UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4118

Fidelity Securities Fund

(Exact name of registrant as specified in charter)

245 Summer St., Boston, Massachusetts 02210

(Address of principal executive offices) (Zip code)

Marc Bryant, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

Date of fiscal year end: | July 31 |

|

|

Date of reporting period: | July 31, 2017 |

Item 1.

Reports to Stockholders

|

Fidelity® Small Cap Growth K6 Fund Annual Report July 31, 2017 |

|

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-835-5092 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2017 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Investment Summary (Unaudited)

Top Ten Stocks as of July 31, 2017

| % of fund's net assets | |

| 2U, Inc. | 2.9 |

| Stamps.com, Inc. | 2.5 |

| The Chemours Co. LLC | 1.9 |

| SiteOne Landscape Supply, Inc. | 1.8 |

| Grand Canyon Education, Inc. | 1.8 |

| WABCO Holdings, Inc. | 1.6 |

| KBR, Inc. | 1.5 |

| Cotiviti Holdings, Inc. | 1.5 |

| Vail Resorts, Inc. | 1.4 |

| Cedar Fair LP (depositary unit) | 1.4 |

| 18.3 |

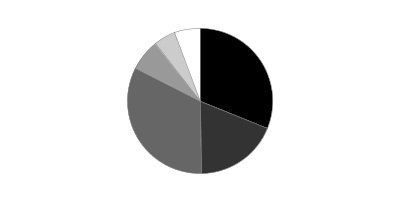

Top Five Market Sectors as of July 31, 2017

| % of fund's net assets | |

| Information Technology | 27.2 |

| Health Care | 19.0 |

| Industrials | 17.4 |

| Consumer Discretionary | 15.6 |

| Financials | 8.2 |

Asset Allocation (% of fund's net assets)

| As of July 31, 2017* | ||

| Stocks | 97.8% | |

| Short-Term Investments and Net Other Assets (Liabilities) | 2.2% | |

* Foreign investments - 9.2%

Investments July 31, 2017

Showing Percentage of Net Assets

| Common Stocks - 97.8% | |||

| Shares | Value | ||

| CONSUMER DISCRETIONARY - 15.6% | |||

| Diversified Consumer Services - 1.8% | |||

| Grand Canyon Education, Inc. (a) | 18,227 | $1,340,960 | |

| Hotels, Restaurants & Leisure - 7.2% | |||

| Boyd Gaming Corp. | 13,900 | 348,334 | |

| Cedar Fair LP (depositary unit) | 15,005 | 1,041,947 | |

| Churchill Downs, Inc. | 2,300 | 430,215 | |

| Dave & Buster's Entertainment, Inc. (a) | 45 | 2,795 | |

| Del Taco Restaurants, Inc. (a) | 14,000 | 183,260 | |

| Marriott Vacations Worldwide Corp. | 3,526 | 412,013 | |

| Papa John's International, Inc. | 3,739 | 266,703 | |

| Texas Roadhouse, Inc. Class A | 14,501 | 685,897 | |

| U.S. Foods Holding Corp. (a) | 21,549 | 606,604 | |

| Vail Resorts, Inc. | 5,139 | 1,083,096 | |

| Wingstop, Inc. | 9,868 | 296,139 | |

| 5,357,003 | |||

| Household Durables - 2.2% | |||

| Cavco Industries, Inc. (a) | 5,336 | 695,814 | |

| LGI Homes, Inc. (a) | 14,203 | 629,193 | |

| SodaStream International Ltd. (a) | 5,414 | 304,916 | |

| 1,629,923 | |||

| Internet & Direct Marketing Retail - 0.3% | |||

| Gaia, Inc. Class A (a) | 15,708 | 189,281 | |

| Media - 1.2% | |||

| Cinemark Holdings, Inc. | 16,562 | 644,262 | |

| Gray Television, Inc. (a) | 18,737 | 279,181 | |

| 923,443 | |||

| Multiline Retail - 0.6% | |||

| Ollie's Bargain Outlet Holdings, Inc. (a) | 9,858 | 440,653 | |

| Specialty Retail - 1.3% | |||

| Cars.com, Inc. (a) | 13,395 | 325,499 | |

| The Children's Place Retail Stores, Inc. | 6,446 | 681,020 | |

| 1,006,519 | |||

| Textiles, Apparel & Luxury Goods - 1.0% | |||

| Akcea Therapeutics, Inc. | 10,372 | 149,253 | |

| Emerald Expositions Events, Inc. | 14,503 | 331,974 | |

| PetIQ, Inc. Class A | 12,700 | 295,656 | |

| 776,883 | |||

| TOTAL CONSUMER DISCRETIONARY | 11,664,665 | ||

| CONSUMER STAPLES - 3.1% | |||

| Beverages - 0.0% | |||

| National Beverage Corp. | 16 | 1,634 | |

| Food & Staples Retailing - 0.7% | |||

| Performance Food Group Co. (a) | 18,938 | 545,414 | |

| Food Products - 0.8% | |||

| Post Holdings, Inc. (a) | 7,473 | 621,754 | |

| Household Products - 1.2% | |||

| Central Garden & Pet Co. (a) | 10,569 | 338,208 | |

| Central Garden & Pet Co. Class A (non-vtg.) (a) | 17,827 | 548,359 | |

| 886,567 | |||

| Personal Products - 0.4% | |||

| Herbalife Ltd. (a) | 4,332 | 288,121 | |

| TOTAL CONSUMER STAPLES | 2,343,490 | ||

| ENERGY - 0.5% | |||

| Energy Equipment & Services - 0.4% | |||

| Dril-Quip, Inc. (a) | 17 | 758 | |

| Frank's International NV | 18,730 | 151,713 | |

| Tesco Corp. (a) | 27,028 | 124,329 | |

| 276,800 | |||

| Oil, Gas & Consumable Fuels - 0.1% | |||

| Callon Petroleum Co. (a) | 117 | 1,324 | |

| StealthGas, Inc. (a) | 30,300 | 90,900 | |

| 92,224 | |||

| TOTAL ENERGY | 369,024 | ||

| FINANCIALS - 8.2% | |||

| Banks - 0.4% | |||

| Banner Corp. | 4,533 | 261,871 | |

| Investors Bancorp, Inc. | 168 | 2,231 | |

| 264,102 | |||

| Capital Markets - 2.9% | |||

| Apollo Global Management LLC Class A | 23,765 | 667,797 | |

| CBOE Holdings, Inc. | 7,452 | 704,438 | |

| MSCI, Inc. | 7,654 | 833,903 | |

| 2,206,138 | |||

| Diversified Financial Services - 1.5% | |||

| Cotiviti Holdings, Inc. (a) | 25,376 | 1,092,437 | |

| Insurance - 2.1% | |||

| Assured Guaranty Ltd. | 9,664 | 434,977 | |

| Enstar Group Ltd. (a) | 2,619 | 530,609 | |

| ProAssurance Corp. | 10,171 | 628,568 | |

| 1,594,154 | |||

| Thrifts & Mortgage Finance - 1.3% | |||

| Essent Group Ltd. (a) | 15,004 | 576,454 | |

| Meridian Bancorp, Inc. Maryland | 23,975 | 423,159 | |

| 999,613 | |||

| TOTAL FINANCIALS | 6,156,444 | ||

| HEALTH CARE - 19.0% | |||

| Biotechnology - 5.4% | |||

| Achaogen, Inc. (a) | 9,365 | 178,029 | |

| Acorda Therapeutics, Inc. (a) | 9,777 | 211,672 | |

| Advanced Accelerator Applications SA sponsored ADR (a) | 3,800 | 182,362 | |

| Alder Biopharmaceuticals, Inc. (a) | 7,765 | 83,474 | |

| Amarin Corp. PLC ADR (a) | 23,362 | 82,701 | |

| Amicus Therapeutics, Inc. (a) | 23,368 | 302,616 | |

| Ascendis Pharma A/S sponsored ADR (a) | 9,600 | 270,720 | |

| Blueprint Medicines Corp. (a) | 7,756 | 405,871 | |

| Coherus BioSciences, Inc. (a) | 7,213 | 94,130 | |

| Curis, Inc. (a) | 56,174 | 109,539 | |

| DBV Technologies SA sponsored ADR (a) | 3,630 | 161,680 | |

| Five Prime Therapeutics, Inc. (a) | 3,600 | 101,304 | |

| Heron Therapeutics, Inc. (a) | 7,700 | 122,045 | |

| Intercept Pharmaceuticals, Inc. (a) | 700 | 81,991 | |

| Iovance Biotherapeutics, Inc. (a) | 7,015 | 41,038 | |

| La Jolla Pharmaceutical Co. (a) | 5,100 | 151,113 | |

| Loxo Oncology, Inc. (a) | 4,029 | 291,337 | |

| Macrogenics, Inc. (a) | 5,855 | 96,725 | |

| Otonomy, Inc. (a) | 7,955 | 149,554 | |

| Proteostasis Therapeutics, Inc. (a) | 5,749 | 16,327 | |

| Puma Biotechnology, Inc. (a) | 2,821 | 268,136 | |

| Repligen Corp. (a) | 5,841 | 235,217 | |

| Sarepta Therapeutics, Inc. (a) | 40 | 1,543 | |

| TESARO, Inc. (a) | 2,014 | 257,107 | |

| Ultragenyx Pharmaceutical, Inc. (a) | 2,618 | 173,626 | |

| 4,069,857 | |||

| Health Care Equipment & Supplies - 5.8% | |||

| Cantel Medical Corp. | 8,055 | 597,681 | |

| Globus Medical, Inc. (a) | 11,686 | 359,345 | |

| Inogen, Inc. (a) | 3,324 | 313,719 | |

| Insulet Corp. (a) | 7,049 | 354,635 | |

| Integra LifeSciences Holdings Corp. (a) | 12,084 | 600,091 | |

| iRhythm Technologies, Inc. | 12,189 | 504,137 | |

| Novocure Ltd. (a) | 33,904 | 698,422 | |

| NxStage Medical, Inc. (a) | 24,093 | 567,390 | |

| Wright Medical Group NV (a) | 13,081 | 343,638 | |

| 4,339,058 | |||

| Health Care Providers & Services - 1.2% | |||

| LHC Group, Inc. (a) | 7,050 | 408,195 | |

| Premier, Inc. (a) | 13,300 | 464,170 | |

| 872,365 | |||

| Health Care Technology - 1.7% | |||

| athenahealth, Inc. (a) | 2,600 | 359,632 | |

| Evolent Health, Inc. (a) | 18,213 | 449,861 | |

| Veeva Systems, Inc. Class A (a) | 7,058 | 450,018 | |

| 1,259,511 | |||

| Life Sciences Tools & Services - 2.6% | |||

| Accelerate Diagnostics, Inc. (a) | 9,872 | 259,140 | |

| Bio-Rad Laboratories, Inc. Class A (a) | 1,712 | 403,399 | |

| Cambrex Corp. (a) | 9,868 | 601,948 | |

| ICON PLC (a) | 6,343 | 665,698 | |

| 1,930,185 | |||

| Pharmaceuticals - 2.3% | |||

| Aclaris Therapeutics, Inc. (a) | 5,640 | 162,432 | |

| Aerie Pharmaceuticals, Inc. (a) | 4,634 | 251,626 | |

| Avexis, Inc. (a) | 3,700 | 342,805 | |

| Catalent, Inc. (a) | 12,590 | 436,873 | |

| Collegium Pharmaceutical, Inc. (a) | 43 | 515 | |

| NeuroDerm Ltd. (a) | 39 | 1,509 | |

| SCYNEXIS, Inc. (a) | 20,784 | 35,748 | |

| The Medicines Company (a) | 6,543 | 251,578 | |

| Theravance Biopharma, Inc. (a) | 6,900 | 221,697 | |

| 1,704,783 | |||

| TOTAL HEALTH CARE | 14,175,759 | ||

| INDUSTRIALS - 17.4% | |||

| Aerospace & Defense - 3.2% | |||

| BWX Technologies, Inc. | 18,119 | 954,509 | |

| Elbit Systems Ltd. | 2,418 | 304,716 | |

| HEICO Corp. Class A | 11,079 | 787,163 | |

| Teledyne Technologies, Inc. (a) | 2,815 | 383,797 | |

| 2,430,185 | |||

| Airlines - 0.4% | |||

| Allegiant Travel Co. | 13 | 1,680 | |

| SkyWest, Inc. | 8,663 | 316,200 | |

| 317,880 | |||

| Building Products - 1.2% | |||

| A.O. Smith Corp. | 10,170 | 544,604 | |

| Universal Forest Products, Inc. | 4,435 | 371,875 | |

| 916,479 | |||

| Commercial Services & Supplies - 1.1% | |||

| Viad Corp. | 15,214 | 814,710 | |

| Construction & Engineering - 2.0% | |||

| Dycom Industries, Inc. (a) | 4,230 | 383,238 | |

| KBR, Inc. | 75,653 | 1,128,743 | |

| 1,511,981 | |||

| Electrical Equipment - 0.6% | |||

| Regal Beloit Corp. | 5,037 | 419,834 | |

| Machinery - 5.6% | |||

| AGCO Corp. | 10,268 | 740,734 | |

| Allison Transmission Holdings, Inc. | 24,369 | 921,148 | |

| Colfax Corp. (a) | 8,460 | 349,229 | |

| IDEX Corp. | 22 | 2,564 | |

| John Bean Technologies Corp. | 4,231 | 390,944 | |

| Kornit Digital Ltd. (a) | 9,367 | 193,897 | |

| Milacron Holdings Corp. (a) | 22,254 | 400,127 | |

| WABCO Holdings, Inc. (a) | 8,756 | 1,204,563 | |

| 4,203,206 | |||

| Professional Services - 0.4% | |||

| CBIZ, Inc. (a) | 21,759 | 323,121 | |

| Road & Rail - 0.3% | |||

| Marten Transport Ltd. | 12,286 | 195,962 | |

| Trading Companies & Distributors - 2.6% | |||

| SiteOne Landscape Supply, Inc. (a) | 25,980 | 1,363,950 | |

| Univar, Inc. (a) | 17,830 | 553,443 | |

| 1,917,393 | |||

| TOTAL INDUSTRIALS | 13,050,751 | ||

| INFORMATION TECHNOLOGY - 27.2% | |||

| Communications Equipment - 0.6% | |||

| InterDigital, Inc. | 4,130 | 300,871 | |

| Viavi Solutions, Inc. (a) | 9,799 | 107,495 | |

| 408,366 | |||

| Electronic Equipment & Components - 1.9% | |||

| Cardtronics PLC | 13,499 | 422,519 | |

| Cognex Corp. | 2,819 | 267,974 | |

| Jabil, Inc. | 18,247 | 556,534 | |

| Novanta, Inc. (a) | 5,641 | 208,153 | |

| 1,455,180 | |||

| Internet Software & Services - 11.3% | |||

| 2U, Inc. (a) | 42,712 | 2,210,340 | |

| Alarm.com Holdings, Inc. (a) | 7,051 | 268,150 | |

| BlackLine, Inc. | 2,618 | 101,500 | |

| Five9, Inc. (a) | 18,737 | 413,338 | |

| GoDaddy, Inc. (a) | 22,359 | 960,990 | |

| Gogo, Inc. (a) | 53,572 | 652,507 | |

| Instructure, Inc. (a) | 18,136 | 586,700 | |

| LogMeIn, Inc. | 100 | 11,645 | |

| MINDBODY, Inc. (a) | 28,147 | 730,415 | |

| Stamps.com, Inc. (a) | 12,789 | 1,894,051 | |

| The Trade Desk, Inc. | 5,238 | 279,238 | |

| Wix.com Ltd. (a) | 5,839 | 360,266 | |

| 8,469,140 | |||

| IT Services - 1.5% | |||

| EPAM Systems, Inc. (a) | 7,756 | 666,473 | |

| Euronet Worldwide, Inc. (a) | 5,037 | 486,625 | |

| 1,153,098 | |||

| Semiconductors & Semiconductor Equipment - 5.0% | |||

| Cavium, Inc. (a) | 7,747 | 479,849 | |

| Cypress Semiconductor Corp. | 24,568 | 348,866 | |

| Entegris, Inc. (a) | 30,914 | 806,855 | |

| Integrated Device Technology, Inc. (a) | 25,074 | 655,434 | |

| Monolithic Power Systems, Inc. | 1,913 | 195,738 | |

| Nanometrics, Inc. (a) | 17,629 | 469,813 | |

| PDF Solutions, Inc. (a) | 27,702 | 444,617 | |

| Semtech Corp. (a) | 8,073 | 319,691 | |

| 3,720,863 | |||

| Software - 6.9% | |||

| ACI Worldwide, Inc. (a) | 16,823 | 389,789 | |

| Blackbaud, Inc. | 4,735 | 437,230 | |

| CommVault Systems, Inc. (a) | 10,263 | 611,162 | |

| Digimarc Corp. (a) | 2,000 | 62,700 | |

| HubSpot, Inc. (a) | 7,000 | 506,450 | |

| Parametric Technology Corp. (a) | 4,874 | 268,996 | |

| Paycom Software, Inc. (a) | 9,364 | 656,323 | |

| Pegasystems, Inc. | 2,324 | 140,486 | |

| Proofpoint, Inc. (a) | 5,136 | 437,793 | |

| PROS Holdings, Inc. (a) | 13,997 | 403,534 | |

| RingCentral, Inc. (a) | 11,686 | 406,673 | |

| Tableau Software, Inc. (a) | 3,526 | 227,251 | |

| Take-Two Interactive Software, Inc. (a) | 7,754 | 616,288 | |

| 5,164,675 | |||

| TOTAL INFORMATION TECHNOLOGY | 20,371,322 | ||

| MATERIALS - 4.5% | |||

| Chemicals - 2.8% | |||

| Innospec, Inc. | 1,618 | 100,963 | |

| Platform Specialty Products Corp. (a) | 39,791 | 557,472 | |

| The Chemours Co. LLC | 29,787 | 1,418,159 | |

| Trinseo SA | 56 | 3,937 | |

| 2,080,531 | |||

| Construction Materials - 0.6% | |||

| Summit Materials, Inc. | 15,100 | 429,444 | |

| Containers & Packaging - 0.5% | |||

| Berry Global Group, Inc. (a) | 6,357 | 356,501 | |

| Paper & Forest Products - 0.6% | |||

| Neenah Paper, Inc. | 4,936 | 394,386 | |

| Quintis Ltd. | 273,256 | 64,488 | |

| 458,874 | |||

| TOTAL MATERIALS | 3,325,350 | ||

| REAL ESTATE - 2.0% | |||

| Equity Real Estate Investment Trusts (REITs) - 2.0% | |||

| CoreSite Realty Corp. | 3,021 | 328,020 | |

| Hudson Pacific Properties, Inc. | 10,779 | 352,689 | |

| Store Capital Corp. | 19,140 | 447,685 | |

| Terreno Realty Corp. | 9,765 | 338,064 | |

| 1,466,458 | |||

| UTILITIES - 0.3% | |||

| Independent Power and Renewable Electricity Producers - 0.3% | |||

| Ormat Technologies, Inc. | 3,526 | 209,092 | |

| TOTAL COMMON STOCKS | |||

| (Cost $73,189,288) | 73,132,355 | ||

| Money Market Funds - 2.0% | |||

| Fidelity Cash Central Fund, 1.11% (b) | |||

| (Cost $1,519,640) | 1,519,336 | 1,519,640 | |

| TOTAL INVESTMENT PORTFOLIO - 99.8% | |||

| (Cost $74,708,928) | 74,651,995 | ||

| NET OTHER ASSETS (LIABILITIES) - 0.2% | 168,767 | ||

| NET ASSETS - 100% | $74,820,762 |

Legend

(a) Non-income producing

(b) Affiliated fund that is generally available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC's website or upon request.

Affiliated Central Funds

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows:

| Fund | Income earned |

| Fidelity Cash Central Fund | $118 |

| Total | $118 |

Investment Valuation

The following is a summary of the inputs used, as of July 31, 2017, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used below, please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| Valuation Inputs at Reporting Date: | ||||

| Description | Total | Level 1 | Level 2 | Level 3 |

| Investments in Securities: | ||||

| Equities: | ||||

| Consumer Discretionary | $11,664,665 | $11,664,665 | $-- | $-- |

| Consumer Staples | 2,343,490 | 2,343,490 | -- | -- |

| Energy | 369,024 | 369,024 | -- | -- |

| Financials | 6,156,444 | 6,156,444 | -- | -- |

| Health Care | 14,175,759 | 14,175,759 | -- | -- |

| Industrials | 13,050,751 | 13,050,751 | -- | -- |

| Information Technology | 20,371,322 | 20,371,322 | -- | -- |

| Materials | 3,325,350 | 3,260,862 | -- | 64,488 |

| Real Estate | 1,466,458 | 1,466,458 | -- | -- |

| Utilities | 209,092 | 209,092 | -- | -- |

| Money Market Funds | 1,519,640 | 1,519,640 | -- | -- |

| Total Investments in Securities: | $74,651,995 | $74,587,507 | $-- | $64,488 |

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| July 31, 2017 | ||

| Assets | ||

| Investment in securities, at value — See accompanying schedule: Unaffiliated issuers (cost $73,189,288) | $73,132,355 | |

| Fidelity Central Funds (cost $1,519,640) | 1,519,640 | |

| Total Investments (cost $74,708,928) | $74,651,995 | |

| Receivable for investments sold | 176,872 | |

| Receivable for fund shares sold | 50,646 | |

| Dividends receivable | 62 | |

| Distributions receivable from Fidelity Central Funds | 46 | |

| Total assets | 74,879,621 | |

| Liabilities | ||

| Payable for fund shares redeemed | $56,744 | |

| Accrued management fee | 2,115 | |

| Total liabilities | 58,859 | |

| Net Assets | $74,820,762 | |

| Net Assets consist of: | ||

| Paid in capital | $74,878,444 | |

| Accumulated undistributed net realized gain (loss) on investments and foreign currency transactions | (749) | |

| Net unrealized appreciation (depreciation) on investments | (56,933) | |

| Net Assets, for 7,181,213 shares outstanding | $74,820,762 | |

| Net Asset Value, offering price and redemption price per share ($74,820,762 ÷ 7,181,213 shares) | $10.42 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| For the period May 25, 2017 (commencement of operations) to July 31, 2017 |

||

| Investment Income | ||

| Dividends | $545 | |

| Income from Fidelity Central Funds | 118 | |

| Total income | 663 | |

| Expenses | ||

| Management fee | $2,414 | |

| Independent trustees' fees and expenses | 1 | |

| Total expenses | 2,415 | |

| Net investment income (loss) | (1,752) | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 904 | |

| Foreign currency transactions | 1 | |

| Total net realized gain (loss) | 905 | |

| Change in net unrealized appreciation (depreciation) on investment securities | (56,933) | |

| Net gain (loss) | (56,028) | |

| Net increase (decrease) in net assets resulting from operations | $(57,780) |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| For the period May 25, 2017 (commencement of operations) to July 31, 2017 |

|

| Increase (Decrease) in Net Assets | |

| Operations | |

| Net investment income (loss) | $(1,752) |

| Net realized gain (loss) | 905 |

| Change in net unrealized appreciation (depreciation) | (56,933) |

| Net increase (decrease) in net assets resulting from operations | (57,780) |

| Share transactions | |

| Proceeds from sales of shares | 74,935,286 |

| Cost of shares redeemed | (56,744) |

| Net increase (decrease) in net assets resulting from share transactions | 74,878,542 |

| Total increase (decrease) in net assets | 74,820,762 |

| Net Assets | |

| Beginning of period | – |

| End of period | $74,820,762 |

| Other Information | |

| Shares | |

| Sold | 7,186,659 |

| Redeemed | (5,446) |

| Net increase (decrease) | 7,181,213 |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights — Fidelity Small Cap Growth K6 Fund

| Years ended July 31, | 2017 A |

| Selected Per–Share Data | |

| Net asset value, beginning of period | $10.00 |

| Income from Investment Operations | |

| Net investment income (loss)B | (.01) |

| Net realized and unrealized gain (loss) | .43 |

| Total from investment operations | .42 |

| Net asset value, end of period | $10.42 |

| Total ReturnC | 4.20% |

| Ratios to Average Net AssetsD,E | |

| Expenses before reductions | .60%F |

| Expenses net of fee waivers, if any | .60%F |

| Expenses net of all reductions | .60%F |

| Net investment income (loss) | (.45)%F |

| Supplemental Data | |

| Net assets, end of period (000 omitted) | $74,821 |

| Portfolio turnover rateG | 79%H,I |

A For the period May 25, 2017 (commencement of operations) to July 31, 2017.

B Calculated based on average shares outstanding during the period.

C Total returns for periods of less than one year are not annualized.

D Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

E Expense ratios reflect operating expenses of the Fund. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the Fund during periods when reimbursements or reductions occur. Expense ratios before reductions for start-up periods may not be representative of longer term operating periods. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the Fund.

F Annualized

G Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

H Portfolio turnover rate excludes securities received or delivered in-kind.

I Amount not annualized.

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements

For the period ended July 31, 2017

1. Organization.

Fidelity Small Cap Growth K6 Fund (the Fund) is a fund of Fidelity Securities Fund (the Trust) and is authorized to issue an unlimited number of shares. Share transactions on the Statement of Changes in Net Assets may contain exchanges between affiliated funds. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. Shares generally are available only to employer-sponsored retirement plans that are recordkept by Fidelity.

2. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies generally available only to other investment companies and accounts managed by the investment adviser and its affiliates. The Fund's Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but does not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of the investment adviser. Annualized expenses of the Money Market Central Funds as of their most recent shareholder report date are less than .005%.

A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) website at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC website or upon request.

3. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investments Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Board of Trustees (the Board) has delegated the day to day responsibility for the valuation of the Fund's investments to the Fair Value Committee (the Committee) established by the Fund's investment adviser. In accordance with valuation policies and procedures approved by the Board, the Fund attempts to obtain prices from one or more third party pricing vendors or brokers to value its investments. When current market prices, quotations or currency exchange rates are not readily available or reliable, investments will be fair valued in good faith by the Committee, in accordance with procedures adopted by the Board. Factors used in determining fair value vary by investment type and may include market or investment specific events. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The Committee oversees the Fund's valuation policies and procedures and reports to the Board on the Committee's activities and fair value determinations. The Board monitors the appropriateness of the procedures used in valuing the Fund's investments and ratifies the fair value determinations of the Committee.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

Valuation techniques used to value the Fund's investments by major category are as follows:

Equity securities, including restricted securities, for which market quotations are readily available, are valued at the last reported sale price or official closing price as reported by a third party pricing vendor on the primary market or exchange on which they are traded and are categorized as Level 1 in the hierarchy. In the event there were no sales during the day or closing prices are not available, securities are valued at the last quoted bid price or may be valued using the last available price and are generally categorized as Level 2 in the hierarchy. For foreign equity securities, when market or security specific events arise, comparisons to the valuation of American Depositary Receipts (ADRs), futures contracts, Exchange-Traded Funds (ETFs) and certain indexes as well as quoted prices for similar securities may be used and would be categorized as Level 2 in the hierarchy. Utilizing these techniques may result in transfers between Level 1 and Level 2. For equity securities, including restricted securities, where observable inputs are limited, assumptions about market activity and risk are used and these securities may be categorized as Level 3 in the hierarchy.

Investments in open-end mutual funds, including the Fidelity Central Funds, are valued at their closing net asset value (NAV) each business day and are categorized as Level 1 in the hierarchy.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The aggregate value of investments by input level as of July 31, 2017 is included at the end of the Fund's Schedule of Investments.

Foreign Currency. The Fund may use foreign currency contracts to facilitate transactions in foreign-denominated securities. Gains and losses from these transactions may arise from changes in the value of the foreign currency or if the counterparties do not perform under the contracts' terms.

Foreign-denominated assets, including investment securities, and liabilities are translated into U.S. dollars at the exchange rates at period end. Purchases and sales of investment securities, income and dividends received and expenses denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date.

The effects of exchange rate fluctuations on investments are included with the net realized and unrealized gain (loss) on investment securities. Other foreign currency transactions resulting in realized and unrealized gain (loss) are disclosed separately.

Investment Transactions and Income. For financial reporting purposes, the Fund's investment holdings and NAV include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day. Gains and losses on securities sold are determined on the basis of identified cost. Dividend income is recorded on the ex-dividend date, except for certain dividends from foreign securities where the ex-dividend date may have passed, which are recorded as soon as the Fund is informed of the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Income and capital gain distributions from Fidelity Central Funds, if any, are recorded on the ex-dividend date. Certain distributions received by the Fund represent a return of capital or capital gain. The Fund determines the components of these distributions subsequent to the ex-dividend date, based upon receipt of tax filings or other correspondence relating to the underlying investment. These distributions are recorded as a reduction of cost of investments and/or as a realized gain. Investment income is recorded net of foreign taxes withheld where recovery of such taxes is uncertain.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. As of July 31, 2017, the Fund did not have any unrecognized tax benefits in the financial statements; nor is the Fund aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction. Foreign taxes are provided for based on the Fund's understanding of the tax rules and rates that exist in the foreign markets in which it invests.

Distributions are declared and recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to foreign currency transactions, partnerships, net operating losses, passive foreign investment companies (PFIC), and losses deferred due to wash sales.

The federal tax cost of investment securities and unrealized appreciation (depreciation) as of period end were as follows:

| Gross unrealized appreciation | $367,881 |

| Gross unrealized depreciation | (425,570) |

| Net unrealized appreciation (depreciation) on securities | $(57,689) |

| Tax Cost | $74,709,684 |

The tax-based components of distributable earnings as of period end were as follows:

| Undistributed long-term capital gain | $7 |

| Net unrealized appreciation (depreciation) on securities and other investments | $(57,689) |

4. Purchases and Sales of Investments.

Purchases and sales of securities, other than short-term securities and in-kind transactions, aggregated $650,588 and $329,654, respectively.

5. Fees and Other Transactions with Affiliates.

Management Fee. Fidelity Management & Research Company (the investment adviser) and its affiliates provide the Fund with investment management related services for which the Fund pays a monthly management fee that is based on an annual rate of .60% of average net assets. Under the management contract, the investment adviser or an affiliate pays all other expenses of the Fund, excluding fees and expenses of the independent Trustees, and certain miscellaneous expenses such as proxy and shareholder meeting expenses.

Brokerage Commissions. The Fund placed a portion of its portfolio transactions with brokerage firms which are affiliates of the investment adviser. Brokerage commissions are included in net realized gain (loss) and change in net unrealized appreciation (depreciation) in the Statement of Operations. The commissions paid to these affiliated firms were $59 for the period.

Interfund Trades. The Fund may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act. Interfund trades are included within the respective purchases and sales amounts shown in the Purchases and Sales of Investments note.

Exchanges In-Kind. During the period, an affiliated entity completed an exchange in-kind with the Fund. The affiliated entity delivered investments and cash valued at $74,384,639 in exchange for 7,131,797 shares of the Fund. The amount of in-kind exchanges is included in share transactions in the accompanying Statement of Changes in Net Assets. The Fund recognized no gain or loss for federal income tax purposes.

6. Other.

The Fund's organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

At the end of the period, the investment adviser or its affiliates were the owners of record of 100% of the total outstanding shares of the Fund.

Report of Independent Registered Public Accounting Firm

To the Trustees of Fidelity Securities Fund and Shareholders of Fidelity Small Cap Growth K6 Fund:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Fidelity Small Cap Growth K6 Fund (a fund of Fidelity Securities Fund) as of July 31, 2017, the results of its operations, the changes in its net assets and the financial highlights for the period May 25, 2017 (commencement of operations) through July 31, 2017, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fidelity Small Cap Growth K6 Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of July 31, 2017 by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audit provides a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Boston, Massachusetts

September 19, 2017

Trustees and Officers

The Trustees, Members of the Advisory Board (if any), and officers of the trust and fund, as applicable, are listed below. The Board of Trustees governs the fund and is responsible for protecting the interests of shareholders. The Trustees are experienced executives who meet periodically throughout the year to oversee the fund's activities, review contractual arrangements with companies that provide services to the fund, oversee management of the risks associated with such activities and contractual arrangements, and review the fund's performance. Except for Jonathan Chiel, each of the Trustees oversees 190 funds. Mr. Chiel oversees 142 funds.

The Trustees hold office without limit in time except that (a) any Trustee may resign; (b) any Trustee may be removed by written instrument, signed by at least two-thirds of the number of Trustees prior to such removal; (c) any Trustee who requests to be retired or who has become incapacitated by illness or injury may be retired by written instrument signed by a majority of the other Trustees; and (d) any Trustee may be removed at any special meeting of shareholders by a two-thirds vote of the outstanding voting securities of the trust. Each Trustee who is not an interested person (as defined in the 1940 Act) of the trust and the fund is referred to herein as an Independent Trustee. Each Independent Trustee shall retire not later than the last day of the calendar year in which his or her 75th birthday occurs. The Independent Trustees may waive this mandatory retirement age policy with respect to individual Trustees. Officers and Advisory Board Members hold office without limit in time, except that any officer or Advisory Board Member may resign or may be removed by a vote of a majority of the Trustees at any regular meeting or any special meeting of the Trustees. Except as indicated, each individual has held the office shown or other offices in the same company for the past five years.

The fund’s Statement of Additional Information (SAI) includes more information about the Trustees. To request a free copy, call Fidelity at 1-800-835-5092.

Experience, Skills, Attributes, and Qualifications of the Trustees. The Governance and Nominating Committee has adopted a statement of policy that describes the experience, qualifications, attributes, and skills that are necessary and desirable for potential Independent Trustee candidates (Statement of Policy). The Board believes that each Trustee satisfied at the time he or she was initially elected or appointed a Trustee, and continues to satisfy, the standards contemplated by the Statement of Policy. The Governance and Nominating Committee also engages professional search firms to help identify potential Independent Trustee candidates who have the experience, qualifications, attributes, and skills consistent with the Statement of Policy. From time to time, additional criteria based on the composition and skills of the current Independent Trustees, as well as experience or skills that may be appropriate in light of future changes to board composition, business conditions, and regulatory or other developments, have also been considered by the professional search firms and the Governance and Nominating Committee. In addition, the Board takes into account the Trustees' commitment and participation in Board and committee meetings, as well as their leadership of standing and ad hoc committees throughout their tenure.

In determining that a particular Trustee was and continues to be qualified to serve as a Trustee, the Board has considered a variety of criteria, none of which, in isolation, was controlling. The Board believes that, collectively, the Trustees have balanced and diverse experience, qualifications, attributes, and skills, which allow the Board to operate effectively in governing the fund and protecting the interests of shareholders. Information about the specific experience, skills, attributes, and qualifications of each Trustee, which in each case led to the Board's conclusion that the Trustee should serve (or continue to serve) as a trustee of the fund, is provided below.

Board Structure and Oversight Function. James C. Curvey is an interested person and currently serves as Chairman. The Trustees have determined that an interested Chairman is appropriate and benefits shareholders because an interested Chairman has a personal and professional stake in the quality and continuity of services provided to the fund. Independent Trustees exercise their informed business judgment to appoint an individual of their choosing to serve as Chairman, regardless of whether the Trustee happens to be independent or a member of management. The Independent Trustees have determined that they can act independently and effectively without having an Independent Trustee serve as Chairman and that a key structural component for assuring that they are in a position to do so is for the Independent Trustees to constitute a substantial majority for the Board. The Independent Trustees also regularly meet in executive session. Ned C. Lautenbach serves as Chairman of the Independent Trustees and as such (i) acts as a liaison between the Independent Trustees and management with respect to matters important to the Independent Trustees and (ii) with management prepares agendas for Board meetings.

Fidelity® funds are overseen by different Boards of Trustees. The fund's Board oversees Fidelity's high income and certain equity funds, and other Boards oversee Fidelity's investment-grade bond, money market, asset allocation, and sector funds. The asset allocation funds may invest in Fidelity® funds overseen by the fund's Board. The use of separate Boards, each with its own committee structure, allows the Trustees of each group of Fidelity® funds to focus on the unique issues of the funds they oversee, including common research, investment, and operational issues. On occasion, the separate Boards establish joint committees to address issues of overlapping consequences for the Fidelity® funds overseen by each Board.

The Trustees operate using a system of committees to facilitate the timely and efficient consideration of all matters of importance to the Trustees, the fund, and fund shareholders and to facilitate compliance with legal and regulatory requirements and oversight of the fund's activities and associated risks. The Board, acting through its committees, has charged FMR and its affiliates with (i) identifying events or circumstances the occurrence of which could have demonstrably adverse effects on the fund's business and/or reputation; (ii) implementing processes and controls to lessen the possibility that such events or circumstances occur or to mitigate the effects of such events or circumstances if they do occur; and (iii) creating and maintaining a system designed to evaluate continuously business and market conditions in order to facilitate the identification and implementation processes described in (i) and (ii) above. Because the day-to-day operations and activities of the fund are carried out by or through FMR, its affiliates, and other service providers, the fund's exposure to risks is mitigated but not eliminated by the processes overseen by the Trustees. While each of the Board's committees has responsibility for overseeing different aspects of the fund's activities, oversight is exercised primarily through the Operations, Audit, and Compliance Committees. In addition, the Independent Trustees have worked with FMR to enhance the Board's oversight of investment and financial risks, legal and regulatory risks, technology risks, and operational risks, including the development of additional risk reporting to the Board. For example, a working group comprised of Independent Trustees and FMR has worked and continues to work to review the Fidelity® funds' valuation-related activities, reporting and risk management. Appropriate personnel, including but not limited to the fund's Chief Compliance Officer (CCO), FMR's internal auditor, the independent accountants, the fund's Treasurer and portfolio management personnel, make periodic reports to the Board's committees, as appropriate, including an annual review of Fidelity's risk management program for the Fidelity® funds. The responsibilities of each standing committee, including their oversight responsibilities, are described further under "Standing Committees of the Trustees."

Interested Trustees*:

Correspondence intended for a Trustee who is an interested person may be sent to Fidelity Investments, 245 Summer Street, Boston, Massachusetts 02210.

Name, Year of Birth; Principal Occupations and Other Relevant Experience+

Jonathan Chiel (1957)

Year of Election or Appointment: 2016

Trustee

Mr. Chiel also serves as Trustee of other Fidelity funds. Mr. Chiel is Executive Vice President and General Counsel for FMR LLC (diversified financial services company, 2012-present). Previously, Mr. Chiel served as general counsel (2004-2012) and senior vice president and deputy general counsel (2000-2004) for John Hancock Financial Services; a partner with Choate, Hall & Stewart (1996-2000) (law firm); and an Assistant United States Attorney for the United States Attorney’s Office of the District of Massachusetts (1986-95), including Chief of the Criminal Division (1993-1995). Mr. Chiel is a director on the boards of the Boston Bar Foundation and the Maimonides School.

James C. Curvey (1935)

Year of Election or Appointment: 2007

Trustee

Chairman of the Board of Trustees

Mr. Curvey also serves as Trustee of other Fidelity® funds. Mr. Curvey is a Director of Fidelity Research & Analysis Co. (investment adviser firm, 2009-present), and Vice Chairman (2007-present) and Director of FMR LLC (diversified financial services company). In addition, Mr. Curvey serves as an Overseer for the Boston Symphony Orchestra and a member of the board of Artis-Naples, Naples, Florida, and as a Trustee for Brewster Academy, Wolfeboro, New Hampshire. Previously, Mr. Curvey served as a Director of Fidelity Investments Money Management, Inc. (investment adviser firm, 2009-2014) and a Director of FMR and FMR Co., Inc. (investment adviser firms, 2007-2014).

Charles S. Morrison (1960)

Year of Election or Appointment: 2014

Trustee

Mr. Morrison also serves as Trustee of other funds. He serves as President of Fidelity Management & Research Company (FMR) (investment adviser firm, 2016-present), a Director of Fidelity Investments Money Management, Inc. (FIMM) (investment adviser firm, 2014-present), Director of Fidelity SelectCo, LLC (investment adviser firm, 2014-present), President, Asset Management (2014-present), and is an employee of Fidelity Investments. Previously, Mr. Morrison served as Vice President of Fidelity's Fixed Income and Asset Allocation Funds (2012-2014), President, Fixed Income (2011-2014), Vice President of Fidelity's Money Market Funds (2005-2009), President, Money Market Group Leader of FMR (investment adviser firm, 2009), and Senior Vice President, Money Market Group of FMR (2004-2009). Mr. Morrison also served as Vice President of Fidelity's Bond Funds (2002-2005), certain Balanced Funds (2002-2005), and certain Asset Allocation Funds (2002-2007), and as Senior Vice President (2002-2005) of Fidelity's Bond Division.

* Determined to be an “Interested Trustee” by virtue of, among other things, his or her affiliation with the trust or various entities under common control with FMR.

+ The information includes the Trustee's principal occupation during the last five years and other information relating to the experience, attributes, and skills relevant to the Trustee's qualifications to serve as a Trustee, which led to the conclusion that the Trustee should serve as a Trustee for the fund.

Independent Trustees:

Correspondence intended for an Independent Trustee may be sent to Fidelity Investments, P.O. Box 55235, Boston, Massachusetts 02205-5235.

Name, Year of Birth; Principal Occupations and Other Relevant Experience+

Dennis J. Dirks (1948)

Year of Election or Appointment: 2005

Trustee

Mr. Dirks also serves as Trustee of other Fidelity® funds. Prior to his retirement in May 2003, Mr. Dirks was Chief Operating Officer and a member of the Board of The Depository Trust & Clearing Corporation (DTCC). He also served as President, Chief Operating Officer, and Board member of The Depository Trust Company (DTC) and President and Board member of the National Securities Clearing Corporation (NSCC). In addition, Mr. Dirks served as Chief Executive Officer and Board member of the Government Securities Clearing Corporation, Chief Executive Officer and Board member of the Mortgage-Backed Securities Clearing Corporation, as a Trustee and a member of the Finance Committee of Manhattan College (2005-2008), as a Trustee and a member of the Finance Committee of AHRC of Nassau County (2006-2008), as a member of the Independent Directors Council (IDC) Governing Council (2010-2015), and as a member of the Board of Directors for The Brookville Center for Children’s Services, Inc. (2009-2017). Mr. Dirks is a member of the Finance Committee (2016-present) and Board of Directors (2017-present) of the Asolo Repertory Theatre.

Alan J. Lacy (1953)

Year of Election or Appointment: 2008

Trustee

Mr. Lacy also serves as Trustee of other Fidelity® funds. Mr. Lacy serves as a Director of Bristol-Myers Squibb Company (global pharmaceuticals, 2008-present). He is a Trustee of the California Chapter of The Nature Conservancy (2015-present) and a Director of the Center for Advanced Study in the Behavioral Sciences at Stanford University (2015-present). In addition, Mr. Lacy served as Senior Adviser (2007-2014) of Oak Hill Capital Partners, L.P. (private equity) and also served as Chief Executive Officer (2005) and Vice Chairman (2005-2006) of Sears Holdings Corporation (retail) and Chief Executive Officer and Chairman of the Board of Sears, Roebuck and Co. (retail, 2000-2005). Previously, Mr. Lacy served as Chairman (2014-2017) and a member (2010-2017) of the Board of Directors of Dave & Buster’s Entertainment, Inc. (restaurant and entertainment complexes), as Chairman (2008-2011) and a member (2006-2015) of the Board of Trustees of the National Parks Conservation Association, and as a member of the Board of Directors for The Hillman Companies, Inc. (hardware wholesalers, 2010-2014), Earth Fare, Inc. (retail grocery, 2010-2014), and The Western Union Company (global money transfer, 2006-2011).

Ned C. Lautenbach (1944)

Year of Election or Appointment: 2000

Trustee

Chairman of the Independent Trustees

Mr. Lautenbach also serves as Trustee of other Fidelity® funds. Mr. Lautenbach currently serves as the Lead Director of the Eaton Corporation Board of Directors (diversified industrial, 1997-present). Mr. Lautenbach is Chairman of the Board of Directors of Artis-Naples in Naples, Florida (2012-present), a member of the Council on Foreign Relations (1994-present), and currently Vice Chair of the Board of Governors, State University System of Florida (2013-present). Previously, Mr. Lautenbach was a Partner and Advisory Partner at Clayton, Dubilier & Rice, LLC (private equity investment, 1998-2010), as well as a Director of Sony Corporation (2006-2007). Mr. Lautenbach also had a 30-year career with IBM (technology company) during which time he served as Senior Vice President and a member of the Corporate Executive Committee (1968-1998).

Joseph Mauriello (1944)

Year of Election or Appointment: 2008

Trustee

Mr. Mauriello also serves as Trustee of other Fidelity® funds. Prior to his retirement in January 2006, Mr. Mauriello served in numerous senior management positions including Deputy Chairman and Chief Operating Officer (2004-2005), and Vice Chairman of Financial Services (2002-2004) of KPMG LLP US (professional services, 1965-2005). Mr. Mauriello currently serves as a member of the Board of Directors of XL Group plc. (global insurance and re-insurance, 2006-present) and the Independent Directors Council (IDC) Governing Council (2015-present). Previously, Mr. Mauriello served as a Director of the Hamilton Funds of the Bank of New York (2006-2007) and of Arcadia Resources Inc. (health care services and products, 2007-2012).

Cornelia M. Small (1944)

Year of Election or Appointment: 2005

Trustee

Ms. Small also serves as Trustee of other Fidelity® funds. Ms. Small is a member of the Board of Directors (2009-present) and Chair of the Investment Committee (2010-present) of the Teagle Foundation. Ms. Small also serves on the Investment Committee of the Berkshire Taconic Community Foundation (2008-present). Previously, Ms. Small served as Chairperson (2002-2008) and a member of the Investment Committee and Chairperson (2008-2012) and a member of the Board of Trustees of Smith College. In addition, Ms. Small served as Chief Investment Officer, Director of Global Equity Investments, and a member of the Board of Directors of Scudder, Stevens & Clark and Scudder Kemper Investments.

William S. Stavropoulos (1939)

Year of Election or Appointment: 2002

Trustee

Vice Chairman of the Independent Trustees

Mr. Stavropoulos also serves as Trustee of other Fidelity® funds. Mr. Stavropoulos serves as President and Founder of the Michigan Baseball Foundation, the Great Lakes Loons (2007-present). Mr. Stavropoulos is Chairman Emeritus of the Board of Directors of The Dow Chemical Company, where he previously served in numerous senior management positions, including President, CEO (1995-2000; 2002-2004), Chairman of the Executive Committee (2000-2006), and as a member of the Board of Directors (1990-2006). Currently, Mr. Stavropoulos is Chairman of the Board of Directors of Univar Inc. (global distributor of commodity and specialty chemicals), a Director of Teradata Corporation (data warehousing and technology solutions), and a member of the Advisory Board for Metalmark Capital LLC (private equity investment, 2005-present). Mr. Stavropoulos is an operating advisor to Clayton, Dubilier & Rice, LLC (private equity investment). In addition, Mr. Stavropoulos is a member of the University of Notre Dame Advisory Council for the College of Science, a Trustee of the Rollin L. Gerstacker Foundation, and a Director of Artis-Naples in Naples, Florida. Previously, Mr. Stavropoulos served as a Director of Chemical Financial Corporation (bank holding company, 1993-2012) and Tyco International, Ltd. (multinational manufacturing and services, 2007-2012).

David M. Thomas (1949)

Year of Election or Appointment: 2008

Trustee

Mr. Thomas also serves as Trustee of other Fidelity® funds. Mr. Thomas serves as Non-Executive Chairman of the Board of Directors of Fortune Brands Home and Security (home and security products, 2011-present), as a member of the Board of Directors (2004-present) and Presiding Director (2013-present) of Interpublic Group of Companies, Inc. (marketing communication), and as a member of the Board of Trustees of the University of Florida (2013-present). Previously, Mr. Thomas served as Executive Chairman (2005-2006) and Chairman and Chief Executive Officer (2000-2005) of IMS Health, Inc. (pharmaceutical and healthcare information solutions), and a Director of Fortune Brands, Inc. (consumer products, 2000-2011).

+ The information includes the Trustee's principal occupation during the last five years and other information relating to the experience, attributes, and skills relevant to the Trustee's qualifications to serve as a Trustee, which led to the conclusion that the Trustee should serve as a Trustee for the fund.

Advisory Board Members and Officers:

Correspondence intended for an officer or Peter S. Lynch may be sent to Fidelity Investments, 245 Summer Street, Boston, Massachusetts 02210. Officers appear below in alphabetical order.

Name, Year of Birth; Principal Occupation

Peter S. Lynch (1944)

Year of Election or Appointment: 2003

Member of the Advisory Board

Mr. Lynch also serves as Member of the Advisory Board of other Fidelity® funds. Mr. Lynch is Vice Chairman and a Director of FMR (investment adviser firm) and FMR Co., Inc. (investment adviser firm). In addition, Mr. Lynch serves as a Trustee of Boston College and as the Chairman of the Inner-City Scholarship Fund. Previously, Mr. Lynch served on the Special Olympics International Board of Directors (1997-2006).

Elizabeth Paige Baumann (1968)

Year of Election or Appointment: 2017

Anti-Money Laundering (AML) Officer

Ms. Baumann also serves as AML Officer of other funds. She is Chief AML Officer (2012-present) and Senior Vice President (2014-present) of FMR LLC (diversified financial services company) and is an employee of Fidelity Investments. Previously, Ms. Baumann served as AML Officer of the funds (2012-2016), and Vice President (2007-2014) and Deputy Anti-Money Laundering Officer (2007-2012) of FMR LLC.

Marc R. Bryant (1966)

Year of Election or Appointment: 2015

Secretary and Chief Legal Officer (CLO)

Mr. Bryant also serves as Secretary and CLO of other funds. Mr. Bryant serves as CLO, Secretary, and Senior Vice President of Fidelity Management & Research Company (investment adviser firm, 2015-present) and FMR Co., Inc. (investment adviser firm, 2015-present); Secretary of Fidelity SelectCo, LLC (investment adviser firm, 2015-present) and Fidelity Investments Money Management, Inc. (investment adviser firm, 2015-present); and CLO of Fidelity Management & Research (Hong Kong) Limited and FMR Investment Management (UK) Limited (investment adviser firms, 2015-present) and Fidelity Management & Research (Japan) Limited (investment adviser firm, 2016-present). He is Senior Vice President and Deputy General Counsel of FMR LLC (diversified financial services company). Previously, Mr. Bryant served as Secretary and CLO of Fidelity Rutland Square Trust II (2010-2014) and Assistant Secretary of Fidelity's Fixed Income and Asset Allocation Funds (2013-2015). Prior to joining Fidelity Investments, Mr. Bryant served as a Senior Vice President and the Head of Global Retail Legal for AllianceBernstein L.P. (2006-2010), and as the General Counsel for ProFund Advisors LLC (2001-2006).

William C. Coffey (1969)

Year of Election or Appointment: 2009

Assistant Secretary

Mr. Coffey also serves as Assistant Secretary of other funds. He is Senior Vice President and Deputy General Counsel of FMR LLC (diversified financial services company, 2010-present), and is an employee of Fidelity Investments. Previously, Mr. Coffey served as Vice President and Associate General Counsel of FMR LLC (2005-2009).

Jonathan Davis (1968)

Year of Election or Appointment: 2010

Assistant Treasurer

Mr. Davis also serves as Assistant Treasurer of other funds, and is an employee of Fidelity Investments. Previously, Mr. Davis served as Vice President and Associate General Counsel of FMR LLC (diversified financial services company, 2003-2010).

Adrien E. Deberghes (1967)

Year of Election or Appointment: 2016

Assistant Treasurer

Mr. Deberghes also serves as an officer of other funds. He serves as Executive Vice President of Fidelity Investments Money Management, Inc. (FIMM) (investment adviser firm, 2016-present) and is an employee of Fidelity Investments (2008-present). Prior to joining Fidelity Investments, Mr. Deberghes was Senior Vice President of Mutual Fund Administration at State Street Corporation (2007-2008), Senior Director of Mutual Fund Administration at Investors Bank & Trust (2005-2007), and Director of Finance for Dunkin' Brands (2000-2005). Previously, Mr. Deberghes served in other fund officer roles.

Stephanie J. Dorsey (1969)

Year of Election or Appointment: 2010

Assistant Treasurer

Ms. Dorsey also serves as an officer of other funds. She is an employee of Fidelity Investments (2008-present) and has served in other fund officer roles. Prior to joining Fidelity Investments, Ms. Dorsey served as Treasurer (2004-2008) of the JPMorgan Mutual Funds and Vice President (2004-2008) of JPMorgan Chase Bank.

Howard J. Galligan III (1966)

Year of Election or Appointment: 2014

Chief Financial Officer

Mr. Galligan also serves as Chief Financial Officer of other funds. Mr. Galligan serves as President of Fidelity Pricing and Cash Management Services (FPCMS) (2014-present) and as a Director of Strategic Advisers, Inc. (investment adviser firm, 2008-present). Previously, Mr. Galligan served as Chief Administrative Officer of Asset Management (2011-2014) and Chief Operating Officer and Senior Vice President of Investment Support for Strategic Advisers, Inc. (2003-2011).

Thomas C. Hense (1964)

Year of Election or Appointment: 2008, 2010, or 2015

Vice President

Mr. Hense serves as Vice President of Fidelity Advisor® Multi-Asset Income Fund (2015) and other funds (High Income (2008), Small Cap (2008), and Value (2010) funds), and is an employee of Fidelity Investments (1993-present). Previously, Mr. Hense served as a portfolio manager for Fidelity's Institutional Money Management Group (Pyramis) (2003-2008).

Brian B. Hogan (1964)

Year of Election or Appointment: 2009

Vice President

Mr. Hogan also serves as Trustee or Vice President of other funds. Mr. Hogan serves as a Director of FMR Investment Management (UK) Limited (investment adviser firm, 2015-present) and Fidelity SelectCo, LLC (investment adviser firm, 2014-present) and President of the Equity Division of FMR (investment adviser firm, 2009-present). Previously, Mr. Hogan served as Senior Vice President, Equity Research of FMR (2006-2009) and as a portfolio manager. Mr. Brian B. Hogan is not related to Mr. Colm A. Hogan.

Colm A. Hogan (1973)

Year of Election or Appointment: 2016

Deputy Treasurer

Mr. Hogan also serves as an officer of other funds. Mr. Hogan is an employee of Fidelity Investments (2005-present). Mr. Colm A. Hogan is not related to Mr. Brian B. Hogan.

Chris Maher (1972)

Year of Election or Appointment: 2013

Assistant Treasurer

Mr. Maher serves as Assistant Treasurer of other funds. Mr. Maher is Vice President of Valuation Oversight and is an employee of Fidelity Investments. Previously, Mr. Maher served as Vice President of Asset Management Compliance (2013), Vice President of the Program Management Group of FMR (investment adviser firm, 2010-2013), and Vice President of Valuation Oversight (2008-2010).

Rieco E. Mello (1969)

Year of Election or Appointment: 2017

Assistant Treasurer

Mr. Mello also serves as Assistant Treasurer of other funds. Mr. Mello is an employee of Fidelity Investments (1995-present).

Kenneth B. Robins (1969)

Year of Election or Appointment: 2016

Chief Compliance Officer

Mr. Robins also serves as an officer of other funds. Mr. Robins serves as Compliance Officer of Fidelity Management & Research Company and FMR Co., Inc. (investment adviser firms, 2016-present) and is an employee of Fidelity Investments (2004-present). Previously, Mr. Robins served as Executive Vice President of Fidelity Investments Money Management, Inc. (investment adviser firm, 2013-2016) and served in other fund officer roles.

Stacie M. Smith (1974)

Year of Election or Appointment: 2016

President and Treasurer

Ms. Smith also serves as an officer of other funds. She is an employee of Fidelity Investments (2009-present) and has served in other fund officer roles. Prior to joining Fidelity Investments, Ms. Smith served as Senior Audit Manager of Ernst & Young LLP (accounting firm, 1996-2009). Previously, Ms. Smith served as Deputy Treasurer of certain Fidelity® funds (2013-2016).

Marc L. Spector (1972)

Year of Election or Appointment: 2016

Assistant Treasurer

Mr. Spector also serves as an officer of other funds. Mr. Spector is an employee of Fidelity Investments (2016-present). Prior to joining Fidelity Investments, Mr. Spector served as Director at the Siegfried Group (accounting firm, 2013-2016), and prior to Siegfried Group as audit senior manager at Deloitte & Touche (accounting firm, 2005-2013).

Renee Stagnone (1975)

Year of Election or Appointment: 2016

Assistant Treasurer

Ms. Stagnone also serves as an officer of other funds. Ms. Stagnone is an employee of Fidelity Investments (1997-present). Previously, Ms. Stagnone served as Deputy Treasurer of certain Fidelity® funds (2013-2016).

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The actual expense Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (May 25, 2017 to July 31, 2017). The hypothetical expense Example is based on an investment of $1,000 invested for the one-half year period (February 1, 2017 to July 31, 2017).

Actual Expenses

The first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Annualized Expense RatioA | Beginning Account Value | Ending Account Value July 31, 2017 | Expenses Paid During Period |

|

| Actual | .60% | $1,000.00 | $1,042.00 | 1.14B |

| HypotheticalC | $1,000.00 | $1,021.82 | 3.01D |

A Annualized expense ratio reflects expenses net of applicable fee waivers.

B Actual expenses are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by 68/365 (to reflect the period May 25, 2017 to July 31, 2017).

C 5% return per year before expenses

D Hypothetical expenses are equal to the Fund's annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Distributions (Unaudited)

The fund hereby designates as a capital gain dividend with respect to the taxable year ended July 31, 2017, $7, or, if subsequently determined to be different, the net capital gain of such year.

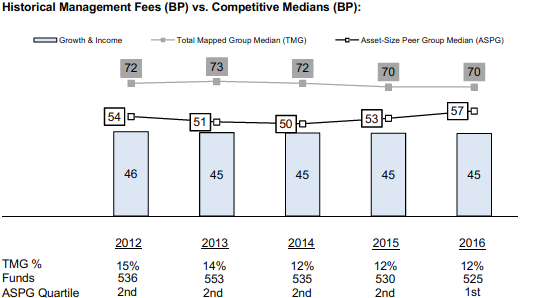

Board Approval of Investment Advisory Contracts and Management Fees

Fidelity Small Cap Growth K6 Fund

On January 18, 2017 the Board of Trustees, including the Independent Trustees (together, the Board), voted to approve the management contract with Fidelity Management & Research Company (FMR) and the sub-advisory agreements with affiliates of FMR (together, the Advisory Contracts) for the fund. The Board, assisted by the advice of fund counsel and Independent Trustees' counsel, considered a broad range of information.