UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

|

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

OR | |

|

|

|

|

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-14740

|

North American Nickel Inc. |

|

(Exact name of Registrant as specified in its charter) |

|

|

|

Province of British Columbia, Canada |

|

(Jurisdiction of incorporation or organization) |

|

|

|

1055 West Hastings Street, Vancouver, BC, Canada, V6E 2E9 |

|

(Address of principal executive offices) |

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class |

|

Name of each exchange on which registered |

|

|

|

|

|

None |

|

None |

Securities registered or to be registered pursuant to Section 12(g) of the Act. Common Shares, no par value

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common shares as of the close of the period covered by the annual report:

554,598,167 inclusive of the conversion of the outstanding Series 1 Convertible Preferred Shares

Indicate by check mark if the registrant is a well-known seasoned issuer.

o Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

Accelerated filer o |

Non-accelerated filer x |

Emerging growth company o |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which financial statement item the registrant has elected to follow.

x Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act.

o Yes x No

Unless otherwise indicated, all references herein are expressed in Canadian dollars and United States currency is stated as “U.S. $ .”

THIS SUBMISSION SHOULD BE CONSIDERED IN CONJUNCTION WITH PREVIOUSLY FILED FORMS 20-F AND 6-K. THE AUDITED FINANCIAL STATEMENTS AND NOTES THERETO ATTACHED ARE AN INTEGRAL PART OF THIS SUBMISSION.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not required

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not required

ITEM 3. KEY INFORMATION

A. Selected financial data.

The following financial data summarizes selected financial data for our company prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) for the five fiscal years ended December 31, 2017, 2016, 2015, 2014 and 2013. The information presented below for the five year period ended December 31, 2017, 2016, 2015, 2014 and 2013 is derived from our financial statements which were examined by our independent auditors. The information set forth below should be read in conjunction with our audited annual financial statements and related notes thereto included in this annual report, and with the information appearing under the heading “Item 5 — Operating and Financial Review and Prospects”. Al financial information is expressed in thousands of Canadian dollars and in thousands of Danish Krones (“DKK”), except per share amounts and except as otherwise indicated.

North American Nickel Inc. (the “Company”) was incorporated on September 23, 1983. The Company changed its name from Widescope Resources Inc. to North American Nickel Inc. effective April 19, 2010. The Company’s principal business activity is the exploration of natural resource properties.

Effective April 19, 2010 the Company’s shareholders approved a special resolution to reorganize the Company’s capital structure by consolidating in a reverse stock split the existing common shares on the basis of each two (2) old shares being equal to one (1) new share and concurrently increasing the authorized capital of the Company from 100,000,000 common shares without par value to an unlimited number of common shares without par value. All references to common shares, stock options, warrants and weighted average number of shares outstanding in this Form 20-F retroactively reflect the share consolidation unless otherwise noted. The net effect of the above was to reduce the existing outstanding common shares from 10,883,452 to 5,441,730.

North American Nickel Inc.

Selected Financial Data in accordance with IFRS for the years 2017, 2016, 2015, 2014 and 2013

(Expressed in thousands of Canadian dollars, except per share amounts)

|

|

|

Years Ended December 31 |

| |||||||||

|

|

|

2017 |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

| |

|

Net operating revenues |

|

$ |

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Loss from operations |

|

$ |

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Net loss |

|

$ |

(2,879 |

) |

(2,877 |

) |

(2,389 |

) |

(3,741 |

) |

(1,260 |

) |

|

Comprehensive loss |

|

$ |

(2,879 |

) |

(2,877 |

) |

(2,389 |

) |

(3,74 |

) |

(1,260 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Loss per share from operations |

|

$ |

(0.01 |

) |

(0.01 |

) |

(0.01 |

) |

(0.02 |

) |

(0.01 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Share capital |

|

$ |

74,189 |

|

62,906 |

|

51,165 |

|

43,268 |

|

33,631 |

|

|

Common shares issued |

|

554,598,167 |

|

368,581,886 |

|

207,629,506 |

|

169,964,679 |

|

140,576,584 |

| |

|

Weighted average shares outstanding |

|

465,929,638 |

|

269,778,932 |

|

188,384,506 |

|

157,986,561 |

|

111,753,433 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Total assets |

|

$ |

53,697 |

|

41,882 |

|

32,729 |

|

27,050 |

|

18,716 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Net assets (liabilities) |

|

$ |

52,728 |

|

41,700 |

|

32,480 |

|

26,753 |

|

18,680 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Cash dividends declared per common share |

|

$ |

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

|

Exchange rates (CAD$ to U.S.$) period average |

|

$ |

1.2980 |

|

1.2785 |

|

1.2785 |

|

1.1046 |

|

1.0298 |

|

|

Exchange rates (CAD$ to U.S.$) for most recent six months |

|

Period High |

|

Period Low |

| |

|

October 2017 |

|

$ |

0.8018 |

|

0.7756 |

|

|

November 2017 |

|

$ |

0.7885 |

|

0.7759 |

|

|

December 2017 |

|

$ |

0.7971 |

|

0.7760 |

|

|

January 2017 |

|

$ |

0.8135 |

|

0.7978 |

|

|

February 2018 |

|

$ |

0.8138 |

|

0.7807 |

|

|

March 2018 |

|

$ |

0.7794 |

|

0.7641 |

|

|

Exchange rate (CAD$ to U.S.$) April 24, 2018 |

|

$ |

0.7805 |

|

0.7775 |

|

B. Not required

C. Not required

D. Risk factors.

The business of the Company entails significant risks, and an investment in the securities of the Company should be considered highly speculative. An investment in the securities of the Company should only be undertaken by persons who have sufficient financial resources to enable them to assume such risks. The following is a general description of all material risks, which can adversely affect the business and in turn the financial results, ultimately affecting the value of an investment the Company.

The Company has no viable commercial business.

Having no viable business it is difficult to determine a price for the common shares. That price must therefore be dependent on the value that each individual buyer and seller place on the future prospects of the company, rather than any objective measurement. This is a very risk position for shareholders, as the majority perception may turn negative and price decline severely.

The Company has limited funds.

Funds are the fuel needed to drive the company. Should current funds be consumed, and the company not be able to attract more capital, prospects for shareholders would become extremely negative, and shareholder losses will inevitably occur.

There is no assurance that the Company can access additional capital.

The company will need to demonstrate performance in order to attract additional capital. As the mineral exploration business has a high element of chance associated with it, it is possible that none of the current properties will have any value. The capital markets could perceive this to be a demonstration of poor performance, and be unwilling to provide additional funds. Should this happen, shareholders will incur significant losses.

There is no assurance that the transactions disclosed herein will be successful in its quest to find a commercially viable quantity of mineral resources.

Unless the Company is able to secure other more viable projects, providing better future prospects, buyer interest for common shares will decline severely, resulting in lower prices and significant shareholder losses.

There is no assurance that other prospective mineral properties or other assets can be acquired, and if acquired that the necessary additional capital can be attracted.

Either of these is possible. Either occurring will have the same inevitable outcome. Demand for the common shares will decline severely, resulting in a drop in trading price, and significant shareholder losses.

The Company has a history of operating losses and may have operating losses and a negative cash flow in the future.

This will mean that additional shares will need to be sold to fund operations. Without a concurrent improvement in future prospects, this will result in supply of stock exceeding demand, and much lower prices. This will cause shareholders to lose money.

The Company’s auditors have indicated that U.S. reporting standards would require them to raise a concern about the company’s ability to continue as a going concern.

Additional capital will need to be raised. This could result in the perception of lowered future prospects, lower demand for the Company’s common share, lower stock prices, and shareholder losses.

There can be no assurance that a liquid market will develop for the Company’s shares and therefore no assurance that shareholders will be able to sell their shares. Lack of liquidity that prevents shareholders from selling, or limits their abilities to sell, will all too likely lead to significant losses for shareholders.

Management has little expertise in mining, which may ultimately cause shareholders to lose money.

Management may waste the Company’s limited capital on worthless properties, or it may do the wrong things with properties that could have value. Either way, the outcome will be the same. Money will have been wasted without any corresponding creation of value. This will cause shareholders to lose patience and lose interest. This could lead to significantly increased selling of shares, driving down the price, and leading to losses for investors.

The Company’s common stock is thinly traded so it is more susceptible to extreme rises or declines in price, and you may not be able to sell your shares at or above the price paid.

You may have difficulty reselling shares of our common stock, either at or above the price paid, or even at fair market value. The stock market often experiences significant price and volume changes that are not related to the operating performance of individual companies, and because our common stock is thinly traded it is particularly susceptible to such changes. These broad market changes may cause the market price of our common shares to decline, regardless of how well the company performs. This may be exaggerated by the fact that the shares trade on the over-the-counter bulletin board (“OTCBB”), which is owned and operated by the Financial Industry Regulatory Authority (“FINRA”). Trading on the OTCBB is often extremely sporadic, and subject to manipulation by market-makers, and short sellers. This may cause you to lose money as you may have difficulty selling the shares that you own.

The Company’s common stock is subject to the “penny stock” regulations, which are likely to make it more difficult to sell.

A “penny stock” is generally a stock trading under $5.00 per share, and not registered on a national securities exchange or quoted on the NASDAQ national market. The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. These rules, intended to protect investors, generally have the result of reducing trading in such stocks, restricting the pool of potential investors, and making it more difficult for investors to sell their shares once acquired. Since our common shares are subject to the “penny stock” rules, you may find it more difficult to sell your shares.

As a foreign issuer, the Company is exempt from certain informational requirements of the Exchange Act to which domestic issuers are subject.

As a foreign issuer we are not required to comply with all of the informational requirements of the Exchange Act. As a result, there may be less information concerning our company publicly available than if we were a domestic United States issuer. In addition, our officers, directors, and principal shareholders are exempt from the reporting and short profit provisions of Section 16 of the Exchange Act, and the rules promulgated thereunder. Therefore, our shareholders may not know on a timely basis when our officers, directors, and principal shareholders purchase or sell shares of our common stock.

As a Canadian company with most assets and key personnel located outside the United States, you may have difficulty in acquiring United States jurisdiction, or enforcing a United States judgment against us, our key personnel, or assets.

As a Canadian company many of our assets and key personnel, including directors and officers, reside outside the United States. As a result, it may be difficult or impossible for you to effect service of process within the United States upon us or any of our key personnel or to enforce against us or any of our key personnel judgments obtained in United States’ courts, including judgments relating to United States federal securities laws. Canadian courts may not permit you to bring an original action in Canada, or recognize or enforce judgments of United States courts obtained against us predicated upon the civil liability provisions of federal securities laws of the United States, or of any state thereof. Furthermore, because many of our assets are located in Canada, it would be extremely difficult to access these assets to satisfy any award entered against us in a United States court. Accordingly, you may have more difficulty in protecting your interests in the face of actions taken by our management, members of our board of directors, or our controlling shareholders than you would otherwise as shareholders of a United States public company.

The Company does not intend to pay any common stock dividends in the foreseeable future.

We have never declared or paid a dividend on our common stock, and, because we have very limited resources, we do not anticipate declaring or paying any dividends in the foreseeable future. It is unlikely that the holders of our common shares will have an opportunity to profit from anything other than potential appreciation in the value of our common shares. If you require dividend income, you should not rely in an investment in our common shares to provide it.

Future issuances of common stock may depress stock prices and dilute your interest.

We may issue additional shares of our common stock in future financings, or grant stock options to our employees, officers, directors, and consultants under our stock incentive plan. Any such issuances could have the effect of depressing the market price of our common stock, and, in any case, would dilute the percentage ownership interests in our company of our shareholders. In addition we could issue securities having rights, preferences and privileges senior to those of our common shares. This could depress the value of our common shares.

ITEM 4. INFORMATION ON THE COMPANY

A. History and development of the Company.

North American Nickel Inc. (the “Company”) was incorporated under the laws of the Province of British Columbia, Canada, by filing of Memorandum and Articles of Association on September 20, 1983, under the name Rainbow Resources Ltd. The company’s name was changed to Widescope Resources Ltd. on May 1, 1984, and to Gemini Technology Inc. on September 17, 1985. In conjunction with a reverse split of its common shares on a five-old for one-new basis, the Company adopted the name International Gemini Technology Inc., effective September 23, 1993. The Company’s name was changed to Widescope Resources Inc., effective July 12, 2006. Effective April 19, 2010, the Company’s shareholders approved a special resolution to reorganize the Company’s capital structure by consolidating in a reverse stock split the existing common shares on the basis of every 2 old shares being equal to 1 new share and concurrently increasing the authorized capital of the Company from 100,000,000 common shares without par value to an unlimited number of common shares without par value. Also effective this date, the Company’s name was changed to North American Nickel Inc. to reflect its new focus. All references to common shares, stock options, warrants and weighted average number of shares outstanding in this discussion and the accompanying consolidated financial statements retroactively reflect the share consolidation unless otherwise noted.

In April 2010, the Company initiated a series of actions to realign its focus into the field of nickel exploration in the prolific nickel belts around Sudbury, Ontario and Thompson, Manitoba. Concurrently, the directors of the Company appointed new senior management to oversee the daily operations of the Company.

On May 3, 2011, the Company’s listing application was conditionally accepted by the TSX-V Venture Exchange. On May 30, 2011, the common shares of the Company began trading under the symbol “NAN”.

On August 15, 2011, the Company was granted an exploration license by the Bureau of Minerals and Petroleum of Greenland for exclusive exploration rights over an area totalling 4,841 square kilometres located near Sulussugut, Greenland.

On March 4, 2012, the Company was granted an additional exploration license by the Bureau of Minerals and Petroleum of Greenland for exclusive exploration rights over an area covering a total of 142 square kilometres license and located near Ininngui, Greenland.

On January 19, 2015, the Company signed an exclusivity agreement with Minelco AS (“Minelco”) to acquire the deep water Seqi Port (the “Port”). A report was prepared summarizing environmental due diligence and preliminary assessment of reindeer by Golder Associates — INUPLAN in and around the Port and upon further review, the decided to not pursue the Seqi Port assignment.

On March 29, 2017, the Company announced the grant of a watershed prospecting licence for the assessment and development of potential hydropower resources on its wholly-owned Maniitsoq nickel sulphide project in southwest Greenland. The Company intends to assess the watershed as a potential source of power for its Maniitsoq project consistent with the emphasis by the Greenland Government on securing environmentally friendly energy sources for any industrial development, including mining.

On July 13, 2017, the Company announced that it has finalized the details for the acquisition of a watershed (“0.6H”) prospecting licence that overlaps the eastern boundary of its 100% owned Maniitsoq nickel sulphide project in southwest Greenland.

On March 1, 2018, the Company announced that it had received the final Hydropower Feasibility Assessment Study within watershed 06.H located on the eastern flank of the Company’s 100% owned Maniitsoq nickel sulphide project in Southwest Greenland.

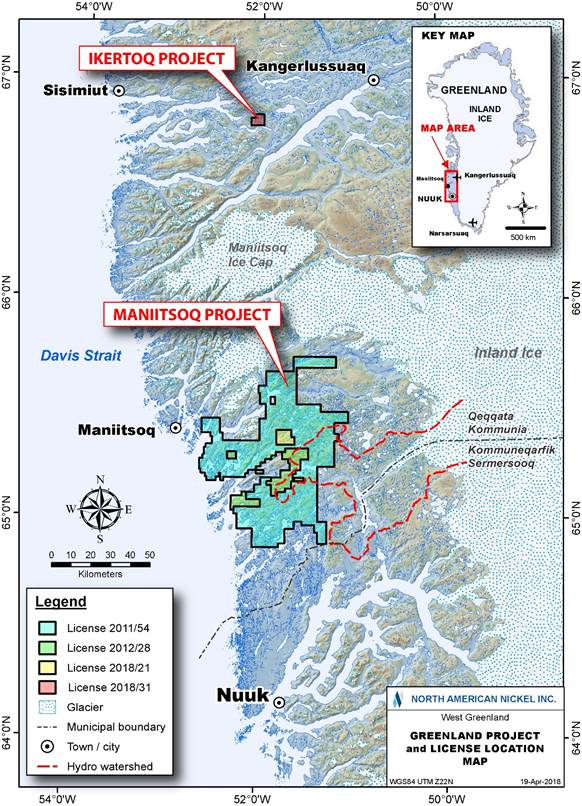

On April 5, 2018, the Company acquired new properties, Ikertoq, mineral licence No. 2018/31 and Carbonatite, mineral licence No. 2018/21 located on the Company’s 100% owned Maniitsoq nickel sulphide project in Southwest Greenland.

B. Business overview

In conjunction with the April 2010 refocusing of the Company on nickel exploration, as of April 23, 2010 the Company entered into an agreement with an independent third party that resulted in divesting its interest in Outback Capital Inc., and its remaining interest in the Rice Lake properties. The sale was completed as of May 31, 2010, and the proceeds from the sale were $53.

In conducting its business operations, the Company is not dependent on any patented or license processes, technology, industrial, commercial or financial contract or new manufacturing processes.

With the dramatic and possibly unprecedented contraction of global financial markets experienced in 2008, a tidal wave of qualified people became available. Suddenly, capital became unavailable. Exploration companies everywhere reduced overhead.

Access to capital eased marginally toward the latter part of 2009 and beyond. More capital became available, and enthusiasm for mining projects increased at much the same time. The latter, because of expectations of increased inflation, brought increased demand for precious metals and because of the expectation of an increasing demand for base metals from Asia.

To focus on the expected increased demand for base metals, the Company entered into agreements to acquire rights to four properties in the Sudbury Ontario nickel belt, and one agreement to acquire 100% ownership of another property in the area of the Thompson Manitoba nickel belt. As part of this change in focus, the Company entered into an arm’s length agreement to divest its interest in Outback Capital Inc., and through this, its interest in the Pine Falls Manitoba gold properties.

Concurrent with the refocusing of the Company in April 2010, the Company arranged two non-brokered private placements to finance working capital and the first exploration work at Post Creek and Bell Lake in the Sudbury nickel belt. It also attracted four new directors, each with significant experience in mineral exploration, to replace three previous directors, and add one additional director.

Effective August 15, 2011, the Company was granted an exploration license (the “Sulussugut License”) by the Bureau of Minerals and Petroleum (“BMP”) of Greenland for exclusive exploration rights of an area located near Sulussugut, Greenland. The Company paid a license fee of $6 (Danish Krones (“DKK”) 31) upon granting of the Sulussugut License. The Sulussugut License was valid for 5 years until December 31, 2015, with December 31, 2011 being the first year providing the Company meets the terms of the license, which includes that specified eligible exploration expenditures must be made. The application for another 5 year term on the Sulussugut License was submitted to the Greenland Mineral Licence & Safety Authority (MLSA) which was effective on April 11, 2016, with December 31, 2017 being the seventh year.

On the first 5 year license, the Company completed the exploration requirements of an estimated minimum of DKK 83,809 (approximately $15,808) between the years ended December 31, 2011 to 2015 by incurring $26,111 on the Sulussugut License. The accumulated exploration credits held at the end to December 31, 2015, of DKK 100,304 can be carried forward until 2019. Under the terms of the second license period, the Company had no minimum required exploration for the year ended December 31, 2016. As of December 31, 2017, the Company has spent $44,937 on exploration costs for the Sulussugut License.

To December 31, 2017 and 2016, the Company has completed all obligations with respect to required reduction of the area of the license.

During the year ended December 31, 2017, the Company had approved exploration expenditures of DKK 85,094 (approximately $16,746) which results in the total carried credits for the Sulussugut License at DKK 246,507 (approximately $48,513).

During the year ended December 31, 2017, the Company spent a total of $11,079 in exploration and license related expenditures on the Sulussugut License.

Effective March 4, 2012, the Company was granted an additional exploration license (the “Ininngui License”) by the BMP of Greenland for exclusive exploration rights over an area covering a total of 142 square kilometres. The license is located near Ininngui, Greenland. The Company paid a license fee of DKK 32 upon granting of the Ininngui License. The Ininngui License is valid for 5 years until December 31, 2016, with December 31, 2012 being the first year. The Ininngui License is contiguous with the Sulussugut License.

On the first 5 year license, the Company completed the exploration requirements of an estimated minimum of DKK 8,697 (approximately $1,635) between the years ended December 31, 2012 to 2016 by incurring $2,722 on the Ininngui License. To December 31, 2016, the Company’s expenditures exceeded the minimum requirement and the Company has a surplus of DKK 15,677 (approximately $3,044) and the Company was granted a credit for the excess, which may be used towards future expense requirements on the Ininngui License until the following years; year 2018 - DKK 2,276, year 2019 - DKK 6,790 and year 2020 - DKK 9,367, should the Company be granted an extension on the exploration license.

The required minimum exploration expenditures on the Ininngui License for year 5, ending December 31, 2016 was DKK 2,715 (approximately $535). As of December 31, 2017, the Company has spent $3,698 on exploration costs for the Ininngui License.

The Company may terminate the licenses at any time; however any unfulfilled obligations according to the license will remain in force, regardless of the termination.

In April, 2013 the Company completed a non-brokered private placement of 41,494,692 units at a price of $0.17 per unit for aggregate proceeds of $7,054.

On May 29, 2014, the Company closed a private placement of 28,424,152 shares at a price of $0.33 per share for proceeds of $9,380.

On July 20, 2015, the Company closed a private placement of 29,054,079 units at a price of $0.22 per unit for proceeds of $6,392.

On January 4, 2016, the Company made and entered into a 10 year Metallic Minerals Lease with the Michigan Department of Natural Resources for an area covering approximately 320 acres. Under the terms of the lease, an annual rental fee will be required at a rate of US $3.00 per acre per lease for years 1-5 and US $6.00 per acre per lease year for the years 6-10. A minimum royalty of US $10 per acre is due for the eleventh year of the lease and increases by $US 5 per acre through to the twentieth year. For the twentieth year of the lease and thereafter for the life of the lease, the minimum royalty is US $55 per acre per year.

On April 28, 2016 the Company issued to Sentient Executive GP IV Limited 952,380 common shares for a fee on the advance of the loan. The shares were booked at a fair value of $95.

On April 22, 2016, the Company entered into a term loan with Sentient Executive GP IV Limited (“Sentient”) and received an advance of $4,500. The loan is due on April 30, 2017 and has been made on an interest free basis. Sentient is to be paid 952,380 common shares, which is the equivalent value of 2.2% of the principal amount of the loan, as a fee for advancing the loan. The fee was booked at a fair value of $95. The loan is subject to early pre-payment in the event that, during the term of the loan, the Company completes a private placement of gross proceeds of $2,000 or more. On July 21, 2016, the Company closed its market offering of units of the Company for total gross proceeds of $6,950 and on September 12, 2016, the Company closed a non-brokered private placement for gross proceeds of $5,050 which being the maximum offering amount raised, Sentient was repaid the full loan of $4.5 million.

On July 21, 2016 the Company issued 92,668,908 units at a price of $0.075 per unit in a market offering for gross proceeds of $6,950. The Company reported $458 in issuance costs against the raised funds.

On July 21, 2016 the Company issued 1,203,695 warrants at a price of $0.075 per unit for an agent fee to Paradigm as per the Company’s amended and restated short form prospectus.

On September 12, 2016 the Company closed a non-brokered private placement and issued 67,331,093 units at a price of $0.075 per unit for gross proceeds of $5,050.

On August 15, 2017 the Company closed a non-brokered private placement and issued 40,982,448 units at a price of $0.075 per unit for gross proceeds of $3,074.

On June 8, 2017 the Company closed a brokered placement through a prospectus and issued 145,030,833 units at a price of $0.075 per unit for gross proceeds of $10,877. The Company also issued 1,965,093 warrants at a price of $0.075 per unit for an agent fee to Paradigm as per the Company’s prospectus.

Organizational structure.

The Company is part of no other group. During the year ended June 30, 2006 Outback Capital Inc. dba Pinefalls Gold (“PFG”) a private Alberta corporation became a majority-owned subsidiary of the Company. PFG was incorporated under the Alberta Business Corporations Act on February 6, 2001. Effective May 31, 2010, the Company completed an agreement with an arm’s length entity that resulted in it divesting of its interest in Outback Capital Inc. In June 2015 the Company incorporated North American Nickel (US) Inc. to hold a mineral lease in Michigan, which was granted in January 2016.

C. Property, plants and equipment.

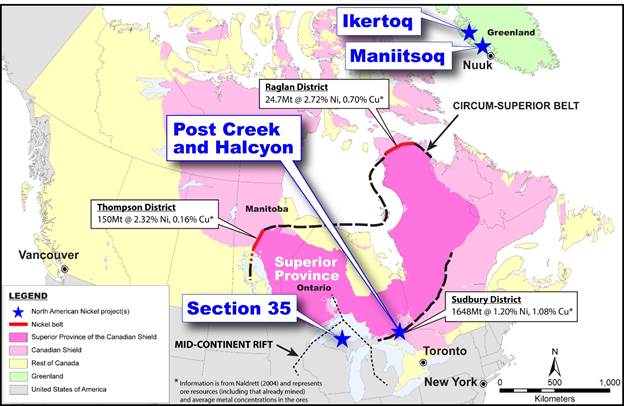

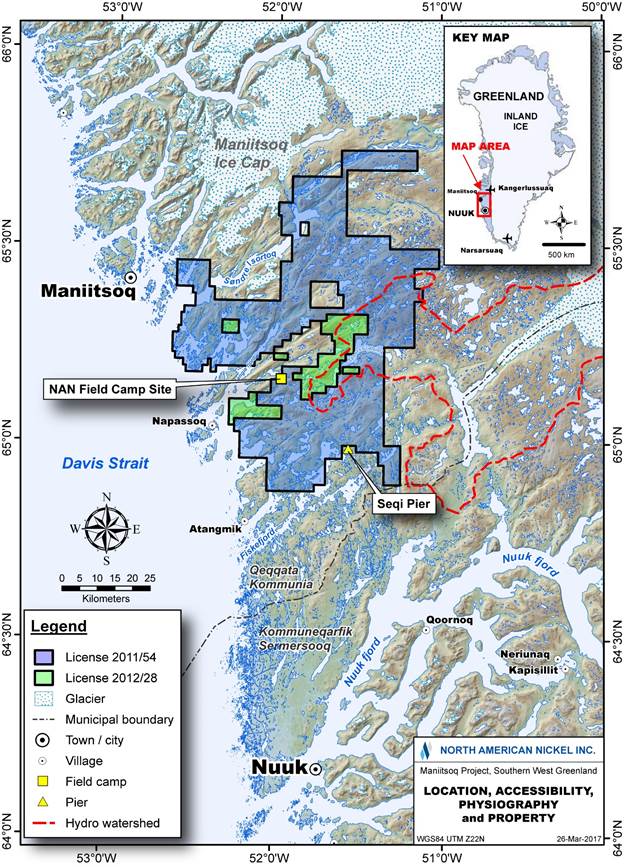

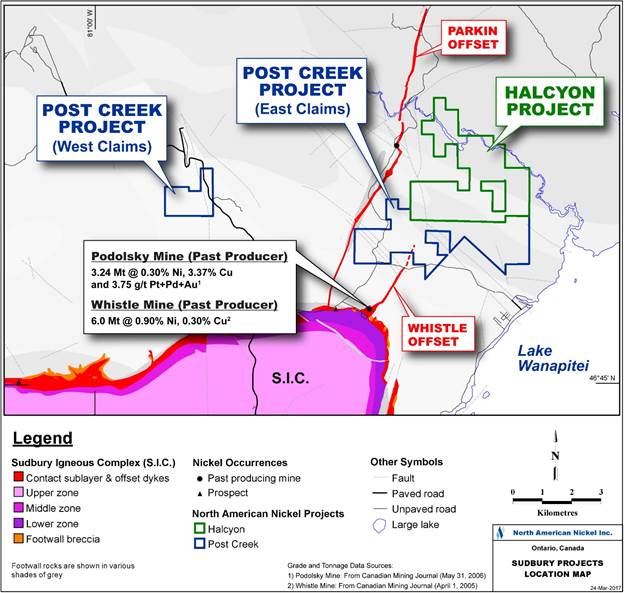

The Company has a large land package in southwest Greenland, collectively known at the Maniitsoq property. In addition, the Company has two properties, Post Creek and Halcyon, in Sudbury nickel district of Ontario and a small property, Section 35, in the Mid-Continental Rift setting of Michigan. A figure showing the locations of all of the company’s properties is displayed below.

Maniitsoq (Greenland Mineral Exploration Licenses 2011/54 and 2012/28)

The Greenland properties currently being explored for nickel-copper-copper-PGM sulphides by North American Nickel are exploration properties without mineral resources or reserves. The Maniitsoq project is centered 100 kilometres north of Nuuk, the capital of Greenland which is a safe, stable, mining-friendly jurisdiction. The centre of the project is located at 65 degrees 18 minutes north and 51 degrees 43 minutes west and has an artic climate. It is accessible year-round either by helicopter or by boat from Nuuk or Maniitsoq, the latter located on the coast approximately 15 kilometres to the west. The deepwater coastline adjacent to Maniitsoq is typical of Greenland’s southwest coast which is free of pack ice with a year-round shipping season. The optimum shipping conditions are due to the Irminger current, a tributary of the warming Gulf Stream flowing continuously past the south west coastline of Greenland. There is no infrastructure on the property; however, the Seqi deepwater pier and a quantified watershed for hydropower are located peripheral to the project. A location map for the property is given below.

The Maniitsoq property consists of four exploration licences, No. 2011/54 (2,689 km2), No. 2012/28 (296 km2), No. 2018/21 (63 km2) and No 2018/31 (33 km2). The property is centered on the 75 kilometre by 15 kilometre Greenland Norite Belt which hosts numerous high-grade nickel-copper sulphide occurrences associated with mafic and ultramafic intrusions.

Between 1995 and 2011, various companies carried out exploration over portions of the project area. The most extensive work was carried out by Kryolitselskabet Øresund A/S Company (KØ) who explored the project area from 1959 to 1973. KØ discovered a number of surface and near surface nickel-copper sulphide occurrences and this work was instrumental in proving the nickel prospectivity of the Greenland Norite Belt.

The Company acquired the Maniitsoq project because it believed that modern, time-domain, helicopter-borne electromagnetic (EM) systems would be more effective at detecting nickel sulphide deposits in the rugged terrain of Maniitsoq than previous, older airborne fixed wing geophysical surveys available to previous explorers. In addition, modern, time domain surface and borehole EM systems could be used to target mineralization in the sub-surface.

Effective August 15, 2011, the Company was granted an exploration license, No. 2011/54(the “Sulussugut License”), by the Bureau of Minerals and Petroleum (“BMP”) of Greenland for exclusive exploration rights of an area located near Sulussugut, Greenland. The Company paid a license fee of $6 (Danish Krones (“DKK”) 31) upon granting of the Sulussugut License. The Sulussugut License was valid for 5 years until December 31, 2015, with December 31, 2011 being the first year providing the Company meets the terms of the license, which includes that specified eligible exploration expenditures must be made. The application for another 5 year term on the Sulussugut License was submitted to the Greenland Mineral Licence & Safety Authority (MLSA) which was effective on April 11, 2016, with December 31, 2017 being the seventh year.

Under the terms of the Sulussugut License the Company was obligated to reduce the area of the license by at least 30% (1,452 square kilometres) by December 31, 2013. The Company completed this prior to year-end 2013

The Greenland MLSA for the years 2017 and 2016 has adjusted the minimum required exploration expenditures to zero. The accumulated exploration credits held at the end of 2017, DKK 246,507 (approximately $48,513) can be carried forward until 2020 DKK 85,094, until 2019 DKK 61,109 and until 2018 DKK 59,150. There will be an annual licence fee on the Sulussugut License for year 7 and forward of approximately DKK 41. Details of required work expenditures and accrued work credits are tabulated and given below.

Sulussugut License — 2011/54 (All amounts in table are expressed in thousands of DKK)

|

Exploration Commitment |

|

2012 |

|

2013 |

|

2014 |

|

2015 |

|

2016 |

|

2017 |

| |

|

Fixed amount |

|

149 |

|

310 |

|

313 |

|

317 |

|

— |

|

650 |

| |

|

4841 km2 of DKK 1.460 per km2 |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

4841 km2 of DKK 1.490 per km2 |

|

7,213 |

|

|

|

|

|

|

|

|

|

|

| |

|

3336 km2 of DKK 7.760 per km2 |

|

|

|

25,887 |

|

|

|

|

|

|

|

|

| |

|

2689 km2 of DKK 7.830 per km2 |

|

|

|

|

|

21,055 |

|

— |

|

— |

|

|

| |

|

2689 km2 of DKK 7.940 per km2 |

|

|

|

|

|

|

|

21,351 |

|

— |

|

|

| |

|

2689 km2 of DKK 16.260 per km2 |

|

|

|

|

|

|

|

|

|

|

|

43,723 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Exploration obligation |

|

7,362 |

|

26,197 |

|

21,368 |

|

21,668 |

|

— |

|

44,374 |

| |

|

Approved exploration expenditures |

|

23,616 |

|

37,349 |

|

55,509 |

|

59,150 |

|

61,109 |

|

85,094 |

| |

|

Exploration obligation |

|

(7,362 |

) |

(26,198 |

) |

(21,368 |

) |

(21,668 |

) |

— |

|

— |

| |

|

Credit from previous year |

|

1,276 |

|

17,530 |

|

28,681 |

|

62,822 |

|

100,304 |

|

161,413 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Total Credit |

DDK |

|

17,530 |

|

28,681 |

|

62,822 |

|

100,304 |

|

161,413 |

|

246,507 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Average Annual Rate DDK to CAD |

|

0.1726 |

|

0.1834 |

|

0.1968 |

|

0.1901 |

|

0.1969 |

|

0.1968 |

| |

The accumulated exploration credits held at the end of 2017, DKK 246,507 (approximately $48,513) can be carried forward as follows:

Carry forward period:

a) DKK 59,150 from 2015 until December 31, 2018

b) DKK 61,109 from 2016 until December 31, 2019

c) DKK 85,094 from 2017 until December 31, 2020

On the first 5 year license, the Company completed the exploration requirements of an estimated minimum of DKK 83,809 (approximately $15,808) between the years ended December 31, 2011 to 2015 by incurring $26,115,831 on the Sulussugut License.

In 2016, there was no exploration commitment. The Company completed approved expenditures for 2017 DKK 85,094, for 2016, DKK 61,109 (approximately, $16,746 and $12,032, respectively). With a credit from 2015 of DKK 59,150 (approximately $11,250) and credit from 2016 of DKK 61,109 (approximately $12,032), and a commitment of $nil left the Company with excess credits of DKK 246,507 (approximately $48,513). The Sulussugut License area was not reduced in 2017.

Effective March 4, 2012, the Company was granted an additional exploration license, No. 2012/28 (the “Ininngui License”), by the BMP of Greenland for exclusive exploration rights over an area covering a total of 142 square kilometres near Ininngui, Greenland. The Ininngui License is contiguous with the Sulussugut License. The Company paid a license fee of DKK 32 upon granting of the Ininngui License. The Ininngui License was valid for 5 years until December 31, 2016, with December 31, 2012 being the first year. The application for another 5 year term on the Ininngui License was submitted to the Greenland Mineral Licence & Safety Authority (MLSA) which was effective March 3, 2017, with December 31, 2017 being the sixth year.

Details of required work expenditures and accrued work credits are tabulated and given below.

Ininngui License - 2012/28 (All amounts in table are expressed in thousands of DKK)

|

Exploration Commitment |

|

2012 |

|

2013 |

|

2014 |

|

2015 |

|

2016 |

|

2017 |

| |

|

Fixed amount |

|

149 |

|

155 |

|

313 |

|

318 |

|

323 |

|

— |

| |

|

142 km2 of DKK 1.490 per km2 |

|

211 |

|

|

|

|

|

|

|

|

|

|

| |

|

265 km2 of DKK 1.550 per km2 |

|

|

|

411 |

|

|

|

|

|

|

|

|

| |

|

265 km2 of DKK 7.830 per km2 |

|

|

|

|

|

2,075 |

|

|

|

|

|

|

| |

|

296 km2 of DKK 7.940 per km2 |

|

|

|

|

|

|

|

2,350 |

|

|

|

|

| |

|

296 km2 of DKK 8.080 per km2 |

|

|

|

|

|

|

|

|

|

2,392 |

|

|

| |

|

296 km2 of DKK 8.080 per km2 |

|

|

|

|

|

|

|

|

|

|

|

— |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Exploration obligation |

|

360 |

|

566 |

|

2,388 |

|

2,668 |

|

2,715 |

|

— |

| |

|

Total Credits Available |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Approved exploration expenditures |

|

2,872 |

|

2,966 |

|

5,470 |

|

6,276 |

|

6,790 |

|

9,367 |

| |

|

Exploration obligation |

|

(360 |

) |

(576 |

) |

(2,388 |

) |

(2,668 |

) |

(2,715 |

) |

— |

| |

|

Credit from previous year |

|

— |

|

2,512 |

|

4,902 |

|

7,984 |

|

11,592 |

|

15,667 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Total Credit |

DDK |

|

2,512 |

|

4,902 |

|

7,984 |

|

11,592 |

|

15,667 |

|

25,044 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Average Annual Rate DDK to CAD |

|

0.1726 |

|

0.1834 |

|

0.1968 |

|

0.1901 |

|

0.1969 |

|

0.1968 |

| |

Carry forward period:

a) DKK 6,276 from 2015 until December 31, 2018

b) DKK 6,790 from 2016 until December 31, 2019

c) DKK 9,367 from 2017 until December 31, 2020

On the first 5 year license, the Company completed the exploration requirements of an estimated minimum of DKK 8,697 (approximately $1,635) between the years ended December 31, 2012 to 2016 by incurring $2,722 on the Ininngui License.

In 2016 (year 5 of the Ininngui License), there was an exploration commitment of DKK 2,715 (approximately $535). The Company completed approved expenditures for 2016 of DKK 6,790 (approximately $1,337). With a credit from 2015 of DKK 2,276 and 2016 of DKK 6,790 (approximately $433 and $1,337, respectively) and a commitment of DKK Nil for 2017, resulting in excess credits of DKK 25,044 (approximately $4,929). The Ininngui License area was not reduced in 2017.

The required minimum exploration expenditures on the Ininngui License for year 5, ending December 31, 2016 was based on an annual approximation of DKK 2,715 (approximately CDN $535).

For both licenses, future required minimum eligible exploration expenses will be adjusted each year on the basis of the change to the Danish Consumer Price Index.

Should the Company not incur the minimum eligible exploration expenses on either license in any one year from years 2-5, the Company may pay 50% of the difference in cash to BMP as full compensation for that year. This procedure may not be used for more than 2 consecutive calendar years and to December 31, 2012, the Company has not used the procedure for either license.

The Company may terminate the licenses at any time; however any unfulfilled obligations according to the licenses will remain in force, regardless of the termination.

For both licenses, at the expiration of the second licence period (years 6-10), the Company may apply for a new 3-year licence for years 11 to 13. Thereafter, the Company may apply for additional 3-year licences for years 14 to 16, 17 to 19 and 20 to 22. The Company will be required to pay additional license fees and will be obligated to incur minimum eligible exploration expenses for such years.

The Company may terminate the licenses at any time; however any unfulfilled obligations according to the licenses will remain in force, regardless of the termination.

In conjunction with the granting of the Sulussugut License, on August 12, 2011, the Company entered into an arm’s length Intellectual Property and Data Acquisition Agreement (the “IP Acquisition Agreement”) with Hunter Minerals Pty Limited (“Hunter”) and Spar Resources Pty Limited (“Spar”). Pursuant to the IP Acquisition Agreement, Hunter and Spar agreed to sell the IP Rights to the Company in consideration for the Company paying $300 in cash ($150 to each of Hunter and Spar which is paid) and the issuing of 12,960,000 share purchase warrants, 6,480,000 to each of Hunter and Spar exercisable for a period of five years expiring on August 30, 2016. The warrants were exercisable at the following prices, 4,750,000 of the warrants are at a price of $0.50 per share, 4,750,000 of the warrants are at a price of $0.70 per share and 3,460,000 of the warrants are at a price of $1.00 per share. The warrants were subject to an accelerated exercise provision in the event the Company relinquished its interests in the Maniitsoq Licenses or any other mineral titles held within a defined area of interest without receiving consideration for such relinquishment. The granted warrants were recorded at a fair value of $1,813 using the Black-Scholes option-pricing model. As of August 30, 2016 the warrants expired unexercised and the Company has reversed the fair value of $1,813 to deficit. The Company also granted to each of Hunter and Spar or their designates a 1.25% net smelter returns royalty, subject to rights of the Company to reduce both royalties to a 0.5% net smelter returns royalty upon payment to each of Hunter and Spar (or their designates) of $1,000 on or

before the 60th day following a decision to commence commercial production on the mineral properties. On August 30, 2011 the Company issued 200,000 common shares at $0.14 per share for a value of $28 as a finder’s fee on the Greenland project.

A NI 43-101 compliant Technical Report and updated 43-101 compliant Technical Report, both completed by J. F. Ravenelle and L. Weiershäuser, were completed in March 2016 and March 2017, respectively. Both reports were filed on SEDAR.

During the period 2011 to 2017, the Company has carried out extensive exploration drilling programs on the Maniitsoq property to search for Ni-Cu-Co-PGM sulphide deposits. Cumulative exploration expenditures totaled C$48.6 million as of December 31, 2017.

In 2017, the Company implemented an $11.1M exploration program consisting of 8,767 metres of diamond drilling in 23 holes, two regional and four detailed induced polarisation (IP) surveys covering 13km2, surface and borehole electromagnetic (EM) surveys, borehole gyro, optical televiewer and physical properties surveys, a comprehensive review of geochemistry and petrology of the noritic intrusions, a surface geology sampling and mapping program, and 3D modeling of the mineral zones.

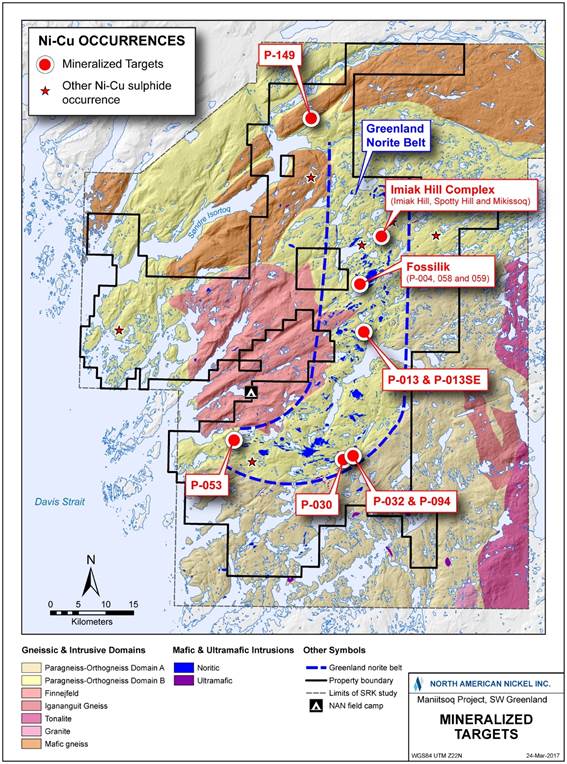

The Company’s exploration efforts have been focused on defining in three dimensions the extent of nickel sulphide mineralization and attaining a greater understanding of the geological environment hosting the high grade nickel mineralization. This work has been successful and resulted in the following:

The Company continued its systematic evaluation of the depth extent of known mineral zones to identify thicker and more extensive sheets of breccia-style mineralization. This work continues to advance the understanding of the host intrusions and refine geophysical targeting tools. The result has been the intersection of significant nickel-copper sulphide mineralization at multiple locations.

The Mikissoq zone was extended by 60 meters down plunge; the P-013 SE mineral zone was extended for 140m down-plunge and the P-058 zone at Fossilik was extended to a vertical depth of 650 m. Extensive zones of melanorite were mapped in the footprint of the mineral zones of the Imiak Hill Complex (IHC) as well as Fossilik.

Petrological and geochemical studies of the differentiated mafic intrusions underscores the importance of melanorite as a host to high grade semi-massive breccia style nickel-copper sulphides enveloped in a halo of lower grade mineralization.

Interpretation of IP and gravity data coupled with petrology and geochemistry highlights the potential for the known mineral zones to expand in width within the adjacent melanorite intrusions.

The figure and table below, respectively, show the location of significant mineralized targets and drill intersections on the property.

Location of Significant Mineralized Targets:

Summary of

Drilling Assay Highlights

|

Target |

|

Drillhole |

|

Zone |

|

From (m) |

|

To (m) |

|

Core Length |

|

True Width |

|

Ni % |

|

Cu % |

|

Co % |

|

Pt+Pd+Au |

|

|

Imiak Hill Complex |

| ||||||||||||||||||||

|

Imiak Hill |

|

MQ-12-001 |

|

|

|

56.10 |

|

59.94 |

|

3.84 |

|

2.07 |

|

1.19 |

|

0.14 |

|

0.04 |

|

0.01 |

|

|

|

|

MQ-12-002 |

|

|

|

55.90 |

|

70.08 |

|

14.18 |

|

7.14 |

|

1.33 |

|

0.38 |

|

0.04 |

|

0.01 |

|

|

|

|

MQ-13-024 |

|

|

|

135.70 |

|

150.90 |

|

15.20 |

|

8.80 |

|

2.62 |

|

0.43 |

|

0.09 |

|

0.02 |

|

|

|

|

Incl. |

|

|

|

136.75 |

|

141.98 |

|

5.23 |

|

3.02 |

|

5.03 |

|

0.30 |

|

0.16 |

|

0.03 |

|

|

|

|

MQ-13-026 |

|

|

|

156.70 |

|

175.32 |

|

18.62 |

|

12.35 |

|

4.31 |

|

0.62 |

|

0.14 |

|

0.02 |

|

|

|

|

MQ-13-028 |

|

|

|

182.09 |

|

206.84 |

|

24.75 |

|

13.65 |

|

3.19 |

|

1.14 |

|

0.11 |

|

0.01 |

|

|

|

|

MQ-14-037 |

|

|

|

220.51 |

|

231.54 |

|

11.03 |

|

6.65 |

|

3.07 |

|

0.53 |

|

0.08 |

|

0.02 |

|

|

|

|

Incl. |

|

|

|

220.51 |

|

223.76 |

|

3.25 |

|

1.96 |

|

6.48 |

|

0.29 |

|

0.17 |

|

0.02 |

|

|

|

|

MQ-14-072 |

|

|

|

173.75 |

|

190.10 |

|

16.35 |

|

7.92 |

|

2.51 |

|

0.77 |

|

0.08 |

|

0.02 |

|

|

|

|

Incl. |

|

|

|

179.90 |

|

186.25 |

|

6.35 |

|

3.08 |

|

3.14 |

|

1.05 |

|

0.10 |

|

0.02 |

|

|

Spotty Hill |

|

MQ-12-005 |

|

|

|

63.00 |

|

157.00 |

|

94.00 |

|

28.69 |

|

0.94 |

|

0.24 |

|

0.03 |

|

0.30 |

|

|

|

|

Incl. |

|

|

|

113.00 |

|

136.87 |

|

23.87 |

|

6.83 |

|

1.70 |

|

0.42 |

|

0.05 |

|

0.52 |

|

|

|

|

MQ-14-009 |

|

|

|

79.00 |

|

96.50 |

|

17.50 |

|

6.43 |

|

0.27 |

|

0.06 |

|

0.01 |

|

0.08 |

|

|

|

|

MQ-14-052 |

|

|

|

55.70 |

|

64.00 |

|

8.30 |

|

3.81 |

|

0.25 |

|

0.06 |

|

0.01 |

|

0.08 |

|

|

|

|

MQ-14-058 |

|

|

|

167.32 |

|

202.05 |

|

34.73 |

|

18.73 |

|

0.53 |

|

0.17 |

|

0.02 |

|

0.18 |

|

|

|

|

MQ-14-062 |

|

|

|

45.20 |

|

72.12 |

|

26.92 |

|

11.08 |

|

1.16 |

|

0.28 |

|

0.04 |

|

0.41 |

|

|

|

|

Incl. |

|

|

|

62.65 |

|

71.20 |

|

8.55 |

|

3.39 |

|

2.98 |

|

0.59 |

|

0.10 |

|

0.86 |

|

|

|

|

MQ-14-065 |

|

|

|

50.00 |

|

111.29 |

|

61.29 |

|

20.54 |

|

0.66 |

|

0.17 |

|

0.02 |

|

0.25 |

|

|

|

|

Incl. |

|

|

|

79.50 |

|

90.10 |

|

10.60 |

|

3.38 |

|

1.69 |

|

0.34 |

|

0.05 |

|

0.50 |

|

|

|

|

MQ-15-075 |

|

|

|

236.45 |

|

255.70 |

|

19.25 |

|

8.03 |

|

0.92 |

|

0.21 |

|

0.03 |

|

0.28 |

|

|

|

|

Incl. |

|

|

|

236.45 |

|

252.00 |

|

15.55 |

|

6.73 |

|

1.06 |

|

0.24 |

|

0.04 |

|

0.31 |

|

|

|

|

MQ-16-121 |

|

|

|

382.25 |

|

387.00 |

|

4.75 |

|

2.84 |

|

1.59 |

|

0.30 |

|

0.04 |

|

0.66 |

|

|

|

|

MQ-17-143 |

|

|

|

381.00 |

|

388.80 |

|

7.80 |

|

|

|

1.35 |

|

0.26 |

|

0.04 |

|

1.85 |

|

|

|

|

Incl |

|

|

|

381.00 |

|

386.00 |

|

5.00 |

|

|

|

1.69 |

|

0.33 |

|

0.05 |

|

2.71 |

|

|

|

|

Incl |

|

|

|

381.00 |

|

382.00 |

|

1.00 |

|

|

|

1.62 |

|

0.93 |

|

0.04 |

|

10.71 |

|

|

Mikissoq |

|

MQ-13-027 |

|

HW |

|

33.84 |

|

58.82 |

|

24.98 |

|

20.02 |

|

0.71 |

|

0.31 |

|

0.02 |

|

0.06 |

|

|

|

|

|

|

Central |

|

66.99 |

|

70.09 |

|

3.10 |

|

2.48 |

|

0.53 |

|

0.18 |

|

0.02 |

|

0.02 |

|

|

|

|

|

|

FW |

|

88.25 |

|

96.00 |

|

7.75 |

|

6.21 |

|

0.76 |

|

0.28 |

|

0.02 |

|

0.07 |

|

|

|

|

MQ-13-029 |

|

HW |

|

45.00 |

|

71.22 |

|

26.22 |

|

18.02 |

|

0.48 |

|

0.22 |

|

0.02 |

|

0.04 |

|

|

|

|

|

|

Central |

|

82.01 |

|

103.51 |

|

21.50 |

|

14.90 |

|

0.68 |

|

0.48 |

|

0.02 |

|

0.05 |

|

|

|

|

|

|

FW |

|

103.51 |

|

113.50 |

|

9.99 |

|

6.96 |

|

4.65 |

|

0.33 |

|

0.12 |

|

0.14 |

|

|

|

|

MQ-14-073 |

|

HW |

|

57.75 |

|

77.58 |

|

19.83 |

|

12.65 |

|

0.76 |

|

0.26 |

|

0.02 |

|

0.04 |

|

|

|

|

|

|

Central |

|

88.50 |

|

101.40 |

|

12.90 |

|

8.27 |

|

0.83 |

|

0.24 |

|

0.02 |

|

0.05 |

|

|

Target |

|

Drillhole |

|

Zone |

|

From (m) |

|

To (m) |

|

Core Length |

|

True Width |

|

Ni % |

|

Cu % |

|

Co % |

|

Pt+Pd+Au |

|

|

|

|

|

|

FW |

|

112.54 |

|

117.34 |

|

4.80 |

|

3.10 |

|

2.10 |

|

0.27 |

|

0.05 |

|

0.04 |

|

|

|

|

MQ-16-113 |

|

New |

|

233.75 |

|

287.00 |

|

53.25 |

|

32.36 |

|

0.81 |

|

0.36 |

|

0.02 |

|

0.05 |

|

|

|

|

Incl. |

|

|

|

233.75 |

|

238.90 |

|

5.15 |

|

3.12 |

|

2.56 |

|

0.38 |

|

0.05 |

|

0.12 |

|

|

|

|

And |

|

|

|

256.00 |

|

261.00 |

|

5.00 |

|

3.04 |

|

1.10 |

|

0.57 |

|

0.03 |

|

0.10 |

|

|

|

|

And |

|

|

|

275.85 |

|

279.65 |

|

3.80 |

|

2.32 |

|

1.87 |

|

0.28 |

|

0.05 |

|

0.06 |

|

|

|

|

MQ-16-117 |

|

New |

|

268.70 |

|

342.75 |

|

74.05 |

|

37.59 |

|

1.08 |

|

0.54 |

|

0.03 |

|

0.11 |

|

|

|

|

Incl. |

|

|

|

285.70 |

|

291.00 |

|

5.30 |

|

2.67 |

|

2.10 |

|

0.44 |

|

0.04 |

|

0.08 |

|

|

|

|

And |

|

|

|

309.25 |

|

322.90 |

|

13.65 |

|

6.96 |

|

1.84 |

|

0.64 |

|

0.05 |

|

0.10 |

|

|

|

|

And |

|

|

|

329.85 |

|

335.40 |

|

5.55 |

|

2.84 |

|

1.26 |

|

0.45 |

|

0.03 |

|

0.39 |

|

|

|

|

MQ-16-118 |

|

New |

|

322.00 |

|

369.00 |

|

47.00 |

|

21.40 |

|

0.51 |

|

0.25 |

|

0.01 |

|

0.15 |

|

|

|

|

Incl. |

|

|

|

323.00 |

|

338.00 |

|

15.00 |

|

6.80 |

|

1.03 |

|

0.32 |

|

0.02 |

|

0.17 |

|

|

|

|

MQ-17-135 |

|

|

|

359.85 |

|

435.60 |

|

75.75 |

|

|

|

1.10 |

|

0.43 |

|

0.03 |

|

0.12 |

|

|

|

|

Incl |

|

|

|

359.85 |

|

370.10 |

|

10.25 |

|

|

|

2.29 |

|

1.33 |

|

0.05 |

|

0.27 |

|

|

|

|

Incl |

|

|

|

416.35 |

|

435.60 |

|

19.25 |

|

|

|

1.89 |

|

0.26 |

|

0.04 |

|

0.07 |

|

|

|

|

Incl |

|

|

|

417.00 |

|

423.00 |

|

6.00 |

|

|

|

2.94 |

|

0.29 |

|

0.07 |

|

0.05 |

|

|

|

|

Incl |

|

|

|

425.90 |

|

426.20 |

|

0.30 |

|

|

|

9.55 |

|

0.80 |

|

0.24 |

|

0.61 |

|

|

Fossilik Area |

| ||||||||||||||||||||

|

P-058 |

|

MQ-12-007 |

|

|

|

78.24 |

|

82.31 |

|

4.07 |

|

2.03 |

|

0.30 |

|

0.13 |

|

0.01 |

|

0.02 |

|

|

|

|

MQ-14-054 |

|

|

|

70.60 |

|

76.18 |

|

5.58 |

|

3.01 |

|

1.72 |

|

0.26 |

|

0.04 |

|

0.08 |

|

|

|

|

Incl. |

|

|

|

70.60 |

|

71.22 |

|

0.62 |

|

0.33 |

|

6.18 |

|

0.56 |

|

0.16 |

|

0.08 |

|

|

|

|

And |

|

|

|

73.65 |

|

74.46 |

|

0.81 |

|

0.44 |

|

5.23 |

|

0.07 |

|

0.11 |

|

0.35 |

|

|

|

|

MQ-14-059 |

|

|

|

22.26 |

|

24.00 |

|

1.74 |

|

0.44 |

|

2.54 |

|

2.75 |

|

0.07 |

|

0.09 |

|

|

|

|

Incl. |

|

|

|

23.55 |

|

24.00 |

|

0.45 |

|

0.11 |

|

4.19 |

|

7.73 |

|

0.12 |

|

0.10 |

|

|

|

|

MQ-15-077 |

|

|

|

149.00 |

|

170.50 |

|

21.50 |

|

7.04 |

|

0.55 |

|

0.27 |

|

0.02 |

|

0.08 |

|

|

|

|

MQ-16-105 |

|

|

|

323.55 |

|

333.75 |

|

10.20 |

|

4.43 |

|

3.41 |

|

0.28 |

|

0.10 |

|

0.13 |

|

|

|

|

Incl. |

|

|

|

324.20 |

|

328.30 |

|

4.10 |

|

1.78 |

|

4.85 |

|

0.29 |

|

0.14 |

|

0.13 |

|

|

|

|

And |

|

|

|

330.90 |

|

331.85 |

|

0.95 |

|

0.41 |

|

6.31 |

|

0.12 |

|

0.18 |

|

0.07 |

|

|

|

|

MQ-16-111 |

|

|

|

392.09 |

|

395.15 |

|

3.06 |

|

1.04 |

|

3.93 |

|

0.25 |

|

0.10 |

|

0.09 |

|

|

|

|

MQ-17-146 |

|

|

|

408.30 |

|

410.20 |

|

1.90 |

|

|

|

2.51 |

|

0.15 |

|

0.08 |

|

0.03 |

|

|

|

|

Incl |

|

|

|

408.30 |

|

408.90 |

|

0.60 |

|

|

|

4.70 |

|

0.40 |

|

0.18 |

|

0.06 |

|

|

|

|

Incl |

|

|

|

409.80 |

|

410.20 |

|

0.40 |

|

|

|

4.73 |

|

0.07 |

|

0.12 |

|

0.06 |

|

|

|

|

|

|

|

|

451.50 |

|

462.20 |

|

10.70 |

|

|

|

2.53 |

|

1.26 |

|

0.07 |

|

0.11 |

|

|

|

|

Incl |

|

|

|

452.50 |

|

456.00 |

|

3.50 |

|

|

|

4.97 |

|

2.30 |

|

0.13 |

|

0.20 |

|

|

|

|

Incl |

|

|

|

458.00 |

|

460.20 |

|

2.20 |

|

|

|

3.35 |

|

1.31 |

|

0.10 |

|

0.16 |

|

|

P-059 |

|

MQ-15-078 |

|

|

|

79.25 |

|

91.40 |

|

12.15 |

|

NC |

|

1.16 |

|

1.00 |

|

0.03 |

|

0.27 |

|

|

P-004 |

|

MQ-13-018 |

|

|

|

40.24 |

|

72.43 |

|

32.19 |

|

NC |

|

0.59 |

|

0.18 |

|

0.02 |

|

0.21 |

|

|

|

|

Incl. |

|

|

|

51.75 |

|

56.28 |

|

4.53 |

|

NC |

|

1.06 |

|

0.23 |

|

0.04 |

|

0.33 |

|

|

Target |

|

Drillhole |

|

Zone |

|

From (m) |

|

To (m) |

|

Core Length |

|

True Width |

|

Ni % |

|

Cu % |

|

Co % |

|

Pt+Pd+Au |

|

|

|

|

MQ-14-051 |

|

|

|

231.14 |

|

235.45 |

|

4.31 |

|

NC |

|

0.94 |

|

0.17 |

|

0.03 |

|

0.99 |

|

|

P-013 Area |

| ||||||||||||||||||||

|

P-013 |

|

MQ-14-066 |

|

|

|

157.00 |

|

168.00 |

|

11.00 |

|

6.68 |

|

1.31 |

|

0.15 |

|

0.04 |

|

0.07 |

|

|

|

|

Incl. |

|

|

|

158.43 |

|

164.28 |

|

5.85 |

|

3.55 |

|

2.07 |

|

0.12 |

|

0.05 |

|

0.07 |

|

|

|

|

MQ-14-068 |

|

|

|

126.70 |

|

142.55 |

|

15.85 |

|

12.06 |

|

0.87 |

|

0.27 |

|

0.03 |

|

0.09 |

|

|

|

|

Incl. |

|

|

|

130.85 |

|

134.25 |

|

3.40 |

|

2.59 |

|

2.07 |

|

0.34 |

|

0.06 |

|

0.15 |

|

|

|

|

MQ-15-079 |

|

|

|

185.05 |

|

195.70 |

|

10.65 |

|

2.93 |

|

1.03 |

|

0.39 |

|

0.04 |

|

0.06 |

|

|

|

|

|

|

|

|

200.75 |

|

206.00 |

|

5.25 |

|

1.43 |

|

1.15 |

|

0.18 |

|

0.03 |

|

0.07 |

|

|

|

|

MQ-15-094 |

|

|

|

212.75 |

|

224.70 |

|

11.95 |

|

5.66 |

|

0.94 |

|

0.44 |

|

0.02 |

|

0.10 |

|

|

|

|

Incl. |

|

|

|

215.10 |

|

217.00 |

|

1.90 |

|

0.90 |

|

1.63 |

|

0.37 |

|

0.05 |

|

0.08 |

|

|

|

|

And |

|

|

|

220.20 |

|

224.70 |

|

4.50 |

|

2.13 |

|

1.23 |

|

0.22 |

|

0.03 |

|

0.08 |

|

|

P-013 SE |

|

MQ-16-109 |

|

|

|

166.90 |

|

205.65 |

|

38.75 |

|

NC |

|

1.19 |

|

0.43 |

|

0.03 |

|

0.23 |

|

|

|

|

Incl. |

|

|

|

166.90 |

|

180.25 |

|

13.35 |

|

NC |

|

2.88 |

|

0.80 |

|

0.06 |

|

0.47 |

|

|

|

|

MQ-17-140 |

|

|

|

247.35 |

|

268.20 |

|

20.85 |

|

NC |

|

0.65 |

|

0.47 |

|

0.02 |

|

0.38 |

|

|

|

|

Incl |

|

|

|

247.35 |

|

261.60 |

|

14.25 |

|

NC |

|

0.75 |

|

0.64 |

|

0.02 |

|

0.52 |

|

|

|

|

Incl |

|

|

|

267.00 |

|

268.20 |

|

1.20 |

|

NC |

|

1.65 |

|

0.12 |

|

0.04 |

|

0.19 |

|

|

|

|

MQ-17-142 |

|

|

|

298.00 |

|

303.70 |

|

5.70 |

|

NC |

|

0.50 |

|

0.51 |

|

0.02 |

|

0.79 |

|

|

|

|

|

|

|

|

316.91 |

|

317.50 |

|

0.59 |

|

NC |

|

0.72 |

|

0.27 |

|

0.02 |

|

0.30 |

|

|

|

|

|

|

|

|

431.30 |

|

438.45 |

|

7.15 |

|

NC |

|

0.23 |

|

0.09 |

|

0.01 |

|

0.13 |

|

|

|

|

Incl |

|

|

|

431.55 |

|

432.45 |

|

0.90 |

|

NC |

|

0.59 |

|

0.29 |

|

0.02 |

|

0.39 |

|

|

P-030-032-094 Area |

| ||||||||||||||||||||

|

P-030 |

|

MQ-14-070 |

|

|

|

40.75 |

|

60.85 |

|

20.10 |

|

NC |

|

0.63 |

|

0.20 |

|

0.02 |

|

0.18 |

|

|

|

|

Incl. |

|

|

|

53.30 |

|

54.50 |

|

1.20 |

|

NC |

|

1.86 |

|

0.52 |

|

0.06 |

|

0.49 |

|

|

P-032 |

|

MQ-15-090 |

|

|

|

71.90 |

|

85.70 |

|

13.80 |

|

NC |

|

0.79 |

|

0.27 |

|

0.02 |

|

0.07 |

|

|

|

|

Incl. |

|

|

|

71.90 |

|

77.00 |

|

5.10 |

|

NC |

|

1.06 |

|

0.37 |

|

0.03 |

|

0.09 |

|

|

|

|

And |

|

|

|

84.20 |

|

85.70 |

|

1.50 |

|

NC |

|

2.47 |

|

0.69 |

|

0.08 |

|

0.23 |

|

|

|

|

MQ-15-100 |

|

|

|

122.50 |

|

130.50 |

|

8.00 |

|

NC |

|

0.58 |

|

0.14 |

|

0.02 |

|

0.06 |

|

|

|

|

Incl. |

|

|

|

125.90 |

|

126.90 |

|

1.00 |

|

NC |

|

1.60 |

|

0.34 |

|

0.05 |

|

0.19 |

|

|

P-094 |

|

MQ-16-124 |

|

|

|

55.00 |

|

63.00 |

|

8.00 |

|

NC |

|

0.54 |

|

0.16 |

|

0.02 |

|

0.07 |

|

|

P-053 Area |

| ||||||||||||||||||||

|

P-053 |

|

MQ-15-082 |

|

HW |

|

93.00 |

|

116.70 |

|

23.70 |

|

16.12 |

|

1.98 |

|

0.62 |

|

0.09 |

|

0.19 |

|

|

|

|

Incl. |

|

|

|

93.00 |

|

104.50 |

|

11.50 |

|

7.84 |

|

1.12 |

|

0.91 |

|

0.05 |

|

0.12 |

|

|

|

|

And |

|

|

|

104.50 |

|

116.70 |

|

12.20 |

|

8.28 |

|

2.78 |

|

0.36 |

|

0.13 |

|

0.26 |

|

|

|

|

MQ-15-084 |

|

HW |

|

196.00 |

|

201.60 |

|

5.60 |

|

4.73 |

|

1.03 |

|

0.34 |

|

0.05 |

|