Post Q4 2010 Earnings Release - Last updated March 15, 2011

INVESTOR REFERENCE BOOK

Exhibit 99.1

The information contained in this presentation includes certain estimates, projections and other

forward-looking information that reflect our current views with respect to future events and financial

performance. These estimates, projections and other forward-looking information are based on

assumptions that HealthSouth believes, as of the date hereof, are reasonable. Inevitably, there will

be differences between such estimates and actual results, and those differences may be material.

forward-looking information that reflect our current views with respect to future events and financial

performance. These estimates, projections and other forward-looking information are based on

assumptions that HealthSouth believes, as of the date hereof, are reasonable. Inevitably, there will

be differences between such estimates and actual results, and those differences may be material.

There can be no assurance that any estimates, projections or forward-looking information will be

realized.

realized.

All such estimates, projections and forward-looking information speak only as of the date hereof.

HealthSouth undertakes no duty to publicly update or revise the information contained herein.

HealthSouth undertakes no duty to publicly update or revise the information contained herein.

You are cautioned not to place undue reliance on the estimates, projections and other forward-

looking information in this presentation as they are based on current expectations and general

assumptions and are subject to various risks, uncertainties and other factors, including those set

forth in the Form 10-K for the year ended December 31, 2010, and in other documents we

previously filed with the SEC, many of which are beyond our control, that may cause actual results

to differ materially from the views, beliefs and estimates expressed herein.

looking information in this presentation as they are based on current expectations and general

assumptions and are subject to various risks, uncertainties and other factors, including those set

forth in the Form 10-K for the year ended December 31, 2010, and in other documents we

previously filed with the SEC, many of which are beyond our control, that may cause actual results

to differ materially from the views, beliefs and estimates expressed herein.

Note Regarding Presentation of Non-GAAP Financial Measures

The following presentation includes certain “non-GAAP financial measures” as defined in

Regulation G under the Securities Exchange Act of 1934. Schedules are attached that reconcile

the non-GAAP financial measures included in the following presentation to the most directly

comparable financial measures calculated and presented in accordance with Generally

Accepted Accounting Principles in the United States. Our Form 8-K, dated March 15, 2011, to which

the following supplemental slides are attached as Exhibit 99.1, provides further explanation and

disclosure regarding our use of non-GAAP financial measures and should be read in conjunction

with these supplemental slides.

The following presentation includes certain “non-GAAP financial measures” as defined in

Regulation G under the Securities Exchange Act of 1934. Schedules are attached that reconcile

the non-GAAP financial measures included in the following presentation to the most directly

comparable financial measures calculated and presented in accordance with Generally

Accepted Accounting Principles in the United States. Our Form 8-K, dated March 15, 2011, to which

the following supplemental slides are attached as Exhibit 99.1, provides further explanation and

disclosure regarding our use of non-GAAP financial measures and should be read in conjunction

with these supplemental slides.

Forward-Looking Statements

2

Exhibit 99.1

Table of Contents

3

Exhibit 99.1

|

Inpatient Rehabilitation Hospitals (“IRF”)

|

|

|

Outpatient Rehabilitation Satellite Clinics

|

|

|

Long-Term Acute Care Hospitals (“LTCH”)

|

|

|

Hospital-Based Home Health Agencies

|

|

|

Employees

|

|

|

Revenue in 2010

|

|

|

Inpatient Discharges in 2010

|

|

|

Outpatient Visits in 2010

|

|

|

Number of States

|

|

|

Exchange (Symbol)

|

|

4

Largest Provider of Inpatient Rehabilitative Healthcare Services in the U.S.

Our Company

|

Marketshare

|

|

~ 8% of IRFs

~ 17% of Licensed Beds ~ 22% of Patients Served |

Exhibit 99.1

Our Hospitals

Major Services

• Rehabilitation Physicians: manage and treat medical needs of patients

• Rehabilitation Nurses: oversee treatment programs of patients

• Physical Therapists: address physical function, mobility, safety

• Occupational Therapists: promote independence and re-integration

• Speech-Language Therapists: treat communication & swallowing disorders

• Case Managers: coordinate care plan with physician, caregivers and family

• Post-discharge services: outpatient therapy and home health

5

Exhibit 99.1

Our Patients

6

Most Common Conditions (2010)

1.Stroke 17.2%

2.Neurological 15.2%

3.Debility 11.3%

4.Fracture of the lower extremity 11.0%

5.Knee/Hip replacement 9.5%

6.Other orthopedic conditions 9.5%

7.Brain injury 7.4%

8.Cardiac conditions 4.3%

9.Spinal cord injury 3.6%

10.All other 11.0%

Referral Sources

94% Acute Care Hospitals

5% Physician Offices

1% Skilled Nursing Facilities

Admission to an IRF

• Physicians and acute care

hospital case managers are key

decision-makers.

hospital case managers are key

decision-makers.

• All IRF patients must meet

reasonable and necessary criteria

and must be admitted by a

physician.

reasonable and necessary criteria

and must be admitted by a

physician.

• All IRF patients must be medically

stable and have potential to

tolerate three hours of therapy per

day (minimum).

stable and have potential to

tolerate three hours of therapy per

day (minimum).

• IRF patients receive 24-hour, 7

days a week nursing care.

days a week nursing care.

• Average length of stay (ALOS) =

14.1 days

14.1 days

Exhibit 99.1

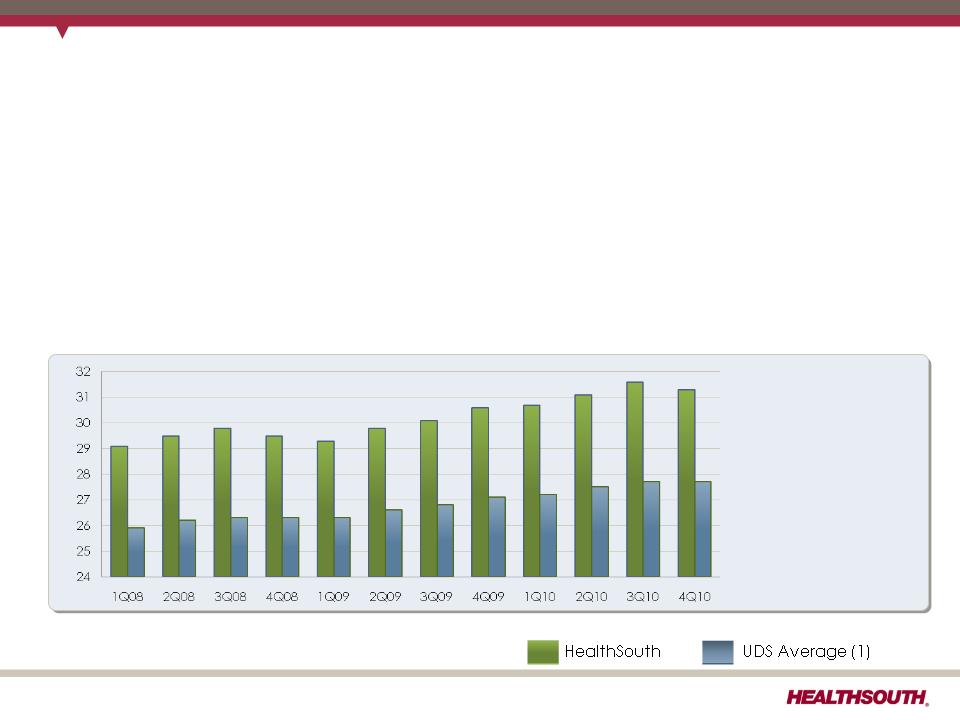

Our Quality

FIM Gain

Change in

Functional

Independence

Measurement

(based on an 18

point assessment)

from admission to

discharge

Functional

Independence

Measurement

(based on an 18

point assessment)

from admission to

discharge

7

(1) Average = Expected, Risk-adjusted

• Inpatient rehabilitation hospitals evaluate all patients at admission and upon

discharge to determine their functional status.

discharge to determine their functional status.

− The Functional Independence Measurement (“FIM”) patient assessment

instrument is used for these evaluations.

instrument is used for these evaluations.

• The difference between the FIM scores at admission and upon discharge is called

the “FIM Gain.”

the “FIM Gain.”

− The greater the FIM Gain, the greater the patient’s level of independence, the

better the patient outcome.

better the patient outcome.

Exhibit 99.1

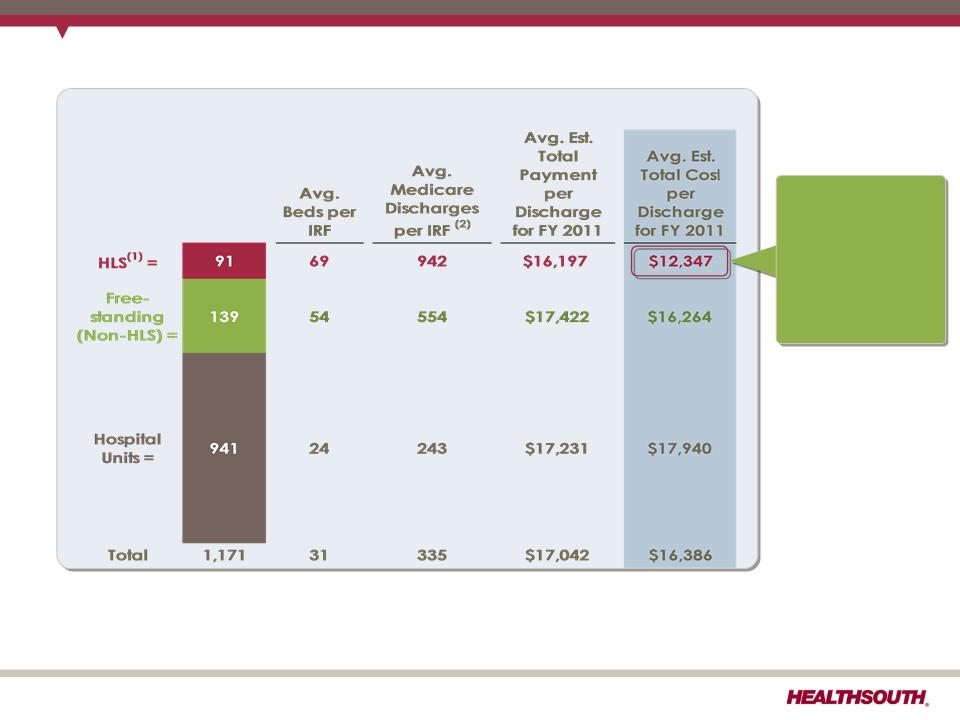

(1) The 1,171 total and the 91 for HLS do not include HealthSouth Rehabilitation Hospital of Northern Virginia; Rehabilitation Hospital of Southwest Virginia;

Rehabilitation Hospital of Mesa, AZ; and Rehabilitation Hospital of Fredericksburg, VA. that were opened after the data collection. Desert Canyon

Rehabilitation Hospital and HealthSouth Sugar Land Rehabilitation Hospital, currently owned by HLS, were included in the 139 non-HLS freestanding.

Rehabilitation Hospital of Mesa, AZ; and Rehabilitation Hospital of Fredericksburg, VA. that were opened after the data collection. Desert Canyon

Rehabilitation Hospital and HealthSouth Sugar Land Rehabilitation Hospital, currently owned by HLS, were included in the 139 non-HLS freestanding.

(2) In 2009, HealthSouth averaged 1,177 total Medicare and non-Medicare discharges in its 90 consolidated hospitals and 6 long-term acute care hospitals.

Sources: FY 2011 CMS Rate Setting File - see next page

8

Total Inpatient Rehabilitation Facilities (IRFs): 1,171 (1)

Our Cost-Effectiveness

HealthSouth

differentiates

itself by

providing

superior quality

care at a

differentiates

itself by

providing

superior quality

care at a

lower cost.

Exhibit 99.1

CMS Fiscal Year 2011 IRF Rate Setting File Analysis

Notes:

(1) All data provided was filtered and compiled from the Centers for Medicare and

Medicaid Services (CMS) Fiscal Year 2011 IRF rate setting Final Rule file found at

http://www.cms.hhs.gov/InpatientRehabFacPPS/07_DataFiles.asp#TopOfPage. The

data presented was developed entirely by CMS and is based on its definitions

which are different in form and substance from the criteria HealthSouth uses for

external reporting purposes. Because CMS does not provide its detailed

methodology, HealthSouth is not able to reconstruct the CMS projections or the

calculation.

Medicaid Services (CMS) Fiscal Year 2011 IRF rate setting Final Rule file found at

http://www.cms.hhs.gov/InpatientRehabFacPPS/07_DataFiles.asp#TopOfPage. The

data presented was developed entirely by CMS and is based on its definitions

which are different in form and substance from the criteria HealthSouth uses for

external reporting purposes. Because CMS does not provide its detailed

methodology, HealthSouth is not able to reconstruct the CMS projections or the

calculation.

(2) The CMS file contains data for each of the 1,171 inpatient rehabilitation facilities

used to estimate the policy updates for the FY 2011 IRF-PPS Final Rule. Most of the

data represents historical information from the CMS fiscal year 2009 period and

does not reflect the same HealthSouth hospitals in operation today. The data

presented was separated into three categories: Freestanding, Units, and

HealthSouth. HealthSouth is a subset of Freestanding and the Total.

used to estimate the policy updates for the FY 2011 IRF-PPS Final Rule. Most of the

data represents historical information from the CMS fiscal year 2009 period and

does not reflect the same HealthSouth hospitals in operation today. The data

presented was separated into three categories: Freestanding, Units, and

HealthSouth. HealthSouth is a subset of Freestanding and the Total.

9

Exhibit 99.1

Our Payors (2010)

Prospective Payment System (“PPS”)

• Payments based on Case Mix Groups

(“CMGs”)

(“CMGs”)

– Diagnosis of patient’s illness

• Fixed payment per CMG adjusted for:

– Acuity/severity

– Regional wage differential

• Per diems for “short stays”

Per Diem or CMG

• Negotiated rate

• Some are “tiered” for acuity/severity

Variety of methodologies

Varies by state

Variety of methodologies

Medicare

Managed Care

• Includes managed

Medicare

Medicare

Other Third-Party Payors

Medicaid

Workers’ Comp./

Patients/Other

Patients/Other

Payment Methodology

Payor Source

10

70.5%

21.5%

2.3%

4.0%

1.7%

Exhibit 99.1

Industry Structure

11

Exhibit 99.1

Sources: Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group, MedPAC.

Data for the year ended December 31, 2009.

Data for the year ended December 31, 2009.

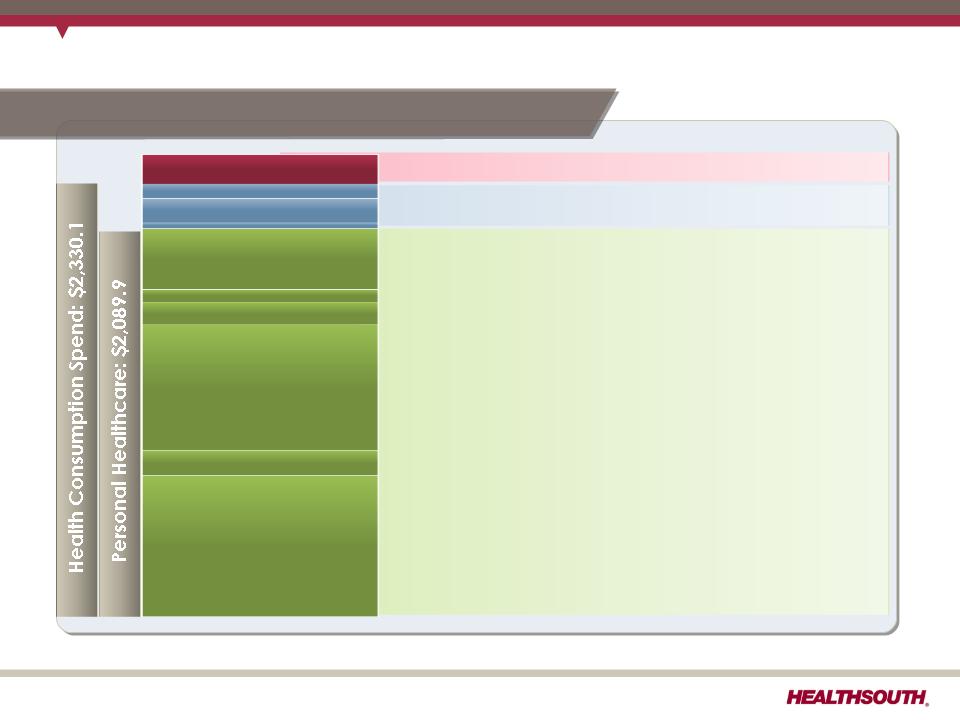

Overall Healthcare Spending

Hospital Care

Includes Inpatient Rehabilitation, Long-Term Care Hospitals

Includes Inpatient Rehabilitation, Long-Term Care Hospitals

$759.1

$137.0

$674.9

$122.6

$68.3

$328.0

Nursing Care Facilities and

Continuing Care Retirement Communities

Continuing Care Retirement Communities

Professional Services

Other Health, Residential and Personal Care

Home Health Care

Retail of Medical Products

$29.8

Government Administration

$133.2

Net Cost of Health Insurance

$77.2

Government Public Health

$156.2

Investment

National Healthcare Spending: $2,486.3 billion

12

(billions)

Exhibit 99.1

Medicare 2010 Spending = $509.1 Billion (1)

(1) Percentages are based upon total Medicare spending of $521 billion, before $11.9 billion of recoveries for 2010 (CBO Medicare August 2010

Medicare Baseline).

Medicare Baseline).

(2) Inpatient Hospital includes spending for acute care hospitals along with, inpatient rehabilitation and long-term care hospital services; in 2009,

Medicare spent $5.7 and $4.9 billion, respectively, for these services (MedPAC Data Handbook, June 2010).

Medicare spent $5.7 and $4.9 billion, respectively, for these services (MedPAC Data Handbook, June 2010).

(3) Other Services reflects spending for hospice; in 2008, Medicare spent $11.2 billion for hospice services. (MedPAC Data Handbook, June 2010). Other

Services also reflects spending for various other outpatient services.

Services also reflects spending for various other outpatient services.

$26B Skilled Nursing

$139B Inpatient Hospital (2)

$ 67.3B Physician Payments

$ 31.1B Outpatient Hospital

$ 19.6B Home Health

$63B Other Services (3)

$ 58.2B Outpatient Rx

5%

27%

22%

11%

12%

4%

6%

13%

$5.7B (1%)

Inpatient Rehabilitation Hospitals

Inpatient Rehabilitation Hospitals

Medicare Part B

Medicare Part B

Medicare Part C

Medicare Part C

Medicare Parts A&B

Medicare Parts A&B

Medicare Part D

Medicare Part D

Medicare Part A

Medicare Part A

13

Exhibit 99.1

Preventive

Routine health

care that

includes

screenings,

check-ups, and

patient

counseling to

prevent illnesses,

disease, or other

health problems.

care that

includes

screenings,

check-ups, and

patient

counseling to

prevent illnesses,

disease, or other

health problems.

Acute

Medical

treatment of

diseases for

which a patient

is treated for a

brief but severe

episode of

illness.

treatment of

diseases for

which a patient

is treated for a

brief but severe

episode of

illness.

Ambulatory

Medical care

delivered on an

outpatient basis.

E.G., blood tests,

X-rays,

endoscopy,

certain biopsies,

certain surgical

procedures.

delivered on an

outpatient basis.

E.G., blood tests,

X-rays,

endoscopy,

certain biopsies,

certain surgical

procedures.

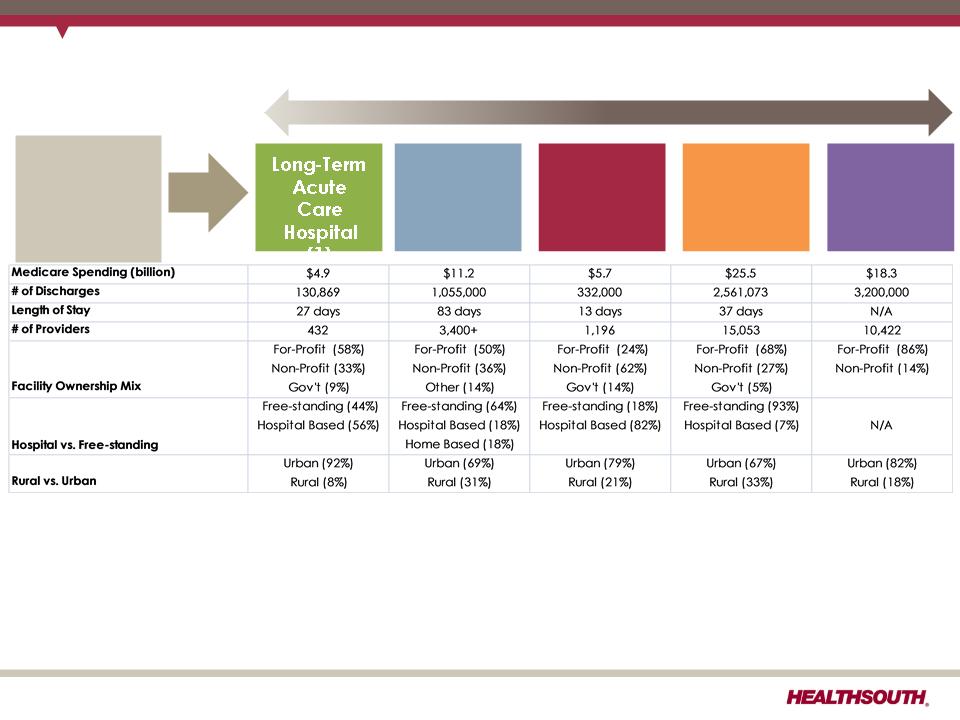

Post-Acute

Medical care

provided after a

period of acute

care. E.G.,

inpatient

rehabilitation

hospitals,

hospice, skilled

nursing homes,

home health

provided after a

period of acute

care. E.G.,

inpatient

rehabilitation

hospitals,

hospice, skilled

nursing homes,

home health

Continuum of Healthcare Services

14

Exhibit 99.1

Note: These numbers are program spending only and do not include beneficiary copayments.

Source: Centers for Medicare and Medicaid Services, Office of the Actuary (MedPAC June 2010 Data Book - Page 130), 2009 and 2010

Medicare Trustee s Report

Medicare Trustee s Report

Medicare Spending on Post-Acute Services

Skilled nursing

facilities 18.1%

facilities 18.1%

Home health

agencies 17.7%

agencies 17.7%

Inpatient

rehabilitation

hospitals 8.4%

Long-term acute

care hospitals 5.7%

15

2009

Medicare

Margin

Medicare

Margin

Post-Acute Settings

Inpatient rehabilitation

spending (% of total

Medicare spending)

spending (% of total

Medicare spending)

Exhibit 99.1

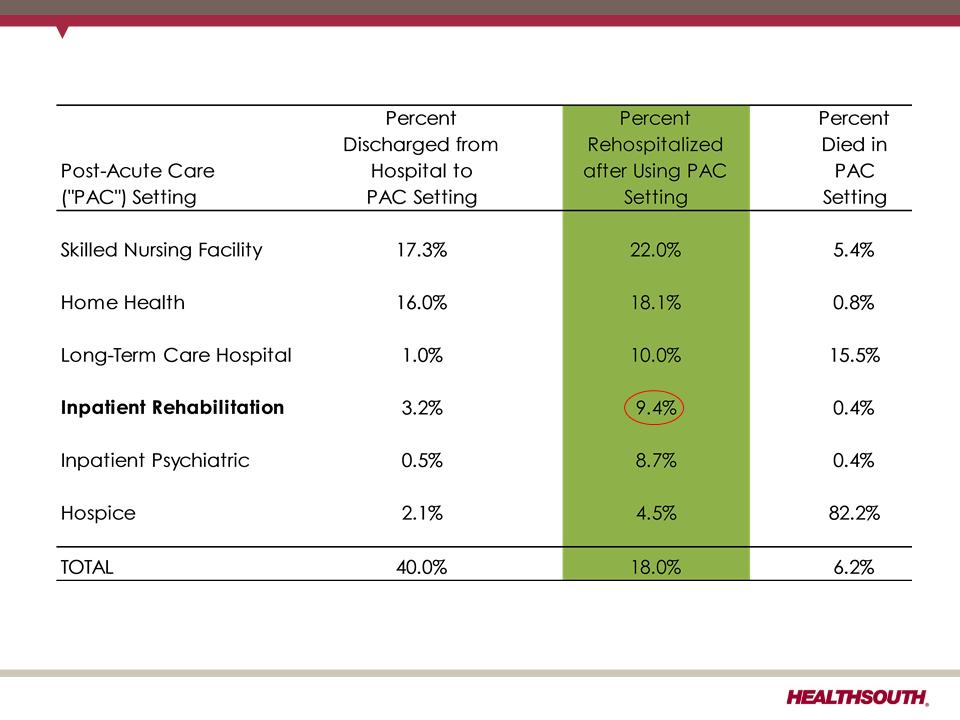

Readmission Rates

Note: Use of home health care and hospice is based on care that starts within three days of discharge. Other PAC care starts within one

day of discharge. Home health use includes episodes that overlap an inpatient stay.

day of discharge. Home health use includes episodes that overlap an inpatient stay.

Source: Medicare Payment Advisory Commission, “A Data Book: Healthcare spending and the Medicare program,” Chart 9-3 (June

2008)

2008)

16

Exhibit 99.1

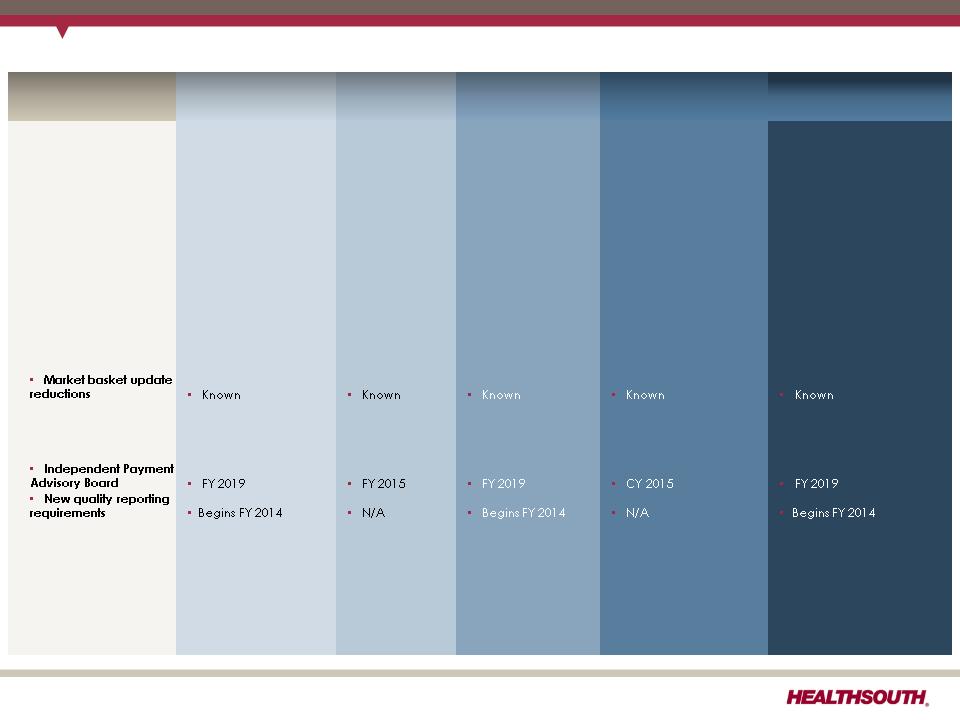

|

Future Regulatory Risk

|

Inpatient Rehabilitation

Facility |

Skilled Nursing

Facility |

Long-Term Acute

Care Hospital |

Home Health

|

Hospice

|

|

1. Re-basing payment

system |

No

|

Yes; RUGS IV and

MDS 3.0 implemented October 1, 2010 |

No

|

Yes; would be required

as part of PPACA starting in 2014 |

Yes: Required by PPACA

beginning in 2013; Modified wage index system being phased in over 7-year period beginning in FY 2010 |

|

2. Major outlier payment

adjustments |

No

|

No

|

Yes; will occur when

MMSEA relief expires (short stay outliers) |

Yes; 10% cap per agency;

2.5% taken out of outlier

pool (per PPACA) |

No

|

|

3. Upcoding adjustments

|

No

|

No

|

Yes; occurring in FY

2011 |

Yes; occurring in CY 2011 (

-3.79%), and potential further reduction 2012 |

No

|

|

4. Patient criteria

|

No; 60% Rule

already in place

|

No

|

Study dictated as

part of MMSEA; Industry developing criteria |

PPACA requires a patient -

physician “face-to-face” encounter; new therapy coverage

|

No

|

|

5. Healthcare Reform

|

|

|

|

|

|

|

• Market basket update

reductions |

|||||

|

• Productivity

adjustments |

• Begins FY 2012

|

• Begins FY 2012

|

• Begins FY 2012

|

• Begins 2015

|

• Begins 2013

|

|

• Bundling pilot

established |

• By 2013

|

• By 2013

|

• By 2013

|

• By 2013

|

• N/A

|

|

• Independent Payment

Advisory Board |

• FY 2019

|

• FY 2015

|

• FY 2019

|

• CY 2015

|

• FY 2019

|

|

• New quality reporting

requirements |

• Begins FY 2014

|

• N/A

|

• Begins FY 2014

|

• N/A

|

• Begins FY 2014

|

|

• Value based

purchasing |

• Pilot begins 2016

|

• Post 2012

|

• Pilot begins 2016

|

• Post 2012

|

• Pilot begins 2016

|

|

•Hospital Acquired

Infections |

• Post 2012

|

• Post 2012

|

• Post 2012

|

• N/A

|

•N/A

|

|

6. Other

|

N/A

|

Forecast error

being implemented in FY 2011 |

25% Rule regulatory

relief expires in 2012/2013; prohibition on new LTCHs through 2012 |

Limits on transfer

of ownership |

MedPac recommending

overhaul of payment system methodology in FY 2013 |

Post-Acute Regulatory Risks

Sources: Healthcare Reform Bill (PPACA, HERA),CMS Regulatory published rules and MMSEA

17

17

Exhibit 99.1

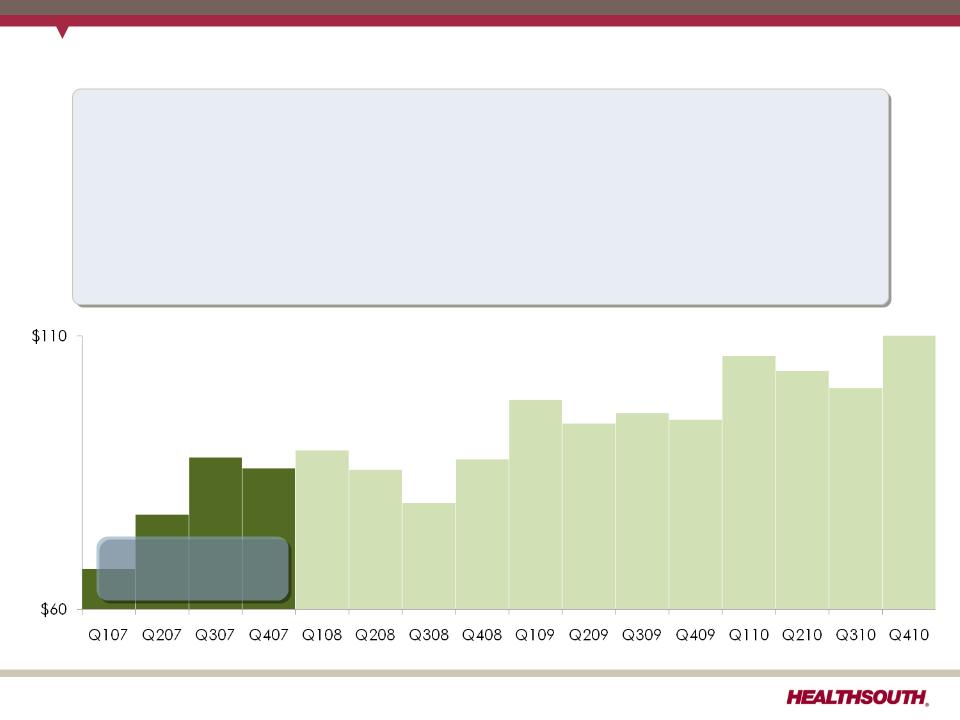

Historical Perspective

18

Exhibit 99.1

Historical Perspective

19

2007 Adjusted

EBITDA = $318.3

(1)

EBITDA = $318.3

(1)

2007

• Completed divestitures of non-core segments (surgery, imaging, O/P

therapy)

therapy)

• Used proceeds plus tax refund to repay $1.4 billion of debt

• Reduced G&A to match residual business size

• Piloted TeamWorks sales and marketing

• 75% rule frozen at 60% (MMSEA)

• Completed all settlement payments

(1) Reconciliation to GAAP provided on slides 38 and 86-90.

Exhibit 99.1

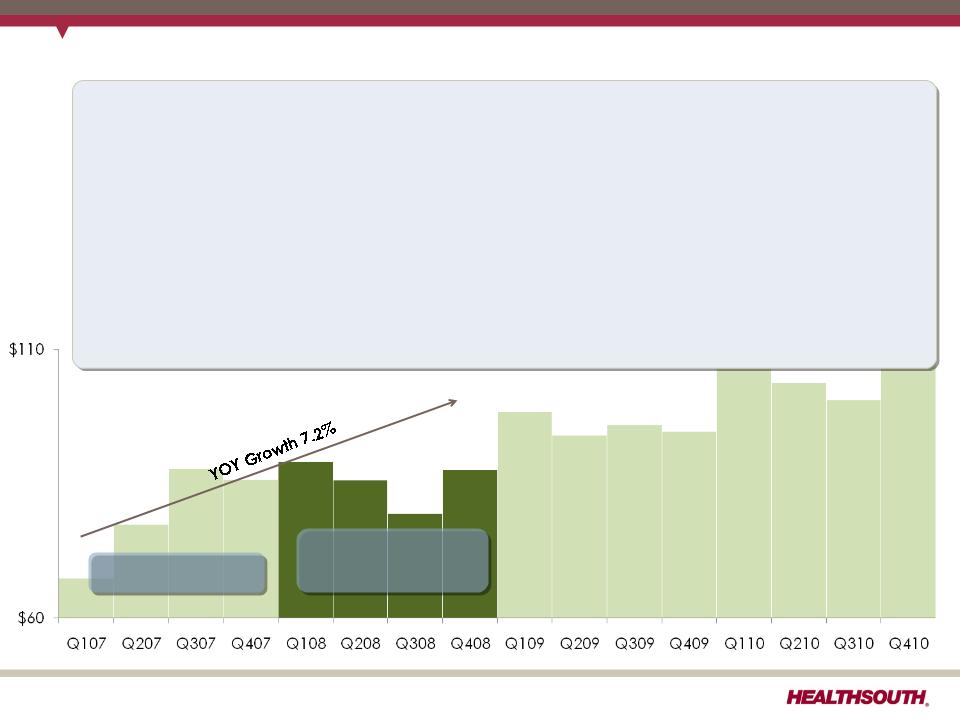

Historical Perspective

20

2008

• Established 2008-2010 business model

• 4% discharge growth; 5-8% Adjusted EBITDA growth;15-20% adjusted EPS

growth

growth

• Balanced deleveraging and growth/development strategies

• Completed TeamWorks sales and marketing roll-out

• Absorbed Medicare reimbursement rollback (Q2)

• Repaid $228 million of long-term debt (8.8 million equity issuance and prior

period tax refunds)

period tax refunds)

• Financial market turmoil (Q3)

• HealthSouth suspended development and increased focus on deleveraging

$318.3

2008 Adjusted

EBITDA = $341.2

(1)

EBITDA = $341.2

(1)

(1) Reconciliation to GAAP provided on slides 38 and 86-90.

Exhibit 99.1

Historical Perspective

21

2009

•Continued focus on deleveraging (~ $151 million repaid)

•Focused on organic growth; TeamWorks sustainability module rolled out

•Issued 5 million shares for securities litigation settlement (Q3)

•Received first Medicare market basket update in 18 months (Q3)

•Reinvigorated development efforts (Q4)

$318.3

$341.2

2009 Adjusted

EBITDA = $383.0

(1)

EBITDA = $383.0

(1)

(1) Reconciliation to GAAP provided on slides 38 and 86-90.

Exhibit 99.1

Historical Perspective

22

$318.3

$341.2

$383.0

2010 Adjusted

EBITDA = $427.4

(1)

EBITDA = $427.4

(1)

2010

•Healthcare reform passed; reduced future market basket updates

•Weak acute care referral volumes

•Adjusted annual volume growth target to 2.5-3.5%

•Development efforts pay off

• 2 de novos, 2 IRF acquisitions, 2 unit acquisitions

•Refinanced term loans and revolver (Q4)

• Repaid $151.2 million in debt

• Flexibility to repay or refinance the 10.75% notes callable in June

(1) Reconciliation to GAAP provided on slides 38 and 86-90.

Exhibit 99.1

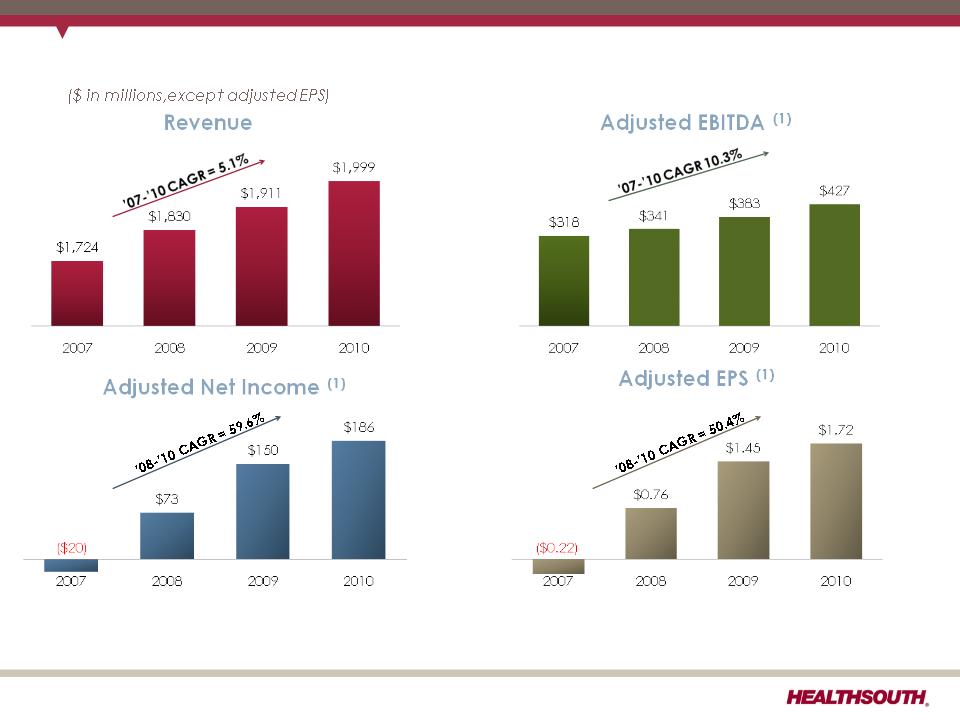

Our Track Record

(1)Reconciliation to GAAP provided on slides 38 and 86-90.

23

Exhibit 99.1

Historical Performance

24

Leverage Ratio(1)

(billions)

(1) Reconciliation to GAAP provided on slides 38-39 and 86-90.

Interest Expense

$229

$126

Exhibit 99.1

Revenues & Expenses (2010 and 2009)

25

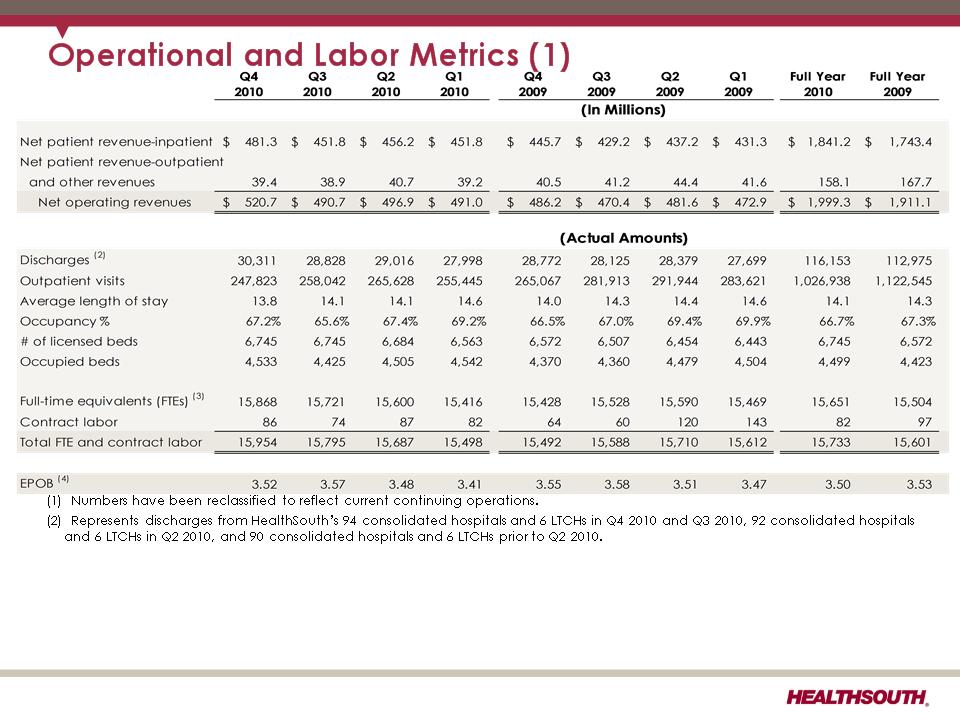

(1) Employees per occupied bed, or “EPOB,” is calculated by dividing the number of full-time equivalents, including an estimate of full-

time equivalents from the utilization of contract labor, by the number of occupied beds during each period. The number of occupied

beds is determined by multiplying the number of licensed beds by the Company’s occupancy percentage.

time equivalents from the utilization of contract labor, by the number of occupied beds during each period. The number of occupied

beds is determined by multiplying the number of licensed beds by the Company’s occupancy percentage.

Exhibit 99.1

Adjusted EBITDA (1)

26

Exhibit 99.1

Notes:

(1) Does not include 2.0 million warrants issued in connection with a January 2004 loan repaid to Credit Suisse First

Boston. In connection with this transaction, we issued warrants to the lender to purchase two million shares of

our common stock. Each warrant has a term of ten years from the date of issuance and an exercise price of

$32.50 per share. The warrants were not assumed exercised for dilutive shares outstanding because they were

antidilutive in the periods presented.

Boston. In connection with this transaction, we issued warrants to the lender to purchase two million shares of

our common stock. Each warrant has a term of ten years from the date of issuance and an exercise price of

$32.50 per share. The warrants were not assumed exercised for dilutive shares outstanding because they were

antidilutive in the periods presented.

(2) The agreement to settle our class action securities litigation received final court approval in January 2007.

These shares of common stock and warrants were issued on September 30, 2009. The 5.0 million of common

shares are now included in the outstanding shares. The warrants to purchase approx. 8.2 million shares of

common stack at a strike price of $41.40 were not assumed exercised for the dilutive shares outstanding

because they are anti-dilutive in the periods presented.

These shares of common stock and warrants were issued on September 30, 2009. The 5.0 million of common

shares are now included in the outstanding shares. The warrants to purchase approx. 8.2 million shares of

common stack at a strike price of $41.40 were not assumed exercised for the dilutive shares outstanding

because they are anti-dilutive in the periods presented.

(3) The difference between the basic and diluted shares outstanding is primarily related to our convertible

perpetual preferred stock. The preferred stock is convertible, at the option of the holder, at any time into

shares of common stock at an initial conversion price of $30.50 per share, which is equal to an initial conversion

rate of approximately 32.7869 shares of common stock per share of preferred stock, subject to a specified

adjustment. On or after July 20, 2011, we may cause the shares of preferred stock to be automatically

converted into shares of our common stock at the conversion rate then in effect if the closing price of our

common stock for 20 trading days within a period of 30 consecutive trading days ending on the trading day

before the date we give the notice of forced conversion exceeds 150% of the conversion price of the

preferred stock.

perpetual preferred stock. The preferred stock is convertible, at the option of the holder, at any time into

shares of common stock at an initial conversion price of $30.50 per share, which is equal to an initial conversion

rate of approximately 32.7869 shares of common stock per share of preferred stock, subject to a specified

adjustment. On or after July 20, 2011, we may cause the shares of preferred stock to be automatically

converted into shares of our common stock at the conversion rate then in effect if the closing price of our

common stock for 20 trading days within a period of 30 consecutive trading days ending on the trading day

before the date we give the notice of forced conversion exceeds 150% of the conversion price of the

preferred stock.

27

Exhibit 99.1

Business Outlook

2011 to 2013

2011 to 2013

28

Exhibit 99.1

Business Outlook: 2011 to 2013

Business Model

• Adjusted EBITDA CAGR: 5-8% (1)

• Adjusted Free Cash Flow CAGR: 12-17% (1)

Strategy

2010

2011

2012

2013

Deleveraging

(2)

(2)

Goal: < 4.0x

debt to EBITDA

debt to EBITDA

Longer-Term Goal: ~ 3.0x

debt to EBITDA (3.5x goal achieved at year-end 2010)

debt to EBITDA (3.5x goal achieved at year-end 2010)

Growth

Organic growth (includes capacity expansions)

De novos (~ 2-3/year)

IRF acquisitions (~ 2-3/year)

Opportunistic, disciplined acquisitions

of complementary post-acute services

of complementary post-acute services

Key Operational

Initiatives

Initiatives

• Beacon (Management Reporting Software) = Labor / outcomes / quality optimization

• TeamWorks = Care Management

• “CPR” (Comfort, Professionalism, Respect) Initiative

(1) Reconciliation to GAAP provided on slides 38-39 and 86-90.

(2) Exclusive of any E&Y recovery.

29

Exhibit 99.1

Business Outlook: Revenue Assumptions

Revenue

Volume

•2.5% to 3.5% annual growth (excludes

acquisitions)

acquisitions)

•Includes bed expansions, de novos

and unit consolidations

and unit consolidations

Medicare

Managed

Care

Care

Other

(1) We believe based on the 2011 Medicare rule for IRFs, HealthSouth should realize an increase of approximately 2.1%

annually.

annually.

(2) Management estimates

30

Exhibit 99.1

Business Outlook: Expense Assumptions

Expense

Salaries & Benefits (1)

Hospital Expenses

•Other operating and supplies

tracking with inflation

tracking with inflation

4.5% of revenue

(excludes stock-based compensation)

Salaries

& Benefits

Hospital

Expenses

Expenses

(1) Salaries, Wages and Benefits: 85% Salaries and Wages; 15% Benefits

31

Exhibit 99.1

Guidance

32

Exhibit 99.1

2011 Guidance - Adjusted EBITDA (as of March 15, 2011)

Adjusted EBITDA (1)

$440 million to $450 million

(1) Reconciliation to GAAP provided on slides 38 and 86-90.

Considerations:

ü 2010 bad debt expense was 0.9% of revenue; expect 2011 bad debt expense to

be approximately 1.5% of revenue, in line with historical average

be approximately 1.5% of revenue, in line with historical average

ü Medicare pricing in Q4 2011 will be reduced by a TBD productivity adjustment,

which we estimate to be 100 basis points.

which we estimate to be 100 basis points.

ü Outpatient revenues subject to approximately $1.4 million reduction related to

the 25% rate reduction for reimbursement of therapy expenses for multiple

the 25% rate reduction for reimbursement of therapy expenses for multiple

therapy services (Medicare physician fee schedule for calendar year 2011CMS).

Reflects:

• 2.9% to 5.3% growth over 2010

• 7.2% to 8.4% CAGR over 2009

33

Exhibit 99.1

Income Tax Considerations

|

GAAP Considerations:

•Valuation allowance reduced at YE 2010 by approximately $825 million resulting in a

$736.6 million benefit to 2010 income tax provision. •As of 12/31/10, the Company had a remaining valuation allowance of approximately

$113 million, primarily related to state NOLs. Future Cash Tax Payments:

•Expects to pay approximately $6-8 million per year of income tax.

•Does not expect to pay significant federal income taxes for up to 10 years.

•HealthSouth is not currently subject to an annual use limitation (“AUL”) under Internal

Revenue Code Section 382 (“Section 382”). A “change of ownership,” as defined by Section 382, would subject us to an AUL, which is equal to the market capitalization of the Company at the time of the “change of ownership” multiplied by the long-term tax exempt rate. |

34

Exhibit 99.1

Adjusted Free Cash Flow (1) Assumptions

(1) Reconciliation to GAAP provided on slide 39.

• Items that will affect Adjusted Free Cash Flow in 2011:

+ Cash settlements for interest rate swaps will be $33.8 million lower in 2011.

− Interest expense will be approximately $4 million per quarter higher in 2011 than 2010,

prior to any repayment/refinancing of the 10.75% senior notes.

prior to any repayment/refinancing of the 10.75% senior notes.

+ Interest expense will be reduced with any repayment/refinancing of 10.75% senior notes

callable in June 2011.

callable in June 2011.

– Maintenance capital expenditures are estimated to be approximately $20 million higher

in 2011 than 2010.

in 2011 than 2010.

• 2010 working capital benefited from a shift in timing of interest payments related to the

refinancing in Q4 2010, offset by the $6.9 million unwind fee related to the termination of

the two forward-starting interest rate swaps.

refinancing in Q4 2010, offset by the $6.9 million unwind fee related to the termination of

the two forward-starting interest rate swaps.

HealthSouth’s GAAP income statement will be affected by a

number of items that will not affect cash flow from operating

activities or adjusted free cash flow:

number of items that will not affect cash flow from operating

activities or adjusted free cash flow:

•Normalized GAAP tax rate resulting from the valuation

allowance reversal in Q4 2010.

allowance reversal in Q4 2010.

•Loss on early extinguishment of debt

Multi-Year Adjusted Free Cash Flow 12% to 17% CAGR

35

Exhibit 99.1

2011 Guidance - EPS (as of March 15, 2011)

Diluted Earnings per Share from

Continuing Operations Attributable

to HealthSouth (1)

Continuing Operations Attributable

to HealthSouth (1)

$1.01 to $1.06

Considerations:

ü Assumes provision for income tax of 40%;

cash taxes expected to be $6-$8 million.

cash taxes expected to be $6-$8 million.

ü Guidance does not include any

repayment/refinancing of the 10.75%

repayment/refinancing of the 10.75%

senior notes callable in June 2011, which

would affect the following items:

• Interest expense which is currently

forecasted to be approximately $4

million per quarter higher in Q1, Q2, and

Q3 2011 vs. prior periods in 2010.

forecasted to be approximately $4

million per quarter higher in Q1, Q2, and

Q3 2011 vs. prior periods in 2010.

• Does not include “loss on early

extinguishment of debt” (non-cash)

extinguishment of debt” (non-cash)

• Depreciation is estimated to be higher

as a result of capital expenditures in

prior periods.

as a result of capital expenditures in

prior periods.

HealthSouth is transitioning EPS guidance to a

GAAP measure.

GAAP measure.

(1) Income from continuing operations attributable to HealthSouth

(2) Current period amounts in income tax provision; see slides 86 and 90

(3) Total income tax provision for full-year 2010, including the reversal of a substantial portion of the Company's valuation allowance against deferred tax assets.

(4) Adjusted income from continuing operations; see slides 38, 86, and 90.

36

Exhibit 99.1

Free Cash Flow

37

Exhibit 99.1

(1) Notes on page 90.

Net Cash Provided by Operating Activities

38

Exhibit 99.1

Adjusted Free Cash Flow

(1) Q4 2010 and full-year 2010 working capital benefited from a shift in timing of interest payments related to the refinancing in Q4 2010.

(2) Q4 2010 and full-year 2010 were negatively affected by the $6.9 million unwind fee related to the termination of two forward-starting

interest rate swaps, which is included in cash provided by operating activities and not included in the net settlements on interest rate

swaps.

interest rate swaps, which is included in cash provided by operating activities and not included in the net settlements on interest rate

swaps.

39

Exhibit 99.1

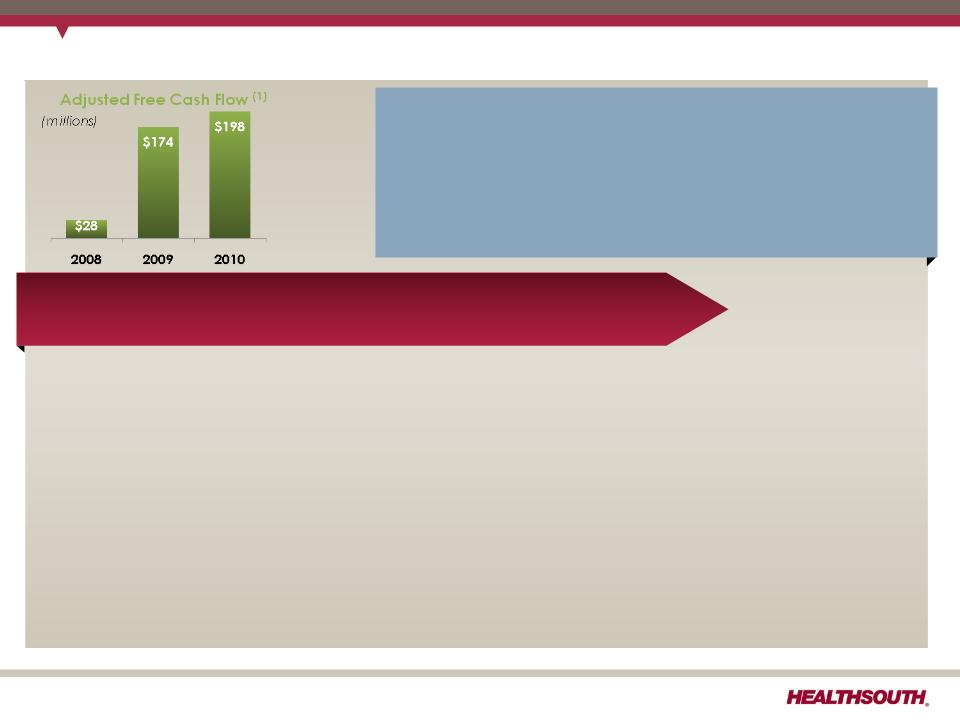

Adjusted Free Cash Flow(1) (2010 vs. 2009)

(1) Reconciliation to GAAP provided on slides 38-39 and 86-90.

40

(1)

Exhibit 99.1

Free Cash Flow Reinvestment

41

• $500 million of 10.75% notes callable June 2011

• Growth in core business

• Bed expansions

• Hospital acquisitions

• Acute care IRF unit acquisition/consolidation

• De novo hospitals

• Lower capital cost

• Share repurchase

• Offset shares underlying convertible preferred

shares

shares

• Offset shares issued in settlement of securities

litigation

litigation

Adjusted free cash flow CAGR: 12-17%

• Acquisitions of complementary business

Exhibit 99.1

Refinancing and Delevering

42

Exhibit 99.1

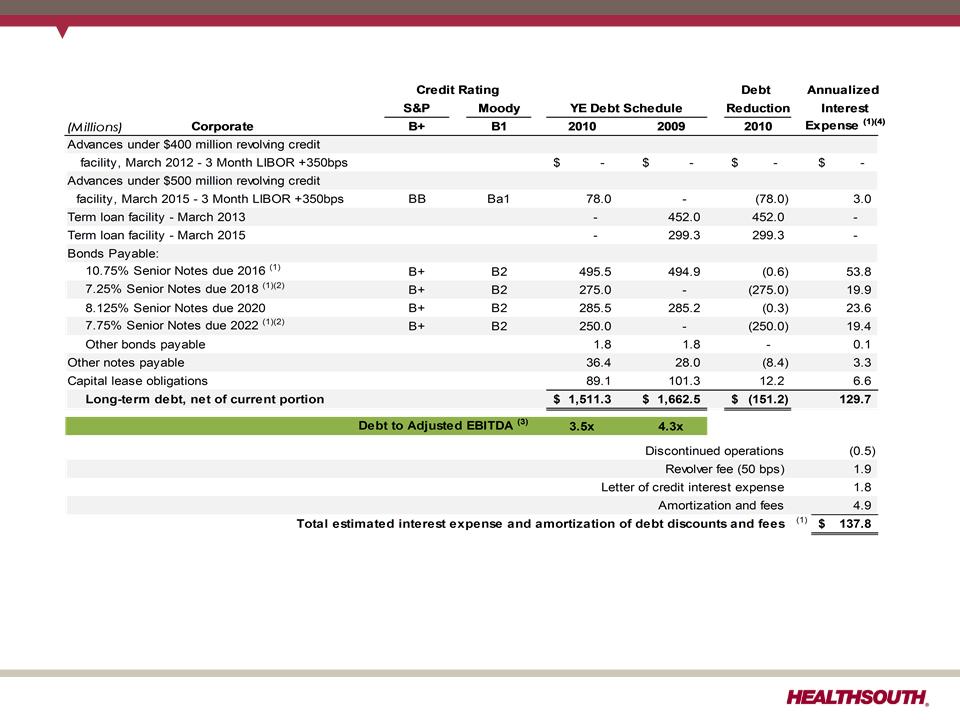

Debt Schedule and Interest Expense

(1) The annualized interest expense does not reflect any anticipated pay down of the 10.75% or the impact of the re-opening of the

7.25% and the 7.75% senior notes.

7.25% and the 7.75% senior notes.

(2) On March 7, 2011, the Company closed on a public offering of $60 million in aggregate principal amount of its 7.25% senior

notes due 2018 at a public offering price of 103.25% of the principal amount and $60 million in aggregate principal amount of its

7.75% senior notes due 2022 at a public offering price of 103.50%.

notes due 2018 at a public offering price of 103.25% of the principal amount and $60 million in aggregate principal amount of its

7.75% senior notes due 2022 at a public offering price of 103.50%.

(3) Based on 2010 and 2009 Adjusted EBITDA of $427.4 million and $383.0 million, respectively; reconciliation to GAAP provided on

slides 38 and 86-90.

slides 38 and 86-90.

(4) Based on debt balances as of December 31, 2010 and assumes 3 month LIBOR of 0.302%.

43

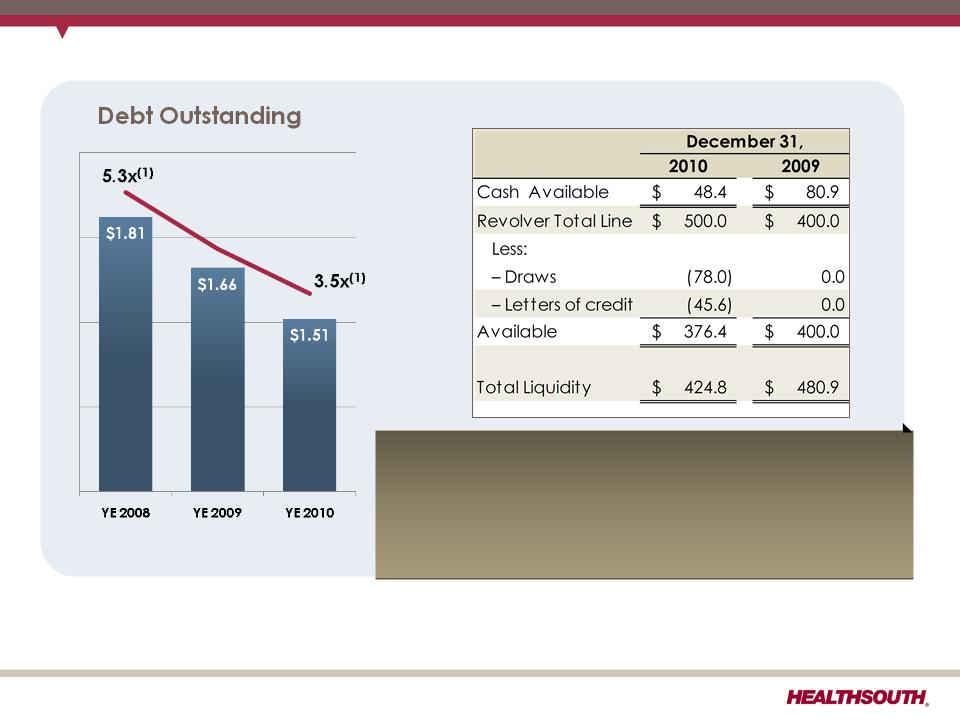

Exhibit 99.1

(1) Based on 2008 and 2010 Adjusted EBITDA of $341.2 million and $427.4 million, respectively; reconciliation to GAAP provided on slides 38

and 86-90.

and 86-90.

(2) Cash settlements flow through investing activities for swaps that do not qualify for hedge accounting. Net notional amount of $884 million

receives 3-month LIBOR and pays 5.22% fixed until expiration in March of 2011.

receives 3-month LIBOR and pays 5.22% fixed until expiration in March of 2011.

(3) Forward-starting interest rate swaps (designated as cash flow hedges) were terminated as part of the refinancing in October of 2010.

Debt, Liquidity, and Swaps

Swaps (2)(3)

The final cash settlement on our net $884 million swaps

for $10.9 million will be made in Q1 2011.

for $10.9 million will be made in Q1 2011.

Liquidity

44

Exhibit 99.1

(2) Includes $77.0 million of the net proceeds from the notes reopening. We intend to use this portion of the net proceeds to redeem a

portion of the 10.75% senior notes.

portion of the 10.75% senior notes.

Debt Maturity Profile (1)

45

|

|

S&P

|

Moodys

|

|

Corporate

Rating |

B+

|

B1

|

|

Revolver Rating

|

BB

|

Ba1

|

|

Senior Notes

Rating |

B+

|

B2

|

Call schedule:

June 15, 2011 (price 105.375);

June 15, 2012 (price 103.583);

June 15, 2013 (price 101.792);

June 15, 2014 and thereafter

(price 100.000)

(price 100.000)

Pro Forma for Notes Re-opening

$46 LC

$500

Revolver

L+350

Exhibit 99.1

Credit Agreement Key Covenant Comparison (1)

(October 2010)

|

|

Old Agreement

|

New Agreement

|

|

Acquisitions

|

$300 million per annum

|

Limited by compliance with leverage and

interest coverage covenants initially established at 5.0x and 2.5x respectively |

|

Restricted payments:

|

|

|

|

10.75% repurchase

|

No specific basket (see other

debt repurchase) |

Unlimited up to 4.5x leverage ratio (revolver

draws available for repurchase) |

|

Share repurchase (2)

|

$50 million per annum

|

$200 million (shared with other debt

repurchase basket) |

|

Other debt repurchase (2)

|

~$200 million remaining from all

relevant repurchase baskets |

$200 million (shared with other debt

repurchase basket) |

|

Unsecured debt issuance

|

$200 million

|

Unlimited up to 4.5x leverage ratio

|

46

(1) Full agreement filed November 23, 2010.

(2) Under the new agreement, the maximum amount limitations above are subject to increase by a “grower” basket equal to 50% of

excess cash flow plus certain other amounts including net cash proceeds from certain equity issuances.

excess cash flow plus certain other amounts including net cash proceeds from certain equity issuances.

Exhibit 99.1

|

Sources

|

$ Million (1)

|

Assumed

Call Price (3) |

Annual

Cash Savings

|

|

Cash on hand

|

$100.0

|

105.375

|

$10.2

|

|

|

|

|

|

|

Revolving credit facility (LIBOR + 350 bps)(2)

|

$100.0

|

105.375

|

$6.4

|

|

|

|

|

|

|

New senior notes (assumed yield of 7.00%)

|

$100.0

|

105.375

|

$3.2

|

|

Accounting effect for early repayment/ refinancing :

|

|||

|

“Loss on early extinguishment of debt” = ~$8 million per $100 million of the 10.75% senior notes.

|

|||

|

|

|||

Options for Addressing the 10.75% Senior Notes

(millions)

(1) Illustrative only

(2) Assumes 3M LIBOR of 0.302%

(3) Call schedule: June 15, 2011 (price 105.375); June 15, 2012 (price 103.583); June 15, 2013 (price 101.792); June 15, 2014 and

thereafter (price 100.000)

thereafter (price 100.000)

We can utilize a number of sources to repay/refinance the 10.75% notes.

Illustration of Potential Interest Expense Reduction by Funding Source

47

Exhibit 99.1

Use of the Revolver to Refinance the 10.75% Notes

• Liquidity should be sufficient to address:

– Short-term disruptions to the financial system

– Short-term disruptions to our business

– Unforeseen cash requirements

• Liquidity target has both objective and subjective components

– The Company’s current target is ~$250 million.

• Liquidity target subject to change based on:

– Economic developments

– Conditions in the financial markets

– Continued balance sheet deleveraging

– Regulatory change

– Growth in our business

48

Refinancing capacity within the revolver is limited by liquidity

considerations

Exhibit 99.1

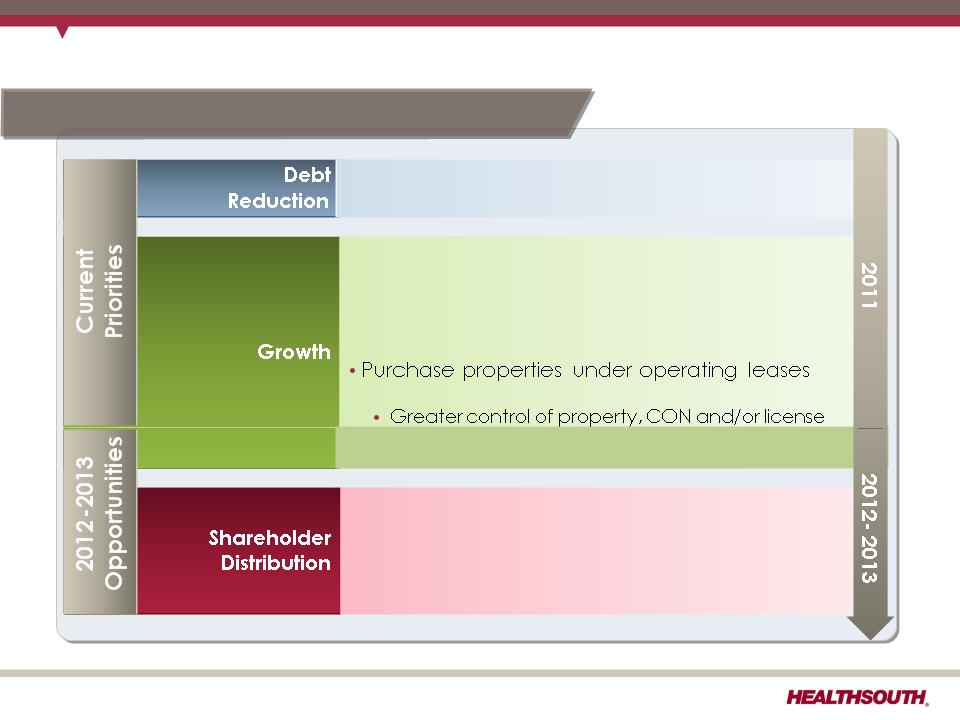

Deleveraging: Summary

• Deleveraging the balance sheet remains a priority.

• The 10.75% notes have an initial call date of June 2011 and represent

our most attractive debt repayment/refinancing opportunity.

our most attractive debt repayment/refinancing opportunity.

• We have at least three potential funding sources for reducing the

10.75% notes:

10.75% notes:

Free Cash Flow

― Benefiting in 2011 due to the expiration of the interest rate swaps

― Will also be used to fund growth opportunities

― Capital allocation based predominately on economic returns

Revolving Credit Facility

― Capacity determined by liquidity considerations

New Debt Issuances

― Interest rate arbitrage opportunity determined by prevailing debt

market conditions

market conditions

49

Exhibit 99.1

Growth

50

Exhibit 99.1

Demographics

+ population growth and changes (weighted by age)

= Rehab CAGR

Growth goals for the market and/or hospital

Sales and Marketing Strategies

•Defining “upstream” opportunities

•Identifying CMS-13 discharges

•“Converting” CMS-13 patients to rehab

Market Dynamics

•Existing IRF beds

•Managed care penetration

•Competition

Organic Growth: A Strategic Framework

Bottoms-up approach

to HealthSouth’s

growth projections

to HealthSouth’s

growth projections

51

Exhibit 99.1

Organic Growth: Compounded Annual Growth Rate (CAGR) (1)

(1) Numbers in map are for illustrative purposes only and do not represent actual results.

(2)“Weighted for Rehab Services” - methodology weights growth in rehab age groups higher.

% CAGR

Rehab by Zip Code

Rehab by Zip Code

Weighted for Rehab Services (1) (2)

Organic Growth

•Demographic

changes

changes

•Population

growth

growth

% CAGR Weighted for Rehab Services

Treasure Coast Primary 2.64%

Treasure Coast SSA - Glades 1.47%

Treasure Coast SSA - Martin 2.92%

Okeechobee 2.34%

Treasure Coast Tertiary 2.24%

Combined 2.45%

State of Florida 2.72%

USA 2.31%

52

Exhibit 99.1

Market Selection Process

53

Active

Development

List

Development

List

Corporate

Priority

Assessment

Priority

Assessment

Strategic

Approach

Approach

•Build

•Buy

•JV

Regional

President

Assessment

President

Assessment

Existing IRF

Assessment

Assessment

Target

Opportunity List

Opportunity List

(160 opportunities

identified)

identified)

National

Market

Assessment

Market

Assessment

(3,141 counties in 48 states studied)

• Population and

Demographics

Demographics

• Acute Care Referral

Sources

Sources

• Inpatient Rehab

Competition

Competition

• Other Competitors

• Payor Environment

• CON/Non-CON

Exhibit 99.1

CON

Approval

Approval

Site

Selection

Selection

Cost

Assessment

Assessment

Pro forma

Financials

Financials

Execution

• Design

• Construction

NO

GO

GO

De Novo Evaluation Process

54

Market

Selection

Selection

GO

NO

GO

Exhibit 99.1

Illustrative De Novo Timeline

55

Day 1

CON Process

Construction

With CON

Design

Planning

& Zoning

Month 20

Groundbreaking

Month 32

Opening

Construction

Design

Planning

& Zoning

Month 11

Groundbreaking

Month 20

Opening

Day 1

Without CON

Exhibit 99.1

Illustrative De Novo Pro forma (40 bed)

56

|

Capital Cost

|

$ Range

|

|

|

(millions)

|

Low

|

High

|

|

Construction, design, permitting, etc.

|

$11.0

|

$14.5

|

|

Land

|

1.5

|

3.5

|

|

Equipment

|

2.5

|

3.0

|

|

|

$15.0

|

$21.0

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pre-opening Expenses

|

|

|

|

(thousands)

|

Low

|

High

|

|

Operating

|

$200

|

$300

|

|

Salaries, wages and benefits

|

150

|

200

|

|

|

$350

|

$500

|

|

|

|

|

|

|

|

|

Exhibit 99.1

(1) Hospital EBITDA = earnings before interest, taxes, depreciation and amortization directly attributable to the related hospital.

De Novo Occupancy and EBITDA(1) Trends

57

Sustained,

positive EBITDA

positive EBITDA

Sustained,

positive EBITDA

positive EBITDA

Occupancy

Sustained positive

EBITDA

EBITDA

Exhibit 99.1

IRF Acquisition Performance

58

|

|

Date Acquired

|

Acquired Census

|

Q4 2010 Census

|

|

Vineland

|

Q3 2008

|

26

|

34

|

|

Desert Canyon

|

Q2 2010

|

16

|

30

|

|

Sugar Land

|

Q3 2010

|

26

|

30

|

|

Ft. Smith

|

Q3 2010

|

15

|

37

|

Value added by HealthSouth

• TeamWorks approach to sales/marketing

• Labor management tools and “best practices”

• Clinical expertise

• Clinical technology and programming

• Supply chain efficiency

• Medical leadership and clinical advisory boards

Exhibit 99.1

Portfolio Growth

Cash Payback Period

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year

7

7

Acquisitions

De novos (1)

(1) Assumes average investment per bed: ~ $450K.

59

• Target: 2-3 de novos and acquisitions/yr

• All projects have minimum IRR of 15%.

• Longer payback on de novos versus

acquisitions is attributable to:

acquisitions is attributable to:

- 12-15 month construction period

- Initial ramp-up of operations on de novos

Exhibit 99.1

60

Acute Care

Hospital

Hospital

Discharge

Hospice

Inpatient

Rehabilitation

Facility (1)

Rehabilitation

Facility (1)

Skilled

Nursing

Facility

Nursing

Facility

Home

Health (1)

Health (1)

(Highest Acuity)

(Lowest Acuity)

Future Growth: Complementary Post-Acute Care Services

Source: MedPac, CMS and Wall Street research

(1) For information on HealthSouth’s hospital portfolio, see slide 4.

Exhibit 99.1

• Growth strategies will complement deleveraging priority.

- “Highest and best use” of FCF will determine where to invest.

• The company continues to have excellent organic growth opportunities.

- Locations in above-average “Rehab CAGR” markets

- Non-discretionary nature of many conditions served

- Track record of consistent market share gains

• De novos and targeted IRF acquisitions will allow entry to, and growth in,

new markets.

new markets.

- Disciplined evaluation process

- Proven track record of success

• Longer-term consideration of acquiring complementary post-acute

services predicated on:

services predicated on:

- Achieving deleveraging objective

- Obtaining regulatory clarity

- Favorable market conditions

Growth: Summary

61

Exhibit 99.1

Operational Initiatives

62

Exhibit 99.1

Key Operational Initiatives: Summary

• Strong track record of providing high-quality, cost-effective care

– Functional gains exceed industry norms

– Consistent market share gains

– Disciplined expense management

• Targeted operational strategies to achieve excellence in:

– Clinical care (Care Management; reduced Acute Care Transfers)

– Operations (BEACON; patient scheduling; supply chain)

– Service (CPR; “customer training”)

• Implementation of a Clinical Information System

– Rehabilitation-specific (Cerner)

– Manageable, five-year rollout beginning in 2012

63

Exhibit 99.1

Operational Strategy

Excellence in …

64

• Initiate Care

Management

TeamWorks project

Management

TeamWorks project

• Identify trends and

establish “best

practices” for the

prevention of

acute care transfers

establish “best

practices” for the

prevention of

acute care transfers

• Provide a robust

rehabilitation

specific clinical

education program

for nurses and

therapists

rehabilitation

specific clinical

education program

for nurses and

therapists

• Develop and roll out

BEACON

management

reporting system

BEACON

management

reporting system

• Evaluate options for

and pilot patient

scheduling systems

and pilot patient

scheduling systems

• Standardize

pharmacy and food

supplies purchasing

pharmacy and food

supplies purchasing

• Implement new

patient satisfaction

survey tool through

Press Ganey

patient satisfaction

survey tool through

Press Ganey

• Launch CPR

(Comfort,

Professionalism,

Respect) patient

experience

campaign

(Comfort,

Professionalism,

Respect) patient

experience

campaign

• Develop and

implement

customer training

videos for hospital

staff

implement

customer training

videos for hospital

staff

Clinical Care

Operations

Service

Exhibit 99.1

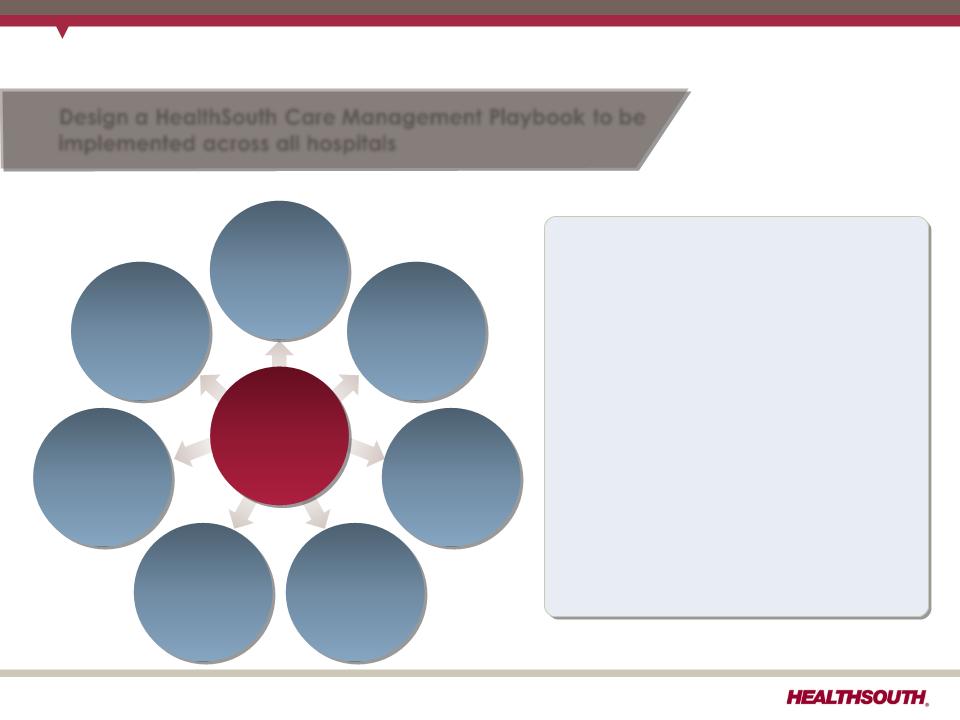

TeamWorks: Care Management

65

Goals

•Improve overall operational,

patient care and satisfaction

outcomes

patient care and satisfaction

outcomes

•Streamline delivery of care

•Engage interdisciplinary teams

•Reduce:

― Complication rate

― Cost per case

― Payor denials

•Increase:

― Reimbursement

― Patient involvement in care

decisions

decisions

Design a HealthSouth Care Management Playbook to be

implemented across all hospitals

implemented across all hospitals

Referral Management

Pre-authorization / Pre-

certification

certification

Patient Assessment

Care Delivery &

Documentation

Documentation

Interdisciplinary Team

Process

Process

Denials & Approvals

Outcomes Analysis

Effective & Efficient

Care Management

Care Management

Exhibit 99.1

Pilot Process

Finalize Training

Modules

Modules

Implement

October - November 2010

Test the application of the

newly designed Playbook,

tools, processes and forms.

Gather feedback and

improve the process for the

2011 implementation.

newly designed Playbook,

tools, processes and forms.

Gather feedback and

improve the process for the

2011 implementation.

December 2010

Review pilot findings and

finalize Playbook and

training.

finalize Playbook and

training.

January 2011

Begin training and

communicate company-wide

implementation strategy.

communicate company-wide

implementation strategy.

TeamWorks: Care Management Project Overview

66

– July 2009 Core team assembled

Current State

Assessment

Assessment

Future State Vision

Design Process

May - June 2010

KPMG visited 10 hospitals (2

within each region) to assess

and document the current

state of the case

management process. Site

visits included interviews,

observation, and

documentation review.

within each region) to assess

and document the current

state of the case

management process. Site

visits included interviews,

observation, and

documentation review.

July 2010

KPMG facilitated an

Accelerated Solutions

Design (ASD) 30-day session

with 23 HealthSouth

employees. The team laid

the framework for the

desired future state of case

management.

Accelerated Solutions

Design (ASD) 30-day session

with 23 HealthSouth

employees. The team laid

the framework for the

desired future state of case

management.

August - September 2010

17 of the HealthSouth

employees involved in the ASD

returned for a 3-week design

session. The team developed or

updated tools and templates

to support the future state. Their

body of work was combined to

form the HealthSouth Care

Management Playbook.

employees involved in the ASD

returned for a 3-week design

session. The team developed or

updated tools and templates

to support the future state. Their

body of work was combined to

form the HealthSouth Care

Management Playbook.

Exhibit 99.1

CPR: Comfort, Professionalism, Respect

• All employees will be trained in the CPR campaign.

• Hospital-based trained facilitators will work directly with

employees.

employees.

• A series of short videos is used to depict common scenarios of

patient/staff situations.

patient/staff situations.

• Facilitator training is highly interactive, encouraging discussions

among staff.

among staff.

CPR is an in-house course designed to train all employees to

realize that even minor encounters between staff and

patients can have a memorable impact on the patient’s

entire experience.

realize that even minor encounters between staff and

patients can have a memorable impact on the patient’s

entire experience.

Ultimate goal is to improve employee-to

-patient interactions, leading to:

-patient interactions, leading to:

•Improved patient satisfaction scores

•Reduced patient complaints

•More satisfied employees

67

Exhibit 99.1

68

Exhibit 99.1

69

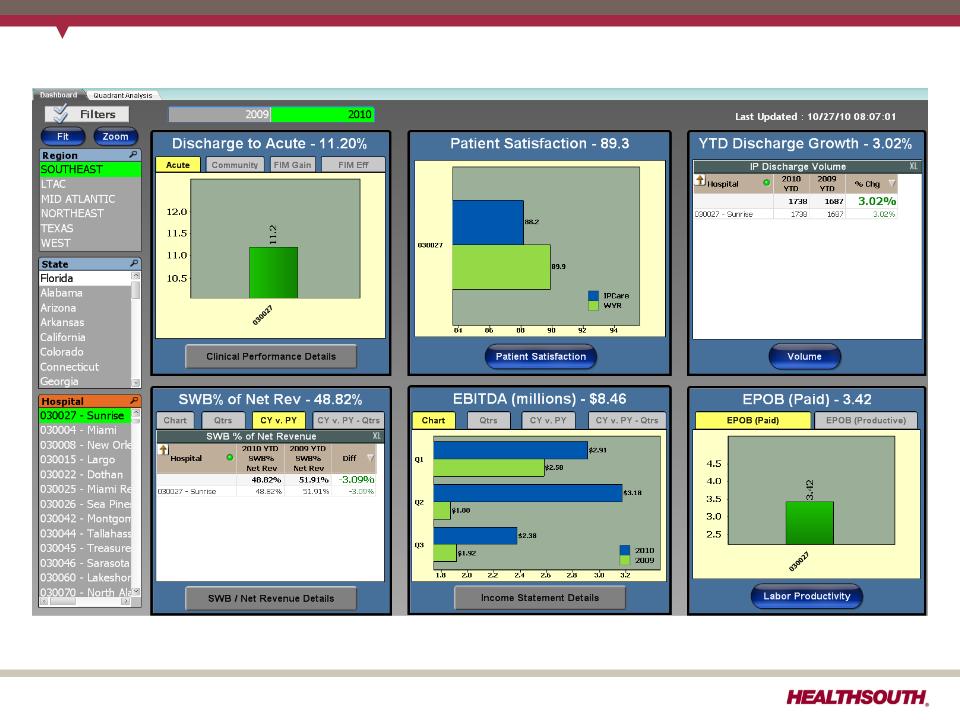

BEACON: Hospital-Specific (1)

(1) Numbers in screen shot have been modified for presentation and do not represent actual results.

Exhibit 99.1

70

BEACON: Regional Roll-up (1)

(1) Numbers in screen shot have been modified for presentation and do not represent actual results.

Exhibit 99.1

Clinical Information Systems in Healthcare

• Clinical information systems (CIS) are a key component of

successful quality, safety and patient satisfaction initiatives in

healthcare.

successful quality, safety and patient satisfaction initiatives in

healthcare.

• Hospitals that implemented Computerized Physician Order

Entry (CPOE) reported better quality of care and lower

mortality rates according to a recent study. (1)

Entry (CPOE) reported better quality of care and lower

mortality rates according to a recent study. (1)

• 2008 100 Most Wired Hospitals achieved significantly better

quality indicators than other hospitals via: (2)

quality indicators than other hospitals via: (2)

– Mortality rate

– Patient safety index

– Core measures index

CIS adoption is not solely responsible for these results,

AND … adoption of CIS in healthcare is very slow!

AND … adoption of CIS in healthcare is very slow!

71

(1) Source: Joint Commission Journal on Quality and Patient Safety, June 2008

(2) Source: The 100 Most Wired Hospitals and Health Systems 2008, Hospitals and Health Networks, July 2008

Exhibit 99.1

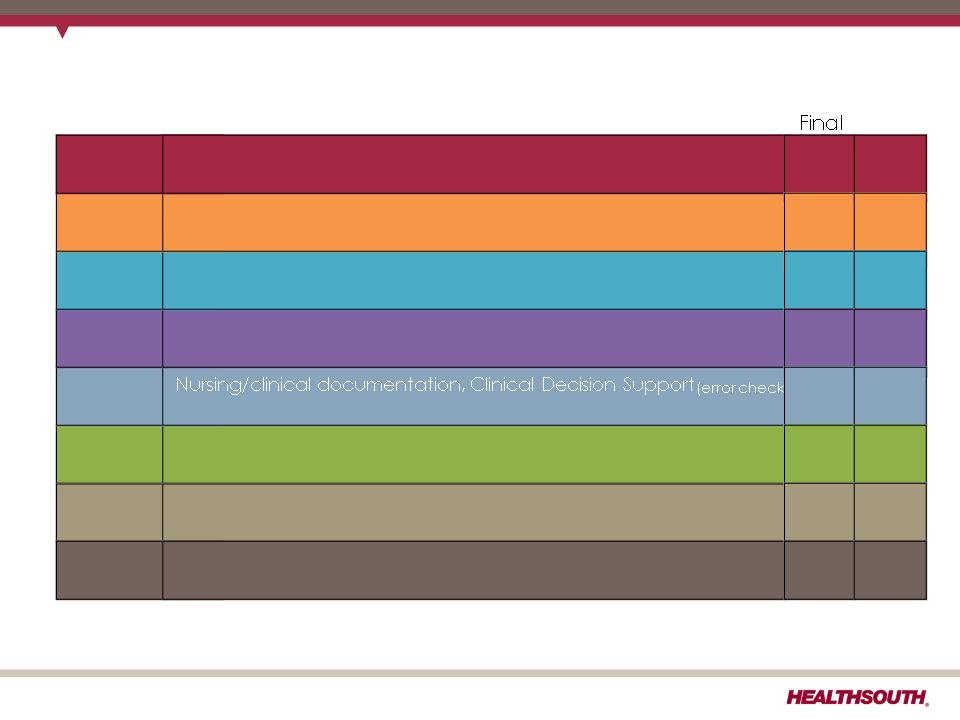

Source: HIMSS AnalyticsTM Database

Stage 2

Clinical Data Repository, Controlled Medical Vocabulary,

may have Document Imaging; Health Info Exchange capable

Stage 3

Digital Radiology

Stage 4

Computerized Physician Order Enter,

Clinical Decision Support (clinical protocols)

Stage 5

Closed loop medication administration, 5 rights with bar code

Stage 6

Physician documentation (structured templates), full Clinical

Decision Support (variance & compliance), full Digital Imaging

Stage 7

Complete EMR; standardized transactions to share data; Data

warehousing; Data continuity with Emergency Dept, ambulatory

Stage 1

Ancillaries - Lab, Radiology, Pharmacy - All Installed

Stage 0

All Three Ancillaries - Lab, Radiology, Pharmacy Not Installed

2005

0.0%

0.0%

.001%

2.5%

10.0%

48.8%

19.6%

18.4%

0.7%

1.6%

3.8%

7.4%

50.9%

16.9%

7.2%

2009

Final

11.5%

2005-2009 Electronic Medical Record (EMR) Adoption

Model Trends

(5,235 non-federal acute care U.S. hospitals)

Model Trends

(5,235 non-federal acute care U.S. hospitals)

72

Exhibit 99.1

EMR Adoption Model

• Most U.S. hospitals are at Stage 3

(Foundation Stage) or below.

(Foundation Stage) or below.

• Stages 0, 1 and 2 are slowing.

• Stage 3 is growing the fastest.

– 10% in 2005 - 50.9% in 2009

• Advanced Stages 3 through 7:

– Require only one service or unit

to be implemented

to be implemented

– Reduce medical errors and

improve clinical outcomes

improve clinical outcomes

• Stage 5 is the most difficult to achieve.

– Integration, technology and reengineering requirements

– Significant investment in capital, executive commitment and culture adoption

• Over 86% of U.S. Hospitals do NOT have CPOE (computerized physician

order entry) implemented.

order entry) implemented.

73

Exhibit 99.1

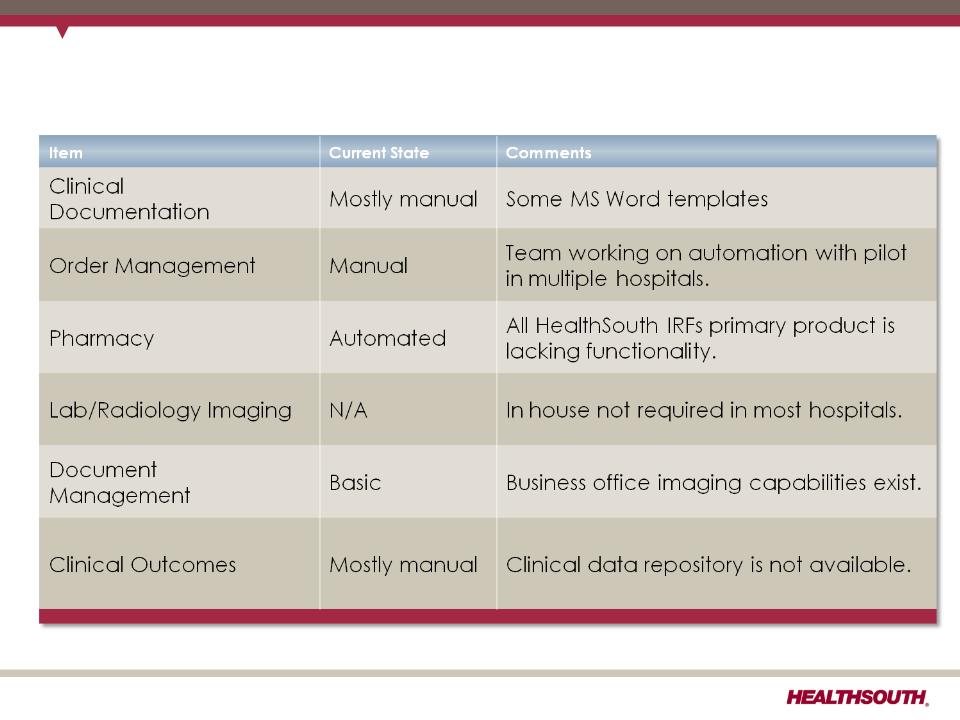

HealthSouth Clinical Information Technology

Current State

Current State

74

Exhibit 99.1

Vendor Selection Process

75

2005

Request for

Proposal

Proposal

2007

Project on

hold

hold

2009

Cerner final

selection

selection

July 2009

Core team

assembled

assembled

13 vendors

responded;

3 finalists

responded;

3 finalists

Due to

business unit

divestitures

business unit

divestitures

Why Cerner?

• Inpatient

rehabilitation-specific

application

rehabilitation-specific

application

• Integrated solution

meeting all functional

requirements

meeting all functional

requirements

• Enterprise capable

vendor with scalability

vendor with scalability

• Positive references

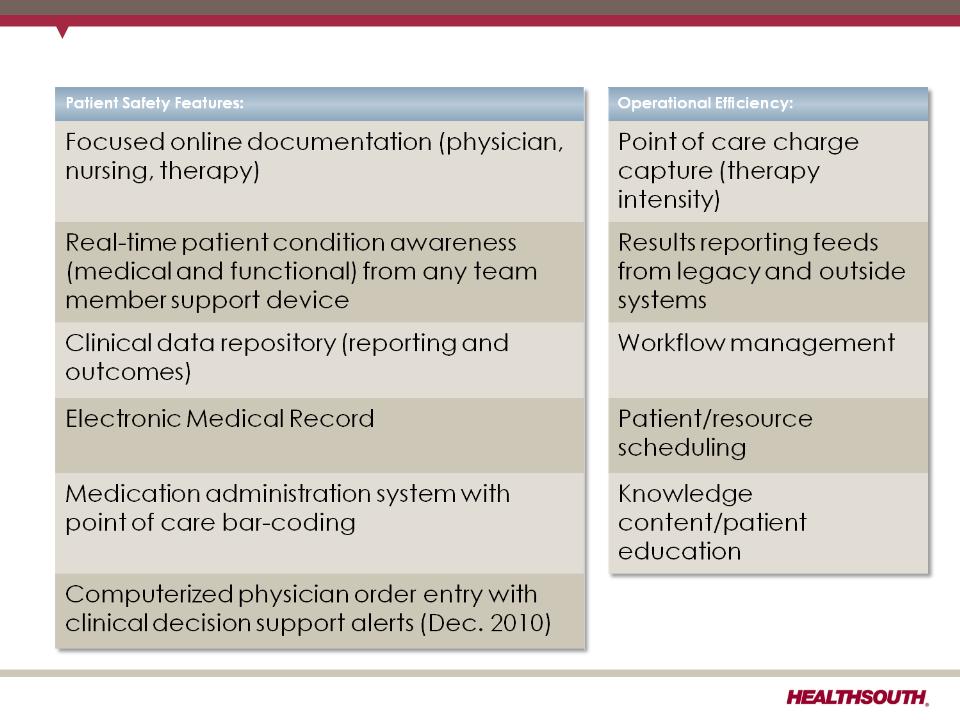

Exhibit 99.1

Key Features

76

Exhibit 99.1

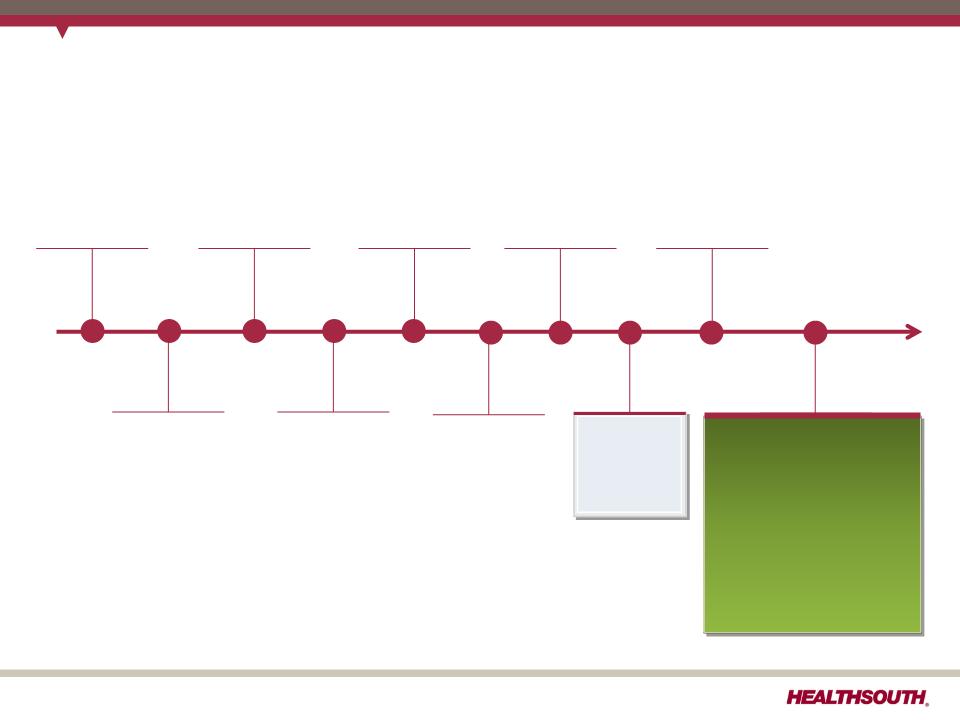

Project Timeline

77

Project On Hold

(Divestitures)

2007

Clinical

Visioning

2005

Cerner

Selected

Feb 2009

Vendor

Evaluations

2006

Project Restart

& Vendor

& Vendor

Re-evaluations

2008

Pilot

Contract

Contract

Negotiation

Jun 2009

Pilot

“Go-Live”

Jun 2010

Pilot Project

Kickoff

Aug 2009

Benefits

Recognition

Study (“BRS”)

Jul - Dec 2010

Next Steps

•Analyze BRS

•Review with Board

•Finalize Vendor

Negotiations

Negotiations

•Plan

Implementation

Implementation

Exhibit 99.1

Operational Metrics

78

Exhibit 99.1

(1) Data provided by UDSMR, a data gathering and analysis organization for the rehabilitation industry; represents ~ 65-70% of industry,

including HealthSouth sites.

including HealthSouth sites.

(2) Includes consolidated HealthSouth inpatient rehabilitation hospitals and long-term acute care hospitals classified as same store during

that time period.

that time period.

Historic Discharge Growth vs. Industry

• HealthSouth’s

volume growth has

outpaced

competitors’.

volume growth has

outpaced

competitors’.

• TeamWorks =

standardized and

enhanced sales &

marketing

standardized and

enhanced sales &

marketing

• Bed additions will

help facilitate

continued organic

growth.

help facilitate

continued organic

growth.

UDS Industry Sites (1)

HLS Same Store (2)

10.7%

9.4%

5.6%

2.6%

4.6%

5.5%

5.8%

5.8%

5.3%

2.5%

2.2%

1.1%

79

Exhibit 99.1

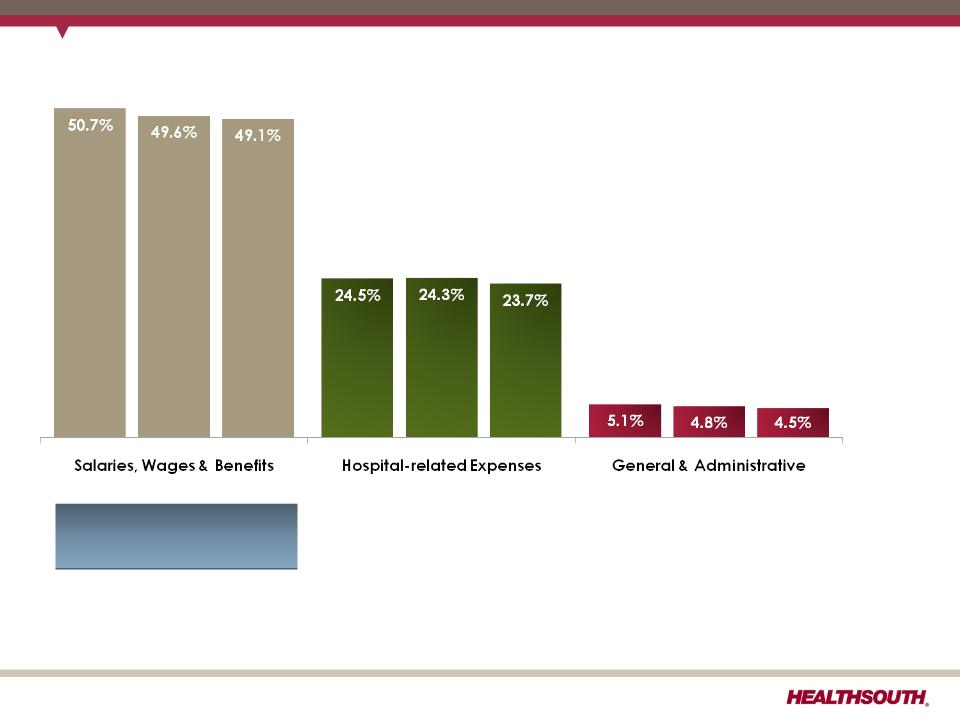

Operational Metrics: Expense Efficiencies

(% of Net Operating Revenues)

2008 2009 2010 2008 2009 2010 2008 2009 2010

3.62 3.53 3.50

EPOB

• Salaries, Wages & Benefits reflects continued improvement from

productivity gains.

productivity gains.

• Hospital-related Expenses includes other operating, supplies,

occupancy, and bad debts expenses.

occupancy, and bad debts expenses.

• General and Administration excludes stock-based compensation.

• Employee per Occupied Bed “EPOB” is calculated by dividing the

number of full-time equivalents, including an estimate of full-time

equivalents from the utilization of contract labor, by the number of

occupied beds during each period. The number of occupied beds

is determined by multiplying the number of licensed beds by the

Company’s occupancy percentage.

number of full-time equivalents, including an estimate of full-time

equivalents from the utilization of contract labor, by the number of

occupied beds during each period. The number of occupied beds

is determined by multiplying the number of licensed beds by the

Company’s occupancy percentage.

80

Exhibit 99.1

(3) Excludes approximately 400 full-time equivalents, who are considered part of corporate overhead with their salaries and benefits

included in general and administrative expenses in the Company’s consolidated statements of operations. Full-time equivalents

included in the above table represent HealthSouth employees who participate in or support the operations of the Company’s

hospitals.

included in general and administrative expenses in the Company’s consolidated statements of operations. Full-time equivalents

included in the above table represent HealthSouth employees who participate in or support the operations of the Company’s

hospitals.

(4) Employees per occupied bed, or “EPOB,” is calculated by dividing the number of full-time equivalents, including an estimate of full-

time equivalents from the utilization of contract labor, by the number of occupied beds during each period. The number of occupied

beds is determined by multiplying the number of licensed beds by the Company’s occupancy percentage.

time equivalents from the utilization of contract labor, by the number of occupied beds during each period. The number of occupied

beds is determined by multiplying the number of licensed beds by the Company’s occupancy percentage.

81

Exhibit 99.1

Payment Sources

(1) Managed Medicare revenues represent ~ 8%, 7%, 8%, and 8% of total revenues for Q4 2010, Q4 2009, 2010, and 2009, respectively, and

are included in “Managed care and other discount plans.”

are included in “Managed care and other discount plans.”

82

Exhibit 99.1

Value Proposition

83

Exhibit 99.1

(1) Reconciliation to GAAP provided on slides 38-39 and 86-90.

The HealthSouth Value Proposition

Poised for Growth

Financial Strength/Strong

Cash Flow Generation

Cash Flow Generation

Industry Leading Position

Attractive Healthcare Sector

84

Exhibit 99.1

Reconciliation to GAAP

85

Exhibit 99.1

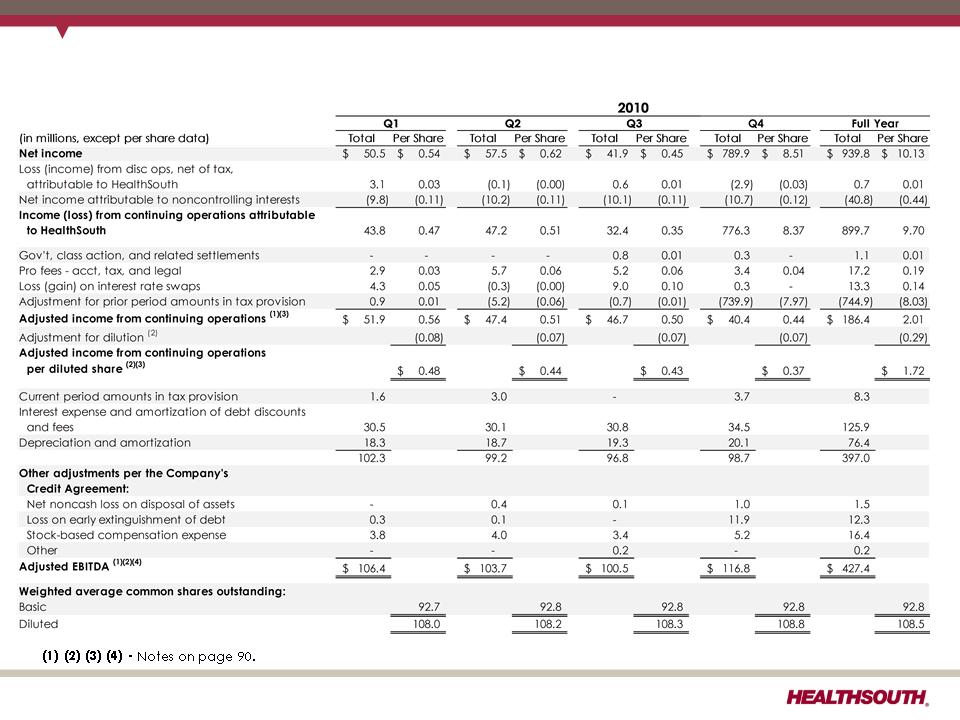

Reconciliation of Net Income to Adjusted Income from Continuing Operations and

Adjusted EBITDA (1) (3) (4)

Adjusted EBITDA (1) (3) (4)

86

Exhibit 99.1

(1) (2) (3) (4) - Notes on page 90.

87

Exhibit 99.1

(1) (2) (3) (4) - Notes on page 90.

88

Exhibit 99.1

89

(1) (2) (3) (4) - Notes on page 90.

Exhibit 99.1

Reconciliation Notes

1. Adjusted income from continuing operations and Adjusted EBITDA are non-GAAP

financial measures. The Company’s leverage ratio (total consolidated debt to

Adjusted EBITDA for the trailing four quarters) is, likewise, a non-GAAP financial

measure. Management and some members of the investment community utilize

adjusted income from continuing operations as a financial measure and Adjusted

EBITDA and the leverage ratio as liquidity measures on an ongoing basis. These

measures are not recognized in accordance with GAAP and should not be viewed as

an alternative to GAAP measures of performance or liquidity. In evaluating these

adjusted measures, the reader should be aware that in the future HealthSouth may

incur expenses similar to the adjustments set forth above.

financial measures. The Company’s leverage ratio (total consolidated debt to

Adjusted EBITDA for the trailing four quarters) is, likewise, a non-GAAP financial

measure. Management and some members of the investment community utilize

adjusted income from continuing operations as a financial measure and Adjusted

EBITDA and the leverage ratio as liquidity measures on an ongoing basis. These

measures are not recognized in accordance with GAAP and should not be viewed as

an alternative to GAAP measures of performance or liquidity. In evaluating these

adjusted measures, the reader should be aware that in the future HealthSouth may

incur expenses similar to the adjustments set forth above.

2. Per share amounts for each period presented are based on basic weighted average

common shares outstanding for all amounts except adjusted income from continuing

operations per diluted share, which is based on diluted weighted average shares

outstanding. The difference in shares between the basic and diluted shares

outstanding is primarily related to our convertible perpetual preferred stock.

common shares outstanding for all amounts except adjusted income from continuing

operations per diluted share, which is based on diluted weighted average shares

outstanding. The difference in shares between the basic and diluted shares

outstanding is primarily related to our convertible perpetual preferred stock.

3. Adjusted income from continuing operations per diluted share and Adjusted EBITDA

are two components of our historical guidance.

are two components of our historical guidance.

4. The Company’s credit agreement allows certain other items to be added to arrive at

Adjusted EBITDA, and there may be certain other deductions required.

Adjusted EBITDA, and there may be certain other deductions required.

90

Exhibit 99.1