UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the quarterly period ended

or

For the transition period from __________________ to __________________

Commission

file number:

(Exact Name Of Registrant As Specified In Its Charter)

| (State of | (I.R.S. Employer | |

| Incorporation) | Identification Number) |

| (Address of Principal Executive Officers) | (Zip Code) |

Registrant’s

Telephone Number, Including Area Code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer (as defined in Rule 12b-2 of the Exchange Act) or a smaller reporting company.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

On August 14, 2024, the Registrant had shares of common stock issued and outstanding.

| -2- |

VIEWBIX INC.

TABLE OF CONTENTS

| Item | Description | Page | ||

| PART I - FINANCIAL INFORMATION | ||||

| ITEM 1. | FINANCIAL STATEMENTS | 3 | ||

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS AND RESULTS OF OPERATIONS | 31 | ||

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 43 | ||

| ITEM 4. | CONTROLS AND PROCEDURES | 43 | ||

| PART II - OTHER INFORMATION | ||||

| ITEM 1. | LEGAL PROCEEDINGS | 43 | ||

| ITEM 1A. | RISK FACTORS | 43 | ||

| ITEM 2. | UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | 45 | ||

| ITEM 3. | DEFAULT UPON SENIOR SECURITIES | 45 | ||

| ITEM 4. | MINE SAFETY DISCLOSURE | 45 | ||

| ITEM 5. | OTHER INFORMATION | 45 | ||

| ITEM 6. | EXHIBITS | 45 | ||

| SIGNATURES | 46 |

| -3- |

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

June 30, 2024

CONTENTS

| -4- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

U.S. dollars in thousands (except share data)

As of June 30 | As of December 31 | |||||||||||

| Note | 2024 | 2023 | ||||||||||

| ASSETS | ||||||||||||

| CURRENT ASSETS | ||||||||||||

| Cash and cash equivalents | ||||||||||||

| Restricted deposits | ||||||||||||

| Accounts receivable | ||||||||||||

| Loan to parent company | 3 | |||||||||||

| Other current assets | ||||||||||||

| Total current assets | ||||||||||||

| NON-CURRENT ASSETS | ||||||||||||

| Deferred taxes | ||||||||||||

| Property and equipment, net | ||||||||||||

| Operating lease right-of-use asset | 4 | |||||||||||

| Intangible assets, net | 5 | |||||||||||

| Goodwill | 5 | |||||||||||

| Total non-current assets | ||||||||||||

| Total assets | ||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -5- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited) (Cont.)

U.S. dollars in thousands (except share data)

As of June 30 | As of December 31 | |||||||||||

| Note | 2024 | 2023 | ||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||||||

| CURRENT LIABILITIES | ||||||||||||

| Accounts payable | ||||||||||||

| Short-term loans | 6 | |||||||||||

| Current maturities of long-term loans | 6 | |||||||||||

| Embedded derivatives | 6,7 | |||||||||||

Short-term convertible loans | 6E | |||||||||||

| Other payables | ||||||||||||

| Operating lease liabilities - short term | 4 | |||||||||||

| Total current liabilities | ||||||||||||

| NON-CURRENT LIABILITIES | ||||||||||||

| Long-term loans, net of current maturities | 6 | |||||||||||

| Derivative warrant liability | 6,7 | |||||||||||

| Operating lease liabilities - long term | 4 | |||||||||||

| Deferred taxes | ||||||||||||

| Total non-current liabilities | ||||||||||||

| Commitments and Contingencies | 8 | |||||||||||

| SHAREHOLDERS’ EQUITY | 9 | |||||||||||

| Common stock of $ par value - Authorized: shares; Issued and outstanding: and shares as of June 30, 2024, and December 31, 2023, respectively. | ||||||||||||

| Additional paid-in capital | ||||||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||||||

| Equity attributed to shareholders of Viewbix Inc. | ||||||||||||

| Non-controlling interests | ||||||||||||

| Total equity | ||||||||||||

| Total liabilities and shareholders’ equity | ||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -6- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

U.S. dollars in thousands (except share data)

| For

the six months ended June 30, | For

the three months ended June 30, | |||||||||||||||||||

| Note | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||

| Revenues | ||||||||||||||||||||

| Costs and Expenses: | ||||||||||||||||||||

| Traffic-acquisition and related costs | ||||||||||||||||||||

| Research and development | ||||||||||||||||||||

| Selling and marketing | ||||||||||||||||||||

| General and administrative | ||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||

| Goodwill impairment | 6B | |||||||||||||||||||

| Other income | 1D,4 | ( | ) | ( | ) | |||||||||||||||

| Operating income (loss) | ( | ) | ( | ) | ||||||||||||||||

| Financial expense, net | 10 | |||||||||||||||||||

| Income (loss) before income taxes | ( | ) | ( | ) | ( | ) | ||||||||||||||

| Income tax expense (benefit) | ( | ) | ( | ) | ||||||||||||||||

| Net loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Less: net income (loss) attributable to non-controlling interests | ( | ) | ( | ) | ||||||||||||||||

| Net loss attributable to shareholders of Viewbix Inc. | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||

| Net income per share – Basic and diluted attributed to shareholders: | ) | ) | ) | ) | ||||||||||||||||

| Weighted average number of shares – Basic and diluted | ||||||||||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -7- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY (Unaudited)

U.S. dollars in thousands (except share data)

| Common stock | Additional paid-in | Accumulated | Total Attributed to the company’s | Non- Controlling | Total | |||||||||||||||||||||||

| Number | Amount | capital | Deficit | Shareholders | Interests | Equity | ||||||||||||||||||||||

| Balance as of January 1, 2024 | ( | ) | ||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||

| Share-based compensation | - | |||||||||||||||||||||||||||

Issuance of shares and warrants in connection with issuance of convertible loans (see 6.E) | (* | ) | ||||||||||||||||||||||||||

Receipts on account of shares and warrants (see note (see note 12.A) | - | |||||||||||||||||||||||||||

| Balance as of June 30, 2024 | ( | ) | ||||||||||||||||||||||||||

| Common stock | Additional paid-in | Accumulated | Total Attributed to the company’s | Non- Controlling | Total | |||||||||||||||||||||||

| Number | Amount | capital | Deficit | Shareholders | Interests | Equity | ||||||||||||||||||||||

| Balance as of April 1, 2024 | ( | ) | ||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||

| Share-based compensation | - | |||||||||||||||||||||||||||

Issuance of shares and warrants in connection with issuance of debt and convertible debt (see 6.E) | (* | ) | ||||||||||||||||||||||||||

Receipts on account of shares and warrants (see note (see note 12.A) | - | |||||||||||||||||||||||||||

| Balance as of June 30, 2024 | ( | ) | ||||||||||||||||||||||||||

| (*) |

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -8- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY (Unaudited)

U.S. dollars in thousands (except share data)

| Common stock | Additional paid-in | Accumulated | Total Attributed to the company’s | Non- Controlling | Total | |||||||||||||||||||||||

| Number | Amount | capital | Deficit | Shareholders | Interests | Equity | ||||||||||||||||||||||

| Balance as of January 1, 2023 | ( | ) | ||||||||||||||||||||||||||

| Net income (loss) | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Share-based compensation (see note 9.A) | ||||||||||||||||||||||||||||

| Transaction with the non-controlling interests (see note 1.C) | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Dividend declared to non-controlling interests | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance as of June 30, 2023 | ( | ) | ||||||||||||||||||||||||||

| Common stock | Additional paid-in | Accumulated | Total Attributed to the company’s | Non- Controlling | Total | |||||||||||||||||||||||

| Number | Amount | capital | Deficit | Shareholders | Interests | Equity | ||||||||||||||||||||||

| Balance as of April 1, 2023 | ( | ) | ||||||||||||||||||||||||||

| Net income (loss) | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Share-based compensation (see note 9.A) | ||||||||||||||||||||||||||||

| Dividend declared to non-controlling interests | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance as of June 30, 2023 | ( | ) | ||||||||||||||||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -9- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

U.S. dollars in thousands (except share data)

| For the six months ended June 30, | For the three months ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Cash flows from Operating Activities | ||||||||||||||||

| Net loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||||||

| Depreciation and amortization | ||||||||||||||||

| Share-based compensation | ||||||||||||||||

| Deferred taxes | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Accrued interest, net | ( | ) | ||||||||||||||

| Interest income | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Amortization of loan discount | ||||||||||||||||

Amortization of deferred debt issuance costs (see note 6.E) | ||||||||||||||||

| Goodwill Impairment | ||||||||||||||||

Equity based debt issuance costs (see note 6.E) | ||||||||||||||||

Loss from substantial debt terms modification (see note 6.E) | ||||||||||||||||

| Loss on sale and disposal of property and equipment | ||||||||||||||||

Loss from termination of lease agreement | ||||||||||||||||

| Changes in assets and liabilities items: | ||||||||||||||||

| Decrease (increase) in accounts receivable | ( | ) | ||||||||||||||

| Decrease (increase) in other current assets | ( | ) | ||||||||||||||

| Decrease (increase) in operating lease right-of-use asset | ( | ) | ||||||||||||||

| Decrease in severance pay, net | ( | ) | ( | ) | ||||||||||||

| Increase (decrease) in accounts payable | ( | ) | ( | ) | ||||||||||||

| Decrease (increase) in other payables | ( | ) | ( | ) | ||||||||||||

| Decrease in operating lease liabilities | ( | ) | ( | ) | ||||||||||||

| Net cash provided by operating activities | ||||||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -10- |

VIEWBIX INC.

INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited) (Cont.)

U.S. dollars in thousands (except share data)

| For the six months ended June 30, | For the three months ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Cash flows from Investing Activities | ||||||||||||||||

| Purchase of property and equipment | ( | ) | ( | ) | ||||||||||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||||||||||

| Cash flows from Financing Activities | ||||||||||||||||

| Cash paid to non-controlling interests (see note 1.C) | ( | ) | ||||||||||||||

| Receipt of short-term bank loan | ||||||||||||||||

| Receipt of short-term loan | ||||||||||||||||

| Repayment of short-term loans | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Receipt of long-term loans (see note 6.B) | ||||||||||||||||

| Repayment of long-term bank loans | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Payment of dividend to non-controlling interests | ( | ) | ( | ) | ||||||||||||

| Payment of dividend to shareholders (see note 9.E.1) | ( | ) | ||||||||||||||

| Increase in loan to parent company | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

Receipts on account of shares and warrants (see note 12.A) | ||||||||||||||||

| Net cash provided by (used in) financing activities | ( | ) | ( | ) | ( | ) | ||||||||||

| Increase (decrease) in cash and cash equivalents and restricted cash | ( | ) | ( | ) | ( | ) | ||||||||||

| Cash and cash equivalents and restricted cash at beginning of period | ||||||||||||||||

| Cash and cash equivalents and restricted cash at end of period | ||||||||||||||||

| Supplemental Disclosure of Cash Flow Activities: | ||||||||||||||||

| Cash paid during the period | ||||||||||||||||

| Taxes paid | ||||||||||||||||

| Interest paid | ||||||||||||||||

| Substantial non-cash activities: | ||||||||||||||||

| Deemed extinguishment and re-issuance of debt (see note 6.B) | ||||||||||||||||

Termination of operating lease agreement (see note 4) | ||||||||||||||||

| Share-based compensation to a director (see note 9.A) | ||||||||||||||||

The accompanying notes are an integral part of these Interim Condensed Consolidated financial statements.

| -11- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 1: GENERAL

A. Organizational Background

Viewbix Inc. (formerly known as Virtual Crypto Technologies, Inc.) (the “Company”) was incorporated in the State of Delaware on August 16, 1985, under a predecessor name, The InFerGene Company (“InFerGene Company”). On August 25, 1995, a wholly owned subsidiary of InFerGene Company merged with Zaxis International, Inc., an Ohio corporation, which following such merger, the surviving entity, InFerGene Company, changed its name to Zaxis International, Inc (“Zaxis”). In 2015 the Company changed its name to Emerald Medical Applications Corp., subsequent to which the Company, through its subsidiary, was engaged in the development of technology for use in detection of skin cancer. On January 29, 2018, the Company ceased its business operations in this field.

On

January 17, 2018, the Company formed a new wholly owned subsidiary under the laws of the State of Israel, Virtual Crypto Technologies

Ltd. (“VCT Israel”), to develop and market software and hardware products facilitating and supporting the purchase and/or

sale of cryptocurrencies. Effective as of March 7, 2018, the Company’s name was changed from Emerald Medical Applications Corp.

to Virtual Crypto Technologies, Inc. VCT Israel ceased its business operation in 2019 and prior to consummation of the Recapitalization

Transaction. On January 27, 2020, VCT Israel was sold to a third party for NIS

On February 7, 2019, the Company entered into a share exchange agreement (the “Share Exchange Agreement” or the “Recapitalization Transaction”) with Gix Internet Ltd., a company organized under the laws of the State of Israel (“Gix” or “Parent Company’’), pursuant to which, Gix assigned, transferred and delivered its % holdings in Viewbix Ltd., a company organized under the laws of the State of Israel (“Viewbix Israel”), to the Company in exchange for shares of the Company, which resulted in Viewbix Israel becoming a subsidiary of the Company. In connection with the Share Exchange Agreement, effective as of August 7, 2019, the Company’s name was changed from Virtual Crypto Technologies, Inc. to Viewbix Inc.

B. Reorganization Transaction

On

December 5, 2021, the Company entered into a certain Agreement and Plan of Merger with Gix Media Ltd. (“Gix Media”), an Israeli

company and the majority-owned (

On

September 19, 2022, (the “Closing Date”) the Reorganization Transaction was consummated and as a result, all outstanding

ordinary shares of Gix Media, having no par value (the “Gix Media Shares”) were delivered to the Company in exchange for

the Company’s shares of common stock, par value $ per share (“Common Stock”).

| -12- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 1: GENERAL (Cont.)

B. Reorganization Transaction (Cont.)

In

connection with the Closing of the Reorganization Transaction, the Company filed an Amended and Restated Certificate of Incorporation

(the “Amended COI”) with the Secretary of State of Delaware, effective as of August 31, 2022, pursuant to which, concurrently

with the effectiveness of the Amended COI, the Company, among other things, effected a

As the Company and Gix Media Ltd. were consolidated both by the Parent Company and Medigus Ltd. (the “Ultimate Parent”), before and after the Reorganization Transaction, the Reorganization Transaction was accounted for as a transaction between entities under common control. Accordingly, the financial information of the Company and Gix Media Ltd. is presented in these financial statements, for all periods presented, reflecting the historical cost of the Company and Gix Media Ltd., as it is reflected in the consolidated financial statements of the Parent Company, for all periods preceding March 1, 2022, the date the Ultimate Parent obtained a controlling interest in the Parent Company and as it is reflected in the consolidated financial statements of the Ultimate Parent for all periods subsequent to March 1, 2022.

C. Business Overview

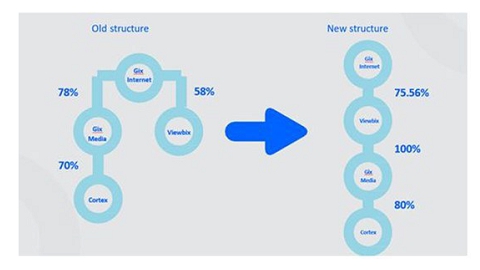

The Company and its subsidiaries (the “Group”), Gix Media and Cortex Media Group Ltd. (“Cortex”), operate in the field of digital advertising. The Group has two main activities that are reported as separate operating segments: the search segment and the digital content segment.

The search segment develops a variety of technological software solutions, which perform automation, optimization, and monetization of internet campaigns, for the purposes of obtaining and routing internet user traffic to its customers. The search segment activity is conducted by Gix Media.

The digital content segment is engaged in the creation and editing of content, in different languages, for different target audiences, for the purposes of generating revenues from leading advertising platforms, including Google, Facebook, Yahoo and Apple, by utilizing such content to obtain and route internet user traffic for its customers. The digital content segment activity is conducted by Cortex.

On

January 23, 2023, Gix Media acquired an additional

The Subsequent Purchase was recorded as a transaction with non-controlling interests in the Company’s statement of changes in shareholders equity for the six months ended June 30, 2023.

| -13- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 1: GENERAL (Cont.)

D. Impact of the “Iron Swords” War on Israel

On October 7, 2023, following the brutal attacks on Israel by Hamas, a terrorist organization located in the Gaza Strip that infiltrated Israel’s southern border and conducted a series of attacks on civilian and military targets, Israel’s security cabinet declared war (the “War”). Following the commencement of the War, hostilities also intensified between Israel and Hezbollah, a terrorist organization located in Lebanon. This may escalate in the future into a greater regional conflict. The War led to a reduction of business activities in Israel, evacuation of residences located in the northern and southern borders of Israel, a significant call up of military reserves and lower availability of work force.

As

the Group’s customers are mainly in the US and Europe, its operations, revenues, and profitability were indirectly affected due

to recruitment of senior employees to military reserves for an extended period of time. In January 2024, the Gix Media and Cortex filed

a request with the Israeli Tax Authority (the “ITA”) to receive compensation for the decrease in revenues related to the

War. In April and May 2024, Gix Media and Cortex received a total of $

As of the date of these financial statements the war is still on going. Therefore, there is no assurance that future developments of the War will not have any impact for reasons beyond the Company’s control, such as expansion of the War to additional regions and the recruitment of more senior employees. The Company has business continuity procedures in place, and will continue to follow developments, assessing potential impact, if any, on the Company’s business, financials, and operations.

E. Cortex Adverse Effect

In

April 2024, the Company was informed by Cortex that a significant customer of Cortex recently notified Cortex it will stop advertising

on Cortex’s sites, as part of its policy decision to cease advertising on Made for Advertising (“MFA”) sites (the “Cortex

Adverse Effect”). The Cortex Adverse Effect, which has materially affected Cortex’s business and operations, has occurred

following certain recent developments relating to publishers that are categorized by a number of on-line advertisers as MFA, including

decisions made by leading media on-line advertisers to prioritize different media categories and implement publishing restrictions in

connection with MFA. Due to the Cortex Adverse Effect and additional circumstances as explained in note 5.B, the Company recorded an impairment

of $

| -14- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 1: GENERAL (Cont.)

F. Going Concern

During the second half of 2023 and the six months ended June 30, 2024 the

Company experienced a decrease in its revenues from the digital content and search segments, as a result of the Cortex Adverse effect

(see note 1.E), a decrease in user traffic acquired from third party advertising platforms, an industry-wide decrease in advertising budget,

changes and updates to internet browsers’ technology, which adversely impacted the Company’s ability to acquire traffic in

the search segment and a decrease in revenues from routing of traffic acquired from third-party strategic partners in the search segment,

as a result of lack of availability of suppliers credit from such third party strategic partners. As a result of the foregoing, during

the six months ended June 30, 2024, the Company recorded an operating loss of $

The decline in revenues and other circumstances described above raise substantial doubts about the Company’s ability to continue as a going concern during the 12-month period following the issuance date of these financial statements.

Management’s response to these conditions included reduction of salaries

and related expenses and reduction of professional services in the research and development, selling and marketing functions, reduction

of other operational expenses, such as lease costs and overheads, as well as creation of new partnerships and other new income sources.

In addition, during the three months ended June 30, 2024, the company entered into a facility agreement (see Note 6.E) and subsequent

to the balance sheet date raised through a private placement and through two additional facility agreements with certain investors and

lenders (see note 12) aggregate gross proceeds of $

These financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern.

| -15- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. Unaudited Interim Financial Statements

The accompanying unaudited interim condensed financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of U.S. Securities and Exchange Commission Regulation S-X. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of management, all adjustments considered necessary for a fair presentation have been included (consisting only of normal recurring adjustments except as otherwise discussed). For further information, reference is made to the consolidated financial statements and footnotes thereto included in the Group’s Annual Report on Form 10-K for the year ended December 31, 2023.

B. Principles of Consolidation

The accompanying condensed consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation.

C. Use of estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expenses during the reporting period. The Company evaluates on an ongoing basis its assumptions, including those related to contingencies, deferred taxes, inventory impairment, stock-based compensation, as well as in estimates used in applying the revenue recognition policy. Actual results may differ from those estimates.

D. Derivative Financial Instruments

The Company evaluates its financial instruments to determine if such instruments are derivatives or contain features that qualify as embedded derivatives in accordance with ASC Topic 815, “Derivatives and Hedging”. Derivative instruments are initially recorded at fair value on the grant date and re-valued at each reporting date, with changes in the fair value reported in the unaudited condensed statements of operations.

E. Fair Value of Financial Instruments

Fair value is defined as the price that would be received for sale of an asset or paid to transfer of a liability, in an orderly transaction between market participants at the measurement date. US GAAP establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). These tiers include:

| ● | Level 1, defined as observable inputs such as quoted prices (unadjusted) for identical instruments in active markets. |

| ● | Level 2, defined as inputs other than quoted prices in active markets that are either directly or indirectly observable such as quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in markets that are not active; and |

| ● | Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions, such as valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable. |

F. Significant Accounting Policies

The significant accounting policies followed in the preparation of these unaudited interim condensed consolidated financial statements are identical to those applied in the preparation of the latest annual financial statements other than the significant accounting policies of derivative financial instruments and fair value of financial instruments (see notes 2.D and 2.E above).

G. Recent Accounting Pronouncements

Management does not believe that any recently issued, but not yet effective, accounting standards, if currently adopted, would have a material effect on the Group’s interim condensed consolidated financial statements.

| -16- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 3: LOAN TO PARENT COMPANY

As of June 30 2024 | As of December 31 2023 | |||||||

| Loan to Parent Company | $ | $ | ||||||

The balance with the Parent Company represents a balance of an intercompany loan under a loan agreement signed between Gix Media and the Parent Company on March 22, 2020. The loan bears interest at a rate to be determined from time to time in accordance with Section 3(j) of the Income Tax Ordinance, new version, and the Income Tax Regulations (Determination of Interest Rate for the purposes of Section 3(j), 1986) or according to a market interest rate decision as agreed between the parties. The amount of the loan is in U.S. dollars. On March 20, 2024, the Company’s board of directors approved to extend the loan between Gix Media and the Parent Company by 6 months until July 1, 2024. All other terms and conditions of the loan remained unchanged.

For

the six months ended June 30, 2024 and 2023, Gix Media recognized interest income in the amount of $

NOTE 4: LEASES

On

February 25, 2021, Gix Media entered into a lease agreement for a new corporate office of

The

Company includes renewal options that it is reasonably certain to exercise in the measurement of the lease liabilities. In December 2023,

the Company exercised the option to extend the lease period for an additional term of 24 months (from March 1, 2024, to

On June 20, 2024, Gix Media

and the lessor of its offices entered into a lease termination agreement. According to the agreement, the lease, which originally had

a termination date of February 28, 2026, terminated on June 30, 2024. In compensation for the lessor’s consent to early termination

Gix Media paid to the lessor $

As a result of the early termination of the agreement, the Company recorded

a capital loss of $

| -17- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 5: GOODWILL AND INTANGIBLE ASSETS, NET

| A. | Composition: |

| Internal-use Software | Customer Relations | Technology | Goodwill | Total | ||||||||||||||||

| Cost: | ||||||||||||||||||||

| Balance as of January 1, 2024 | ||||||||||||||||||||

| Additions | ||||||||||||||||||||

| Impairment of goodwill | ( | ) | ( | ) | ||||||||||||||||

| Balance as of June 30, 2024 | ||||||||||||||||||||

| Accumulated amortization: | ||||||||||||||||||||

| Balance as of January 1, 2024 | ||||||||||||||||||||

| Amortization recognized during the period | ||||||||||||||||||||

| Balance as of June 30, 2024 | ||||||||||||||||||||

| Amortized cost: | ||||||||||||||||||||

| As of June 30, 2024 | ||||||||||||||||||||

| Internal-use Software | Customer Relations | Technology | Goodwill | Total | ||||||||||||||||

| Cost: | ||||||||||||||||||||

| Balance as of January 1, 2023 | ||||||||||||||||||||

| Additions | ||||||||||||||||||||

| Impairment of goodwill | ( | ) | ( | ) | ||||||||||||||||

| Balance as of December 31, 2023 | ||||||||||||||||||||

| Accumulated amortization: | ||||||||||||||||||||

| Balance as of January 1, 2023 | ||||||||||||||||||||

| Amortization recognized during the year | ||||||||||||||||||||

| Balance as of December 31, 2023 | ||||||||||||||||||||

| Amortized cost: | ||||||||||||||||||||

| As of December 31, 2023 | ||||||||||||||||||||

| -18- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 5: GOODWILL AND INTANGIBLE ASSETS, NET (Cont.)

| B. | Impairment of goodwill: |

As

of June 30, 2024, the Company identified indicators of impairment of the digital content reporting unit. As a result, the Company

performed an impairment test which included a quantitative analysis of the fair value of the reporting unit. The fair value was

estimated using the income approach, which is based on the present value of the future cash flows attributable to the reporting

unit. The Company compared the fair value of the reporting unit to its carrying amount. As the carrying amount exceeded the fair

value, the Company recognized an impairment loss of $

As

of December 31, 2023, the Company recognized an impairment loss of $

NOTE 6: LOANS

| A. | Composition of long-term and short-term loans of the Group: |

| Interest rate | As of June 30, 2024 | As of December 31, 2023 | ||||||||||

| Short-term bank loan – Gix Media | % | |||||||||||

| Short-term bank loan – Gix Media (received on June 13, 2024) | % | |||||||||||

| Short-term bank loan – Cortex | % | |||||||||||

| Long-term bank loan, including current maturity – Gix Media (received on October 13, 2021) | % | |||||||||||

| Long-term bank loan, including current maturity – Gix Media (received on January 17, 2023) | % | |||||||||||

| Long-term loan – Viewbix Israel | % | |||||||||||

Short-term convertible loan - June 2024 Facility Agreement – Viewbix Inc | % | |||||||||||

| B. | Gix Media’s Loan Agreement |

On

January 23, 2023, Gix Media acquired an additional

On

June 13, 2024, Gix Media and Leumi entered into an addendum to an existing loan agreement between the parties which was be effective

from May 15, 2024, pursuant to which, inter alia: (i) the addendum will be effective until August 31, 2024; (ii) the Company is

obligated to transfer to Gix Media $

| C. | Cortex’s Loan Agreement: |

On

September 21, 2022, Cortex and Leumi entered into an addendum to an existing loan agreement between the parties, dated August 15, 2020

(“Cortex Loan Agreement”). As part of the addendum to the Cortex Loan Agreement, Leumi provided Cortex with a monthly renewable

credit line of $

On

April 27, 2023, Leumi increased the Cortex Credit Line by $

On

May 27, 2024, Cortex and Leumi entered into an amendment to Cortex Loan Agreement, pursuant to which, the credit facility to Cortex will

be

As

of June 30, 2024, Cortex has drawn $

| -19- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 6: LOANS (Cont.)

| D. | Long term loan and issuance of warrants: |

On November 15, 2023, Viewbix Israel entered

into a Loan Agreement (the “2023 Loan”) with certain lenders (the “Lenders”) whereby the Lenders provided Viewbix

Israel with loans in the aggregate amount of $

The terms of the 2023 Loan were substantially amended on June 18, 2024, by the June 2024 Facility Agreement (see note 6.E). These amendments represent a substantial modification in accordance with ASC Topic 470. Accordingly, the terms modification was accounted for as an extinguishment of the original financial liability and the initial recognition of new financial instruments issued at their fair value as of the effective date of the June 2024 Facility Agreement. As a result of the substantial modification of terms, the Company recognized finance expense of $2,515 in its interim condensed consolidated statement of operations for the six months period ended June 30, 2024.

| -20- |

NOTE 6: LOANS (Cont.)

| E. | June 2024 Facility Agreement: |

On

June 18, 2024, the Company entered into a credit facility agreement which was amended and restated on July 22, 2024 (the “June

2024 Facility Agreement”) for a $

The

term (the “June 2024 Facility Term”) of the June 2024 Facility Agreement expires

The

June 2024 Facility Loan Amount accrues interest at a rate of

Immediately

following the effectiveness of the Uplist, (i) $

The

June 2024 Facility Warrants are exercisable upon issuance at an exercise price of $

In

addition and in connection with the June 2024 Facility Agreement, the Company agreed to pay the June 2024 Lead Lender a commission consisting

of (i) shares of common stock, (ii) a warrant in substantially the same form and on substantially the same terms as the June

2024 Facility Warrant to purchase

The conversion and conversion related features of the June 2024 facility loan were bifurcated from their host debt contract and recognized as liabilities measured at fair value at each cut-off date. The facility loan was initially recorded at its fair value and subsequently measured at cost. The shares and Warrants A issued as prepayment of interest and as commission to the 2024 Lead Lender were initially recognized at fair value and classified in equity. The June 2024 Lead Lender Warrant was initially recognized at fair value and classified as a liability measured at fair value at each cut-off date (see note 7).

| -21- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 7: FINANCIAL INSTRUMENTS AT FAIR VALUE

Financial instruments:

The Company has financial instruments measured at level 3 from the June 2024 Facility Agreement (see note 6.E).

The

fair value of the financial instruments under the June 2024 Facility Agreement, as of June 18, 2024, was

calculated using the following unobservable inputs: share price: $, expected volatility:

The fair value of the financial instruments estimated by the Company’s management as of June 30 and June 18, 2024, was substantially the same.

The following table presents the financial liabilities that were measured at fair value through profit or loss:

June 30, 2024 | December 31, 2023 | |||||||

| Level 3 | Level 3 | |||||||

| Embedded derivatives | ||||||||

| Derivative warrant liability | ||||||||

NOTE 8: COMMITMENTS AND CONTINGENCIES

Liens:

On September 19, 2022, as part of the Reorganization Transaction terms, the Company has provided several liens under Gix Media’s Financing Agreement with Leumi in connection with the Cortex Transaction, as follows: (1) a guarantee to Bank Leumi of all of Gix Media’s obligations and undertakings to Bank Leumi unlimited in amount; (2) a subordination letter signed by the Company to Leumi Bank; (3) A first ranking all asset charge over all of the assets of the Company; and (4) a Deposit Account Control Agreement over the Company’s bank accounts.

Gix Media has provided several liens under the Financing Agreement with Leumi in connection with the Cortex Transaction, as follows: (1) a floating lien on Gix Media’s assets; (2) a lien on Gix Media’s bank account in Leumi; (3) a lien on Gix Media’s rights under the Cortex Transaction; (4) a fixed lien on Gix Media’s intellectual property; and (5) a lien on Gix Media’s full holdings in Cortex.

Gix

Media restricted deposits in the amount of $

NOTE 9: SHAREHOLDERS’ EQUITY

A. Shares of Common Stock:

On May 18, 2023, the Company’s Board of Directors (the “Board”) approved to issue and grant shares of restricted Common Stock (“Equity Grant”) to one of the Company’s directors (the “Director”). The Equity Grant was granted for consulting services provided to the Company by the Director, specifically in connection with securing favorable terms for a bank financing. The Company recorded a share-based compensation expense of $ in general and administrative expenses in connection to the Equity Grant.

On

June 18, 2024, as part of the June 2024 Facility Agreement the Company issued to June 2024 Lenders shares of common stock and

warrant to purchase shares of common stock with an exercise price of $

B. Warrants:

The following table summarizes information of outstanding warrants as of June 30, 2024:

| Warrants | Warrant Term | Exercise Price | Exercisable | |||||||||||

| Class J Warrants | ||||||||||||||

| Class K Warrants | ||||||||||||||

| 2023 Warrants (see note 6.D) | ||||||||||||||

| June 2024 Facility Agreement Warrants | ||||||||||||||

| June 2024 Lead Lender Warrants (see note 12.B) | ||||||||||||||

| -22- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 9: SHAREHOLDERS’ EQUITY (Cont.)

C. Share option plan

In 2017, after the completion of Gix Media’s acquisition by the Parent Company, the Parent Company granted options to Gix Media’s employees. These options entitle the employees to purchase ordinary shares of the Parent Company that are traded on Tel-Aviv Stock Exchange.

On

March 2, 2023, the Board approved the adoption of the 2023 Stock Incentive Plan (the “2023 Plan”). The 2023 Plan permits

the issuance of up to (i) shares of Common Stock, plus (ii) an annual increase equal to the lesser of (A)

The 2023 Plan provides for the grant of stock options, restricted stock, restricted stock units, stock or other stock-based awards, under various tax regimes, including, without limitation, in compliance with Section 102 and Section 3(i) of the Israeli Income Tax Ordinance (New Version) 5271-1961, and for awards granted to United States employees or service providers, including those who are deemed to be residents of the United States for tax purposes, Section 422 and Section 409A of the United States Internal Revenue Code of 1986.

In connection with the adoption of the 2023 Plan, on March 7, 2023, the Company entered into certain intercompany reimbursement agreements with two of its subsidiaries, Viewbix Israel and Gix Media (the “Recharge Agreements”). The Recharge Agreements provide for the offer of awards under the 2023 Plan to employees or service providers of Viewbix Israel and Gix Media (the “Affiliates”) under the 2023 Plan. Under the Recharge Agreements, the Affiliates will each bear the costs of awards granted to its employees or its service providers under the 2023 Plan and will reimburse the Company upon the issuance of shares of Common Stock pursuant to an award, for the costs of shares issued, but in any event not prior to the vesting of an award. The reimbursement amount will be equal to the lower of (a) the book expense for such award as recorded on the financial statements of one of the respective Affiliates, determined and calculated according to U.S. GAAP, or any other financial reporting standard that may be applicable in the future, or (b) the fair value of the shares of Common Stock at the time of exercise of an option or at the time of vesting of an RSU, as applicable.

On July 20, 2023, the Company granted restricted share units (the “RSUs”) under the 2023 Plan to Gix Media’s CEO, as part of his employment terms, (the “Grantee”) under the following terms and conditions:

| -23- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 9: SHAREHOLDERS’ EQUITY (Cont.)

C. Share option plan (Cont.)

On July 1, 2023, following the Grant and upon the vesting of the First Tranche, the Company issued shares of Common Stock to the Grantee. The Company recorded a share-based compensation expense of $ in general and administrative expenses with connection to the issuance of shares upon the vesting of the First Tranche. Subsequent to the balance sheet date, upon the vesting of the Second Tranche, the Company issued shares of Common Stock to the Grantee (see note 12.G).

D. Dividends:

On

September 14, 2022, Gix Media declared a dividend to its shareholders prior to the consummation of the Reorganization Transaction in

the amount of $

On

December 25, 2022, Cortex declared a dividend in the total amount of $

dividends were distributed during the six-month period ending June 30, 2024.

| -24- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 10: FINANCIAL EXPENSE, NET

| For the six months ended June 30, | For the three months ended June 30, | |||||||||||||||

| 2024 | 2023 | 2024 | 2023 | |||||||||||||

| Financial expense (income): | ||||||||||||||||

| Bank fees | ||||||||||||||||

| Exchange rate differences | ( | ) | ( | ) | ||||||||||||

| Interest expense on bank loans | ||||||||||||||||

| Loss from substantial debt terms modification | ||||||||||||||||

| Interest income on loans from Parent Company | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other | ( | ) | ( | ) | ||||||||||||

| Financial expense, net | ( | ) | ||||||||||||||

NOTE 11: SEGMENT REPORTING

The

Group operates in

Search segment- the search segment develops a variety of technological software solutions, which perform automation, optimization and monetization of internet campaigns, for the purposes of obtaining and routing internet user traffic to its customers.

Digital content segment- the digital content segment is engaged in the creation and editing of content, in different languages, for different target audiences, for the purposes of generating revenues from leading advertising platforms, including Google, Facebook, Yahoo and Apple, by utilizing such content to obtain internet user traffic for its customers.

The segments’ results include items that directly serve and/or are used by the segment’s business activity and are directly allocated to the segment. As such they do not include depreciation and amortization expenses for intangible assets created at the time of the purchase of those companies, financing expenses created for loans taken for the purpose of purchasing those companies and therefore these items are not allocated to the various segments.

Segments’ assets and liabilities are not reviewed by the Group’s chief operating decision maker and therefore were not reflected in the segment reporting.

Segments revenues and operating results:

| For the six months ended June 30, 2024 | ||||||||||||||||

| Search segment | Digital content segment | Adjustments (See below) | Total | |||||||||||||

| Revenues from external customers | ||||||||||||||||

| Depreciation and amortization | ||||||||||||||||

| Goodwill Impairment | ||||||||||||||||

| Segment operating income (loss) | ( | ) | ( | ) | ( | ) | ||||||||||

| Financial expenses, net | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Segment Income (loss), before income taxes | ( | ) | ( | ) | ( | ) | ||||||||||

| For the six months ended June 30, 2023 | ||||||||||||||||

| Search segment | Digital content segment | Adjustments (See below) | Total | |||||||||||||

| Revenues from external customers | ||||||||||||||||

| Depreciation and amortization | ||||||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||

| Financial expenses, net | ( | ) | ( | ) | ( | ) (*) | ( | ) | ||||||||

| Segment Income (loss), before income taxes | ( | ) | ( | ) | ||||||||||||

| -25- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 11: SEGMENT REPORTING (Cont.)

| For the three months ended June 30, 2024 | ||||||||||||||||

| Search segment | Digital content segment | Adjustments (See below) | Total | |||||||||||||

| Revenues from external customers | ||||||||||||||||

| Depreciation and amortization | ||||||||||||||||

| Goodwill Impairment | ||||||||||||||||

| Segment operating income (loss) | ( | ) | ( | ) | ||||||||||||

| Financial expenses, net | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Segment Income (loss), before income taxes | ( | ) | ( | ) | ||||||||||||

| For the three months ended June 30, 2023 | ||||||||||||||||

| Search segment | Digital content segment | Adjustments (See below) | Total | |||||||||||||

| Revenues from external customers | ||||||||||||||||

| Depreciation and amortization | ||||||||||||||||

| Segment operating income (loss) | ( | ) | ||||||||||||||

| Financial expenses, net | ( | ) | ( | ) | ( | ) (*) | ( | ) | ||||||||

| Segment Income (loss), before income taxes | ( | ) | ||||||||||||||

The “adjustment” column for segment operating income includes unallocated selling, general, and administrative expenses and certain items which management excludes from segment results when evaluating segment performance, as follows:

For the six June 30, 2024 | For the three June 30, 2024 | |||||||

| Depreciation and amortization expenses not attributable to segments (**) | ( | ) | ( | ) | ||||

| General and administrative not attributable to the segments (***) | ( | ) | ( | ) | ||||

| Goodwill Impairment | ( | ) | ( | ) | ||||

| ( | ) | ( | ) | |||||

| -26- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 11: SEGMENT REPORTING (Cont.)

For the six June 30, 2023 | For the three June 30, 2023 | |||||||

| Depreciation and amortization expenses not attributable to segments (**) | ( | ) | ( | ) | ||||

| General and administrative not attributable to the segments (***) | ( | ) | ( | ) | ||||

| ( | ) | ( | ) | |||||

| (*) | Mainly consist of financial expenses from the Financing Agreement of bank loans taken for business combinations (see note 6). |

| (**) | ||

| (***) |

| -27- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 12: SUBSEQUENT EVENTS

A. Private Placement

On

July 3, 2024, the Company entered into a definitive securities purchase agreement (the “Purchase Agreement”) with a certain

investor (the “Lead Investor”) for the purchase and sale in a private placement (the “Private Placement”) of

units consisting of (i) shares of the Company’s common stock at a purchase price of $ per share (the “PIPE

Shares”) and (ii) common stock purchase warrants to purchase up to

The

aggregate gross proceeds received by the Company from the Private Placement were $

Upon

the closing of the Private Placement, the Company agreed to pay the Lead Investor: (1) $

In July 2024, the Company issued to the Investors 1,027,500 shares of common stock and 1,541,250 warrants in connection with the Private Placement.

| -28- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 12: SUBSEQUENT EVENTS (Cont.)

B. June 2024 Facility Agreement

Following

the closing of the Private Placement (as defined in note 12.A), the exercise price of the June 2024 Lead Lender Warrant was adjusted

to $

C. First July 2024 Facility Agreement

On

July 4, 2024, the Company entered into a credit facility agreement, as restated on July 22, 2024, and amended on July 25, 2024 (the “First

July 2024 Facility Agreement”) for a $

The

First July 2024 Facility Loan Amount will remain available until the earliest of (a)(i) its drawing down in full, (ii) the 36-month anniversary

of the First July 2024 Facility Agreement and (b) upon such date that the Company completes a $

The

First July 2024 Facility Agreement sets forth a drawdown schedule as follows:

The

First July 2024 Facility Amount will accrue interest at a rate of

| -29- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 12: SUBSEQUENT EVENTS (Cont.)

C. First July 2024 Facility Agreement (Cont.)

Immediately

following the effectiveness of the Uplist, (i) $

In

addition, the Company agreed to pay the First July 2024 Lender a one-time fee consisting of: (i) shares of the Company’s

common stock, representing five percent (

D. Services Agreements

On July 14, 2024 and July 25, 2024, the Company entered into consulting agreements with certain consultants (the “Consultants”) pursuant to which the Consultants agreed to provide certain services to the Company in connection with the Uplist. In consideration with the Consultants’ services, the Company issued to the Consultants shares of common stock in July 2024.

E. Second July 2024 Facility Agreement

On

July 28, 2024, the Company entered into a credit facility agreement (the “Second July 2024 Facility Agreement”) for a $

The

Second July 2024 Facility Loan Amount will remain available until the earliest of (a)(i) its drawing down in full, (ii) the 40-month

anniversary of the Second July 2024 Facility Agreement and (b) upon such date that the Company completes a $

| -30- |

VIEWBIX INC.

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

U.S. dollars in thousands (except share data)

NOTE 12: SUBSEQUENT EVENTS (Cont.)

E. Second July 2024 Facility Agreement (cont.)

The

Second July 2024 Facility Loan Amount will accrue interest at a rate of

Immediately

following the effectiveness of the Uplist, (i) $

In

addition, the Company agreed to pay the Second July 2024 Lenders a one-time fee consisting of shares of the Company’s common

stock, representing five percent (

F. Securities Exchange Agreement

On July 31, 2024, the Company entered into a Securities Exchange Agreement, with Metagramm Software Ltd. (“Metagramm”) pursuant to which the Company agreed to issue to Metagramm % of its issued and outstanding share capital in exchange for % of Metagramm’s issued and outstanding share capital. The transactions contemplated by the Securities Exchange Agreement are expected to close following the Uplist (as defined in note 6.E).

G. Grant of shares

On July 1, 2024, the Company issued shares of Common Stock to Gix Media’s CEO.

H. Reverse stock split

On

July 15, 2024, the Company filed an amendment to its Certificate of Incorporation (the “Amendment”) to effect a

| -31- |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS AND RESULTS OF OPERATIONS

Special Note Regarding Forward-Looking Statements

The following management’s discussion and analysis section should be read in conjunction with the Company’s unaudited financial statements as of June 30, 2024 and 2023, and the related statements of statement operation, statement of changes in shareholders’ equity and statements of cash flows for the six and three months then ended, and the related notes thereto contained in this Quarterly Report on Form 10-Q (this “Quarterly Report”).

Our reporting currency and functional currency is the U.S. dollar. Unless otherwise expressly stated or the context otherwise requires, references in this prospectus to “NIS” are to New Israeli Shekels, and references to “dollars” or “$” mean U.S. dollars.

On July 10, 2024, our board of directors approved a one-for-four consolidation of our share capital, pursuant to which holders of our shares of common stock will receive one share of common stock for every four shares of common stock held. The reverse split is not yet in effect, and will be effectuated upon approval by FINRA. Unless the context expressly indicates otherwise, all references to share and per share amounts referred to herein reflect the amounts before giving effect to the reverse split.

Forward-Looking Statements

This management discussion and analysis section contains forward-looking statements, such as statements of the Company’s plans, objectives, expectations, and intentions. Any statements that are not statements of historical fact are forward-looking statements. When used, the words “believe,” “plan,” “intend,” “anticipate,” “target,” “estimate,” “expect” and the like, and/or future tense or conditional constructions “will,” “may,” “could,” “should,” etc., or similar expressions, identify certain of these forward-looking statements. These forward-looking statements are subject to risks and uncertainties that could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. Forward-looking statements are based on information we have when those statements are made or our management’s good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

● the continued demand of digital advertising as an integral part of corporate marketing and internal communications plans and the continued growth and acceptance of digital advertising as effective alternatives to traditional offline marketing products and service;

● our ability to retain and attract a programmatic advertiser, and the associated payments received from such programmatic advertisers’ ads on websites which have been categorized as “Made for Advertising”;

● our ability to generate enough cash flow to meet our debt obligations or fund our other liquidity needs, and substantial doubt regarding our ability to continue as a going concern;

● our need to raise additional capital to meet our business requirements in the future and such capital raising may be costly or difficult to obtain and could dilute out shareholders’ ownership interests;

● our ability to receive credit facility to fund our operations, at favorable terms, or at all;

● our ability to pay our obligations when they become due, including our loan and facility agreements and Financing Agreement (as defined below);

● our subsidiaries’ future performance, including our ability to instill potential measures to assist Cortex and Gix Media in mitigating future economic harm;

● entry of new competitors and products, the impact of large and established internet and technology companies and potential technological obsolescence of our offered platforms; and

● political, economic and military conditions in Israel, including the recent attack by Hamas and other terrorist organizations from the Gaza Strip and elsewhere in the region and Israel’s war against them, as well as the war’s potential impact on our business and operation.

The foregoing does not represent an exhaustive list of matters that may be covered by the forward-looking statements contained herein or risk factors that we are faced with which may cause our actual results to differ from those anticipated in our forward-looking statements. For a discussion of these and other risks that relate to our business and investing in our common stock, you should carefully review the risks and uncertainties described in this Quarterly Report on Form 10-Q, and those contained in section captioned “Risk Factors” of our Annual Report on Form 10-K for the fiscal year ended December 31, 2023, filed with the Securities and Exchange Commission (the “SEC”) on March 25, 2024 (the “Annual Report”). The Company’s actual results could differ materially from those contemplated in these forward-looking statements as a result of these factors. The Company does not undertake any obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this Quarterly Report.

| -32- |

Overview and Background

Viewbix Inc. (the “Registrant”, “Viewbix” or the “Company”) is a digital advertising platform that develops and markets a variety of technological platforms that automate, optimize and monetize digital online campaigns. Viewbix’s operations were previously focused on analysis of the video marketing performance of its clients as well as the effectiveness of their messaging (“Video Advertising Platform”). With the Video Advertising Platform, Viewbix allowed its clients with digital video properties the ability to use its platforms in a way that allows viewers to engage and interact with the video. The Video Advertising Platform measures when a viewer performs a specific action while watching a video and collects and reports the results to the client. However, due to the Company’s failure to meet predetermined sales targets which were set pursuant to the Recapitalization Transaction (as defined in note 1.A to the interim condensed consolidated financial statements). with Gix Internet Ltd., in January 2020, the Company determined to reduce its operations and the size of its sales and R&D team in Video Advertising Platform.

The Company, through its subsidiaries Gix Media Ltd. (“Gix Media”) and Cortex Media Group Ltd. (“Cortex”), expanded its digital advertising operations across two main sectors: ad search and digital content (the “Search Platform” and the “Content Platform”, respectively”). Gix Media and Cortex develop and market a variety of technological software solutions that automate, optimize and monetize online campaigns. Cortex also creates, edits and markets content in various languages to different target audiences in order to generate revenues from advertisements displayed together with the content, which are posted on digital content, marketing and advertising platforms. These technological tools enable advertisers and website owners to earn more from their advertising campaigns and generate additional profits from their sites.

Through its Search Platform, the Company provides services to leading search engines worldwide (“Search Engines”) by developing, marketing and distributing software products to internet users. The operations and activity on this platform are powered by Gix Media.

Through the Content Platform, the Company provides editing and marketing services of content in different languages and to different target audiences with the goal of generating revenues from advertising employed in such content, which is based on digital content marketing and advertising platforms. The operations and activity on this platform are powered by Cortex.

Search Platform

Gix Media’s Search Platform allows for the referral of user traffic (i.e., searches that are performed by internet users) to the Search Engines, such as Yahoo and Bing, where the Search Engines display the ads of their customers. The Search Engines pay Gix Media for the searches that were referred by it, based on the amount of consideration that the Search Engine receives from the advertisers for the user traffic generated, less a certain percentage from the revenues attributed to the Search Engine. Since the customers of Gix Media are the Search Engines, and not the advertisers, Gix Media recognizes revenues for the actual amount received from the Search Engines, and not from the advertisement revenue itself.

The referral of user traffic by Gix Media to the Search Engines is possible after users download Gix Media’s products, which are browser add-ons, usually from the browser stores (mostly Google Chrome browsers) and by downloading desktop software products, free of charge, for the Apple operating system (for Mac computers) and for the Microsoft operating system (for PC computers). When downloading Gix Media’s products, the users grant permission to Gix Media to refer the searches performed while using Gix Media’s products to the Search Engines.

In addition, Gix Media provides user traffic referral services to Search Engines through the referral of traffic of browsers who engage content generated by Gix Media. This content is displayed on ad spaces that are purchased by the Company by content recommendation companies (such as Yahoo!, Outbrain, Taboola and Gemini). When occasional users click on such content, Gix Media transfers user traffic to a Search Engine which contains search words that are related to the advertising content.

| -33- |

Content Platform

Cortex’s Content Platform produces engaging content and marketing material in various languages to various target audiences, in order to generate revenues from advertisements displayed together with the content, which are posted on digital content, marketing and advertising platforms. Cortex acts as a digital content platform that publishes content written by creative writers and editors which it employs. The content is displayed on several different content websites owned by Cortex, covering various subjects including culture, history, trips, pets, entertainment and leisure, food, etc. (the “Cortex Websites”). Cortex developed capabilities that enable it and its customers to profit from the original content which it publishes by advertising the content on leading international third-party websites and online ad platforms (the “Third Party Platforms”). Readers are exposed to the articles on the Third-Party Platforms and may choose to read them by clicking an ad, after which readers are directed automatically to the Cortex Websites where the content is posted.

The technological tools developed by Cortex allow businesses in the digital advertising market (Search Engines, ad exchanges, advertisers, content owners and brand owners) to earn more from their advertising campaigns and generate additional profit from their websites, both from its content and from its advertising.

Advertisers display ads on various platforms for potential customers (internet users and readers). In order to help maximize the effectiveness of advertising, Cortex developed different advertising systems and tools for content management, content distribution and campaigns and measurement of performance on the various platforms that display the content.

Recent Developments

Credit Facilities of the Company

2023 Loan Agreement

On November 15, 2023, Viewbix Ltd., the Company’s subsidiary (“Viewbix Israel”) entered into a Loan Agreement (the “2023 Loan”) with certain lenders (the “2023 Loan Lenders”) whereby the Lenders provided Viewbix Israel with loans in the aggregate amount of $480,000 (which sum may be increased to up to $1,000,000, at the discretion of the 2023 Loan Lenders). In accordance with the terms of the 2023 Loan, the principal amount bears an annual interest at a rate of 9% and shall be repaid over the course of two years following January 1, 2024. In the event that Viewbix Israel fails to repay a part or all of the loan amount (including the accrued interest) and subject to certain conditions, the outstanding loan amount may be converted, at each 2023 Loan Lender’s discretion, into shares of the Company’s Common Stock, at a price per share equal to the 30-day average of the closing bid price of the Common Stock, calculated as of such date the respective portion of the outstanding loan amount becomes repayable.

In connection with the 2023 Loan, the Company issued to each 2023 Loan Lender a warrant to purchase shares of Common Stock (the “2023 Warrants”), such that the number of shares of Common Stock underlying each 2023 Warrant will reflect (one-for-one) the number of dollars provided by each Lender as part of the principal amount. Each 2023 Warrant has an exercise price per share of Common Stock of $0.50 and will expire and cease to be exercisable on December 31, 2025. The 2023 Warrants were issued to the Lenders pursuant to Regulation S of the Securities Act of 1933, as amended (“Regulation S”).

June 2024 Facility Agreement

On July 22, 2024, we entered into an amended and restated facility agreement (the “June 2024 Facility Agreement”) for a $1 million (the “June 2024 Facility Loan Amount”) credit facility (the “June 2024 Credit Facility”) with the 2023 Loan Lenders and certain lenders set forth therein (the “June 2024 Lenders”) that amends and restates the prior facility agreement entered into on June 18, 2024 between the Company and the June 2024 Lenders (the “Prior June 2024 Facility Agreement”). In addition to the June 2024 Facility Loan Amount, the June 2024 Facility Agreement contemplates the inclusion of an additional $530,657 of outstanding debt owed by us to the June 2024 Lenders (the “June 2024 Prior Loan Amount”, and together with the June 2024 Facility Loan Amount, the “June 2024 Loan Amount”), which June 2024 Prior Loan Amount is entitled to certain rights under the June 2024 Credit Facility.

The term (the “June 2024 Facility Term”) of the June 2024 Credit Facility expires 12 months following the date of the June 2024 Facility Agreement (the “Initial Maturity Date”), provided that, if the effectiveness of an uplisting of our shares of common stock to a NASDAQ security exchange securities exchange (the “Uplist”) occurs prior to the Initial Maturity Date, the June 2024 Facility Term shall expire 12 months following the effective date of the Uplist. The June 2024 Facility Agreement sets forth a drawdown schedule as follows: (i) an aggregate of $350,000 was drawn down on the date of the Prior June 2024 Facility Agreement, (ii) an aggregate of $150,000 was drawn down upon the filing of the Registration Statement (as defined below) and (iii) an aggregate of $500,000 drawn down upon the effectiveness of the Uplist.

| -34- |

The June 2024 Credit Facility accrues interest at a rate of 12% per annum, and we will also pay such interest on the June 2024 Prior Loan Amount, which is equal to $183,679 (the “June 2024 Facility Interest”). The June 2024 Facility Interest was paid in advance for the first year of the June 2024 Facility in (i) shares of our common stock at a conversion rate of $0.25 for each U.S. dollar of June 2024 Facility Interest accrued on the respective June 2024 Loan Amount, equal to an aggregate of 734,716 shares of common stock (the “June 2024 Facility Shares”) and (b) a warrant to purchase a number of shares of common stock equal to the June 2024 Facility Shares (the “June 2024 Facility Warrant”).

Immediately following the effectiveness of the Uplist, (i) $662,957 of the June 2024 Loan Amount will convert into shares of common stock at a conversion rate equal to $0.25 per share of our common stock (the “June 2024 Convertible Stock”) and (ii) we will issue a warrant in substantially the same form and on substantially the same terms as a June 2024 Facility Warrant to purchase a number of shares of our common stock equal to the June 2024 Convertible Stock with an exercise price of $0.25 per share (the “June 2024 Conversion Warrant”, and (i) and (ii), collectively a “June 2024 Conversion Unit”). Such portion of the June 2024 Loan Amount that is not converted into a June 2024 Conversion Unit will remain outstanding and will not convert following the Uplist. For the duration of the June 2024 Facility Term of the June 2024 Credit Facility, the June 2024 Lenders may elect to convert such unconverted portion of the June 2024 Loan Amount into additional June 2024 Conversion Units or, upon the expiration of the June 2024 Facility Term, such unconverted portion of the June 2024 Loan Amount will be repaid in accordance with the terms of the June 2024 Facility Agreement.

The June 2024 Facility Warrants are exercisable upon issuance at an exercise price of $0.25 per share of common stock, subject to certain beneficial ownership limitations and price adjustments set forth therein, and will have a three-year term from the issuance date.

In addition and in connection with the June 2024 Credit Facility, we agreed to pay L.I.A. Pure Capital Ltd. (the “June 2024 Lead Lender”) a commission consisting of (i) 200,000 shares of common stock, (ii) a warrant in substantially the same form and on substantially the same terms as the June 2024 Facility Warrant to purchase 200,000 shares of common stock with an exercise price of $0.25 per share (the “June 2024 Lead Lender Warrant”) and (iii) a warrant to purchase 2,500,000 shares of common stock with an exercise price of $1.00 per share, representing an aggregate exercise amount of $2.5 million, subject to beneficial ownership limitations and adjustments (the “June 2024 Lead Lender Fee Warrant” and together with the June 2024 Lead Lender Warrant and the June 2024 Facility Warrants, the “June 2024 Warrants”).

The June 2024 Lead Lender Fee Warrant were immediately exercisable upon issuance and have a three-year term from the issuance date. Following the closing of the Private Placement (as defined below), the exercise price of the June 2024 Lead Lender Fee Warrant was adjusted to $0.118, which is the effective price per share of common stock in the Private Placement, or the June 2024 Lead Lender Fee Warrant Adjusted Exercise Price, and the number of shares of common stock issuable upon the exercise of the June 2024 Lead Lender Fee Warrant was also adjusted to a total 21,186,440 shares, or the June 2024 Lead Lender Fee Warrant Adjusted Shares, such that the product of the June 2024 Lead Lender Fee Warrant Adjusted Exercise Price and the June 2024 Lead Lender Fee Warrant Adjusted Shares is equal to an aggregate exercise amount of $2.5 million.

We undertook to file a registration statement (the “Registration Statement”) with the Securities and Exchange Commission (the “SEC”) to register, inter alia, the resale by the June 2024 Lenders of shares of common stock underlying the June 2024 Credit Facility, the June 2024 Warrants and the June 2024 Conversion Units, which we filed on July 31, 2024.

Private Placement

On July 3, 2024, we entered into a definitive securities purchase agreement (the “Purchase Agreement”) with a global investment firm (the “Lead Investor”) for the purchase and sale in a private placement (the “Private Placement”) of units (the “Units”) consisting of (i) 1,027,500 shares of our common stock (the “PIPE Shares”) and (ii) common stock purchase warrants (the “PIPE Warrants”) to purchase up to 1,541,250 shares of our common stock (the “PIPE Warrant Shares”) to the Lead Investor and other investors (collectively, the “Investors”) acceptable to the Lead Investor and us. The Private Placement closed on July 3, 2024. The purchase price per Unit was $0.25.

| -35- |

The PIPE Warrants are exercisable upon issuance at an exercise price of $0.25 per share, subject to certain adjustments and certain anti-dilution protection set forth therein, and will have a three-year term from the issuance date. In addition, the PIPE Warrants are subject to an automatic exercise provision in the event that our shares of common stock are approved for listing on the Nasdaq Capital Market.

The aggregate gross proceeds to us from the Private Placement were $256,875.

In connection with the Private Placement, we entered into a registration rights agreement (the “Registration Rights Agreement”) with the Investors. Pursuant to the Registration Rights Agreement, we are required to file a resale registration statement (the “PIPE Registration Statement”) with the SEC to register for resale of the PIPE Shares issued in the Private Placement and the PIPE Warrant Shares issuable upon exercise of the PIPE Warrants, within 30 days of the date of the Purchase Agreement, and to have such PIPE Registration Statement declared effective within 30 days following the filing date of the PIPE Registration Statement in the event the PIPE Registration Statement is not reviewed by the SEC, or 60 days following the filing date of the PIPE Registration Statement in the event the PIPE Registration Statement is reviewed by the SEC. We will be obligated to pay certain liquidated damages if we fail to file the PIPE Registration Statement when required, fail to cause the PIPE Registration Statement to be declared effective by the SEC when required, or if we fail to maintain the effectiveness of the PIPE Registration Statement. We filed the PIPE Registration Statement on July 31, 2024.