UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

or

For the transition period from _______ to _______

Commission File Number 1-1687

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||||||||

| Registrant’s telephone number, including area code: | |||||||||||||||||

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by checkmark whether the registrant has submitted electronically every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| (Do not check if a smaller reporting company) | Emerging growth company | ||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The aggregate market value of common stock held by non-affiliates as of June 30, 2022, was $26,830 million.

As of January 31, 2023, 235,179,993 shares of the Registrant’s common stock, with a par value of $1.66 2/3 per share, were outstanding. As of that date, the aggregate market value of common stock held by non-affiliates was $30,608 million.

DOCUMENTS INCORPORATED BY REFERENCE

2022 PPG ANNUAL REPORT AND FORM 10-K 1

PPG INDUSTRIES, INC.

AND CONSOLIDATED SUBSIDIARIES

As used in this report, the terms “PPG,” “Company,” “Registrant,” “we,” “us” and “our” refer to PPG Industries, Inc., and its subsidiaries, taken as a whole, unless the context indicates otherwise.

TABLE OF CONTENTS

| Page | ||||||||

| Part I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Part III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Part IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2022 PPG ANNUAL REPORT AND FORM 10-K 2

Part I

Item 1. Business

PPG Industries, Inc. manufactures and distributes a broad range of paints, coatings and specialty materials. PPG was incorporated in Pennsylvania in 1883. PPG’s vision is to be the world’s leading coatings company by consistently delivering high-quality, innovative and sustainable solutions that customers trust to protect and beautify their products and surroundings.

PPG has a proud heritage with a demonstrated commitment to innovation, sustainability, community engagement and development of leading-edge paint, coatings and specialty materials technologies. Through dedication and industry-leading expertise, we solve our customers’ biggest challenges, collaborating closely to find the right path forward. PPG is a global leader with manufacturing facilities and equity affiliates in more than 70 countries.

PPG supplies paints, coatings and specialty materials to customers serving a wide array of end-uses, including industrial equipment and components; packaging material; aircraft and marine equipment; automotive original equipment; automotive refinish; pavement marking products; as well as coatings for other industrial and consumer products. PPG also serves commercial and residential new build and maintenance customers by supplying coatings to painting and maintenance contractors and directly to consumers for decoration and maintenance.

The coatings industry is highly competitive and consists of several large firms with global presence and many firms supplying local or regional markets. PPG competes in its primary markets with the world’s largest coatings companies, most of which have global operations, and with many regional coatings companies.

PPG’s business is comprised of two reportable business segments: Performance Coatings and Industrial Coatings as described below:

2022 PPG ANNUAL REPORT AND FORM 10-K 3

PERFORMANCE COATINGS

| Strategic Business Unit | Products | Primary Customers / End-uses | Main Distribution Methods | Primary Brands | ||||||||||

| Aerospace Coatings | Coatings, sealants, transparencies, transparent armor, adhesives, engineered materials, packaging and chemical management services for the aerospace industry | Commercial, military, regional jet and general aviation aircraft | Direct to customers and company-owned distribution network | PPG® | ||||||||||

| Architectural Coatings Americas and Asia Pacific | Paints, wood stains, adhesives and purchased sundries | Painting and maintenance contractors and consumers for decoration and maintenance of residential and commercial building structures | Company-owned stores, home centers and other regional or national consumer retail outlets, paint dealers, concessionaires, independent distributors and direct to consumers | PPG®, GLIDDEN®, COMEX®, OLYMPIC®, DULUX® (in Canada), PPG PITTSBURGH PAINTS®, MULCO®, FLOOD®, LIQUID NAILS®, SICO®, RENNER®, TAUBMANS®, WHITE KNIGHT®, BRISTOL® and HOMAX® | ||||||||||

| Architectural Coatings Europe, Middle East and Africa (EMEA) | SIGMA®, HISTOR®, SEIGNEURIE®, GUITTET®, PEINTURES GAUTHIER®, RIPOLIN®, JOHNSTONE’S®, LEYLAND®, PRIMALEX®, DEKORAL®, TRILAK®, PROMINENT PAINTS®, GORI®, BONDEX®, DANKE!® and TIKKURILA® | |||||||||||||

| Automotive Refinish Coatings | Coatings, solvents, adhesives, sealants, purchased sundries, software and putties | Automotive and commercial transport/fleet repair and refurbishing, light industrial coatings and specialty coatings for signs | Independent distributors and direct to customers | PPG®, SEM®, SPRINT® | ||||||||||

| Protective and Marine Coatings | Coatings and finishes for the protection of metals and structures | Metal fabricators, heavy duty maintenance contractors and manufacturers of ships, bridges and rail cars | Direct to customers, company-owned architectural coatings stores, independent distributors and concessionaires | PPG® | ||||||||||

| Traffic Solutions | Paints, thermoplastics, pavement marking products and other advanced technologies for pavement marking | Government, commercial infrastructure, painting and maintenance contractors | Direct to customers, government agencies and independent distributors | Ennis-Flint® | ||||||||||

| Segment Overview | This reportable business segment primarily supplies a variety of protective and decorative coatings, sealants and finishes along with pavement marking products, paint strippers, stains and related chemicals, as well as transparencies and transparent armor. | ||||

| Alliances | PPG has an established alliance with Asian Paints Ltd. to serve certain automotive refinish customers in India. | ||||

| Major Competitive Factors | Product performance, technology, quality, technical and customer service, price, customer productivity, distribution and brand recognition | ||||

| Global Competitors | Akzo Nobel N.V., Axalta Coating Systems Ltd., BASF Corporation, Benjamin Moore, Hempel A/S, Kansai Paints, the Jotun Group, Masco Corporation, Nippon Paint, RPM International Inc., The Sherwin-Williams Company and 3M Company | ||||

| Principal Manufacturing and Distribution Facilities | Amsterdam, Netherlands; Birstall, United Kingdom; Busan, South Korea; Carrollton, Texas; Clayton, Australia; Delaware, Ohio; Deurne, Belgium; Ennis, Texas; Gonfreville, France; Greensboro, North Carolina; Huntsville, Alabama; Huron, Ohio; Kunshan, China; Little Rock, Arkansas; Mexico City, Mexico; Milan, Italy; Mojave, California; Nykvarn, Sweden; Oakwood, Georgia; Ontario, Canada; Ostrow Wielkopolski, Poland; Ruitz, France; Shildon, United Kingdom; Sylmar, California; Stowmarket, United Kingdom; Tepexpan, Mexico; Vantaa, Finland; and Wroclaw, Poland. | ||||

2022 PPG ANNUAL REPORT AND FORM 10-K 4

INDUSTRIAL COATINGS

| Strategic Business Unit | Products | Primary Customers / End-uses | Main Distribution Methods | Primary Brands | ||||||||||

Automotive OEM(a) Coatings | Specifically formulated coatings, adhesives and sealants and metal pretreatments | Automotive original equipment, including both combustion engine and electric vehicles, and automotive parts and accessories, including battery-related components | Direct to manufacturing companies and various coatings applicators | PPG® | ||||||||||

| Industrial Coatings | Specifically formulated coatings, adhesives and sealants and metal pretreatments; services and coatings application | Appliances, agricultural and construction equipment, consumer electronics, building products (including residential and commercial construction), kitchenware, transportation vehicles and numerous other finished products; On-site coatings services within several customer manufacturing locations as well as at regional service centers. | PPG® | |||||||||||

| Packaging Coatings | Specifically formulated coatings | Metal cans, closures, and plastic tubes for food, beverage and personal care, and promotional and specialty packaging | PPG® | |||||||||||

| Specialty Coatings and Materials | Amorphous precipitated silicas, TESLIN® substrate, Organic Light Emitting Diode (OLED) materials, optical lens materials and photochromic dyes | Silicas - Tire, battery separator and other end-uses TESLIN - Labels, e-passports, drivers’ licenses, breathable membranes, loyalty cards and identification cards OLED - displays and lighting Lens materials - optical lenses and color-change products | PPG® TESLIN® | |||||||||||

(a) Original equipment manufacturer (OEM)

| Segment Overview | This reportable business segment primarily supplies a variety of protective and decorative coatings and finishes along with adhesives, sealants, metal pretreatment products, optical monomers and coatings, low-friction coatings, precipitated silicas and other specialty materials. | ||||

| Alliances | PPG has established alliances with Kansai Paints to serve Japanese-based automotive OEM customers in North America and Europe and Asian Paints Ltd. to serve certain aftermarket customers and automotive OEM customers in India. | ||||

| Major Competitive Factors | Product performance, technology, quality, technical and customer service, price, customer productivity and distribution. | ||||

| Global Competitors | Akzo Nobel N.V., Axalta Coating Systems Ltd., BASF Corporation, Kansai Paints, Nippon Paint and The Sherwin-Williams Company | ||||

| Principal Manufacturing and Distribution Facilities | Barberton, Ohio; Busan, South Korea; Cieszyn, Poland; Cleveland, Ohio; Delfzijl, Netherlands; Lake Charles, Louisiana; Oak Creek, Wisconsin; Quattordio, Italy; San Juan del Rio, Mexico; Springdale, Pennsylvania; Sumaré, Brazil; Weingarten, Germany; and Suzhou, Tianjin and Zhangjiagang, China. | ||||

2022 PPG ANNUAL REPORT AND FORM 10-K 5

Research and Development

| ($ in millions, except percentages) | 2022 | 2021 | 2020 | ||||||||||||||

| Research and development costs, including depreciation of research facilities | $470 | $463 | $401 | ||||||||||||||

| % of annual net sales | 2.7 | % | 2.8 | % | 2.9 | % | |||||||||||

Technology innovation has been a hallmark of PPG’s success throughout its history. The Company seeks to optimize its investment in research and development to create new products to drive profitable growth. We align our product development with the macro trends in the markets we serve, including a focus on sustainability, and leverage core technology platforms to develop products to address unmet market needs. Additionally, we operate laboratories in close geographic proximity to our customers and we customize our products for our customers' end-use applications. Our history of successful technology introductions is based on a commitment to an efficient and effective innovation process and disciplined portfolio management. We have obtained government funding for a small portion of the Company’s research efforts, and we will continue to pursue government funding, where appropriate.

We own and operate several facilities to conduct research and development for new and improved products and processes. In addition to the Company’s centralized principal research and development centers (see Item 2. “Properties” of this Form 10-K), operating segments manage their development through centers of excellence. As part of our ongoing efforts to manage our formulations and raw material costs effectively, we operate global competitive sourcing laboratories. Because of our broad array of products and customers, we are not materially dependent upon any single technology platform.

Raw Materials, Energy and Logistics

PPG uses a wide variety of complex raw materials that serve as the building blocks of our manufactured products. The Company’s most significant raw materials include resins, reactants, solvents, titanium dioxide, epoxy and emulsions. Raw materials include both organic, primarily petroleum-derived, materials and inorganic materials. Raw materials represent PPG’s single largest production cost component.

Most of the raw materials and energy used in production are purchased from outside sources, and the Company has made, and continues to make, supply arrangements to meet our planned operating requirements for the future. Supply of critical raw materials and energy is managed by establishing contracts with multiple sources and identifying alternative materials or technology whenever possible. In support of our decarbonization efforts, we are increasing the amount of renewable energy secured for our operating facilities and increasingly evaluating alternative raw materials that offer sustainable benefits and support the circular economy, including recycled, bio-based, bio-circular feedstocks and biomass balance products. Prices for certain of our raw materials typically fluctuate with energy prices and global supply and demand changes; however, pricing may be impacted by the fact that the manufacture of our raw materials is several steps downstream from crude oil, natural gas, and other key feedstocks.

Through effective management of raw materials, energy and logistics, the Company aims to maintain a competitive cost position and ensure ongoing security of supply. Security of a sufficient supply of high-quality raw materials is important to PPG’s continued success as it allows the Company to increase production as necessary to keep pace with customer demand. In 2022, we continued to experience shortages of certain raw materials, which negatively impacted our ability to fully meet some of our customers’ demand. We continue to focus on improving our competitive cost position and expanding our supply of high-quality raw materials, including strategic initiatives to qualify multiple sources of supply.

We typically experience fluctuating prices for energy and raw materials driven by various factors, including changes in supplier feedstock costs and inventories, global industry activity levels, foreign currency exchange rates, government regulation, and global supply and demand factors. For 2022 versus 2021, we experienced increases in our operating costs of more than $1 billion, including significant raw material and energy cost inflation. The increases in raw material costs were primarily driven by higher supplier feedstock costs, higher energy prices, labor availability challenges, transportation shortages and higher ocean freight costs. Also in 2022, we experienced increases in other logistics costs, driven by supply chain disruptions, logistical challenges, labor shortages and manufacturing interruptions at both our factories and those of our suppliers and customers.

Given the uncertainty associated with the various factors that drive raw material prices, we are not able to predict the 2023 full-year impact of changes in raw material costs versus 2022; however, we expect the negative impact of raw material inflation to lessen as 2023 progresses.

We are subject to existing and evolving standards relating to the regulation and registration of chemicals which could potentially impact the availability and viability of some of the raw materials we use in our production processes. Our ongoing, global product stewardship efforts are directed at maintaining our compliance with these standards. We anticipate that the number of chemical registration regulations will continue to increase globally, and we have implemented programs to track and comply with these regulations.

2022 PPG ANNUAL REPORT AND FORM 10-K 6

Our commitment to sustainability extends to our suppliers as an extension of our internal focus on sustainability. The PPG Global Supplier Code of Conduct clarifies our global expectations in the areas of business integrity, labor practices, associate health and safety, and environmental management. Our Supplier Sustainability Policy builds upon our Global Supplier Code of Conduct by establishing expectations for sustainability within our supply chain. This policy reinforces our expectations that our suppliers, as well as their subcontractors, will comply fully with applicable laws and adhere to internationally recognized environmental, social and corporate-governance standards.

In both 2022 and 2021, PPG earned a Gold rating from EcoVadis™, a trusted business sustainability ratings platform. EcoVadis experts evaluate company performance on 21 factors related to environment, labor and human rights, ethics, and sustainable procurement. The rating methodology is based on international sustainability standards and initiatives, such as the Global Reporting Initiative (GRI) Standards, United Nations Global Compact and ISO 26000 standard (social responsibility). Maintaining a Gold rating from EcoVadis underscores PPG’s ongoing commitment to corporate social responsibility and our efforts to manage our economic, social and environmental impact.

Global Operations

PPG has a significant investment in non-U.S. operations. This broad geographic footprint serves to lessen the significance to us of economic impacts occurring in any one region of the world. As a result of our global footprint, we are subject to certain inherent risks, including economic and political conditions in international markets, trade protection measures and fluctuations in foreign currency exchange rates. During 2022, unfavorable foreign currency translation decreased Net sales by approximately $775 million and Income before income taxes by approximately $85 million.

Refer to Note 20, “Revenue Recognition” in Item 8 of this Form 10-K for additional geographic information pertaining to sales and Note 21, “Reportable Business Segment Information” in Item 8 of this Form 10-K for geographic information related to PPG’s property, plant and equipment.

Seasonality

PPG’s Income before income taxes has typically been greater in the second and third quarters and Cash from operating activities has been greatest in the fourth quarter due to end-use market seasonality, primarily in our architectural coatings and traffic solutions businesses. Demand for our architectural coatings and traffic solutions products is typically the strongest in the second and third quarters due to higher home improvement, maintenance and construction activity during the spring and summer months in the U.S., Canada and Europe. The Latin American paint season is the strongest in the fourth quarter. These cyclical activity levels result in the collection of outstanding receivables and lower inventory on hand in the fourth quarter generating higher Cash from operating activities.

Human Capital

The average number of people employed by PPG during 2022 was approximately 52,000, of which approximately 15,600 were in the United States and approximately 36,400 were elsewhere in the world. The Company has numerous collective bargaining agreements throughout the world. We observe local customs, laws and practices in labor relations when negotiating collective bargaining agreements. There were no significant work stoppages in 2022. While we have experienced occasional work stoppages and may experience some work stoppages in the future, we believe that we will be able to negotiate all labor agreements on satisfactory terms. To date, these work stoppages have not had a significant impact on our results of operations. Overall, we believe we have good relationships with our employees.

The PPG Way is a set of behaviors that enables, empowers and engages each employee to fully live our values and realize our full potential as an organization. It guides our employees and leaders as we strive to achieve our purpose of protecting and beautifying the world. Employee engagement is a measure of the extent to which our employees are involved in, enthusiastic about, and committed to our work and workplace. We conduct employee surveys to increase dialogue among teams and implement meaningful action to improve results.

Our human capital management strategies provide the foundation for our teams to thrive and deliver exceptional performance. These strategies in the areas of culture and purpose, employee engagement, development and pay equity are overseen by the Human Capital Management and Compensation Committee of our Board of Directors. We are committed to ensuring our employees are safe, healthy, enabled, engaged and valued for the diverse talents they bring to PPG. We believe that having quality dialogue with our people, recognizing the value they bring and championing an authentic culture generates engaged employees and a company that is more innovative, productive and competitive. Our focus on and investment in learning and development are crucial to ensuring we keep our people engaged, productive and successful at every stage of their careers. We are committed to promoting from within wherever possible while also bringing in new ideas, thoughts and insights.

2022 PPG ANNUAL REPORT AND FORM 10-K 7

Our environmental, health and safety policy and standards define our expectations, and we implement programs and initiatives to reduce health and safety risk in our operations. We measure progress against our health and safety goals using the injury and illness rate, which is calculated as the number of illness and injury incidents per 200,000 work hours. For 2022 and 2021, our injury and illness rate was 0.30 and 0.26, respectively.

One of PPG’s greatest strengths is the diversity of our people, who represent wide-ranging nationalities, cultures, languages, religions, ethnicities, and professional and educational backgrounds. Their unique perspectives enable us to meet challenges quickly, creatively and effectively, providing a significant competitive advantage in today’s global economy. To ensure our people feel valued and respected, we are committed to providing a workplace that embraces a culture of diversity and inclusion and is free from harassment and bullying. In connection with our focus on diversity, equity and inclusion, PPG operates eight Employee Resource Networks (“ERNs”). These ERNs are open to all employees and are intended to provide an opportunity for in-depth discussion, focus and recommendations on how PPG can deliver higher growth and performance by creating a more diverse, equitable and inclusive organization.

More information about PPG’s human capital management strategies and our workforce can be found in the Proxy Statement for our 2023 Annual Meeting of Shareholders and in our ESG Report located at http://sustainability.ppg.com.

Environmental Matters

PPG is committed to operating in a sustainable manner and to helping our customers meet their sustainability goals. Our sustainability efforts are governed by the Sustainability and Innovation Committee of our Board of Directors. At the management level, day-to-day implementation of our environmental, social and governance (“ESG”) initiatives is led by our Vice President, Global Sustainability, who is responsible for coordinating PPG’s ESG and sustainability programs and for communicating our ESG progress with our customers, shareholders and other stakeholders. The Vice President, Global Sustainability works with PPG’s Sustainability Committee, a committee of management consisting of senior corporate executives, to establish and monitor our sustainability goals, policies, programs and procedures that incorporate sustainability into our business practices, including resource management, climate change impacts, innovation, community engagement, communications, procurement, manufacturing and employee wellness.

Our dedication to innovation is intertwined with sustainability. We are marketing an ever-growing variety of products and services that protect the environment and provide safety and other benefits to our customers. Our products contribute to lighter, more fuel-efficient vehicles, airplanes and ships, and they help our customers reduce their energy consumption, conserve water and reduce waste. These products include compact automotive paint processes and low cure capabilities that save energy and reduce water usage at customer manufacturing sites; sustainable, waterborne coatings formulations; sustainable powder coatings; lightweight sealants and coatings for aircraft; coatings that cool surfaces; coatings for recyclable metal packaging; antimicrobial products; coatings that contain reduced materials of concern; architectural coatings that contain lower carbon content raw materials; silica products for tires that improve vehicle fuel economy; and solutions for autonomous and battery-powered vehicles. Sales from sustainable products represented 39% of the Company’s total Net sales for the year ended December 31, 2022.

PPG is committed to using resources efficiently and driving sustainability throughout our entire value chain, including continued focus on reducing greenhouse gas emissions, water withdrawal and total energy use. More information about PPG’s sustainability values, efforts, goals and data and our community and employee engagement programs can be found in our ESG Report located at http://sustainability.ppg.com.

We are subject to existing and evolving standards relating to the protection of the environment. In management’s opinion, the Company operates in an environmentally sound manner and is well positioned, relative to environmental matters, within the industries in which it operates. PPG is negotiating with various government agencies concerning current and former manufacturing sites and offsite waste disposal locations, including certain sites on the National Priority List. While PPG is not generally a major contributor of wastes to these offsite waste disposal locations, each potentially responsible party may face governmental agency assertions of joint and several liability. Generally, however, a final allocation of costs is made based on relative contributions of wastes to the site. There is a wide range of cost estimates for cleanup of these sites, due largely to uncertainties as to the nature and extent of their condition and the methods that may have to be employed for their remediation. The Company has established reserves for onsite and offsite remediation of those sites where it is probable that a liability has been incurred and the amount of loss can be reasonably estimated.

Our experience to date regarding environmental matters leads us to believe that we will have continuing expenditures for compliance with provisions regulating the protection of the environment and for present and future remediation efforts at waste and plant sites. Management anticipates that such expenditures will occur over an extended period of time.

In addition to the $217 million currently reserved for environmental remediation efforts, we may be subject to loss contingencies related to environmental matters estimated to be approximately $100 million to $200 million. These reasonably possible unreserved losses relate to environmental matters at a number of sites, none of which are individually

2022 PPG ANNUAL REPORT AND FORM 10-K 8

significant. The loss contingencies related to these sites include significant unresolved issues such as the nature and extent of contamination at these sites and the methods that may have to be employed to remediate them.

| ($ in millions) | 2022 | 2021 | 2020 | ||||||||||||||

| Capital expenditures for environmental control projects | $22 | $17 | $12 | ||||||||||||||

It is expected that capital expenditures for such projects in 2023 will be in the range of $25 million to $35 million. Actual future capital expenditures may differ from expectations due to the inherent uncertainties involved in estimating future environmental remediation compliance costs, including possible technological, regulatory and enforcement developments, the results of environmental studies and other factors.

Management believes that the outcome of these environmental contingencies will not have a material adverse effect on PPG’s financial position or liquidity; however, any such outcome may be material to the results of operations of any particular period in which costs, if any, are recognized. Refer to Note 15, “Commitments and Contingent Liabilities” in Item 8 of this Form 10-K for additional information related to environmental matters and our accrued liability for estimated environmental remediation costs.

Available Information

The Company’s website address is www.ppg.com. The Company posts, and shareholders may access without charge, the Company’s recent filings and any amendments of its annual reports on Form 10-K, quarterly reports on Form 10-Q and its proxy statements as soon as reasonably practicable after such reports are filed with the Securities and Exchange Commission (“SEC”). The Company also posts all financial press releases, including earnings releases, to its website. All other reports filed or furnished to the SEC, including reports on Form 8-K, are available via direct link on PPG’s website to the SEC’s website, www.sec.gov. Reference to the Company’s, the SEC’s or other websites herein does not incorporate by reference any information contained on those websites, and such information should not be considered part of this Form 10-K.

Item 1A. Risk Factors

As a global manufacturer of paints, coatings and specialty materials, we operate in a business environment that includes risks. Each of the risks described in this section could adversely affect our results of operations, financial position and liquidity. While the factors listed here are considered to be the more significant factors, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles which may adversely affect our businesses and our results of operations, financial position and liquidity.

Economic Risks

The effects of the COVID-19 pandemic have negatively impacted and are continuing to adversely impact our financial condition and results of operations.

The effects of the public health crisis caused by COVID-19 have interfered with the ability of PPG, our suppliers, customers, and others to conduct business and have negatively affected consumer confidence and the global economy. Public health officials have recommended or mandated certain precautions to mitigate the spread of COVID-19, including prohibitions on congregating in groups, shelter-in-place orders, vaccination requirements or similar measures. Preventative and protective actions that public health officials, governments or PPG have taken with respect to COVID-19 have and will continue to adversely impact our business, suppliers, distribution channels, and customers, including business shutdowns or disruptions for an indefinite period of time, reduced operations, reduced workforce availability, reduced ability to supply products, or reduced demand for our products. Our financial condition, liquidity and results of operations have been and will continue to be adversely impacted by these preventative actions and the disruption to our business and that of our suppliers and customers. As we cannot predict the duration or scope of COVID-19, the negative financial impact to our business cannot be reasonably estimated, but could be material.

Increases in prices and declines in the availability of raw materials could negatively impact our financial results.

Our financial results are significantly affected by the cost of raw materials. Raw materials include both organic, primarily petroleum-derived, materials and inorganic materials, including titanium dioxide. These raw materials represent PPG’s single largest production cost component.

While not our customary practice, we also import raw materials and intermediates, particularly for use at our manufacturing facilities in the emerging regions of the world. In most cases, those imports are priced in the currency of the supplier and, therefore, if that currency strengthens against the currency of our manufacturing facility, our margins may be lower.

Most of our raw materials are purchased from outside sources, and the Company has made, and plans to continue to make, supply arrangements to meet the planned operating requirements for the future. Adequate supply of critical raw

2022 PPG ANNUAL REPORT AND FORM 10-K 9

materials is managed by establishing contracts, procuring from multiple sources, and identifying alternative materials or technology whenever possible. The Company is continuing its aggressive sourcing initiatives to effectively broaden our supply of high quality raw materials. These initiatives include qualifying multiple and local sources of supply, within Asia and other lower cost regions of the world, diversification of our resin supply including adding on-site resin production at certain manufacturing locations, and a reduction in the amount of titanium dioxide and other raw materials used in our product formulations. Despite our actions undertaken to maintain supply arrangements adequate to meet planned operating requirements, raw material supply chain disruptions, including logistical and transportation challenges in many regions, have adversely impacted, and may continue to adversely impact, our ability to procure raw materials, adversely impacting our financial results.

An inability to obtain certain critical raw materials has adversely impacted our ability to produce certain products and could do so in the future. Increases in the cost of raw materials may have an adverse effect on our Income from continuing operations or Cash from operating activities in the event we are unable to offset these higher costs in a timely manner.

The pace of economic growth and level of uncertainty could have a negative impact on our results of operations and cash flows.

Demand for our products and services depends, in part, on the general economic conditions affecting the countries and markets in which we do business. Weak economic conditions in certain geographies and changing supply and demand balances in the markets we serve have negatively impacted demand for our products and services in the past and may do so in the future. Recently, global economic uncertainty has increased due to a number of factors, including the war in Ukraine, COVID-19, consumer sentiment and commodity market volatility, disruption in supply chains globally, potential changes to international trade agreements, the imposition of tariffs and the threat of additional tariffs, and labor shortages in certain regions of the world. PPG provides products and services to a variety of end-use markets in many geographies. This broad end-use market exposure and expanded geographic presence lessens the significance of any individual decrease in activity levels; nonetheless, lower demand levels may result in lower sales, which would result in reduced Income from continuing operations and Cash from operating activities.

Fluctuations in foreign currency exchange rates could affect our financial results.

We are exposed to foreign currency exchange rate risk with respect to our sales, expenses, profits, assets and liabilities denominated in currencies other than the U.S. dollar. Because our consolidated financial statements are presented in U.S. dollars, we must translate revenues and expenses into U.S. dollars at the average exchange rate during each reporting period, as well as assets and liabilities into U.S. dollars at exchange rates in effect at the end of each reporting period. Therefore, increases or decreases in the value of the U.S. dollar against other currencies will affect our Net sales, Net income and the value of balance sheet items denominated in foreign currencies. We may use derivative financial instruments to reduce our net exposure to currency exchange rate fluctuations related to foreign currency transactions. However, fluctuations in foreign currency exchange rates, particularly the strengthening or weakening of the U.S. dollar against major currencies, could adversely or positively affect our financial condition and results of operations which are expressed in U.S. dollars.

The industries in which we operate are highly competitive.

With each of our businesses, an increase in competition may cause us to lose market share, lose customers, or compel us to reduce prices to remain competitive, which could result in reduced margins for our products. Additionally, our ability to increase prices may impact the overall economics for the products we offer. Competitive pressures may not only reduce our margins but may also impact our revenues and our growth which could adversely affect our results of operations.

Legal, Regulatory, and Tax Risks

We are subject to existing and evolving standards relating to the protection of the environment.

Environmental laws and regulations control, among other things, the discharge of pollutants into the air and water, the handling, use, treatment, storage and clean-up of hazardous and non-hazardous waste, and the investigation and remediation of soil and groundwater affected by hazardous substances. In addition, various laws regulate health and safety matters. The environmental laws and regulations we are subject to impose liability for the costs of, and damages resulting from, cleaning up current sites, past spills, disposals and other releases of hazardous substances. Violations of these laws and regulations can also result in fines and penalties. Future environmental laws and regulations may require substantial capital expenditures or may require or cause us to modify or curtail our operations, which may have a material adverse impact on our business, financial condition and results of operations.

We are involved in a number of lawsuits and claims, and we may be involved in future lawsuits and claims, in which substantial monetary damages are sought.

PPG is involved in a number of lawsuits and claims, both actual and potential, in which substantial monetary damages are sought. Those lawsuits and claims may relate to contract, patent, environmental, product liability, asbestos exposure,

2022 PPG ANNUAL REPORT AND FORM 10-K 10

antitrust, employment, securities and other matters arising out of the conduct of PPG’s current and past business activities. Any such claims, whether with or without merit, could be time consuming and expensive to defend and could divert management’s attention and resources. We maintain insurance against some, but not all, of these potential claims, and the levels of insurance we maintain may not be adequate to fully cover any and all losses. We believe that, in the aggregate, the outcome of all current lawsuits and claims involving PPG, including those described in Note 15, “Commitments and Contingent Liabilities” in Item 8 of this Form 10-K, will not have a material effect on PPG’s consolidated financial position or liquidity; however, such outcome may be material to the results of operations of any particular period in which costs, if any, are recognized. Nonetheless, the results of any future litigation or claims are inherently unpredictable, and such outcomes could have a material adverse effect on our results of operations, Cash from operating activities or financial condition.

We are subject to a variety of complex U.S. and non-U.S. laws and regulations, which could increase our compliance costs and could adversely affect our results of operations.

We are subject to a wide variety of complex U.S. and non-U.S. laws and regulations, and legal compliance risks, including securities laws, tax laws, environmental laws, employment and pension-related laws, competition laws, U.S. and foreign export and trading laws, and laws governing improper business practices, including bribery. We are affected by new laws and regulations and changes to existing laws and regulations, as well as interpretations by courts and regulators. These laws and regulations effectively expand our compliance obligations and costs.

For example, regulations concerning the composition, use and transport of chemical products continue to evolve. Developments concerning these regulations could potentially impact the availability or viability of some of the raw materials we use in our product formulations and/or our ability to supply certain products to some customers or markets. Import/export sanctions and regulations also continue to evolve and could result in increased compliance costs, slower product movements or additional complexity in our supply chains.

Further, although we believe that we have appropriate risk management and compliance programs in place, we cannot guarantee that our internal controls and compliance systems will always protect us from improper acts committed by employees, agents, business partners or businesses that we acquire. Any non-compliance or such improper actions or allegations could damage our reputation and subject us to civil or criminal investigations and shareholder lawsuits, could lead to substantial civil and criminal, monetary and non-monetary penalties, and could cause us to incur significant legal and investigatory costs.

Changes in the tax regimes and related government policies and regulations in the countries in which we operate could adversely affect our results and our effective tax rate.

As a multinational corporation, we are subject to various taxes in both the U.S. and non-U.S. jurisdictions. Due to economic and political conditions, tax rates in these various jurisdictions may be subject to significant changes. Our future effective income tax rate could be affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets or changes in tax laws or their interpretation. Further, PPG may continue to refine its estimates to incorporate new or better information as it becomes available. Recent developments, including potential U.S. or international tax reform, the European Commission’s investigations on illegal state aid as well as the Organisation for Economic Co-operation and Development project on Base Erosion and Profit Shifting may result in changes to long-standing tax principles, which could adversely affect our effective tax rate or result in higher cash tax liabilities. If our effective income tax rate were to increase, our Cash from operating activities, financial condition and results of operations would be adversely affected. Although we believe that our tax filing positions are appropriate, the final determination of tax audits or tax disputes may be different from what is reflected in our historical income tax provisions and accruals. If future audits find that additional taxes are due, we may be subject to incremental tax liabilities, possibly including interest and penalties, which could have a material adverse effect on our Cash from operating activities, financial condition and results of operations.

Operational and Strategic Risks

Our international operations expose us to additional risks and uncertainties that could affect our financial results.

PPG has a significant investment in global operations. This broad geographic footprint serves to lessen the significance of economic impacts occurring in any one region. Notwithstanding the benefits of geographic diversification, our ability to achieve and maintain profitable growth in international markets is subject to risks related to the differing legal, political, social and regulatory requirements and economic conditions of many countries. As a result of our operations outside the U.S., we are subject to certain inherent risks, including political and economic uncertainty, inflation rates, exchange rates, trade protection measures, local labor conditions and laws, restrictions on foreign investments and repatriation of earnings, and weak intellectual property protection. Our percentage of sales generated in 2022 by products sold outside the U.S. was approximately 60%.

2022 PPG ANNUAL REPORT AND FORM 10-K 11

Business disruptions could have a negative impact on our results of operations and financial condition.

Unexpected events, including supply disruptions, temporary plant and/or power outages, work stoppages, natural disasters and severe weather events, including those potentially due to climate change, significant public health issues, computer system disruptions, fires, war or terrorist activities, could increase the cost of doing business or otherwise harm the operations of PPG, our customers and our suppliers. It is not possible for us to predict the occurrence or consequence of any such events. However, such events could reduce our ability to supply products, reduce demand for our products or make it difficult or impossible for us to receive raw materials from suppliers or to deliver products to customers.

Integrating acquired businesses into our existing operations.

Growth through acquisitions is an important component of the Company’s strategy. Over the last decade, we have successfully completed more than 50 acquisitions, and we will likely acquire additional businesses and enter into additional joint ventures in the future. Growth through acquisitions and the formation of joint ventures involve risks, including:

•difficulties in assimilating acquired companies and products into our existing business;

•delays in realizing the benefits from the acquired companies or products;

•diversion of our management’s time and attention from other business concerns;

•difficulties due to lack of or limited prior experience in any new markets we may enter;

•unforeseen claims and liabilities, including unexpected environmental exposures, product liability, or existing information technology vulnerabilities;

•unexpected losses of customers or suppliers of the acquired or existing business;

•difficulty in conforming the acquired business’ standards, processes, procedures and controls to those of our operations; and

•difficulties in retaining key employees of the acquired businesses.

These risks or other problems encountered in connection with our past or future acquisitions and joint ventures could cause delays in realizing the anticipated benefits of such acquisitions or joint ventures, or such anticipated benefits may never be realized, which could adversely affect our results of operations, Cash from operating activities or financial condition.

Our ability to understand our customers’ specific preferences and requirements, and to innovate, develop, produce and market products that meet customer demand is critical to our business results.

Our business relies on continued global demand for our brands and products. To achieve our business goals, we must develop and sell products that appeal to customers. This is dependent on a number of factors, including our ability to produce products that meet the quality, performance and price expectations of our customers and our ability to develop effective sales, advertising and marketing programs.

We believe the automotive industry will experience significant and continued change in the coming years, including an increase in the production of electric vehicles. Vehicle manufacturers continue to develop new safety features such as collision avoidance technology and self-driving vehicles that may reduce vehicle collisions in the future, potentially lowering demand for our automotive refinish coatings. In addition, through the introduction of new technologies, new business models or new methods of travel, such as ridesharing, the number of automotive OEM new-builds may decline, potentially reducing demand for our automotive OEM coatings and related automotive parts.

Additionally, the development of customer-facing digital channels has and will continue to transform certain retail industries. An inability to develop such solutions and our customer’s pace of adoption of those solutions could negatively affect our business or the market demand for our products.

Our future growth will depend on our ability to continue to innovate our existing products and to develop and introduce new products. If we fail to keep pace with product innovation on a competitive basis or to predict market demands for our products, our businesses, financial condition and results of operations could be adversely affected.

The security of our information technology systems could be compromised, which could adversely affect our ability to operate.

Increased global information technology security requirements, threats and sophisticated and targeted computer crime pose a risk to the security of our systems, networks and the confidentiality, availability and integrity of our data. Despite our efforts to protect intellectual property and confidential and personal data, our facilities and systems may be vulnerable to security breaches. This could lead to negative publicity, theft or other financial loss, modification or destruction of

2022 PPG ANNUAL REPORT AND FORM 10-K 12

proprietary information or key information, manufacture of defective products, production downtimes and operational disruptions, which could adversely affect our reputation, competitiveness and results of operations.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

PPG’s corporate headquarters is located in the United States in Pittsburgh, Pa. The Company’s manufacturing facilities, sales offices, research and development centers and distribution centers are located throughout the world. Refer to Item 1. “Business” of this Form 10-K for the principal manufacturing and distribution facilities by reportable business segment.

The Company’s principal research and development centers are located in Allison Park, Pa.; Tianjin, China; Cleveland, Oh.; Springdale, Pa.; Milan, Italy; Monroeville, Pa.; Harmar, Pa.; Ingersheim, Germany; Marly, France; Oak Creek, Wi.; Sumare, Brazil; Amsterdam, Netherlands; Vantaa, Finland; Tepexpan, Mexico; Burbank, Ca.; Zhangjiagang, China; Cheonan, Republic of Korea; Wroclaw, Poland; Bangplee, Thailand; and Sylmar, Ca.

Our headquarters, certain distribution centers and substantially all company-owned paint stores are located in facilities that are leased while our other facilities are generally owned. Our facilities are considered to be suitable and adequate for the purposes for which they are intended and overall have sufficient capacity to conduct business in the upcoming year.

Item 3. Legal Proceedings

PPG is involved in a number of lawsuits and claims, both actual and potential, including some that it has asserted against others, in which substantial monetary damages are sought. These lawsuits and claims may relate to contract, patent, environmental, product liability, asbestos exposure, antitrust, employment, securities and other matters arising out of the conduct of PPG’s current and past business activities. To the extent these lawsuits and claims involve personal injury, property damage and certain other claims, PPG believes it has adequate insurance; however, certain of PPG’s insurers are contesting coverage with respect to some of these claims, and other insurers may contest coverage. PPG’s lawsuits and claims against others include claims against insurers and other third parties with respect to actual and contingent losses related to environmental, asbestos and other matters.

From the late 1880’s until the early 1970’s, PPG owned property located in Cadogan and North Buffalo Townships, Pennsylvania which was used for the disposal of solid waste from PPG’s former glass manufacturing facility in Ford City, Pennsylvania. In October 2018, the Pennsylvania Department of Environmental Protection (the “DEP”) approved PPG’s cleanup plan for the Cadogan Property. In April 2019, PPG and the DEP entered into a consent order and agreement (“CO&A”) which incorporated PPG’s approved cleanup plan and a draft final permit for the collection and discharge of seeps emanating from the former disposal area. The CO&A includes a civil penalty of $1.2 million for alleged past unauthorized discharges. PPG’s former disposal area is also the subject of a citizens’ suit filed by the Sierra Club and PennEnvironment seeking remedial measures beyond the measures specified in PPG’s approved cleanup plan, a civil penalty in addition to the penalty included in the CO&A and plaintiffs’ attorneys fees. PPG and the plaintiffs settled plaintiffs’ claims for injunctive relief and PPG agreed to enhancements to the DEP approved cleanup plan and a $250,000 donation to a Pennsylvania nonprofit organization. This settlement has been memorialized by an amendment to the CO&A which was appended to a Consent Agreement between PPG and the plaintiffs which has been entered by the federal Court. The remaining claims in the case for attorneys’ fees and a civil penalty are not affected by this settlement. PPG believes that the remaining claims are without merit and intends to defend itself against these claims vigorously.

For many years, PPG has been a defendant in lawsuits involving claims alleging personal injury from exposure to asbestos. For a description of asbestos litigation affecting the Company, see Note 15, “Commitments and Contingent Liabilities” to the accompanying consolidated financial statements in Part I, Item 8 of this Form 10-K.

In the past, the Company and others have been named as defendants in several cases in various jurisdictions claiming damages related to exposure to lead and remediation of lead-based coatings applications. PPG has been dismissed as a defendant from most of these lawsuits and has never been found liable in any of these cases. After having not been named in a new lead-related lawsuit for 15 years, PPG was named as a defendant in two Pennsylvania state court lawsuits filed by Montgomery County and Lehigh County in the respective counties on October 4, 2018 and October 12, 2018. Both suits seek declaratory relief arising out of alleged public nuisances in the counties associated with the presence of lead paint on various buildings constructed prior to 1980. The Company believes these actions are without merit and intends to defend itself vigorously.

2022 PPG ANNUAL REPORT AND FORM 10-K 13

Information About Our Executive Officers

Set forth below is information related to the Company’s executive officers as of February 16, 2023.

| Name | Age | Title | ||||||

Michael H. McGarry (a) | 64 | Executive Chairman since January 2023 | ||||||

Timothy M. Knavish (b) | 57 | President and Chief Executive Officer since January 2023 | ||||||

Anne M. Foulkes (c) | 60 | Senior Vice President and General Counsel since September 2018 | ||||||

Vincent J. Morales (d) | 57 | Senior Vice President and Chief Financial Officer since March 2017 | ||||||

Amy R. Ericson (e) | 57 | Senior Vice President, Protective and Marine Coatings since January 2023 | ||||||

Ramaprasad Vadlamannati (f) | 60 | Senior Vice President, Global Operations since January 2023 | ||||||

(a)On October 19, 2022, Mr. McGarry was elected as Executive Chairman, effective January 1, 2023. Mr. McGarry served as Chairman and Chief Executive Officer of the Company from September 2016 through December 2022 and as President and Chief Executive Officer from September 2015 through August 2016. Mr. McGarry previously served as President and Chief Operating Officer from March 2015 through August 2015, Chief Operating Officer from August 2014 through February 2015, Executive Vice President from September 2012 through July 2014; and Senior Vice President, Commodity Chemicals from July 2008 through August 2012.

(b)On October 19, 2022, Mr. Knavish was elected as President and Chief Executive Officer, effective January 1, 2023. Mr. Knavish served as Chief Operating Officer of the Company from March 2022 through December 2022. He previously served as Executive Vice President from October 2019 through February 2022, Senior Vice President, Architectural Coatings and President, PPG EMEA from January 2019 through September 2019, Senior Vice President, Industrial Coatings from October 2017 through December 2018, Senior Vice President, Automotive Coatings from March 2016 through September 2017, Vice President, Protective and Marine Coatings from August 2012 through February 2016 and Vice President, Automotive Coatings, Americas from March 2010 through July 2012.

(c)Ms. Foulkes served as Senior Vice President, General Counsel and Secretary from April 2022 to June 2022 and from August 2018 to September 2018, Vice President and Associate General Counsel and Secretary from March 2016 through July 2018 and Assistant General Counsel and Secretary from April 2011 through February 2016.

(d)Mr. Morales served as Vice President, Finance from June 2016 through February 2017. From June 2015 through June 2016, he served as Vice President, Investor Relations and Treasurer and from October 2007 through May 2015 he served as Vice President, Investor Relations.

(e)In January 2023, Ms. Ericson was named Senior Vice President, Protective and Marine Coatings. Ms. Ericson served as Senior Vice President, Packaging Coatings from July 2018 through December 2022. She served as President of SUEZ Chemical Monitoring and Solutions from 2017 until 2018, President of General Electric Water Services Company from 2015 to 2017 and President and Chief Executive Officer of Alstom SA’s U.S. business from 2013 to 2015.

(f)In January 2023, Mr. Vadlamannati was named Senior Vice President, Global Operations. Mr. Vadlamannati served as Senior Vice President, Protective and Marine Coatings and President PPG EMEA from October 2019 through December 2022, Senior Vice President, Protective and Marine Coatings from March 2016 through September 2019, Vice President, Architectural Coatings, EMEA and Asia Pacific from August 2014 through February 2016, Vice President, Architectural Coatings, EMEA from February 2012 through July 2014, Vice President, Architectural Coatings, EMEA for Region Western Europe from March 2011 through January 2012 and Vice President, Automotive Refinish, EMEA from September 2010 through February 2011.

Item 4. Mine Safety Disclosures

Not Applicable.

2022 PPG ANNUAL REPORT AND FORM 10-K 14

Part II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

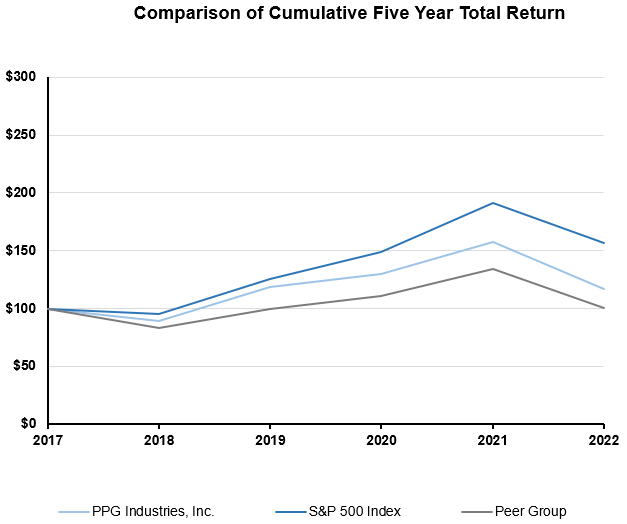

The information required by Item 5 regarding market information, including PPG’s stock exchange listing and quarterly stock market prices, dividends, holders of common stock, and the stock performance graph is included in Exhibit 13.1 filed with this Form 10-K and is incorporated herein by reference.

No shares were repurchased in the three months ended December 31, 2022 under the current $2.5 billion share repurchase program approved in December 2017. The maximum number of shares that may yet be purchased under this program is 8,830,144 shares as of December 31, 2022. This repurchase program has no expiration date.

Item 6. [Reserved]

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion includes a comparison of our results of operations and liquidity and capital resources for the years ended December 31, 2022 and 2021. A discussion of changes in our results of operations for the year ended December 31, 2021 as compared to the year ended December 31, 2020 has been omitted from this Form 10-K, but may be found in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” of our 2021 Form 10-K, filed with the Securities and Exchange Commission on February 17, 2022.

Highlights

Net sales were approximately $17.7 billion in 2022, an increase of 5% compared to the prior year, driven by higher selling prices resulting from continued selling price initiatives. The Company increased net sales despite softer demand conditions in Europe due in part to geopolitical issues, pandemic-related demand disruptions in China and unfavorable foreign currency translation impacts due to the strong appreciation of the U.S. dollar versus many foreign currencies.

Income before income taxes was $1,381 million in 2022, a decrease of $434 million compared to the prior year. This decrease was primarily due to raw material and other cost inflation, lower sales volumes, unfavorable foreign currency translation impacts, higher manufacturing costs related to supply and labor disruptions and impairment and other related charges, partially offset by increased selling prices.

Performance Overview

Net Sales by Region

| % Change | |||||||||||

| ($ in millions, except percentages) | 2022 | 2021 | 2022 vs. 2021 | ||||||||

| United States and Canada | $7,383 | $6,676 | 10.6% | ||||||||

| Europe, Middle East and Africa (EMEA) | 5,458 | 5,436 | 0.4% | ||||||||

| Asia Pacific | 2,824 | 2,977 | (5.1)% | ||||||||

| Latin America | 1,987 | 1,713 | 16.0% | ||||||||

| Total | $17,652 | $16,802 | 5.1% | ||||||||

Net sales increased $850 million due to the following:

● Higher selling prices (+11%)

● Acquisition-related sales (+3%)

Partially offset by:

● Unfavorable foreign currency translation (-5%)

● Lower sales volumes (-3%)

● Divestiture-related sales and the wind down of Russia operations (-1%)

For specific business results, see the Performance of Reportable Business Segments section within Item 7 of this Form 10-K.

Cost of sales, exclusive of depreciation and amortization

| % Change | |||||||||||

| ($ in millions, except percentages) | 2022 | 2021 | 2022 vs. 2021 | ||||||||

| Cost of sales, exclusive of depreciation and amortization | $11,096 | $10,286 | 7.9% | ||||||||

| Cost of sales as a % of net sales | 62.9 | % | 61.2 | % | 1.7% | ||||||

2022 PPG ANNUAL REPORT AND FORM 10-K 15

Cost of sales, exclusive of depreciation and amortization, increased $810 million due to the following:

● Raw material, energy, wage and other cost inflation

● Cost of sales from acquired businesses

Partially offset by:

● Favorable foreign currency translation

● Lower sales volumes

Selling, general and administrative expenses

| % Change | |||||||||||

| ($ in millions, except percentages) | 2022 | 2021 | 2022 vs. 2021 | ||||||||

| Selling, general and administrative expenses | $3,842 | $3,780 | 1.6% | ||||||||

| Selling, general and administrative expenses as a % of net sales | 21.8 | % | 22.5 | % | (0.7)% | ||||||

Selling, general and administrative expenses increased $62 million primarily due to:

● Selling, general and administrative expenses from acquired businesses

● Wage and other cost inflation

Partially offset by:

● Favorable foreign currency translation

● Restructuring cost savings

Other charges and other income

| % Change | |||||||||||

| ($ in millions, except percentages) | 2022 | 2021 | 2022 vs. 2021 | ||||||||

| Interest expense | $167 | $121 | 38.0% | ||||||||

| Interest income | ($54) | ($26) | 107.7% | ||||||||

| Impairment and other related charges, net | $245 | $21 | 1,066.7% | ||||||||

| Pension settlement charge | $— | $50 | N/A | ||||||||

| Asbestos-related claims reserve adjustment | $— | ($133) | N/A | ||||||||

| Business restructuring, net | $33 | $31 | 6.5% | ||||||||

| Other (income)/charges, net | ($60) | ($143) | (58.0)% | ||||||||

Interest expense

Interest expense increased $46 million 2022 versus 2021 primarily due the unfavorable impact of higher interest rates on PPG’s variable rate debt obligations and slightly higher levels of debt in the current year.

Interest income

Interest income increased $28 million primarily due to higher interest rates.

Impairment and other related charges, net

Impairment and other related charges of $290 million were recorded in the first quarter 2022 associated with the wind down of the Company's operations in Russia. Subsequently, the Company released a portion of the previously established reserves due to the collection of certain trade receivables and recorded recoveries due to the realization of certain previously written-down inventories, resulting in recognition of income of $63 million. The Company continues to consider actions to exit Russia, including a possible sale of its Russian business or controlled withdrawal from the Russian market.

During 2022 and 2021, the Company recorded impairment charges of $14 million and $21 million, respectively, related to certain smaller, non-strategic businesses. PPG committed to plans to sell these business and they were reclassified as held for sale. The impairment charges recorded represent the excess net book value of the net assets over the anticipated sales proceeds less costs to sell. The revenue of these businesses represent less than 1% of PPG annual net sales.

In the fourth quarter 2022, the Company recorded an impairment charge of $4 million to reduce the carrying value of certain indefinite-lived trademarks based on the results of the annual impairment test.

Refer to Note 6, “Goodwill and Other Identifiable Intangible Assets and Note 7 ”Impairment and Other Related Charges, Net” in Item 8 of this Form 10-K for additional information.

2022 PPG ANNUAL REPORT AND FORM 10-K 16

Pension settlement charge

In December 2021, the Company purchased group annuity contracts that transferred pension benefit obligations for certain of the Company’s retirees in Canada to a third-party insurance company. This transaction resulted in a pension settlement charge of $50 million. Refer to Note 14, “Employee Benefit Plans" in Item 8 of this Form 10-K for additional information.

Asbestos-related claims reserve adjustment

In 2021, the reserve for asbestos-related claims was reduced to reflect the Company’s current estimate of potential liability for these claims. Refer to Note 15 “Commitments and Contingent Liabilities” in Item 8 of this Form 10-K for additional information.

Business restructuring, net

Pretax restructuring charges of $84 million related to recent acquisitions were recorded in 2022, partially offset by certain changes in estimates to complete previously recorded programs of $51 million. Pretax restructuring charges of $54 million were recorded in 2021, offset by certain changes in estimates to complete previously recorded programs of $23 million. Refer to Note 8, "Business Restructuring" in Item 8 of this Form 10-K for additional information.

Other (income)/charges, net

Other (income)/charges, net was lower in 2022 compared to the prior year primarily due to a $34 million gain on the sale of a production facility in 2021 in connection with the Company’s manufacturing footprint consolidation plans and associated restructuring programs as well as favorable legal settlements in 2021. Refer to Note 18, “Other (Income)/Charges, Net” in Item 8 of this Form 10-K for additional information.

Effective tax rate and earnings per diluted share, continuing operations

| % Change | |||||||||||

| ($ in millions, except percentages) | 2022 | 2021 | 2022 vs. 2021 | ||||||||

| Income tax expense | $325 | $374 | (13.1)% | ||||||||

| Effective tax rate | 23.5 | % | 20.6 | % | 2.9% | ||||||

| Adjusted effective tax rate, continuing operations* | 22.0 | % | 20.0 | % | 2.0% | ||||||

| Earnings per diluted share, continuing operations | $4.33 | $5.93 | (27.0)% | ||||||||

| Adjusted earnings per diluted share, continuing operations* | $6.05 | $6.77 | (10.6)% | ||||||||

| *See the Regulation G reconciliations - results of operations | |||||||||||

The effective tax rate for the year-ended December 31, 2022 was 23.5%, an increase of 2.9% from the prior year primarily driven by charges associated with PPG’s operations in Russia along with a reduction in the release of reserves for uncertain tax positions compared to the prior year.

Earnings per diluted share and adjusted earnings per diluted share from continuing operations for the year ended December 31, 2022 decreased year over year primarily due raw material cost inflation, lower sales volumes, unfavorable foreign currency translation impact and higher manufacturing costs related to supply and labor disruptions, partially offset by increased selling prices. Refer to the Regulation G Reconciliations - Results from Operations for additional information.

Regulation G Reconciliations - Results from Operations

PPG believes investors’ understanding of the Company’s performance is enhanced by the disclosure of net income from continuing operations, earnings per diluted share from continuing operations, PPG’s effective tax rate and segment income adjusted for certain items. PPG’s management considers this information useful in providing insight into the Company’s ongoing performance because it excludes the impact of items that cannot reasonably be expected to recur on a quarterly basis or that are not attributable to our primary operations. Net income from continuing operations, earnings per diluted share from continuing operations, the effective tax rate and segment income adjusted for these items are not recognized financial measures determined in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) and should not be considered a substitute for net income from continuing operations, earnings per diluted share from continuing operations, the effective tax rate, segment income or other financial measures as computed in accordance with U.S. GAAP. In addition, adjusted net income, adjusted earnings per diluted share and the adjusted effective tax rate may not be comparable to similarly titled measures as reported by other companies.

Income before income taxes from continuing operations is reconciled to adjusted income before income taxes from continuing operations, the effective tax rate from continuing operations is reconciled to the adjusted effective tax rate from continuing operations and net income from continuing operations (attributable to PPG) and earnings per share – assuming

2022 PPG ANNUAL REPORT AND FORM 10-K 17

dilution (attributable to PPG) are reconciled to adjusted net income from continuing operations (attributable to PPG) and adjusted earnings per share – assuming dilution below.

| ($ in millions, except percentages and per share amounts) | Income Before Income Taxes | Income Tax Expense | Effective Tax Rate | Net income from continuing operations (attributable to PPG) | Earnings per diluted share(1) | ||||||||||||||||||||||||

Year-ended December 31, 2022 | |||||||||||||||||||||||||||||

| As reported, continuing operations | $1,381 | $325 | 23.5 | % | $1,028 | $4.33 | |||||||||||||||||||||||

| Includes: | |||||||||||||||||||||||||||||

Impairment and other related charges, net(2) | 245 | 31 | 12.7 | % | 214 | 0.90 | |||||||||||||||||||||||

| Acquisition-related amortization expense | 166 | 40 | 24.1 | % | 126 | 0.53 | |||||||||||||||||||||||

Business restructuring-related costs, net(3) | 75 | 19 | 25.3 | % | 56 | 0.24 | |||||||||||||||||||||||

Transaction-related costs, net(4) | 10 | (2) | (20.0 | %) | 12 | 0.05 | |||||||||||||||||||||||

| Adjusted, continuing operations, excluding certain items | $1,877 | $413 | 22.0 | % | $1,436 | $6.05 | |||||||||||||||||||||||

| ($ in millions, except percentages and per share amounts) | Income Before Income Taxes | Income Tax Expense | Effective Tax Rate | Net income from continuing operations (attributable to PPG) | Earnings per diluted share(1) | ||||||||||||||||||||||||

Year-ended December 31, 2021 | |||||||||||||||||||||||||||||

| As reported, continuing operations | $1,815 | $374 | 20.6 | % | $1,420 | $5.93 | |||||||||||||||||||||||

| Includes: | |||||||||||||||||||||||||||||

| Acquisition-related amortization expense | 172 | 42 | 24.4 | % | 130 | 0.55 | |||||||||||||||||||||||

Transaction-related costs, net(4) | 86 | 17 | 19.8 | % | 69 | 0.29 | |||||||||||||||||||||||

| Pension settlement charge | 50 | 14 | 26.6 | % | 36 | 0.15 | |||||||||||||||||||||||

| Net charges related to environmental remediation | 35 | 9 | 24.3 | % | 26 | 0.11 | |||||||||||||||||||||||

| Net tax charge related to U.K. statutory rate change | — | (22) | N/A | 22 | 0.09 | ||||||||||||||||||||||||

Business restructuring-related costs, net(3) | 27 | 7 | 25.9 | % | 20 | 0.08 | |||||||||||||||||||||||

Expenses incurred due to natural disasters(5) | 17 | 4 | 24.3 | % | 13 | 0.06 | |||||||||||||||||||||||

Impairment and other related charges, net(2) | 21 | 6 | 29.2 | % | 12 | 0.05 | |||||||||||||||||||||||

| Decrease in allowance for doubtful accounts related to COVID-19 | (14) | (3) | 24.7 | % | (11) | (0.05) | |||||||||||||||||||||||

| Income from legal settlements | (22) | (5) | 24.3 | % | (17) | (0.07) | |||||||||||||||||||||||

Asbestos-related claims reserve adjustment(6) | (133) | (32) | 24.3 | % | (101) | (0.42) | |||||||||||||||||||||||

| Adjusted, continuing operations, excluding certain items | $2,054 | $411 | 20.0 | % | $1,619 | $6.77 | |||||||||||||||||||||||

(1)Earnings per diluted share is calculated based on unrounded numbers. Figures in the table may not recalculate due to rounding.

(2)In the first quarter 2022, the Company recorded impairment and other related charges due to the wind down of the company’s operations in Russia. Subsequently, the Company released a portion of the previously established reserves for Receivables and Inventories due to the collection of certain trade receivables and the realization of certain inventories. Also in 2022, impairment and other related charges were recorded for the write-down of certain assets and liabilities related to the planned sale of a non-core business and for certain asset write downs. In 2021, an impairment charge was recorded for the write-down of certain assets related to the previously planned sale of certain smaller entities in non-strategic regions. Net loss of $3 million related to the 2021 impairment charge was attributable to noncontrolling interests.

(3)Included in business restructuring-related costs, net are business restructuring charges, accelerated depreciation of certain assets and other related costs, offset by releases related to previously approved programs and a $34 million gain on the sale of certain assets in 2021 in connection with the Company’s manufacturing footprint consolidation plans and associated restructuring programs. This gain is included in Other (income)/charges, net in the consolidated statement of income.