Table of Contents

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON DECEMBER 29, 2011

File Nos. 002-98772

811-04347

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 |

¨ | |||

| Pre-Effective Amendment No. |

¨ | |||

| Post-Effective Amendment No. 156 |

x | |||

REGISTRATION STATEMENT

UNDER

THE INVESTMENT COMPANY ACT OF 1940

| Amendment No. 196 | x |

GMO TRUST

(Exact Name of Registrant as Specified in Charter)

40 Rowes Wharf, Boston, Massachusetts 02110

(Address of principal executive offices)

617-330-7500

(Registrant’s telephone number, including area code)

with a copy to:

| J.B. Kittredge, Esq. GMO Trust 40 Rowes Wharf Boston, Massachusetts 02110 |

Thomas R. Hiller, Esq. | |||

| Ropes & Gray LLP Prudential Tower 800 Boylston Street Boston, Massachusetts 02199 | ||||

| (Name and address of agents for service) |

It is proposed that this filing will become effective:

| ¨ | Immediately upon filing pursuant to paragraph (b), or |

| x | On January 1, 2012, pursuant to paragraph (b), or |

| ¨ | 60 days after filing pursuant to paragraph (a)(1), or |

| ¨ | On , pursuant to paragraph (a)(1), or |

| ¨ | 75 days after filing pursuant to paragraph (a)(2) of Rule 485. |

This filing relates solely to Class III and Class IV shares of GMO Benchmark-Free Allocation Fund. No information contained herein is intended to amend or supersede any prior filing relating to any other series of the Registrant.

Table of Contents

GMO Trust

Prospectus

January 1, 2012

| n | GMO Benchmark-Free Allocation Fund |

Class III: GBMFX

Class IV: —

n Shares of the Fund described in this Prospectus may not be available for purchase in all states. This Prospectus does not offer shares in any state where they may not lawfully be offered.

Grantham, Mayo, Van Otterloo & Co. LLC

40 Rowes Wharf • Boston, Massachusetts 02110

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

| Page | ||||

| 1 | ||||

| ADDITIONAL INFORMATION ABOUT THE FUND’S INVESTMENT STRATEGIES, RISKS, AND EXPENSES |

8 | |||

| 11 | ||||

| 24 | ||||

| 25 | ||||

| 28 | ||||

| 28 | ||||

| 31 | ||||

| 34 | ||||

| 35 | ||||

| 37 | ||||

| 41 | ||||

| 42 | ||||

| 49 | ||||

| back cover | ||||

| back cover | ||||

| back cover | ||||

i

Table of Contents

GMO Benchmark-Free Allocation Fund

Investment objective

The Fund seeks a positive total return.

Fees and expenses

The tables below describe the fees and expenses that you may pay for each class of shares if you buy and hold shares of the Fund.

Shareholder fees

(fees paid directly from your investment)

| Class III | Class IV | |||||||

| Purchase premium (as a percentage of amount invested) |

0.09 | % | 0.09 | % | ||||

| Redemption fee (as a percentage of amount redeemed) |

0.09 | % | 0.09 | % | ||||

Annual Fund operating expenses

(expenses that you pay each year as a percentage of the value of your investment)

| Class III | Class IV | |||||||

| Management fee |

0.65 | % | 0.65 | % | ||||

| Shareholder service fee |

0.15 | % | 0.10 | % | ||||

| Other expenses |

0.02 | % | 0.02 | % | ||||

| Acquired fund fees and expenses (underlying fund expenses) |

0.57 | %1 | 0.57 | %1 | ||||

| Total annual operating expenses |

1.39 | % | 1.34 | % | ||||

| Expense reimbursement/waiver |

(0.50 | %)2 | (0.50 | %)2 | ||||

| Total annual operating expenses after expense reimbursement/waiver (Fund and underlying fund expenses) |

0.89 | % | 0.84 | % | ||||

| 1 | Restated as of June 2011. The amount includes purchase premiums and redemption fees of the underlying GMO Funds. |

| 2 | The Manager has agreed to waive and/or reduce the Fund’s management and shareholder service fees in order to offset the management and shareholder service fees charged by the underlying GMO Funds in which the Fund invests. In addition, the Manager has agreed to reimburse the Fund for certain of its operational expenses. |

-1-

Table of Contents

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same as those shown in the table. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| If you sell your shares | If you do not sell your shares | |||||||||||||||||||||||||||||||

| 1 Year* | 3 Years** | 5 Years** | 10 Years** | 1 Year* | 3 Years** | 5 Years** | 10 Years** | |||||||||||||||||||||||||

| Class III |

$ | 109 | $ | 350 | $ | 610 | $ | 1,353 | $ | 100 | $ | 340 | $ | 599 | $ | 1,340 | ||||||||||||||||

| Class IV |

$ | 104 | $ | 334 | $ | 583 | $ | 1,295 | $ | 95 | $ | 324 | $ | 572 | $ | 1,282 | ||||||||||||||||

| * | After expense reimbursements/waivers noted in expense table. |

| ** | Reflects fee reductions set forth in the Fund’s management agreement and servicing and supplemental support agreement. |

Portfolio turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in Annual Fund operating expenses or in the Example, affect the Fund’s performance. During its fiscal year ended February 28, 2011, the Fund’s portfolio turnover rate (excluding short-term investments) was 19% of the average value of its portfolio.

Principal investment strategies

The Fund is a fund of funds and invests primarily in shares of other GMO Funds, which may include the International Equity Funds, the U.S. Equity Funds, the Fixed Income Funds, GMO Alpha Only Fund, GMO Alternative Asset Opportunity Fund, GMO Debt Opportunities Fund, GMO High Quality Short-Duration Bond Fund, GMO Special Situations Fund, GMO World Opportunity Overlay Fund and GMO Implementation Fund (collectively, the “underlying Funds”), each of which is described in a separate prospectus or private placement memorandum. In addition, the Fund may invest in securities directly.

The Fund implements its strategy by allocating its assets among asset classes represented by the underlying Funds (e.g., foreign equity, U.S. equity, emerging country equity, emerging country debt, foreign fixed income, U.S. fixed income and commodities). The Fund is not restricted in its exposure to any particular asset class, and at times may be substantially invested in underlying Funds that primarily invest in a single asset class (e.g., GMO Real Estate Fund and the Fixed Income Funds). In addition, the Fund is not restricted in its exposure to any particular market and may invest in securities of companies of any market capitalization. Although the Fund generally will have exposure to both emerging countries and developed countries, including the U.S., at times, it also may have substantial exposure to a particular country or type of country (e.g., emerging countries). The Fund may have indirect exposure to derivatives and short sales through its investment in the underlying Funds. The Fund does not have a particular securities market index as a benchmark and does not seek to outperform a particular index or blend of indices (i.e., the Fund seeks positive return, not “relative” return).

The Manager uses multi-year forecasts of relative value and risk among asset classes (e.g., foreign equity, U.S. equity, emerging country equity, emerging country debt, foreign fixed income, U.S. fixed income and commodities) to select the underlying Funds in which the Fund invests and to decide

-2-

Table of Contents

how much to invest in each. The Manager changes the Fund’s holdings of underlying Funds in response to changes in its investment outlook and market valuations and may use redemption/purchase activity to rebalance the Fund’s investments. The Manager’s ability to shift investments among the underlying Funds is not subject to any limits. The Fund may invest substantially all of its assets in a few underlying Funds that primarily invest in the same asset class and may, at times, also invest a substantial portion of its assets in a single underlying Fund. The Fund also reserves the right to invest directly in asset classes, or to adjust its exposure to asset classes, through direct investments.

Prior to January 1, 2012, the Fund served predominantly as the principal component of a broader real return strategy, and the Fund’s investors were predominantly separate account clients of the Manager. The Fund was also offered on a stand-alone basis to the Manager’s partners and employees. Beginning on January 1, 2012, the Fund will be managed as a stand-alone investment strategy. The Manager expects that the Fund’s investment exposures will not differ significantly from the allocations the Fund would have had as a component of the broader real return, although the Fund will likely allocate a greater percentage of its assets to strategies that have cash-like benchmarks.

For cash management purposes, the Fund may invest in GMO U.S. Treasury Fund (“U.S. Treasury Fund”), a GMO Fund described in a separate prospectus, and unaffiliated money market funds.

Principal risks of investing in the Fund

The value of the Fund’s shares changes with the value of the Fund’s investments. Many factors can affect this value, and you may lose money by investing in the Fund. References to investments include those held directly by the Fund and indirectly through the Fund’s investments in the underlying Funds. Some of the underlying Funds are non-diversified investment companies under the Investment Company Act of 1940, as amended, and therefore a decline in the market value of a particular security held by those Funds may affect their performance more than if they were diversified. The principal risks of investing in the Fund are summarized below. For a more complete discussion of these risks, including those risks to which the Fund is exposed as a result of its investments in the underlying Funds, see “Description of Principal Risks.”

| • | Market Risk – Equity Securities – The market value of equity investments may decline due to factors affecting the issuing companies, their industries, or the economy and equity markets generally. If an underlying Fund purchases equity investments at a discount from their value as determined by the Manager, the Fund runs the risk that the market prices of these investments will not increase to that value for a variety of reasons, one of which may be the Manager’s overestimation of the value of those investments. An underlying Fund also may purchase equity investments that typically trade at higher multiples of current earnings than other securities, and the market values of these investments often are more sensitive to changes in future earnings expectations than those other securities. Declines in stock market prices generally are likely to reduce the net asset value of the Fund’s shares. |

| • | Foreign Investment Risk – The market prices of many foreign securities fluctuate more than those of U.S. securities. Many foreign markets are less stable, smaller, less liquid and less regulated than U.S. markets, and the cost of trading in those markets often is higher than in U.S. markets. Foreign portfolio transactions generally involve higher commission rates, transfer taxes and custodial costs than similar transactions in the U.S. In addition, the Fund may be subject to foreign taxes on capital gains or other income payable on foreign securities, on transactions in those securities and on the repatriation of proceeds generated from those securities. Also, many foreign markets require a license for the Fund to invest directly in those markets, and the Fund is subject to the risk that it could not invest if its license were terminated or suspended. In some foreign markets, prevailing custody and trade settlement practices (e.g., the requirement to pay for securities prior to receipt) expose the Fund to credit and other risks with respect to participating brokers, custodians, clearing banks or other clearing agents, escrow agents and issuers. Further, adverse changes in investment regulations, capital |

-3-

Table of Contents

| requirements or exchange controls could adversely affect the value of the Fund’s investments. These and other risks (e.g., nationalization, expropriation or other confiscation of assets of foreign issuers) tend to be greater for investments in companies tied economically to emerging countries, the economies of which tend to be more volatile than the economies of developed countries. |

| • | Market Risk — Fixed Income Securities – Typically, the market value of fixed income securities will decline during periods of rising interest rates and widening of credit spreads. |

| • | Market Risk – Asset-Backed Securities – Asset-backed securities are subject to severe credit downgrades, illiquidity, defaults and declines in market value. |

| • | Smaller Company Risk – Smaller companies may have limited product lines, markets or financial resources, may lack the competitive strength of larger companies, or may lack managers with experience or depend on a few key employees. The securities of companies with smaller market capitalizations often are less widely held and trade less frequently and in lesser quantities, and their market prices often fluctuate more, than the securities of companies with larger market capitalization. |

| • | Liquidity Risk – Low trading volume, lack of a market maker, large size of position or legal restrictions may limit or prevent the Fund or an underlying Fund from selling particular securities or unwinding derivative positions at desirable prices. The more less-liquid securities the Fund holds, the more likely it is to honor a redemption request in-kind. |

| • | Derivatives Risk – The use of derivatives involves the risk that their value may not move as expected relative to the value of the relevant underlying assets, rates or indices. Derivatives also present other Fund risks, including market risk, liquidity risk, currency risk and counterparty risk. |

| • | Currency Risk – Fluctuations in exchange rates can adversely affect the market value of foreign currency holdings and investments denominated in foreign currencies. |

| • | Fund of Funds Risk – The Fund is indirectly exposed to all of the risks of an investment in the underlying Funds, including the risk that the underlying Funds in which it invests do not perform as expected. |

| • | Management and Operational Risk – The Fund relies on GMO’s ability to achieve its investment objective by effectively implementing its investment approach. The Fund runs the risk that GMO’s proprietary investment techniques will fail to produce the desired results. The Fund’s portfolio managers may use quantitative analyses and/or models and any imperfections or limitations in such analyses and/or models could affect the ability of the portfolio managers to implement strategies. By necessity, these analyses and models make simplifying assumptions that limit their efficacy. Models that appear to explain prior market data can fail to predict future market events. Further, the data used in models may be inaccurate and/or it may not include the most recent information about a company or a security. The Fund is also subject to the risk that deficiencies in the Manager’s or another service provider’s internal systems or controls will cause losses for the Fund or impair Fund operations. |

| • | Credit Risk – The Fund runs the risk that the issuer or guarantor of a fixed income security or the obligor of an obligation underlying an asset-backed security will be unable or unwilling to satisfy its obligations to pay principal or interest payments or to otherwise honor its obligations. The market value of a fixed income security normally will decline as a result of the issuer’s failure to meet its payment obligations or the market’s expectation of a default, which may result from the downgrading of the issuer’s credit rating. Below investment grade securities have speculative characteristics, and |

| changes in economic conditions or other circumstances are more likely to impair the capacity of issuers to make principal and interest payments than is the case with issuers of investment grade securities. |

| • | Counterparty Risk – The Fund runs the risk that the counterparty to an over-the-counter (OTC) derivatives contract or a borrower of the Fund’s securities will be unable or unwilling to make timely settlement payments or otherwise honor its obligations. |

-4-

Table of Contents

| • | Commodities Risk – To the extent an underlying Fund has exposure to global commodity markets, the value of its shares is affected by factors particular to the commodity markets and may fluctuate more than the value of shares of a fund with a broader range of investments. |

| • | Leveraging Risk – The use of reverse repurchase agreements and other derivatives and securities lending may cause the Fund’s portfolio to be leveraged. Leverage increases the Fund’s portfolio losses when the value of its investments decline. |

| • | Real Estate Risk – To the extent an underlying Fund concentrates its assets in real estate-related investments, the value of its portfolio is subject to factors affecting the real estate industry and may fluctuate more than the value of a portfolio that consists of securities of companies in a broader range of industries. |

| • | Short Sales Risk – The Fund runs the risk that an underlying Fund’s loss on a short sale of securities that the underlying Fund does not own is unlimited. |

| • | Natural Resources Risk – To the extent an underlying Fund concentrates its assets in the natural resources sector, the value of its portfolio is subject to factors affecting the natural resources industry and may fluctuate more than the value of a portfolio that consists of securities of companies in a broader range of industries. |

| • | Focused Investment Risk – Focusing investments in countries, regions, sectors or companies or in industries with high positive correlations to one another creates additional risk. |

| • | Market Disruption and Geopolitical Risk – Geopolitical and other events may disrupt securities markets and adversely affect global economies and markets. Those events as well as other changes in foreign and domestic economic and political conditions could adversely affect the value of the Fund’s investments. |

| • | Large Shareholder Risk – To the extent that shares of the Fund are held by large shareholders (e.g., institutional investors), the Fund is subject to the risk that these shareholders will disrupt the Fund’s operations by purchasing or redeeming Fund shares in large amounts and/or on a frequent basis. |

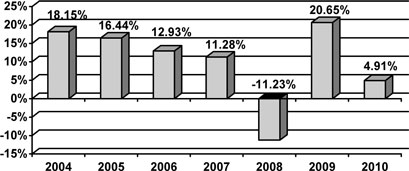

Performance

The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s annual total returns from year to year for the periods indicated and by comparing the Fund’s average annual total returns for different calendar periods with those of a broad-based index and the Consumer Price Index. Purchase premiums and redemption fees are not reflected in the bar chart, but are reflected in the table; as a result, the returns in the table are lower than the returns in the bar chart. Returns in the table reflect current purchase premiums and redemption fees. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on your tax situation and may differ from those shown. After-tax returns shown are not relevant if you are tax-exempt or if you hold your Fund shares through tax-deferred arrangements (such as a 401(k) plan or individual retirement account). Past performance (before and after taxes) is not an indication of future performance.

-5-

Table of Contents

Annual Total Returns/Class III Shares*

Years Ending December 31

Highest Quarter: 9.19% (2Q2009)

Lowest Quarter: -6.90% (4Q2008)

Year-to-Date (as of 3/31/11): 1.92%

| * | The returns are for Class III shares of the Fund under the Fund’s prior fee arrangement. Under the Fund’s current fee arrangement, the returns would have been lower. |

Average Annual Total Returns*

Periods Ending December 31, 2010

| 1 Year | 5 Years | 10 Years | Inception | |||||||||||

| Class III |

7/23/03 | |||||||||||||

| Return Before Taxes |

4.72 | % | 7.11 | % | N/A | 12.00 | % | |||||||

| Return After Taxes on Distributions |

4.19 | % | 4.42 | % | N/A | 9.27 | % | |||||||

| Return After Taxes on Distributions and Sale of Fund Shares |

3.14 | % | 4.86 | % | N/A | 9.18 | % | |||||||

| MSCI World Index (returns reflect no deduction for fees or expenses, but are net of withholding tax on dividend reinvestments) |

11.76 | % | 2.43 | % | N/A | 7.14 | % | |||||||

| Consumer Price Index (reflects no deduction for fees, expenses, or taxes) |

1.25 | % | 2.18 | % | N/A | 2.47 | % | |||||||

| * | The returns are for Class III shares of the Fund under the Fund’s prior fee arrangement. Under the Fund’s current fee arrangement, the returns would have been lower. |

Management of the Fund

Investment Adviser: Grantham, Mayo, Van Otterloo & Co. LLC

Investment Division and Senior Members of GMO responsible for day-to-day management of the Fund:

| Investment Division |

Senior Member (Length of Service) |

Title | ||

| Asset Allocation |

Ben Inker (since 1996) |

Director, Asset Allocation Division, GMO. |

-6-

Table of Contents

Purchase and sale of Fund shares

Under ordinary circumstances, you may purchase the Fund’s shares directly from GMO Trust (the “Trust”) when the New York Stock Exchange (“NYSE”) is open for business. In addition, certain brokers and agents are authorized to accept purchase and redemption orders on the Fund’s behalf.

Eligibility to purchase Fund shares or different classes of Fund shares depends on the client’s meeting either (i) the minimum “Total Fund Investment,” which includes only a client’s total investment in the Fund, or (ii) the minimum “Total GMO Investment,” both set forth in the table below. No minimum additional investment is required to purchase additional shares of the Fund.

Minimum Investment Criteria for Class Eligibility

| Minimum Total Fund Investment |

Minimum Total GMO Investment | |||

| Class III Shares |

N/A | $10 million | ||

| Class IV Shares |

$125 million | $250 million |

Fund shares are redeemable and, under ordinary circumstances, you may redeem the Fund’s shares when the NYSE is open for business. Redemption requests should be submitted directly to the Trust unless the Fund shares to be redeemed were purchased through a broker or agent, in which case the redemption request should be effected through that broker or agent. For instructions on redeeming shares directly, call the Trust at 1-617-346-7646 or send an e-mail to SHS@GMO.com.

Purchase order forms and redemption requests can be submitted by mail or facsimile (and with respect to purchase order forms, by other form of communication pre-approved by GMO Shareholder Services) to the Trust at:

GMO Trust

c/o Grantham, Mayo, Van Otterloo & Co. LLC

40 Rowes Wharf

Boston, Massachusetts 02110

Facsimile: 1-617-439-4192

Attention: Shareholder Services

Tax information

The Fund normally distributes net investment income and net realized capital gains, if any, to shareholders. These distributions are generally taxable to you as ordinary income or capital gains, unless you are an entity that is exempt from income tax or are investing through a tax-advantaged account. If you are investing through a tax-advantaged account, you may be taxed upon withdrawals from that account.

Financial intermediary compensation

If you purchase shares of the Fund through a broker-dealer, agent or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

-7-

Table of Contents

ADDITIONAL INFORMATION ABOUT THE FUND’S INVESTMENT STRATEGIES,

RISKS, AND EXPENSES

Fund Summary. The preceding section contains a summary of the investment objective, fees and expenses, principal investment strategies, principal risks, management, and other important information for the Fund. The summary is not all-inclusive, and the Fund may make investments, employ strategies, and be exposed to risks that are not described in the summary. More information about the Fund’s investments and strategies is contained in the Statement of Additional Information (“SAI”). See the back cover of this Prospectus for information about how to receive the SAI.

Fundamental Investment Objectives/Policies. The Board of Trustees (“Trustees”) of the Trust may change the Fund’s investment objective or policies without shareholder approval or prior notice unless an objective or policy is identified in this Prospectus or in the SAI as “fundamental.” The Fund does not currently have any investment objectives that are fundamental. There is no guarantee that the Fund will be able to achieve its investment objective.

Tax Consequences and Portfolio Turnover. Unless otherwise specified in this Prospectus or in the SAI, GMO is not obligated to, and generally will not, consider tax consequences when seeking to achieve the Fund’s investment objective (e.g., the Fund may engage in transactions that are not tax efficient for U.S. federal income or other federal, state, local, or non-U.S. tax purposes). Portfolio turnover is not a principal consideration when GMO makes investment decisions for the Fund, and the Fund has not placed any limit on the rate of portfolio turnover and portfolio securities may be sold without regard to the time they have been held. Based on its assessment of market conditions and purchase or redemption requests, GMO may cause the Fund to trade more frequently at some times than at others. High turnover rates may adversely affect the Fund’s performance by generating higher transaction costs. Additionally, portfolio turnover may give rise to additional taxable income for shareholders, including through the realization of capital gains or other types of income that are taxable to Fund shareholders when distributed to them unless the shareholders themselves are exempt from taxation or otherwise investing in the Fund through a tax-advantaged account. If portfolio turnover results in the recognition of short-term capital gains, those gains typically are taxed to shareholders, when distributed to them, at ordinary income tax rates. See “Distributions and Taxes” below for more information about the tax consequences of these types of income.

Certain Definitions. When used in this Prospectus, the term “invest” includes both direct investing and indirect investing and the term “investments” includes both direct investments and indirect investments. For example, the Fund may invest indirectly by investing in another GMO Fund or by investing in derivatives and synthetic instruments. When used in this Prospectus, (i) the terms “equity investments” and “equities” refer to investments (as defined above) in common stocks and other stock-related securities, such as preferred stocks, convertible securities and depositary receipts, (ii) the term “total return” includes capital appreciation and income, and (iii) the term “emerging countries” means the world’s less developed countries.

For purposes of this Prospectus, the terms “fixed income securities” and “bonds” include (i) obligations of an issuer to make payments of principal and/or interest (whether fixed or variable) on future dates and (ii) synthetic debt instruments created by the Manager by using derivatives (e.g., a futures contract, swap contract, currency forward or option). In addition, (a) sovereign debt means fixed income securities issued or guaranteed by a government or a governmental agency or political subdivision, or synthetic sovereign debt and (b) the term “duration” is defined as the weighted measure of interest rate sensitivity of a fixed income security.

For purposes of this Prospectus, the term “investment grade” refers to a rating of Baa3/P-2 or better given by Moody’s Investors Service, Inc. (“Moody’s”) or BBB-/A-2 or better given by Standard &

-8-

Table of Contents

Poor’s Ratings Services (“S&P”) to a particular fixed income security/commercial paper, and the term “below investment grade” refers to any rating below Baa3/P-2 given by Moody’s or below BBB-/A-2 given by S&P to a particular fixed income security/commercial paper. Fixed income securities rated below investment grade are also known as high yield or “junk” bonds. In addition, in this Prospectus, investment grade securities/commercial paper that are given a rating of Aa/P-1 or better by Moody’s or AA/A-1 or better by S&P are referred to as “high quality.” Securities referred to as investment grade, below investment grade, or high quality include not only securities rated by Moody’s and/or S&P, but also unrated securities that the Manager determines have credit qualities comparable to securities rated by Moody’s or S&P as investment grade, below investment grade, or high quality, as applicable.

When used in this Prospectus, references to the U.S. Equity Funds, International Equity Funds, and/or Fixed Income Funds include the GMO Funds listed below:

| U.S. Equity Funds |

Fixed Income Funds | |

| —Quality Fund* |

—Asset Allocation Bond Fund | |

| —Real Estate Fund |

—Asset Allocation International Bond Fund | |

| —U.S. Core Equity Fund |

—Core Plus Bond Fund | |

| —U.S. Growth Fund |

—Currency Hedged International Bond Fund | |

| —U.S. Intrinsic Value Fund |

—Domestic Bond Fund | |

| —U.S. Small/Mid Cap Growth Fund** |

—Emerging Country Debt Fund | |

| —U.S. Small/Mid Cap Value Fund*** |

—Global Bond Fund | |

| —Inflation Indexed Plus Bond Fund | ||

| International Equity Funds |

—International Bond Fund | |

| —Asset Allocation International Small Companies Fund |

—Short-Duration Collateral Fund | |

| —Currency Hedged International Equity Fund |

—Short-Duration Collateral Share Fund | |

| —Developed World Stock Fund |

—Short-Duration Investment Fund | |

| —Emerging Markets Fund |

—Strategic Fixed Income Fund | |

| —Emerging Domestic Opportunities Fund |

—U.S. Treasury Fund | |

| —Flexible Equities Fund |

||

| —Global Focused Equity Fund |

||

| —International Core Equity Fund |

||

| —International Growth Equity Fund |

||

| —International Intrinsic Value Fund |

||

| —International Intrinsic Value Extended Markets Fund |

||

| —International Large/Mid Cap Value Fund |

||

| —International Small Companies Fund |

||

| —Resources Fund |

||

| * | Although Quality Fund is categorized as a “U.S. Equity Fund,” Quality Fund also invests in non-U.S. equities. |

| ** | It is expected that GMO U.S. Small/Mid Cap Growth Fund will be liquidated on or about January 31, 2012. |

| *** | Effective January 16, 2012, GMO U.S. Small/Mid Cap Value Fund is renamed “GMO U.S. Small/Mid Cap Fund.” |

Investments in Unaffiliated Money Market Funds and GMO U.S. Treasury Fund. For cash management purposes, the Fund may invest in unaffiliated money market funds and also may invest in GMO U.S. Treasury Fund, a GMO Fund described in a separate prospectus.

-9-

Table of Contents

Fee and Expense Information. The following paragraphs contain additional information about the fee and expense information included in the Fund Summary.

Annual Fund Operating Expenses – Other Expenses and Acquired Fund Fees and Expenses. The amount listed under “Other expenses” in the “Annual Fund operating expenses” table included in the Fund Summary generally reflects direct expenses associated with an investment in the Fund for the fiscal year ended February 28, 2011. The Fund may invest in certain other funds of the Trust (each fund of the Trust, including the Fund, a “GMO Fund,” and collectively, the “GMO Funds”), and certain other pooled investment vehicles (“underlying funds”), and the indirect net expenses associated with the Fund’s investment in underlying funds (i.e., “acquired fund fees and expenses”) are reflected in the “Annual Fund operating expenses” table under “Acquired fund fees and expenses.” Acquired fund fees and expenses do not include expenses associated with investments in the securities of unaffiliated issuers unless those issuers hold themselves out to be investment companies. Acquired fund fees and expenses are generally based on expenses incurred by the Fund for the fiscal year ended February 28, 2011, and actual indirect expenses will vary depending on the particular underlying funds in which the Fund invests.

Fee and Expense Example. The expense example under “Example” included in the Fund Summary assumes that all dividends and distributions are reinvested.

Temporary Defensive Positions. The Fund may take temporary defensive positions. To the extent the Fund takes a temporary defensive position, it may not achieve its investment objective.

Fund Codes. See “Fund Codes” on the inside back cover of this Prospectus for information regarding the Fund’s ticker, news-media symbol, and CUSIP number.

This Prospectus does not offer shares in any state where they may not lawfully be offered.

-10-

Table of Contents

DESCRIPTION OF PRINCIPAL RISKS

Investing in mutual funds involves many risks, and factors that may affect the Fund’s portfolio as a whole, called “principal risks,” are discussed briefly in the Fund’s summary and are summarized in additional detail in this section. The risks of investing in the Fund depend on the types of investments in its portfolio and the investment strategies the Manager employs on its behalf. This section describes the nature of these principal risks and some related risks, but does not describe every potential risk of investing in the Fund. The Fund could be subject to additional risks because of the types of investments it makes and market conditions, which may change over time. The SAI includes more information about the Fund and its investments.

Because the Fund invests in other GMO Funds and other investment companies (as indicated under “Principal Investment Strategies” in the Fund’s summary), it is exposed to all the risks to which the underlying funds in which it invests are exposed. Therefore, unless otherwise noted, the principal risks summarized below include both direct and indirect principal risks of the Fund, and, as indicated in the “Additional Information About the Fund’s Investment Strategies, Risks, and Expenses” section of this Prospectus, references in this section to investments made by the Fund include those made both directly by the Fund and indirectly by the Fund through other GMO Funds and other investment companies. Some of the underlying GMO Funds are non-diversified investment companies under the Investment Company Act of 1940, as amended (the “1940 Act”), and therefore a decline in the market value of a particular security held by those GMO Funds may affect their performance more than if they were diversified.

The Fund, by itself, generally is not a complete investment program but rather is intended to serve as part of a diversified portfolio of investments. An investment in the Fund is not a bank deposit and, therefore, is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

• MARKET RISK. The Fund is subject to market risk, which is the risk that the market value of its holdings will decline. Market risks include:

Equity Securities Risk. The Fund runs the risk that the market value of its equity investments will decline. The market value of an equity investment may decline for reasons that directly relate to the issuing company, such as management performance, financial leverage and reduced demand for its goods or services. It also may decline due to factors that affect a particular industry, such as a decline in demand, labor or raw material shortages, increased production costs, regulation, or competitive industry conditions. In addition, market value may decline as a result of general market conditions that are not specifically related to a company or industry, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. Equity investments generally have greater price volatility than fixed-income and other investments with a scheduled stream of payments, and the market price of equity investments is more susceptible to moving up or down in a rapid or unpredictable manner.

The Fund may invest a substantial portion of its assets in equities and, as described under Additional Information About the Fund’s Investment Strategies, Risks, and Expenses — Temporary Defensive Positions,” generally does not take temporary defensive positions. As a result, declines in stock market prices generally are likely to reduce the net asset values of the Fund’s shares.

If the Fund purchases equity investments at a discount from their value as determined by the Manager, the Fund runs the risk that the market prices of these investments will not increase to that value for a variety of reasons, one of which may be the Manager’s overestimation of the value of those investments.

-11-

Table of Contents

Equity investments trading at higher multiples of current earnings than other securities have market values that often are more sensitive to changes in future earnings expectations than other securities. At times when the market is concerned that these expectations may not be met, the market values of those securities typically fall.

Fixed Income Securities Risk. The Fund’s investments in fixed income securities (including bonds, notes, bills, synthetic debt instruments and asset-backed securities) are subject to various market risks. These risks include, but are not limited to, loss on its investments, lack of liquidity of its investments, and the impact of fluctuating interest rates. During periods of economic uncertainty and change, the market price of the Fund’s investments in below investment grade securities (also known as “junk bonds”) may be particularly volatile. Often junk bonds are subject to greater sensitivity to interest rate and economic changes than higher rated bonds and can be more difficult to value and are more likely to be fair valued (see “Determination of Net Asset Value”), resulting in differences between the values realized on the sale of the investments and the value at which the investments are carried on the books of the Fund. See “Credit Risk” and “Liquidity Risk” below for more information about these risks.

A principal risk of the Fund’s investments in fixed income securities is that an increase in prevailing interest rates will cause the market value of those investments to decline. The risk associated with increases in interest rates (also called “interest rate risk”) is generally greater when the Fund invests in fixed income securities with longer durations and in some cases duration can increase.

The extent to which a fixed income security’s price changes with changes in interest rates is referred to as interest rate duration, which can be measured mathematically or empirically. A longer-maturity investment generally has longer interest rate duration because the investment’s fixed rate is locked in for longer periods of time. Floating-rate or adjustable-rate securities, however, generally have shorter interest rate durations because their interest rates are not fixed but rather float up and down with the level of prevailing interest rates. Conversely, inverse floating-rate securities have durations that move in the opposite direction from short-term interest rates and thus tend to underperform the market for fixed rate securities when interest rates rise but outperform the market when interest rates decline. To the extent the Fund invests in fixed income securities paying no interest, such as zero coupon and principal-only securities, it will be exposed to additional interest rate risk.

The value of inflation indexed bonds (including Inflation-Protected Securities issued by the U.S. Treasury (“TIPS”)) normally changes when real interest rates change. Their value typically will decline during periods of rising real interest rates and increase during periods of declining real interest rates (i.e., nominal interest rate minus inflation). Real interest rates may not fluctuate in the same manner as nominal interest rates. In some interest rate environments, such as when real interest rates are rising faster than nominal interest rates, the value of inflation indexed bonds may decline more than the value of non-inflation indexed (or nominal) fixed income bonds with similar maturities. There can be no assurance that the value of the Fund’s inflation indexed bonds will change in the same proportion as changes in nominal interest rates, and short term increases in inflation may lead to a decline in their value. Moreover, if the index measuring inflation falls, the principal value of inflation indexed bond investments will be adjusted downward, and, consequently, the interest they pay (calculated with respect to a smaller principal amount) will be reduced. The interest payments on these investments cannot be known with certainty. The U.S. government guarantees the repayment of the original bond principal upon maturity (as adjusted for inflation) in the case of TIPS.

Market risk for fixed income securities denominated in foreign currencies is also affected by currency risk. See “Currency Risk” below.

Asset-Backed Securities Risk. Investments in asset-backed securities are subject to all of the market risks for fixed-income securities described above under “Fixed Income Securities Risk” and other

-12-

Table of Contents

market risks. These risks include, but are not limited to, loss on investments, lack of liquidity and impact of fluctuating interest rates.

Funds investing in asset-backed securities are exposed to the risk that these securities experience severe credit downgrades, illiquidity, defaults and declines in market value. These risks are particularly acute during periods of adverse market conditions, such as those that occurred in 2008. Asset-backed securities may be backed by many types of assets, including pools of residential and commercial mortgages, automobile loans, educational loans, home equity loans, or credit-card receivables. They also may be backed by pools of corporate or sovereign bonds, bank loans made to corporations, or a combination of these bonds and loans (commonly referred to as “collateralized debt obligations” or “collateralized loan obligations”) and by the fees earned by service providers. Payment of interest on asset-backed securities and repayment of principal largely depend on the cash flows generated by the assets backing the securities. The market risk of a particular asset-backed security depends on many factors, including the deal structure (e.g., determination as to the amount of underlying assets or other support needed to produce the cash flows necessary to service interest and make principal payments), the quality of the underlying assets and, if any, the level of credit support and the credit quality of the credit-support provider. Asset-backed securities involve risk of loss of principal if obligors of the underlying obligations default and the value of the defaulted obligations exceeds whatever credit support the securities may have. The obligations of issuers (and obligors of underlying assets) also are subject to bankruptcy, insolvency and other laws affecting the rights and remedies of creditors. See “Credit Risk” below for more information about credit risk.

With the deterioration of worldwide economic and liquidity conditions that occurred and became acute in 2008, the markets for asset-backed securities became fractured, and uncertainty about the creditworthiness of those securities (and underlying assets) caused credit spreads (the difference between yields on asset-backed securities and U.S. Government securities) to widen dramatically. Concurrently, systemic risks of the type evidenced by the insolvency of Lehman Brothers and subsequent market disruptions reduced the ability of financial institutions to make markets in many fixed income securities. These events reduced liquidity and contributed to substantial declines in the market value of asset-backed and other fixed income securities. These conditions may occur again. Also, government actions and proposals affecting the terms of underlying home and consumer loans, changes in demand for products (e.g., automobiles) financed by those loans, and the inability of borrowers to refinance existing loans (e.g., sub-prime mortgages) have had, and may continue to have, adverse valuation and liquidity effects on asset-backed securities.

The market value of an asset-backed security may depend on the servicing of its underlying assets and is, therefore, subject to risks associated with the negligence or defalcation of its servicer. In some circumstances, the mishandling of related documentation also may affect the rights of security holders in and to the underlying assets. The insolvency of entities that generate receivables or that utilize the assets may result in a decline in the value of the underlying assets, as well as costs and delays. The obligations underlying asset-backed securities, in particular securities backed by pools of residential and commercial mortgages, also are subject to unscheduled prepayment, and the Fund may be unable to invest prepayments at as high a yield as is provided by the asset-backed security.

The risk of investing in asset-backed securities has increased because performance of the various sectors in which the assets underlying asset-backed securities are concentrated (e.g., auto loans, student loans, sub-prime mortgages, and credit card receivables) has become more highly correlated since the deterioration in worldwide economic and liquidity conditions referred to above. See “Focused Investment Risk” below for more information about risks of investing in correlated sectors. A single financial institution may serve as a trustee for many asset-backed securities. As a result, a disruption in that institution’s business may have a material impact on many investments.

-13-

Table of Contents

• CREDIT RISK. This is the risk that the issuer or guarantor of a fixed income security (including an asset-backed security) will be unable or unwilling to satisfy its obligations to pay principal or interest payments or to otherwise honor its obligations. The market value of a fixed income security normally will decline as a result of the issuer’s failure to meet its payment obligations or the market’s expectation of a default, which may result from the downgrading of the issuer’s credit rating. This risk is particularly acute in environments (like those experienced recently) in which financial services firms are exposed to systemic risks of the type evidenced by the insolvency of Lehman Brothers in 2008 and subsequent market disruptions.

All fixed income securities are subject to credit risk. Financial strength and solvency of an issuer are the primary factors influencing credit risk. The risk varies depending upon whether the issuer is a corporation or domestic or foreign government (or sub-division or instrumentality) and whether the particular security has a priority over other obligations of the issuer in payment of principal and interest and whether it has any collateral backing or credit enhancement. Credit risk may change over the life of a fixed income security. U.S. government securities are subject to varying degrees of credit risk depending upon whether the securities are supported by the full faith and credit of the United States, supported by the ability to borrow from the U.S. Treasury, supported only by the credit of the issuing U.S. government agency, instrumentality, or corporation, or otherwise supported by the United States. For example, issuers of many types of U.S. government securities (e.g., the Federal Home Loan Mortgage Corporation (“Freddie Mac”), Federal National Mortgage Association (“Fannie Mae”), and Federal Home Loan Banks), although chartered or sponsored by Congress, are not funded by Congressional appropriations and their fixed income securities, including mortgage-backed and other asset-backed securities, are neither guaranteed nor insured by the U.S. government. These securities are subject to more credit risk than U.S. government securities that are supported by the full faith and credit of the United States (e.g., U.S. Treasury bonds). Investments in sovereign debt involve the risk that the governmental entities responsible for repayment of the debt may be unable or unwilling to pay interest and repay principal when due.

As noted under “Market Risk — Asset-Backed Securities” above, asset-backed securities may be backed by many types of assets, including pools of residential and commercial mortgages, automobile loans, educational loans, home equity loans and credit-card receivables. Asset-backed securities also may be collateralized by the fees earned by service providers or by pools of corporate or sovereign bonds, bank loans made to corporations, or a combination of these bonds and loans (commonly referred to as “collateralized debt obligations”). Payment of interest on asset-backed securities and repayment of principal largely depend on the cash flows generated by the assets backing the securities. The credit risk of a particular asset-backed security depends on many factors, including the deal structure (e.g., determination as to the amount of underlying assets or other support needed to produce the cash flows necessary to service interest and make principal payments), the quality of the underlying assets, and, if any, the level of credit support and the credit quality of the credit-support provider. See “Market Risk — Asset-Backed Securities” above for more information regarding credit and other risks associated with investments in asset-backed securities.

In some cases, the credit risk of some of the Fund’s fixed income securities are reflected in their credit ratings. Because the Fund invests in fixed income securities, it is also subject to varying degrees of risk that the credit ratings of the securities will be downgraded. However, credit ratings reflect only the opinions of the agencies issuing them, may change less quickly than relevant circumstances and are not absolute guarantees of the quality of the rated securities. Credit ratings agencies have been criticized for issuing credit ratings that did not fully reflect the risks of the rated securities or were not promptly downgraded when the risks increased. The Manager may rely on its own independent analysis of the credit quality and risks associated with individual securities considered for the Fund, rather than relying on ratings agencies or third-party research. The Manager’s capabilities in analyzing credit quality and

-14-

Table of Contents

associated risks for securities in which the Fund invests are particularly important, and there can be no assurance that the Manager will be successful in this regard.

The obligations of issuers also are subject to bankruptcy, insolvency, and other laws affecting the rights and remedies of creditors. The Fund also will be exposed to credit risk on the reference security to the extent it writes protection under credit default swaps. See “Derivatives Risk” below for more information regarding risks associated with the use of credit default swaps.

Credit risk is particularly pronounced for below investment grade securities (i.e., junk bonds), which are defined in this Prospectus under “Additional Information About the Fund’s Investment Strategies, Risks, and Expenses.” The sovereign debt of many foreign governments, including their sub-divisions and instrumentalities, is below investment grade. Many asset-backed securities also are below investment grade. Although offering the potential for higher investment returns, below investment grade securities have speculative characteristics, often are less liquid than higher quality securities, present a greater risk of default and are more susceptible to real or perceived adverse economic and competitive industry conditions. In the event of default of sovereign debt, the Fund may lack recourse against the sovereign issuer involved.

• LIQUIDITY RISK. The effect of liquidity risk is particularly pronounced when low trading volume, lack of a market maker, large size of position, or legal restrictions (including daily price fluctuation limits or “circuit breakers”) limit or prevent the Fund from selling particular securities or unwinding derivative positions at desirable prices. In addition, the more less-liquid securities the Fund holds, the more likely it is to honor a redemption request in-kind. Because the Fund’s principal investment strategies may involve investment in asset-backed securities, emerging country debt securities, securities of companies with smaller market capitalizations or smaller total float-adjusted market capitalizations, foreign securities (in particular emerging market securities), derivatives (in particular over-the-counter (“OTC”) derivatives), and/or securities subject to restrictions on resale, the Fund has increased exposure to liquidity risk. These types of investments can be difficult to value and are more likely to be fair valued (see “Determination of Net Asset Value”), resulting in differences between the values realized on the sale of the investments and the value at which the investments are carried on the books of the Fund. Less liquid securities are more susceptible than other securities to market value declines when markets decline generally.

The Fund is also exposed to liquidity risk when it has an obligation to purchase particular securities (e.g., as a result of entering into reverse repurchase agreements, writing a put, or closing out a short position). Some of the markets, exchanges or securities in which the Fund invests may be less liquid and this would affect the price at which, and the time period in which, the Fund may liquidate positions to meet redemption requests or other funding requirements. Although U.S. Treasury securities have historically been among the most liquid fixed income investments, these securities may become less liquid in the future.

The Fund makes (or may make) investments in emerging market securities that are not widely traded and are sometimes subject to purchase and sale restrictions and/or in securities of companies with smaller market capitalizations that are not widely held and trade less frequently and in lesser quantities than securities of companies with larger market capitalizations.

• SMALLER COMPANY RISK. Market risk and liquidity risk are particularly pronounced for securities of companies with smaller market capitalizations, including small- and mid-cap companies. These companies may have limited product lines, markets or financial resources, may lack the competitive strength of larger companies, or may lack managers with experience or depend on a few key employees. In addition, their securities often are less widely held and trade less frequently and in lesser quantities, and their market prices often fluctuate more, than the securities of companies with larger market capitalizations.

-15-

Table of Contents

• DERIVATIVES RISK. The Fund may invest in derivatives, which are financial contracts whose value depends on, or is derived from, the value of underlying assets, reference rates, or indices. Derivatives include futures, foreign currency contracts, swap contracts, reverse repurchase agreements and other OTC contracts. Derivatives may relate to securities, interest rates, currencies or currency exchange rates, inflation rates, commodities and indices. The SAI contains a description of the various types and uses of derivatives in the Fund’s investment strategies.

The use of derivatives involves risks that are in addition to, and potentially greater than, the risks associated with investing directly in securities and other more traditional assets. In particular, the use of OTC derivatives exposes the Fund to the risk that the counterparty to a derivatives contract will be unable or unwilling to make timely settlement payments or otherwise honor its obligations. OTC derivatives contracts typically can be closed only with the other party to the contract. If the counterparty defaults, the Fund will have contractual remedies but may not be able to enforce them. Because the contract for each OTC derivative is individually negotiated, the counterparty may interpret contractual terms (e.g., the definition of default) differently than the Fund, and if that occurs, the Fund may decide not to pursue its claims against the counterparty in order to avoid incurring the cost and unpredictability of legal proceedings. The Fund, therefore, may be unable to obtain payments the Manager believes are owed under OTC derivatives contracts or those payments may be delayed or made only after the Fund has incurred the costs of litigation.

The Fund may invest in derivatives that do not require the counterparty to post collateral (e.g., foreign currency forwards), that require collateral but that do not provide for the Fund’s security interest in it to be perfected, that require a significant upfront deposit by the Fund unrelated to the derivative’s intrinsic value, or that do not require the collateral to be regularly marked-to-market (e.g., certain OTC derivatives). Even when obligations are required by contract to be collateralized, there is usually a lag between the day the collateral is called for and the day the Fund receives it. When a counterparty’s obligations are not fully secured by collateral, the Fund is exposed to the risk of having limited recourse if the counterparty defaults. The Fund may invest in derivatives with a limited number of counterparties, and events affecting the creditworthiness of any of those counterparties may have a pronounced effect on the Fund. Derivatives risk is particularly acute in environments (like those experienced recently) in which financial services firms are exposed to systemic risks of the type evidenced by the insolvency of Lehman Brothers and subsequent market disruptions. During these periods of market disruptions, the Fund may have a greater need for cash to provide collateral for large swings in its mark-to-market obligations under the derivatives used by the Fund.

Derivatives also present risks described elsewhere in this “Description of Principal Risks” section, including market risk, liquidity risk, currency risk, credit risk and counterparty risk. Many derivatives, in particular OTC derivatives, are complex and their valuation often requires modeling and judgment, which increases the risk of mispricing or improper valuation. The pricing models used by the Fund or its pricing agents may not produce valuations that are consistent with the values realized when OTC derivatives are actually closed out or sold. This valuation risk is more pronounced when the Fund enters into OTC derivatives with specialized terms because the value of those derivatives in some cases is determined only by reference to similar derivatives with more standardized terms. As a result, incorrect valuations may result in increased cash payments to counterparties, undercollateralization and/or errors in the calculation of the Fund’s net asset value.

The Fund’s use of derivatives may not be effective or have the desired results. Moreover, suitable derivatives will not be available in all circumstances. For example, the economic costs of taking some derivative positions may be prohibitive, and if a counterparty or its affiliate is deemed to be an affiliate of the Fund, the Fund will not be permitted to trade with that counterparty. In addition, the Manager may decide not to use derivatives to hedge or otherwise reduce the Fund’s risk exposures, potentially resulting in losses for the Fund.

-16-

Table of Contents

Derivatives also involve the risk that changes in their value may not move as expected relative to the value of the assets, rates or indices they are designed to track. The use of derivatives also may increase the taxes payable by shareholders.

When the Fund uses credit default swaps to obtain synthetic long exposure to a fixed income security such as a debt instrument or index of debt instruments, the Fund is exposed to the risk that it will be required to pay the full notional value of the swap contract in the event of a default.

Swap contracts and other OTC derivatives are highly susceptible to liquidity risk (see “Liquidity Risk” above) and counterparty risk (see “Counterparty Risk” below), and are subject to documentation risks. Because many derivatives have a leverage component (i.e., a notional value in excess of the assets needed to establish and/or maintain the derivative position), adverse changes in the value or level of the underlying asset, rate or index may result in a loss substantially greater than the amount invested in the derivative itself (see “Leveraging Risk” below).

The U.S. government recently enacted legislation that provides for new regulation of the derivatives market, including clearing, margin, reporting and registration requirements. Because the legislation leaves much to rule making, its ultimate impact remains unclear. New regulations could, among other things, restrict the Fund’s ability to engage in derivatives transactions for example, by making certain types of derivatives transactions no longer available to the Fund) and/or increase the costs of such derivatives transactions (for example, by increasing margin or capital requirements), and the Fund may be unable to execute its investment strategy as a result. It is unclear how the regulatory changes will affect counterparty risk.

• FOREIGN INVESTMENT RISK. Because the Fund invests in foreign (non-U.S.) securities, it is subject to additional and more varied risks than funds whose investments are limited to U.S. securities. The securities markets of many foreign countries involve securities of only a limited number of companies in a limited number of industries. As a result, the market prices of many of those securities fluctuate more than those of U.S. securities. In addition, issuers of foreign securities often are not subject to the same degree of regulation as U.S. issuers. Reporting, accounting, custody and auditing standards of foreign countries differ, in some cases significantly, from U.S. standards. Foreign portfolio transactions generally involve higher commission rates, transfer taxes and custodial costs. The Fund may be subject to foreign taxation on realized capital gains, dividends or interest payable on those securities, on transactions in those securities and on the repatriation of proceeds generated from those securities. Transaction-based charges are generally calculated as a percentage of the transaction amount and are paid upon the sale or transfer of portfolio securities subject to such taxes. In addition, some jurisdictions may limit the Fund’s ability to profit from short term trading (as defined in the relevant jurisdiction).

Also, investing in foreign countries exposes the Fund to the risk of nationalization, expropriation or confiscatory taxation of assets of issuers to which the Fund is exposed, adverse changes in investment regulations, capital requirements or exchange controls (which may include suspension of the ability to transfer currency from a country), and adverse political and diplomatic developments that could adversely affect the market value of the Fund’s investments.

In some foreign markets, custody arrangements for securities provide significantly fewer protections than custody arrangements in U.S. markets, and prevailing custody and trade settlement practices (e.g., the requirement to pay for securities prior to receipt) expose the Fund to credit and other risks with respect to participating brokers, custodians, clearing banks or other clearing agents, escrow agents and issuers. Fluctuations in foreign currency exchange rates also will affect the market value of the Fund’s foreign investments (see “Currency Risk” below).

U.S. investors are required to maintain a license to invest directly in many foreign markets. These licenses are often subject to limitations, including maximum investment amounts. Once a license is

-17-

Table of Contents

obtained, the Fund’s ability to continue to invest directly is subject to the risk that the license will be terminated or suspended. If a license is terminated or suspended, the Fund will be required to obtain exposure to the market through the purchase of American Depositary Receipts, Global Depositary Receipts, shares of other funds that are licensed to invest directly, or derivative instruments. The receipt of a foreign license by one of the Manager’s clients may preclude other clients, including the Fund, from obtaining a similar license, and this could limit the Fund’s investment opportunities. In addition, the activities of another of the Manager’s clients could cause the suspension or revocation of a license and thereby limit the Funds’ investment opportunities.

Because the Fund may invest a significant portion of its assets in securities of issuers tied economically to emerging countries, it is subject to greater foreign investment risk than funds investing primarily in more developed foreign countries. The risks of investing in those securities include: greater fluctuations in currency exchange rates; increased risk of default (by both government and private issuers); greater social, economic, and political uncertainty and instability (including the risk of war or natural disaster); increased risk of nationalization, expropriation, or other confiscation of assets of issuers to which the Fund is exposed; greater governmental involvement in the economy; less governmental supervision and regulation of the securities markets and participants in those markets; controls on foreign investment, capital controls and limitations on repatriation of invested capital, dividends, interest and other income and on the Fund’s ability to exchange local currencies for U.S. dollars; inability to purchase and sell investments or otherwise settle security or derivative transactions (i.e., a market freeze); unavailability of currency hedging techniques; differences in, or lack of, auditing and financial reporting standards and resulting unavailability of material information about issuers; slower clearance and settlement; difficulties in obtaining and/or enforcing legal judgments; and significantly smaller market capitalizations of issuers.

• CURRENCY RISK. Currency risk is the risk that fluctuations in exchange rates will adversely affect the market value of the Fund’s investments. Currency risk includes the risk that currencies in which the Fund’s investments are traded and/or in which the Fund receives income, or currencies in which the Fund has taken an active investment position, will decline in value relative to other currencies, in the case of long positions, or increase in value relative to other currencies, in the case of short positions. In the case of hedging positions, currency risk includes the risk that the currency to which the Fund has obtained exposure through hedging declines in value relative to the foreign currency being hedged. In such event, the Fund may realize a loss on the hedging instrument at the same time the Fund is realizing a loss on the currency being hedged. Currency exchange rates can fluctuate significantly for many reasons, including changes in supply and demand in the currency exchange markets, trade balances, actual or perceived changes in interest rates, differences in relative values of similar assets in different currencies, long-term opportunities for investment and capital appreciation, intervention (or the failure to intervene) by U.S. or foreign governments, central banks or supranational agencies such as the International Monetary Fund, and currency or exchange controls or other political and economic developments in the U.S. or abroad. See “Market Disruption and Geopolitical Risk” below.

The Fund may use derivatives to acquire positions in currencies whose value the Manager expects to correlate with the value of currencies the Fund owns, currencies the Manager wants the Fund to own, or currencies the Fund is exposed to through its investments. To the extent the Fund takes overweighted or underweighted currency positions and/or alters the currency exposure of the securities in which it has invested, its currency exposure may differ (in some cases significantly) from the currency exposure of its investments. If the exchange rates of the currencies involved do not move as expected, the Fund could lose money on its holdings of a particular currency and also lose money on the derivative. See also “Foreign Investment Risk” above.

Because the Fund may invest or trade in securities denominated in foreign currencies and may use related derivatives and have foreign currency holdings, it may be adversely affected by changes in the exchange rates of foreign currencies. In addition, some currencies are illiquid (e.g., some emerging

-18-

Table of Contents

country currencies), and the Fund may not be able to convert these currencies into U.S. dollars, in which case the Manager may decide to purchase U.S. dollars in a parallel market where the exchange rate is materially and adversely different. Exchange rates for many currencies (e.g., some emerging country currencies) are particularly affected by exchange control regulations.

Derivative transactions in foreign currencies (such as futures, forwards, options and swaps) may involve leveraging risk in addition to currency risk, as described below under “Leveraging Risk.” In addition, the obligations of counterparties in currency derivative transactions are often not secured by collateral, which increases counterparty risk (see “Counterparty Risk” below).

• FOCUSED INVESTMENT RISK. Funds whose investments are focused in particular countries, regions, sectors, or companies or in industries with high positive correlations to one another (e.g., different industries within broad sectors, such as technology or financial services) are subject to greater overall risk than funds whose investments are more diversified. To the extent the Fund invests in the securities of a limited number of issuers, it is particularly exposed to adverse developments affecting those issuers, and a decline in the market value of a particular security held by the Fund may affect the Fund’s performance more than if the Fund invested in the securities of a larger number of issuers.

To the extent the Fund focuses its investments in a particular type of security or sector, or in securities of companies in a particular industry, it is vulnerable to events affecting those securities, sectors or companies. Securities, sectors or companies that share common characteristics are often subject to similar business risks and regulatory burdens, and often react similarly to specific economic, market, political or other developments. See also “Real Estate Risk” below.

Similarly, to the extent the Fund invests a significant portion of its assets in investments tied economically to a particular geographic region, foreign country or particular market (e.g., emerging markets), it has more exposure to regional and country economic risks than funds making foreign investments throughout the world. The political and economic prospects of one country or group of countries within the same geographic region may affect other countries in that region. In addition, a recession, debt crisis, or decline in currency valuation in one country within a region can spread to other countries in that region. Furthermore, to the extent the Fund invests in the debt or equity securities of companies located in a particular geographic region or foreign country, it is particularly vulnerable to events affecting companies located in that region or country because those companies often share common characteristics, are exposed to similar business risks and regulatory burdens, and react similarly to specific economic, market, political or other developments. See also “Foreign Investment Risk” above.

• REAL ESTATE RISK. To the extent the Fund concentrates its assets in real-estate related investments, the value of its portfolio is subject to factors affecting the real estate industry and may fluctuate more than the value of a portfolio that consists of securities of companies in a broader range of industries. Factors affecting real estate values include the supply of real property in particular markets, overbuilding, changes in zoning laws, casualty or condemnation losses, delays in completion of construction, changes in real estate values, changes in operations costs and property taxes, levels of occupancy, adequacy of rent to cover operating expenses, possible environmental liabilities, regulatory limitations on rent, fluctuations in rental income, increased competition and other risks related to local and regional market conditions. The value of real-estate related investments also may be affected by changes in interest rates, macroeconomic developments, and social and economic trends. For instance, during periods of declining interest rates, certain mortgage REITs may hold mortgages that the mortgagors elect to prepay, which prepayment may diminish the yield on securities issued by those REITs. Some REITs have relatively small market capitalizations, which can tend to increase the volatility of the market price of their securities. REITs are subject to the risk of fluctuations in income from underlying real estate assets, their inability to manage effectively the cash flows generated by those assets, prepayments and defaults by borrowers, and failing to qualify for the special tax treatment granted

-19-

Table of Contents

to REITs under the Internal Revenue Code of 1986, as amended, and/or to maintain their exemption from investment company status under the1940 Act.

• LEVERAGING RISK. The Fund’s use of reverse repurchase agreements and other derivatives and securities lending may cause its portfolio to be leveraged (i.e., the Fund’s exposure to underlying securities, assets or currencies exceeds its net asset value). Leverage increases the Fund’s portfolio losses when the value of its investments declines. Because many derivatives have a leverage component (i.e., a notional value in excess of the assets needed to establish and/or maintain the derivative position), adverse changes in the value or level of the underlying asset, rate or index may result in a loss substantially greater than the amount invested in the derivative itself. In the case of swaps, the risk of loss generally is related to a notional principal amount, even if the parties have not made any initial investment. Some derivatives have the potential for unlimited loss, regardless of the size of the initial investment. The Fund’s use of reverse repurchase agreements also subjects the Fund to interest costs based on the difference between the sale and repurchase price of a security involved in such a transaction. The Fund’s portfolio also will be leveraged if it borrows money to meet redemption requests or settle investment transactions or if it avails itself of the right to delay payment on a redemption.

The Fund may manage some of its derivative positions by offsetting derivative positions against one another or against other assets. To the extent offsetting positions do not behave in relation to one another as expected, the Fund may perform as if it were leveraged.

• COUNTERPARTY RISK. This is the risk that the counterparty to a repurchase agreement or reverse repurchase agreement or other OTC derivatives contract or a borrower of the Fund’s securities will be unable or unwilling to make timely settlement payments or otherwise honor its obligations. If a counterparty fails to meet its contractual obligations, goes bankrupt, or otherwise experiences a business interruption, the Fund could miss investment opportunities or otherwise hold investments it would prefer to sell, resulting in losses for the Fund. Counterparty risk is pronounced during unusually adverse market conditions and is particularly acute in environments (like those experienced recently) in which financial services firms are exposed to systemic risks of the type evidenced by the insolvency of Lehman Brothers in 2008 and subsequent market disruptions.