Casablanca Capital Nominates Slate of Six Highly Qualified Directors

For Election to Board of Cliffs Natural Resources

Says Majority of Incumbent Board Should Be Replaced For Failed Expansion Strategy

And 80% Decline in Shareholder Value

Calls for New Strategy Focused on Core U.S. Business and Reiterates Support

For Metals and Mining Veteran Lourenco Goncalves to Lead Cliffs as CEO

______________________________________________________________

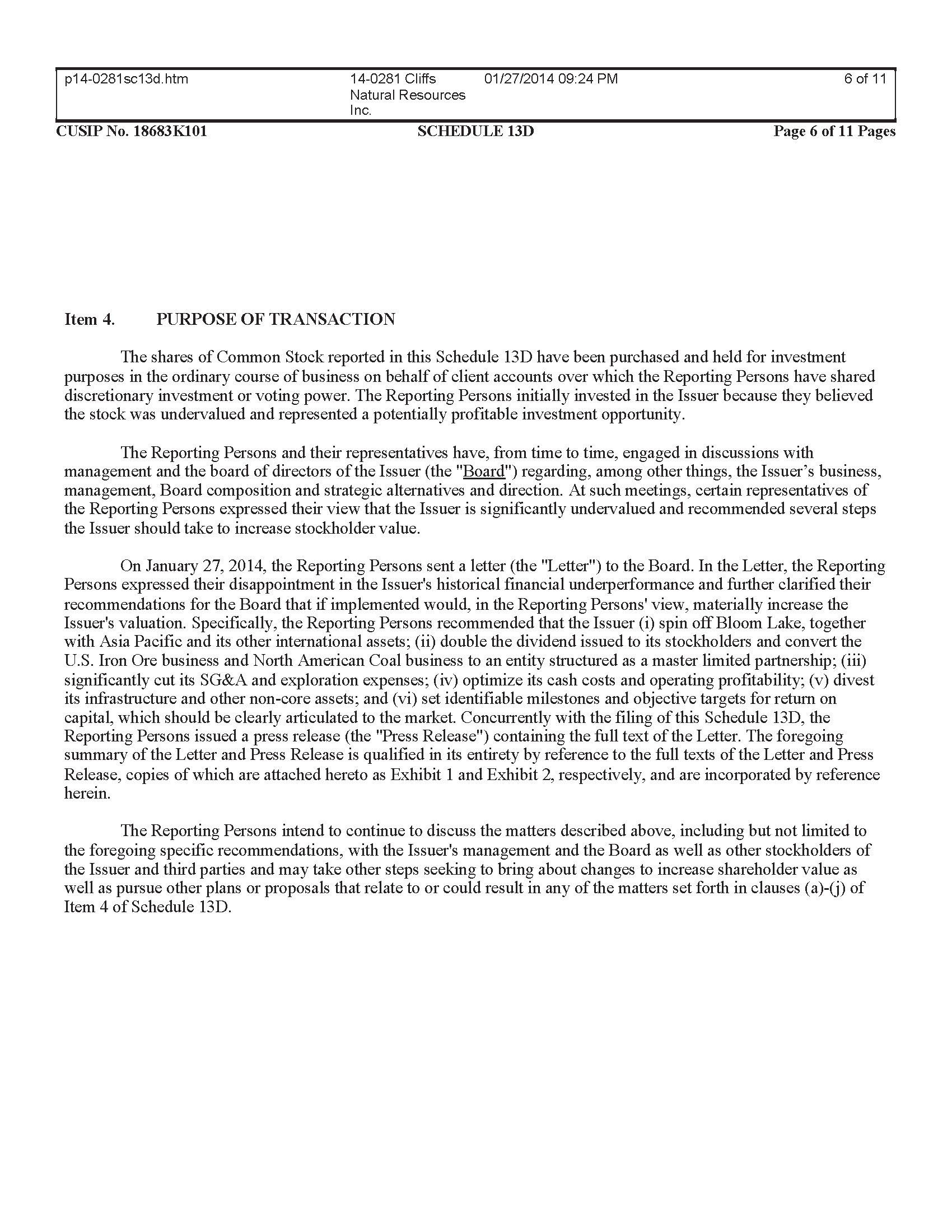

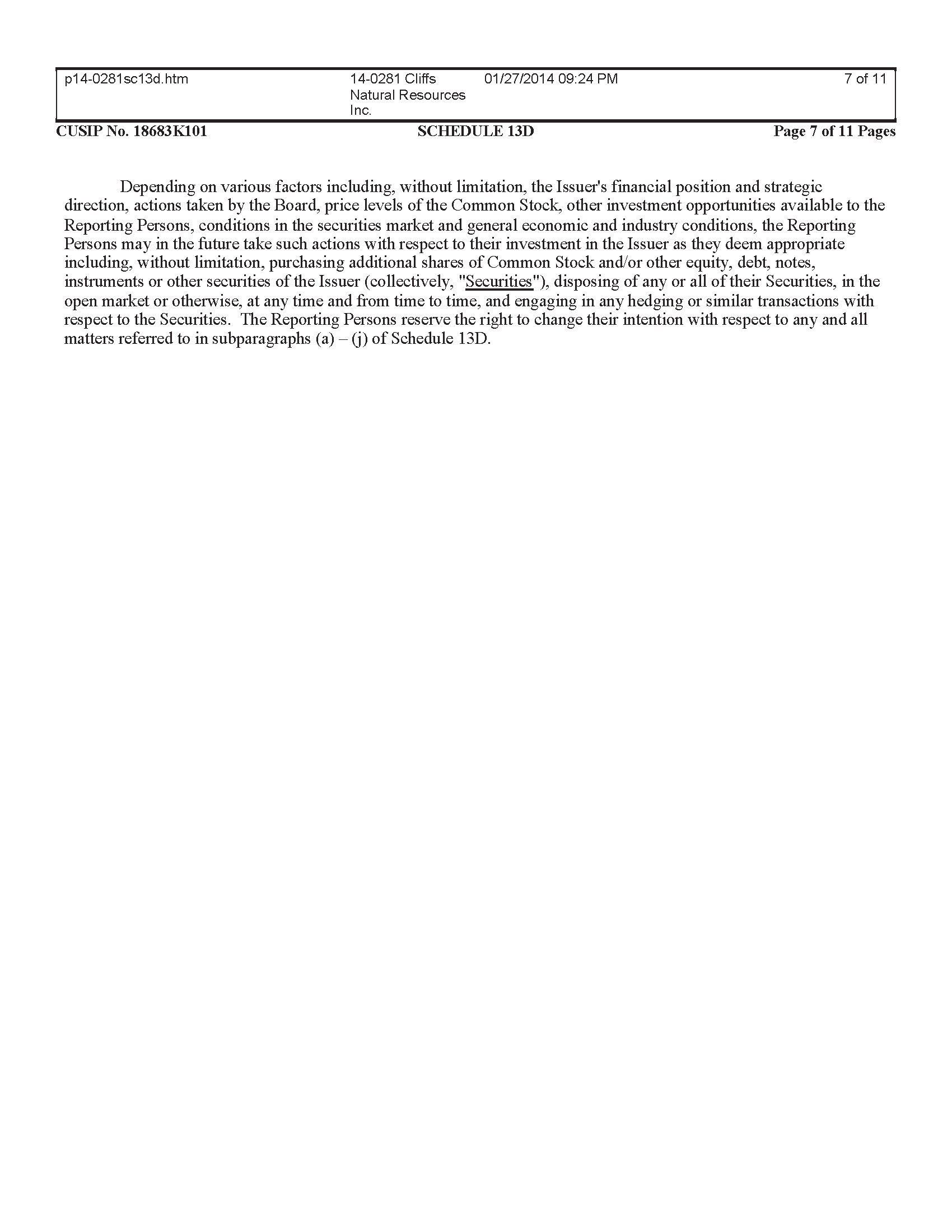

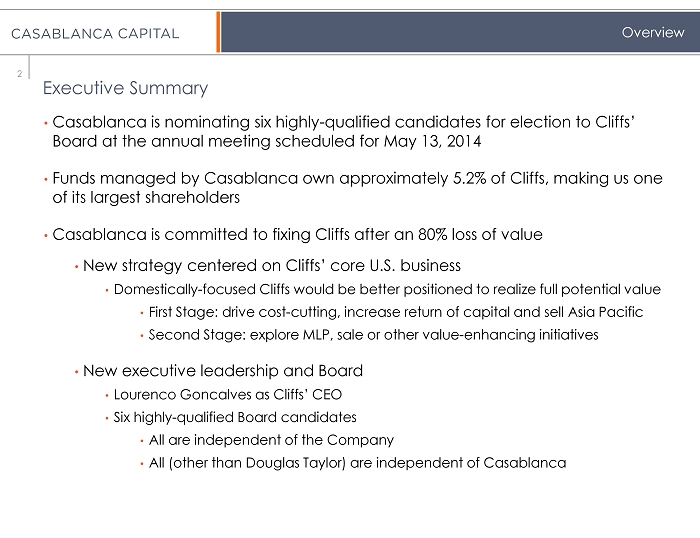

NEW YORK – March 6, 2014 – Casablanca Capital LP, (“Casablanca”) the beneficial owner of approximately 5.2% of Cliffs Natural Resources Inc. (NYSE: CLF), today sent a letter to the Cliffs Board of Directors nominating six highly qualified director candidates for election to the Board at the 2014 Annual Meeting of shareholders scheduled for May 13, 2014.

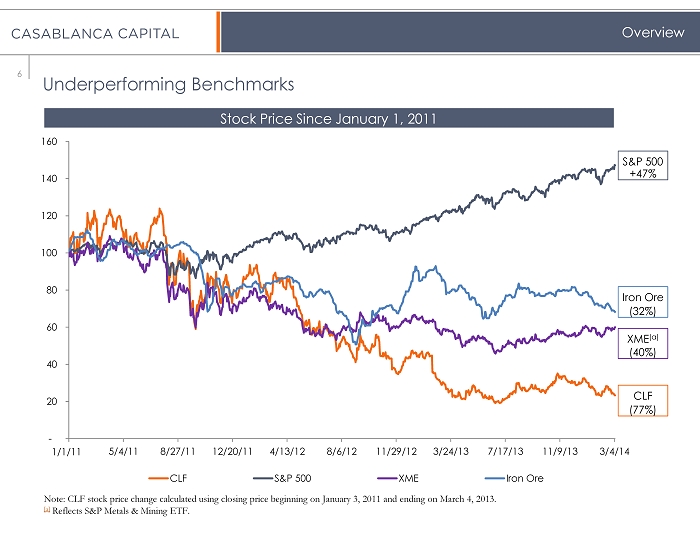

In the letter, Casablanca highlighted Cliffs’ failed expansion strategy and loss of over 80% of the Company’s market value which has been overseen by a majority of the current 11-member Board of Directors. Casablanca also outlined its proposal for a new strategy focused on Cliffs’ core U.S. assets to restore value for shareholders and reiterated its support for 30-year metals and mining veteran Lourenco Goncalves as the right leader to assume the position of CEO of Cliffs.

“Casablanca is committed to fixing Cliffs and restoring its value on behalf of all shareholders,” said Donald Drapkin, Chairman of Casablanca. “We are putting forward a highly-qualified slate of independent directors, including Lourenco Goncalves, who are far better equipped than the incumbent board members to implement a new strategic direction for Cliffs and to take the steps we believe are urgently required for the Company to get back on track and realize its full potential value.”

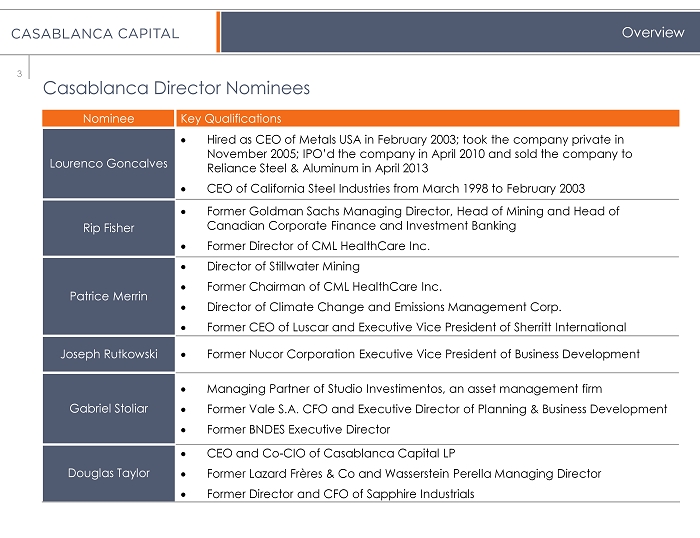

The six Casablanca nominees are:

| Nominee | Key Qualifications |

| Lourenco Goncalves |

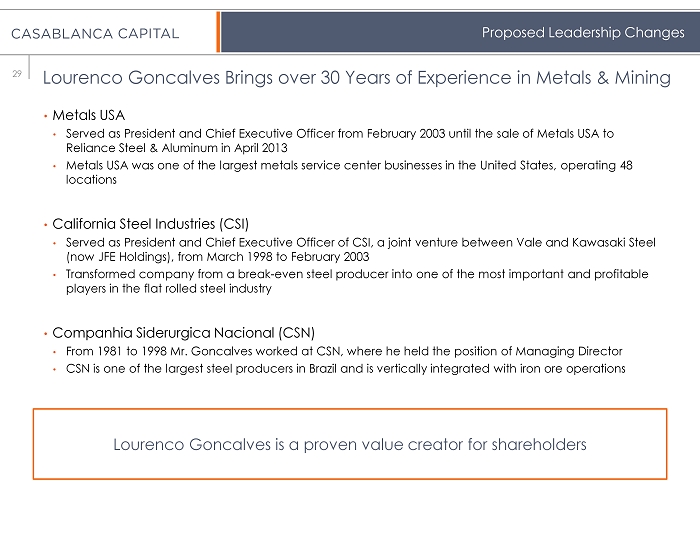

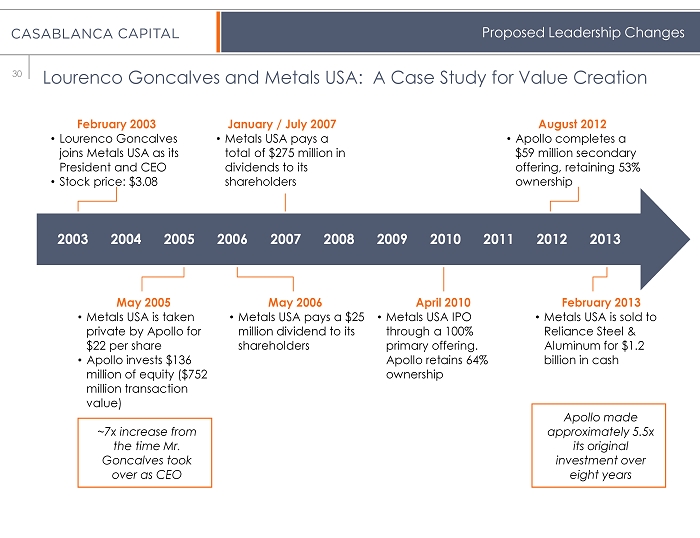

· Hired as CEO of Metals USA in February 2003; took the company private in November 2005; IPO’d the company in April 2010 and sold the company to Reliance Steel & Aluminum in April 2013 · CEO of California Steel Industries from March 1998 to February 2003 |

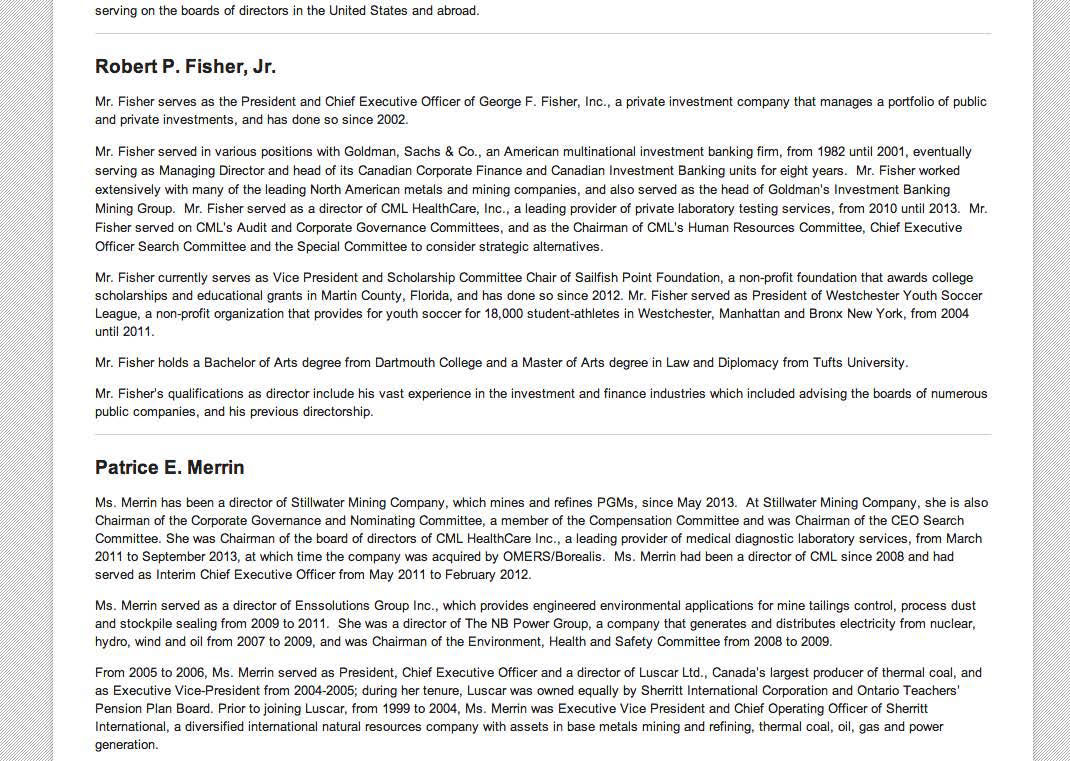

| Rip Fisher |

· Former Goldman Sachs Managing Director, Head of Mining and Head of Canadian Corporate Finance and Investment Banking · Former Director of CML HealthCare Inc. |

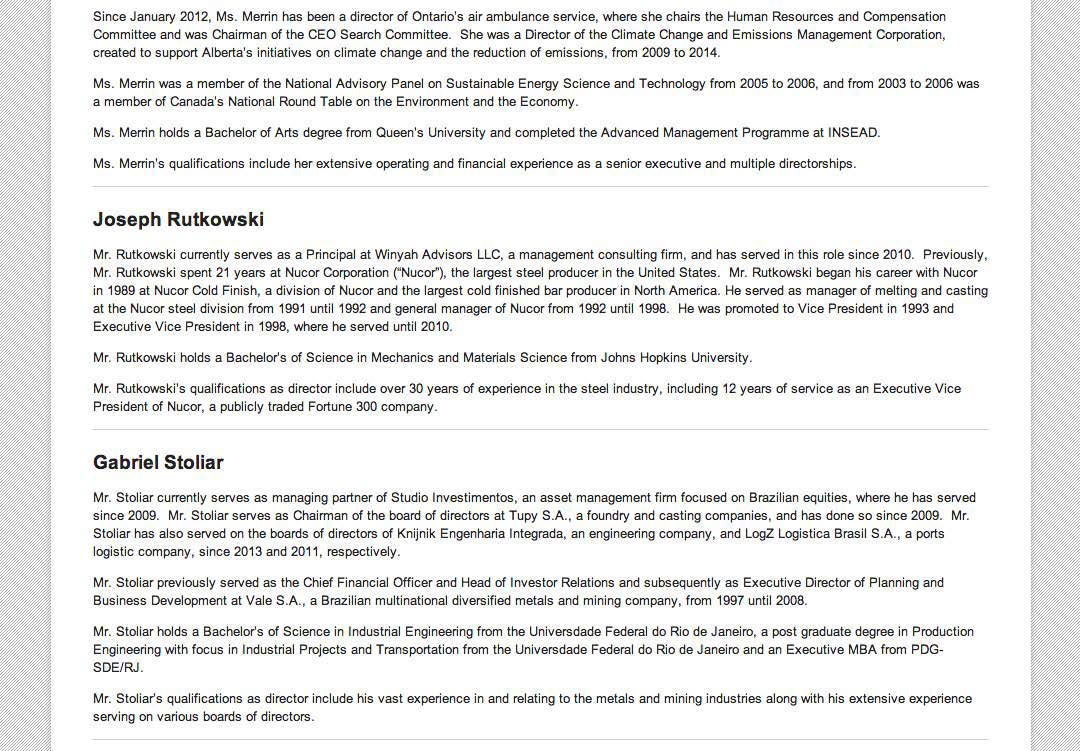

| Patrice Merrin |

· Director of Stillwater Mining · Former Chairman of CML HealthCare Inc. · Director of Climate Change and Emissions Management Corp. · Former CEO of Luscar and Executive Vice President of Sherritt International |

| Joseph Rutkowski | · Former Nucor Corporation Executive Vice President of Business Development |

| Gabriel Stoliar |

· Managing Partner of Studio Investimentos, an asset management firm · Former Vale S.A. CFO and Executive Director of Planning and Business Development · Former BNDES Executive Director |

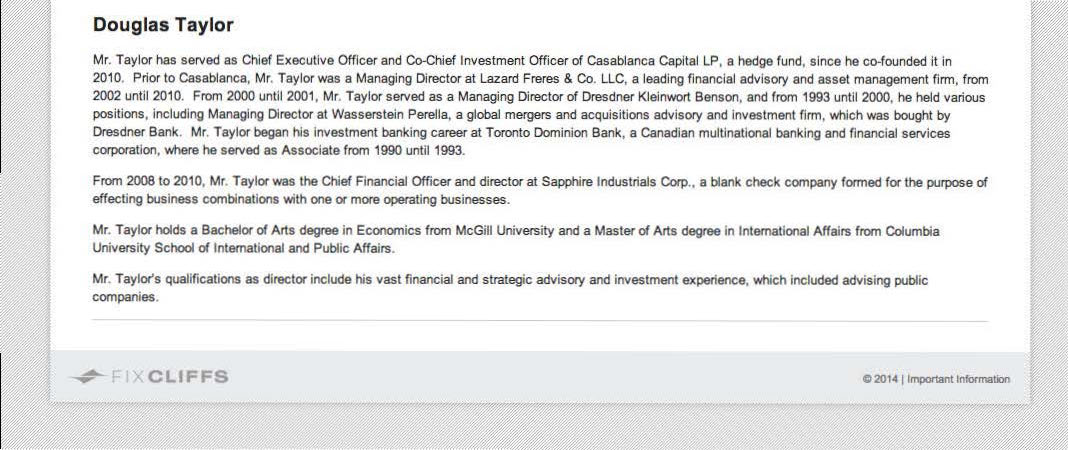

| Douglas Taylor |

· CEO and Co-CIO of Casablanca Capital LP · Former Lazard Frères & Co and Wasserstein Perella Managing Director · Former Director and CFO of Sapphire Industrials |

Casablanca also issued a presentation summarizing its recommendations for Cliffs. The presentation can be found at www.fixcliffs.com, along with other announcements, filings and background materials related to Casablanca’s investment in Cliffs.

Cliffs has established through notices to shareholders and filings with the SEC a record date of March 13, 2014 for voting eligibility at the May 13, 2014 annual meeting.

The letter Casablanca today sent to the Cliffs Board follows:

March 6, 2014

Members of Cliffs Natural Resources, Inc. Board of Directors

In care of:

James F. Kirsch

Executive Chairman

Cliffs Natural Resources Inc.

200 Public Square, Suite 3300

Cleveland, OH 44114

Members of the Board:

We are writing to provide more information regarding our intention to nominate six highly-qualified candidates for election to the Cliffs Natural Resources Inc. (“Cliffs”) Board of Directors at the Company’s annual meeting scheduled for May 13, 2014. Funds managed by Casablanca Capital LP (“Casablanca”) own approximately 5.2% of the outstanding common stock of Cliffs, making us one of your largest shareholders.

Casablanca is taking these actions because you have responded to our proposals to restore value with defensive half-measures, a hastily-announced CEO appointment and analytically-flawed attacks. In fact, we believe the Company has not come close to adequately addressing its 80% destruction of value. The notion that Cliffs is operating under new leadership with a new strategy is simply not true, in our view.

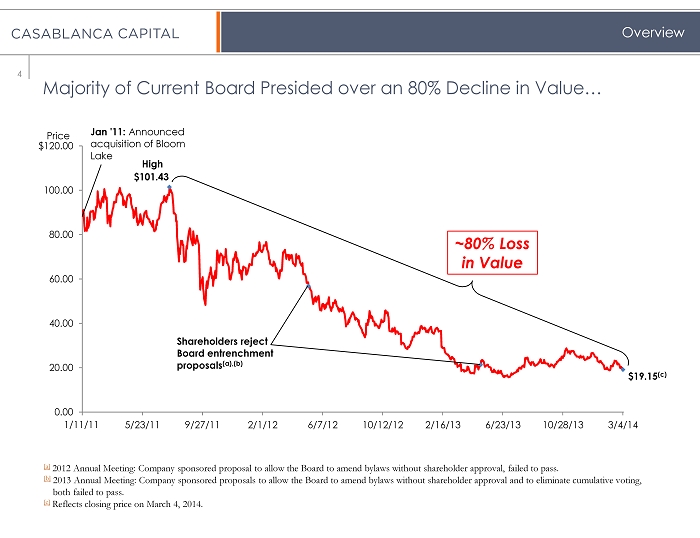

A Majority of the Current Board Presided over an 80% Decline in Value…

This Board presided over Cliffs’ dangerous and failed expansion strategy and engaged in continued entrenchment tactics, in our view. Further, a majority of the Board was in place, and is responsible for the approval, execution and continued pursuit of the Bloom Lake debacle.

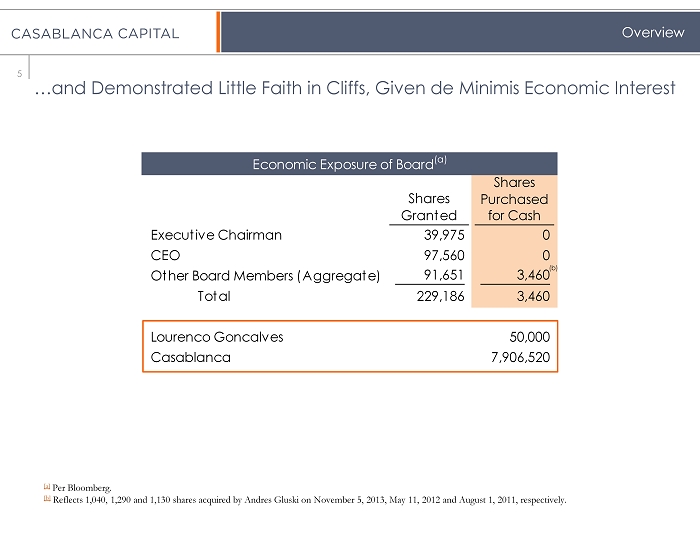

…and Lacks Meaningful Economic Alignment with Shareholders

| (a) 2012 Annual Meeting: Company-sponsored proposal to allow the Board to amend bylaws without shareholder approval fails to pass. |

|

(b) 2013 Annual Meeting: Company-sponsored proposals to allow the Board to amend bylaws without shareholder approval and to eliminate cumulative voting both fail to pass. |

(c) Share price based on Bloomberg as of March 4, 2014. |

…and Have Demonstrated Little Faith in Cliffs Given a de Minimis Economic Interest

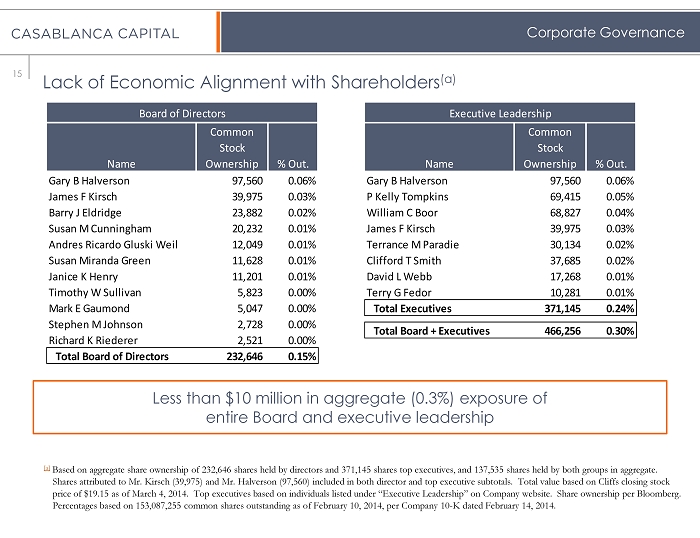

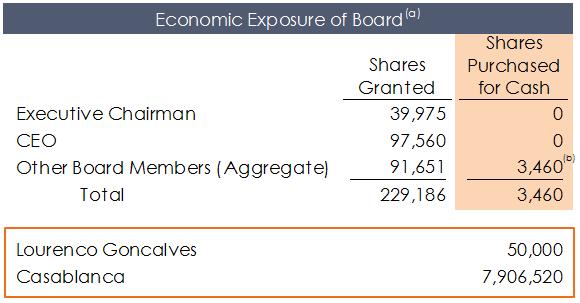

Lack of Economic Alignment with Shareholders. Based on publicly-available information, only a single director has purchased shares for cash, with the remainder simply receiving grants from the Company. The Board and top executives in the aggregate own or have an economic interest valued at less than $10 million at current prices.1 Casablanca believes this de minimis ownership poorly aligns management and the Board with shareholder interests and contributes to the irresponsible way in which the Company approaches key strategic and financial decisions.

(a) |

Per Bloomberg. | |

| (b) | Reflects 1,040, 1,290 and 1,130 shares acquired by Andres Gluski on November 5, 2013, May 11, 2012 and August 1, 2011, respectively. |

Casablanca is Committed to Fixing Cliffs and Restoring Value

Casablanca is committed to restoring value on behalf of all Cliffs shareholders, and proposes the following:

| · | A New Strategy for Cliffs Centered on Its Core U.S. Business. We believe a domestically-focused Cliffs will be better positioned to realize its full potential value. After taking steps to address the more immediate issues of cost-cutting and dividends (among others), Cliffs should consider second-stage value-creating steps for its U.S. business, including a master limited partnership (“MLP”), an eventual sale of the Company or other initiatives. |

| · | A New Board and Executive Leadership. Casablanca proposes Lourenco Goncalves as Cliffs’ CEO, and today sets forth its intention to nominate six highly-qualified candidates for election to Cliffs’ Board at the 2014 annual meeting. We believe our nominees bring the fresh perspective needed to reorient the Company and develop value-maximizing strategies. Our slate of directors comprises highly-qualified professionals, with considerable strategic, operating and financial experience. |

1 Based on aggregate share ownership of 232,646 shares held by directors, 371,145 shares held by top executives, and 466,256 shares held by both groups in aggregate. Shares attributed to Mr. Kirsch (39,975) and Mr. Halverson (97,560) included in both director and top executive subtotals. Total value based on Cliffs closing stock price of $19.15 as of March 4, 2014. Top executives selected based on individuals listed under “Executive Leadership” on Company website. Share ownership per Bloomberg.

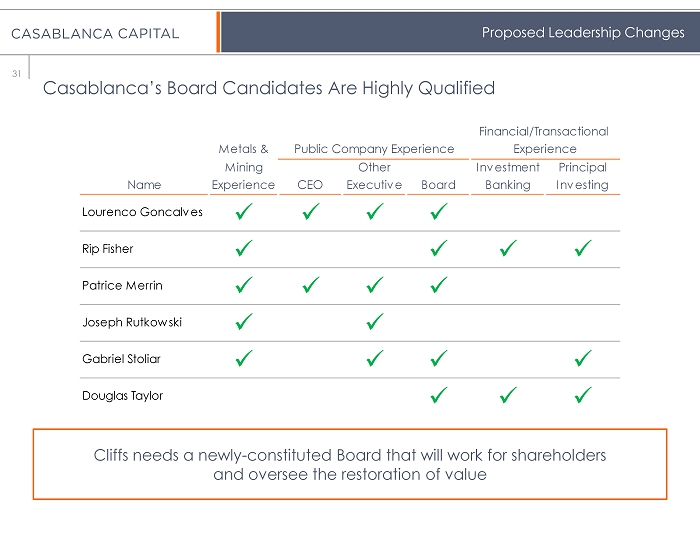

Casablanca’s Nominees

| Nominee | Key Qualifications |

| Lourenco Goncalves |

· Hired as CEO of Metals USA in February 2003; took the company private in November 2005; IPO’d the company in April 2010 and sold the company to Reliance Steel & Aluminum in April 2013 · CEO of California Steel Industries from March 1998 to February 2003 |

| Rip Fisher |

· Former Goldman Sachs Managing Director, Head of Mining and Head of Canadian Corporate Finance and Investment Banking · Former Director of CML HealthCare Inc. |

| Patrice Merrin |

· Director of Stillwater Mining · Former Chairman of CML HealthCare Inc. · Director of Climate Change and Emissions Management Corp. · Former CEO of Luscar and Executive Vice President of Sherritt International |

| Joseph Rutkowski |

· Former Nucor Corporation Executive Vice President of Business Development |

| Gabriel Stoliar |

· Managing Partner of Studio Investimentos, an asset management firm · Former Vale S.A. CFO and Executive Director of Planning and Business Development · Former BNDES Executive Director |

| Douglas Taylor |

· CEO and Co-CIO of Casablanca Capital LP · Former Lazard Frères & Co and Wasserstein Perella Managing Director · Former Director and CFO of Sapphire Industrials |

The Board Must Be Held Accountable

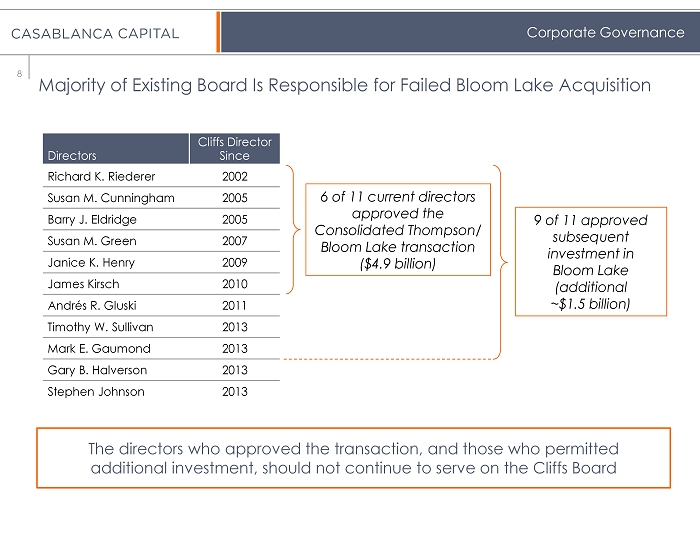

The Board Is Responsible for the Failed Bloom Lake Acquisition. Six of the Company’s eleven directors, including the Executive Chairman, held their Board seats at the time of the $4.9 billion Consolidated Thompson transaction in which the Company acquired the Bloom Lake project in Eastern Canada, and nine of the current directors were in their seats as the Company allocated an additional $1.5 billion in capital expenditures. With the critical Phase II expansion project now “indefinitely suspended,” approximately $6.5 billion spent to date, an estimated $(14) million2 operating loss last year and only difficult prospects ahead, we believe we are well founded in characterizing Bloom Lake as an abject failure. Casablanca believes the directors who approved the transaction, and those who oversaw the continued investment in this ill-conceived project, must be held accountable for their poor judgment and should not continue to serve on Cliffs’ Board.

2 Based on $111 million gross margin, less $125 million for estimated railroad take-or-pay obligations and volume penalties.

The Bloom Lake Acquisition Is Part of a Broader ~$9 Billion Value-Destroying Diversification Strategy, for which Members of the Board Are Responsible. The transactions below, which all appear to have lost money, were part of the Board’s spending spree:

| Estimated Investment |

Sitting Directors Responsible for Approving: | |||

| Project | Project Status | Acquisition | Further Investment | |

| Chromite3 | $500 million | Suspended in 2Q 2013 | 5 / 6 | 8 |

| Coal4 | $1.23 billion | Estimated 2014 breakeven | 6 | 10 |

| Amapa5 | $500 million | Divested for “nominal” amount in 3Q 2013 | 3 | 8 |

| Wabush6 | $285 million | Idled in 1Q 2014 | 5 | 10 |

These acquisitions, together with the Consolidated Thompson transaction, were approved or endorsed through further investment by a majority of the current Board and account for an estimated $9 billion in value destruction over the past eight years, totaling 1.4x the Company’s enterprise value and over 2.5x its equity value. Casablanca believes this demonstrates a pattern of continued mismanagement at the Board level, and that the directors responsible for these steps should not continue to hold their seats.

This Board Has Repeatedly Engaged in What We Consider To Be Entrenchment Tactics. In addition to persisting in a failed expansion and diversification strategy, the Board has on numerous occasions attempted to further entrench itself:

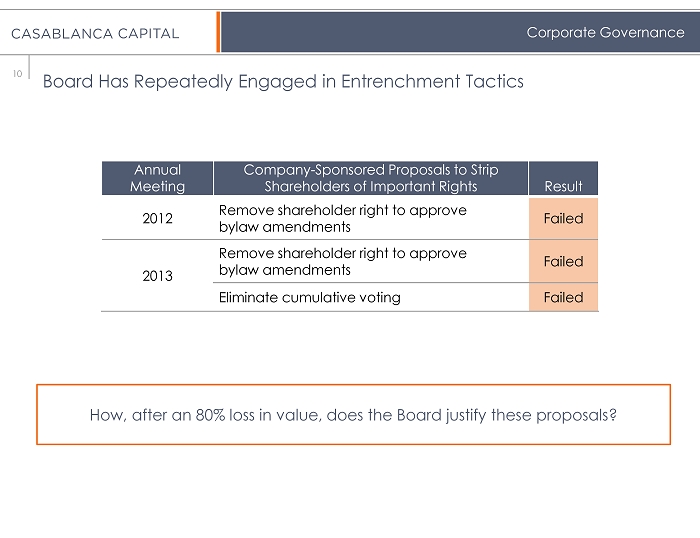

| · | Repeated Attempts to Strip Shareholders of Important Rights. For two years in a row, Cliffs has introduced proposals seeking to strip shareholders of their rights to approve all changes to Board bylaws (failing to gain approval on both occasions). Last year, the Company introduced a proposal to strip shareholders of their right to cumulate votes for directors in annual elections (which also failed to gain approval). Casablanca believes that shareholders’ rejection of these proposals reflects their concerns about this Board and its intentions. |

3 Five of the current directors were on the Board at the time of the $154 million Chromite Ontario transaction (11/23/09) and 6 were on the Board at the time of the $78 million Chromite Far North transaction (5/25/10). $500 million estimated total investment includes ~$70 million per year for feasibility and assessment studies, over 3 years.

4 Based on $757 million acquisition of West Virginia Coal (7/6/10) plus ~$470 million cumulative capex between 2010 and 2013. Excludes impact of Sonoma Coal (acquired for $140 million (1/9/07), divested for $141 million (7/10/12)). 2014 breakeven assumption based on midpoint of Company guidance of $85 – $90 expected revenues/ton and $85 – $90 expected cash costs/ton.

5 Based on $498.6 million book value and accounted for under the equity method as of 12/31/11.

6 Based on $103 million purchase price (initial stake acquired (1/1/97) for $15 million and remaining interest acquired (10/9/09) for $88 million), plus Casablanca-estimated $80 million cumulative capex, plus Company-announced $100 million idling costs. Cumulative capex estimated based on difference between $183 million asset impairment charge incurred in Q4 2013 and $103 million purchase price.

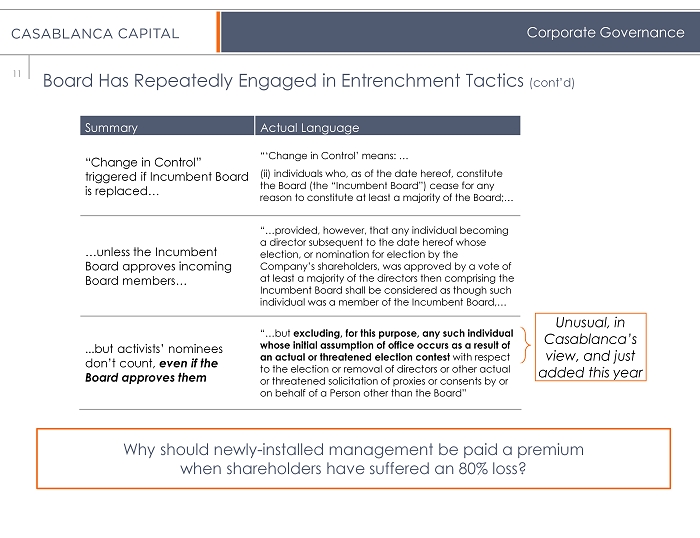

| · | Unusual Change in Control Provisions in Employment Agreements. Cliffs recently disclosed that its employee severance agreements include change in control payments to employees that are triggered if the current directors cease to be a majority on the Board.7 Importantly, this provision gives rise to payments if the new directors assume office as a result of an actual or threatened proxy contest—even if the current directors approve the new Board members. We believe this provision is an inappropriate and unreasonable entrenchment device that benefits senior executives at the expense of shareholders. |

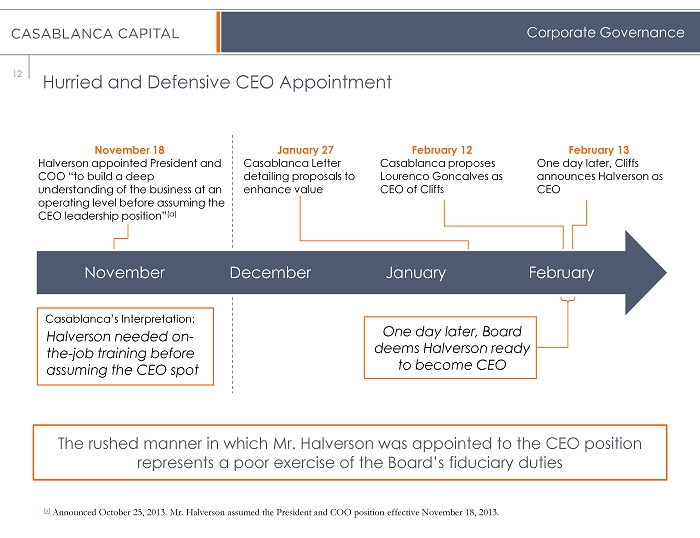

| · | Rushed and Defensive CEO Appointment. Just one day after Casablanca announced its support for Lourenco Goncalves to fill Cliffs’ vacant CEO seat, the Board rushed Mr. Halverson into the CEO role after months of failing to appoint a CEO. We do not believe this timing was a coincidence, particularly when the Board had stated that Mr. Halverson needed “the opportunity to build a deep understanding of the business at an operating level before assuming the CEO leadership position.”8 Mr. Halverson has no experience in leading a public company or in ferrous metals. We believe the hasty manner in which Mr. Halverson was appointed to the CEO position represents a defensive reaction by the Board and a poor exercise of its fiduciary duties. |

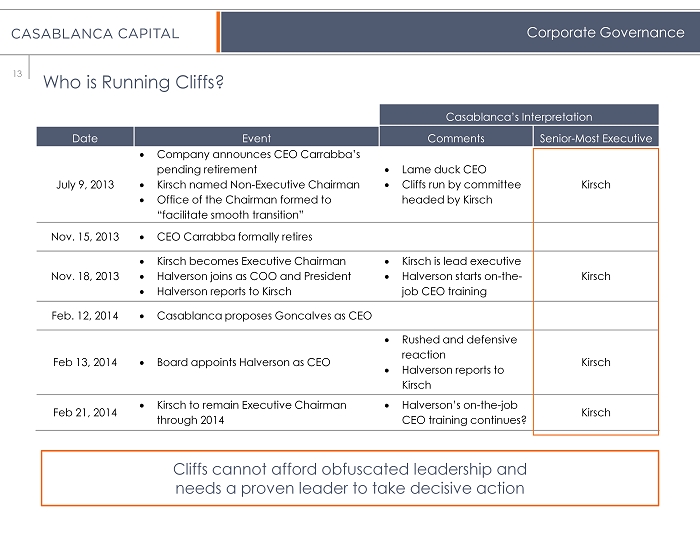

Questionable Reporting Relationship between CEO and Chairman. It appears that Mr. Halverson continues to report directly to the Executive Chairman. We believe this creates serious questions about who, in fact, is at the helm of Cliffs and why Mr. Kirsch remains Executive Chairman now that a CEO has been named.9 The Company, at this critical juncture, cannot afford obfuscated leadership, in our view.

Executive Chairman Has a Poor Track Record. We question Mr. Kirsch’s qualifications as Executive Chairman, given the 86% loss of value suffered by shareholders of Ferro Corp during his tenure as CEO from 2005 to 2012, and the fact that Ferro’s share price recovered most of these losses soon after Mr. Kirsch’s departure from that company.10 Cliffs cannot, in our view, afford an Executive Chairman that oversaw such an extensive loss of value.

7 Based on review of form of Change in Control Severance Agreement filed as exhibit to the Company’s Form 10-K dated February 14, 2014.

8 Company press release dated October 25, 2013.

9 Since Mr. Halverson's appointment as CEO, Cliffs has failed to publicly disclose the current reporting scheme of the Company's management. Prior to the appointment, Cliffs disclosed that Mr. Halverson was to report to Mr. Kirsch; however, the Company's presentation filed with the SEC on February 21, 2014 does not include Mr. Kirsch in its organizational chart setting forth Cliffs' management team.

10 Ferro’s stock sunk from its price of $19.52 on November 29, 2005 (the date Kirsch joined Ferro) to $2.64 on November 13, 2012 (the date Kirsch resigned as CEO of Ferro)—a decline of approximately 86%. Ferro’s stock had recovered to $13.55 as of March 4, 2014, a 413% rally since Kirsch’s resignation.

Cliffs Does Not Have a New Strategy

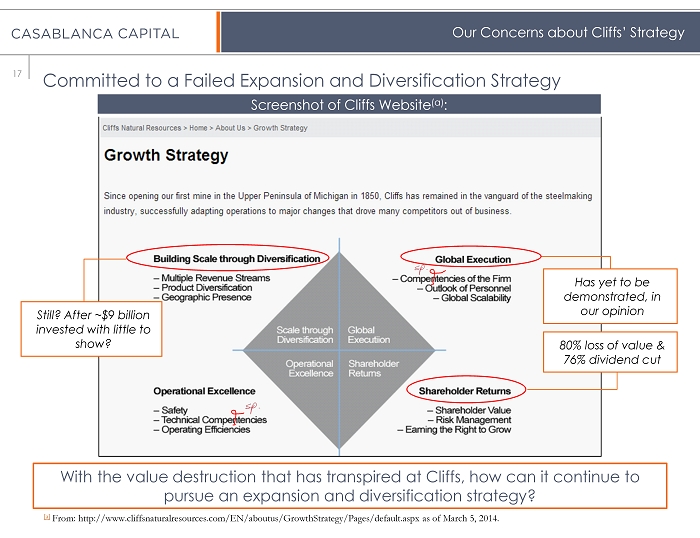

Despite Cliffs’ assertions around its “new strategic direction,” Casablanca sees only variations on what it considers to be the same failed strategy of international expansion and diversification.

Set to Continue with a Failed Expansion Strategy. Approximately three weeks ago, Cliffs reiterated its “ability to gain scale and diversify our geographic footprint” as a key component of its overall strategy.11 On Cliffs’ February 14, 2014 earnings call, Mr. Halverson, while discussing Asia Pacific’s mine life beyond 2020, stated that Cliffs is “looking at adjacent properties in the neighborhood” and “there's more to be added there.”12 In fact, Cliffs’ website highlights expansion and diversification as core tenets of the Company’s strategy, despite the extraordinary costs incurred pursuing this very strategy.

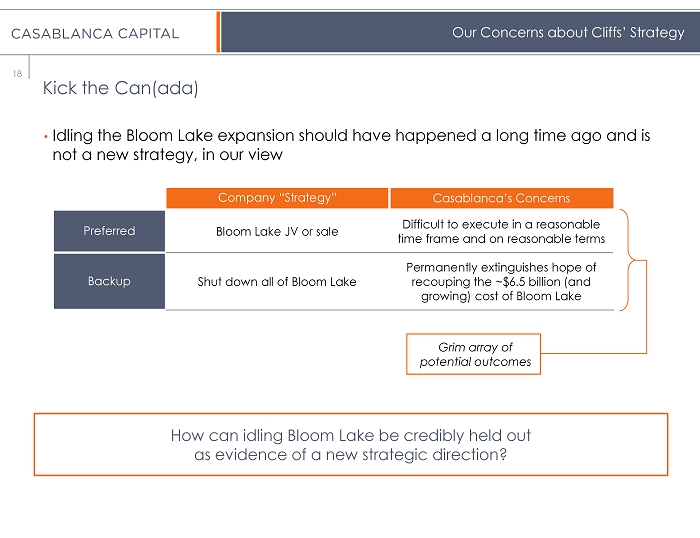

Kick the Can(ada). Idling the Bloom Lake expansion was in Casablanca’s view an obvious step that should have been taken long ago. As management acknowledges, however, this is only a temporary measure, and we do not accept an indefinite suspension as evidence of a new strategy. Beyond this preliminary step, Cliffs has only offered what we consider to be a vague outline for a permanent solution. We remain concerned that its preferred solution of a joint venture (or sale) transaction will be difficult to execute in a reasonable time frame and on reasonable terms. If these efforts fail, Cliffs intends to shut down Bloom Lake altogether—a move that, in our view, would permanently extinguish any hope of recouping the approximately $6.5 billion (and growing) cost of Bloom Lake. Similarly, the Company’s decisions to stop pursing the costly chromite project and to idle the loss-making Wabush mine underscore the Board’s multi-billion dollar mistakes.

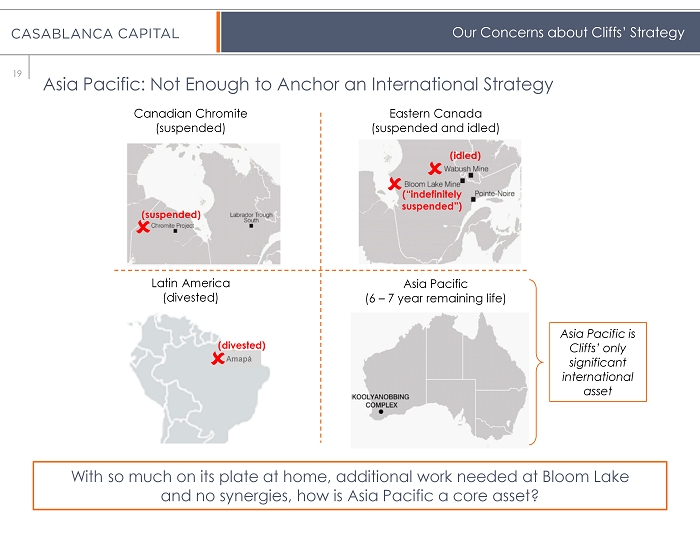

Asia Pacific: Not Enough to Anchor an International Strategy. With Bloom Lake on indefinite hold, Wabush idled, the chromite project suspended and Amapa divested, Cliffs’ international portfolio has been reduced to its Asia Pacific asset. Management has indicated it expects this asset to reach the end of its productive life between 2020 and 2021. Given its location on the other side of the globe and its expected life, we believe the Asia Pacific asset alone is insufficient to anchor a continuing international strategy.

Managing Capital to Fund Expansion Efforts

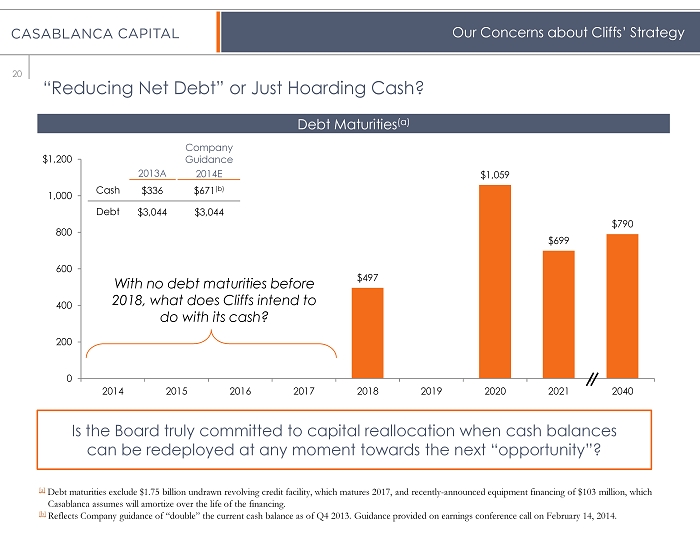

Hoarding Cash. Cliffs has aligned its capital allocation policy with its expansion strategy, announcing its intention to retain cash on the balance sheet—a step it characterized as “reducing net debt,” but that Casablanca believes merely constitutes hoarding cash. With no immediate significant debt maturities,13 Company-projected year-end 2014 cash balances of approximately $600 million and access to the undrawn $1.75 billion revolver, Cliffs appears to be saving up for the next “opportunity.”

11 See Cliffs Form 10K filed February 14, 2014 for the period ending December 31, 2013 (“Strategy” section).

12 Cliffs earnings conference call on February 14, 2014.

13 The Company’s first bond maturity, for $497 million, won’t occur until 2018, and the lion’s share of its bonds don’t mature until 2020-2021 ($1,059 and $699 million, respectively), per Bloomberg. Debt maturities exclude $1.75 billion revolving credit facility (since it is undrawn) and recently-announced equipment financing of $103 million, which Casablanca assumes will amortize over the life of the financing.

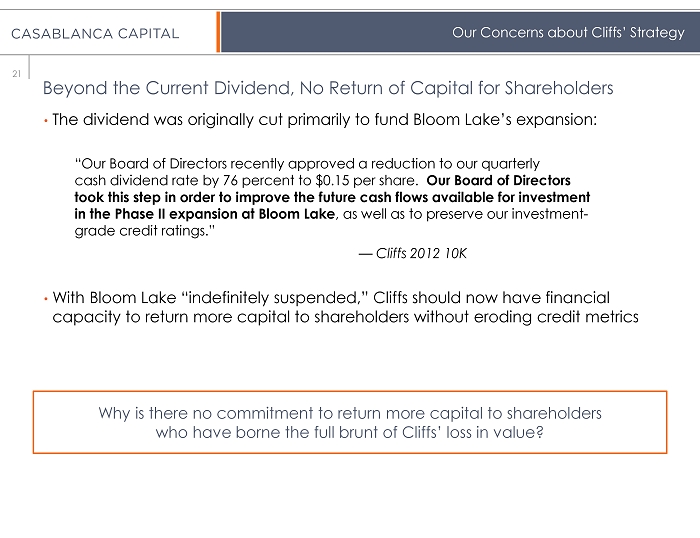

Beyond the Current Dividend, No Return of Capital for Shareholders. Last year, the Board cut the dividend by 76% to “improve the future cash flows available for investment in the Phase II expansion at Bloom Lake, as well as to preserve our investment-grade credit ratings.” Yet, with Bloom Lake now on indefinite hold and an improved financial profile, Cliffs has not indicated any intention to increase distributions to shareholders.

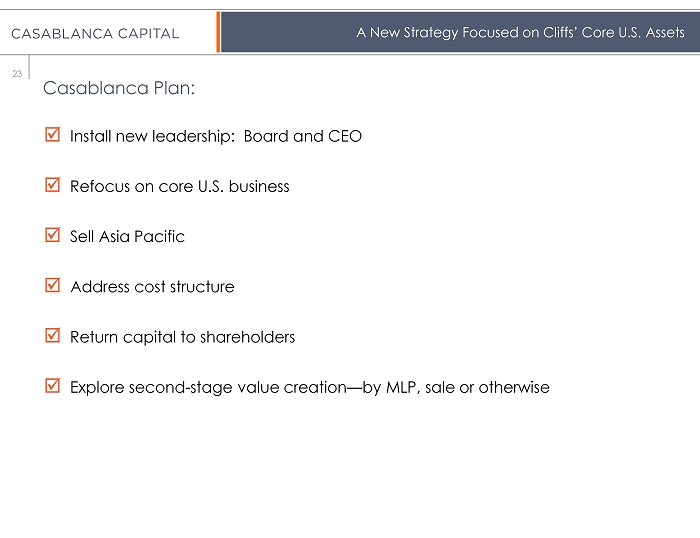

Casablanca Proposes a New Strategy Focused on Cliffs’ Core U.S. Assets

We believe Cliffs should refocus on its core U.S. operations, cement customer relationships, position itself to capitalize on domestic growth opportunities, accelerate cost cuts and return additional capital to shareholders. Cliffs’ assets have strategic value and, under the right management, warrant a valuation far in excess of what the market accords them today, in our view.

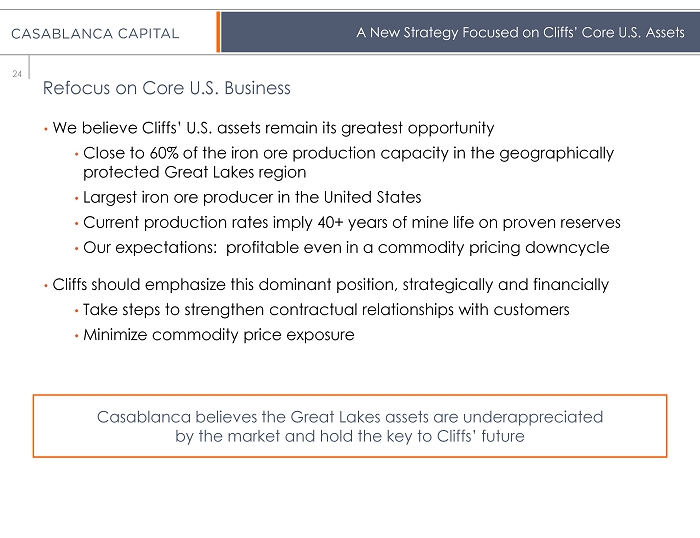

Refocus on Core U.S. Business. We continue to believe that Cliffs’ U.S. assets remain its greatest opportunity. Cliffs has close to 60% of the iron ore production capacity in the geographically-protected Great Lakes region and is the largest iron ore producer in the United States. At current production rates, its proven reserves offer over 40 years of mine life. According to our analysis, these assets should continue to operate profitably, even in a depressed commodity pricing environment. Cliffs needs to better emphasize this dominant position, both strategically and financially, and minimize commodity price exposure to highlight value.

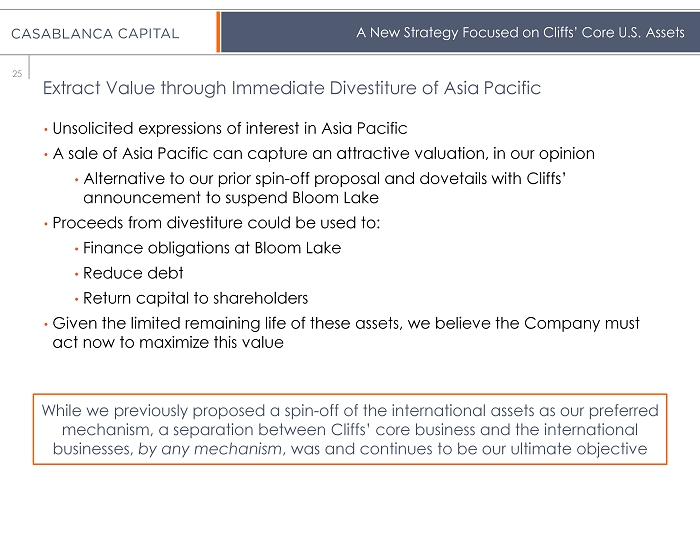

Extract Value through Immediate Divestiture of Asia Pacific. Since Casablanca publicly announced its position in Cliffs, we have received a number of unsolicited expressions of interest in the Asia Pacific assets. Accordingly, we believe these assets should command an attractive valuation if sold—an alternative transaction to a spin-off that achieves most of the same objectives and dovetails with Cliffs’ announcement to suspend the Bloom Lake expansion. Proceeds from the sale of Asia Pacific could finance remaining obligations at Bloom Lake, debt reduction and return of capital to shareholders. Given the remaining life of these assets, we believe Cliffs must act immediately to capture this strategic value. While we previously proposed a spin-off of the international assets, a separation between Cliffs’ core business and the international businesses, by any mechanism, was and continues to be our ultimate objective.

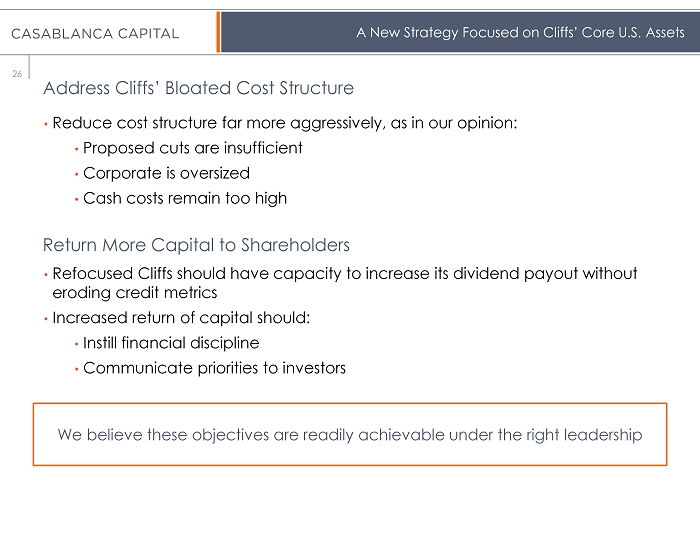

Address Bloated Cost Structure. Cliffs must reduce its cost structure far more aggressively, as its proposed cuts are insufficient given an oversized corporate infrastructure, and cash costs remain too high, in our opinion. We expect, with a more narrowly-focused company, management will be better able to concentrate on further reducing SG&A expenses and improving operating margins.

Return More Capital to Shareholders. With the international assets divested, commodity price exposure greatly reduced, and costs addressed, we believe a de-risked and more profitable Cliffs will have ample capacity to return more capital without eroding credit metrics. A commitment to return capital will, in our view, instill financial discipline, clearly communicate priorities and better position Cliffs to realize its full potential value.

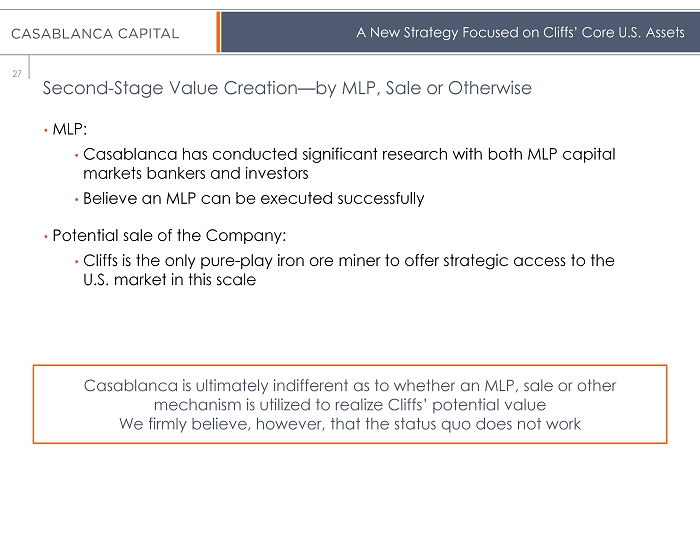

Second-Stage Value Creation—by MLP, Sale or Otherwise. Casablanca has conducted significant research with both MLP capital markets bankers and investors, and continues to believe the transaction can be executed successfully. We also believe Cliffs, after taking the steps outlined above, could potentially realize an attractive valuation in a sale of the Company, as it is the only pure-play iron ore miner of this scale to offer strategic access to the U.S. market. However, we are ultimately indifferent as to whether an MLP, sale or other mechanism is utilized to realize Cliffs’ potential value.

Casablanca Proposes Leadership Changes to Cliffs Executive Ranks and Board

Casablanca Believes New Leadership Is Required. We are putting forward a new slate of directors that, together with Lourenco Goncalves as CEO, will be better equipped, in our view, to implement a new strategic direction for Cliffs and to take the steps required for it to realize its full value potential.

Lourenco Goncalves Is a Proven Value Creator. As previously announced, we are proposing that Lourenco Goncalves lead Cliffs. A 30-year veteran of the metals and mining industry, Mr. Goncalves is a proven value creator who brings deep experience with companies in the ferrous value chain and has both the strategic and operational skills needed to effect urgent change and restore the fundamental value of Cliffs.

Casablanca’s Board Candidates Are Well Qualified to Oversee the Restoration of Value. Cliffs requires a fresh perspective, independent thinking, and analytical rigor—traits that we believe the incumbent Board lacks. Casablanca has nominated six highly-qualified directors whose experience should immediately add value to a Board that in our view is entrenched and unaccountable.

Conclusion

As a significant shareholder, we are troubled by the value destruction that has occurred under the current Board’s watch and firmly believe the status quo is unacceptable—shareholders have suffered enough. Cliffs desperately needs a new strategy and leadership with a fresh perspective. We are confident that substantial shareholder representation among a group of highly-qualified, independent directors on Cliffs’ Board and a new CEO are critical components of any solution. We firmly believe Casablanca’s slate of nominees is overwhelmingly qualified and offers a superior alternative to the incumbent directors up for reelection at the 2014 annual meeting.

Very truly yours,

/s/ |

/s/ |

/s/ |

|

Donald G. Drapkin Chairman |

Douglas Taylor Chief Executive Officer |

Gregory S. Donat Partner & Portfolio Manager |

About Casablanca Capital LP

Casablanca Capital is an Event Driven and Activist investment manager based in New York, founded in 2010 by Donald G. Drapkin and Douglas Taylor. Casablanca invests in high quality but underperforming public companies that have multiple levers to unlock shareholder value. The firm seeks to engage with the management, boards, and shareholders of those companies in a constructive dialogue in order to enhance shareholder value through improved operational efficiencies, strategic divestitures, capital structure optimization and increased corporate focus. In 2011, Casablanca successfully initiated a campaign at Mentor Graphics Corporation to improve profitability and enhance value at the company, working with shareholders to elect three nominees to Mentor’s Board.

Cautionary Statement Regarding Opinions and Forward-Looking Statements

Certain information contained herein constitutes “forward-looking statements” with respect to Cliffs Natural Resources Inc. ("Cliffs"), which can be identified by the use of forward-looking terminology such as “may,” “will,” “seek,” “should,” "could," “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities. Due to various risks, uncertainties and assumptions, actual events or results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. The opinions of Casablanca Capital LP ("Casablanca") are for general informational purposes only and do not have regard to the specific investment objective, financial situation, suitability or particular need of any specific person, and should not be taken as advice on the merits of any investment decision. This material does not recommend the purchase or sale of any security. Casablanca reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. Casablanca disclaims any obligation to update the information contained herein. Casablanca and/or one or more of the investment funds it manages may purchase additional Cliffs shares or sell all or a portion of their shares or trade in securities relating to such shares.

# # #

Media Contacts:

Sard Verbinnen & Co

George Sard/Matt Benson

212-687-8080

Investor Contacts:

Okapi Partners

Bruce H. Goldfarb/Patrick McHugh/Lydia Mulyk

212-297-0720

CASABLANCA CAPITAL LP, DONALD G. DRAPKIN AND DOUGLAS TAYLOR (COLLECTIVELY, “CASABLANCA") INTEND TO FILE WITH THE SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) A DEFINITIVE PROXY STATEMENT AND ACCOMPANYING FORM OF PROXY CARD TO BE USED IN CONNECTION WITH THE SOLICITATION OF PROXIES FROM STOCKHOLDERS OF CLIFFS NATURAL RESOURCES INC. (THE "COMPANY") IN CONNECTION WITH THE COMPANY'S 2014 ANNUAL MEETING OF STOCKHOLDERS. ALL STOCKHOLDERS OF THE COMPANY ARE ADVISED TO READ THE DEFINITIVE PROXY STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF PROXIES BY CASABLANCA, ROBERT P. FISHER, JR., CELSO LOURENCO GONCALVES, PATRICE E. MERRIN, JOSEPH RUTKOWSKI AND GABRIEL STOLIAR (COLLECTIVELY, THE "PARTICIPANTS"), WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL INFORMATION RELATED TO THE PARTICIPANTS. WHEN COMPLETED, THE DEFINITIVE PROXY STATEMENT AND AN ACCOMPANYING PROXY CARD WILL BE FURNISHED TO SOME OR ALL OF THE COMPANY'S STOCKHOLDERS AND ARE, ALONG WITH OTHER RELEVANT DOCUMENTS, AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, OKAPI PARTNERS LLC, CASABLANCA'S PROXY SOLICITOR, WILL PROVIDE COPIES OF THE DEFINITIVE PROXY STATEMENT AND ACCOMPANYING PROXY CARD WITHOUT CHARGE UPON REQUEST BY CALLING (212) 297-0720 OR TOLL-FREE AT (877) 274-8654.

INFORMATION ABOUT THE PARTICIPANTS AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS BY SECURITY HOLDINGS WILL BE CONTAINED IN THE PRELIMINARY PROXY STATEMENT ON SCHEDULE 14A TO BE FILED BY CASABLANCA WITH THE SEC ON MARCH 6, 2014. THIS DOCUMENT CAN BE OBTAINED FREE OF CHARGE FROM THE SOURCES INDICATED ABOVE.