Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration No. 333-165376

The information in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated March 16, 2011

Preliminary Prospectus Supplement

To Prospectus dated March 10, 2010

$

Cliffs Natural Resources Inc.

$ % Senior Notes due 2021

$ 6.25% Senior Notes due 2040

We are offering $ aggregate principal amount of % senior notes due 2021, which we refer to in this prospectus supplement as our “2021 senior notes,” and an additional issuance of $ aggregate principal amount of our 6.25% senior notes due 2040, $500,000,000 aggregate principal amount of which have been issued previously, which we refer to as the “existing 2040 senior notes.” The 2040 senior notes offered by this prospectus supplement will become part of the same series as the existing 2040 senior notes for all purposes under the indenture and together are referred to in this prospectus supplement as the “2040 senior notes.” We collectively refer to both series of notes offered hereby as our “notes.”

We will pay interest on the 2021 senior notes on and of each year, beginning on , 2011. We will pay interest on the 2040 senior notes on April 1 and October 1 of each year, beginning on October 1, 2011. The 2021 senior notes will mature on , 2021, and the 2040 senior notes will mature on October 1, 2040. The notes will be issued only in denominations of $2,000 and integral multiples of $1,000 above that amount.

We have the option to redeem some or all of the notes at any time and from time to time, as described under the heading “Description of the Notes—Optional Redemption.” If a change of control triggering event occurs, we will be required to offer to purchase the notes at a purchase price equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to the date of purchase. See “Description of the Notes—Change of Control Triggering Event.”

The 2021 senior notes will be subject to a special mandatory redemption in the event our pending acquisition of Consolidated Thompson Iron Mines Limited, or Consolidated Thompson, is not consummated on or prior to July 29, 2011, or if prior to July 29, 2011, the definitive arrangement agreement with Consolidated Thompson is terminated, subject to certain conditions. In such an event, the 2021 senior notes will be redeemed at a price equal to 101% of the principal amount thereof plus accrued and unpaid interest from the date of initial issuance, or the most recent date to which interest has been paid or provided for, whichever is later, to but excluding the special mandatory redemption date.

The notes will be our senior unsecured obligations and will rank equally with all of our other existing and future senior unsecured and unsubordinated indebtedness, but will be effectively junior to any secured indebtedness which we may incur in the future. The notes will not be the obligation of any of our subsidiaries. For a more detailed description of the notes, see “Description of the Notes.”

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

See “Risk Factors” beginning on page S-12 of this prospectus supplement and the risk factors contained in our Annual Report on Form 10-K for the fiscal year ended December 31, 2010, which are incorporated by reference herein, for a discussion of certain risks that you should consider in connection with an investment in the notes.

| Per

2021 Senior Note |

Total | Per

2040 Senior Note |

Total | |||||||||||||

| Public Offering Price(1)(2) |

% | $ | % | $ | ||||||||||||

| Underwriting Discount |

% | $ | % | $ | ||||||||||||

| Proceeds to us (before expenses)(1)(2) |

% | $ | % | $ | ||||||||||||

| (1) | In the case of the 2021 senior notes, plus accrued interest, if any, from , 2011. |

| (2) | In the case of the 2040 senior notes, plus accrued interest, if any, from , 2011. |

The notes will not be listed on any securities exchange. Currently, there is no public market for the notes.

The underwriters expect to deliver the notes to purchasers through the book-entry delivery system of The Depository Trust Company for the benefit of its participants, including Euroclear Bank S.A./N.V. and Clearstream Banking, société anonyme, on or about , 2011 in the case of the 2021 senior notes, and on or about April 1, 2011 in the case of the 2040 senior notes. Purchasers who wish to trade their notes prior to the third business day before the applicable date of delivery will be required to specify alternate settlement arrangements to prevent a failed settlement. For a more detailed description of the alternate settlement cycle, see “Underwriting.”

Joint Book-Running Managers

| BofA Merrill Lynch | Citi | J.P. Morgan |

, 2011

Table of Contents

Prospectus Supplement

| Page | ||||

| ii | ||||

| ii | ||||

| ii | ||||

| iii | ||||

| S-1 | ||||

| S-12 | ||||

| S-17 | ||||

| S-18 | ||||

| Unaudited Pro Forma Condensed Consolidated Financial Information |

S-19 | |||

| S-27 | ||||

| S-36 | ||||

| S-41 | ||||

| S-43 | ||||

| S-47 | ||||

| S-47 | ||||

| F-1 | ||||

| Prospectus | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 3 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 15 | ||||

| 17 | ||||

| 17 | ||||

i

Table of Contents

About This Prospectus Supplement

We provide information to you about this offering in two separate documents. The accompanying prospectus provides general information about us and the securities we may offer from time to time, some of which may not apply to this offering. This prospectus supplement describes the specific details regarding this offering. Generally, when we refer to the “prospectus,” we are referring to both documents combined. Additional information is incorporated by reference in this prospectus supplement. If information in this prospectus supplement is inconsistent with the accompanying prospectus, you should rely on this prospectus supplement.

We have not authorized anyone to provide any information other than contained or incorporated by reference in this prospectus supplement or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. You should not assume that the information contained in this prospectus supplement, the accompanying prospectus or any document incorporated by reference is accurate as of any date other than the date mentioned on the cover page of these documents. We are not, and the underwriters are not, making offers to sell the securities in any jurisdiction in which an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make an offer or solicitation.

References in this prospectus supplement to the terms “we,” “us,” “the Company” or “Cliffs” or other similar terms mean Cliffs Natural Resources Inc. and its consolidated subsidiaries, unless we state otherwise or the context indicates otherwise. As used in this prospectus supplement, the term “ton” means a long ton (equal to 2,240 pounds) when referring to our North American Iron Ore business segment, the term “ton” means a short ton (equal to 2,000 pounds) when referring to our North American Coal business segment and the term “metric ton” means a metric ton (equal to 1,000 kilograms or 2,205 pounds).

Where You Can Find More Information

We are subject to the informational reporting requirements of the Securities Exchange Act of 1934. We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available over the Internet at the SEC’s website at www.sec.gov. You may read and copy any reports, statements and other information filed by us at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Please call 1-800-SEC-0330 for further information on the Public Reference Room. You may also inspect our SEC reports and other information at the New York Stock Exchange, 20 Broad Street, New York, New York 10005, or at our website at www.cliffsnaturalresources.com. The information contained on or accessible through our website is not part of this prospectus supplement, other than the documents that we file with the SEC that are incorporated by reference in this prospectus supplement or the accompanying prospectus.

Information We Incorporate By Reference

The SEC allows us to “incorporate by reference” into this prospectus supplement the information in documents we file with it, which means that we can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be a part of this prospectus supplement and information that we file later with the SEC will automatically update and supersede this information. Any statement contained in any document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded for purposes of this prospectus supplement to the extent that a statement contained in or omitted from this prospectus supplement, or in any other subsequently filed document which also is or is deemed to be incorporated by reference herein, modifies or supersedes such statement. Any such statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this prospectus supplement.

ii

Table of Contents

We incorporate by reference the documents listed below and any future filings we make with the SEC under Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act until the completion of the offering of securities described in this prospectus supplement:

| • | our Annual Report on Form 10-K for the year ended December 31, 2010; |

| • | our Current Reports on Form 8-K, as filed with the SEC on January 7, 2011, January 12, 2011, January 14, 2011, January 18, 2011, February 8, 2011, February 9, 2011 and March 8, 2011; and |

| • | our Preliminary Proxy Statement on Schedule 14A, as filed with the SEC on March 14, 2011. |

We will not, however, incorporate by reference in this prospectus supplement any documents or portions thereof that are not deemed “filed” with the SEC, including any information furnished pursuant to Item 2.02 or Item 7.01 of our current reports on Form 8-K unless, and except to the extent, specified in such current reports. You may obtain copies of these filings without charge by accessing the investor relations section of cliffsnaturalresources.com or by requesting the filings in writing or by telephone at the following address.

Cliffs Natural Resources Inc.

Investor Relations

200 Public Square

Suite 3300

Cleveland, Ohio 44114

Telephone Number: (216) 694-5700

Disclosure Regarding Forward-Looking Statements

This prospectus supplement and the accompanying prospectus, including the documents incorporated by reference, contain statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements may be identified by the use of predictive, future-tense or forward-looking terminology, such as “believes,” “anticipates,” “expects,” “estimates,” “intends,” “may,” “will” or similar terms. These statements speak only as of the date of this prospectus supplement or the date of the document incorporated by reference, as applicable, and we undertake no ongoing obligation, other than that imposed by law, to update these statements. These statements appear in a number of places in this prospectus supplement, including the documents incorporated by reference, and relate to, among other things, our intent, belief or current expectations of our directors or our officers with respect to: our future financial condition; results of operations or prospects; estimates of our economic iron ore and coal reserves; our business and growth strategies; and our financing plans and forecasts. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve significant risks and uncertainties, and that actual results may differ materially from those contained in or implied by the forward-looking statements as a result of various factors, some of which are unknown, including, without limitation:

| • | the ability to successfully complete the pending acquisition of Consolidated Thompson; |

| • | the ability to successfully integrate acquired companies into our operations, including without limitation, Consolidated Thompson if it is successfully acquired; |

| • | uncertainty or weaknesses in global economic conditions, including downward pressure on prices; |

| • | trends affecting our financial condition, results of operations or future prospects; |

| • | the ability to reach agreement with our iron ore customers regarding modifications to sales contract pricing escalation provisions to reflect a shorter-term or spot-based pricing mechanism; |

| • | the outcome of any contractual disputes with our customers or significant energy, material or service providers; |

iii

Table of Contents

| • | the outcome of any arbitration or litigation; |

| • | changes in sales volume or mix; |

| • | the impact of price-adjustment factors on our sales contracts; |

| • | the ability of our customers to meet their obligations to us on a timely basis or at all; |

| • | our actual economic ore reserves; |

| • | the success of our business and growth strategies; |

| • | our ability to successfully identify and consummate any strategic investments; |

| • | events or circumstances that could impair or adversely impact the viability of a mine and the carrying value of associated assets; |

| • | impacts of increasing governmental regulation including failure to receive or maintain required environmental permits, approvals, modifications or other authorization of, or from, any governmental or regulatory entity; |

| • | adverse changes in currency values; |

| • | the success of our cost-savings efforts; |

| • | our ability to maintain adequate liquidity and successfully implement our financing plans; |

| • | our ability to maintain appropriate relations with unions and employees; |

| • | uncertainties associated with unanticipated geological conditions, natural disasters, weather conditions, disruption of energy, equipment failures and other unexpected events; |

| • | risks related to international operations; and |

| • | the potential existence of significant deficiencies or material weakness in our internal control over financial reporting. |

These factors and the other risk factors described in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference, are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors also could harm our results. Consequently, there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to or effects on us. Given these uncertainties, prospective investors are cautioned not to place undue reliance on such forward-looking statements.

iv

Table of Contents

This summary highlights information about us and the notes being offered by this prospectus supplement. This summary is not complete and may not contain all of the information that you should consider prior to investing in our notes. For a more complete understanding of our company, we encourage you to read this entire document, including the information incorporated by reference in this document and the other documents to which we have referred.

Our Company

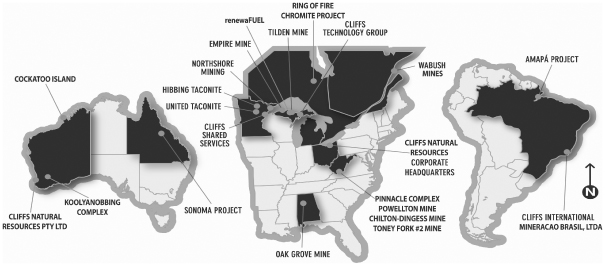

Cliffs Natural Resources Inc. is an international mining and natural resources company that traces its corporate history back to 1847. We are the largest producer of iron ore pellets in North America, a major supplier of direct-shipping lump and fines iron ore out of Australia and a significant producer of metallurgical coal. With core values of environmental and capital stewardship, our colleagues across the globe endeavor to provide all stakeholders operating and financial transparency as embodied in the Global Reporting Initiative framework. Our company’s primary operations are currently organized according to product category and geographic location: North American Iron Ore; North American Coal; Asia Pacific Iron Ore; Asia Pacific Coal; Latin American Iron Ore; Alternative Energies; Ferroalloys; and our Global Exploration Group. The Asia Pacific Coal, Latin American Iron Ore, Alternative Energies, FerroAlloys and Global Exploration Group operating segments do not meet reportable segment disclosure requirements and therefore are not separately reported.

In North America, we operate six iron ore mines in Michigan, Minnesota and Eastern Canada, five metallurgical coal mines located in West Virginia and Alabama and one thermal coal mine located in West Virginia. Our Asia Pacific operations are comprised of two iron ore mining complexes in Western Australia and a 45% economic interest in a coking and thermal coal mine in Queensland, Australia. In Latin America, we have a 30% interest in Amapá, a Brazilian iron ore operation. Our Ferroalloys operations are comprised of our recently acquired chromite deposits in Northern Ontario, Canada. Our operations also include our 95% controlling interest in renewaFUEL located in Michigan. In addition, our Global Exploration Group was established in 2009 and is focused on early involvement in exploration activities to identify new world-class projects for future development or projects that add significant value to existing operations.

The following map shows our global footprint:

S-1

Table of Contents

North American Iron Ore

We are the largest producer of iron ore pellets in North America and primarily sell our production to integrated steel companies. We manage and operate six North American iron ore mines located in Michigan, Minnesota and Eastern Canada that currently have an annual rated capacity of 38.4 million tons of iron ore pellet production, representing 45.3% of total North American pellet production capacity.1 Based on our equity ownership in the North American mines we currently operate, our share of the annual rated pellet production capacity is currently 29.9 million tons, representing 35.3% of total North American annual pellet capacity.2

Our North American Iron Ore revenues are primarily derived from sales of iron ore pellets to the North American integrated steel industry, consisting of seven major customers. Generally, we have multi-year supply agreements with our customers. Sales volume under these agreements is largely dependent on customer requirements, and in many cases, we are the sole supplier of iron ore pellets to the customer. Historically, each agreement has contained a base price that is adjusted annually using one or more adjustment factors. Factors that could result in a price adjustment include international pellet prices, measures of general industrial inflation and steel prices. Additionally, certain of our supply agreements have a provision that limits the amount of price increase or decrease in any given year. In 2010, the world’s largest iron ore producers moved away from the annual international benchmark pricing mechanism referenced in certain of our customer supply agreements, resulting in a shift in the industry toward shorter-term pricing arrangements linked to the spot market. These changes caused us to assess the impact a change to the historical annual pricing mechanism would have on certain of our larger existing North American Iron Ore customer supply agreements. We reached final pricing settlements with some of our North American Iron Ore customers through the fourth quarter of 2010 for the 2010 contract year.

Each of our North American Iron Ore mines is located near the Great Lakes or, in the case of Wabush, near the St. Lawrence Seaway, which provides us access to the seaborne market. The majority of our iron ore pellets are transported via railroads to loading ports for shipment via vessel to steelmakers.

For the year ended December 31, 2010, we produced a total of 32 million tons of iron ore pellets, including 25.4 million tons for our account and 6.6 million tons on behalf of steel company owners of the mines. For the year ended December 31, 2009, we produced a total of 19.6 million tons of iron ore pellets, including 17.1 million tons for our account and 2.5 million tons on behalf of steel company owners of the mines. For the year ended December 31, 2008, we produced a total of 35.2 million tons of iron ore pellets, including 22.9 million tons for our account and 12.3 million tons on behalf of steel company owners of the mines. For the years ended December 31, 2010, 2009 and 2008, we sold 26.2 million, 16.4 million and 22.7 million tons of iron ore pellets, respectively, from our share of production from our North American Iron Ore mines.

At the end of 2010, our North American Iron Ore mines had proven and probable mineral reserves totaling approximately 906 million tons.

We have been a leader in iron ore mining technology for more than 160 years. We pioneered early open-pit and underground mining methods. From the first application of electrical power in Michigan’s underground mines to the use of today’s sophisticated computer networks and global positioning satellite systems, we have been a leader in the application of new technology to the centuries-old business of mineral extraction. Today, our engineering and technical staffs are engaged in full-time technical support of our operations and improvement of existing products.

| 1 | North American pellet capacity as reported includes plants in the U.S. and Canada, but excludes Mexico. |

| 2 | On February 1, 2010, we acquired U.S. Steel Canada’s 44.6% interest and ArcelorMittal Dofasco’s 28.6% interest in Wabush, thereby increasing our ownership interest in Wabush from 26.8% as of December 31, 2009 to 100% as of December 31, 2010. |

S-2

Table of Contents

We will continue to leverage our strong technical competencies in the mining, processing and concentrating of lower-grade ores into high quality products that are critical inputs depended on by North American integrated steel producers.

North American Coal

We are a leading supplier of metallurgical coal in North America. As of December 31, 2010, we owned and operated five metallurgical coal mines in West Virginia and Alabama and one thermal coal mine located in West Virginia that currently have a rated capacity of 9.4 million tons of production annually. The metallurgical coal mines produce either high-quality, low-volatility or high-quality, high-volatility metallurgical coals, which are used to make coke, a key component in the steelmaking process. These coals generally sell at a premium over the more prevalent and mined, thermal coal, which is generally used to generate electricity. Metallurgical coal receives this premium because of its coking characteristics, which include expansion and contraction when heated, and volatility, which refers to the loss in mass when coal is heated in the absence of air. Coals with lower volatility produce more efficient coke for steelmaking and are more highly valued than coals with a higher volatility, all else being equal. At the end of 2010, we had over 350 million tons of metallurgical coal in-place proven and probable reserves.

At the end of 2010, we estimate a total of approximately 163.2 million tons of total proven and probable recoverable reserves of metallurgical coal and, further, we estimate a total of approximately 61.8 million tons of proven and probable recoverable reserves of thermal coal. For the year ended December 31, 2010, we sold a total of 3.3 million tons, compared with 1.9 million tons for the year ended December 31, 2009 and 3.2 million tons for the year ended December 31, 2008. Each of our North American coal mines is positioned near rail or barge lines providing access to international shipping ports, which allows for export of our coal production. International and North American sales represented 55% and 45%, respectively, of our North American Coal sales in 2010.

Asia Pacific Iron Ore

Our Asia Pacific Iron Ore operations are located in Western Australia and include our 100% owned Koolyanobbing complex and our 50% equity interest in Cockatoo Island. We serve the Asian iron ore markets with direct-shipping fines and lump ore. Production in 2010 was 9.3 million metric tons, compared with 8.3 million metric tons in 2009 and 7.7 million metric tons in 2008. We have recently announced an expansion program that is anticipated to increase annual production to 11.0 million metric tons annually beginning in 2012.

At the end of 2010, we had approximately 101.3 million metric tons of proven and probable reserves in our Asia Pacific Iron Ore business. In recent years, through a near-mine drilling program our reserve base has remained relatively constant, despite annual production of approximately eight million metric tons of iron ore.

We have five-year term supply agreements with steel producers in China and Japan that account for approximately 82% and 18% respectively, of sales. The contracts were renegotiated for the period 2008 through 2012. Sales volume under the agreements is partially dependent on customer requirements. As a result of the move away from the annual international benchmark pricing mechanism in 2010, we renegotiated the terms of our supply agreements with our Chinese and Japanese Asia Pacific Iron Ore customers moving to shorter-term pricing mechanisms of various durations based on the average daily spot prices, with certain pricing mechanisms that have a duration of up to a quarter. This change was effective in the first quarter of 2010 for our Chinese customers and the second quarter of 2010 for our Japanese customers. During 2010, 2009 and 2008, we sold 9.3 million, 8.5 million and 7.8 million metric tons of iron ore, respectively, from our Western Australia mines.

S-3

Table of Contents

Investments

Amapá. We are a 30% minority interest owner in Amapá, which consists of an iron ore deposit, a 120-mile railway connecting the mine location to an existing port facility and 71 hectares of real estate on the banks of the Amazon River, reserved for a loading terminal. Amapá initiated production in late December 2007. The remaining 70% of Amapá is owned by Anglo American plc.

As the operator of the property, Anglo American declared commercial production achievement during 2010 with annual production totaling 4.0 million metric tons, compared with 2.7 million metric tons and 1.2 million metric tons in 2009 and 2008, respectively. Anglo American has indicated that it expects Amapá will produce and sell 4.5 million metric tons of iron ore fines products in 2011 and 5.1 million metric tons in 2012 based on continued improvements in operational processes. The majority of Amapá’s production is committed under a long-term supply agreement with an operator of an iron oxide pelletizing plant in the Kingdom of Bahrain.

Sonoma. We own a 45% economic interest in Sonoma, located in Queensland, Australia. Production and sales totaled approximately 3.5 million metric tons, respectively, in 2010. This compares with production and sales of approximately 2.8 million and 3.1 million metric tons and 2.4 million and 2.1 million metric tons in 2009 and 2008, respectively. The project is expected to produce approximately 3.6 million metric tons of coal annually in 2011 and beyond. Production is expected to include a mix of approximately two-thirds thermal and one-third metallurgical grade coal. In 2009, Sonoma experienced intrusions in the coal seams which affected raw coal quality, recoverability in the washing process, and ultimately the quantity of metallurgical coal in the production mix. As a result, the geological model for Sonoma has been enhanced to reflect the presence of the intrusions and to refine the mining sequence in order to optimize the mix of metallurgical and thermal coal despite being lower than initially planned levels. Sonoma has economically recoverable reserves of 20 million metric tons. Of the 3.5 million metric tons produced in 2010, approximately 3.0 million metric tons were committed under supply agreements. As of December 31, 2010, approximately 2.0 million metric tons, of the 3.6 metric tons expected to be produced in 2011, are committed under supply agreements.

Growth Strategy and Recent Developments

Over recent years, we have been executing a strategy designed to achieve scale in the mining industry and focused on serving the world’s largest and fastest growing steel markets. Throughout 2010, we continued to increase our operating scale and presence as an international mining and natural resources company by expanding both geographically and through the minerals we mine and market. The long-term outlook remains healthy and we are now focusing on our growth projects with sustained investment in our core businesses. Our growth in North America, as well as acquisitions in minerals outside of iron ore and coal, illustrates the execution of this strategy during 2010.

We also expect to achieve growth through early involvement in exploration activities by partnering with junior mining companies, which provide us low-cost entry points for potentially significant reserve additions. We established a global exploration group in 2009, led by professional geologists who have the knowledge and experience to identify new world-class projects for future development or projects that add significant value to existing operations.

Specifically, we continued our strategic growth as an international mining and natural resources company through the following transactions in 2010:

Freewest. On January 27, 2010, we acquired all of the remaining outstanding shares of Freewest Resources Canada Inc., or Freewest, for C$1.00 per share, including its interest in the Ring of Fire properties in Northern Ontario Canada which comprise three premier chromite deposits. The acquisition of Freewest is consistent with our strategy to broaden our geographic and mineral diversification and allows us to apply our expertise in open-pit mining and mineral processing to a chromite ore resource base that could form the foundation of North

S-4

Table of Contents

America’s only ferrochrome production operation. The planned mine is expected to produce 1 million to 2 million metric tons of high-grade chromite ore annually, which would be further processed into 400 thousand to 800 thousand metric tons of ferrochrome.

Wabush. On February 1, 2010, we acquired entities from our former partners that held their respective interests in the Wabush Mines Joint Venture, or Wabush, for $103 million, thereby increasing our ownership interest to 100%. With Wabush’s 5.5 million tons of production capacity, acquisition of the remaining interest has increased our North American Iron Ore equity production capacity by approximately 4.0 million tons and has added more than 50 million tons of additional reserves. Furthermore, acquisition of the remaining interest has provided us additional access to the seaborne iron ore markets serving steelmakers in Europe and Asia.

Spider. We commenced a formal cash offer to acquire all of the outstanding common shares of Spider Resources Inc., or Spider, a Canadian-based mineral exploration company, for C$0.19 per share during the second quarter of 2010. On July 6, 2010, all of the conditions to acquire the remaining common shares of Spider had been satisfied or waived and we increased our ownership percentage to 52%, representing a majority of the common shares outstanding on a fully-diluted basis. Subsequently, we extended the cash offer to permit additional shares to be tendered and taken up, thereby increasing our ownership percentage in Spider to 85% as of July 26, 2010. Effective October 6, 2010, we completed the acquisition of all of the remaining shares of Spider through an amalgamation. Consequently, we own 100% of Spider as of December 31, 2010 and have obtained majority ownership of the “Big Daddy” chromite deposit located in Northern Ontario. The “Big Daddy” chromite deposit is one of the three premier chromite deposits that we originally acquired interest in through the Freewest acquisition as discussed above.

CLCC. On July 30, 2010, we acquired all of the coal operations of privately-owned INR Energy, LLC, or INR, for $775.9 million, and since that date, the operations acquired from INR have been conducted through our wholly-owned subsidiary known as Cliffs Logan County Coal, or CLCC. CLCC is a producer of high-volatile metallurgical and thermal coal located in southern West Virginia. CLCC’s operations include two underground continuous mining method metallurgical coal mines and one open surface thermal coal mine, a coal preparation and processing facility as well as a large, long-life reserve base with an estimated 59 million tons of metallurgical coal and 62 million tons of thermal coal. This reserve base increases our total global reserve base to over 166 million tons of metallurgical coal and over 67 million tons of thermal coal. This acquisition represents an opportunity for us to add complementary high-quality coal products and provides certain advantages, including among other things, long-life mine assets, operational flexibility, and new equipment.

We plan to continue our strategic growth as an international mining and natural resources company in 2011. Specifically:

Consolidated Thompson. On January 11, 2011, we entered into a definitive arrangement agreement with Consolidated Thompson to acquire all of its common shares in an all-cash transaction including net debt, valued at approximately C$4.9 billion, or C$17.25 per share, which we refer to as the Arrangement Agreement. The proposed acquisition, which we refer to as the Acquisition, reflects our strategy to build scale by owning expandable and exportable steelmaking raw material assets serving international markets. On February 25, 2011, the shareholders of Consolidated Thompson approved the plan of arrangement pursuant to which the Acquisition will be completed. Completion of the Acquisition is subject to additional customary closing conditions, including government and regulatory approvals.

Consolidated Thompson is a Canadian exploration and development mining company producing iron ore of high-quality concentrate. Consolidated Thompson operates an iron ore mine and processing facility near Bloom Lake in Quebec, Canada. Wuhan Iron and Steel (Group) Corporation, which we refer to as Wuhan, is a 25% partner in the Bloom Lake property. The Bloom Lake property is currently ramping up towards an initial production rate of 8.0 million metric tons of iron ore concentrate per year, which Consolidated Thompson

S-5

Table of Contents

expects to increase to 16.0 million metric tons per year by mid-2013. Consolidated Thompson also owns two additional development properties, Lamêlée and Peppler Lake, in Quebec. The Bloom Lake, Lamêlée and Peppler Lake properties are in close proximity to our own Canadian operations and will allow us to leverage our port facilities and supply this ore to the seaborne market. All of Consolidated Thompson’s current production capacity is contracted under long-term off-take arrangements with large Asian customers at sales-per-ton rates that move with the global seaborne prices. The Acquisition is expected to further diversify our customer base by increasing sales to these customers, including Wuhan, Worldlink Resources Limited and SK Networks Co., Ltd., a subsidiary of SK Group. In addition, we expect to realize approximately $75 million in pre-tax annual operating synergies in connection with the Acquisition.

Bridge Credit Agreement. On March 4, 2011, we entered into an unsecured bridge credit agreement with a syndicate of banks. The bridge credit agreement provides for up to a $2,450 million bridge credit facility, which we refer to as the bridge credit facility, that matures one year from the date of the funding. The commitments under the bridge credit facility will continue to reduce prior to the closing date of the Acquisition as we obtain permanent financing. Borrowings under the bridge credit facility will bear interest at a floating rate based upon a negotiated base rate or the LIBOR rate plus a margin depending on our credit rating and the length of time the borrowings, if any, remain outstanding.

New Term Loan. On March 4, 2011, we entered into a new unsecured term loan agreement with a syndicate of banks. The term loan agreement provides for a $1,250 million term loan, which we refer to as the new term loan, that matures on the fifth anniversary of the date the new term loan is funded, and requires principal payments on each three-month anniversary following funding of the new term loan. Borrowings under the new term loan will bear interest at a floating rate based upon a negotiated base rate or the LIBOR rate plus a margin depending on the leverage ratio.

The bridge credit facility and the new term loan contain certain representation and warranties, certain affirmative and negative covenants, certain financial covenants and events of default customary for such financings.

We intend to use borrowings under the bridge credit facility and our new term loan, along with the net proceeds from this offering, to pay a portion of the purchase price of the Acquisition. We do not intend to borrow under the bridge credit facility or our new term loan until the funding, which is expected to be not more than three business days prior to the date of closing of the pending Acquisition.

Corporate Information

Our principal executive offices are located at 200 Public Square, Suite 3300, Cleveland, Ohio 44114. Our main telephone number is (216) 694-5700, and our website address is www.cliffsnaturalresources.com. The information contained on or accessible through our website is not part of this prospectus supplement, other than the documents that we file with the SEC that are incorporated by reference in this prospectus supplement or the accompanying prospectus.

S-6

Table of Contents

The Offering

The following summary contains basic information about the notes and is not intended to be complete. It does not contain all of the information that is important to you. For a more detailed description of the notes, please refer to the section entitled “Description of the Notes” in this prospectus supplement and the section entitled “Description of Debt Securities” in the accompanying prospectus.

| Issuer |

Cliffs Natural Resources Inc. |

| Notes offered |

$ aggregate principal amount of notes, consisting of $ aggregate principal amount of 2021 senior notes and $ aggregate principal amount of 2040 senior notes. The offered amount of the 2040 senior notes will constitute an additional issuance of our 2040 senior notes, $500,000,000 aggregate principal amount of which have been previously issued and are outstanding. |

| Maturity |

The 2021 senior notes will mature on , 2021. |

| The 2040 senior notes will mature on October 1, 2040. |

| Interest rate |

The 2021 senior notes will bear interest at % per year. |

| The 2040 senior notes will bear interest at 6.25% per year. |

| Interest payment dates |

The 2021 senior notes will pay interest on and of each year, commencing on , 2011. |

| The 2040 senior notes will pay interest on April 1 and October 1 of each year, commencing on October 1, 2011. |

| Ranking |

The notes will be our senior unsecured obligations and will rank equally with all of our other senior unsecured indebtedness, including all other unsubordinated debt securities issued under the indenture, from time to time outstanding. The indenture does not restrict the issuance by us or our subsidiaries of senior unsecured indebtedness. See “Description of the Notes.” |

| Form and denomination |

The notes will be issued in fully registered form in denominations of $2,000 or integral multiples of $1,000 in excess thereof. |

| Further issuances |

We may create and issue further notes ranking equally and ratably with either series of notes offered by this prospectus supplement in all respects, so that such further notes will be consolidated and form a single series with the applicable series of notes offered by this prospectus supplement and will have the same terms as to status, redemption or otherwise. |

| Optional redemption |

We may redeem the notes of either series, in whole or in part, at any time and from time to time, as described under the heading “Description of the Notes—Optional Redemption.” |

S-7

Table of Contents

| If the 2021 senior notes are redeemed on or after the date that is three months prior to their maturity date, the 2021 senior notes will be redeemed at a redemption price equal to 100% of the principal amount of the notes to be redeemed, plus accrued and unpaid interest to the date of redemption. |

| Mandatory special redemption |

The 2021 senior notes will be subject to a special mandatory redemption in the event the Acquisition is not consummated on or prior to July 29, 2011, or if prior to July 29, 2011, the Arrangement Agreement is terminated other than in connection with the consummation of the Acquisition and is not otherwise amended or replaced. In such an event, the 2021 senior notes will be redeemed at a price equal to 101% of the principal amount thereof plus accrued and unpaid interest from the date of initial issuance, or the most recent date to which interest has been paid or provided for, whichever is later, to but excluding, the special mandatory redemption date, such redemption being a special mandatory redemption. The “special mandatory redemption date” means the date no later than the tenth business day following the earlier to occur of (a) July 29, 2011, if the Acquisition has not been completed on or prior to July 29, 2011 and (b) the date that the Arrangement Agreement is terminated other than in connection with the consummation of the Acquisition and is not otherwise amended or replaced. See “Description of the Notes—Special Mandatory Redemption.” |

| Offer to repurchase upon change of control triggering event |

If we experience a Change of Control Triggering Event (as defined herein), we will be required, unless we have already exercised our option to redeem the notes of the applicable series, to offer to purchase the notes of the applicable series at a purchase price equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to the date of purchase. See “Description of the Notes—Change of Control Triggering Event.” |

| Certain covenants |

The indenture governing the notes contains covenants that restrict our ability, with certain exceptions, to: |

| • | incur debt secured by liens; and |

| • | engage in sale and leaseback transactions. |

| See “Description of the Notes—Certain Covenants.” |

| DTC eligibility |

The notes of each series will be represented by global certificates deposited with, or on behalf of, The Depository Trust Company, which we refer to as DTC, or its nominee. See “Description of the Notes—Book-Entry Delivery and Settlement.” |

| Same-day settlement |

Beneficial interests in the notes will trade in DTC’s same-day funds settlement system until maturity. Therefore, secondary market trading activity in such interests will be settled in immediately available funds. |

S-8

Table of Contents

| Use of proceeds |

We expect to receive net proceeds, after deducting underwriting discounts but before deducting other offering expenses, of approximately $ million from this offering. We intend to use the net proceeds from this offering, together with cash on hand and borrowings under the bridge credit facility and our new term loan, to fund the Acquisition and to pay related fees and expenses. The closing of this offering is expected to occur prior to the consummation of the Acquisition. If the Acquisition is not consummated, we are required to redeem the 2021 senior notes in a special mandatory redemption as further described under “Description of the Notes—Special Mandatory Redemption” and we intend to use the net proceeds from the 2040 senior notes offered hereby for general corporate purposes, including, without limitation, to fund capital expenditures and other strategic acquisitions. See “Use of Proceeds.” |

| No listing of the notes |

We do not intend to apply to list the notes on any securities exchange or to have the notes quoted on any automated quotation system. |

| Governing law |

The notes will be, and the indenture is, governed by the laws of the State of New York. |

| Risk factors |

Investing in the notes involves risk. See “Risk Factors” on page S-12 of this prospectus supplement, in the accompanying prospectus and the documents incorporated by reference herein or therein for a discussion of certain risks you should consider in connection with an investment in the notes. |

| Trustee, registrar and paying agent |

U.S. Bank National Association |

S-9

Table of Contents

Summary Consolidated and Pro Forma Financial Data

The table below sets forth a summary of our financial and other statistical data for the periods presented. We derived the financial data as of and for the years ended December 31, 2010, 2009 and 2008 from our audited consolidated financial statements. The table below also sets forth unaudited summary pro forma condensed consolidated financial data for the year ended December 31, 2010, which we have derived from the historical financial statements of Cliffs and Consolidated Thompson and should be read in conjunction with the unaudited pro forma condensed consolidated financial and other data included elsewhere in this prospectus supplement. The unaudited condensed consolidated pro forma statement of operations data set forth below gives effect to the Acquisition as if it had occurred on January 1, 2010 and the unaudited condensed consolidated pro forma balance sheet data set forth below gives effect to the Acquisition as if it had occurred as of December 31, 2010. The summary pro forma condensed consolidated financial information set forth below should not be considered indicative of actual results that would have been achieved had the Acquisition occurred on the respective dates indicated and do not purport to indicate balance sheet data or results of operations as of any future date or for any future period. We cannot assure you that the assumptions used in the preparation of the pro forma condensed consolidated financial information will prove to be correct. Prospective investors should read the summary consolidated and pro forma financial and other statistical data in conjunction with our consolidated financial statements, the related notes and other financial information incorporated by reference into this prospectus supplement.

| Year Ended December 31, | Pro Forma for the Year Ended December 31, |

|||||||||||||||

| 2008(a) | 2009 | 2010(b) | 2010 | |||||||||||||

| Financial data (in millions) |

||||||||||||||||

| Revenue from product sales and services |

$ | 3,609.1 | $ | 2,342.0 | $ | 4,682.2 | $ | 4,984.8 | ||||||||

| Cost of goods sold and operating expenses |

(2,449.4 | ) | (2,033.1 | ) | (3,158.7 | ) | (3,455.5 | ) | ||||||||

| Other operating expense |

(220.8 | ) | (78.7 | ) | (258.5 | ) | (298.6 | ) | ||||||||

| Operating income |

938.9 | 230.2 | 1,265.0 | 1,230.7 | ||||||||||||

| Net income(c) |

537.0 | 204.3 | 1,019.7 | 890.5 | ||||||||||||

| Less: Net income (loss) attributable to noncontrolling interest |

21.2 | (0.8 | ) | (0.2 | ) | 13.9 | ||||||||||

| Net income attributable to Cliffs shareholders |

515.8 | 205.1 | 1,019.9 | 876.6 | ||||||||||||

| Preferred stock dividends |

(1.1 | ) | — | — | — | |||||||||||

| Income attributable to Cliffs common shareholders |

514.7 | 205.1 | 1,019.9 | 876.6 | ||||||||||||

| Total assets |

4111.1 | 4,639.3 | 7,778.2 | 13,365.6 | ||||||||||||

| Long-term obligations |

580.2 | 644.3 | 1,881.3 | 4,254.7 | ||||||||||||

| Ratio of earnings to fixed charges |

15.2x | 6.1x | 18.7x | |||||||||||||

| Net cash from operating activities |

853.2 | 185.7 | 1,320.0 | |||||||||||||

| Redeemable cumulative convertible perpetual preferred stock |

0.2 | — | — | |||||||||||||

| Distributions to preferred shareholders cash dividends |

1.1 | — | — | |||||||||||||

| Distributions to common shareholders cash dividends(d) |

36.1 | 31.9 | 68.9 | |||||||||||||

| Iron ore and coal production and sales statistics |

||||||||||||||||

| (tons in millions—North America; metric tons in millions—Asia Pacific) |

||||||||||||||||

| Production tonnage—North American iron ore |

35.2 | 19.6 | 32.0 | 35.0 | (e) | |||||||||||

| —North American coal |

3.5 | 1.7 | 3.2 | |||||||||||||

| —Asia Pacific iron ore |

7.7 | 8.3 | 9.3 | |||||||||||||

| Production tonnage—North American iron ore (Cliffs’ share) |

22.9 | 17.1 | 25.4 | |||||||||||||

| Sales tonnage—North American iron ore |

22.7 | 16.4 | 26.2 | 28.9 | (e) | |||||||||||

| —North American coal |

3.2 | 1.9 | 3.3 | |||||||||||||

| —Asia Pacific iron ore |

7.8 | 8.5 | 9.3 | |||||||||||||

S-10

Table of Contents

| (a) | On May 21, 2008, Portman authorized a tender offer to repurchase shares, and as a result, our ownership interest in Portman increased from 80.4% to 85.2% on June 24, 2008. On September 10, 2008, we announced an off-market takeover offer to acquire the remaining shares in Portman, which closed on November 3, 2008. We subsequently proceeded with a compulsory acquisition of the remaining shares and have full ownership of Portman as of December 31, 2008. Results for 2008 reflect the increase in our ownership of Portman since the date of each step acquisition. |

| (b) | On January 27, 2010, we acquired all of the remaining outstanding shares of Freewest, including its interest in the Ring of Fire properties in Northern Ontario Canada. On February 1, 2010, we acquired entities from our former partners that held their respective interests in Wabush, thereby increasing our ownership interest from 26.8 percent to 100%. On July 30, 2010, we acquired all of the coal operations of privately-owned INR, and since that date, the operations acquired from INR have been conducted through our wholly-owned subsidiary known as CLCC. Results for 2010 include Freewest’s, Wabush’s and CLCC’s results since the respective acquisition dates. As a result of acquiring the remaining ownership interest in Freewest and Wabush, our 2010 results were impacted by realized gains of $38.6 million primarily related to the increase in fair value of our previous ownership interest in each investment held prior to the business acquisition. |

| (c) | In December 2010, we completed a legal entity restructuring that resulted in a change to deferred tax liabilities of $78.0 million on certain foreign investments to a deferred tax asset of $9.4 million for tax basis in excess of book basis on foreign investments as of December 31, 2010. A valuation allowance of $9.4 million was recorded against this asset due to the uncertainty of realization. The deferred tax changes were recognized as a reduction to our income tax provision in 2010. |

| (d) | On May 12, 2009, our Board of Directors enacted a 55% reduction in our quarterly common share dividend to $0.04 from $0.0875 for the second and third quarters of 2009 in order to enhance financial flexibility. The $0.04 common share dividends were paid on June 1, 2009 and September 1, 2009 to shareholders of record as of May 22, 2009 and August 14, 2009, respectively. In the fourth quarter of 2009, the dividend was reinstated to its previous level. On May 11, 2010, our Board of Directors increased our quarterly common share dividend from $0.0875 to $0.14 per share. The increased cash dividend was paid on June 1, 2010, September 1, 2010, and December 1, 2010 to shareholders on record as of May 14, 2010, August 13, 2010, and November 19, 2010, respectively. |

| (e) | The pro forma statistical data for the year ended December 31, 2010 reflects actual Consolidated Thompson iron ore concentrate production and sales of 3.0 million and 2.7 million metric tons, respectively. The Consolidated Thompson production and sales results for 2010 were impacted by ramp-up activities at the Bloom Lake mine. Annual production capacity of 8 million metric tons is expected to be reached during 2011. |

S-11

Table of Contents

An investment in the notes involves risk. Prior to making a decision about investing in our notes, and in consultation with your own financial and legal advisors, you should carefully consider the following risk factors, as well as the risk factors discussed in our Annual Report on Form 10-K for the fiscal year ended December 31, 2010, which are incorporated herein by reference. You should also refer to the other information in this prospectus supplement and the accompanying prospectus, including our consolidated financial statements and the related notes incorporated by reference in this prospectus supplement. Additional risks and uncertainties that are not yet identified may also materially harm our business, operating results and financial condition.

Risks Related to this Offering and the Notes

The notes are subject to prior claims of any secured creditors and the creditors of our subsidiaries, and if a default occurs we may not have sufficient funds to fulfill our obligations under the notes.

The notes are our unsecured general obligations, ranking equally with our other senior unsecured indebtedness and liabilities but junior to any secured indebtedness and effectively subordinated to the debt and other liabilities of our subsidiaries. The indenture governing the notes permits us and our subsidiaries to incur secured debt under specified circumstances. If we incur any secured debt, our assets and the assets of our subsidiaries will be subject to prior claims by our secured creditors. In the event of our bankruptcy, liquidation, reorganization or other winding up, assets that secure debt will be available to pay obligations on the notes only after all debt secured by those assets has been repaid in full. Holders of the notes will participate in our remaining assets ratably with all of our unsecured and unsubordinated creditors, including our trade creditors.

If we incur any additional obligations that rank equally with the notes, including trade payables, the holders of those obligations will be entitled to share ratably with the holders of the notes in any proceeds distributed upon our insolvency, liquidation, reorganization, dissolution or other winding up. This may have the effect of reducing the amount of proceeds paid to you. If there are not sufficient assets remaining to pay all of these creditors, all or a portion of the notes then outstanding would remain unpaid.

The indenture does not limit the amount of indebtedness that we and our subsidiaries may incur.

The indenture under which the notes will be issued does not limit the amount of indebtedness that we and our subsidiaries may incur. The indenture does not contain any financial covenants or other provisions that would afford the holders of the notes any substantial protection in the event we participate in a highly leveraged transaction.

Our existing and future indebtedness may limit cash flow available to invest in the ongoing needs of our business, which could prevent us from fulfilling our obligations under the notes.

After giving effect to this notes offering, and after giving effect to borrowings under the bridge credit facility, our new term loan and the debt that will be assumed in the Acquisition, our total indebtedness at December 31, 2010 would have been approximately $ million. Additionally, we have the ability under our existing credit facility to incur substantial additional indebtedness in the future. Our level of indebtedness could have important consequences to you. For example, it could:

| • | require us to dedicate a substantial portion of our cash flow from operations to the payment of debt service, reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes; |

| • | increase our vulnerability to adverse economic or industry conditions; |

| • | limit our ability to obtain additional financing in the future to enable us to react to changes in our business; or |

| • | place us at a competitive disadvantage compared to businesses in our industry that have less indebtedness. |

S-12

Table of Contents

Additionally, any failure to comply with covenants in the instruments governing our debt could result in an event of default which, if not cured or waived, would have a material adverse effect on us.

To service our indebtedness, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control. We also depend on the business of our subsidiaries to satisfy our cash needs. If we cannot generate the required cash, we may not be able to make the necessary payments under the notes.

Our ability to make payments on our indebtedness, including the notes, and to fund planned capital expenditures will depend on our ability to generate cash in the future. Our ability to generate cash, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

A significant portion of our operations is conducted through our subsidiaries. As a result, our ability to service our debts, including our obligations under the notes and other obligations, is dependent to some extent on the earnings of our subsidiaries and the payment of those earnings to us in the form of dividends, loans or advances and through repayment of loans or advances from us. Our subsidiaries are separate and distinct legal entities. Our subsidiaries have no obligation to pay any amounts due on the notes or to provide us with funds to meet our payment obligations on the notes, whether in the form of dividends, distributions, loans or other payments. In addition, any payment of dividends, loans or advances by our subsidiaries could be subject to statutory or contractual restrictions. Payments to us by our subsidiaries will also be contingent upon our subsidiaries’ earnings and business considerations. Our right to receive any assets of any of our subsidiaries upon their liquidation or reorganization, and therefore the right of the holders of the notes to participate in those assets, will be effectively subordinated to the claims of that subsidiary’s creditors, including trade creditors. In addition, even if we are a creditor of any of our subsidiaries, our rights as a creditor would be subordinate to any security interest in the assets of our subsidiaries and any indebtedness of our subsidiaries senior to that held by us. Finally, changes in the laws of foreign jurisdictions in which we operate may adversely affect the ability of some of our foreign subsidiaries to repatriate funds to us.

Additionally, our historical financial results have been, and we anticipate that our future financial results will be, subject to fluctuations. We cannot assure you that our business will generate sufficient cash flow from our operations or that future borrowings will be available to us in an amount sufficient to enable us to pay our indebtedness, including the notes, or to fund our other liquidity needs and make necessary capital expenditures.

An active trading market for the notes may not develop.

There is no existing market for the notes and we do not intend to apply for listing of the notes on any securities exchange or any automated quotation system. Accordingly, there can be no assurance that a trading market for the notes will ever develop or will be maintained. Further, there can be no assurance as to the liquidity of any market that may develop for the notes, your ability to sell your notes or the price at which you will be able to sell your notes. Future trading prices of the notes will depend on many factors, including prevailing interest rates, our financial condition and results of operations, the then-current ratings assigned to the notes and the market for similar debt securities. Any trading market that develops would be affected by many factors independent of and in addition to the foregoing, including:

| • | the time remaining to the maturity of the notes; |

| • | the outstanding amount of the notes; |

| • | the terms related to optional redemption of the notes; and |

| • | the level, direction and volatility of market interest rates generally. |

The underwriters have advised us that they currently intend to make a market in the notes of each series, but they are not obligated to do so and may cease market-making at any time in their sole discretion without notice.

S-13

Table of Contents

Risks Related to the Acquisition

Failure to successfully and efficiently integrate Consolidated Thompson into our operations may adversely affect our operations and financial condition.

The proceeds of this offering will be used to pay a portion of the purchase price of the acquisition of Consolidated Thompson. The integration of Consolidated Thompson into our operations will be a significant undertaking and will require significant attention from our management team. The Acquisition involves the integration of two companies that previously operated independently and the unique business culture of the two companies may prove to be incompatible. This integration is a complex, costly and time-consuming process, and we cannot assure you that this process will be successful. In addition, the integration of Consolidated Thompson into our operations will require significant one-time costs for tasks such as site visits and audits and may be difficult to execute, and we cannot guaranty or accurately estimate these costs at this time. Additional integration challenges include, among other things:

| • | managing a larger company than before completion of the Acquisition; |

| • | retaining existing employees; |

| • | the possibility of faulty assumptions underlying our expectations for the integration process; |

| • | incorporating new facilities into our business operations; |

| • | coordinating sales and delivery functions; |

| • | integrating mining logistics, information, communication and other systems; |

| • | maintaining our standards, controls, procedures and policies; and |

| • | unforeseen expenses, liabilities or delays associated with the Acquisition. |

We may not achieve the benefits we expect from the Acquisition if we are unable to successfully overcome these integration challenges.

We may not realize the growth opportunities and cost synergies that are anticipated from our Acquisition of Consolidated Thompson.

The benefits we expect to achieve as a result of our acquisition of Consolidated Thompson will depend, in part, on our ability to realize anticipated growth opportunities and cost synergies. Our success in realizing these growth opportunities and cost synergies, and the timing of this realization, depends on the successful integration of Consolidated Thompson’s business and operations with our business and operations. Even if we are able to integrate our business with Consolidated Thompson’s business successfully, this integration may not result in the realization of the full benefits of the growth opportunities and cost synergies we currently expect from this integration within the anticipated time frame or at all. For example, we may be unable to eliminate duplicative costs. Moreover, we anticipate that we will incur substantial expenses in connection with the integration of our business with Consolidated Thompson’s business. While we anticipate that certain expenses will be incurred, such expenses are difficult to estimate accurately, and may exceed current estimates. Accordingly, the benefits from the Acquisition may be offset by costs incurred or delays in integrating the companies, which could cause our revenue assumptions to be inaccurate.

Our historical and pro forma condensed consolidated financial information may not be representative of our results as a combined company.

The pro forma condensed consolidated financial information included in this prospectus supplement is constructed from the separate financial statements of us and Consolidated Thompson and may not represent the financial information that would result from operations of the combined companies. In addition, the pro forma condensed consolidated financial information presented in this prospectus supplement is based in part on certain assumptions regarding the Acquisition that we believe are reasonable. We cannot assure you that our

S-14

Table of Contents

assumptions will prove to be accurate over time. Accordingly, the historical and pro forma condensed consolidated financial information included in this prospectus supplement may not reflect what our results of operations and financial condition would have been had we been a combined entity during the periods presented, or what our results of operations and financial condition will be in the future. The challenge of integrating previously independent businesses makes evaluating our business and our future financial prospects difficult. Our potential for future business success and operating profitability must be considered in light of the risks, uncertainties, expenses and difficulties typically encountered by recently combined companies.

Consolidated Thompson is an exploration and development mining company whose full potential has not yet been realized, and we may encounter unexpected set-backs in bringing operations up to their full potential, which could hinder our ability to realize the full value of the Acquisition or decrease the anticipated value of the Acquisition.

Consolidated Thompson is an exploration and development mining company. Mining operations generally involve a high degree of risk and Consolidated Thompson’s operations are subject to the hazards and risks normally encountered in the exploration, development and production of iron ore, including environmental hazards and periodic interruptions in both production and transportation due to inclement or hazardous weather conditions. Such risks could result in damage to, or destruction of, mineral properties or producing facilities, personal injury, environmental damage, delays in mining, monetary losses and possible legal liability.

Development projects generally have a limited operating history upon which to base estimates of future cash capital and operating costs. For development projects, resource estimates and estimates of cash operating costs are, to a large extent, based upon the interpretation of geologic data obtained from drill holes and other sampling techniques, and feasibility studies, which derive estimates of capital and operating costs based upon anticipated tonnage and grades of ore to be mined and processed, ground conditions, the configuration of the ore body, expected recovery rates of minerals from the ore, estimated operating costs and other factors. As a result, future actual production, cash operating costs and economic returns could differ significantly from those estimated. It is not unusual for new mining operations to experience problems during the start-up phase, and delays in the commencement and initial acceleration of production often can occur. Any of these events could hinder our ability to realize the full value of the Acquisition or decrease the anticipated value of the Acquisition.

Consolidated Thompson’s ability to increase present iron ore production levels through the successful development of new mines and/or the expansion of existing mining operations is subject to numerous uncertainties and conditions.

Consolidated Thompson’s ability to increase present iron ore production levels is dependent, in part, on the successful development of new mines and/or the expansion of existing mining operations, including the planned increase of production capacity at its Bloom Lake Property from 8 million metric tons per year to 16 million metric tons per year and development of its Lamêlée Property and Peppler Lake Property. Development and expansion projects rely on the accuracy of predicted factors including: capital and operating costs; metallurgical recoveries; reserve estimates; and future metal prices. Development and expansion projects are also subject to accurate feasibility studies, the acquisition of surface or land rights, the issuance of necessary governmental permits, including environmental permits, and obtaining governmental approvals necessary for the operation of a project. As a result of the substantial expenditures involved, developments are also prone to material cost overruns versus budget. Any one of the above factors could delay or restrict our ability to increase present iron ore production levels and have a material adverse effect on our business, results of operations and financial condition.

S-15

Table of Contents

The historical financial statements of Consolidated Thompson may not be representative of the future financial position, future results of operations or future cash flows of the Consolidated Thompson business as part of our company nor do they reflect what the financial position, results of operations or cash flows of the Consolidated Thompson business would have been as a part of our company during the periods presented.

To date, Consolidated Thompson has only recorded revenues from operations in three quarters and net income from operations in two quarters. The development of Consolidated Thompson’s assets, which involved heavy investments that were not off-set by revenue, resulted in significant losses in previous periods. Since production has begun, these historical financial statements may not be representative of Consolidated Thompson’s future financial position, results of operations or cash flows. Additionally, there are a number of factors that may result in differences between the historical financial statements of Consolidated Thompson and the future financial position, results of operations or cash flows of Consolidated Thompson’s business as part of our company.

The holders of the 2040 senior notes will not have the benefit of the special mandatory redemption provisions if the Arrangement Agreement is terminated other than in connection with the consummation of the Acquisition or the Acquisition is not consummated on or prior to July 29, 2011.

The special mandatory redemption provisions are applicable only to the 2021 senior notes. If the definitive arrangement agreement is terminated other than in connection with the consummation of the Acquisition or the Acquisition is not consummated on or prior to July 29, 2011, the 2040 senior notes will remain outstanding and we will use the proceeds of the 2040 senior notes for general corporate purposes as further described under “Use of Proceeds”.

S-16

Table of Contents

We expect to receive net proceeds, after deducting underwriting discounts but before deducting other offering expenses, of approximately $ million from this offering. We intend to use the net proceeds from this offering, together with cash on hand and borrowings under the bridge credit facility and our new term loan, to fund the Acquisition of Consolidated Thompson and to pay related fees and expenses. Pending final use, we may invest the net proceeds from this offering in short-term marketable securities.

The closing of this offering is expected to occur prior to the consummation of the Acquisition. If the Acquisition is not consummated, we will be required to redeem the 2021 senior notes in a special mandatory redemption and we intend to use the net proceeds from the 2040 senior notes offered hereby for general corporate purposes, including, without limitation, to fund capital expenditures and other strategic acquisitions.

The following table sets forth the anticipated sources and uses of funds in connection with this offering, the Acquisition and related financing.

| Sources of Funds |

Uses of Funds |

|||||||||

| 2021 senior notes offered hereby |

$ | Consolidated Thompson acquisition |

$ | 4,501.8 | ||||||

| 2040 senior notes offered hereby |

Transaction fees and expenses |

95.9 | ||||||||

| Cash on hand |

Total |

$ | 4,597.7 | |||||||

| Bridge credit facility |

||||||||||

| New term loan |

||||||||||

| Total |

$ | 4,597.7 | ||||||||

S-17

Table of Contents

The following table sets forth our cash and cash equivalents and consolidated capitalization as of December 31, 2010:

| • | on a historical basis; |

| • | as adjusted to give effect to this offering; and |

| • | pro forma as adjusted to give effect to this offering, our borrowing under the bridge credit facility and the new term loan and the anticipated application of the use proceeds therefrom in connection with the Acquisition as described under “Use of Proceeds,” as well as the debt that will be assumed in the Acquisition. |

You should read this table in conjunction with our consolidated financial statements, the related notes and other financial information contained in our Annual Report on Form 10-K for the year ended December 31, 2010, which is incorporated by reference in this prospectus supplement, as well as the other financial information incorporated by reference in this prospectus supplement and the accompanying prospectus.

| As of December 31, 2010 | ||||||||||||

| (in millions) |

Actual | As adjusted | Pro forma as adjusted |

|||||||||

| Cash and cash equivalents |

$ | 1,566.7 | $ | $ | 234.4 | |||||||

| Capitalization: |

||||||||||||

| Long-term debt |

||||||||||||

| Revolving portion of credit facility(1) |

$ | — | $ | — | $ | — | ||||||

| Bridge credit facility |

— | — | 1,038.2 | |||||||||

| New term loan |

— | — | 1,250.0 | |||||||||

| Private placement senior notes |

325.0 | 325.0 | 325.0 | |||||||||

| 2020 5.9% senior notes |

397.8 | 397.8 | 397.8 | |||||||||

| 2020 4.8% senior notes |

499.0 | 499.0 | 499.0 | |||||||||

| Senior notes offered hereby(2) |

— | |||||||||||

| Existing 2040 6.25% senior notes |

491.3 | 491.3 | 491.3 | |||||||||

| Consolidated Thompson unsecured credit facility |

— | — | 49.8 | |||||||||

| Consolidated Thompson convertible debentures |

— | — | 253.9 | |||||||||

| Total long-term debt |

$ | 1,713.1 | $ | $ | ||||||||

| Total equity |

$ | 3,838.7 | $ | 3,838.7 | $ | 4,964.2 | ||||||

| Total capitalization |

$ | 5,551.8 | $ | $ | ||||||||

| (1) | As of December 31, 2010, no revolving loans were drawn under the credit facility; however, the principal amount of letter of credit obligations totaled $64.7 million, reducing available borrowing capacity to $535.3 million. |

| (2) | Includes 2021 senior notes and 2040 senior notes offered hereby, net of discount. |

S-18

Table of Contents

Unaudited Pro Forma Condensed Consolidated Financial Information

The following unaudited pro forma condensed consolidated financial information (Pro Forma Information) is based upon the historical consolidated financial information of Cliffs, which is incorporated by reference in this prospectus supplement, and Consolidated Thompson, which is included elsewhere in this prospectus supplement, and has been prepared to reflect the pending Acquisition of Consolidated Thompson by Cliffs. The unaudited pro forma condensed consolidated statement of financial position as of December 31, 2010 is presented as if the Acquisition and related financing had occurred on that date. The unaudited pro forma condensed consolidated statement of operations for the year ended December 31, 2010 assumes that the Acquisition and related financing occurred on January 1, 2010. The historical consolidated financial information has been adjusted to give effect to estimated pro forma events that are (1) directly attributable to the Acquisition, (2) factually supportable and (3) with respect to the statement of operations, expected to have a continuing impact on the consolidated results of operations.