| As filed with the Securities and Exchange Commission on | ||

| <R> | ||

| September 26, 2018 | ||

| </R> | ||

| SECURITIES AND EXCHANGE COMMISSION | ||

| WASHINGTON, D.C. 20549 | ||

| ---------------- | ||

| FORM N-1A | ||

| ---- | ||

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | / X / | |

| ---- | ||

| ---- | ||

| Pre-Effective Amendment No. | / / | |

| ---- | ||

| ---- | ||

| <R> | ||

| Post-Effective Amendment No. 39 | / X / | |

| </R> | ||

| and | ---- | |

| ---- | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY | / X / | |

| ACT OF 1940 | ---- | |

| ---- | ||

| <R> | ||

| Amendment No. 40 | / X / | |

| </R> | ||

| (Check appropriate box or boxes) | ---- | |

| --------------- | ||

| PUTNAM NEW JERSEY TAX EXEMPT INCOME FUND | ||

| (Registration No. 33-32550; 811-05977) | ||

| (Exact name of registrants as specified in charter) | ||

| ---- | ||

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | / X / | |

| ---- | ||

| ---- | ||

| Pre-Effective Amendment No. | / / | |

| ---- | ||

| ---- | ||

| <R> | ||

| Post-Effective Amendment No. 48 | / X / | |

| </R> | ||

| and | ---- | |

| ---- | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY | / X / | |

| ACT OF 1940 | ---- | |

| ---- | ||

| <R> | ||

| Amendment No. 49 | / X / | |

| </R> | ||

| (Check appropriate box or boxes) | ---- | |

| --------------- | ||

| PUTNAM MASSACHUSETTS TAX EXEMPT INCOME FUND | ||

| Registration No. 33-5416; 811-04518 | ||

| PUTNAM MINNESOTA TAX EXEMPT INCOME FUND | ||

| Registration No. 33-8916; 811-04527 | ||

| PUTNAM OHIO TAX EXEMPT INCOME FUND | ||

| Registration No. 33-8924; 811-04528 | ||

| (Exact name of registrants as specified in charter) | ||

| ---- | ||

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | / X / | |

| ---- | ||

| ---- | ||

| Pre-Effective Amendment No. | / / | |

| ---- | ||

| ---- | ||

| <R> | ||

| Post-Effective Amendment No. 41 | / X / | |

| </R> | ||

| and | ---- | |

| ---- | ||

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY | / X / | |

| ACT OF 1940 | ---- | |

| ---- | ||

| <R> | ||

| Amendment No. 42 | / X / | |

| </R> | ||

| (Check appropriate box or boxes) | ---- | |

| --------------- | ||

| PUTNAM PENNSYLVANIA TAX EXEMPT INCOME FUND | ||

| (Registration No. 33-28321; 811-05802) | ||

| (Exact name of registrant as specified in charter) | ||

| One Post Office Square, Boston, Massachusetts 02109 | ||

| (Address of principal executive offices) | ||

| Registrants' Telephone Number, including Area Code (617) 292-1000 | ||

| --------------- | |

| It is proposed that this filing will become effective | |

| (check appropriate box) | |

| ---- | |

| / / | immediately upon filing pursuant to paragraph (b) |

| ---- | |

| ---- | |

| <R> | |

| / X / | on September 30, 2018 pursuant to paragraph (b) |

| </R> | |

| ---- | |

| ---- | |

| / / | 60 days after filing pursuant to paragraph (a)(1) |

| ---- | |

| ---- | |

| / / | on (date) pursuant to paragraph (a)(1) |

| ---- | |

| ---- | |

| / / | 75 days after filing pursuant to paragraph (a)(2) |

| ---- | |

| ---- | |

| / / | on (date) pursuant to paragraph (a)(2) of Rule 485. |

| ---- | |

| If appropriate, check the following box: | |

| ---- | |

| / / | this post-effective amendment designates a new |

| ---- | effective date for a previously filed post-effective amendment. |

| -------------- | |

| ROBERT T. BURNS, Vice President | |

| PUTNAM MASSACHUSETTS TAX EXEMPT INCOME FUND | |

| PUTNAM MINNESOTA TAX EXEMPT INCOME FUND | |

| PUTNAM NEW JERSEY TAX EXEMPT INCOME FUND | |

| PUTNAM OHIO TAX EXEMPT INCOME FUND | |

| PUTNAM PENNSYLVANIA TAX EXEMPT INCOME FUND | |

| One Post Office Square | |

| Boston, Massachusetts 02109 | |

| (Name and address of agent for service) | |

| --------------- | |

| Copy to: | |

| BRYAN CHEGWIDDEN, Esquire | |

| ROPES & GRAY LLP | |

| 1211 Avenue of the Americas | |

| New York, New York 10036 | |

| ---------------------- | |

<R>

</R>

Fund summaries

Putnam massachusetts Tax Exempt Income Fund

Goal

Putnam Massachusetts Tax Exempt Income Fund seeks as high a level of current income exempt from federal income tax and Massachusetts personal income tax as we believe is consistent with preservation of capital.

Fees and expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in class A shares or $50,000 in class M shares of Putnam funds. More information about these and other discounts is available from your financial advisor and in How do I buy fund shares? beginning on page 31 of the fund’s prospectus, in the Appendix to the fund’s prospectus, and in How to buy shares beginning on page II-1 of the fund’s statement of additional information (SAI).

Shareholder fees (fees paid directly from your investment)

<R>

| Share class | Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, whichever is lower) |

| Class A | 4.00% | 1.00%* |

| Class B | NONE | 5.00%** |

| Class C | NONE | 1.00%*** |

| Class M | 3.25% | NONE |

| Class R6 | NONE | NONE |

| Class Y | NONE | NONE |

</R>

Annual fund operating expenses

(expenses you pay each year as a percentage of the value of your investment)

<R>

| Share class | Management fees | Distribution and service (12b-1) fees | Other expenses | Total annual fund operating expenses |

| Class A | 0.43% | 0.22%† | 0.14% | 0.79% |

| Class B | 0.43% | 0.85% | 0.14% | 1.42% |

| Class C | 0.43% | 1.00% | 0.14% | 1.57% |

| Class M | 0.43% | 0.50% | 0.14% | 1.07% |

| Class R6 | 0.43% | N/A | 0.12%< | 0.55% |

| Class Y | 0.43% | N/A | 0.14% | 0.57% |

</R>

| * | Applies only to certain redemptions of shares bought with no initial sales charge. |

| ** | This charge is phased out over six years. |

| *** | This charge is eliminated after one year. |

2 Prospectus

| † | Represents a blended rate. |

| < | Other expenses are based on expenses of class A shares for the fund’s last fiscal year, restated to reflect the lower investor servicing fees applicable to class R6 shares. |

</R>

Example

The following hypothetical example is intended to help you compare the cost of investing in the fund with the cost of investing in other funds. It assumes that you invest $10,000 in the fund for the time periods indicated and then, except as indicated, redeem all your shares at the end of those periods. It assumes a 5% return on your investment each year and that the fund’s operating expenses remain the same. Your actual costs may be higher or lower.

<R>

| Share class | 1 year | 3 years | 5 years | 10 years |

| Class A | $477 | $642 | $821 | $1,339 |

| Class B | $645 | $749 | $976 | $1,530 |

| Class B (no redemption) | $145 | $449 | $776 | $1,530 |

| Class C | $260 | $496 | $855 | $1,867 |

| Class C (no redemption) | $160 | $496 | $855 | $1,867 |

| Class M | $431 | $654 | $896 | $1,588 |

| Class R6 | $56 | $176 | $307 | $689 |

| Class Y | $58 | $183 | $318 | $714 |

Portfolio turnover

The fund pays transaction-related costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher turnover rate may indicate higher transaction costs and may result in higher taxes when the fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the above example, affect fund performance. The fund’s turnover rate in the most recent fiscal year was 22%.

</R>

Investments, risks, and performance

Investments

<R>

We invest mainly in bonds that pay interest that is exempt from federal income tax and Massachusetts personal income tax (but that may be subject to federal alternative minimum tax (AMT)), are investment-grade in quality, and have intermediate- to long-term maturities (i.e., three years or longer). Under normal circumstances, we invest at least 80% of the fund’s net assets in tax-exempt investments. Such tax-exempt investments in which the fund invests are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and Massachusetts personal income tax. This investment policy cannot be changed without the approval of the fund’s shareholders. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments.

</R>

Prospectus 3

Risks

It is important to understand that you can lose money by investing in the fund.

The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

The risks associated with bond investments include interest rate risk, which means the value of the fund’s investments is likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuers of the fund’s investments may default on payment of interest or principal. Since the fund invests in tax-exempt bonds, which, to be treated as tax-exempt under the Internal Revenue Code, may be issued only by limited types of issuers for limited types of projects, the fund’s investments may be focused in certain market segments. Consequently, the fund may be more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. The fund’s performance will be closely tied to the economic and political conditions in Massachusetts, and can be more volatile than the performance of a more geographically diversified fund. Interest the fund receives might be taxable.

The fund may not achieve its goal, and it is not intended to be a complete investment program. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Performance

The performance information below gives some indication of the risks associated with an investment in the fund by showing the fund’s performance year to year and over time. The bar chart does not reflect the impact of sales charges. If it did, performance would be lower. Please remember that past performance is not necessarily an indication of future results. Monthly performance figures for the fund are available at putnam.com.

4 Prospectus

<R>

Annual total returns for class A shares before sales charges

Average annual total returns after sales charges (for periods ended 12/31/17)

| Share class | 1 year | 5 years | 10 years |

| Class A before taxes | 0.47% | 1.46% | 3.70% |

| Class A after taxes on distributions | 0.44% | 1.43% | 3.65% |

| Class A after taxes on distributions and sale of fund shares | 1.51% | 1.80% | 3.65% |

| Class B before taxes | -0.88% | 1.30% | 3.59% |

| Class C before taxes | 2.94% | 1.50% | 3.32% |

| Class M before taxes | 0.97% | 1.34% | 3.49% |

| Class R6 before taxes* | 4.98% | 2.52% | 4.38% |

| Class Y before taxes | 4.98% | 2.52% | 4.38% |

| Bloomberg Barclays Municipal Bond Index (no deduction for fees, expenses or taxes) | 5.45% | 3.02% | 4.46% |

| * | Performance for class R6 shares prior to its inception (5/22/18) is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher. |

</R>

After-tax returns reflect the historical highest individual federal marginal income tax rates and do not reflect state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are shown for class A shares only and will vary for other classes. These after-tax returns do not apply if you hold your fund shares through a 401(k) plan, an IRA, or another tax-advantaged arrangement.

Class B share performance reflects conversion to class A shares after eight years.

Your fund’s management

Investment advisor

Putnam Investment Management, LLC

<R>

Portfolio managers

Paul Drury

Portfolio Manager, portfolio manager

of the fund since 2002

Garrett

Hamilton

Portfolio Manager, portfolio manager

of the fund since 2016

</R>

Prospectus 5

Sub-advisor

Putnam Investments Limited*

| * | Though the investment advisor has retained the services of Putnam Investments Limited (PIL), PIL does not currently manage any assets of the fund. |

For important information about the purchase and sale of fund shares, tax information, and financial intermediary compensation, please turn to Important additional information about all funds beginning on page 22.

Putnam Minnesota Tax Exempt Income Fund

Goal

Putnam Minnesota Tax Exempt Income Fund seeks as high a level of current income exempt from federal income tax and Minnesota personal income tax as we believe is consistent with preservation of capital.

Fees and expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in class A shares or $50,000 in class M shares of Putnam funds. More information about these and other discounts is available from your financial advisor and in How do I buy fund shares? beginning on page 31 of the fund’s prospectus, in the Appendix to the fund’s prospectus, and in How to buy shares beginning on page II-1 of the fund’s statement of additional information (SAI).

Shareholder fees (fees paid directly from your investment)

<R>

| Share class | Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, whichever is lower) |

| Class A | 4.00% | 1.00%* |

| Class B | NONE | 5.00%** |

| Class C | NONE | 1.00%*** |

| Class M | 3.25% | NONE |

| Class R6 | NONE | NONE |

| Class Y | NONE | NONE |

</R>

6 Prospectus

Annual

fund operating expenses

(expenses you pay each year as a percentage of the value of your investment)

<R>

| Share class | Management fees | Distribution and service (12b-1) fees | Other expenses | Total annual fund operating expenses |

| Class A | 0.43% | 0.23%† | 0.21% | 0.87% |

| Class B | 0.43% | 0.85% | 0.21% | 1.49% |

| Class C | 0.43% | 1.00% | 0.21% | 1.64% |

| Class M | 0.43% | 0.50% | 0.21% | 1.14% |

| Class R6 | 0.43% | N/A | 0.18%< | 0.61% |

| Class Y | 0.43% | N/A | 0.21% | 0.64% |

</R>

| * | Applies only to certain redemptions of shares bought with no initial sales charge. |

| ** | This charge is phased out over six years. |

| *** | This charge is eliminated after one year. |

| † | Represents a blended rate. |

| < | Other expenses are based on expenses of class A shares for the fund’s last fiscal year, restated to reflect the lower investor servicing fees applicable to class R6 shares. |

</R>

Example

The following hypothetical example is intended to help you compare the cost of investing in the fund with the cost of investing in other funds. It assumes that you invest $10,000 in the fund for the time periods indicated and then, except as indicated, redeem all your shares at the end of those periods. It assumes a 5% return on your investment each year and that the fund’s operating expenses remain the same. Your actual costs may be higher or lower.

<R>

| Share class | 1 year | 3 years | 5 years | 10 years |

| Class A | $485 | $666 | $863 | $1,430 |

| Class B | $652 | $771 | $1,013 | $1,612 |

| Class B (no redemption) | $152 | $471 | $813 | $1,612 |

| Class C | $267 | $517 | $892 | $1,944 |

| Class C (no redemption) | $167 | $517 | $892 | $1,944 |

| Class M | $437 | $675 | $932 | $1,666 |

| Class R6 | $62 | $195 | $340 | $762 |

| Class Y | $65 | $205 | $357 | $798 |

Portfolio turnover

The fund pays transaction-related costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher turnover rate may indicate higher transaction costs and may result in higher taxes when the fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the above example, affect fund performance. The fund’s turnover rate in the most recent fiscal year was 17%.

</R>

Prospectus 7

Investments, risks, and performance

Investments

<R>

We invest mainly in bonds that pay interest that is exempt from federal income tax and Minnesota personal income tax (but that may be subject to federal alternative minimum tax (AMT)), are investment-grade in quality, and have intermediate- to long-term maturities (i.e., three years or longer). Under normal circumstances, we invest at least 80% of the fund’s net assets in tax-exempt investments. Such tax-exempt investments in which the fund invests are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and Minnesota personal income tax. This investment policy cannot be changed without the approval of the fund’s shareholders. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments.

Risks

It is important to understand that you can lose money by investing in the fund.

</R>

The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

The risks associated with bond investments include interest rate risk, which means the value of the fund’s investments is likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuers of the fund’s investments may default on payment of interest or principal. Since the fund invests in tax-exempt bonds, which, to be treated as tax-exempt under the Internal Revenue Code, may be issued only by limited types of issuers for limited types of projects, the fund’s investments may be focused in certain market segments. Consequently, the fund may be more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. The fund’s performance will be closely tied to the economic and political conditions in Minnesota, and can be more volatile than the performance of a more geographically diversified fund. Interest the fund receives might be taxable.

The fund may not achieve its goal, and it is not intended to be a complete investment program. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

8 Prospectus

Performance

The performance information below gives some indication of the risks associated with an investment in the fund by showing the fund’s performance year to year and over time. The bar chart does not reflect the impact of sales charges. If it did, performance would be lower. Please remember that past performance is not necessarily an indication of future results. Monthly performance figures for the fund are available at putnam.com.

<R>

Annual total returns for class A shares before sales charges

Average annual total returns after sales charges (for periods ended 12/31/17)

| Share class | 1 year | 5 years | 10 years |

| Class A before taxes | 0.18% | 1.59% | 3.54% |

| Class A after taxes on distributions | 0.09% | 1.54% | 3.51% |

| Class A after taxes on distributions and sale of fund shares | 1.32% | 1.87% | 3.49% |

| Class B before taxes | -1.29% | 1.43% | 3.45% |

| Class C before taxes | 2.56% | 1.62% | 3.18% |

| Class M before taxes | 0.69% | 1.48% | 3.34% |

| Class R6 before taxes* | 4.69% | 2.67% | 4.22% |

| Class Y before taxes | 4.69% | 2.67% | 4.22% |

| Bloomberg Barclays Municipal Bond Index (no deduction for fees, expenses or taxes) | 5.45% | 3.02% | 4.46% |

| * | Performance for class R6 shares prior to its inception (5/22/18) is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher. |

</R>

After-tax returns

reflect the historical highest individual federal marginal income tax rates and do not reflect state and local taxes. Actual after-tax

returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are shown for class A shares

only and will vary for other classes. These after-tax returns do not apply if you hold your fund shares through a 401(k) plan,

an IRA, or another tax-advantaged arrangement.

Class B share performance reflects conversion to class A shares after eight years.

Prospectus 9

Your fund’s management

Investment advisor

Putnam Investment Management, LLC

Portfolio managers

Paul Drury

Portfolio Manager, portfolio manager

of the fund since 2002

Garrett

Hamilton

Portfolio Manager, portfolio manager

of the fund since 2016

Sub-advisor

Putnam Investments Limited*

| * | Though the investment advisor has retained the services of Putnam Investments Limited (PIL), PIL does not currently manage any assets of the fund. |

For important information about the purchase and sale of fund shares, tax information, and financial intermediary compensation, please turn to Important additional information about all funds beginning on page 22.

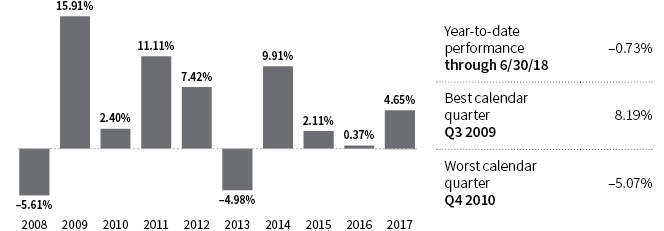

Putnam New Jersey Tax Exempt Income Fund

Goal

Putnam New Jersey Tax Exempt Income Fund seeks as high a level of current income exempt from federal income tax and New Jersey personal income tax as we believe is consistent with preservation of capital.

Fees and expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in class A shares or $50,000 in class M shares of Putnam funds. More information about these and other discounts is available from your financial advisor and in How do I buy fund shares? beginning on page 31 of the fund’s prospectus, in the Appendix to the fund’s prospectus, and in How to buy shares beginning on page II-1 of the fund’s statement of additional information (SAI).

Shareholder fees (fees paid directly from your investment)

<R>

| Share class | Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, whichever is lower) |

| Class A | 4.00% | 1.00%* |

| Class B | NONE | 5.00%** |

| Class C | NONE | 1.00%*** |

| Class M | 3.25% | NONE |

| Class R6 | NONE | NONE |

| Class Y | NONE | NONE |

</R>

10 Prospectus

Annual

fund operating expenses

(expenses you pay each year as a percentage of the value of your investment)

<R>

| Share class | Management fees | Distribution and service (12b-1) fees | Other expenses | Total annual fund operating expenses |

| Class A | 0.43% | 0.23%† | 0.15% | 0.81% |

| Class B | 0.43% | 0.85% | 0.15% | 1.43% |

| Class C | 0.43% | 1.00% | 0.15% | 1.58% |

| Class M | 0.43% | 0.50% | 0.15% | 1.08% |

| Class R6 | 0.43% | N/A | 0.13%< | 0.56% |

| Class Y | 0.43% | N/A | 0.15% | 0.58% |

</R>

| * | Applies only to certain redemptions of shares bought with no initial sales charge. |

| ** | This charge is phased out over six years. |

| *** | This charge is eliminated after one year. |

| † | Represents a blended rate. |

| < | Other expenses are based on expenses of class A shares for the fund’s last fiscal year, restated to reflect the lower investor servicing fees applicable to class R6 shares. |

</R>

Example

The following hypothetical example is intended to help you compare the cost of investing in the fund with the cost of investing in other funds. It assumes that you invest $10,000 in the fund for the time periods indicated and then, except as indicated, redeem all your shares at the end of those periods. It assumes a 5% return on your investment each year and that the fund’s operating expenses remain the same. Your actual costs may be higher or lower.

<R>

| Share class | 1 year | 3 years | 5 years | 10 years |

| Class A | $479 | $648 | $832 | $1,362 |

| Class B | $646 | $752 | $982 | $1,542 |

| Class B (no redemption) | $146 | $452 | $782 | $1,542 |

| Class C | $261 | $499 | $860 | $1,878 |

| Class C (no redemption) | $161 | $499 | $860 | $1,878 |

| Class M | $432 | $657 | $901 | $1,599 |

| Class R6 | $57 | $179 | $313 | $701 |

| Class Y | $59 | $186 | $324 | $726 |

Portfolio turnover

The fund pays transaction-related costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher turnover rate may indicate higher transaction costs and may result in higher taxes when the fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the above example, affect fund performance. The fund’s turnover rate in the most recent fiscal year was 18%.

</R>

Prospectus 11

Investments, risks, and performance

Investments

<R>

We invest mainly in bonds that pay interest that is exempt from federal income tax and New Jersey personal income tax (but that may be subject to federal alternative minimum tax (AMT)), are investment-grade in quality, and have intermediate- to long-term maturities (i.e., three years or longer). Under normal circumstances, we invest at least 80% of the fund’s net assets in tax-exempt investments. Such tax-exempt investments in which the fund invests are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and New Jersey personal income tax. This investment policy cannot be changed without the approval of the fund’s shareholders. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments.

Risks

It is important to understand that you can lose money by investing in the fund.

</R>

The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

The risks associated with bond investments include interest rate risk, which means the value of the fund’s investments is likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuers of the fund’s investments may default on payment of interest or principal. Since the fund invests in tax-exempt bonds, which, to be treated as tax-exempt under the Internal Revenue Code, may be issued only by limited types of issuers for limited types of projects, the fund’s investments may be focused in certain market segments. Consequently, the fund may be more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. The fund’s performance will be closely tied to the economic and political conditions in New Jersey, and can be more volatile than the performance of a more geographically diversified fund. Interest the fund receives might be taxable.

The fund may not achieve its goal, and it is not intended to be a complete investment program. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

12 Prospectus

Performance

The performance information below gives some indication of the risks associated with an investment in the fund by showing the fund’s performance year to year and over time. The bar chart does not reflect the impact of sales charges. If it did, performance would be lower. Please remember that past performance is not necessarily an indication of future results. Monthly performance figures for the fund are available at putnam.com.

<R>

Annual total returns for class A shares before sales charges

Average annual total returns after sales charges (for periods ended 12/31/17)

| Share class | 1 year | 5 years | 10 years |

| Class A before taxes | 1.35% | 1.35% | 3.48% |

| Class A after taxes on distributions | 1.28% | 1.32% | 3.46% |

| Class A after taxes on distributions and sale of fund shares | 2.13% | 1.76% | 3.51% |

| Class B before taxes | -0.08% | 1.21% | 3.37% |

| Class C before taxes | 3.86% | 1.41% | 3.11% |

| Class M before taxes | 1.98% | 1.25% | 3.28% |

| Class R6 before taxes* | 5.80% | 2.43% | 4.15% |

| Class Y before taxes | 5.80% | 2.43% | 4.15% |

| Bloomberg Barclays Municipal Bond Index (no deduction for fees, expenses or taxes) | 5.45% | 3.02% | 4.46% |

| * | Performance for class R6 shares prior to its inception (5/22/18) is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher. |

</R>

After-tax returns reflect the historical highest individual federal marginal income tax rates and do not reflect state and

local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax

returns are shown for class A shares only and will vary for other classes. These after-tax returns do not apply if you hold

your fund shares through a 401(k) plan, an IRA, or another tax-advantaged arrangement.

Class B share performance reflects conversion to class A shares after eight years.

Prospectus 13

Your fund’s management

Investment advisor

Putnam Investment Management, LLC

Portfolio managers

Paul Drury

Portfolio Manager, portfolio manager

of the fund since 2002

Garrett

Hamilton

Portfolio Manager, portfolio manager

of the fund since 2016

Sub-advisor

Putnam Investments Limited*

| * | Though the investment advisor has retained the services of Putnam Investments Limited (PIL), PIL does not currently manage any assets of the fund. |

For important

information about the purchase and sale of fund shares, tax information, and financial intermediary compensation, please turn to

Important additional information about all funds beginning on page 22.

Putnam

Ohio Tax Exempt Income Fund

Goal

Putnam Ohio Tax Exempt Income Fund seeks as high a level of current income exempt from federal income tax and Ohio personal income tax as we believe is consistent with preservation of capital.

Fees and expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in class A shares or $50,000 in class M shares of Putnam funds. More information about these and other discounts is available from your financial advisor and in How do I buy fund shares? beginning on page 31 of the fund’s prospectus, in the Appendix to the fund’s prospectus, and in How to buy shares beginning on page II-1 of the fund’s statement of additional information (SAI).

Shareholder fees (fees paid directly from your investment)

<R>

| Share class | Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, whichever is lower) |

| Class A | 4.00% | 1.00%* |

| Class B | NONE | 5.00%** |

| Class C | NONE | 1.00%*** |

| Class M | 3.25% | NONE |

| Class R6 | NONE | NONE |

| Class Y | NONE | NONE |

</R>

14 Prospectus

Annual

fund operating expenses

(expenses you pay each year as a percentage of the value of your investment)

<R>

| Share class | Management fees | Distribution and service (12b-1) fees | Other expenses | Total annual fund operating expenses |

| Class A | 0.43% | 0.22%† | 0.18% | 0.83% |

| Class B | 0.43% | 0.85% | 0.18% | 1.46% |

| Class C | 0.43% | 1.00% | 0.18% | 1.61% |

| Class M | 0.43% | 0.50% | 0.18% | 1.11% |

| Class R6 | 0.43% | N/A | 0.16%< | 0.59% |

| Class Y | 0.43% | N/A | 0.18% | 0.61% |

</R>

| * | Applies only to certain redemptions of shares bought with no initial sales charge. |

| ** | This charge is phased out over six years. |

| *** | This charge is eliminated after one year. |

| † | Represents a blended rate. |

| < | Other expenses are based on expenses of class A shares for the fund’s last fiscal year, restated to reflect the lower investor servicing fees applicable to class R6 shares. |

</R>

Example

The following hypothetical example is intended to help you compare the cost of investing in the fund with the cost of investing in other funds. It assumes that you invest $10,000 in the fund for the time periods indicated and then, except as indicated, redeem all your shares at the end of those periods. It assumes a 5% return on your investment each year and that the fund’s operating expenses remain the same. Your actual costs may be higher or lower.

<R>

| Share class | 1 year | 3 years | 5 years | 10 years |

| Class A | $481 | $654 | $842 | $1,384 |

| Class B | $649 | $762 | $997 | $1,575 |

| Class B (no redemption) | $149 | $462 | $797 | $1,575 |

| Class C | $264 | $508 | $876 | $1,911 |

| Class C (no redemption) | $164 | $508 | $876 | $1,911 |

| Class M | $434 | $666 | $917 | $1,633 |

| Class R6 | $60 | $189 | $329 | $738 |

| Class Y | $62 | $195 | $340 | $762 |

Portfolio turnover

The fund pays transaction-related costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher turnover rate may indicate higher transaction costs and may result in higher taxes when the fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the above example, affect fund performance. The fund’s turnover rate in the most recent fiscal year was 33%.

</R>

Prospectus 15

Investments, risks, and performance

Investments

<R>

We invest mainly in bonds that pay interest that is exempt from federal income tax and Ohio personal income tax (but that may be subject to federal alternative minimum tax (AMT)), are investment-grade in quality, and have intermediate- to long-term maturities (i.e., three years or longer). Under normal circumstances, we invest at least 80% of the fund’s net assets in tax-exempt investments. Such tax-exempt investments in which the fund invests are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and Ohio personal income tax. This investment policy cannot be changed without the approval of the fund’s shareholders. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments.

Risks

It is important to understand that you can lose money by investing in the fund.

</R>

The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

The risks associated with bond investments include interest rate risk, which means the value of the fund’s investments is likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuers of the fund’s investments may default on payment of interest or principal. Since the fund invests in tax-exempt bonds, which, to be treated as tax-exempt under the Internal Revenue Code, may be issued only by limited types of issuers for limited types of projects, the fund’s investments may be focused in certain market segments. Consequently, the fund may be more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. The fund’s performance will be closely tied to the economic and political conditions in Ohio, and can be more volatile than the performance of a more geographically diversified fund. Interest the fund receives might be taxable.

The fund may not achieve its goal, and it is not intended to be a complete investment program. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

16 Prospectus

Performance

The performance information below gives some indication of the risks associated with an investment in the fund by showing the fund’s performance year to year and over time. The bar chart does not reflect the impact of sales charges. If it did, performance would be lower. Please remember that past performance is not necessarily an indication of future results. Monthly performance figures for the fund are available at putnam.com.

<R>

Annual total returns for class A shares before sales charges

Average annual total returns after sales charges (for periods ended 12/31/17)

| Share class | 1 year | 5 years | 10 years |

| Class A before taxes | 0.14% | 1.38% | 3.21% |

| Class A after taxes on distributions | 0.14% | 1.38% | 3.20% |

| Class A after taxes on distributions and sale of fund shares | 1.26% | 1.76% | 3.27% |

| Class B before taxes | -1.45% | 1.19% | 3.11% |

| Class C before taxes | 2.51% | 1.42% | 2.84% |

| Class M before taxes | 0.65% | 1.26% | 2.99% |

| Class R6 before taxes* | 4.54% | 2.46% | 3.87% |

| Class Y before taxes | 4.54% | 2.46% | 3.87% |

| Bloomberg Barclays Municipal Bond Index (no deduction for fees, expenses or taxes) | 5.45% | 3.02% | 4.46% |

| * | Performance for class R6 shares prior to its inception (5/22/18) is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher. |

</R>

After-tax returns reflect the historical highest individual federal marginal income tax rates and do not reflect state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are shown for class A shares only and will vary for other classes. These after-tax returns do not apply if you hold your fund shares through a 401(k) plan, an IRA, or another tax-advantaged arrangement.

Class B share performance reflects conversion to class A shares after eight years.

Prospectus 17

Your fund’s management

Investment advisor

Putnam Investment Management, LLC

Portfolio managers

Paul Drury

Portfolio Manager, portfolio manager

of the fund since 2002

Garrett

Hamilton

Portfolio Manager, portfolio manager

of the fund since 2016

Sub-advisor

Putnam Investments Limited*

| * | Though the investment advisor has retained the services of Putnam Investments Limited (PIL), PIL does not currently manage any assets of the fund. |

For important

information about the purchase and sale of fund shares, tax information, and financial intermediary compensation, please turn to

Important additional information about all funds beginning on page 22.

Putnam

Pennsylvania Tax Exempt Income Fund

Goal

Putnam Pennsylvania Tax Exempt Income Fund seeks as high a level of current income exempt from federal income tax and Pennsylvania personal income tax as we believe is consistent with preservation of capital.

Fees and expenses

The following table describes the fees and expenses you may pay if you buy and hold shares of the fund. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in class A shares or $50,000 in class M shares of Putnam funds. More information about these and other discounts is available from your financial advisor and in How do I buy fund shares? beginning on page 31 of the fund’s prospectus, in the Appendix to the fund’s prospectus, and in How to buy shares beginning on page II-1 of the fund’s statement of additional information (SAI).

Shareholder fees (fees paid directly from your investment)

<R>

| Share class | Maximum sales charge (load) imposed on purchases (as a percentage of offering price) | Maximum deferred sales charge (load) (as a percentage of original purchase price or redemption proceeds, whichever is lower) |

| Class A | 4.00% | 1.00%* |

| Class B | NONE | 5.00%** |

| Class C | NONE | 1.00%*** |

| Class M | 3.25% | NONE |

| Class R6 | NONE | NONE |

| Class Y | NONE | NONE |

</R>

18 Prospectus

Annual

fund operating expenses

(expenses you pay each year as a percentage of the value of your investment)

<R>

| Share class | Management fees | Distribution and service (12b-1) fees | Other expenses | Total annual fund operating expenses |

| Class A | 0.43% | 0.23%† | 0.16% | 0.82% |

| Class B | 0.43% | 0.85% | 0.16% | 1.44% |

| Class C | 0.43% | 1.00% | 0.16% | 1.59% |

| Class M | 0.43% | 0.50% | 0.16% | 1.09% |

| Class R6 | 0.43% | N/A | 0.14%< | 0.57% |

| Class Y | 0.43% | N/A | 0.16% | 0.59% |

</R>

| * | Applies only to certain redemptions of shares bought with no initial sales charge. |

| ** | This charge is phased out over six years. |

| *** | This charge is eliminated after one year. |

| † | Represents a blended rate. |

| < | Other expenses are based on expenses of class A shares for the fund’s last fiscal year, restated to reflect the lower investor servicing fees applicable to class R6 shares. |

</R>

Example

The following hypothetical example is intended to help you compare the cost of investing in the fund with the cost of investing in other funds. It assumes that you invest $10,000 in the fund for the time periods indicated and then, except as indicated, redeem all your shares at the end of those periods. It assumes a 5% return on your investment each year and that the fund’s operating expenses remain the same. Your actual costs may be higher or lower.

<R>

| Share class | 1 year | 3 years | 5 years | 10 years |

| Class A | $480 | $651 | $837 | $1,373 |

| Class B | $647 | $756 | $987 | $1,556 |

| Class B (no redemption) | $147 | $456 | $787 | $1,556 |

| Class C | $262 | $502 | $866 | $1,889 |

| Class C (no redemption) | $162 | $502 | $866 | $1,889 |

| Class M | $433 | $660 | $906 | $1,611 |

| Class R6 | $58 | $183 | $318 | $714 |

| Class Y | $60 | $189 | $329 | $738 |

Portfolio turnover

The fund pays transaction-related costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher turnover rate may indicate higher transaction costs and may result in higher taxes when the fund’s shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or the above example, affect fund performance. The fund’s turnover rate in the most recent fiscal year was 24%.

</R>

Prospectus 19

Investments, risks, and performance

Investments

<R>

We invest mainly in bonds that pay interest that is exempt from federal income tax and Pennsylvania personal income tax (but that may be subject to federal alternative minimum tax (AMT)), are investment-grade in quality, and have intermediate- to long-term maturities (i.e., three years or longer). Under normal circumstances, we invest at least 80% of the fund’s net assets in tax-exempt investments. Such tax-exempt investments in which the fund invests are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and Pennsylvania personal income tax. This investment policy cannot be changed without the approval of the fund’s shareholders. We may consider, among other factors, credit, interest rate and prepayment risks, as well as general market conditions, when deciding whether to buy or sell investments.

Risks

It is important to understand that you can lose money by investing in the fund.

</R>

The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings.

The risks associated with bond investments include interest rate risk, which means the value of the fund’s investments is likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuers of the fund’s investments may default on payment of interest or principal. Since the fund invests in tax-exempt bonds, which, to be treated as tax-exempt under the Internal Revenue Code, may be issued only by limited types of issuers for limited types of projects, the fund’s investments may be focused in certain market segments. Consequently, the fund may be more vulnerable to fluctuations in the values of the securities it holds than a fund that invests more broadly. Interest rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds. The fund’s performance will be closely tied to the economic and political conditions in Pennsylvania, and can be more volatile than the performance of a more geographically diversified fund. Interest the fund receives might be taxable.

The fund may not achieve its goal, and it is not intended to be a complete investment program. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

20 Prospectus

Performance

The performance information below gives some indication of the risks associated with an investment in the fund by showing the fund’s performance year to year and over time. The bar chart does not reflect the impact of sales charges. If it did, performance would be lower. Please remember that past performance is not necessarily an indication of future results. Monthly performance figures for the fund are available at putnam.com.

<R>

Annual total returns for class A shares before sales charges

Average annual total returns after sales charges (for periods ended 12/31/17)

| Share class | 1 year | 5 years | 10 years |

| Class A before taxes | 0.57% | 1.58% | 3.40% |

| Class A after taxes on distributions | 0.54% | 1.57% | 3.39% |

| Class A after taxes on distributions and sale of fund shares | 1.56% | 1.93% | 3.43% |

| Class B before taxes | -0.87% | 1.40% | 3.28% |

| Class C before taxes | 2.96% | 1.60% | 3.02% |

| Class M before taxes | 1.08% | 1.46% | 3.19% |

| Class R6 before taxes* | 5.00% | 2.64% | 4.07% |

| Class Y before taxes | 5.00% | 2.64% | 4.07% |

| Bloomberg Barclays Municipal Bond Index (no deduction for fees, expenses or taxes) | 5.45% | 3.02% | 4.46% |

| * | Performance for class R6 shares prior to its inception (5/22/18) is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher. |

</R>

After-tax returns reflect the historical highest individual federal marginal income tax rates and do not reflect state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are shown for class A shares only and will vary for other classes. These after-tax returns do not apply if you hold your fund shares through a 401(k) plan, an IRA, or another tax-advantaged arrangement.

Class B share performance reflects conversion to class A shares after eight years.

Prospectus 21

Your fund’s management

Investment advisor

Putnam Investment Management, LLC

Portfolio managers

Paul Drury

Portfolio Manager, portfolio manager

of the fund since 2002

Garrett

Hamilton

Portfolio Manager, portfolio manager

of the fund since 2016

Sub-advisor

Putnam Investments Limited*

| * | Though the investment advisor has retained the services of Putnam Investments Limited (PIL), PIL does not currently manage any assets of the fund. |

Important Additional Information About All Funds

Purchase and sale of fund shares

You can open an account, purchase and/or sell fund shares, or exchange them for shares of another Putnam fund by contacting your financial advisor or by calling Putnam Investor Services at 1-800-225-1581. Purchases of class B shares are closed to new and existing investors except by exchange from class B shares of another Putnam fund or through dividend and/or capital gains reinvestment.

When opening an account, you must complete and mail a Putnam account application, along with a check made payable to the fund, to: Putnam Investor Services, P.O. Box 8383, Boston, MA 02266-8383. The minimum initial investment of $500 is currently waived, although Putnam reserves the right to reject initial investments under $500 at its discretion. There is no minimum for subsequent investments.

You can sell your shares back to the fund or exchange them for shares of another Putnam fund any day the New York Stock Exchange (NYSE) is open. Shares may be sold or exchanged by mail, by phone, or online at putnam.com. Some restrictions may apply.

Tax information

The fund intends to distribute income that is exempt from federal income tax and personal income tax of the state identified in the fund’s name, but distributions will be subject to federal income tax to the extent attributable to other income, including income earned by the fund on investments in taxable securities or capital gains realized on the disposition of its investments.

22 Prospectus

Financial intermediary compensation

If you purchase the fund through a broker/dealer or other financial intermediary (such as a bank or financial advisor), the fund and its related companies may pay that intermediary for the sale of fund shares and related services. Please bear in mind that these payments may create a conflict of interest by influencing the broker/dealer or other intermediary to recommend the fund over another investment. Ask your advisor or visit your advisor’s website for more information.

What are each fund’s main investment strategies and related risks?

This section contains greater detail on each fund’s main investment strategies and the related risks you would face as a fund shareholder. It is important to keep in mind that risk and reward generally go hand in hand; the higher the potential reward, the greater the risk.

<R>

As mentioned in the fund summaries, we pursue each fund’s goal by investing mainly in tax-exempt investments. Under normal circumstances, we invest at least 80% of a fund’s net assets in tax-exempt investments that are investment-grade quality. This investment policy cannot be changed without the approval of a fund’s shareholders. Certain states may impose additional requirements on the composition of a fund’s portfolio in order for distributions from that fund to be exempt from state taxes.

</R>

- Tax-exempt investments. These investments are issued by or for states, territories or possessions of the United States or by their political subdivisions, agencies, authorities or other government entities, and the income from these investments is exempt from both federal and the applicable state’s income tax. These investments are issued to raise money for public purposes, such as loans for the construction of housing, schools or hospitals, or to provide temporary financing in anticipation of the receipt of taxes and other revenue. They also include private activity obligations of public authorities to finance privately owned or operated facilities. Changes in law or adverse determinations by the Internal Revenue Service or a state tax authority could make the income from some of these obligations taxable. Investments in securities of issuers located outside the applicable state may be applied toward meeting a requirement to invest in a tax-exempt investment if the security pays interest that is exempt from federal and the applicable state’s income tax.

Interest income from private activity bonds may be subject to federal AMT for individuals. As a policy that cannot be changed without the approval of fund shareholders, we cannot include these investments for the purpose of complying with the 80% investment policies described above. Corporate shareholders will be required to include all exempt interest dividends in determining their federal AMT. For more information, including possible state, local and other taxes, contact your tax advisor.

Prospectus 23

- General obligations. These are backed by the issuer’s authority to levy taxes and are considered an obligation of the issuer. They are payable from the issuer’s general unrestricted revenues, although payment may depend upon government appropriation or aid from other governments. These investments may be vulnerable to legal limits on a government’s power to raise revenue or increase taxes, as well as economic or other developments that can reduce revenues.

<R>

- Revenue obligations. These are payable from revenue earned by a particular project or other revenue source. They include private activity bonds such as industrial development bonds, which are paid only from the revenues of the private owners or operators of the facilities. Investors can look only to the revenue generated by the project or the private company operating the project rather than the credit of the state or local government authority issuing the bonds. Revenue obligations are typically subject to greater credit risk than general obligations because of the relatively limited source of revenue.

</R>

- Interest rate risk. The values of bonds and other debt instruments usually rise and fall in response to changes in interest rates. Declining interest rates generally increase the value of existing debt instruments, and rising interest rates generally decrease the value of existing debt instruments. Changes in a debt instrument’s value usually will not affect the amount of interest income paid to a fund, but will affect the value of a fund’s shares. Interest rate risk is generally greater for investments with longer maturities.

Some investments give the issuer the option to call or redeem an investment before its maturity date. If an issuer calls or redeems an investment during a time of declining interest rates, we might have to reinvest the proceeds in an investment offering a lower yield, and, therefore, a fund might not benefit from any increase in value as a result of declining interest rates.

- Credit risk. Investors normally expect to be compensated in proportion to the risk they are assuming. Thus, debt of issuers with poor credit prospects usually offers higher yields than debt of issuers with more secure credit. Higher-rated investments generally have lower credit risk.

We invest mostly in investment-grade debt investments. These are rated at least BBB or its equivalent at the time of purchase by a nationally recognized securities rating agency, or are unrated investments that we believe are of comparable quality. We may invest up to 25% of the fund’s total assets in non-investment-grade investments. However, we will not invest in investments that are rated lower than BB or its equivalent by each agency rating the investment, or are unrated securities that we believe are of comparable quality. We will not necessarily sell an investment if its rating is reduced after we buy it.

Investments rated below BBB or its equivalent are below-investment-grade (sometimes referred to as “junk bonds”). This rating reflects a greater possibility that the issuers may be unable to make timely payments of interest and principal and thus default. If default occurs, or is perceived as likely to occur, the values of those investments will usually be more volatile and are likely to fall. A default

24 Prospectus

or expected default could also make it difficult for us to sell the investments at prices approximating the values we had previously placed on them. Tax-exempt debt, particularly lower-rated tax-exempt debt, usually has a more limited market than taxable debt, which may at times make it difficult for us to buy or sell certain debt instruments or to establish their fair value. Credit risk is generally greater for investments that are required to make interest payments only at maturity rather than at intervals during the life of the investment.

We may buy investments that are insured as to the payment of principal and interest in the event the issuer defaults. Any reduction in the insurer’s ability to pay claims may adversely affect the value of insured investments and, consequently, the value of a fund’s shares.

- Focus of investments. We may make significant investments in a particular segment of the tax-exempt debt market, such as tobacco settlement bonds or revenue bonds for health care facilities, housing or airports. These investments may cause the value of a fund’s shares to fluctuate more than the values of shares of funds that invest in a greater variety of investments. Certain events may adversely affect all investments within a particular market segment. Examples include legislation or court decisions, concerns about pending legislation or court decisions, and lower demand for the services or products provided by a particular market segment.

Investing mostly in tax-exempt investments of a single state makes a fund more vulnerable to that state’s economy and to factors affecting tax-exempt issuers in that state than would be true for a more geographically diversified fund. These risks include:

- the inability or perceived inability of a government authority to collect sufficient tax or other revenues to meet its payment obligations, which could result in a downgrade of a state’s credit rating or the ratings of authorities or political sub-divisions of the state,

- the introduction of constitutional or statutory limits on a tax-exempt issuer’s ability to raise revenues or increase taxes,

- economic or demographic factors that may cause a decrease in tax or other revenues for a government authority or for private operators of publicly financed facilities, and

- increased expenditures on domestic security or reduced monetary support from the federal government.

These risks are also present in the securities issued by any other state that the fund might invest in.

The Massachusetts Fund: The fund’s investments in Massachusetts municipal securities may be vulnerable to events adversely affecting the Massachusetts economy. These events include tax, legislative, or political changes as well as a deterioration in the state or local budgets. Although Massachusetts’s economy is relatively diverse, industries significant to the state’s economy, such as the education, technology, biotech, financial services or healthcare, could experience downturns or fail to develop as expected, hurting the local economy, and negatively impacting the fund’s performance. Massachusetts generally has a high degree of job stability and

Prospectus 25

an educated work force due to its large concentration of colleges and universities, but the high cost of doing business in Massachusetts may serve as an impediment to job creation. Additionally, fluctuations in unemployment levels or in the state or national economy could result in decreased tax revenues, which could also impact the fund’s performance.

The Minnesota Fund: The fund’s investments in Minnesota securities may be vulnerable to events adversely affecting the Minnesota economy. While the Minnesota economy is relatively diverse, including the agriculture, forestry, mining, manufacturing, retail, financial services, healthcare, and biomedical industries, a downturn in any of these could hurt Minnesota economic conditions. Minnesota businesses generally face a high cost of doing business, which also may negatively affect economic conditions in the state. While Minnesota is currently experiencing budget surpluses, fluctuation in unemployment levels or in the state or national economy could result in decreased tax revenues.

The New Jersey Fund: The fund’s investment in New Jersey municipal securities may be vulnerable to events adversely affecting the New Jersey economy. New Jersey’s diverse economic base, consisting of a variety of manufacturing, construction and service industries, and supplemented by commercial agriculture in rural areas, could experience downturns or fail to develop as expected, hurting the local economy. The labor market in New Jersey continues to expand (although growth has slowed) and the state’s housing market continues to improve, however, New Jersey continues to have a high number of homes in foreclosure. Fluctuations in labor market growth, unemployment levels or in the state or national economy could result in decreased tax revenues.

<R>

The Ohio Fund: The fund’s investments in Ohio municipal securities may be vulnerable to events adversely affecting Ohio and its economy as a whole, or industry segments in that economy or geographic areas within the State. Economic activity in Ohio, as in other industrially-developed states, tends to be somewhat more cyclical than in some other states and in the nation as a whole. Ohio ranks third among the states in the manufacturing sector and fourth in the durable goods sector with manufacturing responsible for 16.6% and the production of goods responsible for 23.0% of Ohio’s preliminary 2017 gross state product (GSP). The greatest growth in Ohio’s economy in recent years has been in the non-manufacturing sections, with the business services sectors, including finance, insurance and real estate, accounting for another 34.2% of that preliminary 2017 GSP. Ohio is the ninth largest exporting state with 2017 merchandise exports totaling $50.1 billion, with machinery (including electrical machinery), motor vehicles, aircraft/spacecraft and plastics, accounting for 55.6% of that total. And, with 14.0 million acres (of a total land area of 26.4 million acres) in farmland and an estimated 74,500 individual farms, agriculture combined with related agricultural sectors remains an important segment of the State’s economy. Ohio’s 2010 decennial census population of 11,536,504 ranked it seventh among the states.

26 Prospectus

The Pennsylvania Fund: The fund’s investment in Pennsylvania municipal securities may be vulnerable to events adversely affecting the Pennsylvania economy. Pennsylvania is one of the most populous states, ranking sixth behind California, Texas, Florida, New York and Illinois. Pennsylvania is an established state with a diversified economy. Pennsylvania had been historically identified as a heavy industrial state. That reputation has changed over the last thirty years as the coal, steel and railroad industries declined. Pennsylvania’s business environment readjusted with a more diversified economic base. This economic readjustment was a direct result of a long-term shift in jobs, investment, and workers away from the northeast part of the nation. Currently, the major sources of growth in Pennsylvania are in the service sector, including trade, medical, health services, education and financial institutions. As in other industrially developed states, economic activity in Pennsylvania may be more cyclical than in some other states or in the nation as a whole. Other factors that may negatively affect economic conditions in Pennsylvania include adverse changes in employment rates, Federal revenue sharing laws or laws with respect to tax exempt financing. Pennsylvania continues to experience structural imbalances and projected budget deficits.

</R>

In addition, because of the relatively small number of issuers of tax-exempt securities, we are more likely to invest a higher percentage of assets in a single issuer. We may, therefore, be more exposed to the risk of loss due to investing in relatively fewer issuers than a fund that invests more broadly.

At times, the funds and other accounts that Putnam Management and its affiliates manage may own all or most of the debt of a particular issuer. This concentration of ownership may make it more difficult to sell, or to determine the fair value of, these investments.

- Derivatives. We may engage in a variety of transactions involving derivatives, such as futures, options, swap contracts and inverse floaters, although they do not represent a primary focus of the funds. Derivatives are financial instruments whose value depends upon, or is derived from, the value of something else, such as one or more underlying investments, pools of investments or indexes. We may make use of “short” derivatives positions, the values of which typically move in the opposite direction from the price of the underlying investment, pool of investments, or index. We may use derivatives both for hedging and non-hedging purposes, such as to modify the behavior of an investment so that it responds differently than it would otherwise respond to changes in a particular interest rate. For example, derivatives may increase or decrease an investment’s exposure to long- or short-term interest rates or cause the value of an investment to move in the opposite direction from prevailing short-term or long-term interest rates. We may also use derivatives as a substitute for a direct investment in the securities of one or more issuers. However, we may also choose not to use derivatives, based on our evaluation of market conditions or the availability of suitable derivatives. Investments in derivatives may be applied toward meeting a requirement to invest in a particular kind of investment if the derivatives have economic characteristics similar to that investment.

Prospectus 27

<R>

Derivatives involve special risks and may result in losses. The successful use of derivatives depends on our ability to manage these sophisticated instruments. Some derivatives are “leveraged,” which means they provide a fund with investment exposure greater than the value of a fund’s investment in the derivatives. As a result, these derivatives may magnify or otherwise increase investment losses to a fund. The risk of loss from certain short derivatives positions is theoretically unlimited. The value of derivatives may move in unexpected ways due to the use of leverage or other factors, especially in unusual market conditions, and may result in increased volatility.

</R>

Other risks arise from the potential inability to terminate or sell derivatives positions. A liquid secondary market may not always exist for the fund’s derivatives positions. In fact, many over-the-counter instruments (investments not traded on an exchange) will not be liquid. Over-the-counter instruments also involve the risk that the other party to the derivatives transaction will not meet its obligations. For further information about additional types and risks of derivatives and the funds’ asset segregation policies, see Miscellaneous Investments, Investment Practices and Risks in the SAI.

- Market risk. The value of bonds in a fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions (including perceptions about the risk of default and expectations about monetary policy or interest rates), changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings. During those periods, a fund may experience high levels of shareholder redemptions, and may have to sell securities at times when it would otherwise not do so, and at unfavorable prices.

- Other investments. In addition to the main investment strategies described above, a fund may also make other types of investments, which may produce taxable income and be subject to other risks, as described under Miscellaneous Investments, Investment Practices and Risks in the SAI.

- Temporary defensive strategies. In response to adverse market, economic, political or other conditions, we may take temporary defensive positions, such as investing some or all of a fund’s assets in cash and cash equivalents, that differ from the fund’s usual investment strategies. However, we may choose not to use these temporary defensive strategies for a variety of reasons, even in very volatile market conditions. These strategies may cause a fund to miss out on investment opportunities, and may prevent a fund from achieving its goal. Additionally, while temporary defensive strategies are mainly designed to limit losses, such strategies may not work as intended.

- Changes in policies. The Trustees may change a fund’s goal, investment strategies and other policies set forth in this prospectus without shareholder approval, except as otherwise provided.

28 Prospectus

<R>

- Portfolio turnover rate. A fund’s portfolio turnover rate measures how frequently a fund buys and sells investments. A portfolio turnover rate of 100%, for example, would mean that the fund sold and replaced securities valued at 100% of the fund’s assets within a one-year period. From time to time, a fund may engage in frequent trading. Funds with high turnover may be more likely to realize capital gains that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance. A fund’s portfolio turnover rate and the amount of brokerage commissions it pays will vary over time based on market conditions.

</R>

- Portfolio holdings. The SAI includes a description of each fund’s policies with respect to the disclosure of its portfolio holdings. For more specific information on a fund’s portfolio, you may visit the Putnam Investments website, putnam.com/individual, where each fund’s top 10 holdings and related portfolio information may be viewed monthly beginning approximately 15 days after the end of each month, and full portfolio holdings may be viewed beginning on the last business day of the month after the end of each calendar quarter. This information will remain available on the website until a fund files a Form N-CSR or N-Q with the SEC for the period that includes the date of the information, after which such information can be found on the SEC’s website at http://www.sec.gov.

Who oversees and manages the funds?

The funds’ Trustees

As a shareholder of a mutual fund, you have certain rights and protections, including representation by a Board of Trustees. The Putnam Funds’ Board of Trustees oversees the general conduct of the funds’ business and represents the interests of the Putnam fund shareholders. At least 75% of the members of the Putnam Funds’ Board of Trustees are independent, which means they are not officers of the funds or affiliated with Putnam Investment Management, LLC (Putnam Management).

The Trustees periodically review each fund’s investment performance and the quality of other services such as administration, custody, and investor services. At least annually, the Trustees review the fees paid to Putnam Management and its affiliates for providing or overseeing these services, as well as the overall level of each fund’s operating expenses. In carrying out their responsibilities, the Trustees are assisted by an administrative staff, auditors and legal counsel that are selected by the Trustees and are independent of Putnam Management and its affiliates.

Contacting

the funds’ Trustees

Address correspondence to:

The Putnam Funds Trustees

One Post Office Square

Boston, MA 02109

Prospectus 29

The funds’ investment manager

The Trustees have retained Putnam Management, which has managed mutual funds since 1937, to be each fund’s investment manager, responsible for making investment decisions for each fund and managing each fund’s other affairs and business.

<R>

The basis for the Trustees’ approval of each fund’s management contract and the sub-management contract described below is discussed in each fund’s semiannual report to shareholders dated November 30, 2017.

</R>

Each fund pays a monthly management fee to Putnam Management. The fee is calculated by applying a rate to each fund’s average net assets for the month. The rate is based on the monthly average of the aggregate net assets of all open-end funds sponsored by Putnam Management (excluding net assets of funds that are invested in, or that are invested in by, other Putnam funds to the extent necessary to avoid “double counting” of those assets), and generally declines as the aggregate net assets increase.

The funds paid Putnam Management a management fee (after any applicable waivers) for each fund’s last fiscal year at the following rates (reflected as a percentage of average net assets for each fund’s last fiscal year).

| Fund | Management Fees (after applicable waivers) | |

| <R> | ||

| The Massachusetts Fund | 0.43% | |

| The Minnesota Fund | 0.43% | |

| The New Jersey Fund | 0.43% | |

| The Ohio Fund | 0.43% | |

| The Pennsylvania Fund | 0.43% |

</R>

Putnam Management’s

address is One Post Office Square, Boston, MA 02109.

<R>