UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-04764 | |||||

| BNY Mellon Opportunistic Municipal Securities Fund | ||||||

| (Exact name of Registrant as specified in charter) | ||||||

|

c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 |

||||||

| (Address of principal executive offices) (Zip code) | ||||||

|

Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 |

||||||

| (Name and address of agent for service) | ||||||

| Registrant's telephone number, including area code: | (212) 922-6400 | |||||

|

Date of fiscal year end:

|

04/30 | |||||

| Date of reporting period: |

04/30/24

|

|||||

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Opportunistic Municipal Securities Fund

ANNUAL REPORT April 30, 2024 |

|

IMPORTANT NOTICE – UPCOMING CHANGES TO ANNUAL AND SEMI-ANNUAL REPORTS The Securities and Exchange Commission (the “SEC”) has adopted rule and form amendments that will result in changes to the design and delivery of annual and semi-annual fund reports (“Reports”). Beginning in July 2024, Reports will be streamlined to highlight key information. Certain information currently included in Reports, including financial statements, will no longer appear in the Reports but will be available online, delivered free of charge to shareholders upon request, and filed with the SEC. If you previously elected to receive the fund’s Reports electronically, you will continue to do so. Otherwise, you will receive paper copies of the fund’s re-designed Reports by USPS mail in the future. If you would like to receive the fund’s Reports (and/or other communications) electronically instead of by mail, please contact your financial advisor or, if you are a direct investor, please log into your mutual fund account at www.bnymellonim.com/us and select “E-Delivery” under the Profile page. You must be registered for online account access before you can enroll in E-Delivery. |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

Information About the Renewal of | |

FOR MORE INFORMATION

Back Cover

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period from May 1, 2023, through April 30, 2024, as provided by Daniel Rabasco and Jeffrey Burger, Portfolio Managers employed by the fund’s sub-adviser, Insight North America LLC.

Market and Fund Performance Overview

For the 12-month period ended April 30, 2024, BNY Mellon Opportunistic Municipal Securities Fund (the “fund”) produced a total return of 3.15% for Class A shares, 2.33% for Class C shares, 3.31% for Class I shares, 3.44% for Class Y shares and 3.19% for Class Z shares.1 In comparison, the Bloomberg U.S. Municipal Bond Index (the “Index”), the fund’s benchmark index, achieved a total return of 2.08% for the same period.2

Municipal bonds posted gains during the reporting period as inflation eased, and investors anticipated rate cuts by the U.S. Federal Reserve (the “Fed”). The fund outperformed the Index mainly due to strong security selection across many subsectors.

The Fund’s Investment Approach

The fund seeks to maximize current income exempt from federal income tax to the extent consistent with the preservation of capital. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in municipal bonds that provide income exempt from federal income tax. Typically, the fund invests substantially all of its assets in such municipal bonds. The fund invests at least 70% of its assets in municipal bonds rated, at the time of purchase, investment grade (Baa/BBB or higher) or the unrated equivalent as determined by the fund’s sub-adviser, Insight North America LLC (“INA”). For additional yield, the fund may invest up to 30% of its assets in municipal bonds rated below investment grade (“high yield” or “junk” bonds) or the unrated equivalent as determined by INA. The dollar-weighted, average maturity of the fund’s portfolio normally exceeds 10 years, but the fund may invest without regard to maturity or duration.

The fund’s sub-adviser focuses on identifying undervalued sectors and securities and minimizes the use of interest-rate forecasting. To select municipal bonds for the fund, the sub-adviser uses fundamental credit analysis to estimate the relative value and attractiveness of various sectors and securities and actively trades among various sectors and securities based on their apparent relative values. The fund seeks to invest in several different sectors and does not seek to overweight any particular sector but may do so depending on each sector’s relative value at any given time.

Declining Inflation, Fed Dovishness Support Market

The municipal bond market experienced weakness due to higher rates through much of the reporting period. Toward the end of 2023, declining inflation and investor anticipation of Fed rate cuts provided the market with a degree of support. As 2024 progressed, however, investors began to accept that rate cuts would be fewer and later than anticipated.

The Fed continued to make progress in reducing pricing pressures early in the reporting period. It raised the federal funds rate twice, in May and July 2023, bringing the target rate to 5.25%–5.50%. But with inflation seemingly trending downward toward the 2.0% target, the Fed left rates unchanged through the remainder of the period.

The yield on the 10-year Treasury trended higher as well, but despite the higher rates, the U.S. economy surprised investors by continuing to avoid a long-anticipated recession. The economy grew by 2.1% in the second quarter of 2023, 4.9% in the third quarter and 3.4% in the fourth quarter. Growth moderated in the first quarter of 2024, coming in at 1.6%.

2

With inflation continuing to ease late in 2023, investors began to look ahead to interest-rate reductions by the Fed. Heading into 2024, municipal mutual bond funds began to receive inflow from retail investors, who had largely been absent, resulting in favorable technical conditions as demand was more than adequate to handle increasing new issue supply.

The surprisingly strong economy, including a robust labor market, bolstered the case that the Fed would achieve a “soft landing” — taming inflation while avoiding a recession. But inflation remained above the Fed’s 2% target. In fact, the personal consumption expenditure (“PCE”) index rose to 2.5% year over year in February 2024, though the core PCE, which excludes food and energy, edged downward to 2.8%. Like the PCE, the consumer price index (“CPI”) has remained higher than expected in 2024.

The relative stubbornness of inflation further raised the odds that rate cuts anticipated to occur in early-to-mid 2024 would be delayed. This caused the market to move sideways during the first months of 2024 and decline somewhat in April. However, this made valuations even more attractive, extending the opportunity for interested investors.

Security Selection Drove Outperformance

The fund’s performance was driven primarily by favorable security selection. Selections of general obligation bonds were especially beneficial, as were selections in many revenue bond subsectors. The latter included continuing care and retirement centers (“CCRC”), special tax, public power, transportation, industrial development and water & sewer. Sector allocation decisions were also favorable. Overweight positioning in revenue bonds, especially in airports, CCRCs, prepaid gas and tobacco, was particularly beneficial. An underweight position in water & sewer also contributed positively.

The fund’s duration positioning detracted from returns. The fund’s duration was long relative to the Index, and this hampered performance as interest rates rose. This was partially offset by curve positioning, however, as the extra yield on bonds with maturities of 10 to 30 years was beneficial. Security selections in the education subsector also detracted, as did an overweight to education bonds. The fund did not make use of derivatives.

Positioned for Expected Monetary Easing

Market sentiment has shifted somewhat, and the number of anticipated rate cuts by the Fed is now less than expected not that long ago. Employment remains strong, and inflation has proven to be higher than anticipated. On the plus side, this means that the entry point for the municipal bond market is attractive, as yields remain high. Inflows to municipal bond mutual funds have picked up, however, and we believe they are likely to remain strong.

We remain constructive on the market for the second half of 2024. While supply has picked up, it remains manageable, and demand remains strong. Credit fundamentals are also healthy, supported by a resilient economy and improving housing market. In this environment, we anticipate that municipal bond spreads could tighten, enhancing the potential for total return. We continue to focus on opportunities for improving incremental yields.

Historically, the municipal bond market has performed well when the Fed has ended a tightening cycle, and an end to tightening remains a likely scenario as 2024 progresses. The presidential election in November 2024 adds some uncertainty to this outlook and is likely to result in issuance earlier in the year than would otherwise have been the case. We will monitor the impact of the election, inflation trends and macro-economic conditions and, when warranted, adjust portfolio positioning.

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

May 15, 2024

1 Total return includes reinvestment of dividends and any capital gains paid and does not take into consideration the maximum initial sales charge in the case of Class A shares or the applicable contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Class I, Class Y and Class Z are not subject to any initial or deferred sales charge. Past performance is no guarantee of future results. Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Income may be subject to state and local taxes, and some income may be subject to the federal alternative minimum tax (AMT) for certain investors. Capital gains, if any, are taxable.

2 Source: Lipper Inc. — The Bloomberg U.S. Municipal Bond Index covers the U.S. dollar-denominated, long-term, tax-exempt bond market. Investors cannot invest directly in any index.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

High yield bonds involve increased credit and liquidity risk than higher-rated bonds and are considered speculative in terms of the issuer’s ability to pay interest and repay principal on a timely basis.

The amount of public information available about municipal bonds is generally less than that for corporate equities or bonds. Special factors, such as legislative changes, and state and local economic and business developments, may adversely affect the yield and/or value of the fund’s investments in municipal bonds. Other factors include the general conditions of the municipal bond market, the size of the particular offering, the maturity of the obligation and the rating of the issue. Changes in economic, business or political conditions relating to a particular municipal project, municipality or state in which the fund invests may have an impact on the fund’s share price.

References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations.

4

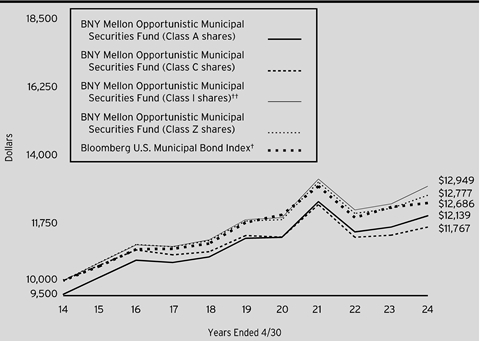

FUND PERFORMANCE (Unaudited)

Comparison of change

in value of a $10,000 investment in Class A shares, Class C shares, Class I shares and Class Z shares

of BNY Mellon Opportunistic Municipal Securities Fund with a hypothetical investment of $10,000 in the

Bloomberg U.S. Municipal Bond Index (the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class I shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 8/31/16 (the inception date for Class I shares), not reflecting the applicable sales load for Class A shares.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in each of the Class A shares, Class C shares, Class I shares and Class Z shares of BNY Mellon Opportunistic Municipal Securities Fund on 4/30/14 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses on Class A shares, Class C shares, Class I shares and Class Z shares. The Index, unlike the fund, covers the U.S. dollar-denominated long-term tax-exempt bond market. These factors can contribute to the Index potentially outperforming or underperforming the fund. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

5

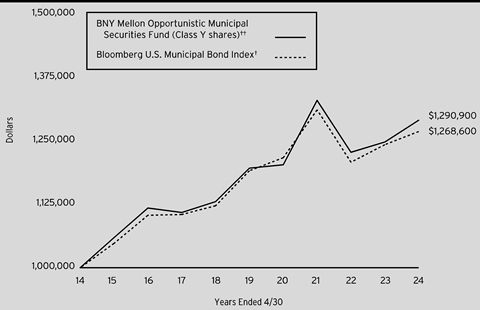

FUND PERFORMANCE (Unaudited) (continued)

Comparison

of change in value of a $1,000,000 investment in Class Y shares of BNY Mellon Opportunistic Municipal

Securities Fund with a hypothetical investment of $1,000,000 in the Bloomberg U.S. Municipal Bond Index

(the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 8/31/16 (the inception date for Class Y shares), not reflecting the applicable sales load for Class A shares.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $1,000,000 investment made in Class Y shares of BNY Mellon Opportunistic Municipal Securities Fund on 4/30/14 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the graph above takes into account all applicable fees and expenses of the fund’s Class Y shares. The Index, unlike the fund, covers the U.S. dollar-denominated long-term tax-exempt bond market. These factors can contribute to the Index potentially outperforming or underperforming the fund. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

Average Annual Total Returns as of 4/30/2024 |

|

|

| |

| Inception | 1 Year | 5 Years | 10 Years |

Class A shares | ||||

with maximum sales charge (4.50%) | 11/26/86 | -1.45% | .35% | 1.96% |

without sales charge | 11/26/86 | 3.15% | 1.27% | 2.43% |

Class C shares | ||||

with applicable redemption charge † | 7/13/95 | 1.33% | .48% | 1.64% |

without redemption | 7/13/95 | 2.33% | .48% | 1.64% |

Class I shares | 8/31/16 | 3.31% | 1.52% | 2.62%†† |

Class Y shares | 8/31/16 | 3.44% | 1.53% | 2.59%†† |

Class Z shares | 10/14/04 | 3.19% | 1.32% | 2.48% |

Bloomberg U.S. Municipal Bond Index | 2.08% | 1.26% | 2.41% | |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return performance figures presented for Class I shares and Class Y shares of the fund reflect the performance of the fund’s Class A shares for the period prior to 8/31/16 (the inception date for Class I shares and Class Y shares), not reflecting the applicable sales load for Class A shares.

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in BNY Mellon Opportunistic Municipal Securities Fund from November 1, 2023 to April 30, 2024. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment |

| ||||||

Assume actual returns for the six months ended April 30, 2024 |

| ||||||

|

|

|

|

|

|

|

|

|

| Class A | Class C | Class I | Class Y | Class Z |

|

Expenses paid per $1,000† | $4.04 | $8.17 | $2.80 | $2.59 | $3.84 |

| |

Ending value (after expenses) | $1,084.80 | $1,080.30 | $1,086.10 | $1,086.30 | $1,085.00 |

| |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (“SEC”) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment |

| ||||||

Assuming a hypothetical 5% annualized return for the six months ended April 30, 2024 |

| ||||||

|

|

|

|

|

|

|

|

|

| Class A | Class C | Class I | Class Y | Class Z |

|

Expenses paid per $1,000† | $3.92 | $7.92 | $2.72 | $2.51 | $3.72 |

| |

Ending value (after expenses) | $1,020.98 | $1,017.01 | $1,022.18 | $1,022.38 | $1,021.18 |

| |

† | Expenses are equal to the fund’s annualized expense ratio of .78% for Class A, 1.58% for Class C, .54% for Class I, .50% for Class Y and .74% for Class Z, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). | ||||||

8

STATEMENT OF INVESTMENTS

April

30, 2024

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Bonds and Notes - .4% | |||||||||

Collateralized Municipal-Backed Securities - .4% | |||||||||

Arizona Industrial Development Authority, Revenue Bonds, Ser. 2019-2 | 3.63 | 5/20/2033 | 964,085 | 890,594 | |||||

Washington Housing Finance Commission, Revenue Bonds, Ser. A1 | 3.50 | 12/20/2035 | 956,672 | 870,382 | |||||

Total Bonds

and Notes | 1,760,976 | ||||||||

Long-Term Municipal Investments - 100.3% | |||||||||

Alabama - 2.2% | |||||||||

Birmingham-Jefferson Civic Center Authority, Special Tax Bonds, Ser. B | 5.00 | 7/1/2043 | 2,500,000 | 2,540,942 | |||||

Black Belt Energy Gas District, Revenue Bonds, Refunding, Ser. D1 | 4.00 | 6/1/2027 | 1,000,000 | a | 1,003,066 | ||||

Jefferson County, Revenue Bonds, Refunding | 5.25 | 10/1/2049 | 1,000,000 | 1,053,704 | |||||

Jefferson County, Revenue Bonds, Refunding | 5.50 | 10/1/2053 | 3,250,000 | 3,480,951 | |||||

University of Alabama at Birmingham, Revenue Bonds (Board of Trustees) Ser. B | 4.00 | 10/1/2035 | 2,000,000 | 2,047,922 | |||||

10,126,585 | |||||||||

Arizona - 3.7% | |||||||||

Arizona Industrial Development Authority, Revenue Bonds (Sustainable Bond) (Equitable School Revolving Fund Obligated Group) Ser. A | 4.00 | 11/1/2038 | 3,065,000 | 3,005,604 | |||||

Arizona Industrial Development Authority, Revenue Bonds (Sustainable Bond) (Equitable School Revolving Fund Obligated Group) Ser. A | 5.25 | 11/1/2048 | 2,000,000 | 2,112,112 | |||||

Arizona Industrial Development Authority, Revenue Bonds, Refunding (BASIS Schools Projects) Ser. A | 5.38 | 7/1/2050 | 2,500,000 | b | 2,453,321 | ||||

Glendale Industrial Development Authority, Revenue Bonds, Refunding (Sun Health Services Obligated Group) Ser. A | 5.00 | 11/15/2054 | 1,500,000 | 1,397,472 | |||||

9

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Arizona - 3.7% (continued) | |||||||||

La Paz County Industrial Development Authority, Revenue Bonds (Harmony Public Schools) Ser. A | 5.00 | 2/15/2048 | 1,000,000 | 932,704 | |||||

La Paz County Industrial Development Authority, Revenue Bonds (Harmony Public Schools) Ser. A | 5.00 | 2/15/2046 | 2,000,000 | b | 1,891,237 | ||||

Maricopa County Industrial Development Authority, Revenue Bonds (Banner Health Obligated Group) Ser. A | 5.00 | 1/1/2041 | 1,175,000 | 1,205,794 | |||||

Maricopa County Industrial Development Authority, Revenue Bonds (Benjamin Franklin Charter School Obligated Group) | 6.00 | 7/1/2038 | 2,750,000 | b | 2,858,283 | ||||

The Phoenix Arizona Industrial Development Authority, Revenue Bonds, Refunding (BASIS Schools Projects) Ser. A | 5.00 | 7/1/2046 | 1,000,000 | b | 947,243 | ||||

16,803,770 | |||||||||

Arkansas - 1.1% | |||||||||

Arkansas Development Finance Authority, Revenue Bonds (Sustainable Bond) (U.S. Steel Corp.) | 5.70 | 5/1/2053 | 4,800,000 | 4,936,436 | |||||

California - 4.9% | |||||||||

Alameda Corridor Transportation Authority, Revenue Bonds (Insured; Assured Guaranty Municipal Corp.) Ser. C | 5.00 | 10/1/2052 | 2,500,000 | 2,658,504 | |||||

California, GO, Refunding | 5.00 | 4/1/2042 | 650,000 | 711,136 | |||||

California, GO, Refunding | 5.25 | 9/1/2047 | 1,000,000 | 1,103,122 | |||||

California Community Choice Financing Authority, Revenue Bonds (Sustainable Bond) (Clean Energy Project) Ser. G | 5.25 | 4/1/2030 | 2,500,000 | a | 2,661,542 | ||||

California County Tobacco Securitization Agency, Revenue Bonds, Refunding, Ser. A | 4.00 | 6/1/2040 | 400,000 | 401,816 | |||||

California Health Facilities Financing Authority, Revenue Bonds, Refunding (Sutter Health Obligated Group) Ser. B | 5.00 | 11/15/2046 | 1,480,000 | 1,502,024 | |||||

California Housing Finance Agency, Revenue Bonds, Ser. 2021-1 | 3.50 | 11/20/2035 | 1,430,324 | 1,322,509 | |||||

10

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

California - 4.9% (continued) | |||||||||

California Municipal Finance Authority, Revenue Bonds (United Airlines Project) | 4.00 | 7/15/2029 | 3,675,000 | 3,654,356 | |||||

California Municipal Finance Authority, Revenue Bonds, Refunding (HumanGood California Obligated Group) Ser. A | 5.00 | 10/1/2044 | 2,500,000 | 2,536,048 | |||||

California University, Revenue Bonds, Refunding, Ser. B2 | 0.55 | 11/1/2026 | 1,000,000 | a | 897,850 | ||||

Orange County Community Facilities District, Special Tax Bonds (Community Facilities District No. 2021-1) Ser. A | 5.00 | 8/15/2047 | 1,000,000 | 1,003,707 | |||||

San Diego County Regional Airport Authority, Revenue Bonds, Ser. B | 4.00 | 7/1/2046 | 1,750,000 | 1,626,127 | |||||

San Francisco City & County Airport Commission, Revenue Bonds, Refunding, Ser. B | 5.00 | 5/1/2041 | 1,500,000 | 1,512,794 | |||||

San Jose Evergreen Community College District, GO, Ser. C | 4.00 | 9/1/2045 | 1,000,000 | 1,005,526 | |||||

22,597,061 | |||||||||

Colorado - 4.0% | |||||||||

Colorado Health Facilities Authority, Revenue Bonds (Children's Hospital Colorado Obligated Group) Ser. A | 5.00 | 12/1/2041 | 2,500,000 | 2,525,472 | |||||

Colorado Health Facilities Authority, Revenue Bonds (Covenant Retirement Communities) | 5.00 | 12/1/2043 | 3,280,000 | 3,226,756 | |||||

Colorado Health Facilities Authority, Revenue Bonds, Refunding (CommonSpirit Health Obligated Group) Ser. A | 5.00 | 8/1/2044 | 1,250,000 | 1,285,083 | |||||

Colorado Health Facilities Authority, Revenue Bonds, Refunding (Intermountain Healthcare Obligated Group) Ser. A | 4.00 | 5/15/2052 | 2,000,000 | 1,892,361 | |||||

Colorado Health Facilities Authority, Revenue Bonds, Refunding (School Health System) Ser. A | 4.00 | 1/1/2036 | 2,000,000 | 2,034,619 | |||||

Denver City & County Airport System, Revenue Bonds, Refunding, Ser. A | 5.00 | 12/1/2048 | 3,000,000 | 3,034,064 | |||||

11

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Colorado - 4.0% (continued) | |||||||||

Denver City & County Airport System, Revenue Bonds, Refunding, Ser. A | 5.50 | 11/15/2053 | 3,000,000 | 3,234,349 | |||||

Regional Transportation District, Revenue Bonds, Refunding (Denver Transit Partners) Ser. A | 5.00 | 1/15/2031 | 950,000 | 1,034,082 | |||||

18,266,786 | |||||||||

Connecticut - .2% | |||||||||

Connecticut Health & Educational Facilities Authority, Revenue Bonds, Refunding (Fairfield University) Ser. T | 4.00 | 7/1/2055 | 1,000,000 | 906,511 | |||||

Delaware - .2% | |||||||||

Delaware Economic Development Authority, Revenue Bonds (ACTS Retirement-Life Communities Obligated Group) Ser. B | 5.25 | 11/15/2053 | 1,000,000 | 1,021,595 | |||||

District of Columbia - 2.3% | |||||||||

District of Columbia, Revenue Bonds, Refunding (Children's Hospital Obligated Group) | 5.00 | 7/15/2035 | 1,500,000 | 1,530,920 | |||||

District of Columbia, Revenue Bonds, Ser. A | 5.50 | 7/1/2047 | 3,000,000 | 3,334,892 | |||||

Metropolitan Washington Airports Authority, Revenue Bonds, Refunding | 5.00 | 10/1/2035 | 1,500,000 | 1,555,552 | |||||

Metropolitan Washington Airports Authority, Revenue Bonds, Refunding (Dulles Metrorail) Ser. B | 4.00 | 10/1/2049 | 2,500,000 | 2,282,791 | |||||

Metropolitan Washington Airports Authority, Revenue Bonds, Refunding, Ser. A | 5.00 | 10/1/2035 | 1,000,000 | 1,023,192 | |||||

Washington Metropolitan Area Transit Authority, Revenue Bonds (Sustainable Bond) Ser. A | 4.13 | 7/15/2047 | 1,000,000 | 967,063 | |||||

10,694,410 | |||||||||

Florida - 4.1% | |||||||||

Broward County Airport System, Revenue Bonds | 5.00 | 10/1/2037 | 1,560,000 | 1,605,521 | |||||

Escambia County, Revenue Bonds | 5.00 | 10/1/2046 | 2,000,000 | 2,064,631 | |||||

Florida Municipal Power Agency, Revenue Bonds, Ser. A | 3.00 | 10/1/2032 | 1,000,000 | 928,799 | |||||

Hillsborough County Aviation Authority, Revenue Bonds (Tampa International Airport) | 5.00 | 10/1/2034 | 1,000,000 | 1,091,991 | |||||

12

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Florida - 4.1% (continued) | |||||||||

Jacksonville, Revenue Bonds, Refunding (Brooks Rehabilitation Project) | 4.00 | 11/1/2045 | 1,500,000 | 1,329,520 | |||||

JEA Water & Sewer System, Revenue Bonds, Refunding, Ser. A | 4.00 | 10/1/2040 | 800,000 | 801,482 | |||||

Miami Beach Redevelopment Agency, Tax Allocation Bonds, Refunding | 5.00 | 2/1/2033 | 1,000,000 | 1,002,644 | |||||

Miami Beach Stormwater, Revenue Bonds, Refunding | 5.00 | 9/1/2047 | 2,500,000 | 2,379,560 | |||||

Mid-Bay Bridge Authority, Revenue Bonds, Refunding, Ser. A | 5.00 | 10/1/2040 | 1,000,000 | 1,003,349 | |||||

Orange County Health Facilities Authority, Revenue Bonds (Orlando Health Obligated Group) Ser. A | 5.00 | 10/1/2053 | 2,000,000 | 2,080,015 | |||||

Palm Beach County Health Facilities Authority, Revenue Bonds, Refunding (Baptist Health South Florida Obligated Group) | 4.00 | 8/15/2049 | 3,305,000 | 2,959,860 | |||||

Village Community Development District No. 15, Special Assessment Bonds | 5.25 | 5/1/2054 | 1,500,000 | b | 1,533,238 | ||||

18,780,610 | |||||||||

Georgia - 3.6% | |||||||||

Georgia Municipal Electric Authority, Revenue Bonds (Plant Vogtle Units 3&4 Project) | 5.00 | 1/1/2037 | 1,100,000 | 1,151,619 | |||||

Georgia Municipal Electric Authority, Revenue Bonds (Plant Vogtle Units 3&4 Project) (Insured; Assured Guaranty Municipal Corp.) Ser. A | 5.00 | 7/1/2055 | 1,000,000 | 1,034,583 | |||||

Georgia Municipal Electric Authority, Revenue Bonds (Plant Vogtle Units 3&4 Project) Ser. A | 5.00 | 7/1/2052 | 3,250,000 | 3,321,348 | |||||

Georgia Municipal Electric Authority, Revenue Bonds, Refunding (Project No. 1) Ser. A | 5.00 | 1/1/2028 | 1,500,000 | 1,539,174 | |||||

Georgia Ports Authority, Revenue Bonds | 4.00 | 7/1/2052 | 1,250,000 | 1,200,393 | |||||

Main Street Natural Gas, Revenue Bonds, Ser. A | 5.00 | 6/1/2030 | 2,500,000 | a | 2,597,769 | ||||

Main Street Natural Gas, Revenue Bonds, Ser. B | 5.00 | 6/1/2029 | 2,000,000 | a | 2,077,781 | ||||

Main Street Natural Gas, Revenue Bonds, Ser. C | 4.00 | 9/1/2026 | 3,750,000 | a | 3,753,031 | ||||

16,675,698 | |||||||||

13

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Hawaii - .3% | |||||||||

Hawaii Airports System, Revenue Bonds, Ser. A | 5.00 | 7/1/2047 | 1,250,000 | 1,297,092 | |||||

Illinois - 7.8% | |||||||||

Chicago Board of Education, GO, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. A | 5.00 | 12/1/2033 | 1,000,000 | 1,043,049 | |||||

Chicago Board of Education, GO, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. C | 5.00 | 12/1/2030 | 1,500,000 | 1,567,501 | |||||

Chicago Board of Education, GO, Ser. A | 6.00 | 12/1/2049 | 1,000,000 | 1,095,565 | |||||

Chicago Board of Education, Revenue Bonds | 5.00 | 4/1/2042 | 1,000,000 | 1,015,320 | |||||

Chicago O'Hare International Airport, Revenue Bonds, Refunding, Ser. A | 5.00 | 1/1/2034 | 2,100,000 | 2,109,634 | |||||

Chicago O'Hare International Airport, Revenue Bonds, Ser. A | 5.50 | 1/1/2055 | 1,500,000 | 1,587,013 | |||||

Chicago Park District, GO, Refunding, Ser. C | 5.00 | 1/1/2039 | 1,150,000 | 1,213,678 | |||||

Chicago Wastewater, Revenue Bonds, Refunding (Insured; Build America Mutual) Ser. A | 5.00 | 1/1/2044 | 1,500,000 | 1,610,981 | |||||

Cook County II, Revenue Bonds, Refunding | 5.00 | 11/15/2035 | 2,500,000 | 2,602,687 | |||||

Illinois, GO, Refunding, Ser. D | 4.00 | 7/1/2037 | 1,750,000 | 1,724,559 | |||||

Illinois Finance Authority, Revenue Bonds, Refunding (OSF Healthcare System Obligated Group) Ser. A | 5.00 | 11/15/2045 | 1,000,000 | 1,006,298 | |||||

Illinois Finance Authority, Revenue Bonds, Refunding (Rush University Medical Center Obligated Group) Ser. A | 5.00 | 11/15/2033 | 3,000,000 | 3,026,371 | |||||

Illinois Finance Authority, Revenue Bonds, Refunding (The University of Chicago) Ser. A | 4.00 | 4/1/2050 | 3,760,000 | 3,493,637 | |||||

Illinois Housing Development Authority, Revenue Bonds (Sustainable Bond) (Insured; GNMA, FNMA, FHLMC) Ser. A | 3.00 | 4/1/2051 | 1,485,000 | 1,428,857 | |||||

Northern Illinois University, Revenue Bonds, Refunding (Insured; Build America Mutual) Ser. B | 4.00 | 4/1/2040 | 1,475,000 | 1,397,392 | |||||

Regional Transportation Authority, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) | 6.00 | 6/1/2025 | 1,000,000 | 1,006,182 | |||||

14

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Illinois - 7.8% (continued) | |||||||||

Sales Tax Securitization Corp., Revenue Bonds, Refunding, Ser. A | 4.00 | 1/1/2039 | 2,350,000 | 2,279,198 | |||||

Sales Tax Securitization Corp., Revenue Bonds, Refunding, Ser. A | 4.00 | 1/1/2038 | 1,000,000 | 983,103 | |||||

Sales Tax Securitization Corp., Revenue Bonds, Refunding, Ser. A | 5.00 | 1/1/2034 | 1,400,000 | 1,584,847 | |||||

Sales Tax Securitization Corp., Revenue Bonds, Refunding, Ser. A | 5.00 | 1/1/2036 | 3,500,000 | 3,762,862 | |||||

35,538,734 | |||||||||

Indiana - .7% | |||||||||

Indiana Finance Authority, Revenue Bonds, Refunding (CWA Authority Project) Ser. 1 | 4.00 | 10/1/2036 | 2,980,000 | 3,062,916 | |||||

Iowa - 2.6% | |||||||||

Iowa Finance Authority, Revenue Bonds, Refunding (Iowa Fertilizer Co. Project) | 5.00 | 12/1/2050 | 2,730,000 | 2,843,935 | |||||

Iowa Finance Authority, Revenue Bonds, Refunding (Lifespace Communities Obligated Group) Ser. B | 7.25 | 5/15/2038 | 2,000,000 | 2,230,780 | |||||

Iowa Student Loan Liquidity Corp., Revenue Bonds, Ser. B | 5.00 | 12/1/2030 | 1,500,000 | 1,574,789 | |||||

Iowa Tobacco Settlement Authority, Revenue Bonds, Refunding, Ser. A2 | 4.00 | 6/1/2049 | 2,000,000 | 1,784,399 | |||||

Iowa Tobacco Settlement Authority, Revenue Bonds, Refunding, Ser. B1 | 4.00 | 6/1/2049 | 1,220,000 | 1,202,254 | |||||

PEFA, Revenue Bonds (Gas Project) | 5.00 | 9/1/2026 | 2,000,000 | a | 2,037,192 | ||||

11,673,349 | |||||||||

Kentucky - 2.0% | |||||||||

Henderson, Revenue Bonds (Pratt Paper Project) Ser. A | 4.70 | 1/1/2052 | 1,015,000 | b | 999,485 | ||||

Kentucky Economic Development Finance Authority, Revenue Bonds, Refunding (Louisville Arena Project) (Insured; Assured Guaranty Municipal Corp.) Ser. A | 5.00 | 12/1/2045 | 2,000,000 | 2,056,155 | |||||

Kentucky Public Energy Authority, Revenue Bonds, Refunding, Ser. A1 | 5.25 | 2/1/2032 | 4,500,000 | a | 4,758,864 | ||||

Kentucky Public Energy Authority, Revenue Bonds, Ser. A1 | 4.00 | 8/1/2030 | 1,500,000 | a | 1,482,572 | ||||

9,297,076 | |||||||||

15

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Louisiana - 1.8% | |||||||||

Louisiana Public Facilities Authority, Revenue Bonds (Franciscan Missionaries of Our Lady Health System Obligated Group) Ser. A | 5.00 | 7/1/2047 | 1,500,000 | 1,509,922 | |||||

New Orleans Aviation Board, Revenue Bonds (Parking Facilities Corp.) (Insured; Assured Guaranty Municipal Corp.) | 5.00 | 10/1/2048 | 1,250,000 | 1,278,048 | |||||

New Orleans Aviation Board, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) | 5.00 | 1/1/2036 | 1,135,000 | 1,192,030 | |||||

New Orleans Aviation Board, Revenue Bonds, Ser. B | 5.00 | 1/1/2040 | 2,175,000 | 2,175,003 | |||||

St. John the Baptist Parish, Revenue Bonds, Refunding (Marathon Oil Corp.) | 2.20 | 7/1/2026 | 1,000,000 | a | 952,457 | ||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. A | 5.25 | 5/15/2035 | 1,220,000 | 1,230,702 | |||||

8,338,162 | |||||||||

Maryland - .6% | |||||||||

Maryland Economic Development Corp., Revenue Bonds (Sustainable Bond) (Purple Line Transit Partners) Ser. B | 5.25 | 6/30/2055 | 2,490,000 | 2,550,829 | |||||

Massachusetts - .6% | |||||||||

Massachusetts Development Finance Agency, Revenue Bonds, Refunding (Boston Medical Center Corp. Obligated Group) | 4.38 | 7/1/2052 | 1,000,000 | 944,634 | |||||

Massachusetts Development Finance Agency, Revenue Bonds, Refunding (Suffolk University) | 5.00 | 7/1/2027 | 1,750,000 | 1,797,082 | |||||

2,741,716 | |||||||||

Michigan - 4.9% | |||||||||

Great Lakes Water Authority, Revenue Bonds, Ser. B | 5.00 | 7/1/2046 | 3,000,000 | 3,043,658 | |||||

Karegnondi Water Authority, Revenue Bonds, Refunding | 5.00 | 11/1/2041 | 1,000,000 | 1,021,355 | |||||

Lansing Board of Water & Light, Revenue Bonds, Ser. B | 2.00 | 7/1/2026 | 2,500,000 | a | 2,364,919 | ||||

Michigan Finance Authority, Revenue Bonds (Henry Ford Health System Obligated Group) Ser. A | 4.00 | 11/15/2050 | 1,665,000 | 1,474,771 | |||||

Michigan Finance Authority, Revenue Bonds (Sustainable Bond) (Henry Ford) | 4.38 | 2/28/2054 | 1,000,000 | 957,503 | |||||

16

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Michigan - 4.9% (continued) | |||||||||

Michigan Finance Authority, Revenue Bonds, Refunding (Beaumont-Spectrum) | 4.00 | 4/15/2042 | 2,425,000 | 2,352,361 | |||||

Michigan Finance Authority, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. D1 | 5.00 | 7/1/2037 | 2,000,000 | 2,002,356 | |||||

Michigan Housing Development Authority, Revenue Bonds, Ser. A | 3.50 | 12/1/2050 | 1,305,000 | 1,276,018 | |||||

Michigan Strategic Fund, Revenue Bonds (I-75 Improvement Project) | 5.00 | 6/30/2033 | 3,900,000 | 4,037,354 | |||||

Michigan Trunk Line, Revenue Bonds | 4.00 | 11/15/2046 | 1,140,000 | 1,101,655 | |||||

Pontiac School District, GO (Insured; Qualified School Board Loan Fund) | 4.00 | 5/1/2045 | 1,800,000 | 1,736,099 | |||||

Wayne County Airport Authority, Revenue Bonds, Ser. D | 5.00 | 12/1/2045 | 1,000,000 | 1,006,488 | |||||

22,374,537 | |||||||||

Minnesota - .5% | |||||||||

Minnesota Agricultural & Economic Development Board, Revenue Bonds (HealthPartners Obligated Group) | 5.25 | 1/1/2054 | 2,000,000 | 2,129,964 | |||||

Missouri - .7% | |||||||||

Kansas City Industrial Development Authority, Revenue Bonds (Kansas City International Airport) Ser. B | 5.00 | 3/1/2054 | 3,060,000 | 3,071,189 | |||||

Nebraska - .4% | |||||||||

Public Power Generation Agency, Revenue Bonds, Refunding | 5.00 | 1/1/2037 | 2,000,000 | 2,042,600 | |||||

Nevada - 2.6% | |||||||||

Clark County, GO, Ser. A | 5.00 | 6/1/2043 | 5,000,000 | 5,204,418 | |||||

Clark County School District, GO, Ser. A | 5.00 | 6/15/2039 | 5,000,000 | 5,484,719 | |||||

Reno, Revenue Bonds, Refunding (Reno Transportation Rail Access Project) | 5.00 | 6/1/2048 | 1,070,000 | 1,093,519 | |||||

11,782,656 | |||||||||

17

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

New Hampshire - .3% | |||||||||

New Hampshire Business Finance Authority, Revenue Bonds (University of Nevada Reno Project) (Insured; Build America Mutual) Ser. A | 4.00 | 12/1/2040 | 515,000 | 506,059 | |||||

New Hampshire Business Finance Authority, Revenue Bonds (University of Nevada Reno Project) (Insured; Build America Mutual) Ser. A | 4.13 | 12/1/2043 | 1,000,000 | 971,597 | |||||

1,477,656 | |||||||||

New Jersey - 3.7% | |||||||||

New Jersey Educational Facilities Authority, Revenue Bonds, Refunding (Stockton University) Ser. A | 5.00 | 7/1/2041 | 1,000,000 | 1,015,552 | |||||

New Jersey Health Care Facilities Financing Authority, Revenue Bonds (Inspira Health Obligated Group) | 5.00 | 7/1/2037 | 1,600,000 | 1,648,477 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds | 5.50 | 6/15/2050 | 1,000,000 | 1,086,343 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds, Refunding, Ser. AA | 4.25 | 6/15/2044 | 1,000,000 | 977,302 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds, Ser. BB | 5.00 | 6/15/2044 | 2,000,000 | 2,054,522 | |||||

New Jersey Transportation Trust Fund Authority, Revenue Bonds, Ser. BB | 5.25 | 6/15/2050 | 1,500,000 | 1,606,174 | |||||

New Jersey Turnpike Authority, Revenue Bonds, Ser. B | 4.13 | 1/1/2054 | 1,000,000 | 964,948 | |||||

South Jersey Transportation Authority, Revenue Bonds | 4.63 | 11/1/2047 | 1,000,000 | 1,002,869 | |||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. A | 5.00 | 6/1/2046 | 3,880,000 | 3,967,406 | |||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. A | 5.00 | 6/1/2036 | 2,000,000 | 2,096,726 | |||||

Tobacco Settlement Financing Corp., Revenue Bonds, Refunding, Ser. A | 5.25 | 6/1/2046 | 620,000 | 642,041 | |||||

17,062,360 | |||||||||

New York - 10.4% | |||||||||

Metropolitan Transportation Authority, Revenue Bonds, Refunding (Sustainable Bond) Ser. C1 | 5.00 | 11/15/2050 | 3,000,000 | 3,099,296 | |||||

New York City, GO, Ser. F1 | 4.00 | 3/1/2047 | 200,000 | 192,056 | |||||

18

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

New York - 10.4% (continued) | |||||||||

New York City Housing Development Corp., Revenue Bonds (Sustainable Bond) (Insured; Federal Housing Administration) Ser. F2 | 0.60 | 7/1/2025 | 980,000 | a | 930,522 | ||||

New York City Municipal Water Finance Authority, Revenue Bonds, Ser. CC1 | 4.25 | 6/15/2054 | 1,355,000 | 1,334,007 | |||||

New York Liberty Development Corp., Revenue Bonds, Refunding (Class 1-3 World Trade Center Project) | 5.00 | 11/15/2044 | 2,500,000 | b | 2,477,775 | ||||

New York Liberty Development Corp., Revenue Bonds, Refunding (Goldman Sachs Headquarters) | 5.25 | 10/1/2035 | 1,000,000 | 1,152,146 | |||||

New York State Dormitory Authority, Revenue Bonds, Refunding, Ser. E | 4.00 | 3/15/2038 | 1,400,000 | 1,424,308 | |||||

New York Transportation Development Corp., Revenue Bonds (Delta Air Lines) | 4.38 | 10/1/2045 | 2,500,000 | 2,417,189 | |||||

New York Transportation Development Corp., Revenue Bonds (Delta Air Lines) | 5.00 | 1/1/2032 | 1,500,000 | 1,547,359 | |||||

New York Transportation Development Corp., Revenue Bonds (JFK International Airport Terminal) | 5.00 | 12/1/2040 | 2,000,000 | 2,090,853 | |||||

New York Transportation Development Corp., Revenue Bonds (LaGuardia Airport Terminal B Redevelopment Project) Ser. A | 5.00 | 7/1/2046 | 2,500,000 | 2,438,341 | |||||

New York Transportation Development Corp., Revenue Bonds (Sustainable Bond) (JFK International Airport Terminal One Project) (Insured; Assured Guaranty Municipal Corp.) | 5.13 | 6/30/2060 | 1,000,000 | 1,033,976 | |||||

Tender Option Bond Trust Receipts (Series 2023-XF1639), (New York State Urban Development Corp., Revenue Bonds, Ser. A) Non-Recourse, Underlying Coupon Rate 5.00% | 7.25 | 3/15/2053 | 10,000,000 | b,c,d | 10,594,961 | ||||

Triborough Bridge & Tunnel Authority, Revenue Bonds (MTA Bridges & Tunnels) Ser. A | 5.25 | 5/15/2057 | 2,500,000 | 2,686,181 | |||||

19

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

New York - 10.4% (continued) | |||||||||

Triborough Bridge & Tunnel Authority, Revenue Bonds, Refunding (MTA Bridges & Tunnels) Ser. C2 | 5.00 | 11/15/2042 | 1,500,000 | 1,558,412 | |||||

Triborough Bridge & Tunnel Authority, Revenue Bonds, Refunding, Ser. C | 5.25 | 5/15/2052 | 5,000,000 | 5,368,080 | |||||

Triborough Bridge & Tunnel Authority, Revenue Bonds, Ser. A1 | 5.25 | 5/15/2059 | 5,000,000 | 5,416,691 | |||||

TSASC, Revenue Bonds, Refunding, Ser. B | 5.00 | 6/1/2045 | 815,000 | 737,145 | |||||

Westchester County Local Development Corp., Revenue Bonds, Refunding (Purchase Senior Learning Community Obligated Group) | 5.00 | 7/1/2046 | 1,000,000 | b | 947,355 | ||||

47,446,653 | |||||||||

North Carolina - .8% | |||||||||

Charlotte Airport, Revenue Bonds, Refunding, Ser. B | 5.00 | 7/1/2038 | 1,000,000 | 1,073,796 | |||||

North Carolina Medical Care Commission, Revenue Bonds (Twin Lakes Community) Ser. A | 5.00 | 1/1/2038 | 1,000,000 | 1,006,128 | |||||

The Charlotte-Mecklenburg Hospital Authority, Revenue Bonds (Atrium Health Obligated Group) | 5.00 | 12/1/2028 | 1,500,000 | a | 1,605,620 | ||||

3,685,544 | |||||||||

North Dakota - .3% | |||||||||

University of North Dakota, COP (Insured; Assured Guaranty Municipal Corp.) Ser. A | 4.00 | 6/1/2046 | 1,470,000 | 1,403,052 | |||||

Ohio - 2.2% | |||||||||

Buckeye Tobacco Settlement Financing Authority, Revenue Bonds, Refunding, Ser. A2 | 4.00 | 6/1/2048 | 7,335,000 | 6,540,886 | |||||

Cuyahoga County, Revenue Bonds, Refunding (The MetroHealth System) | 5.25 | 2/15/2047 | 1,000,000 | 1,002,385 | |||||

Ohio, Revenue Bonds (Cleveland Clinic Health System Obligated Group) | 2.75 | 5/1/2028 | 1,000,000 | a | 967,231 | ||||

Ohio, Revenue Bonds, Refunding (Lease Appropriations-Adult Correctional Building Fund Projects) Ser. A | 5.00 | 10/1/2037 | 1,430,000 | 1,485,538 | |||||

9,996,040 | |||||||||

20

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Oregon - 1.2% | |||||||||

Port of Portland, Revenue Bonds, Refunding (Sustainable Bond) Ser. 29 | 5.50 | 7/1/2053 | 3,250,000 | 3,485,985 | |||||

Port of Portland, Revenue Bonds, Refunding, Ser. 28 | 4.00 | 7/1/2047 | 2,250,000 | 2,075,706 | |||||

5,561,691 | |||||||||

Pennsylvania - 5.9% | |||||||||

Allentown Neighborhood Improvement Zone Development Authority, Revenue Bonds (City Center Project) | 5.00 | 5/1/2033 | 2,750,000 | b | 2,794,838 | ||||

Geisinger Authority, Revenue Bonds, Refunding (Geisinger Health System Obligated Group) | 5.00 | 2/15/2027 | 1,350,000 | a | 1,390,317 | ||||

Luzerne County Industrial Development Authority, Revenue Bonds, Refunding (Pennsylvania-American Water Co.) | 2.45 | 12/3/2029 | 1,750,000 | a | 1,554,302 | ||||

Montgomery County Industrial Development Authority, Revenue Bonds, Refunding (ACTS Retirement-Life Communities Obligated Group) | 5.00 | 11/15/2036 | 3,500,000 | 3,589,506 | |||||

Pennsylvania Economic Development Financing Authority, Revenue Bonds (The Penndot Major Bridges) (Insured; Assured Guaranty Municipal Corp.) | 5.00 | 12/31/2057 | 2,000,000 | 2,084,090 | |||||

Pennsylvania Higher Education Assistance Agency, Revenue Bonds, Ser. A | 5.00 | 6/1/2029 | 1,400,000 | 1,456,054 | |||||

Pennsylvania Turnpike Commission Oil Franchise, Revenue Bonds, Refunding, Ser. A | 5.00 | 12/1/2046 | 3,000,000 | 3,180,172 | |||||

Pennsylvania Turnpike Commission Oil Franchise, Revenue Bonds, Ser. B | 5.25 | 12/1/2048 | 4,000,000 | 4,163,250 | |||||

Philadelphia Water & Wastewater, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. B | 4.50 | 9/1/2048 | 1,000,000 | 1,011,268 | |||||

The Philadelphia School District, GO (Insured; State Aid Withholding) Ser. A | 4.00 | 9/1/2036 | 1,420,000 | 1,436,760 | |||||

21

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Pennsylvania - 5.9% (continued) | |||||||||

The Philadelphia School District, GO (Insured; State Aid Withholding) Ser. A | 5.00 | 9/1/2038 | 1,000,000 | 1,039,349 | |||||

The Philadelphia School District, GO (Insured; State Aid Withholding) Ser. A | 5.00 | 9/1/2044 | 3,000,000 | 3,113,746 | |||||

26,813,652 | |||||||||

Rhode Island - .3% | |||||||||

Rhode Island Health & Educational Building Corp., Revenue Bonds (Lifespan Obligated Group) | 5.25 | 5/15/2054 | 1,250,000 | 1,305,252 | |||||

South Carolina - 2.1% | |||||||||

Piedmont Municipal Power Agency, Revenue Bonds, Refunding, Ser. D | 4.00 | 1/1/2033 | 3,000,000 | 3,051,489 | |||||

South Carolina Public Service Authority, Revenue Bonds, Refunding (Santee Cooper) | 5.13 | 12/1/2043 | 5,000,000 | 4,787,056 | |||||

South Carolina Public Service Authority, Revenue Bonds, Refunding (Santee Cooper) Ser. A | 4.00 | 12/1/2055 | 2,000,000 | 1,749,840 | |||||

9,588,385 | |||||||||

Tennessee - 1.2% | |||||||||

Metropolitan Government Nashville & Davidson County Health & Educational Facilities Board, Revenue Bonds (Belmont University) | 5.25 | 5/1/2048 | 1,750,000 | 1,859,462 | |||||

Tennergy Corp., Revenue Bonds, Ser. A | 4.00 | 9/1/2028 | 2,000,000 | a | 1,984,025 | ||||

The Metropolitan Nashville Airport Authority, Revenue Bonds, Ser. B | 5.50 | 7/1/2052 | 1,500,000 | 1,602,231 | |||||

5,445,718 | |||||||||

Texas - 11.1% | |||||||||

Clifton Higher Education Finance Corp., Revenue Bonds (International Leadership of Texas) Ser. D | 5.75 | 8/15/2033 | 5,000,000 | 5,110,133 | |||||

Clifton Higher Education Finance Corp., Revenue Bonds, Refunding (IDEA Public Schools) (Insured; Permanent School Fund Guarantee Program) | 5.00 | 8/15/2031 | 2,325,000 | 2,331,884 | |||||

Corpus Christi Utility System, Revenue Bonds, Refunding, Ser. A | 4.00 | 7/15/2035 | 1,000,000 | 1,018,902 | |||||

Dallas Area Rapid Transit, Revenue Bonds, Refunding, Ser. B | 4.00 | 12/1/2051 | 1,925,000 | 1,810,187 | |||||

22

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Texas - 11.1% (continued) | |||||||||

Dallas Fort Worth International Airport, Revenue Bonds, Refunding, Ser. B | 5.00 | 11/1/2040 | 2,500,000 | 2,742,904 | |||||

Garland Electric Utility System, Revenue Bonds, Refunding | 5.00 | 3/1/2044 | 1,500,000 | 1,560,921 | |||||

Georgetown Utility System, Revenue Bonds (Insured; Assured Guaranty Municipal Corp.) | 5.25 | 8/15/2052 | 3,000,000 | 3,167,167 | |||||

Houston Airport System, Revenue Bonds (United Airlines) Ser. C | 5.00 | 7/15/2028 | 1,000,000 | 1,020,421 | |||||

Houston Airport System, Revenue Bonds, Refunding (Insured; Assured Guaranty Municipal Corp.) Ser. B | 4.25 | 7/1/2053 | 3,080,000 | 2,983,467 | |||||

Lamar Consolidated Independent School District, GO | 4.00 | 2/15/2053 | 1,225,000 | 1,125,072 | |||||

Love Field Airport Modernization Corp., Revenue Bonds | 5.00 | 11/1/2034 | 3,500,000 | 3,551,986 | |||||

Lower Colorado River Authority, Revenue Bonds, Refunding (LCRA Transmission Services Corp.) Ser. A | 4.00 | 5/15/2049 | 1,000,000 | 887,519 | |||||

Lubbock Electric Light & Power System, Revenue Bonds | 5.00 | 4/15/2048 | 2,475,000 | 2,538,301 | |||||

Mission Economic Development Corp., Revenue Bonds, Refunding (Natgasoline Project) | 4.63 | 10/1/2031 | 4,175,000 | b | 4,132,272 | ||||

North Texas Tollway Authority, Revenue Bonds, Refunding, Ser. A | 5.00 | 1/1/2039 | 4,000,000 | 4,067,696 | |||||

Plano Independent School District, GO | 5.00 | 2/15/2043 | 1,000,000 | 1,078,670 | |||||

Tarrant County Cultural Education Facilities Finance Corp., Revenue Bonds (Baylor Scott & White Health Obligated Group) Ser. F | 5.00 | 11/15/2030 | 2,000,000 | a | 2,169,357 | ||||

Tarrant County Cultural Education Facilities Finance Corp., Revenue Bonds (CHRISTUS Health Obligated Group) Ser. A | 5.00 | 7/1/2032 | 1,500,000 | a | 1,649,417 | ||||

Texas Municipal Gas Acquisition & Supply Corp. IV, Revenue Bonds, Ser. B | 5.50 | 1/1/2034 | 2,000,000 | a | 2,206,771 | ||||

23

STATEMENT OF INVESTMENTS (continued)

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Texas - 11.1% (continued) | |||||||||

University of Texas System Board of Regents, Revenue Bonds, Refunding, Ser. A | 4.13 | 8/15/2054 | 5,000,000 | 4,785,198 | |||||

Waxahachie Independent School District, GO (Insured; Permanent School Fund Guarantee Program) | 4.25 | 2/15/2053 | 1,000,000 | 972,662 | |||||

50,910,907 | |||||||||

U.S. Related - 2.4% | |||||||||

Puerto Rico, GO, Ser. A1 | 5.63 | 7/1/2029 | 3,000,000 | 3,237,143 | |||||

Puerto Rico, GO, Ser. A1 | 5.63 | 7/1/2027 | 7,500,000 | 7,801,811 | |||||

11,038,954 | |||||||||

Utah - .7% | |||||||||

Salt Lake City Airport, Revenue Bonds, Ser. A | 5.00 | 7/1/2034 | 2,000,000 | 2,064,838 | |||||

Utah Telecommunication Open Infrastructure Agency, Revenue Bonds, Refunding | 5.50 | 6/1/2040 | 1,200,000 | 1,337,649 | |||||

3,402,487 | |||||||||

Virginia - 1.1% | |||||||||

Virginia Public Building Authority, Revenue Bonds, Ser. A | 4.00 | 8/1/2039 | 2,500,000 | 2,545,040 | |||||

Virginia Small Business Financing Authority, Revenue Bonds, Refunding, Ser. I | 5.00 | 12/31/2052 | 1,500,000 | 1,505,917 | |||||

Williamsburg Economic Development Authority, Revenue Bonds (William & Mary Project) (Insured; Assured Guaranty Municipal Corp.) Ser. A | 4.13 | 7/1/2058 | 1,250,000 | 1,165,978 | |||||

5,216,935 | |||||||||

Washington - 2.6% | |||||||||

Port of Seattle, Revenue Bonds, Refunding | 4.00 | 8/1/2047 | 1,500,000 | 1,358,168 | |||||

Tacoma Electric System, Revenue Bonds, Refunding (Sustainable Bond) Ser. A | 5.00 | 1/1/2054 | 1,250,000 | 1,322,332 | |||||

Washington, GO, Ser. B | 5.00 | 2/1/2043 | 2,710,000 | 2,969,548 | |||||

Washington Convention Center Public Facilities District, Revenue Bonds | 5.00 | 7/1/2058 | 2,450,000 | 2,484,520 | |||||

Washington Convention Center Public Facilities District, Revenue Bonds, Ser. B | 4.00 | 7/1/2058 | 2,000,000 | 1,710,923 | |||||

24

Description | Coupon

| Maturity Date | Principal Amount ($) | Value ($) | |||||

Long-Term Municipal Investments - 100.3% (continued) | |||||||||

Washington - 2.6% (continued) | |||||||||

Washington Housing Finance Commission, Revenue Bonds, Refunding (Emerald Heights Project) Ser. A | 5.00 | 7/1/2043 | 1,000,000 | 1,026,907 | |||||

Washington Housing Finance Commission, Revenue Bonds, Refunding (Seattle Academy of Arts & Sciences) | 6.38 | 7/1/2063 | 1,000,000 | b | 1,078,472 | ||||

11,950,870 | |||||||||

Wisconsin - 2.2% | |||||||||

Public Finance Authority, Revenue Bonds (Astro Texas Land Project) | 5.50 | 12/15/2028 | 1,250,000 | b | 1,253,581 | ||||

Public Finance Authority, Revenue Bonds (Cone Health) Ser. A | 5.00 | 10/1/2052 | 1,500,000 | 1,571,167 | |||||

Public Finance Authority, Revenue Bonds, Refunding (Duke Energy Progress) Ser. B | 4.00 | 10/1/2030 | 2,855,000 | a | 2,842,598 | ||||

Public Finance Authority, Revenue Bonds, Refunding (Renown Regional Medical Center Obligated Group) Ser. A | 5.00 | 6/1/2040 | 2,000,000 | 2,021,384 | |||||

Public Finance Authority, Revenue Bonds, Ser. 1 | 5.75 | 7/1/2062 | 2,350,000 | 2,525,052 | |||||

10,213,782 | |||||||||

Total Long-Term Municipal Investments | 459,230,220 | ||||||||

Total Investments (cost $470,982,212) | 100.7% | 460,991,196 | |||||||

Liabilities, Less Cash and Receivables | (0.7%) | (3,207,666) | |||||||

Net Assets | 100.0% | 457,783,530 | |||||||

a These securities have a put feature; the date shown represents the put date and the bond holder can take a specific action to retain the bond after the put date.

b Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2024, these securities were valued at $33,962,061 or 7.42% of net assets.

c The Variable Rate is determined by the Remarketing Agent in its sole discretion based on prevailing market conditions and may, but need not, be established by reference to one or more financial indices.

d Collateral for floating rate borrowings. The coupon rate given represents the current interest rate for the inverse floating rate security.

25

STATEMENT OF INVESTMENTS (continued)

Portfolio Summary (Unaudited) † | Value (%) |

General | 22.1 |

Airport | 11.0 |

Medical | 10.3 |

Education | 10.0 |

Development | 7.2 |

Transportation | 6.6 |

General Obligation | 5.7 |

Power | 5.4 |

Water | 4.7 |

School District | 4.3 |

Tobacco Settlement | 4.1 |

Nursing Homes | 3.7 |

Utilities | 2.3 |

Multifamily Housing | .9 |

Special Tax | .8 |

Student Loan | .7 |

Single Family Housing | .6 |

Facilities | .3 |

100.7 |

† Based on net assets.

See notes to financial statements.

26

Summary of Abbreviations (Unaudited) | |||

ABAG | Association of Bay Area Governments | AGC | ACE Guaranty Corporation |

AGIC | Asset Guaranty Insurance Company | AMBAC | American Municipal Bond Assurance Corporation |

BAN | Bond Anticipation Notes | BSBY | Bloomberg Short-Term Bank Yield Index |

CIFG | CDC Ixis Financial Guaranty | COP | Certificate of Participation |

CP | Commercial Paper | DRIVERS | Derivative Inverse Tax-Exempt Receipts |

EFFR | Effective Federal Funds Rate | FGIC | Financial Guaranty Insurance Company |

FHA | Federal Housing Administration | FHLB | Federal Home Loan Bank |

FHLMC | Federal Home Loan Mortgage Corporation | FNMA | Federal National Mortgage Association |

GAN | Grant Anticipation Notes | GIC | Guaranteed Investment Contract |

GNMA | Government National Mortgage Association | GO | General Obligation |

IDC | Industrial Development Corporation | LOC | Letter of Credit |

LR | Lease Revenue | NAN | Note Anticipation Notes |

MFHR | Multi-Family Housing Revenue | MFMR | Multi-Family Mortgage Revenue |

MUNIPSA | Securities Industry and Financial Markets Association Municipal Swap Index Yield | OBFR | Overnight Bank Funding Rate |

PILOT | Payment in Lieu of Taxes | PRIME | Prime Lending Rate |

PUTTERS | Puttable Tax-Exempt Receipts | RAC | Revenue Anticipation Certificates |

RAN | Revenue Anticipation Notes | RIB | Residual Interest Bonds |

SFHR | Single Family Housing Revenue | SFMR | Single Family Mortgage Revenue |

SOFR | Secured Overnight Financing Rate | TAN | Tax Anticipation Notes |

TRAN | Tax and Revenue Anticipation Notes | TSFR | Term Secured Overnight |

USBMMY | U.S. Treasury Bill Money Market Yield | U.S. T-BILL | U.S. Treasury Bill |

XLCA | XL Capital Assurance | ||

See notes to financial statements.

27

STATEMENT OF ASSETS AND LIABILITIES

April

30, 2024

|

|

|

|

|

|

|

|

|

| Cost |

| Value |

|

Assets ($): |

|

|

|

| ||

Investments in securities—See Statement of Investments | 470,982,212 |

| 460,991,196 |

| ||

Cash |

|

|

|

| 3,348,516 |

|

Interest receivable |

| 6,700,150 |

| |||

Receivable for shares of Beneficial Interest subscribed |

| 305,970 |

| |||

Prepaid expenses |

|

|

|

| 50,171 |

|

|

|

|

|

| 471,396,003 |

|

Liabilities ($): |

|

|

|

| ||

Due to BNY Mellon Investment Adviser, Inc. and affiliates—Note 3(c) |

| 205,646 |

| |||

Payable for inverse floater notes issued—Note 4 |

| 7,500,000 |

| |||

Payable for investment securities purchased |

| 4,811,500 |

| |||

Payable for shares of Beneficial Interest redeemed |

| 952,611 |

| |||

Interest

and expense payable related to |

| 41,789 |

| |||

Trustees’ fees and expenses payable |

| 3,076 |

| |||

Other accrued expenses |

|

|

|

| 97,851 |

|

|

|

|

|

| 13,612,473 |

|

Net Assets ($) |

|

| 457,783,530 |

| ||

Composition of Net Assets ($): |

|

|

|

| ||

Paid-in capital |

|

|

|

| 477,258,661 |

|

Total distributable earnings (loss) |

|

|

|

| (19,475,131) |

|

Net Assets ($) |

|

| 457,783,530 |

| ||

Net Asset Value Per Share | Class A | Class C | Class I | Class Y | Class Z |

|

Net Assets ($) | 132,643,891 | 3,468,265 | 199,136,882 | 37,754 | 122,496,738 |

|

Shares Outstanding | 11,055,730 | 288,377 | 16,591,969 | 3,147 | 10,209,431 |

|

Net Asset Value Per Share ($) | 12.00 | 12.03 | 12.00 | 12.00 | 12.00 |

|

|

|

|

|

|

|

|

See notes to financial statements. |

|

|

|

|

|

|

28

STATEMENT OF OPERATIONS

Year

Ended April 30, 2024

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment Income ($): |

|

|

|

| ||

Interest Income |

|

| 17,430,018 |

| ||

Expenses: |

|

|

|

| ||

Management fee—Note 3(a) |

|

| 1,619,599 |

| ||

Shareholder servicing costs—Note 3(c) |

|

| 838,158 |

| ||

Interest

and expense related to inverse |

|

| 165,289 |

| ||

Professional fees |

|

| 108,092 |

| ||

Registration fees |

|

| 100,908 |

| ||

Trustees’ fees and expenses—Note 3(d) |

|

| 53,306 |

| ||

Distribution fees—Note 3(b) |

|

| 28,400 |

| ||

Prospectus and shareholders’ reports |

|

| 25,755 |

| ||

Chief Compliance Officer fees—Note 3(c) |

|

| 20,359 |

| ||

Loan commitment fees—Note 2 |

|

| 12,240 |

| ||

Custodian fees—Note 3(c) |

|

| 9,498 |

| ||

Miscellaneous |

|

| 51,666 |

| ||

Total Expenses |

|

| 3,033,270 |

| ||

Less—reduction in fees due to earnings credits—Note 3(c) |

|

| (44,399) |

| ||

Net Expenses |

|

| 2,988,871 |

| ||

Net Investment Income |

|

| 14,441,147 |

| ||

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): |

|

| ||||

Net realized gain (loss) on investments | (2,223,693) |

| ||||

Net change in unrealized appreciation (depreciation) on investments | 2,156,351 |

| ||||

Net Realized and Unrealized Gain (Loss) on Investments |

|

| (67,342) |

| ||

Net Increase in Net Assets Resulting from Operations |

| 14,373,805 |

| |||

|

|

|

|

|

|

|

See notes to financial statements. | ||||||

29

STATEMENT OF CHANGES IN NET ASSETS

|

|

|

| Year Ended April 30, | |||||

|

|

|

| 2024 |

| 2023 |

| ||

Operations ($): |

|

|

|

|

|

|

|

| |

Net investment income |

|

| 14,441,147 |

|

|

| 12,731,211 |

| |

Net realized gain (loss) on investments |

| (2,223,693) |

|

|

| (7,832,079) |

| ||

Net

change in unrealized appreciation |

| 2,156,351 |

|

|

| 2,808,746 |

| ||

Net Increase

(Decrease) in Net Assets | 14,373,805 |

|

|

| 7,707,878 |

| |||

Distributions ($): |

| ||||||||

Distributions to shareholders: |

|

|

|

|

|

|

|

| |

Class A |

|

| (4,400,549) |

|

|

| (4,413,191) |

| |

Class C |

|

| (83,888) |

|

|

| (90,724) |

| |

Class I |

|

| (6,071,371) |

|

|

| (5,509,053) |

| |

Class Y |

|

| (1,238) |

|

|

| (1,140) |

| |

Class Z |

|

| (3,888,641) |

|

|

| (3,833,610) |

| |

Total Distributions |

|

| (14,445,687) |

|

|

| (13,847,718) |

| |

Beneficial Interest Transactions ($): |

| ||||||||

Net proceeds from shares sold: |

|

|

|

|

|

|

|

| |

Class A |

|

| 11,152,842 |

|

|

| 44,202,389 |

| |

Class C |

|

| 137,329 |

|

|

| 1,177,878 |

| |

Class I |

|

| 85,233,912 |

|

|

| 207,421,428 |

| |

Class Z |

|

| 1,262,814 |

|

|

| 904,549 |

| |

Distributions reinvested: |

|

|

|

|

|

|

|

| |

Class A |

|

| 3,910,657 |

|

|

| 3,912,381 |

| |

Class C |

|

| 83,700 |

|

|

| 90,724 |

| |

Class I |

|

| 6,048,498 |

|

|

| 5,482,981 |

| |

Class Z |

|

| 3,216,668 |

|

|

| 3,170,521 |

| |

Cost of shares redeemed: |

|

|

|

|

|

|

|

| |

Class A |

|

| (36,540,649) |

|

|

| (51,993,308) |

| |

Class C |

|

| (1,355,345) |

|

|

| (1,297,793) |

| |

Class I |

|

| (79,568,979) |

|

|

| (147,641,083) |

| |

Class Z |

|

| (14,958,949) |

|

|

| (12,497,483) |

| |

Increase

(Decrease) in Net Assets | (21,377,502) |

|

|

| 52,933,184 |

| |||

Total Increase (Decrease) in Net Assets | (21,449,384) |

|

|

| 46,793,344 |

| |||

Net Assets ($): |

| ||||||||

Beginning of Period |

|

| 479,232,914 |

|

|

| 432,439,570 |

| |

End of Period |

|

| 457,783,530 |

|

|

| 479,232,914 |

| |

30

|

|

|

| Year Ended April 30, | |||||

|

|

|

| 2024 |

| 2023 |

| ||

Capital Share Transactions (Shares): |

| ||||||||

Class Aa |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 937,210 |

|

|

| 3,717,469 |

| |

Shares issued for distributions reinvested |

|

| 328,245 |

|

|

| 328,961 |

| |

Shares redeemed |

|

| (3,076,429) |

|

|

| (4,369,471) |

| |

Net Increase (Decrease) in Shares Outstanding | (1,810,974) |

|

|

| (323,041) |

| |||

Class C |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 11,413 |

|

|

| 99,982 |

| |

Shares issued for distributions reinvested |

|

| 7,009 |

|

|

| 7,612 |

| |

Shares redeemed |

|

| (113,293) |

|

|

| (108,804) |

| |

Net Increase (Decrease) in Shares Outstanding | (94,871) |

|

|

| (1,210) |

| |||

Class Ia,b |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 7,154,241 |

|

|

| 17,338,674 |

| |

Shares issued for distributions reinvested |

|

| 506,960 |

|

|

| 461,008 |

| |

Shares redeemed |

|

| (6,679,678) |

|

|

| (12,363,537) |

| |

Net Increase (Decrease) in Shares Outstanding | 981,523 |

|

|

| 5,436,145 |

| |||

Class Zb |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 104,966 |

|

|

| 75,614 |

| |

Shares issued for distributions reinvested |

|

| 269,958 |

|

|

| 266,515 |

| |

Shares redeemed |

|

| (1,251,270) |

|

|

| (1,047,280) |

| |

Net Increase (Decrease) in Shares Outstanding | (876,346) |

|

|

| (705,151) |

| |||

|

|

|

|

|

|

|

|

|

|

a | During the period ended April 30, 2023, 45,328 Class A shares representing $525,906 were exchanged for 45,289 Class I shares. | ||||||||

b | During the period ended April 30, 2023, 5,913 Class Z shares representing $72,611 were exchanged for 5,908 Class I shares. | ||||||||

See notes to financial statements. | |||||||||

31

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated. All information (except portfolio turnover rate) reflects financial results for a single fund share. Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption at net asset value on the last day of the period. Net asset value total return includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. These figures have been derived from the fund’s financial statements.

Year Ended April 30, | |||||||||

Class A Shares | 2024 | 2023 | 2022 | 2021 | 2020 | ||||

Per Share Data ($): | |||||||||

Net asset value, beginning of period | 11.99 | 12.17 | 13.55 | 12.62 | 12.93 | ||||

Investment Operations: | |||||||||

Net investment incomea | .36 | .31 | .29 | .33 | .36 | ||||

Net realized and unrealized | .01 | (.16) | (1.33) | .96 | (.31) | ||||

Total from Investment Operations | .37 | .15 | (1.04) | 1.29 | .05 | ||||

Distributions: | |||||||||

Dividends from net investment | (.36) | (.30) | (.28) | (.33) | (.36) | ||||

Dividends from net realized | - | (.03) | (.06) | (.03) | − | ||||

Total Distributions | (.36) | (.33) | (.34) | (.36) | (.36) | ||||

Net asset value, end of period | 12.00 | 11.99 | 12.17 | 13.55 | 12.62 | ||||

Total Return (%)b | 3.15 | 1.40 | (7.92) | 10.27 | .32 | ||||

Ratios/Supplemental Data (%): | |||||||||

Ratio

of total expenses | .76 | .72 | .72 | .72 | .73 | ||||

Ratio of net expenses | .75 | .72 | .72 | .72 | .73 | ||||

Ratio

of interest and expense related | .04 | - | - | - | - | ||||

Ratio

of net investment income | 3.01 | 2.56 | 2.14 | 2.47 | 2.75 | ||||

Portfolio Turnover Rate | 20.10 | 21.69 | 9.69 | 9.40 | 21.90 | ||||

Net Assets, end of period ($ x 1,000) | 132,644 | 154,320 | 160,455 | 185,393 | 145,636 | ||||

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

32

Year Ended April 30, | ||||||||||

Class C Shares | 2024 | 2023 | 2022 | 2021 | 2020 | |||||

Per Share Data ($): | ||||||||||

Net asset value, beginning of period | 12.02 | 12.19 | 13.58 | 12.65 | 12.96 | |||||

Investment Operations: | ||||||||||

Net investment incomea | .27 | .21 | .18 | .23 | .26 | |||||

Net

realized and unrealized | .01 | (.14) | (1.33) | .96 | (.31) | |||||

Total from Investment Operations | .28 | .07 | (1.15) | 1.19 | (.05) | |||||

Distributions: | ||||||||||

Dividends from net investment | (.27) | (.21) | (.18) | (.23) | (.26) | |||||

Dividends

from net realized | - | (.03) | (.06) | (.03) | − | |||||

Total Distributions | (.27) | (.24) | (.24) | (.26) | (.26) | |||||

Net asset value, end of period | 12.03 | 12.02 | 12.19 | 13.58 | 12.65 | |||||

Total Return (%)b | 2.33 | .61 | (8.62) | 9.39 | (.46) | |||||

Ratios/Supplemental Data (%): | ||||||||||

Ratio

of total expenses | 1.55 | 1.51 | 1.50 | 1.51 | 1.51 | |||||

Ratio

of net expenses | 1.54 | 1.50 | 1.50 | 1.51 | 1.51 | |||||

Ratio

of interest and expense related | .04 | - | - | - | - | |||||

Ratio

of net investment income | 2.22 | 1.78 | 1.36 | 1.68 | 1.97 | |||||

Portfolio Turnover Rate | 20.10 | 21.69 | 9.69 | 9.40 | 21.90 | |||||

Net Assets, end of period ($ x 1,000) | 3,468 | 4,608 | 4,688 | 5,930 | 4,980 | |||||

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

33

FINANCIAL HIGHLIGHTS (continued)

Year Ended April 30, | ||||||||

Class I Shares | 2024 | 2023 | 2022 | 2021 | 2020 | |||

Per Share Data ($): | ||||||||

Net asset value, beginning of period | 12.00 | 12.17 | 13.55 | 12.62 | 12.93 | |||

Investment Operations: | ||||||||

Net investment incomea | .39 | .34 | .31 | .36 | .39 | |||

Net realized and unrealized | .00b | (.15) | (1.31) | .96 | (.30) | |||

Total from Investment Operations | .39 | .19 | (1.00) | 1.32 | .09 | |||

Distributions: | ||||||||

Dividends

from net investment | (.39) | (.33) | (.32) | (.36) | (.40) | |||

Dividends from net realized | - | (.03) | (.06) | (.03) | − | |||

Total Distributions | (.39) | (.36) | (.38) | (.39) | (.40) | |||

Net asset value, end of period | 12.00 | 12.00 | 12.17 | 13.55 | 12.62 | |||

Total Return (%) | 3.31 | 1.64 | (7.62) | 10.53 | .57 | |||

Ratios/Supplemental Data (%): | ||||||||

Ratio of total expenses | .52 | .49 | .48 | .49 | .48 | |||

Ratio

of net expenses | .51 | .48 | .48 | .49 | .48 | |||

Ratio of interest and expense related | .04 | - | - | - | - | |||

Ratio of net investment income | 3.26 | 2.80 | 2.38 | 2.71 | 2.97 | |||

Portfolio Turnover Rate | 20.10 | 21.69 | 9.69 | 9.40 | 21.90 | |||

Net Assets, end of period ($ x 1,000) | 199,137 | 187,299 | 123,812 | 72,900 | 55,013 | |||

a Based on average shares outstanding.

b Amount represents less than $.01 per share.

See notes to financial statements.

34

Year Ended April 30, | ||||||||

Class Y Shares | 2024 | 2023 | 2022 | 2021 | 2020 | |||

Per Share Data ($): | ||||||||

Net asset value, beginning of period | 11.99 | 12.16 | 13.55 | 12.62 | 12.93 | |||

Investment Operations: | ||||||||

Net investment incomea | .39 | .34 | .32 | .36 | .40 | |||

Net realized and unrealized | .01 | (.15) | (1.33) | .96 | (.31) | |||

Total from Investment Operations | .40 | .19 | (1.01) | 1.32 | .09 | |||

Distributions: | ||||||||

Dividends from net investment | (.39) | (.33) | (.32) | (.36) | (.40) | |||

Dividends from net realized | - | (.03) | (.06) | (.03) | − | |||

Total Distributions | (.39) | (.36) | (.38) | (.39) | (.40) | |||

Net asset value, end of period | 12.00 | 11.99 | 12.16 | 13.55 | 12.62 | |||

Total Return (%) | 3.44 | 1.65 | (7.69) | 10.54 | .57 | |||

Ratios/Supplemental Data (%): | ||||||||

Ratio of total expenses | .48 | .48 | .46 | .49 | .47 | |||

Ratio