BARRICK GOLD CORP0000756894--12-312020Q26-K2020-06-30false————————3———————3,7430000756894iso4217:USD0000756894abx:PorgeraMember2020-04-0100007568942020-01-012020-06-3000007568942020-04-012020-06-3000007568942019-04-012019-06-3000007568942019-01-012019-06-30iso4217:USDxbrli:shares00007568942020-03-3100007568942019-03-3100007568942019-12-3100007568942018-12-3100007568942020-06-3000007568942019-06-30xbrli:shares0000756894ifrs-full:IssuedCapitalMember2019-12-310000756894ifrs-full:RetainedEarningsMember2019-12-310000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2019-12-310000756894ifrs-full:OtherEquityInterestMember2019-12-310000756894ifrs-full:EquityAttributableToOwnersOfParentMember2019-12-310000756894ifrs-full:NoncontrollingInterestsMember2019-12-310000756894ifrs-full:RetainedEarningsMember2020-01-012020-06-300000756894ifrs-full:EquityAttributableToOwnersOfParentMember2020-01-012020-06-300000756894ifrs-full:NoncontrollingInterestsMember2020-01-012020-06-300000756894ifrs-full:IssuedCapitalMember2020-01-012020-06-300000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-06-300000756894ifrs-full:OtherEquityInterestMember2020-01-012020-06-300000756894abx:TanzanianMinesMemberifrs-full:NoncontrollingInterestsMember2020-01-012020-06-300000756894abx:TanzanianMinesMember2020-01-012020-06-300000756894ifrs-full:IssuedCapitalMember2020-06-300000756894ifrs-full:RetainedEarningsMember2020-06-300000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2020-06-300000756894ifrs-full:OtherEquityInterestMember2020-06-300000756894ifrs-full:EquityAttributableToOwnersOfParentMember2020-06-300000756894ifrs-full:NoncontrollingInterestsMember2020-06-300000756894ifrs-full:IssuedCapitalMember2018-12-310000756894ifrs-full:RetainedEarningsMember2018-12-310000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2018-12-310000756894ifrs-full:OtherEquityInterestMember2018-12-310000756894ifrs-full:EquityAttributableToOwnersOfParentMember2018-12-310000756894ifrs-full:NoncontrollingInterestsMember2018-12-310000756894ifrs-full:RetainedEarningsMember2019-01-012019-06-300000756894ifrs-full:EquityAttributableToOwnersOfParentMember2019-01-012019-06-300000756894ifrs-full:NoncontrollingInterestsMember2019-01-012019-06-300000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-06-300000756894abx:RandgoldCorporationMemberifrs-full:IssuedCapitalMember2019-01-012019-06-300000756894ifrs-full:EquityAttributableToOwnersOfParentMemberabx:RandgoldCorporationMember2019-01-012019-06-300000756894abx:RandgoldCorporationMemberifrs-full:NoncontrollingInterestsMember2019-01-012019-06-300000756894abx:RandgoldCorporationMember2019-01-012019-06-300000756894ifrs-full:IssuedCapitalMember2019-01-012019-06-300000756894ifrs-full:OtherEquityInterestMember2019-01-012019-06-300000756894ifrs-full:IssuedCapitalMember2019-06-300000756894ifrs-full:RetainedEarningsMember2019-06-300000756894ifrs-full:AccumulatedOtherComprehensiveIncomeMember2019-06-300000756894ifrs-full:OtherEquityInterestMember2019-06-300000756894ifrs-full:EquityAttributableToOwnersOfParentMember2019-06-300000756894ifrs-full:NoncontrollingInterestsMember2019-06-300000756894ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2020-06-300000756894ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2019-06-300000756894ifrs-full:AdditionalPaidinCapitalMember2020-06-300000756894ifrs-full:AdditionalPaidinCapitalMember2019-12-310000756894ifrs-full:AdditionalPaidinCapitalMember2019-06-300000756894ifrs-full:ProvisionForDecommissioningRestorationAndRehabilitationCostsMember2020-04-012020-06-300000756894ifrs-full:ProvisionForDecommissioningRestorationAndRehabilitationCostsMember2019-04-012019-06-300000756894ifrs-full:ProvisionForDecommissioningRestorationAndRehabilitationCostsMember2020-01-012020-06-300000756894ifrs-full:ProvisionForDecommissioningRestorationAndRehabilitationCostsMember2019-01-012019-06-300000756894country:CLabx:PascuaLamaMember2020-06-300000756894country:CLabx:PascuaLamaMember2019-12-310000756894abx:PascuaLamaMembercountry:AR2020-06-300000756894abx:PascuaLamaMembercountry:AR2019-12-31xbrli:pure0000756894abx:MassawaMember2020-03-042020-03-040000756894abx:MassawaMember2020-03-040000756894abx:CashAndCashEquivalents1Memberabx:MassawaMember2020-03-042020-03-040000756894abx:TerangaGoldCorporationMemberabx:MassawaMember2020-03-040000756894abx:ContingentPaymentMemberabx:MassawaMember2020-03-042020-03-040000756894abx:ContingentPaymentMemberifrs-full:AtFairValueMemberabx:MassawaMember2020-03-042020-03-040000756894abx:MassawaMember2020-01-012020-03-31abx:minesite0000756894abx:ConsolidatedtotalMember2019-06-30abx:investment0000756894ifrs-full:OperatingSegmentsMember2019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:CarlinMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:Cortez1Member2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:TurquoiseRidgeMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PuebloViejoMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:LouloGounkotoMember2020-04-012020-06-300000756894abx:KibaliMemberifrs-full:OperatingSegmentsMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:VeladeroMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PorgeraMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:NorthMara1Member2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberifrs-full:AllOtherSegmentsMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMember2020-04-012020-06-300000756894abx:KibaliMemberifrs-full:InvestmentsAccountedForUsingEquityMethodMember2020-04-012020-06-300000756894abx:ConsolidatedtotalMember2020-04-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:CarlinMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:Cortez1Member2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:TurquoiseRidgeMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PuebloViejoMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:LouloGounkotoMember2019-04-012019-06-300000756894abx:KibaliMemberifrs-full:OperatingSegmentsMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:VeladeroMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PorgeraMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:NorthMara1Member2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberifrs-full:AllOtherSegmentsMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMember2019-04-012019-06-300000756894abx:KibaliMemberifrs-full:InvestmentsAccountedForUsingEquityMethodMember2019-04-012019-06-300000756894abx:ConsolidatedtotalMember2019-04-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:CarlinMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:Cortez1Member2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:TurquoiseRidgeMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PuebloViejoMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:LouloGounkotoMember2020-01-012020-06-300000756894abx:KibaliMemberifrs-full:OperatingSegmentsMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:VeladeroMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PorgeraMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:NorthMara1Member2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberifrs-full:AllOtherSegmentsMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMember2020-01-012020-06-300000756894abx:KibaliMemberifrs-full:InvestmentsAccountedForUsingEquityMethodMember2020-01-012020-06-300000756894abx:ConsolidatedtotalMember2020-01-012020-06-300000756894ifrs-full:OperatingSegmentsMemberabx:CarlinMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:Cortez1Member2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:TurquoiseRidgeMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PuebloViejoMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:LouloGounkotoMember2019-01-012019-06-300000756894abx:KibaliMemberifrs-full:OperatingSegmentsMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:VeladeroMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:PorgeraMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberabx:NorthMara1Member2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMemberifrs-full:AllOtherSegmentsMember2019-01-012019-06-300000756894ifrs-full:OperatingSegmentsMember2019-01-012019-06-300000756894abx:KibaliMemberifrs-full:InvestmentsAccountedForUsingEquityMethodMember2019-01-012019-06-300000756894abx:ConsolidatedtotalMember2019-01-012019-06-300000756894abx:NevadaGoldMinesMember2020-04-012020-06-300000756894abx:PuebloViejoMember2020-04-012020-06-300000756894abx:PuebloViejoMember2019-04-012019-06-300000756894abx:LouloGounkotoMember2020-04-012020-06-300000756894abx:LouloGounkotoMember2019-04-012019-06-300000756894abx:TanzanianMinesMember2020-04-012020-06-300000756894abx:TanzanianMinesMember2019-04-012019-06-300000756894abx:TongonMember2020-04-012020-06-300000756894abx:TongonMember2019-04-012019-06-300000756894abx:NevadaGoldMinesMember2020-01-012020-06-300000756894abx:PuebloViejoMember2020-01-012020-06-300000756894abx:PuebloViejoMember2019-01-012019-06-300000756894abx:LouloGounkotoMember2020-01-012020-06-300000756894abx:LouloGounkotoMember2019-01-012019-06-300000756894abx:TanzanianMinesMember2020-01-012020-06-300000756894abx:TanzanianMinesMember2019-01-012019-06-300000756894abx:TongonMember2020-01-012020-06-300000756894abx:TongonMember2019-01-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMember2020-04-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMember2019-04-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMember2020-01-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMember2019-01-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:TanzanianMinesMember2020-04-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:TanzanianMinesMember2019-04-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:NevadaGoldMinesMember2020-04-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:NevadaGoldMinesMember2019-04-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:TanzanianMinesMember2020-01-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:TanzanianMinesMember2019-01-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:NevadaGoldMinesMember2020-01-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberabx:NevadaGoldMinesMember2019-01-012019-06-300000756894ifrs-full:UnallocatedAmountsMember2020-04-012020-06-300000756894ifrs-full:UnallocatedAmountsMember2019-04-012019-06-300000756894ifrs-full:UnallocatedAmountsMember2020-01-012020-06-300000756894ifrs-full:UnallocatedAmountsMember2019-01-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberifrs-full:AllOtherSegmentsMember2020-04-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberifrs-full:AllOtherSegmentsMember2019-04-012019-06-300000756894ifrs-full:MaterialReconcilingItemsMemberifrs-full:AllOtherSegmentsMember2020-01-012020-06-300000756894ifrs-full:MaterialReconcilingItemsMemberifrs-full:AllOtherSegmentsMember2019-01-012019-06-300000756894ifrs-full:AllOtherSegmentsMember2020-04-012020-06-300000756894ifrs-full:AllOtherSegmentsMember2019-04-012019-06-300000756894ifrs-full:AllOtherSegmentsMember2020-01-012020-06-300000756894ifrs-full:AllOtherSegmentsMember2019-01-012019-06-300000756894abx:SpotMarketGoldMember2020-04-012020-06-300000756894abx:SpotMarketGoldMember2019-04-012019-06-300000756894abx:SpotMarketGoldMember2020-01-012020-06-300000756894abx:SpotMarketGoldMember2019-01-012019-06-300000756894abx:GoldConcentrateMember2020-04-012020-06-300000756894abx:GoldConcentrateMember2019-04-012019-06-300000756894abx:GoldConcentrateMember2020-01-012020-06-300000756894abx:GoldConcentrateMember2019-01-012019-06-300000756894abx:GoldProvisionalPricingAdjustmentsMember2020-04-012020-06-300000756894abx:GoldProvisionalPricingAdjustmentsMember2019-04-012019-06-300000756894abx:GoldProvisionalPricingAdjustmentsMember2020-01-012020-06-300000756894abx:GoldProvisionalPricingAdjustmentsMember2019-01-012019-06-300000756894abx:GoldMember2020-04-012020-06-300000756894abx:GoldMember2019-04-012019-06-300000756894abx:GoldMember2020-01-012020-06-300000756894abx:GoldMember2019-01-012019-06-300000756894abx:CopperconcentrateMember2020-04-012020-06-300000756894abx:CopperconcentrateMember2019-04-012019-06-300000756894abx:CopperconcentrateMember2020-01-012020-06-300000756894abx:CopperconcentrateMember2019-01-012019-06-300000756894abx:CopperProvisionalPricingAdjustmentsMember2020-04-012020-06-300000756894abx:CopperProvisionalPricingAdjustmentsMember2019-04-012019-06-300000756894abx:CopperProvisionalPricingAdjustmentsMember2020-01-012020-06-300000756894abx:CopperProvisionalPricingAdjustmentsMember2019-01-012019-06-300000756894abx:CopperMember2020-04-012020-06-300000756894abx:CopperMember2019-04-012019-06-300000756894abx:CopperMember2020-01-012020-06-300000756894abx:CopperMember2019-01-012019-06-300000756894abx:OtherProductsMember2020-04-012020-06-300000756894abx:OtherProductsMember2019-04-012019-06-300000756894abx:OtherProductsMember2020-01-012020-06-300000756894abx:OtherProductsMember2019-01-012019-06-300000756894abx:SilverMember2020-04-012020-06-300000756894abx:SilverMember2019-04-012019-06-300000756894abx:SilverMember2020-01-012020-06-300000756894abx:SilverMember2019-01-012019-06-300000756894ifrs-full:NoncurrentAssetsOrDisposalGroupsClassifiedAsHeldForSaleMember2020-04-012020-06-300000756894ifrs-full:NoncurrentAssetsOrDisposalGroupsClassifiedAsHeldForSaleMember2019-04-012019-06-300000756894ifrs-full:NoncurrentAssetsOrDisposalGroupsClassifiedAsHeldForSaleMember2020-01-012020-06-300000756894ifrs-full:NoncurrentAssetsOrDisposalGroupsClassifiedAsHeldForSaleMember2019-01-012019-06-300000756894ifrs-full:IntangibleAssetsOtherThanGoodwillMember2020-04-012020-06-300000756894ifrs-full:IntangibleAssetsOtherThanGoodwillMember2019-04-012019-06-300000756894ifrs-full:IntangibleAssetsOtherThanGoodwillMember2020-01-012020-06-300000756894ifrs-full:IntangibleAssetsOtherThanGoodwillMember2019-01-012019-06-300000756894country:MLcountry:AR2020-01-012020-06-300000756894country:AR2017-01-012017-12-310000756894country:AR2019-01-012019-12-310000756894country:AR2018-01-012018-12-310000756894country:AR2020-01-012020-06-300000756894country:TZ2020-01-012020-03-310000756894country:TZ2020-04-012020-06-300000756894abx:KibaliMember2018-12-310000756894abx:JabalSayidMember2018-12-310000756894abx:ZaldivarMember2018-12-310000756894abx:OtherJVMember2018-12-310000756894ifrs-full:JointVenturesMember2018-12-310000756894abx:KibaliMember2019-01-012019-12-310000756894abx:JabalSayidMember2019-01-012019-12-310000756894abx:ZaldivarMember2019-01-012019-12-310000756894abx:OtherJVMember2019-01-012019-12-310000756894ifrs-full:JointVenturesMember2019-01-012019-12-310000756894abx:KibaliMember2019-12-310000756894abx:JabalSayidMember2019-12-310000756894abx:ZaldivarMember2019-12-310000756894abx:OtherJVMember2019-12-310000756894ifrs-full:JointVenturesMember2019-12-310000756894abx:KibaliMember2020-01-012020-06-300000756894abx:JabalSayidMember2020-01-012020-06-300000756894abx:ZaldivarMember2020-01-012020-06-300000756894abx:OtherJVMember2020-01-012020-06-300000756894ifrs-full:JointVenturesMember2020-01-012020-06-300000756894abx:KibaliMember2020-06-300000756894abx:JabalSayidMember2020-06-300000756894abx:ZaldivarMember2020-06-300000756894abx:OtherJVMember2020-06-300000756894ifrs-full:JointVenturesMember2020-06-300000756894abx:PorgeraMember2020-04-012020-06-300000756894abx:PorgeraMember2020-06-300000756894abx:TanzanianMinesMember2020-01-012020-03-310000756894abx:TanzanianMinesMemberabx:ShortTermMember2020-01-012020-03-310000756894abx:TanzanianMinesMemberabx:LongTermMember2020-01-012020-03-310000756894srt:MinimumMemberabx:TanzanianMinesMember2020-01-012020-03-310000756894srt:MaximumMemberabx:TanzanianMinesMember2020-01-012020-03-310000756894ifrs-full:IndividualAssetsOrCashgeneratingUnitsMemberabx:BulyanhuluMember2020-01-012020-03-310000756894ifrs-full:IndividualAssetsOrCashgeneratingUnitsMemberabx:NorthMara1Member2020-01-012020-03-310000756894ifrs-full:IndividualAssetsOrCashgeneratingUnitsMemberabx:BulyanhuluMember2020-03-310000756894ifrs-full:IndividualAssetsOrCashgeneratingUnitsMemberabx:NorthMara1Member2020-03-310000756894abx:ThreePointEightFivePercentBGCNotesDue2022Member2020-01-312020-01-310000756894abx:ThreePointEightFivePercentBGCNotesDue2022Member2020-01-310000756894abx:AcaciaCreditFacilityMember2020-01-012020-01-310000756894abx:CashAndCashEquivalents1Memberifrs-full:Level1OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:CashAndCashEquivalents1Memberifrs-full:Level2OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level3OfFairValueHierarchyMemberabx:CashAndCashEquivalents1Memberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:CashAndCashEquivalents1Memberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:OtherinvestmentsMemberifrs-full:Level1OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level2OfFairValueHierarchyMemberabx:OtherinvestmentsMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level3OfFairValueHierarchyMemberabx:OtherinvestmentsMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:OtherinvestmentsMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:DerivativesMemberifrs-full:Level1OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:DerivativesMemberifrs-full:Level2OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:DerivativesMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:DerivativesMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:ReceivablesfromprovisionalcopperandgoldsalesMemberifrs-full:Level1OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:ReceivablesfromprovisionalcopperandgoldsalesMemberifrs-full:Level2OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level3OfFairValueHierarchyMemberabx:ReceivablesfromprovisionalcopperandgoldsalesMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:ReceivablesfromprovisionalcopperandgoldsalesMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level1OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level2OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:OtherAssetsMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894ifrs-full:OtherAssetsMemberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894ifrs-full:OtherAssetsMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894ifrs-full:OtherAssetsMemberifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894abx:OtherinvestmentsMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894abx:OtherinvestmentsMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894abx:OtherinvestmentsMemberifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894ifrs-full:DerivativesMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894ifrs-full:DerivativesMemberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894ifrs-full:DerivativesMemberifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894ifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894ifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894ifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894abx:Borrowings1Memberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894abx:Borrowings1Memberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:Borrowings1Memberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894abx:Borrowings1Memberifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894ifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMemberifrs-full:DerivativesMember2020-06-300000756894ifrs-full:RecurringFairValueMeasurementMemberifrs-full:DerivativesMember2020-06-300000756894ifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMemberifrs-full:DerivativesMember2019-12-310000756894ifrs-full:RecurringFairValueMeasurementMemberifrs-full:DerivativesMember2019-12-310000756894abx:OtherLiabilities1Memberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2020-06-300000756894abx:OtherLiabilities1Memberifrs-full:RecurringFairValueMeasurementMember2020-06-300000756894abx:OtherLiabilities1Memberifrs-full:NotMeasuredAtFairValueInStatementOfFinancialPositionButForWhichFairValueIsDisclosedMember2019-12-310000756894abx:OtherLiabilities1Memberifrs-full:RecurringFairValueMeasurementMember2019-12-310000756894ifrs-full:OrdinarySharesMember2020-06-300000756894ifrs-full:LegalProceedingsContingentLiabilityMemberabx:PascuaLamaMemberabx:CanadianSecuritiesClassActionsMember2020-06-300000756894ifrs-full:TaxContingentLiabilityMemberabx:TaxAssessmentAndCriminalChargesMemberabx:VeladeroMember2020-06-300000756894ifrs-full:LegalProceedingsContingentLiabilityMemberabx:MarcopperMinesMemberabx:WritOfKalikasanMember2020-06-300000756894abx:TanzanianMinesMember2020-01-012020-06-300000756894abx:MassawaMember2020-05-070000756894abx:TaxDisputeMemberifrs-full:TaxContingentLiabilityMemberabx:MassawaMember2020-06-30

MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

QUARTERLY REPORT ON THE SECOND QUARTER OF 2020

This portion of the Quarterly Report provides management’s discussion and analysis (“MD&A”) of the financial condition and results of operations, to enable a reader to assess material changes in financial condition and results of operations as at, and for the three and six month periods ended June 30, 2020, in comparison to the corresponding prior-year periods. The MD&A is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial performance and present and future business environment. This MD&A, which has been prepared as of August 7, 2020, is intended to supplement and complement the condensed unaudited interim consolidated financial statements and notes thereto, prepared in accordance with International Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), for the three and six month periods ended June 30, 2020 (collectively, the “Financial Statements”), which are included in this Quarterly Report on pages 112 to 128. You are encouraged to review the Financial Statements in conjunction with your review of this MD&A. This MD&A should be read in conjunction with both the annual audited consolidated financial statements for the two years ended December 31, 2019, the related

annual MD&A included in the 2019 Annual Report, and the most recent Form 40–F/Annual Information Form on file with the U.S. Securities and Exchange Commission (“SEC”) and Canadian provincial securities regulatory authorities. These documents and additional information relating to the Company are available on SEDAR at www.sedar.com and EDGAR at www.sec.gov. Certain notes to the Financial Statements are specifically referred to in this MD&A and such notes are incorporated by reference herein. All dollar amounts in this MD&A are in millions of United States dollars (“$” or “US$”), unless otherwise specified.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this MD&A, including any information as to our strategy, projects, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “believe”, “expect”, “anticipate”, “target”, “plan”, “objective”, “assume”, “intend”, “project”, “pursue”, “goal”, “continue”, “budget”, “estimate”, “potential”, “may”, “will”, “can”, “could”, “would”, “should” and similar expressions identify forward-looking statements. In particular, this MD&A contains forward-looking statements including, without limitation, with respect to: Barrick’s forward-looking production guidance; estimates of future cost of sales per ounce for gold and per pound for copper, total cash costs per ounce and C1 cash costs per pound, and all-in-sustaining costs per ounce/pound; cash flow forecasts; projected capital, operating and exploration expenditures; mine life and production rates; Barrick’s engagement with local communities to manage the Covid-19 pandemic; estimated timing for construction of, and production from, new projects, including the Goldrush twin exploration declines and the Veladero Phase 6 leach pad expansion; timing of completion of a final feasibility study for Goldrush and approval of the plan of operations; the potential for plant expansion at Pueblo Viejo to increase throughput; potential benefits of the chloride leach project at Zaldívar and the power transmission project at Veladero; the partnership between Barrick and the Government of Tanzania ("GoT") and the agreement to resolve all outstanding disputes between Acacia and the GoT; Barrick and Barrick Niugini Limited’s (“BNL”) response to the government of Papua New Guinea’s decision not to extend

Porgera’s special mining lease and to the Internal Revenue Commission’s proposed tax adjustments; the duration of the temporary suspension of operations at Porgera; our pipeline of high confidence projects at or near existing operations; potential mineralization and metal or mineral recoveries; our ability to convert resources into reserves; asset sales, joint ventures and partnerships; Barrick’s strategy, plans, targets and goals in respect of environmental and social governance issues; and expectations regarding future price assumptions, financial performance and other outlook or guidance.

Forward-looking statements are necessarily based upon a number of estimates and assumptions including material estimates and assumptions related to the factors set forth below that, while considered reasonable by the Company as at the date of this MD&A in light of management’s experience and perception of current conditions and expected developments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements and undue reliance should not be placed on such statements and information. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper or certain other commodities (such as silver, diesel fuel, natural gas and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation and exploration successes; risks associated with projects in the early stages of evaluation and for which additional engineering and other analysis is

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

21 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

required; the benefits expected from recent transactions being realized, including Nevada Gold Mines; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; non-renewal of key licenses by governmental authorities, including non-renewal of Porgera’s Special Mining Lease; timing of receipt of, or failure to comply with, necessary permits and approvals; uncertainty whether some or all of Barrick's targeted investments and projects will meet the Company’s capital allocation objectives and internal hurdle rate; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations and/or changes in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company or its affiliates do or may carry on business in the future; lack of certainty with respect to foreign legal systems, corruption and other factors that are inconsistent with the rule of law; risks associated with illegal and artisanal mining; risks associated with new diseases, epidemics and pandemics, including the effects and potential effects of the global Covid-19 pandemic; disruption of supply routes which may cause delays in construction and mining activities; damage to the Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not; the possibility that future exploration results will not be consistent with the Company’s expectations; risks that exploration data may be incomplete and considerable additional work may be required to complete further evaluation, including but not limited to

drilling, engineering and socioeconomic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation and legal and administrative proceedings; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; our ability to successfully integrate acquisitions or complete divestitures, including our ability to successfully reintegrate Acacia’s operations; risks associated with working with partners in jointly controlled assets; employee relations including loss of key employees; increased costs and physical risks, including extreme weather events and resource shortages, related to climate change; and availability and increased costs associated with mining inputs and labor. Barrick also cautions that its 2020 guidance may be impacted by the unprecedented business and social disruption caused by the spread of Covid-19. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks).

Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward-looking statements and the risks that may affect Barrick’s ability to achieve the expectations set forth in the forward-looking statements contained in this MD&A. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

22 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

USE OF NON-GAAP FINANCIAL PERFORMANCE MEASURES

We use the following non-GAAP financial performance measures in our MD&A:

•"adjusted net earnings"

•"free cash flow"

•"EBITDA"

•"adjusted EBITDA"

•"total cash costs per ounce"

•"C1 cash costs per pound"

•"all-in sustaining costs per ounce/pound"

•"all-in costs per ounce" and

•"realized price"

For a detailed description of each of the non-GAAP financial performance measures used in this MD&A and a detailed reconciliation to the most directly comparable measure under International Financial Reporting Standards (“IFRS”), please refer to the Non-GAAP Financial Performance Measures section of this MD&A on pages 79 to 103. Each non-GAAP financial performance measure has been annotated with a reference to an endnote on page 104. The non-GAAP financial performance measures set out in this MD&A are intended to provide additional information to investors and do not have any standardized meaning under IFRS, and therefore may not be comparable to other issuers, and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

|

|

|

|

|

|

| |

|

| INDEX |

page |

| |

|

| Overview |

|

| |

|

| Financial and Operating Highlights |

|

| Key Business Developments |

|

| Environmental and Social Governance |

|

| Outlook |

|

| Production and Cost Summary |

|

|

|

| Operating Divisions Performance |

|

|

|

| Nevada Gold Mines |

|

| Carlin |

|

| Cortez |

|

| Turquoise Ridge |

|

| Other Mines - Nevada Gold Mines |

|

| Pueblo Viejo |

|

| Loulo-Gounkoto |

|

| Kibali |

|

| Veladero |

|

| Porgera |

|

| North Mara |

|

| Other Mines - Gold |

|

| Other Mines - Copper |

|

| Growth Projects |

|

| Exploration and Mineral Resource Management |

|

|

|

| Review of Financial Results |

|

| |

|

| Revenue |

|

| Production Costs |

|

| Capital Expenditures |

|

| General and Administrative Expenses |

|

| Exploration, Evaluation and Project Expenses |

|

| Finance Costs, Net |

|

| Additional Significant Statement of Income Items |

|

| Income Tax Expense |

|

| |

|

| Financial Condition Review |

|

| |

|

| Balance Sheet Review |

|

| Shareholders’ Equity |

|

| Financial Position and Liquidity |

|

| Summary of Cash Inflow (Outflow) |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Commitments and Contingencies |

|

| |

|

| Review of Quarterly Results |

|

| |

|

Internal Control over Financial Reporting and

Disclosure Controls and Procedures |

|

| |

|

| IFRS Critical Accounting Policies and Accounting Estimates |

|

| |

|

| Non-GAAP Financial Performance Measures |

|

| |

|

| Technical Information |

|

| |

|

| Endnotes |

|

|

|

| Financial Statements |

|

|

|

| Notes to Consolidated Financial Statements |

|

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

23 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

OVERVIEW

Financial and Operating Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the three months ended |

|

|

|

|

For the six months ended |

|

|

| |

6/30/20 |

3/31/20 |

% Change |

6/30/19 |

% Change |

6/30/20 |

6/30/19 |

% Change |

Financial Results ($ millions) |

|

|

|

|

|

|

|

|

| Revenues |

3,055 |

|

2,721 |

|

12 |

% |

2,063 |

|

48 |

% |

5,776 |

|

4,156 |

|

39 |

% |

| Cost of sales |

1,900 |

|

1,776 |

|

7 |

% |

1,545 |

|

23 |

% |

3,676 |

|

3,035 |

|

21 |

% |

Net earningsa |

357 |

|

400 |

|

(11) |

% |

194 |

|

84 |

% |

757 |

|

305 |

|

148 |

% |

Adjusted net earningsb |

415 |

|

285 |

|

46 |

% |

154 |

|

169 |

% |

700 |

|

338 |

|

107 |

% |

Adjusted EBITDAb |

1,697 |

|

1,466 |

|

16 |

% |

972 |

|

75 |

% |

3,163 |

|

1,974 |

|

60 |

% |

Adjusted EBITDA marginb,c |

56 |

% |

54 |

% |

4 |

% |

47 |

% |

19 |

% |

55 |

% |

47 |

% |

17 |

% |

Minesite sustaining capital expendituresd |

420 |

|

370 |

|

14 |

% |

267 |

|

57 |

% |

790 |

|

520 |

|

52 |

% |

Project capital expendituresd |

85 |

|

76 |

|

12 |

% |

108 |

|

(21) |

% |

161 |

|

228 |

|

(29) |

% |

Total consolidated capital expendituresd,e |

509 |

|

451 |

|

13 |

% |

379 |

|

34 |

% |

960 |

|

753 |

|

27 |

% |

| Net cash provided by operating activities |

1,031 |

|

889 |

|

16 |

% |

434 |

|

138 |

% |

1,920 |

|

954 |

|

101 |

% |

Net cash provided by operating activities marginf |

34 |

% |

33 |

% |

3 |

% |

21 |

% |

62 |

% |

33 |

% |

23 |

% |

43 |

% |

Free cash flowb |

522 |

|

438 |

|

19 |

% |

55 |

|

849 |

% |

960 |

|

201 |

|

378 |

% |

|

|

|

|

|

|

|

|

|

| Net earnings per share (basic and diluted) |

0.20 |

|

0.22 |

|

(9) |

% |

0.11 |

|

82 |

% |

0.43 |

|

0.17 |

|

153 |

% |

Adjusted net earnings (basic)b per share |

0.23 |

|

0.16 |

|

44 |

% |

0.09 |

|

156 |

% |

0.39 |

|

0.19 |

|

105 |

% |

| Weighted average diluted common shares (millions of shares) |

1,778 |

|

1,778 |

|

0 |

% |

1,752 |

|

1 |

% |

1,778 |

|

1,749 |

|

2 |

% |

| Operating Results |

|

|

|

|

|

|

|

|

Gold production (thousands of ounces)g |

1,149 |

|

1,250 |

|

(8) |

% |

1,353 |

|

(15) |

% |

2,399 |

|

2,720 |

|

(12) |

% |

Gold sold (thousands of ounces)g |

1,224 |

|

1,220 |

|

0 |

% |

1,372 |

|

(11) |

% |

2,444 |

|

2,737 |

|

(11) |

% |

|

|

|

|

|

|

|

|

|

| Market gold price ($/oz) |

1,711 |

|

1,583 |

|

8 |

% |

1,309 |

|

31 |

% |

1,645 |

|

1,307 |

|

26 |

% |

Realized gold priceb,g ($/oz) |

1,725 |

|

1,589 |

|

9 |

% |

1,317 |

|

31 |

% |

1,657 |

|

1,312 |

|

26 |

% |

Gold cost of sales (Barrick’s share)g,h ($/oz) |

1,075 |

|

1,020 |

|

5 |

% |

964 |

|

12 |

% |

1,048 |

|

956 |

|

10 |

% |

Gold total cash costsb,g ($/oz) |

716 |

|

692 |

|

3 |

% |

651 |

|

10 |

% |

704 |

|

641 |

|

10 |

% |

Gold all-in sustaining costsb,g ($/oz) |

1,031 |

|

954 |

|

8 |

% |

869 |

|

19 |

% |

993 |

|

842 |

|

18 |

% |

Copper production (millions of pounds)i |

120 |

|

115 |

|

4 |

% |

97 |

|

24 |

% |

235 |

|

203 |

|

16 |

% |

Copper sold (millions of pounds)i |

123 |

|

110 |

|

12 |

% |

96 |

|

28 |

% |

233 |

|

199 |

|

17 |

% |

|

|

|

|

|

|

|

|

|

| Market copper price ($/lb) |

2.43 |

|

2.56 |

|

(5) |

% |

2.77 |

|

(12) |

% |

2.49 |

|

2.80 |

|

(11) |

% |

Realized copper priceb,i ($/lb) |

2.79 |

|

2.23 |

|

25 |

% |

2.62 |

|

6 |

% |

2.53 |

|

2.85 |

|

(11) |

% |

Copper cost of sales (Barrick’s share)i,j ($/lb) |

2.08 |

|

1.96 |

|

6 |

% |

2.04 |

|

2 |

% |

2.03 |

|

2.13 |

|

(5) |

% |

Copper C1 cash costsb,i ($/lb) |

1.55 |

|

1.55 |

|

0 |

% |

1.59 |

|

(3) |

% |

1.55 |

|

1.62 |

|

(4) |

% |

Copper all-in sustaining costsb,i ($/lb) |

2.15 |

|

2.04 |

|

5 |

% |

2.28 |

|

(6) |

% |

2.10 |

|

2.37 |

|

(11) |

% |

|

|

|

|

|

|

|

|

|

| |

As at 6/30/20 |

As at 3/31/20 |

% Change |

As at 6/30/19 |

% Change |

|

|

|

Financial Position ($ millions) |

|

|

|

|

|

|

|

|

| Debt (current and long-term) |

5,168 |

|

5,179 |

|

0 |

% |

5,807 |

|

(11) |

% |

|

|

|

| Cash and equivalents |

3,743 |

|

3,327 |

|

13 |

% |

2,153 |

|

74 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Debt, net of cash |

1,425 |

|

1,852 |

|

(23) |

% |

3,654 |

|

(61) |

% |

|

|

|

a.Net earnings represents net earnings attributable to the equity holders of the Company.

b.Adjusted net earnings, adjusted EBITDA, adjusted EBITDA margin, free cash flow, adjusted net earnings per share, realized gold price, all-in sustaining costs, total cash costs, C1 cash costs and realized copper price are non-GAAP financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-GAAP measure to the most directly comparable IFRS measure, please see pages 79 to 103 of this MD&A.

c.Represents adjusted EBITDA divided by revenue.

d.Amounts presented on a consolidated cash basis. Project capital expenditures are included in our calculation of all-in costs, but not included in our calculation of all-in sustaining costs.

e.Total consolidated capital expenditures also includes capitalized interest.

f.Represents net cash provided by operating activities divided by revenue.

g.Includes North Mara, Bulyanhulu and Buzwagi on a 84% basis starting January 1, 2020 (and on a 63.9% basis from January 1, 2019 to September 30, 2019; notwithstanding the completion of the Acacia transaction on September 17, 2019, we consolidated our interest in Acacia and recorded a non-controlling interest of 36.1% in the income statement for the entirety of the third quarter of 2019 as a matter of convenience, and on a 100% basis from October 1, 2019 to December 31, 2019), Pueblo Viejo on a 60% basis, South Arturo on a 36.9% basis from July 1, 2019 onwards as a result of its contribution to Nevada Gold Mines (and on a 60% basis from January 1, 2019 to June 30, 2019), Veladero on a 50% basis, Loulo-Gounkoto on an 80% basis, Kibali on a 45% basis, Tongon on an 89.7% basis, and Morila on a 40% basis until the second quarter of 2019, which reflects our equity share of production and sales. Also removes the non-controlling interest of 38.5% Nevada Gold Mines from July 1, 2019 onwards.

h.Gold cost of sales (Barrick’s share) is calculated as gold cost of sales on an attributable basis (excluding sites in care and maintenance) divided by ounces sold.

i.Amounts reflect production and sales from Jabal Sayid and Zaldívar on a 50% basis, which reflects our equity share of production, and Lumwana.

j.Copper cost of sales (Barrick’s share) is calculated as copper cost of sales plus our equity share of cost of sales attributable to Zaldívar and Jabal Sayid divided by pounds sold.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

24 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

a.These are non-GAAP financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-GAAP measure to the most directly comparable IFRS measure, please see pages 79 to 103 of this MD&A.

b.Cost of sales applicable to gold per ounce is calculated using cost of sales applicable to gold on an attributable basis (removing the non-controlling interest of 40% Pueblo Viejo; 20% Loulo-Gounkoto; 10.3% Tongon; 16% North Mara, Bulyanhulu and Buzwagi starting January 1, 2020, the date the GoT's 16% free carried interest was made effective (36.1% from January 1, 2019 to September 30, 2019; notwithstanding the completion of the Acacia transaction on September 17, 2019, we consolidated our interest in Acacia and recorded a non-controlling interest of 36.1% in the income statement for the entirety of the third quarter of 2019 as a matter of convenience); 63.1% South Arturo from cost of sales from July 1, 2019 onwards as a result of its contribution to Nevada Gold Mines (and on a 40% basis from January 1, 2019 to June 30, 2019); and our proportionate share of cost of sales attributable to equity method investments (Kibali, and Morila until the second quarter of 2019), divided by attributable gold ounces. Also removes the non-controlling interest of 38.5% Nevada Gold Mines from cost of sales from July 1, 2019 onwards. Cost of sales applicable to copper per pound is calculated using cost of sales applicable to copper including our proportionate share of cost of sales attributable to equity method investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds (including our proportionate share of copper pounds from our equity method investments).

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

25 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

Factors affecting net earnings and adjusted net earnings1 - three months ended June 30, 2020 versus March 31, 2020

Net earnings attributable to equity holders of Barrick ("net earnings") for the three months ended June 30, 2020 were $357 million compared to $400 million in the prior quarter. The decrease was primarily due to items occurring in the prior quarter:

•a net impairment reversal of $115 million ($336 million before tax) resulting from the agreement with the GoT being signed and made effective in the first quarter of 2020; and

•a gain of $54 million (no tax impact) on the sale of Massawa.

After adjusting for items that are not indicative of future operating earnings, adjusted net earnings1 of $415 million for the three months ended June 30, 2020 were 46% higher than the prior quarter. The increase in adjusted net earnings1 was mainly due to the higher realized gold price1 of $1,725 per ounce in the three months ended June 30, 2020 compared to $1,589 per ounce in the prior quarter. This was combined with marginally higher gold sales volumes following the re-commencement of exports of concentrate stockpiled in Tanzania, together with production from the end of the first quarter of 2020, which was sold at the start of the current quarter at Loulo-Gounkoto. This was partially offset by lower gold sales volumes across the rest of the portfolio, primarily due to reduced production at Porgera as the mine entered care and maintenance on April 25, 2020, a planned maintenance shutdown at Pueblo Viejo, and the impact of Covid-19 at Veladero where movement and social distancing restrictions slowed the remobilization of employees and contractors back to site following the lifting of quarantine restrictions in April.

Factors affecting net earnings and adjusted net earnings1 - three months ended June 30, 2020 versus June 30, 2019

Net earnings for the second quarter of 2020 were $357 million compared to $194 million in the same prior year period. After adjusting for items that are not indicative of future operating earnings, adjusted net earnings1 of $415 million in the second quarter of 2020 were $261 million higher than the same prior year period. The increase was primarily due to the higher realized gold price1 of $1,725 per ounce in the three months ended June 30, 2020 compared to $1,317 per ounce in the same prior year period, combined with the impact of the formation of Nevada Gold Mines on July 1, 2019. This was partially offset by lower gold sales volumes, primarily due to lower grades mined and processed at Cortez, and Porgera entering care and maintenance on April 25, 2020, combined with the sale of our 50% interest in Kalgoorlie on November 28, 2019. Gold sales volumes in the current period were further impacted by the Covid-19 quarantine and movement restrictions at Veladero, partially offset by the re-commencement of exports of concentrate stockpiled in Tanzania.

Significant adjusting items in the three months ended June 30, 2020 include:

•$33 million ($48 million before tax and non-controlling interest) in other expense adjustments, mainly related to care and maintenance expenses at Porgera and donations relating to Covid-19;

•$20 million ($23 million before tax and non-controlling interest) in net impairment charges, relating to miscellaneous assets.

Refer to page 80 for a full list of reconciling items between net earnings and adjusted net earnings1 for the current and previous periods.

Factors affecting net earnings and adjusted net earnings1 - six months ended June 30, 2020 versus June 30, 2019

Net earnings for the six months ended June 30, 2020 were $757 million compared to $305 million in the same prior year period. The increase was partially due to the net impairment reversal of $111 million ($332 million before tax) resulting from the agreement with the GoT being signed and made effective in the first quarter of 2020 and the gain of $54 million (no tax impact) on the sale of Massawa. After adjusting for items that are not indicative of future operating earnings, adjusted net earnings1 of $700 million for the six months ended June 30, 2020 were $362 million higher than the same prior year period. The significant increase in adjusted net earnings was primarily due to an increase in the realized gold price1 of $1,657 per ounce in the six months ended June 30, 2020 compared to $1,312 per ounce in the same prior year period, combined with the impact of the formation of Nevada Gold Mines on July 1, 2019. This was partially offset by lower sales volume primarily due to lower grades mined and processed at Cortez as mining from the Cortez Hills Open Pit was completed in the second quarter of 2019 and the sale of our 50% interest in Kalgoorlie on November 28, 2019. Gold sales in the current period were further impacted by Porgera entering care and maintenance on April 25, 2020 and the Covid-19 quarantine and movement restrictions at Veladero, partially offset by the re-commencement of exports of concentrate stockpiled in Tanzania.

Significant adjusting items in the six months ended June 30, 2020 include:

•$95 million ($313 million before tax and non-controlling interest) in net impairment reversals, primarily relating to the Tanzanian assets;

•$52 million (no tax impact) in acquisition/disposition gains mainly relating to the sale of Massawa; partly offset by

•$124 million ($146 million before tax and non-controlling interest) in other expense adjustments, primarily related to the impact of changes in the discount rate assumptions on our closed mine rehabilitation provision, care and maintenance expenses at Porgera and donations related to Covid-19.

Refer to page 80 for a full list of reconciling items between net earnings and adjusted net earnings1 for the current and previous periods.

* Numerical annotations throughout the text of this document refer to the endnotes found on page 104.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

26 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

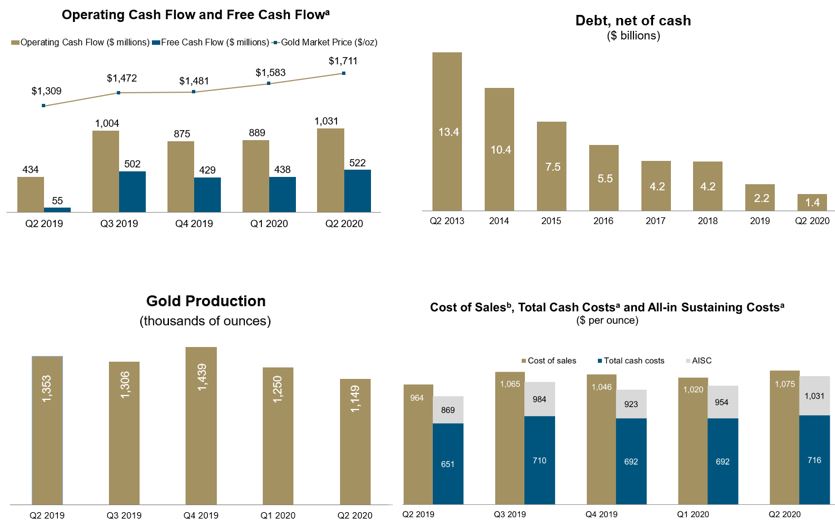

Factors affecting Operating Cash Flow and Free Cash Flow1 - three months ended June 30, 2020 versus March 31, 2020

In the three months ended June 30, 2020, we generated $1,031 million in operating cash flow, compared to $889 million in the prior quarter. The increase of $142 million was primarily due to a favorable movement in working capital, mainly in other current assets and liabilities, accounts payable and inventory. This was combined with the higher realized gold price1 of $1,725 per ounce in the three months ended June 30, 2020 compared to $1,589 per ounce in the prior quarter, combined with slightly higher gold sales volume. This was partially offset by higher cash taxes and interest paid.

Free cash flow1 for the three months ended June 30, 2020 was $522 million, compared to $438 million in the prior quarter, reflecting higher operating cash flows, partially offset by higher capital expenditures. In the second quarter of 2020, higher capital expenditures were mainly attributed to increased capitalized stripping at Loulo-Gounkoto and our investment on the tailings storage facility, other water management initiatives and land acquisitions at North Mara.

Factors affecting Operating Cash Flow and Free Cash Flow1 - three months ended June 30, 2020 versus June 30, 2019

In the second quarter of 2020, we generated $1,031 million in operating cash flow, compared to $434 million in the same prior year period. The increase of $597 million was primarily due to the higher realized gold price1 of $1,725 per ounce in the three months ended June 30, 2020 compared to $1,317 per ounce in the same prior year period, partially offset by lower gold sales volume and higher cash taxes paid.

In the second quarter of 2020, we generated free cash flow1 of $522 million compared to $55 million in the same prior year period. The increase primarily reflects higher operating cash flows, partially offset by higher capital expenditures. In the second quarter of 2020, capital expenditures on a cash basis were $509 million compared to $379 million in the second quarter of 2019. The increase in capital expenditures of $130 million was primarily due to the impact of the sites acquired as part of the formation of Nevada Gold Mines on July 1, 2019, which is consolidated and included at 100%. This was further impacted by increased capitalized stripping at Loulo-Gounkoto and expenditure on the tailings storage facility, other water management initiatives and land acquisitions at North Mara.

Factors affecting Operating Cash Flow and Free Cash Flow1 - six months ended June 30, 2020 versus June 30, 2019

For the six months ended June 30, 2020, we generated $1,920 million in operating cash flow, compared to $954 million in the same prior year period. The increase of $966 million was primarily due to the higher realized gold price1 of $1,657 per ounce in the six months ended June 30, 2020 compared to $1,312 per ounce in the same prior year period, partially offset by lower gold sales volume and higher cash taxes paid.

For the six months ended June 30, 2020, we generated free cash flow1 of $960 million compared to $201 million in the same prior year period. The increase primarily reflects higher operating cash flows, partially offset by higher capital expenditures. In the six months ended June 30, 2020, capital expenditures on a cash basis were $960 million compared to $753 million in the same prior year period. Higher capital expenditures of $207 million were primarily due to the impact of the sites acquired as part of the formation of Nevada Gold Mines on July 1, 2019, which is consolidated and included at 100%. This was further impacted by increased capitalized stripping at Loulo-Gounkoto and expenditure on the tailings storage facility, other water management initiatives and land acquisitions at North Mara.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

27 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

Key Business Developments

Covid-19 pandemic

Barrick continues to work closely with our local communities on managing the impacts of the Covid-19 pandemic on our people and our business. Barrick has a strong culture of caring for the welfare of its employees and communities. Our well-established prevention practices and procedures, and the experience we gained from dealing with two Ebola outbreaks around our African operations, has assisted us as we face this new and unprecedented challenge. We have been actively working to support government responses to the Covid-19 pandemic, both financially and using our supply chain to secure key supplies for the benefit of the communities in which we operate.

Our preference for employing nationals in the countries where we operate rather than expatriates, means that we are not dependent upon a workforce traveling to a site on a regular basis from other parts of the globe. Although we have adapted certain operating procedures to respond to Covid-19 to date, our operations have not been significantly impacted by the pandemic with the exception of Veladero. In Argentina, a mandatory nationwide quarantine was lifted in April, while movement and social distancing restrictions slowed the remobilization of employees and contractors back to Veladero.

Early and considered actions by management including social distancing, screening and contact tracing measures have been implemented at all our sites. This has allowed our sites to continue to produce and sell their production as well as keep our people and local communities safe at the same time. These actions have minimized the impacts of the pandemic at our operations and facilitated the delivery of strong operating cash flow in the first half of 2020. Our focus on strengthening our balance sheet in recent years has given us the financial strength to endure any short-term impacts to our operations. We have $3.7 billion in cash, an undrawn $3.0 billion credit facility and no significant debt repayments due until 2033, providing us with sufficient liquidity to execute on our strategic goals.

We also recognize the situation remains dynamic and as such, we continue to monitor developments around the world and believe we have positioned Barrick as best we can to weather the storm.

Porgera Special Mining Lease Extension

Porgera's Special Mining Lease (“SML”) terminated on August 16, 2019. The Company applied for a 20-year extension of the SML in June 2017 and has been engaging with the Government of Papua New Guinea on this matter since then. On August 2, 2019, the National Court of Papua New Guinea ruled that the provisions of the country’s 1992 Mining Act applied to the Porgera gold mine, thus allowing it to continue operating while the application to extend its SML was being considered. Also in 2019, in response to a request from Papua New Guinea Prime Minister Marape, the Company proposed a benefit-sharing arrangement that would deliver more than half the economic benefits from the Porgera mine to Papua New Guinea stakeholders, including the Government, for the remainder of the life of mine, estimated at 20 years.

On April 24, 2020, Barrick Niugini Limited (“BNL”), the majority owner and operator of the Porgera joint venture, received a communication from the Government of Papua New Guinea that the SML would not be extended. The Company believes the Government’s decision not to extend the SML is tantamount to nationalization without due process and in violation of the Government’s legal obligations to BNL. The Company remains willing to discuss the issue with Prime Minister Marape and his Government in light of the potentially catastrophic impact of this decision for the communities at Porgera and in Enga Province, and for the country as a whole. BNL will pursue all legal avenues to challenge the Government’s decision and to recover any damages that BNL may suffer as a result of the Government’s decision. The Company will not discuss transitional arrangements for the management of the Porgera mine, as proposed by the Government, as this is not consistent with BNL’s rights. Based on the communication received from the Government of Papua New Guinea that the SML would not be extended, Porgera was placed on temporary care and maintenance on April 25, 2020 to ensure the safety and security of our employees and communities.

On April 28, 2020, BNL filed a Judicial Review action against the Government of Papua New Guinea in the Papua New Guinea National Court of Justice. Judicial Review is a proceeding that challenges the procedural and constitutional adequacy of government administrative actions. The Judicial Review action seeks to quash the decision not to extend the SML on the grounds that the Government did not comply with the applicable legal standards and processes. On June 5, 2020, the National Court granted BNL leave to apply for Judicial Review.

BNL asked the National Court for a stay of the decision not to extend the SML to enable BNL to stay in possession of the mine to put it on temporary care and maintenance and to protect the mine’s assets. After a hearing on April 30, 2020, the National Court ordered that BNL could stay in possession of the Porgera mine “to ensure that the environment, the integrity of the mine and the rights of the landowners are not compromised” and ordered the Government of Papua New Guinea to cooperate with that objective. On July 17, 2020, the Court stayed any further actions to implement the decision not to extend the SML.

Trial was set to commence in the Judicial Review action on August 12, 2020. BNL sought leave to appeal two procedural rulings of the National Court that would affect the trial to the Supreme Court of Papua New Guinea. In hearings on August 5 and 6, 2020, the Supreme Court granted leave for BNL's appeals and stayed the trial.

On July 9, 2020, BNL initiated conciliation proceedings before the World Bank’s International Centre for Settlement of Investment Disputes (“ICSID”). Through this conciliation, BNL seeks to reach an agreement for the extension of the SML on terms that will be mutually beneficial to the Company and to all Papua New Guinea stakeholders.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

28 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

Simultaneously with BNL initiating the conciliation proceedings, Barrick (PD) Australia Pty Limited (“Barrick PD”), the Company’s subsidiary and an investor in the Porgera mine, has given notice to the Government of Papua New Guinea that a dispute has arisen under the Bilateral Investment Treaty (“BIT”) between Papua New Guinea and Australia, and has referred the dispute to arbitration before the ICSID. Barrick PD seeks to recover damages it has already suffered and damages it may suffer in the future by virtue of the Government’s wrongful refusal to grant an extension of the SML. The dispute notice expressly invites the Government to engage in consultations and negotiations in an attempt to resolve the investment treaty dispute.

Our priority remains the health and safety of all our employees and community stakeholders. Due to the uncertainty related to the timing and scope of future developments on the mine’s operating outlook, we have withdrawn our full year 2020 guidance for Porgera. As this is a rapidly evolving situation, we will reassess on an ongoing basis and provide further updates in due course, while maintaining operational readiness.

Partial Monetization of Investment in Shandong Gold

In June 2020, we sold 79,268,800 shares of Shandong Gold Mining Co., Ltd. (“Shandong Gold”), for net proceeds of $208 million. Barrick continues to hold 10,250,000 shares of Shandong Gold, representing a 2.05% interest in Shandong Gold’s Hong-Kong listed (H-class) shares, re-affirming its commitment to the strong existing long-term strategic partnership between the two companies.

Sale of Massawa

On March 4, 2020, Barrick and our Senegalese joint venture partner completed the sale of our aggregate 90% interest in the Massawa project (“Massawa”) in Senegal to Teranga Gold Corporation (“Teranga”) for total consideration fair valued at $440 million on the date of closing. Barrick received 92.5% of the consideration for its interest in the Massawa project, with the balance received by Barrick’s local Senegalese partner. Barrick received a net of $256 million in cash and 19,164,403 Teranga common shares (worth $104 million at the date of closing) plus a contingent payment of up to $46.25 million based on the three year average gold price, which was valued at $28 million at the date of closing. The cash consideration received was net of $25 million that Barrick provided through its participation in the $225 million syndicated debt financing facility secured by Teranga in connection with the transaction. The facility has a final repayment date of December 31, 2022. The difference between the fair value of consideration received and the carrying value of the assets on closing was $54 million and was recognized as a gain in the first quarter of 2020.

Refer to note 4 to the Financial Statements for more information.

Tanzania

On January 24, 2020, Barrick announced that the Company had ratified the creation of Twiga Minerals Corporation

(“Twiga”) at a signing ceremony with the President of Tanzania, formalizing the establishment of a joint venture between Barrick and the Government of Tanzania (“GoT”) and resolution of all outstanding disputes between Barrick and the GoT, including the lifting of the previous concentrate export ban, effective immediately. Effective January 1, 2020, the GoT received a free carried shareholding of 16% in each of the Tanzania mines (Bulyanhulu, Buzwagi and North Mara), a 16% interest in the shareholder loans owed by the operating companies and will receive half of the economic benefits from the Tanzanian operations from taxes, royalties, clearing fees and participation in all cash distributions made by the mines and Twiga, after the recoupment of capital investments. Twiga will provide management services to the mines. Refer to note 13 to the Financial Statements for further information.

The terms of the signed agreement are consistent with those previously announced, including the payment of $300 million to settle all outstanding tax and other disputes (the “Settlement Payment”); the lifting of the concentrate export ban; the sharing of future economic benefits from the mines on a 50/50 basis; and a dispute resolution mechanism that provides for binding international arbitration. The 50/50 division of economic benefits will be maintained through an annual true-up mechanism, which is exclusive of the Settlement Payment.

Barrick and the GoT continue efforts to fulfill their respective obligations to satisfy all conditions of the signed agreement, primarily with respect to the execution and delivery of formal termination documents for the settlement of all outstanding disputes between the two parties. In the second quarter of 2020, exports of the concentrate stockpiled in Tanzania commenced and we began recognizing these sales in revenue and cost of sales. We also made a payment of $100 million to the GoT representing the first installment of the Settlement Payment in the second quarter of 2020, reducing the previously recorded Settlement Payment liability of $300 million on the balance sheet.

Operating results are included at 84% from January 1, 2020. We recognized a net impairment reversal of $111 million ($332 million before tax) resulting from the agreement with the GoT being signed and made effective in the first quarter. Refer to note 13 to the Financial Statements for more information.

Debt Management

On January 31, 2020, Barrick paid $356 million, including $4 million of accrued and unpaid interest, to complete a make-whole repurchase of the $337 million of outstanding principal on our 3.85% Notes due April 2022. A loss on debt extinguishment of $15 million was recorded in the first quarter of 2020. The debt repayment is expected to result in an annualized interest savings of $13 million.

|

|

|

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2020 |

29 |

MANAGEMENT'S DISCUSSION AND ANALYSIS |

Environmental and Social Governance

At Barrick, Environmental and Social Governance ("ESG") has been a key focus for our business since we began. Making sure we respect human rights, protect the health and safety of our people and local communities, share the benefits of our operations, and manage our impacts on the environment is both embedded in our business decision-making processes and every facet of our operations. It is enshrined in our sustainability vision and mission as well as in our guiding principles. We monitor our sustainability performance because it helps us make better decisions, helps to de-risk projects, discover new opportunities and deliver real value for our business. Sustainable development is truly at the heart of Barrick, and our sustainability vision is embedded in every aspect of what we do.

To reinforce our belief in transparently disclosing our sustainability performance and to better understand our performance relative to our industry peers, we developed and published our inaugural Sustainability Scorecard with the publication of our 2019 Sustainability Report released in April 2020. The scorecard ranks us against our peers, where applicable, and against our own internal metrics and aggregates that performance into an overall score. It compares our performance across our priority ESG areas: Health and Safety, Social and Economic Development, Human Rights, the Environment as well as Governance. After reviewing the published performance metrics from our peers, we were able to quantify our score. Overall, we scored a B grade (on a scale where A represents high performance and E represents poor performance), which we believe accurately reflected our improvements in sustainability performance through 2019, but also acknowledges that there are still areas that we strive to improve.

Our sustainability vision puts four key ambitions at the center of our business: creating economic benefits; protecting health and safety; respecting human rights; and minimizing our environmental impact.

Safety

Our safety vision is “Every person going home safe and healthy every day.” In the first half of 2020, we have operated with zero fatalities.

Barrick is fully committed to the safety, health and well-being of our people, their families and the communities in which we operate. We review safety performance and incidents, share lessons learned and communicate best practices across our business during weekly Executive Committee meetings, which is the main forum for senior management to review our current safety performance. Safety performance is also reported as part of our quarterly Environmental & Social Oversight Committee ("E&S Committee") meetings and to the Board's Corporate Governance & Nominating Committee.

With 17 operations spanning four continents together with a range of operating environments, how our Safety policy and commitments are translated on the ground varies. Each site has its own site-specific safety procedures, management plans and systems in place, informed by its operating context. All site systems, plans and procedures

align with international best practice. Our goal is for the safety management systems at all operational mines to be certified to the internationally recognized ISO 45001 standard by the end of 2021, with three sites already accredited.

During 2019, we rolled out new controls including our ten Fatality Prevention Commitments to help eliminate fatalities and serious injuries. Our Fatality Prevention Commitments align with the International Council on Mining and Metal’s Life Saving Controls, which are based upon lessons learned from fatal incidents within the mining industry, including Barrick’s experience. Our Commitments and Unacceptable Behaviors guideline has also been implemented, which reaffirms our zero-tolerance policy for behavior such as working on site under the influence of drugs or alcohol.

The group has also started the roll out of our “Journey to Zero Harm” initiative which is focused on Visible Felt Leadership, engagement with our workforce, aligning and improving our standards, ensuring accountability to our safety commitments and ensuring employees are fit for duty. The continued focus on safety has helped drive safety performance improvements across the group in the first half of 2020. Our Total Reportable Injury Frequency Rate (“TRIFR”) for the quarter was 1.65, a slight increase from the prior quarter of 1.64.

The group recorded fewer Lost Time Injuries ("LTIs") compared to the prior quarter, with the related frequency rates also decreasing quarter on quarter. For the second quarter of 2020, our group Lost Time Injury Frequency Rate ("LTIFR") was 0.27 compared to 0.32 in the first quarter of 2020.

Environment

Barrick continues to rebuild its reputation for environmental excellence and aims to become the world’s most valued gold mining business by delivering sustainable returns for our owners and partners, including the host communities and countries in which we operate.

We have set a corporate goal for all sites to have their Environmental Management System (“EMS”) certified to the ISO 14001:2015 standard by the end of 2020. Currently, all operations, except the Jabal Sayid mine in Saudi Arabia and the three Tanzanian mines, are certified to this standard. Certification audits for these assets are scheduled to take place late in the second half of 2020.

We maintained our strong track record of stewardship and did not record any Class 1 environmental incidents in the first half of 2020.

Climate