EX-99.1

Exhibit 99.1

SECOND QUARTER REPORT 2013

Barrick Reports Second Quarter 2013 Results

| ¡ |

|

$8.7 billion in after-tax impairment charges, largely driven by recent declines in metal prices |

| ¡ |

|

Strong operating results from gold and copper mines; 2013 production guidance maintained, cost guidance for both gold and copper lowered

|

| ¡ |

|

Reduced 2013 budgeted capital and costs by about $1.5 billion during the second quarter and by about $2.0 billion in H1 2013 |

| ¡ |

|

2013 capital guidance reduced to $4.5-$5.0 billion from $5.7-$6.3 billion; cost of sales guidance reduced to $7.2-$7.8 billion from $7.9-$8.4 billion

|

| ¡ |

|

Lowered quarterly dividend to $0.05 per share |

TORONTO, August 1, 2013 - Barrick Gold Corporation (NYSE: ABX) (TSX: ABX) (Barrick or the “company”) today reported a second quarter net loss of $8.56 billion ($8.55 per share), reflecting

$8.7 billion in after-tax impairment charges largely driven by significant decreases in long-term metal price assumptions following the sharp declines in spot prices in the second quarter. The total charge is comprised of: $5.1 billion for the

Pascua-Lama project, $2.3 billion in goodwill impairments and $1.3 billion in other asset impairment charges.

Second quarter financial

highlights include:

| ¡ |

|

Adjusted net earnings of $663 million ($0.66 per share)1 |

| ¡ |

|

Operating cash flow of $896 million |

| ¡ |

|

Adjusted operating cash flow of $804

million1 |

SECOND QUARTER 2013 OPERATING HIGHLIGHTS AND FULL YEAR 2013 GUIDANCE

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold |

|

Q2 2013 |

|

|

Current Guidance |

|

|

Original Guidance |

|

| Production (000s of ounces) |

|

|

1,811 |

|

|

|

7,000-7,400 |

|

|

|

7,000-7,400 |

|

| All-in sustaining costs ($ per ounce)1 |

|

|

919 |

|

|

|

900-975 |

|

|

|

1,000-1,100 |

|

| Adjusted operating costs ($ per ounce)1 |

|

|

552 |

|

|

|

575-615 |

|

|

|

610-660 |

|

| Copper |

|

|

|

|

|

|

|

|

|

| Production (millions of pounds) |

|

|

134 |

|

|

|

500-540 |

|

|

|

480-540 |

|

| C1 cash costs ($ per pound)1 |

|

|

1.75 |

|

|

|

1.95-2.15 |

|

|

|

2.10-2.30 |

|

| C3 fully allocated costs ($ per pound)1 |

|

|

2.27 |

|

|

|

2.50-2.75 |

|

|

|

2.60-2.85 |

|

“We are pleased with our second quarter operating performance and our improved

2013 guidance. These results reflect the high quality of Barrick’s portfolio of assets and our increasingly effective efforts at controlling costs. We are disappointed with the impairment charges for Pascua-Lama and other assets but are

confident that these assets, some with mine lives in excess of 25 years, will generate substantially more economic benefits over time,” said Jamie Sokalsky, Barrick’s President and CEO.

| 1 |

Adjusted net earnings, adjusted net earnings per share, adjusted operating cash flow, all-in sustaining costs per ounce, adjusted operating costs per ounce, C1

cash costs per pound and C3 fully allocated costs per pound are non-GAAP financial performance measures with no standardized definition under IFRS. The World Gold Council’s adjusted operating cost measure was previously described as total cash

costs. See pages 45-48 of Barrick’s Second Quarter 2013 Report. |

|

Financial results are based on IFRS and expressed in US dollars. For

a full explanation of results, the Financial Statements and Management Discussion & Analysis, please see the company’s website, www.barrick.com.

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

1 |

|

PRESS RELEASE |

“Over the past year, we have taken and are continuing to take a

series of steps to reduce costs as part of our disciplined capital allocation framework, which allowed us to respond quickly to the new metal price environment. We have reduced 2013 budgeted capital and costs by about $2.0 billion which has offset

the cash flow impact of the drop in gold and copper prices that has occurred this year. We have reduced all-in sustaining cost guidance by about $100 per ounce this year from levels which are the lowest of our peers. The bulk of our expected 2013

gold production is at all-in sustaining costs well below current spot levels, and for those operations that are not generating positive cash flow, we will change mine plans, suspend, close or divest them.

“We have sold Barrick Energy and are well advanced in a process to divest certain Australian assets as part of our

portfolio optimization strategy. We are progressing the Pascua-Lama project by extending the overall construction schedule over a longer period, which substantially alleviates near-term capital spend, and we are also working to meet regulatory

requirements. We also termed out $3.0 billion of debt at attractive rates to reduce near-term maturities. And finally, in light of the current environment, we have also made a decision to lower the quarterly dividend to improve liquidity. We

recognize the importance of dividends to our shareholders, and it is our goal to return more capital to investors in the future, but at this time, this is the prudent course of action.”

POSITIONING BARRICK IN A LOWER METAL PRICE ENVIRONMENT

High Quality Asset Base and Aggressive Cost

Reductions Provide Operational Flexibility

Barrick’s strategy prioritizes shareholder value creation by focusing on maximizing

risk-adjusted rates of return and free cash flow based on the principle that returns will drive production, production will not drive returns. In today’s environment, Barrick has no plans to build new mines.

As part of our increased focus on disciplined capital allocation adopted a year ago, we have reduced costs and improved

cash flow, initially cutting or deferring about $4.0 billion of previously budgeted capital expenditures over a four year period, shelving certain major projects and launching a portfolio optimization process.

Barrick’s comprehensive cost reductions and high quality asset base provide the company with significant

operational flexibility. Its superior group of five key mines – Cortez, Goldstrike, Pueblo Viejo, Veladero and Lagunas Norte – are expected to generate some 60 percent of 2013 production at average all-in sustaining costs (AISC) of

$650-$700 per ounce. An additional seven mines have AISC below $1,000 per ounce, bringing the total amount of expected 2013 production with costs below this level to about 75 percent.

Developing Plans to Maximize Cash Flow

For the remaining operations with expected 2013 AISC

above $1,000 per ounce, we will either change mine plans, suspend, close or divest these assets to improve cash flow. Actions currently being considered as part of an ongoing process include:

| ¡ |

|

Bald Mountain (US) - mine plan changes to reduce the number of pits and focus on the most profitable ounces, while retaining the option to access other ore in

the future |

| ¡ |

|

Round Mountain and Marigold (US) - working with our joint venture partners to optimize mine plans |

| ¡ |

|

Hemlo (Canada) - defer the open pit expansion and optimize the underground mine plan |

| ¡ |

|

Porgera (Papua New Guinea) - evaluate mine plan changes and explore other alternatives |

| ¡ |

|

Plutonic, Yilgarn South (Australia) - optimize the mine plans and/or divest |

| ¡ |

|

African Barrick Gold (ABG) (Tanzania) - finalizing a detailed operational review to aggressively optimize mine plans and improve operations

|

| ¡ |

|

Pierina (Peru) - assessing closure options |

Under the direction of the new leadership appointed last year, a turnaround team of functional experts and site management have been working to improve operations and reduce costs at the Lumwana copper

mine. Lumwana delivered a substantially improved performance this quarter. We have made changes to the mine plan to decrease costs and maximize cash flow. The changes include a reduction to waste stripping as a result of mine

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

2 |

|

PRESS RELEASE |

re-sequencing and significant labor reductions, including termination of a major mining contractor. A number of further business improvement initiatives continue to be implemented at site to

enhance the productivity of the core mining fleet and build upon the cost reductions achieved so far. We continue to see positive results from these actions, and the improvements at Lumwana have allowed us to significantly improve 2013 copper cost

guidance.

Long-Term Production Targets Will Be Aligned with Portfolio Optimization and Mine Planning Changes

We are developing mine plans to maximize cash flows at every mine. The outcome of this process could have an impact on our year-end 2013 proven and

probable reserves and expected future production levels; however, where possible, we will maintain the option to access the metal in the future. As a result of the schedule delay at Pascua-Lama, expected mine plan changes to maximize cash flow and

the likelihood of further asset divestitures, we are no longer targeting eight million ounces of gold production in 2016.

2013 Guidance Improvements

Reflect Ongoing Cost Reductions Totalling $2.0 Billion in First Half

Total reductions to budgeted capital and costs for 2013 of

about $2.0 billion have offset the cash flow impact of the declines in metal prices that have occurred this year. During the first quarter of 2013, Barrick reduced budgeted 2013 capital and costs by approximately $500 million and lowered 2013 cost

guidance for total capex and exploration. In the second quarter, the company has accelerated actions to improve cash flow. Operating cost reductions also reflect the softening of input costs such as steel and tires, as well as the weakening

Australian dollar, and we continue to evaluate additional ways to reduce costs.

As a result of the strong

measures taken in the second quarter alone, reductions to budgeted 2013 capital expenditures and costs include approximately:

| ¡ |

|

$600 million in operating costs; |

| ¡ |

|

$200 million in sustaining, development and mine expansion capital; |

| ¡ |

|

$600 million in project capital, primarily related to Pascua-Lama; and, |

| ¡ |

|

$50 million in exploration and evaluation expenditures. |

In addition, the company has reduced its corporate office staff by approximately 30 percent and made other significant

job reductions at regional locations. As part of the ongoing company-wide overhead and operational review initiated in the first quarter, Barrick is also evaluating further changes and cost reductions to make the organization more efficient by

simplifying the management structure and placing a greater emphasis on clearly defined responsibilities and accountabilities.

FINANCIAL RESULTS

DISCUSSION

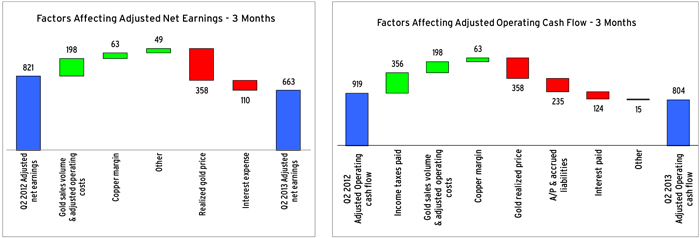

The second quarter net loss and adjusted net earnings of $8.56 billion ($8.55 per share) and $663 million ($0.66 per

share), respectively, compare to net earnings and adjusted net earnings of $787 million ($0.79 per share) and $821 million ($0.82 per share), respectively, in the same prior year period. The net loss reflects after-tax impairment charges of $8.7

billion and a $0.5 billion loss on the sale of Barrick Energy.

The fair values in the impairment assessment

were calculated as at June 30 assuming metal prices that were influenced by only recent spot price declines, yet which are then applied and held constant over mine lives that in some instances are in excess of 25 years. As a result of these

significant price declines, we have revised our gold, copper and silver price assumptions utilized for impairment testing to $1,300 per ounce, $3.25 per pound and $23 per ounce, respectively. We are confident our assets will generate substantially

more economic benefits over time for our shareholders than these current valuation levels imply. Although Barrick does not rely on higher prices to drive its business plans, we remain positive on long term price fundamentals for these metals. With

higher prices

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

3 |

|

PRESS RELEASE |

in the future, we would reassess the fair value of our high quality, long-life assets such as Pascua-Lama, and could potentially reverse some of the impairment charges recorded.

Significant adjusting items (net of tax and non-controlling interest effects) for the quarter include:

| |

¡ |

|

$5.1 billion in asset impairment charges against the carrying value of the Pascua-Lama project; |

| |

¡ |

|

$2.3 billion in goodwill impairments to the Global Copper, Australia Pacific, Capital Projects and ABG segments; |

| |

¡ |

|

$1.3 billion in other asset impairment charges, including $423 million for Buzwagi, $401 million for Jabal Sayid and $107 million for Kanowna; and,

|

| |

¡ |

|

$0.5 billion loss related to the sale of Barrick Energy. |

Second quarter 2013 operating cash flow of $896 million compares to $919 million in the second quarter of 2012.

Adjusted operating cash flow of $804 million removes the impact of the settlement of foreign currency and commodity derivative contracts and non-recurring tax payments, and compares to $919 million in the same prior year period. Realized gold and

copper prices for the quarter were $1,411 per ounce and $3.28 per pound, respectively, both in line with the spot averages.

LIQUIDITY AND FINANCIAL

FLEXIBILITY

At June 30, Barrick had cash and equivalents of $2.4 billion and $4.0 billion available under its five-year credit

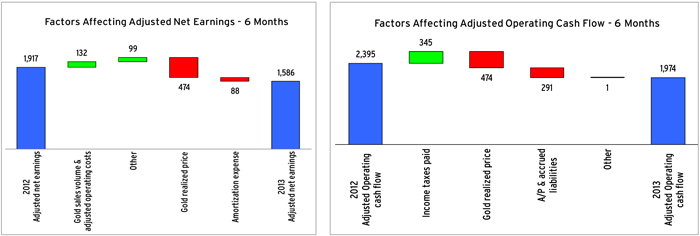

facility. The company generated strong operating cash flow of $2.0 billion in the first half of 2013 and is on track to meet 2013 production guidance at costs well below original guidance. Barrick’s consolidated tangible net worth at

June 30 was $6.3 billion. In addition to the reductions to budgeted 2013 capital and costs, Barrick further strengthened its liquidity in the second quarter by terming out $3.0 billion in debt at attractive interest rates to reduce near-term

maturities. The company has approximately only $1.8 billion of cumulative debt maturing through to the end of 2015.

Subsequent to the second quarter, the company divested Barrick Energy for total consideration of $442 million, including cash of $394 million plus a royalty on certain assets valued at $48 million. The

proceeds will be recorded in the third quarter of 2013. In addition, a process to divest certain Australian assets is well advanced, and the company continues to actively pursue other portfolio optimization opportunities, including the divestiture

of other non-core assets. The company’s Board of Directors has reduced the quarterly dividend to $0.05 per share as a further prudent step to improve liquidity. The dividend is payable on September 16, 2013 to shareholders of record at the

close of business on August 30, 20132.

OPERATING RESULTS DISCUSSION

Second quarter

2013 gold production was 1.81 million ounces, benefiting from strong performances at Cortez, Veladero and Lagunas Norte. In June 2013, the World Gold Council (WGC) finalized its definition of adjusted operating costs (previously called total

cash costs), all-in sustaining costs and all-in costs. Barrick has revised its disclosure to align with these definitions and is voluntarily adopting the all-in cost measure. The manner in which the adjusted operating cost measure is calculated has

not been changed from the total cash cost measure. The revised AISC measure is similar to our prior measure with the exception of the classification of sustaining capital; certain capital expenditures which had previously not been reported as

sustaining capital are now included in this category. The all-in cost measure starts with AISC and adds non-sustaining capital expenditures at new operations and existing operations which will significantly increase production. For Barrick this

consists primarily of capital for the Pascua-Lama and Goldstrike thiosulphate projects. For the second

2 The declaration and payment of dividends is at the discretion of the Board of Directors and will depend on the company’s financial results, cash requirements, future

prospects and other factors deemed relevant by the Board.

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

4 |

|

PRESS RELEASE |

quarter, Barrick’s adjusted operating costs, AISC and all-in costs were $552 per ounce, $919 per ounce and $1,276 per ounce3, respectively.

North America

Regional Business Unit

North America produced 0.93 million ounces at AISC of $797 per ounce, ahead of expectations.

Barrick’s 60 percent share of production from the Pueblo Viejo mine was 0.12 million ounces at AISC of $635 per ounce. Production at Pueblo Viejo increased from the first quarter of 2013 primarily due to higher tons processed as the mine

ramps up to full capacity, expected in the second half of this year. The new 215 megawatt power plant is expected to be commissioned on schedule in the third quarter. Barrick’s share of 2013 production from Pueblo Viejo is anticipated to be

500,000-600,000 ounces at AISC of $525-$575 per ounce. During the quarter, Pueblo Viejo Dominicana Corporation reached an agreement in principle with the Government of the Dominican Republic concerning amendments to the Pueblo Viejo Special Lease

Agreement (SLA). Discussions to finalize a Definitive Agreement continue, but to date the parties have not concluded an agreement. The proposed amendments will require the approval of the Boards of Directors of Barrick and Goldcorp, the project

lenders, and the Congress of the Dominican Republic. The SLA will remain in effect according to its present terms unless and until the Definitive Agreement is executed and approved. The Government has reaffirmed its support for this world class

mine.

The Cortez mine delivered a strong performance, producing 0.42 million ounces at AISC of $376 per

ounce on higher grade oxide ore. Goldstrike produced 0.19 million ounces at AISC of $1,226 per ounce, reflecting processing of lower grade ore at the autoclave facility, which is currently undergoing modifications to enable about

3.5 million ounces to be brought forward in the mine plan through the thiosulphate project. The project is on track to enter production in the third quarter of 2014 and contribute average annual production of 350,000-400,000 ounces over its

first full five years of operation. We expect production to increase and AISC to significantly decrease at Goldstrike in the second half of 2013.

We continue to expect full year production to be in the range of 3.55-3.70 million ounces and now expect AISC to be in the range of $750-$800 per ounce, lower than our previous range of $820-$870

per ounce.

South America Regional Business Unit

South America produced 0.30 million ounces at better than expected AISC of $821 per ounce. The Veladero mine had a strong quarter, contributing 0.14 million ounces at AISC of $768 per ounce on higher

silver recoveries. Lagunas Norte produced 0.13 million ounces at AISC of $663 per ounce, reflecting positive grade reconciliations and a build-up of ounces placed on the leach pad. The new carbon-in-column plant at Lagunas Norte, which is

designed to de-bottleneck ore feed from the expanded leach pad to the Merrill Crowe plant, is on track to start up in Q4.

We continue to expect full year production to be in the range of 1.25-1.35 million ounces and AISC to be in the

range of $875-$925 per ounce.

Australia Pacific Regional Business Unit

Australia Pacific produced 0.47 million ounces at AISC of $1,033 per ounce. Porgera, the region’s largest mine, contributed 0.12 million ounces at AISC of $1,306 per ounce.

We continue to expect full year production to be in the range of 1.70-1.85 million ounces and now expect AISC to be

in the range of $1,100-$1,200 per ounce, lower than our previous range of $1,200-$1,300 per ounce.

| 3 |

All-in costs are a non-GAAP financial performance measure with no standardized definition under IFRS. See pages 45-48 of Barrick’s Second Quarter 2013

Report. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

5 |

|

PRESS RELEASE |

African Barrick Gold plc

Second quarter attributable production from ABG was 0.12 million ounces at AISC of $1,416 per ounce. We continue to expect Barrick’s share of 2013 production from ABG to be 0.40-0.45 million ounces

at AISC of $1,550-$1,600 per ounce. Our AISC guidance does not take into account the implementation of ABG’s Operational Review.

Global Copper

Business Unit

Copper production in Q2 was 134 million pounds at C1 cash costs of $1.75 per pound and C3 fully allocated costs

of $2.27 per pound. Performance from the Lumwana mine improved significantly this quarter with production of 65 million pounds at C1 cash costs of $1.96 per pound, primarily due to changes to the mine plan and a number of business improvement

initiatives which continue to enhance productivity. The improved costs in the second quarter primarily reflect a major reduction in contract mining costs due to the termination of one of the main mining contractors. The Zaldívar mine produced

69 million pounds at C1 cash costs of $1.60 per pound.

We now expect full year copper production to be

500-540 million pounds, within our original guidance range of 480-540 million pounds, at C1 cash costs of $1.95-$2.15 per pound and C3 fully allocated costs of $2.50-$2.75 per pound, both lower than our previous ranges of $2.10-$2.30 per

pound and $2.60-$2.85 per pound, respectively.

Utilizing option collar hedging

strategies, the company has protected the downside on approximately half of its remaining 2013 copper production at an average floor price of $3.50 per pound and can participate on the same amount up to an average price of $4.25 per pound4. As of June 30, 60 million pounds of copper sales were subject to final

settlement at an average provisional price of $3.06 per pound.

PASCUA-LAMA PROJECT UPDATE

Pascua-Lama is one of the world’s largest gold and silver resources with nearly 18 million ounces of proven and

probable gold reserves5, 676 million ounces of silver contained within

the gold reserves5, and an anticipated mine life of 25 years. It is expected

to produce an average of 800,000-850,000 ounces of gold and 35 million ounces of silver in its first full five years of operation at very low costs. While we recorded a significant impairment to this asset in the second quarter, we fully expect

this mine to be one of the best in the world when in operation, and to contribute substantial economic value to the company. Pascua-Lama has significant value for Barrick shareholders and the project’s host jurisdictions of San Juan Province,

Argentina and the Atacama Region of Chile. We continue to work closely with the governments of both countries to ensure Pascua-Lama is on the right path to deliver value for all of our stakeholders.

In the second quarter, the company received a resolution from Chile’s Superintendence of the Environment

(Superintendencia del Medio Ambiente or “SMA”) that required completion of the project’s water management system in accordance with previously granted environmental permits before other construction activities in Chile could resume.

Barrick is committed to operating at the highest environmental standards at all of its operations around the world, including at Pascua-Lama, and is working to meet all regulatory requirements at the project. The company has submitted a compliance

plan for approval by Chilean regulatory authorities to complete the water management system by the end of 2014, subject to regulatory approval of specific permit applications. Following completion of the water management system to the satisfaction

of the SMA, we expect to be in a position to resume construction in Chile, including pre-stripping. Under this scenario, ore from Chile is expected to be available for processing by mid-2016. In line with this timeframe and in light of materially

lower metal prices, the company has decided to re-sequence construction of the process plant and other facilities in Argentina to target production by this date.

| 4 |

The realized price on all 2013 copper production is expected to be reduced by approximately $0.04 per pound as a result of the net premium paid on option

hedging strategies. Our remaining copper production is subject to market prices. |

| 5 |

For a breakdown of reserves and resources by category and additional information relating to reserves and resources, see pages 25-35 of Barrick’s Form

40-F. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

6 |

|

PRESS RELEASE |

The decision to re-sequence the project, which

entails a major reduction in project staffing levels over the extended schedule, will result in a significant deferral of planned capital spending in 2013-2014. Capital expenditures at Pascua-Lama over this period are expected to be reduced by a

total of $1.5-$1.8 billion6. For 2013, capital expenditures are expected to be

reduced by approximately $0.7-$0.8 billion (including $300 million in previously announced deferrals) to approximately $1.8-$2.0 billion. Capital expenditures in 2014 are expected to be reduced by approximately $0.8-$1.0 billion to approximately

$1.0-$1.2 billion. The company is targeting to provide an updated total capital cost estimate for the project with third quarter 2013 results which is expected to reflect an increase from the latest capital cost estimate. This is subject to

obtaining greater clarity on timing of regulatory approvals and completing the re-sequenced construction schedule. As of June 30, 2013, approximately $5.4 billion had been spent on the project.

Subsequent to the quarter end, the Copiapo Court of Appeals in Chile issued its ruling on a constitutional rights

protection action filed in September 2012 on behalf of four indigenous communities, on the basis of which a preliminary injunction suspending construction activities had been granted in April 2013. In its ruling, the Court stated that Barrick must

complete construction of the water management system in compliance with applicable environmental permits to the satisfaction of the SMA before resuming construction activities in Chile. The Court’s ruling is consistent with the earlier SMA

resolution which Barrick has been implementing. The water management design and construction scope has been awarded to Fluor, who has already mobilized a team of industry experts to the site.

Our Chief Operating Officer, Igor Gonzales, retired in the second quarter and the company is in the process of a global search to fill this

position. In the interim, the Regional Presidents are reporting directly to the CEO. Barrick thanks Igor for his significant contributions to Barrick over the past 15 years.

| 6 |

Includes Pascua-Lama initial project capital plus infrastructure capital. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

7 |

|

PRESS RELEASE |

Key Statistics

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Barrick Gold Corporation (in United

States dollars) |

|

Three months ended June 30, |

|

|

Six months ended June 30, |

|

| |

|

|

|

| (Unaudited) |

|

2013 |

|

|

2012 (restated)7 |

|

|

2013 |

|

|

2012 (restated)7 |

|

| |

|

| Operating Results |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold production (thousands of ounces)1 |

|

|

1,811 |

|

|

|

1,742 |

|

|

|

3,608 |

|

|

|

3,623 |

|

| Gold sold (thousands of ounces) |

|

|

1,815 |

|

|

|

1,690 |

|

|

|

3,562 |

|

|

|

3,473 |

|

| Per ounce data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average spot gold price |

|

$ |

1,415 |

|

|

$ |

1,609 |

|

|

$ |

1,523 |

|

|

$ |

1,651 |

|

| Average realized gold price2 |

|

|

1,411 |

|

|

|

1,608 |

|

|

|

1,518 |

|

|

|

1,651 |

|

| Adjusted operating costs2 |

|

|

552 |

|

|

|

591 |

|

|

|

558 |

|

|

|

568 |

|

| All-in sustaining costs2 |

|

|

919 |

|

|

|

1,061 |

|

|

|

931 |

|

|

|

1,000 |

|

| All-in costs2 |

|

|

1,276 |

|

|

|

1,549 |

|

|

|

1,323 |

|

|

|

1,387 |

|

| Adjusted operating costs (on a co-product basis)

2 |

|

|

580 |

|

|

|

610 |

|

|

|

587 |

|

|

|

587 |

|

| All-in sustaining costs (on a co-product basis)2 |

|

|

947 |

|

|

|

1,080 |

|

|

|

960 |

|

|

|

1,019 |

|

| All-in costs (on a co-product basis)2 |

|

|

1,304 |

|

|

|

1,568 |

|

|

|

1,352 |

|

|

|

1,406 |

|

| Copper production (millions of

pounds) |

|

|

134 |

|

|

|

109 |

|

|

|

261 |

|

|

|

226 |

|

| Copper sold (millions of pounds) |

|

|

135 |

|

|

|

116 |

|

|

|

250 |

|

|

|

234 |

|

| Per pound data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average spot copper price |

|

$ |

3.24 |

|

|

$ |

3.57 |

|

|

$ |

3.42 |

|

|

$ |

3.67 |

|

| Average realized copper price2 |

|

|

3.28 |

|

|

|

3.45 |

|

|

|

3.41 |

|

|

|

3.62 |

|

| C1 cash costs2 |

|

|

1.75 |

|

|

|

2.21 |

|

|

|

2.08 |

|

|

|

2.13 |

|

| Depreciation3 |

|

|

0.42 |

|

|

|

0.59 |

|

|

|

0.38 |

|

|

|

0.51 |

|

| Other4 |

|

|

0.10 |

|

|

|

(0.02 |

) |

|

|

0.15 |

|

|

|

0.09 |

|

| C3 fully allocated costs2 |

|

|

2.27 |

|

|

|

2.78 |

|

|

|

2.61 |

|

|

|

2.73 |

|

| |

|

| Financial Results (millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenues |

|

$ |

3,201 |

|

|

$ |

3,244 |

|

|

$ |

6,600 |

|

|

$ |

6,846 |

|

| Net earnings (loss)5 |

|

|

(8,555 |

) |

|

|

787 |

|

|

|

(7,708 |

) |

|

|

1,826 |

|

| Adjusted net earnings2 |

|

|

663 |

|

|

|

821 |

|

|

|

1,586 |

|

|

|

1,917 |

|

| Operating cash flow |

|

|

896 |

|

|

|

919 |

|

|

|

1,992 |

|

|

|

2,293 |

|

| Adjusted operating cash flow2 |

|

|

804 |

|

|

|

919 |

|

|

|

1,974 |

|

|

|

2,395 |

|

| Per Share Data

(dollars) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings (loss) (basic) |

|

|

(8.55 |

) |

|

|

0.79 |

|

|

|

(7.70 |

) |

|

|

1.83 |

|

| Adjusted net earnings (basic)2 |

|

|

0.66 |

|

|

|

0.82 |

|

|

|

1.58 |

|

|

|

1.92 |

|

| Net earnings (loss) (diluted) |

|

|

(8.55 |

) |

|

|

0.79 |

|

|

|

(7.70 |

) |

|

|

1.83 |

|

| Weighted average basic common shares

(millions) |

|

|

1,001 |

|

|

|

1,000 |

|

|

|

1,001 |

|

|

|

1,000 |

|

| Weighted average diluted common shares

(millions)6 |

|

|

1,001 |

|

|

|

1,001 |

|

|

|

1,001 |

|

|

|

1,001 |

|

| |

|

| |

|

|

|

|

|

|

|

As at June 30, |

|

|

As at

December 31, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

2013 |

|

|

2012 (restated)7 |

|

| |

|

| Financial Position (millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and equivalents |

|

|

|

|

|

|

|

|

|

$ |

2,422 |

|

|

$ |

2,097 |

|

| Non-cash working capital |

|

|

|

|

|

|

|

|

|

|

3,415 |

|

|

|

2,884 |

|

| |

|

| |

1 |

Production includes our equity share of gold production at Highland Gold up to April 26, 2012, the effective date of our sale of Highland Gold.

Production also includes African Barrick Gold on a 73.9% basis and Pueblo Viejo on a 60% basis, both of which reflect our equity share of production. |

| |

2 |

Realized price, adjusted operating costs, all-in sustaining costs, all-in costs, C1 cash costs, C3 fully allocated costs, adjusted net earnings and adjusted

operating cash flow are non-gaap financial performance measures with no standard definition under IFRS. Refer to the Non-Gaap Financial Performance Measures section of the Company’s MD&A. |

| |

3 |

Represents equity depreciation expense divided by equity ounces of gold sold or pounds of copper sold. |

| |

4 |

For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound in the Non-Gaap Financial Performance Measures

section of the Company’s MD&A. |

| |

5 |

Net earnings represents net income attributable to the equity holders of the Company. |

| |

6 |

Fully diluted includes dilutive effect of stock options. |

| |

7 |

Balances related to 2012 have been restated to reflect the impact of the adoption of new accounting pronouncements. See note 2B of the interim consolidated

financial statements. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

8 |

|

SUMMARY INFORMATION |

Production and Cost Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Gold Production (attributable ounces) (000’s) |

|

|

|

All-in sustaining costs4 ($/oz) |

|

|

|

|

|

| |

|

|

|

Three months ended June 30, |

|

Six months ended June 30, |

|

Three months ended June 30, |

|

Six months ended June 30, |

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

2013 |

|

2012 |

|

2013 |

|

2012 |

|

|

|

2013 |

|

|

|

2012 |

|

|

|

2013 |

|

|

|

2012 |

| |

|

|

|

|

|

|

| Gold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| North America |

|

|

|

928 |

|

854 |

|

1,800 |

|

1,742 |

|

$ |

|

797 |

|

$ |

|

894 |

|

$ |

|

789 |

|

$ |

|

850 |

| South America |

|

|

|

296 |

|

327 |

|

666 |

|

778 |

|

|

|

821 |

|

|

|

929 |

|

|

|

765 |

|

|

|

773 |

| Australia Pacific |

|

|

|

465 |

|

445 |

|

912 |

|

871 |

|

|

|

1,033 |

|

|

|

1,201 |

|

|

|

1,065 |

|

|

|

1,154 |

| African Barrick Gold1 |

|

|

|

122 |

|

113 |

|

230 |

|

220 |

|

|

|

1,416 |

|

|

|

1,536 |

|

|

|

1,507 |

|

|

|

1,465 |

| Other2 |

|

|

|

- |

|

3 |

|

- |

|

12 |

|

|

|

- |

|

|

|

- |

|

|

|

- |

|

|

|

- |

| |

| Total |

|

|

|

1,811 |

|

1,742 |

|

3,608 |

|

3,623 |

|

$ |

|

919 |

|

$ |

|

1,061 |

|

$ |

|

931 |

|

$ |

|

1,000 |

| |

|

|

|

|

| |

|

Copper Production (attributable pounds) (millions) |

|

|

|

C1 Cash Costs ($ /lb) |

|

|

|

|

|

| |

|

|

|

Three months ended June 30, |

|

Six months ended June 30, |

|

Three months ended

June 30, |

|

Six months ended June 30, |

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

2013 |

|

2012 |

|

2013 |

|

2012 |

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

| |

| Total |

|

|

|

134 |

|

109 |

|

261 |

|

226 |

|

$ |

|

1.75 |

|

$ |

|

2.21 |

|

$ |

|

2.08 |

|

$ |

|

2.13 |

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Gold Production Costs ($/oz) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

Three months ended

June 30, |

|

Six months ended June 30, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

|

|

|

|

|

|

|

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

| |

|

|

| Direct mining costs at market foreign exchange rates |

|

|

|

$ |

|

602 |

|

$ |

|

620 |

|

$ |

|

608 |

|

$ |

|

607 |

| Gains realized on currency hedge and commodity hedge/economic hedge contracts |

|

|

|

(42) |

|

|

|

(40) |

|

|

|

(46) |

|

|

|

(49) |

| Other3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

(14) |

|

|

|

(12) |

|

|

|

(14) |

|

|

|

(13) |

| By-product credits |

|

|

|

|

|

|

|

|

|

|

|

|

|

(27) |

|

|

|

(18) |

|

|

|

(28) |

|

|

|

(17) |

| Royalties |

|

|

|

|

|

|

|

|

|

|

|

|

|

33 |

|

|

|

41 |

|

|

|

38 |

|

|

|

40 |

| |

| Adjusted operating costs4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

552 |

|

|

|

591 |

|

|

|

558 |

|

|

|

568 |

| Depreciation |

|

|

|

|

|

|

|

|

|

|

|

|

|

210 |

|

|

|

188 |

|

|

|

203 |

|

|

|

185 |

| Other3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

|

12 |

|

|

|

14 |

|

|

|

13 |

| |

| Total production costs |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

776 |

|

$ |

|

791 |

|

$ |

|

775 |

|

$ |

|

766 |

| |

| Adjusted operating costs4 |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

552 |

|

$ |

|

591 |

|

$ |

|

558 |

|

$ |

|

568 |

| General & administrative costs |

|

|

|

|

|

|

|

37 |

|

|

|

59 |

|

|

|

44 |

|

|

|

59 |

| Rehabilitation - accretion and amortization |

|

|

|

|

|

19 |

|

|

|

21 |

|

|

|

22 |

|

|

|

20 |

| Mine on-site exploration and evaluation costs |

|

|

|

|

|

9 |

|

|

|

17 |

|

|

|

8 |

|

|

|

14 |

| Mine development expenditures |

|

|

|

|

|

|

|

173 |

|

|

|

173 |

|

|

|

164 |

|

|

|

166 |

| Sustaining capital expenditures |

|

|

|

|

|

|

|

129 |

|

|

|

200 |

|

|

|

135 |

|

|

|

173 |

| |

| All-in sustaining costs4 |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

919 |

|

$ |

|

1,061 |

|

$ |

|

931 |

|

$ |

|

1,000 |

| |

| All-in costs4 |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

1,276 |

|

$ |

|

1,549 |

|

$ |

|

1,323 |

|

$ |

|

1,387 |

| |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Copper Production Costs ($/lb) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

Three months ended June 30, |

|

Six months ended June 30, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Unaudited) |

|

|

|

|

|

|

|

|

|

|

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

|

|

|

2013 |

|

|

|

2012 (restated) 6 |

| |

|

|

| C1 cash costs4 |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

1.75 |

|

$ |

|

2.21 |

|

$ |

|

2.08 |

|

$ |

|

2.13 |

| Depreciation |

|

|

|

|

|

|

|

|

|

|

|

|

|

0.42 |

|

|

|

0.59 |

|

|

|

0.38 |

|

|

|

0.51 |

| Other5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

0.10 |

|

|

|

(0.02) |

|

|

|

0.15 |

|

|

|

0.09 |

| |

| C3 fully allocated costs4 |

|

|

|

|

|

|

|

|

|

|

|

$ |

|

2.27 |

|

$ |

|

2.78 |

|

$ |

|

2.61 |

|

$ |

|

2.73 |

| |

| |

1 |

Figures relating to African Barrick Gold are presented on a 73.9% basis, which reflects our equity share of production. |

| |

2 |

Includes our equity share of gold production at Highland Gold up to April 26, 2012, the effective date of our sale of Highland Gold.

|

| |

3 |

Represents the Barrick Energy gross margin divided by equity ounces of gold sold. |

| |

4 |

Adjusted operating costs, all-in sustaining costs, all-in costs, C1 cash costs and C3 fully allocated costs are non-gaap financial performance measures with

no standard meaning under IFRS. Refer to the Non-Gaap Financial Performance Measures section of the Company’s MD&A. |

| |

5 |

For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound in the Non-Gaap Financial Performance Measures

section of the Company’s MD&A. |

| |

6 |

Balances related to 2012 have been restated to reflect the impact of the adoption of new accounting pronouncements. See note 2B of the interim consolidated

financial statements. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

9 |

|

SUMMARY INFORMATION |

MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

This portion of the Quarterly Report provides management’s discussion and analysis

(“MD&A”) of the financial condition and results of operations to enable a reader to assess material changes in financial condition and results of operations as at and for the three and six month periods ended June 30, 2013, in

comparison to the corresponding prior-year period. The MD&A is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial

performance and present and future business environment. This MD&A, which has been prepared as of July 31, 2013, is intended to supplement and complement the condensed unaudited interim consolidated financial statements and notes thereto,

prepared in accordance with International Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), for the three and six month periods ended June 30,

2013 (collectively, the “Financial Statements”), which are included in this Quarterly Report on pages 49 to 78. You are encouraged to review the Financial Statements in conjunction with your review of this MD&A. This MD&A should be

read in conjunction with both the annual audited

consolidated financial statements for the two years ended December 31, 2012, the related annual MD&A included in the 2012 Annual Report, and the most recent Form 40–F/Annual

Information Form on file with the US Securities and Exchange Commission (“SEC”) and Canadian provincial securities regulatory authorities. Certain notes to the Financial Statements are specifically referred to in this MD&A and such

notes are incorporated by reference herein. All dollar amounts in this MD&A are in millions of US dollars, unless otherwise specified.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a

significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the

total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this MD&A, including any

information as to our strategy, projects, plans or future financial or operating performance constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words

“believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “intend”, “continue”, “budget”, “estimate”, “may”, “will”,

“schedule” and similar expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company, are inherently subject to

significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements. Such factors include, but are not

limited to: fluctuations in the spot and forward price of gold and copper or certain other commodities (such as silver, diesel fuel and electricity); changes in national and local government legislation, taxation, controls,

regulations, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company does or may carry on

business in the future; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital projects; the impact of global liquidity and credit availability on the

timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit rating; the impact of inflation; fluctuations in the currency markets; operating or technical difficulties in

connection with mining or development activities; the speculative nature of mineral exploration and development, including the risks of obtaining necessary licenses and permits; contests over title to properties, particularly title to undeveloped

properties; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; litigation; business opportunities that may be presented to, or

pursued by, the Company; our

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

10 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

ability to successfully integrate acquisitions or complete divestitures; employee relations; availability and increased costs associated with mining inputs and labor; and the organization of our

African gold operations and properties under a separate listed company. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents,

unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion, copper cathode or gold/copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these

uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or

implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking

statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a

discussion of some of the factors underlying forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as

required by applicable law.

CHANGES IN PRESENTATION OF NON-GAAP FINANCIAL PERFORMANCE MEASURES

Beginning with our 2012 Annual Report, we adopted a non-GAAP “all-in sustaining costs per

ounce” measure. This was based on the expectation that the World Gold Council (“WGC”) (a market development organization for the gold industry made up of and funded by 18 gold mining companies from around the world, including Barrick)

was developing a similar metric and that investors and industry analysts were interested in a measure that better represented the total recurring costs associated with producing gold. The WGC is not a regulatory organization. In June 2013, the WGC

published its definition of “adjusted operating costs”, “all-in sustaining costs” and also a definition of “all-in costs.” Barrick is voluntarily adopting the definition of these metrics starting with this MD&A.

The “all-in sustaining costs” measure is similar to our presentation in previous reports, with the exception of the

classification of sustaining capital. In our previous calculation, certain capital expenditures were presented as mine expansion projects, whereas they meet the definition of sustaining capital expenditures under the WGC definition, and therefore

these expenditures have been reclassified as sustaining capital expenditures.

The new “all-in costs” measure starts with

“all-in sustaining costs” and adds additional costs, which reflect the varying costs of producing gold over the life-cycle of a mine, including: non-sustaining capital expenditures (capital expenditures at new projects and capital

expenditures at existing operations that

significantly increase the productive capacity of the mine), and other non-sustaining costs (primarily exploration and evaluation (“E&E”) costs, community relations costs and

general and administrative costs that are not associated with current operations). This definition recognizes that there are different costs associated with the life-cycle of a mine and that it is therefore appropriate to distinguish between

sustaining and non-sustaining costs.

We believe that “All-in sustaining costs” and “all-in costs” will better meet

the needs of analysts, investors and other stakeholders of Barrick in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing our operating performance and also our ability to generate free cash

flow from current operations and to generate free cash flow on an overall Company basis. Due to the capital intensive nature of the industry and the long useful lives over which these items are depreciated, there can be a disconnect between net

earnings calculated in accordance with IFRS and the amount of free cash flow that is being generated by a mine. In the current market environment for gold mining equities, many investors and analysts are more focused on the ability of gold mining

companies to generate free cash flow from current operations, and consequently we believe these measures are useful non-GAAP operating metrics and supplement our IFRS disclosures. These measures are not representative of all of our cash expenditures

as they do not include income tax payments, interest costs or dividend payments. “All-

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

11 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

in sustaining costs” and “all-in costs” are intended to provide additional information only and do not have standardized definitions under IFRS and should not be considered in

isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Although the WGC has published a

standardized definition, other companies may calculate these measures differently.

This quarter we have also renamed the non-GAAP

measure “total cash costs” with “adjusted operating

costs” in order to conform with the WGC definition of the comparable measure. The manner in which this measure is calculated has not been changed.

We have also calculated these metrics on a co-product basis, which removes the impact of other metal sales that are produced as a by-product of our

gold production.

The table on page 47 reconciles these non-GAAP measures to the most directly comparable IFRS measures and previous

periods have been recalculated to conform to our current definition.

INDEX

|

|

|

|

|

| |

|

page |

|

| Overview |

|

|

|

|

|

|

| Review of 2013 Second Quarter Results |

|

|

13 |

|

|

|

| Key Business Developments |

|

|

16 |

|

|

|

| Business Update and Full year 2013 Outlook |

|

|

17 |

|

|

|

| Market Overview |

|

|

19 |

|

|

|

| Review of Financial Results |

|

|

|

|

|

|

| Revenues |

|

|

22 |

|

|

|

| Production Costs |

|

|

22 |

|

|

|

| Corporate Administration |

|

|

23 |

|

|

|

| Other Expense (Income) |

|

|

23 |

|

|

|

| Exploration and Evaluation |

|

|

23 |

|

|

|

| Capital Expenditures |

|

|

23 |

|

|

|

| Finance Cost/ Finance Income |

|

|

24 |

|

|

|

| Impairment Charges |

|

|

24 |

|

|

|

| Income Tax |

|

|

25 |

|

|

|

| Operational Overview |

|

|

25 |

|

|

|

| Review of Operating Segments Performance |

|

|

26 |

|

|

|

| Financial Condition Review |

|

|

|

|

|

|

| Balance Sheet Review |

|

|

34 |

|

|

|

| Financial Position and Liquidity |

|

|

35 |

|

|

|

| Financial Instruments |

|

|

38 |

|

|

|

| Commitments and Contingencies |

|

|

38 |

|

|

|

| Adoption of Advance Notice By-law |

|

|

39 |

|

|

|

| Review of Quarterly Results |

|

|

40 |

|

|

|

| IFRS Critical Accounting Policies and Estimates |

|

|

40 |

|

|

|

| Non-GAAP Financial Performance Measures |

|

|

45 |

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

12 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

Review of 2013 Second Quarter Results

2013 Second Quarter Results

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ($ millions, except where indicated) |

|

For the three months ended June 30 |

|

|

For the six months ended June 30 |

|

| |

|

| |

|

2013 |

|

|

2012 |

|

|

2013 |

|

|

2012 |

|

| |

|

| Financial Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenue |

|

|

$ 3,201 |

|

|

|

$ 3,244 |

|

|

|

$ 6,600 |

|

|

|

$ 6,846 |

|

| Net earnings (loss)1 |

|

|

(8,555) |

|

|

|

787 |

|

|

|

(7,708) |

|

|

|

1,826 |

|

| Per share (“EPS”)2 |

|

|

(8.55) |

|

|

|

0.79 |

|

|

|

(7.70) |

|

|

|

1.83 |

|

| Adjusted net earnings3 |

|

|

663 |

|

|

|

821 |

|

|

|

1,586 |

|

|

|

1,917 |

|

| Per share (“adjusted EPS”)2,3 |

|

|

0.66 |

|

|

|

0.82 |

|

|

|

1.58 |

|

|

|

1.92 |

|

| Total project capital expenditures4 |

|

|

686 |

|

|

|

700 |

|

|

|

1,301 |

|

|

|

1,330 |

|

| Total capital expenditures - expansion, sustaining and mine development4 |

|

|

779 |

|

|

|

839 |

|

|

|

1,502 |

|

|

|

1,491 |

|

| Operating cash flow |

|

|

896 |

|

|

|

919 |

|

|

|

1,992 |

|

|

|

2,293 |

|

| Adjusted operating cash flow3 |

|

|

804 |

|

|

|

919 |

|

|

|

1,974 |

|

|

|

2,395 |

|

| Free cash flow3 |

|

|

$ (752) |

|

|

|

($ 797) |

|

|

|

$ (967) |

|

|

|

($ 680) |

|

| Adjusted return on equity3 |

|

|

15% |

|

|

|

13% |

|

|

|

18% |

|

|

|

16% |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| Operating Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold produced (000s ounces)5 |

|

|

1,811 |

|

|

|

1,742 |

|

|

|

3,608 |

|

|

|

3,623 |

|

| Gold sold (000s ounces) |

|

|

1,815 |

|

|

|

1,690 |

|

|

|

3,562 |

|

|

|

3,473 |

|

| Realized price ($ per ounce)3 |

|

|

$ 1,411 |

|

|

|

$ 1,608 |

|

|

|

$ 1,518 |

|

|

|

$ 1,651 |

|

| Adjusted operating costs ($ per

ounce)3 |

|

|

$ 552 |

|

|

|

$ 591 |

|

|

|

$ 558 |

|

|

|

$ 568 |

|

| Adjusted operating costs on a co-product basis ($ per

ounce)3 |

|

|

$ 580 |

|

|

|

$ 610 |

|

|

|

$ 587 |

|

|

|

$ 587 |

|

| All-in sustaining costs ($ per

ounce)3 |

|

|

$ 919 |

|

|

|

$ 1,061 |

|

|

|

$ 931 |

|

|

|

$ 1,000 |

|

| All-in sustaining costs on a co-product basis ($ per

ounce)3 |

|

|

$ 947 |

|

|

|

$ 1,080 |

|

|

|

$ 960 |

|

|

|

$ 1,019 |

|

| All-in costs ($ per ounce)3 |

|

|

$ 1,276 |

|

|

|

$ 1,549 |

|

|

|

$ 1,323 |

|

|

|

$ 1,387 |

|

| All-in costs on a co-product basis ($ per

ounce)3 |

|

|

$ 1,304 |

|

|

|

$ 1,568 |

|

|

|

$ 1,352 |

|

|

|

$ 1,406 |

|

| Copper |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Copper produced (millions of pounds) |

|

|

134 |

|

|

|

109 |

|

|

|

261 |

|

|

|

226 |

|

| Copper sold (millions of pounds) |

|

|

135 |

|

|

|

116 |

|

|

|

250 |

|

|

|

234 |

|

| Realized price ($ per pound)3 |

|

|

$ 3.28 |

|

|

|

$ 3.45 |

|

|

|

$ 3.41 |

|

|

|

$ 3.62 |

|

| C1 cash costs ($ per pound)3 |

|

|

$ 1.75 |

|

|

|

$ 2.21 |

|

|

|

$ 2.08 |

|

|

|

$ 2.13 |

|

| |

|

| |

1 |

Net earnings (loss) represent net income attributable to the equity holders of the Company. |

| |

2 |

Calculated using weighted average number of shares outstanding under the basic method. |

| |

3 |

These are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see

pages 45 - 48 of this MD&A. |

| |

4 |

These amounts are presented on a cash basis consistent with the amounts presented on the consolidated cash flows. |

| |

5 |

We sold our 20.4% investment in Highland Gold with an effective date of April 26, 2012. Production includes our equity share of gold production at

Highland Gold up to that date. |

Key Highlights:

| |

• |

|

Overall, our high quality portfolio of mines provided strong underlying operating results in the first half of 2013, and we remain on track to meet our

original production guidance, at lower adjusted operating costs and all-in sustaining costs compared to our original guidance. |

| |

• |

|

During the second quarter 2013, the market prices of gold, silver and copper declined significantly. These metal prices are the primary drivers of our ability

to generate earnings and cash flow, and as a result, this sustained drop in metal prices has had a significant impact on our business, and in particular our financial position and liquidity, and has been the primary cause of the impairments we

recorded against the carrying value of our goodwill and non-current assets, including our Pascua-Lama project. (Please refer to pages 35 to 37 and 41 to 44 of this MD&A for further information on liquidity risks and impairments, respectively.)

|

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

13 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

• |

|

In second quarter 2013, we recorded impairments against the carrying value of our goodwill and non-current assets totaling $8.7 billion (net of tax and

non-controlling interest effects). This included $5.1 billion against the carrying value of our Pascua-Lama project as a result of the significant decrease in long-term gold and silver price assumptions, as well as the schedule delay and related

capital cost increase. Other significant impairments recorded in the quarter include $2.3 billion in goodwill impairments in our global copper, Australia Pacific, Capital Projects and African Barrick Gold segments. |

| |

• |

|

The fair values in the impairment assessment were calculated as at June 30 assuming metal prices that were influenced by only recent spot price declines,

yet which are then applied and held constant over mine lives that in some instances are in excess of 25 years. As a result of these significant price declines, we have revised our gold, copper and silver price assumptions utilized for impairment

testing to $1,300 per ounce, $3.25 per pound and $23 per ounce, respectively. We are confident our assets will generate substantially more economic benefits over time for our shareholders than these current valuation levels imply. Although Barrick

does not rely on higher prices to drive its business plans, we remain positive on long term price fundamentals for these metals. With higher prices in the future, we would reassess the fair value of our high quality, long-life assets such as

Pascua-Lama, and could potentially reverse some of the impairment charges recorded. |

SECOND QUARTER FINANCIAL AND OPERATING HIGHLIGHTS

| |

• |

|

Net loss in the second quarter 2013 was $8.6 billion compared to net earnings of $787 million recorded in second quarter 2012. The decrease reflects the

impact of impairment charges of $8.7 billion (net of tax and non- controlling interest effects), lower realized gold and copper prices and higher interest expense primarily as a result of lower capitalized interest, partially offset by higher gold

and copper sales volumes. Adjusted net earnings for the second quarter 2013 were $663 million compared to adjusted net earnings of $821 million recorded in second quarter 2012. The decrease reflects lower realized gold and copper prices and higher

cost of sales applicable to gold, partially offset by higher gold and copper sales volumes. |

| |

• |

|

EPS and adjusted EPS for the second quarter 2013 were $(8.55) and $0.66. The decreases over the same prior year period were due to the decrease in both net

earnings and adjusted net earnings, as described above. |

| |

• |

|

Gold production for the second quarter 2013 was 1.81 million ounces, up 4% from the same prior year period, due to higher production in North America and

Australia Pacific, partially offset by lower production in South America. |

| |

• |

|

Adjusted operating costs for the second quarter 2013 were $552 per ounce, down 7% over the same prior year period. The decrease reflects higher direct mining

costs largely due to the impact of processing more ore tons at lower grades, which were more than offset by the increase in sales volumes. All-in sustaining costs for the second quarter 2013 were $919 per ounce, down 13% over the same prior year

period primarily reflecting lower adjusted operating costs and decreases in general & administrative costs and sustaining capital expenditures. All-in costs for the second quarter 2013 were $1,276 per ounce, down 18% over the same prior

year period primarily reflecting lower all-in sustaining costs and lower non-sustaining capital as a result of the construction slow-down at Pascua-Lama and the completion of our Pueblo Viejo project. |

|

|

|

|

|

| BARRICK SECOND QUARTER 2013 |

|

14 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

| |

• |

|

Copper production for the second quarter 2013 was 134 million pounds, up 23% over the same prior year period, due to higher production from Lumwana.

Copper C1 cash costs for the second quarter 2013 were $1.75 per pound, down 21% over the same prior year period, primarily due to lower operating costs at Lumwana. |

| |

• |

|

Significant adjusting items (net of tax and non-controlling interest effects) in the second quarter 2013 include: $8.7 billion in impairment charges; $475

million in re-measurement losses related to the disposition of Barrick Energy; $86 million in project care and maintenance and demobilization costs; and $21 million in restructuring costs related to the company-wide overhead review; partially offset

by $23 million in realized and unrealized gains on non-hedge derivative instruments; and $8 million in unrealized foreign currency translation gains on working capital balances. |

| |

• |

|

Operating cash flow for the second quarter 2013 was $896 million, down 3% over the same prior year period. The decrease in operating cash flow primarily