UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2010

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _______________ to _____________

Commission File Number 0-13888

CHEMUNG FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

|

NEW YORK

|

16-123703-8

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

One Chemung Canal Plaza, P.O. Box 1522, Elmira, New York

|

14902

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant's telephone number, including area code: (607) 737-3711

|

Securities registered pursuant to Section 12(b) of the Act:

|

None

|

|

|

Securities registered pursuant to Section 12(g) of the Act:

|

Common Stock, par value $0.01 a share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicated by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

Non-accelerated filer

|

o

|

Smaller Reporting Company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES o NO x

Based upon the closing price of the registrant's Common Stock as of June 30, 2010, the aggregate market value of the voting stock held by non-affiliates of the registrant was $41,351,063.

As of February 28, 2011 there were 3,565,610 shares of Common Stock, $0.01 par value outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Shareholders to be held on May 11, 2011 are incorporated by reference into Part III, Items 10, 11, 12, 13, and 14 of this Form 10-K.

CHEMUNG FINANCIAL CORPORATION

ANNUAL REPORT ON FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

|

Form 10-K Item Number:

|

Page No.

|

|

|

PART I

|

1

|

|

|

Item 1. Business

|

1

|

|

|

Item 1A. Risk Factors

|

12

|

|

|

Item 1B. Unresolved Staff Comments

|

16

|

|

|

Item 2. Properties

|

16

|

|

|

Item 3. Legal Proceedings

|

17

|

|

|

Item 4. Removed and Reserved

|

17

|

|

|

PART II

|

17

|

|

|

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

Securities

|

17

|

|

|

Item 6. Selected Financial Data

|

20

|

|

|

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operation

|

22

|

|

|

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

|

39

|

|

|

Item 8. Financial Statements and Supplementary Data

|

39

|

|

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

39

|

|

|

Item 9A. Controls and Procedures

|

39

|

|

|

Item 9B. Other Information

|

40

|

|

|

PART III

|

41

|

|

|

Item 10. Directors, Executive Officers and Corporate Governance

|

41

|

|

|

Item 11. Executive Compensation

|

42

|

|

|

Item 12. Security Ownership of Certain Beneficial Owners and Management, and Related Stockholder Matters

|

42

|

|

|

Item 13. Certain Relationships and Related Transactions, and Director Independence

|

42

|

|

|

Item 14. Principal Accountant Fees and Services

|

42

|

|

|

PART IV

|

42

|

|

|

Item 15. Exhibits and Financial Statement Schedules

|

42

|

|

|

Index to Consolidated Financial Statements

|

44

|

|

|

Report of Independent Registered Public Accounting Firm-Crowe Horwath LLP

|

F-1

|

|

|

SIGNATURES

|

Some of the information contained in this report concerning the markets and industry in which we operate is derived from publicly available information and from industry sources. Although we believe that this publicly available information and information provided by these industry sources are reliable, we have not independently verified the accuracy of any of this information.

PART I

ITEM 1. BUSINESS

General Development of Business

Chemung Financial Corporation (the "Corporation") was incorporated on January 2, 1985 under the laws of the State of New York. The Corporation was organized for the purpose of acquiring Chemung Canal Trust Company (the "Bank"). The Bank was established in 1833 under the name Chemung Canal Bank, and was subsequently granted a New York State bank charter in 1895. In 1902, the Bank was reorganized as a New York State trust company under the name Elmira Trust Company, and its name was changed to Chemung Canal Trust Company in 1903.

The Corporation has been a financial holding company since June 22, 2000. Financial holding company status provides the Corporation with the flexibility to offer an array of financial services, such as insurance products, mutual funds, and brokerage services, which provide additional sources of fee based income and allow the Corporation to better serve its customers. The Corporation established a financial services subsidiary, CFS Group, Inc., in September 2001 which offers non-banking financial services such as mutual funds, annuities, brokerage services and insurance. As such, the Corporation currently operates as a financial holding company with two subsidiaries, Chemung Canal Trust Company, a full-service community bank with full trust powers, and CFS Group, Inc.

The Securities and Exchange Commission (the "SEC") maintains a web site at www.sec.gov that contains reports, proxy and information statements, and other information regarding the Corporation. You may also read and copy materials we file with the SEC at the SEC's Public Reference Room at 100 F St., NE, Washington, D.C. 20549. You may obtain information concerning the operation of the Public Reference Room by calling 1-800-SEC-0330. In addition, we maintain a corporate web site at www.chemungcanal.com. We make available free of charge through our web site our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports pursuant to Section 13(a) or 15(d) of the Exchange Act and filed with the SEC. These items are available as soon as reasonably practicable after we electronically file or furnish such material with or to the SEC. The contents of our web site are not a part of this report. These materials are also available free of charge by written request to: Jane H. Adamy, Senior Vice President and Secretary, Chemung Canal Trust Company, One Chemung Canal Plaza, Elmira, NY 14901.

Description of Business

Business

The Bank is a New York chartered commercial bank which engages in full-service commercial and consumer banking and trust business. The Bank's services include accepting time, demand and savings deposits, including NOW accounts, regular savings accounts, insured money market accounts, investment certificates, fixed-rate certificates of deposit and club accounts. The Bank's services also include making secured and unsecured commercial and consumer loans, financing commercial transactions (either directly or participating with regional industrial development and community lending corporations), and making commercial, residential and home equity mortgage loans, revolving credit loans with overdraft checking protection and small business loans. Additional services include renting safe deposit facilities and the provision of networked automated teller facilities.

Trust services provided by the Bank include services as executor and trustee under wills and agreements, and guardian, custodian, trustee and agent for pension, profit-sharing and other employee benefit trusts, as well as various investment, pension, estate planning and employee benefit administrative services.

CFS Group, Inc. offers an array of financial services including mutual funds, full and discount brokerage services, annuity and other insurance products and tax preparation services.

1

For additional information, including information concerning the results of operations of the Corporation and its subsidiaries, see Management's Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7.

There have been no material changes in the manner of doing business by the Corporation or its subsidiaries during the fiscal year ended December 31, 2010.

Market Area and Competition

Seven of the Bank's 23 full-service offices, including the main office, are located in Chemung County, New York. The Bank has thirteen full-service offices located in the adjacent counties of Broome, Schuyler, Steuben, Tioga and Tompkins, with a Trust and Investment Center located in Herkimer County within New York State and 3 full-service offices located in Bradford County, Pennsylvania. The Corporation defines its primary market areas as those areas within a 25-mile radius of its New York offices in Broome, Chemung, Herkimer, Steuben, Schuyler, Tioga and Tompkins counties, including the northern tier of Pennsylvania. The Bank's lending policy restricts substantially all lending efforts to these geographical regions.

Within these market areas, the Bank encounters intense competition in the lending and deposit gathering aspects of its business from commercial and thrift banking institutions, credit unions and other providers of financial services, such as brokerage firms, investment companies, insurance companies and Internet vendors. The Bank also competes with non-financial institutions, including retail stores and certain utilities that maintain their own credit programs, as well as governmental agencies that make available loans to certain borrowers. Unlike the Bank, many of these competitors are not subject to regulation as extensive as that affecting the Bank and, as a result, they may have a competitive advantage over the Bank in certain respects. This is particularly true of credit unions because their pricing structure is not encumbered by income taxes.

Competition for the Bank's Trust Department investment services comes primarily from brokerage firms and independent investment advisors. These firms devote much of their considerable resources toward gaining larger positions in these markets. The market value of the Bank's trust assets under administration totaled approximately $1.6 billion at year-end 2010. The Trust and Investment Division is responsible for the largest component of non-interest revenue.

Supervision and Regulation

The Corporation is regulated under the Bank Holding Company Act of 1956, as amended (the "BHC Act"), and is subject to the supervision of the Board of Governors of the Federal Reserve System (the "Federal Reserve Board"). As a bank holding company, the Corporation generally may engage in the activities permissible for a bank holding company, which includes banking, managing or controlling banks, performing certain servicing activities for subsidiaries, and engaging in other activities that the Federal Reserve Board has determined to be so closely related to banking as to be a proper incident thereto. Because the Corporation also has elected financial holding company status, it may also engage in a broader range of activities that are determined by the Federal Reserve and the Secretary of the Treasury to be financial in nature or incidental to financial activities or activities that are determined by the Federal Reserve Board to be complementary to a financial activity and that do not pose a substantial risk to the safety and soundness of depository institutions or the financial system generally.

The Corporation is also under the jurisdiction of the SEC and is subject to the disclosure and regulatory requirements of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended, as administered by the SEC.

The Bank is chartered under the laws of New York State and is supervised by the New York State Banking Department ("NYSBD"). The Bank also is a member bank of the Federal Reserve System and, therefore, the Federal Reserve Board serves as its primary federal regulator.

CFS Group, Inc. is subject to supervision by other regulatory authorities as determined by the activities in which it is engaged. Insurance activities are supervised by the New York State Insurance Department, and brokerage activities are subject to supervision by the SEC and the Financial Industry Regulatory Authority ("FINRA").

2

The Corporation is subject to capital adequacy guidelines of the Federal Reserve Board. The guidelines apply on a consolidated basis and require bank holding companies to maintain a minimum ratio of Tier 1 capital to total assets (or "leverage ratio") of 4%. For the most highly rated bank holding companies, the minimum ratio is 3%. The Federal Reserve Board capital adequacy guidelines also require bank holding companies to maintain a minimum ratio of Tier 1 capital to risk-weighted assets of 4% and a minimum ratio of qualifying total capital to risk-weighted assets of 8%. Any bank holding company whose capital does not meet the minimum capital adequacy guidelines is considered to be undercapitalized, and is required to submit an acceptable plan to the Federal Reserve Board for achieving capital adequacy. In addition, an undercapitalized company's ability to pay dividends to its shareholders and expand its lines of business through the acquisition of new banking or non-banking subsidiaries also could be restricted by the Federal Reserve Board. The Federal Reserve Board may set higher minimum capital requirements for bank holding companies where circumstances warrant, such as companies anticipating significant growth or facing unusual risks. As of December 31, 2010, the Corporation's leverage ratio was 8.72%, its ratio of Tier 1 capital to risk-weighted assets was 12.92% and its ratio of qualifying total capital to risk-weighted assets was 14.54%. The Federal Reserve Board has not advised the Corporation that it is subject to any special capital requirements.

Pursuant to Federal Reserve Board regulations and supervisory policies, bank holding companies also are expected to serve as a source of financial and managerial strength to their subsidiary depository institutions. Therefore, to the extent the Bank is in need of capital, the Corporation could be expected to provide additional capital to the Bank, including, potentially, raising new capital for that purpose.

The Bank is subject to leverage and risk-based capital requirements and minimum capital guidelines of the Federal Reserve Board that are similar to those applicable to the Corporation. As of December 31, 2010, the Bank was in compliance with all minimum capital requirements. The Bank's leverage ratio as of that date was 8.30%, its ratio of Tier 1 capital to risk-weighted assets was 12.31%, and its ratio of qualifying total capital to risk-weighted assets was 13.93%.

The Bank also is subject to substantial regulatory restrictions on its ability to pay dividends to the Corporation. Under Federal Reserve Board and NYSBD regulations, the Bank may not pay a dividend without prior approval of the Federal Reserve and the NYSBD if the total amount of all dividends declared during such calendar year, including the proposed dividend, exceeds the sum of its retained net income to date during the calendar year and its retained net income over the preceding two calendar years. As of December 31, 2010, approximately $5.1 million was available for the payment of dividends by the Bank to the Corporation without prior approval, after giving effect to the payment of dividends in the fourth quarter of 2010. The Bank's ability to pay dividends also is subject to the Bank being in compliance with regulatory capital requirements. The Bank is currently in compliance with these requirements.

The deposits of the Bank are insured up to regulatory limits by the Federal Deposit Insurance Corporation (the "FDIC") and are subject to the deposit insurance premium assessments of the Deposit Insurance Fund ("DIF"). The FDIC currently maintains a risk-based assessment system under which assessment rates vary based on the level of risk posed by the institution to the DIF. For institutions that have a long-term public debt rating, the individual risk assessment is based on its supervisory ratings and its debt rating. For institutions such as the Bank that do not have a long-term public debt rating, the individual risk assessment is based on its supervisory ratings and certain financial ratios and other measurements of its financial condition. The assessment rate may, therefore, change after any of these measurements change.

In February 2011, the FDIC adopted a final rule making certain changes to the deposit insurance assessment system, many of which were made as a result of provisions of the Dodd-Frank Act. The final rule also revises the assessment rate schedule effective April 1, 2011, and adopts additional rate schedules that will go into effect when the Deposit Insurance Fund (DIF) reserve ratio reaches various milestones. The final rule changes the deposit insurance assessment system from one that is based on domestic deposits to one that is based on average consolidated total assets minus average tangible equity. In addition, the rule suspends FDIC dividend payments if the DIF reserve ratio exceeds 1.5 percent but provides for decreasing assessment rates when the DIF reserve ratio reaches certain thresholds.

3

The Bank is also a member of the Federal Home Bank ("FHLB") of New York, which provides a central credit facility primarily for member institutions for home mortgage and neighborhood lending. The Bank is subject to the rules and requirements of the FHLB, including the requirement to acquire and hold shares of capital stock in the FHLB. The Bank was in compliance with the rules and requirements of the FHLB at December 31, 2010.

Recent Legislation

On July 21, 2010, the President signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"). This new law will significantly change the current bank regulatory structure and affect the lending, deposit, investment, trading and operating activities of financial institutions and their holding companies. The Dodd-Frank Act requires various federal agencies to adopt a broad range of new rules and regulations, and to prepare various studies and reports for Congress. The federal agencies are given significant discretion in drafting such rules and regulations. With that discretion, market litigation, and continued legislative efforts, many of the details and much of the impact of the Dodd-Frank Act may not be known for months or years.

Certain provisions of the Dodd-Frank Act are expected to have a near term impact on the Corporation. For example, effective July 21, 2011, a provision of the Dodd-Frank Act eliminates the federal prohibitions on paying interest on demand deposits, thus allowing businesses to offer interest-bearing checking accounts. Depending on competitive responses, this significant change to existing law could have an adverse impact on the Corporation’s interest expense.

The Dodd-Frank Act also broadens the base for Federal Deposit Insurance Corporation insurance assessments. Assessments will now be based on the average consolidated total assets less tangible equity capital of a financial institution. The Dodd-Frank Act also permanently increases the maximum amount of deposit insurance for banks, savings institutions and credit unions to $250,000 per depositor per insured institution, retroactive to January 1, 2008, and qualifying non-interest bearing transaction accounts have unlimited deposit insurance through December 31, 2012.

The Dodd-Frank Act and recently promulgated rules of the SEC will require publicly traded companies to give stockholders a non-binding vote on executive compensation and so-called "golden parachute" payments, and allow greater access by shareholders to the Corporation’s proxy material in connection with shareholder director nominations.

The Dodd-Frank Act creates a new Consumer Financial Protection Bureau with wide-ranging powers to supervise and enforce consumer protection laws. The Consumer Financial Protection Bureau has broad rule-making authority for a wide range of consumer protection laws that apply to all banks and savings institutions, including the authority to prohibit "unfair, deceptive or abusive" acts and practices. The Consumer Financial Protection Bureau has examination and enforcement authority over all banks and savings institutions with more than $10 billion in assets. The Dodd-Frank Act also weakens the federal preemption rules that have been applicable to national banks and federal savings associations, and gives state attorneys general certain powers to enforce federal consumer protection laws.

It is difficult to predict at this time with specificity the full range of the impact the Dodd-Frank Act and the yet to be written implementing rules and regulations will have on the Corporation. The legislation and any implementing rules that are ultimately issued could have adverse implications on the financial industry, the competitive environment, and the Corporation’s ability to conduct business. The Corporation will have to apply resources to ensure that it is in compliance with all applicable provisions of the Dodd-Frank Act and any implementing rules, which may increase its costs of operations and adversely impact its earnings.

4

Other Regulatory and Legislative Actions

On September 29, 2009, the FDIC increased annual assessment rates uniformly by 3 basis points beginning January 1, 2011. At least semi-annually thereafter, the FDIC will update its loss and income projections for the DIF and, if necessary to achieve its target reserve ratio, will change assessment rates via a rulemaking that will include a public notice and comment period.

In addition, all institutions with deposits insured by the FDIC are required to pay assessments to fund interest payments on bonds issued by the Financing Corporation ("FICO"), an agency of the Federal government established to recapitalize the predecessor to the Savings Association Insurance Fund. These assessments will continue until the FICO bonds mature in 2017. The FDIC's FICO assessment authority is separate from its authority to assess risk-based premiums for deposit insurance. The FICO assessment rate is adjusted quarterly to reflect changes in the assessment bases of the fund and is not risk-based by institution. The FICO assessment rate for the first quarter of 2011, due December 30, 2010, was 1.02% of insured deposits.

The Federal Deposit Insurance Reform Act of 2005 also gave a credit to all insured depository institutions to be used as an offset to the institutions’ assessments. The Bank received a $598,000 credit, which entirely offset its 2007 and partially offset its 2008 deposit insurance settlement. Due to the full utilization of the credit in 2008, the systemic increase in deposit insurance assessments and the emergency special assessment, the Bank will be subject to increased deposit premium expenses in future periods.

On October 14, 2008, the FDIC announced the Temporary Liquidity Guarantee Program ("TLGP"), which provides unlimited deposit insurance on funds invested in noninterest-bearing transaction deposit accounts in excess of the existing deposit insurance limit of $250,000. Participating institutions were assessed a $0.10 surcharge per $100 of deposits above the existing deposit insurance limit. The TLGP also provides that the FDIC, for an additional fee, will guarantee qualifying senior unsecured debt issued prior to October 2009 by participating banks and certain qualifying holding companies. The Bank and the Corporation elected to opt in to both portions of the TLGP. The TLPG expired on December 31, 2010, but was replaced by section 343 of the Dodd-Frank Act.

Transactions between the Bank and either the Corporation or CFS Group, Inc. are governed by sections 23A and 23B of the Federal Reserve Act ("FRA") and the Federal Reserve Board’s implementing Regulation W. Generally, these provisions are intended to protect insured depository institutions from suffering losses arising from transactions with non-insured affiliates, by placing quantitative and qualitative limitations on covered transactions between a bank and any one affiliate as well as all affiliates of the bank in the aggregate, and requiring that such transactions be on terms that are consistent with safe and sound banking practices. Sections 22(g) and (h) of the FRA and their implementing Regulation O restrict the amounts and terms of loans to directors, executive officers and principal shareholders.

In 2007, the Federal Reserve Board and SEC issued Regulation R to clarify that traditional banking activities involving some elements of securities brokerage activities, such as most trust and fiduciary activities, may continue to be performed by banks rather than being "pushed" out to affiliates supervised by the SEC. These rules took effect for the Bank on January 1, 2009.

5

Under the privacy and data security provisions of the Financial Modernization Act of 1999, also known as the Gramm-Leach-Bliley Act ("GLB Act"), and rules promulgated thereunder, all financial institutions, including the Corporation, the Bank and CFS Group, Inc., are required to establish policies and procedures to restrict the sharing of nonpublic customer data with nonaffiliated parties at the customer's request and to protect customer data from unauthorized access. In addition, the Fair Credit Reporting Act ("FCRA"), as amended by the Fair and Accurate Credit Transactions Act of 2003 ("FACT Act"), includes many provisions affecting the Corporation, Bank, and/or CFS Group, Inc., including provisions concerning obtaining consumer reports, furnishing information to consumer reporting agencies, maintaining a program to prevent identity theft, sharing of certain information among affiliated companies, and other provisions. For instance, FCRA requires persons subject to FCRA to notify their customers if they report negative information about them to a credit bureau or if they are granted credit on terms less favorable that those generally available. The Federal Reserve Board and the Federal Trade Commission ("FTC") have extensive rulemaking authority under the FACT Act, and the Corporation and the Bank are subject to the rules that have been promulgated by the Federal Reserve Board and FTC thereunder, including recent rules regarding limitations on affiliate marketing and implementation of programs to identify, detect and mitigate the risk of identity theft through red flags. The Corporation has developed policies and procedures for itself and its subsidiaries to maintain compliance and believes it is in compliance with all privacy, information sharing and notification provisions of the GLB Act and FCRA.

The GLB Act and FCRA also impose requirements regarding data security and the safeguarding of customer information. The Bank is subject to the Interagency Guidelines Establishing Information Security Standards (Security Guidelines), which implement section 501(b) of the GLB Act and section 216 of the FACT Act. The Security Guidelines establish standards relating to administrative, technical, and physical safeguards to ensure the security, confidentiality, integrity and the proper disposal of customer information. The Bank believes it is in compliance with all such standards.

Under Title III of the USA PATRIOT Act, also known as the International Money Laundering Abatement and Anti-Terrorism Financing Act of 2001, all financial institutions are required in general to identify their customers, adopt formal and comprehensive anti-money laundering programs, scrutinize or prohibit altogether certain transactions of special concern, and be prepared to respond to inquiries from U.S. law enforcement agencies concerning their customers and their transactions. Additional information-sharing among financial institutions, regulators, and law enforcement authorities is encouraged by the presence of an exemption from the privacy provisions of the GLB Act for financial institutions that comply with this provision and the authorization of the Secretary of the Treasury to adopt rules to further encourage cooperation and information-sharing. The effectiveness of a financial institution in combating money laundering activities is a factor to be considered in any application submitted by the financial institution under the Bank Merger Act, which applies to the Bank, or the BHC Act, which applies to the Corporation.

The Bank has a responsibility under the Community Reinvestment Act of 1977 ("CRA") to help meet the credit needs of its communities, including low- and moderate-income neighborhoods. The CRA does not establish specific lending requirements or programs for financial institutions nor does it limit an institution’s discretion to develop the types of products and services that it believes are best suited to its particular community, consistent with the CRA. Regulators assess the Bank’s record of compliance with the CRA. In addition, the Equal Credit Opportunity Act and the Fair Housing Act prohibit discrimination in lending practices on the basis of characteristics specified in those statutes. The Bank’s failure to comply with the provisions of the CRA could, at a minimum, result in regulatory restrictions on its activities and the activities of the Corporation. The Bank’s failure to comply with the Equal Credit Opportunity Act and the Fair Housing Act could result in enforcement actions against it by its regulators as well as other federal regulatory agencies and the Department of Justice. The Bank’s latest CRA rating was "Outstanding".

6

The Sarbanes-Oxley Act of 2002 implemented a broad range of measures to increase corporate responsibility, enhance penalties for accounting and auditing improprieties at publicly traded companies, and protect investors by improving the accuracy and reliability of corporate disclosures for companies that have securities registered under the Exchange Act, including publicly-held financial holding companies such as the Corporation. It includes very specific additional disclosure requirements and corporate governance rules, and the SEC and securities exchanges have adopted extensive additional disclosures, corporate governance and other related rules pursuant to its mandate. The Act represents significant federal involvement in matters traditionally left to state regulatory systems, such as the regulation of the accounting profession, and to state corporate law, such as the relationship between a board of directors and management and between a board of directors and its committees. In addition, the federal banking regulators have adopted generally similar requirements concerning the certification of financial statements by bank officials.

Home mortgage lenders, including banks, are required under the Home Mortgage Disclosure Act to make available to the public expanded information regarding the pricing of home mortgage loans, including the "rate spread" between the interest rate on loans and certain Treasury securities and other benchmarks. The availability of this information has led to increased scrutiny of higher-priced loans at all financial institutions to detect illegal discriminatory practices and to the initiation of a limited number of investigations by federal banking agencies and the U.S. Department of Justice. The Corporation has no information that it or its affiliates are the subject of any investigation.

In the past two years, declining housing values have resulted in deteriorating economic conditions across the U.S., resulting in significant writedowns in the values of mortgage-backed securities and derivative securities by financial institutions, government sponsored entities, and major commercial and investment banks. This has led to decreased confidence in financial markets among borrowers, lenders, and depositors as well as extreme volatility in the capital and credit markets and the failure of some entities in the financial sector. The Company is fortunate that the markets it serves have been impacted to a lesser extent than many areas around the country.

Employees

As of December 31, 2010, the Corporation and its subsidiaries employed 317 persons on a full-time equivalent basis. None of the Corporation's employees are covered by collective bargaining agreements, and the Corporation believes that its relationship with its employees is good.

Financial Information about Foreign and Domestic Operations and Export Sales

Neither the Corporation nor its subsidiaries relies on foreign sources of funds or income.

Statistical Disclosure by Bank Holding Companies

The following disclosures present certain summarized statistical data covering the Corporation and its subsidiaries. See also Management's Discussion and Analysis of Financial Condition and Results of Operations in Part II, Item 7, of this report for other required statistical data.

7

Investment Portfolio

The following table sets forth the carrying amount of available for sale and held to maturity investment securities at the dates indicated (in thousands of dollars):

|

December 31,

|

|||

|

2010

|

2009

|

2008

|

|

|

Obligations of U.S. Government and U.S Government sponsored enterprises

|

$102,132

|

$ 84,621

|

$ 61,543

|

|

Mortgage-backed securities, residential

|

62,762

|

93,945

|

102,933

|

|

Obligations of states and political subdivisions

|

46,480

|

44,284

|

24,859

|

|

Corporate bonds and notes

|

11,694

|

12,185

|

1,750

|

|

Trust preferred securities

|

2,344

|

2,261

|

3,285

|

|

Corporate stocks

|

5,848

|

5,847

|

5,324

|

|

Total

|

$231,260

|

$243,143

|

$199,694

|

Included in the above table are $223,545, $230,984 and $191,255 (in thousands of dollars) of securities available for sale at December 31, 2010, 2009 and 2008, respectively. Also included in the above table are $7,715, $12,160 and $8,439 (in thousands of dollars) of securities held to maturity at December 31, 2010, 2009 and 2008, respectively.

The following table sets forth the carrying amounts and maturities of debt securities at December 31, 2010 and the weighted average yields of such securities (all yields are calculated on the basis of the amortized cost and weighted for the scheduled maturity of each security, except mortgage-backed securities which are based on the average life at the projected prepayment speed of each security). Federal tax equivalent adjustments have not been made in calculating yields on municipal obligations:

|

Maturing

|

||||

|

Dollars in thousands

|

||||

|

Within One Year

|

After One, But Within Five Years

|

|||

|

Amount

|

Yield

|

Amount

|

Yield

|

|

|

Obligations of U.S. Government and U.S Government

sponsored enterprises

|

$35,740

|

1.58%

|

$ 61,097

|

1.39%

|

|

Mortgage-backed securities, residential

|

1,240

|

3.16%

|

58,643

|

4.13%

|

|

Obligations of states and political subdivisions

|

6,570

|

2.41%

|

25,582

|

2.42%

|

|

Corporate bonds and notes

|

513

|

5.28%

|

11,181

|

4.59%

|

|

Trust preferred securities

|

-

|

-

|

-

|

-

|

|

Total

|

$44,063

|

1.79%

|

$156,503

|

2.79%

|

|

Maturing

|

||||

|

Dollars in thousands

|

||||

|

After Five, But

Within Ten Years

|

After Ten Years

|

|||

|

Amount

|

Yield

|

Amount

|

Yield

|

|

|

Obligations of U.S. Government and U.S Government

sponsored enterprises

|

$ 5,295

|

3.75%

|

$ -

|

-

|

|

Mortgage-backed securities, residential

|

477

|

2.16%

|

2,402

|

2.29%

|

|

Obligations of states and political subdivisions

|

14,136

|

3.38%

|

192

|

3.80%

|

|

Corporate bonds and notes

|

-

|

-

|

-

|

-

|

|

Trust preferred securities

|

2,009

|

9.22%

|

335

|

16.10%

|

|

Total

|

$21,917

|

3.96%

|

$ 2,929

|

5.41%

|

8

Loan Portfolio

The following table shows the Corporation's loan distribution at the end of each of the last five years, net of deferred origination fees and costs, and unearned income (in thousands of dollars):

|

December 31,

|

|||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

|

|

Commercial, financial and agricultural

|

$114,892

|

$118,478

|

$122,761

|

$129,533

|

$137,646

|

|

Commercial mortgages

|

133,070

|

123,669

|

92,978

|

72,318

|

55,358

|

|

Residential mortgages

|

172,727

|

162,087

|

156,150

|

159,087

|

133,286

|

|

Indirect consumer loans

|

97,787

|

92,902

|

99,723

|

89,609

|

65,853

|

|

Consumer loans

|

92,573

|

96,467

|

91,137

|

86,572

|

83,733

|

|

Net deferred origination fees and

costs, and unearned income

|

2,635

|

2,250

|

2,436

|

2,403

|

1,788

|

|

Total

|

$613,684

|

$595,853

|

$565,185

|

$539,522

|

$477,664

|

The following table shows the maturity of loans (excluding residential mortgages, indirect consumer, and consumer loans) outstanding as of December 31, 2010. Also provided are the amounts due after one year, classified according to the sensitivity to changes in interest rates (in thousands of dollars):

|

Within One Year

|

After One But Within Five Years

|

After

Five Years

|

Total

|

|

|

Commercial, financial and agricultural

|

$ 53,703

|

$ 57,138

|

$ 137,121

|

$ 247,962

|

|

Loans maturing after one year with:

|

||||

|

Fixed interest rates

|

N/A

|

$ 34,882

|

$ 12,368

|

$ 47,250

|

|

Variable interest rates

|

N/A

|

22,256

|

124,753

|

147,009

|

|

Total

|

N/A

|

$ 57,138

|

$ 137,121

|

$ 194,259

|

Loan Concentrations

The loan portfolio is widely diversified by types of borrowers, industry groups, and market areas within our core footprint. Significant loan concentrations are considered to exist for a financial institution when there are amounts loaned to numerous borrowers engaged in similar activities that would cause them to be similarly impacted by economic or other conditions. At December 31, 2010, 10.4% of the Corporation’s loans consist of commercial real estate loans to borrowers in the real estate, rental or leasing sector. The major portion of this sector comprises borrowers that rent, lease or otherwise allow the use of their own assets by others. No other significant concentrations existed in the Corporation’s portfolio in excess of 10% of total loans as of December 31, 2010.

9

Allocation of the Allowance for Loan Losses

The allocated portions of the allowance reflect management's estimates of specific known risk elements in the respective portfolios. Management's methodology followed in evaluating the allowance for loan losses includes a detailed analysis of historical loss factors for pools of similarly graded loans, as well as specific collateral reviews of relationships graded special mention, substandard or doubtful with outstanding balances of $1.0 million or greater. Among the factors considered in allocating portions of the allowance by loan type are the current levels of past due, non-accrual and impaired loans, as well as historical loss experience and the evaluation of collateral. In addition, management has formally documented factors considered in determining the appropriate level of unallocated allowance, including current economic conditions, forecasted trends in the credit quality cycle, loan growth, entry into new markets, and industry and peer group trends. From 2007 to 2009, these amounts, which had previously been shown as unallocated, have been included in the allocated portion of the loan categories to which they relate. At December 31, 2010, in addition to the qualitative factors allocated within the allowance, the Corporation maintained $776 thousand of the allowance as unallocated. While we have seen some preliminary improvements in the local economy and while some loans have improved, the recovery is still very fragile and management believes it is prudent to see a period of sustained improvement before completely reflecting this in the allowance. Additionally, management monitors coverage ratios of nonperforming loans and total loans compared to peers on a regular basis. This analysis also suggests that it would not be prudent to eliminate the unallocated portion of the allowance at this time.

The following table summarizes the Corporation’s allocation of the loan loss allowance for each year in the five-year period ended December 31, 2010:

|

Amount of loan loss allowance (in thousands) and Percent of Loans

by Category to Total Loans (%)

|

||||||||||

|

Balance at end of period applicable to:

|

2010

|

%

|

2009

|

%

|

2008

|

%

|

2007

|

%

|

2006

|

%

|

|

Commercial, financial and agricultural

|

$2,118

|

18.6

|

$3,133

|

19.9

|

$3,854

|

21.7

|

$3,955

|

24.0

|

$4,122

|

28.8

|

|

Commercial mortgages

|

2,575

|

21.7

|

3,073

|

20.7

|

3,058

|

16.4

|

3,113

|

13.4

|

2,473

|

11.6

|

|

Residential mortgages

|

1,302

|

28.3

|

1,125

|

27.3

|

753

|

27.7

|

479

|

29.6

|

214

|

28.0

|

|

Consumer loans

|

2,727

|

31.4

|

2,636

|

32.1

|

1,441

|

34.2

|

906

|

33.0

|

574

|

31.6

|

|

8,722

|

100.0

|

9,967

|

100.0

|

9,106

|

100.0

|

8,453

|

100.0

|

7,383

|

100.0

|

|

|

Unallocated

|

776

|

N/A

|

-

|

N/A

|

-

|

N/A

|

-

|

N/A

|

600

|

N/A

|

|

Total

|

$9,498

|

100.0

|

$9,967

|

100.0

|

$9,106

|

100.0

|

$8,453

|

100.0

|

$7,983

|

100.0

|

The allocation of the allowance to each category does not restrict the use of the allowance to absorb losses in any category.

10

Deposits

The average daily amounts of deposits and rates paid on such deposits are summarized for the periods indicated in the following table (in thousands of dollars):

|

Year Ended December 31,

|

||||||

|

2010

|

2009

|

2008

|

||||

|

Amount

|

Rate

|

Amount

|

Rate

|

Amount

|

Rate

|

|

|

Non-interest-bearing demand deposits

|

$196,822

|

-%

|

$176,305

|

-%

|

$156,191

|

- %

|

|

Interest-bearing demand deposits

|

52,314

|

0.09%

|

47,250

|

0.17%

|

41,282

|

0.60%

|

|

Savings and insured money market deposits

|

296,492

|

0.32%

|

245,425

|

0.58%

|

195,602

|

1.08%

|

|

Time deposits

|

272,016

|

1.70%

|

283,408

|

2.44%

|

256,661

|

3.57%

|

|

$817,644

|

$752,388

|

$649,736

|

||||

Scheduled maturities of time deposits at December 31, 2010 are summarized as follows (in thousands of dollars):

|

2011

|

$176,436

|

|

2012

|

57,165

|

|

2013

|

11,284

|

|

2014

|

6,274

|

|

2015

|

2,641

|

|

Thereafter

|

4

|

|

$253,804

|

Maturities of time deposits in denominations of $100,000 or more outstanding at December 31, 2010 are summarized as follows (in thousands of dollars):

|

3 months or less

|

$ 21,343

|

|

Over 3 through 6 months

|

12,786

|

|

Over 6 through 12 months

|

21,029

|

|

Over 12 months

|

26,784

|

|

$ 81,942

|

Return on Equity and Assets

The following table shows consolidated operating and capital ratios of the Corporation for each of the last three years:

|

Year Ended December 31,

|

2010

|

2009

|

2008

|

|

Return on average assets

|

1.02%

|

0.56%

|

1.00%

|

|

Return on average equity

|

10.64%

|

6.13%

|

9.36%

|

|

Dividend payout ratio

|

34.85%

|

67.30%

|

42.07%

|

|

Average equity to average assets ratio

|

9.60%

|

9.19%

|

10.65%

|

|

Year-end equity to year-end assets ratio

|

10.16%

|

9.23%

|

9.90%

|

Short-Term Borrowings

For each of the three years ended December 31, 2010, 2009 and 2008, respectively, the average outstanding balance of short-term borrowings did not exceed 30% of shareholders' equity.

Securities Sold Under Agreements to Repurchase and Federal Home Loan Bank ("FHLB") Advances

Information regarding securities sold under agreements to repurchase and FHLB advances is included in notes 8 and 9 to the consolidated financial statements appearing elsewhere in this report.

11

ITEM 1A. RISK FACTORS

The Corporation’s business is subject to many risks and uncertainties. Although the Corporation seeks ways to manage these risks and develop programs to control those that management can, the Corporation ultimately cannot predict the extent to which these risks and uncertainties could affect results. Actual results may differ materially from management's expectations. The material risks and uncertainties that management believes affect the Corporation are discussed below.

Economic conditions may adversely affect the Corporation’s financial performance.

As a consequence of the economic slowdown that the United States experienced, business activity across a wide range of industries continues to face serious difficulties due to reduced consumer spending, the weakened financial condition of some borrowers and employment levels. A continued weakness or further weakening in business and economic conditions generally or specifically in the principal markets in which the Corporation does business could have one or more of the following adverse effects on the Corporation’s business: (i) a decrease in the demand for loans and other products and services; (ii) a decrease in the value of the Corporation’s loans or other assets secured by consumer or commercial real estate; (iii) an impairment of certain of the Corporation’s intangible assets, such as goodwill; and (iv) an increase in the number of borrowers and counterparties who become delinquent, file for protection under bankruptcy laws or default on their loans or other obligations to the Corporation. An increase in the number of delinquencies, bankruptcies or defaults could result in a higher level of nonperforming assets, net charge-offs and provision for loan losses.

Commercial real estate and business loans increase the Corporation’s exposure to credit risks.

At December 31, 2010, the Corporation’s portfolio of commercial real estate and business loans totaled $247.8 million or 40.4% of total loans. The Corporation’s plans are to continue to emphasize the origination of these types of loans, which generally expose the Corporation to a greater risk of nonpayment and loss than residential real estate or consumer loans because repayment of such loans often depends on the successful operations and income stream of the borrower’s business. Additionally, such loans typically involve larger loan balances to single borrowers or groups of related borrowers compared to residential real estate and consumer loans. Also, some of the Corporation’s borrowers have more than one commercial loan outstanding. Consequently, an adverse development with respect to one loan or one credit relationship can expose the Corporation to a significantly greater risk of loss compared to an adverse development with respect to residential real estate and consumer loans. The Corporation targets its business lending and marketing strategy towards small to medium-sized businesses. These small to medium-sized businesses generally have fewer financial resources in terms of capital or borrowing capacity than larger entities. If general economic conditions negatively impact these businesses, the Corporation’s results of operations and financial condition may be adversely affected.

Increases to the allowance for loan losses may cause the Corporation’s earnings to decrease.

The Corporation’s customers may not repay their loans according to the original terms, and the collateral securing the payment of those loans may be insufficient to pay any remaining loan balance. Hence, we may experience significant loan losses, which could have a material adverse effect on our operating results. Management makes various assumptions and judgments about the collectability of its loan portfolio, including the creditworthiness of its borrowers and the value of the real estate and other assets serving as collateral for the repayment of loans. In determining the amount of the allowance for credit losses, management relies on loan quality reviews, past loss experience, and an evaluation of economic conditions, among other factors. If these assumptions prove to be incorrect, the allowance for loan losses may not be sufficient to cover losses inherent in the Corporation’s loan portfolio, resulting in additions to the allowance. Material additions to the allowance would materially decrease net income.

The Corporation’s emphasis on the origination of commercial loans is one of the more significant factors in evaluating its allowance for credit losses. As the Corporation continues to increase the amount of these loans, additional or increased provisions for loan losses may be necessary and as a result could result in a decrease in earnings.

12

Bank regulators periodically review the Corporation’s allowance for loan losses and may require the Corporation to increase its provision for loan losses or loan charge-offs. Any increase in the allowance for loan losses or loan charge-offs as required by these regulatory authorities could have a material adverse effect on our results of operations and/or financial condition.

Changes in interest rates could adversely affect the Corporation’s results of operations and financial condition.

The Corporation’s results of operations and financial condition are significantly affected by changes in interest rates. Our financial results depend substantially on net interest income, which is the difference between the interest income that we earn on interest-earning assets and the interest expense paid on interest-bearing liabilities. If the Corporation’s interest-earning assets mature or reprice more quickly than its interest-bearing liabilities in a given period as a result of decreasing interest rates, net interest income may decrease. Likewise, net interest income may decrease if interest-bearing liabilities mature or reprice more quickly than interest-earning assets in a given period as a result of increasing interest rates. The Corporation has taken steps to mitigate this risk, such as holding fewer longer-term residential mortgages, as well as investing excess funds in shorter-term investments.

Changes in interest rates also affect the fair value of the Corporation’s interest-earning assets and, in particular, its investment securities available for sale. Generally, the fair value of investment securities fluctuates inversely with changes in interest rates. Decreases in the fair value of investment securities available for sale, therefore, could have an adverse effect on our shareholders’ equity or earnings if the decrease in fair value is deemed to be other than temporary.

Changes in interest rates may also affect the average life of loans and mortgage-related securities. Decreases in interest rates can result in increased prepayments of loans and mortgage-related securities, as borrowers refinance to reduce borrowing costs. Under these circumstances, the Corporation is subject to reinvestment risk to the extent that it is unable to reinvest the cash received from such prepayments at rates that are comparable to the rates on its existing loans and securities. Additionally, increases in interest rates may decrease loan demand and make it more difficult for borrowers to repay adjustable rate loans.

Strong competition within our industry and market area could limit the Corporation’s growth and profitability.

The Corporation faces substantial competition in all phases of its operations from a variety of different competitors. Future growth and success will depend on the ability to compete effectively in this highly competitive environment. The Corporation competes for deposits, loans and other financial services with a variety of banks, thrifts, credit unions and other financial institutions as well as other entities which provide financial services. Some of the financial institutions and financial services organizations with which we compete are not subject to the same degree of regulation as the Corporation. Many competitors have been in business for many years, have established customer bases, are larger, and have substantially higher lending limits. The financial services industry is also likely to become more competitive as further technological advances enable more companies to provide financial services. These technological advances may diminish the importance of depository institutions and other financial intermediaries in the transfer of funds between parties.

The Corporation’s growth strategy may not prove to be successful and our market value and profitability may suffer.

As part of the Corporation's strategy for continued growth, we may open additional branches. New branches do not initially contribute to operating profits due to the impact of overhead expenses and the start-up phase of generating loans and deposits. To the extent that additional branches are opened, the Corporation may experience the effects of higher operating expenses relative to operating income from the new operations, which may have an adverse effect on the Corporation's levels of net income, return on average equity and return on average assets.

In addition, the Corporation may acquire banks and related businesses that it believes provide a strategic fit with its business, such as the pending acquisition of Fort Orange Financial Corp. To the extent that the Corporation grows through acquisitions, it cannot provide assurance that such strategic decisions will be accretive to earnings.

13

The Corporation operates in a highly regulated environment and may be adversely affected by changes in laws and regulations.

Currently, the Corporation and its subsidiaries are subject to extensive regulation, supervision, and examination by regulatory authorities. For example, the Corporation is regulated by the Federal Reserve and the Bank is regulated by the Federal Reserve, the Federal Deposit Insurance Corporation (the "FDIC") and the New York State Banking Department. Such regulators govern the activities in which the Corporation and its subsidiaries may engage. These regulatory authorities have extensive discretion in connection with their supervisory and enforcement activities, including the imposition of restrictions on the operation of a bank, the classification of assets by a bank, and the adequacy of a bank’s allowance for loan losses. Any change in such regulation and oversight, whether in the form of regulatory policy, regulations, or legislation, could have a material impact on the Corporation and its operations. The Corporation believes that it is in substantial compliance with applicable federal, state and local laws, rules and regulations. Because our business is highly regulated, the laws, rules and applicable regulations are subject to regular modification and change. There can be no assurance that proposed laws, rules and regulations, or any other law, rule or regulation, will not be adopted in the future, which could make compliance more difficult or expensive or otherwise adversely affect our business, financial condition or prospects.

Recent legislative reforms may result in the Corporation’s business becoming subject to significant and extensive additional regulations and/or can adversely affect the Corporation’s results of operations and financial condition.

On July 21, 2010, the President signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"). This new law will significantly change the current bank regulatory structure and affect the lending, deposit, investment, trading and operating activities of financial institutions and their holding companies. The Dodd-Frank Act requires various federal agencies to adopt a broad range of new rules and regulations, and to prepare various studies and reports for Congress. The federal agencies are given significant discretion in drafting such rules and regulations. With that discretion, market litigation, and continued legislative efforts, many of the details and much of the impact of the Dodd-Frank Act may not be known for months or years.

Certain provisions of the Dodd-Frank Act are expected to have a near term impact on the Corporation. Among other things, these provisions: (i) abolish the Office of Thrift Supervision and transfer its functions to other federal banking agencies; (ii) relax rules regarding interstate branching; (iii) allow financial institutions to pay interest on business checking accounts; (iv) change the scope of federal deposit insurance coverage; and (v) impose new capital requirements on bank holding companies.

It is difficult to predict at this time with specificity the full range of the impact the Dodd-Frank Act and the yet to be written implementing rules and regulations will have on the Corporation. The Dodd-Frank Act substantially increases regulation of the financial services industry and imposes restrictions on the operations and general ability of firms within the industry to conduct business consistent with historical practices. The Corporation will have to apply resources to ensure that it is in compliance with all applicable provisions of the Dodd-Frank Act and any implementing rules, which may increase its costs of operations and adversely impact its earnings.

The Corporation is a holding company and depends on its subsidiaries for dividends, distributions and other payments.

The Corporation is a legal entity separate and distinct from the Bank and other subsidiaries. Its principal source of cash flow, including cash flow to pay dividends to its shareholders, is dividends from the Bank. There are statutory and regulatory limitations on the payment of dividends by the Bank to the Corporation, as well as by the Corporation to its shareholders. Federal Reserve regulations affect the ability of the Bank to pay dividends and other distributions and to make loans to the Corporation. If the Bank is unable to make dividend payments to the Corporation and sufficient capital is not otherwise available, we may not be able to make dividend payments to our common shareholders.

14

The Corporation holds certain intangible assets that could be classified as impaired in the future. If these assets are considered to be either partially or fully impaired in the future, our earnings and the book values of these assets would decrease.

The Corporation is required to test its goodwill and core deposit intangible assets for impairment on a periodic basis. The impairment testing process considers a variety of factors, including the current market price of its common stock, the estimated net present value of its assets and liabilities, and information concerning the terminal valuation of similarly situated insured depository institutions. If an impairment determination is made in a future reporting period, our earnings and the book value of these intangible assets would be reduced by the amount of the impairment. If an impairment loss is recorded, it will have little or no impact on the tangible book value of our common shares or our regulatory capital levels, but such an impairment loss could significantly restrict the Bank from paying a dividend to the Corporation.

The Corporation continually encounters technological change and the failure to understand and adapt to these changes could adversely effect our business.

The banking industry is undergoing rapid technological changes with frequent introductions of new technology-driven products and services. The Corporation's future success will depend, in part, on the ability to address the needs of customers by using technology to provide products and services that will satisfy customer demands for convenience as well as to create additional efficiencies in operations. Many competitors have substantially greater resources to invest in technological improvements. There can be no assurance that the Corporation will be able to effectively implement new technology-driven products and services or be successful in marketing such products and services to customers.

The Corporation is subject to security and operational risks relating to its use of technology.

Despite instituted safeguards, the Corporation cannot be certain that all of its systems are entirely free from vulnerability to attack or other technological difficulties or failures. The Corporation relies on the services of a variety of vendors to meet its data processing and communication needs. If information security is breached or other technology difficulties or failures occur, information may be lost or misappropriated, services and operations may be interrupted and the Corporation could be exposed to claims from customers. Any of these results could have a material adverse effect on the Corporation's business, financial condition, results of operations or liquidity.

Risk factors related to the Corporation’s pending acquisition of Fort Orange Financial Corporation, ("FOFC"), the parent company of Capital Bank & Trust Company ("Capital Bank").

The Corporation may fail to realize the anticipated benefits of the merger.

The success of the merger will depend on, among other things, the Corporation’s ability to realize anticipated cost savings and to combine the businesses of the Bank and Capital Bank in a manner that permits growth opportunities and does not materially disrupt the existing customer relationships of Capital Bank or result in decreased revenues due to loss of customers. If the Corporation is not able to successfully achieve these objectives, the anticipated benefits of the merger may not be realized fully or at all or may take longer to realize than expected.

The Merger Agreement may be terminated in accordance with its terms and the merger may not be completed.

While required regulatory approvals have been received, the Merger Agreement remains subject to a number of conditions which must be fulfilled in order to complete the merger. Those conditions include: (i) approval of the Merger Agreement by FOFC shareholders; (ii) approval of the Merger by the Corporation’s shareholders; (iii) absence of court orders prohibiting the completion of the Merger; (iv) the continued accuracy of the representations and warranties by both parties; (v) the performance by both parties of their covenants and agreements; and (vi) the receipt by both parties of legal opinions from their respective tax counsels.

In addition, certain circumstances exist whereby the Corporation or FOFC may choose to terminate the Merger Agreement. There can be no assurance that the conditions to closing of the merger will be fulfilled or that the merger will be completed.

15

A lawsuit challenging the merger has been filed against FOFC, the FOFC board of directors and the Corporation, and an adverse judgment in this lawsuit or any future similar lawsuits may prevent the merger from becoming effective or from becoming effective within the expected timeframe.

FOFC, the FOFC board of directors and the Corporation have been named as defendants in a purported class action lawsuit in the Supreme Court of the State of New York, County of Albany, challenging the proposed merger and seeking, among other things, to enjoin the defendants from completing the merger on the agreed-upon terms and rescission of the merger to the extent it has been completed. See “Item 3. Legal Proceedings” hereof.

One of the conditions to the closing of the merger is that no order, injunction or decree that enjoins or prohibits the completion of the merger be in effect. If any plaintiff were successful in obtaining an injunction prohibiting the FOFC or the Corporation defendants from completing the merger on the agreed upon terms, then such injunction may prevent the merger from becoming effective or from becoming effective within the expected timeframe.

The pending acquisition of FOFC may distract our management from their other responsibilities.

The pending acquisition of FOFC could cause our management to focus their time and energies on matters related to the acquisition that otherwise would be directed to our business and operations. Management has considered this possibility and is confident that it has the resources necessary to manage this process effectively. Nonetheless, any such distraction on the part of management, if significant, could affect management's ability to service existing business and develop new business and otherwise adversely affect us following the acquisition.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

The Corporation and the Bank currently conduct all their business activities from the Bank's main office in Elmira, NY, 22 full-service branch locations in a seven-county area, owned office space adjacent to the Bank's main office in Elmira, NY and eleven off-site automated teller facilities (ATMs), nine of which are located on leased property. The main office is a six-story structure located at One Chemung Canal Plaza, Elmira, New York, in the downtown business district. The main office consists of approximately 59,342 square feet of space, of which 745 square feet is occupied by the Corporation's subsidiary CFS Group, with the remaining 58,597 square feet entirely occupied by the Bank. The combined square footage of the 23 branch banking facilities totals approximately 110,836 square feet. The office building adjacent to the main office was acquired in 1995 and consists of approximately 33,186 square feet of which 30,766 square feet are occupied by operating departments of the Bank and 2,420 square feet are leased. The leased automated teller facility spaces total approximately 435 square feet. The Bank operates six of its facilities (Bath, Binghamton, Community Corners, Oakdale Mall, Tioga and Vestal Offices) and nine automated teller facilities (four Byrne Dairy Food Stores, Convenient Food Mart, Elmira/Corning Regional Airport, General Revenue Corp., Ithaca College and Quality Beverage) under lease arrangements. The rest of its offices, including the main office and the adjacent office building, are owned by the Bank. All properties owned or leased by the Bank are considered to be in good condition.

The Corporation holds no real estate in its own name.

16

ITEM 3. LEGAL PROCEEDINGS

Following the public announcement on October 15, 2010 of the execution of the merger agreement by and between the Corporation and Fort Orange Financial Corp. (“FOFC”), Allan O. Birkett filed a stockholder class action lawsuit in the Supreme Court of the State of New York, County of Albany, on March 11, 2011 against the Corporation, FOFC and the directors of FOFC challenging the Corporation’s proposed acquisition of FOFC. The lawsuit purports to be brought on behalf of all public stockholders of FOFC and alleges, among other things, that the directors of FOFC breached their fiduciary duties of care, loyalty, good faith and fair dealing by agreeing to the proposed transaction at an unfair price and through an unfair process. The lawsuit further alleges that FOFC and the Corporation aided and abetted the alleged fiduciary duty breaches. The lawsuit seeks, among other things, an order enjoining the defendants from proceeding with or consummating the transaction, rescission in the event the transaction is consummated, damages and attorney’s fees.

The Corporation, FOFC and the directors of FOFC deny any wrongdoing in connection with the merger and intend to vigorously defend the action.

ITEM 4. REMOVED AND RESERVED

PART II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Corporation's stock is traded in the over-the-counter market under the symbol CHMG.OB.

Below are the quarterly market price ranges for the Corporation's stock for the past two years, based upon actual transactions as reported by securities brokerage firms which maintain a market or conduct trades in the Corporation's stock and other transactions known by the Corporation's management.

Market Prices During Past Two Years (dollars)

|

2010

|

2009

|

||

|

1st Quarter

|

$19.65 - $21.40

|

$15.00 - $22.00

|

|

|

2nd Quarter

|

$19.90 - $21.55

|

$17.25 - $23.00

|

|

|

3rd Quarter

|

$20.15 - $22.00

|

$18.75 - $21.25

|

|

|

4th Quarter

|

$20.50 - $24.00

|

$19.55 - $23.00

|

Below are the dividends paid quarterly by the Corporation for each share of the Corporation's common stock over the last two years:

Dividends Paid Per Share During Past Two Years

|

2010

|

2009

|

||

|

January

|

$0.25

|

$0.25

|

|

|

April

|

0.25

|

0.25

|

|

|

July

|

0.25

|

0.25

|

|

|

October

|

0.25

|

0.25

|

|

|

$1.00

|

$1.00

|

17

The Bank is also subject to legal limitations on the amount of dividends that can be paid to the Corporation without prior regulatory approval. Dividends are limited to retained net profits, as defined by regulations, for the current year and the two preceding years. At December 31, 2010, approximately $5.1 million was available for the declaration of dividends from the Bank to the Corporation.

As of February 28, 2011 there were 534 registered holders of record of the Corporation's stock.

The table below sets forth the information with respect to purchases made by the Corporation of our common stock during the quarter ended December 31, 2010:

|

Period

|

Total

number of

shares

purchased

|

Average price

paid per share

|

Total number of shares

purchased as part of

publicly announced

plans or programs

|

Maximum number of

shares that may yet be

purchased under the

plans or programs

|

|

10/1/10-10/31/10

|

-

|

$ -

|

-

|

69,269

|

|

11/1/10-11/18/10

|

-

|

$ -

|

-

|

69,269

|

|

11/19/10-11/30/10 (1)

|

-

|

$ -

|

-

|

69,269

|

|

12/1/10-12/31/10

|

-

|

$ -

|

-

|

69,269

|

|

Quarter ended 12/31/10

|

-

|

$ -

|

-

|

69,269

|

|

(1) On November 17, 2010, the Corporation’s Board of Directors approved a one year extension of the stock repurchase program that had been initially approved on November 18, 2009. The extension authorizes purchases of up to 90,000 shares of the Corporation's outstanding common stock, including those shares purchased during the first year of the plan. Purchases will be made from time to time on the open-market or in private negotiated transactions and will be at the discretion of management.

|

||||

18

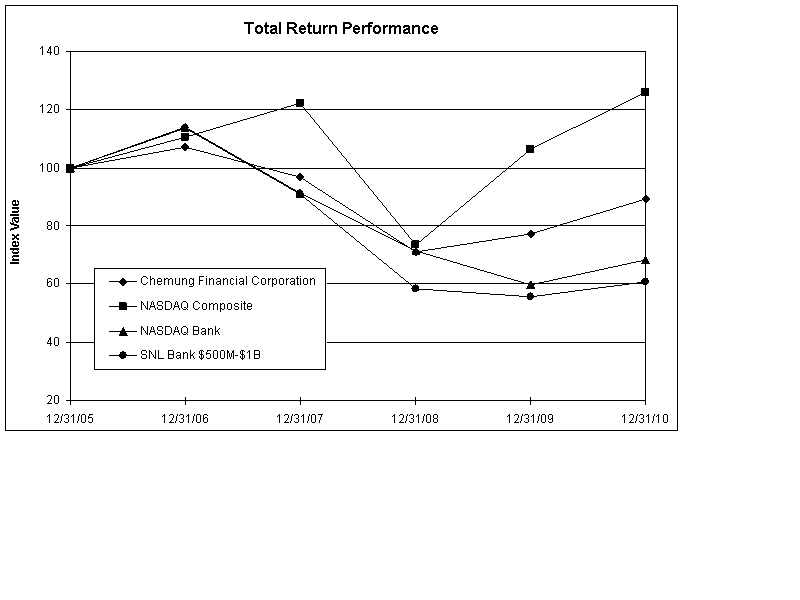

STOCK PERFORMANCE GRAPH

The following graph compares the yearly change in the cumulative total shareholder return on the Corporation’s common stock against the cumulative total return of the NASDAQ Stock Market (U.S. Companies), NASDAQ Bank Stocks Index and SNL $500M - $1B Bank Index for the period of five years commencing December 31, 2005.