UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2017 | |

or | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For transition period from to | |

Commission file number 0-5734

AGILYSYS, INC.

(Exact name of registrant as specified in its charter)

Ohio | 34-0907152 |

State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification No.) |

425 Walnut Street, Suite 1800, Cincinnati, Ohio | 45202 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: (770) 810-7800

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Shares, without par value | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer þ Non-accelerated filer ¨ Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of Common Shares held by non-affiliates as of June 30, 2016 was $152,839,898.

As of May 24, 2017, 23,212,789 shares of the registrant's common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement to be used in connection with its 2017 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K.

AGILYSYS, INC.

Annual Report on Form 10-K

Year Ended March 31, 2017

Table of Contents

Page | ||

PART I | ||

ITEM 1. | Business | |

ITEM 1A. | Risk Factors | |

ITEM 1B. | Unresolved Staff Comments | |

ITEM 2. | Properties | |

ITEM 3. | Legal Proceedings | |

ITEM 4. | Mine Safety Disclosures | |

PART II | ||

ITEM 5. | Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities | |

ITEM 6. | Selected Financial Data | |

ITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

ITEM 7A. | Quantitative and Qualitative Disclosures about Market Risk | |

ITEM 8. | Financial Statements and Supplementary Data | |

ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

ITEM 9A. | Controls and Procedures | |

ITEM 9B. | Other Information | |

PART III | ||

ITEM 10. | Directors, Executive Officers and Corporate Governance | |

ITEM 11. | Executive Compensation | |

ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | |

ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | |

ITEM 14. | Principal Accountant Fees and Services | |

PART IV | ||

ITEM 15. | Exhibits and Financial Statement Schedules | |

SIGNATURES | ||

2

Forward Looking Information

This Annual Report and other publicly available documents, including the documents incorporated herein and therein by reference, contain, and our officers and representatives may from time to time make, "forward-looking statements" within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as: "anticipate," "intend," "plan," "goal," "seek," "believe," "project," "estimate," "expect," "strategy," "future," "likely," "may," "should," "will" and similar references to future periods. These statements are not guarantees of future performance and involve risks, uncertainties, and assumptions that are difficult to predict. These statements are based on management's current expectations, intentions, or beliefs and are subject to a number of factors, assumptions, and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. Factors that could cause or contribute to such differences or that might otherwise impact the business include the risk factors set forth in Item 1A of this Annual Report. We undertake no obligation to update any such factor or to publicly announce the results of any revisions to any forward-looking statements contained herein whether as a result of new information, future events, or otherwise.

3

Part I

Item 1. Business.

Overview

Agilysys is a leading technology company that provides innovative software for point-of-sale (POS), property management (PMS), inventory and procurement, workforce management, analytics, document management and mobile and wireless solutions and services to the hospitality industry. Our solutions and services allow property managers to better connect, interact and transact with their customers and enhance their customer relationships by streamlining operations, improving efficiency, increasing guest recruitment and wallet share, and enhancing the overall guest experience. We serve four major market sectors: Gaming, both corporate and tribal; Hotels, Resorts and Cruise; Foodservice Management; and Restaurants, Universities, Stadia and Healthcare. A significant portion of our consolidated revenue is derived from contract support, maintenance and subscription services.

Agilysys operates throughout North America, Europe and Asia, with corporate services located in Alpharetta, GA. For more information, visit www.agilysys.com.

The sales of our Retail Solutions Group (RSG) business and United Kingdom business entity (UK entity) each represented a disposal of a component of an entity. As such, the operating results of RSG and the UK entity have been reported as a component of discontinued operations in Item 6. Selected Financial Data, of this Annual Report, for the twelve months ended March 31, 2014 and March 31, 2013.

Our principal executive offices are located at 425 Walnut Street, Suite 1800, Cincinnati, Ohio, 45202 and our corporate services are located at 1000 Windward Concourse, Suite 250, Alpharetta, Georgia, 30005.

Reference herein to any particular year or quarter refers to periods within our fiscal year ended March 31. For example, fiscal 2017 refers to the fiscal year ended March 31, 2017.

History and Significant Events

Organized in 1963 as Pioneer-Standard Electronics, Inc., an Ohio corporation, we began operations as a distributor of electronic components and, later, enterprise computer solutions. Exiting the former in fiscal 2003 with the sale of our Industrial Electronic Division, we used the proceeds to reduce debt, fund growth of our enterprise solutions business and acquire businesses focused on higher-margin and more specialized solutions for the hospitality and retail industries. At the same time, we changed our name to Agilysys, Inc.

In fiscal 2004, we acquired Kyrus Corporation and became a provider of IBM retail solutions and services in the supermarket, chain drug, general retail, and hospitality segments. In that same year, the acquisition of Inter-American Data, Inc. allowed us to become the leading developer and provider of technology solutions for property and inventory management in the casino and resort industries.

In calendar 2007, we divested KeyLink Systems and exited the enterprise computer distribution business. We used the proceeds from that sale to return cash to shareholders and fund a number of acquisitions that broadened our solutions and capabilities portfolios. We acquired InfoGenesis and Visual One Systems Corp. in calendar 2007, significantly expanding our specialized offerings to the hospitality industry through enterprise-class, POS and software solutions tailored for a variety of applications in cruise, golf, spa, gaming, lodging, resort, and catering. These offerings feature highly intuitive, secure and robust solutions, easily scalable across multiple departments or property locations. In fiscal 2008, we began reporting three primary operating segments: Hospitality Solutions Group (HSG), Retail Solutions Group (RSG) and Technology Solutions Group (TSG).

In fiscal 2012, we sold our TSG segment and restructured our business model to focus on higher-margin, profitable growth opportunities in the hospitality and retail sectors. We also reduced our real-estate footprint and lowered overhead costs by relocating corporate services from Solon, Ohio to Alpharetta, Georgia, thus moving our senior management team closer to our operating units.

On July 3, 2014 we purchased certain assets from Dining Ventures, Inc. The acquired assets are the base for our rGuest® Seat product, a dining reservations and table management application.

4

On July 1, 2013, we completed the sale of our RSG business to Kyrus Solutions, Inc. (Kyrus), an affiliate of Clearlake Capital Group, L.P. Following completion of the transaction, our business focused exclusively on hospitality solutions and the growth opportunities in the hospitality market.

On March 31, 2014, we completed the sale of our United Kingdom business entity (UK entity) to Verteda Limited (Verteda), led by the Company’s former European management team. In connection with the sale, we have entered into a multi-year distribution agreement, whereby Verteda distributes certain Agilysys products within the U.K. marketplace. We continue to manage all property management system accounts as well as key global accounts in the EMEA market.

Today, we are focused on providing state-of-the-art, end-to-end solutions that enhance guest experiences and allow our customers to promote their respective brands. We help our customers win the guest recruitment battle and, in turn, grow revenue, reduce costs and increase efficiency. This is accomplished by developing and deploying intuitive solutions that increase speed and accuracy, thereby enabling more effective management, intelligent upselling, reduced shrinkage, improved brand recognition and better control of the customer relationship. Our strategy is to increase the proportion of revenue we derive from ongoing support and maintenance agreements, software as a subscription services, cloud applications and professional services.

Products, Support and Professional Services

We are a leading developer and marketer of software enabled solutions and services to the hospitality industry, including: hardware and software products; support, maintenance and subscription services; and, professional services. Areas of specialization are point-of-sale, property management, inventory and procurement, workforce management, and mobile and wireless solutions designed to streamline operations, improve efficiency and enhance the guest experience.

We present revenue and costs of goods sold in three categories:

• | Products (hardware and software) |

• | Support, maintenance and subscription services |

• | Professional services |

Total revenue from continuing operations for these three specific areas is as follows:

Year ended March 31, | |||||||||

(In thousands) | 2017 | 2016 | 2015 | ||||||

Products | $ | 38,339 | $ | 41,445 | $ | 31,846 | |||

Support, maintenance and subscription services | 63,308 | 60,104 | 56,013 | ||||||

Professional services | 26,031 | 18,817 | 15,655 | ||||||

Total | $ | 127,678 | $ | 120,366 | $ | 103,514 | |||

Products:

The hospitality industry has long been focused on operating an end-to-end business, but the technology vendors that serviced the industry have been focused on product-centric solutions that make use of a high number of software modules and operating silos. We have evolved our approach to the industry to an integrated "platform" centric solutions for Lodging, Food & Beverage and Payments applications that looks to leverage the entire business, by investing in the development of a web services oriented architecture enterprise platform. Our rGuest™ platform is aimed at transitioning our product and services offerings to better address the needs of hospitality operators as they focus on building better connections with guests, pre-, during and post-visit. The rGuest platform facilitates an end-to-end solution that helps our customers improve guest services, increase top-line performance and reduce operating costs, which leads to opportunities for higher profitability. Our next-generation of products and services are aimed at helping hospitality operators recruit customers into their facilities, increase their wallet share from each customer and improve the overall guest experience from the initial customer touch point through the post-visit experience.

5

Our proprietary product suite is comprised of:

The rGuest platform underlies our industry leading hospitality solutions that are being introduced to operators of all sizes and with varying needs. The rGuest platform is designed to run as a Software as a Service (“SaaS”)-based platform on the public cloud, private cloud, on-premise, or in a hybrid configuration where the infrastructure may be above premise but the data resides on premise. rGuest’s architecture seamlessly functions as well for a multi-property customer as it does for a single property.

The rGuest enterprise platform helps operators more efficiently manage their business and grow their sales by:

• | Identifying and tracking guest profile and behavior so that it may be used to create effective loyalty programs and the right promotions and offers to ensure the best guest experience while ensuring the property extracts the maximum wallet share from each customer; |

• | Enabling historical analysis of data; |

• | Allowing for real-time management through mobile and web interfaces for immediate remediation of business and guest related issues; |

• | Creating a framework for core services for the delivery of business applications faster with the critical benefit of having fewer moving parts to manage; |

• | Ensuring that all new rGuest modules will be written on top of the rGuest platform to create a common look/feel, functions and usage paradigms and reduce the overhead of managing and learning multiple systems; |

• | Providing for easy integration with other hospitality management systems; and, |

• | Incorporating key infrastructure design elements such as global and multi-language support, regulatory compliance and security, including authentication, authorization, encryption, tokenization, handling of payment & PII information and overall application data and user security. |

Our rGuest product suite is designed to maximize the insight and value available in “big data” by:

• | Identifying the right data and determining how to best use it; |

• | Empowering users to be capable of both working with new technologies and of interpreting the data to find meaningful business insights; |

• | Creating data access and connectivity across the majority of guest touch points; |

• | Providing an IT platform that can adapt to changes in the landscape in an efficient manner; |

• | Working across functions' organizational challenges and finding ways of collaborating across functions and businesses; and, |

• | Implementing the highest levels of security to ensure data protection. |

The rGuest platform currently includes the following in-market solutions:

rGuest® Stay is the company’s groundbreaking cloud-based property management system and hospitality platform that optimizes operational efficiency, increases revenue and enhances guest service. rGuest Stay is currently generally available for limited service at select service hotels and chains.

The guest-centric PMS leverages a standards-based solution on an open architecture with public APIs to enable richly integrated applications delivered from Agilysys, its partners and customers. rGuest Stay offers powerful capabilities for multi-property operations. Managers can view guest profiles, history and reservations, as well as room availability and operational reports, seamlessly across multiple properties.

Focused on improving revenue and streamlining operations, rGuest Stay is designed to enable hotels to gather and analyze guest information that can be used to create loyalty-generating offers and increase guest wallet share. In addition, running natively in a browser on both desktop and tablet devices, it delivers real-time operating metrics so that hotels can more accurately forecast demand and scale guest services accordingly.

To help improve property operations, rGuest Stay offers a next-generation housekeeping optimization engine built using the included rGuest workflow engine that assigns staff resources to balance guest needs and operational efficiency. In addition, its intuitive user interface and online help functionality reduce team training time and ensure superior guest service with rapid solution ROI.

6

rGuest Buy is an enterprise-class self-service, customer-facing point of sale solution for the hospitality industry. It is ideal for food & beverage venues such as Grab N Go, corporate cafeterias and food courts. It includes self-service “order and pay” kiosks, and kitchen workflow management systems. rGuest Buy is currently deployed at more than 25 customer sites across the country, including corporate cafeterias at a top five U.S. bank, a top 40 U.S. law firm, one of the nation's largest technology manufacturers, and at a national financial services firm.

rGuest Buy’s intuitive customer-facing order and pay experiences transfer the control and convenience to the end user. The self-service components reduce on-site labor needed to manage venue operations, while improving customer throughput, check size, order accuracy, customer experience and satisfaction. The platform-driven and cloud-based solution allows for easy deployments and management at scale resulting in a lowered overall cost of ownership.

rGuest Buy offers:

• | Extensibility & partner ecosystem: The technology architecture allows for rich data integrations for all Agilysys products (InfoGenesis, rGuest Pay, rGuest Analyze, etc.), as well as easy integrations for a partner development ecosystem, and customer applications. |

• | “Self-managed” Cloud Solution: Fully managed cloud solution pushes latest releases, patches and features automatically to all rGuest Buy devices at the property. This ensures quicker support turn-around times, zero on-site IT resources for maintenance, robust security and uptimes. |

• | “Always on” Business - No offline interruptions: rGuest Buy offers “always-on” customer experience with robust network tolerance and offline capabilities. |

• | Manage at Scale: rGuest Buy allows to map a complex business structure in an intuitive way to support propagation of brands, concepts, and other policies. |

• | Reduce Risk - PCI validated payment platform: rGuest Buy integrates with rGuest Pay, our secure payment platform. Protect brand value and avoid liability with our encrypted card data solution. Safeguard against fraud and chargebacks by implementing EMV solutions, and protect application data via SSL. |

rGuest Pay is our innovative payments gateway. rGuest Pay protects guests’ financial data and reduces risk by leveraging point-to-point encryption (P2PE) and tokenization with every credit card transaction. rGuest Pay Gateway leverages one of the first payment gateways in the world to receive official PCI-P2PE validation, allowing us to offer PCI cost and scope reduction that other providers cannot. These security benefits are built on top of a full-featured, enterprise-grade gateway that offers broad support for U.S. credit card processors and a wide variety of payment device options for every use-case, including countertop, pay-at-table, EMV, mobile tablet, and signature capture scenarios.

rGuest Pay offers:

• | A full suite of credit card processing services |

• | Industry-leading payment security through tokenization and P2PE |

• | Flexible hardware supporting EMV and NFC contactless transactions |

• | Integration with 3rd Party POS/PMS applications through a simple-to-use API |

• | Consolidated transaction reporting |

• | Comprehensive payment processor support |

7

rGuest Seat is a guest centric table, reservation and wait list management solution that helps restaurants increase revenue by retaining repeat customers and providing a superior guest experience. Online dining reservations enable restaurants to increase bookings by allowing diners to reserve a table through the restaurant’s website or mobile app. Wait list management optimizes the restaurant’s use of tables and resources, helping staff estimate wait times more accurately and avoiding lost or dissatisfied customers.

rGuest Seat offers:

• | Streamlined online reservations increase guest bookings without tying staff up on the phone |

• | Wait list automation to accurately predict wait times and meet guest expectations |

• | Two-way text communications with waiting guests |

• | Toggle between restaurants within peer group to get a complete view of the reservation or wait list status |

• | Accessibility of guest data based on their previous dining experiences to provide a much higher level of guest service |

• | Library of reconfigurable reports can be accessed in real time or received through email at a scheduled delivery time |

• | Integration with InfoGenesis allows the POS system to be automatically updated with guest data for a more personalized dining experience |

• | Real-time table status is relayed between rGuest Seat and InfoGenesis (POS) to help maximize table turns and keep restaurant operations and reservations running smoothly |

rGuest Analyze is a platform-based subscription data analysis service focused on the needs of the hospitality industry. It is a full business intelligence solution that is delivered through the cloud (SaaS). rGuest Analyze collects data from Agilysys point of sale and property management solutions and helps food & beverage and property operators gain critical insight into business operations and performance. Out-of-the-box analysis helps hospitality operators manage costs, minimize loss due to fraud, boost item sales, increase server productivity, occupancy, room revenue, and other profit enhancing capabilities.

rGuest Analyze offers:

• | Cross-enterprise and centralized reporting across sites, venues and profit centers |

• | Slice-and-dice reporting without the need for IT/DBA resources immediately drives insight into food & beverage as well as lodging operations |

• | Out-of-the-box customizable reports provide insight into sales, revenue, server/cashier activity, discounts, tenders, ADR, RevPAR, and Occupancy |

• | Easy to learn, web-based reporting tool with simple drag-and-drop capabilities for fast data exploration and report generation |

• | Design, publish and disseminate executive level dashboards as easily as creating a word document with both web and mobile views |

Going forward, Agilysys plans to introduce additional functionality and modules for the rGuest platform.

Agilysys’ additional well established offerings for point-of-sale, property management, inventory procurement, workforce management, document management and activity booking product and services include:

Point-of Sale

• |  |

Agilysys InfoGenesis®™ POS is award-winning point-of-sale software that combines powerful reporting and configuration capabilities in the back office with a fast, intuitive and easy-to-use terminal application. The flexible system is easy to set up, and its scalable architecture enables customers to add workstations without having to build out expensive infrastructure. The system's detailed and high-quality reporting capabilities give insight into sales data and guest purchasing trends. Other features include packages and prix fixe menus, signature capture and multi-language capability. InfoGenesis POS is available as an on-premise solution or through a subscription service.

• | |

Agilysys InfoGenesis Flex is a mobility solution that offers full POS functionality on a Windows tablet. It provides a sleek, modern alternative to traditional POS installations and can be used as a slim fixed terminal or as a convertible simply by removing the tablet from its base.

8

• |  |

Agilysys eCash takes traditional cashless payment and stored value card capabilities and integrates them directly with InfoGenesis POS, increasing consumers' payment options.

All POS products are available through traditional software licensing or via subscription.

Property Management Systems (“PMS”)

• |  |

Agilysys Lodging Management System® (LMS) is an on-premises, web-enabled PMS solution targeting the Casino/Gaming segment (also offered as a hosted solution). It runs 24/7 to automate every aspect of hotel operations in properties of 1,000 rooms or more, and has interfaces to all core casino management systems. Its foundation expands to incorporate modules for sales and catering, activities scheduling, attraction ticketing and more.

• |  |

Agilysys Visual One™ PMS is installed in hotels and resorts ranging from 50-1,500 rooms. It is a complete PMS solution enabling the resort to run its end-to-end operations, including Front Desk, House Keeping, Sales & Catering, Maintenance, Accounting, SPA, Golf and Activities. For complex resorts that require an enterprise-wide system, Visual One provides an integrated solution with interfaces to leading global distribution systems (GDSs) and our other products.

• | Agilysys Insight™ Mobile Manager is a mobile dashboard application that enables hotel managers to quickly view key property information - including arrivals and departures, VIPs, total guests, housekeeping, revenue and groups - from a mobile device. It is supported by iPad®, iPad mini and iPhone® mobile devices and integrates fully with the Agilysys LMS property management solution. |

Inventory and Procurement

• |  |

Agilysys Eatec® provides core purchasing, inventory, recipe, forecasting, production and sales analysis functions and is unique in offering catering, restaurant, buffet management and nutrition modules in a single web-enabled solution.

• | |

Agilysys EatecTouch is an optional software applet that operates on any MicroSoft®Windows®-based POS terminal, providing users with access to the Eatec application from any terminal location.

• | |

Agilysys EatecPocket is a Microsoft Windows Mobile compatible application designed to work on a handheld wireless device, enabling users to perform inventory transactions. The software incorporates barcode scanner functionality for mobile updates of the database.

• |  |

Agilysys Stratton Warren System (SWS) integrates with all leading financial and POS software products. The software manages the entire procurement process via e-commerce, from business development to the management of enterprise-wide backend systems and daily operations.

• | |

Agilysys SWS Direct is an add-on module for SWS that provides a convenient, efficient and intuitive shopping cart experience to SWS users. SWS Direct streamlines operations, provides enhanced bidding and request for pricing services, and offers supplier registration tools and self-service maintenance capabilities.

Eatec and Stratton Warren System solutions are available through traditional software licensing or via subscription.

9

Document Management

• |  |

Agilysys DataMagine™ is a U.S.-patented imaging module and archiving solution that allows users to securely capture and retrieve documents and system-generated information. DataMagine integrates with our products, adding functionality and increasing benefit to customers.

Activities

• |  |

Agilysys GolfPro is a module that offers golf property managers complete pro shop management with tee time scheduling, member profile/billing, tournament management and Web and e-mail access bundled into one solution.

• | |

Agilysys Spa Management software covers all aspects of running a spa business, from scheduling guests for services to managing staff schedules. The software also integrates with our PMS solutions.

• | |

Agilysys LMS ARTS® interfaces with hotel guest data, allowing reservationists to pre-plan activities when booking a guest's room. The application also places canceled activities back into inventory for resale, resulting in optimum property utilization and profitability.

• | |

Agilysys Visual One Activities software streamlines the management of all of the amenities and activities a property has to offer. Staff can easily schedule and personalize reservations for guests; activities then appear on itinerary/confirmations.

Products revenue also includes remarketed hardware and proprietary and remarketed software that is deployed as an integral component of the solutions we provide.

Support, Maintenance and Subscription Services: Contracted technical support, maintenance and subscription services are a significant portion of our consolidated revenue and typically generate higher profit margins than products revenue. Growth has been driven by a strategic focus on developing and promoting these offerings while market demand for maintenance services and updates that enhance reliability, as well as the desire for flexibility in purchasing options, continue to reinforce this trend. Our commitment to exceptional service has enabled us to become a trusted partner with customers who wish to optimize the level of service they provide to their guests and maximize commerce opportunities both on- and off-premise.

Professional Services: We have industry-leading expertise in designing, implementing, integrating and installing customized solutions into both traditional and newly created platforms. For existing enterprises, we seamlessly integrate new systems and for start-ups and fast-growing customers, we become a partner that can manage large-scale rollouts and tight construction schedules. Our extensive experience ranges from staging equipment to phased rollouts as well as training staff to provide operational expertise to help achieve maximum effectiveness and efficiencies in a manner that saves our customers time and money. In addition to our hosted solutions for InfoGenesis, Stratton Warren Systems and Eatec, Agilysys has recently added the ability to migrate on premise property lodging data to the LMS® or Visual One Property Management System hosted solution.

10

Representative Agilysys clients include:

AVI Foodsystems, Inc. | The Cosmopolitan of Las Vegas | Prairie Band Casino & Resort |

Banner Health | CSU Fullerton Auxiliary Services Corporation | Resorts World Bimini |

Benchmarc Restaurants | Drury Hotels | Rosen Hotels & Resorts |

Black Rock Resort | Farmers Restaurant Group | Royal Caribbean International |

Boyd Gaming Corporation | Golden Nugget Lake Charles | Royal Lahaina Resort |

BR Guest Hospitality | Grand Sierra Resort and Casino | Sands Casino Resort Bethlehem |

The Breakers Palm Beach | Harbor Winds Hotel | SAVOR |

The Broadmoor's Ranch at Emerald Valley | Hialeah Park | Spooky Nook Sports |

Caesars Entertainment | Hilton Worldwide | Sugar Factory |

Cal Dining at UC Berkeley | Ho-Chunk Gaming | SUNY Cobleskill |

Camelback Lodge & Waterpark | Maryland Live! Casino | The Venetian Resort Hotel Casino |

Casa Ybel Resort | Norwegian Cruise Line | University of Akron |

Casino del Sol Resort | Oxford Casino | Vail Resorts |

Compass Group North America | Palm Garden Hotel | Valley View Casino & Hotel |

Comanche Nation of Oklahoma | Pinehurst Resort | Vanderbilt University |

Copper Mountain | Pinnacle Entertainment | Yale University |

Industry and Markets

We offer innovative point-of-sale, property management, inventory and procurement, workforce management, analytics, document management and mobile and wireless solutions and services for customers of varying sizes in the hospitality industry. We serve

four major market sectors: Gaming, both corporate and tribal; Hotels, Resorts and Cruise; Foodservice Management; and Restaurants, Universities, Stadia and Healthcare.

The hospitality industry encompasses a wide variety of market sectors and customers. We operate throughout North America, Europe and Asia, with corporate services located in Alpharetta, GA. Sales to customers outside of the United States represent approximately 6% of total sales.

The hospitality industry is highly fragmented and composed of a number of defined markets including lodging, casinos, cruise ships, resorts and spas, franchise operators, restaurant chains, stadiums, and arenas, among others. For example, in the lodging segment, no single hotel brand accounts for more than 4% of all hotel rooms in the United States. According to STR Global, the U.S. lodging industry generated approximately $189.5 billion in lodging revenue in calendar 2015, a 7.2% increase over 2014, while PwC's, Hospitality Directions US 2017, reports an average of approximately 65.5% of approximately 5.0 million available rooms occupied in 2016 at an average daily rate (ADR) of $124.01. This compares with 65.4% in 2015 at an ADR of $120.31.

The hospitality business is sensitive to the strength of domestic and global economic and credit conditions. Business and destination resort travel are highly correlated with the economic conditions in their respective markets. Competition is intense for consumer spending, and hospitality industry participants are seeking ways to increase their visibility and appeal as well as enhance the experience of their guests. In its 2017 Travel and Hospitality Industry Outlook, Deloitte observed that travel companies should leverage an increased awareness of customer expectations, re-imagined technology strategy, and differentiated offerings to provide unmatched travel experiences. Our products and solutions are meant to leverage the opportunity these challenges create by providing our customers with a higher degree of guest connectivity and added engagement tools that will enable them to better capitalize on their brand equity, and more profitably manage their operations, and grow their business. In addition to product solutions that are designed and customized to meet unique facility or multi-facility needs, we also provide an array of support and subscription options geared towards maintaining systems and professional services for implementation and rollouts.

We have a significant customer base in the commercial casino and gaming sector. According to CPA firm Rubin Brown's Gaming Services Group, US Gaming industry annual revenues surpassed $73 billion in 2016, as compared to approximately $71 billion in 2015. Amenities in contemporary casinos extend well beyond gaming to include a variety of entertainment and leisure options as well as modern convention centers and meeting facilities to attract the corporate market. International gaming markets are growing rapidly both in size and new jurisdictions. Asian gaming markets continue to generate robust growth. Gross gaming revenue in Macau exceeds that of the Las Vegas Strip, with a number of the current and planned properties in the region operated by U.S.-based companies. As the market share leader in providing PMS systems to casinos on the Las Vegas Strip, we are well positioned to benefit from these strong and long-standing relationships as our customer base expands into international markets. Additionally, as gaming operators

11

migrate toward cashless operations, optimization of non-gaming spend and digital track-and-log of unique guest behavior, we are able to provide the requisite technologies and expertise to satisfy their needs.

We also have expertise in serving the unique needs of Cruise ship operators. Guests and potential customers are expecting an experience that reflects their unique tastes, preferences and travel habits and cruise operators have seen the need to adequately support the increasing level of personalization and detail required to capture the highest level of guest satisfaction. Our products and services are designed to best help them deliver on this critical part of their business. According to the Cruise Lines International Association and Cruise Market Watch 2017, cruise lines continued the growth trends of recent years in 2016. The worldwide cruise ship fleet currently stands at 448 ships and the current order book for 2016 includes 26 new builds, with 97 new ships to be delivered by 2026. The industry carried an estimated 24.2 million passengers in 2016, up from nearly 23.2 million passengers in 2015.

Customers

Our customers include large, medium-sized and boutique companies, both owned and franchised, as well as divisions or departments of large corporations in the hospitality industry. We concentrate on serving the needs of customers in a range of customer-focused settings where brand differentiation is important, particularly in the lodging, casino, destination resort, cruise line, foodservice industries where competition for guest recruitment is intense. Our current customer base is highly fragmented, with the exception of one customer representing approximately 10% of consolidated revenue from continuing operations for the period ended March 31, 2017.

Seasonality

We have traditionally experienced seasonal revenue weakness during our fiscal first quarter ending June 30. Additionally, the timing of large one-time orders, such as those associated with significant remarketed product sales around large customer refresh cycles or significant volume rollouts, occasionally creates volatility in our quarterly results.

Competition

Our solutions face a highly competitive market. Competition exists with respect to developing and maintaining relationships with customers, pricing for products and solutions, and customer support and service.

We compete with other full-service providers that sell and service bundled POS and PMS solutions comprised of hardware, software, support and services. These companies, some of which are much larger than we are, include Oracle Corp., NCR, Constellation Software, Inc. and Infor. We also compete with software companies like IDeaS Revenue Solutions, POSitouch, Northwind and Xpient Solutions. In addition, we compete with PMS systems that are designed and maintained in-house by large hotel chains.

Environmental Matters

We believe we are in compliance in all material respects with all applicable environmental laws. Presently, we do not anticipate that such compliance will have a material effect on capital expenditures, earnings or competitive position with respect to any of our operations.

Employees

As of May 24, 2017, we had 596 employees. We are not a party to any collective bargaining agreements, have had no strikes or work stoppages and consider our employee relations to be good.

Access to Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports are available free of charge through our corporate website, http://www.agilysys.com, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (SEC). The information posted on our website is not incorporated into this Annual Report on Form 10-K (Annual Report). Reports, proxy and information statements, and other information regarding issuers that file electronically, are maintained on the SEC website, http://www.sec.gov.

12

Item 1A. Risk Factors.

Risks Relating to Our Business

Our future success will depend on our ability to develop new products, product upgrades and services that achieve market acceptance.

Our business is characterized by rapid and continual changes in technology and evolving industry standards. We believe that in order to remain competitive in the future we will need to continue to develop new products, product upgrades and services, requiring the investment of significant financial resources. If we fail to accurately anticipate our customer's needs and technological trends, or are otherwise unable to complete the development of a product or product upgrade on a timely basis, we will be unable to introduce new products or product upgrades into the market on a timely basis, if at all, and our business and operating results would be materially and adversely affected.

The development process for most new products and product upgrades is complicated, involves a significant commitment of time and resources and is subject to a number of risks and challenges including:

• | Managing the length of the development cycle for new products and product enhancements, which has frequently been longer than we originally expected; |

• | Adapting to emerging and evolving industry standards and to technological developments by our competitors and customers; and |

• | Extending the operation of our products and services to new and evolving platforms, operating systems and hardware products, such as mobile devices. |

If we are not successful in managing these risks and challenges, or if our new products, product upgrades, and services are not technologically competitive or do not achieve market acceptance, our business and operating results could be adversely affected.

If we fail to meet our customers' performance expectations, our reputation may be harmed, and we may be exposed to legal liability.

Our ability to attract and retain customers depends to a large extent on our relationships with our customers and our reputation for high quality professional services and integrity. As a result, if a customer is not satisfied with our services or solutions, our reputation may be damaged. Moreover, if we fail to meet our clients' performance expectations, we may lose clients and be subject to legal liability, particularly if such failure adversely impacts our clients' businesses.

In addition, many of our projects are critical to the operations of our customers' businesses. While our contracts typically include provisions designed to limit our exposure to legal claims relating to our products and services, these provisions may not adequately protect us or may not be enforceable in all cases. The general liability insurance coverage that we maintain, including coverage for errors and omissions, is subject to important exclusions and limitations. We cannot be certain that this coverage will continue to be available on reasonable terms or will be available in sufficient amounts to cover one or more large claims, or that the insurer will not disclaim coverage as to any future claim. A successful assertion of one or more large claims against us that exceeds our available insurance coverage or changes in our insurance policies, including premium increases or the imposition of large deductible or co-insurance requirements, could adversely affect our profitability.

We face extensive competition in the markets in which we operate, and our failure to compete effectively could result in price reductions and/or decreased demand for our products and services.

Several companies offer products and services similar to ours. The rapid rate of technological change in the hospitality market makes it likely we will face competition from new products designed by companies not currently competing with us. We believe our competitive ability depends on our product offerings, our experience in the hospitality industry, our product development and systems integration capability, and our customer service organization. There is no assurance, however, that we will be able to compete effectively in the hospitality technology market in the future.

13

We compete for customers based on several factors, including price. In some cases, we may have to reduce our pricing to obtain business. If we are not able to maintain favorable pricing for our products and services, our profit margin and our profitability could suffer.

Actual or perceived security vulnerabilities in our software products may result in reduced sales or liabilities.

Our software may be used in connection with processing sensitive data (e.g., credit card numbers). It may be possible for the data to be compromised if our customer does not maintain appropriate security procedures. In those instances, the customer may attempt to seek damages from us. While we believe that all of our current software complies with applicable industry security requirements and that we take appropriate security measures to reduce the possibility of breach through our support and other systems, we cannot assure that our customers' systems will not be breached, or that all unauthorized access can be prevented. If a customer, or other person, seeks redress from us as a result of a security breach, our business could be adversely affected.

Cloud-based platform and software applications presents increased security risks.

As we expand our cloud-based platform and software hosting capabilities, including our rGuest products, and offer more of our software applications to our customers on a cloud-based basis, our responsibility for data and system security with respect to data held in our hosting centers increases significantly. While we believe that our current platform, software applications and data centers comply with applicable laws and industry security requirements, and while we believe that we use appropriate security measures to reduce the possibility of unauthorized access or misuse of data in the data centers, we cannot provide absolute assurance that our cloud-based applications will not be breached, or that all unauthorized access can be prevented. If a security breach were to occur, a customer, regulatory agency, or other person could seek redress from us, which could adversely affect our business.

If we fail to attract and retain key employees, our business may be harmed.

Our success depends on the skill, experience and dedication of our employees. If we are unable to attract and retain sufficiently experienced and capable personnel, especially in product development, customer services and support, operations, sales and management, our business and financial results may suffer. For example, if we are unable to attract and retain a sufficient number of skilled technical personnel, our ability to develop high quality products and provide high quality customer service may be impaired. Experienced and capable personnel in the technology industry remain in high demand, and there is continual competition for their talents. When talented employees leave, we may have difficulty replacing them, and our business may suffer. There can be no assurance that we will be able to successfully attract and retain the personnel that we need.

We may incur goodwill, intangible asset and capitalized software development impairment charges that adversely affect our operating results.

As of March 31, 2017 we had $19.6 million, $8.5 million, and $47.0 million of goodwill, intangible assets, net, and software development costs, net, respectively, on our consolidated balance sheet. We review our goodwill, intangible assets and capitalized software development costs for impairment on at least an annual basis. Our future operating results and the market price of our common stock could be materially adversely affected if we are required to write down the carrying value of goodwill, intangible assets or capitalized software development in the future.

We may be subject to claims of infringement of third-party intellectual property rights.

While we do not believe that our products and services infringe any patents or other intellectual property rights, from time to time, we receive claims that we have infringed the intellectual property rights of others. On April 6, 2012, Ameranth, Inc. filed a complaint against us for patent infringement in the United States District Court for the Southern District of California alleging that point-of-sale and property management and other hospitality information technology products sold by us infringe patents owned by Ameranth. This lawsuit remains pending.

This lawsuit and any other such claim, with or without merit, could result in costly litigation and distract management from day-to-day operations. If we are found liable, we could be obligated to pay significant damages or enter into license agreements.

We may not be able to enforce or protect our intellectual property rights.

We rely on a combination of copyright, patent, trademark and trade secret laws and restrictions on disclosure to protect our intellectual property rights. We cannot be certain that the steps we have taken will prevent unauthorized use of our technology. Any failure to protect our intellectual property rights would diminish or eliminate the competitive advantages that we derive from our proprietary technology.

14

We are subject to litigation, which may be costly.

As a company that does business with many customers, employees and suppliers, we are subject to litigation. The results of such litigation are difficult to predict, and we may incur significant legal expenses if any such claim were filed. While we generally take steps to reduce the likelihood that disputes will result in litigation, litigation is very commonplace and could have an adverse effect on our business.

Our cloud-based solutions present execution and competitive risks.

Our solutions offered in the cloud accessible via the web without present new and difficult technology challenges. These offerings depend on integration of third-party hardware, software and cloud hosting vendors working together with our products. As a result, we may be subject to claims if customers experience service disruptions, breaches or other quality issues related to our cloud-based solutions.

Continuing challenging global economic conditions could adversely affect our business and financial results.

Global economic conditions continue to be challenging. Our revenue and profitability depend significantly on general economic conditions and the level of capital available to our customers. Our business trends and revenue growth continue to be affected by the challenging economic climate. These difficult economic conditions and the uncertainty about future economic conditions may adversely affect our customers' level of spending, ability to obtain financing for purchases, ability to make timely payments to us and adoption of new technologies, which could require us to increase our allowance for doubtful accounts, negatively impact our days sales outstanding, lead to increased price competition and adversely affect our results of operations.

Our dependence on certain strategic partners makes us vulnerable to the extent we rely on them.

We rely on a concentrated number of vendors for the majority of our hardware and for certain software and related services needs. We do not have long term agreements with many of these vendors. If we can no longer obtain these hardware, software or services needs from our major suppliers due to mergers, acquisitions or consolidation within the marketplace, material changes in their partner programs, their refusal to continue to supply to us on reasonable terms or at all, and we cannot find suitable replacement suppliers, it may have a material adverse impact on our future operating results and gross margins.

If we fail to maintain an effective system of internal controls, we may not be able to detect fraud, which could have a material adverse effect on our business.

While we believe our internal control over financial reporting is effective, a controls system cannot provide absolute assurance that the objectives of the controls system are met, and no evaluation of controls can provide absolute assurance that control issues and instances of fraud, if any, within our company have been detected.

We have encountered risks associated with maintaining large cash balances.

While we have attempted to invest our cash balances in investments generally considered to be relatively safe, we nevertheless confront credit and liquidity risks. Bank failures could result in reduced liquidity or the actual loss of money held in deposit accounts in excess of federally insured amounts, if any.

We may have exposure to greater than anticipated tax liabilities.

Some of our products and services may be subject to sales taxes in states where we have not collected and remitted such taxes from our customers. We have reserves for certain state sales tax contingencies based on the likelihood of obligation. These contingencies are included in “Accrued liabilities” in our Consolidated Balance Sheets. We believe we have appropriately accrued for these contingencies. In the event that actual results differ from these reserves, we may need to make adjustments, which could materially impact our financial condition and results of operations.

If we acquire new businesses, we may not be able to successfully integrate them or attain the anticipated benefits.

As part of our operating history and growth strategy, we have acquired other businesses. In the future, we may continue to seek acquisitions. We can provide no assurance that we will be able to identify and acquire targeted businesses or obtain financing for such acquisitions on satisfactory terms. The process of integrating acquired businesses into our operations may result in unforeseen difficulties and may require a disproportionate amount of resources and management attention. If integration of our acquired businesses is not successful, we may not realize the potential benefits of an acquisition or suffer other adverse effects.

15

Risks Relating to the Industries We Serve

Our business depends to a significant degree on the hospitality industry and a weakening could adversely affect our business and results of operations.

Because our customer base is concentrated in the hospitality industry, our business is largely dependent on the health of that industry. Our sales are dependent in large part on the health of the hospitality industry, which in turn is dependent on the domestic and international economy. Instabilities or downturns in the hospitality industry could disproportionately impact our revenue, as clients may exit the industry or delay, cancel or reduce planned expenditures for our products. A general downturn in the hospitality industry could disproportionately impact our revenue, as clients may exit the industry or delay, cancel or reduce planned expenditures for our products.

Higher oil and gas prices worldwide could have a material adverse impact on the hospitality industry, and indirectly, on our business.

Material increases in oil and gas prices tend to reduce discretionary spending by consumers, such as on travel and dining, as well as on retail spending generally. Reductions in discretionary spending by consumers adversely affects our customers and, indirectly, our business. Moreover, increases in oil and gas prices also directly adversely affects our customer base in other ways. For example, oil and gas price increases can result in higher ingredient and food costs for our restaurant customers.

Consolidation in the hospitality industry could adversely affect our business.

Customers that we serve may seek to achieve economies of scale and other synergies by combining with or acquiring other companies. The hospitality industry has experienced recent consolidations, including the hotel and casino sectors of the industry. Although recent consolidations in the hospitality industry have not materially adversely affected our business, there is no assurance that future consolidations will not have such affect. For example, if one of our current customers merges or consolidates with a company that relies on another provider's products or services, it could decide to reduce or cease its purchases of products or services from us, which could have an adverse effect our business.

Risks Relating to Our Stock

Our stock has been volatile and we expect that it will continue to be volatile.

Our stock price has been volatile, and we expect it will continue to be volatile. For example, during the year ended March 31, 2017, the trading price of our common stock ranged from a high of $11.76 to a low of $8.78. The volatility of our stock price may be due to factors other than those specific to our business, such as economic news or other events generally affecting the trading markets. Additionally, our ownership base has been and may continue to be concentrated in a few shareholders, which could increase the volatility of our common share price over time.

Our largest shareholder, MAK Capital, currently holds approximately 31% of our common shares, which could impact corporate policy and strategy, and MAK Capital's interests may differ from those of other shareholders.

Pursuant to the approval by shareholders of a control share acquisition proposal, MAK Capital holds approximately 31% of our outstanding common shares. As a significant shareholder whose responses could potentially affect the interests of Agilysys and the other shareholders, our Board may consider MAK Capital's potential response to a particular decision of the Board in considering the range of possible corporate policies and strategies in the future, potentially influencing corporate policy and strategic planning.

MAK entered into a Voting Trust Agreement with Computershare, as trustee, which provides that, for both strategic and other transactions requiring at least two-thirds of the voting power to approve, the trustee will vote a certain percentage of MAK Capital's shares in favor of, against, or abstaining from voting in the same proportion as all other shares voted by shareholders (including MAK Capital's shares not being voted by the trustee). If the Voting Trust Agreement, as amended, that MAK entered into with Computershare were to terminate for any reason, MAK Capital would have a level of control that would highly influence the approval or disapproval of transactions requiring under Ohio law the approval of two-thirds of the outstanding common shares, such as a business combination, or majority share acquisition involving the issuance of common shares entitling the holders to exercise one-sixth or more of the voting power of our common shares, each of which requires approval by two-thirds of the outstanding common shares. MAK Capital might also be able to initiate or substantially assist any such transaction. Even with the limitations on MAK Capital's voting power imposed by the Voting Trust Agreement, as amended, it would be more difficult for the other shareholders to approve such a transaction if MAK Capital opposed it, and MAK Capital's interests may differ from those of other shareholders.

16

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

Our corporate services are located in Alpharetta, Georgia where we lease approximately 34,000 square feet of office space. In addition, we lease approximately 34,000 square feet of office space in Las Vegas, Nevada, 22,000 square feet of office space in Bellevue, Washington, and 12,000 square feet of office space in Santa Barbara, California. Internationally, we lease approximately 17,000 square feet of office space in Chennai, India and lease several other smaller office locations throughout Europe and Asia. Our major leases contain renewal options for periods of up to 10 years. We believe that our current facilities and office space are sufficient to meet our needs and do not anticipate any difficulty securing additional space as needed.

Item 3. Legal Proceedings.

We are involved in legal actions that arise in the ordinary course of business. It is the opinion of management that the resolution of any current pending litigation will not have a material adverse effect on our financial position or results of operations.

On April 6, 2012, Ameranth, Inc. filed a complaint against us for patent infringement in the United States District Court for the Southern District of California. The complaint alleges, among other things, that point-of-sale and property management and other hospitality information technology products, software, components and/or systems sold by us infringe three patents owned by Ameranth purporting to cover generation and synchronization of menus, including restaurant menus, event tickets, and other products across fixed, wireless and/or internet platforms as well as synchronization of hospitality information and hospitality software applications across fixed, wireless and internet platforms. The complaint seeks monetary damages, injunctive relief, costs and attorneys’ fees. At this time, we are not able to predict the outcome of this lawsuit, or any possible monetary exposure associated with the lawsuit. However, we dispute the allegations of wrongdoing and are vigorously defending ourselves in this matter.

Item 4. Mine Safety Disclosures.

Not applicable.

17

Part II

Item 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

Our common shares, without par value, are traded on the NASDAQ Stock Market LLC under the symbol “AGYS”. The high and low sales prices for the common shares for each quarter during the past two fiscal years are presented in the table below.

2017 | High | Low | |||||

Fourth quarter | $ | 10.85 | $ | 8.78 | |||

Third quarter | $ | 11.17 | $ | 9.13 | |||

Second quarter | $ | 11.57 | $ | 10.28 | |||

First quarter | $ | 11.76 | $ | 9.90 | |||

2016 | High | Low | |||||

Fourth quarter | $ | 11.77 | $ | 8.50 | |||

Third quarter | $ | 12.56 | $ | 9.62 | |||

Second quarter | $ | 12.19 | $ | 7.97 | |||

First quarter | $ | 10.43 | $ | 8.72 | |||

The closing price of the common shares on May 24, 2017, was $9.52 per share. There were 1,618 active shareholders of record.

We did not pay dividends in fiscal 2017 or 2016 and are unlikely to do so in the foreseeable future. The current policy of the Board of Directors is to retain any available earnings for use in the operations of our business.

18

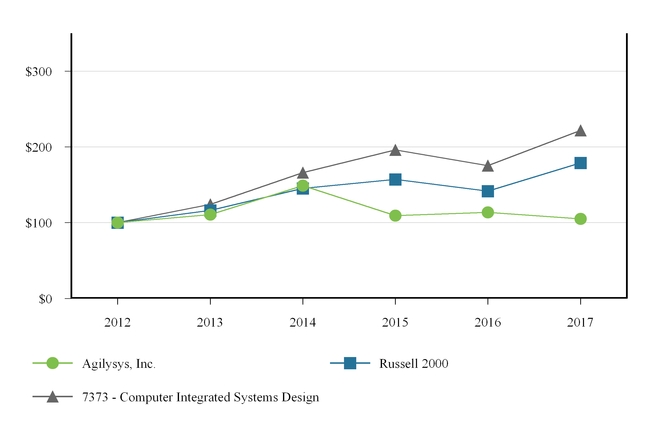

Shareholder Return Performance Presentation

The following chart compares the value of $100 invested in our common shares, including reinvestment of dividends, with a similar investment in the Russell 2000 Index (the “Russell 2000”) and with the companies listed in the SIC Code 7373-Computer Integrated Systems Design for the period March 31, 2012 through March 31, 2017. The stock price performance in this graph is not necessarily indicative of the future performance of our common shares.

Comparison of 5 Year Cumulative Total Return

INDEXED RETURNS | ||||||||||||||||||

Fiscal Years Ended March 31, | ||||||||||||||||||

Base Period | ||||||||||||||||||

Company Name / Index | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||

Agilysys, Inc. | $ | 100.00 | $ | 110.57 | $ | 149.05 | $ | 109.45 | $ | 113.50 | $ | 105.12 | ||||||

Russell 2000 | $ | 100.00 | $ | 116.30 | $ | 145.26 | $ | 157.19 | $ | 141.85 | $ | 179.03 | ||||||

Peer Group | $ | 100.00 | $ | 124.28 | $ | 166.09 | $ | 196.23 | $ | 175.36 | $ | 221.69 | ||||||

This performance graph shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended or incorporated by reference into any of our filings under the Securities Act of 1933, as amended, of the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

19

Item 6. Selected Financial Data.

The following selected consolidated financial and operating data was derived from our audited consolidated financial statements and the current and prior period operating results of our UK entity and RSG have been classified within discontinued operations for all periods presented as discussed in Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations. The selected financial data should be read in conjunction with the Consolidated Financial Statements and Notes thereto, and Item 7 contained in Part II of this Annual Report.

Year ended March 31, | |||||||||||||||

(In thousands, except per share data) | 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||

Operating results | |||||||||||||||

Net revenue | $ | 127,678 | $ | 120,366 | $ | 103,514 | $ | 101,261 | $ | 94,008 | |||||

Gross profit | 63,785 | 68,106 | 60,081 | 64,040 | 57,619 | ||||||||||

Operating loss | (11,408 | ) | (4,313 | ) | (12,467 | ) | (6,188 | ) | (9,307 | ) | |||||

Loss from continuing operations, net of taxes | (11,721 | ) | (3,765 | ) | (11,497 | ) | (2,895 | ) | (6,214 | ) | |||||

Income from discontinued operations, net of taxes | — | — | — | 19,992 | 4,916 | ||||||||||

Net (loss) income | $ | (11,721 | ) | $ | (3,765 | ) | $ | (11,497 | ) | $ | 17,097 | $ | (1,298 | ) | |

Per share data (1) | |||||||||||||||

Basic and diluted | |||||||||||||||

Loss from continuing operations | $ | (0.52 | ) | $ | (0.17 | ) | $ | (0.51 | ) | $ | (0.13 | ) | $ | (0.28 | ) |

Income from discontinued operations | — | — | — | 0.90 | 0.22 | ||||||||||

Net (loss) income | $ | (0.52 | ) | $ | (0.17 | ) | $ | (0.51 | ) | $ | 0.77 | $ | (0.06 | ) | |

Weighted-average shares outstanding - basic and diluted | 22,615 | 22,483 | 22,338 | 22,135 | 21,880 | ||||||||||

Balance sheet data at year end | |||||||||||||||

Cash and cash equivalents | $ | 49,255 | $ | 60,608 | $ | 75,067 | $ | 99,566 | $ | 82,444 | |||||

Working capital | 27,183 | 41,401 | 54,407 | 81,711 | 72,122 | ||||||||||

Total assets | 167,305 | 185,157 | 181,525 | 190,895 | 197,498 | ||||||||||

Total debt | 237 | 333 | 189 | 335 | 86 | ||||||||||

Total shareholders’ equity | 113,669 | 123,473 | 124,188 | 132,873 | 113,856 | ||||||||||

(1) When a loss is reported, the denominator of diluted earnings per share cannot be adjusted for the dilutive impact of share-based compensation awards because doing so would be anti-dilutive. In addition, when a loss from continuing operations is reported, adjusting the denominator of diluted earnings per share would also be anti-dilutive to the loss per share, even if the entity has net income after adjusting for a discontinued operation. Therefore, for all periods presented, basic weighted-average shares outstanding were used in calculating the diluted net loss per share.

20

Item 7. Managements’ Discussion and Analysis of Financial Condition and Results of Operations.

In “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (“MD&A”), management explains the general financial condition and results of operations for Agilysys and subsidiaries including:

— what factors affect our business;

— what our earnings and costs were;

— why those earnings and costs were different from the year before;

— where the earnings came from;

— how our financial condition was affected; and

— where the cash will come from to fund future operations.

The MD&A analyzes changes in specific line items in the Consolidated Statements of Operations and Consolidated Statements of Cash Flows and provides information that management believes is important to assessing and understanding our consolidated financial condition and results of operations. This discussion should be read in conjunction with the Consolidated Financial Statements and related Notes that appear in Item 8 of this Annual Report titled, "Financial Statements and Supplementary Data." Information provided in the MD&A may include forward-looking statements that involve risks and uncertainties. Many factors could cause actual results to be materially different from those contained in the forward-looking statements. See “Forward-Looking Information” on page 3 of this Annual Report and Item 1A “Risk Factors” in Part I of this Annual Report for additional information concerning these items. Management believes that this information, discussion, and disclosure is important in making decisions about investing in Agilysys.

Overview

Agilysys is a leading technology company that provides innovative software for point-of-sale (POS), property management systems

(PMS), inventory and procurement, workforce management, analytics, document management and mobile and wireless solutions and services to the hospitality industry. Our solutions and services allow property managers to better connect, interact and transact with their customers and enhance their customer relationships by streamlining operations, improving efficiency, increasing guest recruitment and wallet share, and enhancing the overall guest experience. Agilysys serves four major market sectors: Gaming, both corporate and tribal; Hotels, Resorts and Cruise; Foodservice Management; and Restaurants, Universities, Stadia and Healthcare. A significant portion of our consolidated revenue is derived from contract support, maintenance and subscription services.

Agilysys operates throughout North America, Europe and Asia, with corporate services located in Alpharetta, GA. For more information, visit www.agilysys.com.

Following the divestiture of the Retail Solutions Group (RSG) in July 2013, and our United Kingdom business entity (UK entity) in March 2014, Agilysys operates as one operating segment and as a pure play software-driven solutions provider to the hospitality industry. The sales of RSG and the UK entity each represented the disposal of a component of an entity. As such, the operating results of RSG and the UK entity have been reported as a component of discontinued operations in Item 6. Selected Financial Data, of this Annual Report, for the twelve months ended March 31,2014 and March 31, 2013.

Our top priority is increasing shareholder value by improving operating and financial performance and profitably growing the business through superior products and services. To that end, we expect to invest a certain portion of our cash on hand to develop and market new software products, to fund enhancements to existing software products, and to expand our customer breadth, both vertically and geographically.

Our strategic plan specifically focuses on:

• Strong customer focus, with clear and realistic service commitments.

• | Growing sales of our proprietary offerings: products, support, maintenance and subscription services and professional services. |

• Diversifying our customer base across industries and geographies.

• Capitalizing on our intellectual property and emerging technology trends.

The primary objective of our ongoing strategic planning process is to create shareholder value by capitalizing on growth opportunities and strengthening our competitive position within the specific technology solutions and in the end markets we service. The plan builds on our existing strengths and targets industry leading growth and peer beating financial and operating results driven by new technology trends and market opportunities. Industry leading growth and peer beating financial and operational results will be achieved through tighter coupling and management of operating expenses of the business and sharpening the focus of our investments

21

to concentrate on growth opportunities with the highest return by seeking the highest margin revenue opportunities in the markets in which we compete.

Revenue - Defined

As required by the SEC, we separately present revenue earned as products revenue, support, maintenance and subscription services revenue or professional services revenue in our Consolidated Statements of Operations. In addition to the SEC requirements, we may, at times, also refer to revenue as defined below. The terminology, definitions, and applications of terms we use to describe our revenue may be different from those used by other companies and caution should be used when comparing these financial measures to those of other companies. We use the following terms to describe revenue:

• Revenue – We present revenue net of sales returns and allowances.

• | Products revenue – Revenue earned from the sales of hardware equipment and proprietary and remarketed software. |

• | Support, maintenance and subscription services revenue – Revenue earned from the sale of proprietary and remarketed ongoing support, maintenance and subscription or hosting services. |

• | Professional services revenue – Revenue earned from the delivery of implementation, integration and installation services for proprietary and remarketed products. |

Results of Operations

Fiscal 2017 Compared with Fiscal 2016

Net Revenue and Operating Loss

The following table presents our consolidated revenue and operating results for the fiscal years ended March 31, 2017 and 2016:

Year ended March 31, | Increase (decrease) | |||||||||||||

(Dollars in thousands) | 2017 | 2016 | $ | % | ||||||||||

Net revenue: | ||||||||||||||

Products | $ | 38,339 | $ | 41,445 | $ | (3,106 | ) | (7.5 | )% | |||||

Support, maintenance and subscription services | 63,308 | 60,104 | 3,204 | 5.3 | % | |||||||||

Professional services | 26,031 | 18,817 | 7,214 | 38.3 | % | |||||||||

Total net revenue | 127,678 | 120,366 | 7,312 | 6.1 | % | |||||||||

Cost of goods sold: | ||||||||||||||

Products, inclusive of developed technology amortization | 28,244 | 23,326 | 4,918 | 21.1 | % | |||||||||

Support, maintenance and subscription services | 16,965 | 15,394 | 1,571 | 10.2 | % | |||||||||

Professional services | 18,684 | 13,540 | 5,144 | 38.0 | % | |||||||||

Total cost of goods sold | 63,893 | 52,260 | 11,633 | 22.3 | % | |||||||||

Gross profit | 63,785 | 68,106 | (4,321 | ) | (6.3 | )% | ||||||||

Gross profit margin | 50.0 | % | 56.6 | % | ||||||||||

Operating expenses: | ||||||||||||||

Product development | 29,048 | 26,688 | 2,360 | 8.8 | % | |||||||||

Sales and marketing | 20,823 | 19,740 | 1,083 | 5.5 | % | |||||||||

General and administrative | 19,875 | 21,818 | (1,943 | ) | (8.9 | )% | ||||||||

Depreciation of fixed assets | 2,409 | 2,199 | 210 | 9.5 | % | |||||||||

Amortization of intangibles | 1,392 | 1,243 | 149 | 12.0 | % | |||||||||

Restructuring, severance and other charges | 1,561 | 283 | 1,278 | 451.5% | ||||||||||

Impairments and other fair value adjustments | — | 180 | (180 | ) | (100.0 | )% | ||||||||

Legal settlements | 85 | 268 | (183 | ) | (68.3 | )% | ||||||||

Operating loss | $ | (11,408 | ) | $ | (4,313 | ) | $ | (7,095 | ) | 164.5 | % | |||

Operating loss percentage | (8.9 | )% | (3.6 | )% | ||||||||||

22

The following table presents the percentage relationship of our Consolidated Statement of Operations line items to our consolidated net revenues for the periods presented:

Year ended March 31, | |||||

2017 | 2016 | ||||

Net revenue: | |||||

Products | 30.0 | % | 34.4 | % | |

Support, maintenance and subscription services | 49.6 | 50.0 | |||

Professional services | 20.4 | 15.6 | |||

Total net revenue | 100.0 | 100.0 | |||

Cost of goods sold: | |||||

Products, inclusive of developed technology amortization | 22.1 | 19.4 | |||

Support, maintenance and subscription services | 13.3 | 12.8 | |||

Professional services | 14.6 | 11.2 | |||

Total net cost of goods sold | 50.0 | 43.4 | |||

Gross profit | 50.0 | 56.6 | |||

Operating expenses: | |||||

Product development | 22.8 | 22.2 | |||

Sales and marketing | 16.3 | 16.4 | |||

General and administrative | 15.6 | 18.1 | |||

Depreciation of fixed assets | 1.9 | 1.8 | |||

Amortization of intangibles | 1.1 | 1.0 | |||

Restructuring, severance and other charges | 1.2 | 0.1 | |||

Impairments and other fair value adjustments | — | 0.2 | |||

Legal settlements | 0.1 | 0.2 | |||

Operating loss | (8.9 | )% | (3.6 | )% | |