UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

Filed by the Registrant þ

Filed by a Party other than the Registrant o

Check the appropriate box:

|

o

|

Preliminary Proxy Statement

|

|

|

|

|

o

|

Confidential, for use of the Commission Only (as permitted by Rule 14a-6(e)(2))

|

|

|

|

|

þ

|

Definitive Proxy Statement

|

|

|

|

|

o

|

Definitive Additional Materials

|

|

|

|

|

o

|

Soliciting Material Pursuant to § 240.14a-11(c) or § 240.14a-12

|

UNITED BANCORP, INC.

(Name of Registrant as Specified in its Charter)

Payment of Filing Fee (Check the appropriate box):

|

þ

|

No Fee Required

|

||

|

|

|

|

|

|

o

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11

|

||

|

|

|

|

|

|

|

•

|

Title of each class of securities to which transaction applies:

|

|

|

|

•

|

Aggregate number of securities to which transaction applies:

|

|

|

|

•

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined):

|

|

|

|

•

|

Proposed maximum aggregate value of transaction:

|

|

|

|

•

|

Total fee paid:

|

|

|

|

|

|

|

|

o

|

|

Fee paid previously with preliminary materials.

|

|

|

o

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

|

|

|

|

|

|

|

|

(1)

|

Amount Previously Paid:

|

|

|

(2)

|

Form, Schedule or Registration Statement No.:

|

|

|

(3)

|

Filing Party:

|

|

|

(4)

|

Date Filed:

|

Notice of

Annual Meeting of Shareholders

and

Proxy Statement

|

|

2013

|

P. O. Box 1127

Ann Arbor, MI 48104

Notice of Annual Meeting

of Shareholders

May 7, 2013

The Annual Meeting of Shareholders of United Bancorp, Inc. will be held at the Downing Center, United Bank & Trust, 209 E. Russell Road, Tecumseh, Michigan, on Tuesday, May 7, 2013 at 4:30 p.m., local time. At the meeting, we will consider and vote on the following matters:

|

1.

|

Election of three directors constituting Class I of the Board of Directors, to serve until the 2016 Annual Meeting of Shareholders and upon the election of their successors.

|

|

|

|

|

2.

|

Advisory approval of the Company's executive compensation.

|

|

|

|

|

3.

|

Advisory vote on the frequency of advisory approval of executive compensation.

|

|

|

|

|

4.

|

Ratification of the appointment of BKD, LLP as independent auditors.

|

We will also conduct such other business as may properly come before the meeting or any adjournment of the meeting. The Notice of Annual Meeting, Proxy Statement and Proxy are first being mailed to shareholders on approximately March 25, 2013.

The Board of Directors has fixed the close of business on March 11, 2013 as the record date for the determination of shareholders entitled to notice of and to vote at the meeting.

You are invited to attend the meeting in person. However, whether or not you expect to attend in person, please promptly sign and date your Proxy, and mail it in the return envelope that is enclosed for that purpose. It will assist us in preparing for the meeting, and it is important that your shares be represented at the meeting.

Important Notice Regarding the Availability of Proxy Materials for the Shareholder Meeting to Be Held on May 7, 2013. Our Proxy Statement, form of Proxy and 2012 Annual Report to Shareholders are available free of charge at www.proxyvote.com and on our website, www.ubat.com.

|

March 25, 2013

|

By Order of the Board of Directors

|

|

|

/s/ Randal J. Rabe

|

|

|

Randal J. Rabe

|

Table of Contents

Proxy Statement

Annual Meeting of Shareholders

May 7, 2013

This Proxy Statement is furnished in connection with the solicitation by the Board of Directors of United Bancorp, Inc. (the "Company" or "UBI") of the accompanying Proxy to be used at the 2013 Annual Meeting of Shareholders of the Company and any adjournment of the meeting. The meeting will be held on May 7, 2013 at the time and place and for the purposes stated in the accompanying Notice of Annual Meeting of Shareholders.

The Notice of Annual Meeting, Proxy Statement and Proxy are first being mailed to shareholders on approximately March 25, 2013. If you have elected to receive your Proxy Statement and Annual Report to Shareholders electronically, we will mail your Proxy by that same date, along with the address of the website where you may download and view your other materials. The mailing address of the principal executive offices of the Company is P.O. Box 1127, Ann Arbor, Michigan 48104.

Only shareholders of record at the close of business on March 11, 2013 will be entitled to notice of and to vote at the meeting. On March 11, 2013, there were 12,705,983 shares of the Company's Common Stock outstanding and entitled to vote at the meeting. Each share of Common Stock is entitled to one vote. Common Stock constitutes the only voting security of the Company entitled to vote upon the proposals to be presented at the meeting.

Shares represented by properly executed Proxies received by the Company will be voted at the meeting in the manner specified in the Proxies. If no instructions are specified in any Proxy, the shares represented by the Proxy will be voted for election of all Director nominees, for Proposals 2 and 4 and "1 year" on Proposal 3. Any Proxy may be revoked by the person giving it at any time before being voted, either by giving another Proxy bearing a later date or by notifying the Secretary of the Company, Randal J. Rabe, at the Company's principal executive offices, in writing of revocation or by attending the meeting and voting in person.

The cost of soliciting Proxies will be borne by the Company. The Company will solicit proxies by mail, internet, telephone or other means. Directors, officers and employees of the Company and its subsidiaries who engage in the solicitation of proxies will receive no additional compensation. Arrangements may also be made directly by the Company with banks, brokerage houses, custodians, nominees, and fiduciaries to forward soliciting matter to the beneficial owners of stock held of record by them and to obtain authorization for the execution of Proxies. The Company may reimburse institutional holders for reasonable expenses incurred by them in connection with this process. The Company has engaged Broadridge at an estimated cost of $5,500 to assist in the distribution of proxy materials.

|

Planning to attend the meeting?

If your Company stock is held in a brokerage account or by a bank or other nominee, you are considered the beneficial owner of shares "held in street name," and this Proxy Statement is being forwarded to you by your broker or nominee. Your name does not appear on the register of shareholders and, in order to be admitted to the meeting, you must bring a letter or account statement showing that you are the beneficial owner of the shares. You will not be able to vote at the meeting, and should instruct your broker or nominee how to vote on your behalf, unless you have a legal proxy from the shareholder of record appointing you as its proxy. If you have any questions about the meeting or require special assistance, please call Diane Skeels, Executive Assistant, at (517) 423-1760.

|

Generally, broker non-votes occur when shares held by a broker in street name for a beneficial owner are not voted with respect to a particular proposal because the broker has not received voting instructions from the beneficial owner and the broker lacks discretionary voting power to vote those shares. If you do not provide your broker with voting instructions, then your broker has discretionary authority to vote your shares on certain "routine" matters. Election of directors and Proposals 2 and 3 are not considered routine matters and your broker will not have discretionary authority to vote your shares on election of directors and Proposals 2 and 3. It is important that you promptly provide your broker with voting instructions if you want your shares voted in the election of directors and on Proposals 2 and 3. We expect that Proposal 4 will be considered a routine matter and your broker will have discretionary authority to vote your shares on the proposal.

Election of Directors. A plurality of the shares voting is required to elect Directors. This means that if there are more nominees than positions to be filled, the nominees who receive the most votes will be elected to the open director positions. Abstentions, broker non-votes and other shares that are not voted in person or by proxy will not be included in the vote count.

Proposals 2 and 4. Proposals 2 and 4 will be approved if a majority of the shares that are voted on each proposal at the meeting are voted in favor of each proposal. Abstentions, broker non-votes and other shares that are not voted on Proposals 2 and 4 in person or by proxy will not be included in the vote count.

Proposal 3. The choice (1 year, 2 years, 3 years or abstain) that receives the most votes will be approved. Abstentions, broker non-votes and other shares that are not voted on Proposal 3 in person or by proxy will not be included in the vote count.

Required Vote for Other Matters. We do not know of any other matters to be presented at the meeting. Generally, any other proposal to be voted on at the meeting would be approved if a majority of the shares that are voted on the proposal at the meeting are voted in favor of the proposal. Abstentions, broker non-votes and other shares that are not voted on the proposal in person or by proxy would not be included in the vote count.

If any other matter should be presented upon which a vote properly may be taken, the shares represented by Proxies will be voted on the matter in accordance with the judgment of the person or persons named in the Proxies.

Under the Company's Articles of Incorporation and Bylaws, the Board of Directors is divided into three classes. Each year, on a rotating basis, the term of office of the Directors in one of the three classes will expire. Successors to the class of Directors whose terms have expired will be elected for a three-year term. The terms of Directors Karen F. Andrews, James D. Buhr and James C. Lawson expire at the 2013 Annual Meeting of Shareholders. These individuals are Class I Directors.

The Compensation & Governance Committee and the Board of Directors have nominated Karen F. Andrews, James D. Buhr and James C. Lawson for election as Class I Directors at the 2013 Annual Meeting of Shareholders. If elected as Class I Directors at the 2013 Annual Meeting of Shareholders, these individuals will hold office until their terms expire at the 2016 Annual Meeting of Shareholders and thereafter until their successor is elected and qualified, subject, however, to prior death, resignation, retirement, disqualification or removal from office.

It is intended that the shares represented by Proxies will be voted for the election of the three nominees unless a contrary direction is indicated. The nominees are each willing to be elected and to serve as Directors. If any of the nominees is unable to serve, the number of Directors to be elected at the meeting may be reduced by the number unable to serve or the individuals named in your Proxy may vote the shares to elect any substitute nominee recommended by the Board of Directors.

Your Board of Directors and Compensation & Governance Committee, which consists entirely of independent directors, recommend that you vote "FOR" the election of all three nominees as Class I Directors

The Dodd-Frank Act requires that the Company provide its shareholders with the opportunity to cast a non-binding, advisory vote on the compensation of the named executive officers, as disclosed pursuant to Item 402 of Regulation S-K in this proxy statement.

This proposal (sometimes referred to as a "Say-on-Pay" proposal) gives you as a shareholder the opportunity to approve or not approve the compensation of our named executive officers through the following resolution:

"Resolved, that the shareholders approve the compensation paid to the Company's named executive officers, as disclosed pursuant to Item 402 of Regulation S-K in the Proxy Statement, including the Compensation Discussion and Analysis, the compensation tables and narrative discussion."

The Company believes that our executive compensation programs appropriately align executives' incentives with shareholder interests and are designed to attract and retain high quality executive talent. We believe that our executive compensation policies are and have been conservative within the industry and in comparison with the compensation policies of competitors in the markets that we serve. We also believe that both the Company and shareholders benefit from responsive corporate governance policies and dialogue.

This vote is not intended to address any specific item of compensation, but rather the overall compensation of the named executive officers and the philosophy and compensation programs described in this proxy statement.

The vote is advisory and not binding upon the Board, and may not be construed as overruling a decision by the board or creating an additional fiduciary duty of the Board. However, the Board and the Compensation & Governance Committee will take into account the outcome of the vote when considering future executive compensation decisions.

The Dodd-Frank Act requires the Company to obtain, at least once every six years, a shareholder vote on the frequency of the advisory approval of the compensation of the named executive officers.

This proposal gives the Company's shareholders the opportunity to determine whether the frequency of the advisory approval of the compensation of the named executive officers will occur every one, two or three years. Shareholders may also abstain from voting on this proposal.

The frequency – one year, two years or three years – that receives the greatest number of votes will be considered to have been approved by the shareholders. This vote is advisory and not binding upon the Company and its Board of Directors. However, the Board of Directors and Compensation & Governance Committee value the opinions of the shareholders and will take into account the outcome of the vote when considering the frequency of the advisory approval of compensation of the named executive officers.

After careful consideration, the Board of Directors has decided to recommend that shareholders vote in favor of holding the advisory approval of the compensation of the named executive officers every year. The Board supports an annual advisory approval because we believe that this will provide our shareholders with the most consistent and clear communication channel for shareholder concerns about the compensation of the named executive officers.

Your Board of Directors and Compensation & Governance Committee, which consists

entirely of independent directors, unanimously recommends

that you vote "ONE YEAR" on Proposal 3.

The Audit Committee and the Board of Directors recommend the ratification of the appointment of BKD, LLP as independent auditors for the Company for the year ending December 31, 2013 to audit the consolidated financial statements of the Company and to perform such other appropriate accounting services as may be approved by the Audit Committee. BKD, LLP has been appointed as the Company's independent public accountants to audit the Company's financial statements since the year ended December 31, 2002. One or more representatives of the firm of BKD, LLP are expected to be present at the meeting, will have the opportunity to make a statement if they desire to do so, and are expected to be available to respond to appropriate questions.

Your Board of Directors and Audit Committee, which consists entirely of

independent directors, recommend that you vote "FOR" Proposal 4.

The following table discloses the name and age of each incumbent Director and Director Nominee, his or her five year business experience, the specific experience qualifications, attributes and skills that led to the conclusion of the Compensation & Governance Committee and the Board of Directors that the person should serve as a Director, and the year each became a Director of the Company. All information is as of the date of this proxy statement.

|

Director Nominees – Terms to Expire in 2016 (Class I)

|

|

Karen F. Andrews, age 46; Consultant and Managing Director with The Andrews Group, a human resources consulting service in Ann Arbor, Michigan. Director of UBI and United Bank & Trust ("UBT") since 2012. Ms. Andrews is a human resources professional and holds a Senior Professional in Human Resources certification. She has held leadership positions with Henry Ford Health System and McKinley, a real estate investment firm. In 2012, she launched The Andrews Group, which offers solutions and strategies to help business leaders create teams and cultures that allow them to meet their goals. In nominating Ms. Andrews, the Compensation & Governance Committee considered as important factors her extensive business experience, her familiarity with the markets in which we operate, her experience in the commercial real estate industry, and her extensive background in human resources management.

|

|

James D. Buhr, age 65; Owner, J.D. Buhr & Company, LLC, corporate finance advisors, Ann Arbor, MI; Vice-Chairman of the Board of UBI since 2011; Director of UBI since 2004; Director of UBT since 2010; Director of United Bank & Trust – Washtenaw ("UBTW") (2001 – 2010). Mr. Buhr has an extensive financial background, including experience as a bank credit analyst, commercial lender and investment banker. He is a native of Washtenaw County, is a registered stock broker, and holds an MBA from the University of Michigan. Mr. Buhr currently owns his own corporate finance advisory practice, which provides corporate finance advisory services to Michigan and Midwestern based companies. In nominating Mr. Buhr, the Compensation & Governance Committee considered as important factors his extensive business experience including commercial lending, his extensive background in corporate finance, his familiarity with the markets in which we operate, his reputation as a respected business leader in our community, and his familiarity with and ability to understand financial statements.

|

|

James C. Lawson, age 65; General Manager, Avery Oil & Propane, Tecumseh, MI; Director of UBI and UBT since 1986; Chairman of the Board of United Bancorp, Inc. since 2011; Vice-Chairman of the Board of United Bancorp, Inc. (2010 – 2011). In nominating Mr. Lawson, the Compensation & Governance Committee considered as important factors his familiarity with the markets in which we operate, his reputation as a respected business leader in our community, his familiarity with and ability to understand financial statements, his diverse background into the formation and operation of a successful business, and his leadership, strategic planning, human resources and administrative skills and background.

|

|

Incumbent Directors – Terms Expiring in 2014 (Class II)

|

|

Stephanie H. Boyse, age 44; President and Chief Executive Officer, Brazeway, Inc., manufacturer of extruded aluminum tubing and related products, Adrian, MI; Director of UBI and UBT since 2008; Director of Tecumseh Products Company, manufacturer of compressors and refrigeration components, engines, and power train components, Tecumseh, MI (2013). In nominating Ms. Boyse, the Compensation & Governance Committee considered as important factors her diverse range of experience including sales, marketing, operations, human resources, licensing and acquisitions including international experience, her familiarity with the markets in which we operate, her reputation as a respected business leader in our community, and her extensive work with non-profit organizations in our markets.

|

|

Kenneth W. Crawford, age 55; Independent financial consultant. Director of UBI and UBT since 2011. Retired Senior Vice President, Chief Financial Officer, Corporate Controller and Assistant Secretary of Kaydon Corporation, Ann Arbor, MI. Kaydon Corporation is a leading designer and manufacturer of custom engineered, performance-critical products, supplying a broad and diverse group of alternative energy, military, industrial, aerospace, medical and electronic equipment, and aftermarket customers. Mr. Crawford has held various accounting and finance positions with a number of public companies. In nominating Mr. Crawford, the Compensation & Governance Committee considered as important factors his strong accounting and financial background, his experience with mergers and acquisitions, his ability to understand financial statements and qualify as an "audit committee financial expert," and his experience working with public companies.

|

|

John H. Foss, age 70; Director, La-Z-Boy Incorporated; Retired Director, Vice President, Treasurer and Chief Financial Officer, Tecumseh Products Company; Director of UBI and UBT since 1992. Mr. Foss is a CPA, and his work experience includes financial management and auditing. He has served as CFO of two publicly traded companies and as Chairman of the Audit Committee of La-Z-Boy. In nominating Mr. Foss, the Compensation & Governance Committee considered as important factors his extensive financial management and auditing experience, his ability to understand financial statements and qualify as an "audit committee financial expert," his experience working with public companies, and his extensive practical experience and understanding in the areas of strategic planning, compensation management, internal controls, mergers and acquisitions and corporate governance.

|

|

Incumbent Directors – Terms to Expire in 2015 (Class III)

|

|

Robert K. Chapman, age 69; President (since 2003) and Chief Executive Officer (since 2006) of the Company; Director of UBI and UBT since 2001; Chief Executive Officer (2001 – 2007) of the Company's former subsidiary, UBTW; President and Chief Executive Officer of UBT since 2010. Mr. Chapman is a CPA. In nominating Mr. Chapman, the Compensation & Governance Committee considered as important factors his experience in the financial industry in a financial role and in mergers and acquisitions, his strong background in risk management, his ability to understand financial statements, his familiarity with the markets in which we operate, and his extensive work with non-profit organizations in our markets.

|

|

Norman G. Herbert, age 70; Independent financial consultant. Director of UBI since 2009; Director of UBT since 2010; Director of UBTW (2006 – 2010). Mr. Herbert has an extensive financial background. For thirty-five years, he was a part of the financial management team for the University of Michigan, with responsibilities including management of endowment and working capital, real estate acquisitions and dispositions, external financing activities and risk management. In nominating Mr. Herbert, the Compensation & Governance Committee considered as important factors his extensive financial background, his ability to understand financial statements, his analytical background and a meticulous attention to detail, and his work with professional, civic and non-profit organizations.

|

|

Len M. Middleton, age 49; Professor of Strategy and Entrepreneurship, Ross School of Business at the University of Michigan. Director of UBI and UBT since 2010; Director of UBTW (2009 – 2010). Trustee at the Ann Arbor Hands-On Museum. He holds an MBA, and is founder of a private equity firm that specializes in buyouts and other investment opportunities. In nominating Mr. Middleton, the Compensation & Governance Committee considered as important factors his extensive financial background, his experience with mergers and acquisitions, his ability to understand financial statements, his broad range of entrepreneurial experience, and his work with entrepreneurial companies and non-profit organizations.

|

None of the Director nominees or incumbents, with the exception of Stephanie H. Boyse, John H. Foss and Len M. Middleton, serves as a director, or at any time during the past five years served as a director, of any other company with a class of securities registered pursuant to Section 12 of the Securities Exchange Act of 1934, as amended, or subject to the requirements of Section 15(d) of such act, or any company registered as an investment company under the Investment Company Act of 1940, as amended. Ms. Boyse is a director of Tecumseh Products Company. Mr. Foss is a director of La-Z-Boy Incorporated. Mr. Middleton is a Director of Arcadia Funds, Castle Oaks and One Tree. With the exception of Mr. Chapman, each Director and Director Nominee, and each person who served as a Director at any time during the last fiscal year, is or was independent as that term is defined under NASDAQ Listing Rules for service on the Board of Directors and each committee on which the Director serves. While the Company is not subject to these standards, it has chosen to comply with them voluntarily.

The Board of Directors reviews transactions with companies owned or managed by Directors, for the purpose of determining whether those transactions impact the independence of Directors. The Company conducted transactions in the normal course of business with companies affiliated with a single director during 2012 and 2011. The Board determined that these transactions did not impact the independence of that Director.

The Board of Directors has established a standing Audit Committee and Compensation & Governance Committee. The Compensation & Governance Committee also performs the functions of a nominating committee.

Audit Committee

The Audit Committee consists of Kenneth W. Crawford, John H. Foss, Norman G. Herbert and Len M. Middleton. The Audit Committee met eight times during the year ended December 31, 2012. Each of the current members meets the requirements for independence as defined under NASDAQ listing rules. While the Company is not subject to these standards, it has chosen to comply with them voluntarily. In addition, the Board of Directors determined that Mr. Crawford and Mr. Foss have met the qualifications to be considered an "audit committee financial expert" as set forth under rules adopted by the Securities and Exchange Commission.

The Audit Committee has selected BKD LLP ("BKD") as its independent registered public accounting firm for 2013. BKD has served in that capacity since 2002. The services provided by BKD are limited by the Audit Committee to audit services and certain permitted audit related and tax services.

The Board of Directors has adopted a written charter for the Audit Committee, a copy of which is available on the Company's website at www.ubat.com. The Board of Directors reviews and approves changes to the Audit Committee charter annually.

The Audit Committee has full power and authority to perform the responsibilities of a public company audit committee under applicable law, regulations, stock exchange listing standards, generally accepted accounting principles and public company custom and practice. The Audit Committee assists the Board in its oversight responsibilities of the integrity of the Company's financial statements, the system of disclosure controls and procedures and internal control over financial reporting, the independence and performance of the Company's internal auditor, the independence and performance of the independent registered public accounting firm, the Company's process for monitoring compliance with legal and regulatory requirements, the integrity and security of the Company's information systems and technology and the Company's enterprise risk management. Management is responsible for the Company's financial statements and the financial reporting process, and for establishing and maintaining the Company's system of internal controls. The independent registered public accounting firm is responsible for expressing an opinion on the conformity of the Company's financial statements with U.S. generally accepted accounting principles.

The Audit Committee reports that with respect to the audit of the Company's consolidated financial statements for the year ended December 31, 2012:

|

•

|

The Audit Committee has reviewed and discussed the Company's 2012 audited consolidated financial statements with the Company's management.

|

|

|

|

|

•

|

The Audit Committee has discussed with its independent registered public accounting firm, BKD, LLP, the matters required to be discussed by the Statement on Auditing Standards No. 61, as amended (AICPA, Professional Standards, Vol. 1. AU Section 380) as adopted by the Public Company Accounting Oversight Board in Rule 3200T.

|

|

|

|

|

•

|

The Audit Committee has received the written disclosures and the letter from its independent registered public accounting firm required by applicable requirements of the Public Company Accounting Oversight Board regarding BKD's communications with the Audit Committee concerning independence, and has discussed with BKD its independence.

|

Based on the review and the discussions referenced above, the Audit Committee recommended to the Board of Directors that the Company's 2012 audited consolidated financial statements be included in the Company's Annual Report on Form 10-K for the year ended December 31, 2012.

|

|

Audit Committee

|

|

|

Norman G. Herbert, Chairman

|

|

|

Kenneth W. Crawford

|

|

|

John H. Foss

|

|

|

Len M. Middleton

|

The Board of Directors of the Company has established a Compensation & Governance Committee, which addresses matters relating to employment, compensation, and management performance. The Compensation & Governance Committee also performs the functions of a nominating committee for the Board of Directors. The Board of Directors has adopted a written charter for the Compensation & Governance Committee, a copy of which is available on the Company's website at www.ubat.com.

Our Compensation & Governance Committee annually reviews and approves our compensation program, evaluates the performance of our Chief Executive Officer and, with input from the Chief Executive Officer, reviews the performance of the executive officers in achieving our business objectives, and recommends executive officers' compensation to our Board of Directors for approval. The Chief Executive Officer of the Company provides input into the recommended compensation of the executive officers to the Compensation & Governance Committee, but does not determine, recommend or participate in compensation decisions regarding his own compensation. Although input from the Chief Executive Officer is considered by the Compensation & Governance Committee and the Board, it is not given any disproportionate weight. The committee has the authority to recommend executive officers' compensation to our Board of Directors for approval in its discretion. The committee also recommends targets for bonuses and profit sharing and has sole authority to grant stock options and other equity awards to eligible individuals. The Compensation & Governance Committee and the Board have the final authority on compensation matters. Except to the extent prohibited by exchange rules (if applicable) and state law, the committee may delegate its authority to subcommittees when it deems it appropriate and in the best interests of the Company.

The Compensation & Governance Committee considers various potential candidates for Director that may come to its attention through current board members, shareholders or other persons. The Compensation & Governance Committee will review and evaluate candidates for Director nominated by shareholders in the same manner as it evaluates all other candidates. When considering and evaluating candidates for nomination to the Board, the committee considers a number of factors. The Compensation & Governance Committee considers board diversity as a factor in identifying nominees for Director, but diversity is not a dispositive factor and the Company has no formal diversity policy for Directors. In addition, the Compensation & Governance Committee believes that a Board candidate should:

|

•

|

Be a shareholder of United Bancorp, Inc.

|

|

|

|

|

•

|

Be willing and able to devote full interest and attendance to the Board and its committees

|

|

|

|

|

•

|

Bring their financial business to the Company, including personal and business accounts

|

|

|

|

|

•

|

Lend credibility to the Company and enhance its image

|

|

|

|

|

•

|

Help develop business and promote the Company and its subsidiaries

|

|

|

|

|

•

|

Provide advice and counsel to the CEO

|

|

|

|

|

•

|

Maintain integrity and confidentiality at all times.

|

The Compensation & Governance Committee will consider shareholder nominations for candidates for membership on the Board when properly submitted in accordance with the Company's bylaws. The bylaws provide that no less than 120 days prior to the date of the meeting, in the case of an annual meeting, and not more than seven days following the date of notice of the meeting, in the case of a special meeting, any shareholder who intends to make a nomination at the meeting shall deliver a notice to the secretary of the Company setting forth (i) the name, age, business address and residence of each nominee proposed in such notice, (ii) the principal occupation or employment of each such nominee, (iii) the number of shares of each class and series of capital stock of the Company which are beneficially owned by each such nominee and (iv) such other information concerning each such nominee as would be required, under the rules of the Securities and Exchange Commission, in a proxy statement soliciting proxies for the election of such nominee.

The Compensation & Governance Committee met seven times during 2012, and is composed of the following Directors of the Company: Karen F. Andrews, Stephanie H. Boyse, James D. Buhr, John H. Foss and James C. Lawson. All members of the Company's Compensation & Governance Committee meet the requirements for independence under NASDAQ Listing Rules. While the Company is not subject to these standards, it has chosen to comply with them voluntarily.

The Company has adopted a comprehensive Corporate Governance Policy. The policy is designed to promote accountability and transparency for the Board of Directors and management of the Company. The policy contains guidelines regarding the responsibilities, membership, and structure of the Board of Directors, including policies addressing:

|

•

|

Board leadership;

|

|

•

|

Director independence, diversity, education, and conflicts of interest; and

|

|

•

|

Majority vote requirement for uncontested elections.

|

The policy also contains guidelines for other significant corporate governance matters, such as the Board of Directors' responsibility for risk management and succession planning. The Corporate Governance Policy is available at the Company's website, www.ubat.com, under the "About Us – Investor Relations – Governance Documents" section.

The Company has adopted a comprehensive Code of Ethics. The code is intended to deter wrongdoing and to promote:

|

•

|

Honest and ethical conduct, including the ethical handling of actual or apparent conflicts of interest between personal and professional relationships;

|

|

|

|

|

•

|

Full, fair, accurate, timely and understandable disclosure in documents the Company files with, or submits to, the SEC and in all public communications made by the Company;

|

|

•

|

Compliance with applicable governmental laws, rules and regulations; and

|

|

|

|

|

•

|

Prompt internal reporting to designated persons of violations of the code.

|

The Code of Ethics is available on the Company's website, www.ubat.com, under "About Us – Investor Relations – Governance Documents" section.

The Board of Directors of United is led by its Chairman of the Board, who is not the Chief Executive Officer of the Company. The Compensation & Governance Committee believes that separation of the positions of Chairman of the Board and Chief Executive Officer recognizes the difference between the two roles and reflects good corporate governance practice. The Chairman of the Board leads the Board of Directors in adopting an overall strategic plan for the Company, sets the agenda for the meetings of the Board of Directors, presides over all meetings of the Board of Directors, and provides guidance to the Chief Executive Officer. The Chief Executive Officer implements the strategic plan for the Company, as adopted by the Board of Directors, and leads the Company, its management and its employees on a day-to-day basis. Because of these differences, the Company currently believes keeping the Chairman of the Board and Chief Executive Officer as separate positions is the appropriate leadership structure for the Company.

James C. Lawson was elected as Chairman of the Board following the 2011 Annual Meeting of Shareholders. Mr. Lawson has a diverse background in the formation and operation of a successful business, and has served as a Director of the Company since 1986. Robert K. Chapman serves as the Company's President and Chief Executive Officer, and brings more than thirty years of banking experience in various roles, as well as leadership in the Washtenaw County market, to his role.

The Company continues to enhance and implement its enterprise risk management ("ERM") process. The Board is responsible for overseeing the ERM process. The Enterprise Risk Management Committee implements the ERM process by overseeing policies, procedures and practices relating to enterprise-wide risk and compliance with bank and regulatory obligations. The committee consists of members of the executive management team and other appointed individuals from the various identified risk areas. The Company's Chief Financial Officer serves as chair of the committee.

Among other things, the committee is responsible for designing and implementing effective ERM processes and practices, ensuring that management understands and accepts responsibility for identifying, assessing and managing risk, ensuring that risk assessments are completed for each identified risk area, and reviewing and updating risk assessments on at least a quarterly basis. The committee has identified and monitors twelve risk areas. In 2011 and 2012, the ERM process involved a heightened focus on risks related to credit quality of the loan portfolio and earnings and capital, as both of these areas presented elevated levels of risk to the Company. The committee must meet at least four times per year. The Chief Financial Officer must report on the ERM process to the Board of Directors on at least a quarterly basis.

The Board of Directors, and the Audit Committee under authority and responsibility delegated by the Board of Directors, play a key role in the oversight of the Company's risk management. To that end, the Board of Directors or the Audit Committee must periodically require and receive direct reports from the Enterprise Risk Management Committee.

Shareholders may communicate with the Board of Directors, its committees or any member of the Board of Directors by writing to Chairman of the Board, United Bancorp, Inc., P. O. Box 1127, Ann Arbor, Michigan, 48104. All shareholder communications will be forwarded to the Board, the committee or the Director as indicated in the writing. The Chairman has discretion to screen and not forward to directors communications which the Chairman determines in his discretion to be communications unrelated to the business or governance of the Company and its subsidiaries, commercial solicitations, offensive, obscene or otherwise inappropriate. The Chairman shall, however, collect all security holder communications which are not forwarded, and such communications shall be available to any director upon request.

During the year ended December 31, 2012, the Board of Directors of the Company met a total of six times. Each of the Directors attended at least 75% of the aggregate of the total number of meetings of the Board and of the Board committees of which he or she is a member.

The Company encourages members of its Board of Directors to attend the Annual Meeting of Shareholders. All directors serving at May 8, 2012 other than Stephanie H. Boyse attended the Company's 2012 Annual Meeting of Shareholders held on that date.

Meetings of Independent Directors

The Company's independent directors meet periodically in executive sessions without any management directors in attendance. If the Board of Directors convenes a special meeting, the independent directors may hold an executive session if the circumstances warrant.

The Audit Committee has established a program for employees of the Company and its subsidiaries to report violations of standards of conduct specified in the program, improper activity or other suspected wrongdoing by any officer or employee to the Chairman of the Audit Committee, in particular any activity that may jeopardize the accuracy of financial reporting, represent a conflict of interest, violate corporate ethics policies, or violate any provision of federal law. Retaliation against any employee who reports a good faith concern is not permitted.

Following is a current listing of executive officers of the Company and biographical information about each executive officer. All information is as of the date of this proxy statement. Officer appointments for the Company are made or reaffirmed annually at the Organizational Meeting of the Board of Directors. The Board may also designate executive officers at regular or special meetings of the Board. Executive officers of the Company serve at the pleasure of the Board.

|

Name, Age, and Five Year Business Experience

|

Executive Officer Since

|

|

Robert K. Chapman, age 69; Director of UBI since 2001; President (since 2003) and Chief Executive Officer (since 2006) of the Company; President (2010–February, 2013) and Chief Executive Officer of UBT since 2010; President (2001–2005) and Chief Executive Officer (2001–2007) of UBTW; Director of UBTW (2001–2010)

|

2001

|

|

Randal J. Rabe, age 54; Executive Vice President (since 2003) and Chief Financial Officer (since December, 2007) of the Company; President (2003–2007) & Chief Executive Officer (2005–2007) and Director (2003–2007) of UBT

|

2003

|

|

Todd C. Clark, age 43; Executive Vice President of the Company; President (since February, 2013) of UBT; Chief Operating Officer and Washtenaw Community President (2010–2013); President (2006–2010) and Chief Executive Officer (2007–2010) of UBTW; Director (2006–2010) of UBTW

|

2005

|

|

Gary D. Haapala, age 49; Executive Vice President of the Company since 2006; Executive Vice President – Wealth Management Group of UBT since 2006

|

2006

|

|

Joseph R. Williams, age 49; Executive Vice President of the Company (since 2007); Lenawee Community President (since 2010); President and Chief Executive Officer and Director of UBT (2007–2010); Executive Vice President – Community Banking of UBT (2003–2007)

|

2007

|

Executive Summary

This discussion describes all material elements of our compensation program for our executive officers named in the Summary Compensation Table below ("named executive officers").

We believe our executive compensation programs continue to provide a competitive pay-for-performance package that helps us attract, retain, and motivate our executives. We believe that it is important that our executive compensation also reflect the relative financial performance of the Company. Prior to June 2012, we were subject to limitations on executive compensation as a result of our participation in the TARP Capital Purchase Plan, as described below. In spite of the lifting of the limitations resulting from this program, we made no significant changes to our executive compensation programs in 2012.

Our Compensation & Governance Committee continued to work with Findley Davies, the committee's independent executive compensation consultant. In 2012, Findley Davies assisted the committee in evaluating Director compensation compared to peers, and performed a review and analysis of the Company's current Management Committee Incentive Plan. Minimum levels were not met in 2012 for payment under the Company's Management Committee Incentive Compensation Plan, and no payments were made under the plan in 2012. The Company granted Restricted Stock Unit awards in 2012, with vesting based on satisfaction of time based and performance based vesting requirements. Those grants performance vested at 97.5% of target in 2012.

We continue to monitor all of our compensation program elements and practices to determine how they compare with current market practices and align with our overall compensation philosophy. At our annual meeting of shareholders in 2009, we began providing our shareholders with the opportunity to cast an annual advisory vote on our executive compensation (a "say-on-pay proposal"). At each annual vote of shareholders on this matter, a majority of the votes cast by our shareholders were to approve the compensation we paid to our named executive officers. Our compensation committee takes this result into account in determining compensation policies and setting compensation and will consider such results in the future.

Compensation Philosophy and Objectives

Our executive compensation program is overseen by our Compensation & Governance Committee. The Compensation & Governance Committee believes that our compensation program should be designed to tie annual and long-term cash and stock incentives to achievement of measurable business and individual performance objectives. The Compensation & Governance Committee believes that this approach aligns executives' incentives with shareholder value creation and allows the Company to attract and retain high quality executive talent. Accordingly, a portion of our executives' overall compensation is tied to our financial performance (including our return on assets and net income). Our compensation philosophy is intended to compensate our executives with base salary targeted at the midrange of market competitive levels, while rewarding for outstanding corporate performance with our performance based plans. If performance goals are achieved, the result will likely be total compensation above the midrange of market competitive levels.

The Company provides its shareholders with the opportunity to cast an annual advisory vote on executive compensation (a "say-on-pay proposal"). At the Company's annual meeting of shareholders held in May 2012, 81.0% of the votes cast on the say-on-pay proposal at that meeting were voted in favor of the Company's executive compensation for 2011. The Compensation & Governance Committee believes this affirms shareholders' support of the Company's approach to executive compensation. In light of the voting results, the Committee did not materially change its approach in 2012. The Compensation & Governance Committee will continue to consider the outcome of advisory votes on the Company's say-on-pay proposals when making future compensation decisions for the named executive officers.

Compensation Process

In its process for deciding how to compensate our named executive officers, the Compensation & Governance Committee considers, among other things, competitive market data. Some of the resources considered were the ABA Executive Compensation Standard Report, American Bankers Association Compensation Benefits Survey, BAI Bank Cash Compensation Survey, Crowe Chizek Financial Institutions Compensation Survey, Mercer Benchmark Database Human Resource Management, Michigan Bankers Association Compensation Survey and Watson Wyatt Benchmark Compensation Report for Financial Institutions.

None of the resources was specifically prepared or customized for the Company and each resource contained only aggregate data with regard to the institutions surveyed. While the Compensation & Governance Committee considered these resources, it determined compensation levels in its judgment based on what it considered to be reasonable and appropriate for the Company.

For 2012, the Committee engaged the services of Findley Davies as compensation consultants. Findley Davies assisted the Compensation & Governance Committee in evaluating Director compensation compared to peers, and performed a review and analysis of the Company's current Management Committee Incentive Plan. Findley Davies did not provide any other services to the Company during 2012.

The Compensation & Governance Committee also uses tally sheets prepared by our payroll department with respect to each of our named executive officers. Tally sheets include the dollar value of each component of the named executive officers' compensation, including current cash compensation, accumulated deferred compensation balances, outstanding equity awards, retirement benefits, perquisites and any other compensation. The primary purpose of the tally sheets is to bring together in one place all of the elements of compensation of our named executive officers so that the Compensation & Governance Committee may analyze both the individual elements of compensation (including the compensation mix) as well as the aggregate total amount of compensation. The Compensation & Governance Committee generally compares the information on the tally sheets, on an individual and aggregate basis, to the extent comparisons are available, to market data. In addition, such tallies are also used to determine internal equity conformance.

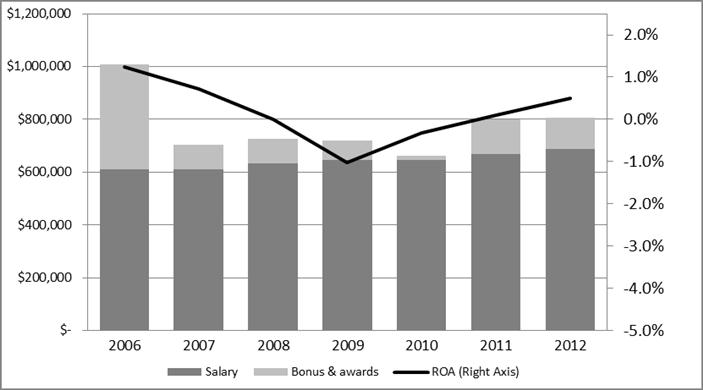

We believe that it is important that our executive compensation reflect the relative financial performance of the Company. The table below shows the aggregate base salary and bonus and awards of the named executive officers, compared to the return on average assets ("ROA") of the Company for the past seven years.

Targets and Peer Data

The Compensation & Governance Committee has the authority to set targets at other than those contained in the current year Board-approved financial plan.

For 2012, the targets for payouts under the 2009 Management Committee Incentive Compensation Plan were set at a level that was higher than the 2012 board-approved financial plan, and targets for performance based vesting of Restricted Stock Units granted in 2012 were based on the 2012 board-approved financial plan.

The Compensation & Governance Committee has utilized comparison to a number of peer groups for the purpose of ranking our financial performance with peers in order to validate our performance targets. However, these peer groups were not used specifically to compare our compensation practices and levels to peer companies.

Compensation Components

The key components of our executive compensation program consist of a base salary and participation in various performance-based compensation plans, including our Management Committee Incentive Compensation Plan, Senior Management Bonus Deferral Stock Plan, 401(k) Plan, and our Stock Incentive Plan of 2010.

Base Salary

We use base salary to attract and retain executive officers near the midpoint of market rates, and rely on our performance-based plans to reward for performance. The Company generally hires executive officers at market rates necessary to attract talent. Raises and salary adjustments for named executive officers are provided primarily to allow us to retain our existing talent.

Generally, we believe that base salary should be set at mid-level market competitive levels. Base salaries are reviewed annually and are compared to several databases and public information, and adjusted from time to time.

2009 Management Committee Incentive Compensation Plan

The named executive officers participate in the Management Committee Incentive Compensation Plan. Under the plan, a participant is paid a percentage of his or her base salary based on the achievement of business and individual performance objectives. Bonuses under the plan are based all or in part on our achieving a target return on assets ("ROA") as established annually by the Board of Directors. For 2012, our target ROA was 1.0%.

The plan is divided into groups, each with differing payout levels based on a percentage of base salary. Participants in the plan may earn more or less than the prescribed bonus percentages at target levels, with threshold and maximum bonus levels established. The table below details the range of minimum, target and maximum thresholds and payouts for each group of the plan, relating to the named executive officers.

|

|

No Bonus is Earned

if Performance

is Below: |

Bonus Earned

at Minimum Threshold

|

Bonus Earned at

100% of Target

|

Maximum Bonus

That Can Be

Earned

|

Maximum Bonus

is Earned At or Above: |

||

|

Group 1

|

0.50%

|

ROA

|

11.25%

|

45%

|

90%

|

1.625%

|

ROA

|

|

Group 2

|

0.50%

|

ROA

|

8.75%

|

35%

|

70%

|

1.625%

|

ROA

|

Targets for 2012 for all participants were based 100% on ROA, as participants each have responsibilities with regard to the overall performance of the Company. Targets were not achieved in 2012, and as a result, no incentive compensation was paid to any of the named executive officers under the plan.

The table below details the respective named executive officers in each group, the group within the plan that each participates in, the basis upon which the bonus is determined, and the payout percentages for calendar year 2012.

|

Executive Officer

|

Group

|

Based on:

|

2012 Payout

|

|

Chapman

|

1

|

Target ROA (100%)

|

0%

|

|

Rabe

|

2

|

Target ROA (100%)

|

0%

|

|

Clark

|

2

|

Target ROA (100%)

|

0%

|

Under the 1996 Senior Management Bonus Deferral Stock Plan, participating officers are eligible to elect cash bonus deferrals and, after employment termination, to receive payment in the form of shares of Company common stock. During 2011 and 2012, none of the named executive officers received bonuses eligible to be deferred under the plan and, as of December 31, 2012, none of the named executive officers had any balance in the plan.

Stock Incentive Plan of 2010

At the 2010 Annual Meeting of Shareholders, shareholders approved the United Bancorp, Inc. Stock Incentive Plan of 2010 (the "Incentive Plan"). The Incentive Plan is intended to supplement and continue the compensation policies and practices of our other equity compensation plans, which we have used for many years. The Board of Directors believes that the Incentive Plan is important to attract, retain and motivate corporate and subsidiary directors, officers and key employees of exceptional abilities, and to recognize the significant contributions these individuals have made to the long-term performance and growth of the Company and its subsidiaries. The Compensation & Governance Committee awarded grants in 2012 under the Incentive Plan based on the Company's 2011 performance, and in 2011 based on the Company's 2010 performance.

The Incentive Plan includes a number of components, as follows:

Stock Options

The Incentive Plan permits the Company to grant to participants options to purchase shares of common stock at stated prices for specific periods of time. Stock options that may be granted under the Incentive Plan could be either nonqualified stock options or incentive stock options as defined in Section 422 of the Internal Revenue Code. The Compensation & Governance Committee may award options for any amount of consideration or no consideration, as the committee determines. No stock options were granted in 2012 or 2011.

Stock Appreciation Rights

The Incentive Plan permits the Compensation & Governance Committee to grant stock appreciation rights. A stock appreciation right permits the holder to receive the difference between the market value of a share of common stock subject to the stock appreciation right on the exercise date of the stock appreciation right and a "base" price set by the Compensation & Governance Committee. Stock appreciation rights are exercisable on dates determined by the Compensation & Governance Committee at the time of grant. The committee may award stock appreciation rights for any amount of consideration or no consideration, as the committee determines.

Stock appreciation rights are subject to terms and conditions determined by the Compensation & Governance Committee. A stock appreciation right may relate to a particular stock option and may be granted simultaneously with or subsequent to the stock option to which it relates. The Company granted Stock-Only Stock Appreciation Rights ("SOSARs") in 2012 and 2011.

Restricted Stock and Restricted Stock Units

The Incentive Plan permits the Compensation & Governance Committee to award restricted stock and restricted stock units, subject to the terms and conditions set by the committee that are consistent with the Incentive Plan. Shares of restricted stock are shares of common stock, the retention, vesting and transferability of which are subject, for specified periods of time, to such terms and conditions as the Compensation & Governance Committee deems appropriate (including continued service or employment and/or achievement of performance goals established by the committee). The Compensation & Governance Committee may award restricted stock or restricted stock units for any amount of consideration or no consideration, as the committee determines.

The Compensation & Governance Committee establishes the terms of individual awards of restricted stock and restricted stock units in award agreements or certificates of award. Restricted stock and restricted stock units granted to a participant "vest" (i.e., the restrictions on them lapse) in the manner and at the times that the Compensation & Governance Committee determines. The Company awarded restricted stock in 2011 and restricted stock units ("RSUs") during 2012 and 2011.

The period during which restricted stock and RSUs are unvested under the Plan is known as the "Restricted Period." The restrictions imposed on 100% of the restricted stock awarded are time-based, and lapse two years from the date of grant.

RSUs vest upon satisfaction of time based and performance based vesting requirements. Vesting for RSUs granted in 2012 is as follows:

|

·

|

Time Based Vesting. The percentage of RSUs awarded that satisfy the performance based vesting requirements will generally vest and be settled three years from the date of the grant.

|

|

·

|

Performance Based Vesting. The performance period for the RSUs granted in 2012 is the period beginning January 1, 2012 and ending December 31, 2012.

|

The percentage specified below of RSUs awarded will satisfy the performance based vesting requirements of the award if the Company's core earnings, as measured by pre-tax, pre-provision return on assets ("PTPP ROA"), earnings, as measured by return on assets ("ROA") and asset quality, as measured by Classified Assets Coverage,1 as determined by the Company in a manner consistent with the information reported in its filings with the Securities and Exchange Commission, meet the standards set forth in the following schedule:

|

Performance Measure (Metric)

|

Weight

|

Performance

Standard

|

% of RSU Award

Performance Vested

|

|

Core Earnings

(PTPP ROA)

|

1/3

|

1.35%

|

25%

|

|

1.45%

|

50%

|

||

|

1.55%

|

75%

|

||

|

1.65%

|

100%

|

||

|

Earnings

(ROA)

|

1/3

|

0.11%

|

25%

|

|

0.21%

|

50%

|

||

|

0.32%

|

75%

|

||

|

0.42%

|

100%

|

||

|

Asset Quality

(Classified Assets Coverage)

|

1/3

|

55.0%

|

25%

|

|

50.0%

|

50%

|

||

|

45.0%

|

75%

|

||

|

40.0%

|

100%

|

RSUs will not vest upon performance below the minimum performance standards provided above. Vesting upon performance between the performance standards provided above will be interpolated based on the actual performance. For 2012, RSUs performance vested at 97.5% of target.

Stock Awards

The Incentive Plan permits the Compensation & Governance Committee to make stock awards. The committee may make stock awards for any amount of consideration, or no consideration, as the committee determines. A stock award of common stock is subject to terms and conditions set by the Compensation & Governance Committee at the time of the award. Stock award recipients generally have all voting, dividend, liquidation and other rights with respect to awarded shares of common stock. However, the committee may impose restrictions on the assignment or transfer of common stock awarded under the Incentive Plan. No stock awards were granted in 2012 or 2011.

Other Stock-Based Awards

Finally, the Incentive Plan permits the Compensation & Governance Committee to grant a participant one or more types of awards based on or related to shares of common stock, other than the types described above. Any such awards are subject to such terms and conditions as the Compensation & Governance Committee deems appropriate, as set forth in the respective award agreements and as permitted under the Incentive Plan. No other stock-based awards were granted in 2012 or 2011.

Stock Option Plans

Before December 31, 2009, we granted stock options under one of two stock option plans: the 1999 and 2005 stock option plans. The 1999 and 2005 stock option plans have expired and been replaced by the Stock Incentive Plan of 2010. Options granted under the plans and not exercised are still outstanding, and no new options may be granted under either plan.

Under the plans, options were granted at the then-current market price at the time the option was granted. The options have a three-year vesting period and, with certain exceptions, expire at the end of ten years from the date of grant, or three years after retirement. Options granted under our plans are non-qualified stock options as defined under the Internal Revenue Code.

Our Compensation & Governance Committee administers our stock option plans. Option grants for any certain year were generally determined by evaluating the number of option grants available under the plan, divided by the number of years remaining in the plan. The committee allocated some or all of the options available for a particular year to eligible participants based on a number of factors, including the relative rank of the executive officer within our Company and his or her specific contributions to the success of the Company for the prior year. The committee did not time the grant of stock options to take advantage of material non-public information, or time the release of material non-public information to increase the value of option grants.

We believe the options served to enhance shareholder value by aligning the interests of our executive officers with those of the shareholders and also by acting to retain our executive officers through the vesting of the options. The exercise price of all options granted under the plans was higher than the Company's stock price as of December 31, 2012, and accordingly, unless the stock price significantly improves, the ability of those options to assist in retention of our executive officers may not be realized.

401(k) Plan

Under our 401(k) plan, named executive officers and other participants may defer a portion of their compensation, and the Company's 401(k) plan provides for a match of up to 4% of salary, subject to IRS regulations. In addition to the match contributions, the plan includes a profit-sharing feature based on achievement of a net income target as established annually by the Board of Directors. Effective July 1, 2009, the Company discontinued its match and profit sharing contributions to the 401(k) plan as a cost-cutting measure. The Company reinstated match contributions beginning January 1, 2011, but did not make profit sharing contributions in 2012 or 2011.

Severance Arrangements

Each named executive officer has an employment agreement with the Company. The employment agreements renew annually on April 1 for one-year terms, unless either party gives timely notice of non-renewal.

As part of our goal to attract and retain our executive officers, such employment agreements provide that if the Company terminates the employee's employment before a Change in Control (as defined in the agreement) other than for Cause (as defined in the agreement), the employee will receive severance pay consisting of six months' salary continuation and six months of COBRA payments, provided that the severance pay will end if the employee secures other employment. If the Company terminates the employee's employment other than for Cause within 12 months after a Change in Control, or if the employee resigns for Good Reason (as defined in the agreement) within 12 months after a Change in Control, the employee will receive severance pay consisting of a lump sum payment equal to one year's salary, and will also receive 12 months of COBRA payments. The purpose of the severance arrangements is to minimize the uncertainty and distraction caused by bank acquisitions, and to allow our executive officers to focus on performance by providing transition assistance if we are acquired or if there is a change in control.

The employment agreements provide for a general release from the employee as a condition to eligibility for severance pay. The employment agreements also provide that to be eligible for severance pay the employee must comply with confidentiality requirements and 12-month non-solicitation and non-competition commitments included in the employment agreements.

Inter-Relationship of Elements of Compensation Packages

The various elements of the compensation package are not inter-related. There is no significant interplay of the various elements of total compensation between each other. While the Compensation & Governance Committee may recommend, and the Board has discretion to make exceptions to any compensation or bonus payouts under existing plans, the Compensation & Governance Committee has not recommended, and the Board has not approved, any exceptions to the plans with regard to any named executive officer.

Perquisites

We offer minor perquisites to some executive officers, none of which have an annual aggregate incremental cost to us of more than $10,000 per executive.

Limitations on Executive Compensation

Exit from TARP Capital Purchase Program

On June 19, 2012, the United States Department of the Treasury sold all 20,600 shares of the Company's Fixed Rate Cumulative Perpetual Preferred Stock, Series A, Liquidation Preference Amount $1,000 per share ("Preferred Shares") in a modified dutch auction. On July 18, 2012, the Company repurchased from Treasury for $38,000 a Warrant to purchase 311,492 shares of Company common stock. The Company issued the Preferred Shares and Warrant to Treasury in connection with the Company's participation in the TARP Capital Purchase Program.

As a result of these transactions, the Company no longer has any obligation to Treasury in connection with the TARP Capital Purchase Program and the Company is no longer subject to certain requirements of the Emergency Economic Stabilization Act of 2008, as amended by the American Recovery and Reinvestment Act of 2009, leaving the Company with greater flexibility to manage its business and affairs and eliminating the management time and expenses which were required to comply with these provisions.

Section 162(m) of the Internal Revenue Code generally disallows a tax deduction to public companies participating in the CPP for taxable compensation in excess of $500,000 paid to their chief executive officer or certain other highly compensated officers. Qualifying performance-based compensation is not subject to the deduction limitation if certain requirements are met. We consider the impact of Section 162(m) when structuring the performance based portion of our executive compensation, but Section 162(m) is not a dispositive consideration. No compensation was non-deductible because of Section 162(m) in 2011, and we do not expect any compensation to be non-deductible because of Section 162(m) in 2012.

Other Limitations

Section 162(m) of the Internal Revenue Code generally disallows a tax deduction to public companies for taxable compensation in excess of $1,000,000 paid to their chief executive officer or certain other highly compensated officers. Qualifying performance-based compensation is not subject to the deduction limitation if certain requirements are met. We consider the impact of Section 162(m) when structuring the performance based portion of our executive compensation, but Section 162(m) is not a dispositive consideration. No compensation was non-deductible because of Section 162(m) in 2012, and we do not expect any compensation to be non-deductible because of Section 162(m) in 2013.

Pursuant to employment agreements entered into with each named executive officer, United may recover or "claw back" from named executive officers any bonus or incentive compensation based on statements of earnings, revenues, gains or other criteria that are later found to be materially inaccurate. It is anticipated that actions to be taken under such circumstances would be determined by the Compensation & Governance Committee.

Stock Ownership Guidelines

We believe that stock ownership by our executive officers is the clearest, most direct way to align their interests with those of our stockholders and that, by holding an equity position in the Company, executive officers demonstrate their commitment to and belief in the long-term profitability of the Company. Accordingly, guidelines for stock ownership by executive officers were adopted in 2008. As of December 31, 2012, all of the named executive officers had stock ownership in compliance with the stock ownership guidelines. We currently have no policies regarding hedging the economic risk of any ownership of our common stock.

The following table sets forth information concerning the compensation earned by each person who served as Chief Executive Officer during 2012 and the two most highly compensated executive officers other than the Chief Executive Officer during 2012.

Summary Compensation Table

|

Name and Principal Position

|

Year

|

Salary (1)

|

Option Awards (2)

|

Stock Awards (3)

|

Non-Equity Incentive Comp (4)

|

All Other Compensation (5)

|

Total Compensation

|

||||||||||||||||||

|

Robert K. Chapman,

President and Chief Executive Officer

|

2012

|

$

|

274,615

|

$

|

0

|

$

|

38,280

|

$

|

0

|

$

|

21,000

|

$

|

333,895

|

||||||||||||

|

2011

|

267,692

|

0

|

44,976

|

0

|

20,300

|

332,968

|

|||||||||||||||||||

|

2010

|

260,000

|

0

|

0

|

0

|

10,500

|

270,500

|

|||||||||||||||||||

|

Randal J. Rabe, Executive Vice President

and Chief Financial Officer

|

2012

|

$

|

205,846

|

$

|

0

|

$

|

19,140

|

$

|

0

|

$

|

12,259

|

$

|

237,245

|

||||||||||||

|

2011

|

199,231

|

0

|

22,488

|

0

|

11,694

|

233,413

|

|||||||||||||||||||

|

2010

|

190,000

|

0

|

0

|

0

|

3,725

|

193,725

|

|||||||||||||||||||

|

Todd C. Clark,

Executive Vice President

|

2012

|

$

|

205,846

|

$

|

0

|

$

|

19,140

|

$

|

0

|

$

|

10,659

|

$

|

235,645

|

||||||||||||

|

2011

|

200,385

|

0

|

22,488

|

0

|

10,201

|

233,074

|

|||||||||||||||||||

|

2010

|

195,000

|

0

|

0

|

0

|

2,400

|

197,400

|

|||||||||||||||||||

|

(1)

|

Salary amounts include amounts deferred under the Company's 401(k) plan.

|

|

(2)

|

Amounts reflect the grant date fair value computed in accordance with FASB ASC Topic 718. Amounts include awards of stock options. Further information regarding grant valuation is contained in Note 15 of the Notes to Consolidated Financial Statements.

|

|

(3)

|

Amounts reflect the grant date fair value computed in accordance with FASB ASC Topic 718. Amounts include awards of restricted stock, RSUs and SOSARs. Further information regarding grant valuation is contained in Note 15 of the Notes to Consolidated Financial Statements.

|

|

(4)

|

"Non-Equity Incentive Compensation" includes amounts paid under the Management Committee Incentive Compensation Plan and as a profit-sharing contribution under the Company's 401(k) plan as further described in the "Compensation Discussion and Analysis" section of this Proxy Statement. Detail is shown in the table below.

|

|

(5)

|

"All Other Compensation" includes matching contributions made by us under our 401(k) plan and life insurance premiums paid by the Company for the benefit of the named executive officers. Detail is shown in the table below.

|

|

|

Name

|

Year

|

Management Committee Incentive Pay

|

401(k) Profit Sharing

|

Total Non-Equity Incentive Pay

|

401(k) Match Contributions (a)

|

Life Insurance Premiums

|

Total Other Compensation

|

||||||||||||||||||

|

|

Chapman

|

2012

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

10,000

|

$

|

11,000

|

$

|

21,000

|

||||||||||||

|

|

|

2011

|

0

|

0

|

0

|

9,800

|

10,500

|

20,300

|

||||||||||||||||||

|

|

|

2010

|

0

|

0

|

0

|

0

|

10,500

|

10,500

|

||||||||||||||||||

|

|

Rabe

|

2012

|

$

|

0

|

$

|

0

|

$

|

0

|

$

|

8,234

|

$

|

4,025

|

$

|

12,259

|

||||||||||||

|

|

|

2011

|

0

|

0

|

0

|

7,969

|

3,725

|

11,694

|

||||||||||||||||||

|

|

|

2010

|

0

|

0

|