UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-4626

Tax-Free Trust or Oregon

(Exact name of Registrant as specified in charter)

380 Madison Avenue

New York, New York 10017

(Address of principal executive offices) (Zip code)

Joseph P. DiMaggio

380 Madison Avenue

New York, New York 10017

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 697-6666

Date of fiscal year end: 9/30

Date of reporting period: 9/30/12

FORM N-CSR

|

ITEM 1.

|

REPORTS TO STOCKHOLDERS

|

|

|

|

Annual

Report

|

|

September 30, 2012

|

|

TAX-FREE TRUST OF OREGON

A tax-free income investment

|

|

|

Serving Oregon Investors For Over 25 Years

Tax-Free Trust of Oregon

“Research Matters”

|

|

November, 2012

Dear Fellow Shareholder:

While we didn’t necessarily coin the phrases, “Invest in what you know” or “If you don’t understand it, don’t buy it,” these concepts are certainly not new to Tax-Free Trust of Oregon and the Aquila Group of Funds. In fact, they have been at the very core of our investment philosophy since day one.

Our country’s currently volatile economic environment makes these adages ring true louder than ever.

The value provided by a professional investment management team, such as that of Tax-Free Trust of Oregon, which conducts initial research and provides on-going surveillance of issuers and individual bonds as markets develop and credit conditions change, has become increasingly important.

Over the past year or so, you may have read or heard about problems being experienced by certain municipalities – including growing concerns over budget shortfalls, infrastructure demands, pension funding, and high unemployment.

Even when concerns such as these don’t make the mainstream newspapers, it is in your best interest that your Trust’s investment team makes every effort to know about each and every little hiccup. And, since each municipality has its own distinct nuances, we feel it is vital to have a local presence.

Local investment management and research enables us to monitor the local economy, issuers in the state, and policy decisions that will impact issuers, while we conduct research on issues held by the Trust. The research conducted prior to investing in a bond, and ongoing credit monitoring, make it possible to evaluate both the risk associated with an individual bond, and the adequacy of the compensation provided for that risk.

Tax-Free Trust of Oregon specifically benefits from its collective team of local Trustees, portfolio management staff and Trust Officers who seek to be intimately aware of any potential challenges facing the citizens of Oregon throughout the state.

They know the ups and downs that affect you, our shareholders, because they too are affected. Your local representatives are also your friends, neighbors and co-workers.

They hear the same discussions at little league games and pot luck dinners. They read the same small and big town newspapers that you do, shop in the same supermarkets and gas up at the same pumps.

They, like you, are Oregonians.

NOT A PART OF THE ANNUAL REPORT

As you know, by prospectus, Tax-Free Trust of Oregon may only invest in investment grade securities. These higher rated securities are intended to indicate those municipal issues which have not only sufficient, but significant, cash flow strength in order to pay interest when due and to redeem the bonds at maturity. Nonetheless, we firmly believe in the importance of looking beyond credit ratings.

We invest in an issue based on our initial research, and we conduct frequent credit monitoring in order to evaluate the financial condition of the issuer. We devote significant resources to understanding the financial condition of issuers in Oregon, the financing details of individual issues, and how payments of principal and interest on those issues are secured. We monitor the difficult, but necessary, steps being taken to balance budgets within the state. Based on the research we conduct, we select the bonds held in the Trust’s portfolio and decide whether or not to continue holding issues already in the portfolio.

The Aquila Group of Funds has been managing the assets of Oregon investors for over 25 years. Our long history in the Oregon market, the knowledge and experience of the Trust’s portfolio management team, and the research conducted on bonds held in Tax-Free Trust of Oregon continue to provide shareholders with the benefits of local, professional investment management.

Sincerely,

|

|

|

|

Diana P. Herrmann, Vice Chair and President

|

Consideration should be given to the risks of investing, including potential loss of value, market risk, interest rate risk, credit risk, and geographic concentration. Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For certain investors, some dividends may be subject to Federal and state taxes.

NOT A PART OF THE ANNUAL REPORT

|

|

Serving Oregon Investors For Over 25 Years

Tax-Free Trust of Oregon

ANNUAL REPORT

Management Discussion

|

|

2011-12 Review

The tone of the municipal bond market has improved over the past year as we have transitioned from a skeptical market with some investors selling bonds at any price to a market with improved demand due to a greater understanding of the inherent value and risk characteristics of municipal bonds. Nevertheless, headline risk continues to influence bond prices. Although, the theme has changed from Chicken Little, with a much-quoted analyst’s dire warnings of a falling sky through widespread bond defaults which was unrealized, to Goldilocks, or perhaps more fittingly “Gridlocks,” as sequestration, the fiscal cliff, an election year and a challenging interest rate environment are all obstacles preventing the bond market from finding comfort.

The much reported and dramatically named fiscal cliff is a culmination of the expiration of the Bush tax cuts, temporary payroll tax cut and extended unemployment benefits all expiring while higher Medicare taxes and cuts to discretionary spending, agreed to in the Budget Control Act of 2011 (the “BCA”), take effect. While we are optimistic of legislation to reduce the impact of the fiscal cliff, we remain cautious with respect to bonds that have a high degree of dependence on appropriations from the Federal government. In our last commentary we expressed similar sentiment regarding the Federal spending following the Treasury Department’s report that the debt limit of $14.29 trillion had been reached in May 2011.

The fiscal cliff also found its way into election year politics as market participants debated potential outcomes of Republican and Democratic platforms. Other election year issues impacting the market included potential tax reform and state and local credit issues. Speculation leading up to the election proved substantially more disruptive than the result. Ultimately, election results were largely priced into the market by Election Day, resulting in a muted response. The Democratic presidency proved to be a positive event for the bond market as it served to affirm the status quo and provided a degree of assurance that current policies would be carried forward. However, status quo also raises concerns of gridlock at the Federal level as we are again faced with Democratic control of the White House and Senate and Republican control of the House of Representatives. Gridlock is a concern from a credit perspective as the fiscal cliff approaches and decisive action is necessary to avoid disruption at the Federal level. Should a resolution not materialize, a downgrade of U.S. Treasury securities from Moody’s remains a possibility.

The aforementioned BCA requires the Director of the United States Office of Management and Budget to make certain spending cuts referred to as the “sequester.” The BCA cuts can be avoided if Congress enacts other cuts of an equal or larger amount or takes other action to postpone or change the provisions of the BCA prior to January 2, 2013. The municipal bond market is most concerned about the impact these cuts pose to Build America Bonds, none of which are held by the Tax-Free Trust of Oregon. The focus of the portfolio continues to be on high-grade credits supported by property taxes and essential service revenues. However, these concerns reinforce the value of deep credit research and a disciplined approach to portfolio management.

1 | Tax-Free Trust of Oregon

MANAGEMENT DISCUSSION (continued)

In its third attempt to stimulate the U.S. Economy, the Federal Reserve (the “Fed”) implemented its third round of quantitative easing in September, often referred to as QE3. The Fed’s primary objective is to lower mortgage rates and therefore increase spending and hiring as a result of increased activity in the housing market. QE3 is intended to lower mortgage interest rates through purchases of mortgage-backed securities by the Fed in monthly intervals of $40 billion. However, along with low mortgage rates, QE3 has lowered short-term rates in general as the Fed has indicated it plans to maintain short-term interest rates at “exceptionally low levels” until mid-2015. The result of this policy has kept Treasury rates close to historic lows with 2-year securities yielding 0.23% and 10-year bonds at 1.63%. Yields of highly rated municipal bonds have also remained very low with 2-year AAA maturities at 0.30% and 10-year yields at 1.70% as of September 30, 2012. The unusual relationship of tax-exempt yields remaining equal to or higher than taxable interest rates on Treasury and agency securities has persisted due to the Fed’s intervention and uncertainty of the impact from potential changes to the tax code. This environment has forced investors seeking higher yields to add more risk to their portfolios by investing further out on the yield curve or increasing exposure to low rated or nonrated sectors. Our focus will remain on maintaining high credit quality through proprietary research and local expertise. Through our internal credit process we will continue to review lower rated investment grade bonds to find credits with lower risk and a greater probability of outperforming the market.

Through the Fed’s effort to stimulate the economy and a renewed interest in the value presented by municipal bonds, interest rates have been pushed to challengingly low levels over the past year. As Sub-Adviser to Tax-Free Trust of Oregon we have continued our disciplined approach to portfolio management by seeking to (1) reduce interest rate risk with shorter portfolio duration and (2) manage credit risk through rigorous security analysis and surveillance.

Oregon’s economy continues to recover at a gradual pace. The housing market, particularly in the Portland metropolitan area, shows signs of improvement as the backlog of inventory diminishes and approaches levels last seen at the peak of the housing bubble. According to the Regional Multiple Listing Service (“RMLS”), median sales price increased 11.7% for October versus last year. Increases in housing prices have been largely attributed to diminishing inventories and the declining influence of foreclosures. According to Zillow, foreclosures comprise 11% of homes for sale in September versus 22%, or approximately double, last year.

Although employment gains have slowed over the past two quarters, employment in Oregon continues to increase at levels approximately in line with gains seen at the national level. According to the State economist’s December 2012 economic forecast, after adjustments, Oregon added approximately 25,000 jobs over the past year, or 1.5% through third quarter 2012. However, unadjusted employment data indicates employment growth is stagnating. As noted last year, public sector employment continues to fall, with losses declining in recent months. The largest statewide gains in employment have been in professional and business services, leisure and hospitality, and retail trade.

2 | Tax-Free Trust of Oregon

MANAGEMENT DISCUSSION (continued)

The State monitors revenues and provides projections on a quarterly basis and makes adjustments when necessary. As of its December 2012 report, the State Economist forecasts general fund revenues for 2011-13 at $13.96 billion, which is an increase of $40 million from the State’s September 2012 forecast. Tax-Free Trust of Oregon (the “Trust”) has 10% exposure to direct State obligations and an additional 24% exposure to school district obligations, most of which are backed by the State through the Oregon School Bond Guaranty Program. In the forecast, the 2011-13 biennium is now estimated to be $71 million below the close of session forecast and the State estimates that with strong April 2013 tax collections, the State could approach original close of session’s estimates.

Total municipal bond issuance in Oregon for the 12 months ended September 30 decreased by approximately 8% to $3.4 billion as voters were reluctant to approve new issues at the ballot box and issuers either reduced capital spending plans or chose not to put new issues on the ballot. In this low interest rate environment, refunding bonds continue to play an important role. Approximately 39% of the issues brought to market in Oregon over the past year have been refunding bonds issued to realize debt service savings. Many of these issuers were smaller or more rural issuers. A leading indicator of future issuance is the November 2012 ballot, at which 11 issues with a cumulative estimated par amount of $661 million passed statewide. Bonds that were previously rejected by voters are once again making an appearance on the ballot indicating stronger voter sentiment for local money measures. The most prominent example of this is Portland Public Schools which passed a $482 million issue for facilities. This issue was previously rejected at the May, 2011 election and represents the largest local government bond measure ever approved by Oregon voters. In addition, Oregon voters approved ballot measure 85 which amends the Oregon Constitution to allocate corporate “kicker” dollars toward state funding of K-12 public education rather than rebating the money to corporations. The measure does not impact personal income tax kicker rebates.

Over the course of the past year, our conservative approach has provided a relatively stable share price. We have taken profits from longer duration securities and reduced exposure to zero coupon bonds from 10% of the Trust at the beginning of 2011 to the current 3%. As of September 30, 2012, the portfolio had an average maturity of 12.25 years with approximately 30% of the portfolio invested in maturities of less than 10-years. With 71.49% of portfolio holdings rated AAA or AA and 41.78% insured or pre-refunded. Additionally, the portfolio was evenly distributed between revenue and general obligation bonds. The total return for class A investors based on Net Asset Value was 7.14% and the double-exempt dividend yield averaged approximately 3.14% for the year ended September 30, 2012.

3 | Tax-Free Trust of Oregon

MANAGEMENT DISCUSSION (continued)

2012-13 Strategy

Tax-Free Trust of Oregon has maintained a consistent investment strategy that emphasizes intermediate maturities, thorough credit analysis, and investment grade credit quality securities with the goal of providing an above average double tax-exempt dividend and a relatively stable share price. We shall seek to accomplish this goal in the upcoming year by maintaining a neutral to defensive interest rate posture. Despite the Fed’s announced intention to maintain low interest rates, we believe the risk to our shareholders is a meaningful rise in interest rates from the current historic low levels. Positive developments regarding the fiscal cliff or significant progress toward reducing the Federal deficit could be a catalyst for the market to believe the economy will improve and exert upward pressure on interest rates. If it appears that no improvement is on the immediate horizon, it is likely we will remain in the low interest rate environment for the foreseeable future. In that case, legacy portfolio holdings purchased when rates were higher than today’s levels should continue to add stability to the share price and the monthly dividend. We have also made a great effort to reduce our reinvestment risk by limiting the bonds subject to call in the next 2 years to approximately 8% of the portfolio. We intend to closely monitor the yield differentials between long and short maturities as well as the differences between the various credit rating categories. As has always been the case, we will seek to reduce our exposure to longer maturities and lower credit quality bonds when their yields narrow relative to shorter, higher quality securities. Finally, we will continue our diligent credit research and surveillance for our existing holdings and for any securities we consider adding to the portfolio. It is imperative that we stay fully informed on the financial condition of our holdings in this challenging economic environment. We believe this investment strategy will generate a reliable double tax-exempt income stream and a relatively stable share price experience.

Thank you for your investment in Tax-Free Trust of Oregon.

Performance data represents past performance, but does not guarantee future results. Investment return and principal value will fluctuate; shares, when redeemed, may be worth more or less than their original cost; current performance may be lower or higher than the data presented.

NOT FDIC INSURED – NO BANK GUARANTEE – MAY LOSE VALUE

4 | Tax-Free Trust of Oregon

PERFORMANCE REPORT

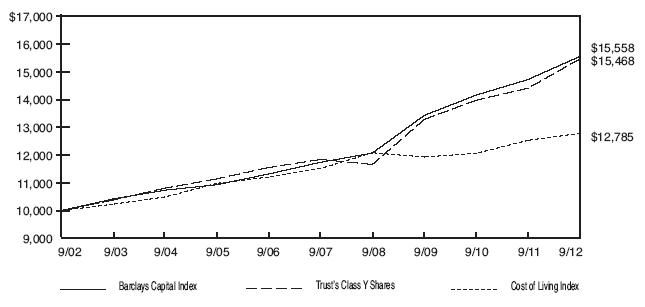

The following graph illustrates the value of $10,000 invested in the Class Y shares of Tax-Free Trust of Oregon for the 10-year period ended September 30, 2012 as compared with the Barclays Capital Quality Intermediate Municipal Bond Index (the “Barclays Capital Index”) and the Consumer Price Index (a cost of living index). The performance of each of the other classes is not shown in the graph but is included in the table below. It should be noted that the Barclays Capital Index does not include any operating expenses nor sales charges, and being nationally oriented, does not reflect state-specific bond market performance.

|

Average Annual Total Return

|

||||||||||||||||

|

for periods ended September 30, 2012

|

||||||||||||||||

|

Since

|

||||||||||||||||

|

Class and Inception Date

|

1 Year

|

5 Years

|

10 Years

|

inception

|

||||||||||||

|

Class A (commenced operations

|

||||||||||||||||

|

on 6/16/86)

|

||||||||||||||||

|

With Maximum Sales Charge

|

2.88 | % | 4.47 | % | 3.88 | % | 5.66 | % | ||||||||

|

Without Sales Charge

|

7.14 | 5.34 | 4.30 | 5.82 | ||||||||||||

|

Class C (commenced operations

|

||||||||||||||||

|

on 4/5/96)

|

||||||||||||||||

|

With CDSC**

|

5.21 | 4.43 | 3.42 | 4.15 | ||||||||||||

|

Without CDSC

|

6.24 | 4.43 | 3.42 | 4.15 | ||||||||||||

|

Class Y (commenced operations

|

||||||||||||||||

|

on 4/5/96)

|

||||||||||||||||

|

No Sales Charge

|

7.30 | 5.48 | 4.46 | 5.20 | ||||||||||||

|

Barclays Capital Index

|

5.66 | 5.79 | 4.52 |

5.87

|

* (Class A) | |||||||||||

|

5.22

|

(Class C & Y) | |||||||||||||||

Total return figures shown for the Trust reflect any change in price and assume all distributions within the period were invested in additional shares. The rates of return will vary and the principal value of an investment will fluctuate with market conditions. Shares, if redeemed, may be worth more or less than their original cost. A portion of each class’s income may be subject to Federal and state income taxes. Past performance is not predictive of future investment results.

* From commencement of the index on 1/1/87.

** CDSC = 1% contingent deferred sales charge imposed on redemptions made within the first 12 months after purchase.

5 | Tax-Free Trust of Oregon

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees and Shareholders of

Tax-Free Trust of Oregon:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Tax-Free Trust of Oregon as of September 30, 2012 and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Trust’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Trust is not required to have, nor were we engaged to perform, an audit of the Trust’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2012, by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Tax-Free Trust of Oregon as of September 30, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

November 27, 2012

6 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (49.2%)

|

(unaudited)

|

Value

|

||||||

|

City & County (6.4%)

|

|||||||||

|

Bend, Oregon

|

|||||||||

| $ | 2,435,000 |

4.000%, 06/01/24

|

Aa2/NR/NR

|

$ | 2,826,037 | ||||

|

Canby, Oregon

|

|||||||||

| 1,060,000 |

5.000%, 06/01/27

|

A2/NR/NR

|

1,228,487 | ||||||

|

Clackamas County, Oregon Refunding

|

|||||||||

| 1,135,000 |

4.000%, 06/01/24

|

Aa2/NR/NR

|

1,301,277 | ||||||

|

Clackamas County, Oregon Tax

|

|||||||||

|

Allocation

|

|||||||||

| 705,000 |

6.500%, 05/01/20

|

NR/NR/NR*

|

706,481 | ||||||

|

Deschutes County, Oregon

|

|||||||||

| 2,260,000 |

5.000%, 12/01/16 AGMC Insured

|

Aa2/NR/NR

|

2,276,747 | ||||||

|

Hillsboro, Oregon

|

|||||||||

| 380,000 |

3.500%, 06/01/15 Series B

|

Aa3/NR/NR

|

405,813 | ||||||

| 390,000 |

3.500%, 06/01/16 Series B

|

Aa3/NR/NR

|

426,582 | ||||||

| 345,000 |

3.500%, 06/01/17 Series B

|

Aa3/NR/NR

|

379,707 | ||||||

|

Hillsboro, Oregon Refunding

|

|||||||||

| 1,305,000 |

4.500%, 06/01/22

|

Aa3/NR/NR

|

1,583,905 | ||||||

|

Portland, Oregon

|

|||||||||

| 6,335,000 |

4.350%, 06/01/23

|

Aa1/NR/NR

|

6,439,718 | ||||||

|

Portland, Oregon Public Safety

|

|||||||||

| 2,130,000 |

4.125%, 06/01/26 Series A

|

Aaa/NR/NR

|

2,384,109 | ||||||

|

Portland, Oregon Revenue Limited Tax,

|

|||||||||

|

Improvement

|

|||||||||

| 1,165,000 |

4.000%, 06/01/22 Series A

|

Aa1/NR/NR

|

1,258,491 | ||||||

|

Portland, Oregon Revenue Refunding

|

|||||||||

|

Limited Tax, Oregon Convention

|

|||||||||

|

Center

|

|||||||||

| 4,765,000 |

5.000%, 06/01/27

|

Aa1/NR/NR

|

5,745,018 | ||||||

|

Redmond, Oregon Refunding

|

|||||||||

| 735,000 |

5.000%, 06/01/23 Series A

|

A1/NR/NR

|

893,231 | ||||||

|

City of Salem, Oregon

|

|||||||||

| 1,585,000 |

4.000%, 06/01/17

|

Aa2/AA-/NR

|

1,803,334 | ||||||

| 1,750,000 |

5.000%, 06/01/29

|

Aa2/AA-/NR

|

2,020,340 | ||||||

|

Washington County, Oregon

|

|||||||||

| 2,465,000 |

5.000%, 06/01/23

|

Aa1/NR/NR

|

2,811,185 | ||||||

|

Total City & County

|

34,490,462 | ||||||||

7 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Community College (5.9%)

|

|||||||||

|

Central Oregon Community College

|

|||||||||

|

District School Bond Guaranty

|

|||||||||

|

Program

|

|||||||||

| $ | 1,850,000 |

4.750%, 06/15/22

|

NR/AA+/NR

|

$ | 2,246,658 | ||||

| 2,195,000 |

4.750%, 06/15/23

|

NR/AA+/NR

|

2,644,580 | ||||||

| 2,175,000 |

4.750%, 06/15/26

|

NR/AA+/NR

|

2,567,500 | ||||||

|

Chemeketa, Oregon Community

|

|||||||||

|

College District

|

|||||||||

| 1,385,000 |

5.500%, 06/01/14 ETM FGIC Insured

|

NR/NR/NR*

|

1,502,310 | ||||||

|

Chemeketa, Oregon Community College

|

|||||||||

|

District School Bond Guaranty Program

|

|||||||||

| 1,010,000 |

5.500%, 06/15/24

|

NR/AA+/NR

|

1,205,516 | ||||||

| 1,235,000 |

5.000%, 06/15/25

|

NR/AA+/NR

|

1,428,574 | ||||||

| 1,540,000 |

5.000%, 06/15/26

|

NR/AA+/NR

|

1,775,112 | ||||||

|

Clackamas, Oregon Community

|

|||||||||

|

College District

|

|||||||||

| 1,535,000 |

5.000%, 05/01/25 NPFG Insured

|

Aa3/AA/NR

|

1,686,520 | ||||||

|

Columbia Gorge, Oregon Community

|

|||||||||

|

College District, Refunding, School

|

|||||||||

|

Board Guaranty Program

|

|||||||||

| 1,000,000 |

4.000%, 06/15/24

|

Aa1/NR/NR

|

1,147,020 | ||||||

|

Lane, Oregon Community College

|

|||||||||

|

School Bond Guaranty Program

|

|||||||||

| 1,840,000 |

5.000%, 06/15/24

|

NR/AA+/NR

|

2,278,693 | ||||||

|

Oregon Coast Community College

|

|||||||||

|

District State School Bond Guaranty

|

|||||||||

|

Program

|

|||||||||

| 1,590,000 |

5.250%, 06/15/17 NPFG Insured

|

||||||||

|

(pre-refunded)

|

Aa1/NR/NR

|

1,722,495 | |||||||

| 1,770,000 |

5.000%, 06/15/25

|

Aa1/NR/NR

|

2,188,516 | ||||||

|

Portland, Oregon Community College

|

|||||||||

|

District

|

|||||||||

| 7,915,000 |

5.000%, 06/15/28

|

Aa1/AA/NR

|

9,528,868 | ||||||

|

Total Community College

|

31,922,362 | ||||||||

8 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Higher Education (1.8%)

|

|||||||||

|

State of Oregon Board of Higher

|

|||||||||

|

Education

|

|||||||||

| $ | 820,000 |

zero coupon, 08/01/16

|

Aa1/AA+/AA+

|

$ | 781,509 | ||||

| 1,125,000 |

5.000%, 08/01/21 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/NR/NR

|

1,268,662 | |||||||

| 875,000 |

5.000%, 08/01/21 Series A

|

Aa1/AA+/NR

|

972,335 | ||||||

| 500,000 |

5.750%, 08/01/29 Series A

|

Aa1/AA+/AA+

|

604,785 | ||||||

| 1,000,000 |

5.000%, 08/01/34

|

Aa1/AA+/AA+

|

1,155,890 | ||||||

| 1,000,000 |

5.000%, 08/01/38

|

Aa1/AA+/AA+

|

1,143,510 | ||||||

|

Oregon State, Oregon University System

|

|||||||||

| 1,170,000 |

4.000%, 08/01/25 Series B

|

Aa1/AA+/AA+

|

1,348,484 | ||||||

|

Oregon State, Oregon University

|

|||||||||

|

System Projects

|

|||||||||

| 2,365,000 |

4.000%, 08/01/26 Series H

|

Aa1/AA+/AA+

|

2,678,433 | ||||||

|

Total Higher Education

|

9,953,608 | ||||||||

|

Housing (0.2%)

|

|||||||||

|

State of Oregon Veterans’ Welfare

|

|||||||||

| 550,000 |

4.800%, 12/01/22

|

Aa1/AA+/AA+

|

592,499 | ||||||

| 400,000 |

4.900%, 12/01/26

|

Aa1/AA+/AA+

|

429,032 | ||||||

|

Total Housing

|

1,021,531 | ||||||||

|

Puerto Rico (0.3%)

|

|||||||||

|

Puerto Rico Commonwealth

|

|||||||||

| 1,270,000 |

6.000%, 07/01/28 NPFG Insured

|

Baa1/BBB/NR

|

1,384,833 | ||||||

|

Puerto Rico Municipal Finance Agency

|

|||||||||

| 500,000 |

5.250%, 08/01/16 AGMC Insured

|

Aa3/AA-/NR

|

501,355 | ||||||

|

Total Puerto Rico

|

1,886,188 | ||||||||

|

School District (22.8%)

|

|||||||||

|

Benton & Linn Counties, Oregon School

|

|||||||||

|

District #509J Corvallis

|

|||||||||

| 4,670,000 |

5.000%, 06/01/21 (pre-refunded)

|

||||||||

|

AGMC Insured

|

Aa1/NR/NR

|

4,815,471 | |||||||

|

Clackamas County, Oregon School

|

|||||||||

|

District #12 (North Clackamas)

|

|||||||||

| 8,000,000 |

5.000%, 06/15/27 Series B AGMC

|

||||||||

|

Insured

|

Aa1/AA+/NR

|

9,125,280 | |||||||

| 9,250,000 |

5.000%, 06/15/29 AGMC Insured

|

Aa1/AA+/NR

|

10,501,987 | ||||||

9 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School District (continued)

|

|||||||||

|

Clackamas County, Oregon School

|

|||||||||

|

District #46 (Oregon Trail) School

|

|||||||||

|

Bond Guaranty Program

|

|||||||||

| $ | 1,000,000 |

5.000%, 06/15/22

|

NR/AA+/NR

|

$ | 1,186,520 | ||||

| 1,865,000 |

5.000%, 06/15/28 Series A

|

NR/AA+/NR

|

2,168,417 | ||||||

| 1,800,000 |

5.000%, 06/15/29 Series A

|

NR/AA+/NR

|

2,086,794 | ||||||

| 2,000,000 |

4.500%, 06/15/30 AGMC Insured

|

Aa1/AA+/NR

|

2,178,120 | ||||||

| 2,000,000 |

5.000%, 06/15/32 Series A

|

NR/AA+/NR

|

2,284,080 | ||||||

| 3,780,000 |

4.750%, 06/15/32 Series A

|

NR/AA+/NR

|

4,259,304 | ||||||

|

Clackamas County, Oregon School

|

|||||||||

|

District #86 (Canby)

|

|||||||||

| 2,240,000 |

5.000%, 06/15/19 AGMC Insured

|

||||||||

|

(pre-refunded)

|

Aa1/AA+/NR

|

2,516,416 | |||||||

| 1,800,000 |

5.000%, 06/15/24

|

Aa1/AA+/NR

|

2,255,886 | ||||||

| 1,110,000 |

5.000%, 06/15/25 Series A

|

Aa1/AA+/NR

|

1,383,404 | ||||||

|

Clackamas & Washington Counties,

|

|||||||||

|

Oregon School District No. 003

|

|||||||||

|

(West Linn-Wilsonville)

|

|||||||||

| 1,110,000 |

5.000%, 06/15/26

|

Aa1/AA+/NR

|

1,310,932 | ||||||

| 500,000 |

5.000%, 06/15/34

|

Aa1/AA+/NR

|

571,020 | ||||||

|

Clackamas & Washington Counties,

|

|||||||||

|

Oregon School District #3J (West

|

|||||||||

|

Linn - Wilsonville) School Bond

|

|||||||||

|

Guaranty Program

|

|||||||||

| 2,850,000 |

5.000%, 06/15/27

|

Aa1/AA+/NR

|

3,352,284 | ||||||

| 2,000,000 |

4.500%, 06/15/29

|

Aa1/AA+/NR

|

2,229,600 | ||||||

| 1,965,000 |

5.000%, 06/15/30

|

Aa1/AA+/NR

|

2,282,033 | ||||||

| 3,000,000 |

5.000%, 06/15/33

|

Aa1/AA+/NR

|

3,441,990 | ||||||

|

Columbia County, Oregon School

|

|||||||||

|

District #502

|

|||||||||

| 2,070,000 |

zero coupon, 06/01/15 NPFG FGIC

|

||||||||

|

Insured

|

Aa3/BBB/NR

|

1,982,998 | |||||||

|

Columbia & Washington Counties,

|

|||||||||

|

Oregon School District #47J (Vernonia)

|

|||||||||

|

State School Bond Guaranty Program

|

|||||||||

| 3,430,000 |

5.00%, 06/15/27

|

NR/AA+/NR

|

4,090,652 | ||||||

10 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School District (continued)

|

|||||||||

|

Deschutes County, Oregon Administrative

|

|||||||||

|

School District #1 Refunding

|

|||||||||

| $ | 400,000 |

5.000%, 06/15/13 AGMC Insured

|

Aa1/NR/NR

|

$ | 413,392 | ||||

|

Deschutes County, Oregon School

|

|||||||||

|

District #6 (Sisters)

|

|||||||||

| 1,735,000 |

5.250%, 06/15/19 AGMC Insured

|

Aa3/AA+/NR

|

2,140,747 | ||||||

| 1,030,000 |

5.250%, 06/15/21 AGMC Insured

|

Aa3/AA+/NR

|

1,291,383 | ||||||

|

Deschutes and Jefferson Counties, Oregon

|

|||||||||

|

School District #02J (Redmond)

|

|||||||||

| 1,000,000 |

5.000%, 06/15/21 NPFG FGIC Insured

|

Aa1/NR/NR

|

1,070,760 | ||||||

| 1,025,000 |

zero coupon, 06/15/23

|

Aa1/NR/NR

|

779,113 | ||||||

| 5,000,000 |

6.000%, 06/15/31

|

Aa1/NR/NR

|

6,027,300 | ||||||

|

Hood River County, Oregon School

|

|||||||||

|

District Refunding School Bond

|

|||||||||

|

Guaranty Program

|

|||||||||

| 365,000 |

3.000%, 06/15/14

|

NR/AA+/NR

|

380,301 | ||||||

| 385,000 |

3.000%, 06/15/15

|

NR/AA+/NR

|

407,469 | ||||||

| 250,000 |

4.000%, 06/15/16

|

NR/AA+/NR

|

278,717 | ||||||

|

Jackson County, Oregon School District

|

|||||||||

|

#9 (Eagle Point)

|

|||||||||

| 2,080,000 |

5.500%, 06/15/15 NPFG Insured

|

Aa1/NR/NR

|

2,325,149 | ||||||

| 1,445,000 |

5.500%, 06/15/16 NPFG Insured

|

Aa1/NR/NR

|

1,672,602 | ||||||

|

Jackson County, Oregon School District

|

|||||||||

|

#549C (Medford) School Board

|

|||||||||

|

Guaranty Program

|

|||||||||

| 1,000,000 |

4.625%, 06/15/27

|

Aa1/AA+/NR

|

1,117,280 | ||||||

| 2,000,000 |

4.750%, 12/15/29 AGMC Insured

|

Aa1/AA+/NR

|

2,226,340 | ||||||

| 1,000,000 |

5.000%, 06/15/33

|

Aa1/AA+/NR

|

1,126,910 | ||||||

|

Jefferson County, Oregon School District

|

|||||||||

|

#509J School Board Guaranty Program

|

|||||||||

| 1,215,000 |

5.250%, 06/15/14 NPFG/ FGIC Insured

|

NR/AA+/NR

|

1,219,289 | ||||||

| 1,025,000 |

5.250%, 06/15/17 NPFG/ FGIC Insured

|

NR/AA+/NR

|

1,028,721 | ||||||

|

Lane County, Oregon School District

|

|||||||||

|

#4J (Eugene) Refunding School Board

|

|||||||||

|

Guaranty Program

|

|||||||||

| 1,000,000 |

5.000%, 07/01/15

|

Aa1/NR/NR

|

1,117,830 | ||||||

| 1,130,000 |

4.000%, 06/15/23

|

Aa1/NR/NR

|

1,288,302 | ||||||

11 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School District (continued)

|

|||||||||

|

Lane County, Oregon School District

|

|||||||||

|

#19 (Springfield)

|

|||||||||

| $ | 3,425,000 |

zero coupon, 06/15/29 AGMC

|

|||||||

|

Insured

|

Aa1/NR/NR

|

$ | 1,672,804 | ||||||

|

Lincoln County, Oregon School District,

|

|||||||||

|

School Board Guaranty Program

|

|||||||||

| 2,370,000 |

4.000%, 06/15/24 Series A

|

Aa1/NR/NR

|

2,685,968 | ||||||

|

Linn County, Oregon School District #9

|

|||||||||

|

(Lebanon) School Board Guaranty

|

|||||||||

|

Program

|

|||||||||

| 3,000,000 |

5.600%, 06/15/30 FGIC Insured

|

||||||||

|

(pre-refunded)

|

NR/AA+/NR

|

3,111,510 | |||||||

|

Morrow County, Oregon School

|

|||||||||

|

District #1

|

|||||||||

| 1,710,000 |

5.250%, 06/15/19 AGMC Insured

|

Aa3/AA+/NR

|

2,109,901 | ||||||

|

Multnomah County, Oregon School

|

|||||||||

|

District #7 (Reynolds) Refunding

|

|||||||||

| 1,165,000 |

5.000%, 06/01/29

|

Aa3/NR/NR

|

1,387,457 | ||||||

|

Multnomah County, Oregon School

|

|||||||||

|

District #40 (David Douglas) School

|

|||||||||

|

Bond Guaranty Program

|

|||||||||

| 1,420,000 |

4.000%, 06/15/23 Series A

|

NR/AA+/NR

|

1,646,163 | ||||||

|

Multnomah and Clackamas Counties,

|

|||||||||

|

Oregon School District #10

|

|||||||||

|

(Gresham-Barlow)

|

|||||||||

| 4,275,000 |

5.250%, 06/15/19 AGMC Insured

|

Aa1/AA+/NR

|

5,320,921 | ||||||

|

Multnomah and Clackamas Counties,

|

|||||||||

|

Oregon School District #28JT

|

|||||||||

|

(Centennial)

|

|||||||||

| 2,680,000 |

5.250%, 12/15/18 AGMC Insured

|

Aa1/NR/NR

|

3,272,816 | ||||||

|

Polk, Marion & Benton Counties,

|

|||||||||

|

Oregon School District #13J (Central)

|

|||||||||

| 1,520,000 |

5.000%, 06/15/21 AGMC Insured

|

Aa3/AA+/NR

|

1,730,870 | ||||||

|

Salem-Keizer, Oregon School District #24J

|

|||||||||

| 1,000,000 |

5.000%, 06/15/19 AGMC Insured

|

Aa1/AA+/NR

|

1,075,010 | ||||||

12 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

School District (continued)

|

|||||||||

|

Wasco County, Oregon School District

|

|||||||||

|

#12 (The Dalles)

|

|||||||||

| $ | 1,400,000 |

5.500%, 06/15/17 AGMC Insured

|

Aa3/AA-/NR

|

$ | 1,676,416 | ||||

| 1,790,000 |

5.500%, 06/15/20 AGMC Insured

|

Aa3/AA-/NR

|

2,245,143 | ||||||

|

Washington County, Oregon School

|

|||||||||

|

District #48J (Beaverton)

|

|||||||||

| 1,280,000 |

5.000%, 06/01/31 AGC Insured

|

Aa2/AA-/NR

|

1,487,974 | ||||||

| 1,000,000 |

5.125%, 06/01/36 AGC Insured

|

Aa2/AA-/NR

|

1,152,160 | ||||||

|

Yamhill County, Oregon School District

|

|||||||||

|

#40 (McMinnville) School Bond

|

|||||||||

|

Guaranty Program

|

|||||||||

| 1,205,000 |

5.000%, 06/15/19 AGMC Insured

|

Aa1/NR/NR

|

1,416,044 | ||||||

| 1,375,000 |

5.000%, 06/15/22 AGMC Insured

|

Aa1/NR/NR

|

1,575,750 | ||||||

|

Total School Districts

|

123,501,700 | ||||||||

|

Special District (1.8%)

|

|||||||||

|

Metro, Oregon

|

|||||||||

| 1,100,000 |

5.000%, 06/01/18

|

Aaa/AAA/NR

|

1,308,175 | ||||||

| 4,000,000 |

4.000%, 06/01/26 Series A

|

Aaa/AAA/NR

|

4,552,520 | ||||||

|

Tualatin Hills, Oregon Park &

|

|||||||||

|

Recreational District

|

|||||||||

| 1,000,000 |

4.250%, 06/01/24

|

Aa1/AA/NR

|

1,126,350 | ||||||

|

Tualatin Valley, Oregon Fire & Rescue

|

|||||||||

|

Rural Fire Protection District

|

|||||||||

| 1,235,000 |

4.000%, 06/01/26

|

Aaa/NR/NR

|

1,394,846 | ||||||

| 1,170,000 |

4.000%, 06/01/27

|

Aaa/NR/NR

|

1,314,600 | ||||||

|

Total Special District

|

9,696,491 | ||||||||

|

State (9.0%)

|

|||||||||

|

Oregon State Alternative Energy Project

|

|||||||||

| 1,255,000 |

4.750%, 04/01/29 Series B

|

Aa1/AA+/AA+

|

1,423,308 | ||||||

| 500,000 |

6.000%, 10/01/29 Series B

|

Aa1/AA+/AA+

|

617,865 | ||||||

|

Oregon State Department of

|

|||||||||

|

Administrative Services

|

|||||||||

| 3,270,000 |

5.000%, 11/01/27 Series C

|

Aa2/AA/AA

|

3,772,010 | ||||||

| 2,155,000 |

5.000%, 11/01/28 Series C

|

Aa2/AA/AA

|

2,478,336 | ||||||

| 5,000,000 |

5.125%, 05/01/33

|

Aa2/AA/AA

|

5,664,950 | ||||||

13 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

General Obligation Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

State (continued)

|

|||||||||

|

Oregon State Department of

|

|||||||||

|

Administrative Services (continued)

|

|||||||||

| $ | 2,000,000 |

5.000%, 11/01/20 NPFG FGIC Insured

|

|||||||

|

(pre-refunded)

|

Aa2/AA/AA

|

$ | 2,281,140 | ||||||

| 2,660,000 |

5.000%, 11/01/23 NPFG FGIC Insured

|

Aa2/AA/AA

|

2,957,707 | ||||||

| 2,945,000 |

5.000%, 11/01/24 NPFG FGIC Insured

|

Aa2/AA/AA

|

3,264,886 | ||||||

| 1,475,000 |

5.000%, 11/01/26 NPFG FGIC Insured

|

Aa2/AA/AA

|

1,632,781 | ||||||

| 3,880,000 |

5.000%, 11/01/27 NPFG FGIC Insured

|

Aa2/AA/AA

|

4,283,869 | ||||||

|

Oregon State Department of

|

|||||||||

|

Administrative Services, Oregon

|

|||||||||

|

Opportunity Refunding

|

|||||||||

| 6,210,000 |

5.000%, 12/01/19

|

Aa1/AA+/AA+

|

7,873,286 | ||||||

|

Oregon State Refunding

|

|||||||||

| 3,000,000 |

5.000%, 05/01/23 Series L

|

Aa1/AA+/AA+

|

3,727,500 | ||||||

| 1,125,000 |

5.000%, 05/01/24 Series L

|

Aa1/AA+/AA+

|

1,393,796 | ||||||

| 2,630,000 |

5.000%, 05/01/26 Series L

|

Aa1/AA+/AA+

|

3,239,713 | ||||||

|

Oregon State Refunding Various Projects

|

|||||||||

| 2,125,000 |

4.000%, 05/01/25 Series O

|

Aa1/AA+/AA+

|

2,410,047 | ||||||

|

Oregon State Various Projects

|

|||||||||

| 1,470,000 |

4.000%, 11/01/26 Series M

|

Aa1/AA+/AA+

|

1,669,788 | ||||||

|

Total State

|

48,690,982 | ||||||||

|

Water & Sewer (0.8%)

|

|||||||||

|

Gearheart, Oregon

|

|||||||||

| 1,060,000 |

4.500%, 03/01/26 AGMC Insured

|

Aa3/NR/NR

|

1,221,639 | ||||||

|

Pacific City, Oregon Joint Water -

|

|||||||||

|

Sanitary Authority

|

|||||||||

| 1,830,000 |

4.800%, 07/01/27

|

NR/NR/NR*

|

1,948,730 | ||||||

|

Rockwood, Oregon Water Peoples

|

|||||||||

|

Utility District Water Revenue

|

|||||||||

|

Refunding

|

|||||||||

| 1,270,000 |

4.250%, 08/15/26

|

A1/NR/NR

|

1,398,994 | ||||||

|

Total Water & Sewer

|

4,569,363 | ||||||||

|

Total General Obligation Bonds

|

265,732,687 | ||||||||

14 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (49.4%)

|

(unaudited)

|

Value

|

||||||

|

City & County (3.8%)

|

|||||||||

|

Newport, Oregon Urban Renewal

|

|||||||||

|

Obligations, Refunding

|

|||||||||

| $ | 565,000 |

4.500%, 06/15/22 Series B

|

NR/A+/NR

|

$ | 651,807 | ||||

|

Portland, Oregon

|

|||||||||

| 2,975,000 |

zero coupon, 06/01/15

|

Aa1/NR/NR

|

2,887,892 | ||||||

|

Portland, Oregon Revenue Refunding

|

|||||||||

|

Limited Tax, Oregon Convention

|

|||||||||

|

Center

|

|||||||||

| 2,825,000 |

5.000%, 06/01/24

|

Aa1/NR/NR

|

3,458,082 | ||||||

|

Portland, Oregon Revenue Refunding

|

|||||||||

|

Limited Tax

|

|||||||||

| 1,000,000 |

4.000%, 04/01/22 Series A

|

Aa1/NR/NR

|

1,118,010 | ||||||

|

Portland, Oregon River District Urban

|

|||||||||

|

Renewal and Redevelopment

|

|||||||||

| 1,915,000 |

5.000%, 06/15/20 AMBAC Insured

|

||||||||

|

(pre-refunded)

|

A1/NR/NR

|

1,978,846 | |||||||

| 1,600,000 |

5.000%, 06/15/22 Series B

|

A1/NR/NR

|

1,910,624 | ||||||

| 1,000,000 |

5.000%, 06/15/23 Series B

|

A1/NR/NR

|

1,182,910 | ||||||

|

Portland, Oregon Urban Renewal and

|

|||||||||

|

Redevelopment, Refunding, North

|

|||||||||

|

Macadam

|

|||||||||

| 1,000,000 |

4.000%, 06/15/25 Series B

|

A1/NR/NR

|

1,052,780 | ||||||

|

Portland, Oregon Urban Renewal Tax

|

|||||||||

|

Allocation (Interstate Corridor)

|

|||||||||

| 1,890,000 |

5.250%, 06/15/20 NPFG FGIC Insured

|

A1/NR/NR

|

2,018,180 | ||||||

| 1,810,000 |

5.250%, 06/15/21 NPFG FGIC Insured

|

A1/NR/NR

|

1,924,464 | ||||||

| 2,030,000 |

5.000%, 06/15/23 NPFG FGIC Insured

|

A1/NR/NR

|

2,127,460 | ||||||

|

Total City & County

|

20,311,055 | ||||||||

|

Electric (2.2%)

|

|||||||||

|

Emerald Peoples Utility District, Oregon

|

|||||||||

| 1,455,000 |

5.250%, 11/01/22 AGMC Insured

|

Aa3/NR/NR

|

1,516,139 | ||||||

|

Eugene, Oregon Electric Utility

|

|||||||||

| 5,635,000 |

5.000%, 08/01/30

|

Aa3/AA-/AA-

|

6,384,568 | ||||||

|

Eugene, Oregon Electric Utility

|

|||||||||

|

Refunding System

|

|||||||||

| 2,000,000 |

5.000%, 08/01/27 Series A

|

Aa3/AA-/AA-

|

2,409,640 | ||||||

15 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Electric (continued)

|

|||||||||

|

Northern Wasco County, Oregon

|

|||||||||

|

Peoples Utility District, McNary Dam

|

|||||||||

|

Fishway Hydroelectric Project,

|

|||||||||

|

Refunding

|

|||||||||

| $ | 1,585,000 |

5.000%, 12/01/21 Series A

|

NR/AA-/NR

|

$ | 1,951,357 | ||||

|

Total Electric

|

12,261,704 | ||||||||

|

Higher Education (7.4%)

|

|||||||||

|

Forest Grove, Oregon Campus

|

|||||||||

|

Improvement (Pacific University

|

|||||||||

|

Project)

|

|||||||||

| 1,500,000 |

6.000%, 05/01/30

|

NR/BBB/NR

|

1,541,670 | ||||||

|

Forest Grove, Oregon (Pacific University)

|

|||||||||

| 4,000,000 |

5.000%, 05/01/22 Radian Insured

|

NR/BBB/NR

|

4,151,560 | ||||||

|

Forest Grove, Oregon Student Housing

|

|||||||||

|

(Oak Tree Foundation)

|

|||||||||

| 5,750,000 |

5.500%, 03/01/37

|

NR/NR/NR*

|

5,891,967 | ||||||

|

Oregon Health Sciences University

|

|||||||||

| 2,890,000 |

5.250%, 07/01/22 NPFG Insured

|

||||||||

|

(pre-refunded)

|

A1/A+/A+

|

2,925,576 | |||||||

|

Oregon State Facilities Authority (Lewis

|

|||||||||

|

& Clark College Project)

|

|||||||||

| 1,000,000 |

5.250%, 10/01/24 Series A

|

A3/A-/NR

|

1,193,610 | ||||||

| 3,000,000 |

5.000%, 10/01/27 Series A

|

A3/A-/NR

|

3,441,900 | ||||||

|

Oregon State Facilities Authority (Linfield

|

|||||||||

|

College Project)

|

|||||||||

| 2,830,000 |

5.000%, 10/01/20 Series A 2005

|

Baa1/NR/NR

|

3,044,769 | ||||||

| 2,115,000 |

5.000%, 10/01/25 Series A 2005

|

Baa1/NR/NR

|

2,229,062 | ||||||

| 1,220,000 |

5.000%, 10/01/31 Series A 2010

|

Baa1/NR/NR

|

1,346,648 | ||||||

|

Oregon State Facilities Authority Revenue

|

|||||||||

|

Refunding (Reed College Project)

|

|||||||||

| 1,500,000 |

5.000%, 07/01/29 Series A

|

Aa2/AA-/NR

|

1,760,190 | ||||||

|

Oregon State Facilities Authority

|

|||||||||

|

(University of Portland)

|

|||||||||

| 3,000,000 |

5.000%, 04/01/32

|

NR/BBB+/NR

|

3,223,170 | ||||||

|

Oregon State Facilities Authority

|

|||||||||

|

(Willamette University)

|

|||||||||

| 1,000,000 |

4.000%, 10/01/24

|

NR/A/NR

|

1,108,420 | ||||||

| 2,500,000 |

5.000%, 10/01/32

|

NR/A/NR

|

2,697,800 | ||||||

16 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Higher Education (continued)

|

|||||||||

|

Portland, Oregon Economic

|

|||||||||

|

Development (Broadway Project)

|

|||||||||

| $ | 5,000,000 |

6.500%, 04/01/35

|

A1/A+/NR

|

$ | 5,616,350 | ||||

|

Total Higher Education

|

40,172,692 | ||||||||

|

Hospital (11.3%)

|

|||||||||

|

Deschutes County, Oregon Hospital

|

|||||||||

|

Facilities Authority (Cascade Health)

|

|||||||||

| 3,500,000 |

8.000%, 01/01/28

|

A3/NR/NR

|

4,468,905 | ||||||

| 3,250,000 |

5.375%, 01/01/35 AMBAC Insured

|

A3/NR/NR

|

3,511,982 | ||||||

|

Medford, Oregon Hospital Facilities

|

|||||||||

|

Authority Revenue Refunding, Asante

|

|||||||||

|

Health Systems

|

|||||||||

| 9,000,000 |

5.500%, 08/15/28 AGMC Insured

|

NR/AA-/NR

|

10,422,450 | ||||||

|

Multnomah County, Oregon Hospital

|

|||||||||

|

Facilities Authority (Adventist

|

|||||||||

|

Health/West)

|

|||||||||

| 500,000 |

5.000%, 09/01/21

|

NR/A/A

|

570,020 | ||||||

|

Multnomah County, Oregon Hospital

|

|||||||||

|

Facilities Authority (Providence

|

|||||||||

|

Health System)

|

|||||||||

| 1,390,000 |

5.250%, 10/01/22

|

Aa2/AA/AA

|

1,492,610 | ||||||

|

Oregon Health Sciences University

|

|||||||||

| 11,550,000 |

zero coupon, 07/01/21 NPFG Insured

|

A1/A+/A+

|

8,907,822 | ||||||

| 2,000,000 |

5.000%, 07/01/23 Series A

|

A1/A+/A+

|

2,405,040 | ||||||

| 4,500,000 |

5.750%, 07/01/39 Series A

|

A1/A+/A+

|

5,271,255 | ||||||

|

Oregon State Facilities Authority

|

|||||||||

|

Revenue Refunding, Legacy Health

|

|||||||||

|

Systems

|

|||||||||

| 2,000,000 |

4.250%, 03/15/17

|

A2/A+/NR

|

2,237,720 | ||||||

| 3,000,000 |

4.500%, 03/15/18

|

A2/A+/NR

|

3,443,880 | ||||||

| 1,000,000 |

4.750%, 03/15/24

|

A2/A+/NR

|

1,098,530 | ||||||

| 1,000,000 |

5.000%, 03/15/30

|

A2/A+/NR

|

1,090,750 | ||||||

|

Oregon State Facilities Authority

|

|||||||||

|

Revenue Refunding, Samaritan

|

|||||||||

|

Health Services

|

|||||||||

| 1,500,000 |

4.375%, 10/01/20

|

NR/A-/NR

|

1,638,945 | ||||||

| 2,000,000 |

4.500%, 10/01/21

|

NR/A-/NR

|

2,174,760 | ||||||

| 1,520,000 |

5.000%, 10/01/23

|

NR/A-/NR

|

1,703,677 | ||||||

17 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Hospital (continued)

|

|||||||||

|

Oregon State Facilities Authority

|

|||||||||

|

Revenue Refunding, Samaritan

|

|||||||||

|

Health Services (continued)

|

|||||||||

| $ | 1,795,000 |

4.875%, 10/01/25

|

NR/A-/NR

|

$ | 1,981,626 | ||||

| 2,000,000 |

5.000%, 10/01/30

|

NR/A-/NR

|

2,204,700 | ||||||

|

Salem, Oregon Hospital Facility

|

|||||||||

|

Authority (Salem Hospital)

|

|||||||||

| 2,000,000 |

5.750%, 08/15/23

|

NR/A/A+

|

2,303,060 | ||||||

| 1,075,000 |

5.000%, 08/15/27 Series A

|

NR/A/A+

|

1,159,431 | ||||||

|

State of Oregon Health Housing

|

|||||||||

|

Educational and Cultural Facilities

|

|||||||||

|

Authority (Peacehealth)

|

|||||||||

| 1,835,000 |

5.250%, 11/15/17 AMBAC Insured

|

NR/A+/AA-

|

1,844,267 | ||||||

| 1,430,000 |

5.000%, 11/15/32 AMBAC Insured

|

NR/A+/AA-

|

1,432,860 | ||||||

|

Total Hospital

|

61,364,290 | ||||||||

|

Housing (1.0%)

|

|||||||||

|

Portland, Oregon Urban Renewal and

|

|||||||||

|

Redevelopment, Interstate Corridor

|

|||||||||

| 1,390,000 |

5.000%, 06/15/27 Series B

|

A1/NR/NR

|

1,544,054 | ||||||

|

State of Oregon Housing and

|

|||||||||

|

Community Services

|

|||||||||

| 1,950,000 |

4.650%, 07/01/25

|

Aa2/NR/NR

|

2,077,569 | ||||||

| 1,580,000 |

5.350%, 07/01/30

|

Aa2/NR/NR

|

1,689,936 | ||||||

|

Total Housing

|

5,311,559 | ||||||||

|

Lottery (4.0%)

|

|||||||||

|

Oregon State Department of

|

|||||||||

|

Administration Services (Lottery

|

|||||||||

|

Revenue)

|

|||||||||

| 2,700,000 |

5.000%, 04/01/19 AGMC Insured

|

||||||||

|

(pre-refunded)

|

Aa2/AAA/AA-

|

2,890,755 | |||||||

| 1,195,000 |

5.000%, 04/01/24 Series A

|

Aa2/AAA/NR

|

1,486,078 | ||||||

| 1,500,000 |

5.000%, 04/01/25 Series B

|

Aa2/AAA/NR

|

1,847,985 | ||||||

| 7,300,000 |

5.250%, 04/01/26

|

Aa2/AAA/NR

|

8,991,045 | ||||||

| 3,000,000 |

5.000%, 04/01/27 AGMC Insured

|

Aa2/AAA/AA-

|

3,453,300 | ||||||

| 2,500,000 |

5.000%, 04/01/29

|

Aa2/AAA/NR

|

2,918,175 | ||||||

|

Total Lottery

|

21,587,338 | ||||||||

18 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Transportation (6.9%)

|

|||||||||

|

Jackson County, Oregon Airport Revenue

|

|||||||||

| $ | 750,000 |

5.250%, 12/01/32 Syncora Guarantee,

|

|||||||

|

Inc. Insured

|

Baa1/NR/NR

|

$ | 779,452 | ||||||

|

Oregon State Department Transportation

|

|||||||||

|

Highway Usertax

|

|||||||||

| 3,025,000 |

5.500%, 11/15/18 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/AAA/AA+

|

3,043,785 | |||||||

| 1,200,000 |

5.000%, 11/15/22 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/AAA/AA+

|

1,319,448 | |||||||

| 1,260,000 |

5.000%, 11/15/23 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/AAA/AA+

|

1,385,420 | |||||||

| 4,545,000 |

5.125%, 11/15/26 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/AAA/AA+

|

4,571,270 | |||||||

| 1,000,000 |

5.000%, 11/15/29 Series A

|

||||||||

|

(pre-refunded)

|

Aa1/AAA/AA+

|

1,099,540 | |||||||

|

Oregon State Department Transportation

|

|||||||||

|

Highway Usertax, Senior Lien

|

|||||||||

| 1,865,000 |

5.000%, 11/15/23 Series A

|

Aa1/AAA/AA+

|

2,213,904 | ||||||

| 2,000,000 |

4.625%, 11/15/25 Series A

|

Aa1/AAA/AA+

|

2,301,080 | ||||||

| 3,540,000 |

4.625%, 11/15/26 Series A

|

Aa1/AAA/AA+

|

3,899,487 | ||||||

| 2,155,000 |

5.000%, 11/15/28 Series A

|

Aa1/AAA/AA+

|

2,458,683 | ||||||

| 1,000,000 |

5.000%, 11/15/24 Series N

|

Aa1/AAA/AA+

|

1,273,510 | ||||||

|

Tri-County Metropolitan Transportation

|

|||||||||

|

District, Oregon

|

|||||||||

| 1,775,000 |

5.000%, 09/01/16

|

Aa1/AAA/NR

|

1,807,465 | ||||||

| 1,010,000 |

5.000%, 09/01/24

|

Aa1/AAA/NR

|

1,275,994 | ||||||

|

Tri-County Metropolitan Transportation

|

|||||||||

|

District, Oregon Capital Grant Receipt

|

|||||||||

| 1,685,000 |

5.000%, 10/01/24 Series A

|

A1/A/NR

|

2,022,438 | ||||||

| 3,480,000 |

5.000%, 10/01/26 Series A

|

A1/A/NR

|

4,133,718 | ||||||

| 3,000,000 |

5.000%, 10/01/27 Series A

|

A1/A/NR

|

3,545,100 | ||||||

|

Total Transportation

|

37,130,294 | ||||||||

|

Water and Sewer (12.8%)

|

|||||||||

|

Ashland, Oregon Refunding

|

|||||||||

| 1,025,000 |

4.000%, 05/01/17 AGMC Insured

|

NR/AA-/NR

|

1,176,126 | ||||||

|

Klamath Falls, Oregon Water

|

|||||||||

| 1,575,000 |

5.500%, 07/01/16 AGMC Insured

|

Aa3/AA-/NR

|

1,723,034 | ||||||

19 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Water and Sewer (continued

|

|||||||||

|

Lane County, Oregon Metropolitan

|

|||||||||

|

Wastewater

|

|||||||||

| $ | 2,500,000 |

5.250%, 11/01/28

|

Aa2/AA/NR

|

$ | 2,876,250 | ||||

|

Portland, Oregon Sewer System,

|

|||||||||

|

Second Lien

|

|||||||||

| 3,005,000 |

5.000%, 03/01/28 Series A

|

Aa3/AA/NR

|

3,632,234 | ||||||

|

Portland Oregon Sewer System Revenue

|

|||||||||

|

Refunding Second Lien

|

|||||||||

| 5,000,000 |

5.000%, 06/15/33 Series B

|

Aa3/AA/NR

|

5,634,550 | ||||||

|

Portland, Oregon Sewer System

|

|||||||||

| 2,760,000 |

5.250%, 06/01/17 AGMC Insured

|

Aa3/AA/NR

|

2,847,906 | ||||||

| 4,595,000 |

5.000%, 06/01/17 AGMC Insured

|

Aa2/AA/NR

|

5,131,788 | ||||||

| 3,470,000 |

5.000%, 06/01/21 AGMC Insured

|

Aa3/AA/NR

|

3,562,371 | ||||||

| 4,410,000 |

5.000%, 06/15/25 NPFG Insured

|

Aa3/AA/NR

|

4,901,098 | ||||||

| 4,630,000 |

5.000%, 06/15/26 NPFG Insured

|

Aa3/AA/NR

|

5,133,374 | ||||||

| 1,610,000 |

5.000%, 06/15/27 NPFG Insured

|

Aa3/AA/NR

|

1,780,773 | ||||||

|

Portland, Oregon Water System

|

|||||||||

|

Revenue Refunding

|

|||||||||

| 1,920,000 |

4.000%, 05/01/14 Series A

|

Aaa/NR/NR

|

2,030,784 | ||||||

| 1,275,000 |

4.000%, 05/01/25 Series A

|

Aaa/NR/NR

|

1,432,475 | ||||||

|

Prineville, Oregon Refunding

|

|||||||||

| 1,255,000 |

4.400%, 06/01/29 AGMC Insured

|

NR/AA-/NR

|

1,428,102 | ||||||

|

Salem, Oregon Water & Sewer

|

|||||||||

| 1,000,000 |

5.375%, 06/01/15 AGMC Insured

|

Aa3/AA-/NR

|

1,121,340 | ||||||

|

Seaside, Oregon Wastewater System

|

|||||||||

| 1,000,000 |

4.250%, 07/01/26

|

A3/NR/NR

|

1,100,330 | ||||||

|

Sunrise Water Authority, Oregon

|

|||||||||

| 2,630,000 |

5.000%, 03/01/19 AGMC Insured

|

Aa3/AA-/NR

|

2,761,421 | ||||||

| 1,350,000 |

5.250%, 03/01/24 AGMC Insured

|

Aa3/AA-/NR

|

1,408,793 | ||||||

| 1,000,000 |

5.000%, 09/01/25 Syncora Guarantee,

|

||||||||

|

Inc.

|

NR/NR/NR*

|

1,044,810 | |||||||

|

Tigard, Oregon Water System Revenue

|

|||||||||

|

Refunding

|

|||||||||

| 2,025,000 |

4.000%, 08/01/21

|

A1/AA-/NR

|

2,342,339 | ||||||

| 1,105,000 |

5.000%, 08/01/24

|

A1/AA-/NR

|

1,382,620 | ||||||

|

Washington County, Oregon Clean

|

|||||||||

|

Water Services

|

|||||||||

| 2,235,000 |

5.250%, 10/01/15 NPFG Insured

|

Aa2/AA/NR

|

2,549,420 | ||||||

| 4,000,000 |

5.000%, 10/01/28

|

Aa2/AA/NR

|

4,621,400 | ||||||

20 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|||

|

SCHEDULE OF INVESTMENTS (continued)

|

|||

|

SEPTEMBER 30, 2012

|

|

Rating

|

|||||||||

|

Moody’s/S&P

|

|||||||||

|

Principal

|

and Fitch

|

||||||||

|

Amount

|

Revenue Bonds (continued)

|

(unaudited)

|

Value

|

||||||

|

Water and Sewer (continued

|

|||||||||

|

Washington County, Oregon Clean

|

|||||||||

|

Water Services Sewer Revenue

|

|||||||||

|

Senior Lien

|

|||||||||

| $ | 2,850,000 |

4.000%, 10/01/26 Series B

|

Aa2/AA/NR

|

$ | 3,194,879 | ||||

| 2,745,000 |

4.000%, 10/01/28 Series B

|

Aa2/AA/NR

|

3,037,507 | ||||||

|

Woodburn, Oregon Wastewater

|

|||||||||

|

Revenue Refunding

|

|||||||||

| 1,090,000 |

5.000%, 03/01/21 Series A

|

A2/NR/NR

|

1,300,087 | ||||||

|

Total Water and Sewer

|

69,155,811 | ||||||||

|

Total Revenue Bonds

|

267,294,743 | ||||||||

|

Total Investments (cost $487,051,513-

|

|||||||||

|

note 4)

|

98.6%

|

533,027,430 | |||||||

|

Other assets less liabilities

|

1.4

|

7,467,098 | |||||||

|

Net Assets

|

100.0%

|

$ | 540,494,528 | ||||||

| * |

Any security not rated (“NR”) by any of the Nationally Recognized Statistical Rating Organizations (“NRSRO” or “Credit Rating Agency”) has been determined by the Investment Sub-Adviser to have sufficient quality to be ranked in the top four credit ratings if a credit rating were to be assigned by a NRSRO.

|

||||||||

|

Percent of

|

||||

|

Portfolio Distribution by Quality Rating (unaudited)

|

Portfolio†

|

|||

|

Aaa of Moody’s or AAA of S&P

|

9.0 | % | ||

|

Pre-refunded bonds †† / Escrowed to Maturity bonds

|

6.9 | |||

|

Aa of Moody’s, AA of S&P or Fitch

|

62.4 | |||

|

A of Moody’s, S&P or Fitch

|

16.6 | |||

|

Baa of Moody’s or BBB of S&P

|

3.3 | |||

|

Not rated*

|

1.8 | |||

| 100.0 | % | |||

21 | Tax-Free Trust of Oregon

TAX-FREE TRUST OF OREGON

SCHEDULE OF INVESTMENTS (continued)

SEPTEMBER 30, 2012

| † | Where applicable, calculated using the highest rating of the three NRSROs. |

| †† | Pre-refunded bonds are bonds for which U.S. Government Obligations have been placed in escrow to retire the bonds at their earliest call date. |

|

PORTFOLIO ABBREVIATIONS:

|

|

|

AGC

|

Assured Guaranty Insurance

|

|

AGMC

|

Assured Guaranty Municipal Corp.

|

|

AMBAC

|

American Municipal Bond Assurance Corporation

|

|

ETM

|

Escrowed to Maturity

|

|

FGIC

|

Financial Guaranty Insurance Co.

|

|

NPFG

|

National Public Finance Guarantee

|

|

NR

|

Not Rated

|

See accompanying notes to financial statements.

22 | Tax-Free Trust of Oregon

|

TAX-FREE TRUST OF OREGON

|

|

STATEMENT OF ASSETS AND LIABILITIES