Exhibit 99.2

| CALEDONIA MINING CORPORATION PLC | August 10, 2023 |

Management’s Discussion and Analysis

This management’s discussion and analysis (“MD&A”) of the consolidated operating results and financial position of Caledonia Mining Corporation Plc (“Caledonia” or the “Company”) is for the quarter ended June 30, 2023 (“Q2 2023” or the “Quarter”). It should be read in conjunction with the Unaudited Condensed Consolidated Interim Financial Statements of Caledonia for the Quarter (the “Interim Financial Statements”) which are available from the System for Electronic Data Analysis and Retrieval at www.sedar.com or from Caledonia’s website at www.caledoniamining.com. The Interim Financial Statements and related notes have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. In this MD&A, the terms “Caledonia”, the “Company”, the “Group”, “we”, “our” and “us” refer to the consolidated operations of Caledonia Mining Corporation Plc and its subsidiaries unless otherwise specifically noted or the context requires otherwise.

Note that all currency references in this document are in thousands of US Dollars (also “$”, “US$” or “USD”), unless stated otherwise.

| 1 |

TABLE OF CONTENTS

Table of Contents

| 2 |

| 1. | OVERVIEW |

Caledonia is a Zimbabwean focussed exploration, development, and mining corporation. Caledonia owns a 64% stake in the gold-producing Blanket Mine (“Blanket”), and 100% stakes in the Bilboes oxide mine, the Bilboes sulphide project, and the Motapa and Maligreen gold mining claims, all situated in Zimbabwe. Caledonia’s shares are listed on the NYSE American LLC (“NYSE American”), depositary interests in Caledonia’s shares are admitted to trading on AIM of the London Stock Exchange plc and depositary receipts in Caledonia’s shares are listed on the Victoria Falls Stock Exchange (“VFEX”) (all under the symbols “CMCL”).

| 2. | SUMMARY |

| Q2 | Q2 | H1 | H1 | Comment | |

| 2023 | 2022 | 2023 | 2022 | ||

| Gold produced (oz) | 18,512 | 20,091 | 34,653 | 38,606 |

Gold produced in the Quarter was 7.9% lower than the second quarter of 2022 (the “comparative” or “comparable quarter”) mainly due to lower grade and lower than budget tonnes milled. Gold production from Blanket was below expectation due to several factors which adversely affected the implementation of the mine plan in certain mining areas. Management has focused intensively on the problem areas and production in late June and in July has shown a marked improvement.

1,076 ounces of gold were produced from the Bilboes oxide mine in the Quarter, an increase from the 105 ounces produced in the first quarter of 2023.

The Bilboes oxide mine was intended to be a small-scale, low-margin, short-term project. Due to the uncertainty that the oxide project can operate profitably, it will be returned to care and maintenance at the end of September 2023. The oxide mineralisation will be mined as part of the larger sulphides project. |

| 3 |

| Q2 | Q2 | H1 | H1 | Comment | |

| 2023 | 2022 | 2023 | 2022 | ||

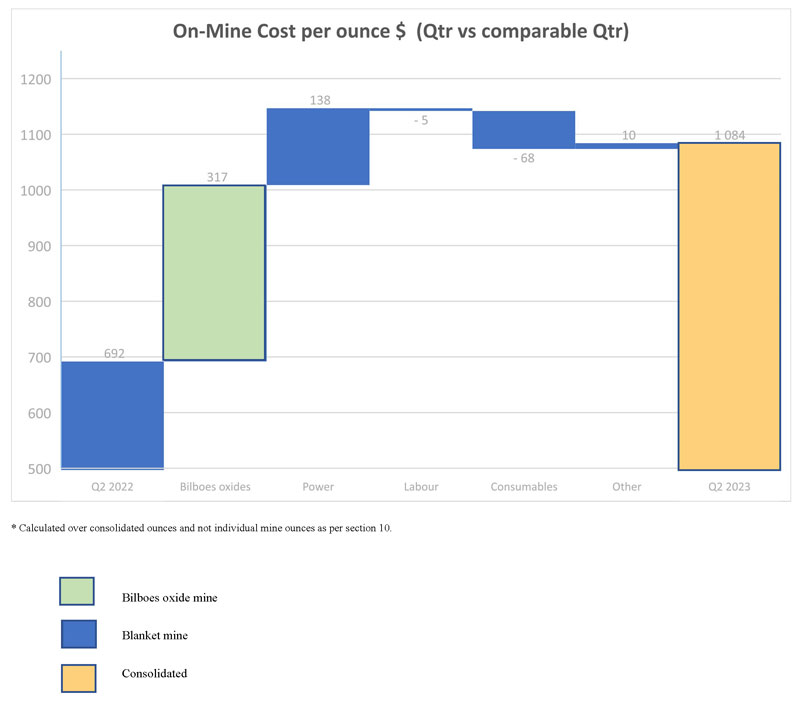

| On-mine cost per ounce ($/oz)1 | 1,084 | 692 | 1,135 | 695 |

On-mine cost per ounce in the Quarter increased by 56.7%. 81% of the increase was due to the high cost per ounce at the Bilboes oxide mine. The remainder of the increase was due to higher on-mine costs at Blanket where lower production meant that fixed costs were spread across fewer production ounces. On-mine costs at Blanket were also affected by higher electricity usage, which contributed approximately $138 per ounce to the overall increase in on-mine costs per ounce compared to the comparative quarter. |

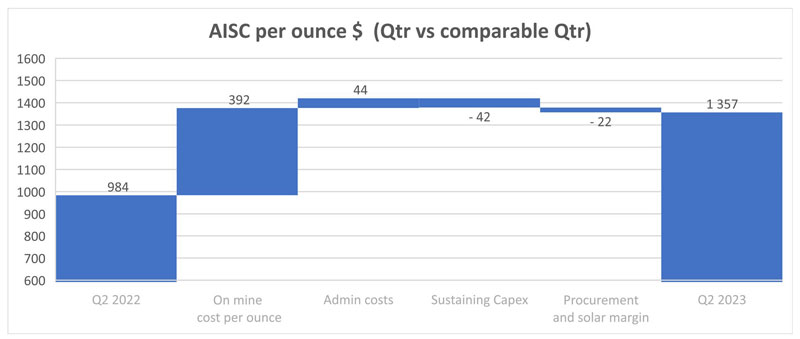

| All-in sustaining cost (“AISC”)1 | 1,357 | 984 | 1,383 | 918 | The AISC per ounce in the Quarter increased by 37.9% compared to the comparative quarter due to the higher on-mine cost per ounce. AISC deducts the benefit of the solar plant electricity saving ($46.84 per ounce) in the Quarter. |

| Average realised gold price ($/oz)1 | 1,949 | 1,840 | 1,909 | 1,844 | The average realised gold price reflects international spot prices. |

| Gross profit2 ($’000) | 10,933 | 17,997 | 16,783 | 34,889 | Gross profit for the Quarter decreased from the comparable quarter due to higher production costs, in particular at the Bilboes oxide mine and increased depreciation. |

| Net (loss) profit attributable to shareholders ($’000) | (513) | 11,378 | (5,542) | 17,318 | Net loss for the Quarter includes a lower gross profit and a foreign exchange loss of $3.6m compared to a foreign exchange gain of $4.2m in the comparable quarter. |

| Basic IFRS (loss) earnings per share (“EPS”) (cents) | (0.6) | 87.7 | (30.8) | 132.3 | IFRS EPS reflects the movement in IFRS profit attributable to shareholders and the effect of new shares issued. |

| Adjusted EPS (cents)1 | 10.0 | 56.2 | (17.3) | 118.8 | Adjusted EPS excludes inter alia net foreign exchange gains and losses, deferred tax and fair value movements on derivative financial instruments. |

| Net cash from operating activities ($’000) | (2,226) | 16,715 | (3,102) | 26,870 | Net cash from operating activities in the Quarter decreased predominantly due to lower gross profit, $6.1m of realised foreign exchange losses and $4.3m of negative working capital movements. |

| Net cash and cash equivalents ($’000) | (2,907) | 10,862 | (2,907) | 10,862 | Net cash decreased due to the negative contributions to cash flows from operating activities from the Bilboes oxides mine. |

1 Non-IFRS measures such as “On-mine cost per ounce”, “AISC”, “average realised gold price” and “adjusted EPS” are used throughout this document. Refer to section 10 of this MD&A for a discussion of non-IFRS measures.

2 Gross profit is after deducting royalties, production costs and depreciation but before administrative expenses, other income, interest and finance charges and taxation.

| 4 |

Fatality at Blaket mine

On August 7, 2023, an accident took place at Blanket. As a result an employee of GMG Pty Ltd, a company contracted to Blanket, succumbed to his injuries in hospital. The accident related to the maintenance of trackless equipment. Caledonia and Blanket express their sincere condolences to the family and colleagues of the deceased. Management has provided the necessary assistance to the Ministry of Mines Inspectorate Department in its enquiries into the incident. Caledonia takes the safety of its employees very seriously and measures have been taken to reinforce adherence to prescribed safety procedures. Safety is discussed further in section 4.1.

Encouraging drilling results at Blanket

The ongoing underground drilling program at Blanket targets the Eroica ore body and has yielded encouraging results. Approximately 5,600 meters ("m") of drilling were completed between January 2023 and the end of May 2023. Initial results indicate that the existing Eroica ore body has a better grade and width than was generally expected. In due course, this new information will be reflected in a revised resource statement and an updated technical report in respect of Blanket. Exploration is discussed further in section 5.

Equity raises

The Company conducted equity raises by way of placings in the previous quarter and the Quarter that targeted institutional investors in the UK, Europe, South Africa and Zimbabwe. The equity raises were over-subscribed; depositary interests in respect of 781,749 shares were issued to investors in the UK, Europe and South Africa on March 30, 2023 and Zimbabwe depositary receipts in respect of 425,765 shares were issued on April 14, 2023. The placings raised $16.6 million before expenses.

The proceeds are to be used for the Bilboes sulphide project feasibility study, a shared services centre in Zimbabwe, the establishment of an international procurement arm to supply future operations and for exploration drilling at Motapa.

On May 18, 2023 the Company entered into an "At the Market" or "ATM" sales agreement with its broker in the United States pursuant to which the Company may, at its discretion, from time to time, sell up to $30 million worth of shares on the NYSE American at market prices. No shares have been sold pursuant to this agreement as at today’s date.

Quarterly Production at Blanket Mine and the Bilboes oxide mine

Blanket Mine

Quarterly gold production at Blanket Mine was 17,436 ounces, 13.2% lower than the 20,091 ounces produced in the comparative quarter. Production at Blanket in the Quarter, although improved from the previous quarter, was still below expectations. This was due to several factors which impacted the implementation of the mine plan in certain mining areas and included a high level of missed blasts and errors in blasting accuracy which contributed to inadequate face advances. Management has focused intensively on the production challenges and production in late June and in July has shown a marked improvement: production in July was 7,829 ounces – an annualised rate of over 93,000 ounces which supports the maintenance of annual production guidance for Blanket for the year to December 31, 2023 of between 75,000 and 80,000 ounces. On-mine cost guidance at Blanket of between $770 and $850 per ounce is also maintained as costs per ounce are expected to be lower in the second half of the year due to the expected increase in production compared to the first six months of 2023. The on-mine cost in July was $715 per ounce.

| 5 |

Bilboes oxide mine

1,076 ounces of gold were produced from the Bilboes oxide mine in the Quarter, showing an increase from the 105 ounces produced in the first quarter of 2023. There was no production at the Bilboes oxide mine in 2022. The Bilboes oxide mine was intended as a small-scale, low-margin, short-term project the primary objective of which was to cover the cost of the Bilboes operation before the start of the larger sulphide project. Due to the lack of certainty that the oxide operation can operate on at least a cash-neutral basis, it will be returned to care and maintenance with effect from October 1, 2023.

Mining and metallurgical processing will continue at the Bilboes oxide mine until the end of September; thereafter leaching of material that has already been deposited on the leach pad will continue. Oxide mining and processing will resume when the stripping of the waste for the sulphide project commences.

The Company withdrew guidance in April 2023 for the Bilboes oxide mine.

Revised marketing arrangements for gold

Since listing on the VFEX and following completion of the Bilboes acquisition, Caledonia has considered various avenues to achieve the direct export of its gold. Unrefined gold continues to be processed at Fidelity Gold Refinery (Private) Limited ("FGR"), a subsidiary of the Reserve Bank of Zimbabwe ("RBZ"), on a toll-treatment basis. The gold is exported from FGR to a refinery outside Zimbabwe, which undertakes the final refining and sells the final gold on behalf of Caledonia. Caledonia receives the proceeds of the gold sales directly into its bank account in Zimbabwe within a few days of delivery to the final refinery.

Retirement of Chairman

On May 5, 2023 the Company announced the retirement of Leigh Wilson from his role as Director and Non-Executive Chairman of the Company. John Kelly, who was already a Non-Executive Director of the Company, has been appointed as Mr. Wilson's successor.

Strategy and Outlook: increased focus on growth opportunities

The immediate strategic focus is to:

| · | maintain production at Blanket at the targeted range of 75,000 - 80,000 ounces for 2023; |

| · | continue deep level drilling at Blanket with the objective of further upgrading inferred mineral resources, thereby extending the life of mine; |

| · | complete the Caledonia feasibility study on the Bilboes sulphide project to determine the best implementation strategy and estimate the funding requirements, and commence development of the sulphide project; and |

| · | commence exploration at Motapa. |

The strategy and outlook of Caledonia is further discussed in section 4.10 of this MD&A.

| 6 |

| 3. | SUMMARY FINANCIAL RESULTS |

The table below sets out the consolidated profit or loss for the Quarter and comparative quarter prepared under IFRS.

| Condensed Consolidated Statements of profit or loss and Other comprehensive income (Unaudited) | ||||||||||||||||

| ($’000’s) | ||||||||||||||||

| 3 months ended June 30 | 6 months ended June 30 | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Revenue | 37,031 | 36,992 | 66,466 | 72,064 | ||||||||||||

| Royalty | (1,963 | ) | (1,854 | ) | (3,443 | ) | (3,612 | ) | ||||||||

| Production costs | (20,726 | ) | (14,502 | ) | (40,576 | ) | (28,861 | ) | ||||||||

| Depreciation | (3,409 | ) | (2,639 | ) | (5,664 | ) | (4,702 | ) | ||||||||

| Gross profit | 10,933 | 17,997 | 16,783 | 34,889 | ||||||||||||

| Other income | 168 | 1 | 186 | 3 | ||||||||||||

| Other expenses | (1,461 | ) | (490 | ) | (2,099 | ) | (1,283 | ) | ||||||||

| Administrative expenses | (3,183 | ) | (2,908 | ) | (9,122 | ) | (5,279 | ) | ||||||||

| Net foreign exchange (loss) gain | (3,610 | ) | 4,172 | (2,077 | ) | 5,081 | ||||||||||

| Cash-settled share-based expense | 9 | 57 | (271 | ) | (310 | ) | ||||||||||

| Equity-settled share-based expense | (221 | ) | - | (331 | ) | (82 | ) | |||||||||

| Net derivative financial instrument expenses | (54 | ) | 41 | (488 | ) | (1,697 | ) | |||||||||

| Operating profit | 2,581 | 18,870 | 2,581 | 31,322 | ||||||||||||

| Net finance costs | (1,057 | ) | (175 | ) | (1,824 | ) | (291 | ) | ||||||||

| Profit before tax | 1,524 | 18,695 | 757 | 31,031 | ||||||||||||

| Tax expense | (1,273 | ) | (5,314 | ) | (4,775 | ) | (10,033 | ) | ||||||||

| Profit (loss) for the period | 251 | 13,381 | (4,018 | ) | 20,998 | |||||||||||

| Other comprehensive income | ||||||||||||||||

| Items that are or may be reclassified to profit or loss | ||||||||||||||||

| Exchange differences on translation of foreign operations | (330 | ) | (852 | ) | (699 | ) | (159 | ) | ||||||||

| Total comprehensive income for the period | (79 | ) | 12,529 | (4,717 | ) | 20,839 | ||||||||||

| Profit (loss) attributable to: | ||||||||||||||||

| Owners of the Company | (513 | ) | 11,378 | (5,542 | ) | 17,318 | ||||||||||

| Non-controlling interests | 764 | 2,003 | 1,524 | 3,680 | ||||||||||||

| Profit (loss) for the period | 251 | 13,381 | (4,018 | ) | 20,998 | |||||||||||

| Total comprehensive income attributable to: | ||||||||||||||||

| Owners of the Company | (843 | ) | 10,526 | (6,241 | ) | 17,159 | ||||||||||

| Non-controlling interests | 764 | 2,003 | 1,524 | 3,680 | ||||||||||||

| Total comprehensive income for the period | (79 | ) | 12,529 | (4,717 | ) | 20,839 | ||||||||||

| (Loss) earnings per share (cents) | ||||||||||||||||

| Basic | (0.6 | ) | 87.7 | (30.8 | ) | 132.3 | ||||||||||

| Diluted | (0.6 | ) | 87.7 | (30.8 | ) | 132.3 | ||||||||||

| Adjusted earnings (loss) per share (cents) | ||||||||||||||||

| Basic | 10.0 | 56.2 | (17.3 | ) | 118.8 | |||||||||||

| Dividends paid per share (cents) | 14.0 | 14.0 | 28.0 | 28.0 | ||||||||||||

| 7 |

Revenue in the Quarter was 0.1% higher than the comparative quarter despite a 5.5% decrease in the quantity of gold sold as this was offset by a 6% increase in the average realised price of gold sold.

The royalty rate payable to the Zimbabwe Government was unchanged at 5%.

Production costs

Production costs increased by 42.9% in the Quarter compared to the comparative quarter and the on-mine cost per ounce increased by 56.6% in the Quarter from the comparative quarter.

The on-mine cost per ounce and the AISC per ounce increased in the Quarter compared to the comparative quarter as illustrated in the graphs below.

| 8 |

The cost of oxide mining at Bilboes contributed $317 per ounce to the overall increase in the on-mine cost per ounce. The large amount of waste that was moved to access the oxide mineralisation proved costly and Bilboes had an on-mine cost of $3,095 per ounce in the Quarter. Due to the uncertainty that the Bilboes oxide project can operate profitably, it will return to care and maintenance at the end of September 2023. Oxide material at Bilboes will be mined and processed in conjunction with the Bilboes sulphide project, as was planned for in the current Bilboes project feasibility study. The net book value of the Bilboes oxide mine of $851,000 was impaired, as the oxides mine cannot be run economically without extracting the sulphide mineralisation. Leaching of the oxide ore on the heap leach pad will continue until the end of the year to recover gold deposited on the leach pad prior to the termination of oxide mining. Bilboes is discussed further in section 4.9.

Production costs at Blanket for the Quarter increased from the comparative Quarter by 14.5% and Blanket's on-mine cost increased from $692 per ounce in comparative Quarter to $915 per ounce in the Quarter. Production costs at Blanket increased predominantly due to the higher than anticipated use of electricity due to the continued heavy use of infrastructure such as the No. 4 Shaft and Jethro shaft which had been expected to be used more sparingly following the commissioning of the Central Shaft.

In April 2023 Blanket concluded a power supply agreement with the Intensive Energy Users Group (“IEUG") and the Zimbabwean power utility to allow the IEUG to obtain power outside Zimbabwe which is "wheeled” to the IEUG members. During the Quarter Blanket paid less for IEUG sourced energy but the incidences of power outages and low voltage occurrences did not reduce due to the poor condition of the Zimbabwe grid which meant that higher than expected diesel costs were incurred to supplement the low voltage occurrences. Management is conducting a study on how to alleviate the effect of the low voltage occurrences in the most economical manner.

The benefit of the solar plant is not recognised in on-mine costs because the solar plant (100%-owned by Caledonia) sells power to Blanket at a price per kilowatt/hour which reflects Blanket's historic blended cost per unit. The economic benefit of the solar plant is therefore recognised by Caledonia, rather than by Blanket, and the benefit (approximately $46.84 per ounce of gold produced) is reflected in the AISC rather than the on-mine cost.

Labour costs at Blanket decreased predominantly because of the lower production bonuses paid in the Quarter compared to last year offset by increased overtime hours, increased employment numbers at Blanket, inflationary increases and an increase in the government mandated minimum wage.

Consumable costs per ounce at Blanket in the Quarter decreased due to higher repair and maintenance costs incurred in the comparative Quarter.

| 9 |

Various government service payments increased in the Quarter compared to the comparative quarter which increased on-mine costs by $10 per ounce compared to the comparative quarter.

Administrative expenses are detailed in note 9 to the Interim Financial Statements and include the costs of Caledonia’s offices and personnel in Johannesburg, the UK and Jersey which provide the following functions: technical services, finance, procurement, investor relations, corporate development, legal and company secretarial. Administrative expenses in the Quarter were 9.5% higher than the comparative quarter predominantly due to the appointment of more technical services staff and the cost of taking over Bilboes staff members.

The depreciation charge in the Quarter increased because of increase in the depreciable cost base following the commissioning of the Central Shaft and the solar plant. A reassessment of the useful lives of some plant and equipment items also increased the depreciation charge. The useful life of the Jethro shaft reduced due to the availability of the new Central Shaft and the useful life of certain generators, load haul dumpers, dump trucks and drill rigs reduced due to their current condition (refer to note 13 of the Interim Financial Statements). This was somewhat offset by the lower production ounces in the Quarter over which a large part of the cost base is depreciated.

Other expenses are detailed in note 8 to the Interim Financial Statements.

Net foreign exchange movements relate to gains and losses arising on monetary assets and liabilities that are held in currencies other than the USD. Large foreign exchange losses in the Quarter arose due to the delays of up to 3 weeks by FGR in the settlement of the RTGS$ denominated bullion receivables. This coincided with a period during which the RTGS$ devalued sharply against the USD from ZWL$2,770 on June 6, 2023 to ZWL$6,927 on June 21, 2023 and resulted in significant realised foreign exchange losses.

The tax expense comprised of the following:

| Analysis of consolidated tax expense/(credit) for the Quarter | ||||||||||||||||||||

| ($’000’s) | Zimbabwe | South Africa | UK | Bilboes | Total | |||||||||||||||

| Income tax | 1,488 | 64 | - | - | 1,552 | |||||||||||||||

| Withholding tax | ||||||||||||||||||||

| Management fee | - | 41 | - | - | 41 | |||||||||||||||

| Deemed dividend | 91 | - | - | - | 91 | |||||||||||||||

| CHZ dividends to GMS-UK | - | - | - | - | - | |||||||||||||||

| Deferred tax | (402 | ) | (53 | ) | - | 44 | (411 | ) | ||||||||||||

| 1,177 | 52 | - | 44 | 1,273 | ||||||||||||||||

The overall effective taxation rate for the Quarter was 83.5% (2022: 28.4%). The effective tax rate bears little relationship to reported consolidated loss before tax for the following reasons:

| · | Operating losses incurred at the Bilboes oxide mine cannot be offset against profits arising elsewhere in the group – thus they reduce profit before tax, with no commensurate reduction in the tax expense; |

| · | Zimbabwean taxable income is calculated in both RTGS$ and USD, whereas the group reports in USD. Large devaluations in the RTGS$ against the USD result in substantial foreign exchange movements on the RTGS$ tax payable which have a significant effect on the income tax calculation; |

| · | 100% of capital expenditure is tax deductible in the year in which it is incurred for tax purposes, whereas depreciation only commences when a project enters production; timing differences can alter the effective tax rate based on the capital expenditure for a quarter; and |

| · | The rate of income tax in Jersey, which is the tax domicile of the parent company of the Group (i.e. the Company), is zero which means there is no benefit to be realised by offsetting expenses incurred in Jersey against taxable profits. |

| 10 |

The effective taxation rate for Blanket was 28.6% (2022: 28.8%), which broadly corresponds to the enacted income tax rate in Zimbabwe which remained unchanged at 24.72%. Zimbabwe income tax payments are made in the same proportion of RTGS$ and USD as revenue is received. Deferred tax predominantly comprises the difference between the accounting and tax treatments of capital investment. Most of the tax expense comprised income tax and deferred tax incurred in Zimbabwe.

South African income tax arises on intercompany profits arising at Caledonia Mining South Africa Proprietary Limited (“CMSA”).

Zimbabwe withholding tax arose on the management fees paid to CMSA and on dividends paid from Caledonia Holdings Zimbabwe (Private) Limited (“CHZ”) to the Company’s subsidiary in the UK Greenstone Management Services Holdings Limited (“GMS-UK”).

IFRS basic EPS for the Quarter decreased by 101% from a profit of 87.7 cents in the comparative quarter to a loss of 0.6 cents. Adjusted EPS for the Quarter excludes inter alia the effect of foreign net exchange movements and deferred tax. Adjusted EPS reduced by 82.3% from a profit of 56.2 cents in the comparative quarter to 10.0 cents for the Quarter. A reconciliation from IFRS EPS to adjusted EPS is set out in section 10.3.

A dividend of 14 cents per share was paid in the Quarter. Caledonia’s dividends are discussed further in section 14.

Risks that may affect Caledonia’s future financial condition are discussed in section 17.

| 11 |

The table below sets out the consolidated statements of cash flows for the Quarter and the comparative quarter prepared under IFRS.

| Condensed Consolidated Statements of Cash Flows (Unaudited) | ||||||||||||||||

| ($’000’s) | ||||||||||||||||

| 3 months ended June 30 | 6 months ended June 30 | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Cash inflow from operations | 2 | 18,341 | 666 | 30,185 | ||||||||||||

| Interest received | 4 | 2 | 9 | 3 | ||||||||||||

| Net finance costs paid | (1,231 | ) | (61 | ) | (1,431 | ) | (92 | ) | ||||||||

| Tax paid | (1,001 | ) | (1,567 | ) | (2,346 | ) | (3,226 | ) | ||||||||

| Net cash (outflow)/inflow from operating activities | (2,226 | ) | 16,715 | (3,102 | ) | 26,870 | ||||||||||

| Cash flows used in investing activities | ||||||||||||||||

| Acquisition of property, plant and equipment | (6,009 | ) | (13,011 | ) | (10,602 | ) | (22,745 | ) | ||||||||

| Acquisition of exploration and evaluation assets | (139 | ) | (412 | ) | (283 | ) | (636 | ) | ||||||||

| Acquisition of put options | (811 | ) | (176 | ) | (811 | ) | (176 | ) | ||||||||

| Net cash used in investing activities | (6,959 | ) | (13,599 | ) | (11,696 | ) | (23,557 | ) | ||||||||

| Cash flows from financing activities | ||||||||||||||||

| Dividends paid | (2,893 | ) | (2,700 | ) | (5,317 | ) | (4,488 | ) | ||||||||

| Payment of lease liabilities | (35 | ) | (39 | ) | (72 | ) | (79 | ) | ||||||||

| Repayments gold loan | - | (3,698 | ) | - | (3,698 | ) | ||||||||||

| Shares issued - equity raise (net of transaction cost) | 4,834 | - | 15,658 | - | ||||||||||||

| Loan note instruments - Motapa payment | (1,288 | ) | - | (6,687 | ) | - | ||||||||||

| Loan note instruments - Solar bond issue receipts | 2,500 | - | 7,000 | - | ||||||||||||

| Net cash from/(used in) from financing activities | 3,118 | (6,613 | ) | 10,582 | (8,441 | ) | ||||||||||

| Net decrease in cash and cash equivalents | (6,067 | ) | (3,321 | ) | (4,216 | ) | (4,952 | ) | ||||||||

| Effect of exchange rate fluctuations on cash and cash equivalents | (30 | ) | (247 | ) | (187 | ) | (451 | ) | ||||||||

| Net cash and cash equivalents at beginning of the period | 3,190 | 14,430 | 1,496 | 16,265 | ||||||||||||

| Net cash and cash equivalents at end of the period | (2,907 | ) | 10,862 | (2,907 | ) | 10,862 | ||||||||||

Cash flows from operating activities in the Quarter are detailed in note 23 to the Interim Financial Statements. Cash inflows from operations before working capital changes in the Quarter was $4.9 million, compared to $13.5 million in the comparative quarter.

Cash flows from operations before working capital changes were negatively affected during the Quarter by lower production and higher costs. Blanket continued to make a positive cash contribution of $8 million; the Bilboes oxide mine contributed a cash outflow of $2.1 million.

| 12 |

Working capital increased by $4.8 million in the Quarter, which was due primarily to payments of $4 million to legacy creditors taken on in the acquisition of Bilboes Gold Limited (“Bilboes Gold”) on January 6, 2023. Working capital was also adversely affected by the accumulation in the last few weeks of the Quarter of 995 ounces of gold with a realisable value of approximately $1.9 million due for export to a foreign refiner in July 2023.

The acquisition of property plant and equipment relates to the investment at Blanket as discussed further in section 4.7; the investment in exploration and evaluation assets relates to the Bilboes oxide acquisition and the ongoing exploration work at Motapa and Maligreen.

Dividends for the Quarter comprise $2.9 million paid to shareholders of the Company. A dividend of 14 cents per share was announced on July 3, 2023.

In March and April 2023, the Company conducted equity raises by way of placings targeting institutional investors in the UK, Europe, South Africa and Zimbabwe. This gave rise to an inflow in the previous quarter of $10.8 million, after expenses in respect of depositary interests that were issued to investors in the UK, Europe and South Africa. A further $5.85 million was received during the Quarter in respect of depositary receipts that were issued to investors in Zimbabwe.

Bonds have been issued by Caledonia Mining Services (Private) Limited (“CMS”), the subsidiary that owns the solar plant. Solar bond issue receipts to the value of $2.5 million were issued by CMS in the Quarter. The bonds have an interest rate of 9.5% payable bi-annually and have a tenor of 3 years from the date of issue. The bond repayments are guaranteed by the Company, and all are issued to Zimbabwean registered commercial entities.

The $1.3 million loan note payment represented the settlement of part of the outstanding consideration in respect of the purchase of the Motapa exploration and evaluation project in 2022. The remainder of the loan notes was settled at the start of July 2023.

The effect of exchange rate fluctuations on cash held reflects gains or losses on cash balances held in currencies other than the US Dollar. The effect on cash balances forms part of an overall foreign exchange gain or loss arising on all affected financial assets and liabilities.

| 13 |

The table below sets out the consolidated statements of Caledonia’s financial position at the end of the Quarter and December 31, 2022 prepared under IFRS.

| Summarised Consolidated Statements of Financial Position (Unaudited) | ||||||||||

| ($’000’s) | As at | Jun-30 | Dec-31 | |||||||

| 2023 | 2022 | |||||||||

| Total non-current assets | 269,286 | 196,764 | ||||||||

| Inventories | 18,454 | 18,334 | ||||||||

| Prepayments | 3,940 | 3,693 | ||||||||

| Trade and other receivables | 8,560 | 9,185 | ||||||||

| Income tax receivable | 103 | 40 | ||||||||

| Cash and cash equivalents | 12,785 | 6,735 | ||||||||

| Derivative financial assets | 763 | 440 | ||||||||

| Total assets | 313,891 | 235,191 | ||||||||

| Total non-current liabilities | 13,779 | 9,291 | ||||||||

| Loan notes payable – short term portion | 771 | 7,104 | ||||||||

| Lease liabilities – short term portion | 136 | 132 | ||||||||

| Trade and other payables | 17,161 | 17,454 | ||||||||

| Income tax payable | 2,511 | 1,324 | ||||||||

| Cash-settled share-based payments - short term portion | 660 | 1,188 | ||||||||

| Overdraft | 15,692 | 5,239 | ||||||||

| Total liabilities | 50,710 | 41,732 | ||||||||

| Total equity | 263,181 | 193,459 | ||||||||

| Total equity and liabilities | 313,891 | 235,191 | ||||||||

The acquisition of Bilboes Gold increased the exploration and evaluation assets by $69.6 million. Property, plant and equipment additions at Blanket amounted to $5.9 million in the Quarter and predominantly related to infrastructure development at 30 and 34 level and the construction of the new tailings storage facility at Blanket (“TSF”).

Inventories include 995 ounces of gold which was held by FGR in transit to Al Etihad Gold refinery DMCC (“AEG”) which was sold in July 2023. Prepayments represent deposits and advance payments for goods and services. $1.1 million of prepayments related to construction work on the new TSF which is discussed in section 4.7. Prepayments further increased by $0.8 million due to RTGS$ suppliers requiring larger deposits to protect against the weakening of the RTGS$ rate against the USD.

Trade and other receivables are detailed in note 17 to the Interim Financial Statements and include $5.3 million (December 31, 2022: $7.4 million) due from FGR in respect of gold deliveries prior to the close of business on June 30, 2023. All outstanding amounts due from FGR were received in full after the end of the Quarter. $2.4 million (December 31, 2022: $1 million) was due from the Zimbabwe Government in respect of VAT refunds.

Trade and other payables at Quarter end marginally decreased from December 31, 2022. On the completion of the acquisition of Bilboes Gold, trade and other payables amounting to $4.1 million were acquired of which $4 million was settled in the Quarter.

Overdrafts increased due to short term funding requirements and are expected to reduce by December 31, 2023. Expiration dates and terms of the overdrafts are set out in section 7 (Financing).

Most cash-settled share-based payments due to staff as at Dec 31, 2022 were settled in the Quarter. On April 7, 2023 the Company made awards of 79,894 PUs and 93,035 EPUs to certain management and employees within the Group pursuant to the provisions of the 2015 Omnibus Equity Incentive Compensation Plan (“OEICP”). The short-term portion of the cash-settled share-based payment liability is in respect of awards made to certain employees at Caledonia, CMSA and Blanket in terms of the OEICP. The awards (other than those made to certain executive officers (the “NEOs”) in 2023 which only settle in shares) can be settled in cash or, subject to conditions, shares at the option of the recipient.

| 14 |

The table below illustrates the distribution of the consolidated cash across the jurisdictions where the Group holds its cash:

Geographical location of cash ($’000’s)

| As at | Sep 30, | Dec 31, | Mar 31, | Jun 30, | ||||||||||||

| 2022 | 2022 | 2023 | 2023 | |||||||||||||

| Zimbabwe | 883 | (2,160 | ) | (9,749 | ) | (7,373 | ) | |||||||||

| South Africa | 932 | 694 | 1,107 | 834 | ||||||||||||

| UK/Jersey | 4,352 | 2,962 | 11,831 | 3,632 | ||||||||||||

| Total net cash and cash equivalents | 6,167 | 1,496 | 3,189 | (2,907 | ) | |||||||||||

Included in the cash and cash equivalents is a restricted cash amount of US$0.9 million (denominated in RTGS$) held by Blanket which has been earmarked by Stanbic Bank Zimbabwe as a letter of credit in favour of CMSA. The letter of credit was issued by Stanbic Bank Zimbabwe on February 28, 2023 in RTGS$ and has a 120-day conversion tenure. The full amount was settled to CMSA on July 3, 2023 in South African rands.

US$1 million was held as a minimum cash balance in Jersey until the final repayment of the Motapa loan notes were made on July 3, 2023.

The following information is provided for each of the eight most recent quarterly periods ending on the dates specified. The amounts are extracted from underlying financial statements that have been prepared using accounting policies consistent with IFRS.

| ($’000’s except per share amounts) | Sep 30, | Dec 31, | Mar 31, | Jun 30, | Sep 30, | Dec 31, | Mar 31, | Jun 30, | ||||||||||||||||||||||||

| 2021 | 2021 | 2022 | 2022 | 2022 | 2022 | 2023 | 2023 | |||||||||||||||||||||||||

| Revenue | 33,496 | 32,136 | 35,072 | 36,992 | 35,840 | 34,178 | 29,435 | 37,031 | ||||||||||||||||||||||||

| Profit/(loss) attributable to owners of the Company | 6,939 | 4,222 | 5,940 | 11,378 | 8,614 | (8,029 | ) | (5,030 | ) | (513 | ) | |||||||||||||||||||||

| EPS – basic (cents) | 56.8 | 33.3 | 44.6 | 87.7 | 63.3 | (62.2 | ) | (30.3 | ) | (0.6 | ) | |||||||||||||||||||||

| EPS – diluted (cents) | 56.7 | 33.3 | 44.6 | 87.7 | 63.3 | (62.2 | ) | (30.2 | ) | (0.6 | ) | |||||||||||||||||||||

| Net cash and cash equivalents | 34,178 | 16,265 | 14,430 | 10,862 | 6,167 | 1,496 | 3,189 | (2,907 | ) | |||||||||||||||||||||||

| 15 |

| 4. | OPERATIONS |

| 4.1.1 | Safety, Health and Environment – |

The following safety statistics have been recorded for the Quarter and the preceding seven quarters.

| Blanket Mine Safety Statistics | ||||||||||||||||||||||||||||||||

| Classification | Q3 2021 | Q4 2021 | Q1 2022 | Q2 2022 | Q3 2022 | Q4 2022 | Q1 2023 | Q2 2023 | ||||||||||||||||||||||||

| Fatal | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | ||||||||||||||||||||||||

| Lost time injury | 0 | 2 | 0 | 2 | 1 | 1 | 0 | 5 | ||||||||||||||||||||||||

| Restricted work activity | 1 | 1 | 0 | 1 | 1 | 2 | 6 | 7 | ||||||||||||||||||||||||

| First aid | 1 | 0 | 2 | 3 | 0 | 0 | 1 | 0 | ||||||||||||||||||||||||

| Medical aid | 6 | 8 | 6 | 3 | 1 | 2 | 4 | 0 | ||||||||||||||||||||||||

| Occupational illness | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||||||

| Total | 8 | 11 | 9 | 9 | 3 | 5 | 12 | 12 | ||||||||||||||||||||||||

| Incidents | 26 | 10 | 9 | 10 | 14 | 6 | 14 | 3 | ||||||||||||||||||||||||

| Near misses | 6 | 2 | 4 | 7 | 6 | 1 | 4 | 4 | ||||||||||||||||||||||||

| Disability Injury Frequency Rate | 0.12 | 0.24 | 0.12 | 0.36 | 0.22 | 0.33 | 0.80 | 1.35 | ||||||||||||||||||||||||

| Total Injury Frequency Rate | 0.98 | 1.58 | 1.07 | 1.08 | 0.34 | 0.56 | 1.36 | 1.35 | ||||||||||||||||||||||||

| Man-hours worked (000’s) | 1,629 | 1,643 | 1,686 | 1,672 | 1,788 | 1,801 | 1,760 | 1,780 | ||||||||||||||||||||||||

No fatality was recorded in the Quarter; on August 8, 2023 Caledonia reported that an employee of a company contracted to Blanket died of injuries sustained in an accident at Blanket.

The number of incidents as reflected in the Total Injury Frequency Rate increased in the Quarter. Although we believe that Blanket’s safety performance compares favourably with other deep level underground gold mines, the safety performance at Blanket could be better. The Nyanzvi 2 initiative (discussed below) is designed to focus on increasing safety awareness and reinforce strict adherence to prescribed safety procedures.

The Blanket Mine Nyanzvi Nation Building Initiative

During the Quarter, Nyanzvi 1 training sessions were held for all the new employees. There was also a co-creation workshop for Nyanzvi 2 which will focus on team, personal, business skills, management systems (daily, weekly and monthly), incentives, monthly rewards and recognition and will be rolled out in the third quarter of 2023. This programme is intended to address the skills shortages, and behavioural and training deficits that have contributed to production issues in the Quarter and the preceding quarter. An industrial theatre group was established to improve safety behaviour with an emphasis on every employee being their co-workers' safety keepers and practising stop think fix and continue. This programme is strengthened through on the job training of the poor performing supervisors and teams led by seasonal experienced mining professionals that were sourced from industry.

| 16 |

The following safety statistics have been recorded for the Quarter and the preceding quarter since acquisition.

| Bilboes Oxide Mine Safety Statistics | ||||||||

| Classification | Q1 2023 | Q2 2023 | ||||||

| Minor injury | 0 | 2 | ||||||

| Lost time injury | 0 | 0 | ||||||

| Occupational Health | 0 | 0 | ||||||

| Property Damage Incidents | 6 | 6 | ||||||

| Environmental Incidents | 1 | 2 | ||||||

| Total | 7 | 10 | ||||||

| Incidents | 9 | 15 | ||||||

| Near misses | 2 | 5 | ||||||

| Lost Time Injury Frequency Rate | 0 | 0 | ||||||

| 4.2 | Social Investment and Contribution to the Zimbabwean Economy - Blanket |

Blanket’s investment in community and social projects which are not directly related to the operation of the mine or the welfare of Blanket’s employees, the payments made to the Gwanda Community Share Ownership Trust (“GCSOT”) in terms of Blanket’s indigenisation, and payments of taxation and other non-taxation charges to the Zimbabwe Government and its agencies are set out in the table below.

| Payments to the Community and the Zimbabwe Government | ||||||

| ($’000’s) | ||||||

| Period | Year | CSR Investment |

Payments to GCSOT |

Payments to Zimbabwe Government (excl. royalties) |

Royalties | Total |

| Year | 2013 | 2,147 | 2,000 | 15,354 | 4,412 | 23,913 |

| Year | 2014 | 35 | - | 12,319 | 3,522 | 15,876 |

| Year | 2015 | 50 | - | 7,376 | 2,455 | 9,881 |

| Year | 2016 | 12 | - | 10,637 | 2,923 | 13,572 |

| Year | 2017 | 5 | - | 11,988 | 3,498 | 15,491 |

| Year | 2018 | 4 | - | 10,140 | 3,426 | 13,570 |

| Year | 2019 | 47 | - | 10,357 | 3,854 | 14,258 |

| Year | 2020 | 1,689 | 184 | 12,526 | 5,007 | 19,406 |

| Year | 2021 | 1,163 | 948 | 16,426 | 6,083 | 24,620 |

| Year | 2022 | 888 | 1,200 | 19,184 | 7,124 | 28,396 |

| Q1 | 2023 | 258 | - | 3,769 | 1,471 | 5,498 |

| Q2 | 2023 | 326 | - | 3,356 | 1,856 | 5,538 |

CSR initiatives fall under seven pillars of education, health, women empowerment and agriculture, environment, charity, youth empowerment and conservation.

| 17 |

The main CSR programme at Blanket relates to the refurbishment of the maternity clinic, the primary and secondary schools and the youth centre at Sitezi, which is located approximately 17 km from Blanket. Activities in respect of this project during the Quarter include:

| · | renovations of five classrooms, three offices, one computer laboratory, and one science laboratory at Sitezi Secondary School. The renovations include redoing skirting, aproning, and re-flooring for all the classrooms and laboratories, underpinning four classrooms that were unstable, roofing of all the classrooms, offices and laboratories. Electrical tubing was done for all the classrooms and laboratories and IT connections installed in the computer laboratory. |

| · | a new septic tank was installed and the soak-away constructed at the clinic. These two facilities will serve the whole clinic complex including the waiting mothers’ shelter that will be constructed. |

| · | the secondary school pumphouse was extended to create room for the new pump and engine. |

| · | a key component of the Sitezi project is the provision of solar power primarily to the clinic to maintain the cold chain for medical supplies and samples and to provide lighting and power for the schools. Clearing of the wayleave and setting up of the overhead power line began in the Quarter. |

| · | to ensure a secure and stable supply of water for the Sitezi irrigation scheme, Blanket continued supplying irrigation water to the garden from Smiler shaft. The water augmentation project to connect four boreholes to the garden began in the Quarter and excavation of the pipeline joining the four boreholes to the garden was completed. Electrical installations such as the overhead power line, the transformer, and distribution boxes were installed. Pipes were procured and the project is expected to be completed next quarter. |

Work on upgrading the Sabiwa Stadium to meet the requirements of the Zimbabwe Football Association for Division 1/Premier Soccer League stadia in the country continued. The stadium, which had been used exclusively by Sabiwa High School, will cater for footballing activities for the entire local community. Work on the stadium upgrade will be completed next quarter.

Blanket undertook road repairs of the old Gwanda Road, patching the potholes on the road, which developed because of the rains experienced early in the Quarter. The road was also graded and widened.

Under the conservation pillar, Dambari Wildlife Trust was granted $113,000 to carry out its work which also includes research. The grant is disbursed in tranches at given periods throughout the year upon request.

A dividend of $250,000 was paid to GCSOT in the Quarter. GCSOT has a 10% shareholding in Blanket.

| 4.3 | Gold Production - Blanket |

| Blanket Mine Production Statistics | |||||

| Year |

Tonnes Milled (t) |

Gold Head (Feed) Grade (g/t Au) |

Gold Recovery (%) |

Gold Produced (oz) | |

| Year | 2020 | 597,962 | 3.21 | 93.8 | 57,899 |

| Q 1 | 2021 | 148,513 | 2.98 | 93.0 | 13,197 |

| Q 2 | 2021 | 165,760 | 3.34 | 93.8 | 16,710 |

| Q 3 | 2021 | 179,577 | 3.48 | 94.2 | 18,965 |

| Q 4 | 2021 | 171,778 | 3.57 | 94.3 | 18,604 |

| Year | 2021 | 665,628 | 3.36 | 93.9 | 67,476 |

| Q1 | 2022 | 165,976 | 3.69 | 94.1 | 18,515 |

| Q2 | 2022 | 179,118 | 3.71 | 93.9 | 20,091 |

| Q3 | 2022 | 198,495 | 3.53 | 93.6 | 21,120 |

| Q4 | 2022 | 208,444 | 3.37 | 93.7 | 21,049 |

| Year | 2022 | 752,033 | 3.56 | 93.8 | 80,775 |

| Q1 | 2023 | 170,721 | 3.11 | 93.8 | 16,036 |

| Q2 | 2023 | 179,087 | 3.22 | 94.0 | 17,436 |

| July | 2023 | 71,419 | 3.63 | 93.6 | 7,829 |

| 18 |

Gold production for the Quarter was 13.2% lower than the comparative quarter due to the lower realised grades and the tonnes mined and milled being less than planned. Tonnes milled and grade are discussed in section 4.4 of this MD&A; gold recoveries are discussed in section 4.5 of this MD&A.

7,829 ounces of gold were produced in July, which equates to an annualised production rate of over 90,000 ounces and confirms the production rates required to achieve the guidance of between 75,000 - 80,000 ounces of gold in 2023.

| 4.4 | Underground - Blanket |

Tonnes milled in the Quarter were similar to the comparative quarter. The recovered grade for the Quarter was 13.3% lower than the exceptionally high-grade in the comparative quarter but was in-line with plan.

Lower than expected production in the Quarter was due to:

| · | a lack of flexibility in terms of available stoping faces due to lag in development at the beginning of the Quarter caused by flooding of the decline at Eroica. The situation improved when Eroica 870 and Blanket 750 sections came into full production in June 2023; |

| · | big boulders were experienced in Blanket Feudal 510, and Blanket Quartz Reef 320 due to sloughing of the hanging wall. This have been addressed by the introduction of draw point systems in the respective areas and removing the quartz schists with the ore bearing reef improving tonnage throughput; |

| · | poor fragmentation which resulted in an increased incidence of large boulders which required secondary blasting. This was addressed by reducing burden and spacing in long hole drilling and the adoption of emulsion for long hole blasting. Significant improvement was noted as the Quarter progressed; |

| · | tramming breakdowns on 14 level and 18 level which meant that broken ore could not be moved easily to surface. A track repair and maintenance action plan were initiated to address tracking logistics in the Quarter and the aging fleet of granby cars was refurbished and replaced: 10 new 2 tonne cars and 4 new 4 tonne cars were procured and dispatched underground to improve logistics. |

| · | commissioning problems with the ore pass system causing hold-ups at Central Shaft and resulted in long tramming distances as ore had to be transported to the No 4 Shaft ore pass system adversely affected hoisting availability. Several measures were put in place which include the development of ore pass inspection accesses on 30 and 34 level. Ore movement from ARS and Blanket 930 sections to No 6 Shaft was also introduced to improve efficiencies in logistics; and |

| · | tramming constraints due to large boulders at the 26-level grizzly. The introduction of ore movement to No 6 Shaft and a tipping point at 840m at AR South to screen for big boulders alleviated the challenge. The installation of a rock breaker which was completed in mid-July is part of the permanent solution to reducing the size of the boulders and improving logistics underground. |

The outlook is positive in terms of production output due to increased flexibility in mining areas and intensive on the job training and coaching, and management control systems initiatives that has been implemented in the second quarter and going forward to improve technical skills of all production employees focussing on the new employees and the poor performers.

| 4.5 | Metallurgical Plant |

Recoveries in the Quarter were 94.0% compared to 93.9% in the comparative quarter; the tail grade of 0.192g/t was lower than achieved in previous quarters and demonstrates the efficiency of the metallurgical plant in terms of overall recoveries.

| 4.6 | Production Costs |

A narrow focus on the direct costs of production (mainly labour, electricity and consumables) does not fully reflect the total cost of gold production. Accordingly, cost per ounce data for the Quarter and the comparative quarter have been prepared in accordance with the Guidance Note issued by the World Gold Council on June 23, 2013 and is set out in the table below on the following bases:

| 19 |

| i. | On-mine cost per ounce3, which shows the on-mine costs of producing an ounce of gold and includes direct labour, electricity, consumables and other costs that are incurred at the mine including insurance, security and on-mine administration; |

| ii. | All-in sustaining cost per ounce7, which shows the on-mine cost per ounce plus royalty paid, additional costs incurred outside the mine (i.e., at offices in Harare, Johannesburg and Jersey), costs associated with maintaining the operating infrastructure and resource base that are required to maintain production at the current levels (sustaining capital investment), the share-based expense (or credit) arising from the LTIP awards less silver by-product revenue; and |

| iii. | All-in cost per ounce7, which shows the all-in sustaining cost per ounce plus the costs associated with activities that are undertaken with a view to increasing production (expansion capital investment). |

| Cost per ounce of gold sold | ||||||||||||||||||||||||||||||||||||||||||||||||

| (US$/ounce) | ||||||||||||||||||||||||||||||||||||||||||||||||

| Bilboes Oxide Mine | Blanket Mine | Consolidated | ||||||||||||||||||||||||||||||||||||||||||||||

| 3 months ended June 30 | 6 months ended June 30 | 3 months ended June 30 | 6 months ended June 30 | 3 months ended June 30 | 6 months ended June 30 | |||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||||||||||||||||||||

| On-mine cost per ounce8 | 3,905 | - | 6,372 | - | 915 | 692 | 951 | 695 | 1,084 | 692 | 1,135 | 695 | ||||||||||||||||||||||||||||||||||||

| All-in sustaining cost per ounce8 | 4,005 | - | 6,470 | - | 1,198 | 984 | 1,204 | 918 | 1,357 | 984 | 1,383 | 918 | ||||||||||||||||||||||||||||||||||||

| All-in cost per ounce8 | 4,026 | - | 8,977 | - | 1,470 | 1,560 | 1,473 | 1,578 | 1,614 | 1,560 | 1,727 | 1,578 | ||||||||||||||||||||||||||||||||||||

A reconciliation of costs per ounce to IFRS production costs is set out in section 10.

On-mine cost

On-mine cost comprises labour, electricity, consumables, and other costs such as security and insurance. Production costs are detailed in note 7 to the Interim Financial Statements. On-mine costs include the procurement margin paid to CMSA and represents a fair value that Blanket would pay for consumables if they were sourced from a third party.

On-mine cost per ounce for the Quarter was 63.3% higher than the comparative quarter due to the increased production costs as discussed in section 3 of this MD&A.

All-in sustaining cost

All-in sustaining cost includes inter alia administrative expenses incurred outside Zimbabwe and excludes the intercompany procurement margin and the benefits of solar power as this reflects the consolidated cost incurred at the Group level. Accordingly, the all-in sustaining cost can only be calculated at a consolidated level and not at the level of individual operations. The all-in sustaining cost per ounce for the Quarter was 37.9% higher than the comparative quarter due to the higher on mine costs as discussed in section 3 of this MD&A which was mitigated by lower sustaining capital expenditure and an increase in the intercompany procurement margin (which is deducted from on-mine costs for the purposes of calculating the consolidated AISC).

________________________

3On-mine cost per ounce, all-in sustaining cost per ounce and all-in cost per ounce are non-IFRS measures. Refer to section 10 for a reconciliation of these amounts to IFRS.

| 20 |

All-in cost

All-in cost includes investment in expansion projects at Blanket and Bilboes which remained at a high level in the Quarter due to the continued investment, as discussed in section 4.7 of this MD&A. All-in cost does not include pre-feasibility investment in exploration and evaluation projects.

| 4.7 | Capital Projects - Blanket |

The main capital development project is the infrastructure which will allow for three new production levels (26, 30 and 34 levels) below the current operations; a fourth level (38 level) to be added in due course via a twin decline that commenced in February this year. 5,207 development metres were achieved in the Quarter compared to 4,160 metres in the previous quarter.

Work on key development areas in the Quarter is detailed below:

| · | 30 and 34 level Central Shaft development: The northern and southern haulages on 30 and 34 level progressed well for the Quarter with a total of 547m. The 30 level northern haulage is within 180m of reaching the Eroica orebody and has been put on the priority ends list for the third quarter. |

| · | Eroica decline 3: The decline development has been behind schedule due to logistical issues but in the Quarter there was an improvement with an advance of 107.8m. Issues of flooding, and air, and water supply challenges affected the advances. The decline reached 885m and in the third quarter the target is to reach 900m. Decline development will be stopped to cater for up-dip development from 990m (30 level), which is expected to result in a saving against planned capital expenditure. |

| · | 930 2 Orebody Hanging Wall Haulage (“2OBHW”): The development of the haulage was slowed down during the Quarter due to waste handling challenges because of the ore pass hold-ups at Central Shaft but the overall advance was 127.8m. The haulage will continue so that the southern extension of the 2OBHW can be exposed for production. The haulage is also important for the establishment of an access crosscut to link 6 Shaft on 930m. |

| · | 34 – 38 level twin declines: The twin declines are earmarked to access the Blanket orebodies on 38 level. The development of the declines will open up mining opportunities below 34 level with one serving as an access route where a chairlift system will be installed, and the other as a return airway system where a conveyor system will be installed. In the Quarter a total advance of 214m was achieved. |

| · | 35 level Central Shaft: At 35 level Central Shaft the construction of the bulkheads below tip 1 and tip 2 were completed at the start of the Quarter. The 34 and 35 level clear and dirty water dams are still under construction and are expected to be completed by the end of the third quarter. |

| · | 35 level conveyor: The conveyor loading system which was powered by compressed air was successfully converted to a hydraulic operated system during the Quarter. The outstanding work is the subsequent conversion of the spillage loading system from compressed air to hydraulics. |

The existing TSF at Blanket is reaching the end of its life accordingly a new TSF is required to allow production to continue. The design parameters for the new facility include:

| · | capacity of 13 million tonnes which is anticipated to be adequate for 14 years of production at current deposition rate; |

| · | “upstream” design, due to the limited space; |

| · | clear water dam and tailings facility will be lined with a double lining (geotextile and clay liner) and polyurethane liner respectively to avoid contamination of ground water; |

| · | the design includes new piping and new pumps for a gland service water and return water system with instrumentation; |

| · | new boreholes for monitoring around the facility; and |

| · | a waste embankment between the TSF and the village for dust prevention. |

| 21 |

The anticipated cost of the new TSF is $25.1 million which will be incurred over 3 years. Work on the TSF commenced in March 2023 and it is expected that the first phase of the project will be completed in the third quarter of 2023 to allow limited deposition on the new TSF in parallel with further deposition onto the existing TSF until it reaches its maximum capacity.

| 4.8 | Indigenisation |

Transactions that implemented the indigenisation of Blanket (which expression in this section and in certain other sections throughout this MD&A refers to the Zimbabwe company that owns Blanket) were completed on September 5, 2012 following which Caledonia owned 49% of Blanket and received a Certificate of Compliance from the Zimbabwe Government which confirms that Blanket is fully compliant with the Indigenisation and Economic Empowerment Act.

Following the appointment of President Mnangagwa in 2017 the requirement for gold mining companies to be indigenised was removed by a change in legislation with effect from March 2018. On November 6, 2018, the Company announced that it had entered into a sale agreement with Fremiro Investments (Private) Limited (“Fremiro”) to purchase Fremiro’s 15% shareholding in Blanket for a gross consideration of $16.7 million which was to be settled through a combination of the cancellation of the loan between the two entities which stood at $11.5 million as at June 30, 2018 and the issue of 727,266 new shares in Caledonia at an issue price of $7.15 per share. This transaction was completed on January 20, 2020 following which Caledonia has a 64% shareholding in Blanket and Fremiro held approximately 6.3% of Caledonia’s enlarged issued share capital.

As a 64% shareholder, Caledonia receives 64% of Blanket’s dividends plus the repayment of vendor facilitation loans which were extended by Blanket to certain of the indigenous shareholders. The outstanding balance of the facilitation loans at June 30, 2023 was $13.4 million (December 31, 2022: $15 million). The facilitation loans (including interest thereon) are repaid by way of dividends from Blanket; 80% of the dividends declared by Blanket which are attributable to the beneficiaries of the facilitation loans are used to repay such loans and the remaining 20% unconditionally accrues to the respective indigenous shareholders. The dividends attributable to GCSOT, which holds 10% of Blanket, were withheld by Blanket to repay the advance dividends which were paid to GCSOT in 2012 and 2013.

The final payment to settle the advance dividend loan to GCSOT was made on September 22, 2021. Dividends to GCSOT after that date are unencumbered.

The facilitation loans are not shown as receivables in Caledonia’s financial statements in terms of IFRS. These loans are effectively equity instruments as their only means of repayment is via dividend distributions from Blanket. Caledonia continues to consolidate Blanket for accounting purposes. Further information on the accounting effects of indigenisation at Blanket is set out in note 6 to the Interim Financial Statements.

| 22 |

| 4.9 | Bilboes |

Sulphides feasibility study

The main objective at Bilboes is to construct a large, open-pit operation to extract sulphide mineralisation. A feasibility study in respect of the Bilboes sulphide project was prepared by the previous owners which targeted mine and processing operations to produce an average of 168,000 ounces of gold per annum over a 10-year mine life. Caledonia has commissioned its own feasibility study for the sulphide project reflecting the prevailing economic environment for capital and operating costs and a revised outlook for the gold price. The feasibility study will identify the most judicious way to commercialise the project in terms of maximising the uplift in value for Caledonia shareholders and this may result in the project potentially being implemented on a phased basis.

Oxide mining activities

In the fourth quarter of 2022, a small operation was started to mine and process oxide mineralisation at Bilboes. The oxide mining activities were restarted predominantly with the objective to generate cash flows to pay for the existing cost structures at Bilboes Holdings (Private) Limited (“Bilboes Holdings”), the operating company for Bilboes, and this would have an added benefit of reducing the waste-stripping required for the later planned sulphide project. The oxide mine was expected to produce between 12,500 and 17,000 ounces of gold in 2023 at an on-mine cost of between $1,200 and $1,320 per ounce.

In the preceding quarter the target mineralisation area which had been identified using old information obtained from the previous owners (i.e. not the vendors from whom Caledonia purchased the project) was found not to exist. Mining activity moved to other target areas in the Quarter where the target oxide mineralisation is based on relatively recent drill data for the oxide mineralisation. However, the large amount of waste-stripping that needed to be done to access the oxide production areas proved too costly. A decision was made to halt the mining of oxides at the end of September 2023 and continue when the waste-stripping for the sulphide project commences, as was the intention in the original plan of the feasibility study. Notice of termination of the oxide mining has been served on the contractor and mining will stop at the end of September 2023 and leaching of ore placed on the heap leach will continue until December 2023.

Production guidance for the oxide mining activities was withdrawn in the Quarter.

| Bilboes Oxides: Operating Statistics | |||

| 6 months to June 30, 2023 | 3 months to June 30, 2023 | ||

| Waste mined | (t) | 1,500,572 | 952,852 |

| Ore mined | (t) | 93,886 | 89,206 |

| Ore grade | (g/t) | 1.17 | 1.19 |

| Contained gold | (g) | 109,484 | 105,740 |

| Gold sales | (g) | 36,497 | 33,476 |

| Gold sales | (oz) | 1,181 | 1,076 |

| Strip Ratio | 16 | 11 | |

| 23 |

| 4.10 | Zimbabwe Commercial Environment |

Monetary Conditions

The current situation in Zimbabwe can be summarized as follows:

| · | Although there continues to be a shortage of foreign currency in Zimbabwe, Blanket has had satisfactory access to foreign exchange to date. |

| · | The rate of local currency (known as “RTGS Dollars” or “RTGS$”) annual inflation increased from 61% by January 2022 to 105% by June 2023. A high rate of RTGS$ inflation has little effect on Blanket’s operations because Blanket’s employees are paid in US Dollars and a large portion of Blanket’s other inputs are denominated in US Dollars. |

| · | Since October 2018, bank accounts in Zimbabwe have been bifurcated between Foreign Currency Accounts (“FCA”), which can be used to make international payments, and RTGS$ accounts which can only be used for domestic transactions. |

| · | On February 20, 2019 the RBZ allowed limited inter-bank trading between currency held in the RTGS$ system and the FCA system. Prior to this, the RBZ had stipulated that a Dollar in the RTGS$ system was worth 1 US Dollar in the FCA system. The interbank exchange rate at each quarter end since the introduction of the interbank rate in February 2019 is set out below. The very large devaluation of the RTGS$ in the Quarter resulted in foreign exchange losses arising on receivables denominated in RTGS$ - mainly amounts owing in respect of the RTGS$ component of revenues and the VAT refund receivable. |

|

Interbank Exchange Rates (RTGS$:US$1) |

|||

| February 20, 2019 | 2.50 | ||

| March 31, 2019 | 3.00 | ||

| June 30, 2019 | 6.54 | ||

| September 30, 2019 | 15.09 | ||

| December 31, 2019 | 16.77 | ||

| March 31, 2020 | 25.00 | ||

| June 30, 2020 | 57.36 | ||

| September 30, 2020 | 81.44 | ||

| December 31, 2020 | 81.79 | ||

| March 31, 2021 | 84.40 | ||

| June 30, 2021 | 85.42 | ||

| September 30, 2021 | 87.67 | ||

| December 31, 2021 | 108.66 | ||

| March 31, 2022 | 142.42 | ||

| June 30, 2022 | 370.96 | ||

| September 30, 2022 | 621.89 | ||

| December 31, 2023 | 684.33 | ||

| March 31, 2023 | 913.67 | ||

| June 30, 2023 | 5,739.80 | ||

| July 31, 2023 | 4,511.93 | ||

| · | In June 2021 the RBZ announced that companies whose shares are listed on the VFEX will receive 100% of the revenue arising from incremental production in US Dollars. Blanket subsequently received confirmation that the “baseline” level of production for the purposes of calculating incremental production is 148.38 kg per month (approximately 57,000 ounces per annum). In addition, the payment of the increased US Dollar proceeds for incremental production was backdated to July 1, 2021. As Blanket has increased its production from approximately 58,000 ounces of gold in 2020 to 80,000 ounces of gold, a listing on the VFEX meant at the time that Blanket received approximately 71.5% of its total revenues in US Dollars and the balance in local currency. Accordingly in December 2021 Caledonia obtained a secondary listing on the VFEX. Blanket has received all amounts due in terms of the policy until it changed on February 6, 2023. |

| 24 |

| · | On February 3, 2023, the RBZ issued Exchange control directive RY002/2023 stating that with effect from February 6, 2023, the US$ export retention threshold across all sectors, including companies listed on the VFEX, had been standardized to 75% of export proceeds. The incremental export incentive scheme was also discontinued with effect from February 1, 2023. The Company is currently awaiting formal confirmation from the RBZ that the directive RY002/2023 does not apply to new projects and therefore the Bilboes project would be able to keep 100% of its revenues in US Dollars. |

| · | Throughout these developments and to the date of issue of the Interim Financial Statements the US Dollar has remained the primary currency in which the Group’s Zimbabwean entities operate and the functional currency of these entities. |

| · | Since listing on the VFEX and following completion of the Bilboes acquisition, Caledonia has evaluated various avenues to achieve the direct export of its gold. In April 2023 the Company successfully implemented a mechanism whereby gold produced by Blanket is exported directly by Caledonia to a refiner outside Zimbabwe, which makes payment directly into Caledonia's bank account in Zimbabwe. Unrefined gold continues to be processed at FGR, a subsidiary of RBZ, on a toll-treatment basis, in accordance with requirements of the Zimbabwe government for in-country refining and to allow the Zimbabwe authorities full visibility over the gold produced and exported by Caledonia. From April 2023, Blanket has exported gold under the gold dealing licence that is held by FGR to a refinery outside Zimbabwe which undertakes the final refining process and sells the gold on behalf of Caledonia. Caledonia receives the proceeds of the gold sales directly into its bank account in Zimbabwe within a few days of delivery to the final refiner. This arrangement in respect of production from Blanket Mine complies with the current requirements to pay a 5% royalty and that Blanket continues to receive 75% of its revenues in US Dollars and the balance in local currency. |

| · | Management believes this new sales mechanism reduces the risk associated with selling and receiving payment from a single refining source in Zimbabwe. It also creates the opportunity to use more competitive offshore refiners and it may allow for the Company to raise debt funding secured against offshore gold sales. |

Electricity supply

The poor quality of electricity supply from the Zimbabwe Electricity Supply Authority (“ZESA”) is the most significant production risk at Blanket. During the Quarter, Blanket experienced interruptions to its power supply from the grid due to an imbalance between electricity demand and supply.

The supply from the grid is also subject to frequent surges and dips in voltage which, if not controlled, may cause severe damage to Blanket’s electrical equipment. The continued deterioration in the ZESA supply means that the power factor regularly fell to 60%, which meant that Blanket was effectively paying for 100% of the power but received only 60% and the power supply is subject to outages.

In the absence of equipment to control these surges, Blanket needs to switch to diesel power to allow mining and processing activity to continue, but generator use increases production costs and capital expenditure.

The following initiatives have been implemented by Blanket to alleviate the power challenges:

| · | Over recent years increased its diesel generating capacity to 18MW of installed capacity which was sufficient to maintain all operations and capital projects but only on a stand-by basis. |

| · | Installed two 10MVA auto tap transformers on the ZESA supply line to protect equipment at No. 4 Shaft and the main metallurgical plant from voltage fluctuations on the incoming grid supply. |

| · | Two further 10MVA auto tap transformers were installed to protect equipment at Central Shaft |

| · | Caledonia’s 12.2 MWac solar plant, fully commissioned in early February 2023, provides approximately 24% of Blanket’s average daily electricity demand. The plant has been providing power to Blanket from its initial connection to the Blanket grid in November 2022. The project was completed at a cost of $14.2 million in 2023 (cost includes construction costs and other project planning, structuring, funding and administration costs). This is discussed further in section 4.13. |

| 25 |

| · | In April 2023 Blanket entered into a power supply agreement with the IEUG and the Zimbabwean power utility to allow the IEUG to obtain power outside of Zimbabwe and strengthen the Zimbabwean power grid. As a result of this arrangement, Blanket has paid a lower tariff for IEUG supplied energy from April 2023 but it has not improved the power quality received at Blanket due to the continued difficulty with the Zimbabwe grid. |

Management is investigating options to alleviate the instability in the utility supply and further reduce the cost of diesel generator usage to supplement low voltage occurrences and power outages.

Water supply

Blanket uses water in the metallurgical process. Blanket is situated in a semi-arid region and rainfall typically only occurs in the period November to February. The 2022/2023 rainy season has been adequate, and management believes the water supply is satisfactory.

Taxation

The main elements of the Zimbabwe tax regime insofar as it affects Blanket and Caledonia are as follows:

| · | A royalty is levied on gold revenues at a rate of 5% if the gold price is above $1,200 per ounce; a royalty rate at 3% applies if the gold price is below $1,200. With effect from January 1, 2020, the royalty is allowable as a deductible expense for the calculation of income tax. On October 9, 2022, the Zimbabwean government announced that 50% of royalty payments will be payable in gold. The announcement was effective October 1, 2022 but no guidance has been received from government on how this will be implemented. Management does not expect a material effect due to this announcement. |

| · | With effect from February 4, 2022 the 5% royalty was payable in the same proportions of currencies as revenues are received. |

| · | Income tax is levied at 24.72% (2022: 24.72%) on taxable income as adjusted for tax deductions. The main adjustments to taxable income for the purposes of calculating tax are the add-back of depreciation and most of the management fees paid by Blanket to CMSA. 100% of all capital expenditure incurred in the year of assessment is allowed as a deductible expense. As noted above, the royalty is deductible for income tax purposes with effect from January 1, 2020. The calculation of taxable income is performed using financial accounts prepared in USD and RTGS$ with actual payments split between USD and RTGS$ based on the proportions in which income was received. Large devaluations in the RTGS$ to the USD reduce the deferred tax liability a significant portion of which was translated at a rate of 1USD:1RTGS$. |

| · | Withholding tax is levied on certain remittances from Zimbabwe i.e., dividend payments from Zimbabwe to the UK and payments of management fees from Blanket to CMSA. |

| 26 |

| 4.11 | Solar project |

As noted in section 4.10, Blanket suffers from unstable grid power and load shedding which results in frequent and prolonged power outages. In late 2019 Caledonia initiated a tender process to identify parties to make proposals for a solar project to reduce Blanket’s reliance on grid power. In 2020, the Caledonia board approved the project and the Company raised $13 million (before commission and expenses) to fund the project through the sale of 597,963 shares at an average price of $21.74 per share. Caledonia’s 12.2 MWac solar plant was connected to the Blanket grid in November, 2022 and was fully commissioned in early February 2023 at a construction cost of $14.2 million.

At the date of the approval of this MD&A the plant provides approximately a quarter of Blanket’s total electricity requirement during the day.

In December 2022, the Caledonia board approved a proposal for CMS (which owns the solar plant) to issue bonds up to a value of $12 million. The decision was taken to optimise the capital structure of the Group and provide additional debt instruments to the Zimbabwean financial market. The bonds have an interest rate of 9.5% payable bi-annually and have a tenor of 3 years from the date of issue. The bond repayments are guaranteed by the Company and up to the date of this MD&A $7 million of bonds have been issued to Zimbabwean commercial entities by CMS.

| 4.12 | Opportunities and Outlook |

Production Guidance

Consolidated production guidance for Blanket in 2023 is unchanged at between 75,000 - 80,000 ounces. Production guidance of 12,500 - 17,000 ounces from the Bilboes oxide mine was withdrawn in April 2023.

This is forward looking information as defined by National Instrument 51-102. Refer to section 18 of this MD&A for further information on forward looking statements.

Cost Guidance

The on-mine cost per ounce at Blanket in the Quarter was $915 which is higher than the guidance range of $770 to $850 per ounce. It is expected that on-mine cost per ounce at Blanket will reduce over the remainder of the year as production increases. Accordingly, this guidance is maintained for the year to December 31, 2023.

Guidance for cost per ounce at the Bilboes oxide mine is withdrawn as production guidance has also been withdrawn.

Guidance for consolidated AISC per ounce was between $1,150 and $1,250 per ounce. AISC is significantly affected by activities at the Bilboes oxide mine in respect of which production and cost guidance has been withdrawn. Accordingly, guidance for AISC is re-stated to exclude production and related production costs at Bilboes oxide mine. AISC excluding bilboes oxides is expected to be in the range of $1,050 to $1,150 per ounce.

This is forward looking information as defined by National Instrument 51-102. Refer to section 18 of this MD&A for further information on forward looking statements.

| 27 |

Capital Expenditure

Capital expenditure at Blanket in 2023 is budgeted to be $31.3 million (inclusive of CMSA’s mark-up). Capital expenditure includes:

| · | New TSF (first phase) - $12.7 million; |

| · | Capital development at 30 and 34 levels - $9.8 million; |

| · | Utilities for the Central Shaft infrastructure - $3.3 million; |

| · | Information technology infrastructure - $1 million; |

| · | Mill and surface engineering - $2.6 million; and |

| · | Staff housing - $500,000. |

In addition, the proceeds of the equity raises are expected to be used for the Bilboes feasibility study, starting a shared services centre in Zimbabwe, establishing an international procurement arm to supply future operations, and furthering exploration drilling at Motapa and Maligreen.

Strategy

The immediate strategic focus is to:

| · | maintain production at Blanket at the targeted range of 75,000 - 80,000 ounces for 2023; |

| · | continue deep level drilling at Blanket with the objective of further upgrading inferred mineral resources, thereby extending the life of mine; |

| · | complete the Caledonia feasibility study on the Bilboes sulphide project to determine the best implementation strategy and estimate the funding requirements and commence development of the sulphide project; and |

| · | commence exploration at Motapa. |

| 5 | EXPLORATION |

Caledonia’s exploration activities are focussed on Blanket and Motapa.

Blanket

Encouraging results were received during the Quarter from the ongoing underground drilling program at Blanket Mine which currently targets the Eroica ore body. Initial results indicate that the Eroica ore body has better grades and widths than expected.

Highlights of the results include:

| Hole Identifier | Orebody Name * | Orebody Intersection | Core Length (m) | True width (m) | Gold Grade (g/t) | Orebody Intersection depth from surface (m) | End of Hole Depth (m) | ||

| From (m) | To (m) | ||||||||

| ERC750EX2303 | ERCN_HW | 262.7 | 278.3 | 15.6 | 8.6 | 15.56 | 891.4 | 356.3 | |

| ERC750EX2301 | ERCN_HW | 263.8 | 281.2 | 17.4 | 13.44 | 6.62 | 914.9 | 352.2 | |

| ERC750EX2206 | ERCN_HW | 203.9 | 246.5 | 42.6 | 22.32 | 4.03 | 870.3 | 281.3 | |

* ERCN_HW - Eroica North Hanging Wall

| 28 |

The complete drilling results and locations are provided on the Company website: https://polaris.brighterir.com/public/caledonia_mining/news/rns_tool/story/w3j603x.