Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended June 30, 2013

or

¨ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the transition period from to

Commission File Number 0-13928

U.S. GLOBAL INVESTORS, INC.

Incorporated in the State of Texas

IRS Employer Identification No. 74-1598370

Principal Executive Offices:

7900 Callaghan Road

San Antonio, Texas 78229

Telephone Number: 210-308-1234

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Class A common stock

($0.025 par value per share)

Registered: NASDAQ Capital Market

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

Yes ¨ No x

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer x |

Non-accelerated filer ¨ |

Small reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ¨ No x

The aggregate market value of the 9,466,282 shares of nonvoting class A common stock held by nonaffiliates of the registrant was $37,959,791, based on the last sale price quoted on NASDAQ as of December 31, 2012, the last business day of the registrant’s most recently completed second fiscal quarter. Registrant’s only voting stock is its class C common stock, par value of $0.025 per share, for which there is no active market. The aggregate value of the 7,899 shares of the class C common stock held by nonaffiliates of the registrant on December 31, 2012 (based on the last sale price of the class C common stock in a private transaction) was $1,974.75. For purposes of this disclosure only, the registrant has assumed that its directors, executive officers, and beneficial owners of 5 percent or more of the registrant’s common stock are affiliates of the registrant.

On August 14, 2013, there were 13,865,021 shares of Registrant’s class A nonvoting common stock issued and 13,401,843 shares of Registrant’s class A nonvoting common stock issued and outstanding, no shares of Registrant’s class B nonvoting common stock outstanding, and 2,070,527 shares of Registrant’s class C voting common stock issued and outstanding.

Documents incorporated by reference: None

Table of Contents

| 1 | ||||

| 1 | ||||

| 7 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 14 | ||||

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

15 | |||

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk |

28 | |||

| 29 | ||||

| Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

53 | |||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| Item 10. Directors, Executive Officers and Corporate Governance |

55 | |||

| 59 | ||||

| 66 | ||||

| Item 13. Certain Relationships and Related Transactions, and Director Independence |

68 | |||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 73 | ||||

| Exhibit 10.3 — Amended and Restated Administrative Services Agreement |

||||

| Exhibit 10.16 — Modification dated March 26, 2013 to Line of Credit Note dated February 26, 2009 |

||||

| Exhibit 21 — Subsidiaries of the Company, Jurisdiction of Incorporation, and Percentage of Ownership |

||||

| Exhibit 23.1 — BDO USA, LLP consent |

||||

| Exhibit 31.1 — Rule 13a – 14(a) Certifications (under Section 302 of the Sarbanes-Oxley Act of 2002) |

||||

| Exhibit 32.1 — Section 1350 Certifications (under Section 906 of the Sarbanes-Oxley Act of 2002) |

||||

i

Table of Contents

| Part I of Annual Report on Form 10-K |

|

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, U.S. Global Investors, Inc. and its subsidiaries (collectively, “U.S. Global” or the “Company”) may make other written and oral communications from time to time that contain such statements. Forward-looking statements include statements as to industry trends, future expectations of the Company, and other matters that do not relate strictly to historical facts and are based on certain assumptions by management. These statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations. These statements are based on the beliefs and assumptions of Company management based on information currently available to management. Such forward-looking statements are subject to risks, uncertainties and other factors that could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Important factors that could cause actual results to differ materially from the forward-looking statements include, among others, the risks described in Part I, Item 1A, Risk Factors, and elsewhere in this report and other documents filed or furnished by U.S. Global from time to time with the U.S. Securities and Exchange Commission (“SEC”). U.S. Global cautions readers to carefully consider such factors. Furthermore, such forward-looking statements speak only as of the date on which such statements are made. Except to the extent required by applicable law, U.S. Global undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements.

U.S. Global, a Texas corporation organized in 1968, is a registered investment adviser under the Investment Advisers Act of 1940, as amended (“Advisers Act”). The Company and its subsidiaries are principally engaged in the business of providing investment advisory and other services to U.S. Global Investors Funds (“USGIF” or the “Funds”), a Delaware statutory trust, as well as offshore clients. USGIF is an investment company offering shares of thirteen mutual funds on a no-load basis.

As part of the mutual fund management business, the Company provides: (1) investment advisory services; (2) transfer agency and record keeping services; (3) distribution services; and (4) administrative services to mutual funds advised by the Company. The fees from investment advisory and transfer agency services, as well as investment income, are the primary sources of the Company’s revenue.

Lines of Business

Investment Management Services

Investment Advisory Services. The Company furnishes an investment program for each of the clients it manages and determines, subject to overall supervision by the applicable board of trustees of the clients, the clients’ investments pursuant to an advisory agreement (the “Advisory Agreement”). Consistent with the investment restrictions, objectives and policies of the particular client, the portfolio team for each client determines what investments should be purchased, sold, and held, and makes changes in the portfolio deemed necessary or appropriate. In the Advisory Agreement, the Company is charged with seeking the best overall terms in executing portfolio transactions and selecting brokers or dealers.

1

Table of Contents

As required by the Investment Company Act of 1940, as amended (“Investment Company Act”), the Advisory Agreement with USGIF is subject to annual renewal and is terminable upon 60-day notice. This agreement has been renewed through September 2014.

In addition to providing advisory services to USGIF, the Company provides advisory services to three offshore clients.

Net assets under management on June 30, 2013, and June 30, 2012, are detailed in the following table.

| Assets Under Management (AUM) | ||||||||||||

| Fund |

Ticker | AUM at June 30, 2013 (in thousands) |

AUM at June 30, 2012 (in thousands) |

|||||||||

| U.S. Global Investors Funds Natural Resources |

||||||||||||

| Global Resources |

PSPFX/PIPFX | $ | 391,429 | $ | 530,604 | |||||||

| World Precious Minerals |

UNWPX/UNWIX | 147,998 | 323,802 | |||||||||

| Gold and Precious Metals |

USERX | 87,657 | 155,570 | |||||||||

|

|

|

|

|

|||||||||

| Total Natural Resources |

627,084 | 1,009,976 | ||||||||||

|

|

|

|

|

|||||||||

| Emerging Markets |

||||||||||||

| Emerging Europe |

EUROX | 130,482 | 177,019 | |||||||||

| China Region |

USCOX | 25,514 | 28,272 | |||||||||

| Global Emerging Markets |

GEMFX | 6,643 | 7,962 | |||||||||

|

|

|

|

|

|||||||||

| Total Emerging Markets |

162,639 | 213,253 | ||||||||||

|

|

|

|

|

|||||||||

| Fixed Income |

||||||||||||

| U.S. Government Securities Savings |

UGSXX | 133,381 | 156,307 | |||||||||

| U.S. Treasury Securities Cash |

USTXX | 78,029 | 85,427 | |||||||||

| Near-Term Tax Free |

NEARX | 51,713 | 38,253 | |||||||||

| Tax Free |

USUTX | 20,021 | 22,783 | |||||||||

|

|

|

|

|

|||||||||

| Total Fixed Income |

283,144 | 302,770 | ||||||||||

|

|

|

|

|

|||||||||

| Domestic Equity |

||||||||||||

| Holmes Growth |

ACBGX | 36,559 | 35,805 | |||||||||

| All American Equity |

GBTFX | 19,734 | 17,010 | |||||||||

| MegaTrends |

MEGAX/MEGIX | 11,286 | 13,116 | |||||||||

|

|

|

|

|

|||||||||

| Total Domestic Equity |

67,579 | 65,931 | ||||||||||

|

|

|

|

|

|||||||||

| Total SEC-Registered Funds |

1,140,446 | 1,591,930 | ||||||||||

|

|

|

|

|

|||||||||

| Other Advisory Clients |

21,715 | 32,551 | ||||||||||

|

|

|

|

|

|||||||||

| Total AUM |

$ | 1,162,161 | $ | 1,624,481 | ||||||||

|

|

|

|

|

|||||||||

2

Table of Contents

Transfer Agency and Other Services. The Company’s wholly-owned subsidiary, United Shareholder Services, Inc. (“USSI”), is a transfer agent registered under the Securities Exchange Act of 1934 (“Exchange Act”), providing transfer agency, printing, and mailing services to investment company clients. The transfer agency utilizes a third party external system providing the Company’s fund shareholder communication network with computer equipment and software designed to meet the operating requirements of a mutual fund transfer agency.

The transfer agency’s duties encompass, but are not limited to, the following: (1) acting as servicing agent in connection with dividend and distribution functions; (2) performing shareholder account and administrative agent functions in connection with the issuance, transfer and redemption, or repurchase of shares; (3) maintaining such records as are necessary to document transactions in the Funds’ shares; (4) acting as servicing agent in connection with mailing of shareholder communications, including reports to shareholders, dividend and distribution notices, and proxy materials for shareholder meetings; and (5) investigating and answering all shareholder account inquiries.

The transfer agency agreements provide that USSI will receive, as compensation for services rendered as transfer agent, certain annual and activity-based fees and will be reimbursed for out-of-pocket expenses. In connection with obtaining/providing administrative services to the beneficial owners of fund shares through institutions that provide such services and maintain an omnibus account with USSI, each fund pays a monthly fee based on the value of the shares of the fund held in accounts at the institution.

The Company’s Board of Directors formally agreed on August 23, 2013, to exit the transfer agency business so that the Company could focus more on its core strength of investment management. On August 23, 2013, the Funds’ board of trustees agreed to continue the existing transfer agency contract with USSI until conversion to the new transfer agent, which is projected to be in December 2013.

Distribution Services. The Company has registered its wholly-owned subsidiary, U.S. Global Brokerage, Inc. (“USGB”), with the Financial Industry Regulatory Authority (“FINRA”), the SEC and appropriate state regulatory authorities as a limited-purpose broker-dealer for the purpose of distributing Fund shares. The distribution agreement with USGIF is subject to annual renewal and is terminable upon 60-day notice. This agreement has been renewed through September 2014.

Administrative Services. The Company also manages, supervises and conducts certain other affairs of USGIF, subject to the control of the Funds’ board of trustees pursuant to an administrative agreement (the “Administrative Services Agreement”). It provides office space, facilities and certain business equipment as well as the services of executive and clerical personnel for administering the affairs of the Funds. U.S. Global and its affiliates compensate all personnel, officers, directors and interested trustees of the Funds if such persons are also employees of the Company or its affiliates. The Administrative Services Agreement with USGIF is subject to renewal on an annual basis and is terminable upon 60-day notice. This agreement has been renewed through September 2014. On August 23, 2013, the Funds’ board of trustees agreed to increase the rate from 0.08 percent to 0.10 percent for each investor class and from 0.06 percent to 0.08 percent for each institutional class plus $10,000 per Fund. This change is expected to take effect in December 2013.

Corporate Investments

Investment Activities. In addition to providing management and advisory services, the Company is actively engaged in trading for its own account. See segment information in the notes to the consolidated financial statements at Note 16 Financial Information by Business Segment.

Employees

As of June 30, 2013, U.S. Global and its subsidiaries employed 65 full-time employees and 3 part-time employees; as of June 30, 2012, it employed 70 full-time employees and 4 part-time employees. The Company considers its relationship with its employees to be good.

3

Table of Contents

Competition

The mutual fund industry is highly competitive. According to the Investment Company Institute, at the end of 2012 there were approximately 8,800 domestically registered open-end investment companies of varying sizes and investment policies, whose shares are being offered to the public worldwide. Generally, there are two types of mutual funds: “load” and “no-load.” In addition, there are both load and no-load funds that have adopted Rule 12b-1 plans authorizing the payment of distribution costs of the funds out of fund assets. USGIF is a trust with no-load funds that have adopted 12b-1 plans. Load funds are typically sold through or sponsored by brokerage firms, and a sales commission is charged on the amount of the investment. No-load funds, such as the USGIF, however, may be purchased directly from the particular mutual fund organization or through a distributor, and no sales commissions are charged.

In addition to competition from other mutual fund managers and investment advisers, the Company and the mutual fund industry are in competition with various investment alternatives offered by insurance companies, banks, securities broker-dealers, and other financial institutions. Many of these institutions are able to engage in more liberal advertising than mutual funds and may offer accounts at competitive interest rates, which may be insured by federally chartered corporations such as the Federal Deposit Insurance Corporation.

A number of mutual fund groups are significantly larger than the funds managed by U.S. Global, offer a greater variety of investment objectives and have more experience and greater resources to promote the sale of investments therein. However, the Company believes it has the resources, products, and personnel to compete with these other mutual funds. In particular, the Company is known for its expertise in the gold mining and exploration, natural resources and emerging markets. Competition for sales of fund shares is influenced by various factors, including investment objectives and performance, advertising and sales promotional efforts, distribution channels, and the types and quality of services offered to fund shareholders.

Success in the investment advisory and mutual fund distribution businesses is substantially dependent on each fund’s investment performance, the quality of services provided to shareholders, and the Company’s efforts to market the Funds effectively. Sales of Fund shares generate management, distribution and administrative services fees (which are based on assets of the Funds), and transfer agent fees (which are based on the number of Fund accounts and the activity in those accounts). Costs of distribution and compliance continue to put pressure on profit margins for the mutual fund industry.

Despite the Company’s expertise in gold mining and exploration, natural resources, and emerging markets, the Company faces the same obstacle many advisers face, namely uncovering undervalued investment opportunities as the markets face further uncertainty and increased volatility. In addition, the growing number of alternative investments, especially in specialized areas, has created pressure on the profit margins and increased competition for available investment opportunities.

| Supervision and Regulation |

The Company, USSI, USGB, and the clients the Company manages and administers operate under certain laws, including federal and state securities laws, governing their organization, registration, operation, and legal, financial, and tax status. Among the potential penalties for violation of the laws and regulations applicable to the Company and its subsidiaries are fines, imprisonment, injunctions, revocation of registration, and certain additional administrative sanctions. Any determination that the Company or its management has violated applicable laws and regulations could have a material adverse effect on the business of the Company. Moreover, there is no assurance that changes to existing laws, regulations, or rulings promulgated by governmental entities having jurisdiction over the Company and the Funds will not have a material adverse effect on the Company’s business. The Company has no control over regulatory rulemaking or the consequences it may have on the mutual fund and investment advisory industry.

4

Table of Contents

Recent and accelerating regulatory pronouncements and oversight have significantly increased the burden of compliance infrastructure with respect to the mutual fund industry and the capital markets. This momentum of new regulations has contributed significantly to the costs of managing and administering mutual funds.

U.S. Global is registered as an investment adviser with the SEC. As a registered investment adviser, it is subject to the requirements of the Advisers Act, and the SEC’s regulations thereunder, as well as to examination by the SEC’s staff. The Advisers Act imposes substantive regulation on virtually all aspects of the Company’s business and relationships with the Company’s clients. Applicable rules relate to, among other things, fiduciary duties to clients, transactions with clients, effective compliance programs, conflicts of interest, advertising, recordkeeping, reporting, and disclosure requirements. The Funds for which the Company acts as the investment adviser are registered with the SEC under the Investment Company Act. The Investment Company Act imposes additional obligations, including detailed operational requirements for both funds and their advisers. Moreover, an investment adviser’s contract with a registered fund may be terminated by the fund on not more than 60 days’ notice and is subject to annual renewal by the fund’s board after an initial two-year term. Both the Advisers Act and the Investment Company Act regulate the “assignment” of advisory contracts by the investment adviser. The SEC is authorized to institute proceedings and impose sanctions for violations of the Investment Advisers Act and the Investment Company Act, ranging from fines and censures to termination of an investment adviser’s registration. The failure of the Company, or the Funds which the Company advises, to comply with the requirements of the SEC could have a material adverse effect on the Company. The Company is also subject to federal and state laws affecting corporate governance, including the Sarbanes-Oxley Act of 2002 (“S-Ox Act”), as well as rules adopted by the SEC.

USGB is subject to regulation by the SEC under the Exchange Act and regulation by FINRA, a self-regulatory organization composed of other registered broker-dealers. U.S. Global, USSI, and USGB are required to keep and maintain certain reports and records, which must be made available to the SEC and FINRA upon request.

| Relationships with Clients |

The businesses of the Company are to a very significant degree dependent on their associations and contractual relationships with USGIF. In the event the advisory or administrative agreements with USGIF are canceled or not renewed pursuant to the terms thereof, the Company would be substantially adversely affected. U.S. Global, and USGB consider their relationships with the Funds to be good, and they have no reason to believe that their management and service contracts will not be renewed in the future; however, there is no assurance that USGIF will choose to continue its relationship with the Company, or USGB. As discussed in Item 1 under the heading “Lines of Business – Transfer Agency and Other Services,” USSI has elected to exit the transfer agency business, and USSI and USGIF have mutually agreed to terminate the related transfer agency services agreement once the conversion to the new transfer agent is complete, which is projected to be in December 2013.

In addition, the Company is also dependent on its relationships with its offshore clients. Even though the Company views its relationship with its offshore clients as stable, the Company could be adversely affected if these relationships ended.

| Available Information |

Available Information. The Company’s Internet website address is www.usfunds.com. Information contained on the Company’s website is not part of this annual report on Form 10-K. The Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed with (or furnished to) the SEC are available through a link on the Company’s Internet website, free of charge, soon after such material is filed or furnished. (The link to the Company’s SEC filings can be found at www.usfunds.com by clicking “About Us,” followed by “Investor Relations,” followed by “SEC Filings.”) The Company routinely posts important information on its website.

5

Table of Contents

The Company also posts its Corporate Governance Guidelines, Code of Business Conduct, Code of Ethics for Principal Executive and Senior Financial Officers and the charters of the audit and compensation committees of its Board of Directors on the Company’s website in the “Policies and Procedures” section. The Company’s SEC filings and governance documents are available in print to any stockholder that makes a written request to: Investor Relations, U.S. Global Investors, Inc., 7900 Callaghan Road, San Antonio, Texas 78229.

The Company files reports electronically with the SEC via the SEC’s Electronic Data Gathering, Analysis and Retrieval system (“EDGAR”), which may be accessed through the Internet. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC, at www.sec.gov.

The public may read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Investors and others should note that we announce material financial information to our investors using the website, SEC filings, press releases, public conference calls and webcasts. We also use social media to communicate with our customers and the public about our company. It is possible that the information we post on social media could be deemed to be material information. Therefore, we encourage investors, the media, and others interested in our company to review the information we post on social media channels listed below. This list may be updated from time to time.

https://www.facebook.com/USFunds

https://twitter.com/USFunds

Information contained on our website or on social media channels is not deemed part of this report.

6

Table of Contents

The Company faces a variety of significant and diverse risks, many of which are inherent in the business. Described below are certain risks that could materially affect the Company. Other risks and uncertainties that the Company does not presently consider to be material, or of which the Company is not presently aware, may become important factors that affect it in the future. The occurrence of any of the risks discussed below could materially and adversely affect the business, prospects, financial condition, results of operations, or cash flow.

The investment management business is intensely competitive.

Competition in the investment management business is based on a variety of factors, including:

| • | Investment performance; |

| • | Investor perception of an investment team’s drive, focus, and alignment of interest with them; |

| • | Quality of service provided to, and duration of relationships with, clients and shareholders; |

| • | Business reputation; and |

| • | Level of fees charged for services. |

The Company competes with a large number of investment management firms, commercial banks, broker-dealers, insurance companies, and other financial institutions. Competitive risk is heightened by the fact that some competitors may invest according to different investment styles or in alternative asset classes which the markets may perceive as more attractive than the Company’s investment approach. If the Company is unable to compete effectively, revenues and earnings may be reduced and the business could be materially affected.

Poor investment performance could lead to a decline in revenues.

Success in the investment management industry is largely dependent on investment performance relative to market conditions and the performance of competing products. Good relative performance generally attracts additional assets under management, resulting in additional revenues. Conversely, poor performance generally results in decreased sales and increased redemptions with a corresponding decrease in revenues. Therefore, poor investment performance relative to the portfolio benchmarks and to competitors could impair the Company’s revenues and growth. Effective October 2009, a performance fee was implemented for the nine equity Funds whereby the base advisory fee is adjusted upwards or downwards by 0.25 percent if there is a performance difference of 5 percent or more between a Fund’s performance and that of its designated benchmark index over the prior rolling 12 months.

The Company’s clients can terminate their agreements with the Company on short notice, which may lead to unexpected declines in revenue and profitability.

The Company’s investment advisory agreements are generally terminable on short notice and subject to annual renewal. If the Company’s investment advisory agreements are terminated, which may occur in a short time frame, the Company may experience a decline in revenues and profitability.

Difficult market conditions can adversely affect the Company by reducing the market value of the assets we manage or causing shareholders to make significant redemptions.

Changes in economic or market conditions may adversely affect the profitability, performance of and demand for the Company’s investment products and services. Under the Company’s advisory fee arrangements, the fees received are primarily based on the market value of assets under management. Accordingly, a decline in the price of securities held in the Funds would be expected to cause revenues and net income to decline, which would result in lower advisory fees, or cause increased shareholder redemptions in favor of investments they perceive as offering greater opportunity or lower risk, which redemptions would also result in lower advisory fees. The ability of the Company to compete and grow is dependent on the relative attractiveness of the types of investment products the Company offers and its investment performance and strategies under prevailing market conditions.

7

Table of Contents

Market-specific risks may negatively impact the Company’s earnings.

The Company manages certain funds in the emerging market and natural resource sectors, which are highly cyclical. The investments in the Funds are subject to significant loss due to political, economic and diplomatic developments, currency fluctuations, social instability, and changes in governmental policies. Foreign trading markets, particularly in some emerging market countries, are often smaller, less liquid, less regulated and significantly more volatile than the U.S. and other established markets.

In addition, yields on government securities, and the investment products investing in them, have remained at record lows. Thus, the Company has voluntarily waived fees and/or reimbursed the USGIF money market funds to maintain each fund’s yield at a certain level as determined by the Company. These waivers could increase in the future. Such increases in fee waivers could be significant and would negatively affect the Company’s net income.

The market price and trading volume of the Company’s class A common stock may be volatile, which could result in rapid and substantial losses for the Company’s stockholders.

The market price of the Company’s class A common stock may be volatile and the trading volume may fluctuate, causing significant price variations to occur. If the market price of the Company’s class A common stock declines significantly, stockholders may be unable to sell their shares at or above their purchase price. The Company cannot assure that the market price of its class A common stock will not fluctuate or decline significantly in the future. Some of the factors that could negatively affect the price of the Company’s class A common stock, or result in fluctuations in price or trading volume, include:

| • | Decreases in assets under management; |

| • | Variations in quarterly and annual operating results; |

| • | Publication of research reports about the Company or the investment management industry; |

| • | Departures of key personnel; |

| • | Adverse market reactions to any indebtedness the Company may incur, acquisitions or disposals the Company may make, or securities the Company may issue in the future; |

| • | Changes in market valuations of similar companies; |

| • | Changes or proposed changes in laws or regulations, or differing interpretations thereof, affecting the business, or enforcement of these laws and regulations, or announcements relating to these matters; |

| • | Adverse publicity about the asset management industry, generally, or individual scandals, specifically; and |

| • | General market and economic conditions. |

The market price of the Company’s class A common stock could decline due to the large number of shares of the Company’s class C common stock eligible for future sale upon conversion to class A shares.

The market price of the Company’s class A common stock could decline as a result of sales of a large number of shares of class A common stock eligible for future sale upon the conversion of class C shares, or the perception that such sales could occur. These sales, or the possibility that these sales may occur, also might make it more difficult for the Company to raise additional capital by selling equity securities in the future, at a time and price the Company deems appropriate.

Failure to comply with government regulations could result in fines, which could cause the Company’s earnings and stock price to decline.

The Company and its subsidiaries are subject to a variety of federal securities laws and agencies, including, but not limited to, the Advisers Act, the Investment Company Act, the S-Ox Act, the Gramm-Leach-Bliley Act of 1999, the Bank Secrecy Act of 1970, as amended, the USA PATRIOT Act of 2001, the SEC, FINRA, and NASDAQ. Moreover, financial reporting requirements and the processes, controls, and procedures that have been put in place to address them, are comprehensive and complex. While management has focused attention and resources on compliance policies and procedures, non-compliance with applicable laws or regulations could result in fines, sanctions or censures which could affect the Company’s reputation, and thus its revenues and earnings.

8

Table of Contents

Our business is subject to substantial risk from litigation, regulatory investigations and potential securities laws liability.

Many aspects of U.S. Global’s business involve substantial risks of litigation, regulatory investigations and/or arbitration. The Company is exposed to liability under federal and state securities laws, other federal and state laws and court decisions, as well as rules and regulations promulgated by the SEC, FINRA and other regulatory bodies. U.S. Global, its subsidiaries, and/or officers could be named as parties in legal actions, regulatory investigations and proceedings. An adverse resolution of any lawsuit, legal or regulatory proceeding or claim against the Company could result in substantial costs or reputational harm to the Company, and have a material adverse effect on the Company’s business, financial condition or results of operations, which, in turn, may negatively affect the market price of the Company’s common stock and U.S. Global’s ability to pay dividends. In addition to these financial costs and risks, the defense of litigation or arbitration may divert resources and management’s attention from operations.

Higher insurance premiums and related insurance coverage risks could increase costs and reduce profitability.

While U.S. Global carries insurance in amounts and under terms that it believes are appropriate, the Company cannot assure that its insurance will cover most liabilities and losses to which it may be exposed, or that our insurance policies will continue to be available at acceptable terms and fees. U.S. Global is subject to regulatory and governmental inquiries and civil litigation. An adverse outcome of any such proceeding could involve substantial financial penalties. From time to time, various claims against us arise in the ordinary course of business, including employment-related claims. There has been increased incidence of litigation and regulatory investigations in the financial services industry in recent years, including customer claims and class action suits alleging substantial monetary damages. Certain insurance coverage may not be available or may be prohibitively expensive in future periods. As U.S. Global’s insurance policies come up for renewal, the Company may need to assume higher deductibles or co-insurance liabilities, or pay higher premiums, which would increase the Company’s expenses and reduce net income.

Increased regulatory and legislative actions and reforms could increase costs and negatively impact the Company’s profitability and future financial results.

During the past decade, federal securities laws have been substantially augmented and made significantly more complex by the S-Ox Act and the USA PATRIOT Act of 2001. With new laws and changes in interpretations and enforcement of existing requirements, the associated time the Company must dedicate to, and related costs the Company must incur in, meeting the regulatory complexities of the business have increased. In order to comply with these new requirements, the Company has had to expend additional time and resources, including substantial efforts to conduct evaluations required to ensure compliance with the S-Ox Act.

The Company is subject to financial services laws, regulations, corporate governance requirements, administrative actions and policies. During 2009 and 2010, as many emergency government programs slowed or wound down, global regulatory and legislative focus generally moved to a second phase of broader reform and a restructuring of financial institution regulation. On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”), which fundamentally changed the U.S. financial regulatory landscape. The full scope of the regulatory changes imposed by the Dodd-Frank Act will only be determined once extensive rules and regulations have been proposed and become effective, which may result in significant changes in the manner in which the Company’s operations are regulated.

Further, adverse results of regulatory investigations of mutual fund, investment advisory, and financial services firms could tarnish the reputation of the financial services industry generally, and mutual funds and investment advisers more specifically, causing investors to avoid further fund investments or redeem their balances. Redemptions would decrease the Company’s assets under management, which would reduce its advisory revenues and net income.

9

Table of Contents

The Company intends to pay regular dividends to its stockholders, but the ability to do so is subject to the discretion of the Board of Directors.

The Company intends to pay cash dividends on a monthly basis, but the Board of Directors, at its discretion, may decrease the level or frequency of dividends or discontinue payment of dividends entirely based on earnings, operations, capital requirements, general financial condition of the Company, and general business conditions.

One person beneficially owns substantially all of our voting stock and controls the outcome of all matters requiring a vote of stockholders, which may influence the value of our publicly traded non-voting stock.

Frank Holmes, CEO, is the beneficial owner of over 99 percent of our class C voting convertible common stock and controls the outcome of all issues requiring a vote of stockholders. All of our publicly traded stock is nonvoting stock. Consequently, except to the extent provided by law, stockholders other than Frank Holmes have no vote with respect to the election of directors or any other matter requiring a vote of stockholders. This lack of voting rights may adversely affect the market value of the publicly traded class A nonvoting common stock.

The loss of key personnel could negatively affect the Company’s financial performance.

The success of the Company depends on key personnel, including the portfolio managers, analysts, and executive officers. Competition for qualified, motivated, and skilled personnel in the asset management industry remains significant. As the business grows, the Company will likely need to increase the number of employees. Moreover, in order to retain certain key personnel, the Company may be required to increase compensation to such individuals, resulting in additional expense. The loss of key personnel or the Company’s failure to attract replacement personnel could negatively affect its financial performance.

The Company could be subject to losses if it fails to properly safeguard sensitive and confidential information.

As part of the Company’s normal operations, it maintains and transmits confidential information about the Company and the Funds’ clients as well as proprietary information relating to its business operations. These systems could be victimized by unauthorized users or corrupted by computer viruses or other malicious software code, or authorized persons could inadvertently or intentionally release confidential or proprietary information. Such a breach could subject the Company to liability for a failure to safeguard client data, result in the termination of relationships with our existing customers, require significant capital and operating expenditures to investigate and remediate the breach and subject the Company to regulatory action.

Item 1B. Unresolved Staff Comments

None

The Company presently owns and occupies an office building as its headquarters in San Antonio, Texas. The office building is approximately 46,000 square feet on approximately 2.5 acres of land.

There are no material legal proceedings in which the Company is involved.

Item 4. Mine Safety Disclosures

Not applicable.

10

Table of Contents

|

|

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

Market Information

The Company has three classes of common equity: class A, class B, and class C common stock, par value $0.025 per share.

The Company’s class A common stock is traded over-the-counter and is quoted daily under NASDAQ’s Capital Markets. Trades are reported under the symbol “GROW.”

There is no established public trading market for the Company’s class B and class C common stock.

The Company’s class A and class B common stock have no voting privileges.

The following table sets forth the range of high and low sales prices of “GROW” from NASDAQ for the fiscal years ended June 30, 2013, and June 30, 2012. The quotations represent prices between dealers and do not include any retail markup, markdown, or commission.

| Sales Price | ||||||||||||||||

| 2013 | 2012 | |||||||||||||||

| High ($) | Low ($) | High ($) | Low ($) | |||||||||||||

| First quarter (9/30) |

6.32 | 4.06 | 8.70 | 6.00 | ||||||||||||

| Second quarter (12/31) |

6.25 | 3.85 | 7.80 | 5.76 | ||||||||||||

| Third quarter (3/31) |

4.48 | 3.50 | 7.83 | 6.03 | ||||||||||||

| Fourth quarter (6/30) |

3.70 | 2.11 | 7.52 | 3.98 | ||||||||||||

Holders

On August 14, 2013, there were approximately 192 holders of record of class A common stock, no holders of record of class B common stock, and 37 holders of record of class C common stock.

Dividends

The Company paid cash dividends of $0.02 per share per month in fiscal year 2012 and through December 2012. After paying a special $0.02 per share dividend in December 2012, the Company lowered its monthly dividend from $0.02 to $0.005 per share per month beginning in January 2013. A monthly dividend of $0.005 is authorized through December 2013 and will be considered for continuation at that time by the Board. Payment of cash dividends is within the discretion of the Company’s Board of Directors and is dependent on earnings, operations, capital requirements, general financial condition of the Company, and general business conditions.

11

Table of Contents

Securities authorized for issuance under equity compensation plans

Information relating to equity compensation plans under which our stock is authorized for issuance is set forth in Item 12 of Part III of this Form 10-K under the heading “Equity Compensation Plan Information.”

Purchases of equity securities by the issuer

Effective January 1, 2013, the Board of Directors approved a share repurchase program authorizing the Company to purchase up to $2.75 million of its outstanding class A common shares as market and business conditions warrant on the open market in compliance with Rule 10b-18 of the Securities Exchange Act of 1934. As of June 30, 2013, the Company had purchased 55,052 class A shares using cash of $173,608. The Company may repurchase stock from employees; however, none were repurchased from employees in fiscal year 2013. Nor were there any repurchases of classes B or C common stock during the fiscal year ended June 30, 2013.

| Period |

Total Number of Shares Purchased 1 |

Total Amount Purchased |

Average Price Paid Per Share 2 |

Total Number of Shares Purchased as Part of Publicly Announced Plan 3 |

Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan |

|||||||||||||||

| 01-01-13 to 01-31-13 |

4,300 | $ | 17,816 | $ | 4.14 | 4,300 | $ | 2,732,184 | ||||||||||||

| 02-01-13 to 02-28-13 |

9,003 | 33,560 | 3.73 | 9,003 | 2,698,624 | |||||||||||||||

| 03-01-13 to 03-31-13 |

8,900 | 33,607 | 3.78 | 8,900 | 2,665,017 | |||||||||||||||

|

04-01-13 to 04-30-13 |

10,800 | 34,456 | 3.19 | 10,800 | 2,630,561 | |||||||||||||||

| 05-01-13 to 05-31-13 |

7,457 | 20,118 | 2.70 | 7,457 | 2,610,443 | |||||||||||||||

| 06-01-13 to 06-30-13 |

14,592 | 34,051 | 2.33 | 14,592 | 2,576,392 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

55,052 | $ | 173,608 | $ | 3.15 | 55,052 | 2,576,392 | |||||||||||||

| 1 | The Board of Directors of the company approved on December 7, 2012, a repurchase of up to $2.75 million of its outstanding class A common stock from time to time on the open market in calendar year 2013 in accordance with all applicable rules and regulations. |

| 2 | The average price paid per share of stock repurchased under the stock repurchase program includes the commissions paid to brokers. |

| 3 | The repurchase plan was approved on December 7, 2012, and will continue for twelve months in calendar year 2013. |

12

Table of Contents

Company Performance Presentation

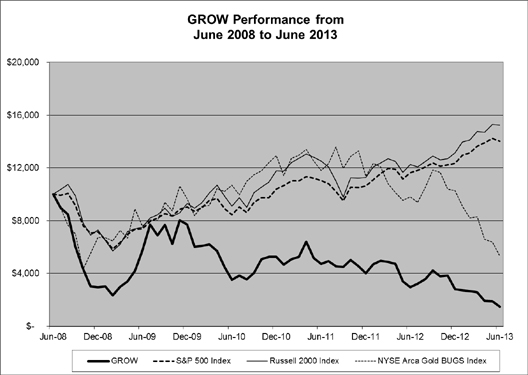

The following graph compares the cumulative total return for the Company’s class A common stock (GROW) to the cumulative total return for the S&P 500 Index, the Russell 2000 Index, and the NYSE Arca Gold BUGS Index for the Company’s last five fiscal years. The graph assumes an investment of $10,000 in the class A common stock and in each index as of June 30, 2008, and that all dividends are reinvested. The historical information included in this graph is not necessarily indicative of future performance and the Company does not make or endorse any predictions as to future stock performance.

| Fiscal Year-End Date | ||||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |||||||||||||||||||

| U.S. Global Investors, Inc., class A (GROW) |

$ | 10,000 | $ | 5,732 | $ | 3,522 | $ | 4,727 | $ | 2,973 | $ | 1,492 | ||||||||||||

| S&P 500 Index |

$ | 10,000 | $ | 7,379 | $ | 8,443 | $ | 11,035 | $ | 11,636 | $ | 14,033 | ||||||||||||

| Russell 2000 Index |

$ | 10,000 | $ | 7,499 | $ | 9,110 | $ | 12,518 | $ | 12,258 | $ | 15,225 | ||||||||||||

| NYSE Arca Gold BUGS Index |

$ | 10,000 | $ | 7,601 | $ | 10,695 | $ | 11,817 | $ | 9,819 | $ | 5,328 | ||||||||||||

13

Table of Contents

Item 6. Selected Financial Data

The following selected financial data is qualified by reference to, and should be read in conjunction with, the Company’s Consolidated Financial Statements and related notes and Management’s Discussion and Analysis of Financial Condition and Results of Operations contained in this Form 10-K. The selected financial data as of June 30, 2009, through June 30, 2013, and the years then ended, is derived from the Company’s audited Consolidated Financial Statements.

| Year Ended June 30, | ||||||||||||||||||||

| Selected Financial Data |

2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||

| Operating revenues |

$ | 18,665,250 | $ | 24,027,570 | $ | 40,925,058 | $ | 34,051,038 | $ | 27,756,791 | ||||||||||

| Operating expenses |

19,106,805 | 21,351,222 | 29,903,607 | 26,521,396 | 26,750,817 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss) |

(441,555 | ) | 2,676,348 | 11,021,451 | 7,529,642 | 1,005,974 | ||||||||||||||

| Other income (loss) |

262,567 | (176,961 | ) | 1,008,568 | 979,115 | (4,616,522 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Pretax income (loss) |

(178,988 | ) | 2,499,387 | 12,030,019 | 8,508,757 | (3,610,548 | ) | |||||||||||||

| Income tax expense (benefit) |

15,224 | 968,953 | 4,197,372 | 3,159,472 | (1,372,969 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (194,212 | ) | $ | 1,530,434 | $ | 7,832,647 | $ | 5,349,285 | $ | (2,237,579 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic income (loss) per share |

(0.01 | ) | 0.10 | 0.51 | 0.35 | (0.15 | ) | |||||||||||||

| Working capital |

23,340,007 | 25,710,714 | 32,366,289 | 28,323,885 | 27,363,133 | |||||||||||||||

| Total assets |

38,695,414 | 41,755,794 | 45,966,603 | 40,983,698 | 37,153,846 | |||||||||||||||

| Dividends per common share |

0.17 | 0.24 | 0.24 | 0.24 | 0.24 | |||||||||||||||

| Shareholders’ equity |

36,849,241 | 38,709,646 | 41,057,447 | 36,191,872 | 34,627,994 | |||||||||||||||

| Net cash provided by operating activities |

461,005 | 1,817,046 | 7,718,529 | 7,632,350 | 3,040,931 | |||||||||||||||

| Net cash used in investing activities |

(368,035 | ) | (4,894,472 | ) | (845,601 | ) | (739,266 | ) | (4,386,782 | ) | ||||||||||

| Net cash used in financing activities |

(2,620,465 | ) | (3,517,749 | ) | (3,502,511 | ) | (3,359,199 | ) | (3,485,630 | ) | ||||||||||

| Average assets under management (in billions) |

1.55 | 2.06 | 2.82 | 2.56 | 2.53 | |||||||||||||||

14

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This discussion reviews and analyzes the consolidated results of operations for the past three fiscal years and other factors that may affect future financial performance. This discussion should be read in conjunction with the Consolidated Financial Statements, Notes to the Consolidated Financial Statements and Selected Financial Data.

Recent Trends in Financial Markets

During the fiscal year ended June 30, 2013, global financial markets responded positively to the change in leadership at the European Central Bank (“ECB”). The head of the ECB, Mario Draghi, declared in late July 2012 that the ECB would “do whatever it takes” to save the euro, and by doing so has put the central bank’s credibility on the line. This was a big confidence boost for the market, which was looking for leadership out of Europe and was a significant driver of the improvement in sentiment and global equity market performance in the second half of 2012.

The Federal Reserve (“Fed”) also followed up with another round of quantitative easing (QE3) in September 2012, an open-ended mandate to purchase $40 billion in mortgages per month until the Fed believes it is no longer necessary to do so. Late in the year, the Fed also rolled over the expiring “operation twist” into an additional $45 billion monthly quantitative easing program. The Fed is on pace for a trillion dollars in QE if this pace continues throughout 2013. Also late last year a change in leadership in Japan led to aggressive government policy changes, including both the fiscal and monetary policy, and the Bank of Japan’s QE program is almost as large as the Fed’s. This initially provided a boost to all risky assets but, as the months have passed, the biggest beneficiary has primarily been the U.S. equity market as gold, commodities and emerging markets are generally flat to down over the past twelve months. As a consequence of these events, U.S. domestic equity mutual funds have seen asset flows while investments in emerging markets, commodity related equities, fixed income and cash have experienced outflows in recent months.

The volatility in the Company’s revenue is correlated to the price swings in natural resources and emerging markets, which represent roughly 70 percent of assets under management. During the past fiscal year, U.S. stocks and the U.S. dollar have been positive, while emerging markets stocks and commodity-related stocks generally have been lagging in performance. For the past 10 years, the one-year normal volatility of one standard deviation has been 17.5 percent for the S&P 500 Index, approximately 30.6 percent for the MSCI Emerging Markets Index and nearly 35.7 percent for gold equities. To manage expenses, the Company maintains a flexible structure for one of its largest costs, compensation expense, by setting relatively lower base salaries with bonuses that are related to average assets under management and fund performance. Thus, our expense model expands and contracts with asset swings and performance.

Business Segments

The Company, with principal operations located in San Antonio, Texas, manages two business segments: (1) the Company offers a broad range of investment management products and services to meet the needs of individual and institutional investors; and (2) the Company invests for its own account in an effort to add growth and value to its cash position. Although the Company generates the majority of its revenues from its investment advisory segment, the Company holds a significant amount of its total assets in investments. The following is a brief discussion of the Company’s two business segments.

15

Table of Contents

Investment Management Products and Services

The Company generates substantially all of its operating revenues from managing and servicing the Funds and other advisory clients. These revenues are largely dependent on the total value and composition of assets under its management. Fluctuations in the markets and investor sentiment directly impact the Funds’ asset levels, thereby affecting income and results of operations.

Detailed information regarding the SEC-registered Funds managed by the Company can be found on the Company’s website, www.usfunds.com, including performance information for each fund for various time periods, assets under management as of the most recent month end, and inception date of each fund.

SEC-registered mutual fund shareholders are not required to give advance notice prior to redemption of shares in the funds; however, the equity funds charge a redemption fee if the fund shares have been held for less than the applicable periods of time set forth in the funds’ prospectuses. The fixed income and money market funds charge no redemption fee. Detailed information about redemption fees can be found in the funds’ prospectus, which is available on the Company’s website, www.usfunds.com.

The Company provides advisory services for three offshore clients and receives monthly advisory fees based on the net asset values of the clients and performance fees, if any, based on the overall increase in net asset values. In fiscal year 2013, the Company recorded advisory and performance fees from these clients totaling $298,521 and $19,202, respectively, and $352,103 and $6,172, respectively, in fiscal year 2012. The performance fees for these clients are calculated and recorded in accordance with the terms of the advisory agreements. These fees may fluctuate significantly from year to year based on factors that may be out of the Company’s control. Frank Holmes, CEO, serves as a director of the offshore clients.

On June 30, 2013, total assets under management as of period end, including both SEC-registered Funds and offshore clients, were $1.162 billion versus $1.624 billion on June 30, 2012, a decrease of 28.5 percent. During fiscal year 2013, average assets under management were $1.552 billion versus $2.055 billion in fiscal year 2012. The decrease was primarily due to market depreciation in the natural resources funds and redemptions in the natural resources and emerging markets funds under management.

16

Table of Contents

The following tables summarize the changes in assets under management for the SEC-registered Funds for fiscal years 2013, 2012, and 2011:

| Changes in Assets Under Management Year Ended June 30, |

||||||||||||

| 2013 | ||||||||||||

| (Dollars in Thousands) |

Equity | Money Market and Fixed Income |

Total | |||||||||

| Beginning Balance |

$ | 1,289,160 | $ | 302,770 | $ | 1,591,930 | ||||||

| Market depreciation |

(146,115) | (87) | (146,202) | |||||||||

| Dividends and distributions |

(14,981) | (1,675) | (16,656) | |||||||||

| Net shareholder redemptions |

(270,762) | (17,864) | (288,626) | |||||||||

|

|

|

|

|

|

|

|||||||

| Ending Balance |

$ | 857,302 | $ | 283,144 | $ | 1,140,446 | ||||||

|

|

|

|

|

|

|

|||||||

| Average investment management fee |

0.98% | 0.00% | 0.79% | |||||||||

| Average net assets |

$ | 1,229,373 | $ | 293,027 | $ | 1,522,400 | ||||||

| Changes in Assets Under Management Year Ended June 30, |

||||||||||||

| 2012 | ||||||||||||

| (Dollars in Thousands) |

Equity | Money Market and Fixed Income |

Total | |||||||||

| Beginning Balance |

$ | 2,225,729 | $ | 336,793 | $ | 2,562,522 | ||||||

| Market appreciation/(depreciation) |

(480,540) | 2,774 | (477,766) | |||||||||

| Dividends and distributions |

(117,744) | (1,506) | (119,250) | |||||||||

| Net shareholder redemptions |

(338,285) | (35,291) | (373,576) | |||||||||

|

|

|

|

|

|

|

|||||||

| Ending Balance |

$ | 1,289,160 | $ | 302,770 | $ | 1,591,930 | ||||||

|

|

|

|

|

|

|

|||||||

| Average investment management fee |

0.99% | 0.00% | 0.83% | |||||||||

| Average net assets |

$ | 1,699,921 | $ | 320,242 | $ | 2,020,163 | ||||||

| Changes in Assets Under Management Year Ended June 30, |

||||||||||||

| 2011 | ||||||||||||

| (Dollars in Thousands) |

Equity | Money Market and Fixed Income |

Total | |||||||||

| Beginning Balance |

$ | 1,985,203 | $ | 382,062 | $ | 2,367,265 | ||||||

| Market appreciation |

528,737 | 1,493 | 530,230 | |||||||||

| Dividends and distributions |

(144,176) | (1,488) | (145,664) | |||||||||

| Net shareholder redemptions |

(144,035) | (45,274) | (189,309) | |||||||||

|

|

|

|

|

|

|

|||||||

| Ending Balance |

$ | 2,225,729 | $ | 336,793 | $ | 2,562,522 | ||||||

|

|

|

|

|

|

|

|||||||

| Average investment management fee |

1.00% | 0.00% | 0.87% | |||||||||

| Average net assets |

$ | 2,418,615 | $ | 358,121 | $ | 2,776,736 | ||||||

As shown above, both average and period-end assets under management decreased in total in fiscal year 2013 compared to fiscal year 2012 and in fiscal year 2012 compared to fiscal year 2011. The decrease in assets under management in fiscal year 2013 was driven by market depreciation, primarily in the natural resources funds, and redemptions, primarily in the natural resources and emerging markets funds. The decrease in assets under management in fiscal year 2012 was driven by market depreciation and redemptions in the equity funds, primarily in the natural resources and emerging markets funds.

17

Table of Contents

A significant portion of the dividends and distributions shown above are reinvested and included in net shareholder redemptions. The money market funds experienced a net decrease as shareholders sought alternatives to low yields for all periods.

While stock market performance for domestic U.S. equities has been steadily rising, while equities linked to gold and broader natural resources, where most of the assets managed by the Company are invested, were generally volatile and declining. The global financial crisis and subsequent volatility in markets, combined with fund performance, were significant factors in the shareholder activity shown in all periods.

The average annualized investment management fee rate (total mutual fund advisory fees, excluding performance fees, as a percentage of average assets under management) was 79 basis points in fiscal year 2013 compared to 83 basis points in fiscal year 2012 and 87 basis points in fiscal year 2011. The average investment management fee for equity funds in fiscal year 2013, 2012, and 2011 was 98, 99, and 100 basis points, respectively. The average investment management fee for the money market and fixed income funds was nil or close to nil for fiscal year 2013, 2012, and 2011. This is due to voluntary fee waivers on these funds as discussed in Note 6 to the consolidated financial statements, including a voluntary agreement to support the yields for the money market funds.

Investment Activities

Management believes it can more effectively manage the Company’s cash position by maintaining certain types of investments utilized in cash management and continues to believe that such activities are in the best interest of the Company.

The following summarizes the market value, cost, and unrealized gain or loss on investments as of June 30, 2013, and June 30, 2012.

| Securities |

Market Value | Cost | Unrealized Gain (Loss) |

Unrealized holding gains

on available-for-sale securities, net of tax |

||||||||||||

| Trading¹ |

$ | 4,758,220 | $ | 5,457,989 | $ | (699,769) | N/A | |||||||||

| Available-for-sale² |

9,053,111 | 8,064,902 | 988,209 | $ | 652,218 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total at June 30, 2013 |

$ | 13,811,331 | $ | 13,522,891 | $ | 288,440 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Trading¹ |

$ | 5,216,139 | $ | 5,960,634 | $ | (744,495) | N/A | |||||||||

| Available-for-sale² |

8,824,311 | 8,117,844 | 706,467 | $ | 466,268 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total at June 30, 2012 |

$ | 14,040,450 | $ | 14,078,478 | $ | (38,028) | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| ¹ | Unrealized and realized gains and losses on trading securities are included in earnings in the statement of operations. |

| ² | Unrealized gains and losses on available-for-sale securities are excluded from earnings and recorded in other comprehensive income as a separate component of shareholders’ equity until realized. |

As of June 30, 2013, and 2012, the Company held approximately $1.6 million in investments other than the clients the Company advises. Investments in securities classified as trading are reflected as current assets on the Consolidated Balance Sheet at their fair market value. Unrealized holding gains and losses on trading securities are included in earnings in the Consolidated Statements of Operations and Comprehensive Income. Investments in securities classified as available for sale, which may not be readily marketable, are reflected as non-current assets on the Consolidated Balance Sheet at their fair value. Unrealized holding gains and losses on available-for-sale securities are excluded from earnings and reported in other comprehensive income as a separate component of shareholders’ equity until realized.

18

Table of Contents

Investment income (loss) from the Company’s investments includes:

| • | realized gains and losses on sales of securities; |

| • | unrealized gains and losses on trading securities; |

| • | realized foreign currency gains and losses; |

| • | other-than-temporary impairments on available-for-sale securities; and |

| • | dividend and interest income. |

Investment income can be volatile and may vary depending on market fluctuations, the Company’s ability to participate in investment opportunities, and timing of transactions. A significant portion of the unrealized gains and losses is concentrated in a small number of issuers. For fiscal years 2013, 2012, and 2011, the Company had net recognized gains (losses) on sales or other-than-temporary impairment of securities of ($26,445), $157,668, and 135,759, respectively. Due to market volatility, the Company expects that gains or losses will continue to fluctuate in the future.

19

Table of Contents

Consolidated Results of Operations

The following is a discussion of the consolidated results of operations of the Company and a detailed discussion of the Company’s revenues and expenses.

| 2013 | 2012 | % Change | 2012 | 2011 | % Change | |||||||||||||||||||

| Net income (loss) (in thousands) |

$ | (194) | $ | 1,530 | (112.7%) | $ | 1,530 | $ | 7,833 | (80.5%) | ||||||||||||||

| Net income (loss) per share |

||||||||||||||||||||||||

| Basic |

$ | (0.01) | $ | 0.10 | (110.0%) | $ | 0.10 | $ | 0.51 | (80.4%) | ||||||||||||||

| Diluted |

$ | (0.01) | $ | 0.10 | (110.0%) | $ | 0.10 | $ | 0.51 | (80.4%) | ||||||||||||||

| Weighted average shares outstanding (in thousands) |

||||||||||||||||||||||||

| Basic |

15,483 | 15,441 | 15,441 | 15,384 | ||||||||||||||||||||

| Diluted |

15,483 | 15,442 | 15,442 | 15,384 | ||||||||||||||||||||

Year Ended June 30, 2013, Compared with Year Ended June 30, 2012

The Company posted net loss of $194,212 ($0.01 loss per share) for the year ended June 30, 2013, compared with net income of $1,530,434 ($0.10 per share) for the year ended June 30, 2012. This decrease in profitability is primarily attributable to the following factors:

Revenues

Total consolidated operating revenues for the year ended June 30, 2013, decreased $5,362,320, or 22.3 percent, compared with the year ended June 30, 2012. This decrease was primarily attributable to the following:

| • | Mutual fund advisory fee revenue decreased by $2,704,458, or 18.6 percent. Mutual fund advisory fees are comprised of two components: a base management fee and a performance fee. The performance fee is a fulcrum fee that is adjusted upwards or downwards by 0.25 percent when there is a performance difference of 5 percent or more between a Fund’s performance and that of its designated benchmark index over the prior rolling 12 months. |

| o | Of that amount, $4,802,258 was attributable to a decrease in mutual fund management fees as a result of lower assets under management due to market depreciation and shareholder redemptions in the natural resources and emerging markets funds. |

| o | This decrease in management fees was offset by a $2,097,800 decrease in performance fee adjustments paid out in the current period versus the prior period. |

| • | Distribution fee revenue decreased by $1,252,717, or 30.8 percent, as a result of lower average net assets under management upon which these fees are based. |

| • | Administrative services fee revenue decreased by $391,586, or 29.6 percent, as a result of lower average net assets under management upon which these fees are based. |

| • | Transfer agent fee revenue decreased by $976,147, or 26.6 percent, as a result of a decline in the number of shareholder accounts and the number of transactions. |

Total consolidated other income for the year ended June 30, 2013, increased $439,528, or 248.4 percent, compared with the year ended June 30, 2012. This increase was primarily attributable to an increase in investment income as a result of changes in trading securities.

20

Table of Contents

Expenses

Total consolidated expenses for the year ended June 30, 2013, decreased by $2,244,417, or 10.5 percent, compared with the prior year and was primarily attributable to the following:

| • | Employee compensation and benefits decreased by $671,337, or 6.7 percent, primarily as a result of lower performance-based bonuses and fewer employees. |

| • | Platform fees decreased by $1,331,842, or 33.3 percent, primarily due to lower assets held through broker-dealer platforms. |

| • | Advertising decreased $320,201, or 27.1 percent, as a result of decreased marketing and sales costs. |

Year Ended June 30, 2012, Compared with Year Ended June 30, 2011

The Company posted net income of $1,530,434 ($0.10 per share) for the year ended June 30, 2012, compared with net income of $7,832,647 ($0.51 per share) for the year ended June 30, 2011. This decrease in profitability is primarily attributable to the following factors:

Revenues

Total consolidated operating revenues for the year ended June 30, 2012, decreased $16,897,488, or 41.3 percent, compared with the year ended June 30, 2011. This decrease was primarily attributable to the following:

| • | Mutual fund advisory fee revenue decreased by $11,996,085, or 45.1 percent, as a result of lower assets under management. Of that amount, $7,384,666 was attributable to a decrease in mutual fund management fees due to market depreciation and shareholder redemptions in the natural resources and emerging markets funds. In addition, $4,611,419 was attributable to a swing in performance fee adjustments driven by net payments to the Funds in the current period versus net receipts from the Funds in the prior period. Performance fees are paid or received when there is a performance difference of 5 percent or more between a fund’s performance and that of its designated benchmark index over the prior rolling 12 months. |

| • | Distribution fee revenue decreased by $1,918,511, or 32.0 percent, as a result of lower average net assets under management upon which these fees are based. |

| • | Transfer agent fee revenue decreased by $1,344,053, or 26.8 percent, as a result of a decline in the number of shareholder accounts and the number of transactions. |

| • | Offshore fund advisory fee revenue decreased by $1,029,083, or 74.2 percent. Of that amount, $949,693 was attributable to a decline in performance fees, while $79,390 was attributable to a decline in offshore fund management fees. |

Other income, which consists of investment income, decreased by $1,185,529, or 117.5 percent, as a result of unrealized losses on trading securities.

Expenses

Total consolidated expenses for the year ended June 30, 2012, decreased by $8,552,385, or 28.6 percent, compared with the prior year and was primarily attributable to the following:

| • | Employee compensation and benefits decreased by $2,476,461, or 19.9 percent, primarily as a result of lower performance-based bonuses and fewer employees. |

| • | General and administrative expenses decreased by $2,361,115, or 28.8 percent, primarily due to prior period software implementation and consulting expenses. |

| • | Platform fees decreased by $2,308,399, or 36.6 percent, primarily due to lower assets held through broker-dealer platforms. |

| • | Advertising decreased $1,281,471, or 52.0 percent, as a result of decreased marketing and sales costs. |

21

Table of Contents

Revenues

| (Dollars in Thousands) |

2013 | 2012 | % Change |

2012 | 2011 | % Change |

||||||||||||||||||

| Investment advisory fees: |

||||||||||||||||||||||||

| Natural resource funds |

$ | 9,302 | $ | 11,085 | (16.1%) | $ | 11,085 | $ | 20,341 | (45.5%) | ||||||||||||||

| Emerging markets funds |

2,170 | 2,991 | (27.4%) | 2,991 | 5,558 | (46.2%) | ||||||||||||||||||

| Domestic equity funds |

399 | 499 | (20.0%) | 499 | 672 | (25.7%) | ||||||||||||||||||

| Fixed income funds |

- | - | 0.0% | - | - | 0.0% | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total mutual fund advisory fees |

11,871 | 14,575 | (18.6%) | 14,575 | 26,571 | (45.1%) | ||||||||||||||||||

| Other advisory fees |

318 | 358 | (11.2%) | 358 | 1,387 | (74.2%) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total investment advisory fees |

12,189 | 14,933 | (18.4%) | 14,933 | 27,958 | (46.6%) | ||||||||||||||||||

| Transfer agent fees |

2,690 | 3,667 | (26.6%) | 3,667 | 5,011 | (26.8%) | ||||||||||||||||||

| Distribution fees |

2,817 | 4,070 | (30.8%) | 4,070 | 5,988 | (32.0%) | ||||||||||||||||||

| Administrative services fees |

929 | 1,321 | (29.7%) | 1,321 | 1,922 | (31.3%) | ||||||||||||||||||

| Other revenues |

40 | 37 | 8.1% | 37 | 46 | (19.6%) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Operating Revenue |

18,665 | 24,028 | (22.3%) | 24,028 | 40,925 | (41.3%) | ||||||||||||||||||

| Other Income (Loss) |

263 | (177) | 248.6% | (177) | 1,009 | (117.5%) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Revenue |

$ | 18,928 | $ | 23,851 | (20.6%) | $ | 23,851 | $ | 41,934 | (43.1%) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Investment Advisory Fees. Investment advisory fees, the largest component of the Company’s revenues, are derived from two sources: SEC-registered mutual fund advisory fees, which in fiscal year 2013 accounted for 97 percent of the Company’s total advisory fees, and offshore investment advisory fees, which accounted for three percent of total advisory fees.

SEC-registered mutual fund investment advisory fees are calculated as a percentage of average net assets, ranging from 0.375 percent to 1.375 percent, and are paid monthly. These advisory fees decreased by approximately $2.7 million, or 18.6 percent, in fiscal year 2013 compared to fiscal year 2012 primarily as a result of decreased assets under management due to market depreciation and shareholder redemptions in the natural resources and emerging markets funds.

Mutual fund investment advisory fees are also affected by changes in assets under management, which include:

| • | market appreciation or depreciation; |

| • | the addition of new client accounts; |

| • | client contributions of additional assets to existing accounts; |

| • | withdrawals of assets from and termination of client accounts; |

| • | exchanges of assets between accounts or products with different fee structures; and |

| • | the amount of fees voluntarily reimbursed. |

The fees on the nine equity USGIF funds consist of a base advisory fee that is adjusted upward or downward by 0.25 percent if there is a performance difference of 5 percent or more between a fund’s performance and that of its designated benchmark index over the prior rolling 12 months. For the year ended June 30, 2013, the Company adjusted its base advisory fees downward by $133,011. For the year ended June 30, 2012, the Company adjusted its base advisory fees downward by $2,230,811. For the year ended June 30, 2011, the Company adjusted its base advisory fees upward by $2,380,608.