As filed with the U.S. Securities

and Exchange Commission on April 27, 2016

Registration File No. 33-00480 and File No. 811-04415

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-3

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | x | |

| Pre-Effective Amendment No. | o | |

| Post-Effective Amendment No. 51 | x | |

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | x | |

| Amendment No. 57 | x | |

| (Check Appropriate Box or Boxes) |

College Retirement Equities Fund

(Exact Name of Registrant)

Not Applicable

(Name of Insurance Company)

730 Third Avenue

New York, New York 10017-3206

(Address of Insurance Company’s Principal Executive Offices)

Insurance Company’s Telephone Number, including Area Code: (212) 490-9000

| Name and Address of Agent for Service: | Copy to: | |

| F. Scott Thomas, Esq. | Jeffrey S. Puretz, Esq. | |

| College Retirement Equities Fund | Dechert LLP | |

| 8500 Andrew Carnegie Boulevard | 1900 K Street, N.W. | |

| Charlotte, N.C. 28262 | Washington, D.C. 20006 |

Securities to be Registered: Interests

in an open-end management investment company for individual and group

flexible payment deferred variable annuity contracts

Approximate Date of Proposed Public Offering:

As soon as practicable after effectiveness of the Registration Statement.

It is proposed that this filing will become effective (check appropriate box):

| o | Immediately upon filing pursuant to paragraph (b) |

| x | On April 29, 2016 pursuant to paragraph (b) |

| o | 60 days after filing pursuant to paragraph (a)(1) |

| o | 75 days after filing pursuant to paragraph (a)(2) |

| o | On (date) pursuant to paragraph (a)(1) |

| o | On (date) pursuant to paragraph 9(a)(2) of rule 485 |

If appropriate, check the following box:

o This post-effective amendment designates a new effective date for a previously filed post-effective amendment.

PROSPECTUS MAY 1, 2016 |

| |

College Retirement Equities Fund (CREF)

Individual, Group and Tax-Deferred Annuities

This prospectus (“Prospectus”) describes the individual, group and tax-deferred variable annuities CREF offers. It contains information you should know before purchasing a CREF variable annuity and selecting your investment options. Please read it carefully before investing and keep it for future reference.

Investment in a CREF variable annuity is subject to risk and you could lose money. CREF does not guarantee the investment performance of its accounts, and you bear the entire investment risk. CREF provides variable annuities for retirement and tax-deferred savings plans for employees of colleges, universities, other educational and research organizations and other governmental and non-profit institutions. CREF’s main purpose is to invest funds for your retirement and pay you income based on your choice of eight investment accounts, each of which offers three classes (each, a “class”) of accumulation or annuity units (collectively, “units”), Class R1, Class R2 and Class R3:

Ticker symbols | Class R1 | Class R2 | Class R3 |

§ Stock Account | QCSTRX | QCSTPX | QCSTIX |

§ Global Equities Account | QCGLRX | QCGLPX | QCGLIX |

§ Growth Account | QCGRRX | QCGRPX | QCGRIX |

§ Equity Index Account | QCEQRX | QCEQPX | QCEQIX |

§ Bond Market Account | QCBMRX | QCBMPX | QCBMIX |

§ Inflation-Linked Bond Account | QCILRX | QCILPX | QCILIX |

§ Social Choice Account | QCSCRX | QCSCPX | QCSCIX |

§ Money Market Account | QCMMRX | QCMMPX | QCMMIX |

You or your employer can purchase a CREF variable annuity certificate or contract (which together will be referred to in this Prospectus as a “contract”) in connection with certain types of retirement plans. CREF offers the following contracts:

§ RA (Retirement Annuity) § GRA (Group Retirement Annuity) § SRA (Supplemental Retirement Annuity) § GSRA (Group Supplemental Retirement Annuity) § Retirement Choice and Retirement Choice Plus Annuity § Accumulation-Only | § GA (Group Annuity) and Institutionally Owned GSRAs § Classic, Roth IRA and Rollover (Individual Retirement Annuity) including SEP IRAs (Simplified Employee Pension Plans) § Keogh § ATRA (After-Tax Retirement Annuity) |

Note that state regulatory approval may be pending for certain of these contracts and they may not currently be available in your state.

More information about CREF is contained in its Statement of Additional Information (“SAI”), dated May 1, 2016, which is incorporated by reference into this Prospectus. The Prospectus, SAI and CREF’s annual and semi-annual reports, which are incorporated by reference herein, are on file with the Securities and Exchange Commission (“SEC”). For a free copy of any of these documents, write to us at 730 Third Avenue, New York, NY 10017-3206, Attn: TIAA Imaging Services, call us at 877 518-9161 or visit our website at www.tiaa.org.

The table of contents for the SAI is on the last page of this Prospectus. The SEC’s website (www.sec.gov) contains this Prospectus, the SAI, annual and semi-annual reports, material incorporated by reference and other information about CREF.

The SEC has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any representation to the contrary is a criminal offense. The CREF Accounts are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Table of contents

Founded in 1952, CREF is a nonprofit membership corporation established in New York State. Its home office is located at 730 Third Avenue, New York, NY 10017-3206. There are also local offices across the United States including Atlanta, Boston, Chicago, Dallas, Denver, Detroit, New York, Philadelphia, San Francisco and Washington, D.C., as well as service centers in New York, Denver and Charlotte. CREF is a diversified, open-end management investment company that is registered with the SEC under the Investment Company Act of 1940, as amended. CREF, the first company in the United States to issue a variable annuity, is the companion organization of Teachers Insurance and Annuity Association of America (“TIAA”). TIAA was founded in 1918 by the Carnegie Foundation for the Advancement of Teaching and offers traditional annuities. TIAA also offers variable annuities that invest in, among other things, real estate (the “TIAA Real Estate Account”) and in mutual funds that invest in equities and fixed-income investments (“TIAA Access”).

Together, CREF and TIAA form the principal retirement system for the nation’s education and research communities, which is one of the largest retirement systems in the world based on assets under management. The TIAA organization serves approximately 5.0 million people at approximately 16,000 institutions. As of December 31, 2015, CREF’s net assets were approximately $215 billion and the combined net assets for TIAA, CREF and other entities within the TIAA organization totaled approximately $854 billion.

College Retirement Equities Fund ■ Prospectus 3

This Prospectus defines certain terms so that you will have a clearer understanding of this Prospectus and your investment.

Account Any of CREF’s investment portfolios. Each Account is a separate portfolio with its own investment objective, which offers three classes of units.

Accumulation The total value of your accumulation units.

Accumulation Period The period during which investment account accumulations are held under a contract prior to their being annuitized or otherwise paid out.

Accumulation Unit A share of participation in a class of an Account for someone in the accumulation period. Each class of each Account has its own accumulation unit value, which typically changes daily.

Annuitant The natural person whose life is used in determining the annuity payments to be received.

Annuity Unit A measure used to calculate the amount of annuity payments, which is based on the expenses of Class R3 of each Account.

Beneficiary Any person or institution named to receive benefits if you die during the accumulation period or if you (and your annuity partner, if you have one) die before the end of any guaranteed period.

Business Day Any day the New York Stock Exchange (“NYSE”) or its affiliated exchanges NYSE Arca Equities or NYSE MKT (collectively with NYSE, the “NYSE Exchanges”) is open for trading. A Business Day generally ends at 4 p.m. Eastern Time or when trading closes on the NYSE Exchanges, if earlier. A Business Day may end early only as of the latest closing time of the regular (or core) trading session of any of the NYSE Exchanges.

Calendar Day Any day of the year. Calendar days end at the same time as Business Days.

Class Each Account issues three classes of units, which have different administrative and distribution expenses. Your eligibility for a particular class will depend upon the asset level of the employer-sponsored plan through which you hold your CREF contract or the product type you own.

Commuted Value The present value of annuity payments due under an income option or method of payment not based on life contingencies.

Eligible Institution A nonprofit institution, including any governmental institution, organized in the United States.

Income Change Method How you choose to have your annuity payments revalued. Under the annual income change method, your payments are revalued once each year. Under the monthly income change method, your payments are revalued every month.

Income Option How you receive your CREF retirement income.

Participant Any person who owns a CREF contract. Sometimes an employer can be a participant.

4 Prospectus ■ College Retirement Equities Fund

Valuation Day Any Business Day.

For purposes of this Prospectus, the term “we” refers to CREF and its affiliates, officers and employees that provide services to CREF, as well as TIAA and its affiliates, to the extent they provide services for CREF.

CREF deducts expenses from the net assets of each class of each Account each Valuation Day for, among other service and expense investment management, administration and distribution services. TIAA or subsidiaries of TIAA provide or arrange for the provision of these services for CREF “at cost” to TIAA and its affiliates. Each Account currently issues three classes of units under the contracts: Class R1, Class R2 and Class R3. There are differences among the expenses associated with each class, such as different administrative and distribution expenses, as described below. Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. Consequently, historical information in this Prospectus that refers to Class R1 of an Account reflects information about the entire Account.

· Investment management expenses. These expenses generally include investment management, portfolio accounting and custodial services, and are the same across all classes.

· Administrative expenses. These cover expenses of administration and operations of CREF and the contracts. Administrative expenses include certain costs associated with the provision by TIAA entities of recordkeeping and other services for retirement plans utilizing the contracts and other pension products in addition to CREF, including other products provided by TIAA or its affiliates. These expenses are allocated to each CREF Account and to each class within an Account in accordance with applicable allocation procedures. This means that participants invested in a particular CREF Account will be subject to different administrative expenses depending upon the class of the Account they own.

· Distribution fees. These are paid under a distribution plan that CREF has adopted authorizing payment of Rule 12b-1 or distribution fees. These fees are for all expenses associated with the provision of distribution services for the CREF contracts. These services include informing you about the contracts and how you can invest, helping employers implement and manage retirement plans and for certain other purposes. The annual distribution expense charge will not be more than 0.25% of an Account’s average daily net assets attributable to any class. These expenses are allocated to each CREF Account and to each class within an Account in accordance with applicable allocation procedures. This means that participants invested in a particular CREF Account will be subject to different distribution fees depending upon the class of the Account they own.

College Retirement Equities Fund ■ Prospectus 5

CREF expenses also include the costs of its audit and legal services, and certain other services provided by third parties, all of which are included in one or more of the expense groups noted above. These expenses may be allocated to one or more particular CREF Accounts and/or classes in accordance with applicable allocation procedures.

CREF also deducts a mortality and expense risk charge that is paid to TIAA to guarantee that CREF participants transferring funds to TIAA for the immediate purchase of lifetime payout annuities will not be charged more than the rate stipulated in the CREF contract. This mortality and expense risk charge is a direct insurance charge. This charge is the same across all classes and Accounts.

All expenses of an Account not specifically attributable to a particular class of that Account are allocated to each class of the Account on the basis of the net assets attributable to that class in relation to the aggregate net assets of the Account. Expenses attributable to an Account allocated to a particular class are borne equally by all units within that class.

The estimated annual expense deduction rates that appear in the following expense table reflect estimates of the amounts we currently expect to deduct to approximate the costs that CREF will incur from May 1, 2016 through April 30, 2017. Actual expenses may be higher or lower.

After the end of every calendar quarter, CREF reconciles the amount deducted from each class of an Account with the expenses actually incurred by the class of the Account and, if there is a difference, it is added to or deducted from the class of the Account in equal daily installments over the remaining days of the quarter, provided that material differences may be repaid in the current calendar quarter, in accordance with accounting principles generally accepted in the United States of America (GAAP). CREF’s at-cost deductions are based on projections of overall expenses and the assets of each class of an Account, and the size of any adjusting payments will be directly affected by how different the projections are from a class of an Account’s actual assets or expenses.

The size of an Account’s assets can be affected by a number of factors, including premium growth, participant transfers into or out of the Account and market performance affecting the value of the Account’s portfolio holdings. In addition, CREF’s operating expenses can fluctuate based on a number of factors, including participant transaction volume, operational efficiency, and technological, personnel and other infrastructure costs. Historically, the adjusting payments have resulted in both upward and downward adjustments to CREF’s expense deductions for the following quarter.

CREF revises its expense rates (the daily deduction rate before the quarterly adjustment) from time to time, usually on an annual basis, in an effort to keep deductions as close as possible to actual expenses.

CREF makes payments to TIAA-CREF Individual & Institutional Services, LLC (“Services”) for distribution services, pursuant to its 12b-1 plan, as described above. In addition, TIAA or its affiliates also may make cash payments to certain third-party broker-dealers and others, such as third-party administrators of

6 Prospectus ■ College Retirement Equities Fund

employer plans, who may provide CREF access to their distribution platforms, as well as transaction processing or administrative services.

Each Account currently issues three classes of units under the contracts. CREF may in the future choose to offer additional or fewer classes of units of the Accounts.

Annual expense deductions

The following table shows the estimated direct and indirect expense deductions for each class of each Account, and is intended to assist you in understanding the costs you will bear directly or indirectly if you buy and hold interests in the Accounts. In addition to these expenses, you may also be subject to state premium taxes. On April 24, 2015, CREF was converted from its one original Class to three different classes, Class R1, Class R2 and Class R3, and all existing participants as of that date received units in the Class for which they were eligible. For information on eligibility for the different classes, see section entitled “Class eligibility” below.

PARTICIPANT TRANSACTION EXPENSES

Charges

for transfers and cash withdrawals | |||||||||||

Deductions from premiums (as a percentage of premiums) |

|

|

|

| |||||||

All CREF Accounts | |||||||||||

Class R1 | none | none | none | none | none | ||||||

Class R2 | none | none | none | none | none | ||||||

Class R3 | none | none | none | none | none | ||||||

College Retirement Equities Fund ■ Prospectus 7

ESTIMATED ANNUAL EXPENSE DEDUCTIONS FROM NET ASSETS

(as a percentage of average net assets)

Investment management expenses | Administrative expenses | Distribution expenses (12b-1) | Mortality and expense risk charges | Total annual expense deductions | ||||||||

Stock Account | ||||||||||||

Class R1 | 0.150 | % | 0.395 | % | 0.165 | % | 0.005 | % | 0.715 | % | ||

Class R2 | 0.150 | 0.245 | 0.090 | 0.005 | 0.490 | |||||||

| Class R3 |

| 0.150 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.380 |

|

Global Equities Account | ||||||||||||

Class R1 | 0.140 | 0.395 | 0.165 | 0.005 | 0.705 | |||||||

Class R2 | 0.140 | 0.245 | 0.090 | 0.005 | 0.480 | |||||||

| Class R3 |

| 0.140 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.370 |

|

Growth Account | ||||||||||||

Class R1 | 0.080 | 0.395 | 0.165 | 0.005 | 0.645 | |||||||

Class R2 | 0.080 | 0.245 | 0.090 | 0.005 | 0.420 | |||||||

| Class R3 |

| 0.080 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.310 |

|

Equity Index Account | ||||||||||||

Class R1 | 0.025 | 0.395 | 0.165 | 0.005 | 0.590 | |||||||

Class R2 | 0.025 | 0.245 | 0.090 | 0.005 | 0.365 | |||||||

| Class R3 |

| 0.025 | 0.165 |

| 0.060 |

| 0.005 |

| 0.255 |

| |

Bond Market Account | ||||||||||||

Class R1 | 0.115 | 0.395 | 0.165 | 0.005 | 0.680 | |||||||

Class R2 | 0.115 | 0.245 | 0.090 | 0.005 | 0.455 | |||||||

| Class R3 |

| 0.115 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.345 |

|

Inflation-Linked Bond Account | ||||||||||||

Class R1 | 0.045 | 0.395 | 0.165 | 0.005 | 0.610 | |||||||

Class R2 | 0.045 | 0.245 | 0.090 | 0.005 | 0.385 | |||||||

| Class R3 |

| 0.045 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.275 |

|

Social Choice Account | ||||||||||||

Class R1 | 0.085 | 0.395 | 0.165 | 0.005 | 0.650 | |||||||

Class R2 | 0.085 | 0.245 | 0.090 | 0.005 | 0.425 | |||||||

| Class R3 |

| 0.085 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.315 |

|

Money Market Account1 | ||||||||||||

Class R1 | 0.040 | 0.395 | 0.165 | 0.005 | 0.605 | |||||||

Class R2 | 0.040 | 0.245 | 0.090 | 0.005 | 0.380 | |||||||

| Class R3 |

| 0.040 |

| 0.165 |

| 0.060 |

| 0.005 |

| 0.270 |

|

1 | Beginning July 16, 2009, TIAA has voluntarily withheld (“waived”) a portion of the 12b-1 distribution and/or administrative expenses for each class of the Money Market Account when a class’s yield was less than zero. TIAA is not obligated to continue this waiver, which is subject to certain regulatory oversight and approval, and TIAA will terminate it by April 14, 2017. There is no assurance that each class of the Account will produce a yield of at least zero. The effect of this waiver is not reflected in the chart. Any expenses waived after October 1, 2010 are subject to possible recovery by TIAA for three years after the waiver. TIAA may recover from a class of the Account a portion of the amounts waived at such time as that | |||||||||||

8 Prospectus ■ College Retirement Equities Fund

class’s daily yield would be positive absent the effect of the waiver, and in such event the amount of recovery on any day will be approximately 25% of the class’s yield (net of all expenses on that day). As a result of the multiclass conversion on April 24, 2015, previously recoverable amounts have been allocated to the various classes. |

The following table shows you an example of the expenses you would incur on a hypothetical investment of $1,000 in each class of each Account over several periods during the accumulation period based on the estimated annual expense deductions in the table above. The table assumes a 5% annual return on assets. Remember that these figures do not represent actual expenses or investment performance, which may differ.

1 year | 3 years | 5 years | 10 years | ||||||

Stock Account | |||||||||

Class R1 | $7 | $23 | $40 | $89 | |||||

Class R2 | $5 | $16 | $27 | $62 | |||||

| Class R3 | $4 |

| $12 |

| $21 |

| $48 |

|

Global Equities Account | |||||||||

Class R1 | $7 | $23 | $39 | $88 | |||||

Class R2 | $5 | $15 | $27 | $60 | |||||

| Class R3 | $4 |

| $12 |

| $21 |

| $47 |

|

Growth Account | |||||||||

Class R1 | $7 | $21 | $36 | $80 | |||||

Class R2 | $4 | $13 | $24 | $53 | |||||

| Class R3 | $3 |

| $10 |

| $17 |

| $39 |

|

Equity Index Account | |||||||||

Class R1 | $6 | $19 | $33 | $74 | |||||

Class R2 | $4 | $12 | $20 | $46 | |||||

| Class R3 | $3 |

| $8 |

| $14 |

| $32 |

|

Bond Market Account | |||||||||

Class R1 | $7 | $22 | $38 | $85 | |||||

Class R2 | $5 | $15 | $25 | $57 | |||||

| Class R3 | $4 |

| $11 |

| $19 |

| $44 |

|

Inflation-Linked Bond Account | |||||||||

Class R1 | $6 | $20 | $34 | $76 | |||||

Class R2 | $4 | $12 | $22 | $49 | |||||

| Class R3 | $3 |

| $9 |

| $15 |

| $35 |

|

Social Choice Account | |||||||||

Class R1 | $7 | $21 | $36 | $81 | |||||

Class R2 | $4 | $14 | $24 | $54 | |||||

| Class R3 | $3 |

| $10 |

| $18 |

| $40 |

|

Money Market Account | |||||||||

Class R1 | $6 | $19 | $34 | $76 | |||||

Class R2 | $4 | $12 | $21 | $48 | |||||

| Class R3 | $3 |

| $9 |

| $15 |

| $34 |

|

College Retirement Equities Fund ■ Prospectus 9

Condensed financial information

Below you will find condensed, audited financial information for Class R1, R2 and R3 units of each Account for each of the periods indicated.

Stock Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $8.076 | $2.108 | $5.968 | $(9.995 | ) | $(4.027 | ) | |||||||||

12/31/14 | 7.897 | 1.620 | 6.277 | 15.744 | 22.021 | ||||||||||||

12/31/13 | 6.581 | 1.476 | 5.105 | 69.661 | 74.766 | ||||||||||||

12/31/12 | 6.328 | 1.244 | 5.084 | 34.469 | 39.553 | ||||||||||||

12/31/11 | 5.308 | 1.151 | 4.157 | (16.066 | ) | (11.909 | ) | ||||||||||

12/31/10 | 4.506 | 1.006 | 3.500 | 29.246 | 32.746 | ||||||||||||

12/31/09 | 4.251 | 0.849 | 3.402 | 47.129 | 50.531 | ||||||||||||

12/31/08 | 5.339 | 1.113 | 4.226 | (107.993 | ) | (103.767 | ) | ||||||||||

12/31/07 | 4.754 | 0.992 | 3.762 | 15.589 | 19.351 | ||||||||||||

12/31/06 | 4.329 | 1.095 | 3.234 | 32.372 | 35.606 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 5.699 | 1.215 | 4.484 | (30.621 | ) | (26.137 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 5.698 | 0.960 | 4.738 | (30.626 | ) | (25.888 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

j | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was (0.90)% and (0.84)%, respectively. | ||||||||||||||||

10 Prospectus ■ College Retirement Equities Fund

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Accumulation

|

| |||||||

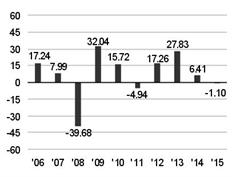

$365.431 | $361.404 | (1.10 | )% | 0.57 | % | 1.60 | % | 52 | % | 39 | ||||||||||

343.410 | 365.431 | 6.41 | 0.46 | 1.77 | 58 | 306 | ||||||||||||||

268.644 | 343.410 | 27.83 | 0.48 | 1.68 | 59 | 330 | ||||||||||||||

229.091 | 268.644 | 17.26 | 0.49 | 2.01 | 57 | 353 | ||||||||||||||

241.000 | 229.091 | (4.94 | ) | 0.48 | 1.73 | 56 | 377 | |||||||||||||

208.254 | 241.000 | 15.72 | 0.47 | 1.63 | 61 | 401 | ||||||||||||||

157.723 | 208.254 | 32.04 | 0.49 | 1.97 | 58 | 418 | ||||||||||||||

261.490 | 157.723 | (39.68 | ) | 0.64 | 1.95 | 53 | 424 | |||||||||||||

242.139 | 261.490 | 7.99 | 0.52 | 1.44 | 49 | 448 | ||||||||||||||

206.533 | 242.139 | 17.24 | 0.49 | 1.44 | 51 | 469 | ||||||||||||||

388.266 | 362.129 | (6.73 | )cj | 0.48 | d | 1.75 | d | 52 | 94 | |||||||||||

388.266 | 362.378 | (6.67 | )cj | 0.38 | d | 1.85 | d | 52 | 148 | |||||||||||

College Retirement Equities Fund ■ Prospectus 11

Condensed financial information

Global Equities Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $3.077 | $0.823 | $2.254 | $(3.090 | ) | $(0.836 | ) | |||||||||

12/31/14 | 3.394 | 0.623 | 2.771 | 2.779 | 5.550 | ||||||||||||

12/31/13 | 2.590 | 0.616 | 1.974 | 26.579 | 28.553 | ||||||||||||

12/31/12 | 2.566 | 0.522 | 2.044 | 14.260 | 16.304 | ||||||||||||

12/31/11 | 2.131 | 0.490 | 1.641 | (9.051 | ) | (7.410 | ) | ||||||||||

12/31/10 | 1.888 | 0.432 | 1.456 | 8.987 | 10.443 | ||||||||||||

12/31/09 | 1.862 | 0.374 | 1.488 | 19.648 | 21.136 | ||||||||||||

12/31/08 | 2.587 | 0.462 | 2.125 | (49.181 | ) | (47.056 | ) | ||||||||||

12/31/07 | 2.069 | 0.409 | 1.660 | 8.522 | 10.182 | ||||||||||||

12/31/06 | 1.716 | 0.481 | 1.235 | 14.969 | 16.204 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 2.030 | 0.468 | 1.562 | (11.301 | ) | (9.739 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 2.030 | 0.370 | 1.660 | (11.304 | ) | (9.644 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

k | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was (0.41)% and (0.34)%, respectively. | ||||||||||||||||

12 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Accumulation

|

| |||||||

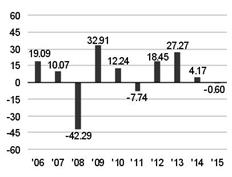

$138.793 | $137.957 | (0.60 | )% | 0.58 | % | 1.59 | % | 49 | % | 24 | ||||||||||

133.243 | 138.793 | 4.17 | 0.46 | 2.04 | 59 | 136 | ||||||||||||||

104.690 | 133.243 | 27.27 | 0.52 | 1.67 | 63 | 141 | ||||||||||||||

88.386 | 104.690 | 18.45 | 0.53 | 2.09 | 70 | 142 | ||||||||||||||

95.796 | 88.386 | (7.74 | ) | 0.52 | 1.74 | 78 | 146 | |||||||||||||

85.353 | 95.796 | 12.24 | 0.50 | 1.69 | 81 | 152 | ||||||||||||||

64.217 | 85.353 | 32.91 | 0.53 | 2.11 | 59 | 155 | ||||||||||||||

111.273 | 64.217 | (42.29 | ) | 0.68 | 2.34 | 76 | 147 | |||||||||||||

101.091 | 111.273 | 10.07 | 0.56 | 1.53 | 108 | 153 | ||||||||||||||

84.887 | 101.091 | 19.09 | 0.52 | 1.35 | 137 | 151 | ||||||||||||||

147.969 | 138.230 | (6.58 | )ck | 0.48 | d | 1.60 | d | 49 | 47 | |||||||||||

147.969 | 138.325 | (6.52 | )ck | 0.38 | d | 1.70 | d | 49 | 62 | |||||||||||

College Retirement Equities Fund ■ Prospectus 13

Condensed financial information

Growth Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $1.663 | $0.683 | $0.980 | $6.976 | $7.956 | |||||||||||

12/31/14 | 1.501 | 0.482 | 1.019 | 14.445 | 15.464 | ||||||||||||

12/31/13 | 1.288 | 0.450 | 0.838 | 28.513 | 29.351 | ||||||||||||

12/31/12 | 1.388 | 0.382 | 1.006 | 10.481 | 11.487 | ||||||||||||

12/31/11 | 0.979 | 0.333 | 0.646 | 0.202 | 0.848 | ||||||||||||

12/31/10 | 0.907 | 0.293 | 0.614 | 8.706 | 9.320 | ||||||||||||

12/31/09 | 0.836 | 0.249 | 0.587 | 16.058 | 16.645 | ||||||||||||

12/31/08 | 0.740 | 0.316 | 0.424 | (30.509 | ) | (30.085 | ) | ||||||||||

12/31/07 | 0.694 | 0.272 | 0.422 | 10.416 | 10.838 | ||||||||||||

12/31/06 | 0.625 | 0.321 | 0.304 | 3.066 | 3.370 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 1.117 | 0.380 | 0.737 | (1.993 | ) | (1.256 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 1.117 | 0.287 | 0.830 | (1.992 | ) | (1.162 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

l | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was 6.40% and 6.47%, respectively. | ||||||||||||||||

14 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Accumulation

|

| |||||||

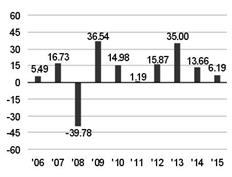

$128.668 | $136.624 | 6.19 | % | 0.51 | % | 0.73 | % | 47 | % | 31 | ||||||||||

113.204 | 128.668 | 13.66 | 0.41 | 0.86 | 57 | 164 | ||||||||||||||

83.853 | 113.204 | 35.00 | 0.46 | 0.86 | 63 | 169 | ||||||||||||||

72.366 | 83.853 | 15.87 | 0.47 | 1.24 | 67 | 176 | ||||||||||||||

71.518 | 72.366 | 1.19 | 0.46 | 0.88 | 57 | 181 | ||||||||||||||

62.198 | 71.518 | 14.98 | 0.46 | 0.96 | 77 | 187 | ||||||||||||||

45.553 | 62.198 | 36.54 | 0.48 | 1.14 | 81 | 190 | ||||||||||||||

75.638 | 45.553 | (39.78 | ) | 0.69 | 0.68 | 82 | 178 | |||||||||||||

64.800 | 75.638 | 16.73 | 0.55 | 0.60 | 127 | 181 | ||||||||||||||

61.430 | 64.800 | 5.49 | 0.52 | 0.49 | 109 | 182 | ||||||||||||||

138.152 | 136.896 | (0.91 | )cl | 0.41 | d | 0.79 | d | 47 | 55 | |||||||||||

138.152 | 136.990 | (0.84 | )cl | 0.31 | d | 0.89 | d | 47 | 73 | |||||||||||

College Retirement Equities Fund ■ Prospectus 15

Condensed financial information

Equity Index Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $3.254 | $0.765 | $2.489 | $(2.523 | ) | $(0.034 | ) | |||||||||

12/31/14 | 2.937 | 0.558 | 2.379 | 15.145 | 17.524 | ||||||||||||

12/31/13 | 2.546 | 0.531 | 2.015 | 33.715 | 35.730 | ||||||||||||

12/31/12 | 2.391 | 0.442 | 1.949 | 12.978 | 14.927 | ||||||||||||

12/31/11 | 1.832 | 0.390 | 1.442 | (0.825 | ) | 0.617 | |||||||||||

12/31/10 | 1.613 | 0.343 | 1.270 | 11.830 | 13.100 | ||||||||||||

12/31/09 | 1.470 | 0.288 | 1.182 | 16.176 | 17.358 | ||||||||||||

12/31/08 | 1.823 | 0.429 | 1.394 | (38.771 | ) | (37.377 | ) | ||||||||||

12/31/07 | 1.806 | 0.383 | 1.423 | 3.050 | 4.473 | ||||||||||||

12/31/06 | 1.636 | 0.385 | 1.251 | 11.332 | 12.583 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 2.443 | 0.414 | 2.029 | (8.184 | ) | (6.155 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 2.443 | 0.302 | 2.141 | (8.185 | ) | (6.044 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

m | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was 0.18% and 0.25%, respectively. | ||||||||||||||||

16 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Accumulation

|

| |||||||

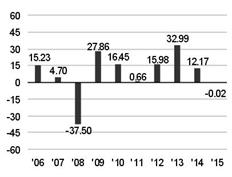

$161.562 | $161.528 | (0.02 | )% | 0.47 | % | 1.52 | % | 5 | % | 20 | ||||||||||

144.038 | 161.562 | 12.17 | 0.37 | 1.58 | 4 | 104 | ||||||||||||||

108.308 | 144.038 | 32.99 | 0.42 | 1.59 | 5 | 108 | ||||||||||||||

93.381 | 108.308 | 15.98 | 0.43 | 1.89 | 4 | 109 | ||||||||||||||

92.764 | 93.381 | 0.66 | 0.41 | 1.53 | 5 | 112 | ||||||||||||||

79.664 | 92.764 | 16.45 | 0.42 | 1.54 | 8 | 116 | ||||||||||||||

62.306 | 79.664 | 27.86 | 0.43 | 1.77 | 5 | 116 | ||||||||||||||

99.683 | 62.306 | (37.50 | ) | 0.59 | 1.67 | 7 | 113 | |||||||||||||

95.210 | 99.683 | 4.70 | 0.47 | 1.39 | 9 | 113 | ||||||||||||||

82.627 | 95.210 | 15.23 | 0.43 | 1.39 | 10 | 116 | ||||||||||||||

168.005 | 161.850 | (3.66 | )cm | 0.37 | d | 1.81 | d | 5 | 35 | |||||||||||

168.005 | 161.961 | (3.60 | )cm | 0.27 | d | 1.90 | d | 5 | 44 | |||||||||||

College Retirement Equities Fund ■ Prospectus 17

Condensed financial information

Bond Market Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $3.015 | $0.637 | $2.378 | $(2.100 | ) | $0.278 | ||||||||||

12/31/14 | 2.665 | 0.494 | 2.171 | 3.764 | 5.935 | ||||||||||||

12/31/13 | 2.485 | 0.482 | 2.003 | (4.211 | ) | (2.208 | ) | ||||||||||

12/31/12 | 2.835 | 0.482 | 2.353 | 3.163 | 5.516 | ||||||||||||

12/31/11 | 3.341 | 0.439 | 2.902 | 3.876 | 6.778 | ||||||||||||

12/31/10 | 3.470 | 0.422 | 3.048 | 3.096 | 6.144 | ||||||||||||

12/31/09 | 3.818 | 0.399 | 3.419 | 2.556 | 5.975 | ||||||||||||

12/31/08 | 4.241 | 0.416 | 3.825 | (2.777 | ) | 1.048 | |||||||||||

12/31/07 | 4.260 | 0.315 | 3.945 | 0.806 | 4.751 | ||||||||||||

12/31/06 | 3.990 | 0.373 | 3.617 | (0.467 | ) | 3.150 | |||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 2.181 | 0.369 | 1.812 | (3.573 | ) | (1.761 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 2.182 | 0.292 | 1.890 | (3.573 | ) | (1.683 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

n | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was 0.44% and 0.51%, respectively. | ||||||||||||||||

18 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| |||||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Portfolio turnover rate excluding mortgage dollar rolls |

| Accumulation

|

| ||||||||

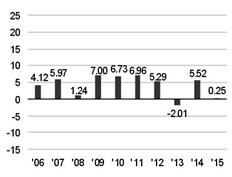

$113.471 | $113.749 | 0.25 | % | 0.56 | % | 2.07 | % | 293 | % | 123 | % | 19 | |||||||||||

107.536 | 113.471 | 5.52 | 0.44 | 1.95 | 290 | 89 | 117 | ||||||||||||||||

109.744 | 107.536 | (2.01 | ) | 0.45 | 1.85 | 363 | 105 | 119 | |||||||||||||||

104.228 | 109.744 | 5.29 | 0.45 | 2.19 | 356 | 117 | 130 | ||||||||||||||||

97.450 | 104.228 | 6.96 | 0.44 | 2.88 | 261 | 62 | 126 | ||||||||||||||||

91.306 | 97.450 | 6.73 | 0.44 | 3.19 | 230 | 62 | 122 | ||||||||||||||||

85.331 | 91.306 | 7.00 | 0.45 | 3.88 | 185 | 96 | 113 | ||||||||||||||||

84.283 | 85.331 | 1.24 | 0.61 | 4.53 | 125 | — | 100 | ||||||||||||||||

79.532 | 84.283 | 5.97 | 0.51 | 4.86 | 174 | — | 89 | ||||||||||||||||

76.382 | 79.532 | 4.12 | 0.48 | 4.69 | 219 | — | 78 | ||||||||||||||||

115.735 | 113.974 | (1.52 | )cn | 0.47 | d | 2.31 | d | 293 | 123 | 40 | |||||||||||||

115.735 | 114.052 | (1.45 | )cn | 0.37 | d | 2.41 | d | 293 | 123 | 55 | |||||||||||||

College Retirement Equities Fund ■ Prospectus 19

Condensed financial information

Inflation-Linked Bond Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $(0.930 | ) | $0.324 | $(1.254 | ) | $(0.034 | ) | $(1.288 | ) | |||||||

12/31/14 | 1.573 | 0.257 | 1.316 | 0.824 | 2.140 | ||||||||||||

12/31/13 | 1.207 | 0.301 | 0.906 | (7.289 | ) | (6.383 | ) | ||||||||||

12/31/12 | 2.050 | 0.310 | 1.740 | 2.523 | 4.263 | ||||||||||||

12/31/11 | 2.817 | 0.272 | 2.545 | 5.187 | 7.732 | ||||||||||||

12/31/10 | 1.596 | 0.254 | 1.342 | 1.929 | 3.271 | ||||||||||||

12/31/09 | 0.974 | 0.241 | 0.733 | 4.119 | 4.852 | ||||||||||||

12/31/08 | 2.700 | 0.249 | 2.451 | (3.367 | ) | (0.916 | ) | ||||||||||

12/31/07 | 2.618 | 0.186 | 2.432 | 2.695 | 5.127 | ||||||||||||

12/31/06 | 1.560 | 0.228 | 1.332 | (1.339 | ) | (0.007 | ) | ||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 1.272 | 0.185 | 1.087 | (3.973 | ) | (2.886 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 1.274 | 0.140 | 1.134 | (3.975 | ) | (2.841 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

o | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was (1.74)% and (1.68)%, respectively. | ||||||||||||||||

20 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Accumulation

|

| |||||||

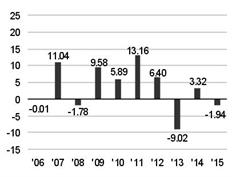

$66.522 | $65.234 | (1.94 | )% | 0.48 | % | (1.87 | )% | 6 | % | 17 | ||||||||||

64.382 | 66.522 | 3.32 | 0.39 | 1.97 | 9 | 107 | ||||||||||||||

70.765 | 64.382 | (9.02 | ) | 0.45 | 1.34 | 13 | 115 | |||||||||||||

66.502 | 70.765 | 6.40 | 0.45 | 2.52 | 11 | 149 | ||||||||||||||

58.770 | 66.502 | 13.16 | 0.43 | 4.05 | 13 | 146 | ||||||||||||||

55.499 | 58.770 | 5.89 | 0.44 | 2.33 | 15 | 135 | ||||||||||||||

50.647 | 55.499 | 9.58 | 0.45 | 1.38 | 11 | 134 | ||||||||||||||

51.563 | 50.647 | (1.78 | ) | 0.58 | 4.69 | 19 | 116 | |||||||||||||

46.436 | 51.563 | 11.04 | 0.50 | 5.00 | 13 | 91 | ||||||||||||||

46.443 | 46.436 | (0.01 | ) | 0.49 | 2.83 | 23 | 77 | |||||||||||||

68.248 | 65.362 | (4.23 | )co | 0.41 | d | 2.38 | d | 6 | 32 | |||||||||||

68.248 | 65.407 | (4.16 | )co | 0.31 | d | 2.48 | d | 6 | 49 | |||||||||||

College Retirement Equities Fund ■ Prospectus 21

Condensed financial information

Social Choice Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $4.618 | $1.017 | $3.601 | $(5.795 | ) | $(2.194 | ) | |||||||||

12/31/14 | 4.446 | 0.773 | 3.673 | 8.760 | 12.433 | ||||||||||||

12/31/13 | 3.804 | 0.757 | 3.047 | 22.950 | 25.997 | ||||||||||||

12/31/12 | 3.866 | 0.677 | 3.189 | 12.242 | 15.431 | ||||||||||||

12/31/11 | 3.732 | 0.619 | 3.113 | (0.595 | ) | 2.518 | |||||||||||

12/31/10 | 3.618 | 0.561 | 3.057 | 11.683 | 14.740 | ||||||||||||

12/31/09 | 3.517 | 0.488 | 3.029 | 19.530 | 22.559 | ||||||||||||

12/31/08 | 4.191 | 0.600 | 3.591 | (34.439 | ) | (30.848 | ) | ||||||||||

12/31/07 | 4.165 | 0.492 | 3.673 | 2.371 | 6.044 | ||||||||||||

12/31/06 | 3.687 | 0.535 | 3.152 | 8.412 | 11.564 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 3.229 | 0.560 | 2.669 | (11.025 | ) | (8.356 | ) | |||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 3.230 | 0.427 | 2.803 | (11.028 | ) | (8.225 | ) | |||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

p | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was (0.93)% and (0.86)%, respectively. | ||||||||||||||||

22 Prospectus ■ College Retirement Equities Fund

(continued)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| |||||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Net investment income (loss) |

| Portfolio turnover rate |

| Portfolio turnover rate excluding mortgage dollar rolls |

| Accumulation

|

| ||||||||

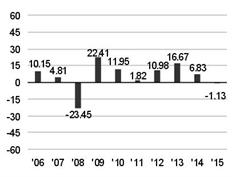

$194.396 | $192.202 | (1.13 | )% | 0.52 | % | 1.83 | % | 115 | % | 57 | % | 12 | |||||||||||

181.963 | 194.396 | 6.83 | 0.41 | 1.95 | 120 | 52 | 72 | ||||||||||||||||

155.966 | 181.963 | 16.67 | 0.45 | 1.79 | 133 | 46 | 72 | ||||||||||||||||

140.535 | 155.966 | 10.98 | 0.45 | 2.14 | 149 | 52 | 71 | ||||||||||||||||

138.017 | 140.535 | 1.82 | 0.44 | 2.22 | 122 | 45 | 72 | ||||||||||||||||

123.277 | 138.017 | 11.95 | 0.44 | 2.39 | 98 | 40 | 72 | ||||||||||||||||

100.718 | 123.277 | 22.41 | 0.45 | 2.81 | 85 | 49 | 68 | ||||||||||||||||

131.566 | 100.718 | (23.45 | ) | 0.61 | 3.02 | 77 | — | 66 | |||||||||||||||

125.522 | 131.566 | 4.81 | 0.48 | 2.81 | 60 | — | 68 | ||||||||||||||||

113.958 | 125.522 | 10.15 | 0.45 | 2.65 | 84 | — | 67 | ||||||||||||||||

200.939 | 192.583 | (4.16 | )cp | 0.42 | d | 1.99 | d | 115 | 57 | 25 | |||||||||||||

200.939 | 192.714 | (4.09 | )cp | 0.32 | d | 2.09 | d | 115 | 57 | 31 | |||||||||||||

College Retirement Equities Fund ■ Prospectus 23

Condensed financial information

Money Market Account

Selected per accumulation unit data |

|

|

|

|

|

| |||||||||||

|

|

|

|

|

|

| |||||||||||

|

| For

the period | Investment

| a | Expenses | a | Net

| a |

|

| Net

|

| |||||

Class R1 | |||||||||||||||||

12/31/15 | h | $0.036 | $0.036 | $0.000 | $0.000 | $0.000 | |||||||||||

12/31/14 | 0.029 | 0.029 | 0.000 | 0.000 | 0.000 | ||||||||||||

12/31/13 | 0.036 | 0.036 | 0.000 | 0.000 | 0.000 | ||||||||||||

12/31/12 | 0.044 | 0.044 | 0.000 | 0.000 | 0.000 | ||||||||||||

12/31/11 | 0.044 | 0.044 | 0.000 | 0.001 | 0.001 | ||||||||||||

12/31/10 | 0.062 | 0.062 | 0.000 | 0.000 | 0.000 | ||||||||||||

12/31/09 | 0.164 | 0.104 | 0.060 | (0.031 | ) | 0.029 | |||||||||||

12/31/08 | 0.700 | 0.124 | 0.576 | 0.032 | 0.608 | ||||||||||||

12/31/07 | 1.258 | 0.092 | 1.166 | (0.004 | ) | 1.162 | |||||||||||

12/31/06 | 1.169 | 0.098 | 1.071 | 0.000 | 1.071 | ||||||||||||

Class R2 | |||||||||||||||||

12/31/15 | g | 0.030 | 0.030 | 0.000 | 0.000 | 0.000 | |||||||||||

Class R3 | |||||||||||||||||

12/31/15 | g | 0.030 | 0.030 | 0.000 | 0.000 | 0.000 | |||||||||||

a | Based on average units outstanding. | ||||||||||||||||

b | Based on per accumulation unit data. Information for Annuity Units is not presented. | ||||||||||||||||

c | The percentages shown for this period are not annualized. | ||||||||||||||||

d | The percentages shown for this period are annualized. | ||||||||||||||||

g | Classes R2 and R3 commenced operations on April 24, 2015. | ||||||||||||||||

h | Prior to April 24, 2015, CREF offered only one class of units, which became Class R1 on that date. | ||||||||||||||||

q | The annual performance for Classes R2 and R3, including performance based on Class R1 prior to inception of the new classes, was 0.00% and 0.00%, respectively. | ||||||||||||||||

24 Prospectus ■ College Retirement Equities Fund

(concluded)

|

|

|

|

|

| Ratios and supplemental data |

|

|

|

| ||||||||||

| Accumulation unit value |

Ratios to average |

|

| ||||||||||||||||

Beginning

|

| End

|

| Total

| b | Gross

|

| Expenses net of TIAA withholding |

| Net investment income (loss) |

| Accumulation

|

| |||||||

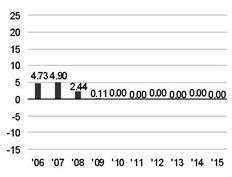

$25.534 | $25.534 | 0.00 | % | 0.50 | % | 0.14 | % | 0.00 | % | 87 | ||||||||||

25.534 | 25.534 | 0.00 | 0.39 | 0.11 | 0.00 | 441 | ||||||||||||||

25.534 | 25.534 | 0.00 | 0.41 | 0.14 | 0.00 | 461 | ||||||||||||||

25.534 | 25.534 | 0.00 | 0.42 | 0.17 | 0.00 | 458 | ||||||||||||||

25.533 | 25.534 | 0.00 | 0.41 | 0.17 | 0.00 | 477 | ||||||||||||||

25.533 | 25.533 | 0.00 | 0.41 | 0.24 | 0.00 | 463 | ||||||||||||||

25.504 | 25.533 | 0.11 | 0.43 | 0.41 | 0.21 | 512 | ||||||||||||||

24.896 | 25.504 | 2.44 | 0.56 | 0.56 | 2.25 | 582 | ||||||||||||||

23.734 | 24.896 | 4.90 | 0.45 | 0.45 | 4.79 | 469 | ||||||||||||||

22.663 | 23.734 | 4.73 | 0.43 | 0.43 | 4.64 | 393 | ||||||||||||||

25.534 | 25.534 | 0.00 | cq | 0.40 | d | 0.17 | d | 0.00 | d | 137 | ||||||||||

25.534 | 25.534 | 0.00 | cq | 0.30 | d | 0.17 | d | 0.00 | d | 215 | ||||||||||

College Retirement Equities Fund ■ Prospectus 25

CREF has eight investment portfolios, or Accounts, which are divided into several categories reflecting different investment management strategies. They are:

Equity Accounts:

· Stock Account

· Global Equities Account

· Growth Account

Index Account:

· Equity Index Account

Fixed-Income Accounts:

· Bond Market Account

· Inflation-Linked Bond Account

Specialty/Balanced Account:

· Social Choice Account

Money Market Account:

· Money Market Account

CREF’s goal is to provide retirement benefits. CREF has a long-term investment perspective and the Accounts provide a wide range of investment alternatives. Each Account has its own investment objective, policies and special risks. The investment objective of an Account cannot be changed without the approval of a majority of Account participants. CREF can change investment policies without such approval. There is no guarantee that any Account will meet its investment objective.

Each of the Stock, Global Equities, Equity Index, Bond Market and Inflation-Linked Bond has a policy of investing, under normal circumstances, at least 80% of its respective assets (net assets, plus the amount of any borrowings for investment purposes) in certain securities implied by its name, including such terms as “equity” and “index.” Each of these Accounts will provide its participants with at least 60 days’ prior notice before making changes to this policy. The Accounts are not appropriate for market timing. You should not invest in the Accounts if you are a market timer.

26 Prospectus ■ College Retirement Equities Fund

Investment Objective: A favorable long-term rate of return through capital appreciation and investment income by investing primarily in a broadly diversified portfolio of common stocks.

Principal Investment Strategies: Under normal circumstances, the Stock Account invests at least 80% of its assets in a broadly diversified portfolio of common stocks. The Account’s investment adviser, TIAA-CREF Investment Management, LLC (“TCIM”), typically uses a combination of three different investment strategies to manage the Account—active management, enhanced indexing and pure indexing—and invests in both domestic and foreign securities. TCIM seeks to achieve the Account’s overall investment objective by managing the Account in segments, each of which may use one of these different investment strategies.

A portion of the Account is managed using an active management strategy. With active management, TCIM concentrates on individual companies rather than sectors or industries. TCIM looks for stocks that it believes are attractively priced based on an analysis of the company’s prospects for growth in earnings, cash flow, revenues or other relevant measures. TCIM also looks for companies whose assets appear undervalued in the market. In general, TCIM focuses on companies with shareholder-oriented management dedicated to creating shareholder value. The Account may invest in companies of any size, including small companies.

A portion of the Account is managed using an enhanced index strategy. With enhanced indexing, TCIM may use several different investment techniques to build a portfolio of stocks that is structured to resemble and share the risk characteristics of various segments of the benchmark index, while also seeking to outperform that benchmark index. Enhanced index strategies often employ proprietary, quantitative modeling techniques for stock selection, country allocation and portfolio construction. Quantitative analysis involves the use of mathematical models and computer programs that attempt to outperform the index by over- and underweighting certain stocks while keeping the Account’s overall financial and risk characteristics similar to those of its benchmark index. Relative to TCIM’s other approaches for managing other equity accounts, in general, the enhanced indexing methodology is designed so that the Account diverges from and may outperform its benchmark more than an indexing approach, but remains closer to the benchmark than other equity accounts using a traditional active management style. Enhanced index strategies will typically hold more stocks than traditional active strategies.

A portion of the Account is managed using a pure index strategy. This portion of the Account is designed to track various segments of the component indices of the Account’s composite benchmark index. This portion of the Account buys most, but not necessarily all, of the stocks in the indices of its composite

College Retirement Equities Fund ■ Prospectus 27

benchmark index, and will attempt to closely match the overall investment characteristics of its composite benchmark index.

The Account invests in foreign stocks and other equity securities. The Account also may invest in fixed-income securities and money market instruments traded on foreign exchanges or in other foreign securities markets, or that are privately placed. Foreign securities have different types and levels of risk than domestic securities. The Account will also invest a portion of its foreign investments in emerging market securities and, to a lesser extent, foreign developed market small-cap equities. Under normal circumstances the Account seeks to maintain the weightings of its holdings as approximately 70–75% domestic equities and 25–30% foreign equities. Under normal circumstances, the foreign equities portion of the Account will include investments in both developed and emerging markets securities and in securities of large-, mid- and small-capitalization issuers. As of December 31, 2015, the market value of the Account was divided as indicated below among U.S., foreign developed and foreign emerging markets securities:

| ||||

69.5 | % | United States | ||

23.9 | % | Foreign developed markets | ||

6.6 | % | Foreign emerging markets |

For a discussion of additional risks concerning investments in foreign securities, see “Additional information about investment strategies and risks” below.

Within the Account’s globally diversified, multi-investment style strategy, the Account allocates assets to a variety of underlying investment strategies. The allocations to such strategies, including domestic or foreign investments in mega-cap, large-cap, mid-cap and small-cap and various industry sector specializations, may change over time. As of December 31, 2015, the equity investments of the Account were divided among issuers with varying market capitalizations as indicated below:

| ||||

41.9 | % | Mega-cap: more than $50 billion | ||

24.1 | % | Large-cap: more than $15 billion–$50 billion | ||

26.5 | % | Mid-cap: more than $2 billion–$15 billion | ||

7.5 | % | Small-cap: $2 billion or less |

The benchmark for the Stock Account is a composite index composed of two unmanaged indices: the Russell 3000® Index and the MSCI All Country World ex-USA Investable Market Index (“MSCI ACWI ex-USA IMI”). The weights in the composite index change to reflect the relative sizes of the domestic and foreign segments of the Account and to maintain its consistency with the Account’s

28 Prospectus ■ College Retirement Equities Fund

investment strategies. See “More about benchmarks and other indices” below for additional information about composite and other benchmarks.

Principal Investment Risks: The Account is subject to the following principal investment risks:

· market risk;

· issuer risk (often called financial risk);

· index risk;

· enhanced index risk;

· quantitative analysis risk;

· foreign investment risk;

· emerging markets risk;

· small-cap risk;

· mid-cap risk;

· large-cap risk; and

· active management risk.

Investing in securities traded in foreign exchanges or foreign markets involves risks beyond those of domestic investing. These include political or social instability, changes in currency rates and the possible imposition of market controls or currency exchange controls. Also, seeking enhanced results relative to an index may cause that portion of the Account that is managed using an enhanced index strategy to underperform the index. Furthermore, because of the Account’s size, it may be buying or selling blocks of stock that are large compared to the stock’s trading volume, making it difficult to reach the positions called for by TCIM’s investment decisions and/or affecting the stock’s price. As a result, TCIM may not be able to adjust the portfolio as quickly as it would like.

As with any investment, you can lose money by investing in this Account.

Who May Want to Invest: The Stock Account may be best for individuals who have a longer time horizon, think stocks will perform well over time and want to invest in a broadly diversified stock portfolio.

See “Principal risks of investing in the Accounts” below and “Additional information about investment strategies and risks” below for more information.

Investment Objective: A favorable long-term rate of return through capital appreciation and income from a broadly diversified portfolio that consists primarily of foreign and domestic common stocks.

Principal Investment Strategies: Under normal circumstances, the Global Equities Account invests at least 80% of its assets in equity securities of foreign and domestic companies. Typically, at least 40% of the Account is invested in foreign securities and at least 25% in domestic securities, as TCIM deems appropriate. The remaining 35% is distributed between foreign and domestic securities. However, when market conditions warrant, the Account may invest

College Retirement Equities Fund ■ Prospectus 29

more than 60% of its assets in U.S. issuers. In such cases the Account will invest at least 30% in foreign issuers. These percentages may vary according to market conditions. As of December 31, 2015, the portfolio of investments of the Account was divided as indicated below among U.S., foreign developed market and foreign emerging market securities:

| ||||

59.2 | % | United States | ||

39.0 | % | Foreign developed markets | ||

1.8 | % | Foreign emerging markets |

Normally, the Account will be invested in at least three different countries, one of which will be the United States, although the Account will usually be more diversified. For a discussion of additional risks concerning investments in foreign securities, see “Additional information about investment strategies and risks” below.

The Account can invest in companies of any size, including small companies. Investing in smaller companies entails more risk. See “Principal investment risks” for the Global Equities Account below.

TCIM typically uses a combination of three different investment strategies to manage the Account—active management, enhanced indexing and pure indexing. TCIM seeks to achieve the Account’s overall investment objective by managing the Account in segments, each of which may use one of these different investment strategies. For that portion of the Account that is actively managed, TCIM looks for stocks that it believes are attractively priced based on an analysis of the company’s prospects for growth in earnings, cash flow, revenues or other relevant measures. TCIM also looks for companies whose assets appear undervalued in the market. In general, TCIM focuses on companies with shareholder-oriented management dedicated to creating shareholder value.

A portion of the Account is managed using an enhanced index strategy. With enhanced indexing, TCIM may use several different investment techniques to build a portfolio that is structured to resemble and share the risk characteristics of various segments of the benchmark index, while also seeking to outperform that benchmark index. Enhanced index strategies often employ proprietary, quantitative modeling techniques for stock selection, country allocation and portfolio construction. Quantitative analysis involves the use of mathematical models and computer programs that attempt to outperform the index by over- and underweighting certain stocks while keeping the Account’s overall financial and risk characteristics similar to those of its benchmark index. Relative to TCIM’s other approaches for managing other equity accounts, in general, the enhanced indexing methodology is designed so that the Account diverges from and may outperform its benchmark more than an indexing approach, but remains closer to the benchmark than other equity accounts using a traditional active management

30 Prospectus ■ College Retirement Equities Fund

style. Enhanced index strategies will typically hold more stock than traditional active strategies.

A portion of the Account is managed using a pure index strategy. This portion of the Account is designed to track various segments of the benchmark index. This portion of the Account buys most, but not necessarily all, of the securities in the Account’s benchmark index, and will attempt to closely match the overall investment characteristics of its benchmark index.

Within the Account’s globally diversified, multi-investment style strategy, the Account allocates assets to a variety of underlying investment strategies. The allocations to such strategies, including domestic or foreign investments in large-cap, mid-cap and small-cap and various industry sector specializations, may change over time.

The benchmark for the Global Equities Account is the MSCI World Index. See “More about benchmarks and other indices” below for additional information about benchmarks.

Principal Investment Risks: The Account is subject to the following principal investment risks:

· market risk;

· issuer risk (often called financial risk);

· quantitative analysis risk;

· index risk;

· enhanced index risk;

· foreign investment risk;

· small-cap risk;

· mid-cap risk;

· active management risk;

· large-cap risk; and

· emerging markets risk.

Investing in securities traded in foreign exchanges or foreign markets involves risks beyond those of domestic investing. These include political or social instability, changes in currency rates and the possible imposition of market controls or currency exchange controls. Also, seeking enhanced results relative to an index may cause that portion of the Account that is managed using an enhanced index strategy to underperform the index. The Account may also be subject to market timing risk due to “stale price arbitrage,” in which an investor seeks to take advantage of the perceived difference in price from a foreign market closing price. If not mitigated through effective policies, market timing can interfere with efficient portfolio management and cause dilution. The Account has in place policies and procedures that are designed to reduce the risk of market timing in the Account.

As with any investment, you can lose money by investing in this Account.

College Retirement Equities Fund ■ Prospectus 31

Who May Want to Invest: The Global Equities Account may be best for individuals who have a longer time horizon, think stocks will perform well over time and want to take advantage of the potential of foreign as well as domestic markets.

See “Principal risks of investing in the Accounts” below and “Additional information about investment strategies and risks” below for more information.

Investment Objective: A favorable long-term rate of return, mainly through capital appreciation, primarily from a diversified portfolio of common stocks that present the opportunity for exceptional growth.

Principal Investment Strategies: Under normal circumstances, the Growth Account invests at least 80% of its assets in common stocks and other equity securities. The Account invests primarily in large, well-known, established companies, particularly when TCIM believes they have new or innovative products, services or processes that enhance future earnings prospects. To a lesser extent, the Account may also invest in smaller, less seasoned companies with growth potential as well as companies in new and emerging areas of the economy. The Account may also invest in companies in order to benefit from prospective acquisitions, reorganizations, corporate restructurings or other special situations.

Growth-oriented companies are companies with a strong competitive position within their industry or a competitive position within a very strong industry. Generally, growth investing entails analyzing the quality of a company’s earnings (i.e., the degree to which earnings are derived from sustainable sources), and analyzing companies as if one would be buying the underlying business, not simply trading its equity. Growth investing also involves fundamental research and qualitative analysis of particular companies in order to identify and benefit from particular companies whose business prospects appear underappreciated by the market.

The Account may buy foreign securities and other instruments if TCIM believes they have superior investment potential. Depending on investment opportunities, the Account may invest up to 20% of its assets in foreign securities. The securities will be those traded on foreign exchanges or in other foreign markets and may be denominated in foreign currencies or other units.

TCIM typically uses a combination of active management, enhanced indexing and pure indexing to manage the Account. These investment strategies are used with respect to different segments of the Account to seek to achieve the Account’s general investment objective. For that portion of the Account that is actively managed, TCIM looks for stocks that it believes are attractively priced based on an analysis of the company’s prospects for growth in earnings, cash flow, revenues or other relevant measures. TCIM also looks for companies whose assets appear undervalued in the market. In general, TCIM focuses on

32 Prospectus ■ College Retirement Equities Fund

companies with shareholder-oriented management dedicated to creating shareholder value.

A portion of the Account is managed using an enhanced index strategy. With enhanced indexing, TCIM may use several different investment techniques to build a portfolio of stocks that is structured to resemble and share the risk characteristics of various segments of the benchmark index, while also seeking to outperform that benchmark index. Enhanced index strategies often employ proprietary, quantitative modeling techniques for stock selection, country allocation and portfolio construction. Quantitative analysis involves the use of mathematical models and computer programs that attempt to outperform the index by over- and underweighting certain stocks while keeping the Account’s overall financial and risk characteristics similar to those of its benchmark index. Relative to TCIM’s other approaches for managing other equity accounts, in general, the enhanced indexing methodology is designed so that the Account diverges from and may outperform its benchmark more than an indexing approach, but remains closer to the benchmark than other equity accounts using a traditional active management style. Enhanced index strategies will typically hold more stocks than traditional active strategies.

A portion of the Account is managed using a pure index strategy. This portion of the Account is designed to track various segments of the Account’s benchmark index. This portion of the Account buys most, but not necessarily all, of the securities in its benchmark index, and will attempt to closely match the overall investment characteristics of its benchmark index.

The benchmark for the Growth Account is the Russell 1000® Growth Index. See “More about benchmarks and other indices” below for additional information about benchmarks.

Principal Investment Risks: The Account is subject to the following principal investment risks:

· market risk;

· issuer risk (often called financial risk);

· foreign investment risk;

· small-cap risk;

· mid-cap risk;

· large-cap risk;

· active management risk;

· index risk;

· quantitative analysis risk;

· style risk/the risks of growth investing; and

· enhanced index risk.

Also, stocks of companies involved in reorganizations and other special situations can often involve more risk than ordinary securities. The Account will

College Retirement Equities Fund ■ Prospectus 33

probably be more volatile than the overall equity market due to its focus on more growth-oriented sectors of the market.

As with any investment, you can lose money by investing in this Account.

Who May Want to Invest: The Growth Account may be best for individuals who are looking for long-term capital appreciation and a favorable long-term return but are willing to tolerate fluctuations in value. It may also be well suited to investors seeking exposure to growth-oriented companies who also have exposure to other segments of the stock market, including selective exposure to value-oriented companies.

See “Principal risks of investing in the Accounts” below and “Additional information about investment strategies and risks” below for more information.

Investment Objective: A favorable long-term rate of return from a diversified portfolio selected to track the overall market for common stocks publicly traded in the United States, as represented by a broad stock market index.

Principal Investment Strategies: The Equity Index Account is designed to track the U.S. stock market as a whole and invests in stocks in its benchmark index, the Russell 3000® Index. The Account buys most, but not necessarily all, of the securities in the Russell 3000® Index, and attempts to closely match the overall investment characteristics of the Index. Using the Russell 3000® Index is not fundamental to the Account’s investment objective and policies. The Account can change the index at any time and will notify its participants if it does so. See “More about benchmarks and other indices” below for additional information about benchmarks.

The Account may also invest in securities and other instruments, such as futures, whose return depends on stock market prices. TCIM selects these instruments to attempt to match the total return of the Russell 3000® Index but may not always do so.

Principal Investment Risks: The Account is subject to the following principal investment risks:

· market risk;

· index risk;

· issuer risk (often called financial risk);

· large-cap risk;

· mid-cap risk; and

· small-cap risk.

Who May Want to Invest: The Equity Index Account may be best for individuals who have a longer time horizon, think U.S. stocks will perform well over time and want to invest in a broad range of securities in the U.S. market.

34 Prospectus ■ College Retirement Equities Fund

As with any investment, you can lose money by investing in this Account. See “Principal risks of investing in the Accounts” below and “Additional information about investment strategies and risks” below for more information.

Non-principal investments of the Equity and Equity Index Accounts

The Equity Accounts and Equity Index Account may make certain other investments, but not as principal strategies. In addition to stocks, the Equity and Equity Index Accounts may hold other types of securities and other investments with equity characteristics, such as convertible bonds, preferred stock, warrants and depository receipts. The Equity and Equity Index Accounts may also invest in short-term debt securities of the same type as those held by the Money Market Account and other kinds of short-term instruments for cash management and other purposes. Investing in these instruments is intended to help the Accounts maintain liquidity, use cash balances effectively and take advantage of attractive investment opportunities. The Equity Accounts also may invest up to 20% of their assets in fixed-income securities. TCIM may also manage cash in the Accounts by investing in money market funds or other short-term instruments.

The Equity and Equity Index Accounts may also buy and sell: (1) put and call options, including covered call options, on securities of the types they each may invest in and on securities indices composed of such securities; (2) futures contracts on securities indices composed of securities of the types in which each may invest; and (3) put and call options on such futures contracts. They may also buy and sell stock index futures contracts. The Equity and Equity Index Accounts may use such options and futures contracts for hedging and cash management purposes (but not for speculation) and to seek to increase total return. Futures contracts permit an Account to gain exposure to groups of securities and thereby have the potential to earn returns that are similar to those that would be earned by direct investments in those securities or instruments.

The Equity and Equity Index Accounts may invest in investment company securities, such as exchange-traded funds (“ETFs”). The Equity and Equity Index Accounts may use ETFs for cash management purposes and other purposes, including to gain exposure to certain sectors or securities that are represented by ownership in ETFs. When an Equity Account or the Equity Index Account invests in ETFs or other investment companies, the Account bears a proportionate share of expenses charged by the investment company in which it invests.

In seeking to manage currency risk, these Accounts also may enter into forward currency contracts and currency swaps and may buy or sell put and call options and futures contracts on, and securities indexed to, foreign currencies. Although the Equity and Equity Index Accounts may use options, futures or currency contracts at times to hedge certain risks, it is not the intent of these Accounts to hedge all equity or currency risks of the Accounts at any particular time.

The Equity and Equity Index Accounts may invest in other derivatives and other similar financial instruments, such as equity swaps, so long as these derivatives

College Retirement Equities Fund ■ Prospectus 35

and financial instruments are consistent with the Account’s investment objective and restrictions, policies and current regulations. The Accounts may use swaps to hedge or manage the risks associated with the assets held in an Account or to facilitate implementation of portfolio strategies of purchasing and selling assets for an Account’s portfolio.