UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

[x] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition period from to

Commission File Number 1-5532-99

PORTLAND GENERAL ELECTRIC COMPANY | ||

(Exact name of registrant as specified in its charter) | ||

Oregon | 93-0256820 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

121 SW Salmon Street

Portland, Oregon 97204

(503) 464-8000

(Address of principal executive offices, including zip code,

and Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, no par value | New York Stock Exchange |

(Title of class) | (Name of exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [x] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [x] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [x]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | [x] | Accelerated filer | [ ] | |||

Non-accelerated filer | [ ] | Smaller reporting company | [ ] | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [x]

As of June 30, 2011, the aggregate market value of voting common stock held by non-affiliates of the Registrant was $1,900,588,219. For purposes of this calculation, executive officers and directors are considered affiliates.

As of February 17, 2012, there were 75,367,284 shares of common stock outstanding.

Documents Incorporated by Reference

Part III, Items 10 - 14 | Portions of Portland General Electric Company’s definitive proxy statement to be filed pursuant to Regulation 14A for the 2012 Annual Meeting of Shareholders to be held on May 23, 2012. |

PORTLAND GENERAL ELECTRIC COMPANY

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2011

TABLE OF CONTENTS

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

Item 15. | |||

3

DEFINITIONS

The following abbreviations or acronyms used throughout this Form 10-K are defined below:

Abbreviation or Acronym | Definition | |

AFDC | Allowance for funds used during construction | |

AUT | Annual Power Cost Update Tariff | |

Beaver | Beaver natural gas-fired generating plant | |

Biglow Canyon | Biglow Canyon Wind Farm | |

Boardman | Boardman coal-fired generating plant | |

BPA | Bonneville Power Administration | |

CAA | Clean Air Act | |

Colstrip | Colstrip Units 3 and 4 coal-fired generating plant | |

Coyote Springs | Coyote Springs Unit 1 natural gas-fired generating plant | |

Dth | Decatherm = 10 therms = 1,000 cubic feet of natural gas | |

DEQ | Oregon Department of Environmental Quality | |

EPA | United States Environmental Protection Agency | |

ESA | Endangered Species Act | |

ESS | Electricity Service Supplier | |

FERC | Federal Energy Regulatory Commission | |

IRP | Integrated Resource Plan | |

ISFSI | Independent Spent Fuel Storage Installation | |

kV | Kilovolt = one thousand volts of electricity | |

kW | Kilowatt = one thousand watts of electricity | |

kWh | Kilowatt hours | |

Moody’s | Moody’s Investors Service | |

MW | Megawatts | |

MWa | Average megawatts | |

MWh | Megawatt hours | |

NRC | Nuclear Regulatory Commission | |

NVPC | Net Variable Power Costs | |

OATT | Open Access Transmission Tariff | |

OEQC | Oregon Environmental Quality Commission | |

OPUC | Public Utility Commission of Oregon | |

PCAM | Power Cost Adjustment Mechanism | |

Port Westward | Port Westward natural gas-fired generating plant | |

REP | Residential Exchange Program | |

RPS | Renewable Portfolio Standard | |

S&P | Standard & Poor’s Ratings Services | |

SEC | United States Securities and Exchange Commission | |

SIP | Oregon Regional Haze State Implementation Plan | |

Trojan | Trojan nuclear power plant | |

USDOE | United States Department of Energy | |

VIE | Variable interest entity | |

4

PART I

ITEM 1. BUSINESS.

General

Portland General Electric Company (PGE or the Company) was incorporated in 1930 and is a vertically integrated electric utility engaged in the generation, purchase, transmission, distribution, and retail sale of electricity in the state of Oregon. PGE operates as a cost-based, regulated electric utility, with revenue requirements and customer prices determined based on the forecasted cost to serve retail customers, and a reasonable rate of return as determined by the Public Utility Commission of Oregon (OPUC). The Company’s retail load requirement is met with both Company-owned generation and power purchased in the wholesale market. The Company also participates in the wholesale market by purchasing and selling electricity and natural gas in order to obtain reasonably-priced power for its retail customers. PGE is publicly-owned, with its common stock listed on the New York Stock Exchange, and operates as a single segment, with revenues and costs related to its business activities maintained and analyzed on a total electric operations basis.

PGE’s state-approved service area allocation of approximately 4,000 square miles is located entirely within Oregon and includes 52 incorporated cities, of which Portland and Salem are the largest. The Company estimates that at the end of 2011 its service area population was 1.7 million, comprising approximately 44% of the state’s population. During 2011, the Company added 1,790 customers and as of December 31, 2011, served a total of 822,466 retail customers.

PGE had 2,634 employees as of December 31, 2011, with 840 employees covered under two separate agreements with Local Union No. 125 of the International Brotherhood of Electrical Workers. Such agreements cover 804 and 36 employees and expire in February 2015 and August 2014, respectively.

Available Information

PGE’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available and may be accessed free of charge through the Investors section of the Company’s Internet website at www.portlandgeneral.com as soon as reasonably practicable after the reports are electronically filed with, or furnished to, the United States Securities and Exchange Commission (SEC). It is not intended that PGE’s website and the information contained therein or connected thereto be incorporated into this Annual Report on Form 10-K. Information may also be obtained via the SEC Internet website at www.sec.gov.

5

Regulation and Rates

PGE is subject to both federal and state regulation, which can have a significant impact on the operations of the Company. In addition to those agencies and activities discussed below, the Company is subject to regulation by certain environmental agencies, as described in the Environmental Matters section in this Item 1.

Federal Regulation

PGE is subject to regulation by several federal agencies, including the Federal Energy Regulatory Commission (FERC), the U.S. Department of Transportation’s Pipeline and Hazardous Materials Safety Administration (PHMSA), and the Nuclear Regulatory Commission (NRC).

FERC Regulation

The Company is a “licensee,” a “public utility,” and a “user, owner and operator of the bulk power system,” as defined in the Federal Power Act, and is subject to regulation by the FERC in matters related to wholesale energy activities, transmission services, reliability standards, natural gas pipelines, hydroelectric projects, accounting policies and practices, short-term debt issuances, and certain other matters.

Wholesale Energy—PGE has authority under its FERC Market-Based Rates tariff to charge market-based rates for wholesale energy sales. Re-authorization for continued use of such rates requires the filing of triennial market power studies with the FERC. The Company’s next triennial market power study is due in June 2013.

Transmission—PGE offers transmission service pursuant to its Open Access Transmission Tariff (OATT), which is filed with the FERC. As required by the OATT, PGE provides information regarding its transmission business on its Open Access Same-time Information System, also known as OASIS. As of December 31, 2011, PGE owned approximately 1,100 circuit miles of transmission lines. For additional information, see the Transmission and Distribution section in this Item 1. and in Item 2.—“Properties.”

Reliability and Cyber Security Standards—Pursuant to the Energy Policy Act of 2005 (EPAct 2005), the FERC has adopted mandatory reliability standards for owners, users and operators of the bulk power system. Such standards, which are applicable to PGE, were developed by the North American Electric Reliability Corporation (NERC) and the Western Electricity Coordinating Council (WECC), which has responsibility for compliance and enforcement of these standards. These standards include Critical Infrastructure Protection standards, a set of cyber security standards that provide a framework to identify and protect critical cyber assets used to support reliable operation of the bulk power system.

Pipeline—The Natural Gas Act of 1938 and the Natural Gas Policy Act of 1978 provide the FERC authority in matters related to the extension, enlargement, safety, and abandonment of jurisdictional pipeline facilities, as well as transportation rates and accounting for interstate natural gas commerce. PGE is subject to such authority as the Company has a 79.5% ownership interest in and is the operator of record of the Kelso-Beaver Pipeline, a 17-mile interstate pipeline that provides natural gas to its Port Westward and Beaver plants. As the operator of record, PGE is subject to the requirements and regulations enacted under the Pipeline Safety Laws administered by the PHMSA, which include safety standards, operator qualification standards and public awareness requirements.

Hydroelectric Licensing—Under the Federal Power Act, PGE’s hydroelectric generating plants are subject to FERC licensing requirements. These include an extensive public review process that involves the consideration of numerous natural resource issues and environmental conditions. PGE holds FERC licenses for the Company’s projects on the Deschutes, Clackamas, and Willamette Rivers. For additional information, see the Environmental Matters section in this Item 1.

Accounting Policies and Practices—Pursuant to applicable provisions of the Federal Power Act, PGE prepares financial statements in accordance with the accounting requirements of the FERC, as set forth in its applicable

6

Uniform System of Accounts and published accounting releases. Such financial statements are included in annual and quarterly reports filed with the FERC.

Short-term Debt—Pursuant to applicable provisions of the Federal Power Act and FERC regulations, regulated public utilities are required to obtain FERC approval to issue certain securities. The Company, pursuant to an order issued by the FERC on December 28, 2011, is authorized to issue up to $700 million of short-term debt through February 6, 2014.

NRC Regulation

The NRC regulates the licensing and decommissioning of nuclear power plants, including PGE’s Trojan nuclear power plant (Trojan), which was closed in 1993. The NRC approved the 2003 transfer of spent nuclear fuel from a spent fuel pool to a separately licensed dry cask storage facility that will house the fuel on the plant site until a U.S. Department of Energy (USDOE) facility is available. Radiological decommissioning of the plant site was completed in 2004 under an NRC-approved plan, with the plant’s operating license terminated in 2005. Spent fuel storage activities will continue to be subject to NRC regulation until all nuclear fuel is removed from the site and radiological decommissioning of the storage facility is completed.

State of Oregon Regulation

PGE is subject to the jurisdiction of the OPUC, which is comprised of three members appointed by Oregon’s governor to serve non-concurrent four-year terms.

The OPUC reviews and approves the Company’s retail prices (see “Ratemaking” below) and establishes conditions of utility service. In addition, the OPUC regulates the issuance of securities, prescribes accounting policies and practices, and reviews applications to sell utility assets, engage in transactions with affiliated companies, and acquire substantial influence over a public utility. The OPUC also reviews the Company’s generation and transmission resource acquisition plans, pursuant to an integrated resource planning process. For additional information on the integrated resource planning process, see Power Supply section of this Item 1.

Oregon’s Energy Facility Siting Council (EFSC) has regulatory and siting responsibility for large electric generating facilities, high voltage transmission lines, gas pipelines, and radioactive waste disposal sites. The EFSC also has responsibility for overseeing the decommissioning of Trojan. The seven volunteer members of the EFSC are appointed to four-year terms by the state’s governor, with staff support provided by the Oregon Department of Energy.

Integrated Resource Plan—Unless the OPUC directs otherwise, PGE is required to file with the OPUC an Integrated Resource Plan (IRP) within two years of its previous IRP acknowledgment order. The IRP guides the utility on how it will meet future customer demand and describes the Company’s future energy supply strategy, reflecting new technologies, market conditions, and regulatory requirements. The primary goal of the IRP is to identify an acquisition plan for generation, transmission, demand-side and energy efficiency resources that, along with the Company’s existing portfolio, provides the best combination of expected cost and associated risks and uncertainties for PGE and its customers.

Ratemaking—Under Oregon law, the OPUC is required to ensure that prices and terms of service are fair, non-discriminatory, and provide regulated companies an opportunity to earn a reasonable return on their investments. Customer prices are determined through formal ratemaking proceedings that generally include testimony by participating parties, discovery, public hearings, and the issuance of a final order. Participants in such proceedings, which are conducted under established procedural schedules, include PGE, OPUC staff, and intervenors.

• | General Rate Cases. PGE periodically evaluates the need to change its retail electric price structure to sufficiently cover its operating costs and provide a reasonable rate of return. Such changes are requested pursuant to a comprehensive general rate case process that includes a forecasted test year, debt-to-equity |

7

capital structure, return on equity, and overall rate of return. Revenue requirements and retail customer price changes are proposed based upon such factors. PGE’s most recent general rate case was the 2011 General Rate Case, which became effective on January 1, 2011. For additional information, see the Overview section of Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

• | Power Costs. In addition to price changes resulting from the general rate case process, the OPUC has approved the following mechanisms by which PGE can adjust retail customer prices to cover the Company’s NVPC, which consists of the cost of power and fuel (including related transportation costs) less revenues from wholesale power and fuel sales: |

▪ | Annual Power Cost Update Tariff (AUT). Under this tariff, customer prices are adjusted annually to reflect the latest forecast of NVPC. Such forecasts assume average regional hydro conditions (based on seventy years of stream flow data covering the period 1928 - 1998) and current hydro operating parameters. The NVPC forecasts also assume average wind conditions (based on wind studies completed in connection with the permitting process of the wind farm) for PGE-owned wind generation and normal operating conditions for thermal generating plants. An initial NVPC forecast, submitted to the OPUC by April 1st each year, is updated during the year and finalized in November. Based upon the final forecast, new prices, as approved by the OPUC, become effective at the beginning of the next calendar year; and |

▪ | Power Cost Adjustment Mechanism (PCAM). Customer prices can also be adjusted to reflect a portion of the difference between each year’s forecasted NVPC included in prices and actual NVPC for the year. Under the PCAM, PGE is subject to a portion of the business risk or benefit associated with the difference between actual NVPC and that included in base prices (baseline NVPC). The PCAM utilizes an asymmetrical deadband range within which PGE absorbs cost variances, with a 90/10 sharing of such variances between customers and the Company outside of the deadband. Annual results of the PCAM are subject to application of a regulated earnings test, under which a refund will occur only to the extent that it results in PGE’s actual regulated return on equity (ROE) for that year being no less than 1% above the Company’s latest authorized ROE. A collection will occur only to the extent that it results in PGE’s actual regulated ROE for that year being no greater than 1% below the Company’s authorized ROE. A final determination of any customer refund or collection is made by the OPUC through a public filing and review typically during the second half of the following year. The OPUC order in PGE’s 2011 General Rate Case provides for a fixed deadband range of $15 million below, to $30 million above, forecasted NVPC, beginning in 2011. For additional information, see the Results of Operations section of Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

• | Renewable Energy. The 2007 Oregon Renewable Energy Act (the Act) established a Renewable Portfolio Standard (RPS) which requires that PGE serve at least 5% of its retail load with renewable resources by 2011, 15% by 2015, 20% by 2020, and 25% by 2025. PGE has sufficient renewable resources to meet the 2011 - 2014 requirements of the Act. Further, the Company expects to have sufficient resources to meet the 2015 requirements with additional resources included in its most recent Integrated Resource Plan (IRP). It is anticipated that requirements for subsequent years will be met by the acquisition of additional renewable resources, as determined pursuant to the Company’s integrated resource planning process. The Act also allows Renewable Energy Credits, resulting from energy generated from qualified renewable resources placed in service after January 1, 1995, to be carried forward, with any excess of what is required to meet the Company’s compliance obligation used to fulfill RPS requirements of future years. For additional information, see the Power Supply section in this Item 1. |

The Act also provides for the recovery in customer prices of all prudently incurred costs required to comply with the RPS. Under a renewable adjustment clause (RAC) mechanism, PGE can recover the revenue requirement of new renewable resources and associated transmission that are not yet included in prices. Under the RAC, PGE submits a filing by April 1st of each year for new renewable resources

8

expected to be placed in service in the current year, with prices to become effective January 1st of the following year. In addition, the RAC provides for the deferral and subsequent recovery of eligible costs incurred prior to January 1st of the following year.

For additional information, see the “Legal, Regulatory and Environmental Matters” discussion in the Overview section of Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Other ratemaking proceedings can involve charges or credits related to specific costs, programs, or activities, as well as the recovery or refund of deferred amounts recorded pursuant to specific OPUC authorization. Such amounts are generally collected from, or refunded to, retail customers through the use of supplemental tariffs.

Retail Customer Choice Program—PGE’s commercial and industrial customers have access to pricing options other than cost-of-service, including direct access and daily market based pricing. All commercial and industrial customers are eligible for direct access, whereby customers purchase their electricity from an Electricity Service Supplier (ESS), and PGE continues to deliver the energy to the customers. Large commercial and industrial customers may elect to be served by PGE on a daily market based price. Certain large commercial and industrial customers may elect to be removed from cost-of-service pricing for a fixed three-year or a minimum five-year term, to be served either by an ESS or under a market price option.

The retail customer choice program has no material impact on the Company’s financial condition or operating results. Revenue changes resulting from increases or decreases in electricity sales to direct access customers are substantially offset by changes in the Company’s cost of purchased power and fuel. Further, the program provides for “transition adjustment” charges or credits to direct access and market based pricing customers that reflect the above- or below-market cost of energy resources owned or purchased by the Company. Such adjustments are designed to ensure that the costs or benefits of the program do not unfairly shift to those customers that continue to purchase their energy requirements from the Company.

Residential and small commercial customers can purchase electricity from PGE among a portfolio of price options that include basic cost-of-service, time-of-use, and renewable resource prices.

Energy Efficiency Funding—Oregon law provides for a “public purpose charge” to fund cost-effective energy efficiency measures, new renewable energy resources, and weatherization measures for low-income housing. This charge, equal to 3% of retail revenues, is collected from customers and remitted to the Energy Trust of Oregon (ETO) and other agencies for administration of these programs. Approximately $51 million was collected from customers for this charge in 2011. The Company estimates that $47 million will be collected from customers in 2012.

In addition to the public purpose charge, PGE also remits to the ETO amounts collected under an Energy Efficiency Adjustment tariff to fund additional energy efficiency measures. This charge was approximately 1.8% in 2011 and increased to 2.7% effective January 1, 2012, for applicable customers. Under the tariff, approximately $28 million was collected from eligible customers in 2011. The Company estimates that $42 million will be collected in 2012.

Decoupling—The decoupling mechanism is intended to provide for recovery of reduced revenues resulting from a reduction in electricity sales attributable to energy efficiency and conservation efforts by residential and certain commercial customers. The mechanism provides for customer collection if weather adjusted use per customer is lower than levels included in the Company’s most recent general rate case; it also provides for customer refunds if weather adjusted use per customer exceeds levels included in the general rate case.

9

During 2011, PGE recorded an estimated refund of $2 million, which resulted primarily from actual weather adjusted use per customer being slightly higher than levels included in the 2011 General Rate case. Pending review and approval by the OPUC, any resulting refund to customers would be expected over a one-year period beginning June 1, 2012. For 2010, the Company recorded an estimated collection of $8 million, as weather adjusted use per customer was less than levels included in the 2009 General Rate Case. After review, the OPUC approved collections from customers over a one-year period that began June 1, 2011.

As part of the Company’s 2011 General Rate Case, the OPUC authorized the continued use of the decoupling mechanism through December 31, 2013.

Regulatory Accounting

PGE is subject to accounting principles generally accepted in the United States of America, and as a regulated public utility, the effects of rate regulation are reflected in its financial statements. These principles provide for the deferral as regulatory assets of certain actual or anticipated costs that would otherwise be charged to expense, based on expected recovery from customers in future prices. Likewise, certain actual or anticipated credits that would otherwise reduce expense can be deferred as regulatory liabilities, based on expected future credits or refunds to customers. PGE records regulatory assets or liabilities if it is probable that they will be reflected in future prices, based on regulatory orders or other available evidence.

The Company periodically assesses the applicability of regulatory accounting to its business, considering both the current and anticipated future rate environment and related accounting guidance. For additional information, see Regulatory Assets and Liabilities in Note 2, Summary of Significant Accounting Policies, and Note 6, Regulatory Assets and Liabilities, in the Notes to Consolidated Financial Statements in Item 8.—“Financial Statements and Supplementary Data.”

Customers and Revenues

PGE conducts retail electric operations exclusively in Oregon within a service area approved by the OPUC. Retail customers are generally classified within one of the following three categories: i) residential; ii) commercial; or iii) industrial. Within its service territory, the Company competes with: i) the local natural gas distribution company for the energy needs of residential and commercial space heating, water heating, and appliances, and ii) fuel oil suppliers, primarily for residential customers’ space heating needs. In addition, the Company distributes power to commercial and industrial customers that choose to purchase their energy supply from an ESS.

In 2011, three ESSs were registered with PGE to transact business with the Company and its customers and provided an average of 242 direct access customers with a total retail load of 988 thousand megawatt hours (MWh) representing 8.5% of PGE’s commercial and industrial retail energy deliveries and 5.1% of the Company’s total retail energy deliveries for the year. In 2010, ESSs supplied an average of 221 direct access customers with a total retail load representing 9.3% of PGE’s commercial and industrial retail energy deliveries and 5.6% of the Company’s total retail energy deliveries for the year.

Beginning in January 2012, two ESSs are registered with PGE to transact business with the Company and its customers and are expected to supply energy to 484 direct access customers with an estimated annual load representing 11% of the Company’s expected commercial and industrial load and 6% of total retail deliveries. Of these direct access customers, a total of 137, with an estimated annual retail load requirement representing 8% of the Company’s expected commercial and industrial load and 5% of total retail deliveries, will be served on a three- or five-year basis.

The Company includes direct access customers in its customer counts and energy delivered to such customers in its total retail energy deliveries although Retail revenues reflect only delivery charges and transition adjustments for these customers.

10

PGE’s Revenues are comprised of the following (dollars in millions):

Years Ended December 31, | ||||||||||||||||||||

2011 | 2010 | 2009 | ||||||||||||||||||

Amount | % | Amount | % | Amount | % | |||||||||||||||

Retail: | ||||||||||||||||||||

Residential | $ | 877 | 48 | % | $ | 803 | 45 | % | $ | 856 | 47 | % | ||||||||

Commercial | 635 | 35 | 601 | 34 | 642 | 36 | ||||||||||||||

Industrial | 226 | 13 | 221 | 12 | 166 | 9 | ||||||||||||||

Subtotal | 1,738 | 96 | 1,625 | 91 | 1,664 | 92 | ||||||||||||||

Other accrued revenues, net | (16 | ) | (1 | ) | 39 | 2 | (7 | ) | — | |||||||||||

Total retail revenues | 1,722 | 95 | 1,664 | 93 | 1,657 | 92 | ||||||||||||||

Wholesale revenues | 60 | 3 | 87 | 5 | 112 | 6 | ||||||||||||||

Other operating revenues | 31 | 2 | 32 | 2 | 35 | 2 | ||||||||||||||

Revenues | $ | 1,813 | 100 | % | $ | 1,783 | 100 | % | $ | 1,804 | 100 | % | ||||||||

Certain averages for retail customers who purchase their energy requirements from the Company* are as follows:

Years Ended December 31, | ||||||||||||||

2011 | 2010 | 2009 | ||||||||||||

Average usage per customer (in kilowatt hours): | ||||||||||||||

Residential | 10,740 | 10,384 | 11,059 | |||||||||||

Commercial | 68,835 | 68,040 | 70,853 | |||||||||||

Industrial | 14,932,550 | 12,986,466 | 9,343,838 | |||||||||||

Average revenue per customer (in dollars): | ||||||||||||||

Residential | $ | 1,160 | $ | 1,049 | $ | 1,111 | ||||||||

Commercial | 6,091 | 5,769 | 6,127 | |||||||||||

Industrial | 919,764 | 859,251 | 660,839 | |||||||||||

Average revenue per kilowatt hour (in cents): | ||||||||||||||

Residential | 10.80 | ¢ | 10.10¢ | 10.05¢ | ||||||||||

Commercial | 8.85 | 8.48 | 8.65 | |||||||||||

Industrial | 6.16 | 6.62 | 7.07 | |||||||||||

* | Excludes customers who purchase their energy requirements from ESSs. | |||

For additional information, see Results of Operations in Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Retail Revenues

Retail customers are classified as residential, commercial, or industrial, with no single customer representing more than 4% of PGE’s total retail revenues or 5% of total retail deliveries. Commercial and industrial customer classes are not dominated by any single industry. While the 20 largest commercial and industrial customers constituted 12% of total retail revenues in 2011, they represented nine different groups, including high technology, paper manufacturing, metal fabrication, health services, and governmental agencies.

11

Averages over the past three-year period by customer class are as follows, with energy deliveries and revenues expressed as a percentage of the totals:

Average Number of Customers | Energy Deliveries | Revenues | |||||

Residential | 717,358 | 40% | 51% | ||||

Commercial | 102,148 | 39 | 37 | ||||

Industrial | 264 | 21 | 12 | ||||

In accordance with state regulations, PGE’s retail customer prices are determined through general rate case proceedings and various tariffs filed with the OPUC from time to time, and are based on the Company’s cost of service. Additionally, the Company offers different pricing options. Under PGE’s daily market price option, the Company delivered electricity to 185 commercial and industrial customers in 2011, representing 1.5% of commercial and industrial deliveries and less than 1% of total retail energy deliveries.

Under the renewable energy options, approximately 85,000, residential and small commercial customers were enrolled compared to 77,000 and 82,000 as of December 31, 2010, and 2009, respectively. Under time-of-use options, approximately 4,500 customers were enrolled compared to 2,100, and 2,130 as of December 31, 2010, and 2009, respectively.

For additional information on customer options, see “Retail Customer Choice Program” within the Regulation and Rates section of this Item 1. Additional information on the customer classes follows.

Residential customers include single family housing, multiple family housing (such as apartments, duplexes, and town homes), mobile homes, and small farms.

Residential demand is sensitive to the effects of weather, with demand historically highest during the winter heating season. Due to the increased use of air conditioning in PGE’s service territory, the summer peaks have increased in recent years. Economic conditions can also affect demand from the Company’s residential customers, as historical data suggests that high unemployment rates contribute to a decrease in demand. Residential demand is also impacted by energy efficiency measures; however, the Company’s decoupling mechanism is intended to mitigate the financial effects of such measures.

During 2011, total residential deliveries increased 3.8% compared to 2010 as a result of cooler weather during the heating season, and an increase in the average number of customers. During 2010, total residential deliveries decreased 5.7% compared to 2009, with milder weather conditions accounting for nearly half of the decrease.

Commercial customers consist of non-residential customers who accept energy deliveries at voltages equivalent to those delivered to residential customers. This customer class consists of most businesses, including small industrial companies, and public street and highway lighting accounts.

Demand from the Company’s commercial customers is less susceptible to weather conditions than the residential class. Economic conditions and fluctuations in total employment in the region can also lead to corresponding changes in energy demand from commercial customers. Commercial demand is also impacted by energy efficiency measures, the financial effects of which are partially mitigated by the Company’s decoupling mechanism.

In 2011, favorable weather effects combined with the addition of an average of nearly 700 new customers contributed to the 2% increase in deliveries to commercial customers. During 2011, non-farm employment increased 1.6% in Oregon.

12

During 2010, as the Oregon economy lost approximately 0.9% of its payroll, the Company’s commercial energy deliveries decreased 3.7% compared to 2009 with milder weather, including a very cool summer in 2010, contributing about one-third of the decline.

Industrial customers consist of non-residential customers who accept delivery at higher voltages than commercial customers, with pricing based on the amount of electricity delivered and the applicable tariff. Demand from industrial customers is primarily affected by economic conditions, with weather having little impact on this customer class.

A change in economic activity in Oregon and the United States can also lead to a change in energy demand from the Company’s industrial customers. In 2011, industrial deliveries rose 4.7% as demand increased from certain paper production customers, and the general economic conditions improved. In 2010, the Company’s industrial energy deliveries rose 3.3% compared to 2009, driven by increased demand from certain paper production customers in the latter half of 2010.

Other accrued revenues, net include items that are not currently in customer prices, but are expected to be in prices in a future period. Such amounts include deferrals recorded under regulatory mechanisms for the renewable adjustment clause, the power cost adjustment, and decoupling. See “State of Oregon Regulation” in the Regulation and Rates section of this Item 1 for further information on these items.

Other accrued revenues also include deferrals recorded pursuant to the Residential Exchange Program (REP). Under the REP, the Bonneville Power Administration (BPA) provides federal hydropower benefits to residential and small farm customers of certain investor-owned electric utilities that are expected to continue until the year 2028. PGE receives monthly payments from BPA under the program and passes such payments along to eligible customers in the form of monthly billing credits. For the twelve months ended September 30, 2011, PGE received payments totaling $55 million and received $44 million during each of the twelve month periods ended September 30, 2010 and 2009. Payments for the twelve month period ending September 30, 2012 are expected to be approximately $58 million, with such benefits to be credited to eligible customers.

Wholesale Revenues

PGE participates in the wholesale electricity marketplace in order to balance its supply of power to meet the needs of its retail customers. In doing so, the Company attempts to secure reasonably priced power, manage risk, and administer its current long-term wholesale contracts through economic dispatch decisions for its own generation. Interconnected transmission systems in the western United States serve utilities with diverse load requirements and allow the Company to purchase and sell electricity within the region depending upon the relative price and availability of power, hydro conditions, and daily and seasonal retail demand.

The majority of PGE’s wholesale electricity sales is to utilities and power marketers and is predominantly short-term. The Company may net purchases and sales with the same counterparty rather than simultaneously receiving and delivering physical power, with only the net amount of those purchases or sales required to meet retail and wholesale obligations physically settled.

Other Operating Revenues

Other operating revenues consist primarily of the sale of excess natural gas and oil, as well as revenues from transmission services, excess transmission capacity resales, pole contact rentals, and other electric services provided to customers.

Seasonality

Demand for electricity by PGE’s residential customers is affected by seasonal weather conditions, as discussed above. The Company uses heating and cooling degree-days to determine the effect of weather on the demand for

13

electricity. Heating and cooling degree-days provide cumulative variances in the average daily temperature from a baseline of 65 degrees, over a period of time, to indicate the extent to which customers are likely to use, or have used, electricity for heating or air conditioning. The higher the numbers of degree-days, the greater the expected demand for heating or cooling.

The following table indicates the heating and cooling degree-days for the most recent three-year period, along with 15-year averages for the most recent year provided by the National Weather Service, as measured at Portland International Airport:

Heating Degree-Days | Cooling Degree-Days | ||||

2011 | 4,650 | 362 | |||

2010 | 4,187 | 314 | |||

2009 | 4,391 | 627 | |||

15-year average for 2011 | 4,219 | 464 | |||

PGE’s all-time high net system load peak of 4,073 Megawatts (MW) occurred in December 1998. The Company’s all-time “summer peak” of 3,949 MW occurred in July 2009. The following table presents the Company’s average winter and summer loads for the periods indicated along with the corresponding peak load and month in which it occurred:

Average Load | Peak Load | |||||||

MW | Month | MW | ||||||

2011 | Winter | 2,612 | January | 3,555 | ||||

Summer | 2,233 | September | 3,340 | |||||

2010 | Winter | 2,445 | November | 3,582 | ||||

Summer | 2,220 | August | 3,544 | |||||

2009 | Winter | 2,658 | December | 3,851 | ||||

Summer | 2,267 | July | 3,949 | |||||

The Company tracks and evaluates both base load growth and peak capacity for purposes of long-term load forecasting and integrated resource planning as well as for preparing general rate case assumptions. Behavior patterns, conservation, energy efficiency initiatives and measures, weather effects, and demographic changes all play a role in determining expected future customer demand and the resulting resources the Company will need to adequately meet those loads and maintain adequate capacity reserves.

14

Power Supply

PGE relies upon its generating resources as well as short- and long-term power and fuel purchase contracts to meet its customers’ energy requirements. The Company executes economic dispatch decisions concerning its own generation, and participates in the wholesale market as a result of those economic dispatch decisions, in an effort to obtain reasonably priced power for its retail customers.

PGE’s base generating resources consist of five thermal plants, seven hydroelectric plants, and a wind farm located at Biglow Canyon in eastern Oregon. The volume of electricity the Company generates is dependent upon, among other factors, the capacity and availability of its generating resources. Capacity of the thermal plants represents the MW the plant is capable of generating under normal operating conditions, net of electricity used in the operation of the plant. The capacity of the Company’s thermal generating resources is also affected by ambient temperatures. Capacity of both hydro and wind generating resources represent the nameplate MW, which varies from actual energy expected to be received as these types of generating resources are highly dependent upon river flows and wind conditions, respectively. Availability represents the percentage of the year the plant was available for operations, which reflects the impact of planned and forced outages. For a complete listing of these facilities, see Item 2.—“Properties.”

The Company also promotes the expansion of renewable energy resources, as well as energy efficiency measures, to meet its energy requirements and enhance customers’ ability to manage their energy use more efficiently.

PGE’s resource capacity (in MW) was as follows:

As of December 31, | |||||||||||||||||

2011 | 2010 | 2009 | |||||||||||||||

Capacity | % | Capacity | % | Capacity | % | ||||||||||||

Generation: | |||||||||||||||||

Thermal: | |||||||||||||||||

Natural gas | 1,172 | 28 | % | 1,157 | 24 | % | 1,175 | 26 | % | ||||||||

Coal | 670 | 16 | 670 | 14 | 670 | 15 | |||||||||||

Total thermal | 1,842 | 44 | 1,827 | 38 | 1,845 | 41 | |||||||||||

Hydro | 489 | 12 | 489 | 10 | 489 | 11 | |||||||||||

Wind * | 450 | 11 | 450 | 9 | 275 | 6 | |||||||||||

Total generation | 2,781 | 67 | 2,766 | 57 | 2,609 | 58 | |||||||||||

Purchased power: | |||||||||||||||||

Long-term contracts: | |||||||||||||||||

Capacity/exchange | 190 | 4 | 540 | 11 | 640 | 14 | |||||||||||

Mid-Columbia hydro | 335 | 8 | 507 | 10 | 548 | 12 | |||||||||||

Confederated Tribes hydro | 150 | 4 | 150 | 3 | 150 | 3 | |||||||||||

Wind | 44 | 1 | 44 | 1 | 35 | 1 | |||||||||||

Other | 210 | 5 | 221 | 5 | 233 | 5 | |||||||||||

Total long-term contracts | 929 | 22 | 1,462 | 30 | 1,606 | 35 | |||||||||||

Short-term contracts | 458 | 11 | 612 | 13 | 315 | 7 | |||||||||||

Total purchased power | 1,387 | 33 | 2,074 | 43 | 1,921 | 42 | |||||||||||

Total resource capacity | 4,168 | 100 | % | 4,840 | 100 | % | 4,530 | 100 | % | ||||||||

* | Capacity represents nameplate and differs from expected capacity, which is expected to range from 135 MW to 180 MW, dependent upon wind conditions. |

15

For information regarding actual generating output and purchases for the years ended December 31, 2011, 2010 and 2009, see the Results of Operations section of Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Generation

That portion of PGE’s retail load requirements generated by its plants varies from year to year and is determined by various factors, including planned and forced outages, availability and price of coal and natural gas, precipitation and snow-pack levels, the market price of electricity, and wind variability.

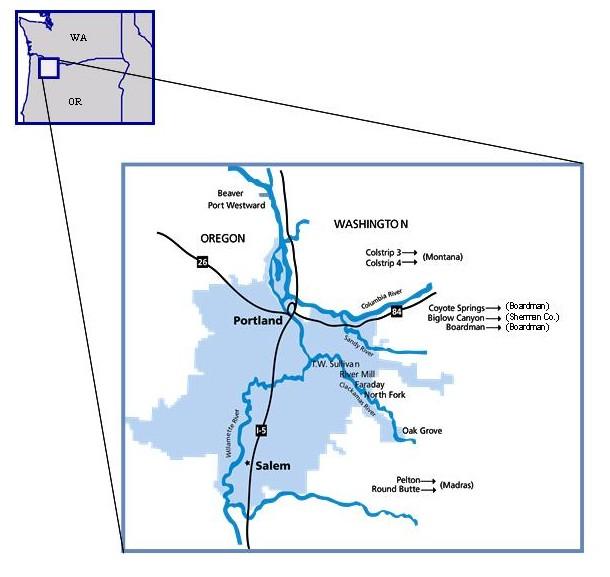

Thermal | PGE has a 65% ownership interest in Boardman, which it operates, and a 20% ownership interest in Colstrip Units 3 and 4. These two coal-fired generating facilities provided approximately 21% of the Company’s total retail load requirement in 2011, compared to 26% in 2010 and 20% in 2009. The Company’s three natural gas-fired generating facilities, Port Westward, Beaver, and Coyote Springs, provided approximately 11% of its total retail load requirement in 2011 and 24% in 2010 and 2009. |

The thermal plants, which have a combined capacity of 1,842 MW, provide reliable power for the Company’s customers with plant availability, excluding Colstrip, of 90% in 2011, 94% in 2010, and 84% in 2009 and Colstrip plant availability of 84% in 2011, 95% in 2010, and 68% in 2009.

Hydro | The Company’s FERC-licensed hydroelectric projects consist of Pelton/Round Butte on the Deschutes River near Madras, Oregon (discussed below), four plants on the Clackamas River, and one on the Willamette River. The licenses for these projects expire at various dates from 2035 to 2055. These plants, which have a combined capacity of 489 MW, provided 10% of the Company’s total retail load requirement in 2011, 2010 and 2009, with availability of 100% in 2011 and 99% in both 2010 and 2009. Northwest hydro conditions have a significant impact on the region’s power supply, with water conditions significantly impacting PGE’s cost of power and its ability to economically displace more expensive thermal generation and spot market power purchases. |

PGE has a 66.67% ownership interest in the 450 MW Pelton/Round Butte hydroelectric project on the Deschutes River, with the remaining interest held by the Confederated Tribes of the Warm Springs Reservation of Oregon (Tribes). A 50-year joint license for the project, which is operated by PGE, was issued by the FERC in 2005. The Tribes have an option to purchase an additional undivided 16.66% interest in Pelton/Round Butte at its discretion no sooner than December 31, 2021. The Tribes have a second option to purchase an undivided 0.02% interest in Pelton/Round Butte at its discretion no sooner than April 1, 2041. If both options are exercised by the Tribes, the Tribes’ ownership percentage would exceed 50%.

Wind | Biglow Canyon Wind Farm (Biglow Canyon), located in Sherman County, Oregon, is PGE’s largest renewable energy resource with 217 wind turbines with a total installed capacity of approximately 450 MW. It was completed and placed in service in three phases between December 2007 and August 2010. In 2011, Biglow Canyon provided 6% of the Company’s total retail load requirement, compared to 4% in 2010 and 3% in 2009, with availability of 97% in 2011 and 96% in both 2010 and 2009. The energy received from wind resources differs from the nameplate capacity and is expected to range from 135 MW to 180 MW for Biglow Canyon, dependent upon wind conditions. |

Dispatchable Standby Generation (DSG)—PGE has a DSG program under which the Company can start, operate, and monitor customer-owned standby generators when needed to meet peak demand. The program helps provide operating reserves for the Company’s generating resources and, when operating, can supply most or all of DSG customer loads. As of December 31, 2011, there were 31 projects that together can provide approximately 69 MW of diesel-fired capacity at peak times. In addition, there were 12 projects under construction that are expected to provide an additional 30 MW.

16

Fuel Supply—PGE contracts for natural gas and coal supplies required to fuel the Company’s thermal generating plants, with certain plants also able to operate on fuel oil if needed. In addition, the Company uses forward, swap, and option contracts to manage its exposure to volatility in natural gas prices.

Coal | Boardman—PGE has fixed-price purchase agreements that provide coal for Boardman into 2014. The coal is obtained from surface mining operations in Wyoming and Montana and is delivered by rail under two separate ten-year transportation contracts which extend through 2013. |

PGE expects to begin seeking requests for proposal in mid-2012 for the purchase of coal to fill open positions for 2013 and beyond. The terms of any contracts and quality of coal are expected to be staged in alignment with the timing of the installation of required emissions controls. For additional information on Boardman’s emissions controls, see the Capital Requirements section in Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.” PGE believes that sufficient market supplies of coal are available to meet anticipated operations of Boardman for the foreseeable future.

Natural Gas | Port Westward and Beaver—PGE manages the price risk of natural gas supply for Port Westward through financial contracts up to 60 months in advance. Physical supplies for Port Westward and Beaver are generally purchased within 12 months of delivery and based on anticipated operation of the plants. PGE owns 79.5%, and is the operator of record, of the Kelso-Beaver Pipeline, which directly connects both generating plants to the Northwest Pipeline, an interstate natural gas pipeline operating between British Columbia and New Mexico. Currently, PGE transports gas on the Kelso-Beaver Pipeline for its own use under a firm transportation service agreement, with capacity offered to others on an interruptible basis to the extent not utilized by the Company. PGE has access to 103,305 Dth per day of firm gas transportation capacity to serve the two plants. |

PGE also has contractual access through April 2017 to natural gas storage in Mist, Oregon, from which it can draw in the event that gas supplies are interrupted or if economic factors require its use. This storage may be used to fuel both Port Westward and Beaver. PGE believes that sufficient market supplies of gas are available to meet anticipated operations of both plants for the foreseeable future.

The Beaver generating plant has the capability to operate on No. 2 diesel fuel oil when it is economical or if the plant’s natural gas supply is interrupted. PGE had an approximate 7-day supply of ultra-low sulfur diesel fuel oil at the plant site as of December 31, 2011. The current operating permit for Beaver limits the number of gallons of fuel oil that can be burned daily, which effectively limits the daily hours of operation of Beaver.

Coyote Springs—PGE manages the price risk of natural gas supply for Coyote Springs through financial contracts up to 60 months in advance, while physical supplies are generally purchased within 12 months of delivery and based on anticipated operation of the plant. Coyote Springs utilizes 41,000 Dth per day of natural gas when operating at full capacity, with firm transportation capacity on three pipeline systems accessing gas fields in Alberta, Canada. PGE believes that sufficient market supplies of gas are available for Coyote Springs for the foreseeable future, based on anticipated operation of the plant. Although Coyote Springs was designed to also operate on fuel oil, such capability has been deactivated in order to optimize natural gas operations.

Purchased Power

PGE supplements its own generation with power purchased in the wholesale market to meet its retail load requirements. The Company utilizes short- and long-term wholesale power purchase contracts in an effort to provide the most favorable economic mix on a variable cost basis. Such contracts have original terms ranging from one month to 30 years and expire at varying dates through 2036.

17

PGE’s medium term power cost strategy helps mitigate the effect of price volatility on its customers due to changing energy market conditions. The strategy allows the Company to take positions in power and fuel markets up to five years in advance of physical delivery. By purchasing a portion of anticipated energy needs for future years over an extended period, PGE mitigates a portion of the potential future volatility in the average cost of purchased power and fuel.

The Company’s major power purchase contracts consist of the following (also see the preceding table which summarizes the average resource capabilities related to these contracts):

Capacity/exchange—PGE has three contracts that provide PGE with firm capacity to help meet the Company’s peak loads. The contracts range from 10 MW to 150 MW and expire at various dates from February 2012 through December 2016. They include a seasonal exchange contract with another western utility that helps meet winter--peaking requirements.

Mid-Columbia hydro—PGE has long-term power purchase contracts with certain public utility districts in the state of Washington for a portion of the output of three hydroelectric projects on the mid-Columbia River. These contracts expire at various dates from 2017 through 2052. Although the projects currently provide a total of 335 MW of capacity, actual energy received is dependent upon river flows.

Confederated Tribes—PGE has a long-term agreement under which the Company purchases, at market prices, the Tribes’ interest in the output of the Pelton/Round Butte hydroelectric project. Although the agreement provides 150 MW of capacity, actual energy received is dependent upon river flows. The term of the agreement coincides with the term of the FERC license for this project, which expires in 2055.

Wind—The Company has three long-term contracts, which extend to various dates between 2028 and 2035, that provide for the purchase of renewable wind-generated electricity. Although these contracts provide a total of 44 MW of capacity, actual energy received is dependent upon wind conditions.

Other—These primarily consist of long-term contracts to purchase power from various counterparties, including other Pacific Northwest utilities, over terms extending into 2036.

Other also includes contracts that provide for the purchase of renewable solar-powered electricity as follows:

• | PGE operates three photovoltaic solar power projects installed in the Portland area, with a combined installed capacity of 3.6 MW. PGE purchases 100% of the energy generated from two of the facilities and purchases any excess energy generated from one facility pursuant to a net metering arrangement with the Oregon Department of Transportation (ODOT); |

• | PGE has two 25-year purchase agreements for the power generated from two photovoltaic solar projects installed near Salem, Oregon. The construction of the projects was completed in mid-2011, with PGE then purchasing the power generated from these facilities, which have a combined generating capacity of 2.8 MW. |

In January 2012, PGE completed the construction of a 1.75 MW photovoltaic solar power project, which was sold and simultaneously leased-back from a financial institution. The Company operates the project and receives 100% of the power generated by the facility.

Short-term contracts—These contracts are for delivery periods of one month up to one year in length. They are entered into with various counterparties to provide additional firm energy to help meet the Company’s load requirement.

PGE also utilizes spot purchases of power in the open market to secure the energy required to serve its retail customers. Such purchases are made under contracts that range in duration from 30 minutes to less than one month. For additional information regarding PGE’s power purchase contracts, see Note 15, Commitments and Guarantees, in the Notes to Consolidated Financial Statements in Item 8.—“Financial Statements and Supplementary Data.”

18

Future Energy Resource Strategy

PGE’s most recent IRP was acknowledged by the OPUC on November 23, 2011. The IRP includes an action plan for the acquisition of new resources and a 20-year strategy that outlines long-term expectations for resource needs and portfolio performance. PGE projects that it needs 873 MWa of new resources by 2015, increasing to 1,396 MWa by 2020, to meet expected customer demand. Such projected energy gaps are driven primarily by continued load growth and the expiration of certain long-term power supply contracts. The projected energy gap increases by approximately 374 MW with the cessation of coal-fired operations at Boardman in 2020.

To meet the projected energy requirements, the IRP includes energy efficiency measures, new renewable resources, new transmission capability, new generating plants, and improvements to existing generating plants, as follows:

• | Acquisition of 214 MWa of energy efficiency through continuation of Energy Trust of Oregon programs, with funding to be provided from the existing public purpose charge and through enabling legislation included in Oregon’s RPS; |

• | An additional 101 MWa of wind or other renewable resources necessary to meet requirements of Oregon’s RPS by 2015; |

• | Transmission capacity additions to interconnect new and existing energy resources in eastern Oregon to PGE’s services territory. For additional information on the Cascade Crossing Transmission Project (Cascade Crossing), see the Transmission and Distribution section in this Item 1; |

• | New natural gas generation facilities to help meet additional base load requirements estimated at 300 to 500 MW, which is expected to be available in the 2015 to 2017 timeframe; |

• | New natural gas generation facilities to help meet peak capacity requirements estimated at up to 200 MW, bi-seasonal peaking supply of 200 MW and winter-only peaking supply of 150 MW, all of which are expected to be available in the 2013 to 2015 timeframe; and |

• | Continued operations of the Boardman plant, including the addition of certain emissions controls and the continuation of coal-fired operation of the plant through 2020. For additional information about emissions controls for the Boardman plant, see the Capital Requirements section in Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

In January 2012, PGE requested that the OPUC acknowledge a draft request for proposals (RFP) that is expected to be issued in the second quarter of 2012, seeking electric power generating resources to help meet PGE’s capacity and energy needs, as outlined in the IRP discussion above. PGE expects to file a second RFP, for renewable resources, later in 2012.

The Company has filed with the OPUC a motion for a one-year extension to file its next IRP. If the motion is approved as submitted, PGE would be required to file its next IRP no later than November 2013. If not approved as submitted, PGE may be required to file its next IRP as early as November 2012.

19

Transmission and Distribution

Transmission systems deliver energy from generating facilities to distribution systems for final delivery to customers. PGE schedules energy deliveries over its transmission system in accordance with FERC requirements and operates one balancing authority area (an electric system bounded by interchange metering) in its service territory. In 2011, PGE delivered approximately 20 million MWh in its balancing authority area through approximately 1,100 circuit miles of transmission lines.

PGE’s transmission system is part of the Western Interconnection, the regional grid in the western United States. The Western Interconnection includes the interconnected transmission systems of 11 western states, two Canadian provinces and parts of Mexico, and is subject to the reliability rules of the WECC and the NERC. PGE relies on transmission contracts with BPA to transmit a significant amount of the Company’s generation to its distribution system. PGE’s transmission system, together with contractual rights to other transmission systems, enables the Company to integrate and access generation resources to meet its customers’ energy requirements. PGE’s generation is managed on a coordinated basis to obtain maximum load-carrying capability and efficiency. The Company’s transmission and distribution systems are located as follows:

• | On property owned or leased by PGE; |

• | Under or over streets, alleys, highways and other public places, the public domain and national forests, and state lands under franchises, easements or other rights that are generally subject to termination; |

• | Under or over private property as a result of easements obtained primarily from the record holder of title; or |

• | Under or over Native American reservations under grant of easement by the Secretary of the Interior or lease or easement by Native American tribes. |

PGE’s wholesale transmission activities are regulated by the FERC. In accordance with its OATT, PGE offers several transmission services to wholesale customers:

• | Network integration transmission service, a service that integrates generating resources to serve retail loads; |

• | Short- and long-term firm point-to-point transmission service, a service with fixed delivery and receipt points; and |

• | Non-firm point-to-point service, an “as available” service with fixed delivery and receipt points. |

These services are offered on a non-discriminatory basis, with all potential customers provided equal access to PGE’s transmission system. In accordance with FERC Standards of Conduct, PGE’s transmission business is managed and operated independently from its power marketing business.

PGE’s current acknowledged IRP includes a proposal for an approximate 210-mile, 500 kV transmission project (the Cascade Crossing Transmission Project) that would help meet future electricity demand and improve future grid reliability by transmitting power from new and existing energy resources in eastern Oregon to the Company’s service territory. PGE continues to work with other stakeholders in the region in planning the project and is actively engaged in the federal, state, and tribal permitting processes. Subject to obtaining all necessary approvals, the expected in-service date would be late 2016 or early 2017. In October 2011, Cascade Crossing was selected as one of seven transmission projects in the nation to participate in the federal inter-agency Rapid Response Team for Transmission program to improve agency collaboration and expedite federal permitting.

PGE continues to meet state regulatory requirements related to power distribution service quality and reliability. Such requirements are reflected in specific indices that measure outage duration, outage frequency, and momentary power interruptions. The Company is required to include performance results related to service quality measures in annual reports filed with the OPUC. Specific monetary penalties can be assessed for failure to attain required performance levels, with amounts dependent upon the extent to which actual results fail to meet such requirements.

20

For additional information regarding the Company’s transmission and distribution facilities, see Item 2.—“Properties.”

Environmental Matters

PGE’s operations are subject to a wide range of environmental protection laws and regulations, which pertain to air quality (including climate change), water quality, endangered species and wildlife protection, and hazardous waste. Environmental matters that relate to the siting and operation of generation, transmission, and substation facilities and the handling, accumulation, cleanup, and disposal of toxic and hazardous substances fall under the jurisdiction of various state and federal agencies. In addition, certain of the Company’s hydroelectric projects and transmission facilities are located on property under the jurisdiction of federal and state agencies, and/or tribal entities that have authority in environmental protection matters. The following discussion provides further information on certain regulations that affect the Company’s operations.

Air Quality

Clean Air Act—PGE’s operations, primarily its thermal generating plants, are subject to regulation under the federal Clean Air Act (CAA), which addresses, among other things, sulfur dioxide (SO2), nitrogen oxides (NOx), carbon monoxide, particulate matter, hazardous air pollutants, and greenhouse gas emissions (GHGs). Oregon and Montana, the states in which PGE facilities are located, also implement and administer certain portions of the CAA and have set standards that are at least equal to federal standards.

In June 2011, the United States Environmental Protection Agency (EPA) approved revised rules to reduce SO2 and NOx emissions at Boardman that have resulted in the installation of certain emissions controls during 2011. To further reduce SO2 emissions, plans call for the use of lower sulfur coal and the addition of a Dry Sorbent Injection system to Boardman in 2014, at an estimated capital cost to the Company of $27 million, including AFDC. The revised rules also provide for coal-fired operation at Boardman to cease no later than December 31, 2020. Construction or acquisition costs of replacement generating capacity will be considered in future customer prices.

In December 2011, the EPA issued new emissions limits under the CAA’s National Emission Standards for Hazardous Air Pollutants (NESHAP) regulating hazardous air pollutant emissions, from coal- and oil-fired electric generating units. Emission limits included in the NESHAP are based on the application of maximum achievable control technology (MACT). Based on its review of the rules and the preliminary full-scale test results, the Company believes the Boardman plant should be able to meet the MACT requirements with the installation of the currently planned controls. The operator of the Colstrip plant has provided the Company with estimated costs for emission control modifications to Units 3 and 4 that may be necessary to meet the MACT requirements. Based on this estimate, the Company expects that its share of these costs, as a 20% owner of Units 3 and 4, will not exceed $10 million.

Regulation of mercury emissions is contemplated under NESHAP. However, the states of Oregon and Montana have previously adopted regulations concerning mercury emissions that have had an impact on the Company as follows:

Oregon—The Oregon Environmental Quality Commission (OEQC) has adopted final rules that pertain to mercury emissions from Boardman. Such rules require compliance with stated mercury limits by July 1, 2012, In 2011, PGE installed controls that are expected to eliminate 90% of the mercury emissions from the plant to comply with the rules.

Montana—The Montana Board of Environmental Review adopted final rules on mercury emissions from coal-fired generating plants, including Colstrip. With the installation of additional mercury control systems, Colstrip is in compliance with these requirements.

21

For additional information, see “Boardman emissions controls” in the Capital Requirements section of Item 7.—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

PGE manages its air emissions by the use of low sulfur fuel, emissions and combustion controls and monitoring, and SO2 allowances awarded under the CAA. The current allowance inventory and expected future annual SO2 allowances, along with the recent and planned installation of emissions controls, are anticipated to be sufficient to permit the Company to continue to meet its compliance requirements and operate its thermal generating plants at forecasted capacity for at least the next several years.

Climate Change—State, regional, and federal legislative efforts continue with respect to establishing regulation of

greenhouse gas (GHG) emissions and their potential impacts on climate change. Recent or pending environmental measures include the following:

• | In 2007, the State of Oregon adopted a non-binding policy guideline that sets a goal to reduce GHG emissions to 10% below 1990 levels by 2020. The guideline does not mandate reductions by any specific entity nor does it include penalties for failure to meet the goal. |

• | In 2009, the U.S. House of Representatives approved legislation that seeks to establish a cap and trade system for GHG emissions. However, the U.S. Senate did not act and it is uncertain whether a cap and trade system will move forward in the near term. |

• | Effective January 1, 2010, the EPA required mandatory measurement and reporting of GHG emissions. PGE is subject to these requirements and is meeting the monitoring and reporting requirements. Reported data will be used to establish a baseline for measuring progress toward any future emissions reduction targets in the United States. |

• | In 2010, the EPA finalized rules creating GHG thresholds that apply to the permitting process for stationary sources, such as electric generating facilities, under the Prevention of Significant Deterioration and Title V operating permit programs. The EPA has also issued guidance under these rules relating to Best Available Control Technology (BACT) requirements for new and modified stationary sources. In April 2011, the OEQC approved new state rules to implement these federal requirements and in December 2011, the rules were approved by the EPA. As a result of these rules, new or modified generating facilities may need to satisfy BACT requirements for limiting GHG emissions. The specific requirements applicable to a particular facility would be determined in connection with the permitting process. |

• | In December 2010, the EPA announced a proposed settlement agreement with states and environmental groups that would require the EPA to set GHG New Source Performance Standards (NSPS) for new and modified fossil fuel-based power plants, and guidelines for state-developed NSPS for existing sources. The deadlines for setting these standards and guidelines have been delayed and the timing is now unclear. |

Any laws that impose mandatory reductions in GHG emissions may have a material impact on PGE, as the Company utilizes fossil fuels in its own power generation and other companies use such fuels to generate power that PGE purchases in the wholesale market. PGE’s Beaver, Coyote Springs, and Port Westward natural gas-fired facilities, and the Company’s ownership interest in Boardman and Colstrip coal-fired facilities, provide approximately 66% of the Company’s net generating capacity. If PGE were to incur incremental costs as a result of changes in the regulations regarding GHGs, the Company would seek recovery in customer prices.

22

Water Quality

The federal Clean Water Act requires that any federal license or permit to conduct an activity that may result in a discharge to waters of the United States must first receive a water quality certification from the state in which the activity will occur. In Oregon, the DEQ is responsible for reviewing proposed projects under this requirement to ensure that federally approved activities will meet water quality standards and policies established by the state. PGE has obtained permits where required, and has certificates of compliance for its hydroelectric operations under the FERC licenses.

Threatened and Endangered Species and Wildlife

Fish Protection—The federal Endangered Species Act (ESA) has granted protection to many populations of migratory fish species in the Pacific Northwest that have declined significantly over the last several decades. Long-term recovery plans for these species have caused major operational changes to many of the region’s hydroelectric projects. Over the years, these changes have resulted in reductions in hydroelectric generation capacity and shifts in the seasonality of much of the generation due to the timing of stored water releases, both of which can affect the price of power in the regional wholesale market. PGE purchases power in the wholesale market to serve its retail load requirements and has contracts to purchase power generated at some of the affected facilities on the mid-Columbia River in central Washington.

PGE is implementing a series of fish protection measures at its hydroelectric projects on the Clackamas, Deschutes, and Willamette rivers that were prescribed by the U.S. Fish and Wildlife Service and the National Marine Fisheries Service under their authority granted in the ESA. As a result of measures contained in their operating licenses, the Deschutes River and Willamette River projects have been certified as low impact hydro, with 50 MWa of their output included as part of the Company’s renewable energy portfolio used to meet the requirements of Oregon’s RPS. Conditions required with the new operating licenses are expected to result in a minor reduction in power production and increase capital spending to modify the facilities to enhance fish passage and survival.

Avian Protection—Various statutory authorities as well as the Migratory Bird Treaty Act have established civil, criminal, and administrative penalties for the unauthorized take of migratory birds. Because PGE operates electric transmission lines and wind generation facilities that can pose risks to a variety of such birds, the Company is required to have an avian protection plan. PGE has developed and implemented such a plan for its transmission and distribution facilities and is in the process of developing a plan for its wind facilities to reduce risks to bird species that can result from Company operations.

Hazardous Waste

PGE has a comprehensive program to comply with requirements of both federal and state regulations related to hazardous waste storage, handling, and disposal. The handling and disposal of hazardous waste from Company facilities is subject to regulation under the federal Resource Conservation and Recovery Act (RCRA). In addition, the use, disposal, and clean-up of polychlorinated biphenyls, contained in certain electrical equipment, are regulated under the federal Toxic Substances Control Act.

The Company’s coal-fired generation facilities, Boardman and Colstrip, produce coal combustion byproducts, which have been exempt from federal hazardous waste regulations under the RCRA. The EPA is revisiting this exemption and is considering listing these residuals as hazardous wastes, which would likely have an impact on current disposal practices and could increase the Company’s cost of handling these materials and affect operations. The EPA has announced that the final rule would likely be issued in late 2012. The Company cannot predict the possible impact of this matter until the EPA provides further guidance on the proposed rules. If PGE were to incur incremental costs as a result of changes in the regulations, the Company would seek recovery in customer prices.

23

PGE is also subject to regulation under the Comprehensive Environmental Response Compensation and Liability Act (CERCLA), commonly referred to as Superfund. The CERCLA provides authority to the EPA to assert joint and several liability for investigation and remediation costs for designated Superfund sites. PGE is listed by the EPA as a Potentially Responsible Party (PRP) at two Superfund sites as follows:

Portland Harbor—A 1997 investigation by the EPA of a segment of the Willamette River, known as the Portland Harbor, revealed significant contamination of river sediments. The EPA subsequently included Portland Harbor on the federal National Priority List as a Superfund site pursuant to CERCLA and listed sixtynine PRPs, including PGE, which has historically owned or operated property near the river. In 2008, the EPA

requested further information from various parties, including PGE, concerning property several miles beyond the original river segment and, as a result, the PRPs now number over one hundred.

Harbor Oil—The Harbor Oil site in north Portland is the location of a company that PGE engaged to process used oil from power plants and electrical distribution systems until 2003. The Harbor Oil facility continues to be utilized by other entities for the processing of used oil and other lubricants. In September 2003, the Harbor Oil site was included on the federal National Priority List as a federal Superfund site and PGE was included among fourteen PRPs.

For additional information on these EPA actions, see Note 18, Contingencies, in the Notes to Consolidated Financial Statements in Item 8.—“Financial Statements and Supplementary Data.”