PG&E Corporation 8-K

Exhibit 99.1

Business Update Investing in California’s Prosperity November 28, 2023

2 Forward - Looking Statements This presentation contains statements regarding PG&E Corporation’s and Pacific Gas and Electric Company’s (the “Utility”) fut ure performance, including expectations, objectives, and forecasts about operating results (including 2023 and 2024 non - GAAP core earnings), equity needs, rate base growth, capital expenditures, cost reductions , wildfire risk mitigation, and regulatory developments. These statements and other statements that are not purely historical constitute forward - looking statements that are necessarily subjec t to various risks and uncertainties. Actual results may differ materially from those described in forward - looking statements. PG&E Corporation and the Utility are not able to predict all the factors tha t may affect future results. Factors that could cause actual results to differ materially include, but are not limited to, risks and uncertainties associated with: • wildfires that have occurred in the Utility’s territory, including the extent of the Utility’s liability in connection with t he 2019 Kincade fire, the 2020 Zogg fire, the 2021 Dixie fire, the 2022 Mosquito fire, and future wildfires; • the Utility’s ability to recover wildfire - related costs, including costs for the 2021 Dixie fire, from the Wildfire Fund (includ ing the Utility’s maintenance of a valid safety certificate and whether the Wildfire Fund has sufficient remaining funds) and through the WEMA and FERC TO rate cases; • the Utility’s implementation of its wildfire mitigation programs, including PSPS, EPSS, situational awareness and response, t he undergrounding initiative, and the programs’ effectiveness; • the Utility’s ability to safely and reliably operate, maintain, construct, and decommission its facilities; • changes in the electric power and gas industries driven by technological advancements and a decarbonized economy; • a cyber incident, cybersecurity breach, severe natural event, or physical attack; • severe weather conditions, extended drought, and climate change, particularly their impact on the likelihood and severity of wil dfires; • the impact of legislative and regulatory developments, including those regarding wildfires, the environment, California’s cle an energy goals, the nuclear industry, extended operations at Diablo Canyon nuclear power plant, regulation of utilities’ transactions with their affiliates, municipalization, privacy, and taxes ; • the timing and outcome of FERC and CPUC proceedings, including regarding ratemaking , cost recovery, and the application to transfer non - nuclear generation assets; • the outcome of self - reports, investigations, or other enforcement actions; • PG&E Corporation and the Utility’s substantial indebtedness, which may adversely affect their financial health and limit thei r o perating flexibility; • the ability of PG&E Corporation and the Utility to finance through securitization up to $1.385 billion of remaining fire risk mi tigation capital expenditures that were or will be incurred by the Utility; • the timing and outcome of PG&E Corporation’s and the Utility’s litigation, including securities class action claims and wildf ire - related litigation; • the Utility’s ability to control operating costs, timely recover costs through rates, and achieve projected savings and the e xte nt of excess unrecoverable costs; • the tax treatment of certain assets and liabilities, including whether PG&E Corporation or the Utility undergoes an “ownershi p c hange” that limits certain tax attributes; • the impact of growing distributed and renewable generation resources, and changing customer demand for its natural gas and el ect ric services; and • the other factors disclosed in PG&E Corporation’s and the Utility’s joint Annual R eport on Form 10 - K for the year ended December 31, 2022, their joint Quarterly R eport on Form 10 - Q for the quarter ended September 30 , 2023 (the “Form 10 - Q”) and other reports filed with the SEC, which are available on PG&E Corporation’s website at www.pgecorp. com and on the SEC website at www.sec.gov. Undefined, capitalized terms have the meanings set forth in the Form 10 - Q. Unless otherwise indicated, the statements in this pr esentation are made as of November 28 , 2023. PG&E Corporation and the Utility undertake no obligation to update information contained herein. This presentation furnished as an exhibit to PG&E Co rporation and the Utility’s joint Current Report on Form 8 - K to the SEC on November 28 , 2023 and is also available on PG&E Corporation’s website at www.pgecorp.com.

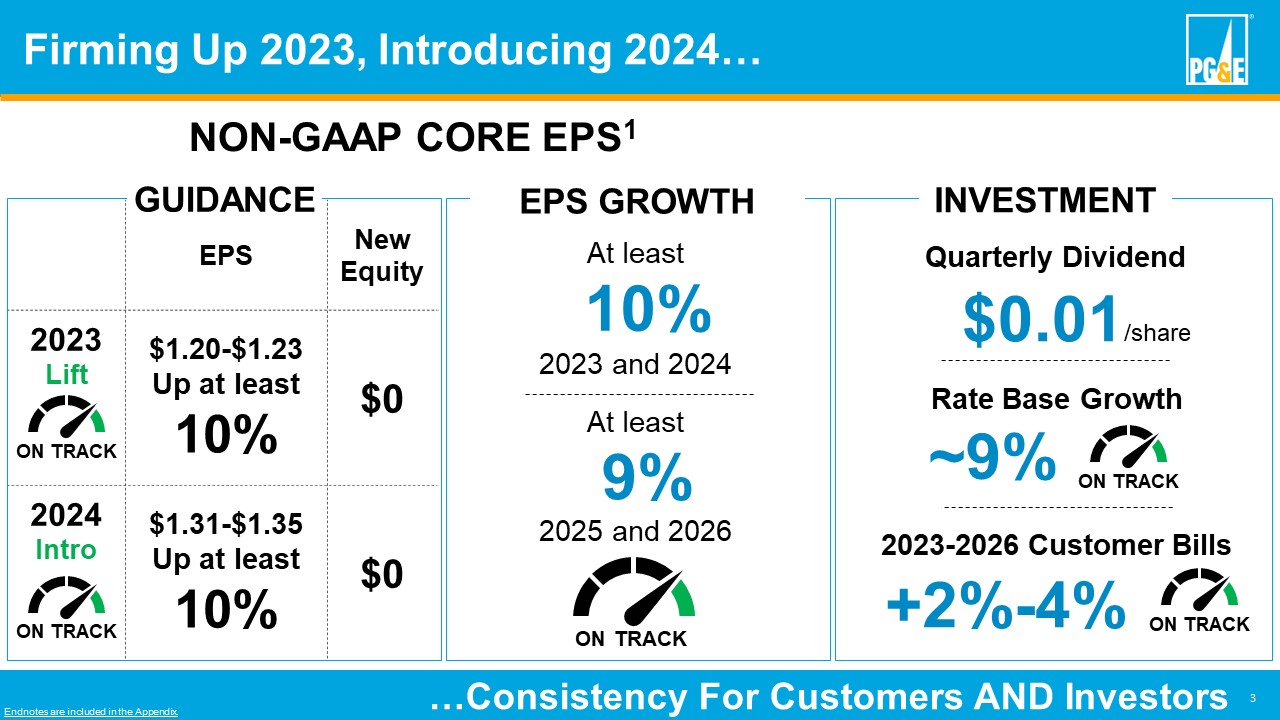

3 Endnotes are included in the Appendix. Firming Up 2023, Introducing 2024… …Consistency For Customers AND Investors New Equity EPS $0 $1.20 - $1.23 Up at least 10% 2023 Lift $0 $1.31 - $1.35 Up at least 10% 2024 Intro NON - GAAP CORE EPS 1 2023 and 2024 10% At least 2025 and 2026 9% At least EPS GROWTH ON TRACK ON TRACK GUIDANCE ON TRACK INVESTMENT $0.01 /share ~9% Rate Base Growth +2% - 4% 2023 - 2026 Customer Bills Quarterly Dividend ON TRACK ON TRACK

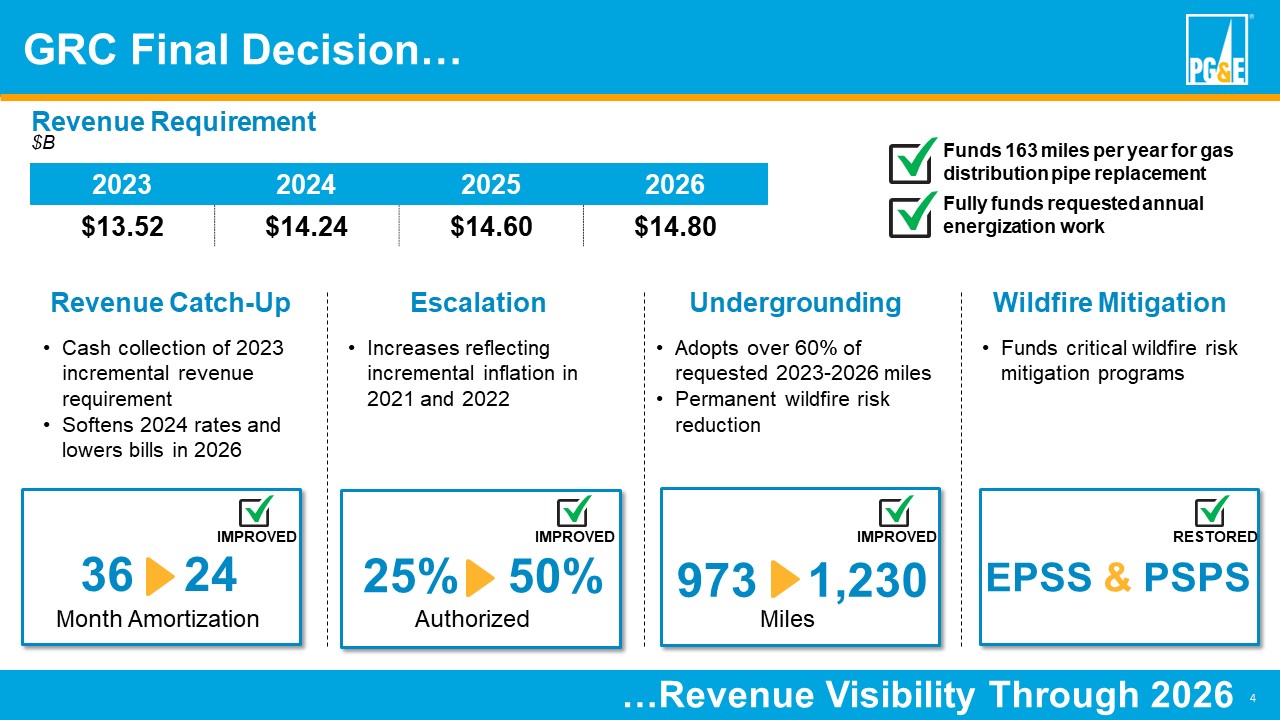

4 GRC Final Decision… …Revenue Visibility Through 2026 2026 2025 2024 2023 $14.80 $14.60 $14.24 $13.52 Revenue Catch - Up • Cash collection of 2023 incremental revenue requirement • Softens 2024 rates and lowers bills in 2026 Escalation • Increases reflecting incremental inflation in 2021 and 2022 Undergrounding • Adopts over 60% of requested 2023 - 2026 miles • Permanent wildfire risk reduction Wildfire Mitigation • F unds critical wildfire risk mitigation programs Authorized Miles EPSS & PSPS Month Amortization Funds 163 miles per year for gas distribution pipe replacement Fully f unds requested annual energization work Revenue Requirement $B IMPROVED 36 24 25% 50% IMPROVED IMPROVED 973 1,230 RESTORED

5 2022 2023 2024 2025 2026 CPUC including GRC Final Decision FERC Customer Capital Investment Opportunities… …Add Another Layer Of Financial Protection Rate Base Weighted Average - $B Potential Incremental CapEx $ 4 B Cost Recovery Applications ~$2B FERC Pending 10 - Year Undergrounding Filing SB 884 ~$74 Up to ~$4B Energization (SB 410) Efficient Financing Cost of Capital Adjustment Diablo Canyon Incentive Lean Management Affordability Drivers 2026 2025 2024 Prior Timing of Capital Investment Opportunities Strengthening Creditworthiness $49.8

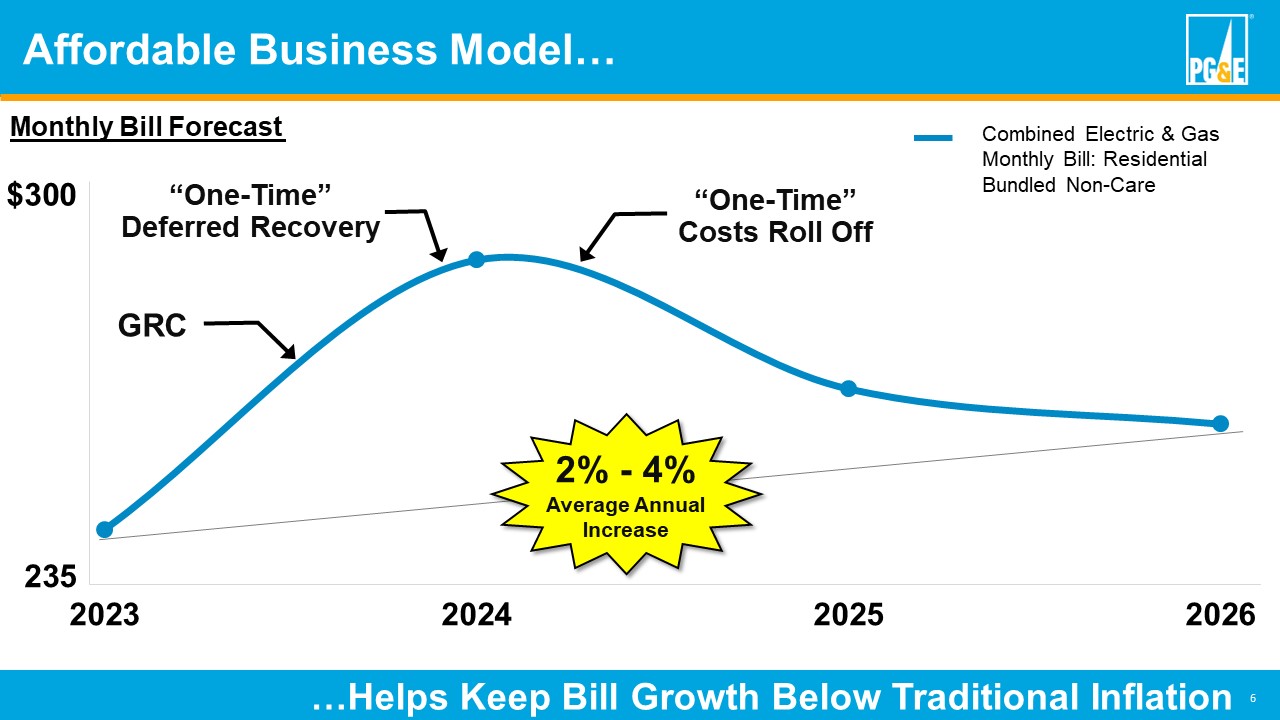

6 Affordable Business Model… …Helps Keep Bill Growth Below Traditional Inflation $235 $300 2023 2024 2025 2026 GRC “One - Time” Deferred Recovery “One - Time” Costs Roll Off Combined Electric & Gas Monthly Bill : Residential Bundled Non - Care Monthly Bill Forecast 2% - 4% Average Annual Increase

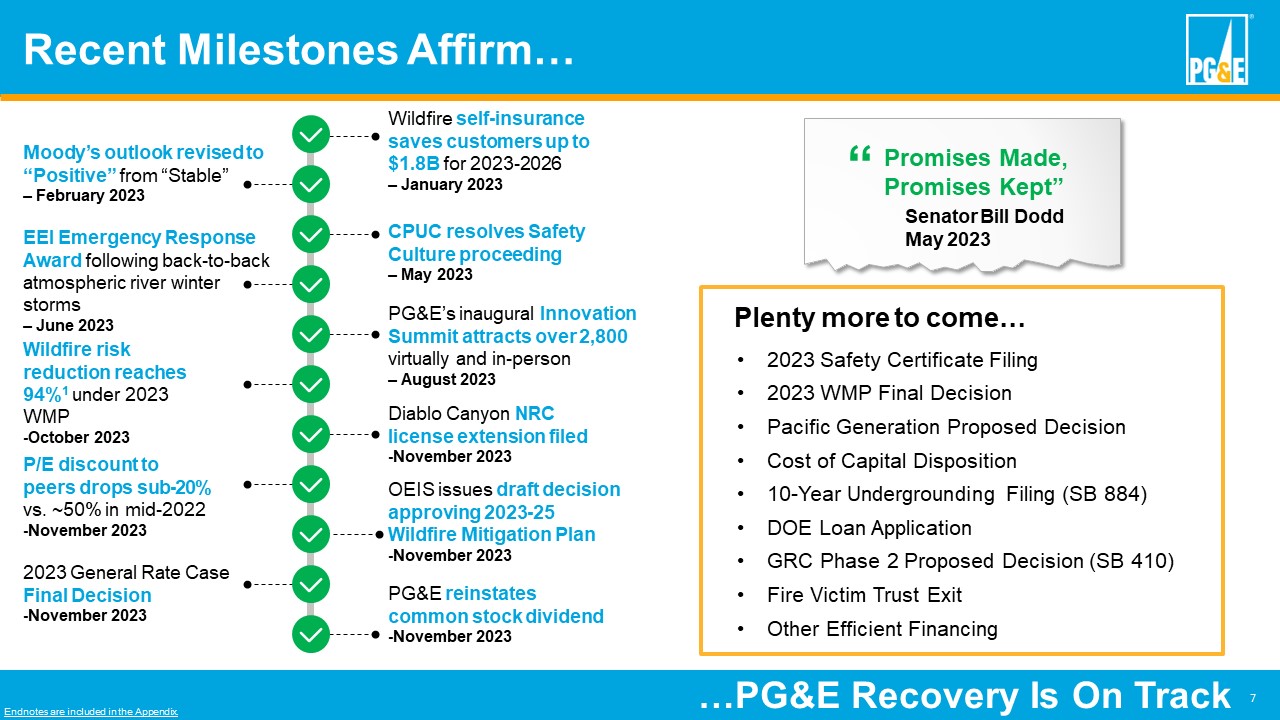

7 Endnotes are included in the Appendix. Recent Milestones Affirm… …PG&E Recovery Is On Track Wildfire self - insurance saves customers up to $1.8B for 2023 - 2026 – January 2023 Moody’s outlook revised to “Positive” from “Stable” – February 2023 CPUC resolves Safety Culture proceeding – May 2023 EEI Emergency Response Award following back - to - back atmospheric river winter storms – June 2023 PG&E’s inaugural Innovation Summit attracts over 2,800 virtually and in - person – August 2023 Diablo Canyon NRC license extension filed - November 2023 Wildfire risk reduction reaches 94% 1 under 2023 WMP - October 2023 2023 General Rate Case Final Decision - November 2023 PG&E reinstates common stock dividend - November 2023 Plenty more to come… • 2023 Safety Certificate Filing • 2023 WMP Final Decision • Pacific Generation Proposed Decision • Cost of Capital Disposition • 10 - Year Undergrounding Filing (SB 884) • DOE Loan Application • GRC Phase 2 Proposed Decision (SB 410) • Fire Victim Trust Exit • Other Efficient Financing OEIS issues draft decision approving 2023 - 25 Wildfire Mitigation Plan - November 2023 P/E discount to peers drops sub - 20% vs. ~50% in mid - 2022 - November 2023 “ Senator Bill Dodd May 2023 Promises Made, Promises Kept”

Q&A Carolyn Burke EVP, Chief Financial Officer Patti Poppe CEO

Appendix

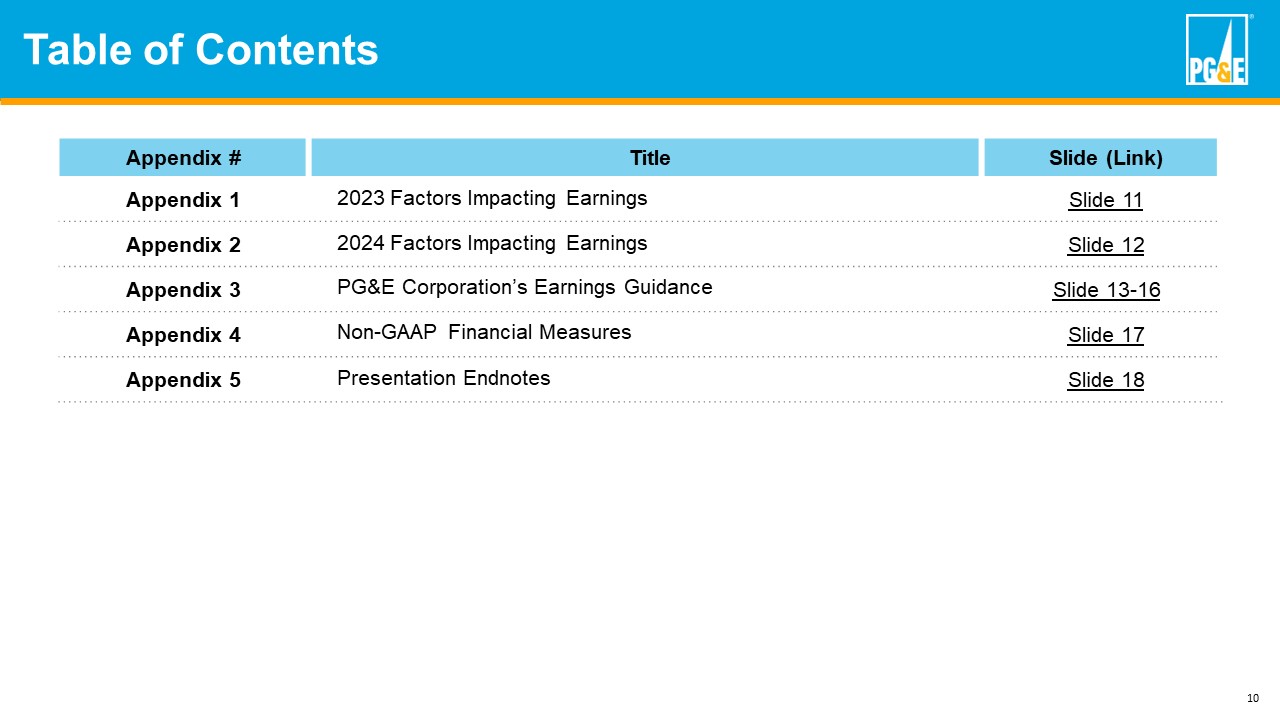

10 Table of Contents Slide (Link) Title Appendix # Slide 11 2023 Factors Impacting Earnings Appendix 1 Slide 12 2024 Factors Impacting Earnings Appendix 2 Slide 13 - 16 PG&E Corporation’s Earnings Guidance Appendix 3 Slide 17 Non - GAAP Financial Measures Appendix 4 Slide 18 Presentation Endnotes Appendix 5

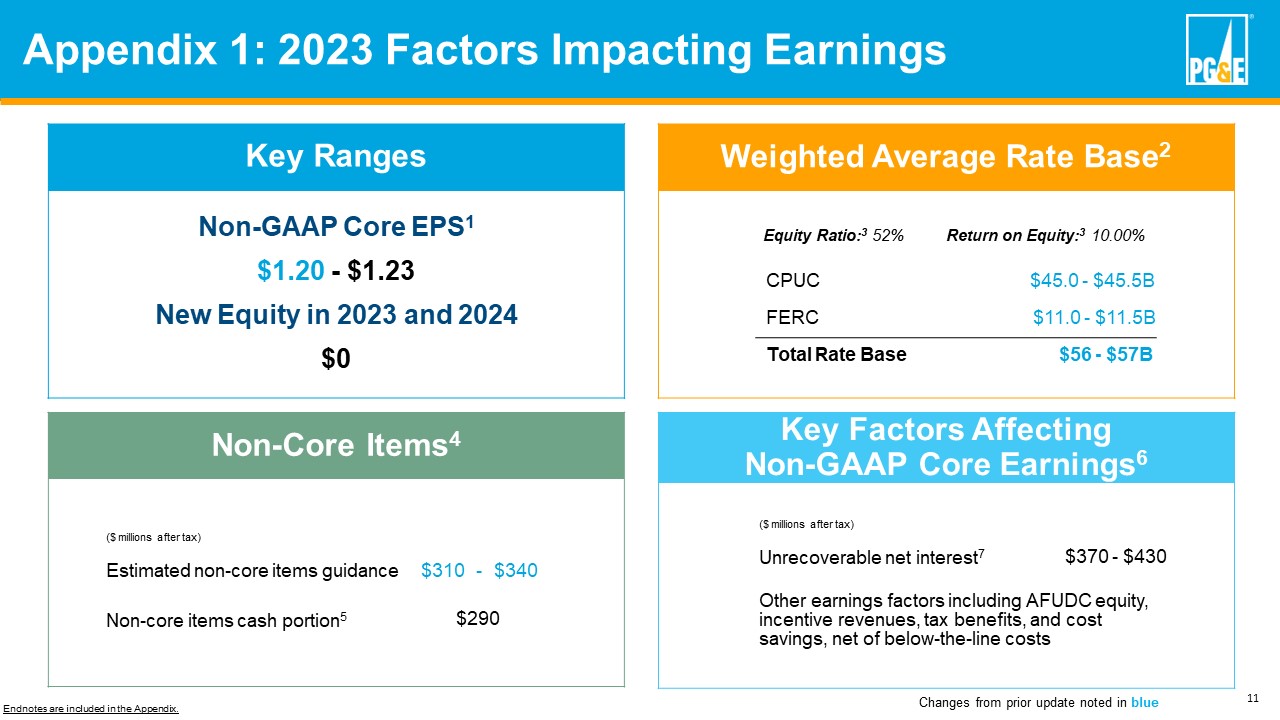

11 Endnotes are included in the Appendix. Non - Core Items 4 Key Factors Affecting Non - GAAP Core Earnings 6 ($ millions after tax) $ 370 - $ 430 Unrecoverable net interest 7 Other earnings factors including AFUDC equity , incentive revenues, tax benefits, and cost savings, net of below - the - line costs Weighted Average Rate Base 2 ($ millions after tax) $ 340 - $ 310 Estimated non - core items guidance $ 29 0 Non - core items cash portion 5 $45.0 - $45.5B CPUC $11.0 - $11.5B FERC $ 56 - $57B Total Rate Base Equity Ratio: 3 52% Return on Equity: 3 10.00 % Key Ranges Non - GAAP Core EPS 1 $1.20 - $1.23 New Equity in 2023 and 2024 $0 Appendix 1: 2023 Factors Impacting Earnings Changes from prior update noted in blue

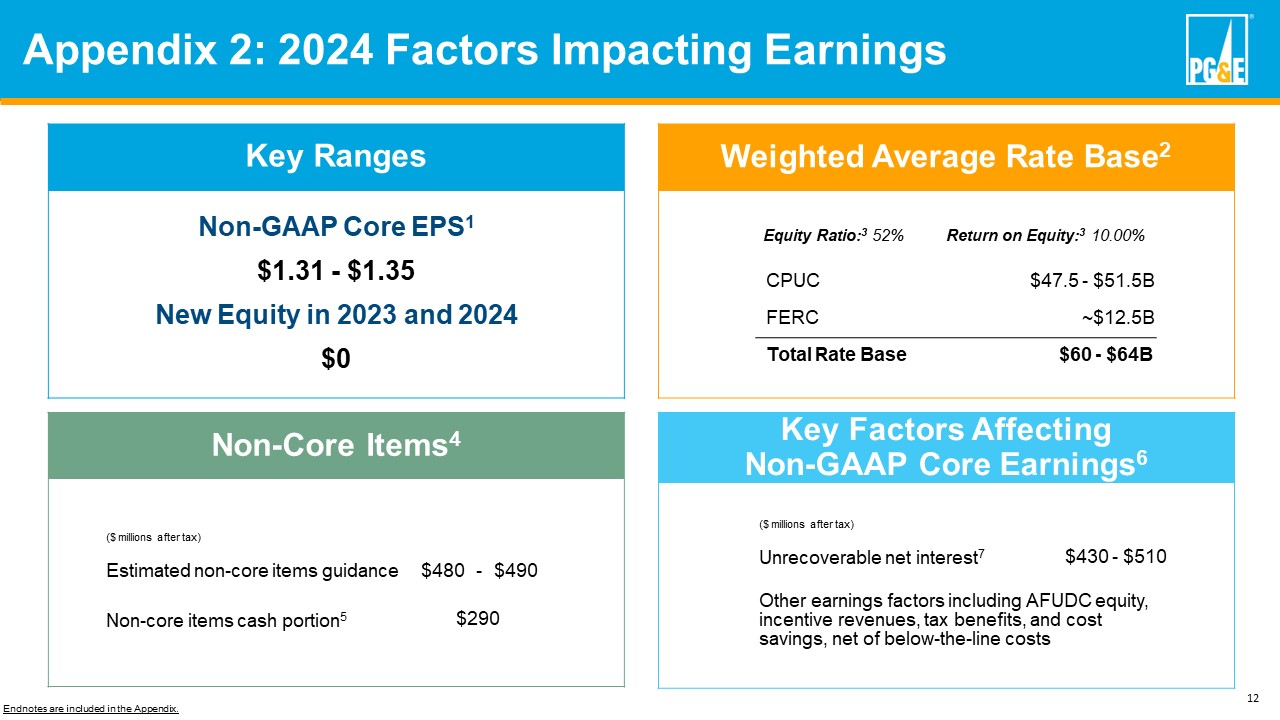

12 Endnotes are included in the Appendix. Non - Core Items 4 Key Factors Affecting Non - GAAP Core Earnings 6 ($ millions after tax) $430 - $ 510 Unrecoverable net interest 7 Other earnings factors including AFUDC equity, incentive revenues, tax benefits, and cost savings, net of below - the - line costs Weighted Average Rate Base 2 ($ millions after tax) $490 - $480 Estimated non - core items guidance $ 29 0 Non - core items cash portion 5 $47.5 - $ 51.5B CPUC ~$ 12.5B FERC $60 - $6 4 B Total Rate Base Equity Ratio: 3 52% Return on Equity: 3 10.00 % Key Ranges Non - GAAP Core EPS 1 $1.31 - $1.35 New Equity in 2023 and 2024 $0 Appendix 2: 2024 Factors Impacting Earnings

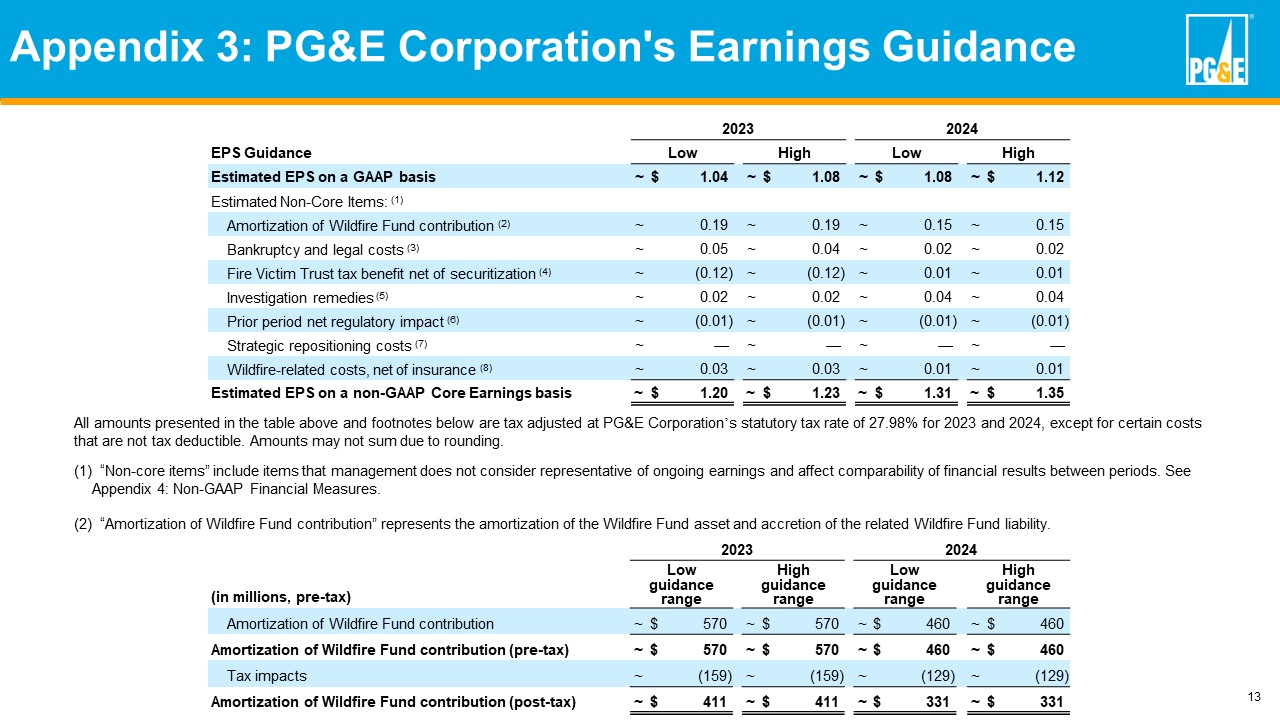

13 All amounts presented in the table above and footnotes below are tax adjusted at PG&E Corporation ’ s statutory tax rate of 27.98% for 2023 and 2024 , except for certain costs that are not tax deductible. Amounts may not sum due to rounding. (1) “Non - core items” include items that management does not consider representative of ongoing earnings and affect comparabilit y of financial results between periods. See Appendix 4 : Non - GAAP Financial Measures. (2) “Amortization of Wildfire Fund contribution” represents the amortization of the Wildfire Fund asset and accretion of the re lated Wildfire Fund liability. Appendix 3: PG&E Corporation's Earnings Guidance 2024 2023 High Low High Low EPS Guidance $ 1.12 ~ $ 1.08 ~ $ 1.08 ~ $ 1.04 ~ Estimated EPS on a GAAP basis Estimated Non - Core Items: (1) 0.15 ~ 0.15 ~ 0.19 ~ 0.19 ~ Amortization of Wildfire Fund contribution (2) 0.02 ~ 0.02 ~ 0.04 ~ 0.05 ~ Bankruptcy and legal costs (3) 0.01 ~ 0.01 ~ (0.12) ~ (0.12) ~ Fire Victim Trust tax benefit net of securitization (4) 0.04 ~ 0.04 ~ 0.02 ~ 0.02 ~ Investigation remedies (5) (0.01) ~ (0.01) ~ (0.01) ~ (0.01) ~ Prior period net regulatory impact (6) — ~ — ~ — ~ — ~ Strategic repositioning costs (7) 0.01 ~ 0.01 ~ 0.03 ~ 0.03 ~ Wildfire - related costs, net of insurance (8) $ 1.35 ~ $ 1.31 ~ $ 1.23 ~ $ 1.20 ~ Estimated EPS on a non - GAAP Core Earnings basis 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ 460 ~ $ 460 ~ $ 570 ~ $ 570 ~ Amortization of Wildfire Fund contribution $ 460 ~ $ 460 ~ $ 570 ~ $ 570 ~ Amortization of Wildfire Fund contribution (pre - tax) (129) ~ (129) ~ (159) ~ (159) ~ Tax impacts $ 331 ~ $ 331 ~ $ 411 ~ $ 411 ~ Amortization of Wildfire Fund contribution (post - tax)

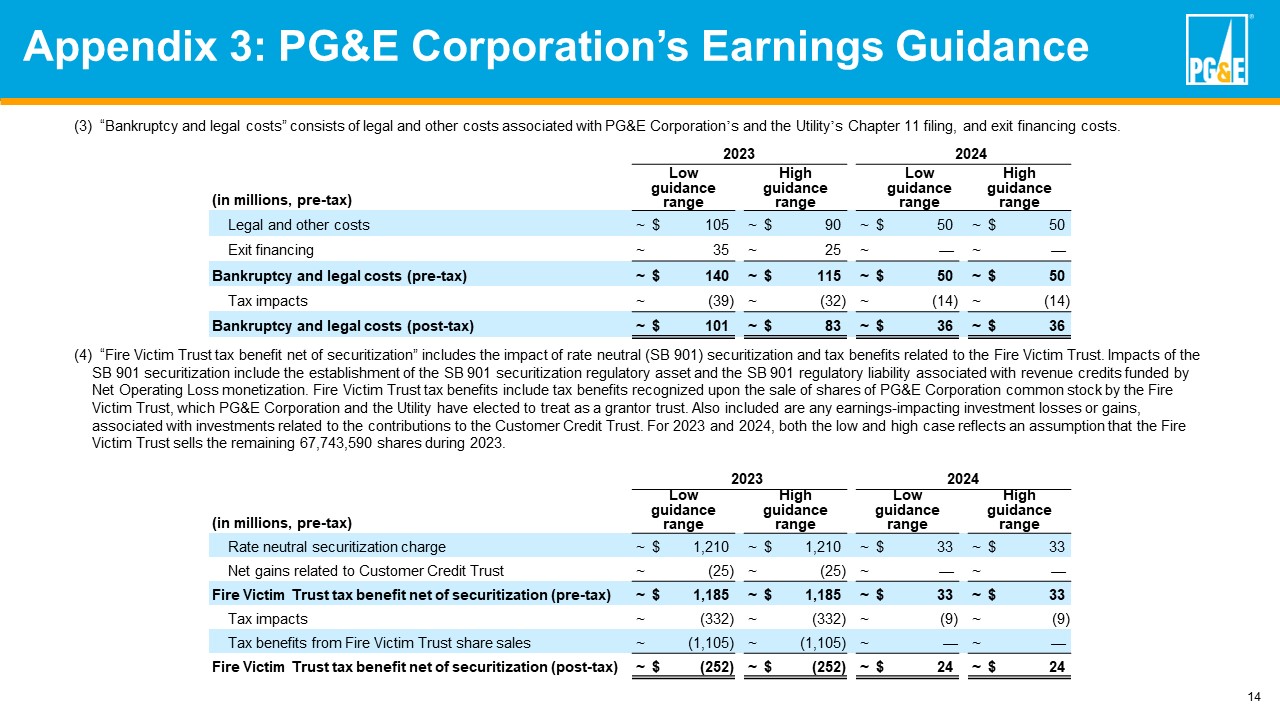

14 Exhibit E: PG&E Corporation's 2020 and 2021 Earnings Guidance (4) “Fire Victim Trust tax benefit net of securitization” includes the impact of rate neutral (SB 901) securitization and tax ben ef its related to the Fire Victim Trust. Impacts of the SB 901 securitization include the establishment of the SB 901 securitization regulatory asset and the SB 901 regulatory liabi lit y associated with revenue credits funded by Net Operating Loss monetization. Fire Victim Trust tax benefits include tax benefits recognized upon the sale of shares of PG &E Corporation common stock by the Fire Victim Trust, which PG&E Corporation and the Utility have elected to treat as a grantor trust. Also included are any earnings - im pacting investment losses or gains, associated with investments related to the contributions to the Customer Credit Trust. For 2023 and 2024, both the low and high case reflects an assumption that the Fire Victim Trust sells the remaining 67,743,590 shares during 2023 . (3) “Bankruptcy and legal costs” consists of legal and other costs associated with PG&E Corporation ’ s and the Utility ’ s Chapter 11 filing, and exit financing costs. Appendix 3: PG&E Corporation’s Earnings Guidance 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ 50 ~ $ 50 ~ $ 90 ~ $ 105 ~ Legal and other costs — ~ — ~ 25 ~ 35 ~ Exit financing $ 50 ~ $ 50 ~ $ 115 ~ $ 140 ~ Bankruptcy and legal costs (pre - tax) (14) ~ (14) ~ (32) ~ (39) ~ Tax impacts $ 36 ~ $ 36 ~ $ 83 ~ $ 101 ~ Bankruptcy and legal costs (post - tax) 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ 33 ~ $ 33 ~ $ 1,210 ~ $ 1,210 ~ Rate neutral securitization charge — ~ — ~ (25) ~ (25) ~ Net gains related to Customer Credit Trust $ 33 ~ $ 33 ~ $ 1,185 ~ $ 1,185 ~ Fire Victim Trust tax benefit net of securitization (pre - tax) (9) ~ (9) ~ (332) ~ (332) ~ Tax impacts — ~ — ~ (1,105) ~ (1,105) ~ Tax benefits from Fire Victim Trust share sales $ 24 ~ $ 24 ~ $ (252) ~ $ (252) ~ Fire Victim Trust tax benefit net of securitization (post - tax)

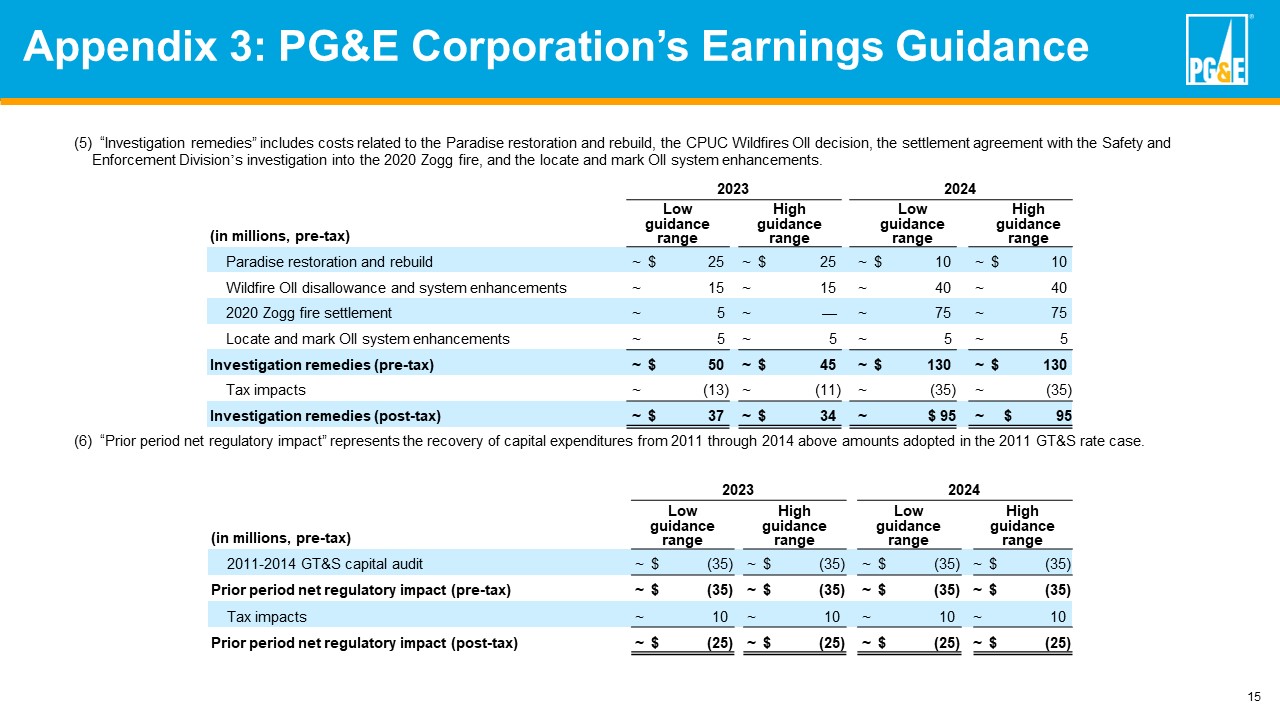

15 (6) “Prior period net regulatory impact” represents the recovery of capital expenditures from 2011 through 2014 above amount s a dopted in the 2011 GT&S rate case. (5) “Investigation remedies” includes costs related to the Paradise restoration and rebuild, the CPUC Wildfires OII decision, the settlement agreement with the Safety and Enforcement Division ’ s investigation into the 2020 Zogg fire, and the locate and mark OII system enhancements. Appendix 3: PG&E Corporation’s Earnings Guidance 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ 10 ~ $ 10 ~ $ 25 ~ $ 25 ~ Paradise restoration and rebuild 40 ~ 40 ~ 15 ~ 15 ~ Wildfire OII disallowance and system enhancements 75 ~ 75 ~ — ~ 5 ~ 2020 Zogg fire settlement 5 ~ 5 ~ 5 ~ 5 ~ Locate and mark OII system enhancements $ 130 ~ $ 130 ~ $ 45 ~ $ 50 ~ Investigation remedies (pre - tax) (35) ~ (35) ~ (11) ~ (13) ~ Tax impacts $ 95 ~ $ 95 ~ $ 34 ~ $ 37 ~ Investigation remedies (post - tax) 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ (35) ~ $ (35) ~ $ (35) ~ $ (35) ~ 2011 - 2014 GT&S capital audit $ (35) ~ $ (35) ~ $ (35) ~ $ (35) ~ Prior period net regulatory impact (pre - tax) 10 ~ 10 ~ 10 ~ 10 ~ Tax impacts $ (25) ~ $ (25) ~ $ (25) ~ $ (25) ~ Prior period net regulatory impact (post - tax)

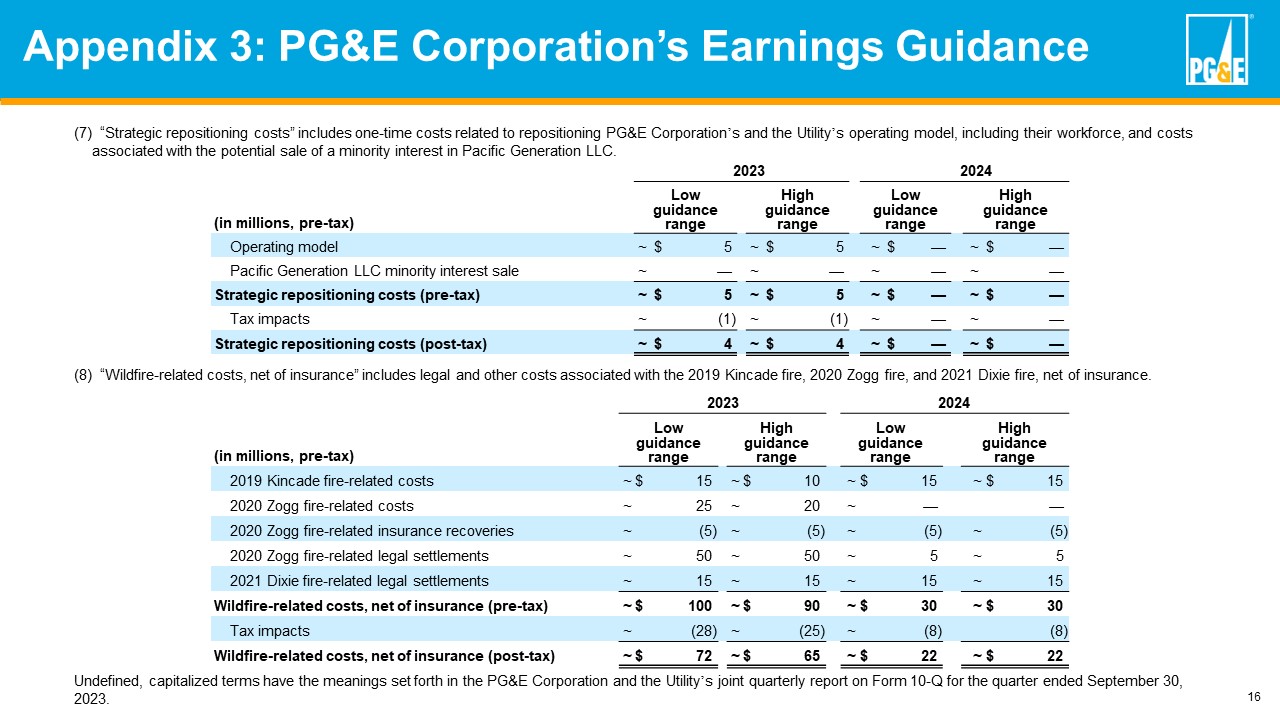

16 (7) “Strategic repositioning costs” includes one - time costs related to repositioning PG&E Corporation ’ s and the Utility ’ s operating model, including their workforce, and costs associated with the potential sale of a minority interest in Pacific Generation LLC. Undefined, capitalized terms have the meanings set forth in the PG&E Corporation and the Utility ’ s joint quarterly report on Form 10 - Q for the quarter ended September 30, 2023. (8) “Wildfire - related costs, net of insurance” includes legal and other costs associated with the 2019 Kincade fire, 2020 Zogg fire, and 2021 Dixie fire, net of insurance. Appendix 3: PG&E Corporation’s Earnings Guidance 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ — ~ $ — ~ $ 5 ~ $ 5 ~ Operating model — ~ — ~ — ~ — ~ Pacific Generation LLC minority interest sale $ — ~ $ — ~ $ 5 ~ $ 5 ~ Strategic repositioning costs (pre - tax) — ~ — ~ (1) ~ (1) ~ Tax impacts $ — ~ $ — ~ $ 4 ~ $ 4 ~ Strategic repositioning costs (post - tax) 2024 2023 High guidance range Low guidance range High guidance range Low guidance range (in millions, pre - tax) $ 15 ~ $ 15 ~ $ 10 ~ $ 15 ~ 2019 Kincade fire - related costs — — ~ 20 ~ 25 ~ 2020 Zogg fire - related costs (5) ~ (5) ~ (5) ~ (5) ~ 2020 Zogg fire - related insurance recoveries 5 ~ 5 ~ 50 ~ 50 ~ 2020 Zogg fire - related legal settlements 15 ~ 15 ~ 15 ~ 15 ~ 2021 Dixie fire - related legal settlements $ 30 ~ $ 30 ~ $ 90 ~ $ 100 ~ Wildfire - related costs, net of insurance (pre - tax) (8) (8) ~ (25) ~ (28) ~ Tax impacts $ 22 ~ $ 22 ~ $ 65 ~ $ 72 ~ Wildfire - related costs, net of insurance (post - tax)

17 Non - GAAP Core Earnings and Non - GAAP Core EPS “Non - GAAP core earnings” and “Non - GAAP core EPS,” also referred to as “non - GAAP core earnings per share,” are non - GAAP financial measures. Non - GAAP core earnings is calculated as income available for common shareholders less non - core items. “Non - core items” include items that management do es not consider representative of ongoing earnings and affect comparability of financial results between periods, consisting of the items listed in Appendix 3 . Non - GAAP core EPS is calculated as non - GAAP core earnings divided by common shares outstanding (taken on a basic basis in the event of a GAAP loss and a diluted basis in the eve nt of a GAAP gain). PG&E Corporation discloses historical financial results and provides guidance based on “non - GAAP core earnings” and “non - GAAP co re EPS” in order to provide a measure that allows investors to compare the underlying financial performance of the business from one period to another, exclusive o f n on - core items. PG&E Corporation and the Utility use non - GAAP core earnings and non - GAAP core EPS to understand and compare operating results across reporting periods fo r various purposes including internal budgeting and forecasting, short - and long - term operating planning, and employee incentive compensation. PG&E Corporation and th e Utility believe that non - GAAP core earnings and non - GAAP core EPS provide additional insight into the underlying trends of the business, allowing for a better comp arison against historical results and expectations for future performance. The reconciling items are primarily due to the future impact of wildfire - related costs, timing of regulatory recoveries, special tax items, and investigation remedies. These reconciling items are uncertain, depend on various factors and could significantly impact, eith er individually or in the aggregate, the GAAP measures. Non - GAAP core earnings and non - GAAP core EPS are not substitutes or alternatives for GAAP measures such as consolidated income a vailable for common shareholders and may not be comparable to similarly titled measures used by other companies. Appendix 4: Non - GAAP Financial Measures

18 Slide titles are hyperlinks Slide 3: Narrowing 2023, Introducing 2024 1. Non - GAAP core EPS is not calculated in accordance with GAAP. See Appendix 3 for a reconciliation of PG&E Corporation’s EPS guida nce on a GAAP basis to non - GAAP core earnings per share and Appendix 4 regarding non - GAAP financial measures. Slide 7: Recent Milestones Affirm 1. Based on a comparison in the Utility's GRC testimony of the wildfire risk score for a baseline risk level to a risk level ref lec ting the Utility’s mitigation work. Risk scores are calculated using the scoring methodology established by the CPUC in the Safety Model Assessment Proceeding, which reflects the frequency with which variou s r isks are expected to occur and the potential safety, reliability, and financial impacts of varying degrees of wildfire severity. Slide 11: Appendix 1: 2023 Factors Impacting Earnings 1. Non - GAAP core EPS is not calculated in accordance with GAAP. See Appendix 3 for a reconciliation of PG&E Corporation’s EPS guidance on a GAAP basis to non - GAAP core earnings per share and Appendix 4 regarding non - GAAP financial measures. 2. 2023 equity earning rate base reflects 2023 GRC Final Decision, TO Formula Rate case filings for TO20 and TO21 and the April 15, 2021 FERC order denying the Utility's request for rehearing related to TO18. 3. The capital structure of an investor - owned utility is the proportional authorization of shareholders’ equity and debt that compr ise a company’s long - range financing or its capitalization. The CPUC currently authorized capital structure is comprised of 47.5% long - term debt, 0.5% preferred equity, and 52% common equity. Base earnings p lan assumes CPUC currently authorized return on equity and long - term capital structure across the enterprise. 4. Refer to Appendix 3: PG&E Corporation's 2023 Earnings Guidance. 5. Cash amounts for non - core items are after tax, directional, and subject to change. 6. Non - GAAP Core Earnings assumptions include: • No 2023 impacts from changes in the federal tax code; and • All potentially dilutive securities were included in the calculation of Non - GAAP core EPS. 7. Unrecoverable net interest includes PG&E Corporation long - term debt, Wildfire Fund contribution debt financing, and other intere st above authorized . Slide 12: Appendix 2: 2024 Factors Impacting Earnings 1. Non - GAAP core EPS is not calculated in accordance with GAAP. See Appendix 3 for a reconciliation of PG&E Corporation’s EPS guidance on a GAAP basis to non - GAAP core earnings per share and Appendix 4 regarding non - GAAP financial measures. 2. 2024 equity earning rate base reflects 2023 GRC Final Decision, TO Formula Rate case filings for TO20 and TO21 and the April 15, 2021 FERC order denying the Utility's request for rehearing rel ated to TO18 . 3. The capital structure of an investor - owned utility is the proportional authorization of shareholders’ equity and debt that compr ise a company’s long - range financing or its capitalization. The CPUC currently authorized capital structure is comprised of 47.5% long - term debt, 0.5% preferred equity, and 52% common equity. Base earnings p lan assumes CPUC currently authorized return on equity and long - term capital structure across the enterprise. 4. Refer to Appendix 3: PG&E Corporation's 2024 Earnings Guidance. 5. Cash amounts for non - core items are after tax, directional, and subject to change. 6. Non - GAAP Core Earnings assumptions include: • No 2024 impacts from changes in the federal tax code; and • All potentially dilutive securities were included in the calculation of Non - GAAP core EPS. 7. Unrecoverable net interest includes PG&E Corporation long - term debt, Wildfire Fund contribution debt financing, and other intere st above authorized . Appendix 5: Presentation Endnotes