UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended | |||||

or

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from __________ -to- __________ | |||||

Commission File Number: 1-6314

| (Exact name of registrant as specified in its charter) | ||||||||

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

( | ||||||||

| (Registrant’s telephone number, including area code) | ||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| | | | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Non-accelerated filer o | |||||||

Smaller reporting company | Emerging growth company | |||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting Common Stock held by non-affiliates of the registrant was $573,656,973 as of June 30, 2021, the last business day of the registrant’s most recently completed second fiscal quarter.

The number of shares of Common Stock, $1.00 par value per share, outstanding at February 17, 2022 was 51,095,706 .

Documents Incorporated by Reference

The information required by Part III of this Annual Report on Form 10-K, to the extent not set forth herein, is incorporated herein by reference to the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders to be held in 2022, which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Annual Report on Form 10-K relates.

TUTOR PERINI CORPORATION

2021 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| PAGE | ||||||||

2

PART I.

Forward-Looking Statements

The statements contained in this Annual Report on Form 10-K that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), including without limitation, statements regarding our management’s expectations, hopes, beliefs, intentions or strategies regarding the future and statements regarding future guidance or estimates and non-historical performance. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effects on us. Our expectations, beliefs and projections are expressed in good faith, and we believe there is a reasonable basis for them. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by such forward-looking statements. These material risks and uncertainties are listed and discussed in Item 1A. Risk Factors, below. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

ITEM 1. BUSINESS

General

Tutor Perini Corporation (together with its consolidated subsidiaries, “Tutor Perini,” the “Company,” “we,” “us,” and “our,” unless the context indicates otherwise) is a leading construction company, based on revenue as ranked by Engineering News-Record (“ENR”), offering diversified general contracting, construction management and design-build services to private customers and public agencies throughout the world. The Company was formed as a result of the 2008 merger between Tutor-Saliba Corporation and Perini Corporation (“Perini”) and our legacy dates back to 1894, when Perini's predecessor businesses began providing construction services. Our corporate headquarters are in Los Angeles (Sylmar), California, and we have various other principal offices throughout the United States and its territories (see Item 2. Properties for a listing of our major facilities). Our common stock is listed on the New York Stock Exchange under the symbol “TPC.” We are incorporated in the Commonwealth of Massachusetts.

We have established a strong reputation within our markets for executing large, complex projects on time and within budget while adhering to strict quality control measures. We offer general contracting, pre-construction planning and comprehensive project management services, including the planning and scheduling of the manpower, equipment, materials and subcontractors required for a project. We also offer self-performed construction services including site work; concrete forming and placement; steel erection; electrical; mechanical; plumbing; heating, ventilation and air conditioning (HVAC); and fire protection. During 2021, we performed work on more than 1,600 construction projects.

In 2021, ENR ranked Tutor Perini as the seventh largest domestic contractor. We are recognized as one of the leading civil contractors in the United States, as evidenced by our performance on several of the country’s largest mass-transit and transportation projects, such as Newark Liberty International Airport Terminal One (“Newark Airport Terminal One”), the East Side Access project in New York City, the California High-Speed Rail System, the Alaskan Way Viaduct Replacement (the “SR 99”) project in Seattle, major portions of the Red Line and Purple Line segments of the Los Angeles Metro subway system, and the San Francisco Central Subway extension to Chinatown. We are also recognized as one of the major building contractors in the United States, as evidenced by our performance on several of the country’s largest building development projects, including Hudson Yards in New York City and CityCenter and the Cosmopolitan Resort and Casino, both in Las Vegas.

Our strengths and expertise in the construction of civil and building infrastructure projects have been augmented by our vertical integration capabilities, which we established more than 10 years ago through the acquisitions of various business entities specializing in electrical, mechanical, plumbing, HVAC and other services that enhanced our market capabilities and expanded our geographic presence. Our vertical integration is a competitive advantage that allows us to self-perform a greater amount of work than our competitors. It also increases our competitiveness in bidding and our efficiency in managing and executing large, complex projects, and provides us with significant cross-selling opportunities across a broad geographic footprint.

3

Business Segment Overview

Our business is conducted through three segments: Civil, Building and Specialty Contractors.

Civil Segment

Our Civil segment specializes in public works construction and the replacement and reconstruction of infrastructure across several major geographic regions of the United States. Our civil contracting services include construction and rehabilitation of highways, bridges, tunnels, mass-transit systems, military defense facilities, and water management and wastewater treatment facilities.

The Civil segment is comprised of the heavy civil construction operations of our predecessors, Tutor-Saliba Corporation, its subsidiary Black Construction, and Perini, as well as our acquired companies, Frontier-Kemper, Lunda Construction and Becho. Our heavy civil units operate primarily on the West and East Coasts of the United States and are engaged in a variety of large mass-transit, tunneling, bridge and highway projects. Black Construction is the largest contractor in Guam and provides a variety of heavy civil, building, mechanical and electrical construction services throughout the Western Pacific region and in other strategic military locations. Frontier-Kemper is a heavy civil contractor engaged in the construction of tunnels for highways, railroads, subways and rapid transit systems; the construction of shafts and other facilities for water supply, wastewater transport and hydroelectric projects; and the development and equipping of mines with innovative hoisting, elevator and vertical conveyance systems. Lunda Construction is a heavy civil contractor specializing in the construction, rehabilitation and maintenance of bridges, railroads and other civil structures throughout the United States. Becho is engaged in drilling, foundation and excavation support for shoring, bridges, piers, roads and highway projects, primarily in the southwestern United States.

In its 2021 rankings, ENR ranked us as the nation’s largest contractor in the transportation market and third largest domestic heavy contractor.

Our Civil segment’s customers primarily award contracts through one of two methods: the traditional public “competitive bid” method, in which price is the major determining factor, or through a best value proposal, where contracts are awarded based on a combination of technical qualifications, proposed project team, schedule, past performance on similar projects and price.

Traditionally, our Civil segment’s customers require each contractor to pre-qualify for construction business by meeting criteria that include technical capabilities and financial strength. Our financial strength, outstanding record of performance on challenging civil works projects, and vertical integration capabilities often enable us to pre-qualify for projects in situations where smaller, less diversified contractors are unable to meet the qualification requirements. We believe this is a competitive advantage that allows us to self-perform a greater amount of work and makes us an ideal lead contractor for the largest, most complex infrastructure projects and on prestigious design-build, design-build-operate-maintain and public-private partnership projects.

We have been active in civil construction since 1894 and believe we have a particular expertise in large, complex civil construction projects. We have completed, or are currently working on, some of the most significant civil construction projects in the United States. For example, we are currently working on Newark Airport Terminal One, the East Side Access project in New York City, the first phase of the California High-Speed Rail project, the Purple Line Segments 2 and 3 expansion projects in Los Angeles, the San Francisco Central Subway extension to Chinatown and the Minneapolis Southwest Light Rail Transit project. We have also completed major projects such as the SR 99 project in Seattle; the platform over the eastern rail yard at Hudson Yards in New York City; the rehabilitation of the Verrazano-Narrows Bridge in New York; and multiple runway reconstruction projects at the John F. Kennedy International Airport in New York, Los Angeles International Airport and Fort Lauderdale-Hollywood International Airport, among others.

We believe the Civil segment provides us with significant opportunities for growth due to the condition of existing infrastructure coupled with large government funding sources dedicated to the replacement and reconstruction of aging U.S. infrastructure. In addition, infrastructure programs generally garner popular, bipartisan support from the public and elected officials due to their favorable long-term economic impacts, including significant job creation. Funding for major Civil segment infrastructure projects is typically provided through a combination of one or more of the following: local, regional, state and federal loans and grants; other direct allocations sourced through tax revenue; bonds; user fees; and, for certain projects, private capital.

On November 15, 2021, the bipartisan Infrastructure Investment and Jobs Act of 2021 (the “IIJA”) was enacted into law. The IIJA provides for $1.2 trillion of federal infrastructure funding, including $550 billion in new spending for improvements to the country’s surface-transportation network and enhancements to core infrastructure. The IIJA marks the largest federal

4

investment in public transit ever, the single largest dedicated bridge investment since the construction of the interstate highway system and the largest federal investment in passenger rail since the creation of Amtrak, all in addition to providing for regular annual spending for numerous infrastructure projects. This significant incremental funding is anticipated to be spent over the next 10 years, and much of it will be invested in end markets that are directly aligned with our market focus. Accordingly, we believe that this significant level of sustained, incremental funding will favorably impact our current work and prospective opportunities over the next decade.

Building Segment

Our Building segment has significant experience providing services to a number of specialized building markets for private and public works customers, including hospitality and gaming, transportation, health care, commercial offices, government facilities, sports and entertainment, education, correctional facilities, biotech, pharmaceutical, industrial and technology. We believe the success of the Building segment results from our proven ability to manage and perform large, complex projects with aggressive fast-track schedules, elaborate designs, and advanced mechanical, electrical and life safety systems, while providing accurate budgeting and strict quality control. Although price is a key competitive factor, we believe our strong reputation, long-standing customer relationships and significant level of repeat and referral business have enabled us to achieve a leading position in the marketplace.

In its 2021 rankings, ENR ranked us as the 17th largest domestic building contractor. We are a recognized leader in the hospitality and gaming market, specializing in the construction of high-end resorts and casinos. We work with hotel operators, Native American tribal councils, developers and architectural firms to provide diversified construction services to meet the challenges of new construction and renovation of hotel and resort properties. We believe that our reputation for completing projects on time is a significant competitive advantage in this market, as any delay in project completion could result in significant loss of revenue for the customer.

The Building segment is comprised of several operating units that provide general contracting, design-build, preconstruction and construction services in various regions of the United States. Rudolph and Sletten focuses on large, complex projects in California in the health care, commercial office, technology, industrial, education, and government facilities markets. Tutor Perini Building Corp. focuses on large, complex building projects nationwide, including significant projects in the hospitality and gaming, commercial office, education, government facilities, and multi-unit residential markets. Roy Anderson Corp. provides general contracting services, including major disaster response and reconstruction support, to public and private customers primarily throughout the southeastern United States. Perini Management Services provides diversified construction and design-build services internationally to U.S. government agencies, as well as to surety companies and multi-national corporations.

We have completed, or are currently working on, various large private and public building projects across a wide array of end markets. Specific projects include Newark Airport Terminal One; three large corporate office buildings in northern California for distinct confidential technology customers; a commercial office tower and a multi-unit residential tower, both at Hudson Yards in New York City; the El Camino Hospital Integrated Medical Office Building in El Camino, California; Kaiser Hospital buildings in San Leandro, Redwood City and Roseville, California; the Choctaw Casino and Resort in Durant, Oklahoma; the Pechanga Resort and Casino expansion in Temecula, California; the O Street Government Office Building in Sacramento, California; and courthouses in San Bernardino and San Diego, California and Broward County, Florida. As a result of our reputation and track record, we were previously awarded and completed contracts for several marquee hospitality and gaming projects in Las Vegas, including CityCenter, the Cosmopolitan Resort and Casino and the Wynn Encore Hotel. These projects span a wide array of building end markets and illustrate our Building segment’s résumé of successfully completed large-scale public and private projects.

Specialty Contractors Segment

Our Specialty Contractors segment specializes in electrical, mechanical, plumbing, HVAC and fire protection systems for a full range of civil and building construction projects in the industrial, commercial, hospitality and gaming, and mass-transit end markets. This segment provides unique strengths and vertically integrated service capabilities that position us as a full-service contractor with greater control over project bids and costs, scheduled work, project delivery and risk management. The majority of work performed by the Specialty Contractors segment is contracted directly with state and local municipal agencies, real estate developers, school districts and other commercial and industrial customers. A significant portion of the segment's work has been, and is expected to continue to be, performed for our Civil and Building segments.

The Specialty Contractors segment is comprised of several operating units that provide unique services in various regions of the United States. Five Star Electric Corp. (“Five Star”) is an industry leader and one of the largest electrical contractors in New York City. Five Star provides construction services, including power, lighting, fire alarm, security, telecommunications, low

5

voltage and wireless systems to both the public and private sectors. These services are provided across end markets that include multi-unit residential, hotels, commercial offices, industrial, mass transit, education, retail, sports and entertainment, health care and water treatment. Fisk Electric (“Fisk”) covers many of the major commercial, transportation and industrial electrical construction markets in California and the southern United States, with the ability to cover other attractive markets nationwide. Fisk’s expertise is in the design and development of electrical and technology systems for major projects spanning a broad variety of project types, including commercial office buildings, sports arenas, hospitals, research laboratories, hotels and casinos, convention centers, manufacturing plants, refineries, and water and wastewater treatment facilities. WDF, Nagelbush and Desert Mechanical each provide mechanical, plumbing, HVAC and fire protection services to a range of customers in a wide variety of markets, including transportation, commercial/industrial, schools and universities and residential. WDF is one of the largest mechanical contractors serving the New York City metropolitan region. Nagelbush operates primarily in Florida and Desert Mechanical operates primarily in the western United States.

Our Specialty Contractors business units have completed, or are currently working on, various portions of the East Side Access project in New York City, various projects at the World Trade Center and at Hudson Yards in New York City, and upgrades and rehabilitations at various New York City public housing facilities. The Specialty Contractors segment has also supported, or is currently supporting, several large projects in our Civil and Building segments, including the SR 99 project in Seattle; the San Francisco Central Subway extension to Chinatown; the Purple Line Segments 2 and 3 expansion projects in Los Angeles; Newark Airport Terminal One; the California High Speed Rail project in central California; McCarran International Airport Terminal 3 in Las Vegas; and several marquee hospitality and gaming projects in Las Vegas, including CityCenter, the Cosmopolitan Resort and Casino, and the Wynn Encore Hotel.

For information regarding the breakdown of our revenue by segment, end market, customer type and contract type, see Note 3 of the Notes to Consolidated Financial Statements. In addition, financial information about geographic areas is discussed in Note 14 of the Notes to Consolidated Financial Statements.

Backlog

Backlog in our industry is a measure of the total value of work that is remaining to be performed on projects that have been awarded. We include a construction project in our backlog when a contract is awarded or when we have otherwise received written definitive notice that the project has been awarded to us and there are no remaining major uncertainties that the project will proceed (e.g., adequate funding is in place). As a result, we believe our backlog is firm, and although cancellations or scope adjustments may occur, historically they have not been material. We estimate that approximately $4 billion, or 46%, of our backlog as of December 31, 2021 will be recognized as revenue in 2022. Our backlog by segment, end market, customer type and contract type is presented in the following tables:

| As of December 31, | |||||||||||||||||||||||

| (in thousands) | 2021 | 2020 | |||||||||||||||||||||

| Backlog by business segment: | |||||||||||||||||||||||

| Civil | $ | 4,553,539 | 55 | % | $ | 4,783,564 | 57 | % | |||||||||||||||

| Building | 2,308,930 | 28 | % | 1,702,305 | 20 | % | |||||||||||||||||

| Specialty Contractors | 1,373,167 | 17 | % | 1,859,848 | 23 | % | |||||||||||||||||

| Total backlog | $ | 8,235,636 | 100 | % | $ | 8,345,717 | 100 | % | |||||||||||||||

| As of December 31, | |||||||||||||||||||||||

| (in thousands) | 2021 | 2020 | |||||||||||||||||||||

| Civil segment backlog by end market: | |||||||||||||||||||||||

| Mass transit (includes certain transportation and tunneling projects) | $ | 3,256,556 | 71 | % | $ | 3,885,275 | 81 | % | |||||||||||||||

| Military defense facilities | 627,407 | 14 | % | 318,389 | 7 | % | |||||||||||||||||

| Bridges | 448,416 | 10 | % | 244,385 | 5 | % | |||||||||||||||||

| Water | 119,707 | 3 | % | 130,274 | 3 | % | |||||||||||||||||

| Other | 101,453 | 2 | % | 205,241 | 4 | % | |||||||||||||||||

| Total Civil segment backlog | $ | 4,553,539 | 100 | % | $ | 4,783,564 | 100 | % | |||||||||||||||

6

| As of December 31, | |||||||||||||||||||||||

| (in thousands) | 2021 | 2020 | |||||||||||||||||||||

| Building segment backlog by end market: | |||||||||||||||||||||||

| Municipal and government | $ | 824,173 | 36 | % | $ | 556,726 | 33 | % | |||||||||||||||

| Health care facilities | 575,006 | 25 | % | 49,655 | 3 | % | |||||||||||||||||

| Mass transit (includes transportation projects) | 476,454 | 21 | % | 144,019 | 8 | % | |||||||||||||||||

| Commercial and industrial facilities | 164,878 | 7 | % | 350,012 | 21 | % | |||||||||||||||||

| Education facilities | 140,822 | 6 | % | 165,766 | 10 | % | |||||||||||||||||

| Hospitality and gaming | 94,732 | 4 | % | 333,315 | 20 | % | |||||||||||||||||

| Other | 32,865 | 1 | % | 102,812 | 5 | % | |||||||||||||||||

| Total Building segment backlog | $ | 2,308,930 | 100 | % | $ | 1,702,305 | 100 | % | |||||||||||||||

| As of December 31, | |||||||||||||||||||||||

| (in thousands) | 2021 | 2020 | |||||||||||||||||||||

| Specialty Contractors segment backlog by end market: | |||||||||||||||||||||||

| Mass transit (includes certain transportation and tunneling projects) | $ | 730,480 | 53 | % | $ | 1,058,479 | 57 | % | |||||||||||||||

| Water | 164,653 | 12 | % | 214,717 | 12 | % | |||||||||||||||||

| Municipal and government | 158,614 | 12 | % | 92,749 | 5 | % | |||||||||||||||||

| Multi-unit residential | 137,824 | 10 | % | 219,139 | 12 | % | |||||||||||||||||

| Commercial and industrial facilities | 96,686 | 7 | % | 122,687 | 7 | % | |||||||||||||||||

| Other | 84,910 | 6 | % | 152,077 | 7 | % | |||||||||||||||||

| Total Specialty Contractors segment backlog | $ | 1,373,167 | 100 | % | $ | 1,859,848 | 100 | % | |||||||||||||||

| As of December 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Backlog by customer type: | |||||||||||

| State and local agencies | 71 | % | 72 | % | |||||||

| Private owners | 16 | % | 20 | % | |||||||

| Federal agencies | 13 | % | 8 | % | |||||||

| Total backlog | 100 | % | 100 | % | |||||||

| As of December 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Backlog by contract type: | |||||||||||

| Fixed price | 77 | % | 76 | % | |||||||

| Guaranteed maximum price | 12 | % | 11 | % | |||||||

| Unit price | 4 | % | 4 | % | |||||||

| Cost plus fee and other | 7 | % | 9 | % | |||||||

| Total backlog | 100 | % | 100 | % | |||||||

Fixed price contracts, particularly with federal, state and local government customers, are expected to continue to represent a sizeable percentage of total backlog.

Competition

While the construction markets include numerous competitors, especially for small to mid-sized projects, much of the work that we target is for larger, more complex projects where there are typically fewer active market participants due to the greater capabilities and resources required to perform the work. In addition to domestic competitors, we have seen certain foreign competitors attempting to grow their presence in the United States over the past several years, particularly through the pursuit of large Civil segment projects. Evolving changes in the construction industry, such as the trend toward an increased use of the progressive design-build project delivery method that may reduce project risks for both owners and contractors, could result in increased competition and potentially lower margins on certain projects in the future. We believe price, experience, reputation, responsiveness, customer relationships, project completion track record, schedule control, risk management and quality of work are key factors customers consider when awarding contracts.

7

In our Civil segment, we compete principally with large civil construction firms, including (alphabetically) Dragados USA; Fluor Corporation; Granite Construction; Kiewit Corporation; OHL USA; Skanska USA; Traylor Bros., Inc.; and The Walsh Group. In our Building segment, we compete with a variety of national and regional contractors, including (alphabetically) AECOM (through its acquisitions of Tishman Construction and Hunt Construction Group); Balfour Beatty Construction; Clark Construction Group; DPR Construction; Gilbane, Inc.; Hensel Phelps Construction Co.; Lendlease Corporation; McCarthy Building Companies, Inc.; Skanska USA; Suffolk Construction; and Turner Construction Company. In our Specialty Contractors segment, we compete principally with various regional and local electrical, mechanical and plumbing subcontractors.

Construction Costs

We strive to eliminate or minimize exposure to labor and material price increases in our project bids and the manner in which we execute our work. Generally, if prices for materials, labor or equipment increase excessively, provisions in certain types of contracts often shift all or a major portion of any adverse impact to the customer. In our fixed price contracts, we attempt to insulate ourselves from the unfavorable effects of inflation, when possible, by incorporating escalating wage and price assumptions into our construction cost estimates, by obtaining firm fixed price quotes from major subcontractors and material suppliers, by securing purchase commitments for materials early in the project schedule and by including contingency for these risks in our bid price. Construction and other materials used in our construction activities are generally available locally from multiple sources. Despite the widespread adverse supply chain impacts related to the effects of the COVID-19 pandemic, we have not yet experienced significant supply chain issues, but we cannot be certain that such issues may not arise in the future. Labor resources for our domestic projects are largely obtained through various labor unions. We have not experienced significant labor shortages in recent years, nor do we expect to in the near future. However, longer-term, the anticipated significant increase in demand for large complex projects driven by the IIJA could lead to labor shortages.

Seasonality

We experience seasonal trends in our business. Our revenue and operating income are typically higher in the second half of the year. Our first fiscal quarter of the year is typically our lowest revenue quarter, as the harsher winter weather conditions that often occur during this period can negatively impact our ability to execute work and our productivity in parts of North America. Our revenue typically increases during the high construction seasons of the summer and fall months in the United States. Within the United States, as well as in other parts of the world, our business generally benefits from milder weather conditions during our third fiscal quarter, which allows for more productivity from our on-site construction operations. For these reasons, it is not unusual for us to experience seasonal changes or fluctuations in our quarterly operating results.

Government Contracts

Most of our federal, state and local government customers can terminate, renegotiate, or modify any of their contracts with us at their election, and many of our federal government contracts are subject to renewal or extension periodically. Revenue derived from federal, state and local government customers was 66%, 63% and 62% of our total revenue for each of the years ended December 31, 2021, 2020 and 2019, respectively.

Environmental, Health and Safety Regulations

Environmental, health and safety regulations and requirements materially affect our business. We are firmly committed to providing a safe and healthy work environment for our employees and to working in a manner that ensures the safety of our subcontractors, customers and the general public, as well as the protection of facilities, equipment and the environment. Compliance with Occupational Safety and Health Administration (“OSHA”) and other health and safety regulations, in particular, is essential to procure business and to attract and retain our workforce. Accordingly, we make considerable investments in our environmental, health and safety programs, and we factor costs associated with compliance into our project bids and proposals.

We provide construction and construction management services at various project sites, and sometimes perform work in and around sensitive environmental areas, such as rivers, lakes and wetlands. We also handle small quantities of hazardous materials on occasion. Significant fines, penalties and other sanctions may be imposed for non-compliance with environmental and health and safety laws and regulations, and some laws provide for joint and several strict liabilities for remediation of releases of hazardous substances.

Contaminants have been detected at some of the sites that we own and where we have worked as a contractor in the past, and we have incurred costs for the investigation and remediation of hazardous substances. However, we do not own the job sites upon which we perform our work. We have pollution liability insurance coverage for such matters, and if applicable, we seek

8

indemnification from customers to cover the risks associated with environmental remediation. Accordingly, we believe that our environmental liabilities are not material. In addition, we continually evaluate our compliance with all applicable environmental laws and regulations, and believe that we are in substantial compliance with those laws and regulations.

Insurance and Bonding

All of our properties and equipment, as well as those of our joint ventures, are covered by insurance in amounts that we believe are consistent with our risk of loss and industry practice. Our wholly owned subsidiary, PCR Insurance Company, issues policies for default insurance for our subcontractors, automobile liability, general liability and workers’ compensation insurance, allowing us to centralize our claims and risk management functions to reduce our insurance-related costs.

As a normal part of the construction business, we are often required to provide various types of surety bonds as an additional level of security for our performance. We also require many of our higher-risk subcontractors to provide surety bonds as security for payment of subcontractors and suppliers and to guarantee their performance. As an alternative to traditional surety bonds, we also have purchased subcontractor default insurance for certain construction projects to insure against the risk of subcontractor default.

Human Capital Resources

The foundation of our continuing success as a leading construction services business is our ability to attract and retain the industry’s best talent by providing a culture of opportunity, development, accountability and empowerment. This understanding guides our approach to managing our human capital resources.

Employees. Our principal asset is our employees, many of whom have technical and professional backgrounds and undergraduate and/or advanced degrees. As of December 31, 2021, we had approximately 7,800 employees (including union employees), of which approximately 1,900 were salaried and 5,900 were hourly employees. The number of employees at any given time depends on the volume and types of active projects in progress, as well as our position within the lifecycle of those projects. We believe that we have strong relationships with our employees and that the quality and level of service that our employees deliver to our customers are among the highest in our industry.

Union Workforce. We are signatory to numerous local and regional collective bargaining agreements, both directly and through trade associations, as a union contractor. These agreements cover all necessary union crafts and are subject to various renewal dates. As of December 31, 2021, our workforce included a total of approximately 3,900 union employees. Estimated amounts for wage escalation related to the expiration of union contracts are included in our bids on various projects; accordingly, the expiration of any union contract in the next year is not expected to have any material impact on us. During the past several years, we have not experienced any significant work stoppages caused by our union employees.

Talent Recruitment, Training and Retention. Our business relies upon an adequate supply of management, supervisory and field personnel. Recruiting, training and retaining key personnel has been and will remain primary goals of our human capital initiative. Through the use of management information systems, on-the-job training and educational seminars, employees are trained to understand the importance of project execution. We place a strong emphasis on training employees in accurate and comprehensive project estimating, project management and project cost control. As is common in our industry, we experience some recurring employee turnover each year, which we believe is comparable to the industry average. Historically, we have successfully attracted and retained sufficient numbers of personnel, including union personnel, to support our operational needs. We strive to ensure a fully competent project management team that includes long-term successors to our current project leaders by investing significant resources to build strong and highly competent project managers. We regularly hire construction management and engineering staff, including interns and recent graduates, and provide them with engaging projects and development programs. On the occasion when we have a need for senior project executives, the broad professional network of our leadership team often provides strong candidates to fill those needs. We also utilize internal and external recruiting specialists to help fill our open job positions. To support retention and motivation of our top talent, we provide very competitive compensation, which may include performance incentives.

Workplace Safety. We place a strong emphasis on the safety of our employees, our customers and the public. Accordingly, we conduct extensive safety training programs that have allowed us to maintain a high safety level at our worksites. All newly hired employees that will be working at project job sites undergo an initial safety orientation, and for certain types of projects or processes we conduct specific hazard training programs. Our project supervisors regularly conduct on-site safety meetings and our safety managers make random site safety inspections and perform daily assessments. In addition, operational employees are required to complete an OSHA 30-hour training program and project-specific courses on various safety topics. Moreover, we promote a culture of safety by encouraging employees to recognize, immediately correct and report all unsafe conditions. To underscore the importance of safety, a portion of annual performance bonus compensation for certain executive management is

9

directly linked to the achievement of a key safety metric. Our strong overall safety performance also helps to reduce our insurance-related costs.

Available Information

Our investor website address is http://investors.tutorperini.com. In the “Financial Reports” portion of our investor website, under the subsection “SEC Filings,” you may obtain free electronic copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to these reports. These reports, and any amendments to them, are made available on our website as soon as reasonably practicable after we electronically file them with the Securities and Exchange Commission (“SEC”).

ITEM 1A. RISK FACTORS

We are subject to a number of known and unknown risks and uncertainties that could have a material adverse effect on our operations. Set forth below, and elsewhere in this report, are descriptions of the material risks and uncertainties that could cause our actual results to differ materially from the results contemplated by the forward-looking statements contained in this report and could have a material adverse effect on our financial condition, results of operations and cash flows.

Risks Related to Our Business and Operations

If we are unable to accurately estimate contract risks, revenue or costs, economic factors such as inflation, the timing of new awards, or the pace of project execution, we may incur a loss or achieve lower than anticipated profit.

Accounting for contract-related revenue and costs requires management to make significant estimates and assumptions that may change substantially throughout the project lifecycle, which has previously resulted, and in the future could result, in a material impact to our consolidated financial statements. In addition, cost overruns, including unanticipated cost increases on fixed price contracts (including contracts performed under the design-build project delivery method, in which we assume the risks associated with the design of the project) and guaranteed maximum price contracts, have previously resulted, and in the future may result, in lower profits or losses. Economic factors, including inflation, could also subject us to higher costs, which we may not be able to fully recover in future projects that we are bidding, and may also decrease profit on our existing contracts, in particular with respect to our fixed price, unit price and guaranteed maximum price contracts. Changes in laws, policies or regulations, including tariffs and taxes, have previously impacted, and in the future could impact, the prices for materials or equipment. Further, our results of operations have historically fluctuated, and may continue to fluctuate, quarterly and annually depending on when new awards occur and the commencement and progress of work on projects already awarded.

We are involved in a significant number of legal proceedings which, if determined unfavorable to us, could adversely affect our financial results and/or cash flows, harm our reputation and/or preclude us from bidding on future projects. We also may invest significant working capital on projects while legal proceedings are being settled.

We are involved in various lawsuits, including the legal proceedings described under Note 8 of the Notes to Consolidated Financial Statements. Litigation is inherently uncertain, and it is not possible to accurately predict what the final outcome will be of any legal proceeding. We must make certain assumptions and rely on estimates, which are inherently subject to risks and uncertainties, regarding potential outcomes of legal proceedings in order to determine an appropriate contingent liability and charge to income. Any adverse legal proceeding outcome or settlement that is materially different from our expectations and estimates could have a material adverse effect on our financial condition, results of operations and cash flows. This may include requiring us to record an expense or reduce revenue that we previously recorded based on our expectations or estimates, requiring us to pay damages or reducing cash collections that we had expected to receive. For example, on December 13, 2019, we received an adverse jury verdict in the case related to the construction of the SR 99 project by a joint venture for which the Company holds a 45% share as a minority partner. As a result of the unexpected adverse jury verdict, we recorded a pre-tax charge of $166.8 million in 2019. Refer to the Alaskan Way Viaduct Matter in Note 8 of the Notes to Consolidated Financial Statements for further discussion. In addition, any adverse judgments could harm our reputation and preclude us from bidding on future projects.

We may bring claims against project owners for additional cost exceeding the contract price or for amounts not included in the original contract price. When these types of events occur and unresolved claims are pending, we may invest significant working capital in projects to cover cost overruns pending the resolution of the relevant claims. A failure to promptly recover on these types of claims has had and could continue to have a material adverse effect on our liquidity and financial results and could result in further legal proceedings.

10

Our contracts often require us to perform extra work beyond the initial project scope, which can result in disputes or claims and adversely affect our working capital, profits and cash flows.

Our contracts often require us to perform extra work beyond the initial project scope as directed by the customer even if the customer has not agreed in advance on the scope and/or price of the work to be performed. This process has resulted and in the future could result in disputes or claims over whether the work performed is beyond the scope of work directed by the customer and/or exceeds the price the customer is willing to pay for the work performed. To the extent we do not recover our costs for this work or there are delays in the recovery of these costs, our working capital, profits and cash flows could continue to be adversely impacted.

Competition for new project awards is intense, and our failure to compete effectively could reduce our market share and profits.

New project awards are determined through either a competitive bid basis or on a negotiated basis. Projects may be awarded based solely upon price, but often take into account other factors, such as technical qualifications, proposed project team, schedule and past performance on similar projects. Within our industry, we compete with many international, regional and local construction firms. If we are unable to compete successfully in such markets, our relative market share and profits could be reduced.

The coronavirus (“COVID-19”) pandemic has adversely impacted, and could continue to adversely impact, our business, financial condition and results of operations.

The COVID-19 pandemic has created volatility, uncertainty and economic disruption for the Company, our customers, subcontractors and suppliers, and the markets in which we do business. The scope and impact of the COVID-19 pandemic continues to evolve, and new strains of the COVID-19 virus have emerged. As a result of the COVID-19 pandemic, we have experienced delays in certain bidding activities and also in legal proceedings and settlement discussions where we have claims against project owners for additional costs exceeding the contract price or for amounts not included in the original contract price. Consequently, our ability to resolve and recover on these types of claims has been and may continue to be delayed, which may adversely affect our liquidity and financial results.

It remains difficult to assess the full impact that the COVID-19 pandemic may have on our business, including the impact of actions that may continue to be taken in response to the pandemic and the impacts that the pandemic will have on our employees, our operating segments and practices, our customers, subcontractors and suppliers, and the regions that we serve, or on our financial condition and results of operations as a whole. The full impact depends on many factors that remain uncertain and subject to ongoing volatility, or that are not yet identifiable, and in many cases are out of our control. These factors could include, among other things: (1) the duration of the COVID-19 pandemic and the types and magnitude of adverse impacts on the U.S. and global economies; (2) the health and welfare, and general availability, of our employees, and those of our customers, subcontractors and suppliers; (3) evolving business and government actions in response to the pandemic, including, but not limited to, social distancing measures, new or increased COVID-19 testing and/or vaccination requirements, and additional health and safety requirements that we may be required to observe in order to continue working on our projects; (4) the varying impact that the pandemic may have on industries we serve and on government spending for infrastructure projects, including reduced government spending on infrastructure as a result of lower revenues from taxes, tolls and fares; (5) the response of our customers or prospective customers to the pandemic, including potential future delays, stoppages or terminations of existing projects or potential new awards; (6) delays in the settlement of receivables if customers are unable to pay, fail to make timely payments, request financial concessions or if we continue to experience delays in resolving claims and disputes (e.g., further delays in court proceedings or settlement discussions); (7) limitations and higher costs associated with obtaining financing; (8) the impact of higher inflation that has resulted, at least in part, from market and government responses to the COVID-19 pandemic, and how long elevated inflation levels may persist, which may increase the cost of labor and materials; (9) supply chain and related logistical challenges that could further limit the availability or increase the cost of materials; (10) potential interruptions to our information systems and technology or breaches in our data security due to increasing use of remote communications and access; and (11) the extent to which COVID-19 vaccines and vaccine boosters are effective against the various current and future virus strains. Such factors may continue to result in fewer or delayed project bidding opportunities or additional or further delays on existing projects.

Any of these events or impacts we have experienced or identified have caused or contributed to, and could continue to cause or contribute to, the risks and uncertainties facing the Company and our customers and could continue to materially and adversely affect our business or portions thereof, and our financial condition and results of operations. The COVID-19 pandemic and the volatile economic conditions stemming from the pandemic, as well as reactions to future pandemics or resurgences of COVID-19, could also aggravate or heighten the risks posed by other risk factors that we have identified in this Annual Report on Form 10-K, which in turn could materially and adversely affect our business, financial condition and results of operations.

11

There may be other adverse consequences to our business, financial condition and results of operations from the spread of COVID-19 that are not presently known or that have not yet become apparent. As a result, we cannot assure you that if the COVID-19 pandemic continues, it would not have a further adverse impact on our business, financial condition and results of operations.

A significant slowdown or decline in economic conditions could adversely affect our operations.

Any significant decline in economic conditions in any of the markets we serve or uncertainty regarding the economic outlook could result in a decline in demand for infrastructure projects and commercial building developments. In addition, any instability in the financial and credit markets could negatively impact our customers’ ability to pay us on a timely basis, or at all, for work on projects already under construction, could cause our customers to delay or cancel construction projects in our backlog or could create difficulties for customers to obtain adequate financing to fund new construction projects. Such consequences could have an adverse impact on our future operating results. Lastly, we are more susceptible to adverse economic conditions in New York and California, as a significant portion of our operations are concentrated in those states.

Our actual results could differ from the assumptions and estimates used to prepare our financial statements.

In preparing our financial statements, we are required under generally accepted accounting principles in the United States (“GAAP”) to make estimates and assumptions as of the date of the financial statements. These estimates and assumptions affect the reported values of assets, liabilities, revenue and expenses, and the disclosure of contingent assets and liabilities. Areas requiring significant estimates by our management include, but are not limited to:

• recognition of contract revenue, costs, profits or losses in applying the principles of revenue accounting;

• recognition of revenue related to project incentives or awards we expect to receive;

• recognition of recoveries under unapproved change orders or claims;

• estimated amounts for expected project losses, warranty costs, contract closeout or other costs;

• collectability of billed and unbilled accounts receivable;

• asset valuations;

• income tax provisions and related valuation allowances;

• determination of expense and potential liabilities under pension and other post-retirement benefit programs; and

• accruals for other estimated liabilities, including litigation and insurance reserves.

Our actual business and financial results could differ from our estimates of such results, which could have a material adverse impact on our financial condition and reported results of operations.

The construction services industry is highly schedule driven, and our failure to meet the schedule requirements of our contracts could adversely affect our reputation and/or expose us to financial liability.

Many of our contracts are subject to specific completion schedule requirements. Failure to meet contractual schedule requirements has subjected us, and in the future could subject us, to liquidated damages, liability for our customer’s actual cost arising out of our delay and damage to our reputation.

We may not fully realize the revenue value reported in our backlog due to cancellations or reductions in scope.

As of December 31, 2021, our backlog of uncompleted construction work was approximately $8.2 billion. The revenue projected in our backlog may not be fully realized and, in some cases, if realized, may not result in profits or may be less profitable than expected. The cancellation or reduction in scope of significant projects included in our backlog could have a material adverse effect on our financial condition, results of operations and cash flows.

We require substantial personnel, including construction and project managers and specialty subcontractor resources, to execute and perform on our contracts in backlog. The successful execution of our business strategies is also dependent upon our ability to attract and retain our key officers, as well as adequately plan for their succession.

Our ability to execute and perform on our contracts in backlog depends in large part upon our ability to hire and retain highly skilled personnel, including project and construction management and trade labor resources, such as carpenters, masons and other skilled workers. In the event we are unable to attract, hire and retain the requisite personnel and subcontractors necessary to execute and perform on our contracts in backlog, we may experience delays in completing projects in accordance with project schedules or an increase in expected costs, both of which could have a material adverse effect on our financial results, our reputation and our relationships. In addition, if we lack the personnel and specialty subcontractors necessary to perform on our current contract backlog, we may find it necessary to curtail our pursuit of new projects. A significant, rapid growth in our backlog has led, and could continue to lead, to situations in which labor resources become constrained.

12

The execution of our business strategies also substantially depends on our ability to retain several key members of our management. Losing any of these individuals could adversely affect our business. The majority of these key individuals are not bound by employment agreements. Volatility or lack of positive performance in our stock price may adversely affect our ability to retain key individuals to whom we have provided share-based compensation. If we lose any key officer due to voluntary or involuntary termination, including as a result of death or disability, and we do not have qualified successors in place, our operating results could be harmed.

The level of federal, state and local government spending for infrastructure and other public projects could adversely affect the number of projects available to us in the future.

The civil construction and public-works building markets are dependent on the amount of work funded by various government agencies, which depends on many factors, including the condition of the existing infrastructure and buildings; the need for new or expanded infrastructure and buildings; and federal, state and local government spending levels. As a result, our future operating results could be negatively impacted by any decrease in demand for public projects or decrease or delay in government funding (even with the passage of the IIJA), which could result from a variety of factors, including extended government shutdowns, delays in the sale of voter-approved bonds, budget shortfalls, credit rating downgrades or long-term impairment in the ability of state and local governments to raise capital in the municipal bond market.

Systems and information technology interruption and breaches in data security and/or privacy could adversely impact our ability to operate and negatively impact our operating results.

We rely on computer, information and communication technology and other related systems, some of which are hosted by third party providers, for various business processes and activities, including project management, accounting, financial reporting and business development. These systems have been and may, in the future, be subject to interruptions or damage by a variety of factors including, but not limited to, cyber-attacks, natural disasters, power loss, telecommunications failures, acts of war, computer viruses, email phishing, obsolescence and physical damage. Such interruptions can result in a loss of critical data, a delay in operations, damage to our reputation or an unintentional disclosure of customer confidential or personally identifiable information, any of which could have a material adverse impact on us and our consolidated financial statements.

Cybersecurity risks include potential attacks on both our information technology infrastructure and those of third parties (both on premises and in the cloud) attempting to gain unauthorized access to our confidential or other proprietary information, classified information, or information relating to our employees, customers and other third parties. We dedicate considerable attention and resources to the safeguarding of our information technology systems. Nevertheless, due to the evolving nature, persistence, sophistication and volume of cyber-attacks, we may not be successful in defending our systems against all such attacks. Consequently, we have engaged, and may again need to engage, significant resources to remediate the impact of, or further mitigate the risk of, such an attack. Any successful cyber-attack can result in the criminal, or otherwise illegitimate use of, confidential data, including our data or third-party data for which we have the responsibility for safekeeping. Additionally, such an attack could have a material adverse impact on our operations, reputation and financial results.

In addition, various privacy and security laws and regulations requiring us to protect sensitive and confidential information from disclosure continue to evolve and pose increasingly complex compliance challenges. Compliance with evolving data privacy laws and regulations may cause us to incur additional costs, and any violation could result in damage to our reputation and/or subject us to fines, payment of damages, lawsuits and restrictions on our use of data, which could have a material adverse impact on our financial results.

Our participation in construction joint ventures exposes us to liability and/or harm to our reputation for failures by our partners.

As part of our business, we enter into joint venture arrangements typically to jointly bid on and execute particular projects, thereby reducing our risk profile while enhancing execution capabilities and increasing surety bonding capacity. Success on these joint projects depends in large part on whether our joint venture partners satisfy their contractual obligations. Generally, we and our joint venture partners are jointly and severally liable for all liabilities and obligations of our joint ventures. If a joint venture partner fails to perform or is financially unable to bear its portion of required capital contributions or other obligations, including liabilities stemming from lawsuits, we could be required to make additional investments, provide additional services or pay more than our proportionate share of a liability to make up for our partner’s shortfall. Further, if we are unable to adequately address our partner’s performance issues, the customer may terminate the project, which could result in legal liability to us, harm our reputation, reduce our profit on a project or, in some cases, result in a loss.

13

Our international operations expose us to economic, political, regulatory and other risks, as well as uncertainty related to U.S. Government funding, which could adversely affect our revenue and earnings.

For the year ended December 31, 2021, we derived $374.1 million of revenue from our work on projects located outside of the United States. Our international operations expose us to risks inherent in doing business in certain hostile regions outside the United States, including political risks; risks of loss due to acts of war; unstable economic, financial and market conditions; potential incompatibility with foreign subcontractors and vendors; foreign currency controls and fluctuations; trade restrictions; logistical challenges; variations in taxes; and changes in labor conditions, labor strikes and difficulties in staffing and managing international operations. Failure to successfully manage risks associated with our international operations could result in higher operating costs than anticipated or could delay or limit our ability to generate revenue and income from construction operations in key international markets.

The U.S. federal government has approved various spending bills for the construction of defense- and diplomacy-related projects and has allocated significant funds to the defense of U.S. interests around the world from the threat of terrorism. The federal government has also approved funds for development in conjunction with the relocation of military personnel into Guam. However, federal government funding levels for construction projects in the Middle East have decreased significantly over the past several years as the U.S. government has reduced the number of military troops and support personnel in the region. As a result, we have seen a decrease in the number and size of federal government projects available to us in this region. Any decrease in U.S. federal government funding for projects in Guam or in other U.S. Territories or countries in which we are pursuing work may result in project delays or cancellations, which could reduce our revenue and earnings.

Weather can significantly affect our revenue and profitability.

Inclement weather conditions, such as significant storms and unusual temperatures, can impact our ability to perform work. Adverse weather conditions can cause delays and increases in project costs, resulting in variability in our revenue and profitability.

We are subject to risks related to government contracts and related procurement regulations.

Our contracts with U.S. federal, as well as state, local and foreign, government entities are subject to various procurement regulations and other requirements relating to their formation, administration and performance. We are subject to audits and investigations relating to our government contracts, and any violations could result in various civil and criminal penalties and administrative sanctions, including termination of contract, refunding or suspending of payments, forfeiture of profits, payment of fines and suspension or debarment from future government business. In addition, most of these contracts provide for termination or renegotiation by the government at any time, without cause, which could have an adverse effect on our business and operations.

Our business and operations could be negatively affected if we become subject to any securities litigation or shareholder activism, which could cause us to incur significant expense, hinder execution of our business and growth strategy, impact our stock price and adversely affect our reputation.

There have been several instances in the past of shareholder activism targeted at some of our peers, as well as at other companies in the broader engineering and construction industry, with activists often seeking board representation and/or advocating for changes to the target company’s operating structure or business strategy. Additionally, following periods of volatility in the market price of companies’ securities, securities class action litigation has often been brought against such companies.

Shareholder activism, which could take many forms and arise in a variety of situations, has been increasing recently, and new universal proxy rules set to take effect later in 2022 could significantly lower the cost and further increase the ease and likelihood of shareholder activism. Volatility in our stock price or other reasons may in the future cause us to become the target of securities litigation or shareholder activism. Securities litigation and shareholder activism, including potential proxy contests, could result in substantial costs, including significant legal fees and other expenses, and divert our management and Board of Directors’ attention and resources from our business. Additionally, securities litigation and shareholder activism could give rise to perceived uncertainties as to our future, adversely affect our relationships with customers and business partners, adversely affect our reputation, and make it more difficult to attract and retain qualified personnel. Our stock price could also be subject to significant fluctuation or otherwise be adversely affected by the events, risks and uncertainties of any securities litigation and shareholder activism.

14

We could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws.

The U.S. Foreign Corrupt Practices Act of 1977, the U.K. Bribery Act of 2010, and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments for the purpose of obtaining or retaining business. While our policies mandate compliance with these anti-bribery laws, there is no assurance that our policies and procedures will protect us from circumstances or actions that could result in possible criminal penalties or other sanctions, including contract cancellations or debarment and loss of reputation, any of which could have a material adverse impact on our business, financial condition, and results of operations.

Adverse health events, such as an epidemic or a pandemic, could adversely impact our business.

From time to time, various diseases have spread across the globe, such as the recent COVID-19. If a disease spreads sufficiently to cause an epidemic or a pandemic, our business or the business of our suppliers, subcontractors or customers could be adversely impacted.

Physical and regulatory risks related to climate change could have a material adverse impact on our business, financial condition and results of operations.

As a business that builds new infrastructure and improves existing infrastructure for customers around the world, physical risks related to climate change, such as rising sea levels and temperatures, severe storms, and energy and technological disruptions, could cause delays and increases in project costs, resulting in variability in our revenue and profitability, as well as potentially adverse impacts to our operating results and financial condition. In addition, growing public concern about climate change has resulted in the increased focus of local, state, regional, national and international regulatory bodies on greenhouse gas emissions and climate change issues. Legislation to regulate greenhouse gas emissions has periodically been introduced in the U.S. Congress and in the legislatures of various states in which we operate, and there has been a wide-ranging policy debate, both in the United States and internationally, regarding the impact of these gases and possible means for their regulation. Such policy changes, including any enactment of increasingly stringent emissions or other environmental regulations, could increase the costs of projects for us and for our clients and, in some cases, delay or even prevent a project from going forward, thereby potentially reducing demand for our services. Consequently, this could result in a material adverse impact on our business.

In connection with mergers and acquisitions, we have recorded goodwill and other intangible assets that could become impaired and adversely affect our operating results. Assessing whether impairment has occurred requires us to make significant judgments and assumptions about the future, which are inherently subject to risks and uncertainties, and if actual events turn out to be materially less favorable than the judgments we make and the assumptions we use, we may be required to record impairment charges in the future.

We had $255.6 million of goodwill and indefinite-lived intangible assets recorded on our Consolidated Balance Sheet as of December 31, 2021. We assess these assets for impairment annually, or more often if required. Our assessments involve a number of estimates and assumptions that are inherently subjective, require significant judgment and involve highly uncertain matters that are subject to change. The use of different assumptions or estimates could materially affect the determination as to whether or not an impairment has occurred. In addition, if future events are less favorable than what we assumed or estimated in our impairment analysis, we may be required to record an impairment charge, which could have a material adverse impact on our consolidated financial statements.

Risks Related to Our Capital Structure

We have a substantial amount of indebtedness which could adversely affect our financial position and prevent us from fulfilling our obligations under our debt agreements.

We currently have, and expect to continue to have, a substantial amount of indebtedness. As of December 31, 2021, our total debt was $1.0 billion, with $24.4 million classified as current debt. If we are unable to meet the terms of the financial covenants or fail to comply with any of the other restrictions contained in the agreements governing our indebtedness, an event of default could occur, causing the debt related to such agreements to become immediately due. If such acceleration occurs, we may not be able to repay such indebtedness as required. Since indebtedness under our credit agreement entered into on August 18, 2020 (the “2020 Credit Agreement”) with BMO Harris Bank N.A., as Administrative Agent, Swing Line Lender and L/C Issuer and other lenders is secured by substantially all of our assets, acceleration of this debt could result in foreclosure of those assets and a negative impact on our operations. In addition, a failure to meet the terms of our 2020 Credit Agreement could result in a reduction of future borrowing capacity under the 2020 Credit Agreement, causing a loss of liquidity. A loss of liquidity could

15

adversely impact our ability to execute projects in our backlog, obtain new projects, engage subcontractors, and attract and retain key employees.

Downgrades in our credit ratings could have a material adverse effect on our business and financial condition.

The Company’s debt rating was downgraded by a major credit rating agency on March 23, 2020. The credit ratings assigned to us and our debt are subject to ongoing evaluation by credit rating agencies and could change based upon, among other things, our results of operations and financial condition. Actual or anticipated changes or downgrades in our credit ratings, including any announcement that our ratings are under review for a downgrade, could have a material adverse effect on our costs and availability of capital, which could in turn have a material adverse effect on our financial condition, results of operations, cash flows and our ability to satisfy our debt service obligations. Negative changes in our credit ratings could also result in more stringent covenants and higher interest rates with regard to any new or refinanced debt.

Risk Related to Our Stock Ownership

Our chairman and chief executive officer could exert influence over the Company due to his position and significant ownership interest.

As of December 31, 2021, our chairman and chief executive officer, Ronald N. Tutor, and three trusts controlled by Mr. Tutor (the “Tutor Group”) owned approximately 15% of the outstanding shares of our common stock. Additionally, one of our current directors was appointed by Mr. Tutor pursuant to his right to nominate one member to our Board of Directors, so long as the Tutor Group owns at least 11.25% of the outstanding shares of our common stock. Accordingly, Mr. Tutor could exert influence over the outcome of a range of corporate matters, including the election of directors and the approval or rejection of other extraordinary transactions, such as a takeover attempt or sale of the Company or its assets.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

16

ITEM 2. PROPERTIES

We have office facilities and equipment yards in the following locations, which we believe are suitable and adequate for our current needs:

| Offices | Owned or Leased by Tutor Perini | Business Segment(s) | ||||||||||||

| Los Angeles (Sylmar), CA | Owned and Leased | Corporate, Civil & Specialty Contractors | ||||||||||||

| Barrigada, Guam | Owned | Civil | ||||||||||||

| Black River Falls, WI | Owned | Civil | ||||||||||||

| Evansville, IN | Owned | Civil | ||||||||||||

| Fort Lauderdale, FL | Leased | Building & Specialty Contractors | ||||||||||||

| Framingham, MA | Owned | Building | ||||||||||||

| Gulfport, MS | Owned | Building | ||||||||||||

| Henderson, NV | Owned | Building & Specialty Contractors | ||||||||||||

| Houston, TX | Owned | Specialty Contractors | ||||||||||||

| Jessup, MD | Owned | Civil | ||||||||||||

| Mount Vernon, NY | Leased | Specialty Contractors | ||||||||||||

| New Rochelle, NY | Owned | Civil | ||||||||||||

| Ozone Park, NY | Owned | Specialty Contractors | ||||||||||||

| Philadelphia, PA | Leased | Building | ||||||||||||

| San Carlos, CA | Leased | Building | ||||||||||||

| Equipment Yards | Owned or Leased by Tutor Perini | Business Segment(s) | ||||||||||||

| Black River Falls, WI | Owned | Civil | ||||||||||||

| Evansville, IN | Owned | Civil | ||||||||||||

| Fontana, CA | Leased | Civil | ||||||||||||

| Hilbert, WI | Owned | Civil | ||||||||||||

| Rosemount, MN | Owned | Civil | ||||||||||||

| Stockton, CA | Owned | Building | ||||||||||||

| Waukesha, WI | Owned | Civil | ||||||||||||

ITEM 3. LEGAL PROCEEDINGS

Legal proceedings are discussed in Note 8 of the Notes to Consolidated Financial Statements and are incorporated herein by reference.

ITEM 4. MINE SAFETY DISCLOSURES

We do not own or operate any mines; however, we may be considered a mine operator under the Federal Mine Safety and Health Act of 1977 because we provide construction services to customers in the mining industry. Accordingly, we provide information regarding mine safety violations and other mining regulation matters in Exhibit 95 to this Form 10-K.

PART II.

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock is traded on the New York Stock Exchange under the symbol “TPC.”

Holders

At February 17, 2022, there were 340 holders of record of our common stock, including holders of record on behalf of an indeterminate number of beneficial owners.

17

Dividends and Issuer Purchases of Equity Securities

We did not repurchase any of our common stock during the fourth quarter of 2021. We have not historically paid dividends on our common stock and have no immediate plans to do so.

Issuance of Unregistered Securities

None.

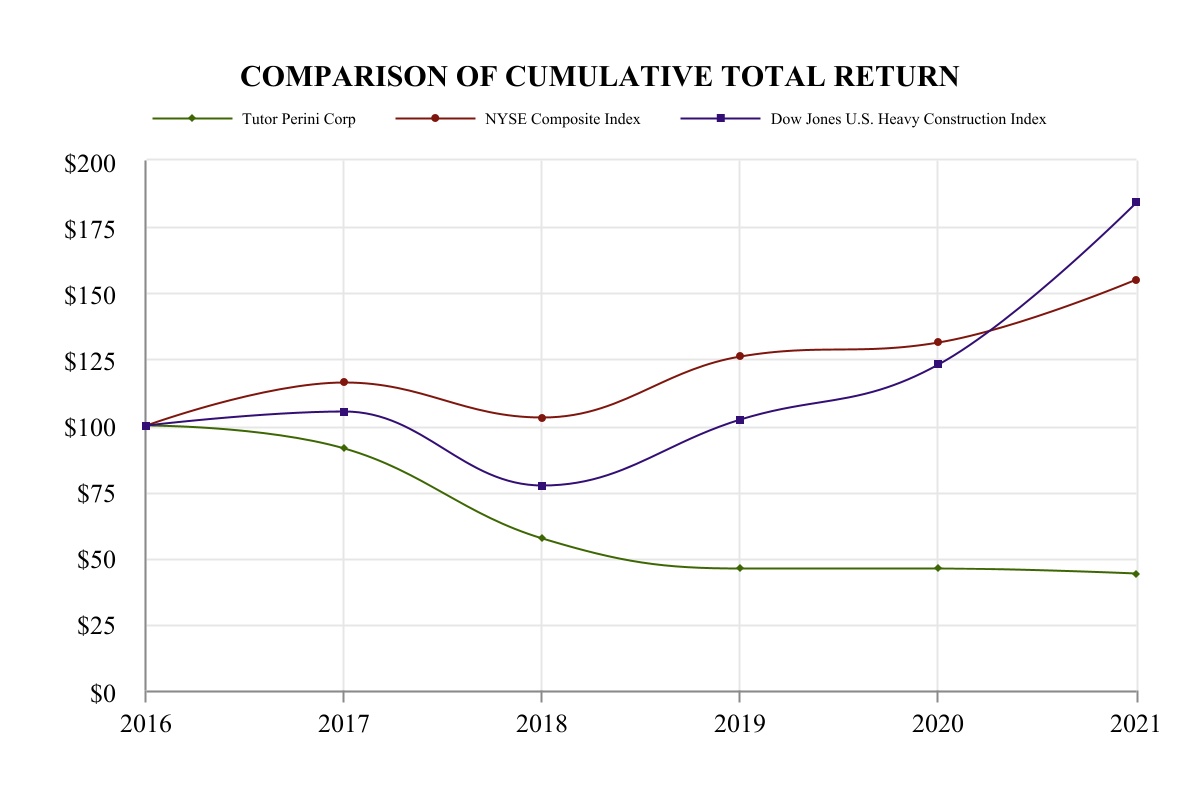

Performance Graph

The following graph compares the cumulative five-year total return to shareholders on our common stock relative to the cumulative total returns of the NYSE Composite Index and the Dow Jones U.S. Heavy Construction Index. We selected the Dow Jones U.S. Heavy Construction Index because we believe the index reflects the market conditions within the industry in which we primarily operate. The comparison of total return on investment, defined as the change in year-end stock price plus reinvested dividends, for each of the periods assumes that $100 was invested on December 31, 2016 in each of our common stock, the NYSE Composite Index and the Dow Jones U.S. Heavy Construction Index, with investment weighted on the basis of market capitalization.

The comparisons in the following graph are based on historical data and are not intended to forecast the possible future performance of our common stock.

ITEM 6. [RESERVED]

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS