Name of Registrant as Specified in Charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (303) 768-3200

Arthur S. Gabinet, Esq.

OppenheimerFunds, Inc.

Two World Financial Center, 225 Liberty Street, New York, New York 10281-1008

(Name and Address of Agent for Service)

It is proposed that this filing will become effective (check appropriate box):

[ ] immediately upon filing pursuant to paragraph (b)

[ ] on _____________ pursuant to paragraph (b)

[ ] 60 days after filing pursuant to paragraph (a)(1)

[X] On February 28, 2012 pursuant to paragraph (a)(1)

[ ] 75 days after filing pursuant to paragraph (a)(2)

[ ] on _______________ pursuant to paragraph (a)(2) of Rule 485.

If appropriate, check the following box:

[ ] this post-effective amendment designates a new effective date for a previously filed post-effective amendment.

|

Oppenheimer |

|

NYSE Ticker Symbols |

|

|

Class A |

OAEIX |

|

Class B |

OBEIX |

|

Class C |

OCEIX |

|

Class N |

ONEIX |

|

Class Y |

OYEIX |

|

Class I |

|

| Prospectus dated February __, 2012 |

| Oppenheimer Equity Income Fund, Inc. is a mutual fund that seeks total return. It invests mainly in common stocks and other equity securities that it believes are undervalued. |

| This prospectus contains important information about the Fund's objective, investment policies, strategies and risks. It also contains important information about how to buy and sell shares of the Fund and other account features. Please read this prospectus carefully before you invest and keep it for future reference about your account. |

| As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved the Fund's securities nor has it determined that this prospectus is accurate or complete. It is a criminal offense to represent otherwise. |

|

|

|

Oppenheimer Equity Income Fund, Inc. |

| Table of contents | |

|

3 |

|

|

3 |

|

|

3 |

|

|

4 |

|

|

5 |

|

|

5 |

|

|

5 |

|

|

5 |

|

|

6 |

|

|

Payments to Broker-Dealers and Other Financial Intermediaries |

6 |

|

7 |

|

|

9 |

|

|

10 |

|

|

10 |

|

|

15 |

|

|

16 |

|

|

22 |

|

|

23 |

To Summary Prospectus

THE FUND SUMMARY

Investment Objective. The Fund seeks total return.

Fees and Expenses of the Fund. This table describes the fees and expenses that you may pay if you buy and hold or redeem shares of the Fund. You may qualify for sales charge discounts if you (or you and your spouse) invest, or agree to invest in the future, at least $25,000 in certain funds in the Oppenheimer family of funds. More information about these and other discounts is available from your financial professional and in the section "About Your Account" beginning on page __ of the prospectus and in the sections "How to Buy Shares" beginning on page __ and "Appendix A" in the Fund's Statement of Additional Information.

|

Shareholder Fees (fees paid directly from your investment) |

||||||

|

Class A |

Class B |

Class C |

Class N |

Class Y |

Class I |

|

|

Maximum Sales Charge (Load) imposed on purchases (as % of offering price) |

5.75% |

None |

None |

None |

None |

None |

|

Maximum Deferred Sales Charge (Load) (as % of the lower of original offering price or redemption proceeds) |

None |

5% |

1% |

1% |

None |

None |

|

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||

|

Class A |

Class B |

Class C |

Class N |

Class Y |

Class I1 |

|

|

Management Fees |

% |

% |

% |

% |

% |

|

|

Distribution and/or Service (12b-1) Fees |

% |

% |

% |

% |

% |

|

|

Other Expenses |

% |

% |

% |

% |

% |

|

|

Total Annual Fund Operating Expenses |

% |

% |

% |

% |

% |

|

|

Fee Waiver and Expense Reimbursement |

% |

% |

% |

% |

% |

|

|

Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement2 |

% |

% |

% |

% |

% |

|

1. Estimated expenses for the first full year that Class I shares are offered. Class I shares will first be offered on the date of this prospectus.

2. The Fund's transfer agent has voluntarily agreed to limit its fees for all classes, except Class A and I, to 0.35% of average annual net assets per class per fiscal year end, and to 0.30% of average net assets per fiscal year for Class A. This limitation may not be amended or withdrawn until one year after the date of this prospectus.

Example. The following Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in a class of shares of the Fund for the time periods indicated. The Example also assumes that your investment has a 5% return each year and that the Fund's operating expenses remain the same. Although your actual costs may be higher or lower, based on these

assumptions your expenses would be as follows:

| If shares are redeemed | If shares are not redeemed | |||||||||||||||||||||||||

| 1 Year | 3 Years | 5 Years | 10 Years | 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||||||||

| Class A | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Class B | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Class C | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Class N | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Class Y | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

| Class I* | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

* Based on estimated expenses for Class I shares for the first fiscal year.

Portfolio Turnover. The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was __% of the average value of its portfolio.

Principal Investment Strategies. The Fund mainly invests in common stocks of U.S. companies that the portfolio manager believes are undervalued. Under normal circumstances, the Fund will invest at least 80% of its assets in equity securities. The Fund may invest in other equity securities, such as preferred stocks, warrants and securities convertible into common stocks. The Fund may invest in equity securities issued by companies of different capitalization ranges, but will typically focus on larger capitalization stocks. The Fund may invest in equity securities both for current income from dividends as well as for growth opportunities.

The Fund can buy securities of companies in developed and emerging market countries. The Fund has no limits on the amounts it can invest in foreign securities. However, currently it does not intend to invest more than 25% of its net assets in securities of issuers in any single foreign country or more than 5% of its net assets in companies or government issuers in emerging market countries.

In selecting investments for the Fund, the portfolio manager mainly relies on a value-oriented investing style. A security may be undervalued because the market is not aware of the issuer's intrinsic value, does not yet recognize its future potential, or the issuer may be temporarily out of favor. The Fund seeks to realize gains in the prices of those securities when other investors recognize their real or prospective worth. The Fund also looks for securities that offer higher than average dividends. The portfolio manager generally uses a fundamental approach to analyzing issuers, for example, by looking at price/earnings ratios and current balance sheet information. Currently, the portfolio manager focuses on securities that have high current income and are believed to have substantial earnings possibilities, have low price/earnings ratios relative to other securities, and that have a low price relative to the underlying value of the issuer's assets, earnings, cash flow or other factors. These criteria may vary in particular cases and may change over time. The Fund may sell securities that the portfolio manager believes no longer meet these criteria, but is not required to do so.

Principal Risks. The price of the Fund's shares can go up and down substantially. The value of the Fund's investments may change because of broad changes in the markets in which the Fund invests or because of poor security selection, which could cause the Fund to underperform other funds with similar investment objectives. There is no assurance that the Fund will achieve its investment objective. When you redeem your shares, they may be worth more or less than what you paid for them. These risks mean that you can lose money by investing in the Fund.

Main Risks of Investing in Stock. The value of the Fund's portfolio may be affected by changes in the stock markets. Stock markets may experience significant short-term volatility and may fall sharply at times. Different stock markets may behave differently from each other and U.S. stock markets may move in the opposite direction from one or more foreign stock markets.

The prices of individual stocks generally do not all move in the same direction at the same time and a variety of factors can affect the price of a particular company's stock. These factors may include, but are not limited to: poor earnings reports, a loss of customers, litigation against the company, general unfavorable performance of the company's sector or industry, or changes in government regulations affecting the company or its industry.

At times, the Fund may emphasize investments in a particular industry or economic or market sector. To the extent that the Fund increases its emphasis on investments in a particular industry or sector, the value of its investments may fluctuate more in response to events affecting that industry or sector, such as changes in economic conditions, government regulations, availability of basic resources or supplies, or other events that affect that industry

or sector more than others.

Main Risks of Other Equity Securities. Most convertible securities are subject to the risks and price fluctuations of the underlying stock. They may be subject to the risk that the issuer will not be able to pay interest or dividends when due and their market value may change based on changes in the issuer's credit rating or the market's perception of the issuer's creditworthiness. Some convertible preferred stocks have a conversion or call feature that allows the issuer to redeem the stock before the conversion date, which could diminish the potential for capital appreciation on the investment. The fixed dividend rate of preferred stocks may cause their prices to behave more like those of debt securities. If interest rates rise, the value of preferred stock having a fixed dividend rate tends to fall. Preferred stock generally rank behind debt securities in claims for dividends and assets of the issuer in a liquidation or bankruptcy. The price of a warrant does not necessarily move parallel to the price of the underlying security and is generally more volatile than that of the underlying security. Rights are similar to warrants, but normally have a shorter duration. The market for rights or warrants may be very limited and it may be difficult to sell them promptly at an acceptable price. Rights and warrants have no voting rights, receive no dividends and have no rights with respect to the assets of the issuer.

Main Risks of Small- and Mid-Sized Companies. The stock prices of small- and mid-sized companies may be more volatile and their securities may be more difficult to sell than those of larger companies. They may not have established markets, may have fewer customers and product lines, may have unseasoned management or less management depth and may have more limited access to financial resources. Smaller companies may not pay dividends or provide capital gains for some time, if at all.

Main Risks of Value Investing. Value investing entails the risk that if the market does not recognize that the Fund's securities are undervalued, the prices of those securities might not appreciate as anticipated. A value approach could also result in fewer investments that increase rapidly during times of market gains and could cause the Fund to underperform funds that use a growth or non-value approach to investing. Value investing has gone in and out of favor during past market cycles and when value investing is out of favor or when markets are unstable, the securities of "value" companies may underperform the securities of "growth" companies.

Dividend Risk. There is no guarantee that the issuers of the stocks held by the Fund will declare dividends in the future or that, if dividends are declared, they will remain at their current levels or increase over time. High-dividend stocks may not experience high earnings growth or capital appreciation. The Fund's performance during a broad market advance could suffer because dividend paying stocks may not experience the same capital appreciation as non-dividend paying stocks.

Main Risks of Foreign Investing. Foreign securities are subject to special risks. Foreign issuers are usually not subject to the same accounting and disclosure requirements that U.S. companies are subject to, which may make it difficult for the Fund to evaluate a foreign company's operations or financial condition. A change in the value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency and in the value of any income or distributions the Fund may receive on those securities. The value of foreign investments may be affected by exchange control regulations, foreign taxes, higher transaction and other costs, delays in the settlement of transactions, changes in economic or monetary policy in the United States or abroad, expropriation or nationalization of a company's assets, or other political and economic factors. These risks may be greater for investments in developing or emerging market countries.

Time-Zone Arbitrage. The Fund may invest in securities of foreign issuers that are traded in U.S. or foreign markets. If the Fund invests a significant amount of its assets in foreign markets, it may be exposed to "time-zone arbitrage" attempts by investors seeking to take advantage of differences in the values of foreign securities that might result from events that occur after the close of the foreign securities market on which a security

is traded and before the Fund's net asset value is calculated. If such time-zone arbitrage were successful, it might dilute the interests of other shareholders. The Fund's use of "fair value pricing" to adjust certain market prices of foreign securities may help deter those activities.

The above risks may be greater for investments in emerging or developing market countries. While the Fund has no limits on the amounts it can invest in foreign securities, currently it does not intend to invest more than 25% of its net assets in securities of issuers in any single foreign country or more than 5% of its net assets in companies or government issuers in emerging market countries.

Who Is the Fund Designed For? The Fund is designed primarily for investors seeking total return from capital appreciation and income over the long term. Those investors should be willing to assume the risks of short-term share price fluctuations and losses that are typical for a fund emphasizing investments in equity securities. Since the Fund's income level will fluctuate, it is not designed for investors needing an assured level of current income. The Fund is not a complete investment program. You should carefully consider your own investment goals and risk tolerance before investing in the Fund.

|

An investment in the Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. |

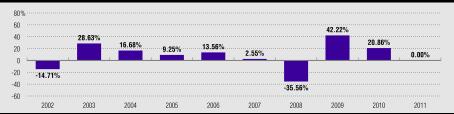

The Fund's Past Performance. The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund's performance from year to year and by showing how the Fund's average annual returns for 1, 5 and 10 years compare with those of a broad measure of market performance. The Fund's past investment performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. More

recent performance information is available by calling the toll-free number on the back of this prospectus and on the Fund's website:

https://www.oppenheimerfunds.com/fund/investors/overview/EquityIncomeFundInc

|

|

Sales charges and taxes are not included and the returns would be lower if they were. During the period shown, the highest return for a calendar quarter was % () and the lowest return was % (). For the period from January 1, 2011 to December 31, 2011 the cumulative return before taxes was %.

The following table shows the average annual total returns for each class of the Fund's shares. After-tax returns are calculated using the highest individual federal marginal income tax rates and do not reflect the impact of state or local taxes. Your actual after-tax returns, depending on your individual tax situation, may differ from those shown and after-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown for only one class and after-tax returns for other classes will vary.

Performance information for Class I shares is not provided because those shares were not available prior to the date of this prospectus.

|

Average Annual Total Returns for the periods ended December 31, 2011 |

||||||

|

1 Year |

5 Years (or life of class, if less) |

10 Years (or life of class, if less) |

||||

|

Class A Shares (inception 2/13/87) |

||||||

|

Return Before Taxes |

% |

% |

% |

|||

|

Return After Taxes on Distributions |

% |

% |

% |

|||

|

Return After Taxes on Distributions and Sale of Fund Shares |

% |

% |

% |

|||

|

Class B Shares (inception 3/03/97) |

% |

% |

% |

|||

|

Class C Shares (inception 3/03/97) |

% |

% |

% |

|||

|

Class N Shares (inception 3/01/01) |

% |

% |

% |

|||

|

Class Y Shares (inception 2/28/11) |

||||||

|

Russell 1000 Value Index |

% |

% |

% |

|||

|

(reflects no deduction for fees, expenses or taxes) |

%* |

|||||

|

S&P 500 Index |

% |

% |

% |

|||

|

(reflects no deduction for fees, expenses or taxes) |

%* |

|||||

* From 02-28-01

Investment Adviser. OppenheimerFunds, Inc. is the Fund's investment adviser (the "Manager").

Portfolio Manager. Michael S. Levine has been Vice President and portfolio manager of the Fund since July 2007.

Purchase and Sale of Fund Shares. You can buy most classes of Fund shares with a minimum initial investment of $1,000 and make additional investments with as little as $50. For certain investment plans and retirement accounts, the minimum initial investment is $500 and, for some, the minimum additional investment is $25. For certain fee based programs the minimum initial investment is $250. For Class I shares, the minimum initial investment is $5 million per account. The Class I share minimum initial investment will be waived for retirement plan service provider platforms.

Shares may be purchased through a financial intermediary or the Distributor and redeemed through a financial intermediary or the Transfer Agent on days the New York Stock Exchange is open for trading. Shareholders may purchase or redeem shares by mail, through the website at www.oppenheimerfunds.com or by calling 1.800.225.5677. Share transactions may be paid by check, by Federal Funds wire or directly from or into your bank account.

Taxes. If your shares are not held in a tax-deferred account, Fund distributions are subject to Federal income tax as ordinary income or as capital gains and they may also be subject to state or local taxes.

Payments to Broker-Dealers and Other Financial Intermediaries. If you purchase Fund shares through a broker-dealer or other financial intermediary (such as a bank), the Fund, the Manager, or their related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

MORE ABOUT THE FUND

The allocation of the Fund's portfolio among different types of investments will vary over time and the Fund's portfolio might not always include all of the different types of investments described below. The Statement of Additional Information contains more detailed information about the Fund's investment policies and risks.

The Fund's Principal Investment Strategies and Risks. The following strategies and types of investments are the ones that the Fund considers to be the most important in seeking to achieve its investment objective and the following risks are those the Fund expects its portfolio to be subject to as a whole.

Common Stock and Other Equity Investments. Equity securities include common stock, preferred stock, rights, warrants and certain debt securities that are convertible into common stock. Equity investments may be exchange-traded or over-the-counter securities. Common stock represents an ownership interest in a company. It ranks below preferred stock and debt securities in claims for dividends and in claims for assets of the issuer in a liquidation or bankruptcy.

Preferred stock has a set dividend rate and ranks ahead of common stocks and behind debt securities in claims for dividends and for assets of the issuer in a liquidation or bankruptcy. The dividends on preferred stock may be cumulative (they remain a liability of the company until paid) or non-cumulative. The fixed dividend rate of preferred stocks may cause their prices to behave more like those of debt securities. When interest rates rise, the value of preferred stock having a fixed dividend rate tends to fall.

A convertible security can be converted into or exchanged for a set amount of common stock of an issuer within a particular period of time at a specified price or according to a price formula. Convertible debt securities pay interest and convertible preferred stocks pay dividends until they mature or are converted, exchanged or redeemed. Some convertible debt securities may be considered "equity equivalents" because of the feature that makes them convertible into common stock. Convertible securities may offer the Fund the ability to participate in stock market movements while also seeking some current income. Convertible securities may provide more income than common stock but they generally provide less income than comparable non-convertible debt securities. Convertible debt securities are subject to credit and interest rate risk. Credit risk is the risk that the issuer of a security might not make interest and principal payments on the security as they become due. Interest rate risk is the risk that when prevailing interest rates fall, the values of already-issued debt securities generally rise; and when prevailing interest rates rise the values of already-issued debt secuirties generally fall, and they may be worth less than the amount the Fund paid for them. However, credit ratings of convertible securities that are considered to be equity equivalents generally have less impact on the value of the securities than they do for non-convertible debt securities.

Investing in Foreign Securities. The Fund may buy stocks and other equity securities of companies that are organized under the laws of a foreign country or that have a substantial portion of their operations or assets in a foreign country or countries, or that derive a substantial portion of their revenue or profits from businesses, investments or sales outside of the United States. The Fund may also invest in foreign securities that are represented in the United States securities markets by American Depository Receipts ("ADRs") or similar depository arrangements. The Fund may invest to a limited degree in companies in emerging markets, which have greater risks than companies in developed market countries, including: less developed trading markets, less market liquidity, less stable economies, less stable currencies, and greater risks of nationalization or government restrictions on foreign ownership or on withdrawing assets from the country. The Fund will hold foreign currency only in connection with buying and selling foreign securities.

Risks of Small- and Mid-Sized Companies. Small- and mid-sized companies may be either established or newer companies, including "unseasoned" companies that have been in operation for less than three years. While smaller companies might offer greater opportunities for gain than larger companies, they also may involve greater risk of loss. They may be more sensitive to changes in a company's earnings expectations and may experience more abrupt and erratic price movements. Smaller companies' securities often trade in lower volumes and in many instances, are traded over-the-counter or on a regional securities exchange, where the frequency and volume of trading is substantially less than is typical for securities of larger companies traded on national securities exchanges. Therefore, the securities of smaller companies may be subject to wider price fluctuations and it might be harder for the Fund to dispose of its holdings at an acceptable price when it wants to sell them. Small- and mid-sized companies may not have established markets for their products or services and may have fewer customers and product lines. They may have more limited access to financial resources and may not have the financial strength to sustain them through business downturns or adverse market conditions. Since small- and mid-sized companies typically reinvest a high proportion of their earnings in their business, they may not pay dividends for some time, particularly if they are newer companies. Smaller companies may have unseasoned management or less depth in management skill than larger, more established companies. They may be more reliant on the efforts of particular members of their management team and management changes may pose a greater risk to the success of the business. Securities of small, unseasoned companies may be particularly volatile, especially in the short term, and may have very limited liquidity. It may take a substantial period of time to realize a gain on an investment in a small- or mid-sized company, if any gain is realized at all.

Other Investment Strategies and Risks. The Fund can also use the investment techniques and strategies described below. The Fund might not use all of these techniques or strategies or might only use them from time to time.

Debt Securities. The Fund does not focus on debt securities as a principal investment strategy; however the Fund can also invest in debt securities, such as U.S. Government securities and domestic and foreign corporate and government bonds and debentures. The Fund may invest in debt securities to seek income, for liquidity or for hedging purposes.

The Fund's debt securities may be rated by nationally recognized statistical rating organizations such as Moody's Investors Services, Inc. or Standard & Poor's Ratings Services or may be unrated. "Investment-grade" refers to securities that are rated in one of the top four rating categories. The Fund can also invest in debt securities that are rated below investment grade, also referred to as "junk bonds." Rating definitions of national rating agencies are described in Appendix B to the Statement of Additional Information.

Master Limited Partnerships. The Fund may invest in publicly traded limited partnerships known as "master limited partnerships" or MLPs. MLPs issue units that are registered with the Securities and Exchange Commission and are freely tradable on a securities exchange or in the over-the-counter market. An MLP consists of one or more general partners, who conduct the business, and one or more limited partners, who contribute capital. The Fund, as a limited partner, normally would not be liable for the debts of the MLP beyond the amounts the Fund has contributed, but would not be shielded to the same extent that a shareholder of a corporation would be. In certain circumstances creditors of an MLP would have the right to seek return of capital distributed to a limited partner. This right of an MLP's creditors would continue after the Fund sold its investment in the MLP. MLPs are typically real estate, oil and gas and equipment leasing vehicles, but they also finance movies, research and development, and other projects.

Diversification and Concentration. The Fund is a diversified fund. It attempts to reduce its exposure to the risks of individual securities by diversifying its investments across a broad number of different issuers. The Fund will not concentrate more than 25% of its total assets in issuers in any one industry. At times, however, the Fund may emphasize investments in some industries more than others.

Derivative Investments. The Fund can invest in "derivative" instruments. A derivative is an instrument whose value depends on (or is derived from) the value of an underlying security, asset, interest rate, index or currency. Derivatives may allow the Fund to increase or decrease its exposure to certain markets or risks.

The Fund may use derivatives to seek to increase its investment return or for hedging purposes. The Fund is not required to use derivatives in seeking its investment objective or for hedging and might not do so.

Options, futures and forward contracts are some of the types of derivatives the Fund can use. The Fund may also use other types of derivatives that are consistent with its investment strategies or for hedging purposes.

"Structured" Notes. "Structured" notes are specially-designed derivative debt instruments. The terms of the instrument may be determined or "structured" by the purchaser and the issuer of the note. Payments of principal or interest on these notes may be linked to the value of an index (such as a currency or securities index), one or more securities, a commodity or the financial performance of one or more obligors. The value of these notes will normally rise or fall in response to the changes in the performance of the underlying security, index, commodity or obligor.

Risks of Structured Notes. Structured notes are subject to interest rate risk. They are also subject to credit risk with respect both to the issuer and, if applicable, to the underlying security or obligor. If the underlying investment or index does not perform as anticipated, the structured note might pay less interest than the stated coupon payment or repay less principal upon maturity. The price of structured notes may be very volatile and they may have a limited trading market, making it difficult to value them or sell them at an acceptable price. In some cases, the Fund may enter into agreements with an issuer of structured notes to purchase a minimum amount of those notes over time.Hedging. Hedging transactions are intended to reduce the risks of securities in the Fund's portfolio. At times, however, a hedging instrument's value might not be correlated with the investment it is intended to hedge, and the hedge might be unsuccessful. If the Fund uses a hedging instrument at the wrong time or judges market conditions incorrectly, the strategy could reduce its return or create a loss.

Risks of Derivative Investments. Derivatives may be volatile and may involve significant risks. The underlying security, obligor or other instrument on which a derivative is based, or the derivative itself, may not perform the way the Manager expects it to. The Fund may lose money on a derivative investment if the issuer or counterparty fails to pay the amount due. Certain derivative investments held by the Fund may be illiquid, making it difficult to close out an unfavorable position. Derivative transactions may require the payment of premiums and can increase portfolio turnover. As a result, the Fund could realize little or no income or lose principal from the investment, or a hedge might be unsuccessful. For some derivatives, it is possible for the Fund to lose more than the amount invested in the derivative instrument. Some derivatives have the potential for unlimited loss, regardless of the size of the Fund's initial investment.

Illiquid and Restricted Securities. Investments that do not have an active trading market, or that have legal or contractual limitations on their resale, are generally referred to as "illiquid" securities. Illiquid securities may be difficult to value or to sell promptly at an acceptable price or may require registration under applicable securities laws before they can be sold publicly. Securities that have limitations on their resale are referred to as "restricted securities." Certain restricted securities that are eligible for resale to qualified institutional purchasers may not be regarded as illiquid.

The Fund will not invest more than 10% of its net assets in illiquid or restricted securities. The Board can increase that limit to 15%. The Manager monitors the Fund's holdings of illiquid securities on an ongoing basis to determine whether to sell any of those securities to maintain adequate liquidity.

Conflicts of Interest. The investment activities of the Manager and its affiliates in regard to other funds and accounts they manage may present conflicts of interest that could disadvantage the Fund and its shareholders. The Manager or its affiliates may provide investment advisory services to other funds and accounts that have investment objectives or strategies that differ from, or are contrary to, those of the Fund. That may result in another fund or account holding investment positions that are adverse to the Fund's investment strategies or activities. Other funds or accounts advised by the Manager or its affiliates may have conflicting interests arising from investment objectives that are similar to those of the Fund. Those funds and accounts may engage in, and compete for, the same types of securities or other investments as the Fund or invest in securities of the same issuers that have different, and possibly conflicting, characteristics. The trading and other investment activities of those other funds or accounts may be carried out without regard to the investment activities of the Fund and, as a result, the value of securities held by the Fund or the Fund's investment strategies may be adversely affected. The Fund's investment performance will usually differ from the performance of other accounts advised by the Manager or its affiliates and the Fund may experience losses during periods in which other accounts advised by the Manager or its affiliates achieve gains. The Manager has adopted policies and procedures designed to address potential conflicts of interest identified by the Manager; however, such policies and procedures may also limit the Fund's investment activities and affect its performance.

Investments in Oppenheimer Institutional Money Market Fund. The Fund can invest its free cash balances in Class E shares of Oppenheimer Institutional Money Market Fund to provide liquidity or for defensive purposes. The Fund invests in Oppenheimer Institutional Money Market Fund, rather than purchasing individual short-term investments, to seek a higher yield than it could obtain on its own. Oppenheimer Institutional Money Market Fund is a registered open-end management investment company, regulated as a money market fund under the Investment Company Act of 1940, and is part of the Oppenheimer family of funds. It invests in a variety of short-term, high-quality, dollar-denominated money market instruments issued by the U.S. Government, domestic and foreign corporations, other financial institutions, and other entities. Those investments may have a higher rate of return than the investments that would be available to the Fund directly. At the time of an investment, the Fund cannot always predict what the yield of the Oppenheimer Institutional Money Market Fund will be because of the wide variety of instruments that fund holds in its portfolio. The return on those investments may, in some cases, be lower than the return that would have been derived from other types of investments that would provide liquidity. As a shareholder, the Fund will be subject to its proportional share of the expenses of Oppenheimer Institutional Money Market Fund's Class E shares, including its advisory fee. However, the Manager will waive a portion of the Fund's advisory fee to the extent of the Fund's share of the advisory fee paid to the Manager by Oppenheimer Institutional Money Market Fund.

Temporary Defensive and Interim Investments. For temporary defensive purposes in times of adverse or unstable market, economic or political conditions, the Fund can invest up to 100% of its total assets in investments that may be inconsistent with the Fund's principal investment strategies. Generally, the Fund would invest in shares of Oppenheimer Institutional Money Market Fund or in the types of money market instruments in which Oppenheimer Institutional Money Market Fund invests or in other short-term U.S. Government securities. The Fund might also hold these types of securities as interim investments pending the investment of proceeds from the sale of Fund shares or the sale of Fund portfolio securities or to meet anticipated redemptions of Fund shares. To the extent the Fund invests in these securities, it might not achieve its investment objective.

Portfolio Turnover. A change in the securities held by the Fund is known as "portfolio turnover." The Fund may engage in active and frequent trading to try to achieve its investment objective and may have a portfolio turnover rate of over 100% annually. Increased portfolio turnover may result in higher brokerage fees or other transaction costs, which can reduce performance. If the Fund realizes capital gains when it sells investments, it generally must pay those gains to shareholders, increasing its taxable distributions. The Financial Highlights table at the end of this prospectus shows the Fund's portfolio turnover rates during past fiscal years.

Changes to the Fund's Investment Policies. The Fund's fundamental investment policies cannot be changed without the approval of a majority of the Fund's outstanding voting shares; however, the Fund's Board can change non-fundamental policies without a shareholder vote. Significant policy changes will be described in supplements to this prospectus. The Fund's investment objective is a fundamental policy. Other investment restrictions that are fundamental policies are listed in the Fund's Statement of Additional Information. An investment policy is not fundamental unless this prospectus or the Statement of Additional Information states that it is.

Portfolio Holdings. The Fund's portfolio holdings are included in its semi-annual and annual reports that are distributed to its shareholders within 60 days after the close of the applicable reporting period. The Fund also discloses its portfolio holdings in its Statements of Investments on Form N-Q, which are public filings that are required to be made with the Securities and Exchange Commission within 60 days after the end of the Fund's first and third fiscal quarters. Therefore, the Fund's portfolio holdings are made publicly available no later than 60 days after the end of each of its fiscal quarters. In addition, the Fund's portfolio holdings information, as of the end of each calendar month, may be posted and available on the Fund's website no sooner than 30 days after the end of each calendar month.

A description of the Fund's policies and procedures with respect to the disclosure of its portfolio holdings is available in the Fund's Statement of Additional Information.

THE MANAGER. OppenheimerFunds, Inc., the Manager, chooses the Fund's investments and handles its day-to-day business. The Manager carries out its duties, subject to the policies established by the Fund's Board of Directors, under an investment advisory agreement that states the Manager's responsibilities. The agreement sets the fees the Fund pays to the Manager and describes the expenses that the Fund is responsible to pay to conduct its business.

The Manager has been an investment adviser since 1960. The Manager is located at Two World Financial Center, 225 Liberty Street, 11th Floor, New York, New York 10281-1008.

Advisory Fees. Under the investment advisory agreement, the Fund pays the Manager an advisory fee, calculated on the daily net assets of the Fund, at an annual rate that declines on additional assets as the Fund grows: 0.70% of the first $400 million of net assets of the Fund, 0.68% of the next $400 million, 0.65% of the next $400 million, 0.60% of the next $400 million, 0.55% of the next $400 million, and 0.50% of net assets in excess of $2 billion. The Fund's advisory fee for the fiscal period ended October 31, 2011 was % of average annual net assets for each class of shares.

The Fund's transfer agent has voluntarily agreed to limit its fees for all classes, except Class A and I, to 0.35% of average annual net assets per class per fiscal year end, and to 0.30% of average net assets per fiscal year for Class A. This limitation may not be amended or withdrawn until one year after the date of this prospectus. The Manager has agreed to waive fees and/or reimburse Fund expenses in an amount equal to the indirect management fees incurred through the Fund's investment in Oppenheimer Institutional Money Market Fund. For the Fund's fiscal year ended October 31, 2011, those indirect fees were less than 0.01% of the Fund's average annual net assets. This undertaking may be amended or withdrawn at any time.

A discussion regarding the basis for the Board of Directors' approval of the Fund's investment advisory contract is available in the Fund's Annual Report to shareholders for the fiscal year ended October 31, 2011.

Portfolio Manager. The Fund's portfolio is managed by Michael Levine who is primarily responsible for the day-to-day management of the Fund's investments. Mr. Levine has been a Vice President and portfolio manager of the Fund since July 2007.

Mr. Levine has been a Vice President of the Manager since June 1998.

The Statement of Additional Information provides additional information about the portfolio manager's compensation, other accounts he manages and his ownership of Fund shares.

MORE ABOUT YOUR ACCOUNT

Where Can You Buy Fund Shares? Oppenheimer funds may be purchased either directly or through a variety of "financial intermediaries" that offer Fund shares to their clients. Financial intermediaries include securities dealers, financial advisors, brokers, banks, trust companies, insurance companies and the sponsors of fund "supermarkets," fee-based advisory or wrap fee programs or college and retirement savings programs.

|

WHAT CLASSES OF SHARES DOES THE FUND OFFER? The Fund offers investors six different classes of shares. The different classes of shares represent investments in the same portfolio of securities, but the classes are subject to different expenses and will usually have different share prices. When you buy shares, be sure to specify the class of shares you wish to purchase. If you do not choose a class, your investment will be made in Class A

shares. |

Certain sales charge waivers may apply to purchases or redemptions of Class A, Class B, Class C or Class N shares. More information about those waivers is available in the Fund's Statement of Additional Information, or by clicking on the hyperlink "Sales Charges & Breakpoints" under the heading "Fund Information" on the OppenheimerFunds website at "www.oppenheimerfunds.com."

What is the Minimum Investment. You can buy most Fund share classes with a minimum initial investment of $1,000. For Class I shares the minimum initial investment is $5 million. The Class I share minimum initial investment is waived for retirement plan service provider platforms. Reduced initial minimums are available for other share classes in certain circumstances, including under the following investment plans:

- For most types of retirement accounts that OppenheimerFunds offers, the minimum initial investment is $500.

- For certain retirement accounts that have automatic investments through salary deduction plans, there is no minimum initial investment.

- For an Asset Builder Plan or Automatic Exchange Plan or a government allotment plan, the minimum initial investment is $500.

- For certain fee-based programs that have an agreement with the Distributor, a minimum initial investment of $250 applies.

You can make additional investments with as little as $50. The minimum additional investment requirement does not apply to reinvested dividends from the Fund or other Oppenheimer funds, to omnibus account purchases or to Class I shares. A reduced additional investment minimum of $25 applies to purchases through an Asset Builder Plan, an Automatic Exchange Plan or a government allotment plan established before November 1, 2002.

Minimum Account Balance. A $12 annual "minimum balance fee" is assessed on Fund accounts with a value of less than $500. The fee is automatically deducted from each applicable Fund account annually in September. See the Statement of Additional Information for information about the circumstances under which this fee will not be assessed. Small accounts may be involuntarily redeemed by the Fund if the value has fallen below $500 for reasons other than a decline in the market value of the shares.

The minimum account balance for Class I shares is $2.5 million. If a Class I account balance falls below $2.5 million, the account may be involuntarily redeemed or converted into a Class Y share account. This minimum balance policy does not apply to accounts for which the minimum initial investment is waived.

Choosing a Share Class. Once you decide that the Fund is an appropriate investment for you, deciding which class of shares is best suited to your needs depends on a number of factors that you should discuss with your financial advisor. The Fund's operating costs that apply to a share class and the effect of the different types of sales charges on your investment will affect your investment results over time. For example, expenses such as the distribution or service fees will reduce the net asset value and the dividends on share classes that are subject to those expenses.

Two of the factors to consider are how much you plan to invest and, while future financial needs cannot be predicted with certainty, how long you plan to hold your investment. For example, with larger purchases that qualify for a reduced initial sales charge on Class A shares, the effect of paying an initial sales charge on purchases of Class A shares may be less over time than the effect of the distribution fees on other share classes. If your goals and objectives change over time and you plan to purchase additional shares, you should re-evaluate each of the factors to see if you should consider a different class of shares.

The discussion below is not intended to be investment advice or a recommendation, because each investor's financial considerations are different. The discussion below assumes that you will purchase only one class of shares and not a combination of shares of different classes. These examples are based on approximations of the effects of current sales charges and expenses projected over time, and do not detail all of the considerations in selecting a class of shares. You should analyze your options carefully with your financial advisor before making that choice.

- Investing for the Shorter Term. While the Fund is meant to be a long-term investment, if you have a relatively short-term investment horizon (that is, if you do not plan to hold your shares for six years or more), you should consider investing in Class C shares. That is because of the effect of the initial sales charge on Class A shares or the Class B contingent deferred sales charge if you redeem within six years.

- Investing for the Longer Term. If you are investing less than $100,000 for the longer term and do not expect to need access to your money for six years or more, Class B shares may be appropriate. However, please note that Class B shares will no longer be offered for sale after June 29, 2012, as described in "About Class B Shares" below.

- Amount of Your Investment. Your choice will also depend on how much you plan to invest. For shorter-term investments of less than $100,000, Class C shares might be the appropriate choice because there is no initial sales charge on Class C shares, and the contingent deferred sales charge does not apply to shares you redeem after holding them for one year or more. However, if you plan to invest more than $100,000, and as your investment horizon increases toward six years, Class C shares might not be as advantageous as Class A shares. That is because over time the ongoing asset-based sales charge on Class C shares will have a greater impact on your account than the reduced front-end sales charge available for Class A share purchases of $100,000 or more. For an investor who is eligible to purchase Class I shares, that share class will be the most advantageous. For other investors who invest $1 million or more, Class A shares will be the most advantageous choice in most cases, no matter how long you intend to hold your shares.

Are There Differences in Account Features That Matter to You? Some account features may not be available for all share classes. Other features may not be advisable because of the effect of the contingent deferred sales charge. Therefore, you should carefully review how you plan to use your investment account before deciding which class of shares to buy.

How Do Share Classes Affect Payments to Your Financial Intermediary? The Class B, Class C, and Class N contingent deferred sales charges and asset-based sales charges have the same purpose as the front-end sales charge or contingent deferred sales charge on Class A shares: to compensate the Distributor for concessions and expenses it pays to brokers, dealers and other financial intermediaries for selling Fund shares. Those financial intermediaries may receive different compensation for selling different classes of shares. The Manager or Distributor may also pay dealers or other financial intermediaries additional amounts from their own resources based on the value of Fund shares held by the intermediary for its own account or held for its customers' accounts. For more information about those payments, see "Payments to Financial Intermediaries and Service Providers" below.

About Class A Shares. Class A shares are sold at their offering price, which is the net asset value of the shares (described below) plus, in most cases, an initial sales charge. The Fund receives the amount of your investment, minus the sales charge, to invest for your account. In some cases, Class A purchases may qualify for a reduced sales charge or a sales charge waiver, as described below and in the Statement of Additional Information.

The Class A sales charge rate varies depending on the amount of your purchase. A portion or all of the sales charge may be retained by the Distributor or paid to your broker, dealer or other financial intermediary as a concession. The current sales charge rates and concessions paid are shown in the table below. There is no initial sales charge on Class A purchases of $1 million or more, but a contingent deferred sales charge (described below) may apply.

|

Amount of Purchase |

Front-End Sales Charge As a Percentage of Offering Price |

Front-End Sales Charge As a Percentage of Net Amount Invested |

Concession As a Percentage of Offering Price |

|||

|

Less than $25,000 |

5.75% |

6.10% |

4.75% |

|||

|

$25,000 or more but less than $50,000 |

5.50% |

5.82% |

4.75% |

|||

|

$50,000 or more but less than $100,000 |

4.75% |

4.99% |

4.00% |

|||

|

$100,000 or more but less than $250,000 |

3.75% |

3.90% |

3.00% |

|||

|

$250,000 or more but less than $500,000 |

2.50% |

2.56% |

2.00% |

|||

|

$500,000 or more but less than $1 million |

2.00% |

2.04% |

1.60% |

|||

Due to rounding, the actual sales charge for a particular transaction may be higher or lower than the rates listed above.

Reduced Class A Sales Charges. Under a "Right of Accumulation" or a "Letter of Intent" you may be eligible to buy Class A shares of the Fund at the reduced sales charge rate that would apply to a larger purchase. Purchases of "qualified shares" of the Fund and certain other Oppenheimer funds may be added to your Class A share purchases for calculating the applicable sales charge.

Class A, Class B and Class C shares of most Oppenheimer funds (including shares of the Fund), and Class A, Class B, Class C, Class G and Class H units owned in adviser sold Section 529 plans, for which the Manager or the Distributor serves as the "Program Manager" or "Program Distributor" are "qualified shares" for satisfying the terms of a Right of Accumulation or a Letter of Intent. Purchases of Class N, Class Y or Class I shares of Oppenheimer funds, purchases made by reinvestment of dividends or capital gains distributions, purchases under the "reinvestment privilege" described below, and purchases of Class A shares of Oppenheimer Money Market Fund, Inc. or Oppenheimer Cash Reserves on which a sales charge has not been paid do not count as "qualified shares" for those purposes. The Fund reserves the right to modify or to cease offering these programs at any time.

-

Right of Accumulation. To qualify for the reduced Class A sales charge that would apply to a larger purchase than you are currently making, you can add the value of qualified shares that you and your spouse currently own, and other qualified share purchases that you are currently making, to the value of your Class A share purchase of the Fund. The Distributor or the financial intermediary through which you are buying shares will determine the value of

the qualified shares you currently own based on the greater of their current offering price or the amount you paid for the shares. For purposes of calculating that value, the Distributor will only take into consideration the value of shares owned as of December 31, 2007 and any shares purchased subsequently. The value of any shares that you have redeemed will not be counted. In totaling your holdings, you may count shares held in:

- your individual accounts (including IRAs, 403(b) plans and eligible 529 plans),

- your joint accounts with your spouse,

- accounts you or your spouse hold as trustees or custodians on behalf of your children who are minors.

A fiduciary can apply a right of accumulation to all shares purchased for a trust, estate or other fiduciary account that has multiple accounts (including employee benefit plans for the same employer and Single K plans for the benefit of a sole proprietor).

If you are buying shares directly from the Fund, you must inform the Distributor of your eligibility and holdings at the time of your purchase in order to qualify for the Right of Accumulation. If you are buying shares through a financial intermediary you must notify the intermediary of your eligibility for the Right of Accumulation at the time of your purchase.

To count shares held in accounts at other firms, you may be requested to provide the Distributor or your current financial intermediary with a copy of account statements showing your current qualified share holdings. Shares purchased under a Letter of Intent may also qualify as eligible holdings under a Right of Accumulation.

- Letter of Intent. You may also qualify for reduced Class A sales charges by submitting a Letter of Intent to the Distributor. A Letter of Intent is a written statement of your intention to purchase a specified value of qualified shares over a 13-month period. The total amount of your intended purchases will determine the reduced sales charge rate that will apply to your Class A share purchases during that period. You must notify the Distributor or your financial intermediary of any qualifying 529 plan purchases or purchases through other financial intermediaries.

Submitting a Letter of Intent does not obligate you to purchase the specified amount of shares. If you do not complete the anticipated purchases, you will be charged the difference between the sales charge that you paid and the sales charge that would apply to the actual value of shares you purchased. A certain portion of your shares will be held in escrow by the Fund's Transfer Agent for this purpose. Please refer to "How to Buy Shares – Letters

of Intent" in the Fund's Statement of Additional Information for more complete information. You may also be able to apply the Right of Accumulation to purchases you make under a Letter of Intent.

Class A Contingent Deferred Sales Charge. Although there is no initial sales charge on Class A purchases of shares of one or more of the Oppenheimer funds totaling $1 million or more, those Class A shares may be subject to a 1.00% contingent deferred sales charge if they are redeemed within an 18-month "holding period" measured from the beginning of the calendar month in which they were purchased (except for shares purchased in certain retirement plans, as described below). That sales charge will be calculated on the lesser of the original net asset value of the redeemed shares at the time of purchase or the aggregate net asset value of the redeemed shares at the time of redemption.

The Class A contingent deferred sales charge does not apply to shares purchased by the reinvestment of dividends or capital gain distributions and will not exceed the aggregate amount of the concessions the Distributor pays on all of your purchases of Class A shares, of all Oppenheimer funds, that are subject to the contingent deferred sales charge.

The Distributor pays concessions from its own resources equal to 1.00% of Class A purchases of $1 million or more (other than purchases by certain retirement plans). The concession will not be paid on shares purchased by exchange or shares that were previously subject to a front-end sales charge and concession.

Class A Purchases by Certain Retirement Plans. There is no initial sales charge on purchases of Class A shares of the Fund by retirement plans that have $1 million or more in plan assets or by certain retirement plans or platforms offered through financial intermediaries or other service providers.

In addition, there is no contingent deferred sales charge on redemptions of certain Class A retirement plan shares offered through financial intermediaries or other service providers. There is no contingent deferred sales charge on redemptions of Class A group retirement plan shares except for shares of certain group retirement plans that were established prior to March 1, 2001 ("grandfathered retirement plans"). Shares purchased in grandfathered retirement plans are subject to the contingent deferred sales charge if they are redeemed within 18 months after purchase.

The Distributor does not pay a concession on Class A retirement plan purchases except on purchases by grandfathered retirement plans and plans that have $5 million or more in plan assets. The concession for grandfathered retirement plan purchases is 0.25%. For purchases of Class A shares by retirement plans that have $5 million or more in plan assets (within the first six months from the time the account was established), the Distributor may pay financial intermediaries concessions equal to 0.25% of the purchase price from its own resources at the time of sale. Those payments are subject to certain exceptions described in "Retirement Plans" in the Statement of Additional Information.

About Class B Shares. Class B shares are sold at net asset value per share without an initial sales charge. However, if Class B shares are redeemed within six years from the beginning of the calendar month in which they were purchased, a contingent deferred sales charge will be deducted from the redemption proceeds. Class B shares are also subject to an asset-based sales charge that is calculated daily based on an annual rate of 0.75%. The Class B contingent deferred sales charge and asset-based sales charge are paid to compensate the Distributor for providing distribution-related services to the Fund in connection with the sale of Class B shares.

The amount of the Class B contingent deferred sales charge will depend on the number of years since you invested, according to the following schedule:

|

Years since Beginning of Month in Which Purchase Order was Accepted |

Contingent Deferred Sales Charge on Redemptions in That Year (As % of Amount Subject to Charge) |

|

0-1 |

5.0% |

|

1-2 |

4.0% |

|

2-3 |

3.0% |

|

3-4 |

3.0% |

|

4-5 |

2.0% |

|

5-6 |

1.0% |

|

More than 6 |

None |

In the table, a "year" is a 12-month period. In applying the contingent deferred sales charge, all purchases are considered to have been made on the first regular business day of the month in which the purchase was made.

Automatic Conversion of Class B Shares. Class B shares automatically convert to Class A shares six years (72 months) after you purchase them. This conversion eliminates the Class B asset-based sales charge, however, the shares will be subject to the ongoing Class A fees and expenses. The conversion is based on the relative net asset value of the two classes, and no sales load or other charge is imposed. When any Class B shares that you hold convert to Class A shares, all other Class B shares that were acquired by reinvesting dividends and distributions on the converted shares will also convert.

Effective July 1, 2011, Class B shares held in certain retirement plan accounts were converted to Class A shares, or to another share class selected by the plan sponsor. For further information on the conversion feature and its tax implications, see "Class B Conversion" in the Statement of Additional Information.

Class B Shares Will No Longer Be Offered For Sale After June 29, 2012. Investors can continue to purchase Class B shares through June 29, 2012, but will need to designate a different share class for subsequent purchases, including for any automatic purchases. After June 29, 2012, Class B shares will continue to mature and convert to Class A shares according to their established conversion schedule. Dividend and/or capital gains distributions will continue to be made in Class B shares, and exchanges of Class B shares into and from accounts holding Class B shares will be permitted until the conversion to Class A shares.

About Class C Shares. Class C shares are sold at net asset value per share without an initial sales charge. However, if Class C shares are redeemed within a 12 month "holding period" from the beginning of the calendar month in which they were purchased, a contingent deferred sales charge of 1.00% may be deducted from the redemption proceeds. Class C shares are also subject to an asset-based sales charge that is calculated daily based on an annual rate of 0.75%. The Class C contingent deferred sales charge and asset-based sales charge are paid to compensate the Distributor for providing distribution-related services to the Fund in connection with the sale of Class C shares.

About Class N Shares. Class N shares are offered to retirement plans (including IRAs and 403(b) plans) that purchase $500,000 or more of Oppenheimer funds Class N shares or to group retirement plans (which do not include IRAs and 403(b) plans) held in omnibus accounts that have assets of $500,000 or more or have 100 or more eligible participants. See "Availability of Class N shares" in the Statement of Additional Information for other circumstances in which Class N shares are available for purchase.

Class N shares are sold at net asset value without an initial sales charge. Class N shares are subject to an asset-based sales charge that is calculated daily based on an annual rate of 0.25%. A contingent deferred sales charge of 1.00% will be imposed on the redemption of Class N shares, if:

- The group retirement plan is terminated, or Class N shares of all Oppenheimer funds are terminated as an investment option of the plan, and the Class N shares are redeemed within 18 months after the plan's first purchase of Class N shares of any Oppenheimer fund; or

- Class N shares are redeemed within 18 months after an IRA or 403(b) plan's first purchase of Class N shares of any Oppenheimer fund.

Retirement plans that offer Class N shares may impose charges on plan participant accounts. For more information about buying and selling shares through a retirement plan, see the section "Investment Plans and Services - Retirement Plans" below.

About Class Y Shares. Class Y shares are sold at net asset value per share without a sales charge directly to institutional investors that have special agreements with the Distributor for that purpose. They may include insurance companies, registered investment companies, employee benefit plans and Section 529 plans, among others.

An institutional investor that buys Class Y shares for its customers' accounts may impose charges on those accounts. The procedures for buying, selling, exchanging and transferring the Fund's other classes of shares (other than the time those orders must be received by the Distributor or Transfer Agent at their Colorado office) and some of the special account features available to investors buying other classes of shares do not apply to Class Y shares. Instructions for buying, selling, exchanging or transferring Class Y shares must be submitted by the institutional investor, not by its customers for whose benefit the shares are held.

Present and former officers, directors, trustees and employees (and their eligible family members) of the Fund, the Manager, its affiliates, its parent company and the subsidiaries of its parent company, and retirement plans established for the benefit of such individuals, are also permitted to purchase Class Y shares of the Fund.

About Class I Shares. Class I shares are only available to eligible institutional investors. To be eligible to purchase Class I shares, an investor must:

- make a minimum initial investment of $5 million or more (waived for retirement plan service provider platforms);

- trade through an omnibus, trust, or similar pooled account; and

- be an" institutional investor" which may include corporations; trust companies; endowments and foundations; defined contribution, defined benefit, and other employer sponsored retirement plans; retirement plan platforms; insurance companies; registered investment advisor firms; bank trusts; 529 college savings plans; and family offices.

Eligible Class I investors will not receive any commission payments, account servicing fees, recordkeeping fees, 12b-1 fees, transfer agent fees, so called "finder's fees," administrative fees or other similar fees on Class I shares. Class I shares are not available directly to individual investors. Individual shareholders who purchase Class I shares through retirement plans or other intermediaries will not be eligible to hold Class I shares outside of their respective retirement plan or intermediary platform.

Class I shares are sold at net asset value per share without a sales charge. An institutional investor that buys Class I shares for its customers' accounts may impose charges on those accounts. The procedures for buying, selling, exchanging and transferring the Fund's other classes of shares (other than the time those orders must be received by the Distributor or Transfer Agent at their Colorado office), and most of the special account features available to investors buying other classes of shares, do not apply to Class I shares.

The Price of Fund Shares. Shares may be purchased at their offering price which is the net asset value per share plus any initial sales charge that applies. Shares are redeemed at their net asset value per share less any contingent deferred sales charge that applies. The net asset value that applies to a purchase or redemption order is the next one calculated after the Distributor receives the order, in proper form as described in this prospectus, or after any agent appointed by the Distributor receives the order in proper form as described in this prospectus. Your financial intermediary can provide you with more information regarding the time you must submit your purchase order and whether the intermediary is an authorized agent for the receipt of purchase and redemption orders.

Net Asset Value. The Fund calculates the net asset value of each class of shares as of the close of the New York Stock Exchange (NYSE), on each day the NYSE is open for trading (referred to in this prospectus as a "regular business day"). The NYSE normally closes at 4:00 p.m., Eastern time, but may close earlier on some days.

The Fund determines the net assets of each class of shares by subtracting the class-specific expenses and the amount of the Fund's liabilities attributable to the share class from the value of the securities and other assets attributable to the share class. The Fund's "other assets" might include, for example, cash and interest or dividends from its portfolio securities that have been accrued but not yet collected. The Fund's securities are valued primarily on the basis of current market quotations.

The net asset value per share for each share class is determined by dividing the net assets of the class by the number of outstanding shares of that class.

Fair Value Pricing . If market quotations are not readily available or (in the Manager's judgment) do not accurately reflect the fair value of a security, or if after the close of the principal market on which a security held by the Fund is traded and before the time as of which the Fund's net asset value is calculated that day, an event occurs that the Manager learns of and believes in the exercise of its judgment will cause a material change in the value of that security from the closing price of the security on the principal market on which it is traded, that security may be valued by another method that the Board believes would more accurately reflect the security's fair value.

In determining whether current market prices are readily available and reliable, the Manager monitors the information it receives in the ordinary course of its investment management responsibilities. It seeks to identify significant events that it believes, in good faith, will affect the market prices of the securities held by the Fund. Those may include events affecting specific issuers (for example, a halt in trading of the securities of an issuer on an exchange during the trading day) or events affecting securities markets (for example, a foreign securities market closes early because of a natural disaster).

The Board has adopted valuation procedures for the Fund and has delegated the day-to-day responsibility for fair value determinations to the Manager's "Valuation Committee." Those determinations may include consideration of recent transactions in comparable securities, information relating to the specific security, developments in the markets and their performance, and current valuations of foreign or U.S. indices. Fair value determinations by the Manager are subject to review, approval and ratification by the Board at its next scheduled meeting after the fair valuations are determined.

The Fund's use of fair value pricing procedures involves subjective judgments and it is possible that the fair value determined for a security may be materially different from the value that could be realized upon the sale of that security. Accordingly, there can be no assurance that the Fund could obtain the fair value assigned to a security if it were to sell the security at approximately the same time at which the Fund determines its net asset value per share.

Pricing Foreign Securities. The Fund may use fair value pricing more frequently for securities primarily traded on foreign exchanges. Because many foreign markets close hours before the Fund values its foreign portfolio holdings, significant events, including broad market movements, may occur during that time that could potentially affect the values of foreign securities held by the Fund.

The Manager believes that foreign securities values may be affected by volatility that occurs in U.S. markets after the close of foreign securities markets. The Manager's fair valuation procedures therefore include a procedure whereby foreign securities prices may be "fair valued" to take those factors into account.

Because some foreign securities trade in markets and on exchanges that operate on weekends and U.S. holidays, the values of some of the Fund's foreign investments may change on days when investors cannot buy or redeem Fund shares.

Contingent Deferred Sales Charge. If you redeem shares during their applicable contingent deferred sales charge holding period, the contingent deferred sales charge generally will be deducted from the redemption proceeds. In some circumstances you may be eligible for one of the waivers described in "Sales Charge Waivers" below and in the "Special Sales Charge Arrangements and Waivers" Appendix to the Statement of Additional Information. You must advise the Transfer Agent or your financial intermediary of your eligibility for a waiver when you place your redemption request.

A contingent deferred sales charge will be based on the net asset value of the redeemed shares at the time of redemption or the original net asset value, whichever is lower. A contingent deferred sales charge is not imposed on:

- any increase in net asset value over the initial purchase price,

- shares purchased by the reinvestment of dividends or capital gains distributions, or

- shares eligible for a sales charge waiver (see "Sales Charge Waivers" below).

The Fund redeems shares in the following order:

- shares acquired by the reinvestment of dividends or capital gains distributions,

- other shares that are not subject to the contingent deferred sales charge, and

- shares held the longest during the holding period.

Sales Charge Waivers. The Fund and the Distributor offer the following opportunities to purchase shares without front-end or contingent deferred sales charges. The Fund reserves the right to amend or discontinue these programs at any time without prior notice.

- Dividend Reinvestment. Dividends or capital gains distributions may be reinvested in shares of the Fund, or any of the other Oppenheimer funds into which shares of the Fund may be exchanged, without a sales charge.

- Exchanges of Shares. There is no sales charge on exchanges of shares except for exchanges of Class A shares of Oppenheimer Money Market Fund, Inc. or Oppenheimer Cash Reserves on which you have not paid a sales charge.

- Reinvestment Privilege. There is no sales charge on reinvesting the proceeds from redemptions of Class A shares or Class B shares that occurred within the previous six months if you paid an initial or contingent deferred sales charge on the redeemed shares. This reinvestment privilege does not apply to reinvestment purchases made through automatic investment options. You must advise the Distributor, the Transfer Agent or your financial intermediary that you qualify for the waiver at the time you submit your purchase order.

How to Buy, Sell and Exchange Shares