UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For quarterly period ended March 31, 2012

¨ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE EXCHANGE ACT

For the transition period from _______________ to ________________

Commission file number 0-14237

First United Corporation

(Exact name of registrant as specified in its charter)

| Maryland | 52-1380770 | |

| (State or other jurisdiction of | (I. R. S. Employer Identification No.) | |

| incorporation or organization) |

19 South Second Street, Oakland, Maryland 21550-0009

(Address of principal executive offices) (Zip Code)

(800) 470-4356

(Registrant's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer £ | Accelerated filer £ |

| Non-accelerated filer £ (Do not check if a smaller reporting company) | Smaller reporting company R |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 6,182,757 shares of common stock, par value $.01 per share, as of April 30, 2012.

INDEX TO QUARTERLY REPORT

FIRST UNITED CORPORATION

| PART I. FINANCIAL INFORMATION | 3 | ||

| Item 1. | Financial Statements (unaudited) | 3 | |

| Consolidated Statements of Financial Condition – March 31, 2012 and December 31, 2011 | 3 | ||

| Consolidated Statements of Operations - for the three months ended March 31, 2012 and 2011 | 4 | ||

| Consolidated Statements of Comprehensive Income/(Loss) – for the three months ended March 31, 2012 and 2011 | 5 | ||

| Consolidated Statements of Changes in Shareholders’ Equity - for the three months ended March 31, 2012 and year ended December 31, 2011 | 6 | ||

| Consolidated Statements of Cash Flows - for the three months ended March 31, 2012 and 2011 | 7 | ||

| Notes to Consolidated Financial Statements | 8 | ||

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 33 | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 51 | |

| Item 4. | Controls and Procedures | 51 | |

| PART II. OTHER INFORMATION | 52 | ||

| Item 1. | Legal Proceedings | 52 | |

| Item 1A. | Risk Factors | 52 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 52 | |

| Item 3. | Defaults Upon Senior Securities | 52 | |

| Item 4. | Mine Safety Disclosures | 52 | |

| Item 5. | Other Information | 52 | |

| Item 6. | Exhibits | 52 | |

| SIGNATURES | 52 | ||

| EXHIBIT INDEX | 53 | ||

| 2 |

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

FIRST UNITED CORPORATION

Consolidated Statements of Financial Condition

(In thousands, except per share and percentage data)

| March 31, 2012 | December 31, 2011 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Cash and due from banks | $ | 85,597 | $ | 52,049 | ||||

| Interest bearing deposits in banks | 12,528 | 13,058 | ||||||

| Cash and cash equivalents | 98,125 | 65,107 | ||||||

| Investment securities – available-for-sale (at fair value) | 226,147 | 245,023 | ||||||

| Investment securities – held to maturity (at cost) | 4,040 | 0 | ||||||

| Restricted investment in bank stock, at cost | 10,726 | 10,726 | ||||||

| Loans | 914,348 | 938,694 | ||||||

| Allowance for loan losses | (17,213 | ) | (19,480 | ) | ||||

| Net loans | 897,135 | 919,214 | ||||||

| Premises and equipment, net | 30,512 | 30,826 | ||||||

| Goodwill and other intangible assets, net | 11,004 | 14,432 | ||||||

| Bank owned life insurance | 30,641 | 31,435 | ||||||

| Deferred tax assets | 30,113 | 28,711 | ||||||

| Other real estate owned | 19,118 | 16,676 | ||||||

| Accrued interest receivable and other assets | 27,980 | 28,715 | ||||||

| Total Assets | $ | 1,385,541 | $ | 1,390,865 | ||||

| Liabilities and Shareholders’ Equity | ||||||||

| Liabilities: | ||||||||

| Non-interest bearing deposits | $ | 155,580 | $ | 149,888 | ||||

| Interest bearing deposits | 874,325 | 877,896 | ||||||

| Total deposits | 1,029,905 | 1,027,784 | ||||||

| Short-term borrowings | 35,227 | 36,868 | ||||||

| Long-term borrowings | 206,779 | 207,044 | ||||||

| Accrued interest payable and other liabilities | 19,924 | 22,513 | ||||||

| Total Liabilities | 1,291,835 | 1,294,209 | ||||||

| Shareholders’ Equity: | ||||||||

| Preferred stock – no par value; Authorized 2,000 shares of which 30 shares of Series A, $1,000 per share liquidation preference, 5% cumulative increasing to 9% cumulative on February 15, 2014, were issued and outstanding on March 31, 2012 and December 31, 2011 (discount of $124 and $140, respectively) | 29,876 | 29,860 | ||||||

| Common Stock – par value $.01 per share; Authorized 25,000 shares; issued and outstanding 6,183 shares at March 31, 2012 and December 31, 2011 | 62 | 62 | ||||||

| Surplus | 21,513 | 21,500 | ||||||

| Retained earnings | 63,116 | 66,196 | ||||||

| Accumulated other comprehensive loss | (20,861 | ) | (20,962 | ) | ||||

| Total Shareholders’ Equity | 93,706 | 96,656 | ||||||

| Total Liabilities and Shareholders’ Equity | $ | 1,385,541 | $ | 1,390,865 | ||||

See accompanying notes to the consolidated financial statements.

| 3 |

FIRST UNITED CORPORATION

Consolidated Statements of Operations

(In thousands, except per share data)

| Three Months Ended March 31, | ||||||||

| 2012 | 2011 | |||||||

| Interest income | (Unaudited) | |||||||

| Interest and fees on loans | $ | 12,049 | $ | 13,914 | ||||

| Interest on investment securities | ||||||||

| Taxable | 1,105 | 705 | ||||||

| Exempt from federal income tax | 555 | 862 | ||||||

| Total investment income | 1,660 | 1,567 | ||||||

| Other | 59 | 147 | ||||||

| Total interest income | 13,768 | 15,628 | ||||||

| Interest expense | ||||||||

| Interest on deposits | 1,893 | 3,671 | ||||||

| Interest on short-term borrowings | 46 | 61 | ||||||

| Interest on long-term borrowings | 1,946 | 2,426 | ||||||

| Total interest expense | 3,885 | 6,158 | ||||||

| Net interest income | 9,883 | 9,470 | ||||||

| Provision for loan losses | 8,124 | 1,344 | ||||||

| Net interest income after provision for loan losses | 1,759 | 8,126 | ||||||

| Other operating income | ||||||||

| Changes in fair value on impaired securities | 328 | 691 | ||||||

| Portion of gain recognized in other comprehensive income (before taxes) | (328 | ) | (710 | ) | ||||

| Net securities impairment losses recognized in operations | 0 | (19 | ) | |||||

| Net gains – other | 1,326 | 101 | ||||||

| Total net gains | 1,326 | 82 | ||||||

| Service charges | 862 | 866 | ||||||

| Trust department | 1,115 | 1,064 | ||||||

| Insurance commissions | 6 | 623 | ||||||

| Debit card income | 492 | 608 | ||||||

| Bank owned life insurance | 971 | 254 | ||||||

| Other | 606 | 347 | ||||||

| Total other income | 4,052 | 3,762 | ||||||

| Total other operating income | 5,378 | 3,844 | ||||||

| Other operating expenses | ||||||||

| Salaries and employee benefits | 4,889 | 5,132 | ||||||

| FDIC premiums | 465 | 895 | ||||||

| Equipment | 682 | 815 | ||||||

| Occupancy | 710 | 738 | ||||||

| Data processing | 680 | 702 | ||||||

| Other | 2,337 | 2,631 | ||||||

| Total other operating expenses | 9,763 | 10,913 | ||||||

| (Loss)/Income before income tax expense | (2,626 | ) | 1,057 | |||||

| Applicable income tax expense | 39 | 100 | ||||||

| Net (Loss)/Income | (2,665 | ) | 957 | |||||

| Accumulated preferred stock dividends and discount accretion | (415 | ) | (394 | ) | ||||

| Net (Loss) Attributable to/Net Income Available to Common Shareholders | $ | (3,080 | ) | $ | 563 | |||

| Basic net (loss)/income per common share | $ | (.50 | ) | $ | .09 | |||

| Diluted net (loss)/income per common share | $ | (.50 | ) | $ | .09 | |||

| Weighted average number of basic and diluted shares outstanding | 6,183 | 6,166 | ||||||

See accompanying notes to the consolidated financial statements.

| 4 |

FIRST UNITED CORPORATION

Consolidated Statements of Comprehensive Income/(Loss)

(In thousands, except per share data)

| Three Months Ended March 31 | ||||||||

| Components of Comprehensive Income/(Loss) (in thousands) | 2012 | 2011 | ||||||

| Net (Loss)/Income | $ | (2,665 | ) | $ | 957 | |||

| Available for sale (AFS) securities with OTTI: | ||||||||

| Securities with OTTI charges during the period | $ | 328 | $ | 691 | ||||

| Less: OTTI charges recognized in income | 0 | (19 | ) | |||||

| Unrealized gains on investments with OTTI | 328 | 710 | ||||||

| Taxes | (132 | ) | (288 | ) | ||||

| Net unrealized gains on investments with OTTI | 196 | 422 | ||||||

| Available for sale securities – all other: | ||||||||

| Unrealized holding gains during the period | 122 | 1,010 | ||||||

| Less: securities with OTTI charges during the period | 328 | 691 | ||||||

| Unrealized (losses)/gains on all other AFS securities | (206 | ) | 319 | |||||

| Taxes | 84 | (128 | ) | |||||

| Net unrealized (losses)/gains on all other AFS securities | (122 | ) | 191 | |||||

| Net unrealized gains on AFS securities | 74 | 613 | ||||||

| Unrealized gains on cash flow hedges | 46 | 169 | ||||||

| Taxes | (19 | ) | (68 | ) | ||||

| Net unrealized gains on cash flow hedges | 27 | 101 | ||||||

| Other comprehensive income, net of tax | $ | 101 | $ | 714 | ||||

| Comprehensive (loss)/income | $ | (2,564 | ) | $ | 1,671 | |||

See accompanying notes to the consolidated financial statements.

| 5 |

FIRST UNITED CORPORATION

Consolidated Statements of Changes in Shareholders’ Equity

(In thousands, except share and per share data)

| Preferred Stock | Common Stock | Surplus | Retained Earnings | Accumulated Other Comprehensive Loss | Total Shareholders’ Equity | |||||||||||||||||||

| Balance at January 1, 2011 | $ | 29,798 | 62 | 21,422 | 64,179 | (19,821 | ) | 95,640 | ||||||||||||||||

| Net income | 3,626 | 3,626 | ||||||||||||||||||||||

| Other comprehensive loss | (1,141 | ) | (1,141 | ) | ||||||||||||||||||||

| Stock based compensation | 78 | 78 | ||||||||||||||||||||||

| Preferred stock discount accretion | 62 | (62 | ) | 0 | ||||||||||||||||||||

| Preferred stock dividends deferred | (1,547 | ) | (1,547 | ) | ||||||||||||||||||||

| Balance at December 31, 2011 | 29,860 | 62 | 21,500 | 66,196 | (20,962 | ) | 96,656 | |||||||||||||||||

| Net loss | (2,665 | ) | (2,665 | ) | ||||||||||||||||||||

| Other comprehensive income | 101 | 101 | ||||||||||||||||||||||

| Stock based compensation | 13 | 13 | ||||||||||||||||||||||

| Preferred stock discount accretion | 16 | (16 | ) | 0 | ||||||||||||||||||||

| Preferred stock dividends deferred | (399 | ) | (399 | ) | ||||||||||||||||||||

| Balance at March 31, 2012 | $ | 29,876 | $ | 62 | $ | 21,513 | $ | 63,116 | $ | (20,861 | ) | $ | 93,706 | |||||||||||

See accompanying notes to the consolidated financial statements.

| 6 |

FIRST UNITED CORPORATION

Consolidated Statements of Cash Flows

(In thousands)

| Three Months Ended March 31, | ||||||||

| 2012 | 2011 | |||||||

| Operating activities | (Unaudited) | |||||||

| Net (loss)/income | $ | (2,665 | ) | $ | 957 | |||

| Adjustments to reconcile net (loss)/income to net cash provided by operating activities: | ||||||||

| Provision for loan losses | 8,124 | 1,344 | ||||||

| Depreciation | 515 | 640 | ||||||

| Stock compensation | 13 | 32 | ||||||

| Amortization of intangible assets | 0 | 67 | ||||||

| Gain on sales of Insurance assets | (88 | ) | 0 | |||||

| (Gain)/loss on sales of other real estate owned | (623 | ) | 7 | |||||

| Write-downs of other real estate owned | 0 | 63 | ||||||

| Gain on loan sales | (20 | ) | (19 | ) | ||||

| Loss on disposal of fixed assets | 4 | 3 | ||||||

| Net amortization of investment securities discounts and premiums | 375 | 610 | ||||||

| Other-than-temporary-impairment loss on securities | 0 | 19 | ||||||

| Gain on sales of investment securities – available-for-sale | (599 | ) | (155 | ) | ||||

| Amortization of deferred Loan Fees | (127 | ) | (139 | ) | ||||

| Decrease in accrued interest receivable and other assets | 781 | 2,090 | ||||||

| Deferred tax benefit | (1,469 | ) | (1,313 | ) | ||||

| Decrease in accrued interest payable and other liabilities | (3,076 | ) | (1,126 | ) | ||||

| Earnings on bank owned life insurance | (971 | ) | (254 | ) | ||||

| Net cash provided by operating activities | 174 | 2,826 | ||||||

| Investing activities | ||||||||

| Proceeds from maturities/calls of investment securities available-for-sale | 8,414 | 20,230 | ||||||

| Proceeds from sales of investment securities available-for-sale | 10,454 | 22,048 | ||||||

| Purchases of investment securities available-for-sale | (3,686 | ) | (37,765 | ) | ||||

| Proceeds from sales of other real estate owned | 2,708 | 532 | ||||||

| Proceeds from loan sales | 1,462 | 0 | ||||||

| Proceeds from disposal of fixed assets | 19 | 0 | ||||||

| Proceeds from sale of insurance assets | 3,604 | 0 | ||||||

| Proceeds from BOLI death benefit | 1,765 | 0 | ||||||

| Net decrease in loans | 8,113 | 26,715 | ||||||

| Purchases of premises and equipment | (224 | ) | (65 | ) | ||||

| Net cash provided by investing activities | 32,629 | 31,695 | ||||||

| Financing activities | ||||||||

| Net increase/(decrease) in deposits | 2,121 | (174,066 | ) | |||||

| Net (decrease)/increase in short-term borrowings | (1,641 | ) | 3,859 | |||||

| Proceeds from long-term borrowings | 20,000 | 0 | ||||||

| Payments on long-term borrowings | (20,265 | ) | (10,264 | ) | ||||

| Net cash provided by/(used in) financing activities | 215 | (180,471 | ) | |||||

| Increase/(decrease) in cash and cash equivalents | 33,018 | (145,950 | ) | |||||

| Cash and cash equivalents at beginning of the year | 65,107 | 299,313 | ||||||

| Cash and cash equivalents at end of period | $ | 98,125 | $ | 153,363 | ||||

| Supplemental information | ||||||||

| Interest paid | $ | 3,553 | $ | 5,283 | ||||

| Non-cash investing activities: | ||||||||

| Transfers from loans to other real estate owned | $ | 4,527 | $ | 562 | ||||

| Transfers from loans to loans held for sale | $ | 0 | $ | 44,502 | ||||

| Transfers from securities available for sale to held-to-maturity | $ | 4,040 | $ | 0 | ||||

See accompanying notes to the consolidated financial statements.

| 7 |

FIRST UNITED CORPORATION

NoteS to Consolidated Financial Statements (UNAUDITED)

for the quarter ended March 31, 2012

Note 1 – Basis of Presentation

The accompanying unaudited consolidated financial statements of First United Corporation and its consolidated subsidiaries, including First United Bank & Trust (the “Bank”), have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) for interim financial information, as required by the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 270, Interim Reporting, and with the instructions to Form 10-Q and Rule 8-03 of Regulation S-X. Accordingly, they do not include all the information and footnotes required for annual financial statements. In the opinion of management, all adjustments considered necessary for a fair presentation, consisting of normal recurring items, have been included. Operating results for the three month period ended March 31, 2012 are not necessarily indicative of the results that may be expected for the full year or for any future interim period. These consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in First United Corporation’s Annual Report on Form 10-K for the year ended December 31, 2011. For purposes of comparability, certain prior period amounts have been reclassified to conform to the 2012 presentation. Such reclassifications had no impact on net income/(loss) or equity.

First United Corporation has evaluated events and transactions occurring subsequent to the statement of financial condition date of March 31, 2012 for items that should potentially be recognized or disclosed in these financial statements as prescribed by ASC Topic 855, Subsequent Events.

As used in these notes to consolidated financial statements, First United Corporation and its consolidated subsidiaries are sometimes collectively referred to as the “Corporation”.

Note 2 – Earnings/(loss) Per Common Share

Basic earnings/(loss) per common share is derived by dividing net income available to/(loss) attributable to common shareholders by the weighted-average number of common shares outstanding during the period and does not include the effect of any potentially dilutive common stock equivalents. Diluted earnings/(loss) per share is derived by dividing net income available to/(loss) attributable to common shareholders by the weighted-average number of shares outstanding, adjusted for the dilutive effect of outstanding common stock equivalents. There were no common stock equivalents during the quarters ended March 31, 2012 and March 31, 2011. There is no dilutive effect on the earnings per share during loss periods.

The following table sets forth the calculation of basic and diluted earnings/(loss) per common share for the three month periods ended March 31, 2012 and 2011:

| For the three months ended March 31, | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| (in thousands, except for per share amount) | Loss | Average Shares | Per Share Amount | Income | Average Shares | Per Share Amount | ||||||||||||||||||

| Basic and Diluted (Loss)/Earnings Per Share: | ||||||||||||||||||||||||

| Net (loss)/income | $ | (2,665 | ) | $ | 957 | |||||||||||||||||||

| Preferred stock dividends deferred | (399 | ) | (379 | ) | ||||||||||||||||||||

| Discount accretion on preferred stock | (16 | ) | (15 | ) | ||||||||||||||||||||

| Net (loss) attributable to/income available to common shareholders | $ | (3,080 | ) | 6,183 | $ | (.50 | ) | $ | 563 | 6,166 | $ | .09 | ||||||||||||

| 8 |

Note 3 – Net Gains

The following table summarizes the gain/(loss) activity for the three-month periods ended March 31, 2012 and 2011:

| Three months ended March 31, | ||||||||

| (in thousands) | 2012 | 2011 | ||||||

| Other-than-temporary impairment charges: | ||||||||

| Available-for-sale securities | $ | 0 | $ | (19 | ) | |||

| Net gains/(losses) – other: | ||||||||

| Available-for-sale securities: | ||||||||

| Realized gains | 663 | 237 | ||||||

| Realized losses | (64 | ) | (82 | ) | ||||

| Gain/(loss) on sales of other real estate owned | 623 | (7 | ) | |||||

| Write-down of other real estate owned | 0 | (63 | ) | |||||

| Gain on sale of consumer loans | 20 | 19 | ||||||

| Gain on sale of insurance assets | 88 | 0 | ||||||

| Loss on disposal of fixed assets | (4 | ) | (3 | ) | ||||

| Net gains – other | 1,326 | 101 | ||||||

| Net gains | $ | 1,326 | $ | 82 | ||||

Note 4 – Cash and Cash Equivalents

Cash and due from banks, which represents vault cash in the retail offices and invested cash balances at the Federal Reserve, is carried at fair value.

| March 31, 2012 | December 31, 2011 | |||||||

| Cash and due from banks, weighted average interest rate of 0.15% (at March 31, 2012) | $ | 85,597 | $ | 52,049 | ||||

Interest bearing deposits in banks, which represent funds invested at a correspondent bank, are carried at fair value and, as of March 31, 2012 and December 31, 2011, consisted of daily funds invested at the Federal Home Loan Bank (“FHLB”) of Atlanta, First Tennessee Bank (“FTN”), Merchants and Traders (“M&T”) and Community Bankers Bank (“CBB”).

| March 31, 2012 | December 31, 2011 | |||||||

| FHLB daily investments, interest rate of 0.005% (at March 31, 2012) | $ | 4,067 | $ | 4,244 | ||||

| FTN daily investments, interest rate of 0.09% (at March 31, 2012) | 1,350 | 1,350 | ||||||

| M&T Fed Funds sold, interest rate of 0.25% (at March 31, 2012) | 6,026 | 6,379 | ||||||

| CBB Fed Funds sold, interest rate of 0.22% (at March 31, 2012) | 1,085 | 1,085 | ||||||

| $ | 12,528 | $ | 13,058 | |||||

| 9 |

Note 5 – Investments

The investment portfolio is classified and accounted for based on the guidance of ASC Topic 320, Investments – Debt and Equity Securities.

The following table shows a comparison of amortized cost and fair values of investment securities at March 31, 2012 and December 31, 2011:

| (in thousands) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | OTTI in AOCI | |||||||||||||||

| March 31, 2012 | ||||||||||||||||||||

| Available for Sale: | ||||||||||||||||||||

| U.S. government agencies | 25,492 | 70 | 68 | 25,494 | 0 | |||||||||||||||

| Residential mortgage-backed agencies | 121,177 | 1,870 | 145 | 122,902 | 0 | |||||||||||||||

| Collateralized mortgage obligations | 10,815 | 0 | 54 | 10,761 | 0 | |||||||||||||||

| Obligations of states and political subdivisions | 54,229 | 2,998 | 191 | 57,036 | 0 | |||||||||||||||

| Collateralized debt obligations | 36,450 | 0 | 26,496 | 9,954 | 17,399 | |||||||||||||||

| Total available for sale | $ | 248,163 | $ | 4,938 | $ | 26,954 | $ | 226,147 | $ | 17,399 | ||||||||||

| Held to Maturity: | ||||||||||||||||||||

| Obligations of states and political subdivisions | $ | 4,040 | $ | 0 | $ | 0 | $ | 4,040 | $ | 0 | ||||||||||

| December 31, 2011 | ||||||||||||||||||||

| U.S. government agencies | $ | 25,490 | $ | 107 | $ | 17 | $ | 25,580 | $ | 0 | ||||||||||

| Residential mortgage-backed agencies | 129,019 | 1,653 | 270 | 130,402 | 0 | |||||||||||||||

| Collateralized mortgage obligations | 10,843 | 58 | 123 | 10,778 | 0 | |||||||||||||||

| Obligations of states and political subdivisions | 65,424 | 3,400 | 8 | 68,816 | 0 | |||||||||||||||

| Collateralized debt obligations | 36,385 | 0 | 26,938 | 9,447 | 17,726 | |||||||||||||||

| Totals | $ | 267,161 | $ | 5,218 | $ | 27,356 | $ | 245,023 | $ | 17,726 | ||||||||||

Proceeds from sales and calls of securities and the realized gains and losses are as follows:

| Three Months Ended March 31, | ||||||||

| (in thousands) | 2012 | 2011 | ||||||

| Proceeds | $ | 10,454 | $ | 22,048 | ||||

| Realized gains | 663 | 237 | ||||||

| Realized losses | 64 | 82 | ||||||

The following table shows the Corporation’s securities with gross unrealized losses and fair values at March 31, 2012 and December 31, 2011, aggregated by investment category and length of time that individual securities have been in a continuous unrealized loss position:

| Less than 12 months | 12 months or more | |||||||||||||||

| (in thousands) | Fair Value | Unrealized Losses | Fair Value | Unrealized Losses | ||||||||||||

| March 31, 2012 | ||||||||||||||||

| U.S. government agencies | 18,732 | 68 | 0 | 0 | ||||||||||||

| Residential mortgage-backed agencies | 23,222 | 145 | 0 | 0 | ||||||||||||

| Collateralized mortgage obligations | 10,152 | 6 | 610 | 48 | ||||||||||||

| Obligations of states and political subdivisions | 3,523 | 191 | 0 | 0 | ||||||||||||

| Collateralized debt obligations | 0 | 0 | 9,954 | 26,496 | ||||||||||||

| Totals | $ | 55,629 | $ | 410 | $ | 10,564 | $ | 26,544 | ||||||||

| 10 |

| December 31, 2011 | ||||||||||||||||

| U.S. government agencies | $ | 9,983 | $ | 17 | $ | 0 | $ | 0 | ||||||||

| Residential mortgage-backed agencies | 47,200 | 269 | 4,779 | 1 | ||||||||||||

| Collateralized mortgage obligations | 0 | 0 | 557 | 123 | ||||||||||||

| Obligations of states and political subdivisions | 0 | 0 | 2,805 | 8 | ||||||||||||

| Collateralized debt obligations | 0 | 0 | 9,447 | 26,938 | ||||||||||||

| Totals | $ | 57,183 | $ | 286 | $ | 17,588 | $ | 27,070 |

Management systematically evaluates securities for impairment on a quarterly basis. Management assesses whether (a) it has the intent to sell a security being evaluated and (b) it is more likely than not that the Corporation will be required to sell the security prior to its anticipated recovery. If neither applies, then declines in the fair values of securities below their cost that are considered other-than-temporary declines are split into two components. The first is the loss attributable to declining credit quality. Credit losses are recognized in earnings as realized losses in the period in which the impairment determination is made. The second component consists of all other losses, which are recognized in other comprehensive loss. In estimating other-than-temporary impairment (“OTTI”) losses, management considers (1) the length of time and the extent to which the fair value has been less than cost, (2) adverse conditions specifically related to the security, an industry, or a geographic area, (3) the historic and implied volatility of the fair value of the security, (4) changes in the rating of the security by a rating agency, (5) recoveries or additional declines in fair value subsequent to the balance sheet date, (6) failure of the issuer of the security to make scheduled interest or principal payments, and (7) the payment structure of the debt security and the likelihood of the issuer being able to make payments that increase in the future. Management also monitors cash flow projections for securities that are considered beneficial interests under the guidance of ASC Subtopic 325-40, Investments – Other – Beneficial Interests in Securitized Financial Assets, (ASC Section 325-40-35). Further discussion about the evaluation of securities for impairment can be found in Item 2 of Part I of this report under the heading “Investment Securities”.

Management believes that the valuation of certain securities is a critical accounting policy that requires significant estimates in preparation of its consolidated financial statements. Management utilizes an independent third party to prepare both the impairment valuations and fair value determinations for its collateralized debt obligation (“CDO”) portfolio consisting of pooled trust preferred securities. Based on management’s review of the assumptions and results of the third-party review, it does not believe that there were any material differences in the valuations between March 31, 2012 and December 31, 2011.

U.S. Government Agencies - Two U.S. government agencies have been in a slight unrealized loss position for less than 12 months as of March 31, 2012. The securities are of the highest investment grade and the Corporation does not intend to sell them, and it is not more likely than not that the Corporation will be required to sell them before recovery of their amortized cost basis, which may be at maturity. Therefore, no OTTI exists at March 31, 2012.

Residential Mortgage-Backed Agencies - Five residential mortgage-backed agencies have been in a slight unrealized loss position for less than 12 months as of March 31, 2012. There were no residential mortgage-backed agency securities in an unrealized loss position for 12 months or more. The securities are of the highest investment grade and the Corporation does not intend to sell it, and it is not more likely than not that the Corporation will be required to sell it before recovery of their amortized cost basis, which may be at maturity. Therefore, no OTTI exists at March 31, 2012.

Collateralized Mortgage Obligations – The collateralized mortgage obligation portfolio consisted of one security at March 31, 2012 that has been in an unrealized loss position for less than 12 months and one security that has been in an unrealized loss position for 12 months or more. The security with an unrealized loss of greater than 12 months is a private label residential mortgage-backed security and is reviewed for factors such as loan to value ratio, credit support levels, borrower FICO scores, geographic concentration, prepayment speeds, delinquencies, coverage ratios and credit ratings. Management believes that this security continues to demonstrate collateral coverage ratios that are adequate to support the Corporation’s investment. At the time of purchase, this security was of the highest investment grade and was purchased at a discount relative to its face amount. As of March 31, 2012, this security remains at investment grade and continues to perform as expected at the time of purchase. The Corporation does not intend to sell this security and it is not more likely than not that the Corporation will be required to sell the investment before recovery of its amortized cost basis, which may be at maturity. Accordingly, management does not consider this investment to be other-than-temporarily impaired at March 31, 2012.

| 11 |

Obligations of State and Political Subdivisions – The unrealized losses on the Corporation’s investments in state and political subdivisions were $191,000 at March 31, 2012. One security has been in an unrealized loss position for less than 12 months. There are no securities that have been in an unrealized loss position for 12 months or more. All of these investments are of investment grade as determined by the major rating agencies and management reviews the ratings of the underlying issuers. Management believes that this portfolio is well-diversified throughout the United States, and all bonds continue to perform according to their contractual terms. The Corporation does not intend to sell these investments and it is not more likely than not that the Corporation will be required to sell the investments before recovery of their amortized cost basis, which may be at maturity. Accordingly, management does not consider these investments to be other-than-temporarily impaired at March 31, 2012.

Collateralized Debt Obligations - The $26.5 million in unrealized losses greater than 12 months at March 31, 2012 relates to 18 pooled trust preferred securities that comprise the CDO portfolio. See Note 8 for a discussion of the methodology used by management to determine the fair values of these securities. Based upon a review of credit quality and the cash flow tests performed by the independent third party, management determined that there were no securities that had credit-related non-cash OTTI charges during the first quarter of 2012. The unrealized losses on the remaining securities in the portfolio are primarily attributable to continued depression in market interest rates, marketability, liquidity and the current economic environment.

The following tables present a cumulative roll-forward of the amount of non-cash OTTI charges related to credit losses which have been recognized in earnings for the trust preferred securities in the CDO portfolio held and not intended to be sold for the three-month periods ended March 31, 2012 and 2011:

| Three months ended | ||||||||

| (in thousands) | March 31, 2012 | March 31, 2011 | ||||||

| Balance of credit-related OTTI at January 1 | $ | 14,424 | $ | 14,653 | ||||

| Additions for credit-related OTTI not previously recognized | 0 | 0 | ||||||

| Additional increases for credit-related OTTI previously recognized when there is no intent to sell and no requirement to sell before recovery of amortized cost basis | 0 | 19 | ||||||

| Decreases for previously recognized credit-related OTTI because there was an intent to sell | 0 | 0 | ||||||

| Reduction for increases in cash flows expected to be collected | (112 | ) | (55 | ) | ||||

| Balance of credit-related OTTI at March 31 | $ | 14,312 | $ | 14,617 | ||||

The amortized cost and estimated fair value of securities by contractual maturity at March 31, 2012 and December 31, 2011 are shown in the following table. Actual maturities will differ from contractual maturities because the issuers of the securities may have the right to call or prepay obligations with or without call or prepayment penalties.

| March 31, 2012 | December 31, 2011 | |||||||||||||||

| (in thousands) | Amortized Cost | Fair Value | Amortized Cost | Fair Value | ||||||||||||

| Contractual Maturity | ||||||||||||||||

| Available for sale: | ||||||||||||||||

| Due in one year or less | $ | 1,700 | $ | 1,707 | $ | 1,700 | $ | 1,716 | ||||||||

| Due after one year through five years | 23,792 | 23,787 | 0 | 0 | ||||||||||||

| Due after five years through ten years | 20,160 | 21,249 | 42,119 | 42,820 | ||||||||||||

| Due after ten years | 70,519 | 45,741 | 83,480 | 59,307 | ||||||||||||

| 116,171 | 92,484 | 127,299 | 103,843 | |||||||||||||

| Residential mortgage-backed agencies | 121,177 | 122,902 | 129,019 | 130,402 | ||||||||||||

| Collateralized mortgage obligations | 10,815 | 10,761 | 10,843 | 10,778 | ||||||||||||

| $ | 248,163 | $ | 226,147 | $ | 267,161 | $ | 245,023 | |||||||||

| Held to Maturity: | ||||||||||||||||

| Due after ten years | $ | 4,040 | $ | 4,040 | $ | 0 | $ | 0 | ||||||||

| 12 |

Note 6 - Restricted Investment in Bank Stock

Restricted stock, which represents required investments in the common stock of the FHLB of Atlanta, Atlantic Central Bankers Bank (“ACBB”) and CBB, is carried at cost and is considered a long-term investment.

Management evaluates the restricted stock for impairment in accordance with ASC Industry Topic 942, Financial Services – Depository and Lending, (ASC Section 942-325-35). Management’s evaluation of potential impairment is based on management’s assessment of the ultimate recoverability of the cost of the restricted stock rather than by recognizing temporary declines in value. The determination of whether a decline affects the ultimate recoverability is influenced by criteria such as (a) the significance of the decline in net assets of the issuing bank as compared to the capital stock amount for that bank and the length of time this situation has persisted, (b) commitments by the issuing bank to make payments required by law or regulation and the level of such payments in relation to the operating performance of that bank, and (c) the impact of legislative and regulatory changes on institutions and, accordingly, on the customer base of the issuing bank. Management has evaluated the restricted stock for impairment and believes that no impairment charge is necessary as of March 31, 2012.

The Corporation recognizes dividends on a cash basis. For the three months ended March 31, 2012, dividends of $34,008 were recognized in earnings. For the comparable period of 2011, dividends of $25,040 were recognized in earnings.

Note 7 – Loans and Related Allowance for Loan Losses

The following table summarizes the primary segments of the loan portfolio as of March 31, 2012 and December 31, 2011:

| (in thousands) | Commercial Real Estate | Acquisition and Development | Commercial and Industrial | Residential Mortgage | Consumer | Total | ||||||||||||||||||

| March 31, 2012 | ||||||||||||||||||||||||

| Total loans | $ | 331,188 | $ | 141,876 | $ | 67,601 | $ | 343,399 | $ | 30,284 | $ | 914,348 | ||||||||||||

| Individually evaluated for impairment | $ | 17,128 | $ | 25,473 | $ | 3,979 | $ | 5,983 | $ | 77 | $ | 52,640 | ||||||||||||

| Collectively evaluated for impairment | $ | 314,060 | $ | 116,403 | $ | 63,622 | $ | 337,416 | $ | 30,207 | $ | 861,708 | ||||||||||||

| December 31, 2011 | ||||||||||||||||||||||||

| Total loans | $ | 336,234 | $ | 142,871 | $ | 78,697 | $ | 347,220 | $ | 33,672 | $ | 938,694 | ||||||||||||

| Individually evaluated for impairment | $ | 16,942 | $ | 25,699 | $ | 13,048 | $ | 6,116 | $ | 21 | $ | 61,826 | ||||||||||||

| Collectively evaluated for impairment | $ | 319,292 | $ | 117,172 | $ | 65,649 | $ | 341,104 | $ | 33,651 | $ | 876,868 | ||||||||||||

The segments of the Bank’s loan portfolio are disaggregated to a level that allows management to monitor risk and performance. The commercial real estate (“CRE”) loan segment is then segregated into two classes. Non-owner occupied CRE loans, which include loans secured by non-owner occupied, nonfarm, nonresidential properties, generally have a greater risk profile than all other CRE loans, which include loans secured by farmland, multifamily structures and owner-occupied commercial structures. The acquisition and development (“A&D”) loan segment is segregated into two classes. One-to-four family residential construction loans are generally made to individuals for the acquisition of and/or construction on a lot or lots on which a residential dwelling is to be built. All other A&D loans are generally made to developers or investors for the purpose of acquiring, developing and constructing residential or commercial structures. These loans have a higher risk profile because the ultimate buyer, once development is completed, is generally not known at the time of the A&D loan. The commercial and industrial (“C&I”) loan segment consists of loans made for the purpose of financing the activities of commercial customers. The residential mortgage loan segment is segregated into two classes: (a) amortizing term loans, which are primarily first liens; and (b) home equity lines of credit, which are generally second liens. The consumer loan segment consists primarily of installment loans (direct and indirect) and overdraft lines of credit connected with customer deposit accounts.

Management uses a 10-point internal risk rating system to monitor the credit quality of the overall loan portfolio. The first six categories are considered not criticized, and are aggregated as “Pass” rated. The criticized rating categories utilized by management generally follow bank regulatory definitions. The Special Mention category includes assets that are currently protected but are potentially weak, resulting in an undue and unwarranted credit risk, but not to the point of justifying a Substandard classification. Loans in the Substandard category have well-defined weaknesses that jeopardize the liquidation of the debt, and have a distinct possibility that some loss will be sustained if the weaknesses are not corrected. All loans greater than 90 days past due are considered Substandard. The portion of a specific allocation of the allowance for loan losses that management believes is associated with a pending event that could trigger loss in the short-term will be classified in the Doubtful category. Any portion of a loan that has been charged off is placed in the Loss category.

| 13 |

To help ensure that risk ratings are accurate and reflect the present and future capacity of borrowers to repay a loan as agreed, the Bank has a structured loan rating process with several layers of internal and external oversight. Generally, consumer and residential mortgage loans are included in the Pass categories unless a specific action, such as bankruptcy, repossession, or death occurs to raise awareness of a possible credit event. The Bank’s Commercial Loan Officers are responsible for the timely and accurate risk rating of the loans in the commercial segments at origination and on an ongoing basis. The Bank’s experienced Credit Quality and Loan Review Department performs an annual review of all commercial relationships $500,000 or greater. Confirmation of the appropriate risk grade is included as part of the review process on an ongoing basis. The Credit Quality and Loan Review Department continually reviews and assesses loans within the portfolio. In addition, the Bank engages an external consultant to conduct loan reviews on at least an annual basis. Generally, the external consultant reviews commercial relationships greater than $750,000 and/or criticized relationships greater than $500,000. Detailed reviews, including plans for resolution, are performed on loans classified as Substandard on a quarterly basis. Loans in the Special Mention and Substandard categories that are collectively evaluated for impairment are given separate consideration in the determination of the allowance.

The following table presents the classes of the loan portfolio summarized by the aggregate Pass and the criticized categories of Special Mention, Substandard and Doubtful within the internal risk rating system as of March 31, 2012 and December 31, 2011:

| (in thousands) | Pass | Special Mention | Substandard | Doubtful | Total | |||||||||||||||

| March 31, 2012 | ||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||

| Non owner-occupied | $ | 123,246 | $ | 5,212 | $ | 26,476 | $ | 0 | $ | 154,934 | ||||||||||

| All other CRE | 118,687 | 17,424 | 40,143 | 0 | 176,254 | |||||||||||||||

| Acquisition and development | ||||||||||||||||||||

| 1-4 family residential construction | 11,444 | 1,560 | 5,404 | 0 | 18,408 | |||||||||||||||

| All other A&D | 79,627 | 932 | 42,909 | 0 | 123,468 | |||||||||||||||

| Commercial and industrial | 60,257 | 648 | 6,696 | 0 | 67,601 | |||||||||||||||

| Residential mortgage | ||||||||||||||||||||

| Residential mortgage - term | 248,420 | 2,462 | 13,701 | 0 | 264,583 | |||||||||||||||

| Residential mortgage – home equity | 75,991 | 794 | 2,031 | 0 | 78,816 | |||||||||||||||

| Consumer | 29,844 | 29 | 411 | 0 | 30,284 | |||||||||||||||

| Total | $ | 747,516 | $ | 29,061 | $ | 137,771 | $ | 0 | $ | 914,348 | ||||||||||

| December 31, 2011 | ||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||

| Non owner-occupied | $ | 119,574 | $ | 4,222 | $ | 32,212 | $ | 0 | $ | 156,008 | ||||||||||

| All other CRE | 123,713 | 18,307 | 38,206 | 0 | 180,226 | |||||||||||||||

| Acquisition and development | ||||||||||||||||||||

| 1-4 family residential construction | 11,512 | 0 | 5,572 | 0 | 17,084 | |||||||||||||||

| All other A&D | 81,268 | 935 | 43,584 | 0 | 125,787 | |||||||||||||||

| Commercial and industrial | 62,152 | 697 | 15,848 | 0 | 78,697 | |||||||||||||||

| Residential mortgage | ||||||||||||||||||||

| Residential mortgage - term | 250,701 | 1,817 | 15,408 | 0 | 267,926 | |||||||||||||||

| Residential mortgage – home equity | 75,517 | 34 | 3,743 | 0 | 79,294 | |||||||||||||||

| Consumer | 33,147 | 34 | 491 | 0 | 33,672 | |||||||||||||||

| Total | $ | 757,584 | $ | 26,046 | $ | 155,064 | $ | 0 | $ | 938,694 | ||||||||||

Management further monitors the performance and credit quality of the loan portfolio by analyzing the age of the portfolio as determined by the length of time a recorded payment is past due. A loan is considered to be past due when a payment has not been received for 30 days past its contractual due date. For all loan segments, the accrual of interest is discontinued when principal or interest is delinquent for 90 days or more unless the loan is well-secured and in the process of collection. All non-accrual loans are considered to be impaired. Interest payments received on non-accrual loans are applied as a reduction of the loan principal balance. Loans are returned to accrual status when all principal and interest amounts contractually due are brought current and future payments are reasonably assured. The Corporation’s policy for recognizing interest income on impaired loans does not differ from its overall policy for interest recognition.

The following table presents the classes of the loan portfolio summarized by the aging categories of performing loans and non-accrual loans as of March 31, 2012 and December 31, 2011:

| 14 |

| (in thousands) | Current | 30-59 Days Past Due | 60-89 Days Past Due | 90 Days+ Past Due | Total Past Due and still accruing | Non-Accrual | Total Loans | |||||||||||||||||||||

| March 31, 2012 | ||||||||||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||||||||||

| Non owner-occupied | $ | 145,136 | $ | 1,796 | $ | 64 | $ | 0 | $ | 1,860 | $ | 7,938 | $ | 154,934 | ||||||||||||||

| All other CRE | 173,841 | 0 | 533 | 0 | 533 | 1,880 | 176,254 | |||||||||||||||||||||

| Acquisition and development | ||||||||||||||||||||||||||||

| 1-4 family residential construction | 18,338 | 70 | 0 | 0 | 70 | 0 | 18,408 | |||||||||||||||||||||

| All other A&D | 106,528 | 1,262 | 363 | 204 | 1,829 | 15,111 | 123,468 | |||||||||||||||||||||

| Commercial and industrial | 67,109 | 168 | 4 | 0 | 172 | 320 | 67,601 | |||||||||||||||||||||

| Residential mortgage | ||||||||||||||||||||||||||||

| Residential mortgage - term | 252,332 | 9,107 | 345 | 303 | 9,755 | 2,496 | 264,583 | |||||||||||||||||||||

| Residential mortgage – home equity | 77,379 | 507 | 148 | 0 | 655 | 782 | 78,816 | |||||||||||||||||||||

| Consumer | 28,900 | 1,089 | 177 | 41 | 1,307 | 77 | 30,284 | |||||||||||||||||||||

| Total | $ | 869,563 | $ | 13,999 | $ | 1,634 | $ | 548 | $ | 16,181 | $ | 28,604 | $ | 914,348 | ||||||||||||||

| December 31, 2011 | ||||||||||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||||||||||

| Non owner-occupied | $ | 146,150 | $ | 359 | $ | 209 | $ | 0 | $ | 568 | $ | 9,290 | $ | 156,008 | ||||||||||||||

| All other CRE | 173,342 | 558 | 5,547 | 0 | 6,105 | 779 | 180,226 | |||||||||||||||||||||

| Acquisition and development | ||||||||||||||||||||||||||||

| 1-4 family residential construction | 17,009 | 0 | 75 | 0 | 75 | 0 | 17,084 | |||||||||||||||||||||

| All other A&D | 109,351 | 840 | 530 | 128 | 1,498 | 14,938 | 125,787 | |||||||||||||||||||||

| Commercial and industrial | 69,119 | 182 | 32 | 0 | 214 | 9,364 | 78,697 | |||||||||||||||||||||

| Residential mortgage | ||||||||||||||||||||||||||||

| Residential mortgage - term | 249,719 | 10,106 | 3,753 | 1,386 | 15,245 | 2,962 | 267,926 | |||||||||||||||||||||

| Residential mortgage – home equity | 77,486 | 476 | 375 | 123 | 974 | 834 | 79,294 | |||||||||||||||||||||

| Consumer | 31,478 | 1,560 | 471 | 142 | 2,173 | 21 | 33,672 | |||||||||||||||||||||

| Total | $ | 873,654 | $ | 14,081 | $ | 10,992 | $ | 1,779 | $ | 26,852 | $ | 38,188 | $ | 938,694 | ||||||||||||||

Non-accrual loans which have been subject to a partial charge-off totaled $9.7 million as of March 31, 2012, compared to $13.4 million as of December 31, 2011.

An allowance for loan losses (“ALL”) is maintained to absorb losses from the loan portfolio. The ALL is based on management’s continuing evaluation of the risk characteristics and credit quality of the loan portfolio, assessment of current economic conditions, diversification and size of the portfolio, adequacy of collateral, past and anticipated loss experience, and the amount of non-performing loans.

The Bank’s methodology for determining the ALL is based on the requirements of ASC Section 310-10-35, Receivables-Overall-Subsequent Measurement, for loans individually evaluated for impairment and ASC Subtopic 450-20, Contingencies-Loss Contingencies, for loans collectively evaluated for impairment, as well as the Interagency Policy Statement on the Allowance for Loan and Lease Losses and other bank regulatory guidance. The total of the two components represents the Bank’s ALL.

| 15 |

The following table summarizes the primary segments of the ALL, segregated by the amount required for loans individually evaluated for impairment and the amount required for loans collectively evaluated for impairment as of March 31, 2012 and December 31, 2011.

| (In thousands) | Commercial Real Estate | Acquisition and Development | Commercial and Industrial | Residential Mortgage | Consumer | Total | ||||||||||||||||||

| March 31, 2012 | ||||||||||||||||||||||||

| Total ALL | $ | 6,635 | $ | 5,879 | $ | 929 | $ | 3,377 | $ | 393 | $ | 17,213 | ||||||||||||

| Individually evaluated for impairment | $ | 901 | $ | 1,156 | $ | 0 | $ | 20 | $ | 0 | $ | 2,077 | ||||||||||||

| Collectively evaluated for impairment | $ | 5,734 | $ | 4,723 | $ | 929 | $ | 3,357 | $ | 393 | $ | 15,136 | ||||||||||||

| December 31, 2011 | ||||||||||||||||||||||||

| Total ALL | $ | 6,218 | $ | 7,190 | $ | 2,190 | $ | 3,430 | $ | 452 | $ | 19,480 | ||||||||||||

| Individually evaluated for impairment | $ | 92 | $ | 2,718 | $ | 1,139 | $ | 2 | $ | 0 | $ | 3,951 | ||||||||||||

| Collectively evaluated for impairment | $ | 6,126 | $ | 4,472 | $ | 1,051 | $ | 3,428 | $ | 452 | $ | 15,529 | ||||||||||||

Management evaluates individual loans in all of the commercial segments for possible impairment, if the loan is greater than $500,000 or is part of a relationship that is greater than $750,000 and is either (a) in nonaccrual status or (b) risk-rated Substandard and greater than 60 days past due. Loans are considered to be impaired when, based on current information and events, it is probable that the Bank will be unable to collect the scheduled payments of principal or interest when due according to the contractual terms of the loan agreement. Factors considered by management in evaluating impairment include payment status, collateral value, and the probability of collecting scheduled principal and interest payments when due. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, including the length of the delay, the reasons for the delay, the borrower’s prior payment record, and the amount of the shortfall in relation to the principal and interest owed. The Bank does not separately evaluate individual consumer and residential mortgage loans for impairment, unless such loans are part of larger relationship that is impaired; otherwise loans in these segments are considered impaired when they are classified as non-accrual.

Once the determination has been made that a loan is impaired, the determination of whether a specific allocation of the allowance is necessary is measured by comparing the recorded investment in the loan to the fair value of the loan using one of three methods: (a) the present value of expected future cash flows discounted at the loan’s effective interest rate; (b) the loan’s observable market price; or (c) the fair value of the collateral less selling costs. The method is selected on a loan-by-loan basis, with management primarily utilizing the fair value of collateral method. If the fair value of the collateral less selling costs method is utilized for collateral securing loans in the commercial segments, then an updated external appraisal is ordered on the collateral supporting the loan if the loan balance is greater than $500,000 and the existing appraisal is greater than 18 months old. If an appraisal is less than 12 months old (the age at which the internal appraisal grid begins) and if management believes that general market conditions in that geographic market have changed considerably, the property has deteriorated or perhaps lost an income stream, or a recent appraisal for a similar property indicates a significant change, then management may adjust the fair value indicated by the existing appraisal until a new appraisal is obtained. If the most recent appraisal is greater than 12 months old or if an updated appraisal has not been received and reviewed in time for the determination of estimated fair value at quarter (or year) end, then the estimated fair value of the collateral is determined by adjusting the existing appraisal by the appropriate percentage from an internally prepared appraisal discount grid. This grid considers the age of a third party appraisal and the geographic region where the collateral is located in order to discount an appraisal that is greater than 12 months old. The discount rates in the appraisal discount grid are updated quarterly to reflect the most current knowledge that management has available, including the results of current appraisals. If there is a delay in receiving an updated appraisal or if the appraisal is found to be deficient in our internal appraisal review process and re-ordered, then the Bank continues to use a discount factor from the appraisal discount grid based on the collateral location and current appraisal age in order to determine the estimated fair value. A specific allocation of the ALL is recorded if there is any deficiency in collateral value determined by comparing the estimated fair value to the recorded investment of the loan. When updated appraisals are received and reviewed, adjustments are made to the specific allocation as needed.

The evaluation of the need and amount of a specific allocation of the ALL and whether a loan can be removed from impairment status is made on a quarterly basis.

| 16 |

The following table presents impaired loans by class, segregated by those for which a specific allowance was required and those for which a specific allowance was not necessary as of March 31, 2012 and December 31, 2011:

| Impaired Loans with Specific Allowance | Impaired Loans with No Specific Allowance | Total Impaired Loans | ||||||||||||||||||

| (in thousands) | Recorded Investment | Related Allowance | Recorded Investment | Recorded Investment | Unpaid Principal Balance | |||||||||||||||

| March 31, 2012 | ||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||

| Non owner-occupied | $ | 3,371 | $ | 901 | $ | 4,850 | $ | 8,221 | $ | 10,951 | ||||||||||

| All other CRE | 0 | 0 | 8,907 | 8,907 | 8,932 | |||||||||||||||

| Acquisition and development | ||||||||||||||||||||

| 1-4 family residential construction | 2,436 | 807 | 0 | 2,436 | 2,524 | |||||||||||||||

| All other A&D | 5,623 | 349 | 17,414 | 23,037 | 27,555 | |||||||||||||||

| Commercial and industrial | 0 | 0 | 3,979 | 3,979 | 4,068 | |||||||||||||||

| Residential mortgage | ||||||||||||||||||||

| Residential mortgage - term | 292 | 20 | 4,661 | 4,953 | 5,460 | |||||||||||||||

| Residential mortgage – home equity | 0 | 0 | 1,030 | 1,030 | 1,178 | |||||||||||||||

| Consumer | 0 | 0 | 77 | 77 | 98 | |||||||||||||||

| Total impaired loans | $ | 11,722 | $ | 2,077 | $ | 40,918 | $ | 52,640 | $ | 60,766 | ||||||||||

| December 31, 2011 | ||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||

| Non owner-occupied | $ | 448 | $ | 92 | $ | 9,129 | $ | 9,577 | $ | 14,765 | ||||||||||

| All other CRE | 0 | 0 | 7,365 | 7,365 | 7,390 | |||||||||||||||

| Acquisition and development | ||||||||||||||||||||

| 1-4 family residential construction | 2,489 | 859 | 0 | 2,489 | 2,577 | |||||||||||||||

| All other A&D | 7,850 | 1,859 | 15,360 | 23,210 | 27,712 | |||||||||||||||

| Commercial and industrial | 9,043 | 1,139 | 4,005 | 13,048 | 13,137 | |||||||||||||||

| Residential mortgage | ||||||||||||||||||||

| Residential mortgage - term | 218 | 2 | 4,816 | 5,034 | 5,488 | |||||||||||||||

| Residential mortgage – home equity | 0 | 0 | 1,082 | 1,082 | 1,177 | |||||||||||||||

| Consumer | 0 | 0 | 21 | 21 | 33 | |||||||||||||||

| Total impaired loans | $ | 20,048 | $ | 3,951 | $ | 41,778 | $ | 61,826 | $ | 72,279 | ||||||||||

Loans that are collectively evaluated for impairment are analyzed with general allowances being made as appropriate. For general allowances, historical loss trends are used in the estimation of losses in the current portfolio. These historical loss amounts are modified by other qualitative factors.

The classes described above, which are based on the Federal call code assigned to each loan, provide the starting point for the ALL analysis. Management tracks the historical net charge-off activity (full and partial charge-offs, net of full and partial recoveries) at the call code level. A historical charge-off factor is calculated utilizing a defined number of consecutive historical quarters. Consumer pools currently utilize a rolling 12 quarters, while Commercial pools currently utilize a rolling eight quarters.

“Pass” rated credits are segregated from “Criticized” credits for the application of qualitative factors. The un-criticized (“pass”) pools for commercial and residential real estate are further segmented based upon the geographic location of the underlying collateral. There are seven geographic regions utilized – six that represent the Bank’s lending footprint and a seventh for all out-of-market credits. Different economic environments and resultant credit risks exist in each region that are acknowledged in the assignment of qualitative factors. Loans in the criticized pools, which possess certain qualities or characteristics that may lead to collection and loss issues, are closely monitored by management and subject to additional qualitative factors.

Management supplements the historical charge-off factor with a number of additional qualitative factors that are likely to cause estimated credit losses associated with the existing loan pools to differ from historical loss experience. The additional factors, which are evaluated quarterly and updated using information obtained from internal, regulatory, and governmental sources, are: (a) national and local economic trends and conditions; (b) levels of and trends in delinquency rates and non-accrual loans; (c) trends in volumes and terms of loans; (d) effects of changes in lending policies; (e) experience, ability, and depth of lending staff; (f) value of underlying collateral; and (g) concentrations of credit from a loan type, industry and/or geographic standpoint.

| 17 |

Management reviews the loan portfolio on a quarterly basis using a defined, consistently applied process in order to make appropriate and timely adjustments to the ALL. When information confirms all or part of specific loans to be uncollectible, these amounts are promptly charged off against the ALL. Residential mortgage and consumer loans are charged off after they are 120 days contractually past due. All other loans are charged off based on an evaluation of the facts and circumstances of each individual loan. When the Bank believes that its ability to collect is solely dependent on the liquidation of the collateral, a full or partial charge-off is recorded promptly to bring the recorded investment to an amount that the Bank believes is supported by an ability to collect on the collateral. The circumstances that may impact the Bank’s decision to charge-off all or a portion of a loan include default or non-payment by the borrower, scheduled foreclosure actions, and/or prioritization of the Bank’s claim in bankruptcy. There may be circumstances where, due to pending events, the Bank will place a specific allocation of the ALL on a loan for which a partial charge-off has been previously recognized. This specific allocation may be either charged off or removed depending upon the outcome of the pending event. Full or partial charge-offs are not recovered until full principal and interest on the loan have been collected, even if a subsequent appraisal supports a higher value. Loans with partial charge-offs remain in non-accrual status. Both full and partial charge-offs reduce the recorded investment of the loan and the ALL and are considered to be charge-offs for purposes of all credit loss metrics and trends, including the historical rolling charge-off rates used in the determination of the ALL.

Activity in the ALL is presented for the three-months ended March 31, 2012 and March 31, 2011:

| Commercial Real Estate | Acquisition and Development | Commercial and Industrial | Residential Mortgage | Consumer | Total | |||||||||||||||||||

| ALL balance at January 1, 2012 | $ | 6,218 | $ | 7,190 | $ | 2,190 | $ | 3,430 | $ | 452 | $ | 19,480 | ||||||||||||

| Charge-offs | (1,161 | ) | (246 | ) | (9,091 | ) | (283 | ) | (173 | ) | (10,954 | ) | ||||||||||||

| Recoveries | 0 | 12 | 330 | 99 | 122 | 563 | ||||||||||||||||||

| Provision | 1,578 | (1,077 | ) | 7,500 | 131 | (8 | ) | 8,124 | ||||||||||||||||

| ALL balance at March 31, 2012 | $ | 6,635 | $ | 5,879 | $ | 929 | $ | 3,377 | $ | 393 | $ | 17,213 | ||||||||||||

| ALL balance at January 1, 2011 | $ | 8,658 | $ | 6,345 | $ | 1,345 | $ | 4,211 | $ | 1,579 | $ | 22,138 | ||||||||||||

| Charge-offs | (1,554 | ) | (395 | ) | (135 | ) | (472 | ) | (232 | ) | (2,788 | ) | ||||||||||||

| Recoveries | 77 | 199 | 2 | 283 | 154 | 715 | ||||||||||||||||||

| Provision | 767 | 982 | 859 | (171 | ) | (1,093 | ) | 1,344 | ||||||||||||||||

| ALL balance at March 31, 2011 | $ | 7,948 | $ | 7,131 | $ | 2,071 | $ | 3,851 | $ | 408 | $ | 21,409 | ||||||||||||

The ALL is based on estimates, and actual losses will vary from current estimates. Management believes that the granularity of the homogeneous pools and the related historical loss ratios and other qualitative factors, as well as the consistency in the application of assumptions, result in an ALL that is representative of the risk found in the components of the portfolio at any given date.

| 18 |

The following tables present the average recorded investment in impaired loans by class and related interest income recognized for the periods indicated:

| Three months ended March 31, 2012 | Three months ended March 31, 2011 | |||||||||||||||||||||||

| (in thousands) | Average investment | Interest income recognized on an accrual basis | Interest income recognized on a cash basis | Average investment | Interest income recognized on an accrual basis | Interest income recognized on a cash basis | ||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||||||

| Non owner-occupied | $ | 8,899 | $ | 6 | $ | 0 | $ | 15,168 | $ | 19 | $ | 0 | ||||||||||||

| All other CRE | 8,136 | 80 | 0 | 5,070 | 69 | 0 | ||||||||||||||||||

| Acquisition and development | ||||||||||||||||||||||||

| 1-4 family residential construction | 2,463 | 24 | 0 | 3,250 | 27 | 0 | ||||||||||||||||||

| All other A&D | 23,124 | 105 | 0 | 27,885 | 145 | 0 | ||||||||||||||||||

| Commercial and industrial | 8,514 | 34 | 0 | 9,451 | 38 | 0 | ||||||||||||||||||

| Residential mortgage | ||||||||||||||||||||||||

| Residential mortgage - term | 4,994 | 35 | 15 | 8,271 | 43 | 0 | ||||||||||||||||||

| Residential mortgage – home equity | 1,056 | 4 | 3 | 652 | 4 | 0 | ||||||||||||||||||

| Consumer | 49 | 0 | 0 | 99 | 0 | 0 | ||||||||||||||||||

| Total | $ | 57,235 | $ | 288 | $ | 18 | $ | 69,846 | $ | 345 | $ | 0 | ||||||||||||

In the normal course of business, the Bank modifies loan terms for various reasons. These reasons may include as a retention strategy to compete in the current interest rate environment, and to re-amortize or extend a loan term to better match the loan’s payment stream with the borrower’s cash flows. A modified loan is considered to be a troubled debt restructure (“TDR”) when the Bank has determined that the borrower is troubled (i.e. experiencing financial difficulties). The Bank evaluates the probability that the borrower will be in payment default on any of its debt in the foreseeable future without modification. To make this determination, the Bank performs a global financial review of the borrower and loan guarantors to assess their current ability to meet their financial obligations.

When the Bank restructures a loan to a troubled borrower, the loan terms (i.e. interest rate, payment amount, amortization period, and/or maturity date) are modified in such a way as to enable the borrower to cover the modified debt service payments based on current financials and cash flow adequacy. If a borrower’s hardship is thought to be temporary, then modified terms are only offered for that time period. Where possible, the Bank obtains additional collateral and/or secondary payment sources at the time of the restructure in order to put the Bank in the best possible position if the borrower is not able to meet the modified terms. To date, the Bank has not forgiven any principal as a restructuring concession. The Bank will not offer modified terms if it believes that modifying the loan terms will only delay an inevitable permanent default.

All loans designated as TDRs are considered impaired loans and may be in either accruing or non-accruing status. The Corporation’s policy for recognizing interest income on impaired loans does not differ from its overall policy for interest recognition. Accordingly, the accrual of interest is discontinued when principal or interest is delinquent for 90 days or more unless the loan is well-secured and in the process of collection. If the loan was accruing at the time of the modification, then it continues to be in accruing status subsequent to the modification. Non-accrual TDRs may return to accruing status when there has been sufficient payment performance for a period of at least six months. Loans may be removed from TDR status in the calendar year following the modification if the interest rate at the time of modification was consistent with the interest rate for a loan with comparable credit risk and the loan has performed according to its modified terms for at least six months.

The volume and type of TDR activity is considered in the assessment of the local economic trends qualitative factor used in the determination of the ALL for loans that are evaluated collectively for impairment.

| 19 |

The following table presents the volume and recorded investment at the time of modification of TDRs by class and type of modification that occurred during the periods indicated:

| Temporary Rate Modification | Extension of Maturity | Modification of Payment and Other Terms | ||||||||||||||||||||||

| (in thousands) | Number of Contracts | Recorded Investment | Number of Contracts | Recorded Investment | Number of Contracts | Recorded Investment | ||||||||||||||||||

| Three months ended March 31, 2012 | ||||||||||||||||||||||||

| Commercial real estate | ||||||||||||||||||||||||

| Non owner-occupied | 0 | $ | 0 | 0 | $ | 0 | 0 | $ | 0 | |||||||||||||||

| All other CRE | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Acquisition and development | ||||||||||||||||||||||||

| 1-4 family residential construction | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| All other A&D | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Commercial and industrial | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Residential mortgage | ||||||||||||||||||||||||

| Residential mortgage – term | 1 | 513 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Residential mortgage – home equity | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Consumer | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Total | 1 | $ | 513 | 0 | $ | 0 | 0 | $ | 0 | |||||||||||||||

There was one new TDR with a temporary rate modification during the three months ended March 31, 2012 for which there was no impact to the recorded investment and a $4,300 reduction of the ALL resulting from the movement of the loan being evaluated collectively for impairment to being evaluated individually for impairment. During the quarters ended March 31, 2012 and March 31, 2011, there were no receivables modified as troubled debt restructurings within the previous 12 months for which there was a payment default during the periods indicated.

Note 8 – Fair Value of Financial Instruments

The Corporation complies with the guidance of ASC Topic 820, Fair Value Measurements and Disclosures, which defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements required under other accounting pronouncements. The Corporation also follows the guidance on matters relating to all financial instruments found in ASC Subtopic 825-10, Financial Instruments – Overall.

Fair value is defined as the price to sell an asset or to transfer a liability in an orderly transaction between willing market participants as of the measurement date. Fair value is best determined by values quoted through active trading markets. Active trading markets are characterized by numerous transactions of similar financial instruments between willing buyers and willing sellers. Because no active trading market exists for various types of financial instruments, many of the fair values disclosed were derived using present value discounted cash flows or other valuation techniques described below. As a result, the Corporation’s ability to actually realize these derived values cannot be assumed.

The Corporation measures fair values based on the fair value hierarchy established in ASC Paragraph 820-10-35-37. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of inputs that may be used to measure fair value under the hierarchy are as follows:

Level 1: Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets and liabilities. This level is the most reliable source of valuation.

Level 2: Quoted prices that are not active, or inputs that are observable either directly or indirectly, for substantially the full term of the asset or liability. Level 2 inputs include inputs other than quoted prices that are observable for the asset or liability (for example, interest rates and yield curves at commonly quoted intervals, volatilities, prepayment speeds, loss severities, credit risks, and default rates). It also includes inputs that are derived principally from or corroborated by observable market data by correlation or other means (market-corroborated inputs). Several sources are utilized for valuing these assets, including a contracted valuation service, Standard & Poor’s (“S&P”) evaluations and pricing services, and other valuation matrices.

Level 3: Prices or valuation techniques that require inputs that are both significant to the valuation assumptions and not readily observable in the market (i.e. supported with little or no market activity). Level 3 instruments are valued based on the best available data, some of which is internally developed, and consider risk premiums that a market participant would require.

| 20 |

The level established within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement.

The Corporation believes that its valuation techniques are appropriate and consistent with the techniques used by other market participants. However, the use of different methodologies and assumptions could result in a different estimate of fair values at the reporting date. The valuation techniques used by the Corporation to measure, on a recurring and non-recurring basis, the fair value of assets as of March 31, 2012 are discussed in the paragraphs that follow.

Investments – The investment portfolio is classified and accounted for based on the guidance of ASC Topic 320, Investments – Debt and Equity Securities.

Securities available-for-sale: The fair value of investments available-for-sale is determined using a market approach. As of March 31, 2012, the U.S. Government agencies, residential mortgage-backed securities, private label residential mortgage-backed securities, and municipal bonds segments are classified as Level 2 within the valuation hierarchy. Their fair values were determined based upon market-corroborated inputs and valuation matrices, which were obtained through third party data service providers or securities brokers through which the Corporation has historically transacted both purchases and sales of investment securities.

The amortized cost of debt securities classified as available-for-sale is adjusted for the amortization of premiums to the first call date, if applicable, or to maturity, and for the accretion of discounts to maturity, or, in the case of mortgage-backed securities, over the estimated life of the security. Such amortization and accretion is included in interest income from investments. Interest and dividends are included in interest income from investments. Gains and losses on the sale of securities are recorded using the specific identification method.

Management systematically evaluates securities for impairment on a quarterly basis. Based upon application of accounting guidance for subsequent measurement in ASC Topic 320 (ASC Section 320-10-35), management assesses whether (a) it has the intent to sell a security being evaluated and (b) it is more likely than not that the Corporation will be required to sell the security prior to its anticipated recovery. If neither applies, then declines in the fair values of securities below their cost that are considered other-than-temporary declines are split into two components. The first is the loss attributable to declining credit quality. Credit losses are recognized in earnings as realized losses in the period in which the impairment determination is made. The second component consists of all other losses, which are recognized in other comprehensive loss. In estimating other-than-temporary impairment losses, management considers (1) the length of time and the extent to which the fair value has been less than cost, (2) adverse conditions specifically related to the security, an industry, or a geographic area, (3) the historic and implied volatility of the fair value of the security, (4) changes in the rating of the security by a rating agency, (5) recoveries or additional declines in fair value subsequent to the balance sheet date, (6) failure of the issuer of the security to make scheduled interest or principal payments, and (7) the payment structure of the debt security and the likelihood of the issuer being able to make payments that increase in the future. Management also monitors cash flow projections for securities that are considered beneficial interests under the guidance of ASC Subtopic 325-40, Investments – Other – Beneficial Interests in Securitized Financial Assets, (ASC Section 325-40-35). Further discussion about the evaluation of securities for impairment can be found in Note 5.

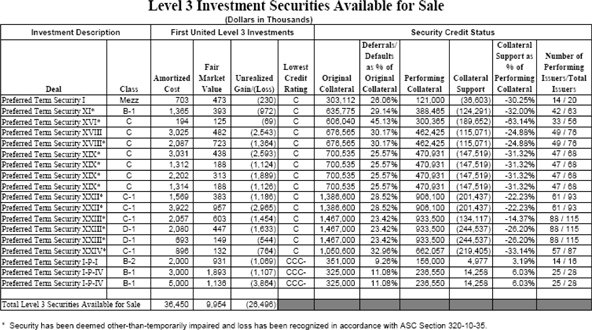

The CDO segment, which consists of pooled trust preferred securities issued by banks, thrifts and insurance companies, is classified as Level 3 within the valuation hierarchy. At March 31, 2012, the Corporation owned 18 pooled trust preferred securities with an amortized cost of $36.5 million and a fair value of $10.0 million. The market for these securities at March 31, 2012 is not active and markets for similar securities are also not active. The inactivity was evidenced first by a significant widening of the bid-ask spread in the brokered markets in which these securities trade and then by a significant decrease in the volume of trades relative to historical levels. The new issue market is also inactive, as few CDOs have been issued since 2007. There are currently very few market participants who are willing to effect transactions in these securities. The market values for these securities or any securities other than those issued or guaranteed by the U.S. Department of the Treasury (the “Treasury”) are very depressed relative to historical levels. Therefore, in the current market, a low market price for a particular bond may only provide evidence of stress in the credit markets in general rather than being an indicator of credit problems with a particular issue. Given the conditions in the current debt markets and the absence of observable transactions in the secondary and new issue markets, management has determined that (a) the few observable transactions and market quotations that are available are not reliable for the purpose of obtaining fair value at March 31, 2012, (b) an income valuation approach technique (i.e. present value) that maximizes the use of relevant observable inputs and minimizes the use of unobservable inputs will be equally or more representative of fair value than a market approach, and (c) the CDO segment is appropriately classified within Level 3 of the valuation hierarchy because management determined that significant adjustments were required to determine fair value at the measurement date.

| 21 |

Management utilizes an independent third party to prepare both the evaluations of other-than-temporary impairment as well as the fair value determinations for its CDO portfolio. Management does not believe that there were any material differences in the impairment evaluations and pricing between March 31, 2012 and December 31, 2011.