UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| [X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2017

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-37769

VBI VACCINES INC.

(Exact name of registrant as specified in its charter)

| British Columbia, Canada | N/A | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

222 Third Street, Suite 2241 Cambridge, Massachusetts |

02142 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 617-830-3031

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] (Do not check if a smaller reporting company) | Smaller reporting company [X] |

| Emerging growth company [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Common Shares, no par value per share | 40,060,622 |

| (Class) | Outstanding at May 11, 2017 |

VBI VACCINES INC.

FORM 10-Q FOR THE QUARTERLY PERIOD ENDED MARCH 31, 2017

TABLE OF CONTENTS

| 2 |

SPECIAL

NOTE REGARDING FORWARD-LOOKING STATEMENTS AND OTHER INFORMATION

CONTAINED IN THIS REPORT

This quarterly report on Form 10-Q (this “Form 10-Q”) contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and the provisions of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. You can find many (but not all) of these statements by looking for words such as “approximates,” “believes,” “hopes,” “expects,” “anticipates,” “estimates,” “projects,” “intends,” “plans,” “would,” “should,” “could,” “may,” or other similar expressions in this Form 10-Q. In particular, these include statements relating to future actions; prospective products, applications, customers and technologies; future performance or results of anticipated products; anticipated expenses; and projected financial results. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our historical experience and our present expectations or projections. Factors that could cause actual results to differ from those discussed in the forward-looking statements include, but are not limited to:

| ● | the timing of, and our ability to, obtain and maintain regulatory approvals for our products and product candidates; | |

| ● | the timing and results of our ongoing and planned clinical studies for our cytomegalovirus (CMV) vaccine candidate (VBI-1501) and clinical studies for our third generation hepatitis-B vaccine (Sci-B-Vac™); | |

| ● | our planned clinical studies for our glioblastoma multiforme (GBM) vaccine candidate; | |

| ● | our estimate regarding the amount of funds we require to continue our investments in our immuno-oncology and infectious disease vaccine candidate pipeline; | |

| ● | the potential benefit of strategic partnership agreements and our ability to enter into strategic partnership arrangements; | |

| ● | our commercialization, marketing and manufacturing capabilities and strategy; | |

| ● | our ability to license our intellectual property; | |

| ● | our ability to maintain a good relationship with our employees; | |

| ● | the suitability and adequacy of our office, manufacturing and research facilities and our ability to secure term extensions or expansions of leased space; | |

| ● | our ability to manufacture, or to have manufactured, any product we develop; | |

| ● | our history of losses; | |

| ● | our ability to eventually generate revenues and achieve profitability; | |

| ● | our limited operating history as a public company; | |

| ● | emerging competition and rapidly advancing technology in our industry that may outpace our technology; | |

| ● | eventual customer demand for the products we are currently developing; | |

| ● | the impact of competitive or alternative products, technologies and pricing; | |

| ● | general economic conditions and events and the impact they may have on us and our potential customers; | |

| ● | our ability to obtain adequate financing in the future, as and when we need it; |

| 3 |

| ● | our ability to continue as a going concern; | |

| ● | our success at managing the risks involved in the foregoing items; and | |

| ● | other factors discussed in this Form 10-Q. |

We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have included important factors in the cautionary statements included in this Form 10-Q, particularly in the “Risk Factors” section, that we believe could cause actual results or events to differ materially from the forward-looking statements that we make. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make or collaborations or strategic partnerships we may enter into.

You should read this Form 10-Q and the documents that we have filed as exhibits to this Form 10-Q completely and with the understanding that our actual future results may be materially different from what we expect. We do not assume any obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Unless otherwise stated or the context otherwise requires, the terms “VBI,” “we,” “us,” “our” and the “Company” refer to VBI Vaccines Inc. and its subsidiaries.

Unless indicated otherwise, all references to the U.S. Dollar, Dollar or $ are to the United States Dollar, the legal currency of the United States of America and all references to € mean Euros, the legal currency of the European Union. We may also refer to NIS, which is the New Israeli Shekel, the legal currency of Israel, and the Canadian Dollar or CAD, which is the legal currency of Canada.

Except for per share amounts or as otherwise specified to be in millions, amounts presented are stated in thousands.

| 4 |

| Item 1. | Condensed Consolidated Financial Statements |

VBI Vaccines Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(in thousands, except number of shares)

| March 31, 2017 | December 31, 2016 | |||||||

| (Unaudited) | ||||||||

| CURRENT ASSETS | ||||||||

| Cash | $ | 23,509 | $ | 32,282 | ||||

| Accounts receivable, net | 43 | 10 | ||||||

| Inventory, net | 959 | 830 | ||||||

| Other current assets | 1,272 | 1,236 | ||||||

| Total current assets | 25,783 | 34,358 | ||||||

| NON-CURRENT ASSETS | ||||||||

| Long-term deposits | 171 | 167 | ||||||

| Other long term assets | 555 | 487 | ||||||

| Property and equipment, net | 2,053 | 1,850 | ||||||

| Intangible assets, net | 59,977 | 59,507 | ||||||

| Goodwill | 8,450 | 8,385 | ||||||

| Total non-current assets | 71,206 | 70,396 | ||||||

| TOTAL ASSETS | $ | 96,989 | $ | 104,754 | ||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | 1,480 | $ | 2,018 | ||||

| Other current liabilities | 6,304 | 5,562 | ||||||

| Deferred revenues | - | 34 | ||||||

| Total current liabilities | 7,784 | 7,614 | ||||||

| NON-CURRENT LIABILITIES | ||||||||

| Long-term debt, net of debt discount of $3,056 and $3,344, respectively | 12,244 | 11,956 | ||||||

| Long-term deferred tax liability | - | 428 | ||||||

| Liabilities for severance pay | 433 | 356 | ||||||

| Deferred revenues, net of current portion | 669 | 669 | ||||||

| Total non-current liabilities | 13,346 | 13,409 | ||||||

| COMMITMENTS AND CONTINGENCIES (NOTE 10) | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common shares (unlimited authorized; no par value) (40,060,622 and 40,018,495 shares issued and outstanding at March 31, 2017 and December 31, 2016, respectively) | 133,410 | 133,312 | ||||||

| Additional paid-in capital | 59,137 | 58,595 | ||||||

| Accumulated other comprehensive income loss | (3,070 | ) | (3,196 | ) | ||||

| Accumulated deficit | (113,618 | ) | (104,980 | ) | ||||

| Total stockholders’ equity | 75,859 | 83,731 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 96,989 | $ | 104,754 | ||||

See accompanying Notes to Condensed Consolidated Financial Statements

| 5 |

VBI Vaccines Inc. and Subsidiaries

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

(in thousands, except per share data)

| For

the Three Months Ended March 31 | ||||||||

| 2017 | 2016 | |||||||

| Revenues | $ | 127 | $ | 48 | ||||

| Operating expenses: | ||||||||

| Cost of revenue | 1,275 | 377 | ||||||

| Research and development | 4,654 | 254 | ||||||

| General and administration | 3,045 | 1,980 | ||||||

| Total operating expenses | 8,974 | 2,611 | ||||||

| Loss from operations | (8,847 | ) | (2,563 | ) | ||||

| Interest expense, net | (704 | ) | (25 | ) | ||||

| Foreign exchange gain | 482 | 1,509 | ||||||

| Loss before incomes taxes | (9,069 | ) | (1,079 | ) | ||||

| Income tax benefit | 431 | - | ||||||

| NET LOSS | $ | (8,638 | ) | $ | (1,079 | ) | ||

| Net loss per share of common shares, basic and diluted | $ | (0.22 | ) | $ | (0.06 | ) | ||

| Weighted-average number of common shares outstanding, basic and diluted | 40,026,270 | 18,914,986 | ||||||

| Other comprehensive income (loss): | ||||||||

| Foreign currency translation adjustments | 126 | (691 | ) | |||||

| COMPREHENSIVE LOSS | $ | (8,512 | ) | $ | (1,770 | ) | ||

See accompanying Notes to Condensed Consolidated Financial Statements

| 6 |

VBI Vaccines Inc. and Subsidiaries

Condensed Consolidated Statements of Stockholders’ Equity

(Unaudited)

(in thousands, except number of shares)

| Number of Common Shares | Share Capital | Additional Paid-in Capital | Accumulated Other Comprehensive Loss - Foreign Currency Translation Adjustments | Accumulated Deficit | Total Stockholders’ Equity | |||||||||||||||||||

| BALANCE AS OF DECEMBER 31, 2016 | 40,018,495 | $ | 133,312 | $ | 58,595 | $ | (3,196 | ) | $ | (104,980 | ) | $ | 83,731 | |||||||||||

| Stock-based compensation | 23,250 | 39 | 542 | - | - | 581 | ||||||||||||||||||

| Common shares issued for services | 12,500 | 43 | - | - | - | 43 | ||||||||||||||||||

| Common shares issued on exercise of stock options | 6,377 | 16 | - | - | - | 16 | ||||||||||||||||||

| Net loss | - | - | - | - | (8,638 | ) | (8,638 | ) | ||||||||||||||||

Foreign currency translation adjustments | - | - | - | 126 | - | 126 | ||||||||||||||||||

| BALANCE AS OF MARCH 31, 2017 | 40,060,622 | $ | 133,410 | $ | 59,137 | $ | (3,070 | ) | $ | (113,618 | ) | $ | 75,859 | |||||||||||

See accompanying Notes to Condensed Consolidated Financial Statements

| 7 |

VBI Vaccines Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(in thousands)

| For

the Three Months Ended March 31 | ||||||||

| 2017 | 2016 | |||||||

| CASH FLOWS FROM: | ||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

| Net loss | $ | (8,638 | ) | $ | (1,079 | ) | ||

| Adjustments to reconcile net loss to cash used in operating activities: | - | |||||||

| Depreciation and amortization | 171 | 132 | ||||||

| Deferred taxes | (431 | ) | - | |||||

| Stock-based compensation | 624 | - | ||||||

| Amortization of debt discount | 288 | - | ||||||

| Net change in operating working capital items, net of business acquisitions: | ||||||||

| (Increase) decrease in accounts receivable | (32 | ) | 174 | |||||

| (Increase) decrease in inventory | (78 | ) | (4 | ) | ||||

| (Increase) decrease in other current assets | (28 | ) | 68 | |||||

| (Decrease) increase in other long-term assets | (27 | ) | 3 | |||||

| (Decrease) increase in accounts payable | (609 | ) | 28 | |||||

| (Decrease) increase in deferred revenues, including related parties | (73 | ) | (806 | ) | ||||

| (Decrease) increase in other current liabilities | 589 | 88 | ||||||

| Net cash flows used in operating activities | (8,244 | ) | (1,396 | ) | ||||

| INVESTING ACTIVITIES | ||||||||

| Changes in long-term deposits | - | (27 | ) | |||||

| Purchase of property and equipment | (266 | ) | (106 | ) | ||||

| Net cash flows provided by investing activities | (266 | ) | (133 | ) | ||||

| FINANCING ACTIVITIES | ||||||||

| Proceeds from issuance of common shares for cash, upon exercise of stock options | 16 | - | ||||||

| Net cash flows provided by financing activities | 16 | - | ||||||

| Effect of exchange rates on cash | (279 | ) | 13 | |||||

| CHANGE IN CASH FOR THE PERIOD | (8,773 | ) | (1,516 | ) | ||||

| CASH, BEGINNING OF PERIOD | 32,282 | 12,476 | ||||||

| CASH, END OF PERIOD | $ | 23,509 | $ | 10,960 | ||||

| Supplementary information: | ||||||||

| Interest paid | $ | 450 | $ | 25 | ||||

| Capital expenditures included in other current liabilities | 76 | - | ||||||

See accompanying Notes to Condensed Consolidated Financial Statements

| 8 |

VBI Vaccines Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

(in thousands, except per share amounts)

| 1. | NATURE OF BUSINESS AND CONTINUATION OF BUSINESS |

Corporate Overview

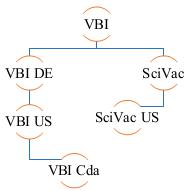

VBI Vaccines Inc. (formerly SciVac Therapeutics, Inc.) and its subsidiaries (collectively referred to as the “Company,” “we,” “us,” “our” or “VBI”) was incorporated under the laws of British Columbia, Canada on April 9, 1965.

The Company has the following wholly-owned subsidiaries, VBI Vaccines (Delaware) Inc., a Delaware corporation (“VBI DE”); VBI DE’s wholly-owned subsidiary, Variation Biotechnologies (US), Inc., a Delaware corporation (“VBI US”); Variation Biotechnologies, Inc. a Canadian company (“VBI Cda”) and the wholly-owned subsidiary of VBI US; SciVac Ltd. an Israeli company (“SciVac”); and SciVac USA, LLC. a Florida limited liability company (“SciVac US”) and the wholly owned subsidiary of SciVac.

The Company’s registered office is located at 1200 Waterfront Centre, 200 Burrard Street, Vancouver, Canada V6C 3L6 with its principal office located at 222 Third Street, Suite 2241, Cambridge, Massachusetts 02142. In addition, the Company has manufacturing facilities located in Rehovot, Israel and research facilities located in Ottawa, Ontario, Canada.

The Company operates in one segment and therefore segment information is not presented.

Principal Operations

We are a commercial stage biopharmaceutical company developing next generation vaccines to address unmet needs in infectious disease and immuno-oncology. VBI’s first marketed product is Sci-B-Vac™, a hepatitis B (“HBV”) vaccine that mimics all three viral surface antigens of the hepatitis B virus. Sci-B-Vac™ is approved for use in Israel and 14 other countries. Recently, VBI completed a post-marketing Phase IV clinical study in Israel to confirm a new in-house reference standard for regulatory and quality control purposes. Sci-B-Vac™ has not yet been approved by the U.S. Food and Drug Administration (the “FDA”), the European Medicines Agency (the “EMA”) or Health Canada (“HC”). VBI is currently developing a Phase III clinical program to obtain FDA, EMA, and HC market approvals for commercial sale of Sci-B-Vac™ in the United States, Europe, and Canada, respectively. Our wholly-owned subsidiary, SciVac Ltd., manufactures Sci-B-Vac™ in Rehovot, Israel.

Following our merger with VBI DE on May 6, 2016 (the “VBI-SciVac Merger”), we are also advancing our two platform technologies – our Enveloped Virus-Like Particle (“eVLP”) platform technology and our Lipid Particle Vaccine (“LPV”) technology. Our eVLP platform technology enables the development of enveloped virus-like particle vaccines that closely mimic the target virus to elicit a potent immune response. We are advancing a pipeline of eVLP vaccines, with lead programs in both infectious disease, with our congenital cytomegalovirus (“CMV”) vaccine, and in immuno-oncology, with our therapeutic glioblastoma multiforme (“GBM” or “glioblastoma”) vaccine candidate. Our LPV thermostability technology is a proprietary formulation of lipids and process that allows vaccines and biologics to preserve stability, potency, and safety at temperatures outside of the most common cold chain storage requirements of 2oC to 8 oC.

| 9 |

Liquidity and Going Concern

The Company has a limited operating history and faces a number of risks, including but not limited to, uncertainties regarding demand and market acceptance of the Company’s products and reliance on major customers. The Company anticipates that it will continue to incur significant operating costs and losses in connection with the development of its products.

The Company has an accumulated deficit of $113,618 as of March 31, 2017 and cash outflows from operating activities of $8,244 for the three months ended March 31, 2017.

The Company will require significant additional funds to conduct clinical and non-clinical studies, achieve regulatory approvals, and, subject to such approvals, commercially launch its products. The Company plans to finance future operations with a combination of existing cash reserves, proceeds from the issuance of equity securities, the issuance of additional debt, and revenues from potential collaborations, if any. There is no assurance the Company will manage to obtain these sources of financing. The above conditions raise substantial doubt about the Company’s ability to continue as a going concern. The report of our independent registered public accounting firm on our consolidated financial statements for the year ended December 31, 2016 contains an explanatory paragraph regarding our ability to continue as a going concern. The condensed consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result should the Company be unable to continue as a going concern.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

Basis of Presentation and Consolidation

The Company’s fiscal year ends on December 31 of each calendar year. The accompanying unaudited condensed consolidated financial statements have been prepared in U.S. dollars (“USD”) and pursuant to the rules and regulations of the United States Securities and Exchange Commission (“SEC”), the instructions to Form 10-Q and the provisions of Regulation S-X pertaining to financial statements. Accordingly, certain information and footnote disclosures normally included in the financial statements prepared in accordance United States of America generally accepted accounting principles (“U.S. GAAP”), have been condensed or omitted pursuant to such rules and regulations. The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenue and expenses during the reporting periods. Actual results could differ from these estimates and are not necessarily indicative of the results to be expected for any future period or the entire fiscal year. The December 31, 2016 consolidated balance sheet in this document was derived from the audited consolidated financial statements and does not include all of the disclosures required by U.S. GAAP. The condensed consolidated financial statements and notes included in this quarterly report on Form 10-Q (this “Form 10-Q”) should be read in conjunction with the financial statements and notes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2016 (the “2016 10-K”), as filed with the SEC on March 20, 2017.

The condensed consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries: SciVac, SciVac USA, and from May 6, 2016 the accounts of VBI DE, VBI US and VBI Cda. Intercompany balances and transactions between the Company and its subsidiaries are eliminated in the condensed consolidated financial statements.

In the opinion of management, these condensed consolidated financial statements include all adjustments and accruals of a normal and recurring nature necessary to fairly state the results of the periods presented. The results for periods are not necessarily indicative of results to be expected for the full year or for any future periods.

| 10 |

Significant Accounting Policies

The significant accounting policies used in the preparation of these condensed consolidated financial statements are disclosed in the 2016 10-K, and there have been no changes to the Company’s significant accounting policies during the three months ended March 31, 2017.

Foreign currency

The functional and reporting currency of the Company is the USD. Each of the Company’s subsidiaries determines its own respective functional currency, and this currency is used to separately measure each entity’s financial position and operating results.

Assets and liabilities of foreign operations with a different functional currency from that of the Company are translated at the closing rate at the end of each reporting period. Profit or loss items are translated at average exchange rates for all the relevant periods. All resulting translation differences are recognized as a component of accumulated other comprehensive loss.

Foreign exchange gains and losses arising from transactions denominated in a currency other than the functional currency of the entity involved, are included in operating results.

Use of Estimates

Preparation of the condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual amounts could differ from the estimates made. We continually evaluate estimates used in the preparation of the condensed consolidated financial statements for reasonableness. Appropriate adjustments, if any, to the estimates used are made prospectively based upon such periodic evaluation. The significant areas of estimation include determining the deferred tax valuation allowance, the estimated lives of property and equipment and intangible assets, the inputs in determining the fair value of equity based awards and warrants issued as well as the values ascribed to assets acquired and liabilities assumed in the business combination. Actual results may differ from those estimates.

Goodwill and In-Process Research and Development

The Company’s intangibles determined to have indefinite useful lives including in-process research and development (“IPR&D”) and goodwill, are tested for impairment annually, or more frequently if events or circumstances indicate that the assets might be impaired.

Goodwill represents the excess of the purchase price over the fair value of the net tangible and identifiable intangible assets acquired in a business combination. Such circumstances could include, but are not limited to: (1) a significant adverse change in legal factors or in business climate, (2) unanticipated competition, or (3) an adverse action or assessment by a regulator. When evaluating goodwill for impairment, we may first perform an assessment qualitatively whether it is more likely than not that a reporting unit’s carrying amount exceeds its fair value, referred to as a “step zero” approach. If, based on the review of the qualitative factors, we determine it is not more likely than not that the fair value of a reporting unit is less than its carrying value, we would bypass the two-step impairment test. If we conclude that it is more likely than not that a reporting unit’s fair value is less than its carrying amount, we would perform the first step (“step one”) of the two-step impairment test. Step 1 compares the fair value of the Company’s reporting unit to which goodwill was allocated to its carrying value. If the fair value of the reporting unit exceeds its carrying value, no further analysis is necessary. If the carrying amount of the reporting unit exceeds its fair value, Step 2 must be completed to quantify the amount of impairment. Step 2 calculates the implied fair value of goodwill by deducting the fair value of all tangible and intangible assets, excluding goodwill, of the reporting unit, from the fair value of the reporting unit as determined in Step 1. The implied fair value of goodwill determined in this step is compared to the carrying value of goodwill. If the implied fair value of goodwill is less than the carrying value of goodwill, an impairment loss, equal to the difference, is recognized. The Company has established August 31st as the date for its annual impairment test of goodwill.

| 11 |

The costs of rights to IPR&D projects acquired in an asset acquisition are expensed in the consolidated statements of operations unless the project has an alternative future use. These costs include initial payments incurred prior to regulatory approval in connection with research and development agreements that provide rights to develop, manufacture, market and/or sell pharmaceutical products.

IPR&D acquired in a business combination is capitalized as an intangible asset and tested for impairment at least annually until commercialization, after which time the IPR&D is amortized over its estimated useful life. The impairment test compares the carrying amount of the IPR&D asset to its fair value. If the carrying amount exceeds the fair value of the asset, such excess is recorded as an impairment loss.

Fair value measurements of financial instruments

Accounting guidance defines fair value as the price that would be received to sell an asset or paid to transfer a liability (the exit price) in an orderly transaction between market participants at the measurement date. The accounting guidance outlines a valuation framework and creates a fair value hierarchy in order to increase the consistency and comparability of fair value measurements and the related disclosures. In determining fair value, the Company uses quoted prices and observable inputs. Observable inputs are inputs that market participants would use in pricing the asset or liability based on market data obtained from independent sources.

The fair value hierarchy is broken down into three levels based on the source of inputs as follows:

Level 1 — Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities.

Level 2 — Valuations based on observable inputs and quoted prices in active markets for similar assets and liabilities.

Level 3 — Valuations based on inputs that are unobservable and models that are significant to the overall fair value measurement.

Financial instruments recognized in the condensed consolidated balance sheet consist of cash, accounts receivable and other current assets, accounts payable and other current liabilities. The Company believes that the carrying value of its current financial instruments approximates their fair values due to the short-term nature of these instruments. The Company does not hold any derivative financial instruments.

The carrying amounts of the Company’s long-term assets and long-term liabilities approximate their respective fair values.

At March 31, 2017 and December 31, 2016, the fair value of our outstanding debt is estimated to be approximately $15,419 and $15,012, respectively.

In determining the fair value of the long-term debt as of March 31, 2017 and December 31, 2016 the Company used the following assumptions:

| March 31, 2017 | December 31, 2016 | |||||||

| Long-term debt: | ||||||||

| Interest rate | 12.0 | % | 12.0 | % | ||||

| Discount rate | 11.5 | % | 13.5 | % | ||||

| Expected time to payment in months | 32 | 35 | ||||||

| 12 |

| 3. | NEW ACCOUNTING PRONOUNCEMENTS |

Recently Adopted Accounting Pronouncements

Stock Compensation

In March 2016, the Financial Accounting Standards Board (the “FASB”) issued Accounting Standards Update (the “ASU”) No. 2016-09, “Compensation - Stock Compensation (Topic 718),” which simplifies several aspects of the accounting for share-based payment award transactions, including the income tax consequences, classification of awards as either equity or liabilities, classification on the statement of cash flows and accounting for forfeitures. ASU No. 2016-09 is effective for fiscal years beginning after December 15, 2016, including periods within those fiscal years. Our adoption of this ASU in the first quarter of 2017 did not have a material impact on our condensed consolidated financial statements.

Cash Flow Classification

The FASB issued ASU 2016-15, an accounting standard that affects the classification of certain cash receipts and cash payments on the statement of cash flows. The standard provides guidance on eight issues: debt prepayment or extinguishment costs, settlement of zero-coupon bonds or bonds issued at a discount with insignificant cash coupon, contingent consideration payments made after a business combination, proceeds from the settlement of insurance claims, proceeds from the settlement of corporate-owned life insurance policies, distributions received from equity method investees, beneficial interests in securitization transactions, separately identifiable cash flows and applying the predominance principle. The standard is effective for public business entities for fiscal years beginning after December 15, 2017 including periods within those fiscal years.

The FASB issued ASU 2016-18, an accounting standard that requires companies to include cash and cash equivalents that have restrictions on withdrawal or use in total cash and cash equivalents on the statement of cash flows. The standard does not define restricted cash or restricted cash equivalents, but companies will need to disclose the nature of the restrictions. The standard is effective for public business entities for fiscal years beginning after December 15, 2017 including interim periods within those fiscal years.

Our adoption of these ASUs in the first quarter of 2017 did not have a material impact on our condensed consolidated financial statements.

Recently Issued Accounting Standards, not yet Adopted

Revenue from Contracts with Customers

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”). ASU 2014-09 outlines a single comprehensive model to use in accounting for revenue arising from contracts with customers and supersedes most current revenue recognition guidance, including industry-specific guidance. ASU 2014-09 also requires entities to disclose sufficient information, both quantitative and qualitative, to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. An entity should apply the amendments in this ASU using one of the following two methods: (1) retrospectively to each prior reporting period presented with a possibility to elect certain practical expedients, or, (2) on a modified retrospective basis with the cumulative effect of initially applying ASU 2014-09 recognized at the date of initial application. If an entity elects the latter transition method, it also should provide certain additional disclosures. For a public entity, the ASU as amended is effective for annual periods beginning after December 15, 2017, including interim reporting periods within that reporting period. Early application is permitted for periods beginning after December 15, 2016. Given the Company’s current level of revenue, we do not expect a significant impact from the adoption of this new accounting guidance on our financial statements and footnote disclosures.

Leases

In February 2016 the FASB issued ASU 2016-02: Leases. The ASU introduces a lessee model that results in most leases impacting the balance sheet by requiring reporting entities to recognize lease assets and lease liabilities for substantially all lease arrangements. The new standard also aligns many of the underlying principles of the new lessor model with those in ASC 606, the FASB’s new revenue recognition standard (e.g., those related to evaluating when profit can be recognized). Furthermore, the ASU addresses other concerns related to the current leases model. For example, the ASU eliminates the requirement in current U.S. GAAP for an entity to use bright-line tests in determining lease classification. The update is Effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. The Company is currently evaluating the impact this new guidance will have on our financial statements and related disclosures.

| 13 |

Accounting for Income Taxes on Intercompany Transfers

The FASB recently issued ASU 2016-16, an accounting standard that requires the seller and buyer to recognize at the transaction date the current and deferred income tax consequences of intercompany asset transfers. The FASB expects the new standard to cause volatility in companies’ effective tax rates, particularly for those that transfer intangible assets to subsidiaries. The standard is effective for public business entities for fiscal years beginning after December 15, 2017 including interim periods within those fiscal years. While the Company continues to assess the potential impact of this standard, the adoption of this standard is not expected to have a material impact on our financial statements.

Recognition and Measurement of Financial Assets and Financial Liabilities

In January 2016, the FASB issued ASU 2016-01, “Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities”. This update will change the income statement impact of equity investments held by an entity; disclosures related to fair value of financial instruments and presentation of financial assets and liabilities. ASU 2016-01 is effective for fiscal years beginning after December 15, 2017, including interim periods within those fiscal years. Entities must apply the standard using a cumulative-effect adjustment to the balance sheet as of the beginning of the fiscal year of adoption. Except for certain early application guidance, early adoption is not permitted. The Company is currently assessing the impact that adopting this new ASU will have on our financial statements and footnote disclosures.

Simplifying the Test for Goodwill Impairment

In January 2017, the FASB issued ASU 2017-04, “Intangibles – Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment” which has eliminated Step 2 from the goodwill impairment test. Under Step 2, an entity had to perform procedures to determine the fair value at the impairment testing date of its assets and liabilities following the procedure that would be required in determining the fair value of assets acquired and liabilities assumed in a business combination. Under the amendments in this update, an entity should perform its goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity should recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value. An entity still has the option to perform the qualitative assessment for a reporting unit to determine if the quantitative impairment test is necessary. ASU 2017-04 is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. While the Company continues to assess the potential impact of this standard, the adoption of this standard is not expected to have a material impact on its financial statements.

| 14 |

| 4. | INTANGIBLES |

| March 31, 2017 | ||||||||||||||||

| Gross

Carrying amount | Accumulated

Amortization | Currency Translation | Net

Book Value | |||||||||||||

| Patents | $ | 669 | $ | (349 | ) | $ | 17 | $ | 337 | |||||||

| IPR&D assets | 61,500 | - | (1,860 | ) | 59,640 | |||||||||||

| $ | 62,169 | $ | (349 | ) | $ | (1,843 | ) | $ | 59,977 | |||||||

| December 31, 2016 | ||||||||||||||||

| Gross

Carrying amount | Accumulated

Amortization | Currency Translation | Net

Book Value | |||||||||||||

| Patents | $ | 669 | $ | (334 | ) | $ | (4 | ) | $ | 331 | ||||||

| IPR&D assets | 61,500 | - | (2,324 | ) | 59,176 | |||||||||||

| $ | 62,169 | $ | (334 | ) | $ | (2,328 | ) | $ | 59,507 | |||||||

The Company amortizes intangible assets with finite lives on a straight-line basis over their estimated useful lives.

Amortization related to the IPR&D assets relate to the May 6, 2016 VBI-SciVac Merger and will not begin amortizing until the Company commercializes its products. Future costs incurred to extend the life of the patents will be expensed.

| 5. | LOSS PER SHARE OF COMMON SHARES |

Basic loss per share is computed by dividing net loss applicable to common stockholders by the weighted average number of shares of common shares outstanding during each period. Diluted loss per share includes the effect, if any, from the potential exercise or conversion of securities, such as warrants, and stock options, which would result in the issuance of incremental shares of common shares unless such effect is anti-dilutive. In computing the basic and diluted net loss per share applicable to common stockholders, the weighted average number of shares remains the same for both calculations due to the fact that when a net loss exists, dilutive shares are not included in the calculation as their effect would be anti-dilutive. These potentially dilutive securities are more fully described in Note 8, Stockholders’ Equity and Additional Paid-in Capital.

The following potentially dilutive securities outstanding at March 31, 2017 and 2016 have been excluded from the computation of diluted weighted average shares outstanding, as they would be antidilutive:

March 31, 2017 | March 31, 2016 | |||||||

| Warrants | 2,068,824 | - | ||||||

| Stock options and equity awards | 3,120,525 | - | ||||||

| 5,189,349 | - | |||||||

| 15 |

| 6. | LONG-TERM DEBT |

As at March 31, 2017 and the December 31, 2016, the unamortized debt discount is as follows:

March 31, 2017 | December 31, 2016 | |||||||

| Long-term debt, net of deferred financing costs and unamortized debt discount based on an imputed interest rate of 20.5% of $3,056 and $3,344 at March 31, 2017 and December 31, 2016, respectively | $ | 12,244 | $ | 11,956 | ||||

As a result of the VBI-SciVac Merger, the Company through VBI DE assumed a term loan facility with Perceptive Credit Holdings, LP (the “Lender”) in the amount of $6,000 (the “Facility”), with an initial advance of $3,000 drawn down on prior to the Merger. As of the merger date, the Company assumed an amount of $2,361 in the Facility. On December 6, 2016, the Company amended the Facility (the “Amended Facility”) and raised an additional $13,200 which was combined with the remaining balance from the Facility of $1,800. The total principal outstanding at March 31, 2017, including the $300 exit fee discussed below, is $15,300 before the net deferred financing costs and unamortized debt discount of $3,056. Borrowings under the Amended Facility are secured by all of VBI assets. The principal on the Amended Facility accrues interest at an annual rate equal to the greater of (a) one-month LIBOR (subject to a 5.00% cap) or (b) 1.00%, plus the Applicable Margin. The Applicable Margin will be 11.00%. The first eighteen months are interest only. The interest rate as of March 31, 2017 was 12%. Upon the occurrence of an event of default, and during the continuance, of an event of default, the Applicable Margin, defined above, will be increased by 4.00% per annum. This term loan facility matures December 6, 2019 and includes both financial and non-financial covenants, including a minimum cash balance requirement. The Company was in compliance with these covenants as of March 31, 2017. Pursuant to the Amended Facility, the Company agreed to appoint a representative of Perceptive Credit on our Board who is also a portfolio manager of the Company’s largest shareholder.

The Company’s obligations under the Amended Facility are secured on a senior basis by a lien on substantially all of the assets of the Company and its U.S. and Canadian subsidiaries and guaranteed by the Company and its U.S. and Canadian subsidiaries. The Amended and Restated Credit Agreement also contains customary events of default.

In connection with the Amended Facility, on December 6, 2016 the Company issued to the lender two tranches of warrants. The first tranche was a warrant to purchase 363,771 common shares at an exercise price of $4.13 per share and the second tranche was a warrant to purchase 1,341,282 common shares at an exercise price per share of $3.355. The total proceeds attributed to the warrants was $2,793 based on the relative fair value of the warrants as compared to the sum of the fair values of the warrants and debt. This resulted in the debt being issued at a discount. The Company incurred $360 of debt issuance costs and is required to pay an exit fee of $300 upon full repayment of the debt resulting in additional debt discount. The total debt discount of $3,453 is being charged to interest expense using the effective interest method over the term of the debt. As of March 31, 2017, the unamortized debt discount is $3,056. The Company recorded $288 of interest expense related to the amortization of the debt discount during the three months ended March 31, 2017.

The following table summarizes the future principal payments that the Company expects to make for long-term debt:

| Period

ending March 31, | Principal

payments on Amended Facility and exit fee | ||||

| 2017 | $ | - | |||

| 2018 | 1,600 | ||||

| 2019 | 13,700 | ||||

| $ | 15,300 | ||||

| 16 |

| 7. | DEFERRED REVENUE AND RELATED PARTY TRANSACTIONS |

| i. | Prior to the VBI-SciVac Merger, one of the Company’s directors was also the chairman of the board of Kevelt AS (“Kevelt”), a wholly owned subsidiary of OAO Pharmsynthez (“Pharmsynthez”), a shareholder of the Company and was also the chairman of the board of Pharmsynthez. Following the VBI-SciVac Merger, in accordance with the merger agreement, this director resigned. |

On April 26, 2013, SciVac entered into a Development and Manufacturing Agreement (“DMA”) with Kevelt, pursuant to which SciVac agreed to develop the manufacturing process for the production of clinical and commercial quantities of certain materials in drug substance form. On July 30, 2016, the Company received a letter of termination from Kevelt, in part containing a request for refund of $2.5 million it had previously transferred to the Company. | |

On March 28, 2017, the Company’s legal counsel provided the requested documentation, indicating that the amount owed to Kevelt is not $800 but rather $690 less any acquisition costs (as defined in the DMA). The Company’s legal counsel proposed a settlement together with mutual waivers of any claims whereby the Company would remit the original $800 as follows: 50% (i.e. $400) to be paid in cash and 50% (i.e. $400) through the issuance of the Company’s common shares. |

| ii. | SciVac entered into a services agreement with OPKO Biologics Ltd. (“OPKO Bio”), a wholly-owned subsidiary of OPKO Health, Inc., a related party shareholder of the Company, dated as of March 15, 2015 as amended on January 25, 2016, pursuant to which SciVac agreed to provide certain aseptic process filling services to OPKO Bio. The terms of the services agreement are based on market rates and comparable to other non-related party service agreements. |

See Note 6, for Facility from a lender that is also affiliated with the Company’s largest shareholder.

Three months ended March 31 | ||||||||

| 2017 | 2016 | |||||||

| Services revenues from related parties: | ||||||||

| OPKO Bio | $ | 1 | $ | 7 | ||||

Subsequent to the VBI-SciVac Merger on May 6, 2016, Kevelt and Pharmsynthez are no longer considered related parties due to the common shareholder no longer having significant influence.

| 17 |

| 8. | STOCKHOLDERS’ EQUITY AND ADDITIONAL PAID-IN CAPITAL |

Stock option plans

The Company’s stock option plans are approved by and administered by the Company’s board of directors (the “Board”) and its Compensation Committee. The Board designates, in connection with recommendations from the Compensation Committee, eligible participants to be included under the plan, and designates the number of options, exercise price and vesting period of the new options.

2006 VBI US Stock Option Plan

No further options will be issued under the 2006 VBI US Stock Option Plan (the “2006 Plan”). As at March 31, 2017, there were 1,314 options outstanding under the 2006 Plan.

2013 Stock Incentive Plan

No further options will be issued under the 2013 Equity Incentive Plan (the “2013 Plan”). As at March 31, 2017, there were 5 options outstanding under the 2013 Plan.

2014 Equity Incentive Plan

No further options will be issued under the 2014 Equity Incentive Plan (the “2014 Plan”). As at March 31, 2017, there were 735 options outstanding under the 2014 Plan.

2016 VBI Equity Incentive Plan

The 2016 VBI Equity Incentive Plan (the “2016 Plan”) is a rolling incentive plan that sets the number of common shares issuable under the 2016 Plan, together with any other security-based compensation arrangement of the Company, at a maximum of 10% of the aggregate common shares issued and outstanding on a non-diluted basis at the time of any grant under the 2016 Plan. The 10% maximum is inclusive of options granted under all equity incentive plans. The 2016 Plan is an omnibus equity incentive plan pursuant to which the Company may grant equity and equity-linked awards to eligible participants in order to promote the success of the Company following the VBI-SciVac Merger by providing a means to offer incentives and to attract, motivate, retain and reward persons eligible to participate in the 2016 Plan. Grants under the 2016 Plan include a grant or right consisting of one or more options, stock appreciation rights (“SARs”), restricted share units (“RSUs”), performance share units (“PSUs”), shares of restricted stock or other such award as may be permitted under the 2016 Plan. As at March 31, 2017, there were 411 options and 656 stock awards outstanding under the 2016 Plan.

The aggregate number of common shares remaining available for issuance for awards under this plan total 585 at March 31, 2017.

| 18 |

Activity related to stock options is as follows (in thousands, except for weighted average exercise price):

| Number of Stock Options | Weighted Average Exercise Price | |||||||

| Balance outstanding at December 31, 2016 | 2,168 | $ | 4.45 | |||||

| Granted | 316 | $ | 3.63 | |||||

| Exercised | (19 | ) | $ | 3.10 | ||||

| Balance outstanding at March 31, 2017 | 2,465 | $ | 4.36 | |||||

| Exercisable at March 31, 2017 | 1,396 | $ | 4.42 | |||||

| Options expected to vest at March 31, 2017 | 1,069 | $ | 4.29 | |||||

Information relating to restricted stock units is as follow (in thousands, except for weighted average fair value at grant date):

| Number of Stock Awards | Weighted Average Fair Value at Grant Date | |||||||

| Unvested shares outstanding at December 31, 2016 | 639 | $ | 3.88 | |||||

| Granted | 57 | $ | 4.72 | |||||

| Vested and exercised | (7 | ) | $ | 5.49 | ||||

| Forfeited | (33 | ) | $ | 3.90 | ||||

| Unvested shares outstanding at March 31, 2017 | 656 | $ | 3.93 | |||||

The fair value of the options expected to vest is recognized as an expense on a straight-line basis over the vesting period. The total stock-based compensation expense recorded in the three months ended March 31, 2017 and 2016 was as follows:

Three months ended March 31 | ||||||||

| 2017 | 2016 | |||||||

| Research and development | $ | 185 | $ | - | ||||

| General and administrative | 423 | - | ||||||

| Cost of revenues | 16 | - | ||||||

| Total stock-based compensation expense | $ | 624 | $ | - | ||||

| 19 |

| 9. | INCOME TAXES |

The Company operates in U.S., Israel and Canadian tax jurisdictions. Its income is subject to varying rates of tax, and losses incurred in one jurisdiction cannot be used to offset income taxes payable in another.

The Company determines its annual effective tax rate at the end of each interim period based on the year to date period results. Since the Company is incorporated in Canada, it is required to use Canada’s statutory tax rate of 26.00 % in the determination of the estimated annual effective tax rate.

The Company’s effective tax rate on loss before tax for the three months ended March 31, 2017 of 4.78% (0% - 2016) differs from the Canadian statutory rate of 26% primarily due to recording a valuation allowance on the Canadian deferred tax assets in excess of the remaining Canadian deferred tax liability, resulting in an income tax benefit, and the effect of recording a valuation allowance against deferred tax assets in all other jurisdictions.

The Company maintains a valuation allowance on some of its deferred tax assets in certain jurisdictions. A valuation allowance is required when, based upon an assessment of various factors, including recent operating loss history, anticipated future earnings, and prudent and reasonable tax planning strategies, it is more likely than not that some portion of the deferred tax assets will not be realized.

| 10. | COMMITMENTS AND CONTINGENCIES |

Licensing

| (a) | The Company’s manufactured and marketed product, Sci-B-Vac™, is a recombinant third generation hepatitis B vaccine whose sales and territories are governed by the Ferring License Agreement (“License Agreement”). Under the License Agreement, the Company is committed to pay Ferring royalties equal to 7% of net sales (as defined therein). Royalty payments of $2 and $0 were recorded in cost of revenues for the years ended March 31, 2017, and 2016, respectively. In addition, the Company is committed to pay 30% of any and all non-royalty consideration, in any form, received by Company from such sub-licensees (other than consideration based on net sales for which a royalty is due under the License Agreement), provided that the payment of 30% shall not apply to a grant of rights in or relating to: (i) the territory (the “Territory”) as such term was defined prior to an amendment dated January 24, 2005; or (ii) the Berna Territory (as defined in therein). |

| The Company is to pay Ferring the above-mentioned royalties on a country-by-country basis until the date which is ten (10) years after the date of commencement of the first royalty year in respect of such country (“License Period”). Upon expiry of the full term of the first License Period having commenced, the Company shall have the option to extend the License Agreement in respect of all the countries that still make up the Territory (as defined in the License Agreement) (as from the respective date of expiry) for an additional seven (7) years by payment to Ferring of a one-time lump sum payment of $100. Royalties will continue to be payable for the duration of the extended License Periods. When the license has been in effect for, and elapsed after, a seventeen (17) year License Period with respect to a country in the Territory, the Company shall thereafter have a royalty-free license to market (as defined in the License Agreement) in such country and when all the License Periods have expired in each country in the Territory, a royalty-free license to manufacture the product in India and the People’s Republic of China. |

| (b) | Under an Assignment and Assumption Agreement, the Company is required to pay royalties to SciGen Singapore equal to 5% of Net Sales. Royalty payments of $1 and $0 were recorded in cost of revenues for the years ended March 31, 2017, and 2016, respectively. |

Legal Proceedings

From time to time, the Company may be involved in certain claims and litigation arising out of the ordinary course of business. Management assesses such claims and, if it considers that it is probable that an asset had been impaired or a liability had been incurred and the amount of loss can be reasonably estimated, provisions for loss are made based on management’s assessment of the most likely outcome. The Company believes that they maintain adequate insurance coverage for any such litigation matters arising in the normal course of business.

See Note 7, for the dispute with Kevelt with regard to the DMA.

| 20 |

Operating Leases

The Company has entered into various non-cancelable lease agreements for its office, lab and manufacturing facilities. These arrangements expire at various times through 2022. Rent expense for the three months ended March 31, 2017 and 2016 was $217 and $95, respectively.

The future annual minimum payments under these leases is as follows:

| Year ending December 31 | ||||

| Remaining 2017 | $ | 661 | ||

| 2018 | 717 | |||

| 2019 | 664 | |||

| 2020 | 442 | |||

| 2021 | 442 | |||

| Thereafter | 37 | |||

| Total | $ | 2,963 | ||

On May 9, 2017, VBI DE signed a one year term extension related to the office space in Cambridge, MA committing it to approximately $144 of rent payments which has been included in the above table.

| 11. | REVENUE BY GEOGRAPHIC REGION |

Three Months Ended March 31 | ||||||||

| 2017 | 2016 | |||||||

| Israel | $ | 111 | $ | 40 | ||||

| Asia | 14 | 4 | ||||||

| South America | 2 | - | ||||||

| Europe | - | 4 | ||||||

| Total | $ | 127 | $ | 48 | ||||

| 12. | PROPERTY AND EQUIPMENT, NET BY GEOGRAPHIC REGION |

March 31, 2017 | December 31, 2016 | |||||||

| Property and equipment in Israel | $ | 1,914 | $ | 1,850 | ||||

| Property and equipment in North America | 139 | - | ||||||

| Total | $ | 2,053 | $ | 1,850 | ||||

| 13. | SUBSEQUENT EVENTS |

On May 15, 2017, the Company entered into an equity distribution agreement (the “Distribution Agreement”) with a registered broker-dealer, as sales agent (the “Sales Agent”), pursuant to which the Company may offer and sell, from time to time, through the Sales Agent its common shares having an aggregate offering price of up to $30 million. The Company is not obligated to sell any common shares under the Distribution Agreement. Subject to the terms and conditions of the Distribution Agreement, the Sales Agent will use commercially reasonable efforts consistent with its normal trading and sales practices, applicable state and federal law, rules and regulations, and the rules of the NASDAQ Capital Market to sell shares from time to time based upon the Company’s instructions, including any price, time or size limits specified by the Company. The Company will pay the Sales Agent a commission of 3.0% of the aggregate gross proceeds from each sale of common shares occurring pursuant to the Distribution Agreement, if any. The Company has also agreed to reimburse the Sales Agent for legal fees and disbursements, not to exceed $50 in the aggregate, in connection with entering into the Distribution Agreement. The Distribution Agreement may be terminated by the Sales Agent or the Company at any time upon ten days’ notice to the other party, or by the Sales Agent at any time in certain circumstances.

In connection with the execution of the Distribution Agreement, on May 12, 2017, the Company entered into a waiver agreement (the “Waiver Agreement”)with Perceptive Credit Holdings, LP (“Perceptive Credit”), pursuant to which Perceptive Credit agreed to waive the Company’s obligations to (i) notify Perceptive Credit of the planned filing of a Registration Statement and (ii) include all or a portion of the common shares issuable to Perceptive Credit upon the exercise of a warrant to purchase common shares in the Registration Statement.

| 21 |

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion of our financial condition and results of operations in conjunction with the consolidated financial statements and the related notes included elsewhere in this Form 10-Q and with our audited consolidated financial statements included in our annual report on Form 10-K for the year ended December 31, 2016, as filed with the U.S. Securities and Exchange Commission (the “SEC”). In addition to our historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates, and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to these differences include those discussed below and elsewhere in this Form 10-Q, particularly in Part II, Item 1A, “Risk Factors.”

Overview

VBI- SciVac Merger

On May 6, 2016, the Company completed its acquisition of VBI DE, pursuant to which Seniccav Acquisition Corporation, a Delaware corporation and a wholly owned subsidiary of SciVac, merged with and into VBI DE, with VBI DE continuing as the surviving corporation and as a wholly-owned subsidiary of SciVac (the “VBI-SciVac Merger”). Upon completion of the VBI-SciVac Merger, SciVac changed its name to “VBI Vaccines Inc.” and received approval for the listing of its common shares on The NASDAQ Capital Market. The common shares began trading on The NASDAQ Capital Market at the opening of trading on May 9, 2016 under the Company’s new name and the ticker symbol “VBIV.” Prior to the VBI-SciVac Merger, the Company’s common shares were also listed on the Toronto Stock Exchange (the “TSX”) under the symbol “VAC.” Following the Effective Time of the VBI-SciVac Merger, the common shares began to trade on the TSX under the new symbol “VBV.”

We are a commercial stage biopharmaceutical company developing next generation vaccines to address unmet needs in infectious disease and immuno-oncology. VBI’s first marketed product is Sci-B-Vac™, a hepatitis B (“HBV”) vaccine that mimics all three viral surface antigens of the hepatitis B virus. Sci-B-Vac™ is approved for use in Israel and 14 other countries. Recently, VBI completed a post-marketing Phase IV clinical study in Israel to confirm a new in-house reference standard for regulatory and quality control purposes. Sci-B-Vac™ has not yet been approved by the U.S. Food and Drug Administration (the “FDA”), the European Medicines Agency (the “EMA”) or Health Canada (“HC”). VBI is currently developing a Phase III clinical program to obtain FDA, EMA, and HC market approvals for commercial sale of Sci-B-Vac™ in the United States, Europe, and Canada, respectively. Our wholly-owned subsidiary, SciVac Ltd., manufactures Sci-B-Vac™ in Rehovot, Israel.

With the acquisition of VBI DE in 2016, a significant R&D priority has been the CMV vaccine candidate’s GMP manufacturing and its clinical development. Our CMV vaccine candidate was designed internally, and its manufacturing and purification processes were designed by the NRC in collaboration with our staff. Such processes and internal knowledge were transferred to our selected GMP manufacturer, Paragon, and required significant project management expertise and confirmatory R&D studies throughout 2014. In 2015, we engaged a contract research organization, ITR Laboratories Canada Inc., and completed GLP toxicology studies to confirm the safety of the CMV vaccine candidate in animals. We initiated a Phase I clinical study in June 2016 to assess the safety and tolerability of our CMV vaccine candidate in healthy, CMV-negative adults. The study will also assess the vaccine immunogenicity by measuring levels of vaccine-induced CMV neutralizing antibodies. We completed enrollment and initial dosing of 128 participants in September 2016. As of May 2017, all participants had received the third and final immunization in the series. Interim Phase I clinical study results are anticipated mid-year 2017.

| 22 |

We are also advancing our two platform technologies – our Enveloped Virus-Like Particle (“eVLP”) platform technology and our Lipid Particle Vaccine (“LPV”) technology. Our eVLP platform technology enables the development of enveloped virus-like particle vaccines that closely mimic the target virus to elicit a potent immune response. We are advancing a pipeline of eVLP vaccines, with lead programs in both infectious disease, with our congenital cytomegalovirus (“CMV”) vaccine, and in immuno-oncology, with our therapeutic glioblastoma multiforme (“GBM” or “glioblastoma”) vaccine candidate.

Our LPV Thermostability technology is a proprietary formulation of lipids and process that allows vaccines and biologics to preserve stability, potency, and safety at temperatures outside of the most common cold chain storage requirements of 2oC to 8 oC.

At present, the Company’s operations are focused on:

| ● | manufacturing and sale of Sci-B-Vac™ in territories where it is currently registered; | |

| ● | reporting the Phase IV study results in Israel as described above; | |

| ● | preparing for the Sci-B-Vac™ Phase III clinical studies to support various marketing authorizations in the U.S., Canada and Europe; | |

| ● | conducting the Phase I clinical study with our CMV vaccine candidate; | |

| ● | preparing for the planned Phase I clinical study of our GBM vaccine candidate; | |

| ● | scaling-up Sci-B-Vac™ manufacturing capabilities to further commercialize this product and other dose forms for which we may obtain regulatory approval; | |

| ● | continuing the research and development of our product candidates, including the exploration and development of new product candidates; | |

| ● | providing contracted services, primarily to customers in the pharmaceutical and biotechnology sectors; | |

| ● | adding operational, financial and management information systems and human resources support, including additional personnel to support our vaccine development and commercialization activities; and | |

| ● | maintaining, expanding and protecting our intellectual property portfolio. |

VBI’s income generating activities have been from sales of its Sci-B-Vac™ product in markets that have generated a limited number of sales to-date as well as fees from research and development (“R&D”) services. VBI has also incurred significant net losses and negative operating cash flows since inception. As of March 31, 2017, VBI had an accumulated deficit of approximately $113,618. Our ability to maintain our status as an operating company is dependent upon obtaining adequate cash to finance our clinical development, our administrative overhead and our research and development activities. We plan to finance future operations with a combination of existing cash reserves, proceeds from the issuance of equity securities, the issuance of additional debt, and revenues from potential collaborations, if any. There is no assurance the Company will manage to obtain these sources of financing. These factors raise substantial doubt about the Company’s ability to continue as a going concern. The accompanying financial statements have been prepared assuming that we will continue as a going concern. The financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result should we be unable to continue as a going concern.

| 23 |

We have incurred operating losses since inception, have not generated significant product sales revenue and have not achieved profitable operations. We incurred a net loss of $8,638 for the three months ended March 31, 2017 and we expect to continue to incur substantial losses in future periods. We anticipate that our operating expenses will increase substantially as we continue the clinical development of the Sci-B-Vac™ product and CMV vaccine candidate as well as advance our pre-clinical-stage product candidate, GBM. These include expenses related to:

| ● | conducting the CMV Phase I clinical study, a planned GBM Phase I clinical study and preparation for a Sci-B-Vac™ Phase III program which will require significant financial resources; | |

| ● | continuing the research and development of our product candidates; | |

| ● | scaling-up manufacturing capabilities through sub-contractors to commercialize products and dose forms for which we may obtain regulatory approval; | |

| ● | maintaining, expanding and protecting our intellectual property portfolio; | |

| ● | hiring additional clinical, manufacturing, and scientific personnel or contractors; and | |

| ● | adding operational, financial and management information systems and human resources support, including additional personnel, to support our vaccine development and commercialization activities. |

In addition, we have incurred and will continue to incur significant expenses as a public company, which subjects us to the reporting requirements of the Exchange Act, the Sarbanes-Oxley Act and the rules and regulations of The NASDAQ Capital Market and the Toronto Stock Exchange.

In 2016, we raised $24.1 million in equity and $13.2 million in debt financing to support our Sci-B-Vac™, CMV and GBM vaccine programs, to continue the advancement of our research programs and for other general corporate purposes. We expect that we will need to secure additional financing in the future to carry out all of our planned clinical, regulatory, R&D, sales and manufacturing activities with respect to the advancement of our Sci-B-Vac™ and new vaccine candidates.

Since inception, VBI and its subsidiaries collectively have raised approximately $124.7 million in total equity and debt financing to support clinical and research development and general business operations.

R&D Services

Pursuant to an agreement with the Office of the Chief Scientist in Israel, the Company is required to make services available for the biotechnology industry in Israel. These services include relevant activities for development and manufacturing of therapeutic proteins according to international standards and cGMP quality level suitable for toxicological studies in animals and clinical studies (Phase I & II) in humans. Service activities include analytics/bio analytics methods for development and process development of therapeutic proteins starting with a lead candidate clone through the upstream, purification, formulation and filling processes and manufacturing for Phase I & II clinical studies.

These R&D services are primarily marketed to the Israeli research community in academia and Israeli biotechnology companies in the life sciences lacking the infrastructure or experience in the development and production of therapeutic proteins and the standards and quality required for clinical studies for human use. In 2016 and 2015, the Company provided services to more than 10 biotech companies including analytical development, upstream development process, protein purification and formulation and filling for Phase I clinical studies.

VBI Cda also provides R&D services pursuant to a research agreement and certain governmental research and development grants.

| 24 |

Financial Overview

Overall Performance

The Company had net losses of approximately $8,638 and $1,079 for the three months ended March 31, 2017 and 2016, respectively. The Company has an accumulated deficit of $113,618 at March 31, 2017. The Company had $23,509 of cash at March 31, 2017 and net working capital of approximately $17,999.

R&D Expenses

R&D expenses consist primarily of costs incurred for the development of our CMV, GBM and Sci-B-Vac™ vaccines, which include:

| ● | the cost of acquiring, developing and manufacturing clinical study materials and other consumables and lab supplies used in our pre-clinical studies | |

| ● | expenses incurred under agreements with contractors or Contract Manufacturing Organizations to advance the vaccines into clinical studies; and | |

| ● | employee-related expenses, including salaries, benefits, travel and stock-based compensation expense. |

We expense R&D costs when we incur them.

General and Administrative Expenses

General and administrative expenses consist principally of salaries and related costs for executive and other administrative personnel and consultants, including stock-based compensation and travel expenses. Other general and administrative expenses include professional fees for legal, patent protection, consulting and accounting services, travel and conference fees, including board and scientific advisory board meeting costs, rent, maintenance of facilities, depreciation, office supplies and expenses, insurance and other general expenses. General and administrative expenses are expensed when incurred.

We expect that our general and administrative expenses will increase in the future as a result of adding employees and scaling our operations commensurate with advancing clinical candidates and continuing to support a public company infrastructure. These increases will likely include increased costs for insurance, hiring of additional personnel, board committees, outside consultants, investor relations, lawyers and accountants, among other expenses.

Interest Income

Interest income consists principally of interest income earned on cash balances and on R&D tax refunds.

Interest Expense

Interest expense is associated with our previously outstanding convertible notes and the credit facility entered into on July 25, 2014 and subsequently amended on December 6, 2016.

| 25 |

Results of Operations

Three Months Ended March 31, 2017 Compared to the Three Months Ended March 31, 2016

All amounts stated below are in thousands, unless otherwise indicated.

Revenues

Revenue for the three months ended March 31, 2017 was $127, as compared to $48 for the three months ended March 31, 2016.

Revenue by Geographic Region

| March 31, 2017 | March 31, 2016 | $ Change | % Change | |||||||||||||

| $ | $ | |||||||||||||||

| Revenue in Israel | $ | 111 | $ | 40 | $ | 71 | 177.5 | % | ||||||||

| Revenue in Asia | 14 | 4 | 10 | 250 | % | |||||||||||

| Revenue in South America | 2 | - | 2 | N/A | ||||||||||||

| Revenue in Europe | - | 4 | (4 | ) | (100 | )% | ||||||||||

| Total Revenue | $ | 127 | $ | 48 | 79 | 164.6 | % | |||||||||

Revenue earned in Israel for the three months ended March 31, 2017 was $111 as compared to $40 for the three months ended March 31, 2016. The revenue earned in Israel increased by $71, or 177.5%, primarily as a result of completion of a fee for service project during the first quarter of 2017 compared to 2016.

Revenue earned in Asia, South America and Europe for the three months ended March 31, 2017 and 2016 were insignificant.

Cost of Revenues

Cost of revenues for the three months ended March 31, 2017 was $1,275 as compared to $377 for the three months ended March 31, 2016. The increase in the cost of revenues of $898, or 238%, was a result of a returning to routine production, increase of production-related headcount compared to previous year. The prior year also experienced a significant decrease of production activities as a result of a partial shutdown of the manufacturing facility for maintenance and upgrades.

Research and Development

R&D expenses for the three months ended March 31, 2017 were $4,654 as compared to $254 for the three months ended March 31, 2016. During the three months ended March 31, 2017, the significant increase in the cost of R&D was due to the R&D expenses incurred by VBI DE since the VBI-SciVac Merger in the amount of $2,423 as well as approximately $1,686 of contractors and consultant costs largely related to Sci-B-Vac™ clinical and product development costs as well as share-based compensation expense related to the issuance of options and restricted shares.

General and Administrative

General and administrative (“G&A”) expenses for the three months ended March 31, 2017 were $3,045 as compared to $1,980 for the three months ended March 31, 2016. The G&A expense increase of $1,065, or 53.8%, was primarily a result of an additional $1,125 in operating costs incurred by VBI DE since the VBI-SciVac Merger. These costs included salaries, facilities related costs, administrative, legal and professional fees. In addition, subsequent to the VBI-SciVac Merger there was share-based compensation expense of approximately $423 related to the issuance of options and restricted shares whereas in the comparative quarter in 2016 there was none. These increases were partially offset by approximately $480 of cost savings primarily related to G&A salaries, as well as legal and professional fees related to the VBI-SciVac merger which were incurred in the three months ended March 31, 2016.

| 26 |

Net Loss from Operations

The net loss from operations for the three months ended March 31, 2017 were $8,847 as compared to $2,563 for the three months ended March 31, 2016. The $6,284 increase in the net loss from operations resulted from the increased R&D and G&A costs resulting from the VBI-SciVac Merger as well as the increase in the cost of revenues.

Interest Expense, net

The interest expense increase of $679 is largely a result of $450 interest paid on the long-term debt as well as the accretion of $288 of non-cash interest expense related to the debt discount for the three months ended March 31, 2017 whereas there was none in the comparative period for 2016. The interest paid on long-term debt during for the three months ended March 31, 2016 was $25.

Foreign Exchange Gain

The foreign exchange gain of $482 in the three months ended March 31, 2017 as compared to a $1,509 in the comparative period for 2016, is the result of the fluctuation in the foreign currency exchange rate of the CAD and the NIS as compared to the U.S. dollar.

Net Loss

The net loss increased by $7,559, or 700.6%, from $1,079 for the three months ended March 31, 2016 to $8,638 for the three months ended March 31, 2017. The increase in our net loss is mainly attributable to the increase in our loss from operations.

Liquidity and Capital Resources

March 31, 2017 | December 31, 2016 | $ Change | % Change | |||||||||||||

| Cash | $ | 23,509 | $ | 32,282 | $ | (8,773 | ) | (27.2 | )% | |||||||

| Current Assets | 25,783 | 34,358 | (8,575 | ) | (25.0 | )% | ||||||||||

| Current Liabilities | 7,784 | 7,614 | 170 | 2.2 | % | |||||||||||

| Working Capital | 17,999 | 26,744 | (8, 745 | ) | (32.7 | )% | ||||||||||

| Accumulated Deficit | (113,618 | ) | (104,980 | ) | (8,638 | ) | 8.2 | % | ||||||||

As at March 31, 2017, we had cash of $23,509 as compared to $32,282 as at December 31, 2016. As at March 31, 2017, the Company had working capital of $17,999 as compared to working capital of $26,744 at December 31, 2016. Working capital is calculated by subtracting current liabilities from current assets.